?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The dominant interpretation of Italian economic stagnation in the last decades is that this is due to insufficient liberalisation, but an alternative explanation emphasises the unintended consequences of Italy's strategy of tying itself to the European mast (‘external constraint’). Based on historical reconstructions of three policy areas, public debt management, privatisation, and labour market policy, this paper seeks to adjudicate between these two rival accounts. It argues that insufficient liberalisation fails to explain the Italian trajectory. The external constraint does a better job of explanation, but more as a necessary condition for stagnation than as a sufficient one. In other words, it would probably have been possible to manage the external constraint differently to produce better outcomes, but without the external constraint, the Italian stagnation would likely have been less deep.

1. Introduction

Italy is often regarded as the ‘sick man’ of a not so healthy Eurozone. After years of stagnating labour productivity and paltry growth, its staggering public debt threatens to plunge the monetary union in a new financial crisis. Yet, not so long ago this country was portrayed as a case of success, as it had posted one of the highest postwar growth rates among advanced nations. In this paper, we investigate the causes of Italy's economic stagnation. Specifically, we ask whether the strategy of deliberately limiting the country's policy-making discretion, known as the strategy of ‘external constraint’ (Dyson and Featherstone Citation1999), has contributed to it.

The question is highly controversial. On the one hand, the dominant explanation of Italy's decline highlights the insufficient liberalisation of the Italian economy, while downplaying the loss of monetary and exchange rate discretion as well as the other strictures of Eurozone membership. On the other hand, a rival explanation highlights the demand compression and negative supply-side effects of the external constraint strategy. Contrary to the former, this account regards Italy's decision to tie its hands to the European mast as the primary cause of the Italian decline.

In this paper we examine the causal properties of the external constraint strategy through historical reconstructions in three policy areas: the management of public debt, the effects of privatisation of state-owned enterprises, and of labour market policy. We adopt a counterfactual approach, which consists in trying to determine which modifications of contextual conditions would have to be introduced in order to produce, respectively: (1) an Italy that does not decline while adopting the external constraint strategy; and (2) an Italy that declines anyway while not adopting the external constraint strategy. If it is difficult to produce (1) under conditions of ‘minimal counterfactual rewrite’ of history, the cause has high properties of sufficiency. If vice versa, it is difficult to produce (2) the cause has high properties of necessity (Montoya and Mahoney Citation2020).

Our main conclusion is that the external constraint strategy did indeed contribute to Italy's stagnation, but more as a necessary than as a sufficient condition. In other words, with some relatively parsimonious counterfactal editing of the context the external constraint strategy could have produced a more positive outcome. However, an Italy that does not embrace the strategy of external constraint and still experiences the same degree of decline requires a more extensive counterfactual rewrite of history. To put it differently, the strategy of the external constraint could have produced better results for Italy if it had been managed differently or other circumstances had been more propitious, but without it, the decline would not have been as deep as the one actually observed.

The paper begins by providing evidence of Italy's decline and reviewing existing explanations, particularly the ‘insufficient liberalization’ hypothesis (Section Two), followed by a discussion of our methodological approach (Section Three). In Section Four, after a short reconstruction of the main steps in the adoption of the external constraint strategy ensues, we consider the three case studies on public debt, privatisation, and labour market policy. We conclude with a compact discussion of the evidence.

2. Italy's Decline

In the 1960s and 1970s, Italy's average annual growth rate was higher than those of France, Germany, the United Kingdom, the United States, and the EU15 countries, while it was the second highest after Germany and the United Kingdom, respectively, in the 1950s and 1980s (). Until the late 1980s-early 1990s, Italy's per capita GDP grew faster than both the US's and Germany's, but declined thereafter, especially after the Great Recession. If the decline vis-à-vis the United States started in the early 1990s, the decline vis-à-vis Germany (a country in deep crisis in the 1990s) started in the mid-2000s.

Table 1. Growth rates in various countries.

The examination of labour productivity trends leads to similar conclusions. Manufacturing labour productivity grew faster in Italy than in Germany, France, and other European countries until the mid-1990s and then stagnated. Thus, Italy's decline is a relatively recent phenomenon. What has caused it?

2.1. Explanations of the Italian Decline

Most of the relevant literature underscores a series of deeply rooted ‘plagues’ of the Italian economy and society. In particular, the prevalence of small or very small firms is often emphasised, as small firms are known to be less productive and innovative than large ones (Amatori, Bugamelli, and Colli Citation2013).

Other dimensions of Italian ‘backwardness’ are also frequently highlighted by the literature: the insufficient levels of human capital, a bank-centred financial system based on personalised relations, a centralised industrial relations system preventing adjustment of wages to local productivity levels, a society prone to familism, as well as cronyism and corruption, a cumbersome bureaucracy with complex and non-transparent rules, and an inefficient court system (on all these elements, see the chapters in Toniolo Citation2013b). Given the long list of deficiencies, some economic historians have come to the paradoxical conclusion that what is in need of explanation is not the Italian decline, but the previous period of growth (Di Martino and Vasta Citation2015, p. 221).

The main problem with this type of argument is that the negative features it concentrates on (cronyism, familism, and so on) have been present for a long time, including when the Italian economy was growing faster than those of other countries, and there is no evidence that they have worsened after the 1990s. Logically, a time-invariant factor should not be invoked as a cause of a time-variant effect.

More convincing are arguments that emphasise the interaction between pre-existing ‘curses’ and time-varying factors. This type of explanation usually argues that, faced with new challenges, the Italian economy should have been more thoroughly liberalised, and that the insufficiency of the liberalisation effort is ultimately responsible for the stagnating trend.

Candidates for time-varying factors are the intensification of trade competition from emerging economies and the IT revolution. For example, Faini and Sapir (Citation2005) argue that the Italian slowdown is due to the country's continued specialisation in traditional sectors (characterised by low human capital and low technology) at a time of increased international competition from emerging countries, especially China, and its inability to upgrade its sectoral specialisation. This argument has been challenged by Pellegrino and Zingales (Citation2017), however, who estimate the impact on country and sectoral level productivity of exposure to China's trade and conclude that between 1995 and 2006 productivity grew faster, rather than more slowly, in countries and sectors with greater exposure to Chinese competition.

In their analysis of the Italian decline, Pellegrino and Zingales (Citation2017) focus on another time-changing factor: the role of information technology. After ruling out several competing explanations (for example, labour rigidity, quality of institutions), they conclude that the most important factor explaining Italy's productivity slowdown is the continued reliance on family management within Italian enterprises as opposed to professional management. This factor prevents the Italian economy from taking advantage of the IT revolution, because IT and ‘modern’ managerial practices complement one another. The authors argue that greater economic liberalisation would encourage more meritocratic management and thus alleviate this problem. However, because the adoption of new technology is a process that takes time to unfold, this explanation is difficult to reconcile with the sudden shift in Italian labour productivity data.

Focusing on total factor productivity,Footnote1 Calligaris et al. (Citation2018) document that firm-level productivity declined in all sectors from 1995 on, both those exposed to trade and those not exposed, and its dispersion increased. They argue that this was due to an increase in the share of low productivity firms within sectors. The authors interpret this phenomenon as the consequence of the insufficient liberalisation of the Italian economy, which interferes with optimal resource allocation. In line with the above explanations, several economists see the Italian economy as shackled by a sclerotic regulatory system, weak competition in product markets, overregulated labour markets, and a pervasive state that stifles individual initiative (for example, Alesina and Giavazzi Citation2006). The result is not just an inefficient economic system, but also a deeply unjust social system, which rewards those who are well connected (thanks to birth or social networks) and penalises those who work hard and play by the rules (Zingales Citation2012).

In brief, the main explanation for Italy's stagnation proceeds as follows: the Italian economy and society are blighted by several ‘scourges’ (small firms, familistic management, and so on). When the economy was still relatively protected and technical change was less tumultuous, these ‘plagues’ had a limited bite and economic performance was still acceptable. When, however, the economy became fully exposed to competition from low-cost countries, and when information technology became a more important competitive factor, the ‘scourges’ became more penalising (Capussela Citation2018; Toniolo Citation2013a). Adaptation to the changed environmental conditions would have required a more aggressive liberalisation effort by policy-makers and a more sustained reduction of the role of the state in the economy. In this scenario, the adoption of external constraints is seen as either inconsequential for the Italian stagnation (for example, Salvati Citation2012), or as a positive, rather than a negative influence.

