ABSTRACT

The British grocery retail sector is experiencing rapid growth in online ordering for home delivery, resulting in considerable supply side investment in delivery and fulfilment infrastructure. For retailers with a physical store network, investments typically utilise larger format stores as delivery and fulfilment hubs. Proximity to the store network and delivery infrastructure capacity thus drive the availability and choice of online groceries provider at the neighbourhood level. We aim to assess the geographical extent of online groceries coverage at a small-area level in Great Britain (GB). We carry out a nationwide assessment of the provision of online groceries, revealing generally excellent coverage within urban and suburban areas, including those neighbourhoods that may have once been considered urban food deserts. However, rural–urban inequalities are evident, with the most remote and rural catchments experiencing comparatively poor online groceries provision. We argue that these inequalities give rise to a new form of food desert: remote and rural neighbourhoods with the compounded effects of poor access to physical retail provision (akin to ‘traditional’ food deserts) and the additional disadvantage of poor coverage by online groceries providers. Many of these neighbourhoods are already the most remote from physical store provision and may also be faced with withdrawal of physical (retail) services. We make a number of recommendations that could support the provision of online groceries services in these areas and reflect on the tremendous potential for ongoing research into widening inequalities in access to grocery retailing driven by the geography of online groceries.

Introduction: spatial components of online groceries

Great Britain (GB) is experiencing rapid growth in the provision and consumer uptake of online groceries (ordering groceries online for home delivery). In 2019 this market was worth £11.6bn (Statista Citation2020), with considerable additional growth evidenced following Covid-19 ‘lockdown’ periods. Whilst some of the earliest small-scale examples of e-shopping for groceries were designed to support vulnerable consumers (CitationWinterman and Kelly), online groceries services experienced initial rapid growth in major urban areas that offered high-density internet-savvy affluent populations and thus high volume and value online order potential. Whilst initial uptake of these services may have been constrained by broadband availability, contemporary variations in online groceries uptake are predominantly driven by sociodemographic and geographic factors such as age, affluence and access to physical retail opportunities (Clarke, Thompson, and Birkin Citation2015; Kirby-Hawkins, Birkin, and Clarke Citation2018; Alexiou and Singleton Citation2018; Hood et al. Citation2020).

Complex spatial relationships between the demand-side (consumer propensity to shop online for groceries) and the supply side (access to physical stores) are well documented. These include two competing theories of ‘innovation-diffusion’ (online groceries spreads or diffuses from major urban areas as centres of innovation) and ‘efficiency’ (poor access to physical retail opportunities results in higher online-groceries uptake in rural areas) (Anderson, Chatterjee, and Lakshmanan Citation2003). A number of studies have found evidence for each theory – including evidence that they can occur concurrently – across a range of spatial scales, product sectors and international contexts (see Beckers, Cárdenas, and Verhetsel Citation2018;; Hood et al. Citation2020, for an excellent summary and further examples). Whilst existing studies highlight the important role of access to physical stores in driving online groceries (Ren and Kwan Citation2009; Clarke, Thompson, and Birkin Citation2015; Farag et al. Citation2016; Kirby-Hawkins, Birkin, and Clarke Citation2018) they are focussed exclusively on indicators of consumer uptake such as self-reported consumer propensity to place online groceries orders (Hood et al. Citation2020) or transaction records capturing order volumes (Kirby-Hawkins, Birkin, and Clarke Citation2018).

Previous research has not considered the provision of online groceries. Unlike other product categories that benefit from near-universal deliverability via postal services, the delivery of perishable online groceries requires retailer-led investment on the supply side (Mortimer et al. Citation2016). Grocers with a nationwide physical store presence have adapted many larger format stores to act as distribution centres (handling online order picking, packing and delivery to consumers’ homes), enabling rapid expansion of this service using existing logistical and warehousing systems (Davies, Dolega, and Arribas-Bel Citation2019; Hübner et al. Citation2016; Wollenburg et al. Citation2018). Other online ‘pure-play’ grocers such as Ocado have utilised a warehouse-based model, developing large scale ‘online fulfilment centres’ (OFCs) (also known as ‘dark stores’) to provide order fulfilment and delivery capacity in major urban areas, discussed further in the following section.

Those consumers living farthest from large-format stores or OFCs – and thus potentially most likely to want to use online groceries as a substitute for shopping in store (cf. efficiency theory) may experience comparatively poorer provision of these services. We aim to assess whether investment in distribution and fulfilment systems at the store and OFC level has resulted in geographical inequalities in the local provision of online groceries, specifically seeking to identify area-based inequalities in coverage and availability of these services. Our focus is on GB (the nations of England, Scotland and Wales). Together with Northern Ireland (NI) these nations comprise the United Kingdom (UK). We are not able to present a UK-wide assessment due to differences in data availability between these nations, preventing creation of our wider index across the full UK geographical extent.

In the following sections, we undertake a GB-wide assessment of the geography of online groceries provision at the neighbourhood level. We present novel research that highlights inequalities in groceries retail provision which are exacerbated by restricted coverage of online groceries. We begin by outlining logistical considerations which drive geographical variations in groceries accessibility, including the provision and coverage of online groceries. We then detail our small-area analysis of online groceries provision using web-scraped whole of the market data, in the first GB-wide assessment of delivery coverage. We unpick some of the urban-rural inequalities in online groceries delivery coverage and extend the ‘food deserts’ debate by additionally considering the impact of online groceries coverage, presenting a new composite indicator of neighbourhood level food desert-like characteristics. In the final section, we recognise a number of potentially low cost solutions which could support retailers in expanding their coverage of these services. We highlight the considerable potential for further research into online groceries provision, especially given the growing consumer uptake of these services and their potential role in reducing long-standing inequalities in access to groceries.

Literature review: online groceries provision as a potential driver of new small-area inequalities

Inequalities in access to grocery retail opportunities

Geographers have long considered inequalities in access to physical grocery retail opportunities. Prominent studies in the late 1990s and early 2000s identified the presence of ‘food deserts’, neighbourhoods that faced poor access to large format grocery stores providing fresh, healthy and affordable food (see Wrigley Citation2002; Wrigley, Warm, and Margetts Citation2003). Many of these neighbourhoods were some of the most deprived in England and Wales and located within inner city areas where residents faced considerable financial and practical (e.g. access to transport) barriers to accessing food store provision (Clarke, Eyre, and Guy Citation2002).

Wider debates surrounding food insecurity (Smith et al. Citation2018), healthy eating (Corfe Citation2018) and access to health-detrimental sources of food (Daras et al. Citation2019) recognise the importance of access to food. However, these studies often take a broader definition of food access to include information (e.g. considering the link between educational attainment and diet, see Wrigley (Citation2002)) and economic factors (addressing the link between food security and poverty (Smith et al. Citation2018)) alongside geographical accessibility. Whilst online groceries could potentially address a number of these food insecurity issues (for example, by targeting product offers to encourage healthy eating or maximising competition within this market), we are unaware of any studies that have considered geographic access to online groceries services in GB.

