?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The COVID-19 outbreak has had severe economic consequences across the globe. The crisis emanating from the pandemic has caused demand and supply side shocks, more far reaching than any crisis in living memory. We use a new data set from the 2020/21 Egyptian Industrial Firm Behavior Survey to examine determinants of firms’ resilience during the pandemic. Crisis present the opportunity for what Schumpeter (In Economics of the Recovery Program, McGraw-Hill, 1934) calls creative destruction. Have manufacturing firms been all hit by the crisis equally, or were less efficient firms more likely to exit or downsize their activities thereby ‘cleansing’ the market? Two sets of factors affect firm dynamics and survival: (1) firms’ innate characteristics and; (2) firm behavior, which captures the extent to which good management, innovation, the adoption of advanced technologies and worker training, have provided an opportunity for firms to adapt their business models and show greater resilience in coping with the crisis. We illustrate the vulnerability of private, smaller, informal firms and those that are not located in industrial zones. Second, pre-COVID behavioral characteristics matter for firm dynamics. The food sector and sectors identified as ‘COVID sectors’ show more resilience. Some behavioral traits vary by sector and are more influential depending on firm size.

1. Introduction

The COVID-19 outbreak has had severe economic consequences across the globe. Most countries have instituted full or partial lock-down measures to save lives during the pandemic. To mitigate the spread of the virus the Egyptian government instituted a partial lockdown as of March 2020. The lockdown restricted opening hours and movement with the exception of grocery shops and supermarkets. Further restrictions were introduced in April which lasted until the end of May 2020. Another round of less strictly enforced restrictions were introduced during the second wave of COVID-19 from December 1st 2020 to January 2021. According to the stringency index constructed by the University of Oxford, Egypt had a moderate policy response in terms of movement restrictions and business closures. However, protecting human life has an economic cost. The measures have resulted in a global economic crisis, which has been both a demand shock, and a supply side shock. Substantial numbers of businesses have been forced to exit the market or to temporarily close. Global supply chains have been substantially disrupted resulting in increased supply costs limiting in turn firms’ ability to enforce the quality and timeliness of contracts (Demertzis and Maslloren Citation2020; Ayadi et al. Citation2021). Sharma, Adhikary, and Borah (Citation2020) use twitter data from NASDAQ to show that US firms are facing grave difficulties in sustaining their supply chains. Consequently, numerous firms have suffered lower productivity, lost previous productivity gains and have seen their sales and profits shrink (Bloom, Fletcher, and Yeh Citation2021).

To absorb the shock of the pandemic on both firms and households, similar to other nations, the government of Egypt rolled out a full-fledged stimulus package. The government adopted a number of fiscal and monetary measures. At the fiscal level, the government announced a $6.13 billion package which accounts for 1.8 percent of GDP (Krafft, Assaad, and Marouani Citation2021). In support of government revenues, a Corona tax of 1% has been levied on all public and private sector salaries and of 0.5% on state pensions. These revenues were supposed to fund some fiscal measures to support the negatively affected sectors. Fiscal measures to support the economy and the financial markets included: lowering the price of electricity and natural gas for industrial use, reducing real estate tax payment settlements for industrial and tourism companies; postponing the capital gains tax on stock market transactions and permanently exempting foreign investors from the duty, cutting tax on dividends, fast-tracking payouts from the Export Subsidy Fund, expanding the Social Security and Pension Act's coverage; providing one-time stipends of EGP 500 for seasonal and temporary workers; postponing the filing deadline for auditors and small and medium-sized enterprises (SMEs) (El-Haddad Citation2020a).

At the monetary and financial levels, a preferential interest rate (8%) has been set for the loans of some industries such as tourism, industry, agriculture and construction sectors, and on mortgages for low-income and middle-class housing. The aim of these measurers was to counter the negative contractionary effects of the pandemic through encouraging industrial sector growth and capital expenditure lending, help shrink the budget deficit (given the new expansionary fiscal measures) and stimulate foreign investments on the stock market. Additionally, the Central Bank of Egypt (CBE) provided a $6.13 billion guarantee to cover lending at preferential rates to the manufacturing, agriculture and contracting sectors.

On the other hand, firms have adopted various strategies to cope with the pandemic such as reducing input costs through worker layoffs and salary adjustments, or upgrading their business model through increased remote work and expanding e-commerce platforms. Some firms have also diversified their products. It is thus important to assess the impact of COVID-19 on firm survival and dynamics so as to identify appropriate measures of support during the pandemic to strengthen firm resilience in the face of future shocks.

A central question in this paper is whether firm dynamics have only been affected by demand and supply side conditions, or have they been also mediated by how firms respond to changing market conditions? Crisis presents the opportunity for what Schumpeter (Citation1934) called creative destruction. During economic distress, less efficient firms are more likely to exit or to downsize their activities, thereby ‘cleansing’ the market. Do the Egyptian data support this hypothesis? Is firm survival positively associated with productivity? Are exporting, innovative, high tech firms and those that undertake good management practices more likely to maintain operations, or even just survive? Will such firms exhibit better dynamics, or has the COVID-19 crisis hit all firms equally hard as argued by Bosio et al. (Citation2020)?

The empirical literature on the impact of COVID-19 on firm dynamics mainly discusses the experience in developed economies. There are some exceptions on Latin America for example (Guerrero-Amezaga et al. Citation2022). In Japan, Miyakawa, Oikawa, and Ueda (Citation2021) show that the pandemic increased firm exit by around 20% compared to the previous year due to firm expectations regarding sales prospects. Bachas, Brockmeyer, and Semelet (Citation2020) find that, while over half of firms will remain profitable by the end of 2020, the likelihood of exit will double. Using firm-level data for 31 economies, Muzi et al. (Citation2021), find that less productive firms have a higher likelihood of permanently closing during the crisis, though it varies by the extent of innovation and digitalization. However, using administrative corporate tax records from ten low- and middle-income countries (Sub-Saharan Africa, Eastern Europe and Latin America), firms in poorer countries are shown to be more resilient because these join the informal sector rather than exit altogether (Bachas, Brockmeyer, and Semelet Citation2020). For most developing countries the informal sector is a buffer to shocks which acts as a survival sector (El-Haddad and Zaki Citation2022a).

Existing literature on firm survival and performance emphasized the significant role that investing in R&D and the adoption of advanced technology play.Footnote1 Firms build resilience by using innovation and technology. Entrepreneurs interact both of these with firm characteristics and strategic behavior to adapt to unfavorable market changes (George and Bock Citation2011). Hall (Citation1987) argues that R&D activities enhance the firm's stock of knowledge, increasing the firm's market value and so its likelihood of survival. Similarly, investing in innovation increases firm-specific assets and so the competitive position of firms (Esteve-Perez and Manez-Castillejo Citation2008). Cefis and Marsili (Citation2005) stress the positive impact of innovation on firm survival. Survival probability is 11% higher for innovative firms compared to their non-innovative counterparts. This probability is 25% higher for those innovating in processes rather than production. Giovannetti, Ricchiuti, and Velucchi (Citation2011) show that being a large firm combined with technology adoption is a sufficient condition for firm survival. Cefis and Marsili (Citation2019) demonstrate that new firms innovating within two years from founding enjoy a long-term adaptive survival premium during and after a crisis. More recently, Cucculelli and Peruzzi (Citation2020) have shown that adaptive business models have influenced post-crisis firm survival by reducing the probability of default.

