?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.IMPACT

This study shows that consolidated financial accounts (CFAs) do not only appear to be useful from a municipal financial accounting perspective. For serious adopters, who change their behaviour and adapt their strategy in line with the information provided, CFAs seem to be a powerful tool for monitoring and governance purposes.

ABSTRACT

The authors analyse the effect of deregulation in the case of the removed requirement for Swedish municipalities to prepare consolidated financial accounts (CFAs) in their interim reports. The findings show that deregulation led to a statistically significant, but not substantial, reduction in CFAs. Municipalities with many municipal corporations tended to continue preparing CFAs. CFAs therefore appear to be more than a compliance exercise, as they are being used for monitoring and co-ordination purposes.

Introduction

In many jurisdictions, governments are legally allowed to organize their service delivery in different forms, including through corporations (Voorn et al., Citation2017; Bernier et al., Citation2020) and through other types of bodies operating at arm’s length from the government (Van Genugten et al., Citation2020). As a result of this trend, central and local governments have started to prepare consolidated financial accounts (CFAs) to disclose financial information about the government group as a whole (Bergmann et al., Citation2016; Chow et al., Citation2019).

Following the emergence of CFAs in some public sector settings, a small body of literature has been established on this topic. As noted by Santis et al. (Citation2018) in their review of this literature, most articles published between 1980 and 2015 were either conceptual or normative in nature and focused primarily on discussing technical issues related to different consolidation approaches. Although the literature has developed and has become increasingly empirically oriented over time, the debate on technical issues, such as the approach to define the perimeter of consolidation (for example Bisogno et al., Citation2015; Grossi & Steccolini, Citation2015; Carini & Teodori, Citation2021; Oulasvirta, Citation2022), continues.

More recent research has begun to empirically examine the perceived benefits of preparing CFAs. After studying the central tier of governments in several countries, Chow et al. (Citation2019) concluded that, in many cases, there were difficulties in identifying any actual use or user of consolidated financial information. Instead, in their decision-making, politicians and managers seemed to favour alternative information sources, such as government statistics and budgets. In a similar vein, Stewart and Connolly’s (Citation2021) study, comparing pre-implementation benefits with post-implementation experiences with respect to the Whole of Government Accounts (WGA) in the UK central government, revealed a substantial gap between claimed and perceived benefits. Nevertheless, in a reflection on the first 10 years of the UK WGA, Stewart and Connolly (Citation2022, p. 462) noted that ‘evidence that WGA is starting to be used is emerging, albeit slowly’.

At the local level, experiences from preparing CFAs appear to be mixed. On the one hand, Carini et al. (Citation2019) surveyed the perceptions of financial officers in a sample of Italian municipalities and found evidence of active internal use of the information, soon after it became mandatory to prepare CFAs. On the other hand, a study by Gomes et al. (Citation2019) revealed that financial officers in Spain (where CFAs are prepared on a voluntary basis), and to some extent those in Portugal (where they are prepared on a mandatory basis), did not see any widespread use of CFAs. Instead of using accrual and consolidated accounting information in their decision-making processes, according to the financial officers, the Spanish and Portuguese municipal officials and politicians mainly relied on other sources of information such as budget reporting. This finding is similar to the situation that has been reported in several central governments, where other sources of financial information are available and are often favoured in decision-making processes (Chow et al., Citation2019). Santis et al. (Citation2019) found that before it was mandatory to prepare CFAs in Italian municipalities, the Italian financial councillors´ and officers´ choice to participate in a test period and to voluntarily prepare CFAs were driven by the desire to (i) understand the technical challenges of preparing CFAs (i.e. technical reasons) and (ii) improve transparency, and to better evaluate the efficiency and effectiveness of their resources (i.e. political reasons).

Although there are exceptions, on the whole, earlier research has raised concerns that making CFAs available is insufficient to achieve active use of the information. Previous public sector accounting research also shows that that financial officers sometimes struggle to comprehend the tangible benefits of the mandatory reporting requirements placed on them (Falkman & Tagesson, Citation2008; Pilcher & Dean, Citation2009). If the concerns of these financial officers are a valid indicator, a situation may occur in which governments spend time and money on financial reporting merely for compliance purposes. Indeed, findings that show little or no use of CFAs raise the question of whether the preparation of CFAs is just another compliance exercise for governments (Stewart & Connolly, Citation2022). One way to shed light on this issue is to study to what extent and at what pace consolidated reporting practices change in the wake of deregulation. The latest accounting reform in Sweden provides such an opportunity. The aim of our study was to explain why, and to what extent, Swedish municipalities continue to prepare CFAs in their interim report after the explicit requirement for CFAs was withdrawn by the national standard setting body. If municipalities continued to prepare consolidated CFAs on a voluntary basis, then municipalities see a value that extends beyond mere compliance. On the other hand, if there is a drastic decrease in preparation, municipalities clearly do not perceive a benefit from preparing CFAs.