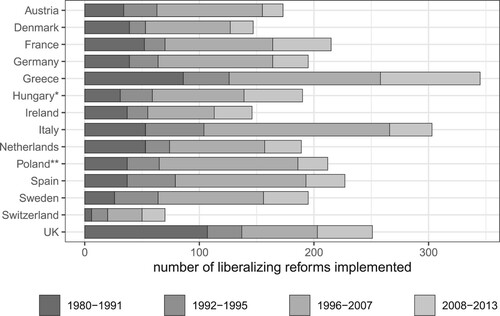

This explanation, however, underplays the large number of liberalising reforms introduced in Italy since the early 1990s, ranging from corporate governance reforms aimed at making corporate control more contestable, to privatisation of the main state-owned banks and enterprises, as well as reforms enhancing labour market flexibility and increasing product-market competition. , which relies on a comparative database on liberalisation reforms (Armingeon et al. Citation2019), shows that Italy introduced liberalising reforms more intensely than most other countries, especially from 1992 on, more than Germany and, especially, France.

Figure 1. Liberalising reforms in 14 countries (1980–2013). Source: Armingeon et al. (Citation2019).

Notes: Policy reforms are coded as liberalising or liberalising; the former imply the loosening of restrictions on free markets, the latter a move in the opposite direction. Policy fields include: active labour market policies, competition, employment protection, finance, industrial relations, non-employment benefits, pensions, privatisation, social security benefits and transfers, tax policy. For more information, see https://liberalization.org.

Data for Hungary begin in 1987;

data for Poland begin in 1989.

It may be argued that liberalisation reforms need to cross an unspecified critical threshold before they produce positive results. However, this makes the link between liberalising reforms and growth very difficult to evaluate empirically, because it is always possible to argue that reforms are insufficient and ‘more is needed’.

An alternative explanation of the Italian decline places it much closer in time and links it tightly to the external constraint strategy, that is, to a set of policy decisions aimed at reducing the country's policy-making discretion. This strategy was supposed to facilitate the modernisation of the country, forcing elites to adopt policies they may otherwise have been unwilling to adopt (Dyson and Featherstone Citation1999; Ferrera and Gualmini Citation1999). Specifically, it should have acted as a ‘beneficial constraint’ (Streeck Citation1997), which would force trade unions to behave more responsibly, and politicians to pursue structural reforms.

Historically, state intervention has played a more important role in the Italian variant of capitalism than in other models of capitalism. For this reason, an argument can be made that Italian capitalism was especially penalised by the European regulatory framework, which has made it more difficult for the state to intervene in the economy (Scharpf Citation1999). Furthermore, a number of (mostly post-Keynesian) macroeconomists have argued that euro membership has had negative consequences for Italy's aggregate demand. Some have underscored the appreciation of the real exchange rate, which has reduced net foreign demand (Bagnai Citation2016; Cesaratto and Zezza Citation2019). Others have argued that the eurozone's conservative fiscal rules have led to multiple years of primary budget surpluses in Italy (Storm Citation2019). Interestingly, the recognition of a possible negative role of the external constraint mirrors in reverse the beneficial constraint view. In brief, the consequences of the external constraint are controversial. Some authors argue that it has nothing to do with Italy's decline, others that it has everything to do with it. In the remainder of the paper, we will try to assess these competing claims. In the next section, we discuss our methodological approach.

3. Counterfactual Analysis

In this paper we use qualitative counterfactual analysis to examine the causal properties of the external constraint strategy. Specifically, we examine the properties of sufficiency and necessity of the explanans, and assess the extent to which history would have to be ‘counterfactually rewritten’ in order for the cause to produce the opposite outcome to the one which is observed (evaluation of the sufficiency properties of the cause), and for the absence of the cause to produce the same outcome (evaluation of the necessity properties).Footnote2 In our case, counterfactual analysis is applied to the hypothesis that adopting the strategy of external constraint (X) contributed to Italian decline (Y) as a necessary and/or a sufficient condition. ‘Contributed to’ indicates that X may operate jointly with other causes. As such, it may be an INUS condition, that is, a necessary component of a sufficient combination of conditions (Mackie Citation1965). To evaluate the plausibility of , we evaluate the ‘path of minimal counterfactual rewrite’ necessary to produce an outcome inconsistent with the hypothesis of a causal impact of the external constraint on Italy's decline.Footnote3

This approach implies assessing the extent to which the context (that is, other factors in the causal configuration not directly modified by the critical event) would have to be ‘edited’ to produce either an Italy that embraces the external constraint strategy but does not experience economic decline (evaluation of the sufficiency properties), or an Italy that does not adopt the external constraint strategy and still experiences the same extent of economic decline or worse (evaluation of the necessity properties). The greater the extent of counterfactual rewrite needed to produce an inconsistent outcome, the stronger the sufficiency or necessity properties of the cause. Vice versa, the easier it is to conceive of a plausible world with inconsistent outcomes on the basis of the available evidence, the smaller the causal relevance of the explanans.

There is already a large literature establishing a relationship between Italy's adoption of the euro and its loss of external competitiveness (increase in relative unit labour costs), which in turn led to real exchange rate appreciation and a decline in net exports (Bagnai Citation2016; Cesaratto and Zezza Citation2019). While acknowledging that this macroeconomic perspective is important for a thorough assessment of the impact of the external constraint, in this paper we will focus on a different and complementary side of the story, namely the use of the external constraint, and in particular the accession to the single currency, as a political device to steer supply side policies as well in a specific direction.

We apply qualitative counterfactual analysis to three policy areas: public debt management, privatisations, and labour market policy. Whenever possible, we use evidence from other countries as counterfactual. This strategy requires caution, however. The ideal counterfactual country is as similar as possible to Italy but has chosen not to sign the Maastricht Treaty and to stay out of the Economic and Monetary Union (EMU). Yet, the countries which are plausibly similar to Italy — that is, the Mediterranean countries and France — all joined the euro, while the ones that did not join (Denmark, Sweden, and the United Kingdom) or did not sign the Maastricht Treaty (Switzerland and Norway), all differ from Italy in important respects. For public debt and labour market policy, we will use Italy in 1993–96 as counterfactual. This was a period in which, despite its best intentions, Italy was forced to leave the European Exchange Rate Mechanism (ERM) and let its exchange rate fluctuate. Arguably, this case comes closest to examining the consequences of the absence of the cause under conditions of as little counterfactual rewrite of context as possible. We hasten to add that any conclusions derived from qualitative counterfactual analysis is inherently uncertain, given that it is impossible to rewind history and observe its course in the absence of the crucial event. Italy in 1993–96 is not a perfect counterfactual for Italy in the euro years. In particular, Chinese competition was much less intense in the early 1990s than it became afterwards and this most likely helped Italian exports in the brief period of floating exchange rates.Footnote4 However, as discussed above, the literature has excluded that Chinese competition was the decisive factor in bringing about economic stagnation in Italy (Calligaris et al. Citation2018; Pellegrino and Zingales Citation2017).

We liken our approach to the evidence to a civil trial, where the standard of proof is ‘preponderance of the evidence’, rather than ‘beyond reasonable doubt’ (Haack Citation2012). Before the trial starts, an impartial judge gives 50% probability each to the null hypothesis (the defendant is not guilty) and alternative hypothesis (guilty). However, she later modifies her prior beliefs depending on the strength of the evidence in favour or against the hypothesis (Kreuzer Citation2016).

4. Adoption and Consequences of the External Constraint

The choice of the external constraint was made in steps:

4.1. The European Monetary System (EMS)

At the end of the 1970s Italy grew faster than other large European countries and, with an unemployment rate below 5 per cent, the country was practically at full employment. However, due to the oil shocks but also to militancy of Italian unions, inflation had increased to two digits (). With rates of industrial conflict at the highest in advanced countries, convincing the Italian unions to moderate their bargaining demands became the overarching problem of Italian political economy in the 1970s and 1980s. A first, more visible, strategy involved tripartite pacts (Lange and Vannicelli Citation1982) and brought to a reform of the wage indexation mechanism (the scala mobile) in 1983 and 1984. It is fair to say that this strategy was only moderately successful: while inflation declined in Italy, it declined everywhere else as well, and therefore it is difficult to attribute disinflation to negotiated wage restraint.

Table 2. The 1960s and 1970s: selected economic indicators.

A less visible strategy was the adoption of an exchange rate anchor. In 1979, the Andreotti government decided to join the EMS, although with a larger oscillation band than other countries (±6 per cent). The decision was controversial among both Italian economists and politicians. The detailed study conducted by Talani (Citation2017, Ch. 7), in which the position of all major political-economic actors is examined, concludes that the main goal of joining the EMS was weakening the Italian unions, thus forcing them to embrace wage moderation. While all employers' organisations supported immediate entry into the EMS, the main trade unions were instead partially divided: CGIL and UIL were not in principle opposed to a system of fixed exchange rates, but they did not support entry into the EMS because it wasn't accompanied by measures to redress economic disparities between poorer and richer European regions. The other major union, CISL, was in favour of entry into the EMS. Among the main political actors, the Communist Party (which was part of the governmental majority although without direct government involvement) voted against the EMS in December 1979 because it considered that the measure would have had deflationary effects and would have reduced Italy's growth rate. One month later, the government of national unity fell.

