?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We examine the determinants and consequences of firms’ interim reporting choices in response to the gradual deregulation of quarterly reporting in the prime market segment of the Vienna Stock Exchange (VSE). Following the deregulation, only a few firms terminate quarterly reporting entirely, while most firms reduce the content of quarterly reports predominantly by omitting the notes disclosures. Our interview and empirical evidence suggest that firms primarily consider the information needs of their key stakeholders, such as institutional (foreign) investors and analysts, as well as their transparency preferences in their interim reporting decisions. Reporting and proprietary costs are less important to prime market firms. Firms that terminate quarterly reporting or substantially reduce the content of quarterly reports experience an economically significant reduction in liquidity, but not a deterioration in analyst forecast properties. Collectively, our results suggest that stakeholders demand quarterly reporting, but not necessarily full quarterly reports.

1. Introduction

One of the fundamental questions in disclosure theory is whether disclosure should be left to the firms (Stigler, Citation1964) or whether mandating and regulating disclosures is useful for capital market participants (e.g., Benston, Citation1973; Coffee, Citation1984; Easterbrook & Fischel, Citation1984). Disclosure regulation is pervasive and has been increasing in developed economies, despite regulators’ difficulty determining the socially optimal level of disclosure (Leuz & Wysocki, Citation2016). Showcasing this difficulty, regulators have struggled to reach a consensus on the frequency and content of interim reporting for decades (Kajüter et al., Citation2022). For example, the European Union (EU) introduced mandatory quarterly reports with the Transparency Directive 2004/109/EC in 2004, only to abolish the mandate in 2013 via the Transparency Directive Amending Directive (TDAD) 2013/50/EU. The TDAD represents a rare phenomenon of disclosure deregulation and a switch from a mandatory to a voluntary disclosure regime. While there is a broad literature on the consequences of disclosure regulation (see Leuz & Wysocki, Citation2016), evidence on firms’ responses to deregulation is scarce.

In this paper, we investigate the determinants and consequences of firms’ responses to the deregulation of quarterly reporting. Specifically, we examine firms’ motives for their choices of the content and frequency of interim reporting and the ensuing capital market consequences. Deregulation leaves it to firms to weigh the costs and benefits of (dis)continuing quarterly reporting as well as the content of these reports. A higher reporting frequency allows stakeholders to monitor managerial action on time, thereby disciplining managers (Gigler et al., Citation2014; Kanodia, Citation2006; Kanodia & Lee, Citation1998) and reducing agency costs (Downar et al., Citation2018). However, more frequent reporting can also lead to increased managerial short-termism (Gigler et al., Citation2014; Stein, Citation1989) and reductions in firms’ investment efficiency (Ernstberger et al., Citation2017; Fu et al., Citation2020; Kraft et al., Citation2018). Other commonly cited costs of a higher reporting frequency are increased direct reporting costs, proprietary costs, and the allegedly misleading nature of the information in a seasonal business (Leftwich et al., Citation1981). Regarding content, firms must trade off the benefits of interim reporting under a uniform reporting regime resulting in lower information asymmetry versus the benefits of catering to the specific information needs of key stakeholders at the expense of potentially higher information asymmetry (Chen et al., Citation2017).

Ex ante it is unclear how firms trade off the relative magnitudes of the various costs and benefits of the frequency and content of interim reporting. In addition, theoretical research provides little guidance on what form, quantity, and frequency of disclosure is relevant for various stakeholders and how firms weigh the information needs of different stakeholders in their reporting decisions (Leuz & Wysocki, Citation2008). This paper examines qualitatively and empirically how firms make these trade-offs following the deregulation of interim reporting.

Specifically, we use the gradual transposition of the TDAD on the prime market segment of the Vienna Stock Exchange (VSE) as our setting. Until 2015, the VSE required its prime market firms to issue full quarterly reports in compliance with International Accounting Standard (IAS) 34 Interim Financial Reporting. Then, it relaxed quarterly reporting in two steps. First, in November 2015, following the transposition of the TDAD, the VSE still mandated quarterly reports in the prime segment, but terminated the requirement to comply with IAS 34 and allowed the omission of the notes to the quarterly financial statements. Second, the VSE abolished the quarterly reporting mandate entirely in February 2019, arguing that ‘firms and investors would know best which interim reporting frequency and content suits their needs’ (Wiener Börse, Citation2019). Analyzing firms’ responses around the two deregulation events allows us to identify the importance of certain contents (i.e., notes) and format (compliance with IAS 34) versus the relevance of frequency to various stakeholders, i.e., investors and analysts.

To gain insights into firms’ internal decision processes and to inform the development of our hypotheses, we started by conducting in-depth, semi-structured interviews with firm experts. All our interviewed experts indicated that the termination of the quarterly reporting mandate was discussed among firms’ executives. Most interviewed firms considered only a reduction of the content of the quarterly reports in accordance with the information needs of key stakeholders (i.e., institutional investors and analysts), rather than the discontinuation of quarterly reporting. Generally, respondents viewed the marginal costs of quarterly reporting as low because of frequent internal reporting and integrated managerial and financial reporting. Proprietary costs were not raised as a concern. While some interviewees mentioned that for seasonal business models quarterly reporting sometimes paints a misleading picture, others noted that investors and analysts would be aware of seasonality. In contrast, the costs of a potential reduction in analyst coverage or competitiveness in capital markets were deemed more important. About half of the interviewed experts mentioned that they generally consider the reporting choices of a small set of peer firms (usually, one to three firms) in their own reporting choice. Overall, our interview evidence suggests that key stakeholders demand quarterly reporting, but not necessarily full quarterly reports.

Our descriptive analysis of firms’ quarterly reporting choices confirms the interview evidence. First, we find that following the first deregulation, 48.5 percent of firms discontinued compliance with IAS 34 by 2018. While most of the non-complying firms omitted the notes from their quarterly reports, some firms merely removed the compliance statement. Second, following the complete deregulation in 2019, only six of 35 prime market firms terminated quarterly reporting entirely. This observation is consistent with that of two prior studies (Hitz & Moritz, Citation2019; Nallareddy et al., Citation2017). However, we also observe that about half of the firms reduced the content in quarterly reports to varying degrees. Ten out of 35 firms maintained the full scope of quarterly reporting, although five firms removed the IAS 34 compliance statement. Overall, this evidence suggests that the previous ‘one-size-fits-all’ reporting requirements were not aligned with firms’ preferences.

Next, we use the insights from our interviews and empirically analyze the determinants of the heterogeneity in firms’ quarterly reporting choices. We predict and find that firms’ investor structure is associated with their quarterly reporting choices. Specifically, firms with higher inside ownership and more concentrated ownership among larger outside investors are more likely to terminate IAS 34 compliance and omit the notes (abandon quarterly reporting altogether) following the first (second) deregulation event. When these firms continue to publish quarterly reports, they significantly reduce the content as captured by our self-constructed reporting score. In contrast, we find that firms with more foreign ownership are less likely to discontinue IAS 34 compliance and abandon quarterly reporting. Taken together, our evidence is in line with the general notion that firms with private information channels to their stakeholders rely less on quarterly reporting as a monitoring tool (Leftwich et al., Citation1981).

We also find that firms with a higher (lower) information environment, measured by the number of analysts following them and bid-ask spreads, are less (more) likely to terminate quarterly reporting entirely and report more (less) content when they continue to publish quarterly reports. These findings are in line with our interview evidence that some firms maintain a strong preference for transparency to remain attractive and/or visible to analysts (Kajüter et al., Citation2022). In contrast, our empirical proxies for reporting and proprietary costs or the seasonality of business are not associated with the reduction in content or the termination of quarterly reporting.

