ABSTRACT

The Sustainable Development Goals have intensified calls for private finance to address a so-called financing gap. This paper provides a critical assessment of the promotion of private finance in infrastructure, assessing two public–private partnerships (PPPs), celebrated for their success in mobilising private funds: a road in Senegal and a hospital in Brazil. While these projects may have had some positive outcomes, their apparent success relies on extensive support from governments and donors. Our findings question the efficacy of private financing as a response to shortages of infrastructure funds. Rather than plugging the financing gap, private finance risks creating fiscal burdens.

Introduction

The introduction of the Sustainable Development Goals (SDGs) in 2015 emphasised an urgent need for additional financial resources to address a so-called financing gap. The shortfall between the costs of achieving the SDGs compared with publicly available financing resources from Official Development Assistance (ODA) together with developing country governments is estimated to be around USD 2.5–3 tn each year (UNCTAD Citation2020). A wealth of donor-sponsored platforms and initiatives has emerged to promote private finance in development. Examples include the World Bank’s Global Infrastructure Facility and the G20’s Global Infrastructure Hub. These promote a variety of financing mechanisms including Public Private Partnerships (PPPs)Footnote1 (see Bayliss and Van Waeyenberge Citation2018). In the wake of Covid-19, there is likely to be greater pressure for the private financing of infrastructure, as fiscal space in developing countries will likely be constrained even further (Dimakou, Romero, and Van Waeyenberge Citation2020).

The intensification of the push for private finance reflects a recent shift in the development narrative, with deficiencies understood mainly in terms of financial resources, separate from structural or systemic causes of underdevelopment or global inequality. This paper explores the ways that this new development finance agenda unfolds. Section 2 critically appraises the drive to increase private finance in the context of Agenda 2030. Section 3 draws out lessons regarding the costs and benefits of private financial involvement in infrastructure on the basis of a desk-based review of two flagship pioneer projects in road transport and health: a road PPP in Senegal and a hospital PPP in Brazil. The paper shows that while private finance may be provided up front, this comes at a cost that is ultimately funded by the state and end users, raising doubts about the long-term efficacy of the private sector in filling the financing gap. Furthermore, attracting and sustaining projects with private finance requires substantial effort and resources from public agencies and international donors. We argue that while PPPs, as one form of private financial involvement in development, tend to represent only a small share of total infrastructure financing, their promotion has implications that reach beyond their financial significance. This includes the way in which infrastructure policy landscapes are re-imagined (or framed) in terms of what might suit potential investors, and comprehensive infrastructure plans become marginalised in favour of pipelines of “bankable” projects.

Promoting private finance in development

Privatisation has been a core development policy since the early 1990s. However, there has been a shift in approach since the early 2000s, as successive United Nations (UN) summits on Financing for Development have incrementally promoted the role of the private sector and increasingly highlighted the role of the state in doing so (Van Waeyenberge Citation2016). We make three observations regarding this shift before providing a summary of the main themes in the debates on private finance in infrastructure.

First, the UN Addis Ababa Agenda for Action (AAAA) in 2015 proposed that public funds could be used to incentivise private investment by reducing risk. The rationale for this approach is that “scarce” public funds can stretch further when used strategically to attract private finance to infrastructure and social sectors. According to the World Bank’s “Cascade” approach, subsequently renamed “Maximizing Finance for Development”, private sector finance should be the default financing option, with public and donor funds used as a last resort (World Bank and IMF Citation2017).

Second, new private players have entered the privatisation landscape. In the 1990s and 2000s, investors in infrastructure privatisations were mainly large infrastructure companies. More recently, infrastructure has become an asset class, attracting financial investors, such as private equity funds, to developing country infrastructure finance.

Third, building on the AAAA, leveraging private finance has become a development objective in its own right and has become integrated into evaluations of policy success. For example, the SDG 17.17.1 target indicator seeks to measure progress on the basis of the “amount of US dollars committed to public–private and civil society partnerships” (see unstats.un.org). Similarly, the World Bank has an evaluation system for development outcomes in the form of a “scorecard” with points allocated to “private mobilizations” (see Tier 3 in https://scorecard.worldbank.org/).

The 2030 Agenda emphasises how just a small portion of the large amounts of finance that the world’s private institutional investors manage (estimated at USD 100tn) would resolve the challenges of development finance. Private financial arrangements like PPPs are also considered to offer additional advantages over publicly financed alternatives, including improved project management, better maintenance, and timely execution (World Bank Citation2017). An evaluation of PPPs raises many challenges depending, for example, on how they are defined and what might be considered success. Yet, there has been extensive criticism of the private financing model (see Bayliss and Van Waeyenberge Citation2018 and citations therein). We sum up a few of the major themes in this literature.

