ABSTRACT

This study examined the effects of a partial credit guarantee in increasing lending to credit constrained farmer cooperatives under the Ethiopian context. The data were generated through questionnaire survey, key informant interviews, focus group discussions, and from banks’ and cooperatives’ records. The scheme improved financial additionality among the targeted cooperatives, but it had limited reach and impacts on terms and conditions of loans. Factors related to borrower cooperatives, lending banks, scheme design and operation, regulatory and business environments affect its effectiveness. This calls for broader interventions that enable loan guarantees to be effectively utilised and generate the desired outcomes.

Introduction

There is a growing realisation that cooperatives can be an effective avenue for the provision of servicesFootnote1 that enhance agricultural productivity and help accelerate the transformation of smallholder agriculture and attain inclusive social and economic development (Okwoche, Asogwa, and Obinne Citation2010). Cooperatives play an important role in generating economies of scale, improving bargaining power, and fostering market integration for the fragmented smallholder farmers. Many African countries embarked on the creation of cooperatives during the colonial period, which were largely set up to facilitate production and exports of commodities for industries in the colonial states (Schwettmann Citation2011). This had negative implications for the image and local ownership of cooperatives. The emergence of modern types of cooperatives in Ethiopia traces its root to the 1960s, after the majority of African countries (Emana Citation2009). During the socialist period cooperative development was considered as a strategy to promote socialism ideology, collective ownership of production factors, and to maintain control over the production and marketing of farm produce (Schwettmann Citation2011). Cooperatives established with such motives undermined the basic principles of cooperative societies, such as voluntary membership. They also experienced widespread embezzlement and misappropriation of resources by their leaders and political cadres. With the end of the military regime in 1991, the cooperative movement almost vanished in Ethiopia and about 99% of them were dissolved (Chanyalew Citation2015).

In recent decades, economic reforms and market liberalisation policies created a favourable environment to reinvigorate the cooperative sector in Ethiopia (Emana Citation2009). The government took several measures towards promoting the development of cooperatives, including the creation of a cooperative promotion agency, facilitating the formation of cooperative structures at different levels, and allowing unique marketing opportunities. These measures led to the creation of a large number of different types of cooperatives (Emana Citation2009), bringing the number of primary cooperatives in the country to 89,000 in 2019 (FCA Citation2019). With the aim of strengthening horizontal networks and vertical integration, the government facilitated the creation of unions by bringing together volunteer primary cooperatives engaged in similar activities. Coffee unions were the first of their kind and emerged towards the end of the 1990s. The first-generation unions enjoyed various privileges that helped them to acquire better asset ownership, managerial capacities, and access to export markets.

In contrast, most primary cooperatives’ institutional and financial capacities remained poor. Cooperative leaders felt that the benefits generated by unions could not be effectively trickled down to strengthen the primary cooperatives. Such rapid expansion in their number also resulted in the formation of many new and weak cooperatives. In general, primary cooperatives experience severe financial constraints that hamper their contribution in improving smallholders’ position in the coffee value chain. Commercial banks tended to avoid or restrict loans to smallholder cooperatives due to the perceived high risk, the lack of collateral, and credit history. Analysis of banks’ credit reports shows that loans extended to the coffee sector are mainly channelled to private coffee traders, exporters, and unions, who have better market integration and facilities that can be pledged as collateral.

In order to address such gaps in the financial market, a five-year partial credit guarantee scheme (with 50% risk-sharing) was implemented in Ethiopia (2011–2016) with the aim to improve smallholder coffee cooperatives’ access to bank loans.Footnote2 The scheme integrated capacity buildingFootnote3 for the lending banks and borrower cooperatives. The Common Fund for Commodities was the main financier and guarantor, while CABI and MoA (Ethiopia), respectively, were the project executing and implementing agencies. Rabo Bank was involved partly in financing and risk-sharing, and Cooperative Bank of Oromia (CBO) participated in the guaranteed lending. The scheme adopted a portfolio approach whereby the guarantor and lending bank agreed on the borrower and loan criteria beforehand. In extending guaranteed loans, banks’ existing lending policies and procedures were used. The maximum security level payable to the lending bank was 1,250,000 USD, with annual risk fee of 1.5%. Based on 50% risk-sharing, the total risk agreement was 2.5 million USD, while the maximum disbursable amount to an individual cooperative was 250,000 USD. The scheme had a five-year lifespan with a maximum tenor of four years for qualifying loans. Defaults and claims procedures were outlined in the agreement. In view of the size of the guarantee fund, the project implementing agency selected 22 cooperativesFootnote4 from 12 districts of the two major coffee-producing regions of Ethiopia: the Oromia and Southern Nations and Nationalities Peoples (SNNP) regions.