This article is organized into six major sections. The next section describes the development of CFAs in the Swedish municipal sector. The third section introduces our hypotheses, and the fourth section describes the method used to test the proposed hypotheses. The fifth section presents the analysis, and the final section offers some conclusions.

Consolidated financial accounting in Swedish municipalities

According to the Municipal Act (2017: 725), Swedish municipalities are allowed to provide goods and public services through wholly or partially owned municipal corporations (we use the term ‘corporations’ to refer to corporations, associations, and foundations, although corporations are most common in Swedish municipalities). Since 1970, the number of municipally owned corporations has gradually increased (Bergh et al., Citation2021) and these organizations now control a significant share of the municipal groups’ revenues and assets (see , descriptive statistics). As the owner, a municipality is responsible for ensuring that municipal corporations only engage in ‘sound economic behaviour’, as defined by the Municipal Act.

Table 1. Descriptive statistics.

Swedish municipalities’ far-reaching freedom of organization is reflected in the requirements placed on financial reporting, as municipalities have been required to prepare CFAs in their annual reports since 1992 (Tagesson & Grossi, Citation2012). However, as early as in the 1980s, consolidated reporting was introduced on a voluntary basis in Swedish municipalities (Grossi & Tagesson, Citation2008). Here, it should also be mentioned that the national standard setting body—the Swedish Council for Municipal Accounting (SCMA)—has pursued a different route to CFAs than the International Public Sector Accounting Standards Board (IPSASB). While the IPSASB has favoured the decision-making approach and the concept of control to define the perimeter of consolidation (Bisogno et al., Citation2015; Grossi & Steccolini, Citation2015), the SCMA has emphasized accountability and economic materiality (Grossi & Tagesson, Citation2008). Based on the SCMA standards, Swedish municipalities should use proportional consolidation according to the purchase method, as the size and use of services are expected to be reflected in the equity interest of jointly owned corporations (Tagesson, Citation2009).

In 1998, when the Municipal Accounting Act (1997: 614) came into force, it became mandatory for municipalities to present an interim report that covered a period of at least half and no more than two thirds of the financial year, in addition to the annual report. Initially, it was not mandatory for municipalities to prepare CFAs in their interim report. In 2013, the national standard setting body issued Accounting Standard No. 22 on interim reporting. In this standard, the SCMA clarified that, as of 2014, the interim report should contain CFAs if:

(i) the municipal corporations’ revenues accounted for 30% or more of a municipality’s tax revenues and government grants; and/or (ii) the municipal corporations’ assets accounted for 30% or more of the municipal group’s total assets.

To summarize: during 1998–2013, it was voluntary for Swedish municipalities to prepare CFAs in the interim report; during 2014–2018, it was mandatory for municipalities exceeding any of the above-specified 30% thresholds; and, as of 2019 and onwards, it is again voluntary to prepare CFAs in the interim report, regardless of the size of the municipal corporations.

Hypotheses

Response to (de)regulation

Not all organizations adapt to institutional pressure for change. AsOliver (Citation1991) explains, organizations can respond to institutional pressure in a variety of ways, ranging from passive conformity, compromise and avoidance to defiance and proactive manipulation of the source of pressure. In particular, resistance to institutional pressure is expected to be salient if there are inconsistent norms and values within important professional groups (Carpenter & Feroz, Citation2001; Oulasvirta, Citation2014). In relation to financial reporting practice, far from all accounting standards become institutionalized—i.e. become legitimate and taken-for-granted practices (Meyer & Rowan, Citation1977; DiMaggio & Powell, Citation1983). Indeed, accounting scholars, such as Carmona and Trombetta (Citation2008) and Daske et al. (Citation2013), differentiate between ‘adopters’:

Label adopters adopt new standards only in name, without making material changes in their behaviour.

Serious adopters modify their financial reporting strategy after the adoption of a new standard.