In 1981 the government decided that the Bank of Italy would no longer be forced to buy any residual treasury bonds that the market refused to absorb (the so called ‘divorce’). The measure was aimed at forcing public deficit reduction and was intended as an anti-inflationary move, because the ‘divorce’ would supposedly give the Bank of Italy better control over the money supply. Furthermore, it would pave the way to liberalisation of capital movements and allow participation in the EMS.

4.2. The Maastricht Treaty

In the 1980s, while unit labour cost growth and inflation came down, and growth remained on a par with other large economies (especially in the late 1980s), the government's fiscal position deteriorated. This was due to a dramatic shift from negative real interest rates in the 1970s to highly positive rates in the 1980s (5.65 per cent on average between 1985 and 1989), along with a large primary budget deficit (close to −4 per cent in the 1980s). The 1980s were the years in which Italy built the public debt problem that would come to haunt it in the euro years, i.e., the Italy's public debt problem precedes the EMU.

Signed in 1992, the Maastricht Treaty imposed much tighter constraints than anything introduced before. The central bank would be explicitly prevented from lending to governments, as a matter of treaty obligation. The fixed but adjustable parities of the EMS would be replaced by the most inflexible of exchange rate arrangements: a common currency. Furthermore, the economic governance model embedded in the treaty was de facto (although not de jure) incompatible with the modus operandi of state-owned enterprises, especially with regard to corporate finance, as discussed below.

The negotiation of the Maastricht Treaty was the triumph of ‘quiet politics’ (Culpepper Citation2010). Negotiations were run by a small number of top-level bureaucrats, while public opinion and even elective assemblies, which overwhelmingly supported European integration, were only partially aware of developments (Dyson and Featherstone Citation1999). Guido Carli, at the time Minister of Treasury, later described the Maastricht Treaty as a golden opportunity to liberalise the Italian economy by stealth, without entering into open conflict with Italy's largest mass parties, the Christian Democrats (DC) and the Communist Party (PCI) (see, for example Carli Citation1993, pp. 7–8).

4.3. Entry into EMU

The signing of the Maastricht Treaty had been preceded by the completion of capital flows liberalisation and a further stiffening of the exchange rate regime: Italy entered the narrow band of the ERM (±2.25 per cent) at the beginning of 1990. This led to a loss of competitiveness, current account deficits, and declining confidence in the lira. In September 1992, Italy was forced to abandon the ERM and let its exchange rate fluctuate. In these years, interest payments on public debt became very high (12 per cent of GDP in 1993), but the recession was V-shaped and growth soon restarted. In fact, in 1995 the Italian economy grew at a rate close to 3 per cent, which was to become a rarity in the following years. Italy decided to reenter the EMS at the end of 1996 as a precondition for joining EMU in 1999. In 1996, the public deficit was 6.6 per cent, very far from the 3 per cent requirement. Admission thus required a significant fiscal correction, but the government's commitment to join the single currency was perceived as credible by financial markets, and this led to a reduction of interest expenditure.

Entry in the common currency implied giving up monetary autonomy and exchange rate flexibility, which Italy had previously resorted to extensively to counterbalance the erosion of competitiveness. This did not seem a big sacrifice at the time, given the largely shared view that devaluation was counterproductive as it increased the price of Italian imports without reducing their quantity, leading to further devaluation down the road. Furthermore, because devaluations allowed firms to protect their profit margins, they reduced incentives for firms to upgrade their products and processes (Graziani and Meloni Citation1980).

In the next section, we examine the effects of the external constraint on public debt, privatisation, and labour market policy. For each case study, we analyze the causal process linking the external constraint to outcomes and assess the properties of sufficiency and necessity. For reasons of space, for each case only the main developments are discussed.

4.4. Management of Public Debt

At first sight, the hypothesis that the external constraint (in this case, entry into the EMU and then the euro) may have had negative consequences for the management of Italy's large public debt seems largely contradicted by data. How can one credibly make this argument when the interest rate on Italian bonds declined from 12.2 per cent in 1995 to 6.8 per cent in 1997, and then continued to decline until 3.5 per cent in 2005, thus reducing interest expenditures on Italy's large public debt from 11 per cent of GDP in 1996 to 4.5 per cent in 2005? But other elements need to be taken into account before passing judgement.

Italy's public debt problem began to emerge in the 1970s.Footnote5 These were years in which the Italian welfare state was being built — for example, with the introduction of a national health service and more generous pension benefits. Increased expenditures were not matched by an increase in tax revenues. It took a while before this began to translate into a growing debt-to-GDP ratio, however. High inflation and debt monetisation, with the Bank of Italy absorbing a large part of the public debt onto its balance sheet, implied negative real interest rates. Thus, the debt only increased from 40 per cent of GDP in 1969 to 60 per cent at the end of 1981, despite persistent public deficits.

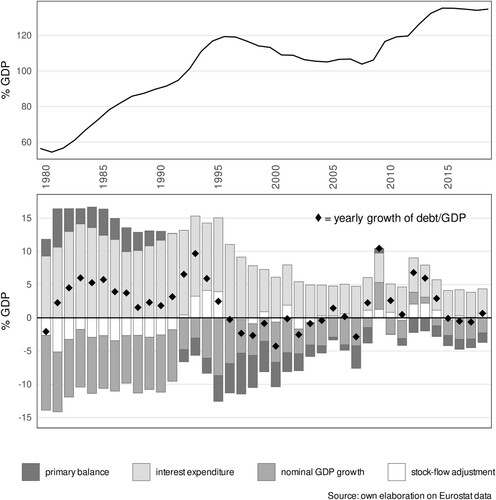

In the 1980s, the global increase in interest rates (initiated by the Federal Reserve under Paul Volcker), the combined effect of higher interest payments and declining inflation, the slowing down of GDP growth, and the absence of an adequate correction of the primary balance (tax revenue remained below primary government expenditure throughout the 1980s) led to a perverse debt dynamic. The relative weight of the various factors that contributed to the increase in debt in this period is shown by the decomposition presented in , which follows the common formula for debt/GDP growth

(1)

(1) where

is the debt-to-GDP ratio at the end of period t,

is the primary balance in t,

and

are, respectively, the nominal interest and the nominal growth rate in the same period (see Appendix 2 online). The debt-to-GDP ratio grew from 60 per cent in 1981 to 91 per cent in 1987, at an annual average rate of 5 per cent. As the decomposition graph shows, the greatest contribution to the increase in public debt came from interest expenditures, not from the primary deficit.

Figure 2. Debt-to-GDP ratio and its decomposition (1980–2018). Source: own elaboration on Eurostat data.

After 1995, Italy benefited from falling interest rates, later reinforced by the effect of joining the single currency. The period between 1997 and 2003 was marked by a progressive reduction of the debt ratio, which was slightly below 104 per cent of GDP at the outbreak of the financial crisis in 2008.

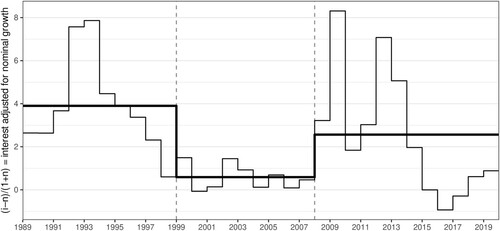

The financial crisis then led to a new upturn in debt (132 per cent in 2013). A sharp increase (+13 per cent) occurred in 2011–13, when tough austerity policies were pursued in response to the sovereign debt crisis. shows that the difference between interest rate and growth rate has almost always been positive, including in the years between 1999 and 2007.

Figure 3. Interest rates on government bonds adjusted for nominal growth (1989–2019). Source: Authors' elaboration on Eurostat data.

The period of low interest rates did not last long. When the sovereign debt crisis hit, interest rates rose and returned to the very high levels of the 1990s (). As argued by De Grauwe (Citation2012), Italy and other peripheral countries found themselves in a situation of vulnerability similar to that of developing countries that issue debt in a foreign currency.