Considerable retail-led investment during the past 20 years may have largely addressed the issue of urban food deserts. These include rapid growth of inner city and suburban convenience stores operated by the major retailers and also growth in discount retailers, the latter showing an initial preference for sites in proximity to relatively more deprived urban communities. There has also been some recognition that online groceries could ‘limit the extent to which [urban] food deserts are a significant problem’ (Corfe Citation2018) for example, by improving access to grocery shopping opportunities among households without private transport. The potential role of online groceries as a tool to improve food access among disadvantaged households has been noted in a US context, with Karsten and West (Citation2017) reporting that the 2017 merger of Amazon and US grocer Whole Foods afforded new potential for food deliveries to reach households who lacked access to affordable and healthy food. Nevertheless, a review of a trial of online groceries as a tool to provide deliveries to low-income households as part of the Supplemental Nutrition Assistance Programme (SNAP) in the US identified that many of those neighbourhoods designated as food deserts had limited coverage of online groceries, especially in rural areas (Brandt et al. Citation2019). Whilst urban food deserts may represent an outdated concept (indeed there was considerable debate at the time about their validity (Cummins and Macintyre Citation2002), declining rural services and cuts to public transport provision may be driving new inequalities in access to groceries, with rural areas faring worst. Whilst there is growing recognition of the potential for rural food deserts in a US context (McEntee and Agyeman Citation2010; Morton and Blanchard Citation2007; Yeager and Gatrell Citation2014; Li and Kim Citation2020), GB food desert research was entirely urban focused. Our analysis explicitly redresses the urban-rural imbalance in food deserts research, focussing on the role of e-commerce in widening inequalities in access to groceries retail opportunities, which we suggest are exacerbated in rural areas, as outlined in the following sub-section.

Area-based inequalities in the provision of online groceries

The perishable nature of groceries, high-order frequency and consumer preferences for rapid delivery has required considerable retailer-led investment to operationalise online groceries at a local level. For those retailers with an extensive store network, investment has typically involved large-format physical stores acting as distribution centres for online home delivery groceries orders from nearby neighbourhoods (Hübner et al. Citation2016; Wollenburg et al. Citation2018). Whilst alternative click-and-collect online grocery channels exist in some localities, their use in GB is dwarfed by home delivery, with around 10 times more regular or occasional users of the home delivery service relative to collection points (Hood et al. Citation2020). Whilst not a direct part of our analysis and discussion in this paper, our ongoing research – in collaboration with a major UK grocer – assesses the geographical distribution of online groceries fulfilment capacity at the store level and will generate further insight into the spatial decision-making undertaken by retailers in relation to online groceries fulfilment.

Some retailers have also introduced online fulfilment centres (OFCs) (also known as ‘dark stores’) in locations where order volumes may make dedicated warehouse-based distribution centres more efficient for order picking/packing and dispatch. Hübner et al. (Citation2016) reported that Tesco served approximately 50% of their GB online order volume from a network of 6 OFCs in the mid-2010s and pure play operators Ocado and Amazon Fresh deliver exclusively from OFCs. At the time of our analysis, Ocado began delivering products for Marks and Spencer (M&S) as part of a joint-ownership deal. Ocado has previously collaborated with grocer Waitrose (who now operate their own store-based online order fulfilment) and operate some of the logistics and warehousing for Morrisons online groceries. In their investigation into the proposed Asda/Sainsbury’s merger in 2019, the Competition and Markets Authority (CMAFootnote1) (CMA Citation2019) recognised that a range of operational, financial and competitive decisions underpinned these investments in groceries home delivery..

where to introduce online groceries operations (which stores to use as distribution centres);

the geographic extent over which deliveries will be made from a given store (termed online service area);

the level of capacity to offer (number of orders that can be handled);

the specific timed delivery slots that will be offered (which may be linked to capacity), and;

the cost of delivery passed onto the consumer (how much to charge for delivery for each available delivery slot).

Although the media have identified limited examples of urban neighbourhoods that have been blacklisted for online groceries provision by individual retailers who refuse to deliver to these postcodes (Schlesinger Citation2010), we are unaware of any wider study of online groceries availability. Clearly, retailers’ online service areas – the spatial extent over which they will delivery orders from a given store or OFC – are a key driver of the provision of online groceries at a neighbourhood level. Retailer-determined service areas influence whether a given household is able to order online groceries from that retailer and is the focus of our analysis.

In determining online service areas, retailers must account for costs associated with ‘the last mile’ – delivery of goods from store or OFC to the consumers’ home. Online groceries inverts the traditional interaction between consumer and retailer in which the consumer travels to the store, transferring costs of the last mile from the consumer onto the retailer (Newing, Hood, and Sterland Citation2020). Grocers must delineate online service areas that contain sufficient consumer demand to make the investment viable, whilst also controlling the costs of delivery. Thus they must delineate compact online service areas with high density affluent populations, balanced with the desire to maximise penetration and market share by extending their online service areas into localities less proximate to the store network.

Research highlights considerable additional costs in making home deliveries in rural areas where order volumes and density are lower (Sousa et al. Citation2020; Gevaers, Van de Voorde, and Vanelslander Citation2014), but where demand for online groceries may be driven by poor access to physical retail opportunities (Cf. efficiency theory) (Brown and Guiffrida Citation2014; Hübner et al. Citation2016; Fernie and McKinnon Citation2009; Aspray, Royer, and Ocepek Citation2013). We thus hypothesise that the opportunities and benefits of online groceries may not have been experienced evenly across the demand side. The nature of online groceries logistics may result in an inverse relationship whereby the availability (retailer online service area coverage) and quality (delivery slot availability and cost, product availability, etc.) of online groceries are better in those areas that have greatest physical store provision or which benefit from order volumes sufficient for the development of OFCs. Whist we lack data on slot-availability and cost, the core aim of this paper is to assess the geographical coverage of retailers’ online service areas.

The unprecedented Covid-19 situation demonstrated that some grocers could rapidly extend online groceries capacity in localities where store-based or OFC infrastructure already existed (e.g. by hiring additional pickers and drivers) (Coupe Citation2020). It also demonstrated how available delivery slots could be prioritised for the most vulnerable consumers (Tesco Citation2020). However, extending the service into localities that are not already served by online groceries operations is costly and requires an existing store network to act as local distribution centres, or costly investment in new OFCs. Much recent investment in online grocery provision has favoured enhancements to provision in areas with existing high provision and uptake. For example, the 2019 launch of the Co-ops online delivery service was focussed entirely on major urban areas of London and Manchester, with subsequent expansion to stores in urban areas including Southampton, Liverpool and Leeds (Co-op Citation2020). Similarly, the decision by M&S to introduce online grocery shopping in a partnership with pure play online grocer Ocado (Neate Citation2019) may limit the spatial extent over which the benefits of the online availability of M&S groceries are realised.