Thus, both serious and label adopters react to institutional pressures, but label adopters’ formal accounting system is decoupled from actual organizational practice (Carruthers, Citation1995). Whether municipalities tend to be label or serious adopters of CFAs in the interim report is likely to influence their response to the deregulation that occurred in Sweden. If CFAs had not been institutionalized in the interim report in the first place (like many other accounting standards), municipalities would have been unlikely to prepare CFAs on a voluntary basis.

Since the accounting standard that made it mandatory to prepare CFAs in the interim report was only applied during a five-year period, CFAs may not have become a legitimate and taken-for-granted reporting practice that was seriously adopted in all municipalities. However, despite the relatively short time during which it was mandatory to prepare CFAs in the interim report, Sweden must be regarded as a mature reporting setting; thus, there should be many municipalities who are serious adopters of CFAs in their interim report. Swedish municipalities have prepared CFAs in the annual report since the late 1980s (Grossi & Tagesson, Citation2008); moreover, accrual-based budgeting and accounting have been around in Swedish municipalities since the mid 1980s (Donatella, Citation2020). As explained by Bergmann (Citation2012), over time, users tend to commit to relying on a new type of financial information, such as accrual-based information. The technical challenges confronted in less mature CFAs settings (Santis et al., Citation2019) and competition from other information sources (Chow et al., Citation2019; Gomes et al., Citation2019) should have faded during the decades that have passed since the implementation of major budget and accounting reforms in the Swedish municipal sector. As a result, CFAs may have become a legitimate and taken-for-granted reporting practice that is seriously adopted by many. Organizations tend to create routines that influence their work (Collin et al., Citation2009) and since serious adopters already have everything set up to produce the consolidated reports, the additional effort in continuing doing so is therefore marginal. If that is the case, deregulation may not necessarily spark a change process (Broadbent & Laughlin, Citation2005), suggesting that most municipalities will act in the same way as they did before the deregulation. Or, to put it differently, due to the strong force of institutional inertia (Aksom, Citation2022), municipalities continue to voluntarily prepare CFAs in their interim report.

Considering the mixed arguments presented above, we hypothesized that:

H1: After the deregulation (in 2019), there was likely to be a small but noticeable decrease in the probability that a municipality prepared CFAs in its interim report.

The composition of the municipal group

Kajüter et al. (Citation2021) argue that—from a theoretical point of view—higher reporting frequency should lead to better monitoring. Increasing the number of activities that are transferred to wholly or partially owned municipal corporations presumably puts more emphasis on the monitoring capacity of the accounting system (Bergmann et al., Citation2016). In turn, this increases the demands on administrative routines and highly qualified accountants to co-ordinate the complex service delivery arrangements and the more advanced accounting system that corporatization implies (Grossi & Reichard, Citation2008). Regardless of the mandatory or voluntary nature of CFAs, the need to consolidate for control purposes increases as more activities are transferred to municipal corporations. Moreover, it is relevant to note that, although it has been voluntary to prepare CFAs in the interim report from 2019 onwards, the Swedish standard setter requires municipalities to disclose both the municipality’s and the municipality group’s expected financial and operational development based on the municipality’s goals for achieving sound economic behaviour (SCMA Accounting Standard No. R17).

As explained earlier, Swedish municipalities can provide goods and public services through wholly or partially owned municipal corporations. The extent to which this occurs varies and, as evidenced by Tagesson and Grossi (Citation2012), the financial picture may therefore be very different—depending on whether one is focused on the whole group, or only the municipality. Municipalities with a relatively large number of municipal corporations, such that a relatively large proportion of the municipality group’s total revenues and assets are controlled by municipal corporations, should be more motivated to see the need to monitor and control the whole group. This monitoring and control may be exercised by preparing CFAs in the municipalities’ interim reports. In addition, municipalities that prefer to provide goods and public services through wholly or partially owned municipal corporations may be more exposed to coercive and normative pressure to disclose financial information for the whole group. We therefore hypothesize that:

H2: The probability that a municipality will prepare CFAs in its interim report will increase with the relative proportion of municipal corporations in the entire group.

Method

Data selection

Our hypotheses were tested using a sample of all Swedish municipalities except for Region Gotland, as the latter has more extensive areas of responsibility than the other municipalities. The sample consisted of 867 municipal-year observations distributed over 289 municipalities from 2018 to 2020. The research is based on manually collected data from the municipalities’ annual and interim reports and from professional auditors’ reports, and on publicly-available data from Statistics Sweden.