Finally, we examine the consequences of firms’ reporting choices on their stock liquidity and analyst forecast properties. We find that the termination of IAS 34 compliance and the omission of the notes to the quarterly reports does not decrease firms’ liquidity relative to firms that continue to comply with IAS 34. This finding suggests that investors do not view notes and IAS 34 compliance statements in quarterly reports as important. Consistent with this interpretation, we find no significant abnormal returns around the announcement of the termination of the IAS 34 mandate on the VSE. However, the termination of quarterly reporting or a substantial reduction of the content in quarterly reports is associated with a significant reduction in liquidity. Accordingly, we also find economically and statistically significant negative abnormal returns around the VSE’s announcement to abolish the quarterly reporting mandate. These results suggest that a quarterly reporting frequency is important to investors. Interestingly, firms’ reporting choices around both deregulation events are not associated with a deterioration in analyst forecast properties, which is consistent with the idea that firms tailor their quarterly reporting to the specific information needs of analysts and key stakeholders.

Our paper makes two key contributions to the literature on firms’ determinants of interim reporting choices (Botosan & Harris, Citation2000; Chen et al., Citation2002; Leftwich et al., Citation1981) and on the consequences of financial reporting (de)regulation (Leuz & Wysocki, Citation2016). First, prior empirical work provides somewhat mixed evidence on a myriad of potential factors that may shape firms’ reporting frequency, including reporting and proprietary costs, the information environment, and business seasonality (Butler et al., Citation2007; Hitz & Moritz, Citation2019; Leftwich et al., Citation1981; Link, Citation2012). We combine interview and empirical evidence to show that, in the prime market segment, firms’ interim reporting choices in response to deregulation are primarily guided by the information demand of key stakeholders as well as the firm’s transparency preferences, and less by the seasonality of the business model or reporting and proprietary costs. The latter findings contrast with prior evidence showing that firms turn away from IFRS reporting (Fiechter et al., Citation2018), go dark, delist, or downlist to less regulated markets (Gutierrez et al., Citation2017; Hitz et al., Citation2020; Leuz et al., Citation2008) to avoid increased (reporting) costs of stricter reporting regulation. Unlike in these settings, the marginal costs of higher reporting frequency are relatively low, because of already established integrated reporting systems and processes.

Second, we extend the scarce evidence on the effects of the deregulation of quarterly reporting (Hitz & Moritz, Citation2019; Nallareddy et al., Citation2017) by documenting that firms’ response to the deregulation is in most cases not a binary decision to (dis)continue quarterly reporting but more nuanced. Specifically, firms weigh the information needs of their various stakeholders differently and tailor the frequency and content of their interim reports according to those needs. Collectively, our findings suggest that investors and financial analysts demand quarterly reporting to monitor managerial action in a timely manner (Gigler et al., Citation2014; Kanodia, Citation2006; Kanodia & Lee, Citation1998), but not necessarily full quarterly reporting. Regarding content, investors and financial analysts do not appear to view compliance with IAS 34 and the notes as important, but nonetheless still require financial statements and the provision of key performance indicators.

Overall, our evidence furthers our understanding of the effects of the deregulation of interim reporting by showing how firms and stakeholders weigh the importance of interim reporting frequency and content. While the findings might not be completely generalizable to other settings, they inform regulators about the trade-offs associated with the deregulation of interim reporting.

2. The Development of the Interim Reporting Environment in Austria

Firms listed on the Vienna Stock Exchange (VSE) experienced a gradual deregulation of interim reporting requirements since 2015. Before the start of the quarterly reporting deregulation, firms listed on the VSE’s Prime Market segment (prime market firms) were mandated to publish quarterly financial reports for the first and third quarters including, at a minimum, a complete set of (condensed) financial statements in accordance with IAS 34.Footnote1 In particular, interim financial reports include condensed statements of financial position, comprehensive income (or separate condensed statements of profit or loss and other comprehensive income), changes in equity, cash flows, and selected explanatory notes. The gradual deregulation of interim reporting came in two steps.

In a first step, in November 2015, the VSE continued to require prime market firms to publish quarterly reports but abandoned the requirement to prepare them in accordance with IAS 34.Footnote2 Thus, prime market firms were allowed to choose their presentation format and, unlike under IAS 34, additional notes disclosures were no longer mandatory. In a second step, in February 2019, the VSE aligned its reporting requirements to the EU Transparency Directive Amending Directive (TDAD)Footnote3 and made quarterly reporting voluntary for its prime market firms. The VSE’s decision was based on a variety of (partly conflicting) evidence on the consequences of increased reporting and disclosure regulation. A ‘one-size-fits-all’ model would not lead to overall economic and societal benefits and firms should best know which frequency and content of reporting is adequate given their individual stakeholders’ demand, operating cycles, and seasonal fluctuations (Wiener Börse AG, Citation2019). As a result, as of February 2019, prime market firms were free to choose their reporting frequency (i.e., quarterly versus semi-annual) and content (i.e., the amount of information provided in these quarterly reports). Figure summarizes the deregulation events.

Figure 1. Event timeline

3. Interviews with Firm Experts and Hypotheses Development

3.1. Interviews with Firm Experts

3.1.1. Interview setup

We first conduct a series of semi-structured interviews with 20 firm insiders of VSE prime market firms. Our interviews offer insights into firms’ interim reporting choices and help ground our predictions. We therefore support our hypotheses development in line with the grounded theory approach (Glaser & Strauss, Citation1999) and its applications in prior accounting research (Bourveau et al., Citation2022; Feller & Schanz, Citation2017).

Our interview questions allow us to get a more nuanced understanding of firms’ decision processes around the deregulation events and the involved stakeholders. First, we asked the participants whether the option to reduce or discontinue quarterly reporting was considered and discussed among executives to gauge the overall significance of the deregulation event. If participants answered in the affirmative, we proceeded to ask which arguments were weighed for and against reducing or terminating quarterly reporting. This question aimed at confirming determinants considered in prior literature (Butler et al., Citation2007; Hitz & Moritz, Citation2019; Link, Citation2012) and uncovering new determinants of firms’ quarterly reporting choices. Given the semi-structured form of our interviews, we let participants freely elaborate on this question first and then followed up with specific questions on the importance of determinants considered in prior literature. Then, we asked our participants which decision-makers within the firm were involved (such as the CEO, CFO, the accounting department, or investor relations) and if external stakeholders, such as investors or analysts, were involved in the decision-making process to get a better understanding of the parties and their interests involved in the process. We summarize our questions and additional information on the interview process in Online Appendix OA.1.

The interviewed experts are primarily leading managers of the sample firms’ accounting and investor relations departments and have several years of work experience. We invited the experts either via our networks or directly contacted the sample firms’ investor relations departments. All experts were contacted via an email that included a short factsheet containing information about the research team, the topic of the research project, and the purpose of the interview (see Online Appendix OA.2 for the translated fact sheet). In total, we contacted 35 potential experts of whom 20 agreed to participate in a phone interview that would last approximately 20 min. In total, 14 experts are employed as Head of Investor Relations, three experts were employed as Head of Group Accounting, one respondent was employed as Chief Financial Officer (CFO), one respondent was employed as Investor Relations Manager, and one respondent served as a board director in the firm. All respondents were able to answer our questions irrespective of their position in the firm and provided comprehensive insights into their decision-making process.

Overall, the firms that participated in our interviews are representative of the firm population of the VSE prime market in terms of firm characteristics and reporting behavior around the deregulation events. After the first deregulation event in 2015, five out of 20 participating firms stop IAS 34 compliance while seven out of 15 non-participating firms stop IAS 34 compliance. After the second deregulation event in 2019, three out of 20 participating (three out of 15 non-participating) firms stop quarterly reporting entirely. In terms of firm characteristics, participating firms are comparable to non-participating firms concerning their size, performance, leverage, risk, growth opportunities, and information environment.Footnote4

We conducted the interviews from June 2022 to August 2022. At the beginning of each interview, we introduced the research team and briefly explained the research study’s topic in broad terms. We also repeated that we would not ask for proprietary or sensitive information or disclose the experts’ identity or that of their employer. The interviews were recorded with the written consent of the interviewees. During the interview, a member of the research team asked questions following the interview guidelines presented in Online Appendix OA.2. The experts were allowed to elaborate on topics they considered important. Next, we present the findings and conclusions from the semi-structured interviews.