First, despite the efforts of donors and governments, the financial impact of the private turn to date has been small and the public sector continues to dominate (Fay et al. Citation2019). Little investment takes place in low-income countries save a handful of large megaprojects in a select number of countries. In Sub-Saharan Africa (SSA), in 2017, 95% of all investment in infrastructure was publicly financed (World Bank Citation2019). However, the rapid rise in the promotion of private finance has implications that reach far beyond the relatively small value of funds raised, as we discuss below.

Second, private infrastructure projects can be at a high cost and create liabilities that are akin to debt in countries that are already at high risk of debt distress. With investor profits financed by end users, there is a risk that the long-term financial impact will be regressive. However, the true value of financial flows is often unknown, as PPP operations are recorded off-balance sheet and they frequently lack transparency and accountability, in part due to the cloak of commercial confidentiality.

Third, bringing in the private sector does not necessarily reduce demands on the public purse. Major public investment is often necessary to attract private finance in sectors with limited commercial returns, both to offset the risks of long-term uncertainty and to ensure that the benefits reach the whole population, not just those who can afford them. In Latin America, for example, the World Bank has noted that

while PPPs account for about 40 percent of Latin America’s infrastructure investments, they depend heavily on government support: about a third of their financing comes from public sources, and about half of all deals receive some type of government guarantee. (Fay et al. Citation2017, 65)

Fourth, PPPs create risks for the public sector. With public policy focused on attracting private finance, there is a risk of cherry-picking by the private sector, and fragmentation of infrastructure policy and practice which can lead to an overall weakening of state capacity. This can be observed where countries design pipelines of so-called bankable (i.e. profitable) projects instead of comprehensive infrastructure plans. In Kenya, for instance, the need to develop and rehabilitate 10,000 km of the national road network has translated into a pipeline of separate “lots”, each accounting for less than 100 km of road, which are packaged into separate PPPs (Government of Kenya Citation2020). Parcelling up the road network into discrete (and small) lots that have clearly identified revenue streams (via the public purse) reflects imperatives of private finance seeking low-risk, profitable investments. This is likely to be at the expense of an integrated, publicly financed approach where planning, procurement, and execution can reap economies of scale as well as reflect developmental imperatives (beyond bankability) and a broader redistributive mandate.

Fifth, there is an inherent contradiction between the quest for profits and the need to deliver social goals. PPP projects have to generate competitive returns for private investors in order to be implemented. The strong focus on identifying “bankable” projects limits the extent to which PPPs can proceed in areas that are not profitable without state subsidy. This has implications for public sector investment priorities: low priority projects may go ahead simply because they are commercially more attractive. This has also transformed infrastructure (or public services) into (private) assets able to generate secure revenue streams, as opposed to infrastructure as a public good (Romero and Van Waeyenberge Citation2020). Innovations such as “results based financing”, where fund disbursements are contingent on achievement of specific targets, are intended to provide incentives to improve targeting of PPPs, such as to reach lower-income users (World Bank Citation2017). However, as Clist (Citation2016) points out, such measures raise challenges, for example, in setting appropriate targets and evaluating progress and they may create perverse incentives in order to meet disbursement milestones.

Finally, and connected to the above, there is clearly an opportunity cost to using donor funds to attract private finance to deliver public services. Where public and donor funds are used to mobilise private finance there is a risk that this will divert public finance from traditional purposes (like social sectors) and regions where it is most needed (like low-income countries). In addition, there is little empirical evidence – including in evaluations conducted by official institutions – that PPP projects are specifically pro-poor or that they reduce inequalities, including gender inequalities. There are concerns that PPPs could become a mechanism for maximising private–sector accumulation rather than reducing poverty, thereby further increasing existing inequalities (Bayliss and Van Waeyenberge Citation2018).

PPPs, then, are associated with additional costs and risks for the public sector. Their promotion has implications that reach beyond the projects themselves, as infrastructure policy landscapes are re-imagined in terms of what might suit private investors. Some of these issues are teased out below, drawing on two examples of PPPs in the Global South.

PPPs in practice: who benefits?

This section presents findings from a desk-based review of two flagship pioneer projects in road transport and health. It draws on extensive consultation of policy documents, official reports, newspaper articles, other media sources available online, and existing scholarly commentary. The two projects are illustrative of wider developments in private finance. On the one hand, they are celebrated as successful examples of PPPs in raising finance for public services. On the other hand, they have played an important role in reshaping the (sectoral) policy landscapes within which they are situated. Both features necessitate closer scrutiny.