Amongst the policy measures taken by governments and aid agencies, the credit guaranteeFootnote5 is considered to be the most effective mechanism employed to alleviate small enterprises’ financial constraints (Beck, Klapper, and Mendoza Citation2010; Tunahan and Dizkirici Citation2012). Partial credit guarantees cause less market distortion compared to other financial interventions because of their limited interference in credit allocations by lending institutions (Saadani, Arvai, and Rocha Citation2010). Credit guarantee can be an effective tool in influencing banks’ behaviour as it allows them to test and ascertain that the risk of lending to such groups is not that high (Levitsky Citation1997; Freedman Citation2004). Loan guarantees also play an important role in influencing banks’ behaviour and inducing competition to improve loan allocations and terms (Green Citation2003; D’ignazio and Menon Citation2013). However, in reality, the lending banks may not exhibit effective responses in taking up the guarantee and improving loan allocations. In some instances, lack of collateral may not be a decisive factor in preventing banks from widely reaching out to small enterprises (Levitsky Citation1997). Under a financial market with heavy state intervention and tight monetary and regulatory environments, such a scheme may have limited influence on banks’ credit allocations to smallholder cooperatives. Some argue that since lending requires capital, credit guarantees may not be able to produce sufficient additionalityFootnote6 due to lack of adequate loanable funds (Meyer and Nagarajan Citation1996). Generally, there is no consensus about the impacts of a credit guarantee in enhancing financial flow to farm households and small enterprise and its outcomes. Some country-specific studies (e.g. Cowling and Mitchell Citation2003; Ridding, Madill, and Haines Citation2007; Zecchini and Ventura Citation2009) reported that credit guarantees have contributed positively to small entrepreneurs’ access to finance, while others (e.g. Kang and Heshmati Citation2008; Zhang and Ye Citation2010) found that it added limited value or encountered complete failure in attaining its aim. Many authors (Levitsky Citation1997; Beck, Klapper, and Mendoza Citation2010; Hansen et al. Citation2012) note that Sub-Sahara African countries have not featured prominently in past studies that looked at the nature and effectiveness of credit guarantee schemes. Most of these studies focused on assessing guarantee schemes for SMEs in Asia, Europe, and North America, where such schemes have been extensively applied. Farmer cooperatives differFootnote7 from private firms in their objectives, nature, and location of business, loan requirement, etc. Therefore, this study examines whether a partial credit guarantee could be effective in increasing bank lending to credit-constrained smallholder cooperatives and generate substantial financial additionality under the Ethiopian context. The study also sheds light on factors influencing its performance and effectiveness.

Design and methodology of the study

The study area

The study was conducted in eight zones of the two major coffee-growing regions of Ethiopia – the Oromia and SNNP regions, which account for 99% of the coffee produced in Ethiopia. The study zones were West and East Wellega, West and East Hararge, Kaffa, Wolayita, Hadiya, and Kembata Tembaro. They possess different coffee production systems, agro-ecological conditions, and socio-economic set-ups.

Sampling, data sources, and collection

Initially, the two major coffee growing regions and all the eight zones where the guarantee scheme was implemented were purposively selected. For the structured survey, 80 primary cooperatives were chosen, including all the 22 cooperatives that were targeted by the guarantee scheme and 58 non-participant cooperatives. The criteria in choosing non-participant cooperatives include: involvement in coffee business, member size, and being located in those zones. For the in-depth qualitative study (KIIs and FGDs) representatives of actors involved in coffee production, processing, marketing, finance, and extension were purposively selected.

We employed a mixed method approach which, as Creswell (Citation1998) suggests, helps to obtain more or better information through the converging or triangulating of the results from qualitative and quantitative methods, and to extend the results generated through one method by using another method. The data were collected from different sources at various stages of the scheme implementation. The first-round survey (baseline) was carried out at an early stage of the intervention (in December 2012 and January 2013), while the second round was conducted after two years (in 2015) to assess the changes in certain variables. Key informant interviews and focus group discussions with different actors were conducted at different stages of the scheme implementation. In addition, the researchers carried out continuous observations of the scheme implementation process, behaviour, and practices of the borrower cooperatives and lending banks using semi-structured checklists to guide the observations with adaptations to suit the different events or occasions. Moreover, data were obtained from the guarantee scheme, banks, and cooperatives records and documentations.

Data analysis

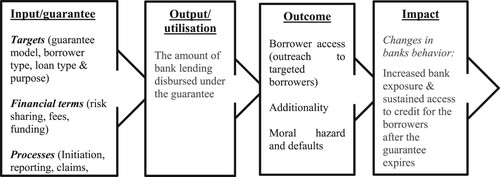

Analysis of the data obtained through qualitative methods was carried out independently from the analysis of the data obtained through quantitative method. Combining the findings of the two components of the study took place during the data interpretation and report-writing stages. Analysis of some of the qualitative data was started during the actual research process, whereby the researcher carried out the continuous processes of fine-tuning the collected information through probing, exploring, and triangulation. A combination of some basic steps proposed by Creswell (Citation1998) and Mouton (Citation2001) were adapted and pursued to analyse the qualitative data (see Annex – 1). Relevant elements of the analytical frameworkFootnote8 proposed by Dalberg (Hansen et al. Citation2012) () were adapted and used to assess features and performance of the credit guarantee. SPSS 17 was used to analyse the descriptive survey data.

Figure 1. Framework for assessing the features and performance of guarantee schemes. Source: Adapted from Dalberg Analysis (Hansen et al. Citation2012).

Results and discussion

Design of the guarantee scheme: inputs, targets, and financial terms

Many (e.g. Levitsky Citation1997; Green Citation2003) concur that design features and institutional arrangements can fundamentally influence effectiveness of a guarantee scheme. The findings of the current study suggest that though operations of the scheme had some limitations, most of its design features are in line with international practices. Vital scheme design features, terms, and conditions were clearly spelt out in the contract signed between the two parties. These include: objectives, eligibility (target group, sector, type, and purpose of loan), maximum volume of guarantee, individual loan ceiling, risk fees, loan tenor, claims procedure, etc. Given the location of the guarantor (which is based in the Netherlands) and considering other factors, the study suggests that the portfolio approach adopted by the scheme was the right choice. International experiences (Hansen et al. Citation2012) also show that such donor-funded schemes are more likely to adopt portfolio guarantees. The lending activities rely on the bank’s existing loan screening and approval processes, thus requiring less administrative work and operational costs from the guarantor’s side. The portfolio model is more flexible and a better approach to increasing the number and volume of guaranteed loans extended to targeted borrowers (Hansen et al. Citation2012). However, this approach involves higher risks as the guarantor is not involved in screening each borrower’s applications (Saadani, Arvai, and Rocha Citation2010). The lending bank did not appreciate the fact that the guarantee fund was resident in the Rabo Bank (guarantee administrator). Some bank officers indicated that paper guarantee may not be attractive enough as it lacks mechanisms that help banks to address their liquidity problem, which is a critical challenge to many commercial banks in Ethiopia. This implies that provision of a cash guarantee whereby funds are deposited in the accounts of the lending banks may motivate them as it helps to ease their liquidity problems.

