?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Against the backdrop of the booming supply chain finance and logistics industry, Logistics 4.0 has emerged. However, the financing capacity of today's logistics companies is still unable to respond to the needs of the rapid development of the supply chain. On the one hand, the problem of logistics companies’ lack of existing high-value collateral in supply chain finance has led to a clutter of their credit data and difficulty in verifying their creditworthiness. On the other hand, the massive access to logistics companies’ business information can also lead to privacy leaks. At the same time, the transparency feature of blockchain is used to solve the financing dilemma of many industries in supply chain finance. On this basis, we propose a blockchain-based financing scheme (BFS) for logistics company. BFS utilises more efficient and interpretative smart contract technology, as well as improved privacy information query and invocation algorithms, to realise automatic control of entity node privacy information flow and significantly simplifying the steps and lowering the thresholds to financing for logistics companies, while protecting the privacy of their data. After extensive simulation testing, BFS can run supply chain blocks at a stable transaction throughput of around 280 RPS, with data transfers that meet the financing needs of logistics companies, providing a higher and more stable performance than the native Hyperledger Fabric.

1 Introduction

With the development of technologies such as the Internet of Things, data-driven and blockchain, the logistics industry has entered the development phase of logistics 4.0 with the pursuit of supply chain transparency and real-time logistics tracking (Woschank & Dallasega, Citation2021). However, small and medium-sized logistics companies are faced with the problem of using their own funds to advance payments for goods, which makes it difficult for their capital pool to support their expansion (Harish et al., Citation2021). Facing the financing needs of logistics companies, the main options are bank financing (Cainelli et al., Citation2020), issuing shares (Gompers & Lerner, Citation2003), issuing bonds (De Fiore & Uhlig, Citation2011), endogenous financing (Flor & Hirth, Citation2013), logistics financing (Li et al., Citation2020) and several other ways. As shown in Table , which demonstrates the specific description and limitations of the existing schemes, these financing methods can provide a direction for logistics companies, but because of various internal problems of small and medium-sized logistics companies, such as sloppy internal management, inadequate financial systems and low existing assets resulting in relatively weak risk resistance, they enter into financing difficulties, making it difficult for these options to achieve satisfactory results (Harish et al., Citation2021).

Table 1. Financing models for logistics companies.

In recent years, supply chain finance has been used to address the financing challenges of upstream and downstream small and medium-sized suppliers. In supply chain finance, the core business guarantees the credit of small and medium-sized suppliers, which reduces banks’ concerns about small and medium-sized suppliers. However, there is still one of the main research gaps in the field of supply chain finance, where logistics companies are used as a starting point to solve their financing dilemmas. However, the supply chain, as a community of interest, is more inclusive of logistics companies (Harish et al., Citation2021). This is demonstrated by the fact that core companies assess the credit of logistics companies not only in terms of the value of their existing assets, but also in terms of their contribution to the overall supply chain and their past supply chain history. This is a great advantage for logistics companies that has access to important logistics information. At the same time, in the field of supply chain finance, due to the rapid changes in the market, there is a risk that data validation may be slow to keep up with the financing needs, or that a large amount of data of logistics companies may be accessed and easily compromised (Chen et al., Citation2020). Therefore, the following problems still exist for logistics companies’ financing scheme in supply chain finance, which makes us think about further solutions.

Firstly, problems of sloppy internal management, unsound financial system, low value of existing assets and relatively weak risk resistance of small and medium-sized logistics companies make the logistics companies’ own credit very low.

Secondly, the financing needs of small and medium-sized logistics companies are characterised by urgent liquidity need, high frequency and small amounts. This makes its data messy and difficult to verify, which ultimately leads to the speed of verification not reaching the speed of financing need.

Thirdly, even if the data of small and medium-sized logistics companies can be verified, there is the problem that the supply chain companies’ access to a large amount of logistics information in order to make a quick response to the market can lead to the exposure of the logistics companies’ private data, and the consequences of data tampering.

In order to fill this gap and solve the problems for logistics companies, this research uses the Hyperledger Fabric (a.k.a. Fabric), a blockchain technology platform, to build a financing platform for logistics companies in supply chain finance, and to protect the credit of the companies by uploading their business data. At the same time, the privacy information of logistics companies is encrypted and smart contracts are written so that the financing process is greatly simplified to improve data verification speed and transaction efficiency. Therefore, the contribution of this paper is as follows:

A blockchain-based financing scheme (BFS) for logistics company in supply chain finance is proposed, which greatly simplifies the process of lending and repayment for logistics company based on the automated execution of smart contracts, while the performance analysis of the proposed scheme is presented.

The registration steps of the blockchain network nodes are improved to greatly reduce the risk of the four types of participants in supply chain finance: logistics company, core business, factoring agency and financial institution being compromised by malicious nodes in the blockchain network.

Algorithms for privacy information control of logistics companies in the blockchain network is proposed, which protects the security of privacy of logistics companies by controlling the privacy information operation flow of each node in the blockchain network.

However, there are still some limitations to our scheme, which are described as follows:

When data is entered into the blockchain, it still requires manual input, which is less supervisable at this stage and has a higher risk of data tampering, resulting in less authentic data.

The BFS scheme does not have a consensus algorithm that fits well, and we need a consensus algorithm that fits better with the financing process to improve the distribution of benefits within the system and achieve block consistency.

In the data validation phase, transactions performed between nodes generally require two and more transactions to be validated in order to improve the legitimacy and reliability of transaction execution, but there are redundant steps in transaction validation that increase the latency of transactions.

The remainder of the paper is divided into the following sections: Section 2 reviews the current landscape of supply chain logistics, as well as financing options for logistics companies and the blockchain technologies that support them. Section 3 clarifies the system architecture of the BFS. Section 4 provides a detailed description of the BFS. In section 5 we analyse the scheme performance. In section 6 we give a summary of the literature.

2 Related work

2.1 Supply chain finance

The concept of supply chain finance was first introduced around 1970 when researchers began working on the relationship between inventories and trade credit policies. However, supply chain finance did not receive sufficient attention until the global financial crisis at the beginning of the twenty-first century, as ample cash flows in the capital markets prevented firms from carefully managing the working capital of their supply chains (Liebl, Hartmann, & Feisel, Citation2016). During this financial crisis, the credit crunch affected the flow of capital in the supply chain, threatening its stability and even leading to the bankruptcy of many suppliers in the supply chain as well as logistics companies. From this time onwards, companies began to recognise the importance of supply chain finance and started to strengthen their supply management from a financial perspective. Current research in the field of supply chain finance has contributed a great deal of theory, technology and management practices for effective planning and control of financial flows between supply chain stakeholders(Bals, Citation2019).