Operationalization

The dependent variable was a dummy variable, where municipalities were coded as 1 if they had CFAs in their interim report in year t, and as 0 otherwise. To test whether there was a decrease in the number of municipalities with CFAs in their interim report after 2018 (H1), dummies for the years 2019 and 2020 were used. We used three different variables to test how a municipality group’s proportion of municipal corporations affected the probability of the municipality having a CFA in its interim report: (1) number of consolidated municipal corporations; (2) proportion of turnover from municipal corporations; and (3) proportion of assets in municipal corporations. The variable consolidated corporations was measured by the number of municipal corporations included in the consolidated annual report in year t (data source: municipalities’ annual reports). We assumed that the number of consolidated entities in the year-end annual report would not differ from the number of consolidated entities in the interim report, as Swedish municipalities’ interim reports typically span from January to August. Size turnover was calculated by deducting the municipality’s operating revenues from the municipal group’s revenues, and then scaling the sum with tax revenues and government grants. Size assets was calculated by deducting the municipality’s assets from the municipal group’s assets, and then scaling the sum with the municipal group’s assets (data source: Statistics Sweden). Year t—1 was used for size turnover and size assets, as the previous year’s data was used by both auditors and municipalities when determining whether it was mandatory to prepare CFAs in the interim report during 2014–2018. In the regression analysis, logarithmized values were used for all three variables.

We used both political and financial control variables. Political competition is generally assumed to stimulate transparency (Rodríguez Bolívar et al., Citation2013). We used changes in government during the last three elections to measure political competition (data source: Statistics Sweden). The ability to form majorities may indicate a lower degree of political competition. Municipalities in which the governing party or parties controlled more than 50% of the seats in the municipal council were coded as 1, and those in which this was not the case were coded as 0 (data source: Statistics Sweden).

Political parties are driven by different ideologies. Right-wing parties can be argued to prefer the corporatization of municipal services, while left-wing parties tend to prefer services being in the hands of the government (Sundell & Lapuente, Citation2012). Therefore, we controlled for political majority based on the election results in 2018, and coded three dummies as follows: Social Democrats, the Left party, and the Green party were coded as left-wing parties, and the Moderates, Christian Democrats, Liberals, the Centre party, and Sweden Democrats were coded as right-wing parties. Municipalities ruled by a mixed majority were used as the reference variable.

Financial control variables included financial strength, as this is related to the risk and increased pressures from providers of dept capital. Long-term financial strength was measured by the municipal group’s equity ratio in year t, including all pension obligations (data source: Statistics Sweden). Another measure of financial strength, from a short-term perspective, is the municipality’s ability to maintain a healthy balance between revenue and expenses. We therefore controlled for the municipal group’s financial results per resident for year t (data source: Statistics Sweden).

We also controlled for the audit firm. Rather uniquely, Swedish municipalities are audited by politically-appointed auditors, assisted by professional auditors. Professional auditors are generally hired from the large auditing firms; however, some municipalities have internal audit offices with employed experts to assist the politically-appointed auditors (Collin et al., Citation2017). PwC, Deloitte, EY, an internal audit office, KPMG, and other audit firms were coded into six different dummy variables. PwC—the market-leading audit firm in the Swedish municipal sector (Donatella, Citation2022)—was used as the reference variable (data source: professional auditors’ reports).

