ABSTRACT

Despite studies on the perceptions of benefits and costs of joining a professional body little empirical evidence is available on the deciding factors for joining one specific professional body, let alone multiple ones in an emerging economy. Using the Theory of Planned Behaviour (TPB) theoretical lens, this paper investigates, through surveys, the factors affecting the decisions by final-year university students and associate members to affiliate with one or more professional bodies in Vietnam. This study used a quantitative approach design. Questionnaires were sent to students studying an undergraduate accounting degree in Vietnam (N = 167) and candidates completing the foundations levels of a foreign professional accounting body programme in Vietnam (N = 145). The results show that attitude is the most significant factor in explaining the intentions of accounting students and foundation candidates to affiliate with a professional accounting body while subjective norm is only marginally significant and perceived behavioural control is not significant. The comparison between those who intend to professionally affiliate and those who do not reveal that the main factors affecting the decision are the reputation of the professional body, career and networking opportunities, international recognition, professional status, international mobility opportunities, perceived expertise of members and continuing professional development.

Introduction

Professions and professionalisation have been a focal point of inquiry from a number of perspectives. They emphasise ‘the peculiarities of particular professions or the special features of the professions in a particular historical context’ (Siegrist, Citation2002, p. 12154). Another approach is to look at the uniqueness of each profession, or its specific characteristics, regardless of time. The latter perspective invariably argues that professions and professionalisation processes have their roots in an almost standardised Anglo-American model, which provides a blueprint for professions to acquire their coveted superior status and which is independent of specific contexts (Johnson, Citation1982). Yee and West (Citation2010, p. 2), on the other hand, emphasise that ‘occupational status and the outcomes of professionalisation processes are contingent upon the particular cultural, political and socio-economic setting within which an occupation is constituted.’ Most emerging economies (EEs) set up their own professional bodies and higher learning institutions in the past few decades and they are often under-resourced and have a dearth of expertise. As a result, many institutions affiliated themselves with Western associations and links (as accredited associates) and Western higher education institutions to gain international recognition (Bennell & Pearce, Citation2003; Yapa, Citation2006, Citation2010; Yapa et al., Citation2016). In the cases of non-settler colonies, the setting up of professional bodies was often part of wider, state-sponsored, human resource development programme (Annisette, Citation2000).

Accounting in Vietnam

As in many EEs, accounting graduates and practitioners in Vietnam have choices with regard to their professional affiliation. In Vietnam, the largest foreign professional accounting body in terms of members is the UK-based Association of Chartered Certified Accountants (ACCA) with more than 8500 students and 700 full members as of June 2016 (ACCA, Citation2016). ACCA opened its representative office in 2002, becoming the first international professional organisation in Vietnam. The initial push for the introduction of international qualifications in Vietnam came from the Big 4 accounting firms who needed internationally qualified audit practitioners to review foreign companies. The next largest foreign professional accounting body in Vietnam is CPA Australia with 500 members and 700 foundation candidates. These foreign professional bodies compete with local professional bodies such as the Vietnam Accounting Association (VAA) with over 12,000 members, the Vietnam Association of Certified Public Accountants (VACPA) with 1100 members, the State Audit of Vietnam (SAV) and the Vietnam Tax Consultants Association (Bui, Citation2011). Traditionally in Vietnam, the state is heavily involved as in many EEs (See Hopper et al., Citation2017; Sian, Citation2011; Uche, Citation2002; Yapa, Citation1999, Citation2003, Citation2010; Yapa et al., Citation2016) in the regulation of accounting.

Surprisingly, while EEs that were former British colonies followed the British accounting rules and conventions even after their independence and mainly due to international reputation (Bakre, Citation2005; Yapa, Citation2006, Citation2010), accounting in Vietnam, which was a French colony, is regulated by the Ministry of Finance (MoF) and ‘was not established by the French during their domination but rather by the independent Vietnamese Government to serve the needs of the post-war economy for building socialism’, for example, to report statistics and collect taxes (Bui et al., Citation2011, p. 4). Although the renovation period (post-1986) saw a lot of changes in the accounting landscape, Bui (Citation2011) argues that there was still no accounting profession in Vietnam at that time as the only professional association, the VAA, had no regulatory power (accounting rules and licences were issued by the MoF) and was effectively acting only as a social organisation. The end of the 1990s saw a milestone reforms among different stakeholders reached by accounting in Vietnam, with VAA membership of the International Federation of Accountants (IFAC) signalling international recognition of Vietnamese accounting (Bui, Citation2011; Bui et al., Citation2017; Bui & Porter, Citation2010). However, each year many Vietnamese accounting graduates encounter difficulty in securing suitable employment. In addition to a surplus of graduates, employers complain that they have difficulties in finding graduates with the requisite knowledge and skills (Bodewig et al., Citation2014). In summary, it can be said that the professionalisation of accounting and auditing in Vietnam is very recent, for example, VACPA was only created in 2005.