Supply chain finance is playing an increasingly important role in the field of supply chain management and finance, and is gradually attracting more attention from industry and academia (Li et al., Citation2020). Supply chain finance aims to coordinate material, information and financial flows. It has grown up to be a “key word” among academics and practitioners, indicating the planning, direction and control of financial flows along the supply chain (Liebl et al., Citation2016). Research in supply chain finance has focused on the supply side, with many researchers in the literature concentrating on logistics and finance research.

The growing relevance of supply chain finance stems from its multifaceted benefits to supply chain performance. Key benefits include enhanced integration between customers, suppliers and service providers and the creation of an alternative resource competitive advantage. It has long been defined and conceptualised as the organisation and coordination of three flows in the supply chain: product, information and money. The ultimate goal is to align financial flows with product and information flows in the supply chain and to improve the management of financial flows from the perspective of suppliers upstream and downstream in the supply chain (Bals, Citation2019). However, among the many studies in the field of supply chain finance, those that take logistics companies as a starting point are still one of the main research gaps. So, our job is to give a scheme that helps them to achieve financing.

2.2 Logistics company finance schemes

Jin et al. (Citation2013) analysed the debt financing of logistics companies and concluded that some small and medium-sized logistics companies do not have the ability to issue debt and choose to borrow from banks and equity financing more often than not. Wang, Yang, Zhuo, and Xiong (Citation2019) and Li and Chen (Citation2019) investigated that the value of collateral required for bank loans is 2.6 times the value of the loan. Tiberius and Hauptmeijer (Citation2021) pointed out that regulators are very strict about equity financing for small logistics companies, which makes it difficult for small and medium-sized logistics companies to achieve financing and creates a financing dilemma. Guida et al. (Citation2021) pointed out that supply chain finance can solve the problem of financing for small and medium-sized logistics companies. Chen et al. (Citation2020) pointed out that there are many credit problems in supply chain finance. Li et al. (Citation2022) used the Hybrid Extreme Gradient Augmented Multilayer Perceptron (XGBoost MLP) model to assess credit risk in digital supply chain finance and experimentally demonstrated a 3.7% increase in the accuracy of the model using numerical characteristics as an evaluation metric, which enhanced the credit reliability of small and medium-sized logistics companies in the supply chain when financing. Many scholars are actively seeking an answer to the credit problem have found that blockchain can play a huge role in this problem (Zhang et al., Citation2021). Therefore, in order to solve the credit problem of logistics companies and to lower the threshold of financing, we need to help logistics companies to finance themselves through blockchain technology.

2.3 Blockchain technology

Blockchain is a new decentralised infrastructure and distributed computing paradigm that takes a chained data structure for authentication and storage, using distributed consensus algorithms to generate and update data. It adapts cryptographic methods to protect data transfers and access, and applies automated script-based smart contracts to manipulate rules and data (Liang et al., Citation2021). Blockchain allows mutually untrusting entities to make financial payments without the need for a central trusted third party, providing transparent and integrity-protected data storage and a consensus mechanism for achieving consistent information (Liang, Fan, et al., Citation2020). In the case of PoW, there is a low probability that a record can be forged only if a block-keeping node controls more than 51% of the bookkeeping nodes in the block, without considering the large number of nodes in the overall blockchain and the loss of the nodes’ own equity. As more and more nodes are added to the blockchain, the likelihood of successful forgery is infinitely close to zero, which effectively prevents information from being illegally tampered with or exploited by malicious nodes (Liang et al., Citation2021). In addition, the blockchain has autonomous smart contracts (Liang, Fan, et al., Citation2020). The terms and conditions of the contract on a smart contract are clearly visible to the different network participants in a given blockchain. Thus, once a contract is established, changes in the business logic are not easily enforced and each transaction by either party to the contract is monitored and controlled by other network nodes in the blockchain, whereas smart contracts automate the execution of this one business logic (Zeng, Liu, Zhu, Wang, & Zhang, Citation2022).

As blockchain applications expand, more areas of complex business logic are involved in smart contracts, including in the area of supply chain finance. Venkatesh et al. (Citation2020) proposed a blockchain-based system framework for supply chain sustainability transparency, a system architecture that monitors multi-layered supply chains and enables instant traceability in supply chain networks. Xue, Dou, and Shang (Citation2020) proposed a conceptual model of a decentralised supply chain based on blockchain that effectively connects production suppliers, logistics providers, retailers and customers to add value to business entities. In the next year, Harish et al. (Citation2021) proposed a logistics financing blockchain platform (Log-Flock) that leverages the capabilities of IoT, CPS and blockchain technology to support logistics financing.

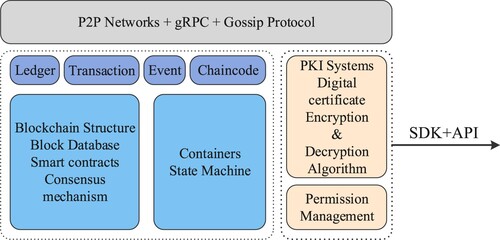

Fabric is a frequently used platform in practical examples of blockchain technology in the supply chain finance sector (Chacko et al., Citation2021). Hyperledger Fabric drives the development of protocols, specifications and standards related to blockchain and distributed ledgers. Fabric introduces rights management and its design supports pluggability and scalability (Ma et al., Citation2019). Fabric is highly scalable and flexible because it uses a modular architecture design. From an application perspective, the fabric is divided into four parts: identity management, ledger management, transaction management and smart contracts. The architecture of Hyperledger Fabric is shown in Figure . Users can access various resources in the Fabric network through APIs. The user only needs to interact with the resources and the rest of the work is done automatically by the system. The hierarchical structure of Fabric improves the scalability and pluggability of the architecture and facilitates developers to develop a modular basis. At the same time, Fabric supports feature-based programming of smart contracts, which can be used for different business scenarios in order to improve transaction efficiency and streamline business processes by writing highly optimised smart contracts to make the transaction process faster (Ma et al., Citation2019).

Figure 1. Hyperledger Fabric architecture diagram.