3.1.2. Importance of the deregulation of the quarterly reporting mandate and involved decision-makers

As our first introductory question, we asked all participants in our interviews whether and to what extent a potential termination or reduction of quarterly reporting was discussed among executives around the termination of the quarterly reporting mandate to gauge the practical relevance of the event. All experts pointed out that the advantages and disadvantages of discontinuation or reduction of quarterly reporting were carefully weighed among the executives of the firm and sometimes also among external decision-makers in round-table discussions and interest groups such as the Cercle Investor Relations Austria.

We then asked participants which decision-makers were involved in the discussion around a potential termination or reduction of quarterly reporting. All our respondents pointed out that group accounting, investor relations, and the CFO were involved in the decision-making process. Ten respondents answered that the CEO was involved in the decision and three pointed out that the board of directors was involved in the decision as well. Overall, the deregulation of the quarterly reporting mandate was of high importance to firms.

3.1.3. Determinants of reporting choice

We asked participants which factors were weighed for and against terminating quarterly reporting during the discussions. This question aimed at confirming determinants considered in prior literature and uncovering new determinants of firms’ quarterly reporting choices. In the following, we summarize the interview evidence along four major sets of quarterly reporting determinants we identified: (i) the information needs of specific users of quarterly reports, (ii) the reporting choices of peer firms, (iii) reporting costs and internal reporting systems, and (iv) the firm’s business model. In Appendix A we provide selected quotes from our interviews. In Online Appendix OA.3 we provide additional anecdotal evidence retrieved from public sources.

Information needs of specific users of quarterly reports. Firms may adapt their quarterly reporting to the information needs of key users of financial statements such as analysts or certain investor groups (Chen et al., Citation2017) allowing outsiders to monitor management (Gigler et al., Citation2014; Kanodia, Citation2006; Kanodia & Lee, Citation1998; Leftwich et al., Citation1981). In total, 14 of 20 participants responded that they either actively engaged with their largest investors and analysts to get feedback on their quarterly information needs or are very well informed about those information needs because of their continuous informal exchange (e.g., through conference calls or road shows). The large consensus among the interviewees is that they consider institutional investors and analysts as the primary users of quarterly reports and their information demand largely boils down to the financial statements and a short update on the development of the fiscal quarter. Two respondents answered that they also considered the information needs of their debt investors to meet the specific needs of a growing debt investor base. Two other respondents considered also international investors who would be irritated by a lack of quarterly financial information. Interestingly, no respondent considered small, retail investors as the primary users of quarterly reports.

Reporting choices of peer firms. Firms’ reporting choices are potentially guided by the reporting choices of their competitors and peers (Botosan & Harris, Citation2000). In total, twelve respondents concluded that they generally consider the reporting choices of a small set of peer firms (usually one to three firms) in their own reporting choice. The main aim is to remain comparable in reporting and meet the transparency of competitors to attract investors and analyst coverage. While some respondents coordinated within informal working groups (e.g., Cercle of Investor Relations Austria) or actively engaged with their peer firms on potential reporting choices, others generally follow the reporting of their peers.

Reporting costs and internal reporting systems. Firms are potentially inclined to abandon or reduce quarterly reporting if the costs outweigh the benefits (Butler et al., Citation2007; Hitz & Moritz, Citation2019; Nallareddy et al., Citation2017; Rahman et al., Citation2007). In total, two representatives of smaller firms out of all firm representatives considered costs to prepare and disseminate quarterly reports including the commitment of internal resources as a significant factor in their quarterly reporting choice. They explicitly mentioned the time needed to prepare the notes to the quarterly financial statements as a significant cost factor. All other respondents considered the costs of quarterly reporting as negligible mainly because the necessary reporting systems have already been implemented and they already produce quarterly (or even monthly) financial reports for internal control, management reporting, and board meetings. Accordingly, quarterly reporting processes are optimized and significantly reduce marginal costs to report information to external stakeholders, especially when firms run fully integrated reporting systems and align management reporting with IFRS. Three interviewees mentioned that quarterly reporting can have positive training, monitoring, and disciplining effects within the group resulting in less time and resources needed to prepare the annual report at year-end.

Sales volatility and seasonal business models. Quarterly reporting can potentially mislead investors if firms are subject to a seasonal business model and fluctuations in sales during the year (Leftwich et al., Citation1981). Firms may therefore abandon or reduce quarterly reporting to communicate a more consistent picture of their business model on an annual or semi-annual basis. In total, two of 20 experts pointed out that a seasonal business model including volatility in sales during the fiscal year is difficult to communicate on a quarterly basis and was a primary reason for reducing or abandoning their quarterly reporting. Other participants pointed out that the communication of a seasonal business model with volatile sales can be difficult to communicate every quarter but usually their investors and analysts are aware of seasonality.

3.1.4. Summary

Overall, the participants in our interviews concluded that a termination of quarterly reporting is not a viable reporting option mainly because large institutional investors and analysts demand at least a limited set of key performance metrics each quarter. The quarterly reporting choice of prime market firms is therefore in most cases not a binary decision but instead a question of the extent to which quarterly reporting can be condensed while meeting the information demand of its key users. To learn about the specific information demand of their key users, our interview evidence suggests that firms either actively engaged with their larger investors and analysts or already had a very good understanding of their information needs allowing them to make a conscious reporting decision. In contrast, direct reporting costs are not a primary factor in the quarterly reporting choice. Overall, most participants expressed their appreciation to be able to adjust quarterly reporting to their stakeholders’ information needs and they had the impression that their stakeholders were content with their choice.

3.2. Hypotheses Development

Our interview evidence collectively suggests that firms’ quarterly reporting choice is primarily guided by the information needs of their key stakeholders such as analysts and large investors as well as firms’ transparency preferences. We therefore focus our hypotheses development for our empirical investigation on the determinants for which we can provide clear predictions based on our interview evidence and prior literature while controlling for other factors such as reporting costs and seasonality.

3.2.1. Investor structure

We first posit that inside ownership is positively associated with firms’ choice to terminate or reduce quarterly reporting. In contrast to outside shareholders, insiders rely less on public information channels, such as financial reporting, to evaluate the expected future performance of the firm and to monitor managerial action (Jensen & Meckling, Citation1976; Leftwich et al., Citation1981). Hence, the demand for timely quarterly reports should decrease in firms’ share of inside ownership in line with prior evidence that firms with higher inside ownership (institutional outside ownership) provide less (more) voluntary disclosure (Boone & White, Citation2015; Eng & Mak, Citation2003; Ruland et al., Citation1990).

Along these lines, we also expect firms to terminate or reduce quarterly reporting when their outside ownership is concentrated in a few block holders. Block holders have easier access to managers facilitating private information acquisition and reducing firms’ incentives to disclose information voluntarily via formal information channels (Ge et al., Citation2021). Hence, firms with block holders have higher incentives to terminate or adapt their quarterly reports to the specific information needs of their large key investors. Our interview evidence suggests that the demand for quarterly financial information by large investors and analysts is often limited to financial statement information and a few key performance metrics allowing them to update their valuation models.

Overall, firms with more inside ownership and concentrated outside ownership depend less on public information channels to disseminate timely and value relevant financial information and realize fewer benefits from extensive quarterly reporting relative to firms with less inside ownership (concentrated outside ownership). We therefore conjecture that:

H1a: Inside ownership and the concentration of outside ownership is positively (negatively) associated with firms’ propensity to terminate quarterly reporting entirely (firms’ quarterly reporting content).

H1b: Foreign ownership is negatively (positively) associated with firms’ propensity to terminate quarterly reporting entirely (firms’ quarterly reporting content).

