?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The article is focused on what it terms a conflictual distributional approach to inflation and economic activity. It presents a brief discussion of the relationships between conflictual approaches and the mainstream approaches. It then makes some remarks on the macro-economic and micro-economic aspects of the analysis of inflation and the role of money. Analyses of price setting and wage determination are brought together to provide employment and real wage levels whereby claims on income are mutually consistent. The framework is utilised to discuss sources of inflationary pressure and the roles of capacity and demand.

1. Introduction

This article considers the contributions of perspectives on inflation in which distributional struggles play a major role. There is often what is termed a conflict theory of inflation; however, it can be expanded to include a conflictual distributional approach to inflation. It is also recognised that the conflictual approach builds on a general perspective of a conflictual society, and that there are many formulations of such an approach that share some common features but also differ in terms of specific representation.

The article begins with reflections on discussions of inflation (Section Two) and the ways in which conflictual claims over income distribution have been downplayed in most approaches to analysis of inflation. When price setting and wage determination are considered, there appear to be divergent claims regarding income shares that have to be reconciled in some way. However, mainstream analyses have ignored or downplayed the consequences of these divergent claims. Section Three provides some general considerations to bear in mind when analysing inflation. Section Four presents a discussion of the analysis of price and wage determination and the factors that influence the outcomes. Section Five brings together price and wage determination to consider what is termed an inflation barrier (a constant inflation level of employment) and discuss inflation dynamics. Section Six provides some concluding commentary.

2. Historical Reflections

Although conflict approaches to inflation became explicit during the 1970s and some contrast with dominant approaches at the time involving some form of Phillips curve and monetarism (with the stock of money being the major causal factor for inflation), they played a rather limited role in general macro-economic discussions on inflation. For example, Laidler and Parkin (Citation1975), in their major review of inflation, placed monetarism, expectations on inflation and excess demand centre stage, and largely ignored any approach that could be linked with a conflict approach, with the exception that studies of wage inflation and trade union strength were included. According to them, ‘Inflation is a process of continuously rising prices, or equivalently, of a continuously falling value of money. … . Inflation is, then, fundamentally a monetary phenomenon’ (p. 741). A statement such as this casts the study of inflation within the macro-economic realm; that is, it is a study between two aggregates (money and price level) for which there is no micro-economic counterpart. It places the relationship between money and prices as central rather than, say, prices and wages — a monetary phenomenon rather than an income distribution issue. Laidler and Parkin made little suggestion of a conflictual approach, although the role played by trade unions in wage inflation was brought in. They quoted Harrod — ‘[the] new wage–price explosion is altogether unprecedented … the causes [of which] are sociological [and] first cousins to the causes of such things as student unrest’ (I972, p. 44) — and then ignored the point.

Approaches to inflation have often been formulated in terms of a Phillips curve, though what is meant by that curve (price or wage inflation, role of expectations, measure of economic activity) and the perceived mechanism underlying it has various explanations. The Phillips curve being a single-equation approach is not suggestive of a conflict concerning income shares. And, in its Friedman (Citation1968) formulation, it becomes associated with a ‘natural rate of unemployment’, which bears a strong similarity to labour market clearing and full employment, and lack of a medium to long-run trade-off between inflation and unemployment. The new Keynesian Phillips curve focuses mainly on price inflation and its relationship with expected inflation and the output gap, and makes the assumption of marginal costs increasing with output. An extension to wage inflation is provided in Galí (Citation2015, Chapter 6), based on the assumption that workers ‘face Calvo-type constraints on the frequency with which they can adjust nominal wages’. Price and wage inflation equations can be placed together to yield equilibrium involving output gap and profit share. However, in comparison to the conflict approach discussed below, this is analysed in the context of a closed economy. Approaches such as those represented in Blanchard, Amighini, and Giavazzi (Citation2021) utilise a wage and price level equation. Here, the equality of the wage–price ratio is asserted, from which a ‘natural rate of unemployment’ is then derived, though one which bears little resemblance to Friedman’s concept. In the simple formulation, the wage–price ratio is effectively set by the pricing decision and the wage decision has to be brought into line through the rate of unemployment. While there is potential conflict regarding the wage–price ratio, little attention is paid to that. Formulations such as that of Layard, Nickell, and Jackman (Citation[1991] 2005) were based on price- and wage-setting behaviour and claims regarding income shares (real product wage) were conflictual but seen to be mutually compatible at the so-called (and mis-named) non-accelerating inflation rate of unemployment (NAIRU). When price- and wage-setting behaviour are portrayed in terms of a relationship between prices and wages, then there is inevitably a degree of conflict. The conflict has tended to be downplayed, and little attention has been given to inflationary processes. Instead, the focus shifted to the operations of the labour market, role of employment protection, etc. and implications for the rate of unemployment.