In terms of privacy protection in blockchain, the commonly used privacy protection algorithms in blockchain technology are secure multi-party computation platform, Homomorphic Encryption, etc., and these privacy protection algorithms are also widely used (Liang et al., Citation2021). Wang, She, et al. (Citation2021) provided an effective solution for blockchain technology with privacy by performing a new optimisation of the secure computation protocol. Liang, Zhang, et al. (Citation2020) established a mathematical model based on homomorphic encryption using blockchain and smart contracts, followed by the design of algorithms including blockchain generation, homomorphic chain encryption/decryption and smart contracts. For supply chain finance scenario, Ma et al. (Citation2019) gave a scenario where the writing of smart contracts in the Fabric platform makes it mandatory for organisations joining the blockchain to be authenticated under the Fabric-CA organisation, preventing illegal organisations from joining the network to steal users’ privacy and ensuring data privacy. Liang, Fan, et al. (Citation2020) proposed a secure data storage and recovery scheme based on blockchain networks that can quickly recover data from failed nodes while protecting user data privacy.

3 System architecture

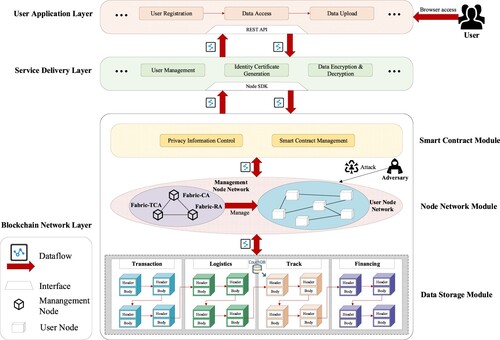

In order to facilitate the financing of small and medium-sized logistics companies in supply chain finance, and to solve the financing dilemma of logistics companies with difficulties in granting credit, slow data validation and easy data leakage, BFS is proposed as an integrated scheme to organise and manage all relevant activities and operations of logistics companies, as well as in the implementation of supply chain finance as a whole. It serves four main categories of participants: logistics company, core business, factoring agency and financial institution. The system architecture is depicted in Figure in a layered structure. It consists of three main layers, including blockchain network layer, service delivery layer, and user application layer.

Figure 2. System architecture diagram.

3.1 Blockchain network layer

This layer is crucial to the implementation of financing scheme for logistics company in supply chain finance, providing real-time visibility and traceability for supply chain finance. The data of the logistics company is stored, including transaction data, logistics data, track data and financing data, providing security for the logistics company to grant credit. The node network provides logistics company with an efficient and highly secure financing scheme under the control of a smart contract deployed in advance. It consists of three modules: data storage module, node network module and smart contract module.

3.1.1 Data Storage Module

The role of the data storage module is to store registration information, transaction information and logistics information etc. uploaded to the blockchain network in the supply chain. We have used CouchDB, a non-relational database, to record relevant information in the supply chain in the form of key-value pairs , where v can be a key-value pair in addition to a number or string etc., i.e.

, after which

is used to express this situation. Based on the characteristics of CouchDB, the data storage module is highly reliable, concurrent and easy to use. In the supply chain finance scenario, the data stored by the data storage module is classified as follows:

Registration information: When a user wants to join the current blockchain platform, he first needs to register for a node. The registration information is the user's identity certificate, and the data is encrypted and uploaded to the blockchain after verification.

Transaction information: Upstream and downstream suppliers or distributors participating in supply chain finance need to encrypt and upload the executed transactions to the blockchain after verification. Logistics companies need to upload the basic logistics information about these transactions, such as the origin, destination, transported goods, etc., to the blockchain after verification and encryption.

Logistics information: This type of information is set up separately for logistics company for financing. It mainly includes vehicle information, freight information, vehicle operation routes, etc.

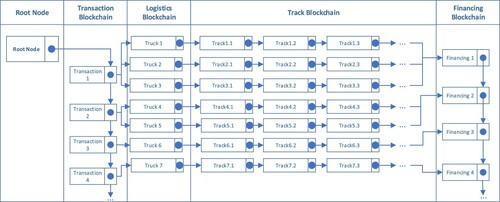

In designing the blockchain data, we divided the blockchain into four parts as the transaction blockchain, logistics blockchain, track blockchain and financing blockchain. The structure of the blockchain is shown in Figure . Among them, the transaction blockchain mainly contains the transaction data of upstream and downstream enterprises in the supply chain. The logistics blockchain records the information of vehicles, the purchase and rental costs of vehicles as the foundation of the business, the fuel costs and passage costs during the delivery of vehicles, and the insurance costs of vehicles and transportation, which play a protective role, should be recorded in the logistics blockchain. The track blockchain records the latitude and longitude position of each vehicle at regular intervals during transport, which enables real-time monitoring and reduces the risk of falsification of data by obtaining track positions. We have defined two operations to query the data storage module for information and add information to the data storage module. Taking the transaction information as an example, the specific function definitions and expressions are as follows:

: Read the latest status of transaction information in the supply chain from the data storage module via key

Figure 3. Block structure of blockchain.

3.1.2 Node Network Module

The node network module is divided into two types of nodes, one is the management node, which is to monitor and manage the behaviour of the nodes in the blockchain network. The management node network is mainly composed of Fabric-CA, Fabric-RA and Fabric-TCA. The functions of these management nodes are as follows:

Fabric-CA: Fabric-CA is Fabric's certificate authority centre, supporting the issuance of registration certificates, and the renewal and revocation of identity certificates.

Fabric-RA: Fabric-RA is the supervisory node of the Fabric and is responsible for authenticating users, verifying data legitimacy, registration and auditing.

Fabric-TCA: Fabric-TCA is used to maintain and manage the certificates associated with transactions.

The other is user nodes. In supply chain finance scenario, the user node network mainly consists of logistics company nodes, core business nodes, factoring agency nodes and financial institution nodes. The functions of these user nodes are as follows:

Logistics company nodes: upload transaction, vehicle and operation route data to core enterprise; sign factoring financing contract and upload to financing blockchain.

Core business nodes: provide business data of logistics company to logistics blockchain and track blockchain; transfer credit limit to logistics company together with factoring agency node and record to financing blockchain; repay loans to restore credit limit and upload records to financing blockchain.

Factoring agency nodes: transfer credit limit to logistics company together with core business node and upload records to the financing blockchain; apply for credit limit value lending to financial institutions for logistics company and upload records to the financing blockchain.

Financial institution nodes: lend money and upload records to the financing blockchain; confirm loan repayment and upload to the financing blockchain.