Grover and Karplus (Citation2021) have shown that good management practices such as target-setting, monitoring, incentives and operational practices are also associated with a higher likelihood of survival for manufacturing firms, though is not the case for firms in services. As Pansiri and Temtime (Citation2008) put it, ‘managerial effectiveness could by definition have avoided or at least minimized [problems’] impact on firm survival’ (252).

Yet, while the literature is rich for the advanced and emerging economies it is rather scant when it comes to the Middle East and North Africa (MENA) region. This paper helps rectify this gap by presenting data for Egypt. In fact, the case of Egypt is of particular interest for three reasons. First, on a macroeconomic level, Egypt's economy was one of the most resilient across the MENA region. Indeed, Egypt was among the few economies that experienced a positive growth rate in 2019/2020 (Eldeep and Zaki Citation2021; El-Haddad Citation2020a). But at the social level the negative consequences of the crisis were more pronounced. Descriptive analysis of the data (El-Haddad and Zaki Citation2022a) illustrates the counter cyclicality of the relation between the formal and the informal sector as the latter is the only alternative way to earn a living. As a ‘survival sector’, it has provided 'helping hand employment' in the course of the current pandemic. There are no accurate official figures on the evolution of informality, inequality and poverty in the wake of the pandemic, but they should be expected to have increased with the lay-offs that have taken place. As shown by El-Haddad and Gadallah (Citation2021), private sector informality is the largest contributor to increased inequality in Egypt. Second, despite being one of the most diversified economies in the MENA region, Egypt's manufacturing sector is still suffering from several longstanding bottlenecks which undermine its competitiveness. Foreign direct investment (FDI) is concentrated in the oil and real estate sectors and Egyptian markets exhibit limited competition. In addition, there is very limited contribution of the private sector in the green economy (Zaki Citation2022) so the manufacturing sector maybe less able to cope with external shocks. Finally, it is important to take a closer look at Egyptian SMEs. SMEs dominate the sector comprising 90% of all firms, but larger firms, both public and private, dominate the market in terms of performance and profitability.

We use unique and recently collected data from the 2020/21 Egyptian Industrial Firm Behavior Survey (EIFBS) of 2,383 Egyptian manufacturing firms.Footnote2 The objective of this paper is to examine determinants of firm resilience and firm dynamics during the COVID-19 crisis. We distinguish between ‘status variables’ or ‘innate characteristics’ and those which are shaped by the behavior of the industrial firm such as managerial practices, investment in innovation or worker training and the adoption of advanced technology. In contrast, ‘innate characteristics’ such as being informal, solely catering to the domestic market or being in the private sector are less endogenous. We also introduce a shock variable and address the problem of endogeneity in our data using an instrumental variable approach.

Our main findings highlight the vulnerability of private, smaller, informal firms and those that are not located in industrial zones. Moreover, consistent with the literature, pre-COVID behavioral characteristics matter for firm dynamics. In terms of sector, the food sector and sectors identified as COVID sectors show more resilience. More nuanced results show that some behavioral traits matter more depending on sector and are more influential depending on size. Overall, our findings support Schumpeter’s (Citation1934) creative destruction theory. Firms that have innovated and invested in favorable behavior have survived the storm, others had to shrink or fade away.

2. Sampling and survey design data and stylized facts

We use a recently collected dataset of 2383 manufacturing firms, namely the 2020/21 Egyptian Industrial Firm Behavior Survey (EIFBS). The data were collected at the beginning of the second wave of COVID-19 extending to the height of it.Footnote3 EIFBS firms comprise a multistage stratified sample drawn from the 2017 economic census sample of 33,331 establishments, which is itself drawn from a sample of 117,149 establishments, the latter covering three other censuses, namely the population, housing and establishments’ census.

The EIFBS sample design is based on three parameters to ensure that the sample produces representative and precise estimates at the national level. These parameters are number of employees, region (urban governorates, lower and upper Egypt) and economic activity level (2 digits). The sample frame, however, excludes firms with less than 5 employees and thus is only representative of small, medium and large enterprises (SMEs). This also implies that informal firms – albeit present – are underrepresented in our sample.

We oversampled by selecting a sample of 3149 establishments in order to be sure to obtain the target number of 2200. First, the sample was allocated proportionally among the three regions (urban governorates, lower Egypt, and upper Egypt), which cover 99.2% of industrial establishments in Egypt. A systematic random sample was drawn to select three governorates from each region using Probability Proportional to Size (PPS). The industrial establishments in each region were allocated among governorates proportional to their size (measured by employment). Next, a systematic random sample was used to select the establishments in each governorate after sorting the establishments according to the number of employees and economic activity at the 4 digits level. Two questionnaires were administered, one for firms that are still in operation, and another, very similar one,Footnote4 for firms that have exited the market or have temporarily shut down operations. The response rate is 75%, meaning that we successfully interviewed 2,383 establishments of which 2338 are in operation and 45 firms that either have exited the market or are temporarily closed. Of the 766 firms we could not interview, an unknown number, and presumably a much higher proportion, have also exited the market. The questionnaire has 14 modules: basic firm identification data, firm size, firm expectations on recovery and potential exit, changes in firm performance, pandemic transmission channels, ownership and management characteristics, innovation, management practices and use of IT, production costs, obstacles to operation, exports and global value chains, obstacles to exports, worker training and government support.

A note on Egyptian bakeries is warranted. Bakeries are to be found on nearly every street in residential areas in Egypt, representing about 30% of all industrial firms. Unlike other micro and small enterprises, bakeries in Egypt have an incentive to formalize in order to be able to collect the bread subsidy from the government. Given protection afforded by the subsidy and the nature of their product which is an inferior good (i.e. demand goes up as income falls), bakeries likely exhibit different behavior to their non-bakery food sector counterparts, as well as other micro and small enterprises and formal counterparts. Their inclusion in the sample therefore strongly affects firm dynamics in the manufacturing sector as captured by a number of behavioral and performance variables. We report below if they are included in the analysis or not.

To measure firms’ dynamics, we focus on two main variables. The first measures the operational status of firms, precisely whether the firm is partially or fully functioning at the time of the interview. This is to assess the depth of its operation if it is not closed – does it operate at full capacity or only partial? The second variable documents firm closures since the start of the pandemic based on the following question ‘Has the establishment been temporarily closed for any period since the beginning of the COVID crisis?’ Thus, while the first variable measures firms’ performance at the level of the intensive margin (the extent to which the firm is operating), the latter assesses it at the extensive one (whether the firm is actually operating).

We distinguish between two possible determinants of firm dynamics: (1) innate firm characteristics such as formality and export status, sector, ownership, age, size and location; and (2) firm behavior, such as good managerial practices, innovation (R&D), the adoption of advanced technologies and investing in worker training. Table summarizes the main descriptive statistics of the used variables.

Table 1. Descriptive statistics.