The emergence of a conflict approach to inflation largely arose on the political left (at least within the UK). Rowthorn (Citation1977b), in the chapter entitled ‘Inflation and crisis’, cites debates in Marxism Today and provides a general perspective. In his paper entitled ‘Conflict, inflation and money’, Rowthorn (Citation1977a) started from the view that ‘conflict is endemic in the capitalist system and concerns all aspects of economic life’ (p. 215). In his approach, inflation rises as a result of the competing claims of workers and capitalists, summarised by the term ‘aspiration gap’. ‘The aspiration gap is determined by the market power of workers and capitalists, and their willingness to use this power. Thus, anything which affects the extent or use of power will affect the aspiration gap and, through it, the rate of inflation’ (215). The scale of the aspiration gap depends on the level of demand providing a route through which level of demand impacts inflation. Taxes and the terms of trade impact the share of income available for post-tax wages and profits, and workers and capitalists seek higher wages or prices to compensate for reduction in real disposable income arising from higher taxes and higher import costs.

My own thinking about inflation and a conflict approach was strongly influenced by the results of empirical work on wage and price inflation in the UK in which I was involved in the second half of the 1970s and into the 1980s. In Henry, Sawyer, and Smith (Citation1976) a range of inflation theories, including both price and wage inflation estimations, were empirically tested for the UK during the period from the late 1940s to the mid-1970s. Simple versions of the Phillips curve (rate of wage change as a function of the unemployment rate and expected inflation) and a monetarist formulation with the stock of money influencing the rate of price inflation were examined and found empirically wanting in our study. We estimated a ‘target real wage’ approach (as, for example, equation 5 below). This approach had not been extensively used at the time, and we drew on Sargan (Citation1964), which had been more of an econometric exploration. It incorporated an error correction mechanism, and indeed was one of the first applications of that technique. As such, it portrays money wages adjusting towards a ‘target’ real wage in light of price inflation expectations, with the process of adjustment influenced by the rate of unemployment. Unemployment plays a constraining role in relation to wage inflation but unemployment reflects (inversely) workers’ bargaining power. In the Phillips curve, unemployment is generally seen as reflecting demand (or, as in Lipsey Citation1960, excess demand for labour). One of the properties of the simple Phillips curve is that, for low rates of unemployment, wages rise faster than (expected) prices, and the real wage (wage to price ratio) rises. Low unemployment would lead to real wages rising year after year. In the excess demand view, a higher real wage would lead to a fall in demand for labour and thereby a rise in unemployment. This adjustment process is clearly absent in the target real wage approach, the implications of which are described below.

In Sawyer with Aaronovitch and Samson (Citation1983) (and also Sawyer et al., Citation1982), price change equations were estimated for 40 UK manufacturing industries over the period 1966 to 1975 on a quarterly basis. In Chapter 2 they argued that price determination can be viewed as a mark-up over unit costs from a wide range of theoretical perspectives. Lee (Citation1998), in his survey of pricing behaviour, confirms that. With ‘target’ price (that is, the price the firm believes to be in its own interests) set as a mark-up over costs, then change in price is related to change in costs and adjustment of price towards the ‘target’ relationship with costs. For example, using a profit maximisation approach, the target price would be a mark-up (depending on price elasticity of demand) over (marginal) costs. One feature of looking at price change at the industry level is that differences between industries in terms of response of price to cost and demand changes. It also reveals that, at the firm/industry level, changes in unit labour costs are relatively unimportant to price changes (to the extent that, on average, a 1 per cent change in unit labour costs leads to a circa 0.2 per cent change in price; this relates to manufacturing) and input prices are rather more important. This is perhaps not surprising in light of the ratio of labour costs to sales revenue.

These empirical studies indicated that price and wage formation had to be approached separately (and hence any single-equation representation, however arrived at, would be inadequate), and conflicting claims would exist regarding income shares. It becomes self-evident that the ‘target’ relationship between price and costs has an implication for the wage–price ratio and the ‘target real wage’ has implications for the wage–price ratio. There is an inevitable conflict between the income claims of these two groups.Footnote1 On the price determination side, while there was a basic mark-up pricing approach, the patterns differed across industries, including whether higher economic activity would be associated with higher prices.

The conflict concerning income shares between workers and capital is placed centre stage in the domestic economy. The pricing decisions, however, depend on wages, domestic input prices and prices of imported goods and services, including commodities, semi-finished and finished goods. The sometimes dramatic rise in some global prices (and often subsequent reversals) has substantial effects on domestic inflation through pricing decisions. Government, via taxation decisions, can affect conflictual claims, as will be briefly mentioned below.

3. Some General Considerations on Inflation Analysis

3.1. Inflation and Macro-economics

The study of inflation is regarded as belonging in macro-economics rather than micro-economics textbooks. As Weber and Wasner (Citation2023) note, ‘the dominant view of inflation holds that it is macroeconomic in origin and must always be tackled with macroeconomic tightening’ (p. 103). The macro-economic origins are located in the level of aggregate demand and/or the stock of money. The policy responses to inflation currently focus on the use of monetary policy and interest rates, but at other times have included deflationary fiscal policies and control of the growth of the money supply.