The years between 2001 and 2005 were characterised by a progressive decrease of primary surpluses (to 0.4 per cent in 2005). Could Italy's public debt under the euro have been better managed? Barta (Citation2018, Ch. 3) argues that, after entry into EMU was secured, a coalition of actors opposed to taxes and dependent on state transfers reemerged under the aegis of the Berlusconi government (2001–06), weakening the effort for fiscal adjustment.Footnote6

It is also common to compare Italy to Belgium (for example, Sapir Citation2018). In 1995, Belgium had an even higher debt level than Italy, but was able to reduce it to 87 per cent by 2007, thanks to — so the argument goes — higher primary surpluses. We note, however, that if Italy had had the same growth rate as Belgium, this alone would have reduced its debt to 90 per cent by 2007, with no need for primary surpluses. This is to say that slow growth mattered at least as much as, if not more than, fiscal discipline for public debt management. Unlike Italy, Belgium had at least one viable demand driver of growth: net exports, which were slightly negative in Italy on average between 1998 and 2007, and strongly positive (3.6 per cent) in Belgium. A more restrictive fiscal policy could have further reduced the already very low Italian growth rate. As argued by post-Keynesian economists, protracted fiscal austerity, along with an overvalued exchange rate, is likely to have depressed demand and, through various channels, negatively affected the growth rate (Girardi, Paternesi Meloni, and Stirati Citation2020).

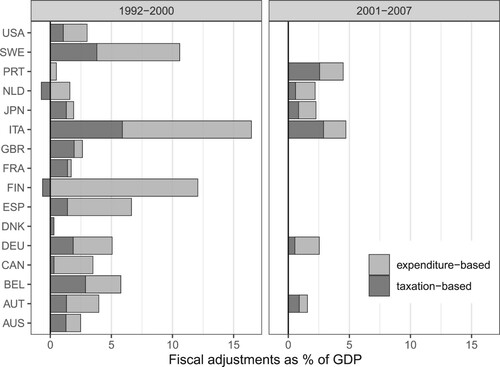

The argument that fiscal corrections have a limited negative impact on growth and may even be expansionary (Giavazzi and Pagano Citation1990) is highly controversial (for example, Guajardo, Leigh, and Pescatori Citation2011). In any case, IMF data (reported in ) suggest that Italy's fiscal adjustment was not only the largest in comparative perspective, but also more reliant on expenditure cuts than in almost any other country, and certainly more than in Belgium.Footnote7

Figure 4. Size of fiscal adjustments. Source: IMF Dataset of Fiscal Consolidation 2011.

What would have happened if Italy had not joined the euro? A useful benchmark is the period between 1993 and 1996, prior to the decision to reenter the EMS in late November 1996. In these four years, Italy had a flexible exchange rate and experienced a large depreciation of the exchange rate (21 per cent vis-á-vis the Deutsche Mark between the end of 1992 and the end of 1995). This is exactly the kind of negative shock that advocates of the euro would argue the euro provides protection from. Nevertheless, during this period Italy was able to stabilise the growth of debt rather quickly: from an increase of almost 10 per cent in 1993, the debt/GDP ratio was brought onto a downward trend by 1996, even though interest expenditure remained above 10 per cent in these years (). The current account moved from a deficit in 1993 to a surplus of almost 3 per cent in 1995, thanks to a large real exchange devaluation. Data presented in suggests that flexible exchange rates (and the associated real devaluation) stimulated Italian exports, whose growth in 1993–96 was higher than the average growth in the other countries that first joined the euro, while it was lower both in the EMS period (1980–1992) and in the Euro pre-crisis period (1997–2007). Moreover, De Grauwe's (Citation2012) lender of last resort argument implies that Italy would have likely escaped the 2011 sovereign debt crisis if it had had its own currency and central bank.

Table 3. Export of goods and services in volume (average annual growth rates).

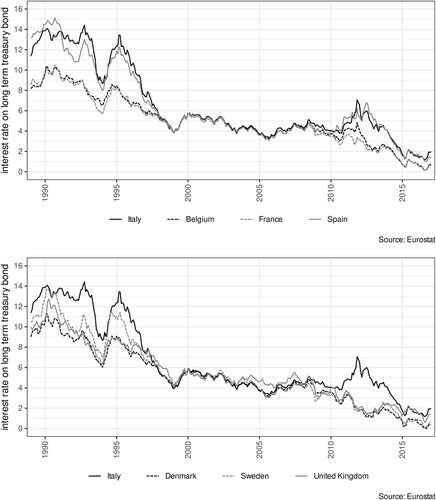

Furthermore, it can be argued that there would have been interest rate decline, at least in part, even if Italy had not joined the euro, as the fall in interest rates was a general trend, common to all advanced economies, including Sweden, Denmark, and the United Kingdom, and not a specific trend of eurozone members ().

Figure 5. Interest rates within and outside the euro (1989–2017). Source: Eurostat.

To summarise, the external constraint provided short-term benefits by helping to reduce interest rates (at least until the crisis), but it arguably also determined a reduction of growth rates by curbing internal (public) and external demand. Could Italy have done better (sufficient conditions)? It is argued that further fiscal consolidation in 2001–06 could have lowered debt vulnerability after 2008, hence less austerity would have been needed in the early 2010s. However, more consolidation would have likely produced less growth via demand effects.

As to necessary conditions, the evidence from 1993–96 does not support the hypothesis that Italy would have found it more difficult to manage its public debt if it had decided not to enter the euro, even under conditions of exchange rate turbulence. In fact, it would probably have found it easier thanks to higher (export-led) growth. Furthermore, the interest rate advantage of euro membership, which to a large extent took place also outside the eurozone, turned into its opposite when the sovereign debt crisis hit.

4.5. Privatisations

One manifestation of the Italian decline is the disappearance of large firms with a significant presence in advanced sectors. As discussed earlier in the paper, the scarcity of large firms has been identified as one of the problems affecting the Italian economy. Did the privatisation of state-owned enterprises play a role? Was the privatisation process influenced by the external constraint? These are the questions addressed in this section.

Italian capitalism inherited from fascism a pervasive role of the state in industry and banking (Shonfield Citation1965). In particular, the Istituto per la Ricostruzione Industriale (IRI), Italy's largest state-owned conglomerate, played a key role in the ‘economic miracle’ years, with a substantial presence in almost all production sectors, including the most technologically advanced ones, such as telecommunications and electronics (Rossi and Toniolo Citation1996).

In 1982, the year of its maximum size, IRI operated in 40 per cent of sectors and directly produced 3.6 per cent of Italy's GDP (5 per cent including indirect linkages). Furthermore, it exported more than 20 per cent of its production, double the figure of private enterprises in the same sectors (Pellegrini Citation2015). IRI companies were more capital-intensive than private companies, more likely to be present in high-tech sectors — such as telecommunications, electronics, informatics, robotics, aeronautics, and electronics — invested more in R&D, and had higher labour productivity levels and productivity growth (Antonelli, Barbiellini Amidei, and Fassio Citation2015; Doria and Tolaini Citation2013). The common image of state-owned enterprises as basket cases is misplaced.

At the end of the 1980s, however, IRI companies faced serious problems. Profitability was negatively impacted by excess capacity (especially in the South), which was linked to the strategy of territorial rebalancing between North and South. Debt and interest payments weighed more heavily on the IRI's balance sheet than on private companies, also due to the reduced size of public recapitalisations in the 1980s and 1990s (Ciocca Citation2015, pp. 60–86). Financial problems were concentrated in three sectors: steel (Finsider), shipbuilding (Fincantieri), and cars (Alfa Romeo). The need to support employment led to excessive manpower levels. Ravazzi (Citation2015) has estimated that the net operational profitability of public companies was 5 per cent lower than that of private companies, arguing that this can either be interpreted as a sign of inefficiency or as a fair price to pay for faster accumulation and employment creation in the depressed areas of the South.

One possible response could have been restructuring through targeted privatisations and equity injections into the endowment fund. This strategy had been followed in the 1980s under Romano Prodi's presidency of the Institute, and had produced a return to (small) profits in 1988 (Ciocca Citation2015). However, the political climate of the early 1990s was very different from that of the 1980s. Public opinion was ill disposed towards state ownership, also as a result of the ‘clean hands’ scandal (Tangentopoli), which led to the arrest of IRI's president Franco Nobili in May 1993 (later cleared of all charges). Moreover, a cultural shift was taking place in Italy and elsewhere in favour of private firms. Furthermore, with Italy in a public debt emergency, public recapitalisation was not considered a viable option.

In this context, an important role was played by the European Commission. In the late 1980s the Commission took a more rigid stance with regard to state aid. A survey conducted by the Commission in 1989 found that Italy alone was responsible for 55 per cent of all state aid in the European Community (Curli Citation2013, p. 206). The survey counted all the public contributions to the operating funds of the state-owned enterprises not as equity injections but as state aid.

An ‘Italian case’ emerged in Brussels, leading to several infringement procedures. At the core of the dispute was the incompatibility between European competition rules and Article 2362 of the Italian Civil Code, which established the unlimited liability of the shareholder in the event of the insolvency of a fully owned controlled company. The European Commission ruled that the provision of such unlimited liability gave state-owned companies a competitive advantage over their private competitors in terms of access to finance, allowing them to maintain higher levels of debt than their competitors.