The continued focus on urban areas for growth of online groceries highlights a potential urban-rural inequality in provision of these services. Whilst a number of existing studies have considered access to food stores in a physical sense, we are unaware of any studies that have considered the geographical provision of online groceries, or which have questioned whether access to groceries could be limited by poor provision of online groceries, which we aim to address in this analysis. In the following section we outline a methodology to assess online grocery delivery availability, before assessing the geography of online groceries provision in GB utilising a bespoke indicator of small-area grocery retail accessibility, the first of its kind to capture online groceries availability.

Methodology: Assessing Delivery Availability

There are no public domain data sources of online groceries provision at a neighbourhood level in GB. Whilst retailers make claims about coverage in press releases or annual reports, they publish no definitive list of areas covered by their service, with consumers required to input their postcode on retailers’ websites to check delivery coverage. In order to meet our aim to build a GB-wide picture of delivery coverage, we web-scraped this information from retailers’ websites. We focussed on five major grocery retailers who operate a store network and online groceries: Tesco, Sainsbury’s, Morrisons, ASDA and Waitrose. We also considered frozen food specialist Iceland and pure play operators Ocado and Amazon Fresh. Whilst no data on online groceries market share are available, our expertise of the GB grocery sector and discussions with industry representatives suggests that these retailers collectively account for at least £9 in every £10 spent on online groceries in GB.

Each retailers’ website terms and conditions were checked to ensure that the research abided by the terms and conditions outlined, including the robots.txt protocol that allows website owners to indicate whether they are willing for their website to be scraped. Web-scraping is an efficient method to gather information from webpages where APIs don’t exist (Mitchell Citation2015). It involves mimicking the behaviour of consumers using retailers’ websites to check delivery availability, extracting the relevant page contents and storing it as structured useable data.

The web scraping undertaken in this work closely adhered to the Office for National Statistics (ONS) Web-Scraping policy (ONS Citation2018), approved by the UK Statistics Authority for ethical, transparent and compliant web-scraping for societally beneficial research. We used the ‘requests’ (2.21.0) module in Python 3.6 to send requests (inputting a target postcode) to retailers’ web servers and to record the responses (delivery coverage available or not available). Each retailer’s website required a slightly different approach, dependent upon the structure of their website delivery availability postcode checker. Additional details on this can be found at: https://github.com/fmav1/WebscrapingDeliveryAvailability.

The terms and conditions of the Tesco website meant that it was not possible to apply web-scraping techniques to extract their delivery availability. Information provided by Tesco to the CMA (Citation2019) reveals that Tesco provided online groceries coverage to 99.7% of UK households. Based on our own analysis of Tesco’s store network, we believe a total of 9,947 households (0.3% of UK households) have no online groceries delivery coverage by Tesco, all of which are located on outlying Scottish Islands. We manually added Tesco delivery coverage to our web-scraped dataset.

We undertook analysis at a Lower Super Output Area (LSOA) level, associating each LSOA with a single-unit postcode representing its population weighted centroid (ONS Citation2019). LSOAs are a small-area geography in England and Wales and part of a statistical hierarchy of zones used for the dissemination of census and population data. They have a maximum population of 3,000 residents or 1,200 households (ONS 2016) and thus represent the neighbourhood level. For our analysis they offer a balance between geographical precision and detail alongside the need for efficient web-scraping and the ability to link to other small-area indicators (of deprivation and rurality for example) which are released at the LSOA level. For our analysis in Scotland, Data Zones were used and represent the closest equivalent to LSOAs in England and Wales. They have a slightly smaller target population of between 500 and 1,000 residents (SNS, CitationNo DateCitationNo Date) but enable equivalent linkage to underlying census and neighbourhood statistics. We have a total of 41,735 LSOAs or DZs within our analysis, representing a total of 25.7 m households.

We also acknowledge that our decision to focus on the 8 major retailers outlined above will miss some localised or smaller scale provision. This includes online delivery offered by the Co-op (which at the time of analysis provided a list of stores that offer this service but no indication of their service areas (Co-op Citation2019), independent community shops offering online groceries (see Plunkett Foundation Citation2017), other local food systems such as farm shops and third sector support for shopping (e.g. see Age UK Citation2019). Whilst these may be an important source of groceries for some consumers, the major players included in our analysis account for the bulk of the market, as outlined above and offer the full range of food and non-food products stocked within larger grocery stores. Additionally, we consider only Amazon’s ‘Amazon Fresh’ groceries service that is akin to online groceries services provided by the major grocers (CMA Citation2019) rather than its more limited product or coverage offering available via ‘Amazon Pantry’ or ‘Amazon Prime Now’.

Results: the geography of online groceries home delivery

Overall delivery coverage

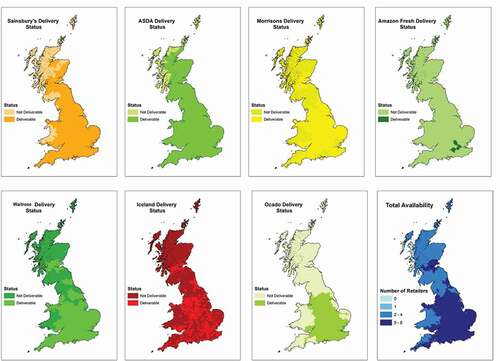

illustrates the delivery coverage of the seven retailers that were part of our web-scraping (Tesco is not illustrated separately given its near-complete national coverage). Our findings are consistent with the CMA investigation into the proposed Sainsbury’s and Asda merger which noted the near-national presence of Tesco, Sainsbury’s and Asda in online groceries (CMA Citation2019). Our analysis reveals that these three retailers each offer delivery coverage to in excess of 98% of all GB households, with less than 500,000 households falling outside the service area of at least one of these three major retailers ().

Table 1. GB delivery coverage by retailer at LSOA and household level

Figure 1. GB groceries delivery coverage by retailer and overall coverage (count of retailers offering delivery) at the LSOA level as of July 2019.

highlights that overall coverage of online groceries by the major three providers is comprehensive, with further coverage enabled by Morrisons, Waitrose and Iceland, each providing delivery coverage to in excess of 80% of GB households, albeit with a clear spatial bias towards England for Waitrose and towards urban areas for Iceland. Pure play operator Ocado provides coverage to approximately 75% of households in GB, though this is entirely focused on England and south Wales with limited or no coverage in large areas of south west England, rural Wales, East Anglia, and large parts of northern England and Scotland. Hübner et al. (Citation2016) report that this coverage is achieved through a network of just two regional fulfilment centres and a series of smaller local warehouses. By contrast Pure Play operator Amazon Fresh has the most geographically restricted delivery coverage centred only on selected London postcodes, yet given the high-density population in these areas is able to offer coverage to almost 15% of GB households.

also highlights total delivery availability (number of retailers providing delivery coverage) by LSOA and reveals a clear distinction whereby most of England and the major urban areas in Wales and Scotland enjoy excellent delivery coverage, whilst a limited number of rural areas in south west and northern England, and much of rural Wales and Scotland face comparatively much poorer choice of delivery providers. Thus, urban-rural geography is clearly important in driving inequalities in provision as considered in the following section.