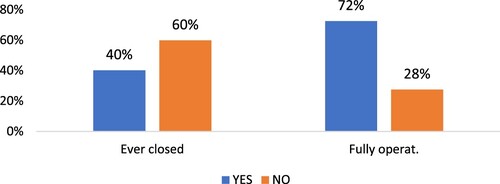

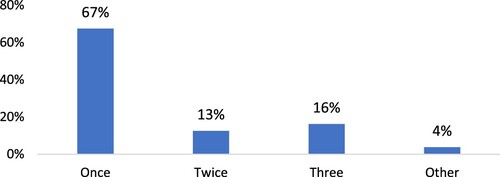

Just under a third of all Egyptian manufacturing firms were not fully functioning at the time of interview (Figure ). Moreover, 60% of firms have never closed. Indeed, since the start of the pandemic around 40% of all firms have at least once been temporarily closed – of those 67% once, 13% twice and 16% three times (see Figure ).

Figure 1. Firm dynamics. Source: Authors’ own elaboration using EIFBS.

Figure 2. Number of closures since start of the COVID-19 crisis. Source: Authors’ own elaboration using EIFBS.

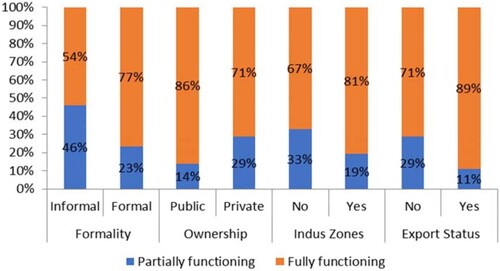

The sample covers 82% of SMEs, 3.4% public firms, 7.2% informal firms and 2.7% exporting firms. Firms are more likely to be fully functioning if they are formal, public, located in an industrial zone or had been exporting prior to the COVID-19 crisis (Figure ). While the share of formal firms that are fully functioning is 77% that share declines to 54% for their informal counterparts. Similarly, the share of firms in the public sector (86%), in industrial zones (81%) and exporters (89%) that are fully functioning is higher than their private (71%), non-zone (67%) and non-exporting (71%) counterparts.

Figure 3. Operational status by firms’ characteristics. Source: Authors’ own elaboration using EIFBS.

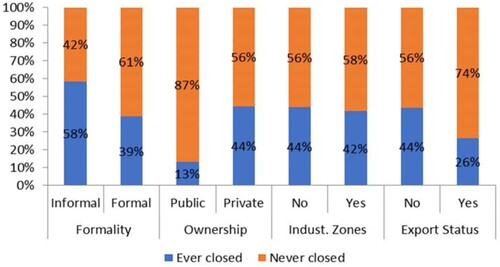

Similar patterns are observed for firm closure. Formal, exporting, public firms and those located in an industrial zone are less likely to witness closures since the start of the COVID-19 crisis (Figure ).

Figure 4. Closure by firms’ characteristics. Source: Authors’ own elaboration using EIFBS.

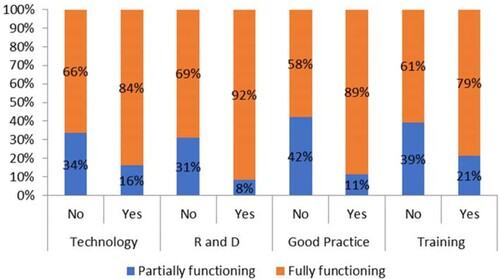

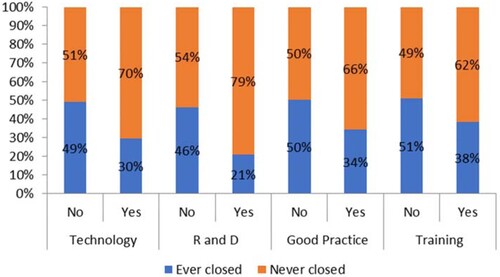

In terms of firm behavior: firms whose managers have adopted advanced technologies prior to the COVID-19 crisis (84% of those firms), innovated (92%), embraced good managerial practices such as monitoring performance indicators or setting production targets (89%) and those who have provided worker training (79%) are more likely to be fully functioning compared to their counterparts (Figure ). They are also less likely to have ever been closed since the start of the COVID-19 crisis (30%, 21%, 34% and 38% respectively) compared to their counterparts (49%, 46%, 50% and 51% respectively; Figure ).

Figure 5. Operational status by firm behavior. Source: Authors’ own elaboration using EIFBS.

Figure 6. Closure by firms’ behavior. Source: Authors’ own elaboration using EIFBS.

3. Methodology

We run the following econometric specification to examine the effect of the COVID19 crisis on firms’ dynamics.

(1)

(1) where Y is the dependent variable of firm i in sector k and governorate g with separate equations estimated for (i) the operational status of the firm, which takes the value of one if the firm is fully functioning and zero otherwise; and (ii) the ever closed status, which takes the value of one if the firm has been temporarily closed for any period since the start of the COVID-19 crisis, and 0 otherwise. δg and µk are governorate and sector dummies respectively to control for governorate and sector unobversables, and ŋikg is the error term. The sectors are classified according to the ISIC Rev. 4 at the 2-digit level.

Two vectors of explanatory variables Xikg and Zikg are included. The first, Xikg measures firm innate characteristics including:

Ln(ageikg) is the age of firm i operating in sector k and governorate g. While older firms might be more resilient given their experience and financial health, younger firms might be more innovative.

Private is a dummy variable that takes the value of 1 if the firm is privately owned and zero if it is publicly owned. Egypt preserves many features of its earlier state-led development model, including that public firms operate under a ‘soft budget constraint’. The state provides cheap credit and bails out public companies in crisis (El-Haddad Citation2015). Hence publicly owned companies may appear more robust with better dynamics.

Ln(Emp BC) gives firm size, measured by the number of employees before COVID. Given their resilience, larger firms are more likely to be fully operational. On the other hand, large firms are mostly also formal and so more likely to have had to fully observe lock-down measures

Formal is a dummy variable that takes the value of one if the firm is formal. We employ a strict definition of formality. A firm is formal if it has a commercial registry, an operating license and a tax record. Firms are more likely to be fully functioning and less likely to have ever closed if they are formal.

Exp Status BC is a dummy variable that takes the value of 1 if the firm was exporting before COVID.

Industrial Zone is a dummy variable that takes the value of 1 if the firm is located in any industrial zone. This variable shows to what extent agglomeration economies might help firms sustain their activities. The zones may mitigate the negative effects of the shock. However, firms in the zones can also be the most hit on account of the disruptions to their value chains of which they are part.

We control for firm behavior. Vector Zikg covers four main dimensions:

Training is a dummy variable taking the value of 1 if the firm provides training for its workers.

Technology is a dummy variable that takes the value of 1 if the firm's manager utilizes technology such as computers, the internet, internal information link networks, distributed machine control systems, and quality control systems. Technology measures the ability of the firm to adapt to unfavorable market changes and to cope with the new normal by adapting their business models.

R and D is a dummy variable that takes the value of 1 if the firm had spent on R&D other than market research surveys prior to COVID. Both, whether undertaken by the firm directly or by companies it contracted with. Both innovation and technology show how entrepreneurs interact firm characteristics and strategic behavior to adapt to unfavorable market changes, thus building greater resilience over time.

Good Practice is a dummy variable that takes the value of 1 if the firm's manager has either specified any performance indicators or production targets; or has monitored these performance indicators.

This baseline regression is extended in three ways. First, we examine the extent to which firm size matters when interacted with the firm's behavioral variables. In other words, we examine whether large firms are more likely to make use of good management practices, innovation or technology, affecting in turn the probability of the operational status favorably.