The confrontation was resolved by an agreement between Andreatta (foreign minister) and the European Commissioner for Competition Van Miert in July 1993. The agreement compelled IRI to reduce its debt levels to acceptable limits (around 60 per cent) without injections of public funds, that is, through sales of assets. It contained a detailed list of firms to be privatised by 1997 (Curli Citation2013, p. 256).

The decision to take Italy into the single currency from the beginning also had an impact on privatisation. Italy did not meet the debt criterion, but as a compromise, it was decided to consider a declining debt to GDP ratio as sufficient evidence of debt reduction. Thus, a commitment to speedy privatisations became essential to prove Italy's commitment to debt reduction, and the proceeds of privatisations were earmarked for that purpose. The existence of a link between EMU entry and privatisation has been noted by several scholars (Artoni Citation2013; Barucci and Pierobon Citation2010; Ciocca Citation2015), and there is an explicit trace of it in official government documents (for example, Ministero del Tesoro e della Programmazione Economica Citation1998, p. 71), as well as in accounts of the protagonists. Recently, Romano Prodi described the privatisation process as a European ‘obligation’.Footnote8

Italy ran the second largest privatisation process after the United Kingdom (whose privatisations were concentrated in the 1980s). Privatised companies improved profitability and increased the distribution of dividends to shareholders. However, the size of the investments made were well below planned levels (Barucci and Pierobon Citation2010), suggesting that a short-term profitability orientation prevailed. According to De Cecco (Citation2007, pp. 775–776), privatisation provided Italian private capitalists with an easy way to increase profitability: rather than facing competition in their own markets, they could purchase utility companies (for example, motorways, telecommunications) and pay for them with loans provided by the privatised banks (see also Cavazzuti Citation2013, p. 65).

An example is the privatisation of Telecom Italia. During the 1980s, telecommunications had been at the forefront of Prodi's attempt to reorient IRI towards high-tech sectors and had absorbed 60 per cent of IRI's total investments (Doria and Tolaini Citation2013). The privatisation of Telecom took place in 1997 without a clear direction and the Treasury never used its golden share. The attempt at creating a stable core of Italian private owners failed, and the company changed ownership four times in a few years, with two leveraged buy-outs that left a legacy of high indebtedness, which negatively affected the company's future development. The high level of debt led the company to reduce industrial investments in the 2000s and to drop projects with more uncertain profitability prospects, which, in retrospect, could have guaranteed Telecom a stronger role in the development of innovative technologies and infrastructures. This led to a loss of positive externalities for the country in a crucial sector.Footnote9

As a result, already a few years after the peak of privatisation, all triumphalism had vanished with regard to its ability to modernise Italian capitalism. Serious doubts can also be raised as to the success of privatisation in terms of public debt reduction. The total proceeds of 9.5 per cent of GDP between 1992 and 2001 were non-negligible, but insufficient to make a dent in the debt problem.

Could the outcome of privatisation have been more positive within the constraint? The need to ‘cash out’ quickly in order to reduce debt levels led to privatisations that were carried out without a comprehensive strategy (Cavazzuti Citation2013). In the case of regulated sectors, they took place before a proper regulatory framework had been set up, leaving room for substantial private economic rent and poorly designed incentives. The privatisation of Autostrade per l'Italia (motorways), which was sold to Benetton in 1999, is a clear illustration. The private profits made after privatisation far exceeded the interest savings made possible by the sale of the company (D'Antoni Citation2013).

It is difficult to articulate a credible counterfactual for privatisations. Key actors such as Carli, Andreatta, Ciampi, Barucci, and Prodi fully agreed with the need for privatisation. In 1993, the Italian voters approved a referendum on the abolition of the Ministry of State-owned enterprises by a majority of 90 per cent. Hence, there was ample domestic support for privatisation and it would have probably happened anyway. With the Andreatta-Van Miert agreement, however, the Sword of Damocles of an infringement procedure was placed over the government. This helped to overcome domestic resistance to the sale of state assets, especially from the management of the state-owned companies themselves (Curli Citation2013, p. 255). Without the external constraint, privatisation could have been conducted in a less haphazard fashion and the state could have maintained a controlling share in strategically important companies in key sectors such as telecommunications, thus acting as a source of patient capital for key firms. An indirect confirmation is provided by the fact that after it became clear that the strategy of full privatisation was a failure, the state opted for partial privatisation in the case of the other state-owned conglomerates ENI, ENEL, and Finmeccanica, maintaining a controlling share (Bulfone Citation2017). Differently from the first wave, this second wave of partial privatizations was conducted between the late 1990s and the early 2000s, when participation in EMU had already been secured. After partial privatisation, ENI, ENEL and Finmeccanica (now Leonardo) were able to upgrade and consolidate their international standing, and are today among the few remaining global players Italy has (Pagano Citation2019).

To sum up, we would expect that a different course of action, characterised by a more careful design of the regulatory framework and ownership structure, although possible, would have been implausible given the pressure to enter EMU (sufficient conditions). On the other hand, a less rigid constraint could have slowed down the privatisation process, and perhaps reduced its intensity, but the trajectory of the companies in which the state has retained control makes it difficult to imagine that the Italian presence in cutting-edge sectors could have undergone a more dramatic downsizing (necessary conditions).

4.6. Industrial Relations and Labour Market Policy

When Italy took the decision to reenter the EMS in late 1996, inflation was still a problem. Between 1993 and 1996, the average inflation rate was 4.5 per cent in Italy and 2.6 per cent in Germany and in the other countries about to join the EMU. The implication of fixing the exchange rate and then entering the common currency was that, unless the inflation differential was eliminated or Italian productivity grew faster than in eurozone partners, Italy would experience a loss of competitiveness (captured by the appreciation of the real exchange rate), and this would lead to a deterioration of the current account. In particular, Italy's exports, which are estimated to be highly sensitive to movements of the real exchange rate (with an elasticity of about per cent), particularly in the manufacturing sector (Paternesi Meloni Citation2018), would suffer. In retrospect, loss of competitiveness is exactly what ultimately happened. Until approximately the late 1990s, Italy relied on nominal wage restraint to compensate for the loss of exchange rate flexibility. Institutionalised union cooperation had been very important to help Italy gain access to EMU (Modigliani, Baldassari, and Castiglionesi Citation1996). Just before the financial crisis of 1992, a tripartite pact between government, unions, and employers abolished the wage indexation mechanism (scala mobile), thus facilitating disinflation. In 1993, a tripartite agreement confirmed the abolition of the scala mobile and introduced a new collective bargaining architecture, which linked wage increases to the government's inflation target. In 1996 another tripartite pact began the liberalisation of flexible employment contracts.

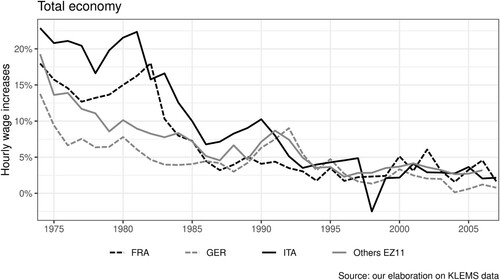

Data on sectoral wages from the KLEMS database reveal that, by the 1990s, Italy had managed to dramatically reduce wage inflation and had brought wage growth into convergence with both Germany and the other ten countries about to join the eurozone (). Furthermore, Italy's real wages grew more slowly than productivity in the 1990s, causing a decline of the wage share from 64 to 59 per cent between 1991 and 1996. The new bargaining structure introduced in 1993, by established that labour productivity gains would no longer be distributed at the industry level, but only at the enterprise or territorial level had the potential to determine such a decline in the wage share.

Figure 6. Yearly increases in Nominal hourly wages (1974–2007). Source: our elaboration on KLEMS data.

The impetus for institutionalised union cooperation declined in the 2000s, due to disagreement among the main union confederations and, above all, a government's shift away from ‘concertation’ towards labour market liberalisation (Baccaro and Howell Citation2017, Ch. 6). In 2003, the Berlusconi government, with full support by Confindustria (the main employer confederation) thoroughly liberalised the use of flexible work contracts.

In 2001–06, Italy's nominal wages grew considerably faster than in Germany (1.4 per cent), although slightly slower than in the other EZ11 countries (3 per cent versus 3.2 per cent per year). The greatest difference was made by the public sector (public administration, education, and health and social work sector), where Italy's hourly wages increased by 4.8 per cent per year, in contrast to 1 per cent in Germany and 3.2 per cent in the other EZ11 countries. The wage share bottomed at 58 per cent in 2001 and then started growing again, reaching 60 per cent in 2006.