3.1.3 Smart contract module

The role of the smart contract module is to automate all activities and operations related to the organisation and management of supply chain finance implementations on the blockchain network, allowing trusted transactions to be made without third parties, which are traceable and tamper-proof. By deploying smart contracts on the blockchain network and thus giving the blockchain programmable features, we modify the content of smart contracts to meet the needs of supply chain finance scenario, based on Fabric's support for the pluggable nature of smart contracts (Chacko et al., Citation2021). Considering that the data stored in the data storage module is visible to all nodes which accessing the blockchain network, we use an efficient cryptographic algorithm to encrypt the privacy information of the logistics company in order to avoid its disclosure. Therefore, the privacy information control in BFS is used to control the operation flow of privacy information by multiple users, encrypting and decrypting the privacy attributes in the read and write information, thus solving the problem of small and medium-sized logistics companies in the face of supply chain enterprises to make rapid responses to the market and obtain a large amount of logistics information, resulting in the leakage of logistics companies’ privacy information, and achieving the purpose of alleviating the financing difficulties of logistics companies. Contract management is used to execute the deployment, update and destruction of smart contracts in the supply chain finance scenario.

3.2 Service delivery layer

As an intermediate layer between the blockchain network layer and the user application layer, the service delivery layer provides a REST API for the user application layer upwards and interacts with the blockchain network layer downwards using the Node SDK, providing functions such as user management, data encryption and decryption. The service delivery layer maps the logical operations of the user application layer to the blockchain network layer and provides portable data interaction functions, making the system's operation logic clearer and performance more efficient, thus meeting the high concurrent and high-speed user application layer requests.

As an intermediate layer between the blockchain network layer and the user application layer, the service delivery layer provides a REST API for the user application layer upwards and interacts with the blockchain network layer downwards using the Node SDK, providing functions such as user management, data encryption and decryption. The service delivery layer maps the logical operations of the user application layer to the blockchain network layer and provides portable data interaction functions, making the system's operation logic clearer and performance more efficient, thus meeting the high concurrent and high-speed user application layer requests.

We focus on data encryption and decryption part of the service delivery layer. When a user node in the blockchain network in the supply chain finance scenario tries to access or upload some privacy information in the transaction information, we need to encrypt and decrypt the data. We define three operations, which are generating a symmetric key by user identity certificate, encrypting information by key and decrypting information by key. Using the transaction information as an example, the specific functions are defined and expressed as follows:

3.3 User application layer

The user application layer provides operation pages for multiple users, through which users can perform operations such as user registration, data access and data upload. The users of data access mainly include terminals that need to view or monitor transaction information and logistics information, such as upstream and downstream enterprises in the supply chain, factoring agency, etc.; the devices of data upload mainly include all terminals in the supply chain that can collect logistics information, such as vehicle GPS devices and monitoring devices, etc. All nodes need to be registered and verified before they can join the blockchain network. The notation we use throughout the paper is shown in Table .

Table 2. Notation list.

4 Our proposal BFS

4.1 Research motivation

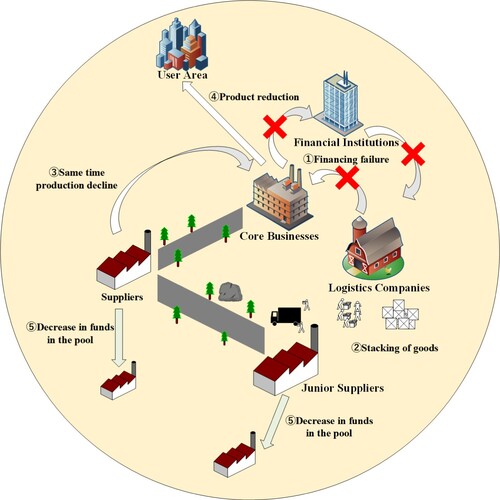

With the development of Logistics 4.0, the demand for logistics in the supply chain becomes greater (Woschank & Dallasega, Citation2021). If logistics companies have difficulties in financing, this will result in the number of trucks not being able to expand and goods being stockpiled in warehouses. Immediately afterwards, both upstream and downstream companies in the supply chain will be affected and the sale and purchase of goods become very slow. For the supply chain as a whole, this slows down the capacity of the supply chain and reduces the collective revenue capture rate. With this comes of slower revenue capture rates for both upstream and downstream companies, and less money in the pools of both upstream and downstream companies as the goods remain on the books. The end result is that all companies in the supply chain are hit by financing. Such a financing distress scenario is shown in Figure .

Figure 4. Logistics company financing dilemma situation diagram.

Numerous researchers have found that the most prevalent factor contributing to financing difficulties is the difficulty in granting credit to logistics companies, as evidenced by the fact that when logistics companies face budget constraints, they typically borrow capital from banks, but the banks require them to provide high-value collateral, which logistics companies typically cannot afford to provide at 2.6 times the value of the loan, resulting in credit difficulties (Li & Chen, Citation2019; Wang et al., Citation2019), and this situation is more prominent among small and medium-sized logistics companies. How to improve the financing dilemma of logistics companies is one of the main research gaps in current supply chain research. Considering these consequences and in order to fill this research gap, we investigate the credit scheme for logistics companies in supply chain finance and propose an efficient and highly secure financing scheme for logistics companies in view of the financing dilemma of small and medium-sized logistics companies with slow logistics data validation and easy logistics data leakage (Chen et al., Citation2020).

4.2 Scheme overview

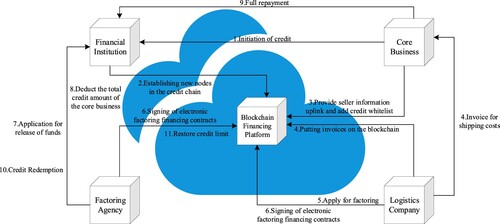

The scheme proposed in this paper is a blockchain-based financing scheme for logistics companied applied under the field of supply chain finance. We illustrate the entire financing process in the supply chain finance. Figure shows the flowchart of the BFS, which depicts the interaction between the nodes in terms of how the logistics companies are granted credit, how it applies for financing and restores its credit line. Our scheme BFS has the following characteristics:

Fast validation: When a blockchain network between nodes is established, every interaction recorded or processed between nodes needs to be uploaded to the blockchain for recording, which facilitates the maintenance of overall reliable ledger data. Our scheme is based on Fabric, which has features such as high concurrency and support for highly optimised components that greatly improve the efficiency of validating transactions (Chacko et al., Citation2021). In our scheme, the registration of blockchain network nodes and the control of privacy information of logistics companies use symmetric encryption algorithms with fast encryption and decryption, while the process of lending and repayment is greatly simplified in the financing scheme of logistics companies, which can well improve the speed of verification of logistics companies and thus ease the financing dilemma.