The Dakar–Diamniadio toll road: the highway of whose future?Footnote2

The first example draws on a critical development in the road transport policy landscape in SSA. In August 2013, a new toll road was inaugurated in Senegal providing a 20 km link between Dakar (Pikine) and Diamniadio, to the west of the capital city – connecting it to the new international airport. This is the first greenfield road PPP in SSA (outside of South Africa), the first toll road in Senegal and West Africa more broadly, as well as the first infrastructure PPP in the country. For the World Bank, the project “pioneered the maximising finance for development (MFD) approach for private sector financing in infrastructure projects in the country” (World Bank Citation2018, 31). However, for some stakeholders, the road is considered to be the “biggest scandal in Senegal since independence”.Footnote3

The project was initiated in 2003. It reflected President Wade’s enthusiasm for private investment, which was expected to provide the answer to the much-needed infrastructure upgrading of the country (see Gainer and Chan Citation2016). For example, from the early 2000s, the Government of Senegal (GoS) started to reform its legal and regulatory framework in order to accommodate (and promote) private participation in infrastructure. With support from the World Bank-hosted multi-donor Public Private Infrastructure Advisory Facility (PPIAF), a law was passed in 2004 to enable public and private entities to use PPP contracts (OECD Citation2014, 6).

The toll road was to be the first PPP project developed within Senegal’s new regulatory framework. Project preparation for the toll road was funded by the GoS, the World Bank, and the PPIAF. This included technical pre-feasibility studies delivered by French and Canadian consulting firms (in 2005), costing in excess of US$1mn and a further feasibility study and preparation of the bidding process undertaken by a Swiss consulting firm which was to act as financial advisor. Legal analysis was subcontracted to a multinational law firm and technical analysis to a French consulting firm. The costs for these studies were financed by a 2003 World Bank loan to Senegal. In 2007, PPIAF provided another grant (US$250,000) to strengthen capacity in the government agency responsible for the promotion of foreign investments in Senegal, the Agency for Investment Promotion and Major Works (APIX) (OECD Citation2014, 7).

The bidding process to select a private sponsor for the toll road started in April 2007 and took 28 months to complete. Three foreign consortia were pre-qualified. In 2009, APIX awarded the concession contract to a consortium led by the French multinational corporation Eiffage, a leading construction and toll road operation company. Eiffage formed SENAC S.A. as a special purpose vehicle to serve as concessionaire for the design, building, financing, and operation of the toll road for 30 years.

A financing package was put together by a set of international (and national) agencies (). The Agence Française du Developpement (AFD) and the African Development Bank (AfDB) each provided a concessional sovereign loan to enable the GoS to finance a subsidy to SENAC, which the original feasibility study had identified as necessary to attract private interest. These concessional sovereign loans were supplemented by non-sovereign loans (on non-concessional terms) from publicly backed international financial institutions directly to SENAC. The private sector share comes to just 17% of total financing.

Table 1. Sources of finance for the Dakar Diamniadio Toll Road PPP (in millions of US$).

The toll road has been considered a success by many. The World Economic Forum distilled a set of five concrete lessons to be learned from the project (Carter Citation2015). For PPIAF the toll road exemplifies the impact of its strategy to encourage PPPs in infrastructure worldwide (PPIAF Citation2010). For APIX the project introduced “a major innovation in the infrastructure policy of Senegal, opening new perspectives of efficient management by entrusting a large part of competencies to the private sector and allowing the state to concentrate on those missions it masters best”.Footnote4 It was instrumental in introducing the practice of infrastructure PPPs in Senegal, and various SSAn countries have indicated their willingness to follow its example in designing road PPPs (Carter Citation2015). Indeed, the World Bank (Citation2018, 22) evaluation report insists that “the project exemplifies how private sector participation can contribute to reduce the infrastructure gap of a country without overburdening public finance”.

However, the private sector brought a small share of the total project finance and risk transfer was low. Most of the finance was provided by different forms of public institutions and included an outright investment subsidy of US$158mn.Footnote5 Yet,

[u]nder the concession contract, SENAC S.A. is authorized to collect tolls based on contractual tariffs fixed according to the sections travelled by users. These rates were considered in the financing model to generate revenue projections … once Eiffage has ensured its return on investment, forthcoming revenues will be shared with the Government. (World Bank Citation2018, 57, emphasis added)

So, only once the private concessionaire has recovered its returns will the state be able to capture some of the revenue flows. The way the state would do so, however, remains unclear and could not be ascertained from the various publicly available project documents. The economic rate of return on the toll road has “exceeded initial expectations”, reaching levels in excess of 30% (World Bank Citation2018, 51). Ndiaye (Citation2017, 4) calculates that the capital pay-back period for the funds injected by Eiffage is less than two years. This reflects much higher traffic volumes than was originally estimated.

The GoS has faced significant costs associated with the PPP. The government was required to provide a grant (or “investment subsidy”) because initial projected traffic flows and toll fees that would be acceptable to users were not considered sufficient for a private investor to recover the costs of construction and maintenance of the road over the timespan of the concession. In return, the concessionaire would pledge to keep the tolls at “relatively low levels” (World Bank Citation2018).