Linkage of our LSOA level delivery coverage (as shown in ) with additional neighbourhood level indicators reveals that delivery coverage is also in line with revealed consumer brand preferences in GB (Newing, Clarke, and Clarke Citation2014) with online groceries coverage by Waitrose and Ocado focussed predominantly on more affluent areas whilst coverage by Iceland and Morrisons is greater in more deprived neighbourhoods (), reflecting the store network and typical location-types favoured by these retailers. Specifically, there is no evidence that consumers in more deprived neighbourhoods – many of which were previously thought of as urban food deserts – experience poor access to online groceries.

Table 2. Delivery coverage by retailer and relative deprivation at the LSOA level (proportion of households in each IMD decile with delivery coverage by stated retailer)

Similarly, our analysis draws on 2011 Census data in relation to car ownership finding evidence that households without access to private transport benefit from online delivery coverage. We do find some evidence to suggest that those households with lower broadband speeds (derived from data provided by CDRC Citation2020) experience poorer choice in online groceries, with those households with the lowest broadband speeds (<10 Mbps) more likely to have limited choice of online delivery provider (coverage provided by two or fewer retailers). This may be a legacy of lower order volumes within these areas, originally driven by poor connectivity (cf. innovation diffusion theory). However, we find no evidence that neighbourhoods with a lower propensity to shop online for groceries (as revealed by the 2018 Internet User Classification (Alexiou and Singleton Citation2018), explored in a little more detail below) have poorer delivery coverage and so propensity to engage in online groceries doesn’t appear to be directly related to coverage.

Urban-rural distinctions

To define degree of rurality, we utilise (by grouping categories) the 2011 Rural–Urban classification (RUC) for small-area geographies (in England and Wales) (ONS Citation2013) and the Scottish Equivalent (Scottish Government Citation2016), as shown in . The Rural–Urban classification is on official statistic used to distinguish rural and urban areas, classing rural areas as those that are outside settlements with a resident population of more than 10,000, providing a clear definition or urbanity and rurality which is consistent with previous research.

Table 3. Definition of urban-rural

We find considerable differences in coverage by degree of rurality, as shown in . All households with no delivery coverage are located in areas that we have classed as remote rural (all of these households are located on Scottish Islands). Consumers living in areas classified as remote rural experience considerably poorer access to online groceries, and more limited choice in provider than their urban counterparts. Whilst urban neighbourhoods typically benefit from delivery coverage by at least four of the six retailers that operate a store network, residents of rural areas are less likely to be able to obtain delivery from Morrisons, Waitrose, Iceland or Ocado. Less than 5% of households in the most remote rural areas fall within the online service areas for Morrisons or Waitrose, with no Ocado or Amazon Fresh coverage in these areas.

Table 4. Delivery coverage by rural-urban classification

Overall, almost 67,000 households have no choice of delivery provider, with over 60% of those being in the areas that we have classified as remote rural, the remainder drawn from areas classified as rural. For almost all of these households delivery is only provided by Tesco. Across GB, just over 230,000 households have a choice of only two retailers, most commonly Tesco and ASDA. Given that these households are likely to represent those with poorest access to physical store provision (due to their predominantly remote rural location), lack of choice of retailer for online groceries may result in a poorer shopping experience for these consumers. Lack of online delivery provider means that consumers may have limited delivery slot availability, restrictive minimum order values to qualify for delivery or prohibitive delivery costs. This was specifically noted by the CMA (Citation2019) in relation to the Sainsbury’s-Asda merger where they identified scope for these ‘coordinated effects’ between the major players in the online groceries sector in situations where consumer choice of online groceries provider is limited.

Our web-scraped assessment of small-area online groceries provision is the first comprehensive assessment of online groceries coverage and reveals geographical inequalities in the availability of online groceries. Whilst geographers have traditionally considered inequalities in grocery retail provision in urban areas (cf. the food deserts debate), our analysis highlights that considerable inequalities in retail provision are evident between urban and rural areas, exacerbated by geographical inequalities in online groceries coverage. In the following sub-section we use our web-scraped delivery availability as part of a bespoke composite indicator which captures the impact of geographical variations in online groceries availability as part of a measure of neighbourhood access to retail services.

Assessing the impact of online groceries on food deserts

In spite of widespread academic and policy interest in geographical access to food, there is not a consistent methodology to measure grocery retail accessibility at a local level. Sparks, Bania, and Leete (Citation2010) note that attempts to identify food deserts typically identify vulnerable neighbourhoods (e.g. low income) that do not meet a specific threshold measure of accessibility to food retail opportunities. The definition of vulnerable neighbourhoods and the appropriate threshold distance to use vary between studies and international contexts – see Sparks, Bania, and Leete (Citation2010) for an excellent overview of the range of accessibility measures utilised within previous studies of food deserts in the UK, USA and Canada.

We draw upon a bespoke composite index which captures the likely presence of food-deserts at a neighbourhood level. The index has been produced by the authors and described fully in Citation(Newing and Videira Citation2020) using a consistent methodology for all neighbourhoods (LSOAs/DZs) in GB, enabling comparison between areas. Whilst we briefly outline the construction and composition of the index in the following paragraphs, our discussion here is concerned with the impact of incorporating online groceries provision (as collated and outlined in the previous section) within the index, assessing the contribution of geographical variations in online groceries provision to this overall measure of grocery retail accessibility.

Our index captures a range of factors that influence the multi-dimensional nature of groceries accessibility as experienced by consumers at the neighbourhood level. A total of 12 input indicators are used, determined based on insight from the literature, our experience of modelling consumer behaviours within the grocery sector and an assessment of multicollinearity between indicators. Each indicator is robust at the small-area level and captured consistently across all LSOAs/DZs. The four equally weighted domains and their indicators are sumarised below, with two domains broadly focused on accessibility of physical grocery retail provision, one domain focussed on demand side characteristics and a final domain concerned exclusively with online groceries. For more detail on the indicators chosen and justification for their inclusion, see Newing and Videira (Citation2020).

Retail opportunities: These measures are widely used in the literature as an indicator of geographic food access (see Charreire et al. (Citation2010) for a detailed overview). We calculate the distance to the nearest large grocery store (greater than 15,069 square foot as defined by the CMA (see Geolytix Citation2019)), the average distance to the nearest three grocery stores (an indicator of consumer choice in physical groceries provision) and the number of stores within 1 km of each neighbourhood (density of retail provision), capturing multiple dimensions of store accessibility, choice and competition as experienced by consumers. We also capture a Hansen-style indicator of store accessibility (which additionally accounts for store size and brand, important measures of store attractiveness) derived from a custom-built spatial interaction model (SIM) to simulate GB-wide grocery retail flows between neighbourhoods and physical grocery stores at the LSOA level.