Pasinetti (Citation1974) described his approach to analysis as

not ‘macro-economic’ in the sense of representing a first simplified rough step towards a more detailed and disaggregated analysis. It is macro-economic because it could not be otherwise. Only problems have been discussed which are of a macro-economic nature; an accurate investigation of them has nothing to do with disaggregation. They would remain the same — i.e. they would still arise at a macro-economic level — even if we were to break down the model into a disaggregated analysis and therefore introduce the necessary additional information (or assumption) about consumers’ choice of goods and producers’ choice of techniques. (p. 118)

The monetarist approach to inflation is macro-economic in nature: a relationship such as MV = PT is macro-economic, and the implied direction of causation runs from M to P. As monetarists argue, an upward change to some prices will not cause inflation for a given money supply because some other prices will need to fall to ensure consistency with MV = PT. Post-Keynesians and many others would, of course, deny the perceived exogenous nature of money and would view the direction of causation running from changes in some prices to changes in money stock (as evidenced in, for example, Hasan Citation1999; Hoover Citation1991).

A change in the general level of demand (‘aggregate demand’) would have widespread effects on prices, production and employment. The effects of such a general change occur via decisions made by firms and others on price. Changes in relative prices can exist as firms may be in different positions in terms of output relative to capacity, and variations across different sectors of the economy may occur in response to how far level of demand has changed.

Viewed in this way, counter-inflation policies could focus on control of individual prices. Attempts at price and incomes policies, particularly from the 1950s to the 1970s, did indeed seek to limit price rises (over a year say) in line with the government’s inflation target.

The macro-economic relations in a conflict approach (as indeed in the NAIRU approach) relate to the derivation of what is termed the constant inflation rate of employment (CIRE), which relates to the level of economic activity (measured by employment rate) and income distribution at which inflation would be constant. This is macro-economic in the sense that there is no corresponding micro-economic relationship.

3.2. Money

A conflict approach to inflation, like most theories of inflation, has to be located within an endogenous money framework. Higher prices and wages have to be financed and paid for, and that applies to all theories of inflation other than a monetarist theory from some form of ‘helicopter money’. Specifically, money in the form of commercial bank deposits (in a current account) is created through the loans process, and destroyed though the repayment of loans. Producers require initial finance (to use circuitist terminology) to cover costs of production, and rising costs of production (whether as a result of costs rising or through purchase of inputs to enable higher output) and banks can provide loans to enable that initial financing. With a reflux mechanism, the loans would be repaid and the stock of money would not rise. Any desire by the public to hold (‘demand’) more money (in the form of bank deposits), say for transaction demand purposes, would mean the reflux mechanism would be incomplete and there would be some increase in the stock of money.

3.3. Conflictual, Income Distribution and Inflation

Conflictual claims over income shares are ever present, with degrees of reconciliation between the competing claims, as suggested in the model below (and many others). When competing claims are mutually consistent, which can be interpreted as a form of ‘stand-off’, each party views the cost of pushing up their share of income as too much. In the CIRE below, there is a possible reconciliation between employment level and the wage–price ratio, and inflation (price and wage inflation) is portrayed as constant when the economy operates at that employment level and wage–price ratio. The reconciliation of income shares can be disturbed in many ways: shifts in the target real wage and pressures to achieve it, shifts in target profit margins, and moves in the prices of imported goods and services are amongst the factors mentioned below. A move in the level of demand from that consistent with the CIRE would involve rising (higher demand) or falling (lower demand) inflation. It is rising inflation rather than level of inflation that arises from conflict when one party pushes for an increased income share. The level of inflation that eventually results is path dependent when inflation rises and, subsequently, when measures such as demand deflation are taken to reduce it.

4. Price and Wage Behaviour

This section considers price-setting behaviour and then wage determination. In each case, I start with a general formulation. It must be stressed that price setting is undertaken in numerous ways, depending on firms’ motivation, interdependences between firms, industrial structure, etc. In a similar vein, wage determination comes in many forms ranging from close to a spot market through to collective bargaining. Seeking to provide an aggregate representation of price and wage setting necessarily involves severe aggregation issues thus, at best, the economy-level representation below can only be indicative. It also the case that there are differences in price and wage determination over time and space, and social, political and institutional factors will have a bearing on those determinations. As argued above, the aggregate representation of price setting is not a macro-economic relationship but, rather, is based on summation of micro-economic relations. The price level is built up as an average of individual prices, and then price inflation is the rate of change of that price level. Further, price changes in one sector depend on wage and cost changes, and some of those cost changes reflect price changes in other sectors.

4.1. Price Setting

Firms set prices seeking to achieve their profit, growth and market share objectives. The target price of a firm can be portrayed as a mark-up over unit costs, with the specific formulation dependent on the objectives of the firm. As a general formulation, the target price at the level of the firm that would aid the firm to achieve its objectives is portrayed as a mark-up of price over unit costs. Formulations of this form can arise from profit maximisation under different industrial structures through to average cost pricing.

The general production relationship at the firm level is viewed in terms of output depending on labour inputs, intermediate domestic inputs, imported inputs and scale of capital stock. A general formulation for what may be termed the target price of firm i is:

(1)

(1) where qi is output of firm, li labour input; di is intermediate domestic inputs with price ci; zi is imported inputs with price fi and m mark-up over costs, where the mark-up depends on the measure of capacity utilisation; and dmi is degree of monopoly/market power. The mark-up may decline with higher capacity utilisation initially, then be broadly constant and then rise with capacity utilisation.