3.2.2. Information environment

A high-quality information environment via a high analyst coverage is associated with increased liquidity in the firm’s stock (Roulstone, Citation2003), lower cost of raising equity capital (Bowen et al., Citation2008), and ultimately creates value for firms (Li & You, Citation2015). Analysts’ interest in and willingness to cover a firm, in turn, depends on the quality and quantity of financial disclosures (Anantharaman & Zhang, Citation2011; Arya & Mittendorf, Citation2007; Bushee & Miller, Citation2012; Healy et al., Citation1999; Lang & Lundholm, Citation1996; Mittendorf & Zhang, Citation2005). Managers therefore have the incentive to create a high-quality information environment to attract and maintain analyst coverage, i.e., via timely quarterly reports. Most of the experts in our interviews expected a potential loss in analyst coverage when terminating quarterly reporting resulting in implicit costs that would outweigh the benefits of cost savings from less frequent reporting. Thus, transparent firms that exhibit a high information environment face relatively higher implicit costs to reduce or terminate quarterly reporting relative to less transparent firms.

Our interview evidence also suggests that some firms have an explicit preference to be transparent toward their stakeholders. For instance, one interviewee stated that ‘we wanted to continue quarterly reporting to remain transparent’ while another respondent answered that ‘we always had the ambition to report very transparently and did not want to reduce the information [in quarterly reports].’ Another firm expert said that ‘we also see ourselves as an interesting company for international investors. So, we decided to keep our quarterly reporting to live up to the expectations of international capital markets and to avoid being asked why we are less transparent.’ Thus, firms with a high (low) information environment and strong (weak) reporting preferences may choose to continue (reduce) quarterly reporting:

H2: Firms’ information environment is negatively (positively) associated with firms’ propensity to terminate quarterly reporting entirely (firms’ quarterly reporting content).

4. Research Design

4.1. Data and Sample

Our starting sample contains 38 firms listed in the prime segment of the VSE at the time of data retrieval and spans the period from 2016 to 2021. We exclude three firms that were added to the Prime Segment in 2019 to ensure data coverage for the whole sample period and one firm that was delisted in 2019 to avoid the delisting affecting the firm’s reporting choices and subsequently our results.Footnote5 We exclude another two firm-year observations for missing financial data. As a result, we obtain in total 208 firm-year observations to test 35 prime market firms’ reporting choices which we hand-collected from quarterly reports. We retrieved all other data from Thomson Reuters Datastream and S&P Capital IQ. Table summarizes the steps of our sample selection.

Table 1. Sample selection

4.2. Research Design

We analyze the determinants of VSE prime market firms’ quarterly reporting choices in response to the two deregulation events. Based on our interview evidence and the hypotheses development, we estimate the following linear probability model to analyze the determinants of firms’ reporting choicesFootnote6:

(1)

(1)

where

is one of the following binary (categorical) variables for firm

in year

.Footnote7 First, we analyze the determinants of firms’ choice to stop IAS 34 compliance and to omit the notes to quarterly statements after the first deregulation event from 2016 to 2018. We therefore use the variable

that equals one for firm-years in which the firm is not IAS 34 compliant, and zero otherwise. Second, to examine firms’ decision to terminate quarterly reporting in response to the abolishment of the mandate in February 2019, we use the variable

that equals one for firm-years in which the firm does not issue quarterly reports, and zero otherwise. Third, we analyze the content of firms’ quarterly reporting, that is, the items that are included in their quarterly reports. We therefore replace

with the categorical disclosure score

that ranges from zero (representing the lowest level of transparency) to four (representing the highest level of transparency). We assign a score of zero when only a presentation or press release is published; a score of one to quarterly reports that include a management report and a condensed or summarized set of financial statements; a score of two to quarterly reports that include a complete set of financial statements (full or condensed); a score of three to quarterly reports that include a management report plus complete set of financial statements (full or condensed); a score of four to quarterly reports that include a management report, a complete set of financial statements (full or condensed) and the notes.

To test our formal predictions around the determinants of firms’ quarterly reporting choices (H1-H2), we include the following test variables in the vector . First, to test whether firms’ ownership structure is associated with their quarterly reporting choice (H1), we include the percentage of closely-held shares (

) to capture inside ownership (H1a).Footnote8 We expect the coefficient on

to be positive (negative) and statistically significant if inside ownership is associated with a higher propensity to terminate IAS 34 compliance or abandon quarterly reporting entirely (with a lower quarterly

score). We also include the percentage of shares held by foreign shareholders among the 100 largest publicly disclosed shareholders (

) to test the association between foreign investor holdings and firms’ quarterly reporting choices (H1b). We expect the coefficient on

to be negative (positive) and statistically significant if foreign ownership is associated with a lower propensity to terminate IAS 34 compliance or the termination of quarterly reporting (with the quarterly

score).

Next, to test whether a firm’s preference for a certain information environment is associated with its quarterly reporting choice (H2), we include analyst following (). If analyst following is associated with a lower propensity to terminate quarterly reporting (a higher quarterly

score), we expect the coefficient on

to be negative (positive) and statistically significant. In addition, we include the natural logarithm of firms’ average yearly bid-ask spread (

) as a catch-all proxy for firms’ information environment. While we use

also as an outcome variable in section 6, we argue that lagged yearly

, on average, captures firms’ preference for a certain level of transparency. This claim is supported by its strong positive correlation with closely-held shares (

) and ownership concentration (

) versus its strong negative correlation with foreign held shares (

) and analyst following (

) (see Panel B of Table OA.5 in the Online Appendix). We expect the coefficient on

to be positively associated with both

and

.

When we use the reporting score () as the dependent variable in equation Equation(1)

(1)

(1) , we expect it to be negatively associated with

,

,

, but positively with

and

.

We additionally control for various economic factors that potentially affect firms’ quarterly reporting choices. First, we include firms’ size () as larger firms can spread fixed reporting costs across a larger asset base to exploit scale effects. One of our interviewees for example stated that ‘we always interpreted the abolishment of the quarterly reporting mandate as a simplification for smaller caps in the market.’ Second, we include firms’ within-year sales volatility (

) to test whether a firm’s seasonal business model is associated with their quarterly reporting choice. Our interviews provide somewhat conflicting statements on seasonality. On the one hand, experts noted that quarterly reporting might mislead investors and that they ‘prefer to review and analyze the earnings […] over a longer period than each quarter’ (CEO, Kapsch TrafficCom, Kapsch TrafficCom Highlights Report Q1 2019/20). On the other hand, other experts indicated that their stakeholders were aware of the seasonality.

Third, we include return on assets () to capture proprietary costs (Fiechter et al., Citation2018) and its standard deviation over the last three years (

) to proxy for performance risk. We include firms’ leverage (

) since some interview experts noted that debt investors scrutinize quarterly reports. Lastly, we include Tobin’s Q (

) to capture firms’ growth opportunities for which we expect a negative relation with firms’ decision to reduce the content and frequency of quarterly reporting (Rahman et al., Citation2007).Footnote9 We lag all financial variables by one year as firms base their reporting and compliance choices on available data (e.g., Hitz & Moritz, Citation2019; Link, Citation2012). To ease the interpretation of the linear probability results, we standardize continuous variables to have zero mean and a standard deviation of one. We cluster standard errors at the firm level. We report a detailed description of all variables used in Appendix B and report descriptive statistics of the variables in Table .

Table 2. Descriptive statistics

5. Results

5.1. Descriptive Evidence on Prime Market Firms’ Quarterly Reporting Choices

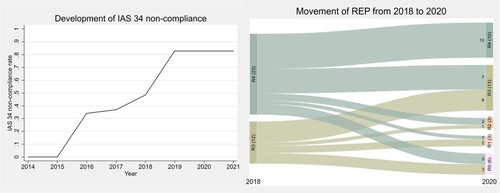

The left panel of Figure shows that following the first deregulation, the share of firms stopping compliance with IAS 34 quickly increases over time (IASNC). By 2018, 17 out of 35 firms stop compliance with IAS 34. Twelve of these firms omit the notes to their quarterly reports, while the other five firms merely remove the compliance statement. In 2019, when quarterly reporting becomes voluntary, compliance with IAS 34 drops to only 17 percent (6 out of 35 firms).

Figure 2. Changes in prime market firms’ reporting choices. Note: This figure shows the development of the average sample firms' IAS 34 non-compliance (IASNC) over the sample period (left) and the movement of firms' quarterly reporting score (REP) from 2018 to 2020 around the second deregulation event. R0 to R4 indicate a quarterly reporting score (REP) from zero to four, respectively.