Unlike accounting associations in China, however, communist ideology is not embedded in the charter in Vietnamese associations, which are not, by definition, political organisations. However, the state still maintains a strong grip on the accounting profession as with most other professions, in general through regulations issued by the respective ministries, creating markets for and maintaining control over services provided. The motivation of this paper emerges from the recent evidence in EEs that shows changing state-led priorities on accounting professionalisation. For example, analysing the Egyptian state’s nativist policy for the registration of accountants, the study tracks attempts of professional reform through different socio-political regimes and suggests a new form of professional closure – i.e. selective market closure (Ghattas et al., Citation2020).

The study of the accounting profession through membership of professional associations in Vietnam is important as it departs from the traditional Anglo-American professionalisation model and contributes to the literature on the development of accounting in EEs. Additionally, Vietnam offers a model of professionalisation with intricate dependencies with the state and thus allows for some comparison with other state-controlled transitional economies.

Using the Theory of Planned Behaviour (TPB), the paper’s main aim is to examine what the key factors that influence students’ choices to select a professional accounting association in a emerging and state-controlled transitional economy? It is intended to explain what drives future and current practitioners to choose one or more professional bodies, as well as their decisions to remain with those bodies or to cease affiliation. The data used in this study were drawn from two discrete cohorts: students studying an undergraduate accounting degree in Vietnam (N = 167) and candidates completing the foundations levels of a foreign professional accounting body programme in Vietnam (N = 145).

Contribution

This study makes several major contributions to previous research. First, this study fills a gap in the existing literature on the use of TPB (Ajzen, Citation1991) by extending TPB into the accounting field. It confirms that positive or negative attitudes towards accounting (majoring in accounting, choosing a general or specific career in accounting or affiliating with a professional accounting body) explain individuals’ intentions, and thus behaviour. This contrasts with findings of previous studies (see, for example, Ajzen, Citation2002) that attitude and subjective norm are overlapping rather than distinct constructs. The originality of our study is that perceived behavioural control (PBC) is found to be not significant for either group. This tends to challenge prior research (see, for example, Armitage and Conner (Citation2001)), suggesting that PBC may overlap with attitude.

Second, this study contributes to the literature on professionalisation of accounting in state-controlled EE and serves to depart from an Anglo-American model of professionalisation with the central tenet of self-regulation. The professionalisation process of accounting and auditing in Vietnam seems to be one where foreign professional accounting bodies do not compete with local ones but provide benefits (career and networking opportunities, quality programmes and international recognition amongst others) that are yet to be found within local bodies. These local professional bodies are in their infancy, and it is, therefore, advisable for them to think that healthy partnerships and mutual recognition schemes with foreign bodies would help develop the local accounting profession.

Third, this study contributes to understanding of the drivers of prospective members’ choices in an EE. It can therefore be used by stakeholders such as accounting associations and universities to inform strategies to counteract the diminishing numbers of accounting students in those environments. It thus provides insights into potential options to rectifying the shortage of qualified accountants, as well as contributing to professional closure in an EE. In addition, this research provides new evidence about drivers of professional affiliation, and builds on the limited previous studies into career and professional association choice in EE. These findings are thus critical to the accounting and auditing profession in EE’s such as Vietnam where there is a shortage of qualified accountants.

The paper is structured as follows. The next section includes a critique of the literature relating to the professionalisation and the development of professions in the context of accounting professions, alternative pathways to the profession, accounting as a career choice and perception of the benefits and costs of professional affiliation. The following section establishes the purpose of this study and the related hypothesis. This is followed by a description of the research approach for the study, including sampling techniques and the development and pre-testing of the instrument. The hypothesis is discussed within the context of the results prior to the final discussions of the implications, where a summary of conclusions are discussed in order to contextualise the conclusions.

Literature review

Professionalisation of accounting

Larson (Citation1977, p. xvi) defines professionalisation as ‘the process by which producers of special services sought to constitute and control a market for their expertise’. Factors that denote professionalisation include the formation of a professional association or body (Carnegie & Edwards, Citation2001; Mihret et al., Citation2012); however, it is not the formation of the professional association itself that creates the profession but the collective social mobility and/or closure of its members. Collective social mobility refers to members acquiring a higher social status as a group, while closure refers to ‘how members of an interest group seek market dominance by monopolising social and economic opportunities and closing off opportunities to outsiders’ (Chua & Poullaos, Citation1998, p. 156). According to Willmott (Citation1986, p. 556), professional associations are primarily, but not exclusively, political bodies whose purpose is to define, organise, secure and advance the interests of their most vocal and influential members. Privileges associated with membership include market monopoly, self-regulation and higher social status.

Professionalisation is viewed as the interaction between professionals and other stakeholders in society (Abbott, Citation1988). Professions begin when people start doing full-time the thing that needs doing. But then the issue of training arises, pushed by recruits or clients. Schools are created. New schools immediately seek affiliation with them. Higher standards, training and earlier commitment to the profession develop. Then, the teaching professionals, along with their first graduates, combine to promote and create a professional association.