Furthermore, the toll road did not depend only on the financial flows documented in , but benefitted from a set of additional publicly mobilised resources. The GoS fully financed the first sections of the highway (from Malick Sy to Patte d’Oie, 7 km, and from Patte d’Oie to Pikine, 5 km), without donor funding, “in order to demonstrate commitment to the project and speed up the construction of the PPP project” (OECD Citation2014, 6). The construction of this part of the highway (12 km in total) was awarded to Senegalese, Chinese, and Portuguese companies under traditional (publicly financed) procurement and was completed in 2009. The first section of the highway remains free of charge to users, the second section is a toll road that was included in the concession after it was built through public procurement (OECD Citation2014, 6; World Bank Citation2018, 4 and 25).

Still, more costs were incurred by the GoS. The construction, maintenance, and operation of the 20 km stretch of road that was parcelled off as a PPP toll road was fully embedded within a larger publicly funded operation that included a resettlement and forest management programme. These actions were essential prerequisites to the PPP project and their costs were carried by the government through a combination of donor credits and GoS budgetary resources. The total cost to enable the construction (maintenance and operation) of the 20 km stretch of road then amounted to US$570mn (see IEG Citation2018a, 2; World Bank Citation2009) – double the amount shown in . This, furthermore, does not include the costs incurred by the GoS on the first two stretches of road that connect Dakar to Diamniadio, which were fully financed through its own budgetary resources, and without which there would be no rationale for the toll road.

The GoS then played a key role in preparing the specific spatial and economic conditions so that a segment (20 km) of an integrated road (of 32 km), from Dakar to Diamniadio, could take the form of a private asset. While for investors, the transformation of infrastructure into private assets often invokes a disembodied set of features that generates a steady revenue-flow, the conditions for the latter often involve dealing with a set of difficult material and institutional realities (easily riddled with contestations) that necessitate costly state interventions. This is clear in the example of the toll road, where the GoS took on the task of resettling the communities that were in the way of the toll road as well as managing the toll road crossing a protected (Mbao) forest. The GoS also publicly financed those parts of the road network that integrate the toll road within the broader road infrastructure. Finally, while the project is financed by the resources shown in , ultimately, it is funded by toll payments from drivers as well as a government subsidy. The road has been well used, but it has not been popular due to the high costs for users, despite government subsidies. For some, its costs to the Senegalese state are considered excessive and its tolls are unaffordable (see above). Eiffage reports that the government is seeking to lower the toll from 3000 to 2000 CFA francs. The company suggests that this could be done by extending the concession’s term or “other compensatory measures” which will ensure that the company does not lose out from a reduction in the toll (Eiffage Citation2018, 116).

The Suburbio hospital in Bahia, Brazil: a success story?

Brazil’s first health PPP contract was signed in May 2010 in Salvador, Northeast Brazil. The Suburbio (or Outskirt) hospital is located in one of the most underserved districts of the city, catering for one million inhabitants. As the first publicly supported hospital constructed in almost 20 years, it served as a model to be replicated in other Brazilian states and municipalities to minimise health care bottlenecks and improve access to medical services.

Generally, the increased role of health PPPs in developing countries has to be set against a backdrop of health system reform through liberalisation, decentralisation, and a contraction of public health systems. In Brazil, the 1988 Federal Constitution declared health a “right of all persons and the duty of the State”, which prompted the creation of the National Health System, with the aim of extending health coverage to all citizens. The World Bank has exerted its influence to shape the health care system according to pro-market assumptions and it was instrumental in changing the regulatory framework at the national level to enable private sector participation in infrastructure and social services, including health.Footnote6

While the construction of the Suburbio hospital started in 2009 under direct management by the Bahian Government, this became compromised when the government encountered fiscal constraints that derived from Brazil’s 2000 Fiscal Responsibility Law, which required fiscal consolidation at all levels of state. The Bahian Government’s Secretariat of Health argued that, apart from addressing financial constraints, the PPP would allow the incorporation of new (and better) mechanisms in hospital management and took up the challenge of building political support for the project. Different trade unions opposed the project, including the Union of Doctors, as they considered the original plans for a hospital in Suburbio a union and social achievement, and the expectation was that the hospital would be publicly managed, offering a career for professional workers (Camargo and Albertin Citation2013; Carrera Citation2012). For the local community, however, the project raised the prospect of increased access to free healthcare, so there was no strong opposition (Carrera Citation2012).