The capacity building and technical support components embedded into the intervention were considered as one of the merits of the scheme. Evidence (Saadani, Arvai, and Rocha Citation2010; Hansen et al. Citation2012) suggests that financial interventions can be more effective if complemented by technical assistance and capacity building both for the lending banks and borrower firms. Interviewed bank officers noted that poor financial and business management impede cooperatives’ access to and effective utilisation of loan finance. Development of such capacities for the borrower cooperatives was seen as a critical factor for the success of the credit guarantee. Banks require their own capacity building in order to efficiently and effectively utilise guarantees and/or to change the way they operate or develop new products for such borrowers (Hansen et al. Citation2012).

The level of risk coverage (50%) was considered low among the mainstream commercial banks, at least at the initial stage. The majority of the interviewed banks expressed reservations regarding its ability to attract lending banks unless it is backed by other incentive packages. This is in view of the prevailing high-risk perception about farmer cooperatives and the stiff competition from other borrowers with more lucrative businesses. One bank key informant notes that, “While there are many low risk borrowers out there, there is no reason for banks to be interested in taking 50% risk”. This view was shared by the majority of the mainstream private commercial banks. We also noted that banks prefer to link loans to other benefits such as export earnings and saving deposits. Most of the bank officers indicated that they would expect borrower cooperatives to provide collateral to cover the remaining 50% risk. International experiences (Saadani, Arvai, and Rocha Citation2010) suggest that guarantee schemes should be allowed to ask for collateral subject to reasonable limits as its complete absence may generate adverse selection and moral hazard effects. However, most cooperatives will struggle to meet substantial collateral requirement. Given the situation of farmer cooperatives and the tight financial market in Ethiopia, bank officers suggested that risk coverage has to be increased (to about 70 or 80%), at least during the initial stage. However, international experiences (Hansen et al. Citation2012) show that, unlike the individual model, portfolio guarantees rarely provide more than a 50% risk coverage.Footnote9 Choosing the level of risk coverage represents a trade-off between minimising moral hazard and maximising the ability of the guarantee to induce additional lending (Freedman Citation2004). Thus, the coverage needs to provide sufficient protection against risks of default, while it also reserves incentives to motivate banks to undertake proper screening, monitoring, and loan recovery efforts (Saadani, Arvai, and Rocha Citation2010).

The level of fees levied on such credit guarantees is another important component that may affect its effectiveness. The current guarantee scheme charges a 1.5% risk fee though it was not clearly indicated whether it should be charged on the disbursed loan amount or on the total volume of the guarantee fund. International experiences (Hansen et al. Citation2012) suggest that fees for portfolio guarantees are likely to be lower, reflecting the reduced administrative burden on the guarantee provider. High fees improve additionality by discouraging banks to use the guarantee for targeted borrowers, but may reduce outreach (Saadani, Arvai, and Rocha Citation2010). Interviewed bank officers indicated that in the presence of such massive loan demand among other clients, banks may not be willing to absorb high risk fees. Some stated that as lenders directly or indirectly transfer guarantee fees to the borrowers, it would make the guaranteed loans more expensive. In fact, the participating bank did not pay any risk fee over the three years of lending, which affects the validity of the guarantee for such loans.

The findings suggest that the five-year life span of the scheme (with four-year effective lending period) was considered too short for an intervention targeting such borrower groups that require substantial in-advance capacity building and long-term loans for coffee processing facilities. More importantly, in order to enable cooperatives to establish strong relationships with the banks, such interventions have to operate for a reasonably long period of time. International experiences (e.g. Levitsky Citation1997) show that the most successful schemes across the world take 5–10 years to develop effective collaborative relationships between the participating parties. Moreover, the targets, eligibility criteria, and coverage ratio were not revised and adapted after the inception of the scheme. Scholars (e.g. Levitsky Citation1997; Deelen and Molenaar Citation2004) underscore the need to periodically review and adapt the scheme’s design and operational features after some time, based on the experiences gained. On the other hand, inclusion of both short-term working capital and long-term investment loans was considered as one of the merits of the current scheme. Interviewed cooperative leaders indicated that the maximum individual loan size provided by the scheme (250,000 USD) is in line with the credit needs of most of the cooperatives in those areas.

The findings suggest that engaging a Cooperative Bank, which is more coops-friendly, with experience in lending to such groups, is one of the right decisions under the current scheme. However, relying on a single lending bank was seen as a limitation as the scheme lacked alternative lenders when this particular bank showed reluctance to reach out to the targeted cooperatives as anticipated. International experiences (e.g. Deelen and Molenaar Citation2004; Tunahan and Dizkirici Citation2012) suggest that participation of more than one competent bank may provide alternatives as well as induce some sort of competition among the banks. However, in addition to posing administrative challenges, thinly spreading such a small guarantee fund across a number of banks may not make much economic sense.