Secure node network: In order to ensure that each node freely transmits and shares data information, it is necessary to establish a secure and reliable node network among them while protecting the data. As the nodes contained in the blockchain network are mostly lightweight nodes, a symmetric encryption scheme should be used in the node registration process to improve the efficiency of building block clusters, taking into account the latency issue. The node registration process on the chain can effectively reduce the risk of intrusion through malicious nodes, as described in Section 4.3.

Strong privacy protection: In the considered scenario of financing logistics companies in supply chain finance, there is the problem that the supply chain enterprises access to a large amount of logistics information in order to react quickly to the market can lead to the privacy information of logistics companies being exposed (Chen et al., Citation2020), and for this problem, encryption and decryption algorithms for privacy attributes in transaction information are proposed. As well as in the supply chain finance scenario, smart contracts for protecting the privacy information of logistics companies are deployed, which can automatically and quickly control the flow of privacy information operations of nodes in the blockchain, as described in Section 4.4.

Highly credible financing process: This is because logistics companies upload their transaction information, logistics information, trajectory information and financing information into the blockchain, providing their contribution to the overall supply chain and their past history of participation in the supply chain for evaluation and credit granting. Logistics companies are not required to provide existing high-priced collateral as in previous financing solutions (Wang et al., Citation2019), which significantly lowers the financing threshold for logistics companies. At the same time, real-time visible and traceable logistics data makes the financing process highly credible. With financing, logistics companies can further expand their company size, increase their business capacity and then continuously improve their credit, which is conducive to the sustainable development of logistics companies. The detailed steps are described in Section 4.5.

High fault tolerance: Logistics companies in the supply chain are likely to be temporarily disconnected by nodes due to unstable signals or bumpy roads, and the transmission of logistics information or track information is out of order. In order to ensure the stability of logistics companies’ transactions, a mechanism based on heartbeat information and pulling can enable nodes reconnected into the blockchain network to obtain the data lost due to disconnection in a timely manner, ensuring the consistency of logistics companies’ transaction data. It has high fault tolerance, as described in Section 4.6.

Figure 5. The blockchain-base financing scheme for logistics company in supply chain finance.

4.3 Blockchain network node registration

There are four types of participants in supply chain finance, including logistics company, core business, factoring agency and financial institution. Before conducting supply chain finance-related activities and operations in the blockchain network, in order to reduce the risk of invasion by malicious nodes, nodes need to be verified. After verification, nodes will obtain an exclusive identity certificate, at which point registration has been successful, and then they can join the blockchain network.

Fabric-CA has the right to authorise nodes that are about to join the blockchain network. When a new node is added to the blockchain, Fabric-CA will perform registration and verification operations on the new node. When Fabric-CA receives the correct feedback from the node, it will cryptographically sign the node's public key using its own private key. In our proposed scheme BFS, as the nodes contained in the blockchain network are mostly lightweight nodes, there is no need to keep all the transaction contents. In terms of node performance as well as system latency analysis, they do not have the capability to complete asymmetric cryptography. Therefore, a secure symmetric encryption scheme is required for the registration verification process.

We assume that a new user node joining the network has its own public key

and private key

. Fabric-CA

has its own public key

and private key

. The whole process of user node registration and verification is divided into the following seven parts (Zeng, Wang, Dong, She, & Jiang, Citation2021):

Fabric-CA

Fabric-CA

Fabric-CA uses

User

The user node

User

Similar to (2), the user node

Fabric-CA

Fabric-CA decrypts

Fabric-CA

Fabric-CA signs

User

The user node

At this point, the user node obtains its own identity certificate, completing the process of verification and registration. At the same time both Fabric-CA and the data storage module store the registration information of user node

. This function we encapsulate as a function

of the data storage module, i.e. generating the ID book

of user node

.

4.4 Privacy information control process

Based on the main threat of privacy information leakage of logistics company, we are able to automatically control the flow of privacy information operations of nodes in the blockchain by deploying smart contracts for protecting privacy information of logistics company in the blockchain network under the supply chain finance scenario.

When a node tries to access or upload privacy information in transaction information, we need to encrypt and decrypt the data. Take transaction information as an example, there are many attributes in transaction information

, which contains public attribute

and privacy attribute

. In order to avoid the problem that supply chain enterprises obtain a large amount of logistics information in order to make a quick response to the market and thus lead to easy leakage of privacy information of logistics company, we use the privacy attribute encryption algorithm of transaction information set, and finally get the transaction record set carrying ciphertext, which protects privacy information of logistics company. The specific steps are shown in Algorithm 1.

Table

Table

Table

4.5 Logistics company financing process

Having solved the problem of easy leakage of privacy information in the logistics company's financing process interacting with the blockchain, BFS is proposed as an integrated and highly trusted scheme to organise and manage all financing-related activities and operations of logistics company based on the financing dilemma of small and medium-sized logistics companies having difficulties in granting credit. Logistics companies upload their transaction information, logistics information, track information and financing information to the blockchain, providing their contribution to the whole supply chain and their past participation history, which can be evaluated by core business, factoring agencies and financial institutions in order to obtain credit and thus provide credit guarantees for their financing. In contrast to the financing dilemma of small and medium-sized logistics companies, which were generally financed by banks (Cainelli et al., Citation2020) and had low creditworthiness due to the difficulty of providing available high-priced collateral (Li & Chen, Citation2019), the BFS, with real-time visible and traceable logistics data of logistics companies, has significantly reduced the logistics companies’ financing threshold, making it easier for logistics companies to raise funds, enabling them to further expand their company scale, increase their business capacity and achieve sustainable development. At the same time, the BFS automatically responds to the activities of logistics companies through the deployment of smart contracts, greatly simplifying the process of lending and repayment and improving the efficiency of financing for logistics companies.

In our BFS, it is assumed that there are three types of nodes on the blockchain node network, namely logistics companies, factoring agencies and financial institutions. In the next discussion, ,

and

will be used instead of logistics companies, factoring agencies and financial institutions. The implementation steps of the scheme are as follows:

Once

When

After a successful transfer,

When

When

When

Figure 6. Lending process diagram.

Table

4.6 Scheme error control

In the process of transporting goods in the supply chain, logistics companies often suffer from temporary equipment failure due to unstable signals or bumpy roads, resulting in temporary node dropouts in the blockchain network, causing the transmission of logistics information or track information, etc. to be out of sync. In order to ensure the stability of logistics company transactions in the blockchain network under the supply chain finance scenario, based on this problem, we need to perform error control on the scheme to improve the fault tolerance of node dropout.