Transport and accessibility: Captures additional domains of grocery store geographical accessibility using indicators of travel time to nearest food store by car and on foot (derived from the Index of Multiple Deprivation and published journey time statistics) and our own measure of average trip distance for grocery shopping. The latter reflects modelled trip distances to stores used for grocery shopping (which may not be the nearest store) by residents in each LSOA, accounting for brand preferences and store attractiveness (store size) and derived from our custom-built SIM.

Neighbourhood socio-economic and demographic indicators: This domain captures income deprivation (derived from the IMD) (the link between poverty and food insecurity is well documented (Smith et al. Citation2018) alongside census-derived measures of car ownership (lack of car ownership may be a barrier to accessing food stores, especially where income barriers may make other sources of transport unaffordable or public transport provision may not be available) and the presence of pensioner households.

Online groceries: This novel domain is the unique contribution captured within this paper, reflecting the availability of online groceries home delivery (using the count of retailers providing delivery to each LSOA as collected in our analysis and outlined above) and the propensity for residents in each LSOA to shop online for groceries, derived from the Internet User Classification (IUC). The IUC provides small area estimates of internet engagement drawn from a range of input data from large-scale surveys and transactional sources (Alexiou Citation2019). It explicitly reports propensity to shop online for groceries, from which we have extracted the relative propensity – by IUC group (n = 10) – to shop online for groceries.

The final index provides a single score for each LSOAs/DZs enabling each area to be ranked or grouped into deciles, with higher scores and lower ranks/decile groupings reflecting that an area experiences comparatively poor provision of and access to grocery retail opportunities – including online groceries. The inclusion of online groceries as a separate domain enables us to explicitly consider novel notions of groceries accessibility across both physical and online channels. Although not the focus of our discussion, removal of the online groceries domain provides a contemporary measure of food deserts by their original definition (based on physical store accessibility, see Wrigley (Citation2002). In 2019, food desert-like characteristics are evident in some of the deprived inner city neighbourhoods of cities such as Leeds, Bradford and Cardiff, which were the focus of previous research into urban food deserts (Wrigley, Warm, and Margetts Citation2003; Wrigley Citation2002; Clarke, Eyre, and Guy Citation2002). Notably, we also find that food desert-like characteristics are exhibited in those areas classified as rural or remote rural, where limited physical store provision and comparatively poorer online groceries provision coincides with pockets of deprivation and lack of access to private transport.

Our analysis reveals that online groceries provision affords some improvement to groceries accessibility in rural areas, with over two thirds of neighbourhoods classified as ‘rural’ exhibiting improved access to groceries (less food desert-like characteristics) following the inclusion of online groceries within our index (). By contrast, incorporation of online groceries resulted in over 87% of those LSOAs/DZs classified as ‘remote rural’ experiencing poorer access to groceries relative to other neighbourhoods (). Thus, we observe that the relatively good coverage of online groceries in (accessible) rural areas (where households typically benefit from a number of providers) improves overall access to groceries in these areas, many of which score relatively poorly in terms of access to large format physical stores.

Table 5. food desert index scores and relative ranks by degree of rurality

Limited coverage (typically manifest in lack of choice of online delivery provider) in the most remote rural areas means that those areas experience a worsening in their overall relative position within the index after online groceries is accounted for. This highlights that poor online groceries coverage in areas classified as remote rural is exacerbating inequalities in access to groceries. These areas are already some of the most remote from physical store provision (as highlighted by the retail opportunities domain), with accessibility not substantially improved by online groceries provision, at least not to the extent that it is in less remote neighbourhoods.

Interestingly, incorporation of online groceries also drives relative improvements in groceries accessibility in many major urban areas. This is likely to be a result of the excellent online groceries coverage within many of these areas, including coverage by pure play grocers Ocado and Amazon Fresh. It may also reflect comparatively poorer provision of large format stores in some of the major conurbations due to the high costs of development and lack of suitable within-centre sites, with larger format stores typically located in fringe and out of town locations. Our index thus highlights a complex relationship between online groceries provision and overall accessibility to groceries retail opportunities as experienced at a neighbourhood level and explored further in the following concluding section.

Discussion and Conclusions: Online Groceries Delivery Coverage

Our web-scraped assessment of small-area online groceries provision is the first GB-wide assessment of delivery coverage. Whilst geographers have traditionally considered inequalities in grocery retail provision in urban areas (cf. the food deserts debate), we suggest that the growth and provision of online groceries are exacerbating existing urban-rural inequalities in retail provision. Notwithstanding the discussion below, our analysis meets its stated aims and reveals that coverage of online groceries at the household level is generally excellent. The three major online players in this market each provide online groceries coverage to in excess of 98% of GB households). However, inequalities in provision and choice of provider remain, notably between urban and rural areas, with retailers facing considerable challenges in providing complete-national delivery coverage. Similar urban-rural inequalities have been identified in other forms of food-based online ordering for home delivery, including Just Eat (the market leading provider of delivered food prepared away-from-home) (see Keeble et al. Citation2021, for an excellent overview).

A minority of households are dispersed among large and sparsely populated rural areas where limited store provision restricts the opportunity for infrastructural investment in online groceries capacity. Only a limited number of retailers (in this case Tesco, Sainsbury’s and Asda) have the scale and geographical distribution of stores in order to offer near-national coverage, and their ability to do so is still restricted in some remote rural areas where store provision is limited or journey times to reach dispersed households are prohibitive in offering this service. Our custom-built multi-domain index capturing physical store accessibility and online groceries coverage reveals that neighbourhoods which are the most remote from large format grocery store provision also face poorer provision of online groceries in the form of limited choice (and in a small number of cases no availability) of online groceries coverage. Previous analysis by the CMA (Citation2019) has highlighted that online groceries is a powerful driver of competition in the grocery sector with implications for online groceries service quality and pricing.

The Covid-19 shift in consumer preference for online groceries evidenced that retailers could rapidly boost delivery capacity via introduction of additional delivery slots (Coupe Citation2020; Tesco Citation2020). However, this was dependent upon existing infrastructural capacity and predominantly benefits those areas where delivery coverage was already available. Expanding coverage beyond the existing store network in order to meet the needs of those consumers with limited coverage (including those with lack of choice of provider) is a more costly process requiring longer-term investment and the introduction of delivery capability at stores that are not currently utilised for this service.

Whilst our analysis is based on the online groceries market in GB where attended delivery (consumer at home to receive delivery) is most common (Wollenburg et al. Citation2018), there are a number of international examples of retailer-led innovations which attempt to extend the coverage of online groceries within rural areas. These include greater use of non-store-based collection points or reception boxes in the most remote rural areas, passing some of the costs of the last mile back onto the consumer and improving the efficiency of the delivery network (Morganti, Dablanc, and Fortin Citation2014; Wollenburg et al. Citation2018). Hood et al. (Citation2020) recognise the potential value in retailers developing collection points in locations where access to physical retail opportunities are low, given evidence that substitution of store visits for online groceries is taking place in these areas. However (and in relation to store-based collection points) Davies, Dolega, and Arribas-Bel (Citation2019) note that groceries collection points still require costly temperature controlled storage that may be a barrier to their roll-out.