Outputs: up-take and utilisation of the loan guarantee by the lending banks

Utilisation of the loan guarantee by the commercial banks is one of the vital aspects under such an arrangement. In this regard, only one bank was interested to participate in the current loan guarantee scheme. A previous study (Tunahan and Dizkirici Citation2012) similarly noted that one of the fundamental problems of the guarantee schemes operated in developing countries is to convince the banks to participate in the programme’s operations and risk-sharing. Hansen et al. (Citation2012) suggested that a bank’s commitment to utilising the guarantee must emanate from a strategic alignment of interest that leads to genuine engagement at various levels of the bank. Although almost all interviewed bank officers believe that the cooperative sector is an important market segment, they do not see them as a lucrative client-base that should be given priority. Cooperatives’ leaders felt that their needs and challenges were not properly understood, valued, and addressed by commercial banks. ITC (Citation2011) notes that the loan products of the formal financial markets often do not take account of the nature of the crop (e.g. coffee) production cycle. Bank officers for their part believe that cooperatives lack viable business (to finance) and capacity to effectively manage their finance and business. For instance, at the launch of the current scheme, only 11% and 33% of the surveyed cooperatives had managers and accountants, respectively. Moreover, the inefficiencies, embezzlement, and massive loan default experienced by cooperatives during the socialist system were still fresh in the memories of lending banks, and continued to affect banks’ confidence in cooperatives’ credit worthiness.

We tried to assess the performance of the scheme in terms of its guarantee utilisation among the lending banks. We found that outreach of the scheme in terms of number of cooperatives reached and number of guaranteed loans disbursed was limited. At the outset, a total of 22 cooperatives were targeted to benefit from the guarantee scheme, out of which 14 were able to access guaranteed loans over the three years lending. Two, eleven, and four cooperatives obtained guaranteed loans during the first (2012/13), second (2013/14), and third (2014/15) seasons, respectively. Out of the 22 cooperatives, 20 had submitted loan applications at least once over the first three years of lending, and close to two-thirds (70%) were able to access guaranteed bank loans. This figure did not include the number of cooperatives that enjoyed improved access to loans provided by parent unions. One of the positive indirect contributions of the intervention was that it had an influence in increasing unionsFootnote10 interest in and loan allocation to cooperatives targeted by the scheme. For instance, during the third year of lending, 13 of the scheme-participant cooperatives were able to receive 7.4 million Birr from their parent unions, which was hardly attained before the launch of the scheme.

The guarantee agreement states that with the 50% risk-sharing, the scheme will provide a total of partially guaranteed loans of up to 60 million Birr. Eventually, a total of 18.4 million Birr guaranteed loans were disbursed to the cooperatives over the first three years of lending (2012/13–2014/15). This constitutes 61% of the total guarantee fund, and only about 31% of the loanable fund under such a partial guarantee with 50% risk-sharing. In respect of individual loan size, the smallest and largest guaranteed loan amount per cooperative were 200,000 Birr and 3 million Birr, respectively. On average, 1.32 million Birr was disbursed to individual cooperatives over the three years of lending. This amount is considerably high as compared to the loan volume (200,000–500,000 Birr) cooperatives were traditionally receiving through their unions.

However, the partner bank failed to properly communicate and provide sufficient information about the guarantee arrangements to its branch offices, which affected the performance of the scheme. Moreover, the lending bank was not periodically informing the guarantor about new guaranteed loans and the status of such a loan portfolio. This has obvious implications for risk fee payment and claims settlement in the event of default. Literature (e.g. Hansen et al. Citation2012) suggests that the portfolio approach requires more regular reporting. There were signs that some of the bank branches still tend to avoid the risk of lending to cooperatives that have never borrowed before. Even after the cooperatives fulfilled all the lending requirements, some of the bank branches were trying to delay loan approval and disbursement. A study (Hansen et al. Citation2012) conducted in four countries in Africa similarly noted that even after banks have invested time and resources in signing a guarantee agreement, a significant number failed to exceed a 60% utilisation of the guarantee fund.

When compared with the volume of loans cooperatives applied for, the actual amount disbursed to cooperatives was on the lower side which shows the prevalence of credit rationing. This could be related to limitations in the institutional and business capacities of the borrower cooperatives and shortage of loanable funds among the banks. Given the current organisational, business, and managerial capacities of the study cooperatives, the volume of loans requested by some of them seems to be unrealistically high. The business plan presented by some of the applicant cooperatives was also not convincing to the lending banks. Previous studies (e.g. Chanyalew Citation2015) similarly noted that in Ethiopia cooperatives often do not operate with proper and strategic planning, especially in acquiring and utilising loan funds. This calls for continued support to strengthen their institutional, business, and financial management capacities.

Loan fund leverage ratio

One of the significances of such a loan guarantee is its role in leveragingFootnote11 a substantial amount of loan funds with limited guarantee funds. Given the partial structure of guarantees and the impossibility of defaults of all the borrowers at the same time, guarantee funds are able to offer a large amount of guarantee compared to their capital (Tunahan and Dizkirici Citation2012). Though a higher leverage ratio is often considered a great achievement, a healthy guarantee programme has to keep its leverage ratio under a certain level without decreasing it to a lower level which may restrict borrowers from benefiting from the guarantees (Ibid). When we assessed the leverage ratio under the current scheme, we found 0.61:1 for the bank loan, and slightly over 1:1 ratio when loans obtained from unions were included. According to Levitsky (Citation1997), a well-performing guarantee fund can attain a leverage level of five times the fund (5:1) after five years of operation. Deelen and Molenaar (Citation2004) similarly note that after three years of operation, a guarantee scheme should attain a leverage ratio of 2:1 or 3:1 and after five years this should reach 5:1. The leverage ratio attained under the current scheme is apparently low when compared with the recommended ratio. Deelen and Molenaar (Citation2004) argue that a level of leverage less than 1:1 can be considered a failure to a guarantee scheme. However, they note that it is normal for guarantee schemes to attain low leverage rates during their early stages. Growth in leverage takes time as trust and confidence has to be developed between the parties involved in the guarantee scheme (Levitsky Citation1997). Given the infancy of the scheme, limitations in the capacity of borrower cooperatives, and the tight regulatory and financial system, the leverage ratio attained under the current scheme should not be taken as a complete failure.

