IMPACT

This article provides new insights to help policy-makers, professional associations and standard setters in developing countries design and implement accrual accounting-based systems applied to the public sector. The detailed discussion of prior research on the main advantages of the accrual basis of accounting, and generally accepted international standards when adapted to the public sector, and the barriers and difficulties experienced by other jurisdictions in similar contexts provides important lessons for reforming public sector accounting systems in developing countries

ABSTRACT

This article presents a bibliometric analysis of the adoption and implementation of accrual accounting in the public sector (AAPS) in the context of emerging economies and identifies gaps where more research is needed. The main findings evidence a significant interest in this topic in the past five years and the authors expect this to grow in the future. The questionnaire method was the most common data collection method, followed by combinations of mixed methods. An interesting finding was a preference for quantitative methods when studying professionals. More qualitative methods were used for politicians and members of international organizations. The NPM agenda and institutional theory dominated the theoretical background. Coercive pressures from investors and auditors, together with the normative pressures from employee training, were found to significantly impact the effective implementation of AAPS in emerging economies.

Introduction

Accrual accounting, a mainstream public financial management reform, is an effort to institute changes in public administrations (Azevedo, de Aquino, et al., Citation2020; Matekele & Komba, Citation2020; Muraina & Dandago, Citation2020; Rozaidy & Siti-Nabiha, Citation2022) to respond to new information needs under New Public Management (NPM) (Lapsley, Citation2009), as well as to progress the international harmonization process (Brito & Jorge, Citation2021). The more comprehensive nature of accrual accounting information has advantages over cash basis accounting from a credibility perspective (Ferry et al., Citation2018). As well, a more informative accounting system serves two functions: it provides comprehensive and reliable information on public finances and a basis for a better financial management and control of government activities (Luder, Citation1992; Wynne, Citation2004). Therefore, public sector accounting promotes financial transparency and supports the prevention of fraud and waste in public sector entities (Brito & Jorge, Citation2021). International organizations, such as the International Monetary Fund (IMF) and the World Bank, have strongly supported the use of accrual accounting in emerging economies (Adhikari & Gårseth-Nesbakk, Citation2016; Adhikari & Jayasinghe, Citation2017; Harun et al., Citation2012). The process of adopting accrual accounting in the public sector (AAPS) in emerging economies has been heavily pushed by coercive and mimetic forces to deal with public sector management and not so much as a way of improving existing government accounting practices (Rozaidy & Siti-Nabiha, Citation2022).

The benefits and effects of AAPS have been criticised in the literature due to the mismatch between benchmark standards that follow private sector rules rather than the specificities of the public sector (Lapsley et al., Citation2009; Oulasvirta, Citation2014). This criticism is particularly relevant in emerging countries with empirical evidence of dysfunctional and unintended consequences and failures in AAPS implementation, with some countries to abandoning reforms (Adhikari & Jayasinghe, Citation2017; Adhikari et al., Citation2019). In addition, accrual accounting provides more comprehensive information on the assets and the full cost of public services, Wynne (Citation2004) questions the effective need and use of this kind of information by public sector managers—particularly in terms of the costs of employing significantly more qualified accountants. Risks and disadvantages, according to Wynne (Citation2004), include the complexity of the accrual accounting system compared to the cash-based system, a general preference for cash-based information for decision-making making governments less accountable; the lack of adequate skills and competences; the greater need for professional judgment; and the lack of good IT systems.

Our study fills a gap in the literature on the process of transition to AAPS in emerging economies. Our aim was to look at all forms of accrual accounting systems used in emerging economies in order to:

Explore and investigate the state of the art on the adoption and implementation of AAPS in the context of emerging economies.

Understand the determinants of the transition to AAPS in this specific context.

Identify gaps and point out future research tracks.

Using bibliometric analysis, we covered the literature on AAPS in emerging economies until 2022; 61 articles were collected using two databases—Scopus and Web of Science (WoS).

The main conclusions of the study point to a growing interest in the topic over the past five years. The costs of implementing new accounting systems, the lack of technical training by professionals and a lack of IT support were found to be determining factors for the success of the reform. A combination of NPM incentives with the isomorphism inspired by the institutional theory helps to explain the main adoption drivers of AAPS in emerging economies, with coercive and normative pressures dominating. It was clear that more research is needed to help governments and institutions in these emerging contexts to move successfully to accrual-based accounting.

Methodological approach

The main objective was to develop a research study on the adoption and implementation of AAPS in the context of emerging economies. The studies by Polzer et al. (Citation2021), Van Helden and Uddin (Citation2016) and Van Helden et al. (Citation2021) were the only relevant studies we knew about. However, the first of these focuses on the adoption of International Public Sector Accounting Standards (IPSAS) (and not specifically on the accrual accounting approach); the second is oriented towards investigating the nature and use of management accounting practices by public entities; and the third presents a systematic review of articles on public accounting in emerging countries published only in the Journal of Accounting in Emerging Economies (JAEE). Therefore, bibliometric analysis makes an important contribution to knowledge about the adoption and implementation of AAPS in the context of emerging economies by mapping publications to date and clarifying the methods, theories and determinants of this reform.

Bibliometric analysis is a good statistical tool to assess and investigate a specific field of knowledge, build relationships and assess the influence of publication in the scientific community (Casprini et al., Citation2020). It adds value to other methodologies in that it offers structured results to a massive volume of information, presents trends and performance over time, clusters and builds an interrelated conceptual framework and identifies the most prolific contributors (authors, affiliations and countries) and offers clues for research on a specific topic (Najaf et al., Citation2021).