Viewed at the firm/sector level, the following (obvious) points arise. A rise in demand facing that sector could well raise profit margin. Price–price spirals may occur whereby one sector’s output price becomes another sector’s input price.

Allowing for different types of labour and input, and recognising that prices of domestic inputs are similarly based, the price equations are expressed in matrix notation:

(2)

(2) where p is vector of prices; elements of A refer to the domestic inputs plus mark-up (i.e., corresponding to the term dm in equation (1)); w is vector of wage rates and B is matrix of labour inputs plus mark-up (corresponding to mi..li.); f is vector of foreign input prices and C is matrix of foreign input requirements plus mark-up (mi.fi. in the above). This provides:

(3)

(3) In general, the elements of the matrices are dependent on output in the relevant sector. This would imply that an expansion of demand would have effects on relative prices, and that the effects would also depend on changes in the composition of demand. This equation clearly refers to price levels. Changes in price result from adjustments of actual prices towards the ‘target’ prices, and also from changes in profit margins, wages and foreign input prices. The rate of change over a given period (i.e., what is calculated as the rate of inflation) depends on the speed of adjustment. From the p vector, price of consumption goods could be highlighted and a consumer price index derived therefrom. The price of investment goods could be treated similarly.

An equation such as (3) should serve as a reminder of the interrelationships between prices and that the feed-through of wages and foreign prices into prices is likely to be subject to lags. More significantly, however, changes in foreign prices will have differential effects on relative prices. A change in relative prices can be significant in terms of income distribution; consider the effects of energy and food prices in the recent inflationary episode.

Expectations (of future costs and prices) may not play significant role. Price here is that at which the product concerned is offered, and can be readily changed. Expectations can be seen to be relevant when price is contracted for a significant period ahead, and the producer (and also the purchaser) pays some attention to the prices expected to appertain during the contracted period. When prices can be adjusted frequently, then expectations regarding the future course of prices are downgraded in significance, and prices respond to actual cost changes.

The relationships involved in equation (3) are complex and do not afford simple aggregate representation. I postulate that a relationship of the general form exists between rp (retail prices) and wages (index); rp/w is a U-shaped function of level of output and is dependent on the ratio of foreign input prices to wages.Footnote2 In turn, level of output is treated as linearly related with total employment:

(4)

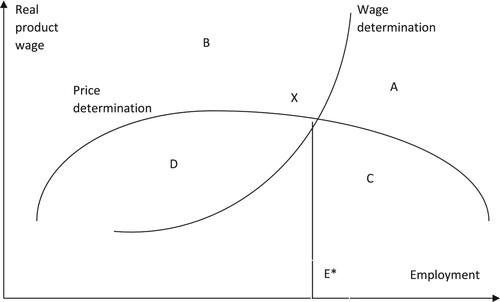

(4) where rp is index of retail prices, Q is aggregate output, Q* is capacity output, w is wage index, L is employment, f is index of imported prices and z is imported inputs. Equation (4) can be re-arranged to express w/rp in terms of employment and ratio of imported prices to wages. This is illustrated in and labelled price determination.

Figure 1. Price determination and wage determination curves. In zone A: ;in zone B:

;in zone C:

; andin zone D:

.

At any point in time, firms would be some way off their target price, and would be adjusting towards the target price. In terms of the price determination curve, when the wage–price ratio is relatively high and hence the price–wage ratio is relatively low, firms would be adjusting their prices upwards, that is, faster than wages are increasing. In a similar vein, a relatively low wage–price ratio would be associated with prices.

The rp–w ratio will be higher for a higher market power reflected in a higher mark-up, m. The position of the price determination curve depends on the number of enterprises, and the scale of the capital stock. A higher price of imported materials, F, leads to higher prices and the ‘paradox of costs’ is in operation under which the profit share rises with imported prices to the detriment of wages.

Price equations such as (4) clearly relate to price level, and do not directly inform us of price changes and the rate of price inflation. It can readily be observed that, if any element of the right-hand side of eqation (4) is higher, then the target price will be higher. This would include wages and input prices and also profit margins. Lerner (Citation1958) called this situation ‘seller-induced inflation’ driven by firms’ pricing decisions. Lerner observed that, ‘[t]here is … no essential asymmetry between the wage element and the profit element in the price asked for the product.’ A sellers’ inflation can just as well be triggered by firms trying to protect or increase their profits as by rising wages. Thus, ‘[p]rices may rise not because of the pressure of buyers who are finding it difficult to buy all they want to buy at the current prices’ but ‘because of pressures by sellers who insist on raising their prices’ (p. 258; quoted in Weber and Wasner Citation2023). Prices are ‘administered’ in the sense that firms make conscious decisions about them, and there can be a degree of ‘stickiness’ on prices resulting from factors such as information collection and decision-making times, etc. A firm facing oligopolistic or monopolistic competition needs to be aware of decisions taken by its competitors when making a decision on price changes. A complaint frequently made about firms’ pricing behaviour (e.g., over oil and gas prices, over loan and deposit interest rates) is that firms are quicker to raise prices in the face of a cost increase than they are to lower prices in the face of a cost decrease. When faced with a substantial increase in costs, a firm may raise its price quickly in the belief that other firms faced with the same increase in costs will also raise theirs. Cost increases may then be passed on quickly and the rate of price increases will match the rate of cost increases. And contrary to the administered price and new Keynesian ‘menu costs’ literature, firms have the capacity to raise prices (and also lower prices) rapidly, though in practice the speed of the process would depend on the contractual arrangements, that is, long-term contracts governing price of supplies and price of output. The degree of monopoly and oligopolistic independence would be expected to impact on the mark-up of prices over costs; however, in an inflationary climate the effects on the speed of adjustment to cost changes may well be more substantial. It could also be noted that prices are often adjusted on a much more frequent basis than wages (and, indeed, on income sources such as pensions and benefits).