The right panel of Figure shows the development of the reporting score (REP) from 2018 to 2020 around the second deregulation event. In 2018, 23 out of 35 firms provided full quarterly reports including notes (REP = 4). The remaining twelve firms omitted the notes from the quarterly reports (REP = 3). By 2020, the number of firms providing full quarterly reports including notes reduced to ten firms (28.5%). 13 firms provide quarterly reports without notes (REP = 3), seven (six) of which previously exhibited a reporting score of 4 (3). Three firms published only a complete set of financial statements ( = 2) as of 2020, two (one) of which previously exhibited a reporting score of 4 (3). Three firms published a management report including a condensed or summarized version of their financial statements (

= 1) as of 2020, one (two) of which previously exhibited a reporting score of 4 (3). Six firms published only a press release, presentation, or summary of results (

= 0), three (three) of which previously exhibited a reporting score of 4 (3). Collectively, no firm increased its level of transparency from 2018 to 2020, and, about half of the firms (16 out of 35) maintained their level of transparency. 19 out of 35 firms reduced their reporting score by at least 1 point. Eleven firms reduced their reporting score by at least two points. Seven firms reduced their reporting score by at least three points. Three firms reduced their reporting score by 4 points.

Overall, our descriptive evidence suggests that the interim reporting choice is not a binary choice of reporting frequency but entails a larger spectrum of reporting decisions regarding the contents of quarterly reports.Footnote10

5.2. Termination of IAS 34 Compliance and Reduction of Quarterly Reporting Content

Table presents the results on the determinants of IASNC, which captures non-compliance with IAS 34 and the omission of the notes. The sample period starts in 2016, the year after the first deregulation in November 2015, and ends in 2018, the year before the abandonment of the quarterly reporting mandate in February 2019. In column 1, we report the results for the baseline regression model without the test variables. In columns 2–8, we then include our test variables individually. In columns 9 and 10, we include the test variables jointly, except for BIDASK because it serves as a catch-all proxy capturing the combined effect of all other test variables.

Table 3. Determinants of IAS 34 non-compliance

Interestingly, most of the control variables do not enter any of the ten specifications significantly. The mostly insignificant results for SIZE and ROA suggest that reporting and proprietary costs are not a driving factor behind non-compliance consistent with the interview evidence. SALESVOL is consistently negative and significant across all specifications, suggesting that, following the first deregulation, firms with more seasonal business models were less likely to discontinue IAS 34 compliance and to omit the notes to the quarterly reports. LEVERAGE is also consistently negative and significant in five out of ten specifications, possibly indicating that debt holders request full quarterly reports as indicated by some interview experts.

Turning to our test variables, we find that inside and concentrated outside ownership is positively associated with the discontinuation of compliance with IAS 34 or the omission of the notes to quarterly reporting. Specifically, the coefficients on CLHELD are positive and significant in columns 2 and 9. Similarly, the coefficients on OWNCON are positive, but only significant in the joint estimation in column 10. In contrast, the share of foreign-held shares (FORHELD) is consistently negative and significant. These findings are in line with our hypotheses H1a and H1b and with our interview evidence, suggesting that investor structure is an important driver of firms’ quarterly reporting decisions.

While analyst coverage (ANFOL) does not enter the analyses significantly, the coefficients on BIDASK in columns 7 and 8 are positive and significant, consistent with H2 that firms with a preference for less (more) transparency are more (less) likely to stop complying with IAS 34 and to omit the notes to the quarterly report.

5.3. Termination of Quarterly Reporting

Next, we present results on the determinants of prime market firms’ reporting choices after the second deregulation event, i.e., the abolishment of the quarterly reporting mandate in the VSE prime market in 2019. In Table , we report the same specifications as in Table , but use as the dependent variable. We observe that all our test variables are highly statistically significant and exhibit the predicted signs. Consistent with H1a and H1b, firms with more inside ownership and concentrated outside ownership are more likely to terminate quarterly reporting, while firms with more foreign ownership have a lower propensity to discontinue quarterly reporting. For example, the coefficient estimates in column 10 imply that a one standard deviation increase in outside ownership concentration (foreign-held shares) increases (decreases) the likelihood of quarterly reporting termination by 14.7 (14.6) percent. These results are consistent with those in Table and suggest that the investor structure and the corresponding information demand shape firms’ quarterly reporting choices. Firms that can use more informal private information channels are more likely to terminate quarterly reporting, while firms that compete more in international capital markets choose to provide timely financial information via quarterly reports. These results support the interview evidence.

Table 4. Determinants of quarterly reporting termination

Consistent with H2, the coefficient on ANFOL is negative and significant in line with the interview evidence suggesting that analysts demand quarterly reporting in some form. In economic terms, a one standard deviation increase in analyst following reduces the likelihood of quarterly reporting termination by 18–20 percent. Finally, the coefficient on is positive and statistically significant at the 1%-level. The economic significance is also large. Specifically, for a one standard deviation increase in

, the likelihood of terminating quarterly reporting increases by about 23–31 percent. Taken together, the results provide some evidence that firms’ preferences for a certain level of transparency also affect their quarterly reporting choice in line with hypothesis H2.

5.4. Content of Quarterly Reporting

In Table , we present the results for the quarterly reporting score as the dependent variable estimating the same specifications as in Tables and . For this analysis, we use the full sample period from 2016 to 2021. However, results are qualitatively similar when we restrict the sample to 2019–2021 only (see Table OA.7 in the Online Appendix). As in the analyses before, most of the control variables do not enter significantly in Table . However, the coefficients on sales volatility (

) and performance risk (

) are positive and statistically significant across almost all specifications. While we do not provide formal predictions on the coefficient’s direction of

due to partly mixed evidence from our interviews, the results suggest that the key stakeholders of firms with more seasonal sales and higher earnings volatility demand more quarterly reporting information. This contrasts, for example, with the decision of Kapsch TrafficCom AG to terminate quarterly reporting because the short-term fluctuations in sales and earnings are arguably not well representing the company’s project business. Economically, our results suggest that a one standard deviation increase in

(

) is associated with approximately a 0.38–0.43 (0.11–0.19) increase in the

score on average. The coefficient on

is consistently positive, but significant in only two out of ten specifications. This is in line with one of the interview responses, i.e., ‘it's our debt investors that have an increased demand for detailed quarterly reports.’

Table 5. Determinants of quarterly reporting content

Turning to our test variables, we find support in line with H1a that inside and concentrated outside ownership are associated with lower reporting scores, i.e., less content in quarterly reports. Specifically, the coefficients on and

are negative and significant, when included individually (columns 2 and 3). In contrast, we only find weak support for H1b that foreign investor holdings determine firms’ quarterly reporting content. The coefficient on

is statistically significant only in the joint specification in column 10.

Finally, our variables capturing firms’ information environment are strongly associated with the content of quarterly reporting. Specifically, the coefficient on is positive and statistically significant at the 1%-level providing support for H2. On average, a one standard deviation increase in analyst following is associated with a 0.36–0.46 higher reporting score. In contrast, BIDASK is strongly negatively associated with the content of quarterly reporting. In economic terms, a one standard deviation increase in bid-ask spreads is associated with a 0.47–0.55 decrease in the reporting score. Overall, our results in Table suggest that firms’ preference for transparency shapes the level of information that is provided in quarterly reports.

6. Consequences of Quarterly Reporting Choices

6.1. Effects on Liquidity

We also examine the liquidity effects of the deregulation of quarterly reporting. We examine VSE prime market firms’ liquidity effects conditional on their choice to stop compliance or terminate quarterly reporting entirely. Ex ante, it is unclear how a change in the reporting content and frequency affects information asymmetry and firms’ share liquidity (Fu et al., Citation2012). On the one hand, theory suggests that more disclosure levels the playing field for sophisticated and unsophisticated investors (Diamond, Citation1985; Diamond & Verrecchia, Citation1991) resulting in less information asymmetry. On the other hand, a higher reporting frequency can provide incentives for sophisticated investors to acquire and benefit from private information acquisition in anticipation of forthcoming disclosures increasing information asymmetry between informed and uninformed investors (Demski & Feltham, Citation1994; Kim & Verrecchia, Citation1991; Cuijpers and Peek, Citation2010).