We collected data using a prescribed and replicable methodology, with the aim of providing a clear path for synthesizing and evaluating the main findings of relevant studies on the topic (Meijer & Bolívar, Citation2016; Santis et al., Citation2018; Tranfield et al., Citation2003; Voorberg et al., Citation2015). An important step was the clarification of inclusion/exclusion criteria based on defined and precise rules (Kroll, Citation2015). We began by identifying articles published in peer-reviewed journals, indexed in Scopus and WoS, which contribute to research on AAPS in the context of emerging economies. These databases were chosen due to the quality of the publications indexed in them in terms of citation counts per article and other additional data (Zhu & Liu, Citation2020). We only included articles published in journals because they are considered validated knowledge (Voorberg et al., Citation2015), while articles published in books and conference proceedings were excluded due to generally inferior (if any) peer review processes.

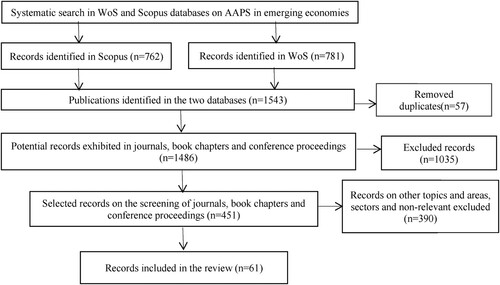

The search for articles was conducted on 28 February 2022 and included all articles in English, without any limitations in terms of year of publication or the scope of the journals publishing them. The search was performed in the title, abstract and keywords fields. Four search terms were defined. Each term was a combination of the keywords accrual accounting with additional keywords: public sector, government, emerging economies and emerging countries. In the first stage of the search 1,543 hits were obtained, with WoS providing the largest number of records (781 documents). The search term that produced the largest number of hits was accrual accounting AND government (734 documents), while the one that produced the fewest results was accrual accounting AND emerging economies (119 documents). Each article was manually selected to analyse whether the content was related to AAPS in emerging economies; articles that did not provide an explicit or sufficient link between accrual accounting and public sector accounting were removed. No time limit was set for our analysis and a considerable amount of time and effort was devoted to data integrity and accurate analyses.

As suggested by Hochrein and Glock (Citation2012), articles were considered relevant if they contained one of the keywords in their title and at least one search term from the keyword group in their abstract. At this stage, the selected articles underwent further analysis of their abstracts and, if deemed relevant or in case of doubt, were chosen for a full reading of their content (Hochrein & Glock, Citation2012; Seuring & Gold, Citation2012). Again, articles that did not directly relate to the topic of the study were removed. The final database consisted of 61 articles. briefly describes the article sample selection process undertaken for this study.

Figure 1. Flow diagram of the research methodology.

Results of the bibliometric analysis

Articles on the adoption and implementation of AAPS in emerging economies were categorized following the approach used by Schmidthuber et al. (Citation2020). Thus, the evolution of publications in terms of quantity and quality, the geographical location of publication, the supporting theories and research methods used were analysed.

Evolution of publications on AAPS in emerging economies

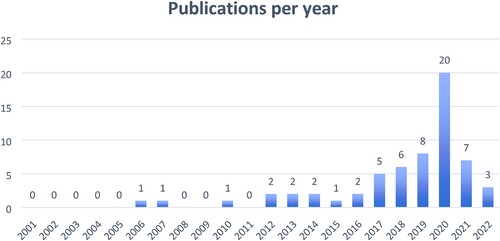

shows that studies on AAPS in emerging economies have been published since 2006, reaching the highest number of publications in 2020, with 20 articles, corresponding to 33% of the sample. There was a growth in interest in research on the subject in the period under analysis. The average number of publications was 2.9 per year. These results demonstrate a growing scientific interest in research on the transition to AAPS in emerging economies.

Figure 2. Number of articles published per year.

Additionally, a growing number of citations indicates the increasing importance of AAPS in academic research. shows the selected articles with the highest impact factor, in descending order of citations received from WoS and Scopus, along with their respective years of publication and authors. We selected our sample of articles according to the citations in WoS, as this is widely considered to be the most demanding database. Bakre et al. (Citation2017) had the highest number of citations (24) and Aquino et al. (Citation2020) had the lowest number (4). However, Aquino et al. (Citation2020) would be in 4th place in the Scopus ranking warning us to take care when analysing citations. Of course Aquino et al. (Citation2020) was recently published and therefore had less time to be cited than the other articles in the list. We found that Bakre et al. (Citation2017) was one of the most influential researchers on AAPS in emerging countries and specifically in Africa.

Table 1. Top 10 articles by number of citations.

Journals

Our articles were published in 26 specialist journals, showing that research on AAPS in the context of emerging economies has received attention from a wide variety of journals (as concluded by Schmidthuber et al., Citation2020). lists the 10 journals that published a higher number of identified articles. The journal Public Money & Management led with the highest number of articles, having published 10 of the 61 articles, corresponding to 16% of the sample. The other journals were: Financial Accountability & Management (five), Journal of Accounting in Emerging Economies (five), Accounting, Auditing & Accountability Journal (four), Accounting Forum (four), International Journal of Public Sector Management (four), Journal of Accounting & Organizational Change (four), Journal of Public Budgeting, Accounting & Financial Management (three), Critical Perspective on Accounting (two) and International Journal of Public Administration (two).

Table 2. Number of articles per journal and JCR 2020 score.

AAPS research was predominantly published in journals focusing on public financial management, while the accounting and finance as well as business management journals published comparatively fewer articles on AAPS. Notably, Abacus and Accounting, Organizations & Society, which are journals with a high impact factor in the accounting field, did not publish any articles on AAPS in this period.

Countries and continents analysed

The second classification criterion was the geographical area investigated in the articles analysed. classifies the articles according to the geographical area on which they focused. Panel A identifies 51 studies that analysed an individual country and 10 studies that adopted a comparative approach (), while Panel B identifies the continents to which the studies conducted belonged (Africa, America, Asia, Europe and more than one continent). Indonesia was the most studied country, with 16 articles, followed by Malaysia with seven published articles.