In their study Bagley et al. (Citation2012) using TPB lens, examined the reasons why some accountants seek careers at Big 4 firms, while other accountants seek careers at non-Big 4 firms. Overall, they found that students’ perceptions in joining Big 4 are more limited and are similar to those of accounting professionals. The study findings also indicate that firm prestige and firm recognition become less important to accounting professionals over time, while firm atmosphere, firm tone, and work-life balance become more important. In investigating audit and tax career paths in public accounting (Dalton et al., Citation2014) indicate that accounting students who plan to pursue careers in the tax profession perceive that they will have a more stable daily routine, develop more specialised skills, and build more collaborative client relationships if they work in tax professional path (as opposed to audit).

Extensive literature exists on the development of imperial or colonial accounting as a means of controlling the empire’s resources from a distance whether it is British (Chua & Poullaos, Citation1998, Citation2002; Sian, Citation2011), American (Dyball et al., Citation2007) or Portuguese (Gomes et al., Citation2013). As was argued earlier, if the Anglo-American pattern is regarded as the model for professionalisation projects, what of other models where the accounting profession is not self-regulated. Could it be that there is in fact no one-size-fits-all model and that the characteristics of professionalisation projects are deeply rooted in social, economic and cultural factors, as demonstrated by MacDonald (Citation1985).

Most professionalisation projects in EEs do not follow an established Anglo-American pattern and do not fall into one of the neatly drawn categories of collective social mobility or closure as described above for developed countries (Hopper et al., Citation2017; Sian, Citation2011; Uche, Citation2002; Yapa, Citation2010, Citation2003, Citation1999; Yapa et al., Citation2016). In EEs the common denominator seems to be state intervention in the accounting profession. A recent study by Mihret et al. (Citation2019) examined accounting professionalisation in Iran to understand state-controlled professional accounting organisation in response to transnational pressure. In particular in socialist or centrally planned economies, studies such as Hao (Citation1999), Seal et al. (Citation1996), Yapa and Hao (Citation2007) and Yee (Citation2012) suggest that when an economy moves away from a centrally planned economy, such as in Vietnam, the need for the professionalisation of financial services emerges. Yapa et al. (Citation2016) explore the field of accounting as a nexus between the rise of industrial societies, strategies of elites to preserve and reproduce privilege, practices of state control, and the external forces of colonisation and globalisation in Cambodia – Southeast Asia. In a centrally planned economy, accounting serves as a tool for the state to administer and control resources whereas market economies place the locus of control and emphasise on accountability and decision making in the hands of the market and therefore managers and shareholders, thus an increased need for professional standards of accounting is a logical evolution.

The professionalisation project in EEs can also be defined by the quality of accounting education and training and its capacity (Bui et al., Citation2017) to include or exclude potential candidates rather than with respect to collective social mobility or closure. Yapa (Citation2000, p. 297) notes that ‘almost all developing countries which have been colonies under powerful Western rulers for a considerable length of time inherited their accounting education from a colonial system’. Consequently, most of these countries that relied on these ‘imported’ training methods failed to adapt to their changing economic context.

Alternative pathways to the accounting profession

In Vietnam, as in many other countries entry into the accounting profession is diverse and can be facilitated through three typical pathways:

Completing a university accounting degree accredited by the professional bodies followed by professional level of qualification run by those same professional bodies.

Completing an accounting conversion course, usually a Master’s degree with eight or more subjects (for non-accounting business graduates).

For non-accounting business graduates direct entry via completion of foundation and professional levels through a professional accounting body.

In Western countries, traditionally the first pathway was the most widespread but the other two pathways are growing in popularity, in particular for non-accounting students with the introduction of ‘alternative pathways’. The aim for the professional accounting bodies is clearly to take control not only of the examination process but of the knowledge dissemination as well.

The available accounting pathways can metaphorically be summarised as follows:

there are three types of accounting education … . Within the university accounting education makes a person capable of being an accountant – the intellectualization of accounting. Within the workplace accounting education makes a person ready to be an accountant – the vocationalization of accounting. Within the profession accounting education enables a person to be professional in being an accountant – the professionalization of accounting. (ICAA, Citation2010)

A justification of these new pathways was lamented by the ICAA (Citation2010, p. 66) when it wrote: ‘The Big 4, who pushed hard for the Institute’s alternate pathway, are arguably ‘professional services’ rather than ‘accounting’ firms and seek the flexibility to mix various forms of expert labour to suit the circumstances of particular engagements.’ One of the main contributing factors to the diversification of entrants profiles has been ‘a perceived need to increase opportunities for attracting individuals with more ‘breadth and depth’ to enter the profession’ (Lane, Citation2007, p. 41). New entrant diversity was not only to satisfy the demands of the Big 4 for more variety and flexibility but also to ‘cure’ the negative image of the accountants as being procedural, mechanical, inflexible and lacking communication skills.