Our interview evidence suggests that firms tailor their quarterly reporting to the specific needs of a subset of large investors and analysts, potentially providing these stakeholders with an information advantage. In addition, some interview respondents did not view small retail investors as users of quarterly reports. Therefore, the reduction in the content of quarterly reporting or its termination may disadvantage less-informed investors, which should manifest in lower liquidity. The gradual deregulation of quarterly reporting allows us to gain insights into the relative importance of (some of) the components of quarterly reports to investors. For example, since in most cases following the first deregulation non-compliance with IAS 34 resulted in the omission of the notes only, our liquidity analyses allow us to disentangle the relative importance of the notes to investors.

We compare the liquidity effects of VSE prime market firms that continue to comply with IAS 34 or continue their quarterly reporting (control firms) with VSE prime market firms that discontinue their IAS 34 compliance or terminate quarterly reporting entirely (treatment firms) (first difference) around both deregulation events (second difference). We regress multiple liquidity measures on an indicator variable that equals one for firm-year observations in which firms discontinue compliance with IAS 34 (or terminate their quarterly reporting), and zero otherwise. We include firm-fixed and year-fixed effects turning our model into a generalized differences-in-differences estimation. We expect the coefficient on

to be positive and statistically significant if firms that discontinue compliance with IAS 34 (quarterly reporting) experience lower liquidity relative to firms that continue IAS 34 compliance (quarterly reporting). We also include lagged firm size

, lagged return volatility (RETURNVOL), lagged share turnover

and the inverse share price (

SHAREPRICE) in line with prior research (e.g., Bischof & Daske, Citation2013). We also include the predicted inverse mills ratio from estimating the full determinants model to account for the endogeneity of firms’ decision to discontinue IAS 34 compliance (or quarterly reporting).Footnote11 We cluster standard errors at the firm level.

We report results for liquidity effects in Table . The dependent variable is the natural logarithm of firms’ yearly average bid-ask spread () in column 1, the fraction of zero return days out of all potential trading days within the year in column 2 (

), the yearly average of the Amihud (Citation2002) illiquidity measure (i.e., daily absolute stock return divided by EUR trading volume) in column 3 (

), and a liquidity factor extracted from the previous three liquidity proxies (

) (Daske et al., Citation2008).Footnote12 Panel A shows the results for firms’ choice to discontinue compliance with IAS 34 and omit the notes.Footnote13 The insignificant coefficients on TERM for all four liquidity proxies suggest that firms’ discontinuation of IAS 34 compliance does not affect information asymmetry and liquidity. This also implies that investors, on average, do not view the notes to quarterly reports as particularly important.

Table 6. Liquidity effects of VSE prime market firms’ reporting choices

Panel B reports the results for the liquidity effects of the termination of quarterly reporting following the second deregulation. The coefficient on TERM is positive across all four specifications and statistically significant when using the logarithm of average yearly bid-ask spreads (BIDASK) (p-value < 5%), zero return days (ZERORET) (p-value < 1%), and the liquidity factor (LIQFACTOR) (p-value < 1%) as dependent variables. In economic terms, firms’ termination of quarterly reporting results in a 10.2 percent increase in bid-ask spreads and a 2.7 percentage points increase in zero return days. Because there are only six firms that terminate quarterly reporting entirely, in Panel C, we code TERM equal to one for firm-year observations in which firms reduce the reporting score by at least three points (seven firms). The results are qualitatively comparable to those reported in Panel B.

Taken together, our results in Panels B and C of Table suggest that firms that discontinue or significantly reduce the contents of their quarterly reporting exhibit lower liquidity and thereby higher information asymmetry relative to firms that extensively continue quarterly reporting after 2019. Our results are also robust to using propensity score matching that assigns more (less) weight to more (less) similar firms across both groups to account for the potentially endogenous relationship between firms’ reporting choice and liquidity.Footnote14 However, we acknowledge that our results still may be affected by firms selecting to discontinue quarterly reporting or IAS 34 compliance based on unobservable factors not accounted for by our research design.

6.2. Effects on Analyst Forecast Accuracy

We also analyze whether firms’ quarterly reporting choice affects analyst forecast properties. Our interview evidence suggests that firms tailor their quarterly reporting to the information needs of their key stakeholders including analysts that usually require a set of key metrics allowing them to update their quarterly forecasts. Thus, we do not expect that reductions in the content of quarterly reporting or its termination affect analyst forecast properties.

We follow the same identification strategy as in our liquidity tests and regress analyst forecast error () and forecast dispersion (

) on an indicator variable

.

equals one for firm-year observations in which firms discontinue compliance with IAS 34 (terminate their quarterly reporting) or significantly reduce the content of their quarterly reporting, and zero otherwise. If the termination of quarterly reporting or the reduction of its content negatively affects analyst forecast properties, we expect the coefficient on

to be negative and statistically significant. We also include additional variables that potentially affect analysts’ forecast accuracy as well as year-fixed and firm-fixed effects. We cluster standard errors at the firm level.

In Table we present results on the effect of the termination or reduction in the content of quarterly reporting on analyst forecast accuracy. In columns 1, 3 and 5 we present results for analyst forecast error as the dependent variable. In columns 2, 3 and 5, we present results for forecast dispersion (

) as the dependent variable. Across all specifications, the coefficient on

remains statistically insignificant, suggesting that firms’ quarterly reporting choices are not associated with a deterioration in analyst forecast accuracy. This finding is in line with our interview evidence that firms and analysts are in continuous exchange through other timely information channels such as road shows and conference calls.

Table 7. Effect of firms’ reporting choices on analyst forecast accuracy

6.3. Market Reactions to Deregulation Key Events

We next analyze market reactions around four key announcements events of the stepwise deregulation of the interim reporting regime in the VSE to gauge average investors’ ex-ante expectations as regards the net benefits of the deregulation of interim reporting. Our event study tests three-day cumulative abnormal returns around the VSE’s announcements to terminate the IAS 34 compliance mandate on November 23, 2015, and to terminate the quarterly reporting mandate on February 25, 2019.Footnote15 We regress the value-weighted portfolio return of all VSE prime market firms subject to the interim reporting deregulation on the value-weighted portfolio return of EUROSTOXX 600 firms (excluding VSE firms) and a three-day event window spanning the event date of interest (). We use daily value-weighted portfolio returns instead of individual daily firm returns to correct for the cross-sectional correlation of abnormal returns as the event day is the same for all our sample firms (Armstrong et al., Citation2010; Sefcik & Thompson, Citation1986).Footnote16

We report event study results in Table . Across all four announcement dates, abnormal returns are negative but only statistically and economically significant around the announcement of the termination of the quarterly reporting mandate on February 25, 2019 (Coeff: −0.02, p-value < 1%) (column 4).Footnote17 These results suggest that investors perceived the termination of the quarterly reporting mandate ex-ante as costly but were less concerned about the termination of the IAS 34 compliance mandate.

Table 8. Market reactions to deregulation announcements

7. Conclusion

We examine the determinants and consequences of firms’ responses to a stepwise deregulation of the quarterly reporting mandate in the prime market of the VSE. We find that in response to the two deregulation events firms gradually stop compliance with IAS 34 and reduce the content of their quarterly reports primarily by omitting the notes disclosures. However, only a handful of firms terminated quarterly reporting entirely. Seasonality in business models, reporting, or proprietary costs are generally not the primary considerations in firms’ reporting decisions. Instead, firms carefully weigh the information needs of their key stakeholders and tailor the frequency and content of quarterly reports according to those needs. Overall, our evidence suggests that investors and analysts require quarterly reports that include financial statements, but they do not deem notes or compliance with IAS 34 as important.