Analyses

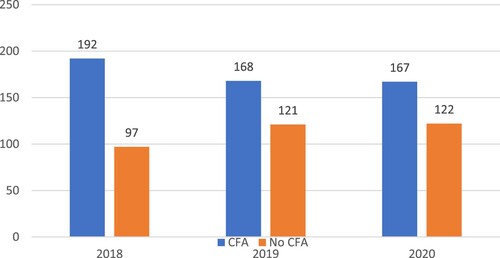

Descriptive statistics for all variables in our sample are presented in ; in information is presented for the dependent variable (CFA in the interim report) for each year of the period 2018–2020. For the whole period, in 60.2% of the municipality-year observations, CFAs were prepared in the interim reports. The statistics presented in show that, over time, there was a small decrease in the number of municipalities preparing CFAs, from 192 out of 289 in 2018 (when it was mandatory to prepare CFA for municipalities that exceeded any of the specified 30% thresholds in SCMA Accounting Standard No. 22), to 168 and 167 in 2019 and 2020, respectively. This corresponds to a decrease of almost 13 percentage points between 2018 and 2020. It should also be mentioned that, in 2018, 42 municipalities voluntarily prepared consolidated interim reports, whereas 53 municipalities were noncompliant with the then applicable legislation. Problems with lack of compliance are not a new phenomenon in the public sector but confirm what previous Swedish (Falkman & Tagesson, Citation2008; Donatella, Citation2020) and international studies have found (Christiaens & van Peteghem, Citation2007; Cohen & Kaimenakis, Citation2011). The descriptive statistics also show considerable variation in the number of consolidated municipal corporations and the proportion of turnover and assets from and in municipal corporations.

Figure 1. Number of municipalities preparing/not preparing CFAs in their interim report (N = 289).

Note: In 2018, municipalities that exceeded any of the specified 30% thresholds in SCMA Accounting Standard No. 22 were required to include CFAs in their interim reports. However, starting in 2019, the inclusion of CFAs in the interim reports became voluntary for all municipalities.

Correlation matrixes present the correlations between the variables in the models (). The correlation matrixes indicate a significant positive correlation between the dependent variable of CFAs in the interim reports and the independent variables of consolidated municipal corporations, proportion of turnover from municipal corporations, and proportion of assets in municipal corporations. The highest correlation is between consolidated corporations and size turnover (.727), indicating problems with multicollinearity, as the pair-wise correlation exceeds 0.7 (Pallant, Citation2013).

Table 2. Correlations and logistic regressions.

We analysed the full dataset by means of a panel data analysis. As the bivariate analysis indicates that consolidated corporations and size turnover measure the same aspects, they cannot be used as variables in the same model. We therefore ran two models (Models 1a and 1b). We also ran a subsample panel data analysis (Models 2a and 2b) to test the stability of the results. In this subsample, the 53 municipalities that were noncompliant in 2018 were dropped. The following logistic model was tested:

Models 1a/b and 2a/b indicate that the number of municipalities that prepared CFAs in the interim reports decreased in both 2019 and 2020 in comparison with 2018, as the odds ratios are below 1. However, as evidenced by the descriptive statistics, this change is not of great magnitude. It is also worth noting that the odds ratio for the first (2019) and second (2020) year after the deregulation were of similar magnitude, confirming that there were almost no additional decreases in CFA reporting in the interim report between 2019 and 2020. Overall, these observations support H1, which predicts a small but noticeable decrease in the probability that a municipality will prepare CFAs in its interim report after the deregulation.

Keeping the effect of year dummies and the political, financial and audit control variables constant, we found that the relative size of a municipality’s corporations increases the probability of municipalities preparing CFAs in their interim reports (as the odds ratios are above 1). The more consolidated corporations a municipality has the more likely it was to prepare CFAs in its interim report (Models 1a and 2a). Models 1b and 2b show that there was a positive significant relationship between the proportion of turnover from municipal corporations (size turnover) and the likelihood that that municipalities will prepare CFAs in their interim reports. All the models include the variable size assets and show that the likelihood that that municipalities will prepare CFAs in their interim reports increases with the proportion of assets in municipal corporations. Overall, these observations support H2, which predicts that the probability that a municipality will prepare CFAs in its interim report will increase with the relative proportion of municipal corporations in the entire group.

The results also indicate that municipalities with an internal audit office are more likely to prepare CFAs in their interim reports compared with those that use external audit firms (Models 1a, 1b and 2b). None of the political control variables were significant, which indicates that political competition and political majority did not influence the probability of municipalities preparing CFAs in their interim report.

Additional tests in which the years 2019 and 2020 were coded into one dummy for the deregulation periods showed the same results as Models 1 and 2. Moreover, additional analyses indicated that the municipalities that voluntarily prepared CFAs in their interim reports (those not exceeding any of the previously mentioned 30% thresholds), and those that were mandated by the previous regulation to prepare CFAs in their interim reports (those exceeding the previously mentioned 30% thresholds), were more likely to continue preparing CFAs, whereas those that were noncompliant with the previous legislation were more likely not to prepare CFAs.

Conclusions

The limitation of this study is that the data stems from a limited period of time; the inclusion of reporting years prior to 2018 could have captured possible earlier adaptation to the upcoming deregulation, as these regulatory changes were known several months before the reporting window for the 2018 interim report was closed.