In complete contrast to the increasing number of pathways to the accounting profession in developed economies, in Vietnam, the main entry to the accounting profession is through a university degree (private and private/public higher education is articulated in government policy). Vietnam and several other Asian countries consider that public and private higher education are a matter of government policy (ICAA, Citation2010) with private providers proliferating over the last decade. In addition, foreign accounting bodies such as ACCA and CPA do offer alternative pathways in Vietnam. CPA Australia offers both foundation level and professional level exams through both their Hanoi and Ho Chi Minh City offices. Those enrolled in alternate professional pathways have not featured as an area of investigation that is featured in the literature to date.

Accounting as a career choice

Numerous studies from researchers around the world point towards a global shortage of suitably qualified accountants. This issue was identified as early as the 1990s and was already predicted to be long lasting (Gul et al., Citation1989). For example, a report from the Department of Education, Training and Youth Affairs in Australia (cited in Jackling & Calero, Citation2006) found that although the number of students selecting a business degree was increasing, the proportion of students choosing accounting as a major was declining, leading to fierce competition in the recruitment of accounting graduates. Despite an increase in the number of accounting graduates in absolute value, this number falls short of the demand for suitably qualified accountants (Birrell & Betts, Citation2018). A 2015 report from the Department of Employment Australia shows that despite accountants technically not being in shortage, employers are still dissatisfied and perceive a mismatch between their needs and the applicants’ skills and would rather wait for the ideal candidate than hire someone they judge unsuitable (Department of Employment Australia, Citation2015). Similar trends are witnessed in the USA (Albrecht & Sack, Citation2000; Simons et al., Citation2003), the UK (Marriot & Marriot, 2003), Southeast Asia, (Berquist et al., Citation2019 ; Pham & Thompson, Citation2019) and South Africa (Myburgh, Citation2005).

Studies in the USA, the UK and Australia show that enrolment numbers in accounting are dropping because of a poor perception of the profession (Albrecht & Sack, Citation2000) and the attractiveness of alternative business majors such as finance and business advisory services. The perceived overemphasis on numeracy skills, perpetuated by traditional bookkeeping tasks, financial statements preparation and tax return completion is not helping promote the profession as challenging or intellectually rewarding, which in turns prevents bright students from selecting accounting as a major (Jackling, 2006; Lowe & Simons, Citation1997). This emphasis on numeracy even in times where accountants in general and auditors in a particular deal more and more with advisory services stems from the origins of the profession where accountants and auditors mostly dealt with numbers and rules (Jackling, Citation2002; Jackling & Calero, Citation2006).

To date, there is no general agreement on what type of factors are important in choosing a career in accounting, with some studies refuting the idea that extrinsic factors are decisive (Jackling & Calero, Citation2006; Sidaway et al., Citation2013) and others citing low entry salaries as adverse factors in an accounting career choice (Tan & Laswad, Citation2006). Studies such as Birrell and Betts (Citation2018), Sugahara et al. (Citation2006) and Law (Citation2010) provide evidence that some Asian countries still consider a career in accounting attractive and prestigious.

Studies such as Inglis et al. (Citation2011) and Salazar-Clemeña (Citation2002) show that the influence of important referents such as parents or professors and the positive or negative experience of an initial exposure to accounting (for example, from an introductory course) were found to be significant. It appears that the normative pressure regarding career choice decreases with exposure to accounting throughout the completion of a degree, indicating that parents have some sort of influence inasmuch as students have no prior knowledge of the field (Tan & Laswad, Citation2006). Many employers are critical of Vietnamese accounting graduates who fail to keep abreast of the latest international accounting standards and lack foreign language (mainly English) skills (CIMA, Citation2014). Whereas Vietnamese universities tend to be heavily theoretical in their course offerings and focused on Vietnamese accounting standards (VAS), the multinationals operating in Vietnam seek graduates with a sound understanding of international accounting standards (IAS) and international financial reporting standards (IFRS, Citation2018).

The Big 4 firms, in particular, have tried to remedy the shortage of qualified accountants by offering internships, but Cheng et al. (Citation2009, p. 349) warns that it will ‘not necessarily solve the issue, unless they attract students into the profession who would otherwise have chosen alternative career paths’. Albrecht and Sack (Citation2000, p. 1) concluded that if declining enrolments in accounting programmes, the obsolete nature of the accounting education model and the poor image advertised by practitioners and academics themselves were not ‘seriously addressed and overcome, they will lead to the demise of accounting education’. Jackling and Calero (Citation2006) suggest that professional bodies could contribute to reducing the shortage of accountant by promoting the profession as challenging rather than boring, and that is based on decision making and problem-solving rather than number crunching. Leading the way, CPA Australia instigated appealing advertising campaigns following the assumption that perception and choice of an accounting major are associated. These campaigns portray young and dynamic accountants in non-stereotypical careers with overrepresentation of females and minorities.