Outcomes: additionalities attained under the scheme

We explored if provision of a loan guarantee really helped commercial banks to reach out to cooperatives that were effectively credit constrained and generated financial additionality. Despite some limitations, the guarantee scheme under assessment made positive contributions in improving cooperatives’ access to bank credit. Analysis of cooperatives' credit history shows that most of the loans obtained by cooperatives were additional finance, which would have not occurred in the absence of the loan guarantee. In total, 11 out of the 14 beneficiary cooperatives (78%) never had direct access to bank loans previously. Even the remaining three cooperatives indicated that they would have not been able to receive such a large volume of loans if it was not for the support of the scheme. About 87% of the total loans disbursed under the scheme over the three years can be taken as additional loans that were made possible because of the intervention. Levitsky (Citation1997) suggests that an additionality of at least 60% should be the minimum acceptable target for justifying the operation of a guarantee scheme. Thus, the loan additionality attained under the current scheme can be taken as a significant achievement.

As presented in , 82% and 86% of the cooperatives targeted by the scheme took bank and/or union loans during 2013 and 2014 as compared with 32% and 68% before participating in the scheme (2010 & 2011), respectively. Further probing shows that before participating in the scheme, cooperatives were heavily relying on parent unions for obtaining loans, which merely provide small seasonal loans. Likewise, access of the majority of the non-participant cooperatives was also limited to such union loans. Loans provided by unions have conditions attached to them, which include selling their coffee to that particular union at a time and price determined by the union, leaving little or no space for negotiations and alternatives. In addition, such loans are often small in volume and merely used for seasonal coffee purchase. Cooperatives that are not affiliated with any union cannot access such loans.

Table 1. Difference in accessing loans before and after participating in the scheme.

As regards the amount borrowed from different sources, the cooperatives targeted by the guarantee scheme, on average, received almost two-folds of the volume obtained by non-participant cooperatives between 2012 and 2014 (). The difference between the two groups was also statistically significant (T = 2.201; P = 0.037). Such a difference can be largely attributed to the effects of the loan guarantee and associated capacity-building activities.

Table 2. Difference between the volume of loans obtained by participant and non-participant cooperatives (2012–2014) (N = 68).

Similarly, the T-test results in show that the mean annual volume of loans obtained by scheme participant cooperatives during first three year implementation of the scheme (2012–2014) was significantly (P = 0.003) higher than the volume they received before the launch of the scheme (in 2010 and 2011). Further probing through key informant interviews reveals that the scheme had an important role in improving the volume of loans accessed by target cooperatives. They noted that the intervention boosted their financial and business planning and management capacity.

Table 3. Difference between amount of loan obtained by cooperatives before (2010 & 2011) and during the scheme (2012–2014) (N = 17).

Improvements in the terms and conditions of loans

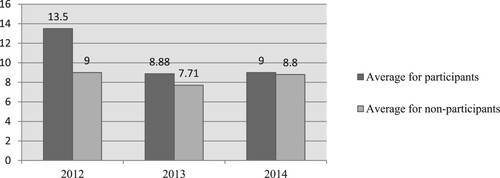

Farmer cooperatives need to be financed in a distinct way with loan terms and products that match the nature and requirements of their business. Contrary to previous studies (e.g. Gudger Citation1998; Freedman Citation2004; D’ignazio and Menon Citation2013), which reported that provision of a credit guarantee can improve the terms and conditionsFootnote12 of loans, we found that the current guarantee scheme had limited impact in this regard. The study reveals that banks were generally reluctant to extend loans of longer maturity to primary cooperatives.Footnote13 Experience demonstrates that in the absence of long-term loans, cooperatives tend to divert short-term loans to long-term investment, which as D’ignazio and Menon (Citation2013) note, affects their loan repayment capacity. The current scheme facilitated access to medium-term loans of three years to a few cooperatives, which had promoted investment in processing (e.g. wet mills) and storage facilities. Apart from improving coffee quality, acquisition of such processing facilities would play an important role in building cooperatives’ asset base, which can serve as collateral. Nevertheless, short-term loans of one-year duration dominated the guaranteed lending activities both in terms of number and volume of guaranteed loans. Medium-term loans accounted for less than 4% of the total volume of loans and 21% of the cooperatives received guaranteed loans over the first three years. During the first year of the guaranteed lending (2012) scheme, participant cooperatives, on average, obtained loans for a longer period (13.5 months) than their non-participant counterparts (nine months). However, we did not find a significant difference between the two groups for the subsequent years (). This shows that regardless of the availability of loan guarantees, banks were still hesitant to provide long-term loans to cooperatives. This could be related to the short lifespan of the scheme and the persistence of the banks’ perception of the risks associated with long-term loans.

Figure 2. Mean length (in months) of loans obtained by participant and non-participant cooperatives (2012–2014).