More innovative solutions to improve delivery coverage in those (rural) localities with a lack of choice of provider could include delivery pooling. Here one retailer (or a trusted third party) delivers online groceries orders from multiple retailers (see Pfeiffer Citation2018, for an example from a German context). Gevaers, Van de Voorde, and Vanelslander (Citation2014) demonstrate the cost savings that this could afford in terms of efficient vehicle routing. The highly competitive nature of the GB grocery market may make this form of long-term collaboration unlikely, although during the initial Covid-19 lockdown phase competition laws were relaxed in order to enable grocers to share warehouse space and home delivery vehicle fleets, maximising the number of online grocery orders that could be serviced (Yorke Citation2020).

Other delivery pooling opportunities to improve coverage in rural areas could include crowdshipping, whereby consumers shopping in-store deliver one or more online customer orders in proximity to their home address on their return journey from the store (Gdowska, Viana, and Pedroso Citation2018). Trialled by US grocer Walmart in 2012 (Gdowska, Viana, and Pedroso Citation2018) and third party platforms Shopwings and MyWays in German and Sweden, this could enable consumers to cover the last mile on behalf of the retailer, typically incentivised with a discount on their own shopping. In a GB context, Beelivery offers same-day online groceries home delivery using third-party drivers who undertake in-store shopping on behalf of the customer, using their own vehicle to deliver the order. Whilst drivers are typically couriers or taxi drivers looking for an additional income, anyone can register with the service (which at the time of writing is predominantly available in cities and major urban areas, though some rural postcodes are represented) and could fulfil these orders alongside their own food shop. If rolled out at scale beyond urban areas, these services could offer considerable improvements to online delivery availability in rural areas, notwithstanding possible issues with delivery reliability and potential for theft/fraud when utilising this form of crowdsourced model (summarised by Hübner et al. Citation2016).

The innovations highlighted above suggest that online groceries could actually offer a mechanism to improve grocery shopping accessibility for those consumers who live in neighbourhoods that are remote from physical store provision. The provision and coverage of online groceries is ultimately a commercial decision on the part of retailers and whilst these suggestions could afford considerable improvements in online groceries coverage and choice for some consumers, their introduction would be reliant on retailers anticipating sufficient benefits relative to costs in the form of consumer orders from these localities. Growing consumer propensity for online groceries (strengthened by uptake during the Covid-19 pandemic) and ongoing retailer expansion of these services suggests that previously under-provided rural localities could afford benefits for retailers looking to expand their online groceries coverage, notwithstanding the infrastructural costs involved.

Our ongoing analysis considers the extent to which online groceries provision and choice is linked to indicators of underlying physical store access. To that end we hope to re-ignite the food deserts debate, assessing the extent to which online groceries provision may be further exacerbating inequalities in groceries accessibility as experienced at the neighbourhood level. Specifically we seek to consider additional geographical indicators of online groceries provision which include delivery slot availability (driven by store capacity and order volume), delivery slot cost (for example Waitrose offers free delivery, ASDA applies consistent national pricing whilst other retailers vary delivery prices locally (CMA Citation2019) or product range and availability.

The analysis presented in this manuscript is an essential starting point in driving forward that research agenda and offers a novel insight into online groceries coverage at the household level. Our web-scraped fine-grained delivery coverage indicators reveal geographical variation in the geography of online groceries, whilst highlighting the potential for online groceries to improve consumer access to groceries and reduce food insecurity at the neighbourhood level.

Acknowledgments

This work was supported by the Leeds Institute for Data Analytics (LIDA) Data Science Internship Programme. Some data used within this research have been provided by the Consumer Data Research Centre, an ESRC Data Investment under project ID CDRC 310, ES/L011840/1; ES/L011891/1. The authors acknowledge the contributions of Ryan Urquhart to a pilot study which supported the development of this project. The authors have no competing interests to declare.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The e-Food Desert Index created by the research team and referred to in this paper can be accessed via the CDRC: https://data.cdrc.ac.uk/dataset/e-food-desert-index

Additional information

Funding

Notes on contributors

Andy Newing

Andy Newing is Associate Professor in Applied Spatial Analysis at the Univeristy of Leeds. His research interests include spatial and quantitative analysis related to retail location planning, service delivery/accessibility and census/neighborhood analysis. He is affiliated with the Consumer Data Research Centre and the Leeds Institute for Data Analytics and undertakes research collaborations with commercial and public sector organisations.

Nick Hood

Nick Hood is a Teaching and Research Fellow based in the School of Geography at the University of Leeds. His research interests are in the areas of retail consumer behaviour, location analysis of public and private services (e.g. retail location planning), geodemographics, voting behaviour, housing, and more broadly, Geographical Information Science. He is part of the Consumer Data Research Centre and the Leeds Institute for Data Analytics and has undertaken a number of collaborative research projects with commercial sector organisations.

Jack Lewis

Francisco Videira and Jack Lewis were Data Science Interns as part of the Leeds Institute for Data Analytics Data Science Internship Programme. The programme gave them both the opportunity to work on multidisciplinary research projects that involved finding data science solutions to complex real world problems. They have both subsequently secured data science roles in the commercial sector.

Notes

1. The UK independent non-ministerial government department which promotes market competition for consumer benefit.

2. Higher score denotes greater presence of characteristics associated with food deserts

References

- Age UK. 2019. “Services in Your Area: Shopping.” London, Accessed 27th June 2019. https://www.ageuk.org.uk/services/in-your-area/shopping/

- Alexiou, A. 2019. “The Great British Geography of Internet Use and Engagement.” CDRC, Accessed 19th June 2019. https://indicators.cdrc.ac.uk/stories/iuc/

- Alexiou, A., and A. Singleton. 2018. ” The 2018 Internet User Classification, ESRC Consumer Data Research Centre.“

- Anderson, W. P., L. Chatterjee, and T. Lakshmanan. 2003. “E-commerce, Transportation, and Economic Geography.” Growth and Change 34 (4): 415–432. doi:https://doi.org/10.1046/j.0017-4815.2003.00228.x.

- Aspray, W., G. Royer, and M. G. Ocepek. 2013. “Anatomy of a Dot-com Failure: The Case of Online Grocer Webvan.” In Food in the Internet Age, ed. W. Aspray, G. Royer, and M. G. Ocepek, 25–35. Boston: Springer.

- Beckers, J., I. Cárdenas, and A. Verhetsel. 2018. “Identifying the Geography of Online Shopping Adoption in Belgium.” Journal of Retailing and Consumer Services 45: 33–41. doi:https://doi.org/10.1016/j.jretconser.2018.08.006.