Table 3. Countries and continents analysed.

Table 4. Studies taking a comparative approach.

Next, comparative studies of the African region (four) and Nigeria (four) were among the most studied countries. However, Brazil (three), Colombia (three) and Sri Lanka (three) also stood out. The continent with the most studies on AAPS was Asia (38 articles); the transition to AAPS in emerging economies is likely associated with the rapid economic growth in this whole region in the past decade. Asia was followed by Africa (11 articles) and America (nine articles) showing a relative lack of research in these continents. As expected, only one study was found for in Europe (Ismaili et al., Citation2021). Two articles covered more than one continent: Adhikari et al. (Citation2019) on the implementation of public sector accounting reforms in Egypt, Nepal and Sri Lanka; and Polzer et al. (Citation2021) on the adoption of IPSAS in emerging economies and low-income countries. Only one article was found on the Middle East, and that focused on Jordan, so we did not have enough evidence to understand the transition to accrual accounting in this region. Furthermore, no study was found from the Oceania context which can be associated with the small size of Polynesian and Melanesian nations.

Supporting theories and paradigms

The use of a robust theoretical framework is a fundamental aspect to increase knowledge in this area. summarizes the main supporting theories found in the studies analysed, highlighting the diversity of theories used to explain the adoption and implementation of AAPS in emerging economies. We found that about 10% of the articles did not clearly define the theoretical framework adopted—this was also concluded by Polzer et al. (Citation2021) in their research on the adoption of IPSAS and Van Helden and Uddin (Citation2016) in their study of the implementation of management accounting practices in emerging economies. On the other hand, the results show that the NPM agenda, inspired by economic theory, was the theoretical framework used in about 46% of the total articles. This result was also confirmed by other studies that concluded on the importance of the NPM agenda in public sector accounting research (see, for example, Bergmann et al., Citation2019 or Van Helden et al., Citation2021). Moreover, about 71% of the articles used the NPM agenda or institutional theory (specifically new institutional sociology) to understand the changes of public accounting in governments (as did Gomes et al., Citation2015 which used both). Additionally, Haija et al. (Citation2021) used institutional theory to show how organizations and countries may react under the pressure of adopting a new set of regulations and changes. Also, Polzer et al. (Citation2021) found that institutional theory dominated research conducted in emerging economies. Diffusion and behavioural theories also appeared to be beginning to capture the interest of academics for this type of research. On the other hand, only Brito and Jorge (Citation2021) used a combination of contingency theory and institutional theory. The development of these new theoretical approaches and their combinations are important clues to our prediction of an increase in future studies.

Table 5. Supporting theories/paradigms.

Data collection methods

summarises the data collection methods. Similarly to the study by Schmidthuber et al. (Citation2020), our results show that the questionnaire method was the most used (21.5% of the articles). Examples are the studies by Alghizzawi and Masruki (Citation2020), Aswar et al. (Citation2021), Hayat et al. (Citation2020), Ismail (Citation2022), Ismail et al. (Citation2018), Ismaili et al. (Citation2021) and Mbelwa et al. (Citation2019). Some authors used mixed methods, combining interviews with documentary analysis (19.5%), such as Adhikari and Jayasinghe (Citation2017), Adhikari et al. (Citation2019), Bakre et al. (Citation2021), Bakre et al. (Citation2017), Aquino et al. (Citation2020), Azevedo, Lino, et al. (Citation2020), Jayasinghe et al. (Citation2020), McLeod and Harun (Citation2014), Ocampo-Salazar (Citation2020). Some used interviews plus questionnaires (5%). We found more descriptive articles, without using an explicit methodology (10%) and the use of official databases (10%). Contrary to Polzer et al. (Citation2021), whose research found that over 50% of studies used content analysis, we found that documentary analysis was used, in isolation, in only 8% of the articles. However, this method was generally used as a complementary method to other methods, such as interviews, case study and questionnaires.

Table 6. Data collection methods.

Comparing methods with the subjects being studied (participants or respondents in the studies, actors, levels of government) and the dominant theories/paradigms, our results did not produce any relevant or standardized patterns. However, some conclusions can be drawn:

The NPM agenda was a common approach and independent of the collection methods.

Institutional theory was usually combined with the NPM agenda.

Politicians, international organizations, and ministries of finance were the subjects of study mainly in qualitative research (based on interviews and case studies) and accounting and auditing professionals were mainly the subjects of research based on questionnaires.

Themes addressed

The themes addressed in the articles focused on understanding how the various countries have reformed their public accounting and financial management processes, particularly whether or not to adopt AAPS and the determinants of success or failure. summarize the main results by different regions.

Table 7. Summary of the themes addressed in Africa's emerging economies.

Table 8. Summary of the themes addressed in emerging economies in South America.

Table 9. Summary of the themes addressed in Asia's emerging economies.

Discussion of results

As with other studies (for example Polzer et al., Citation2021 and Van Helden et al., Citation2021), we found that publications on AAPS have increased over the past five years and we predict this will continue. Most studies focus on Asian contexts (as also concluded by Van Helden & Uddin, Citation2016), as might be expected given the large number of expanding economies in Asia. Recently, there has been more interest in the African and South American economies, so we expect more research on these economies in the future.

Articles were predominantly published in journals focusing on public financial management (such as Public Money & Management and Financial Accountability & Management), while accounting and finance (as well as business management journals) published comparatively fewer articles on the topic. As mentioned earlier, two journals with a high impact factor in accounting—Abacus and Accounting, Organizations & Society—did not publish any articles on AAPS. This trend has been noted in most studies on public accounting topics (Schmidthuber et al., Citation2020; Van Helden & Uddin, Citation2016) showing that these journals are focusing on the private sector.