Likewise, the intervention did not make the credit accessibility process simpler and shorter; banks did not adapt their lending procedures and products. Cooperatives complained about the lengthy and cumbersome loan application and approval processes. Timeliness of loan release is critical for effective and efficient utilisation of the disbursed loans, particularly for cooperatives whose credit need is highly related to crop harvest season. Cooperative records show that in most cases approval and disbursement of guaranteed loans took up to three or four months. This calls for negotiations with the partner banks to relax some of their lending requirements if such guaranteed loans have to be accessed in a timely manner and effectively used by the cooperatives. One of the positive outcomes is that borrower cooperatives were able to demonstrate their credit worthiness to the banks, as well as learning banks’ lending procedures and requirements.

In terms of collateral requirement, being a cooperative bank, the participating bank did not require additional collateral apart from the 50% risk-sharing coverage. This particular bank rather asks for an expression of commitment and support from the cooperative promotion agency. Other commercial banks indicated that they would ask the borrower cooperatives to cover the remaining 50% risk. Likewise, the scheme had little or no impact on reducing interest rates. The 12% and 14% interest rates charged on short- and medium-term guaranteed loans, respectively, were viewed as high rate among the borrower cooperatives. This contrasts with the literature on international experiences (e.g. Gudger Citation1998) which claims that provision of a credit guarantee can lead to reduced lending rates. This implies that in addition to loan security, other important factors were also in play that constrain banks’ lending activities to the cooperative sector.

Default and claims repayment

When this research was undertaken, no loan was declared as default by the lending banks. None of the borrower cooperatives failed to repay the full amount within the loan due period, though five cooperatives (35%) had delayed payment of instalments for reasons such as problems related to the coffee market. Out of the 18.4 million Birr disbursed by the partner bank over the first three years, about 14.5 million Birr of the principal and 400,000 Birr of the interest were recovered from the borrower cooperatives. It is important to note that some of the disbursed loans had not completed their full maturity period by the time this study took place, which calls for further analysis at a later stage. Thus, it was not possible to assess the default rate and the ease of claim repayments in the event of default. However, interviewed bank officers were of the opinion that though it has not been practically tested, the pre-requisites and claims procedures outlined in the guarantee agreement appear to be relevant and acceptable.

Were there signs of moral hazard?

One of the possible effects of a credit guarantee is the incidence of moral hazard, which arises when the presence of a loan guarantee induces reluctanceFootnote14 among the lending banks or borrower firms. The stringent regulatory framework seems to help in minimising possibilities of moral hazard among the lending banks as they are expected to follow standard lending procedures and requirements. Commercial banks need to comply with the regulation of the National Bank by keeping their non-performing loan portfolio under 5%. However, some attempts at loan fund misappropriation and reluctance to repay loan instalments were noticed among the managements of some borrower cooperatives. Hansen et al. (Citation2012) note that if borrowers perceive a guaranteed loan as a development aid, they may exhibit some reluctance in loan repayment. Thus, such donor-funded guaranteed loans need proper follow up and supervision of loan utilisation and recovery.

In addition, we noticed some sort of loan diversion practices among two cooperatives whereby they had tried to use the short-term working capital loanFootnote15 for building warehouses, to acquire a power generator, or to carry out other trade activities such as khat. Generally, cooperatives had shown better performance in terms of proper loan utilisation and repayment in districts with strong support and follow up from the cooperative promoting agency.Footnote16 The finding suggests the need for stepping up efforts to convince lending banks to improve the supply of long-term loans to avoid the diversion of short-term working capital loans to long-term investment.

Conclusion and implications

Most of the design features of the scheme are in line with international practices. However, its operation had some drawbacks which affected its up-take and utilisation among the lending banks. Though it had limited outreach, the guarantee scheme generated substantial loan additionality whereby cooperatives that were credit constrained got access to bank loans. Integration of capacity building and technical support for the lending banks and borrower cooperatives was identified as one of the merits of the scheme. However, the scheme had limited influence on the lending banks’ behaviour and practices to adapt and/or relax their lending approaches, loan terms, and products. Given the prevailing liquidity problem and presence of high loan demand from other sectors, most commercial banks appeared to be reluctant to participate in the guaranteed lending activities with 50% risk-sharing. Thus, the risk coverage level for such borrower groups may be slightly raised to about 60–70%, at least in the early stage, which could be gradually revised downwards. Relying on a single lending bank had its own limitations; thus, where possible, it would be important to involve more than one bank as this stimulates competitive behaviour among lending banks. Though the level of guarantee/risk fee (1.5%) is in line with international practices, it may still act as a disincentive to the lending banks under such short-term schemes targeting rural-based farmer cooperatives. Therefore, the risk fee on such donor-funded schemes targeting such marginalised groups may need to be further reduced and charged on guaranteed loans. The effective lending period of the scheme was considered too short, especially among the lending banks. Future schemes have to be of a longer-term arrangement of at least 7–10 years, with a fairly large guarantee fund, to generate meaningful impacts.

