IMPACT

This article shows that instead of technical skills, traditionally seen as the main element in public sector accounting education, interpersonal skills are competencies that need further development by public sector management accountants. By identifying the importance of competencies, as well as analysing the degree to which professionals possess these competencies, the authors provide a framework for further analysis on the education needs of public sector financial specialists.

ABSTRACT

Using survey data gathered among Dutch public sector management accountants, this contribution shows that appreciative skills and personal skills are considered the most important competencies of these professionals. The authors found gaps between the assigned importance and the actual level of competencies in the fields of interpersonal skills and technical skills. As well, there were differences between age groups.

Introduction

By means of public sector accounting education (PSAE), a wide range of professionals working in public sector organizations are empowered to do their job according to relevant standards. These professionals include management accountants working in the public sector, who are often called ‘public controllers’ (Budding et al., Citation2019). These employees have an active role in advising the organization and its management about formulating, realizing and evaluating social and financial results, as well as the structure and operation of the management control system, reporting and accountability issues. They do so in an independent and objective way (Budding & Wassenaar, Citation2021). As this places high demands on these employees (Sathe, Citation1983), they need the right competencies to adequately fulfil their roles. We define competencies as context-dependent knowledge, skills and approaches that are inseparable, in which emotional, motivational, normative and ethical elements play an important role. It is only partly possible to make them objectively measurable.

Several frameworks are available for distinguishing the competencies that professionals require. One of these is the framework developed by CIPFA (Citation2020), which identifies 30 key competencies, which are mapped in four core thematic areas public sector financial specialists may need. According to CIPFA: ‘Given the rich diversity of career pathways within the public finance profession, it is not the case that everyone will need all the competencies listed’ and the institute hopes that their framework ‘will serve as a ‘conversation-starter’ to help identify training needs' (CIPFA, Citation2020, p. 2).

This article explains which competencies are needed by public sector management accountants and explores whether there are gaps between the importance assigned to specific competencies and the actual level of skills. If such gaps exist, public sector management accounting education can help to bridge this gap.

Research method

In order to understand the competencies public sector management accountants need, we relied on Birkett’s (Citation2002) competency model. We did so as this framework has been used earlier in publications on accounting education (Bots et al., Citation2009; Tan & Laswad, Citation2018) and distinguishes several levels of competencies. Following Bots et al. (Citation2009) we used three out of the originally five levels (). Level 1 consists of two categories of skills: cognitive skills and behavioural skills. Level 2 distinguishes six sets of competencies: technical skills, analytic/design skills, appreciative skills, personal skills, interpersonal skills, and operational skills. Level 3 provides examples of the skills that are elements of those mentioned in level 2.

Table 1. Competencies according to Birkett (Citation2002).

To gather our data, we sent a short questionnaire to a group of people who subscribed to a one-day seminar (held online in May 2021) on competencies of management accountants working in public and not-for-profit organizations. We asked them to fill out this questionnaire before the seminar took place. Out of 71 participants, 54 completed the questionnaire—leading to a satisfactory response rate of 76.1%. About half of the participants were employed at a municipality or in central government; the other half worked for hospitals, schools or other not-for-profit organizations. Most of the participants held the position of ‘senior controller’ (or a comparable title) and had successfully completed a post-experience course in public sector management accounting, most frequently the ‘Certified Public Controller’ programme.

Our questionnaire was mainly based on the competency model as originally built by Birkett (Citation2002) and further developed (and used) by Bots et al. (Citation2009). We asked our respondents to rank six sets of competencies (‘level 2’ in ), first by indicating the importance they assigned to the specific competency; second by giving a self-assessment about the actual level of their skills on the proposed competency. We requested them to do so by putting the six sets of competencies in order of significance—so a competence on position 1 was considered the most important (or most present), and a competence on position 6 was the least important (or the least present).

Importance of competencies

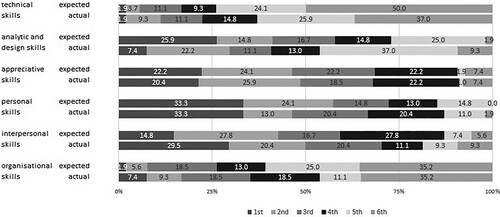

As clearly shows, most respondents considered appreciative skills (for example looking at problems from multi-disciplinary perspectives) as the most important competencies management accountants should possess. Personal skills, analytical/design skills and interpersonal skills ranked second, third and fourth, respectively. Organizational skills and technical skills presented a different picture; most respondents thought that these were less important than the other competencies we distinguished.

Figure 1. Importance of competencies and actual skills.

Note: The numbers in the bars indicate the percentage of respondents that rank a certain competency in a category (for example 35.2% of the respondents ranked the technical skills 6th as far as importance is concerned).

Actual skills

When we focused on the extent to which respondents indicated that they possess the competencies, we observed that the main findings were in line with what they considered to be the importance of the competencies. The main differences were with the competencies interpersonal skills, technical skills, analytical skills and organizational skills. Whereas the respondents thought that their actual interpersonal skills lagged behind the importance of this category, the opposite was found for technical skills, analytical skills and organizational skills. Some smaller differences were found for appreciative skills (ranked higher in importance than in actual competencies) and personal skills. Our findings also held when we looked at the average rank the respondents attached to the importance of the competencies, as well as the actual skills they possessed ().