- Brandt, E. J., D. M. Silvestri, J. R. Mande, M. L. Holland, and J. S. Ross. 2019. “Availability of Grocery Delivery to Food Deserts in States Participating in the Online Purchase Pilot.” JAMA Network Open 2 (12): e1916444. doi:https://doi.org/10.1001/jamanetworkopen.2019.16444.

- Brown, J. R., and A. L. Guiffrida. 2014. “Carbon Emissions Comparison of Last Mile Delivery versus Customer Pickup.” International Journal of Logistics Research and Applications 17 (6): 503–521. doi:https://doi.org/10.1080/13675567.2014.907397.

- CDRC. 2020. “Boadband Speed.” Consumer Data Research Centre, Accessed 30th June 2020. https://data.cdrc.ac.uk/dataset/broadband-speed

- Charreire, H., R. Casey, P. Salze, C. Simon, B. Chaix, A. Banos, D. Badariotti, C. Weber, and J. M. Oppert. 2010. “Measuring the Food Environment Using Geographical Information Systems: A Methodological Review.” Public Health Nutrition 13 (11): 1773–1785. doi:https://doi.org/10.1017/S1368980010000753.

- Clarke, G., C. Thompson, and M. Birkin. 2015. “The Emerging Geography of E-commerce in British Retailing.” Regional Studies, Regional Science 2 (1): 371–391. doi:https://doi.org/10.1080/21681376.2015.1054420.

- Clarke, G., H. Eyre, and C. Guy. 2002. “Deriving Indicators of Access to Food Retail Provision in British Cities: Studies of Cardiff, Leeds and Bradford.” Urban Studies 39 (11): 2041–2060. doi:https://doi.org/10.1080/0042098022000011353.

- CMA. 2019. “Anticipated Merger between J Sainsbury PLC and Asda Group Ltd: Provisional Findings Report,” 20th February 2019.” In. London: Competition and Markets Authority.

- Co-op, 2019. “Stores that Offer Home Delivery.” Co-operative Group Limited, Accessed 26th June 2019. https://assets.ctfassets.net/d1oj5ay6114d/6f5yUu60V2ScsIyIKm2YO0/be8f5074dd6bae608812effea3c054f6/Home_Delivery_Stores_Customer_website_-_England.pdf

- Co-op. 2020. “Annual Report 2019.” In. Manchester: Co-operative Group Limited.

- Corfe, S. 2018. “What are the Barriers to Eating Healthily in the UK?.” London: Social Market Foundation.

- Coupe, M. 2020. “Supporting Elderly and Vulnerable Consumers’.” Email Update to All Registered Customers by Sainsbury’s Chief Executive Mike Coupe on 3rd April 2020. London: Sainsbury’s Supermarkets .

- Cummins, S., and S. Macintyre. 2002. “Food Deserts–evidence and Assumption in Health Policy Making.” BMJ (Clinical Research Ed) 325 (7361): 436–438. doi:https://doi.org/10.1136/bmj.325.7361.436.

- Daras, K., A. Davies, M. Green, A. Singleton, and B. Barr. 2019. “Access to Healthy Assets & Hazards (AHAH).” Consumer Data Research Centre, Accessed 1st July 2020. https://data.cdrc.ac.uk/dataset/access-healthy-assets-hazards-ahah

- Davies, A., L. Dolega, and D. Arribas-Bel. 2019. “Buy Online Collect In-store: Exploring Grocery Click & Collect Using a National Case Study.” International Journal of Retail & Distribution Management 47 (3): 278–291. doi:https://doi.org/10.1108/IJRDM-01-2018-0025.

- Farag, S., J. Weltevreden, T. van Rietbergen, M. Dijst, and F. van Oort. 2016. “E-Shopping in the Netherlands: Does Geography Matter?” Environment and Planning B: Planning and Design 33 (1): 59–74. doi:https://doi.org/10.1068/b31083.

- Fernie, J., and A. McKinnon. 2009. “The Development of E-tail Logistics, Kogan Page, London.” In Logistics and Retail Management: Emerging Issues and New Challenges in the Retail Supply Chain, ed. J. Fernie, 207–232. London: Kogan Page.

- Gdowska, K., A. Viana, and J. Pedroso. 2018. “Stochastic Last-mile Delivery with Crowdshipping.” Transportation Research Procedia 30: 90–100. doi:https://doi.org/10.1016/j.trpro.2018.09.011.

- Geolytix. 2019. Retail Points V13 June 2019. London: Geolytix .

- Gevaers, R., E. Van de Voorde, and T. Vanelslander. 2014. “Cost Modelling and Simulation of Last-mile Characteristics in an Innovative B2C Supply Chain Environment with Implications on Urban Areas and Cities.” Procedia - Social and Behavioral Sciences 125: 398–411. doi:https://doi.org/10.1016/j.sbspro.2014.01.1483.

- Hood, N., R. Urquhart, A. Newing, and A. Heppenstall. 2020. “Sociodemographic and Spatial Disaggregation of E-commerce Channel Use in the Grocery Market in Great Britain.” Journal of Retailing and Consumer Services 55. doi:https://doi.org/10.1016/j.jretconser.2020.102076.

- Hübner, A., X. B. Kotzab, H. Christop, H. Kuhn, and J. Wollenburg. 2016. “Last Mile Fulfilment and Distribution in Omni-channel Grocery Retailing.” International Journal of Retail & Distribution Management 44 (3): 228–247. doi:https://doi.org/10.1108/ijrdm-11-2014-0154.

- Karsten, J., and D. West. 2017. “How the Amazon-Whole Foods Merger Shrinks Food Deserts.” Brookings Techtank, Accessed December 2nd 2021. https://www.brookings.edu/blog/techtank/2017/08/29/how-the-amazon-whole-foods-merger-shrinks-food-deserts/

- Keeble, M., J. Adams, T. R. P. Bishop, and T. Burgoine. 2021. “Socioeconomic Inequalities in Food Outlet Access through an Online Food Delivery Service in England: A Cross-sectional Descriptive Analysis.” Applied Geography 133 (None): 102498. doi:https://doi.org/10.1016/j.apgeog.2021.102498.

- Kirby-Hawkins, E., M. Birkin, and G. Clarke. 2018. “An Investigation into the Geography of Corporate E-commerce Sales in the UK Grocery Market.” Environment and Planning B: Urban Analytics and City Science 239980831875514. doi:https://doi.org/10.1177/2399808318755147.

- Li, J., and C. Kim. 2020. “Exploring Relationships of Grocery Shopping Patterns and Healthy Food Accessibility in Residential Neighborhoods and Activity Space.” Applied Geography 116. doi:https://doi.org/10.1016/j.apgeog.2020.102169.