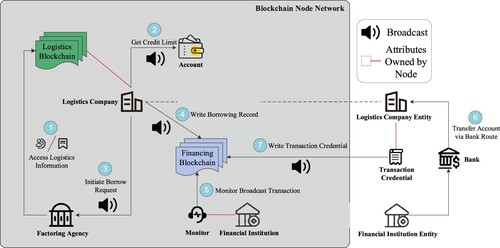

In order to guarantee consistency in the data of logistics company nodes, based on the Gossip protocol, each node in the blockchain network periodically broadcasts a message to indicate that it is alive and successfully connected to the network. Each node maintains a list of all nodes in the network, which records whether all nodes are alive or dead.

Suppose the network now exists with two nodes A and B, when node A receives an ALIVE message from node B, it will mark B as ALIVE. For A, B is a member of the network. If for some time, A does not receive an ALIVE message from B, it marks B as DEAD. So, B is no longer a member of the network. Assuming that B is “fake dead”, marked as DEAD but not dead, A will periodically try to connect to node B to check if it is alive. For example, it is possible that a network problem or a failure of another node caused an ALIVE message from B to not reach A, so when A contacts B directly, it can determine the true state of B. Each node signs the messages it sends, which indicates that there are no evil nodes in the network that fool other nodes by not forwarding messages.

If a logistics company node is temporarily disconnected from the network and reconnected to the network later, it may miss the broadcast process. In order to keep up with the data progress of other members in the network, the logistics company node will request its missing data through a pull-based mechanism, thus synchronising the data with other members of the network. In Fabric, nodes regularly exchange network member data and ledger data. Nodes can stay up to date at this time, even if they miss the broadcast process, and with scalable fault tolerance mechanisms, they can ensure the stability of nodes online and the consistency of data during transactions.

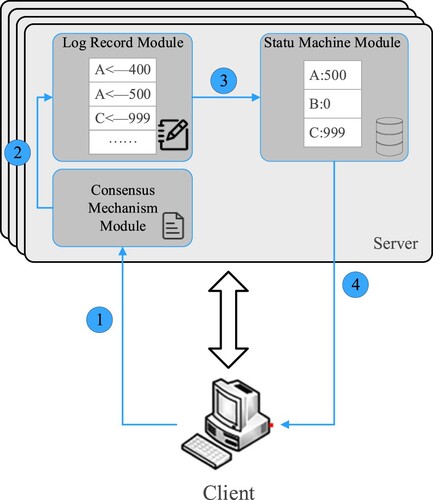

Meanwhile, the Raft consensus algorithm plugin was introduced after Fabric 1.4.1, which is more suitable for the production environment of supply chain finance than the previously existing Solo consensus and Kafka consensus. Raft is a distributed fault-tolerant consensus algorithm that ensures that the system can still process client requests in the event of a non-Byzantine failure of some nodes in the system, allowing the distributed nodes to maintain data consistency (Wang, Li, Xu, & Xu, Citation2021). Figure shows a diagrammatic representation of the Raft consensus algorithm.

Figure 7. Raft consensus algorithm.

Based on the above fault-tolerance mechanism, in the supply chain finance scenario, we can ensure that when the nodes in the blockchain network make the operation of query and invoke, even if a node drops out, the data of the network members can be recovered in time, and the logs of each node remain consistent, so that the behaviour of the whole distributed system remains consistent, and even if some nodes fail, such as a logistics company temporarily dropping out, there will be no major impact on the financing process, which is a good way to achieve error control.

5 System analysis

In this section, we analyse the performance of the proposed scheme. We implemented the entire simulation experiment on a desktop device running Ubuntu 16.04 (64-bit) with an Intel(R) Core(TM) i7-9750H CPU at 2.60 GHz and 16.0 GB of RAM. we put the nodes used into a Docker container to run, organised and coordinated by Docker technology.

To fully examine the performance of BFS, we evaluated the performance of BFS in performing basic operations based on two basic operations on a blockchain network in a supply chain finance scenario, i.e. query and invoke, by analysing the feedback values of system throughput after Locust sends a request. We simulated 5000 user nodes for query and invoke operations to observe the variation of throughput and mean response time (MRT) for different QPS (query per second), different log levels and different block sizes of the system.

5.1 Overhead evaluation

The resource overheads of logistics transactions in Logistics 4.0 can be used to determine whether logistics transactions and validation functions are operating properly and consistently. However, there is a gap in the field of supply chain finance where researchers have studied financing schemes for logistics companies, and there is not a more complete financing scheme for logistics companies. In order to ensure the quality of the efficiency of the transaction process in the supply chain finance scenario, we chose a native Hyperledger Fabric-based financing scheme for logistics companies to evaluate the effectiveness of the proposed approach. To balance the relationship between transaction efficiency and privacy protection in supply chain finance, we proposed a blockchain-based financing scheme (BFS) for logistics companies by classifying their information into types to be entered into the blockchain data storage module. A comparison of the overhead performance is shown in Table . Because the financing process is greatly simplified in BFS, the logistics company, after uploading trusted logistics data, only needs to submit a request when lending and a request when repaying, and all other processes can be carried out automatically by smart contracts, while each transaction process is under supervision and the transmitted data is processed with privacy information, so the time complexity is greatly reduced and the transaction overhead is also decreased, which theoretically proves the superiority of our scheme, while ensuring the trustworthiness of the transaction and data security.