4.2. Wage Determination

In terms of the algebraic representation of the equilibrium relationship between real wages and employment, many of the approaches that are compatible with ours lead to similar outcomes — for example, trade union bargaining models and efficiency wage models (for more details, see Layard, Nickell and Jackman [Citation1991] Citation2005, especially Chapters 8 and 9, and Sawyer Citation2002). The key elements of this approach are that real wages and employment are positively related, and money wages adjust to the experience of inflation as well as contain elements of seeking to adjust the real wage.

From their large empirical study across a range of countries, Blanchflower and Oswald (Citation1994) concluded that,

A worker who is employed in an area of high unemployment earns less than an identical worker in a region with low joblessness. … The nature of the relationship appears to be the same in different countries. … As a crude characterization of the data … the wage curve is described by the formula:

where ln w is the log of the wage [and] ln U is the log of unemployment in the worker’s area … . A hypothetical doubling of unemployment is then associated with a drop in pay of 10 per cent (that is, a fall of one tenth). (p. 5, emphasis in original)

All of these interpretations would fit with the general ideas lying behind the wage determination curve.

Nominal wages are settled in a wide range of institutional settings through various forms of negotiation and bargaining. The specific formula used here is based on the idea of a target real wage on the part of workers, the achievement of which is related to the bargaining strength of workers, including the state of demand and unemployment. This is expressed as:

(5)

(5) where w is money wage, p is retail price level, T is target real wage and U is unemployment rate. A dot over a variable indicates the proportionate rate of change of that variable.

The real wage would be constant when:

(6)

(6) with a2 = 1 assumed for convenience.Footnote3 Equation (6) is interpreted as the wage determination curve in as a relationship between real wage and employment level (under the assumption that employment and unemployment are closely and negatively related).

For positions of the economy above the wage determination curve in terms of demand (as reflected in level of employment) and income distribution (represented by the wage–price ratio), wages tend to rise at a slower rate than prices. For positions of the economy below the wage determination curve, wages tend to rise at a faster rate that prices.

The institutional arrangements for wage determination vary widely from close to a spot market through to collective bargaining. The mechanisms in operation differ across sectors of the economy. In the analysis below I represent wage determination in terms of equations (4) to (6) above but recognise that it is not possible to provide an aggregation for the different forces at work into a single equation.

5. Inflationary Barriers and Inflation Dynamics

These ideas on price and wage determination are now brought together. In doing so, there is a position of the economy (in terms of real product wage and employment) at which wage and price inflation would be constant. Here, this is labelled the constant inflation rate of employment (CIRE), although it also involves a constant real product wage. The CIRE represents a combination of employment and income shares (represented in terms of the price–wage ratio), which is a form of balance in that prices and wages would be rising at the same rate (in a zero-productivity growth world) and inflation would be constant. It represents a position in which the competing claims regarding income are mutually compatible (or rather the abilities of each side to secure their competing claims are).

This position of balance may not be unique — the shape of the p and wage determination curve in is the simplest imaginable and the processes of aggregation could well lead to more complexity. Further, the composition of demand across sectors would influence the price determination curve as the price–output relationship differs across sectors. The CIRE may not operate as an attractor for the economy. For example, above the CIRE, there would be something of a wage–price spiral, and the wage–price ratio can vary. The change in the distribution of income could have effects on the level of demand, but there is no unambiguous movement of the level of demand towards that equivalent to the CIRE. The more general point would be that there is no particular reason to believe that the level of demand would be compatible with the CIRE. In other words, the level of aggregate demand based on the real product wage and the resulting distribution of income may well not be compatible with the CIRE. Fiscal and monetary policies may well be used to bring the level of demand in line with CIRE in pursuit of constraining inflation.

The CIRE evolves over time, particularly through investment and shifts in capacity, which would be reflected in as a shift rightwards on the price determination curve (see Sawyer Citation2002). The ability of the economy to produce non-inflationary full employment depends, inter alia, on there being sufficient productive capacity. In terms of , the question is how does the CIRE compare with the notion of full employment (of labour). Higher levels of productive capacity would shift the price determination curve to the right, and could have the potential to enable CIRE to reach full employment.