The questionnaire method was the most common data collection method, followed by combinations of mixed methods. An interesting finding was a preference for quantitative methods (mainly using questionnaires) when studying professionals and chiefs of accounting, auditing and finance. More qualitative methods (interviews and case studies) were used for politicians and members of international organizations. However, as Polzer et al. (Citation2021) concluded, experimental and longitudinal methods were not found in any article, which shows the dominance of a exploratory research in this area, with little research of a more critical (Van Helden et al., Citation2021) and experimental nature or longitudinal studies.

There were similarities in the results of the studies that used questionnaires—namely a positive impact of the transition to accrual accounting on improving the transparency and efficiency of public sector operations and accountability for the use of public funds. These studies often suggested that pressures from investors, professional accountants and politicians were having a significant impact on the effectiveness of applying AAPS.

Within the scope of the supporting theories and paradigms, the use of institutional theory has been reinforced in recent studies, due to the influence of external pressures on the decisions to reform accounting systems, complementing the impact of the NPM paradigm inspired by the economic theory. This study reinforces the role of isomorphism in the decisions to move forward with the adoption of AAPS and the pressure to increase the levels of efficiency and transparency. Two theories (the NPM agenda and institutional theory) stand out from the rest (71%) in research on public accounting changes in emerging country governments, confirming the usefulness of using more than one theoretical approach in a complementary way (see, for example, Gomes et al., Citation2015; Van Helden et al., Citation2021). We believe that the predominance of the NPM agenda is associated with its theoretical assumptions, namely the goal to bring public sector management closer to private sector practices using accrual-based accounting (Lapsley, Citation2009). These theoretical assumptions are inspired by the economic and positive theories associated with the leading reforms in public sector accounting since 1990s (Christiaens et al., Citation2015). Although public choice theory is sometimes applied to understand the context of public sector reforms, we didn’t find evidence of this in terms of AAPS being adopted in emerging economies. In addition, because NPM has economic and social justifications, some of these findings can be associated with positive accounting theory. Positive accounting theory is concerned with predictions and accounting choices taken by different stakeholders and assumes that the economic consequences of accounting choices explain the motivation behind the choice (Watts & Zimmerman, Citation1990). So, this should be an appropriate theory to explain the accounting choices under the NPM reforms and the transition to business-like tools in public entities (Ariely, Citation2011). Our aim in the theoretical dimension was therefore to bring connections between positive accounting theory and the NPM agenda.

This article has also highlighted the main drivers of AAPS adoption and implementation in the context of emerging economies. Several scholars consider that, in the light of institutional perspectives, legitimacy-seeking behaviours and the presence of coercive, mimetic and normative forces have influenced decisions to adopt accounting changes. They also believe that government accounting reforms have been promoted with the adoption of new principles of public financial management, such as NPM. These reforms started with the introduction of AAPS, using financial information for decision-making and progressed to the adoption of international standards and comparability. Governments have often adopted accrual accounting following financial and political crises. Consequently, the attempt to implement the NPM agenda, specifically the financial management aspects such as market-oriented systems and performance management, seems to be high on the agenda both in public financial management research and in daily governmental administrative practices. On the other hand, the introduction of accrual accounting in emerging economies still faces such obstacles as too few professionals with the necessary skills and qualifications and inadequate information systems.

Despite the costs associated with implementing public sector accounting reforms in emerging economies, when implemented, AAPS has been shown to bring such benefits as international financial comparability, decision support, transparency and accountability and reduced corruption (Ferry et al., Citation2018; Harun et al., Citation2013; Lewis & Hendrawan, Citation2020; Muraina & Dandago, Citation2020). As corruption is a major problem in many emerging economies, there is pressure on governments and policy-makers to continuously adopt anti-corruption best practices (Tawiah, Citation2021), for example international accounting standards (Gómez-Villegas et al., Citation2020; Lewis & Hendrawan, Citation2020; Mbelwa et al., Citation2019; McLeod & Harun, Citation2014). Moreover, the evidence we have presented in this article on the emerging economies of Africa, America and Asia, shows that African countries require more socio-political and cultural reforms to combat corruption, which is the main obstacle to the economic development in that region (Bakre et al., Citation2017), while in South American countries reforms are aimed at achieving legitimacy in the sense of increasing transparency, accountability and support for decision-making in the public sector (Gómez-Villegas et al., Citation2020). Unfortunately, in the Asian context, recent case studies have found that reforms have no causal effect on corruption (Lewis & Hendrawan, Citation2020)). This is not to say that the adoption of accounting reforms cannot necessarily help in reducing corruption in other contexts, such as the African region as mentioned earlier (Lewis & Hendrawan, Citation2020). In the same vein, Mir et al. (Citation2019) also found that, globally, accrual accounting-based reporting has not been very helpful in preventing corruption. On the other hand, the recent reform objectives of Asian countries and America are in line with the study by Ismaili et al. (Citation2021) on the importance and challenges of reform and transition to international public sector accounting and its implementation in the public sector in Kosovo, an emerging economy in Europe. Ismaili et al. (Citation2021) showed that the transition to accrual accounting contributed, significantly, to better decision-making and the efficient use of public funds. The results underline its importance in improving accountability, transparency and financial management and increasing public confidence in Kosovo’s macro-fiscal information and sustainability position.

In addition, although they were not included in our bibliometric analysis, it is important to look at studies and official reports that address this issue in the context of OECD countries, such as the study conducted jointly by IFAC and the OECD (OECD, Citation2017). This study concluded that, in OECD countries, the adoption of accrual accounting aimed to facilitate broader public management reform initiatives. The main motivation for reform was to obtain a fair view of public finances, assess the full costs of government operations, introduce or improve a performance culture and modernize public management. In contrast to emerging countries, some OECD countries noted that IT systems were upgraded as part of the normal replacement cycle, which therefore did not generate significant additional operating costs. Similarly to what was found in emerging economies, this study also concluded on the importance of providing training and support to units in implementing accrual accounting.