However, by studying the deregulation that took place in the Swedish municipal sector in 2019, we provide a piece of empirical evidence in an area that has not been given a great deal of scholarly attention so far. There is a small but growing empirical literature on CFAs in the public sector (Santis et al., Citation2018). While there are individual studies that point to active and meaningful internal governmental use of the consolidated financial information that is prepared (Carini et al., Citation2019), many studies suggest that this is not the case (Chow et al., Citation2019; Gomes et al., Citation2019; Stewart & Connolly, Citation2021). Given this literature, there is reason for concern that CFAs may be prepared merely for compliance purposes—or, to put it differently, that the preparation of CFAs ‘continues to be legitimized through coercive pressure only’ (Stewart & Connolly, Citation2021, p. 580).

Our findings show that a deregulation that made CFAs no longer mandatory in practice in Sweden led to a statistically significant, but not substantial, reduction in CFAs within interim reports. Thus, the deregulation did not result in any dramatic change in practice regarding CFAs in the municipalities’ interim reports, which is in line with the assumptions of institutional inertia. However, when the requirement was withdrawn by the national standard setting body, some municipalities immediately reverted to their old routines of not preparing CFAs in the interim report.

Another finding is that municipalities with many municipal companies that account for a large part of the municipal group’s turnover, as well as municipalities with a large part of the municipal group’s capital being controlled by companies within the group, continue to prepare CFAs in their interim report. In line with our theoretical assumptions, this finding suggests that CFAs are not only prepared in response to coercive pressure from mandatory reporting requirements but are also prepared in order to monitor and co-ordinate municipal activities. Thus, municipalities that need consolidated financial accounting information for the governance of their municipal group continued to prepare and disclose CFAs in their interim report, even after it became voluntary do to so. The strongest evidence for this conclusion is that the interim report, in the context of Swedish municipalities, is primarily regarded as information for internal use. Overall, our findings suggest that CFAs seem to be more than just another compliance exercise for Swedish municipalities.

Financial reporting practices in the public sector context are characterized by institutional inertia, which is not only related to the adoption of new or amended accounting standards but is also salient in a situation of deregulation. These insights underline the challenges associated with harmonizing financial reporting information in the public sector context and demonstrate the need to legitimize a reform, both from an external and an internal perspective, to overcome institutional inertia and to support serious adoption of legal requirements and related GAAPs.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Pierre Donatella

Pierre Donatella is Senior Lecturer in the School of Public Administration at University of Gothenburg, Sweden. He has authored and co-authored several journal articles on financial reporting and auditing in local governments, often focusing on describing and explaining variations in accounting practices. Additionally, he has written textbooks on financial analysis and financial reporting in local governments.

Johanna Sylvander

Johanna Sylvander is Senior lecturer in Business Administration specializing in accounting and auditing at Linkoping University, Sweden. Her research is mainly on accounting and auditing in both the public and private sector.

Torbjörn Tagesson

Torbjörn Tagesson is Professor of Accounting at Linkoping University, Sweden and the Executive Director of the Swedish Council for Municipal Accounting. He is the author of several books and articles on accounting, auditing, and public administration.

References

- Aksom, H. (2022). Institutional inertia and practice variation. Journal of Organizational Change Management, 35(3), 463–487. https://doi.org/10.1108/JOCM-07-2021-0205

- Bergh, A., Erlingsson, GÓ, & Wittberg, E. (2021). What happens when municipalities run corporations? Empirical evidence from 290 Swedish municipalities. Local Government Studies, 48(4), 704–727. https://doi.org/10.1080/03003930.2021.1944857

- Bergmann, A. (2012). The influence of the nature of government accounting and reporting in decision-making: Evidence from Switzerland. Public Money & Management, 32(1), 15–20. https://doi.org/10.1080/09540962.2012.643050

- Bergmann, A., Grossi, G., Rauskala, I., & Fuchs, S. (2016). Consolidation in the public sector: Methods and approaches in Organisation for Economic Co-operation and Development countries. International Review of Administrative Sciences, 82(4), 763–783. https://doi.org/10.1177/00208523155767

- Bernier, L., Florio, M., & Bance, P. (2020). Introduction. In L. Bernier, M. Florio, & P. Bance (Eds.), The Routledge handbook of state-owned enterprises (pp. 1–22). Routledge.