Second, we further analyse research and development (R&D), technology and good management practices to identify which dimension within each of these categories matters the most. Research and development, which is proxy for innovation, is broken down into devoting financial resources to improving products, machines, design, marketing and production processes. Moreover, while technology covers computers, internet, internal information link networks, distributed machine control systems, and quality control systems, good managerial practices cover setting performance indicators or production targets and monitoring them.

Third, the experiences of a number of countries have shown that public support can contribute significantly to firms’ survival and resilience during the COVID-19 pandemic (cf. Bennedsen et al. Citation2020; Lalinsky and Pál Citation2021 and Kozeniauskas, Moreira, and Santos Citation2020). Thus, there is a need to examine whether our variables of interest remain robust in the face of received government support. To do so, we introduce a dummy variable that takes the value of 1 if the firm received any type of government support after the pandemic and zero otherwise. Furthermore, the nature of the shock – especially its demand side has led in particular to an increase in the demand on computers, pharmaceuticals and food products. Given the nature of the shock, firms operating in these sectors might be more resilient to the crisis. Accordingly, we distinguish between four sectors: traditional sectors (including textiles, garments, leather … etc.), COVID sectors, which cover computers; chemicals; and pharmaceuticals; food; and non-traditional sectors (machinery, electronics, and electrical equipment). We had also experimented some more by interacting innate characteristics with firm behavior.

Finally, because some of our firm characteristics and behavioral variables are potentially endogenous with respect to the firm's operational status (ever closed or fully functioning) we test robustness by proceeding with an instrumental variables approach to address the problem of endogeneity.

4. Empirical results

4.1. Baseline regressions

Table presents results of the baseline regression.Footnote5 First, in terms of the firms’ innate characteristics, firms are more likely to be fully functioning if they are public, large or located in an industrial zone. Second, formality matters for the ever being closed probability but not for the operational status. This is probably because, like informal firms, formal firms have significantly reduced their capacity utilization. However, they have reduced working hours significantly more compared to their informal counterparts.Footnote6 This implies that formal firms are less likely to close but that similar to their existing informal counterparts they are equally functional. Indeed, being formal helps firms access post-COVID-19 government designed support programs such as tax deferrals, loans postponements, COVID financial support … etc. Such support is likely to prevent firms from closing during times of crisis.

Table 2. Baseline regression.

The results also show that private firms suffer an increased likelihood of closing and a reduced probability of being fully functioning. Public firms have for years enjoyed greater protection compared to their private sector counterparts through the provision of cheap state credit and a soft budget constraint resulting in the bailing out of public companies in crisis. Public firms are also relatively more concentrated in the more resilient sector, food: 40% of all public firms are in the food sector (excluding bakeries) but only 19% of private firms. The findings here echo the fact that the private sector in Egypt continues to face a number of institutional and competition-related barriers that hinder its expansion (World Bank Citation2020). Plenty of the nascent literature suggests that politically connected firms in Egypt are mostly large in size, and that State-owned enterprises are more likely to enter the exports market than private sector firms, due to privileged connections and superior access to information (cf. Eibl and Malik Citation2016; Aboushady and Zaki Citation2019; El-Haddad Citation2020b).

Exporting is not statistically significant neither for the operational status variable nor for the ever being closed variable. The positive effects of exporting are likely diluted by the presence of the sectoral/economic activity dummies. In fact, both exporting (61% of all exporting firms) and non-exporting firms (56%) have reported similar reductions in demand in the wake of the COVID-19 shock.

There is broad agreement in the trade literature that exporting firms have higher productivity than non-exporting ones (Melitz Citation2003; Fernandes and Isgut Citation2005; Greenaway and Kneller Citation2008; Feng, Li, and Swenson Citation2016). This fact is chiefly attributed to a self-selection process: firms taking up exporting are already the most productive ones and are able to afford the high fixed-costs of entering foreign markets. An alternative explanation is the learning-by-exporting theory, where firms become more productive through exporting. The literature is not conclusive on the expected effects of the pandemic on exporters. A first strand argues that the international exposure of exporting firms increases their vulnerability and makes them more likely to be affected by external shocks. A second strand shows that they are less affected as they are, on average, more productive and more able to sustain their activities in times of crisis. Our results support the first view, that other things being equal, the demand shock hit firms serving the domestic market and those serving the export market equally hard, especially after controlling for economic activity.

The effect of age is not conclusive in the literature (Rossi Citation2016). While older firms can be more resilient due to their experience and financial stability, younger ones are more innovative and thus can also be as resilient (Krammer Citation2021).

While age reduces a firm's likelihood of being fully functioning (columns 1–3), it significantly reduces its probability of closing (columns 4–6). This result is due to the fact that older firms might have more experience, larger stocks, and more resources in order to sustain their activities despite the decrease in sales or exports. The effect of being located in an industrial zone differs also across the two independent variables. While it increases the probability of being fully operational, it does not affect the probability of closure. This can be due to the fact that industrial zones, with their incentives and preferential treatment, can help firms benefit from existing externalities and thus sustain their operation.

Second, in terms of firm behavior, results in Table (columns 3 and 6) show that, worker training, innovation through investing in R&D and implementing good managerial practices increase the probability of being fully operational, whereas the same is not true for technology. Note that we use the combined technology variable and it is likely that certain aspects of technology adoption are more influential than others.

The result on innovation is consistent with a large body of literature (cf. Hall Citation1987; Esteve-Perez and Manez-Castillejo Citation2008; Damanpour Citation1996; Wolfe Citation1994; Gopalakrishnan and Damanpour Citation1997; Helmers and Rogers Citation2010; Garg, Walters, and Priem Citation2003). Similarly, it is standard in the literature that good managerial practices are essential in boosting firm survival and performance (cf. Delaney and Huselid Citation1996; Verbeeten Citation2008; Lakhal, Pasin, and Limam Citation2006). Krammer (Citation2021) shows that, for more than 11,000 firms from 28 countries both before and after COVID-19, firms with better management practices exhibit greater ability to adapt to the crisis. Additionally, the literature has long confirmed the crucial role of technology in firm survival (cf. Suarez and Utterback Citation1995, and more recent evidence from Europe in Wagner Citation2021). We are yet to observe the results when we disentangle the combined technology variable and add other variations on technology.

4.2. Extensions

We extend the previous analysis in three ways. First, we examine how behavioral effects on firm dynamics vary by firm size. Second, we analyse the different aspects of technology and good management practices to identify which of these aspects matter the most for firm resilience. Third, different sectors have been hit to varying degrees by both demand and supply side shocks (cf. Ando and Hayakawa Citation2022). We therefore examine the different extent to which shocks have been transmitted by sector.

Table interacts our behavioral variables of interest with pre-COVID firm size to investigate to what extent their effect varies by firm size. R&D and technology exert a larger positive effect on the likelihood of being fully operational the larger the firm size. On the other hand, while training and good managerial practices exercise a positive impact on the probability of being fully operational, their effect is independent of firm size. This result is plausible since larger firms are more likely to be able to incur the high fixed cost associated with investing in R&D and technology,Footnote7 but there are not such comparable high costs for management practices. In this variation, formality significantly reduces the likelihood of ever closing.

Table 3. Firms’ size and resilience.