Despite the lack of consensus on factors driving students to choose accounting as a career, it seems that two factors recur in most studies and therefore communications to prospective and first-year students should emphasise excellent remuneration, a diversity of work and international mobility (Birrell & Betts, Citation2018). These factors are even more important in times of economic uncertainty and regardless of the cultural context, they should certainly speak to parents in EEs desperate to secure future financial security for their offspring.

Affiliation with professional bodies: perceptions of costs and benefits

Research has shown that in Australia, students graduating with an accounting major typically complete professional training with one of the large professional accounting bodies such as CPA Australia or Chartered Accountants Australia and New Zealand (CAANZ) (De Lange et al., Citation2006; Mathews et al., Citation1990). Researchers have noted that in order to achieve long-term career success, there is a need to be able to adapt to changes in environmental and economic conditions. To gain the status and receive the rewards associated with ‘gold collar’ employees, membership of professional accounting bodies is essential as is a commitment to continuous development of professional skills (Howieson, Citation2003).

However, with the globalisation of economies and professional services (Hopper et al., Citation2017), issues of membership and accreditation are arising as accountants are operating in borderless domains. Memorandums of understanding, reciprocal recognition schemes and cross-accreditation are flourishing.

Some studies tried to identify the drivers of affiliation to professional bodies such as perceived intrinsic benefits (e.g. job satisfaction) and extrinsic benefits (e.g. salary) (Inglis et al., Citation2011; Sidaway et al., Citation2013), but these studies fail to provide an indication of determinants that drive membership choice and decisions to cease membership with a specific professional body. Inglis et al.’s (Citation2011) study of students and practitioners in Australia, Hong Kong, Singapore and Malaysia showed that brand/reputation, international recognition of qualifications and career opportunities were all important in their choice of a professional body followed by place of work and educational requirements. Despite their importance, these factors themselves did not make a difference as to which specific body students would affiliate with. Sidaway et al. (Citation2013) followed a similar research approach and their comparison of students and practitioners indicated significant differences in terms of relative importance of factors affecting affiliation. Similar to Inglis et al. (Citation2011), ‘career opportunities, international recognition and brand or reputation were identified as being the factors that are most important to students in their choice of which professional accounting body to join’ (Sidaway et al., Citation2013, p. 612). For practitioners, only brand and reputation were considered as important factors. A comparison between students and practitioners revealed significant differences between all the factors except for members’ benefits indicating that factors change in importance over time and therefore the associated member marketing strategies required change.

Inglis et al.’s (Citation2011) study showed that almost 20% of the students and 8% of the alumni surveyed had affiliated with more than one professional accounting body. In Sidaway et al. (Citation2013) approximately 50% of the practitioners were members of two or more professional bodies. The comparison by Sidaway et al. (Citation2013) between single and multiple members of factors affecting the decision to affiliate with a professional body revealed that the only difference was in terms of international recognition which multiple members placed more emphasis on. When looking at the characteristics of these multiple members it appeared that many of them were members of a foreign accounting body, for example, the Institute of Chartered Accountants in England and Wales (ICAEW), the Malaysian Institute of Accountants and the Accounting Society of China, which would explain the importance of status and international recognition (Birrell & Betts, Citation2018; Carnegie & Parker, Citation1999).

Purpose of the study and hypothesis

Challenges faced by professional accounting bodies relate to the recruitment of new members (graduates) and retention of existing members (Albrecht & Sack, Citation2000; Tan & Laswad, Citation2006). Despite studies on the perception of the benefits and costs of joining a professional body (Inglis et al., Citation2011; Sidaway et al., Citation2013), little empirical evidence is available on the deciding factors for joining one specific professional body, let alone multiple ones in a EE. In addition, many professional bodies offer alternate membership pathways. Alternate professional pathways are available in Vietnam and we were unable to locate any studies that differentiate pathway preferences between the different cohorts. Using the theoretical lens articulated within the TPB, this study investigates the factors affecting final-year university students as well as foundation candidates’ decisions to affiliate with one or more professional bodies in Vietnam. This study is critical in the context of professionalisation of accounting in an emerging and state-controlled transitional economy and explains the need for understanding the factors that drive future and current practitioners to choose one or more professional bodies, remain with those bodies or cease affiliation.

Following a review of the Theory of Planned Behaviour literature, the following hypotheses were posited:

H1: Foundation candidates and students who have positive attitudes towards affiliating with a professional accounting body are more likely to affiliate with one such body in Vietnam.

H2: Foundation candidates and students who perceive normative pressure (subjective norm) towards affiliating with a professional accounting body are more likely to affiliate with one such body in Vietnam.

H3: Foundation candidates and students who perceive they have control over affiliating with a professional accounting body are more likely to affiliate with one such body in Vietnam.