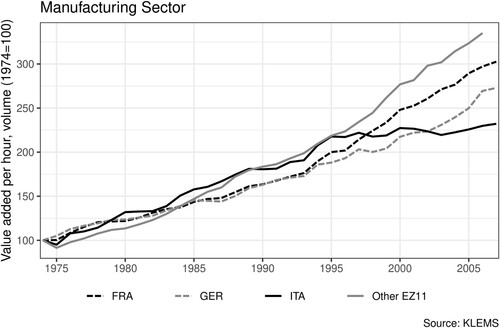

However, Italy's loss of competitiveness was mainly due to the stagnation of labour productivity, not to high wage increases. As shows, between 1974 and 1995 manufacturing sector productivity grew faster in Italy than in Germany and France (3.8 per cent, 3.1 per cent, 3.4 per cent average yearly growth rate, respectively), and in line with the other EZ11 countries. Between 1996 and 2006, however, Italy's productivity growth was only 0.5 per cent per year in contrast to 3.3 per cent for Germany, 3.7 per cent for France, and 3.9 per cent for the remaining EZ11 countries. The real effective exchange rate, which had declined by 42 per cent between 1991 and 1995 and remained stable between 1996 and 2000, increased by 11 per cent between 2001 and 2007.

Figure 7. Labour productivity in manufacturing (1974–2007). Source: KLEMS.

The stagnation of Italian labour productivity is puzzling and there is no consensus explanation, but the heterodox economic literature has highlighted two factors, flexibilisation of employment contracts and demand stagnation, which may account for it. Several studies have concluded that labour market flexibility has a negative impact on labour productivity (for example Lucidi and Kleinknecht Citation2011; Pariboni and Tridico Citation2019; Kleinknecht Citation2020). In Italy, temporary contracts were extensively liberalised.Footnote10 Daveri (Citation2012) has argued that the Italian liberalisation of flexible contracts was intended as a substitute for exchange rate devaluation but failed because it reduced labour productivity.

Advocates of labour market flexibilisation often neglect the effect of labour rigidities (such as high and inflexible wages, protective labour institutions) as a stimulus for labour productivity. The stimulus operates by encouraging investment in physical and human capital, as well as by creating incentives for managers to boost efficiency through reorganisation (Streeck Citation1997).

A second explanation linking labour productivity to the external constraint emphasises the effect of demand compression. As argued by the post-Keynesian literature, demand is positively related to labour productivity through economies of scale (the ‘Kaldor-Verdoorn’ effect). Additionally, the prospect of expanding demand nudges firms to expand their capacity, and the resulting new investments, in turn, incorporate the latest generation of technical progress (Storm and Naastepad Citation2012).

After Italy joined the euro, all components of aggregate demand slowed down (Deleidi and Paternesi Meloni Citation2019). As discussed above, public expenditure growth was contained in an ill-fated attempt to reduce public debt. Exports became more difficult due to the appreciation of the real exchange rate (from the early 2000s on). Other, more endogenous components of aggregate demand also suffered. Household consumption was constrained by limited real wage growth and insufficient increase of debt-financed expenditures; investment was hurt by depressed demand. The extent to which all potential drivers of growth stagnated makes Italy a unique case in comparison with other advanced countries (Baccaro and Pontusson Citation2016).

Could it have gone differently? Italy could perhaps have prevented an appreciation of the real exchange rate by continuing institutionalised nominal wage containment beyond the 1990s, while keeping the efficiency-enhancing labour rigidities in place. The causal link in terms of sufficient conditions relies on the plausibility of such a different course of action. However, the pressure to increase the employment-intensity of growth made flexibilisation of labour contracts difficult to resist; moreover, this task would have been easier to accomplish if Germany had not engaged in ‘internal devaluation’ at the same time, containing its own wage and price growth (Cesaratto and Stirati Citation2010; Flassbeck and Lapavitsas Citation2015).

As to necessary conditions, we ask what would have happened if Italy had not decided to irrevocably fix its exchange rate at the end of 1996. The best counterfactual is again represented by Italy in the four years between late 1992 and late 1996. Both the nominal and the real effective exchange rate declined by 16 per cent between 1992 and 1996 — in other words, Italy gained external competitiveness. This was despite a nominal exchange rate appreciation of 10 per cent in 1996 relative to 1995, which was due to Italy preparing to rejoin the EMS at a parity acceptable to other members of the monetary union (990 lira against the DM). Importantly, the nominal devaluation did not trigger an import prices-wages-domestic price spiral. In fact, the inflation rate declined from 5 per cent in 1992 to 4 per cent in 1996, thanks to institutionalised wage restraint.

Labour productivity grew significantly faster in 1993–96 than in 1997–2007. This is brought out by a regression using KLEMS data for thirty-four sectors, where average yearly labour productivity growth in the two periods is regressed against a period dummy (1 for 1997–2007, 0 for 1993–96), and a dummy proxying for trade exposure (1 if the sector belongs to the manufacturing industry, 0 otherwise) (see ). The coefficient of the period dummy indicates that annual productivity declined significantly by 1.6 per cent on average in 1997–2007 relative to 1993–96, while trade exposure has zero effect. This latter result casts doubt on a direct effect of real exchange rate appreciation on labour productivity at the sectoral level (see also Pellegrino and Zingales Citation2017). It is possible that the reduction of foreign demand for exposed sectors was compensated by a compositional effect whereby less inefficient companies exited and more efficient ones remained.Footnote11

Table 4. Labour productivity growth at the sectoral level (1993–96 vs 1997–2007).

5. Concluding Remarks

In this paper, we have assessed the effects of the external constraint on Italy's economic performance in the past twenty-five years, focussing on three policy areas: public debt, privatisation, and labour market policy. For each policy area, we have reconstructed the process linking the external constraint to outcomes, and assessed its sufficiency and necessity properties.

The decision to enter the ERM in late 1996 and then joining the euro had two contrasting effects on public debt: on the one hand, it reduced interest payments on the large stock of debt; on the other, it probably lowered the growth rate, thus triggering a vicious circle of consolidation, leading to lower growth, requiring further consolidation. With the sovereign debt crisis, the interest advantage evaporated and the spread between Italian and German nominal bond yields returned to the high levels of the early 1990s.

The European Commission's opposition to the particular way state-owned enterprises financed themselves made it almost inevitable for Italy to privatise them. Furthermore, the need to cash in quickly to improve Italy's debt figures on the eve of EMU admission led to hasty privatisation decisions that did not significantly reduce the debt stock, but caused a deterioration of Italy's position in key sectors, such as telecommunications.

The choice to give up the option of currency devaluation made it necessary to increase wage flexibility. Until the 1990s, institutionalised nominal and real wage moderation provided a safety valve. From 2001 on, however, the impetus for wage moderation waned, to be replaced by the liberalisation of flexible contracts. The combination of demand compression and the weakening of efficiency-enhancing rigidities led to a generalised stagnation of labour productivity.

For all three policy areas, it is conceivable that some plausible ‘editing’ of the context would have produced better outcomes. If the effort to reduce (and not simply stabilise) the level of debt had continued in the early 2000s, perhaps Italy would have been less vulnerable to speculative attacks in the early 2010s. Privatisations could have been better conceived and implemented to prevent Italian family capitalism to acquire control of protected public utilities (sometimes through leveraged buyouts). Finally, if institutionalised nominal wage restraint had continued in the 2000s as well, and the proliferation of flexible contracts had been discouraged, perhaps the slowdown of productivity could have been avoided. In brief, the external constraint could have been better managed.

Overall, however, it seems implausible that Italy would have experienced the same degree of economic decline in the absence of the external constraint. If the country had decided not to enter EMU — for example, remaining in the ERM, as Denmark did — the growth rate would probably have been higher and the management of public debt easier, at least in the long run. In particular, the deleterious effects of the sovereign debt crisis could have been avoided. Without the external constraint, Italy would probably not have rushed into full privatisation of key enterprises, but partial privatisations would have preserved the role of the state as provider of ‘patient capital’ for key firms. If Italy had maintained the possibility to correct for nominal divergences by adjusting the exchange rate, at least the depressing effect of aggregate demand compression on productivity could have been avoided. The comparison with the 1993–96 period suggests that Italy had better economic outcomes when economic turbulence forced it to give up the external constraint than in the years that followed.

Recent survey evidence suggests that support for the euro has a clear income and class bias (Baccaro, Bremer, and Neimanns Citation2021a). The perception of having benefited from the euro grows with income and is highest among self-employed professionals and large employers, technical (semi-)professionals, and associate managers, while production and service workers and small business owners are much less likely to report that they have benefited from the euro. In brief, in Italy support for the euro is concentrated among the economically better off and, with regard to partisan choice, among voters of the centre-left.Footnote12 In turn, the more a person has benefited from the euro, the more likely she/he is to report that she/he would vote to remain in the euro in a hypothetical referendum (Baccaro, Bremer, and Neimanns Citation2021b). Importantly, the majority of Italian voters report that they have not benefited from the euro, which makes support for the single currency rather fragile.