A closer look at management practices shows that setting performance indicators or production targets increases the probability of being fully operational, but it does not affect that of closure. However, monitoring these indicators significantly increases the likelihood of being fully functional and reduces that of ever being closed, thus setting targets and indicators per se is not as effective as taking the further step of ensuring those indicators are actually being met (Table ). Monitoring implies assessing risks and factors that affect outcomes which results in updated objectives and production targets, allowing adjustments in product scope to build resilience.

Table 4. Management practices and firms’ resilience.

Regressions (1–8) in Tables and present the details of the combined technology variable (e.g. use of computers, the internet, internal information link networks … etc.). While some variables are insignificant and others are counter-intuitive, quality control in Egyptian manufacturing is the most important determinant. Quality control ensures streamlining production and guarantees that final products meet market requirements.

Table 5. Technology and firms’ resilience I.

Table 6. Technology and firms’ resilience II.

The effect of different components of R&D are shown in Tables and . These components can be divided into two groups (Aboushady and Zaki Citation2021). The first group relates directly to production innovation, which includes firm expenditure on R&D related to machines and products, and production processes. The second group pertains to auxiliary services related to the production process such as design and marketing. While R&D related to production is more important than auxiliary services, it requires more time and involves a much higher fixed cost to be effective. The majority of Egyptian firms in manufacturing cannot afford such high costs, and those who can have no incentive to make such investments, especially as they import the majority of their capital goods.

Table 7. R&D and firms’ resilience II.

Table 8. R&D and firms’ resilience II.

Our results show that all R&D components increase the likelihood of being fully functional (Table ). However, in contrast to some existing studies (e.g. Cefis and Marsili Citation2005), investing in auxiliary services is more effective in times of pandemic than R&D spending on products, processes and machines. That is, firms’ past adoption of new designs and innovative marketing strategies has potentially assisted them to better reach their consumer base and perhaps even engage with new potential consumers during crises (cf. Rangarajan et al. Citation2021). R&D in auxiliary services is, however, not significant for the probability of closure (Table ).

Regressions (1–6) of Tables and address our third extension of results. Here, we place food in a separate category on account of being the most resilient sector by far as shown in the data. We categorize the manufacture of pharmaceuticals, chemicals and computers as COVID-19 sectors. We believe that demand on these sectors has been favorable or has at worst remained stable since the start of the pandemic. We classify the manufacture of electrical equipment, machinery and equipment, motor vehicles and other manufacturing as non-traditional sectors. The remaining sectors are the traditional ones (e.g. textiles and clothing, leather … etc.).

Table 9. Sectoral characteristics and behavior I.

Table 10. Sectoral characteristics and behavior II.

The results show that the food and COVID sectors are more likely to be fully functioning post-COVID-19 compared to the reference category of traditional sectorsFootnote8; the latter were largely hit by both the demand and the supply shock. The same result is less conclusive for non-traditional sectors, which contain a mix of sectors that differ in shock exposure. The second main finding is that some behavioral variables matter for some sectors more than others do. For the non-traditional sectors, investing in innovation and adopting technology makes a significant contribution to firm dynamics. Non-traditional sectors with enhanced adoption of technology and investments in R&D are more likely to be fully functioning and less likely to have ever closed compared to traditional sectors, which rely relatively less on technology compared to their non-traditional counterparts. The effect of innovation and technology adoption in the food sector is counterintuitive (column 3 in Tables and ), possibly reflecting the non-technology intensive nature of that sector in Egypt.

As an exercise, we have also extended the analysis to interact the innate characteristics of the firm with its behavioral ones. An interesting result indicated that private firms that invest in innovation are more likely to be fully functional and less likely to have ever closed, and those that have provided worker training are also less likely to have ever closed (Table and A3 in the Appendix). Additionally, private firms are less likely to have ever closed when we use the aspect of setting performance indicators and production targets rather than the combined good management practice variable (Table in the Appendix).

4.3. Robustness checks

We test the robustness of our results in two ways. First, we take into consideration other potential channels that are likely to affect firm survival. On the one hand, we control for government support provided post-pandemic and introduce a shock variable to our regressors. On the other, we address the potential endogeneity of the behavioral variables. Although all behavioral variables are pre-COVID variables and thus already partially deal with endogeneity.

First, as aforementioned, the experiences of a number of countries have shown that public support can contribute significantly to firms’ survival and resilience during the COVID-19 pandemic (cf. Bennedsen et al. Citation2020; Lalinsky and Pál Citation2021; Kozeniauskas, Moreira, and Santos Citation2020). Thus, there is a need to examine whether our variables of interest remain robust in the face of received government support. In Egypt, post-COVID19 government support has focused predominately on short-term financial and monetary support measures designed to swiftly mitigate the damaging effects of the crisis. These include debt and tax relief measures and were received by about 84% of all firms receiving any post-COVID support (El-Haddad and Zaki Citation2022b, forthcoming). Table shows that, while the impact of government support is not statistically significant,Footnote9 investing in R&D, adopting good managerial practices, and providing worker training continue to be more or less effective with no significant changes from the baseline regression (see also El-Haddad and Zaki Citation2022c). The implication is that behavioral variablesFootnote10 matter more for more resilience than temporary measures such as crisis-induced government support.

Table 11. Government support and firm dynamics.

Second, in order to re-test the robustness of our results, we observe whether the results of our individual and behavioral characteristics hold even after we introduce a sector shock. Since the COVID-19 crisis has induced demand and supply side shocks that have transmitted differently depending on sector, it is important to learn whether the effect of the shock overshadows the effect of our behavioral variables on firm dynamics. Or instead, whether those variables remain significant thus pointing to the importance of adopting these practices in order to curb the negative effect induced by the COVID-19 pandemic.

To analyse the effect of the shock on our results, we construct a dummy variable that takes the value of one if the firm is in a sector, which has witnessed a negative production shock due to the COVID-19 crisis. For this, we use responses from the question: ‘By how much has your production changed on average compared to the last completed financial year prior to the pandemic’. The results show that the shock variable is significant with the effect in the expected direction. The bigger the shock the less likely is the firm to be fully functioning and the more likely it is to have closed at some earlier point (Table ). Similar to the government support results above, investing in R&D, adopting good managerial practices, and providing worker training continue to be more or less effective. R&D spending still has a negative and significant effect on the probability of closure, and both good management practices and providing worker training remain positive and significant for the probability of being fully functioning.

Table 12. Demand shock and firm dynamics.

Third, to control for endogeneity of the behavioral variables (technology, R&D, training, and good management practices), we instrument these variables by the share of the firms in the same industry and the same governorate (less the firm in question) which adopt that behavior. So in total there are four instruments, one for each of these four endogenous variables. In addition to that, we use a fifth instrument: the share of firms that are fully functioning (or, in the second model, that of those that have ever closed) in the same industry and the same governorate. The rationale behind these instruments is that in the same agglomeration (measured by the industry in a specific region), each firm has an incentive to adopt similar technologies and strategies because of fiercer competition from surrounding firms. A competitor's action or status creates an externality (cf. Romer Citation1986) inducing similar behavior by the other firms. For instance, if all neighboring firms adopt a new technology or type of innovation, the firm in question follows them in response to the pressure, in turn affecting its current and future operational status and survival. These instruments follow the principle that a valid instrument induces changes in the explanatory variables but has no ‘independent’ effect on the dependent variable. Its effect may be entirely through the other regressors.