The Bahian Government appointed the IFC as transaction advisor to implement a PPP for the operation and management of the Suburbio hospital. The project was developed under Brazil’s 2007 Private Sector Participation Facility, jointly funded by the Brazilian National Bank for Economic and Social Development (BNDES), the IFC, and the Inter-American Development Bank (IDB) to foster private investment in infrastructure projects. The Facility assisted the Bahian Government in setting up the Suburbio PPP, through technical studies and feasibility analyses, structuring the transaction, drafting the legal documents, conducting a promotional road show, and managing the bidding process.

The project was structured as a 10-year concession contract – renewable for an additional ten years. It transferred the hospital’s operation and management, including clinical and non-clinical services, to the private partner. The project proposal was in the public domain for a month and included a public hearing where different concerns, mainly by interested companies, were raised. On 26 February 2010, the project for the operation and management of a 298-bed hospital was auctioned at the Bovespa Stock Exchange – the main Brazilian institution for capital market operations – with the objective of increasing transparency of the process. The auction resulted in only two consortia participating, with one of them being disqualified due to its high bidding price. While it is difficult to identify the reasons for the low level of interest in the project, Carrera (Citation2012) indicates that the short tendering period (one month) and the setting of a low maximum price could have been critical factors. The project was awarded to the consortium Prodal Saúde, composed of the Brazilian company Promédica (70%), a regional health care company, and Dalkia Brazil (30%), a subsidiary of the French Group Veolia (which after 2013 it changed its name to Vivante, bought by private equity fund Axxon) specialising in facilities management and non-medical services.

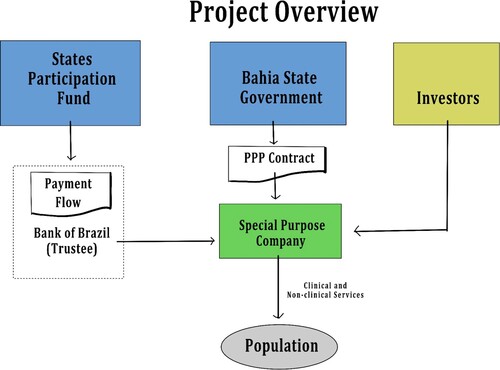

shows that project costs were split between construction, financed by the Bahian Government (for US$27mn), and US$32mn for equipment, financed by the private partner – of which US$23mn was incurred in the first year. Brazil’s public bank, BNDES, provided financing to the private partner. A more detailed breakdown of financing costs is not available from publicly available sources. To operate and manage the hospital, Prodal Saúde requested the maximum annual payment of U$S58mn from the Government of Bahia. Although the rate of return of the project – at the start of operations – was not publicly disclosed, research indicates that it was around 12% (Carrera Citation2014). However, subsequent contract amendments are likely to have improved the return profile for the private consortium (see below). The concession payments by the Bahian Government were linked to key performance (70% quantitative and 30% qualitative) indicators, penalising underperformance. These include inpatient and outpatient care, bed turnover rate and bed substitution rate, and accreditation for the hospital within 24 months from the start of operations (Carrera Citation2012). Finally, payments to the private sector were guaranteed by a mechanism through which federal funds were specifically allocated in a separate account (see States Participation Fund in ).

Figure 1. Project overview. Source: Adapted from IFC (Citation2011).

Table 2: Project cost and sources of finance Suburbio PPP Hospital.

The implementation of the Suburbio PPP exposes some of the challenges in using the PPP model to deliver healthcare. First, the risk allocation was defined in the contract as resting entirely with the private partner. However, a list of exceptions shifted the balance of risk on to the public sector. These include: any decision, either judicial or administrative, that prevents the private partner from providing the services; unpredictable factors of incalculable consequences or cases of force majeure that cannot be covered by insurance; changes in legislation or taxes that alter the private partner’s economic-financial composition; and omission or failures in the regulation or functioning of the public health network, especially regarding the removal and transfer of patients, which compromise the achievement of the quantitative and performance indicators of the concession (Carrera Citation2012). Thus, much of the project risk lies with the public sector, which bears additional risks in implementing the first health PPP in the context of a public health system that is heavily underfunded and over demanded at the State and municipal levels.

Second, demand was much higher than expected, requiring an expansion of the number of beds from 298 at the start in September 2010 to 373 in June 2014. Hence, in the first years of the operation of the hospital, in nearly every quarter, there was a request from the private consortium for adjustments to the contract due to increased demand for hospital services. This resulted in a real increase of 25.3% in the monthly payments made by the state to the private company (Carrera Citation2014; www.sefaz.ba.gov.br). One key reason for the increased demand might be the lack of functioning primary care facilities resulting in the local community’s recourse to the Suburbio hospital for ailments that would otherwise be addressed by these (Camargo and Albertin Citation2013; Carrera Citation2014). This problem was acknowledged by the World Bank’s Independent Evaluation Group (IEG Citation2018b, 33) as it recognised that: “In Bahia, for example, the primary care facilities were not ready when the PPPs started to operate. Therefore, the referral system was inadequate, resulting in an overflow of demand and unexpected fiscal pressures on government”. This highlights the need to situate private finance within the wider sectoral context.