The theory of planned behaviour

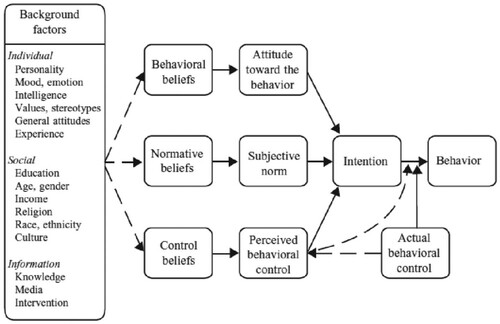

The theory of planned behaviour (TPB) is a social psychology model that aims to explain behaviour. TPB (Ajzen, Citation1991) is an extension of the theory of reasoned action (TRA) (Ajzen & Fishbein, Citation1980; Fishbein & Ajzen, Citation1975) and incorporates the central tenet of an individual’s intention to perform the behaviour. TPB extends TRA by introducing the perceived behavioural control variable. TRA posits that behaviour is directly affected by intention to perform the behaviour, which is itself affected by attitude towards the behaviour and subjective norm.

is a diagrammatic representation of the developed TPB model and shows that the chances of performing a behaviour are positively correlated with the intention to perform it (Ajzen, Citation1991) and perceived behavioural control (PBC), which is the perception of the ease or difficulty of performing the behaviour. There is a presumption that when behaviours are under complete control, behaviours can be accurately predicted through intentions (Ajzen, Citation1988; Sheppard et al., Citation1988). In turn, an individual’s intentions are directly influenced by three independent variables: attitude towards the behaviour (negative or positive perception of the behaviour); subjective norm (perceptions of social pressure to perform or not perform the behaviour); and PBC. Determinants of intention are themselves a function of underlying behavioural, normative and control beliefs, respectively and these salient beliefs can vary as a function of a wide range of background factors such as age, gender, knowledge and experience.

Figure 1. The developed TPB model (Ajzen & Fishbein, Citation2005).

Attitude and subjective norm have been found to be highly correlated, suggesting an overlapping nature of the two constructs: subjective norm may represent other people’s perceived opinion rather than an actual external influence (Warshaw, Citation1980). Like attitude and subjective norm, PBC can be measured by asking direct questions about capability to perform a behaviour or indirectly on the basis of beliefs about ability to deal with specific inhibiting or facilitating factors (Ajzen, Citation2002).

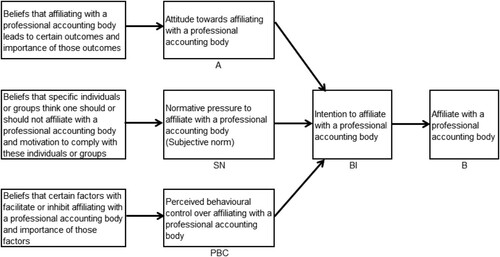

is a diagrammatic representation of the application of the TPB model to students and foundation candidates’ decision to affiliate with a specific professional accounting body. In summary, TPB suggests that behavioural intention (BI) of affiliating with a professional accounting body (B) is a function of attitudes (A) towards affiliating with a professional accounting body, subjective norm (SN) towards affiliating with a professional accounting body and perceived behavioural control (PBC) over affiliating with a professional accounting body. Attitude, subjective norm and PBC are themselves a function of their respective salient behavioural, normative and control beliefs about affiliating with a professional accounting body.

Figure 2. Application of the TPB model (Ajzen, Citation1991) to the decision to affiliate with a professional accounting body.

Research methods

Sample

After being granted ethics approval, the participants in this study were drawn from two discrete cohorts: students studying an undergraduate accounting degree in Vietnam (N = 167) and candidates completing the foundations levels of a foreign professional accounting body programme in Vietnam (N = 145).

The student sample came mainly from one of the largest public Vietnamese universities (50,000 students), which offers undergraduate and postgraduate degrees in economics, business administration, finance, accounting, information systems and law, making them representative of a typical accounting student in Vietnam. The sample was recruited through a lecturer working for that university. CPA Australia foundation candidates are those people who are completing the foundation levels of the CPA programme (the CPA programme is for graduates from non-accounting degrees and comprises 14 levels in total comprising eight foundation levels and six professional levels). The foundation candidates were recruited through CPA Australia employees in Vietnam who contacted them.

The respective response rates were 32% for students and 22% for foundation candidates, which sits well within the average response rate of between 10% and 25% for web-based surveys (Sauermann & Roach, Citation2013).

The foundation candidates sample comprised 61% females and 37% males with two respondents not indicating their gender. Over half (51%) were between 25 and 34 years old and the majority (92%) was a member of only one professional accounting body. Of these candidates, 18.6% were currently studying at university while the remainder were mostly working for one of the Big 4 accounting firms (26.9%), a multinational company (20%) or in financial services (17.2%). Nearly one-third (29.7%) had studied at the University of Economics in Ho Chi Minh City.