Both internal and external factors had affected the effectiveness of the guarantee scheme targeting farmer cooperatives. In this regard, weak business and financial management capacity of cooperatives limited their effective uptake and utilization of the guaranteed loans. This underscores the need to support primary cooperatives to build such capacities, which may involve acquiring professional managers and finance personnel. Supporting cooperatives in accessing attractive and reliable markets could also help in substantially improving access to loan finance and its repayment. Moreover, if such rural-based farmers’ cooperatives have to have easy and timely access to suitable loan products, the participating banks need to revisit and improve their lending terms and requirements. In this regard, identifying and integrating other attractive financial and non-financial incentive packages may motivate the lending banks. In view of their nature and the social and economic benefits they render to the farming community, farmers cooperatives may need to be treated differently in accessing financial resources. This requires creating favourable policy and regulatory environments that would enable banks to effectively reach out to smallholders’ cooperatives with suitable loan products. This may include policy measures that enforce mandatory lending of a certain proportion of banks’ loan portfolios to such marginalised groups, including cooperatives and small-scale agriculture.

Acknowledgements

This article forms part of a PhD study at the University of South Africa, which was based on a CABI-led project titled “Sustainable Credit Guarantee Scheme to Promote Scaling up/out of Enhanced Coffee Processing Practices (Ethiopia and Rwanda)”. The study was financially supported by the Common Fund for Commodities with co-financing from Rabo Bank. We thank all the respondent farmers, cooperative managers, extension staff, and other stakeholders who participated in the key informant interviews, focus group discussions, and surveys. We would also like to thank all the experts who served as enumerators for the survey data collection.

Disclosure statement

No potential conflict of interest was reported by the authors.

Data availability statement

The data that support the findings of this study form part of a larger research project and are available on request from the corresponding author, Dr Negussie E. Gurmessa. The data are not publicly available due to restrictions related to information that could compromise the privacy of research participants.

Additional information

Funding

Notes on contributors

Negussie Efa Gurmessa

Dr Negussie Efa Gurmessa works as Scientific officer and Progammes Manager with CABI. He manages and implements projects in Ethiopia and other African countries. Previously he was a Researcher at the Ethiopian Institute of Agricultural research.

Dr Catherine Ndinda is a Research Director, Human and Social Capabilities, Human Science Research Council, South Africa.

Dr Charles Agwanda is Senior Scientist and Coordinator of Commodities with CABI Africa. Previously he worked as Senior Researcher at the Coffee Research Institute of Kenya.

Dr Morris Akiri is a Senior Regional Director for CABI’s Regional Centre in Africa, Nairobi, Kenya.

Notes

1 Including farm inputs, credit, extension/education, and marketing of members’ produce.

2 Both short-term working capital (for seasonal coffee purchase) and long-term loans to finance coffee processing facilities.

3 Rabo Bank provided technical support and training to the lending banks (on credit evaluation, risk analysis, agri and coops financing) as well as trained cooperatives on good governance and financial literacy. The Ministry of Agriculture and cooperatives promotion agency trained cooperatives management and some member farmers on improved coffee agronomy, coffee processing, quality improvement, business plan development, marketing, etc. These institutions also played an important role in monitoring and backstopping borrower cooperatives.

4 These 22 cooperatives were selected from remote and disadvantaged areas with poor infrastructure and severe credit constraints. They represent typical primary cooperatives in their districts in terms of business activities, asset ownership, and member size.

5 A credit guarantee is a financial product or promise by a guarantor that serves as a partial substitute for collateral that will be paid to the lender in the event of default (Deelen and Molenaar Citation2004).

6 Additionality is one of the primary objectives of credit guarantees, which refers to the capacity of a scheme to provide access to finance to firms which are effectively credit constrained, possibly with better terms/conditions. Additionality also refers to the long-term developmental impact of the scheme (Saadani, Arvai, and Rocha Citation2010), which is beyond the scope of the current study.

7 While the primary objective of a shareholder company is profit making, that of cooperatives is service provision and attaining common economic and social interest. In cooperatives, members make equitable contributions to the capital, and the larger share of the surplus income is distributed to members in the form of dividend on the basis of their use, and not on the basis of their investment or share ownership (Schwettmann Citation2011). Cooperatives also differ from other shareholding firms by their democratic nature, with voting rights being assigned by person rather than by size of shareholding (Ibid). Unlike other sectors or businesses, farmer cooperatives’ loan needs are highly season-sensitive, for example, they critically need loans during or immediately after harvest season to collect members’ produce.

8 Unlike the methodologies employed by other studies that focused on analysing certain aspect(s), this framework provides a comprehensive analytical framework that addresses various features and outcomes of a loan guarantee.

9 This likely reflects the fact that guarantee providers do not screen individual loans

10 Unions have started intervening by providing unusually or record high loans amount (up to 2.1 million Birr) to individual cooperatives targeted by the scheme. Possible reasons include: fear of loss of control over the cooperatives participating in the scheme; the improved capacity, processing facility, and coffee quality has made these cooperatives attractive.

11 This refers to a ratio that is obtained by dividing the guaranteed loans extended to borrowers by the guarantee fund.

12 These may include lowering interest rates, easing collateral requirements, improving loan duration, or offering new products (Hansen et al. Citation2012).

13 Banks tend to consider such loans as very risky ventures in the absence of adequate collateral.

14 Reluctance in properly screening loan applications and following up loan utilisation and recovery, as well as deliberate default among the borrowers.

15 This refers to a loan provided to enable cooperatives to collect members’ coffee during a particular season.

16 This refers to a government body that regulates, promotes, and supports cooperatives' development.

References

- Beck, T., L. Klapper, and C. Mendoza. 2010. “The Typology of Partial Credit Guarantee Funds Around the World.” Journal of Financial Stability 6 (2010): 10–25.

- Chanyalew, D. 2015. Ethiopia’s Indigenous Policy and Growth: Agriculture, Pastoral and Rural Development. Addis Ababa, Ethiopia. P. 892.