Conclusions

This article presents a bibliometric analysis of the transition to AAPS of emerging economies. The characteristics (state of research on accrual accounting, citations and publication vehicles), the geography of research, the theory and methods used were collected from a sample of 61 articles published in the WoS and Scopus databases up to February 2022. The results show a growing academic interest in this topic in the past five years and we believe it will continue to be a huge topic in the short term. A wide variety of theories and methods were used. There were also differences in publication vehicles and their geography, as well in terms of as the benefits, challenges and drivers of AAPS adoption and implementation. Questionnaires were the preferred method for collecting data from managers and accounting and auditing professionals. On the other hand, case studies and interviews were generally used to study the perspective of politicians and international organizations. The NPM agenda and institutional theory dominated the theoretical background and these theoretical perspectives were sometimes used in a complementary way. Emerging economy countries in particular are seeking to reform their government sector, which requires the adoption of good public governance practices, such as transparency, accountability and better decision-making—all of which can be achieved through a rigorous accrual-based accounting system.

Moreover, our research evidenced a significant concern with the high costs associated with the implementation of new accounting regimes which can be problematic for countries where poverty is a reality. We found that the capacity of public sector accountants, official managers and politicians to use the information generated by a new accounting system is a more important practical issue than the mere legal and mandatory requirement to use the new system. Institutional constraints often undermined changes in the accounting practices, for example the absence of accrual measures in fiscal strategies and the predominant use of cash-based budgeting in decision-making.

The implementation of AAPS in emerging economies has been driven by several factors, including local financial scandals, advocacy by civil society and the ambitions and ideology of key actors (Ahn et al., Citation2014). Coercive pressures from investors and auditors, together with normative pressures arising from employee training, are also important (Mbelwa et al., Citation2019) in emerging economies. The implementation of accrual accounting is hampered by a lack of competent accounting staff in emerging economies, coupled with the existence of non-aligned IT systems, but also due to the prevailing values of patronage in those economies.

Cultural factors are positively related to the implementation of accrual accounting in the context of emerging economies. The educational level of the citizens of a municipality positively affects the level of compliance of the municipality, as well as when penalties are not imposed on municipalities that do not comply with accrual accounting rules. In addition, three institutional pressures (coercive, mimetic and normative) clearly influence the speed of adoption of accrual accounting.

Limitations

This study suffers from some limitations, starting with the lack of clarification of the concept of emerging economies, as well as the ambiguity of the criteria defined by the World Bank and the IMF, which may have brought about some limitations in the methodological process of selecting the articles used in this research. On the other hand, the methodological configuration was not exhaustive and there may be works that were not selected for the sample, such as conference proceedings, official reports, book chapters, editorial material, debates or research notes and materials in languages other than English. However, we believe that the most relevant articles with the highest impact factor were included in the analysis, which makes it robust and rigorous in scientific terms.

Contributions

This study not only contributes to expanding the literature on AAPS adoption and implementation in the context of emerging economies, but also provides guidance for future research on this topic. Research on AAPS needs to continue to grow in the future to:

Increase the research in Africa and South America, which have rarely been studied. The literature points to serious difficulties in the development of economies in these contexts, largely due to the political culture in place and the high level of financial corruption, accompanied by low levels of transparency and accountability.

More research with complementary theoretical approaches—combining different theories that fit the institutional and legal context of institutions with a strong dependence on external funders with organizational cultures marked by technical difficulties, lack of leadership and political support and high resistance to change.

Conducting studies with innovative methods, with an emphasis on experimental and longitudinal methods that promote critical-interpretative research (Van Helden et al., Citation2021). Jeacle's suggestion (Citation2021) to start applying ‘netnography’ methodology seems to be appropriate for future studies because it promotes the observation and direct involvement in research of agents and stakeholders involved in reforms, either through discussion forums, focus groups or real-time conservation, taking advantage of new digital platforms.

Finally, comparative studies between emerging and non-emerging countries are to be encouraged so that they can contribute to the definition of a framework for analysing the different political-administrative, social and environmental characteristics that influence the adoption of new public accounting practices with a view to the sustainable development of these economies.

We hope that the present article will leverage other comparative studies that seek to highlight the differences between developed and emerging economies in the adoption and implementation of the AAPS.

Our study provides new insights to help policy-makers, professional bodies and standard setters in developing countries design and implement accrual-based public sector accounting systems. Looking at the barriers and difficulties experienced by other jurisdictions in similar contexts can provide important lessons for the successful reform of public sector accounting systems in developing countries.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Adhikari, P., & Gårseth-Nesbakk, L. (2016). Implementing public sector accruals in OECD member states. Accounting Forum, 40(2), 125–142. https://doi.org/10.1016/j.accfor.2016.02.001

- Adhikari, P., & Jayasinghe, K. (2017). ‘Agents-in-focus’ and ‘agents-in-context’: The strong structuration analysis of central government accounting practices and reforms in Nepal. Accounting Forum, 41(2), 96–115. https://doi.org/10.1016/j.accfor.2017.01.001

- Adhikari, P., Kuruppu, C., & Matilal, S. (2013). Dissemination and institutionalization of public sector accounting reforms in less developed countries. Accounting Forum, 37(3), 213–230. https://doi.org/10.1016/j.accfor.2013.01.001

- Adhikari, P., Kuruppu, C., Ouda, H., Grossi, G., & Ambalangodage, D. (2019). Unintended consequences in implementing public sector accounting reforms in emerging economies: evidence from Egypt, Nepal and Sri Lanka. International Review of Administrative Sciences, 87(4), 870–887. https://doi.org/10.1177/0020852319864156