The students sample comprised 65% females and 30% males with seven respondents not indicating their gender. The majority (95%) were aged between 18 and 24 years old and 98% were not a member of any professional accounting body. Of the students, 82% were currently studying at the University of Economics in Ho Chi Minh City while the remainder were studying at RMIT University in Ho Chi Minh City or Hanoi.

Research instrument and measures

This study used TPB to explain professional accounting body affiliation and retention in Vietnam for two cohorts by measuring the TPB independent variables’ effects on intention to affiliate with a professional accounting body. The questions for the survey were developed using guidelines already established in the literature (Ajzen, Citation1991; Ajzen & Fishbein, Citation1980; Fishbein & Ajzen, Citation1975) and previously validated survey instruments described in the following section.

The foundation candidates’ final questionnaire contained six questions measuring the constructs identified, as well as eight demographic and other related questions and a final open-ended question allowing respondents to add any comment in relation to affiliation of professional accounting bodies. The first part of the survey asked respondents to rate 28 statements corresponding to factors affecting affiliation. Each factor assessed one of the salient beliefs that were hypothesised to affect the three independent variable constructs (attitude, subjective norm and PBC). The same factors listed in the first part of the survey were then rated on a 7-point scale in terms of importance for the respondent in the second part of the survey. The cross-product of the items in the first and second parts of the survey follows the expectancy-value model and is deemed to be an indirect measure of attitude, subjective norm and PBC, respectively. Questions in the third part of the survey measured factors affecting the foundation candidates’ decision to cease affiliation with the professional body. This question was omitted for students as they were not affiliated with any specific professional accounting body. Parts 4, 5 and 6 of the survey included questions that were hypothesised to be a direct measure of attitude, subjective norm and PBC and made use of semantic differential scales. The foundation candidates’ and students’ questionnaires included an additional question asking respondents to rate their likelihood of affiliating with a professional accounting body in the near future (intention) on a 7-point scale. The students’ questionnaire only required respondents to rate deciding factors (e.g. career and networking opportunities, salary of members) in terms of importance and also collected data to measure attitude, subjective norm and PBC. The students were also asked to indicate whether they already belonged to a professional accounting body. The summary of the variable measures and statements are provided in .

Table 1. Variables and variable measures.

The foundation candidates’ questionnaires were sent by email with a Qualtrics link to CPA Australia staff members who forwarded them to their foundation candidates to ensure anonymity. The students’ questionnaire was completed on paper, for convenience, as accounting lecturers at the surveyed university agreed to distribute it during class time. Only a Vietnamese version of the questionnaire was available to students as they belonged to a public Vietnamese university and were unlikely to have a good command of English.

Instrument reliability and validity

Content validity, which ensures that a measure covers the domain of interest entirely and without going beyond was established by adopting questionnaires taken from previous studies on the topic (Inglis et al., Citation2008, april 24–25; Sidaway et al., Citation2013), using commonly listed benefits associated with affiliation available on the professional bodies’ websites as well as discussions with staff members of the professional body in Vietnam. To address the concern of face validity, which assesses whether the questionnaire appears to measure the concepts being investigated (Burns, Citation1994), the questionnaires were piloted with ten foundation candidates completing the questionnaire and providing comments as to the understandability of the questionnaire, appropriateness to the Vietnamese context and more generally to see if any clarity was required.

To determine if the results from this study would be reliable and replicable across other potential studies, reliability estimates of the independent variables (attitude, subjective norm and PBC) were obtained using internal consistency. The reliability of the attitude scale is 0.784 and the reliability of the PBC scale is 0.780, which are considered acceptable as an estimate of 0.60 has long been regarded as a threshold of reliability for research purposes (Nunnally, Citation1978).Footnote1

Harman’s one-factor test and confirmatory factor analysis, post hoc statistical tests, were conducted to test for the presence of the common method bias effect (Podsakoff et al., Citation2003). All variables were entered into an exploratory factor analysis, using unrotated principal components factor analysis, principal component analysis with varimax rotation, and principal axis analysis with varimax rotation to determine the number of factors that are necessary to account for the variance in the variables. If a substantial amount of common method variance is present, either a single factor will emerge from the factor analysis, or one general factor will account for most of the covariance among the variables. The unrotated principal component factor analysis, principal component analysis with varimax rotation, and principal axis analysis with varimax rotation all revealed that all factors possessed Eigen-values exceeding 1 and which in total accounted for 67.2% of the variance. The first (largest) factor did not account for a majority of the variance and the factors together accounting for 67% of the total variance. Thus, no general factor is apparent. Moreover, the confirmatory factor analysis showed that the single-factor model did not fit the data well. While the results of these analyses do not preclude the possibility of common method variance, they do suggest that the common method variance is not of great concern and thus is unlikely to confound the interpretations of results.