- Cowling, M., and P. Mitchell. 2003. “Is the Small Firms Loan Guarantee Scheme Hazardous for Banks or Helpful to Small Business?” Small Business Economics 21: 63–71.

- Creswell, J. W. 1998. Qualitative Inquiry and Research Design: Choosing among Five Traditions. Thousand Oaks, CA: Sage.

- Deelen, L., and K. Molenaar. 2004. Guarantee Funds for Small Enterprises. A Manual for Guarantee Fund Managers. Geneva: International Labour Organisation.

- D’ignazio, A., and C. Menon. 2013. The Causal Effect of Credit Guarantees for SMEs: Evidence From Italy. Banca D’Italia Eurosistema. Working paper, Number 900. February 2013.

- Emana, B. 2009. Cooperatives: A Path to Economic and Social Empowerment in Ethiopia. COOP-Africa Working Paper No. 9. ILO, 2009.

- Federal Cooperative Agency (FCA). 2019. Annual Bulletin of the Federal Cooperative Agency of Ethiopia. June 2013.

- Freedman, P. L. 2004. Designing Loan Guarantee Schemes to Spur Growth in Developing Countries. DC, Washington: US Agency for International Development.

- Green, A. 2003. Credit Guarantee Schemes for Small Enterprises: An Effective Instrument to Promote Private Sector-Led Growth? SME Working Paper Series No 10. UNIDO.

- Gudger, M. 1998. Credit Guarantee: An Assessment of the State of Knowledge and New Avenues of Gesearch, FAO Agricultural Services Bulletin 129, 1998.

- Hansen, A., C. Kimeria, B. Ndirangu, N. Oshry, and J. Wendle. 2012. Assessing Credit Guarantee Schemes for SNE Finance in Africa. Evidence from Ghana, Kenya, South Africa & Tanzania. Agence Francaise de Development. Working Paper 123. April, 2012.

- International Trade Centre (ITC). 2011. MicroFinance in East Africa. Schemes for Women in The Coffee Sector. Technical Paper. ITC, 2011. No. SC-11-195, E. 33 pages.

- Kang, J., and A. Heshmati. 2008. “Effect of Credit Guarantee Policy on Survival and Performance of SMEs in Republic of Korea.” Small Business Economics 31: 445–462.

- Levitsky, J. 1997. “Credit Guarantee Schemes for SMEs – an International Review.” Small Enterprise Development 8 (2): 4–17. June 1997.

- Meyer, R., and G. Nagarajan. 1996. Evaluating Credit Guarantee Programmes in Developing Countries, Paper Presented at the Meetings of the American Agricultural Economics Association, San Antonio, TX, July.

- Mouton, J. 2001. How to Succeed in Your Master’s and Doctoral Studies. Pretoria: Van Schaik Publishers.

- Okwoche, V., B. Asogwa, and P. Obinne. 2010. Evaluation of Agricultural Credit Utilisation by Cooperative Farmers in Benue State of Nigeria. European Journal of Economics, Finance and Administrative Sciences. Issue 47, 2012. http://www.eurojournals.com/EJEFAS.htm.

- Ridding, A., J. Madill, and G. Haines. 2007. “Incrementality of SME Loan Guarantees.” Small Business Economics 29: 47–61.

- Saadani, Y., Z. Arvai, and R. Rocha. 2010. A Review of Credit Guarantee Schemes in the Middle East & North Africa Region. Financial Flagship, The World Bank. October 2010.

- Schwettmann, J. 2011. Capacity Building for Africa’s Cooperatives and Social Economy Organisations. A Contribution to the Expert Group Meeting. Cooperatives in social Development: Beyond 2012; 3–6 May, 2011, Ulaanbaatar, Mongolia.

- Tunahan, H., and A. Dizkirici. 2012. “Evaluating the Credit Guarantee Fund of Turkey as a Partial Guarantee Programme in the Light of International Practices.” International Journal of Business and Social Science 3 (10): 79–82. Special Issue – May 2012.

- Zecchini, S., and M. Ventura. 2009. “The Impact of Public Guarantees on Credit to SMEs.” Small Business Economics 32: 191–206.

- Zhang, P., and Y. Ye. 2010. “Study on the Effective Operation Models of Credit Guarantee System for Small and Medium Enterprises in China.” International Journal of Business and Management 5 (9): 99–106.

Annex – 1.

Adaptation of some basic steps proposed by Creswell (Citation1998) and Mouton (Citation2001) for qualitative data analysis

Initially the hand-written interviews conducted in Amharic were translated to English and transferred into electronic form. The researcher then printed and went through all the information several times, jotting down notes in the margins of the text. In addition, the researcher wrote the key findings in the form of memos and reflective notes as a process of initial sorting-out process.

The researcher carried out the process of reducing the data by developing codes and categories and through sorting text into categories. The categories were generated from research questions, interview guides, and responses of the interviews and group discussions. A simple template was developed to extract, sort, and categorise the information. Colour coding was used to mark and distinguish the different categories and themes emerging from the information. Then the materials from all the respondents who provided similar responses or highlighted similar themes were put into one category or theme.

Finally, the researcher went through the summarised and categorised information to see the convergence and divergences between the views of the different categories of key informants and focus groups. Finally, the various categories or themes were related and these themes and concepts were then integrated into a narrative description. This process largely involved comparing materials within categories to look for variations and similarities in meanings and comparing information across categories to discover links and relations between themes, and identifying emerging patterns.

The bulk of the materials generated through the qualitative data analysis was eventually compared against and were largely integrated into relevant sections of the findings of the quantitative data analysis. However, some of the findings of the qualitative research were separately reported on.