At lower levels of employment, lower output and lower demand, each side is sufficiently weakened that it is difficult to maintain their income share. At higher levels of employment, higher output and higher demand, each side is emboldened to seek a higher income share.

5.1. Aggregate Demand and Price–Wage Inflation

In , four zones, A, B, C and D, are identified that exhibit different patterns of price and wage increases. The economy can be operating in each of the zones depending on the level of aggregate demand (taken to be setting the level of economic activity) and the distribution of income (as reflected in the wage to retail price ratio).

In zone A, there is a price–wage–price spiral: price-setting behaviour results in prices rising faster than wages and wage-setting behaviour results in wages rising faster than prices. From the wage side, wages would tend to rise faster than prices, according to Equationequation (4)(5)

(5) seeking to attain the target real wage. From the price side, since price is lower (relative to wage) than is the firms’ target, then firms would seek to raise prices faster than wages. In zone A, there would be a price–wage spiral, with workers seeking to raise money wages faster than prices, and firms to raise prices faster than wages. This general analysis does not tell us the speed at which inflation would be rising. This would depend on the speed of adjustments in the wage- and price-setting arrangements. Insofar as prices and wages can be changed on, say, a daily basis, the rise in inflation could be rather rapid. On the other hand, if the adjustments are more on an annual basis and adjustment on each round incomplete, the rise in inflation would be rather modest. Insofar as prices can be adjusted more frequently than wages, a higher level of demand could well see prices rising more rapidly than wages. Prices are, in many cases, in the hands of the producers whereas wages involve joint negotiations.

In response to a significant shock (say, a rise in global prices), prices may well adjust more quickly than wages, resulting in declining real wages, at least in the initial phase.

While the economy remains in zone A, price and wage inflation could be anticipated to continue to rise. There are no automatic market forces that would tend to move the economy towards the CIRE. Even if the economy were to reach CIRE, a level of price and wage inflation would be locked into the system. The rate of inflation that would be attained would be path-dependent.

In zone D, there is a reverse price–wage–price spiral: from price-setting behaviour there is downward pressure on prices, which rise more slowly that wages; but, from wage-setting behaviour, there is also a downward pressure on wages. There would likely be a lower limit on price and wage changes such that declines in nominal prices and wages would be rather small. In zone D, there would be a tendency for the pace of wage and price increases to decline, in something of a downward spiral. At low levels of wage and price increases, there may be little further fall, especially if decreases in wages or prices are involved.

In zone B, there would be movement in the wage–price ratio, with the rate of wage increases tending to be less than the rate of price increases from the wage determination perspective, and the rate of price increases tending to be faster than the rate of wage increases from a pricing perspective. In zone C, there would also be a movement in the wage–price ratio and the relationships between wage and price increases are the reversed of those in zone B.

5.2. Shifts in Pressures and Income Shares

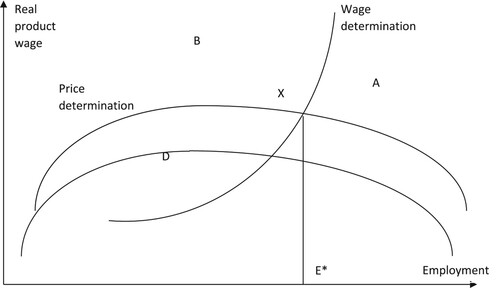

Some moves in conflicts regarding income distribution and implications for inflationary pressure are initiated in an effort to reconcile claims when the economy is at the CIRE, with a corresponding level of demand. Shifts in the price determination curve and/or the wage determination curve, for whatever reason, would disturb an existing ‘equilibrium’ position, and can lead to a different pattern of wage and price changes.

Let us start our story with an economy operating close to CIRE. It can be ‘disturbed’ in a range of ways: a sharp increase in demand, reduction in supply potential, push for higher profits, push for higher wages or global price inflation. A rise in inflation may be relatively small or large, and there is a need to examine speed of response to such a rise. There may also be a need to enquire into patterns of the previous two decades and the shifts from wages to profits and the slow growth of real earnings: these proceeded without in general much effect on inflation.

A push for higher prices (relative to wages) would be represented by a downward shift in the price determination curve. This could result from an enhanced degree of market power in general (in the case of prices). A push for higher wages (relative to prices) would be represented by an upward shift in the wage determination curve and may result from strengthened trade unions (in the case of wages).

The shift in the price determination curve is illustrated in (and a similar discussion could be made for a shift in the wage determination curve). If the economy had been operating at point X, the immediate effect of the portrayed shift is that the economy would now be in a zone A situation, with prices and wages tending to rise faster than hitherto. But what the general observation does not tell us is how much inflation would rise by or over what period. The idea of price and wage changes to adjust price–wage ratios to their ‘desired’ levels has been mooted. But little is said, directly, on the speed of those adjustments. Rapid adjustments would show up as high rates of price and wage inflation.

Figure 2. Shift in the price determination curve.