Table 2. Mean rank of competencies by age group.

Differences in age groups

Following Bots et al. (Citation2009), we also investigated the differences between younger and older management accountants. We divided our sample into four (almost equal) groups. Our first quartile was younger than 45 years old, and our fourth quartile was older than 55. For each group, we calculated the mean rank the respondents attached to the importance of the competencies, as well as the actual skills they thought they possessed (see ).

We found that the youngest quartile of respondents considered the competencies in the fields of technical skills, analytical/design skills, appreciative skills and personal skills as more important than the respondents that did not belong to this group, whereas we found opposite results for interpersonal skills and organizational skills.

Focusing on the gaps between the importance assigned to competencies and the actual skills, we found that our younger management accountants perceived that their actual competencies on the fields of appreciative skills and interpersonal skills lagged behind the importance of them. For the analytical/design skills and organizational skills, the opposite results were observed.

The main findings for the oldest quartile were that the respondents in this group thought that technical skills and personal skills were less important than the respondents that did not belong to this group, whereas interpersonal skills and organizational skills were seen as more important.

When we considered the differences in gaps between the importance assigned to competencies and actual skills, we observed large differences between the age groups. Whereas we found for the oldest quartile that the respondents thought that their actual technical skills scored higher than the importance of these competencies, this gap was almost non-existent in the youngest quartile. The opposite was the case for analytical/design skills and organizational skills: here it was the youngest quartile that expressed that their actual skills scored higher than the importance of these. For appreciative skills, there were indications that the youngest quartile thought that their actual skills lagged behind the importance of these, whereas the gap was much smaller for the oldest quartile. For personal skills, we found that the youngest quartile considered their actual skills were higher than the importance assigned to them, whereas the opposite was the case for the oldest quartile. Finally, for interpersonal skills, the differences between the youngest and oldest quartile were small: both groups considered the importance of these competencies as higher than their actual skills.

Implications for PSAE

The findings of our study have many implications:

Appreciative skills and personal skills were considered to be the two most important competencies of public sector management accountants, much more important than technical skills, which are traditionally an important element in PSAE.

As the respondents to our survey considered the importance of interpersonal skills much higher than their actual level of competencies in this field, this calls for more attention to how this competency could be further developed and the role PSAE can play in this development.

The considerable differences between the age groups indicate differences in training needs between less and more experienced accounting professionals in public sector organizations.

Avenues for further research

This short contribution is not without limitations and several avenues for future research are possible. First, the sample size was relatively small and focused on more experienced public sector management accountants. This limits the generalizability of our findings, therefore future research would be advised to use a larger dataset.

Second, we relied on the self-perception of public sector management accountants considering their own level of skills as well as the importance of competencies. For future research, it would be useful to take the point of view of the ‘customers’ of the public sector management accounting functions into account; as suggested by Budding and Wassenaar (Citation2021).

Finally, self-rating may come at the risk of introducing self-evaluation bias. More specifically, unskilled individuals may often overestimate their ability, whereas the opposite is true for more competent individuals—the so-called ‘Dunning–Kruger effect’ (Kruger & Dunning, Citation1999). Furthermore, individuals may find it difficult to indicate the importance of competencies in a specific number, especially when many competencies are considered important. In our analysis we tried to minimize these problems by using a ranking system, but this may have forced our respondents to rank the competencies in an unbalanced way.

Despite these limitations, we hope that this contribution will add to the debate about the competencies public sector finance professions have and need, and how PSAE can contribute to that.

References

- Birkett, W. P. (2002). Competency profiles for management accounting practice and practitioners. A report of the AIB, Accountants in Business section of the International Federation of Accountants. IFAC.

- Bots, J. M., Groenland, E., & Swagerman, D. M. (2009). An empirical test of Birkett’s competency model for management accountants: Survey evidence from Dutch practitioners. Journal of Accounting Education, 27(1), 1–13.

- Budding, G. T., Schoute, M., Dijkman, A., & De With, E. (2019). The activities of management accountants: Results from a survey study. Management Accounting Quarterly, 20(2), 29–37.

- Budding, G. T., & Wassenaar, M. C. (2021). New development: Is there a management accountants’ expectation gap? Public Money & Management, 41(4), 346–350.

- CIPFA. (2020). Key competencies for public sector finance professionals.

- Kruger, J., & Dunning, D. (1999). Unskilled and unaware of it: How difficulties in recognizing one's own incompetence lead to inflated self-assessments. Journal of Personality and Social Psychology, 77(6), 1121–1134.

- Sathe, V. (1983). The controller's role in management. Organizational Dynamics, 11(3), 31–48.

- Tan, L. M., & Laswad, F. (2018). Professional skills required of accountants: What do job advertisements tell us? Accounting Education, 27(4), 403–432.