Third, linking performance indicators and payments on the concession created strong incentives to promote market practices in the operation of the hospital. Concerns have been raised regarding an excessive emphasis by hospital management on practices that reduce costs, for instance, rejecting the admission of the most complex and potentially costly cases (Silva, De Carvalho, and De Oliveira Citation2019). Moreover, trade unions have questioned the management of the hospital regarding hiring practices and working conditions, which implied a more flexible labour regime than under civil-service law. This highlights the need to examine carefully assessments of the relative efficiency of hospitals under private, as compared with public sector, ownership and control.

Discussion and conclusion

The Senegal and Brazil cases illustrate concerns regarding the efficacy of the private sector in addressing infrastructure deficiencies which have been framed in terms of a lack of finance. While private finance brings up-front financing, this has to be repaid. As the example of the Brazil PPP hospital shows, the hospital services are ultimately paid for by the state, via its payments to the private sector, and the full extent of the costs being diverted to the private shareholders is unknown. In Senegal, the private sector funds are being recouped by toll payments by drivers alongside the public sector subsidy that was required for the project to be commercially viable. In both cases, the public sector has had to create clear revenue streams to meet the needs of the private sector in order to attract the private investment. Furthermore, as the Senegal case shows, the intended “leveraging effect” tends to be upside down, with a small amount of private finance having succeeded in mobilising a much larger share of public funds rather than the other way round.

Second, the effects of PPP promotion go beyond the projects themselves. In Senegal, as well as part-financing the project, the government had to construct an additional stretch of road to connect to the private toll road and bore the costs of the resettlement necessary to enable the private toll road. In Brazil, the construction of the PPP hospital was financed by the Bahian Government and the project has faced difficulties because of lack of integration within wider public health facilities, creating additional costs. The case studies show also that substantial resources are devoted to developing a legal and regulatory structure that incentivises private finance. This includes funds being diverted towards foreign advisers and consultants in these projects, the services of which tend to be financed through development cooperation.

Third, rather than representing a stepping back of the state, PPPs are demanding on the public sector, not just in establishing and funding PPPs but also in the longer term, although this is rarely mentioned in PPP evaluations. The case studies show that substantial risk lies with the state sector, which subsidises the toll in Senegal, and for which costs increased due to greater than expected use of the hospital in Bahia. Rather than plugging the financing gap, scarce public resources are mobilised in support of enabling private sector involvement, and to guarantee returns on private investment by multinational (foreign) operators. These are processes that facilitate revenue extraction by way of infrastructure assets, involving complex and costly publicly funded interventions. This has implications for the notion of public services, as the case studies demonstrate. In Senegal, the road was parcelled off as a PPP toll road with the objective of attracting private investors and, despite government’s efforts, it is not a project at the service of the local population. In Brazil, the Suburbio PPP hospital saw the introduction of market imperatives into healthcare, which may undermine the ability of the state to fulfil universal healthcare coverage commitments, as it takes away resources and creates pressures in the wider health system.

Overall, this paper draws attention to the effects of the accentuation of private finance in development finance under Agenda 2030, which is likely to be reinforced in the post-Covid-19 context. The drive to attract private finance has gathered momentum such that raising private finance is itself seen as meeting some kind of development goal. The projects discussed above have been celebrated for attracting private investment but this is only achieved because of extensive government and donor support and it is not clear whose interests are being promoted. As stated above, for supporters, PPPs are associated with efficiency gains in implementation (World Bank Citation2017), This is an empirical question and careful scrutiny is needed to ascertain the ways in which efficiency gains might be achieved. Typically, little attention is paid to the full value of long term financial outflows, the long-term developmental outcomes such as whether projects are sufficiently pro poor, or the long-term distributional effects of such interventions. However, the SDG narrative has normalised the drive to attract private finance in any shape or form.

The paper shows that there are inherent tensions in bringing the private sector into areas where there are strong social elements associated with provision. In each of these cases, policy settings are designed with the needs of investors in mind. The implementation of PPPs can be highly demanding on public sector capacity in terms of the negotiation and regulation of contracts. Governments face substantial costs and risks when prioritising profitability in public service provision. Thus, ex-ante assessments and ex-post evaluations of PPPs need to be far more comprehensive to capture the full scope of the effects of PPPs in the short and long term. With such a wide-ranging perspective, we anticipate that approaches to the use of private finance for development would be far more circumspect.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Kate Bayliss

Kate Bayliss is a Senior Research Fellow in the Department of Economics at SOAS and a Visiting Research Fellow at the University of Leeds. She has worked for over two decades on the effects of privatisation and the provision of basic services in the UK and the Global South. She has worked for governments, UN agencies, and NGOs. Her particular research interests are on the changing paradigms surrounding private sector engagement in meeting basic needs, and on the distributional outcomes from such interventions.