- Bisogno, M., Santis, S., & Tommasetti, A. (2015). Public-sector consolidated financial statements: An analysis of the comment letters on IPSASB’s exposure draft no. 49. International Journal of Public Administration, 38(4), 311–324. https://doi.org/10.1080/01900692.2015.999605

- Broadbent, J., & Laughlin, R. (2005). Organisational and accounting change: Theoretical and empirical reflections and thoughts on a future research agenda. Journal of Accounting & Organizational Change, 1(1), 7–25. https://doi.org/10.1108/EUM0000000007302

- Carini, C., Giacomini, D., & Teodori, C. (2019). Accounting reform in Italy and perceptions on the local government consolidated report. International Journal of Public Administration, 42(3), 195–204. https://doi.org/10.1080/01900692.2017.1423500

- Carini, C., & Teodori, C. (2021). Debate: Public sector consolidated financial statements—The hybrid approach. Public Money & Management, 41(6), 432–433. https://doi.org/10.1080/09540962.2021.1883286

- Carmona, S., & Trombetta, M. (2008). On the global acceptance of IAS/IFRS accounting standards: The logic and implications of the principles-based system. Journal of Accounting and Public Policy, 27(6), 455–461. https://doi.org/10.1016/j.jaccpubpol.2008.09.003

- Carpenter, V. L., & Feroz, E. H. (2001). Institutional theory and accounting rule choice: An analysis of four US state governments’ decisions to adopt generally accepted accounting principles. Accounting, Organizations and Society, 26(7–8), 565–596. https://doi.org/10.1016/S0361-3682(00)00038-6

- Carruthers, B. G. (1995). Accounting, ambiguity and the new institutionalism. Accounting, Organizations and Society, 20(4), 313–328. https://doi.org/10.1016/0361-3682(95)96795-6

- Chow, D. S., Pollanen, R., Baskerville, R., Aggestam-Pontoppidan, C., & Day, R. (2019). Usefulness of consolidated government accounts: A comparative study. Public Money & Management, 39(3), 175–185. https://doi.org/10.1080/09540962.2018.1535034

- Christiaens, J., & van Peteghem, V. (2007). Governmental accounting reform: Evolution of the implementation in Flemish municipalities. Financial Accountability & Management, 23(4), 375–399. https://doi.org/10.1111/j.1468-0408.2007.00434.x

- Cohen, S., & Kaimenakis, N. (2011). Assessing quality of financial reporting through audit reports: The case of Greek municipalities. Global Business and Economics Review 13(3–4), 187–203. https://doi.org/10.1504/GBER.2011.041848

- Collin, S.-O., Haraldsson, M., Tagesson, T., & Blank, V. (2017). Explaining municipal audit cost in Sweden: Reconsidering the political environment, the municipal organization and the audit market. Financial Accountability & Management, 33(4), 391–405. https://doi.org/10.1111/faam.12130

- Collin, S.-O., Tagesson, T., Andersson, A., Cato, J., & Hansson, K. (2009). Explaining the choice of accounting standards in municipal corporations. Critical Perspectives on Accounting, 20(2), 141–174. https://doi.org/10.1016/j.cpa.2008.09.003

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2013). Adopting a label: Heterogeneity in the economic consequences around IAS/IFRS adoptions. Journal of Accounting Research, 51(3), 495–547. https://doi.org/10.1111/1475-679X.12005

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- Donatella, P. (2020). Determinants of mandatory disclosure compliance in Swedish municipalities. Journal of Public Budgeting, Accounting & Financial Management, 32(2), 247–265. https://doi.org/10.1108/JPBAFM-03-2019-0048

- Donatella, P. (2022). Further evidence on the relationship between audit industry specialisation and public sector audit quality. Financial Accountability & Management, 38(4), 512–529. https://doi.org/10.1111/faam.12278

- Falkman, P., & Tagesson, T. (2008). Accrual accounting does not necessarily mean accrual accounting: Factors that counteract compliance with accounting standards in Swedish municipal accounting. Scandinavian Journal of Management, 24(3), 271–283. https://doi.org/10.1016/j.scaman.2008.02.004

- Gomes, P., Brusca, I., & Fernandes, M. J. (2019). Implementing the International Public Sector Accounting Standards for consolidated financial statements: Facilitators, benefits and challenges. Public Money & Management, 39(8), 544–552. https://doi.org/10.1080/09540962.2019.1654318

- Grossi, G., & Reichard, C. (2008). Municipal corporatization in Germany and Italy. Public Management Review, 10(5), 597–617. https://doi.org/10.1080/14719030802264275

- Grossi, G., & Steccolini, I. (2015). Pursuing private or public accountability in the public sector? Applying IPSASs to define the reporting entity in municipal consolidation. International Journal of Public Administration, 38(4), 325–334. https://doi.org/10.1080/01900692.2015.1001239

- Grossi, G., & Tagesson, T. (2008). Consolidated financial reports in local government: A comparative analysis of IPSASB and SCMA. In S. Jorge (Ed.), Implementing reforms in public sector accounting (pp. 337–349). Coimbra University Press.