Table 3. The comparison of overhead performance for different scheme

5.2 Performance analysis of network query operation

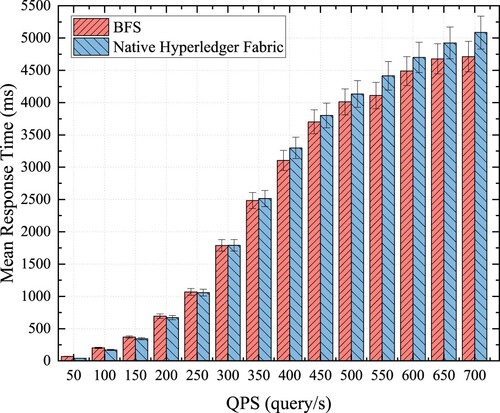

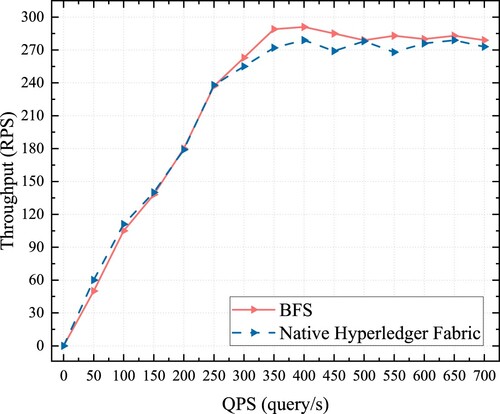

As shown in Figure and Figure , it can be seen that when the QPS is between 0-400, MRT and throughput keep increasing, after which the increasing trend of MRT slows down and throughput gradually decreases, and throughput starts to stabilise after dropping to 280 RPS. When QPS is between 0-250, the performance of native Hyperledger Fabric is slightly better than BFS at this time, because the topology in the blockchain network is not yet stable and Hyperledger Fabric has higher processing efficiency. As the QPS increases, the blockchain network structure and transaction logic gradually stabilises, and because BFS avoids duplicate transaction logic when querying operations, BFS outperforms native Hyperledger Fabric. According to system performance feedback, the system bottleneck is reached at this point, and I/O performance reaches its peak. We can see that our proposed scheme, BFS, outperforms the native Hyperledger Fabric, has a lower mean response time and higher stable throughput and is more stable. By analysing the experimental results, we can conclude that the throughput of BFS queries is about 280 RPS, which can meet the needs of supply chain systems of small and medium-sized logistics companies, improve the data validation speed of logistics companies, and alleviate their financing difficulties. Due to the limitation of hardware conditions, this experiment has more room for improvement in performance.

Figure 8. System MRT performance under different QPS.

Figure 9. System throughput performance of query under different QPS.

5.3 Performance Analysis of Network invoke operation

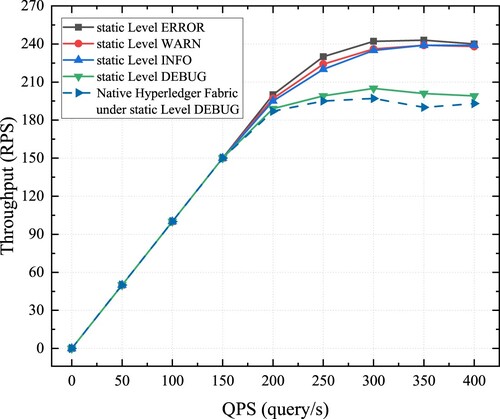

As can be seen in Figure , at a block size of 1024KB, the throughput steadily increases when the QPS is between 0 and 200, independent of the log level. After that, the rising trend of throughput becomes slow and stabilises. As can be seen, the higher the log level, the higher the throughput of the system. When the logging level is set to DEBUG, the stable value of throughput is very different from the other three levels. The reason for this is that the lower the log level in Fabric, the more detailed the log output will be, and the DEBUG level is the lowest log level, making it easier for system administrators to debug problems after they have occurred. However, too much logging information output can reduce the throughput performance of the system. It can be seen that BFS has better transfer performance under the same log level condition. This is because BFS can find the demanded transaction information from the data storage module faster in a stable topology and can optimise many repetitive transaction logics in the related operations in the supply chain finance scenario, which can significantly improve the transaction efficiency and enhance the financing efficiency of logistics companies.

Figure 10. System throughput performance under different log level.

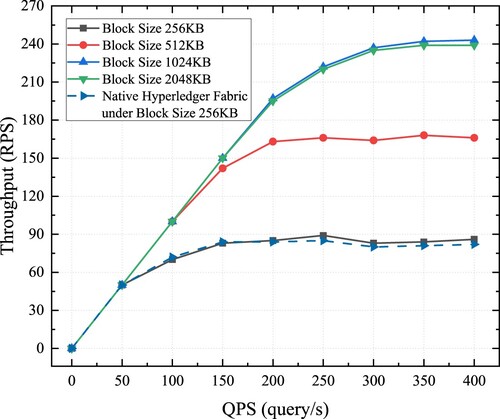

As can be seen from Figure , with a log level of INFO, the block size affects the stable value of system throughput as the QPS increases, and the stable value of system throughput increases with the block size. When the block size is greater than 1024KB, the stable value of throughput no longer varies and stabilises at around 240RPS. It can be seen that in the current experimental environment, when the block size is larger than 1024KB, the bottleneck of the system has been reached and the system performance cannot be further improved. However, it can be seen that BFS still has a high-performance advantage at the same block size as the native Hyperledger Fabric.

Figure 11. System throughput performance under different block size.

As seen above, BFS can achieve greater throughput, lower mean response time and a more stable transaction process than native Hyperledger Fabric, while providing greater privacy data protection. The overall throughput of the scheme can be increased by changing system parameters, such as logging levels and block sizes in the configuration file, depending on the actual production environment of the logistics company in the supply chain.

6 Conclusion

As the financing of logistics company in supply chain finance is hindered by factors such as their low credit, slow data verification, easy privacy leakage and easy data tampering, it is important to solve this development problem. Considering the natural characteristics of blockchain data that cannot be tampered with and shared ledger, this paper proposes a blockchain-based financing scheme for logistics company in supply chain finance, filling a research gap in the supply chain field to solve their financing problems from the perspective of logistics company. With logistics data that is visible and traceable to logistics company in real-time, BFS significantly reduces the financing threshold for logistics company and improves their creditworthiness. It also greatly simplifies the process of financing for logistics company and improves the efficiency of data validation. Experimental results show that the scheme can achieve a stable transaction throughput of around 280 RPS, and the data transfer under different levels of logs and different block sizes can also meet the financing needs of logistics company. At the same time, we also investigated the privacy issues of logistics company. We have modified the content of smart contracts deployed in supply chain finance scenarios and proposed algorithms for privacy information control of logistics company, this work has led to a higher level of security in our financing scheme. Of course, there is still room for improvement in our work. Our future research focuses on three directions, the first of which is to use the Internet of Things to solve the tamper-proof solution for manually entered data, thus achieving full authenticity of the data; the second direction is to select or improve the consensus mechanism suitable for the BFS, where the focus is on how to attract core business to join, achieve the distribution of benefits within the system and achieve block consistency; the third direction is how supply chain managers can further leverage the advantages that logistics companies hold in the supply chain in the face of the development of logistics companies.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Bals, C. (2019). Toward a supply chain finance (SCF) ecosystem–proposing a framework and agenda for future research. Journal of Purchasing and Supply Management, 25(2), 105–117. https://doi.org/10.1016/j.pursup.2018.07.005

- Cainelli, G., Giannini, V., & Iacobucci, D. (2020). Small firms and bank financing in bad times. Small Business Economics, 55(4), 943–953. https://doi.org/10.1007/s11187-019-00164-7

- Chacko J. A., Mayer, R., & Jacobsen, H. A. (2021). Why do my blockchain transactions fail? a study of hyperledger fabric. Proceedings of the 2021 International Conference on Management of Data, 221–234.