Taken together, our findings are consistent with the argument that previously established reporting mandates can be sticky because they shift the voluntary disclosure equilibrium that forms after the reporting mandate is abolished (Bischof & Daske, Citation2013). On the one hand, firms are already invested in reporting systems that reduce marginal costs of future reporting (Dye, Citation1985; Verrecchia, Citation1983, Citation1990) and, on the other hand, investors know about the managers’ information endowment (Dye, Citation1985; Jung & Kwon, Citation1988) resulting in positive net benefits of continuing quarterly reporting for most firms in the VSE.

We acknowledge that the Austrian prime market context is different from the context in other countries and less regulated market segments. Nevertheless, we hope that our insights are useful to regulators, especially of smaller stock markets, who consider relaxing or abandoning the quarterly reporting mandate to alleviate the reporting burden of firms or to attenuate potentially unintended consequences of quarterly reporting.

Supplemental Data and Research Materials

Supplemental data and research material are available in an online Supplement at the journal’s Taylor and Francis website, https://doi.org/10.1080/09638180.2023.2239298.

Appendix OA.1. Internal interview guidelines (translated) Appendix OA.2. Interview invitation and fact sheet (translated)

Appendix OA.3. Anecdotal evidence from public sources

Appendix OA.4. Firm reporting choices

Table OA.5. Pearson correlations of determinants sample

Table OA.6. Descriptive statistics

Table OA.7. Determinants of quarterly reporting content (2019-2021)

Table OA.8. Liquidity effects around termination of IAS 34 mandate (2015)

Table OA.9. Liquidity effects of VSE prime market firms’ reporting choices (PSM)

Table OA.10. Comparison of interview participants

supplemental-materials.docx

Download MS Word (98.7 KB)Acknowledgements:

We thank Beatriz García Osma (editor), two anonymous reviewers, and seminar participants at the 44th EAA Annual Congress and EUFIN 2021 Virtual Workshop for helpful suggestions and feedback.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 As mandated by the Vienna Stock Exchange. Regelwerk Prime Market. Wiener Börse AG (2015).

2 See Vienna Stock Exchange Disclosure Requirements: Regelwerk Prime Market. Wiener Börse AG (Citation2018).

3 Directive 2013/50/EU of the European Parliament and of the Council as transposed into Austrian national law by November 2015. The adoption of the TDAD was a response to the European Commission’s conclusion that the benefits of a higher reporting frequency do not exceed the implicit costs of increased managerial short-termism and higher reporting costs, esp. for small firms (European Commission, Citation2010a; European Commission, Citation2010b).

4 We report descriptive statistics of participating and non-participating firms in Online Appendix OA.10.

5 Specifically, we exclude Addiko Bank AG, Frequentis AG, Marinomed Biotech AG and Valneva SE.

6 We use a linear probability model because of the small number of observations. Long and Freese (Citation2014, p. 85) consider 500 observations as adequate for the use of maximum likelihood estimation. Our sample sizes vary between 103 and 208 observations. Our results are robust to using logit models.

7 Firms choose to terminate quarterly reporting in a given quarter. However, our variables of interest are mostly available at the fiscal year level. We therefore annualize the data and model.

8 In alternative specifications, we replace with the concentration of outside ownership among the 100 largest publicly disclosed investors (

).

9 Prior literature analyzing determinants of firms’ interim reporting choices includes the Herfindahl Index to capture reporting choices of peer firms and proprietary costs (Botosan & Harris, Citation2000; Link, Citation2012; Hitz & Moritz, Citation2019). Our interview evidence suggests that firms consider the reporting choices of a very small set of peer firms (usually, one to three national or international competitors) to remain comparable in transparency instead of considering the collective reporting choices of the industry. Proprietary costs were not raised as concern in our interviews. Therefore, we do not consider industry concentration (the Herfindahl Index) as a potential determinant in our empirical analyses.

10 Online Appendix OA.4 shows the individual reporting choices of each firm included in our sample.

11 Thus, the differences-in-differences estimation generalizes to a Heckman two-stage model (Heckman, Citation1979; Maddala, Citation1983). Specifically, in a first step, we estimate the firm’s propensity to be a treatment firm (i.e., to terminate IAS 34 compliance or quarterly reporting) given the full set of determinants in the determinants model including BIDASK. Based on the results of the first stage, we calculate the inverse mills ratio that we include as a control variable in the second stage (liquidity tests).

12 We employ factor analysis including all three liquidity measures (i.e., bid-ask spread, zero return days, and the Amihud illiquidity measure) with one oblique rotation following Daske et al. (Citation2008).

13 In this analysis, TERM also includes five firms that merely remove the IAS 34 compliance statement but continue to include notes to their quarterly reports. In Table OA.8 of the Online Appendix, we exclude these firms and report qualitatively comparable results.

14 We report the results of replicating Table using propensity score matching in Table OA.9 of the Online Appendix.

15 We also include the EU’s announcement of the Transparency Directive Amending Directive (TDAD) on October 22, 2013 and the announcement of the TDAD’s transposition into Austrian national law on August 3, 2015 as event dates.

16 Using a portfolio approach with value-weighted returns corrects for cross-sectionally correlated abnormal returns.

17 Our results hold when using seemingly unrelated regressions to correct for potentially cross-sectionally correlated abnormal returns around the event dates.

References

- Amihud, Y. (2002). Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets, 5(1), 31–56. https://doi.org/10.1016/S1386-4181(01)00024-6

- Anantharaman, D., & Zhang, Y. (2011). Cover me: Managers’ responses to changes in analyst coverage in the post-regulation FD period. The Accounting Review, 86(6), 1851–1885. https://doi.org/10.2308/accr-10126

- Armstrong, C. S., Barth, M. E., Jagolinzer, A. D., & Riedl, E. J. (2010). Market reaction to the adoption of IFRS in Europe. The Accounting Review, 85(1), 31–61. https://doi.org/10.2308/accr.2010.85.1.31

- Arya, A., & Mittendorf, B. (2007). The interaction among disclosure, competition between firms, and analyst following. Journal of Accounting and Economics, 43(2-3), 321–339. https://doi.org/10.1016/j.jacceco.2006.11.001

- Benston, G. J. (1973). Required disclosure and the stock market: An evaluation of the securities exchange Act of 1934. The American Economic Review, 63(1), 132–155.

- Bischof, J., & Daske, H. (2013). Mandatory disclosure, voluntary disclosure, and stock market liquidity: Evidence from the EU bank stress tests. Journal of Accounting Research, 51(5), 997–1029. https://doi.org/10.1111/1475-679X.12029

- Boone, A. L., & White, J. T. (2015). The effect of institutional ownership on firm transparency and information production. Journal of Financial Economics, 117(3), 508–533. https://doi.org/10.1016/j.jfineco.2015.05.008

- Botosan, C. A., & Harris, M. S. (2000). Motivations for a change in disclosure frequency and its consequences. An Examination of Voluntary Quarterly Segment Disclosures. Journal of Accounting Research, 38(2), 329–353. https://doi.org/10.2307/2672936

- Bourveau, T., Chen, J. V., Elfers, F., & Pierk, J. (2022). Public peers, accounting comparability, and value relevance of private firms’ financial reporting. Review of Accounting Studies, 1–35. https://doi.org/10.1007/s11142-022-09707-y

- Bowen, R. M., Chen, X., & Cheng, Q. (2008). Analyst coverage and the cost of raising equity capital: Evidence from underpricing of seasoned equity offerings. Contemporary Accounting Research, 25(3), 657–700. https://doi.org/10.1506/car.25.3.1

- Bushee, B. J., & Miller, G. S. (2012). Investor relations, firm visibility, and investor following. The Accounting Review, 87(3), 867–897. https://doi.org/10.2308/accr-10211

- Butler, M., Kraft, A., & Weiss, I. S. (2007). The effect of reporting frequency on the timeliness of earnings: The cases of voluntary and mandatory interim reports. Journal of Accounting and Economics, 43(2), 181–217. https://doi.org/10.1016/j.jacceco.2007.02.001