- Kajüter, P., Lessenich, A., Nienhaus, M., & van Gemmern, F. (2021). Consequences of interim reporting: A literature review and future research directions. European Accounting Review, 31(1), 209–239. https://doi.org/10.1080/09638180.2021.1872398

- Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structures as myth and ceremony. American Journal of Sociology, 83(2), 310–363. https://doi.org/10.1086/226550

- Oliver, C. (1991). Strategic response to institutional processes. Academy of Management Review, 16(1), 145–179. https://doi.org/10.5465/amr.1991.4279002

- Oulasvirta, L. (2014). The reluctance of a developed country to choose International Public Sector Accounting Standards of the IFAC. A critical case study. Critical Perspectives on Accounting, 25(3), 272–285. https://doi.org/10.1016/j.cpa.2012.12.001

- Oulasvirta, L. O. (2022). Consolidated financial statement information and group reporting in the central government: A user-oriented approach. Journal of Public Budgeting, Accounting & Financial Management, 35(6), 28–51. https://doi.org/10.1108/JPBAFM-08-2022-0126

- Pallant, J. (2013). SPSS survival manual: A step by step guide to data analysis using IBM SPSS (5th edn). McGraw-Hill.

- Pilcher, R., & Dean, G. (2009). Implementing IFRS in local government: Value adding or additional pain? Qualitative Research in Accounting and Management, 6(3), 180–196. https://doi.org/10.1108/11766090910973920

- Rodríguez Bolívar, M. P., Alcaide Muñoz, L., & López Hernández, A. M. (2013). Determinants of financial transparency in government. International Public Management Journal, 16(4), 557–602. https://doi.org/10.1080/10967494.2013.849169

- Santis, S., Grossi, G., & Bisogno, M. (2018). Public sector consolidated financial statements: A structured literature review. Journal of Public Budgeting, Accounting & Financial Management, 30(2), 230–251. https://doi.org/10.1108/JPBAFM-02-2018-0017

- Santis, S., Grossi, G., & Bisogno, M. (2019). Drivers for the voluntary adoption of consolidated financial statements in local governments. Public Money & Management, 39(8), 534–543. https://doi.org/10.1080/09540962.2019.1618072

- Stewart, E., & Connolly, C. (2021). Recent UK central government accounting reforms: Claimed benefits and experienced outcomes. Abacus, 57(3), 557–592. https://doi.org/10.1111/abac.12222

- Stewart, E., & Connolly, C. (2022). New development: Ten years of consolidated accounts in the United Kingdom public sector—Taking stock. Public Money & Management, 42(6), 460–462. https://doi.org/10.1080/09540962.2022.2031647

- Sundell, A., & Lapuente, V. (2012). Adam Smith or Machiavelli? Political incentives for contracting out local public services. Public Choice, 153(3–4), 469–485. https://doi.org/10.1007/s11127-011-9803-1

- Tagesson, T. (2009). Debate: Arguments for proportional consolidation: The case of Swedish local government. Public Money & Management, 29(4), 215–216.

- Tagesson, T., & Grossi, G. (2012). The materiality of consolidated financial reporting—An alternative approach to IPSASB. International Journal of Public Sector Performance Management, 2(1), 81–95. https://doi.org/10.1504/IJPSPM.2012.048745

- Van Genugten, M., Van Thiel, S., & Voorn, B. (2020). Local governments and their arm’s length bodies. Local Government Studies, 46(1), 1–21. https://doi.org/10.1080/03003930.2019.1667774

- Voorn, B., Van Genugten, M. L., & Van Thiel, S. (2017). The efficiency and effectiveness of municipally owned corporations: A systematic review. Local Government Studies, 43(5), 820–841. https://doi.org/10.1080/03003930.2017.1319360