With the benefit of hindsight, the choice to tie the country's hands to the European mast appears an ill-conceived bet that produced none of the anticipated benefits and several unintended negative consequences. This, of course, does not necessarily mean that a reversal of that choice is desirable or even possible now. Nevertheless, understanding what went wrong is crucial to guide future choices.

Supplemental Material

Download PDF (67.1 KB)Acknowledgments

Many thanks to Roberto Artoni, Fabio Bulfone, Sergio Cesaratto, Sinisa Hadziabdic, Martin Höpner, Renate Mayntz, Ugo Pagano, Michele Salvati, and Fritz Scharpf for comments on a previous version. The final version improved thanks to the comments received from two anonymous referees. All responsibility for the analysis lies with the authors.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 The focus on total factor productivity (TFP), that is, the ‘Solow residual’, is common to most of this literature. TFP is interpreted as a measure of how efficiently production inputs (labour and capital) are used. Yet, as shown analytically by Storm (Citation2017, pp. 9–14), the growth of TFP depends on aggregate demand factors, specifically on the rate of capacity utilisation (which also influences the investment rate). This implies that when aggregate demand is depressed, TFP growth will stagnate, too. For this reason, in this paper we prefer to focus on labour productivity as opposed to TFP.

2 Our approach to counterfactual analysis is inspired by Montoya and Mahoney (Citation2020), especially as regards the analysis of causal effects in terms of properties of sufficiency and necessity, and as regards the notion of ‘counterfactual rewrite of history’. However, the external constraint cannot be considered a critical event in the sense of Montoya and Mahoney (Citation2020), but rather a process involving several steps, as the next section will clarify.

3 If X is a sufficient condition, an inconsistent outcome is (X leads to non-Y). If X is a necessary condition, an inconsistent outcome is

(non-X leads to Y).

4 The validity of the 1993–96 counterfactual is not undermined by different levels of capital account openness. Italy liberalised its capital account in the early 1990s, as a result of its ratification of the Single European Act. Thus, when Italy was ejected from the EMS in September 1992 and forced to float its exchange rate, it already operated under full capital mobility, which in principle restricted its macroeconomic room for maneuver. As shown e.g., by the Chinn-Ito index, a measure of financial openness, by 1993 Italy had reached the maximum value of capital account liberalisation in the sample, joining some early liberalisers like Germany and the UK (http://web.pdx.edu/ito/Chinn-Ito_website.htm).

5 The data used for this section come from various sources: IMF WEO database, OECD.Stat, AMECO database, Eurostat, Istat, and Bank of Italy for data on public finance and debt before 1995.

6 As in other advanced countries, raising taxes was highly unpopular. Italy tax revenue as a percentage to CGP was aligned to the average of Euro area, but the structurally high level of tax evasion concentrated tax payment among dependent employees. While the centre-left government that steered entry into EMU relied on tax increases to reach this goal, the Berlusconi government successfully campaigned on a platform of lower taxes, attracting a constituency of small business owners and public sector employees. This made unlikely that Italy could have implemented a ‘Nordic’ strategy of high taxes and high spending (Baccaro and Bulfone Citation2022).

7 is based on the IMF database on fiscal consolidation, which records episodes of fiscal adjustment on the basis of the ‘narrative method’, aimed to minimise the problem of endogeneity of fiscal adjustment measures (Guajardo, Leigh, and Pescatori Citation2011).

8 In an interview to the TV programme: ‘Mezz'Ora in più’ on 27 October 2019.

9 An example of a wrong strategic decision was the discontinuation of Socrates (based on optical fibre), to which the more profitable but more limited DSL technology was preferred (Mariotti Citation2013).

10 The OECD index of strictness of employment protection for temporary workers declined by 66% (i.e., from 4.75 to 1.63) between 1995–2017, which is the highest percentage decline among advanced countries in this period, see https://stats.oecd.org/Index.aspx?DataSetCode=EPL_T, accessed on Feb 3, 2021.

11 Data from the OECD STAN database suggest that faster export growth in 1993–96 did not have a significant impact on labour productivity. The relation between sector-level export orientation and labour productivity growth shows only a weak and not statistically significant positive relation between the two variables (see Appendix online).

12 Voters of the right (Lega and Fratelli d'Italia) are most likely to express negative attitudes towards euro, while voters of the centre-left and liberal centre (Partito Democratico and Italia Viva), mostly pensioners and public sector workers, are on the opposite side of the spectrum. Voters of Forza Italia and Movimento Cinque Stelle are in an intermediate position, but closer to the Lega's voters than the PD's.

References

- Alesina A., and F. Giavazzi. 2006. The Future of Europe: Reform Or Decline. Cambridge, MA: MIT Press.

- Amatori F., M. Bugamelli, and A. Colli. 2013. ‘Technology, Firm Size, and Entrepreneurship.’ In The Oxford Handbook of the Italian Economy since Unification, edited by G. Toniolo. Oxford: Oxford University Press.

- Antonelli C., F. Barbiellini Amidei, and C. Fassio. 2015. ‘L'IRI, la ricerca, lo sviluppo tecnologico, la crescita (1950–1994). Esternalità e governo della conoscenza.’ In Storia dell'IRI, Vol. 5, edited by F. Russolillo. Bari: Laterza.

- Armingeon K., L. Baccaro, A. Fill, J. Galindo, H. Stefan, and R. Labanino. 2019. ‘Liberalization Database 1973–2013.’

- Artoni R. 2013. ‘Un profilo d'insieme.’ In Storia dell'IRI, Vol. 4, edited by R. Artoni. Bari: Laterza.

- Baccaro L., B. Bremer, and E. Neimanns. 2021a. ‘Better off vs. Left Behind? Patterns of Support for the Euro in Italy and Germany.’ Max Planck Institute for the Study of Societies, Unpublished Paper.

- Baccaro L., B. Bremer, and E. Neimanns. 2021b. ‘Till Austerity Do Us Part? A Survey Experiment on Support for the Euro in Italy.’ European Union Politics 22 (3): 401–423.

- Baccaro L., and F. Bulfone. 2022. ‘Growth and Stagnation in Southern Europe: The Italian and Spanish Growth Models Compared.’ In Diminishing Returns: The New Politics of Growth and Stagnation, edited by L. Baccaro, M. Blyth, and J. Pontusson. Oxford: Oxford University Press.

- Baccaro L., and C. Howell. 2017. Trajectories of Neoliberal Transformation: European Industrial Relations After the 1970s. Cambridge, UK: Cambridge University Press.

- Baccaro L., and J. Pontusson. 2016. ‘Rethinking Comparative Political Economy: The Growth Model Perspective.’ Politics & Society 44 (2): 175–207.

- Bagnai A. 2016. ‘Italy's Decline and the Balance-of-Payments Constraint: A Multicountry Analysis.’ International Review of Applied Economics 30 (1): 1–26.

- Barta Z. 2018. In the Red: The Politics of Public Debt Accumulation in Developed Countries. Ann Arbor, MI: University of Michigan Press.

- Barucci E., and F. Pierobon. 2010. Stato e mercato nella Seconda Repubblica. Dalle privatizzazioni alla crisi finanziaria. Bologna: Il Mulino.

- Bulfone F. 2017. ‘The State Strikes Back: Industrial Policy, State Power and the Emergence of Competitive Multinational Enterprises in Italy and Spain.’ PhD Thesis, Department of Political and Social Sciences, EUI, Florence.

- Calligaris S., M. Del Gatto, F. Hassan, G. I. P. Ottaviano, and F. Schivardi. 2018. ‘Italy's Productivity Conundrum: A Study on Resource Misallocation in Italy.’ Economic Policy 33: 635–684.

- Capussela A. L. 2018. The Political Economy of Italy's Decline. Oxford: Oxford University Press.

- Carli G. 1993. Cinquant'anni di vita italiana. Bari: Laterza.

- Cavazzuti F. 2013. ‘Le privatizzazioni degli anni Novanta: L'IRI tra Parlamento, Governo e dintorni.’ In Storia dell'IRI, Vol. 4, edited by R. Artoni. Bari: Laterza.

- Cesaratto S., and A. Stirati. 2010. ‘Germany and the European and Global Crises.’ International Journal of Political Economy 39 (4): 56–86.

- Cesaratto S., and G. Zezza. 2019. ‘Farsi male da soli. Disciplina esterna, domanda aggregata e il declino economico italiano.’ L'industria 2: 279–318.

- Ciocca P., ed. 2015. Storia dell'IRI. Vol. 6. Bari: Laterza.