- McEntee, J., and J. Agyeman. 2010. “Towards the Development of a GIS Method for Identifying Rural Food Deserts: Geographic Access in Vermont, USA.” Applied Geography 30 (1): 165–176. doi:https://doi.org/10.1016/j.apgeog.2009.05.004.

- Mitchell, R. 2015. Web Scraping with Python: Collecting Data from the Moder Web. Newton, Massachusetts: O’Reilly.

- Morganti, E., L. Dablanc, and F. Fortin. 2014. “Final Deliveries for Online Shopping: The Deployment of Pickup Point Networks in Urban and Suburban Areas.” Research in Transportation Business & Management 11: 23–31. doi:https://doi.org/10.1016/j.rtbm.2014.03.002.

- Mortimer, G., E. H. Syed Fazal, L. Andrews, and J. Martin. 2016. “Online Grocery Shopping: The Impact of Shopping Frequency on Perceived Risk.” The International Review of Retail, Distribution and Consumer Research 26 (2): 202–223. doi:https://doi.org/10.1080/09593969.2015.1130737.

- Morton, L., and T. Blanchard. 2007. “Starved for Access: Life in Rural America’s Food Deserts.” Rural Realities 1: 4.

- Neate, R. 2019. “M&S Agrees £750m Food Delivery Deal with Ocado.” The Guardian, 27th February 2019. London: Guardian.

- Newing, A., G. P. Clarke, and M. Clarke. 2014. “Developing and Applying a Disaggregated Retail Location Model with Extended Retail Demand Estimations.” Geographical Analysis 47 (3): 219–239. doi:https://doi.org/10.1111/gean.12052.

- Newing, A., N. Hood, and I. Sterland. 2020. “Planning Support Systems for Retail Location Planning.” In Handbook on Planning Support Science, ed. J. Stillwell, and S. Geertman, 459–470. Cheltenham: Edward Elgar.

- Newing, A, and Videira, F 2020 E-Food Desert Index (EFDI): Technical report and user guide (Leeds: Consumer Data Research Centre (CDRC), University of Leeds)

- ONS, 2013. “The 2011 Rural-Urban Classification For Small Area Geographies.” Office for National Statistics, Accessed 17th July 2019. https://www.gov.uk/government/statistics/2011-rural-urban-classification

- ONS, 2018. “Web-scraping Policy.” Office for National Statistics, Accessed 17th June 2019. https://www.ons.gov.uk/aboutus/transparencyandgovernance/lookingafterandusingdataforpublicbenefit/policies/policieswebscrapingpolicy

- ONS, 2019. “ONS Postcode Directory (May 2019).” Office for National Statistics, Accessed 28th June 2019. http://geoportal.statistics.gov.uk/datasets/ons-postcode-directory-may-2019

- ONS. No Date. “Census Geography.” Office for National Statistics, Accessed 30th June 2020. https://www.ons.gov.uk/methodology/geography/ukgeographies/censusgeography#census-geography

- Pfeiffer, M. 2018. “Retail Trends from a German Perspective E Part II.”, Accessed 17th March 2020. https://www.retailpilot.de/2018/10/11/retail-trends-from-a-germanperspective-part-ii/

- Plunkett Foundation. 2017. Community Shops: A Better Form of Business. Woodstock: Plunkett Foundation.

- Ren, F., and M. Kwan. 2009. “The Impact of Geographic Context on E-shopping Behavior.” Environment and Planning B: Planning and Design 36 (2): 262–278. doi:https://doi.org/10.1068/b34014t.

- Schlesinger, F. 2010. “Tesco Refuses to Deliver Food to Residents because Their Street Is Blacklisted as ‘A Bad Area’.” Mail Online, Accessed 29th June 2020. https://www.dailymail.co.uk/news/article-1262276/Tesco-refuse-deliver-disabled-woman-street-blacklisted-bad-area.html

- Scottish Government, 2016. “Scottish Government Urban Rural Classification.” 2016.” Scotish Government, Accessed 16th July 2019. https://www.gov.scot/publications/scottish-government-urban-rural-classification-2016/)

- Smith, D., C. Thompson, K. Harland, S. Parker, and N. Shelton. 2018. “Identifying Populations and Areas at Greatest Risk of Household Food Insecurity in England.” Applied Geography 91: 21–31. doi:https://doi.org/10.1016/j.apgeog.2017.12.022.

- SNS, No Date . “SNS Data Zone 2011.” National Records of Scotland. https://www.scotlandscensus.gov.uk/variables-classification/sns-data-zone-2011#:~:text=Data%20zones%20are%20groups%20of,section%20of%20the%20NRS%20website

- Sousa, R., C. Horta, R. Ribeiro, and E. Rabinovich. 2020. “How to Serve Online Consumers in Rural Markets: Evidence-based Recommendations.” Business Horizons 63 (3): 351–362. doi:https://doi.org/10.1016/j.bushor.2020.01.007.

- Sparks, A. L., N. Bania, and L. Leete. 2010. “Comparative Approaches to Measuring Food Access in Urban Areas.” Urban Studies 48 (8): 1715–1737. doi:https://doi.org/10.1177/0042098010375994.

- Statista. 2020. “Market Value of Grocery Retail in the United Kingdom (UK) from 2004 to 2019.” Accessed 18th August 2020. https://www.statista.com/statistics/330171/grocery-retail-market-value-in-the-united-kingdom-uk/

- Tesco. 2020. “Food for All.” Email update to all registered customers, 22nd April 2020.” In.: Tesco Plc.

- Winterman, D., and J. Kelly. “Online Shopping: The Pensioner Who Pioneered a Home Shopping Revolution.” BBC. https://www.bbc.co.uk/news/magazine-24091393

- Wollenburg, J., A. Hübner, H. Kuhn, and A. Trautrims. 2018. “From Bricks-and-mortar to Bricks-and-clicks: Logistics Networks in Omni-channel Grocery Retailing.” International Journal of Physical Distribution & Logistics Management 48 (4): 415–438. doi:https://doi.org/10.1108/IJPDLM-10-2016-0290.

- Wrigley, N., D. Warm, and B. Margetts. 2003. “Deprivation, Diet, and Food-retail Access: Findings from the Leeds `food Deserts’ Study.” Environment and Planning A 35 (1): 151–188. doi:https://doi.org/10.1068/a35150.

- Wrigley, N. 2002. “‘Food Deserts’ in British Cities: Policy Context and Research Priorities.” Urban Studies 39 (11): 2029–2040. doi:https://doi.org/10.1080/0042098022000011344.

- Yeager, C. D., and J. D. Gatrell. 2014. “Rural Food Accessibility: An Analysis of Travel Impedance and the Risk of Potential Grocery Closures.” Applied Geography 53: 1–10. doi:https://doi.org/10.1016/j.apgeog.2014.05.018.

- Yorke, H. 2020. “Supermarkets to Share Staff and Delivery Vans under Government Plans to Relax Competition Laws during Coronavirus Outbreak.” The Telegraph, 20th March 2020.