While the results for investing in R&D and adopting good managerial practices continue to hold, those for the use of technology and worker training are counter-intuitive (Table ).Footnote11 Yet, both Sargan and Basmann tests show that the null hypothesis that all overidentifying restrictions are jointly valid, cannot be rejected, since the p-value is greater than the significance levels (e.g. 0.1 or 0.05) for the likelihood of fully functioning, but to a lesser extent than for the likelihood of ever having closed.

Table 13. Controlling for the endogeneity of behavioral variables.

5. Conclusion

We use data from the 2020/21 Egyptian Industrial Firm Behavior Survey (EIFBS) to examine determinants of firm resilience during the COVID-19 crisis. The COVID-19 crisis induced both demand and supply side shocks which are more far reaching than any crisis in living memory.

In this analysis, we distinguish between ‘status variables’ or ‘innate characteristics’ and those which are shaped by the behavior of the industrial firm such as managerial practices, investment in innovation or worker training and the adoption of technology. In contrast, ‘innate characteristics’ such as being informal, solely catering to the domestic market or being in the private sector are less endogenous.

Overall, our results are in line with Schumpeter’s (Citation1934) creative destructive theory in contrast to post-pandemic results from Bosio et al. (Citation2020). The market shows signs of ‘self-cleansing’, whereby the less efficient are more likely to close or downsize their activities in response to the crisis. The details are as follows:

In terms of innate characteristics, private sector firms are at a clear and consistently disadvantaged position in terms of firm dynamics. They are less likely to be fully functional and more likely to have ever closed since the start of the COVID-19 crisis. Equally, but less consistently, larger, formal and firms in industrial zones exhibit greater resilience to the shock compared to their counterparts. For larger firms this is true until we control for the behavioral factors that larger firms are more likely to adopt, which we find are driving the results we observe for size. These findings support the argument that public firms face a soft budget constraint, and that formal and larger firms are able to sustain their activities in times of crisis on account of their demonstrated resilience.

The existing literature suggests that the ability to adapt to market conditions is a crucial determinant of firm survival. Consistent with this literature, our results confirm that pre-COVID behavioral characteristics matter for firm dynamics. The adoption of good managerial practices, investment in innovation (R&D) and in worker training lead to greater resilience and firm ability to adapt more effectively and thus better cope with the shock.

In terms of sectors, the manufacture of food and the ‘COVID sectors’ – pharmaceuticals, chemicals and the manufacture of computers and electronics – show much more resilience compared to the traditional sectors (e.g. textiles and clothing). The latter have been strongly hit by the crisis; in contrast, ‘COVID sectors’ experienced increased demand on their products, manifesting itself in a positive shock. Food is the most resilient sector of all.

There are some nuances pertaining to firm size and sector. The first is that the larger the size of the firm the larger the positive effect of R&D and technology adoption. In contrast, while worker training and good managerial practices exercise a positive impact on firm dynamics their effect is independent of firm size. This is plausible as larger firms are more likely to incur the high fixed cost associated with investing in R&D and technology whilst there aren't such comparable high costs for management practices. The second is that some behavioral variables matter for some sectors more than others. For the non-traditional sectors, investing in innovation and adopting advanced technology makes a significant contribution to firm dynamics compared to traditional sectors, which rely relatively less on technology.

Finally, controlling for the shock and addressing the potential endogeneity of the behavioral variables’ only slightly mute the main findings. That is, behavioral characteristics exert a significant positive effect on firms’ ability to adapt to changing market conditions and thus cope with the crisis.

From a policy perspective, the results presented in this paper illustrate the fact that the private sector in Egypt continues to face a number of institutional and competition-related barriers that hinder its expansion (World Bank Citation2020). More generally, the results demonstrate the pre-existing fragilities of the private, smaller, informal and, more generally of the lower productivity firms of the manufacturing sector. There is a dire need for reforms across Egyptian manufacturing to address the underlying structural constraints that limit firms’ productivity. Such reforms include an effective competition policy, eliminating the ‘soft budget constraint’ as well as proper investment in education and in health and effectively addressing taxation and the business environment.

This paper also points to clear conclusions as to buffers of firm survival in the presence of shocks. Improving the digital infrastructure – including coverage and outreach – will improve resilience and ability to withstand shocks. Moreover, it is important to increase R&D spending at both the national level and at the level of the firm. Bianchini, Llerena, and Martino (Citation2019) show that public support for R&D can help private sector firms, especially when they are constrained by lower quality institutions. Such support lowers the uncertainty firms’ face, thus encouraging them to invest more in innovation, worker training and in technology. It is also important for government to support the private sector through reskilling programs that promote the complementarity between labor skills and technologies (Ndung’u and Signé Citation2020; Ramzy and Zaki Citation2021).

Finally, firms in industrial zones have done better. The Egyptian government aims to attract foreign investment in and develop industries on a ‘Cluster Based Policy’. These clusters may indeed enable industries to achieve higher productivity by establishing R&D centers and creating efficient sectoral clusters to generate externalities and increase firms’ resilience for future shocks.

Acknowledgements

We are grateful to Dr. Zakaria Othman for undertaking the sampling. Thanks are also due to Marian Adel for superb research assistance and diligence. Our thanks extend to Ismail Umut and Alina Petrova.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 For example, Hall (Citation1987); Esteve-Perez and Manez-Castillejo (Citation2008); Damanpour (Citation1996); Wolfe (Citation1994); Gopalakrishnan and Damanpour (Citation1997); Helmers and Rogers (Citation2010); Bourletidis and Triantafyllopoulos (Citation2014) for SMEs; Giovannetti, Ricchiuti, and Velucchi (Citation2011); Suarez and Utterback (Citation1995); and more recently Muzi et al. (Citation2021) with evidence from Europe in Wagner (Citation2021).

2 Data will be placed in the public domain during the course of the coming year.

3 Precisely between November 19th 2020 and the 5th of February 2021.

4 Only four modules are slightly different. The main difference is that for temporarily closed or closed firms there are no values for current variables such as production, exports, employment or revenues.

5 Given that our innate firm characteristics might be collinear, Table in the Appendix shows that the variance inflation factor is very low (less than ten) and thus there no evidence of multi-collinearity.

6 Results available from the authors upon request.

7 Such as long-term expenditure on hardware depreciation, new equipment, new software … etc.

8 Traditional sectors are the reference category.

9 In a companion paper (El-Haddad and Zaki Citation2022b) on the allocation and effectiveness of post-COVID government support, we control for the endogeneity of firm level received support. Our results remain robust and are available upon request.

10 These are firm level characteristics, other papers have undergone cross country analysis and have found that country specific characteristics such as the degree of international financial integration which in itself depends on the country's quality of economic and legal institutions can influence sectoral comparative advantages (Liang and Lin Citation2022).

11 The first stage of the IV regression is given in Tables A5 and A6 in the Appendix. We run similar regressions where each endogenous variable is instrumented by all the shares of behavioral variables simultaneously and our results remain robust.

References

- Aboushady, N., and C. Zaki. 2019. “Investment Climate and Trade Margins in Egypt: Which Factors Do Matter?” Economics Bulletin 39 (4): 2275–2301. https://EconPapers.repec.org/RePEc:ebl:ecbull:eb-19-00666.