- Ahn, P. D., Jacobs, K., Lim, D. W., & Moon, K. (2014). Beyond self-evident. Financial Accountability & Management, 30(1), 25–48. https://doi.org/10.1111/faam.12026

- Alghizzawi, M. A., & Masruki, R. (2020). Government accountants’ readiness for accrual accounting adoption in Jordan. Asia-Pacific Management Accounting Journal, 15(2), 25–45. https://doi.org/10.24191/apmaj.v15i2-02

- Aquino, A. C. B., Lino, A. F., Cardoso, R. L., & Grossi, G. (2020). Legitimating the standard-setter of public sector accounting reforms. Public Money & Management, 40(7), 499–508. https://doi.org/10.1080/09540962.2020.1769381

- Ariely, G. (2011). Why people (dis)like the public service: citizen perception of the public service and the NPM doctrine. Politics and Policy, 39(6), 997–1019. https://doi.org/10.1111/j.1747-1346.2011.00329.x

- Aswar, K., Ermawati, & Julianto, W. (2021). Implementation of accrual accounting by the Indonesian central government. Public and Municipal Finance, 10(1), 151–163. https://doi.org/10.21511/pmf.10(1).2021.12

- Azevedo, R. R., de Aquino, A. C. B., Neves, F. R., & da Silva, C. M. (2020). Deadlines and software. Public Money & Management, 40(7), 509–518. https://doi.org/10.1080/09540962.2020.1766203

- Azevedo, R. R., Lino, A. F., de Aquino, A. C. B., & Machado-Martins, T. C. P. (2020). Financial management information systems and accounting policies retention in Brazil. International Journal of Public Sector Management, 33(2–3), 207–227. https://doi.org/10.1108/IJPSM-01-2019-0027

- Bakre, O., Lauwo, S. G., & McCartney, S. (2017). Western accounting reforms and accountability in wealth redistribution in patronage-based Nigerian society. Accounting, Auditing and Accountability Journal, 30(6), 1288–1308. https://doi.org/10.1108/AAAJ-03-2016-2477

- Bakre, O., McCartney, S., & Fayemi, S. O. (2021). Accounting as a technology of neoliberalism. Critical Perspectives on Accounting, In press, 102282. https://doi.org/10.1016/j.cpa.2020.102282.

- Bergmann, A., Fuchs, S., & Schuler, C. (2019). A theoretical basis for public sector accrual accounting research. Public Money & Management, 39(8), 560–570. https://doi.org/10.1080/09540962.2019.1654319

- Brito, J. R., & Jorge, S. (2021). The institutionalization of a new accrual-based public sector accounting system. International Journal of Public Administration, 44(5), 372–389.

- Brusca, I., Gómez-villegas, M., & Montesinos, V. (2016). Public financial management reforms. Public Administration and Development, 36(1), 51–64. https://doi.org/10.1002/pad.1747

- Casprini, E., Dabic, M., Kotlar, J., & Pucci, T. (2020). A bibliometric analysis of family firm internationalization research. International Business Review, 29(5), 101715. https://doi.org/10.1016/j.ibusrev.2020.101715

- Castañeda-Rodriguez, V. (2022). Is IPSAS implementation related to fiscal transparency and accountability? BAR—Brazilian Administration Review, 19(1), 1–21.

- Chan, J. L. (2016). Government accounting with Chinese characteristics and challenges. Public Money & Management, 36(3), 201–208. https://doi.org/10.1080/09540962.2016.1133975

- Christiaens, J., Vanhee, C., Manes-Rossi, F., Aversano, N., & Van Cauwenberge, P. (2015). The effect of IPSAS on reforming governmental financial reporting: An international comparison. International Review of Administrative Sciences, 81(1), 158–177. doi: 10.1177/0020852314546580

- Fahmid, I. M., Harun, H., Graham, P., Carter, D., Suhab, S., An, Y., Zheng, X., & Fahmid, M. M. (2020). New development: IPSAS adoption, from G20 countries to village governments in developing countries. Public Money & Management, 40(2), 160–163. https://doi.org/10.1080/09540962.2019.1617540

- Ferry, L., Zakaria, Z., Zakaria, Z., & Slack, R. (2018). Framing public governance in Malaysia. Accounting Forum, 42(2), 170–183. https://doi.org/10.1016/j.accfor.2017.07.002

- Gomes, P. S., Fernandes, M. J., & Carvalho, J. B. D. C. (2015). The international harmonization process of public sector accounting in Portugal. International Journal of Public Administration, 38(4), 268–281. https://doi.org/10.1080/01900692.2015.1001237

- Gómez-Villegas, M., Brusca, I., & Bergmann, A. (2020). IPSAS in Latin America. Public Money & Management, 40(7), 489–498. https://doi.org/10.1080/09540962.2020.1769374

- Haija, A. A. A., Alqudah, A. M., Aryan, L. A., & Azzam, M. J. (2021). Key success factors in implementing international public sector accounting standards. Accounting, 7(1), 239–248. https://doi.org/10.5267/j.ac.2020.9.012

- Harun, H., An, Y., & Kahar, A. (2013). Implementation and challenges of introducing NPM and accrual accounting in Indonesian local government. Public Money & Management, 33(5), 383–388. https://doi.org/10.1080/09540962.2013.817131

- Harun, H., Van Peursem, K., & Eggleton, I. (2012). Institutionalization of accrual accounting in the Indonesian public sector. Journal of Accounting and Organizational Change, 8(3), 257–285. https://doi.org/10.1108/18325911211258308

- Hayat, A., Akhmad, B. A., Budiman, A., & Rajiani, I. (2020). Integrating people and technology in accrual accounting management to support quality financial reporting. Polish Journal of Management Studies, 22(2), 158–172. https://doi.org/10.17512/pjms.2020.22.2.11