Maria Jose Romero

María José Romero is a PhD candidate in Development Economics at SOAS. Her research project is on the global promotion of public private partnerships (PPPs) in health and education. Since 2012, she has worked for the European Network on Development (Eurodad), a Brussels-based NGO, as a Policy and Advocacy Manager on publicly backed private finance and development finance institutions. This includes extensive work on PPPs and blended finance at the European and global level. She has a master's degree in political science from the University of the Republic of Uruguay.

Elisa Van Waeyenberge

Elisa Van Waeyenberge is a Senior Lecturer in the Economics Department at SOAS where she is currently serving as co-Head. Her research interests include alternative macroeconomic policies in developing countries, the role of international financial institutions across policy and scholarly realms, as well as the financing of infrastructure and public service provision. She has authored several articles on these topics as well as edited books with colleagues, including The Political Economy of Development: The World Bank, Neoliberalism and Development Research, together with Kate Bayliss and Ben Fine.

Notes

1 There are different definitions of PPPs (Romero and Van Waeyenberge Citation2020). For the World Bank, a PPP is “a long term contract between a private party and a government entity for providing a public asset or service, in which the private party bears significant risk and management responsibility, and remuneration is linked to performance” (World Bank Citation2017, 1).

2 Word play on the name of the toll road “L’autoroute du future” (the “highway of the future”).

3 See https://senegal-news.net/video-les-deux-plus-gros-scandales-du-senegal-depuis-lindependance/

and civil society groups have called for an audit of the financial involvement of Eiffage in the project, https://www.dakaractu.com/Declaration-du-Forum-Civil-a-propos-de-la-renegociation-du-Contrat-de-Concession-de-l-autoroute-a-peage-Dakar-AIBD_a183016.html

4 “Sur un autre plan, le Projet d’Autoroute à péage a introduit une innovation majeure dans la politique des infrastructures au Sénégal, en ce qu’il ouvre de nouvelles perspectives de gestion efficace des projets en laissant une large part aux compétences du Privé permettant ainsi à l’Etat de se concentrer sur les missions qu’il maîtrise le mieux”, M. Dominique Ndong, coordinator of major works at APIX, quoted in http://reussirbusiness.com/economie/le-contrat-ppp-entre-letat-et-eiffage-seleve-a-148-milliards-de-f-cfa-dinvestissement/ 9 Mai 2016, own translation.

5 In the PPP jargon, this is often referred to as “viability gap funding”.

6 A 2004 World Bank ‘Programmatic Loan for Sustainable and Equitable Growth Project’ (US$505mn) emphasised the need to improve the business environment and advocated for a PPP law to be passed at the federal level.

References

- Bayliss, K., and E. Van Waeyenberge. 2018. “Unpacking the Public Private Partnership Revival.” The Journal of Development Studies 54 (4): 577–593.

- Camargo, F., and N. Albertin. 2013. Conexão local. FGV. Accessed March 6, 2020. https://pesquisa-eaesp.fgv.br/sites/gvpesquisa.fgv.br/files/conexao-local/parceria_publico_privada_-_hospital_do_suburbio.pdf.

- Carrera, M. 2012. “Parceria público-privada na saúde no Brasil: estudo de caso do Hospital do Subúrbio de Salvador — Bahia.” Dissertação (mestrado) — Escola de Administração de Empresas de São Paulo. São Paulo: Fundação Getulio Vargas.

- Carrera, M. 2014. “Parceria público-privada (PPP): análise do mérito de projetos do setor saúde no Brasil.” Tese (doutorado) – Escola de Administração de Empresas de São Paulo. São Paulo: Fundação Getulio Vargas.

- Carter, L. 2015. “5 Lessons from sub-Sahara’s First Public-Private Road” Blog entry for World Economic Forum. Accessed June 8, 2020. https://www.weforum.org/agenda/2015/06/5-lessons-from-sub-saharan-africas-first-public-private-road/.

- Clist, P. 2016. “Payment by Results in Development Aid: All That Glitters is not Gold.” The World Bank Research Observer 31: 290–319. doi:https://doi.org/10.1093/wbro/lkw005.

- Dimakou, O., M. J. Romero, and E. Van Waeyenberge. 2020. “Never Let a Pandemic Go to Waste: Turbocharging the Private Sector for Development at the World Bank.” Canadian Journal of Development Studies / Revue canadienne d'études du développement 42 (1-2): 221–237.

- Eiffage. 2018. “Inventons un avenir à taille humaine” Document de reference. Accessed June 8, 2020. https://www.eiffageinfrastructures.com/files/live/sites/infrastructures-v2/files/6-newsroom/publications/fichier/Document-Ref-2018.pdf, 116.