- Aboushady, N., and C. Zaki. 2021. “Do Exports and Innovation Matter for the Demand of Skilled Labor?” International Review of Applied Economics 35 (1): 25–44. doi:10.1080/02692171.2020.1822298

- Ando, M., and K. Hayakawa. 2022. “Does the Import Diversity of Inputs Mitigate the Negative Impact of COVID-19 on Global Value Chains?” The Journal of International Trade & Economic Development 31 (2): 299–232. doi:10.1080/09638199.2021.1968473

- Ayadi, R., G. Giovannetti, E. Marvasi, G. Vannelli, and C. Zaki. 2021. “Demand and Supply Exposure through Global Value Chains: Euro-Mediterranean Countries During COVID.” The World Economy 45 (3): 637–656. doi:10.1111/twec.13156.

- Bachas, Pierre, Anne Brockmeyer, and Camille Semelet. 2020. “The Impact of COVID-19 on Formal Firms: Micro Tax Data Simulations Across Countries.” World Bank Policy Research Working Paper 9437. Washington, DC: World Bank.

- Bennedsen, M., B. Larsen, I. Schmutte, and D. Scur. 2020. “Preserving Job Matches During the COVID-19 Pandemic: Firm-level Evidence on the Role of Government Aid (No. 588).” GLO Discussion Paper.

- Bianchini, S., P. Llerena, and R. Martino. 2019. “The Impact of R&D Subsidies Under Different Institutional Frameworks.” Structural Change and Economic Dynamics 50: 65–78. doi:10.1016/j.strueco.2019.04.002

- Bloom, N., R. S. Fletcher, and E. Yeh. 2021. “The Impact of COVID-19 on US Firms.” Working Paper No. w28314. National Bureau of Economic Research.

- Bosio, Erica, Simeon Djankov, Filip Jolevski, and Rita Ramalho. 2020. “Survival of Firms During Economic Crisis.” World Bank Policy Research Working Paper 9239. Washington, DC: World Bank.

- Bourletidis, K., and Y. Triantafyllopoulos. 2014. “SMES Survival in Time of Crisis: Strategies, Tactics and Commercial Success Stories.” Procedia - Social and Behavioral Sciences 148: 639–644. doi:10.1016/j.sbspro.2014.07.092

- Cefis, E., and O. Marsili. 2005. “A Matter of Life and Death: Innovation and Firm Survival.” Industrial and Corporate Change 14 (6): 1167–1192. doi:10.1093/icc/dth081

- Cefis, E., and O. Marsili. 2019. “Good Times, Bad Times: Innovation and Survival Over the Business Cycle.” Industrial and Corporate Change 28 (3): 565–587. doi:10.1093/icc/dty072

- Cucculelli, M., and V. Peruzzi. 2020. “Post-crisis Firm Survival, Business Model Changes, and Learning: Evidence from the Italian Manufacturing Industry.” Small Business Economics 54 (2): 459–474. doi:10.1007/s11187-018-0044-2

- Damanpour, F. 1996. “Organizational Complexity and Innovation: Developing and Testing Multiple Contingency Models.” Management Science 42 (5): 693–716. doi:10.1287/mnsc.42.5.693

- Delaney, J. T., and M. A. Huselid. 1996. “The Impact of Human Resource Management Practices on Perceptions of Organizational Performance.” Academy of Management Journal 39: 949–969. doi:10.2307/256718.

- Demertzis, M., and G. Maslloren. 2020. “The Cost of Coronavirus in Terms of Interrupted Global Value Chains.” Bruegel (think tank), March 9. https://www.bruegel.org/2020/03/the-cost-of-coronavirus-in-terms-of-interrupted-global-value-chains/.

- Eibl, M. F., and A. Malik. 2016. “The Politics of Partial Liberalization: Cronyism and Non-tariff Protection in Mubarak's Egypt.” Working Paper Series 2016–27. Oxford: Center for the Study of African Economics (CSAE).

- El-Haddad, A. 2015. Breaking the Shackles: The Structural Challenge of Growth and Transformation for Egypt's Industrial Sector, in Structural Transformation and Industrial Policy: A Comparative Analysis of Egypt, Morocco, Tunisia and Turkey, Vol. 2 & 3, European Investment Bank. 69–107. http://www.eib.org/infocentre/publications/all/femip-study-structural-transformation-and-industrial-policy.htm.

- El-Haddad, A. 2020a. “Discussion of Issues and Options for Covid-19 Response by BMZ for Egypt.” Opinion Piece for the German Ministry of International Cooperation (BMZ), Statement for the BMZ. Unpublished.

- El-Haddad, A. 2020b. “Redefining the Social Contract in the Wake of the Arab Spring: The Experiences of Egypt, Morocco and Tunisia.” World Development 127: 104774. https://authors.elsevier.com/sd/article/S0305750X19304231. doi:10.1016/j.worlddev.2019.104774

- El-Haddad, A., and M. M. Gadallah. 2021. “The Informalization of the Egyptian Economy (1998–2012): A Driver of Growing Wage Inequality.” Applied Economics 53 (1): 115–144. doi:10.1080/00036846.2020.1796917

- El-Haddad, A., and C. Zaki. 2022a. “Firm Closures and Performance in a Time of Pandemic.” ERF Working Paper Series, No. 1530, Cairo: ERF. Firm Closures and Performance in a Time of Pandemic – Economic Research Forum (ERF).

- El-Haddad, A., and C. Zaki. 2022b. “Post COVID-19 Firm-Level Government Support in Egypt: Uneven Allocation and Unequal Effects.” ERF Working Paper Series. Cairo: ERF.

- El-Haddad, A., and C. Zaki. 2022c. “Firm Dynamics in Times of COVID: Evidence from Egyptian Firms.” ERF working paper series. No. 1586, Cairo.

- Eldeep, C., and C. Zaki. 2021. “The Unfinished Business of Stabilization Programs CGE Model of Egypt.” EMNES Working Paper No 54.

- Esteve-Perez, S., and J. A. Manez-Castillejo. 2008. “The Resource-based Theory of the Firm and Firm Survival.” Small Business Economics 30 (3): 231–249. doi:10.1007/s11187-006-9011-4

- Feng, L., Z. Li, and D. L. Swenson. 2016. “The Connection Between Imported Intermediate Inputs and Exports: Evidence from Chinese Firms.” Journal of International Economics 101: 86–101. doi:10.1016/j.jinteco.2016.03.004

- Fernandes, Ana M., and Alberto E. Isgut. 2005. “Learning-by-doing, Learning-by-exporting, and Productivity: Evidence from Colombia.” World Bank Policy Research Working Paper 3544. Washington, DC: World Bank.

- Garg, V. K., B. A. Walters, and R. L. Priem. 2003. “Chief Executive Scanning Emphases, Environmental Dynamism, and Manufacturing Firm Performance.” Strategic Management Journal 24 (8): 725–744. doi:10.1002/smj.335

- George, G., and A. J. Bock. 2011. “The Business Model in Practice and its Implications for Entrepreneurship Research.” Entrepreneurship Theory and Practice 35 (1): 83–111. doi:10.1111/j.1540-6520.2010.00424.x.