5.3. Government

In the ‘target real wage’ approach, the target could be seen as the post-tax real wage. A rise in tax on wages and/or tax on goods and services would lower the post-tax real wage. Government taxation can be introduced in a simple manner by including taxes on wages (tw) and prices (tp). Equation (6) would then be replaced by:

(7)

(7) In terms of the pre-tax real wage, the wage determination curve in shifts upwards for a rise in tax rates, and the pre-tax real product wage rises and employment declines. Insofar as the rise in tax rates is matched by increases in public expenditure, how do workers value those increases in public expenditure? Although the term has somewhat fallen out of use, the idea of a ‘social wage’ was used to suggest benefits from public expenditure.

5.4. Foreign Prices

Higher foreign prices (relative to domestic wages) would lead to a downward shift of the price determination curve. At one level, the role of the foreign sector is straightforward. Variations in global prices feed through into domestic prices.Footnote4 Commodity prices have been particularly volatile as a result a combination of shifts in supply/demand situation, the exercise of market power by producers (especially oil) and speculative activities. One noteworthy aspect here is the ‘paradox of cost’ effects. Import prices, together with wages, are marked-up in pricing equations and higher import prices lead to a rise in prices relative to wages and a rise in profits.

5.5. Loss of Productive Capacity

A major diminution of productive capacity (say, resulting from a natural disaster or the aftermath of war) would shift the price determination curve to the left. Insofar as the level of demand does not parallel the fall in supply potential, there would be inflationary consequences. The onset of high inflation (say, above 50 per cent per annum) and moves toward hyperinflation could be viewed in terms of a substantial loss of productive capacity together with the maintenance of a relatively high level of demand. The private sector and/or the public sector can account for the continuing level of demand. Each episode of high inflation must be examined to determine the sources explaining the effective collapse of capacity and the forces maintaining demand in order to understand these inflationary tendencies. This line of approach is consistent with that remarked upon by Åslund (Citation2012): ‘it is striking how few the causes of hyperinflation were. They were connected with either war/revolution/collapse of a state or utter irresponsibility’ (p. 4).

6. Concluding Comments

‘All happy families are alike; each unhappy family is unhappy in its own way’ (Leo Tolstoy, Anna Karenina). The mainstream approach is based on an ‘all inflations are alike’ focus on a general movement in prices that is demand-driven and can be dampened by interest rate policy. Changes in relative prices and wages are viewed as insignificant features of inflation (and any changes in relative prices and wages reflecting shifts in relative demand and supply). A policy response involving raising interest rates to dampen demand is bizarre. Interest rates have little effect on inflation. In so far as they do have an effect on prices, it will not be on prices in areas of shortage of supply but on other prices and wages. It would be intended to depress wages and address the income inequality effects of the disruptions to supply.

The conflictual shares approach to inflation recognises that different trigger and transmission mechanisms explain inflationary episodes. The experience of inflation in 2022/23 is a clear example of supply disruptions generating rising prices in a key area, which may accompany supply shortages and can have a dramatic income distribution effect. Other experiences of rising inflation across industrialised countries have involved a large upswing in global demand (e.g., the armaments build-up during the Korean War). Policy responses should take into account the causes and mechanisms that have led to the inflationary episode, which is, of course, much easier said than done, not least because differing causes will be identified depending on the perspectives of policy-makers. Further, policy responses and their implementation must be developed for the specifics of the inflationary episode. In some situations, addressing the underlying cause of a rapid rise in prices may be rather difficult. Take, for example, a major failure in domestic food supply: appropriate policy responses are alleviating suffering using price controls and rationing, and securing foreign supplies. To address global price rises, there may be little that domestic governments can do other than appearing to constrain the mark-up applied by domestic firms to imported costs, and raising domestic wages to limit the damaging effects of higher global prices on real wages.

Conflictual shares inflation theory does not provide a ‘one size fits all’ approach to inflation like that of the monetarist approach (‘inflation is always and everywhere a monetary phenomenon’) or the Phillips curve (always demand, though the term Phillips curve is defined in numerous ways and covers different mechanisms). The conflict inflation approach is (as most approaches to inflation are) located with an endogenous money approach, and the drivers of inflation and price and wage decisions.

The conflictual approach is consistent with a broadly constant rate of inflation provided that unemployment and distribution of income are consistent with the CIRE. Competing claims regarding the distribution of income are then ‘reconciled’. An upswing in inflation can then be seen as arising from several possible sources. Some changes may proceed rather slowly — for example, the tendency of industrial concentration and market power to rise (summarised in Sawyer Citation2022) has been associated with a rise in profit share and a decline in wage share. This process has, however, occurred over a number of decades, and to what extent it has contributed to inflation is debatable, even though it appears to have raised profit share. In a similar vein, trade union power has been depleted over a number of decades. The impact of shifts such as these may well be evident to a greater extent on the wage–price ratio and income shares than on the rate of inflation. Major imbalances occurring via destruction of productive capacity or payments for unproductive employment, for example, can readily lead to major upswings in inflation. For industrialised countries (and others), the more significant upswings (and downswings) in inflation appear to result from global prices (as in the most recent episodes). Movements in global prices are transmitted through the domestic price and wage determination systems, which have consequences for the distribution of income.

Acknowledgements

I would like to thank reviewers for their comments on the initial draft.

Disclosure Statement

No potential conflict of interest was reported by the author.