- Fay, M., A. L. Andres, C. Fox, U. Narloch, S. Staub, and M. Slawson. 2017. Rethinking Infrastructure in Latin America and the Caribbean: Spending Better to Achieve More. Washington, DC: World Bank. https://openknowledge.worldbank.org/handle/10986/26390.

- Fay, M., H. Lee, M. Mastruzzi, S. Han, and M. Cho. 2019. “Hitting the Trillion Mark: A Look at How Much Countries Are Spending on Infrastructure”. PRWP 8730. Washington, DC: World Bank.

- Gainer, M., and S. Chan. 2016. A New Route To Development: Senegal’s Toll Highway Public-Private Partnership, 2003-2013. Innovations for Successful Societies, Princeton University. Accessed March 6, 2020. https://successfulsocieties.princeton.edu/publications/development-senegal-toll-highway-public-private-partnership.

- Government of Kenya. 2020. Kenya Public Private Partnerships Pipeline status – January 2020. Accessed June 8, 2020. https://www.pppunit.go.ke/wp-content/uploads/2020/02/Kenya-PPP-Pipeline-Status-Report-January-2020.pdf.

- IEG. 2018a. SN-Dakar –Diamniadio Toll Highway Project. Implementation Completion Report Review. Accessed March 6, 2020. http://documents.worldbank.org/curated/en/479731542811460379/Senegal-SN-Dakar-Diamniado-Toll-Highway-Project.

- IEG. 2018b. “World Bank Group Support to Health Services: Achievements and Challenges” Report by Independent Evaluation Group. Washington, DC: World Bank. https://ieg.worldbankgroup.org/evaluations/world-bank-group-health-services.

- IFC. 2011. Subúrbio Hospital PPP First Health PPP in Brazil. IFC Public-Private Partnerships in Health Johannesburg, South Africa. March 4. Power Point Presentation. Accessed March 6, 2020. https://slideplayer.com/slide/4465098/.

- Ndiyae, E. 2017. “Public/Private Partnership and Tariff Regulation Failure: The Example of Dakar/DAmniadio Toll Highway in Senegal.” International Journal of Economics and Management Sciences 7 (1): 1–4.

- OECD. 2014. “Donor Support to Public-Private Partnerships: The Case of the Dakar Diamniadio Toll Highway Project” Meeting of the Advisory group on investment for development.” Report number COM/DAF/INV/DCD/DAC(2014)4, OECD, Paris. Accessed March 6, 2020. https://one.oecd.org/document/COM/DAF/INV/DCD/DAC(2014)4/en/pdf.

- PPIAF. 2010. “Impact Stories. PPIAF Supports a Pioneering Transaction in Africa: the Dakar Diamniadio Toll Road in Senegal.” Public-Private Infrastructure Advisory Facility. Accessed March 6, 2020. https://ppiaf.org/documents/3048/download.

- Romero, M. J., and E. Van Waeyenberge. 2020. “Beyond Typologies. What is a Public Private Partnership?” In PPPS: A Critical Guide, edited by J. Gideon and E. Unterhalter, 39–63. London: Routledge.

- Silva, M., S. De Carvalho, and M. De Oliveira. 2019. “Desenho organizacional da rede de agentes que envolvem as parcerias público-privadas de saúde na Região Metropolitana de Salvador.” Geosul, Florianópolis, v. 34, n. 73, . 464–496. Accessed May 21, 2020. https://periodicos.ufsc.br/index.php/geosul/article/view/1982-5153.2019v34n73p464/41831.

- UNCTAD. 2020. Trade and Development Report: From Global Pandemic to Prosperity for All: Avoiding Another Lost Decade. Geneva: United Nations.

- Van Waeyenberge, E. 2016. “The Private Turn in Development Finance”. FESSUD Working Paper Series, 140, http://fessud.eu/wp-content/uploads/2015/03/The-private-turn-in-developing-finanace-Working-Paper-140.pdf.

- World Bank. 2009. Financing Agreement (Dakar Diamniadio Toll Highway Project). October 13, 2009.

- World Bank. 2017. Public-Private Partnerships: Reference Guide. Washington, DC: World Bank.

- World Bank. 2018. Dakar Diamniadio Toll Highway: Implementation Completion and Results Report. Report No: ICR00004347. Washington, DC: World Bank.

- World Bank. 2019. Who Sponsors Infrastructure Projects? Disentangling Public and Private Contributions. Washington, DC: World Bank.

- World Bank and IMF. 2017. “Maximizing Finance for Development: Leveraging the Private Sector for Growth and Sustainable Development.” Report No. DC2017-0009 by Joint Ministerial Committee of the World Bank and IMF.