- Giovannetti, G., G. Ricchiuti, and M. Velucchi. 2011. “Size, Innovation and Internationalization: A Survival Analysis of Italian Firms.” Applied Economics 43 (12): 1511–1520. doi:10.1080/00036840802600566

- Gopalakrishnan, S., and F. Damanpour. 1997. “A Review of Innovation Research in Economics, Sociology and Technology Management.” Omega 25 (1): 15–28. doi:10.1016/S0305-0483(96)00043-6

- Greenaway, D., and R. Kneller. 2008. “Exporting, Productivity and Agglomeration.” European Economic Review 52 (5): 919–939. doi:10.1016/j.euroecorev.2007.07.001

- Grover, A., and V. J. Karplus. 2021. “Coping with COVID-19: Does Management Make Firms More Resilient?” World Bank Policy Research Working Paper 9514. Washington, DC: World Bank.

- Guerrero-Amezaga, M. E., J. E. Humphries, C. A. Neilson, N. Shimberg, and Gabriel Ulyssea. 2022. “Small Firms and the Pandemic: Evidence from Latin America.” Journal of Development Economics 155: 102775. doi:10.1016/j.jdeveco.2021.102775

- Hall, B. H. 1987. “The Relationship Between Firm Size and Firm Growth in the US Manufacturing Sector.” The Journal of Industrial Economics 35: 583–606. doi:10.2307/2098589

- Helmers, C., and M. Rogers. 2010. “Innovation and the Survival of New Firms in the UK.” Review of Industrial Organization 36 (3): 227–248. doi:10.1007/s11151-010-9247-7

- Kozeniauskas, Nicholas, Pedro Moreira, and Cezar Santos. 2020. “COVID-19 and Firms: Productivity and Government Policies.” CEPR Discussion Paper No. DP15156.

- Krafft, C., R. Assaad, and M. A. Marouani. 2021. “The Impact of COVID-19 on Middle Eastern and North African Labor Markets: Glimmers of Progress but Persistent Problems for Vulnerable Workers a Year into the Pandemic.” Economic Research Forum Policy Brief No. 57. Cairo, Egypt.

- Krammer, S. M. 2021. “Navigating the New Normal: Which Firms Have Adapted Better to the COVID-19 Disruption?” Technovation 110 (4): 102368. doi;10.1016/j.technovation.2021.102368.

- Lakhal, L., F. Pasin, and M. Limam. 2006. “Quality Management Practices and their Impact on Performance.” International Journal of Quality and Reliability Management 23: 625–646. doi:10.1108/02656710610672461

- Lalinsky, T., and R. Pál. 2021. “Efficiency and Effectiveness of the COVID-19 Government Support: Evidence from Firm-level Data (No. 2021/06).” EIB Working Papers.

- Liang, Claire Y. C., and Pei-Chien Lin. 2022. “Financial Integration and the Comparative Advantage of Exports.” The Journal of International Trade & Economic Development 31 (8): 1127–1148. doi:10.1080/09638199.2022.2073603

- Melitz, J. 2003. “The Impact of Trade on Intra-industry Reallocations and Aggregate Industry Productivity.” Econometrica 71 (6): 1695–1725. doi:10.1111/1468-0262.00467

- Miyakawa, D., K. Oikawa, and K. Ueda. 2021. “Firm Exit During the Covid-19 Pandemic: Evidence from Japan.” Journal of the Japanese and International Economies 59: 101118. doi:10.1016/j.jjie.2020.101118

- Muzi, S., F. Jolevski, K. Ueda, and D. Viganola. 2021. “Productivity and Firm Exit During the COVID-19 Crisis. Cross-country Evidence.” World Bank Policy Research Working Paper 9671. Washington, DC: World Bank.

- Ndung’u, N., and L. Signé. 2020. The Fourth Industrial Revolution and Digitization will Transform Africa into a Global Powerhouse. Brookings Institute, January 8. https://www.brookings.edu/research/the-fourth-industrial-revolution-and-digitization-will-transform-africa-into-a-global-powerhouse/.

- Pansiri, J., and Z. T. Temtime. 2008. “Assessing Managerial Skills in SMEs for Capacity Building.” Journal of Management Development 27 (2): 251–260. doi:10.1108/02621710810849362

- Ramzy, M., and C. Zaki. 2021. “Trade Integration and South-South Cooperation: How Does Digitalization Matter?” Working Paper XX. New York: United Nations Office for South-South Cooperation.

- Rangarajan, D., A. Sharma, T. Lyngdoh, and B. Paesbrugghe. 2021. “Business-to-business Selling in the Post-COVID-19 Era: Developing an Adaptive Sales Force.” Business Horizons 64 (5): 647–658. doi:10.1016/j.bushor.2021.02.030

- Romer, M. Paul. 1986. “Increasing Returns and Long-Run Growth.” The Journal of Political Economy 94 (5): 1002–1037. doi:10.1086/261420

- Rossi, M. 2016. “The Impact of age on Firm Performance: A Literature Review.” Corporate Ownership and Control 13 (2-1): 217–223. doi:10.22495/cocv13i2c1p3

- Schumpeter, J. 1934. “Depressions: Can We Learn from Past Experience?” In Economics of the Recovery Program, edited by D. Brown et al. New York: McGraw-Hill.

- Sharma, A., A. Adhikary, and S. B. Borah. 2020. “Covid-19′ s Impact on Supply Chain Decisions: Strategic Insights from NASDAQ 100 Firms Using Twitter Data.” Journal of Business Research 117: 443–449. doi:10.1016/j.jbusres.2020.05.035

- Suarez, F. F., and J. M. Utterback. 1995. “Dominant Designs and the Survival of Firms.” Strategic Management Journal 16 (6): 415–430. doi:10.1002/smj.4250160602

- Verbeeten, F. H. M. 2008. “Performance Management Practices in Public Sector Organizations: Impact on Performance.” Accounting, Auditing & Accountability Journal 21 (3): 427–454. doi:10.1108/09513570810863996

- Wagner, J. 2021. With a Little Help from My Website Firm Survival and Web Presence in Times of COVID-19 – Evidence from 10 European Countries. University of Lüneburg Working Paper Series in Economics 339. Lüneburg: Leuphana Universität Lüneburg, Institut für Volkswirtschaftslehre.

- Wolfe, R. A. 1994. “Organizational Innovation: Review, Critique and Suggested Research Directions.” Journal of Management Studies 31 (3): 405–431. doi:10.1111/j.1467-6486.1994.tb00624.x

- World Bank. 2020. Creating Markets in Egypt: Realizing the Full Potential of a Productive Private Sector. Country Private Sector Diagnostic. Washington, DC: Country Private Sector Diagnostic, World Bank Group. Available online at https://www.ifc.org/wps/wcm/connect/af513599-08b4-45a4-b346-1a44de58cda6/CPSD-Egypt.pdf?MOD=AJPERES&CVID=npT1-BJ.

- Zaki, C. 2022. “Why Don’t Firms Grow? Evidence from Egypt.” International Journal of Economic Policy in Emerging Economies. doi:10.1504/IJEPEE.2021.10036106.

Appendix

Table A1. Testing for multi-collinearity.

Table A2. Innate characteristics with behavioral traits I.

Table A3. Innate characteristics with behavioral traits II.

Table A4. Innate characteristics versus behavioral traits (setting performance indicators BC).

Table A5. First stage regression (ever closed).

Table A6. First stage regression (fully functioning).