- Culpepper P. D. 2010. Quiet Politics and Business Power: Corporate Control in Europe and Japan. New York: Cambridge University Press.

- Curli B. 2013. ‘Il ‘vincolo europeo’: le privatizzazioni dell'IRI tra Commissione europea e Governo italiano.’ In Storia dell'IRI, Vol. 4, edited by R. Artoni. Bari: Laterza.

- D'Antoni M. 2013. ‘Privatizzazione e monopolio. Il caso della Società Autostrade.’ In Storia dell'IRI, Vol. 4, edited by R. Artoni. Bari: Laterza.

- Daveri F. 2012. ‘La flessibilità parziale del mercato del lavoro, un inefficace sostituto della svalutazione.’ In Il modello di sviluppo dell'economia italiana quarant'anni dopo, edited by M. Messori. Milano: Egea.

- De Cecco M. 2007. ‘Italy's Dysfunctional Political Economy.’ West European Politics 30 (4): 763–83.

- De Grauwe P. 2012. ‘The Governance of a Fragile Eurozone.’ Australian Economic Review 45 (3): 255–268.

- Deleidi M., and W. Paternesi Meloni. 2019. ‘Produttività e domanda aggregata: una verifica della legge di Kaldor-Verdoorn per l'economia italiana.’ Economia & Lavoro 2: 25–44.

- Di Martino P., and M. Vasta. 2015. ‘Wealthy by Accident? Firm Structure, Institutions, and Economic Performance in 150(+4) Years of Italian History: Introduction to the Special Forum.’ Enterprise & Society 16 (2): 215–24.

- Doria M., and R. Tolaini. 2013. ‘Riposizionamento e ristrutturazione del gruppo negli anni Ottanta. Priorità e vincoli.’ In Storia dell'IRI, Vol. 3, edited by F. Silva. Bari: Laterza.

- Dyson K., and K. Featherstone. 1999. The Road to Maastricht. Negotiating Economic and Monetary Union. Oxford: Oxford University Press.

- Faini R., and A. Sapir. 2005. ‘Un modello obsoleto? Crescita e specializzazione dell'economia italiana.’ In Oltre il declino, edited by T. Boeri, R. Faini, A. Ichino, G. Pisauro, and C. Scarpa. Bologna: Il Mulino.

- Ferrera M., and E. Gualmini. 1999. Salvati dall'Europa? Bologna: Il Mulino.

- Flassbeck H., and C. Lapavitsas. 2015. Against the Troika: Crisis and Austerity in the Eurozone. London: Verso.

- Giavazzi F., and M. Pagano. 1990. ‘Can Severe Fiscal Contractions be Expansionary? Tales of Two Small European Countries.’ In NBER Macroeconomics Annual 1990, Vol. 5, edited by O. J. Blanchard and S. Fischer. National Bureau of Economic Research.

- Girardi D., W. Paternesi Meloni, and A. Stirati. 2020. ‘Reverse Hysteresis? Persistent Effects of Autonomous Demand Expansions.’ Cambridge Journal of Economics 44 (4): 835–869.

- Graziani A., and F. Meloni. 1980. ‘Inflazione e fluttuazione della Lira.’ In I difficili anni '70, edited by G. Nardozzi. Milano: ETAS.

- Guajardo J., D. Leigh, and A. Pescatori. 2011. ‘Expansionary Austerity: New International Evidence.’ International Monetary Fund, Working Paper WP/11/158.

- Haack S. 2012. ‘The Embedded Epistemologist: Dispatches From the Legal Front.’ Ratio Juris 25 (2): 206–35.

- Kleinknecht A. 2020. ‘The (Negative) Impact of Supply-Side Labour Market Reforms on Productivity: An Overview of the Evidence1.’ Cambridge Journal of Economics 44 (2): 445–464.

- Kreuzer M. 2016. ‘Assessing Causal Inference Problems with Bayesian Process Tracing: the Economic Effects of Proportional Representation and the Problem of Endogeneity.’ New Political Economy 21 (5): 473–83.

- Lange P., and M. Vannicelli. 1982. ‘Strategy under Stress: The Italian Union Movement and the Italian Crisis in Developmental Perspective.’ In Unions, Change, and Crisis: French and Italian Union Strategy and the Political Economy, 1945–1980, edited by P. Lange, G. Ross, and M. Vannicelli. Boston: George Allen and Unwin.

- Lucidi F., and A. Kleinknecht. 2011. ‘Little Innovation, Many Jobs: An Econometric Analysis of the Italian Labour Productivity Crisis.’ Cambridge Journal of Economics 34 (3): 525–46.

- Mackie J. L. 1965. ‘Causes and Conditions.’ American Philosophical Quarterly 2 (4): 245–64.

- Mariotti S. 2013. ‘Politiche di privatizzazione e competitività dell'industria italiana.’ In Storia dell'IRI, Vol. 4, edited by R. Artoni. Bari: Laterza.

- Ministero del Tesoro e della Programmazione Economica. 1998. ‘Documento di Programmazione Economico-Finanziaria per gli anni 1999-2001.’

- Modigliani F., M. Baldassari, and F. Castiglionesi. 1996. Il miracolo possibile. Bari: Laterza.

- Montoya L. G., and J. Mahoney. 2020. ‘Critical Event Analysis in Case Study Research.’ Sociological Methods and Research. https://journals.sagepub.com/doi/abs/https://doi.org/10.1177/0049124120926201

- Pagano U. 2019. ‘Proprietà e controllo delle grandi imprese: un'interpretazione del resistibile declino italiano.’ L'industria 40 (2): 223–51.

- Pariboni R., and P. Tridico. 2019. ‘Structural Change, Institutions and the Dynamics of Labor Productivity in Europe.’ Journal of Evolutionary Economics. Vol. 30, pp. 1275–1300. https://link.springer.com/article/https://doi.org/10.1007/s00191-019-00641-y

- Paternesi Meloni W. 2018. ‘Italy's Price Competitiveness: An Empirical Assessment Through Export Elasticities.’ Italian Economic Journal 4 (3): 421–62.

- Pellegrini G. 2015. ‘Il ruolo dell'IRI nell'economia italiana: un'analisi multisettoriale (1982).’ In Storia dell'IRI, Vol. 5, edited by F. Russolillo. Bari: Laterza.

- Pellegrino B., and L. Zingales. 2017. ‘Diagnosing the Italian Disease.’ National Bureau of Economic Research, Working Paper 23964.

- Ravazzi P. 2015. ‘Analisi dei bilanci delle imprese private e pubbliche nel periodo 1973–1992.’ In Storia dell'IRI, Vol. 5, edited by F. Russolillo. Bari: Laterza.

- Rossi N., and G. Toniolo. 1996. ‘Italy.’ In Economic Growth in Europe since 1945, edited by N. Crafts and G. Toniolo. Cambridge, UK: Cambridge University Press.

- Salvati M. 2012. ‘Le origini lontane del ristagno economico presente.’ In Il modello di sviluppo dell'economia italiana quarant'anni dopo, edited by M. Messori and D. B. Silipo. Milano: Egea.

- Sapir A. 2018. ‘High Public Debt in Euroarea Countries: Comparing Belgium and Italy.’ Policy Contribution 15, Bruegel.

- Scharpf F. W. 1999. Governing the European Union. Effective and Democratic? Oxford: Oxford University Press.

- Shonfield A. 1965. Modern Capitalism. The Changing Balance of Public and Private Power. London: Oxford University Press.

- Storm S. 2017. ‘The New Normal: Demand, Secular Stagnation and the Vanishing Middle-Class.’ Institute for New Economic Thinking, Working Paper 55.

- Storm S. 2019. ‘Lost in Deflation: Why Italy's Woes Are a Warning to the Whole Eurozone.’ Institute for New Economic Thinking, Working Paper 94.

- Storm S., and C. W. M. Naastepad. 2012. Macroeconomics Beyond the NAIRU. Cambridge, MA: Harvard University Press.

- Streeck W. 1997. ‘Beneficial Constraints: On the Economic Limits of Rational Voluntarism.’ In Contemporary Capitalism: The Embeddedness of Institutions, edited by J. R. Hollingsworth and R. Boyer. Cambridge: Cambridge University Press.

- Talani L. S. 2017. The Political Economy of Italy in the Euro. London: Palgrave.

- Toniolo G. 2013a. ‘An Overview of Italy's Economic Growth.’ In The Oxford Handbook of the Italian Economy since Unification, edited by G. Toniolo. Oxford: Oxford University Press.

- Toniolo G., ed. 2013b. The Oxford Handbook of the Italian Economy Since Unification. Oxford: Oxford University Press.

- Zingales L. 2012. A Capitalism for the People. New York: Basic Books.