- Chen, L., Chan, H. K., & Zhao, X. (2020). Supply chain finance: Latest research topics and research opportunities. International Journal of Production Economics, 229. https://doi.org/10.1016/j.ijpe.2020.107766.

- De Fiore, F., & Uhlig, H. (2011). Bank finance versus bond finance. Journal of Money, Credit and Banking, 43(7), 1399–1421. https://doi.org/10.1111/j.1538-4616.2011.00429.x

- Flor, C. R., & Hirth, S. (2013). Asset liquidity, corporate investment, and endogenous financing costs. Journal of Banking & Finance, 37(2), 474–489. https://doi.org/10.1016/j.jbankfin.2012.09.014

- Gompers, P., & Lerner, J. (2003). “Equity financing.” Handbook of entrepreneurship research. Springer. 267–298.

- Guida, M., Moretto A, M., & Caniato F, F. A. (2021). How to select a supply chain finance solution? Journal of Purchasing and Supply Management, 27(4), 100701. https://doi.org/10.1016/j.pursup.2021.100701

- Harish A. R., Liu X, L., Zhong R, Y., Rachana Harish, A., & Huang, G. Q. (2021). Log-flock: A blockchain-enabled platform for digital asset valuation and risk assessment in E-commerce logistics financing. Computers & Industrial Engineering, 151, 107001. https://doi.org/10.1016/j.cie.2020.107001

- Jin S. Y., Niu Z, X., & Qi, S. (2013). The Analysis of a shares logistics enterprises’ financing structure. Advanced Materials Research. Trans Tech Publications Ltd, 709, 716–720. https://doi.org/10.4028/www.scientific.net/AMR.709.716

- Li, M., Shao, S., Ye, Q., Xu, G., & Huang, G. Q. (2020). Blockchain-enabled logistics finance execution platform for capital-constrained E-commerce retail. Robotics and Computer-Integrated Manufacturing, 65, 101962. https://doi.org/10.1016/j.rcim.2020.101962

- Li, S., & Chen, X. (2019). The role of supply chain finance in third-party logistics industry: A case study from China. International Journal of Logistics Research and Applications, 22(2), 154–171. https://doi.org/10.1080/13675567.2018.1502745

- Li, Y., Stasinakis, C., & Yeo W. M. (2022). A Hybrid XGBoost-MLP model for credit risk assessment on digital supply chain finance. Forecasting, 4(1), 184–207. https://doi.org/10.3390/forecast4010011

- Liang, W., Fan, Y., Li K, C., Zhang, D., & Gaudiot, J.-L. (2020). Secure data storage and recovery in industrial blockchain network environments. IEEE Transactions on Industrial Informatics, 16(10), 6543–6552. https://doi.org/10.1109/TII.2020.2966069

- Liang, W., Xiao, L., Zhang, K., Tang, M., He, D., & Li, K. C. (2021). Data fusion approach for collaborative anomaly intrusion detection in blockchain-based systems. IEEE Internet of Things Journal, 1. https://doi.org/10.1109/JIOT.2021.3053842

- Liang, W., Zhang, D., Lei, X., Tang, M., Li, K.-C., & Zomaya, A. Y. (2020). Circuit copyright blockchain: Blockchain-based homomorphic encryption for IP circuit protection. IEEE Transactions on Emerging Topics in Computing, 9(3), 1410–1420. https://doi.org/10.1109/TETC.2020.2993032

- Liebl, J., Hartmann, E., & Feisel, E. (2016). Reverse factoring in the supply chain: Objectives, antecedents and implementation barriers. International Journal of Physical Distribution & Logistics Management, 46(4), 393–413. https://doi.org/10.1108/IJPDLM-08-2014-0171

- Ma, C., Kong, X., Lan, Q., Wang, X., Huang, F., & Chen, H. (2019). The privacy protection mechanism of Hyperledger Fabric and its application in supply chain finance. Cybersecurity, 2(1), 1–9. https://doi.org/10.1186/s42400-018-0018-3

- Tiberius, V., & Hauptmeijer, R. (2021). Equity crowdfunding: Forecasting market development, platform evolution, and regulation. Journal of Small Business Management, 59(2), 337–369. https://doi.org/10.1080/00472778.2020.1849714

- Venkatesh V. G., Kang, K., Wang, B., Zhong, R. Y., & Zhang, A. (2020). System architecture for blockchain based transparency of supply chain social sustainability. Robotics and Computer-Integrated Manufacturing, 63, 101896. https://doi.org/10.1016/j.rcim.2019.101896

- Wang, F., Yang, X., Zhuo, X., & Xiong, M. (2019). Joint logistics and financial services by a 3PL firm: Effects of risk preference and demand volatility. Transportation Research Part E: Logistics and Transportation Review, 130, 312–328. https://doi.org/10.1016/j.tre.2019.09.006

- Wang, X., She, X., Bai, L., Qing, Y., & Jiang, F. (2021). A novel anonymous authentication scheme based on edge Computing in Internet of vehicles. Computers, Materials & Continua, 67(3), 3349–3361. https://doi.org/10.32604/cmc.2021.012454

- Wang, Y., Li, S., Xu, L., & Xu, L. (2021, September). Improved raft consensus algorithm in high real-time and highly adversarial environment. International Conference on Web Information Systems and Applications.

- Woschank, M., & Dallasega, P. (2021). The impact of logistics 4.0 on performance in manufacturing companies: A pilot study. Procedia Manufacturing, 55, 487–491. https://doi.org/10.1016/j.promfg.2021.10.066

- Xue, X., Dou, J., & Shang, Y. (2020). Blockchain-driven supply chain decentralized operations– information sharing perspective. Business Process Management Journal, 27 (1), 184–203. https://doi.org/10.1108/BPMJ-12-2019-0518

- Zeng, P., Liu, A., Zhu, C., Wang, T., & Zhang, S. (2022). Trust based multi-agent imitation learning for green edge computing in smart cities. IEEE Transactions on Green Communications and Networking, 1. https://doi.org/10.1109/TGCN.2022.3172367

- Zeng, P., Wang, X., Dong, L., She, X., & Jiang, F. (2021). A blockchain scheme based on DAG structure security solution for IIoT. IEEE 20th International Conference on Trust, Security and Privacy in Computing and Communications (TrustCom). https://doi.org/10.1109/TrustCom53373.2021.00131

- Zhang, T. L., Li, J., & Jiang, X. (2021). Analysis of supply chain finance based on blockchain. Procedia Computer Science, 187, 1–6. https://doi.org/10.1016/j.procs.2021.04.025