- Hochrein, S., & Glock, C. H. (2012). Systematic literature reviews in purchasing and supply management research. International Journal of Integrated Supply Management, 7(4), 215–245. https://doi.org/10.1504/IJISM.2012.052773

- Ismail, S. (2022). Perception of the Malaysian federal government accountants of the usefulness of financial information under an accrual accounting system. Meditari Accountancy Research,

- Ismail, S., Siraj, S. A., & Baharim, S. (2018). Implementation of accrual accounting by Malaysian federal government. Journal of Accounting and Organizational Change, 14(2), 234–247. https://doi.org/10.1108/JAOC-03-2017-0020

- Ismaili, A., Ismajli, H., & Vokshi, N. B. (2021). The importance and challenges of the implementation of IPSAS accrual basis to the public sector. Accounting, 7(5), 1109–1118.

- Jayasinghe, K., Adhikari, P., Soobaroyen, T., Wynne, A., Malagila, J., & Abdurafiu, N. (2020). Government accounting reforms in Sub-Saharan African countries and the selective ignorance of the epistemic community: a competing logics perspective. Critical Perspectives on Accounting, 78, 102246. https://doi.org/10.1016/j.cpa.2020.102246

- Jeacle, I. (2021). Navigating netnography. Financial Accountability & Management, 37(1), 88–101. https://doi.org/10.1111/faam.12237

- Krishnan, S. R. (2021). Decision-making processes of public sector accounting reforms in India—institutional perspectives. Financial Accountability & Management, November, 2018, 1–28. https://doi.org/10.1111/faam.12294

- Kroll, A. (2015). Drivers of performance information use. Public Performance and Management Review, 38(3), 459–486. https://doi.org/10.1080/15309576.2015.1006469

- Lapsley, I. (2009). New Public Management. Abacus, 45(1), 1–21. DOI: 10.1111/j.1467-6281.2009.00275.x

- Lapsley, I., Mussari, R., & Paulsson, G. (2009). On the adoption of accrual accounting in the public sector. European Accounting Review, 18(4), 719–723. https://doi.org/10.1080/09638180903334960

- Lassou, P. J. C. (2017). State of government accounting in Ghana and Benin. Journal of Accounting in Emerging Economies, 7(4), 486–506. https://doi.org/10.1108/JAEE-11-2016-0101

- Lewis, B. D., & Hendrawan, A. (2020). The impact of public sector accounting reform on corruption: Causal evidence from subnational Indonesia. Public Administration and Development, 40(5), 245–254. https://doi.org/10.1002/pad.1896

- Lokuwaduge, C. S., & De Silva, K. (2020). Determinants of public sector accounting reforms. International Journal of Public Sector Management, 33(2–3), 191–205. https://doi.org/10.1108/IJPSM-03-2019-0085

- Luder, K. (1992). A contingency model of governmental accounting innovations in the political administrative environment. Research in Governmental and Nonprofit Accounting, 7, 99–127.

- Matekele, C. K., & Komba, G. V. (2020). Factors influencing implementation of accrual based international public sector accounting standards in Tanzanian local government authorities. Asian Journal of Economics, Business and Accounting, 13(3), 1–25. https://doi.org/10.9734/ajeba/2019/v13i330173

- Mbelwa, L. H., Adhikari, P., & Shahadat, K. (2019). Investigation of the institutional and decision-usefulness factors in the implementation of accrual accounting reforms in the public sector of Tanzania. Journal of Accounting in Emerging Economies, 9(3), 335–365. https://doi.org/10.1108/JAEE-01-2018-0005

- McLeod, R. H., & Harun, H. (2014). Public sector accounting reform at local government level in Indonesia. Financial Accountability & Management, 30(2), 238–258. https://doi.org/10.1111/faam.12035

- Meijer, A., & Bolívar, M. P. R. (2016). Governing the smart city. International Review of Administrative Sciences, 82(2), 392–408. https://doi.org/10.1177/0020852314564308

- Mir, M., Harun, H., & Sutiyono, W. (2019). Evaluating the implementation of a mandatory dual reporting system: the case of Indonesian government. Australian Accounting Review, 29(1), 80–94. https://doi.org/10.1111/auar.12232

- Muraina, S. A., & Dandago, K. I. (2020). Effects of implementation of international public sector accounting standards on Nigeria’s financial reporting quality. International Journal of Public Sector Management, 33(2–3), 323–338. https://doi.org/10.1108/IJPSM-12-2018-0277

- Najaf, K., Atayah, O., & Devi, S. (2021). Ten years of Journal of Accounting in Emerging Economies: A review and bibliometric analysis. Journal of Accounting in Emerging Economies, 12(4), 663–694. https://doi.org/10.1108/JAEE-03-2021-0089

- Nakmahachalasint, O., & Narktabtee, K. (2019). Implementation of accrual accounting in Thailand’s central government. Public Money & Management, 39(2), 139–147. https://doi.org/10.1080/09540962.2018.1478516

- Nyamori, R. O., Abdul-Rahaman, A. S., & Samkin, G. (2017). Accounting, auditing and accountability research in Africa. Accounting, Auditing and Accountability Journal, 30(6), 1206–1229. https://doi.org/10.1108/AAAJ-05-2017-2949

- Ocampo-Salazar, C. A. (2020). New development: Governmental accounting reforms in Latin America. Public Money & Management, 40(7), 527–530. https://doi.org/10.1080/09540962.2020.1766196

- OECD. (2017). Accrual practices and reform experiences in OECD countries. In Accrual Practices and Reform Experiences in OECD Countries, https://doi.org/10.1787/9789264270572-en

- Oulasvirta, L. (2014). The reluctance of a developed country to choose international public sector accounting standards of the IFAC. Critical Perspectives on Accounting, 25(3), 272–285.