Notes

1 See Sawyer (Citation1982) for my first attempt to place price and wage determination together.

2 For a similar derivation, see Sawyer (Citation2002).

3 The use of a2 = 1 is a convenient simplification: without that assumption the inflation barrier level of employment developed later would also be a function of the rate of inflation.

4 See, for example, Morlin (Citation2023) for a theoretical exploration of inflation and conflict in an open economy. See Wildauer et al. (Citation2023) for an empirical investigation into recent energy price shocks and inflation.

References

- Åslund, A. 2012. ‘Hyperinflations are Rare, But a Breakup of the Euro Area could Prompt One.’ Peterson Institute for International Economics Working Paper PB12-22.

- Beckerman, W., and T. Jenkinson. 1986. ‘What Stopped the Inflation? Unemployment or Commodity Prices?’ Economic Journal 96 (381): 39–54.

- Blanchard, O., A. Amighini, and F. Giavazzi. 2021. Macroeconomics: A European Perspective. Harlow, England; New York: Pearson.

- Blanchflower, D. G., and A. J. Oswald. 1994. The Wage Curve. Cambridge, Mass.: M.I.T. Press.

- Friedman, M. 1968. ‘The Role of Monetary Policy.’ American Economic Review 58 (1): 1–17.

- Galí, J. 2015. Monetary Policy, Inflation and the Business Cycle. An Introduction to the New Keynesian Framework. Second edition. Princeton, NJ: Princeton University Press.

- Harrod, R. 1972. ‘The Issues: Five Views.’ In Inflation as a Global Problem, edited by R. Hinshaw. London: Johns Hopkins Press.

- Hasan, S. 1999. ‘New Evidence on Causal Relationships Between Money Supply, Prices and Wages in the UK.’ Economic Issues 4 (2): 75–87.

- Henry, S. G. B., M. Sawyer, and P. Smith. 1976. ‘Models of Inflation in the United Kingdom.’ National Institute Economic Review 77: 60–71.

- Hoover, K. D. 1991. ‘The Causal Direction Between Money and Prices: Al Alternative Approach.’ Journal of Monetary Economics 27: 381–423.

- Laidler, D., and M. Parkin. 1975. ‘Inflation: A Survey.’ Economic Journal 85 (340): 741–809.

- Layard, P. R. G., S. J. Nickell, and R. Jackman. (1991) 2005. Unemployment: Macroeconomic Performance and the Labour Market. Oxford: Oxford University Press.

- Lee, F. S. 1998. Post Keynesian Price Theory. Cambridge, New York: Cambridge University Press.

- Lerner, A. P. 1958. ‘Inflationary Depression and the Regulation of Administered Prices.’ In The Relationship of Prices to Economic Stability and Growth: Compendium of Papers Submitted by Panelists Appearing Before the Joint Economic Committee, 257–268. Washington, D.C.: Government Printing Office.

- Lipsey, R. 1960. ‘The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957: A Further Analysis.’ Economica 27 (105): 1–31.

- Morlin, G. S. 2023. ‘Inflation and Conflicting Claims in the Open Economy.’ Review of Political Economy 35 (3): 762–790.

- Pasinetti, L. 1974. Growth and Income Distribution. Cambridge: Cambridge University Press.

- Rowthorn, R. E. 1977a. ‘Conflict, Inflation and Money.’ Cambridge Journal of Economics 1 (3): 215–239.

- Rowthorn, R. E. 1977b. Capitalism, Conflict and Inflation. London: Lawrence and Wishart.

- Sargan, J. D. 1964. ‘Wages and Prices in the United Kingdom: A Study in Econometric Methodology.’ In Econometric Analysis for National Economic Planning, edited by P. E. Hart, G. Mills, and J. K. Whitaker, 25–63. London: Butterworths.

- Sawyer, M. 1982. ‘Collective Bargaining, Oligopoly and Macro-Economics.’ Oxford Economic Papers 34 (4): 428–448.

- Sawyer, M. 2002. ‘The NAIRU, Aggregate Demand and Investment.’ Metroeconomica 53 (1): 66–94.

- Sawyer, M. 2022. ‘Monopoly Capitalism in the Past Four Decades.’ Cambridge Journal of Economics 46 (6): 1225–1241.

- Sawyer, M., S. Aaronovitch, and P. Samson. 1982. ‘The Influence of Cost and Demand Conditions on the Rate of Change of Prices.’ Applied Economics 14 (2): 195–209.

- Sawyer, M., with S. Aaronovitch, and P. Samson. 1983. Business Pricing and Inflation. London: Macmillan and New York: St. Martin’s Press, ix + 118.

- Weber, I. M., and E. Wasner. 2023. ‘Sellers’ Inflation, Profits and Conflict: Why Can Large Firms Hike Prices in an Emergency?’ Review of Keynesian Economics 11 (2): 183–213.

- Wildauer, R., K. Kohler, A. Aboobaker, and A. Guschanski. 2023. ‘Energy Price Shocks, Conflict Inflation, and Income Distribution in a Three-Sector Model.’ Energy Economics 127: 106982. doi:10.1016/j.eneco.2023.106982.