- Chen, Q., Lewis, T. R., Schipper, K., & Zhang, Y. (2017). Uniform versus discretionary regimes in reporting information with unverifiable precision and a coordination role. Journal of Accounting Research, 55(1), 153–196. https://doi.org/10.1111/1475-679X.12130

- Chen, S., DeFond, M. L., & Park, C. W. (2002). Voluntary disclosure of balance sheet information in quarterly earnings announcements. Journal of Accounting and Economics, 33(2), 229–251. https://doi.org/10.1016/S0165-4101(02)00043-5

- Coffee Jr J. C. (1984). Market failure and the economic case for a mandatory disclosure system. Virginia Law Review, 717–753. https://doi.org/10.2307/1073083

- Covrig, V. M., Defond, M. L., & Hung, M. (2007). Home bias, foreign mutual fund holdings, and the voluntary adoption of international accounting standards. Journal of Accounting Research, 45(1), 41–70. https://doi.org/10.1111/j.1475-679X.2007.00226.x

- Cuijpers, R., & Peek, E. (2010). Reporting frequency, information precision and private information acquisition. Journal of Business Finance & Accounting, 37(1-2), 27–59. https://doi.org/10.1111/j.1468-5957.2009.02180.x

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2008). Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research, 46(5), 1085–1142. https://doi.org/10.1111/j.1475-679X.2008.00306.x

- DeFond, M., Hu, X., Hung, M., & Li, S. (2011). The impact of mandatory IFRS adoption on foreign mutual fund ownership: The role of comparability. Journal of Accounting and Economics, 51(3), 240–258. https://doi.org/10.1016/j.jacceco.2011.02.001

- Demski, J. S., & Feltham, G. A. (1994). Market response to financial reports. Journal of Accounting and Economics, 17(1-2), 3–40. https://doi.org/10.1016/0165-4101(94)90003-5

- Diamond, D. W. (1985). Optimal release of information by firms. The Journal of Finance, 40(4), 1071–1094. https://doi.org/10.1111/j.1540-6261.1985.tb02364.x

- Diamond, D. W., & Verrecchia, R. E. (1991). Disclosure, liquidity, and the cost of capital. The Journal of Finance, 46(4), 1325–1359. https://doi.org/10.1111/j.1540-6261.1991.tb04620.x

- Downar, B., Ernstberger, J., & Link, B. (2018). The monitoring effect of more frequent disclosure. Contemporary Accounting Research, 35(4), 2058–2081. https://doi.org/10.1111/1911-3846.12386

- Dye, R. A. (1985). Strategic accounting choice and the effects of alternative financial reporting requirements. Journal of Accounting Research, 23(2), 544–574. https://doi.org/10.2307/2490826

- Easterbrook, F. H., & Fischel, D. R. (1984). Mandatory disclosure and the protection of investors. Virginia Law Review, 70(4), 669–715. https://doi.org/10.2307/1073082

- Eng, L. L., & Mak, Y. T. (2003). Corporate governance and voluntary disclosure. Journal of Accounting and Public Policy, 22(4), 325–345. https://doi.org/10.1016/S0278-4254(03)00037-1

- Ernstberger, J., Link, B., Stich, M., & Vogler, O. (2017). The real effects of mandatory quarterly reporting. The Accounting Review, 92(5), 33–60. https://doi.org/10.2308/accr-51705

- European Commission. (2010a). Commission staff working document: The review of the operation of directive 2004/109/EC: Emerging issues SEC (2009) 611.

- European Commission. (2010b). Operation of directive 2004/109/EC on the harmonisation of transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market, European commission COM(2010)243.

- Feller, A., & Schanz, D. (2017). The three hurdles of tax planning: How business context, aims of tax planning, and tax manager power affect tax expense. Contemporary Accounting Research, 34(1), 494–524. https://doi.org/10.1111/1911-3846.12278

- Fiechter, P., Halberkann, J., & Meyer, C. (2018). Determinants and consequences of a voluntary turn away from IFRS to local GAAP: Evidence from Switzerland. European Accounting Review, 27(5), 955–989. https://doi.org/10.1080/09638180.2017.1375418

- Florou, A., & Pope, P. F. (2012). Mandatory IFRS adoption and institutional investment decisions. The Accounting Review, 87(6), 1993–2025. https://doi.org/10.2308/accr-50225

- Fu, R., Kraft, A., Tian, X., Zhang, H., & Zuo, L. (2020). Financial reporting frequency and corporate innovation. The Journal of Law and Economics, 63(3), 501–530. https://doi.org/10.1086/708706

- Fu, R., Kraft, A., & Zhang, H. (2012). Financial reporting frequency, information asymmetry, and the cost of equity. Journal of Accounting and Economics, 54(2-3), 132–149. https://doi.org/10.1016/j.jacceco.2012.07.003

- Ge, X., Bilinski, P., & Kraft, A. (2021). Institutional blockholders and voluntary disclosure. European Accounting Review, 30(5), 1013–1042. https://doi.org/10.1080/09638180.2021.1979418

- Gigler, F., Kanodia, C., Sapra, H., & Venugopalan, R. (2014). How frequent financial reporting can cause managerial short-termism: An analysis of the costs and benefits of increasing reporting frequency. Journal of Accounting Research, 52(2), 357–387. https://doi.org/10.1111/1475-679X.12043

- Glaser, B. G., & Strauss, A. L. (1999). The discovery of grounded theory: Strategies for qualitative research. Aldine Transaction.

- Gutierrez, E. F., Vulcheva, M., & Rykaczewski, M. (2017). The cost–benefit tradeoff of securities market regulation: European firms’ delisting around major regulatory shocks (May 31, 2022). SSRN Working Paper.

- Healy, P. M., Hutton, A. P., & Palepu, K. G. (1999). Stock performance and intermediation changes surrounding sustained increases in disclosure. Contemporary Accounting Research, 16(3), 485–520. https://doi.org/10.1111/j.1911-3846.1999.tb00592.x

- Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47(1), 153–161. https://doi.org/10.2307/1912352

- Hitz, J. M., Koch, S., & Moritz, F. (2020). Downlistings in European exchange-regulated markets: The role of enforcement. Journal of Accounting and Public Policy, 39(6), 106735. https://doi.org/10.1016/j.jaccpubpol.2020.106735

- Hitz, J. M., & Moritz, F. (2019). Turning back the clock on disclosure regulation? – Evidence from the termination of the quarterly reporting mandate in Europe (September 11, 2019). SSRN Working Paper.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jung, W.-O., & Kwon, Y. K. (1988). Disclosure when the market is unsure of information endowment of managers. Journal of Accounting Research, 26(1), 146–153. https://doi.org/10.2307/2491118

- Kajüter, P., Lessenich, A., Nienhaus, M., & van Gemmern, F. (2022). Consequences of interim reporting: A literature review and future research directions. European Accounting Review, 31(1), 209–239. https://doi.org/10.1080/09638180.2021.1872398

- Kanodia, C. (2006). Accounting disclosure and real effects. Foundations and Trends® in Accounting, 1(3), 167–258. https://doi.org/10.1561/1400000003

- Kanodia, C., & Lee, D. (1998). Investment and disclosure: The disciplinary role of periodic performance reports. Journal of Accounting Research, 36(1), 33–55. https://doi.org/10.2307/2491319

- Kim, O., & Verrecchia, R. E. (1991). Trading volume and price reactions to public announcements. Journal of Accounting Research, 29(2), 302–321. https://doi.org/10.2307/2491051

- Kraft, A. G., Vashishtha, R., & Venkatachalam, M. (2018). Frequent financial reporting and managerial myopia. The Accounting Review, 93(2), 249–275. https://doi.org/10.2308/accr-51838

- Lang, M. H., & Lundholm, R. J. (1996). Corporate disclosure policy and analyst behavior. The Accounting Review, 71(4), 467–492.

- Leftwich, R. W., Watts, R. L., & Zimmerman, J. L. (1981). Voluntary corporate disclosure: The case of interim reporting. Journal of Accounting Research, 19(Suppl.), 50–77. https://doi.org/10.2307/2490984