- Polzer, T., Adhikari, P., Nguyen, C. P., & Gårseth-Nesbakk, L. (2021). Adoption of the international public sector accounting standards in emerging economies and low-income countries. Journal of Public Budgeting, Accounting and Financial Management, https://doi.org/10.1108/JPBAFM-01-2021-0016

- Prabowo, T., Leung, P., & Guthrie, J. (2018). Reforms in public sector accounting and budgeting in Indonesia (2003-2015). Journal of Public Budgeting, Accounting and Financial Management, 30(1), 2–21. https://doi.org/10.1108/JPBAFM-03-2018-002

- Primasari, D., Gaol, M. B. L., Susiana, & Fuad (2018). The implementation effect of accrual based accounting system to organizational performance with two moderating variables (an empirical study in Indonesia). Journal of Business and Retail Management Research, 12(4), 158–166. https://doi.org/10.24052/jbrmr/v12is04/art-16

- Rajib, S. U., Adhikari, P., Hoque, M., & Akter, M. (2019). Institutionalisation of the cash basis international public sector accounting standard in the central government of Bangladesh. Journal of Accounting in Emerging Economies, 9(1), 28–50. https://doi.org/10.1108/JAEE-10-2017-0096

- Rozaidy, M., & Siti-Nabiha, A. K. (2022). Reconstructing identity and logic through the implementation of accrual accounting in Malaysia. In Journal of Management and Governance (Issue 0123456789). Springer US. https://doi.org/10.1007/s10997-021-09615-4.

- Santis, S., Grossi, G., & Bisogno, M. (2018). Public sector consolidated financial statements. Journal of Public Budgeting, Accounting and Financial Management, 30(2), 230–251. https://doi.org/10.1108/JPBAFM-02-2018-0017

- Santos-Ospina, A. C. (2020). New development: Budgetary accounting in Colombia—arguments for a much-needed reform. Public Money & Management, 40(7), 523–526. https://doi.org/10.1080/09540962.2020.1766793

- Schmidthuber, L., Hilgers, D., & Hofmann, S. (2020). International Public Sector Accounting Standards (IPSASs): A systematic literature review and future research agenda. Financial Accountability & Management, 38(1), 119–142. https://doi.org/10.1111/faam.12265

- Seuring, S., & Gold, S. (2012). Conducting content-analysis based literature reviews in supply chain management. Supply Chain Management, 17(5), 544–555. https://doi.org/10.1108/13598541211258609

- Soobaroyen, T., Tsamenyi, M., & Sapra, H. (2017). Accounting and governance in Africa—contributions and opportunities for further research. Journal of Accounting in Emerging Economies, 7(4), 422–427. https://doi.org/10.1108/JAEE-10-2017-0101

- Tallaki, M., & Bracci, E. (2019). NPM reforms and institutional characteristics in developing countries. Journal of Accounting in Emerging Economies, 9(1), 126–147. https://doi.org/10.1108/JAEE-01-2018-0010

- Tawiah, V. (2021). The impact of IPSAS adoption on corruption in developing countries. Financial Accountability & Management, 39(1), 103–124. https://doi.org/10.1111/faam.12288

- Thanh, P. N. T., Thanh, H. P., Thanh, T. N., & Thuy, T. V. T. (2020). Factors affecting accrual accounting reform and transparency of performance in the public sector in Vietnam. Problems and Perspectives in Management, 18(2), 180–193. https://doi.org/10.21511/ppm.18(2).2020.16

- Tranfield, D., Denyer, D., & Smart, P. (2003). Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. British Journal of Management, 14(3), 207–222. https://doi.org/10.1111/1467-8551.00375

- Upping, P., & Oliver, J. (2012). Thai public universities. Journal of Accounting and Organizational Change, 8(3), 403–430. https://doi.org/10.1108/18325911211258362

- Van Helden, J., Adhikari, P., & Kuruppu, C. (2021). Public sector accounting in emerging economies. Journal of Accounting in Emerging Economies, 11(5), 776–798. https://doi.org/10.1108/jaee-02-2020-0038

- Van Helden, J., & Uddin, S. (2016). Public sector management accounting in emerging economies. Critical Perspectives on Accounting, 41, 34–62. https://doi.org/10.1016/j.cpa.2016.01.001

- Voorberg, W. H., Bekkers, V. J. J. M., & Tummers, L. G. (2015). A systematic review of co-creation and co-production. Public Management Review, 17(9), 1333–1357. https://doi.org/10.1080/14719037.2014.930505

- Wang, Z., & Miraj, J. (2018). Adoption of international public sector accounting standards in public sector of developing economies. Research in World Economy, 9(2), 44–51. https://doi.org/10.5430/RWE.V9N2P44

- Watts, R. L., & Zimmerman, J. L. (1990). Positive Accounting Theory: A Ten Year Perspective. The Accounting Review, 65(1), 131–156.

- Wynne, A. (2004). Is the move to accrual based accounting a real priority for public sector accounting. ACCA. https://bambangkesit.files.wordpress.com/2011/02/accrual-based-accounting-bab-4.pdf

- Yuliati, R., Yuliansyah, Y., & Adelina, Y. E. (2019). The implementation of accrual basis accounting by Indonesia’s local governments. International Review of Public Administration, 24(2), 67–80. https://doi.org/10.1080/12294659.2019.1603954

- Zhang, E. (2020). Discourses on public sector accounting reforms in China. Accounting History, 26(2), 255–279. https://doi.org/10.1177/1032373220948627

- Zhu, J., & Liu, W. (2020). A tale of two databases. Scientometrics, 123(1), 321–335. https://doi.org/10.1007/s11192-020-03387-8