Results

In order to test H1, 2 and 3, a regression analysis was performed. The intention was regressed on the attitude, subjective norm and PBC scales. Three separate regression analyses were performed: one overall regression for the two samples combined and one for each sample. The differences between foundation candidates and students in terms of salient beliefs regarding affiliation of professional accounting bodies were tested using independent t-tests. All the statistical tests were performed using SPSS 20.Footnote2

Hypothesised relationships H1 and H2

• H1: Foundation candidates and students who have positive attitudes towards affiliating with a professional accounting body are more likely to affiliate with one such body in Vietnam.

• H2: Foundation candidates and students who perceive normative pressure (subjective norm) towards affiliating with a professional accounting body are more likely to affiliate with one such body in Vietnam.

In relation to H1 and H2, the descriptive statistics of the various constructs for the total population utilised in the regression analysis are presented in . All the items were measured on a bipolar scale from −3 to +3, with +3 indicating, respectively for each variable:

A definite intention to affiliate with a professional accounting body.

A positive attitude towards affiliating with a professional accounting body.

The perception that important referents think the respondent should affiliate with a professional accounting body.

The perception that there are no inhibiting factors to affiliating with a professional accounting body.

Table 2. Intention, attitude, subjective norm and PBC descriptive statistics – full sample.

In general, shows all students and foundation candidates have a favourable attitude towards affiliating with a professional accounting body (M = 1.59), they perceive some pressure to do so (M = 1.59) and perceive no inhibiting factor to do so (M = 1.20). Consequently, they intend to affiliate with a professional accounting body in the near future (M = 1.18).

As shown in , the independent variables explain a significant 14.6% of the variance in intention. Additionally, only attitude is statistically significant and with a high coefficient showing that only positive or negative attitude towards affiliating with a professional accounting body affects intention to affiliate with that body. Normative pressure and factors facilitating or inhibiting affiliation do not seem to have any significant effect on intention.

Table 3. Regression results of intention on attitude, subjective norm, PBC – full sample.

Interestingly, when the regression analysis is performed on each sample separately, for foundation candidates, attitude remains statistically significant (r = 0.355, p < 0.01) in explaining intention to affiliate with a professional accounting body and so is subjective norm (r = 0.183, p < 0.01) which means that foundation candidates do feel some normative pressure albeit a limited one to affiliate with a professional accounting body. PBC is not significant for that sample. The analysis for the accounting students reveals that attitude and subjective norm are only marginally significant (r = 0.260, p = 0.05; r = 0.200, p = 0.1, respectively) showing that students do feel some normative pressure albeit a limited one (coefficient is 0.200) to affiliate with a professional accounting body. PBC is once again not significant.Footnote3

Hypothesised relationship H3

H3: Foundation candidates and students who perceive they have control over affiliating with a professional accounting body are more likely to affiliate with one such body in Vietnam.

Before comparing the different sample groups on different characteristics, this section will explore the individual groups’ ratings and rankings of the proposed salient beliefs to determine which beliefs contribute the most to their overall beliefs about professional accounting bodies. Accounting students are excluded from this analysis as they were not required to rate beliefs statements. shows the ranking of the outcome evaluation of salient beliefs for foundation candidates from the statements with the highest level of agreement to those with the lowest level of agreement on a 7-point scale with 7 being the highest level of agreement possible.

Table 4. Salient beliefs outcome evaluation ranking – foundation candidates.

Reputation of the professional accounting body is the belief with the highest level of agreement and motivation to comply with co-workers the one with the lowest ranking. Overall foundation candidates find that CPA Australia has a good reputation (M = 6.25), affiliating with CPA Australia would enhance their career and networking opportunities (M = 6.15), the programme is flexible (M = 6.12), its international recognition is high (M = 6.09) and affiliating with CPA Australia would enhance their professional status (M = 6.07) and international mobility opportunities (M = 5.89). However, despite the perceived quality of the programmes (M = 5.88), the associated tuition fees are considered high (M = 5.69) and foundation candidates are also more likely to affiliate with CPA Australia if their employer covers the programme fees and membership fees (M = 5.71 and 5.57, respectively). The respondents are quite neutral as to how easy it is to become and remain a member (M = 4.08 and 4.42, respectively). Finally, there does not seem to be any strong normative pressure to affiliate with CPA Australia except maybe marginally from employers (M = 4.95) and no motivation to comply with any of the referents, which would confirm why subjective norm was significant but small for this group as only one referent group seems to be influential.

shows the full list of behavioural and control factors with their mean rating (out of 7) by order of importance for the foundation candidates sample group.

Table 5. Factors importance – foundation candidates.

When asked about the importance of each factor in influencing their choice to join CPA Australia, the most important factors rated by foundations candidates are career and networking opportunities (M = 6.30) followed by quality of professional education programmes (M = 6.25), reputation of the professional body (M = 6.20), international recognition (M = 6.17) and professional status (M = 6.08). In addition, the factors perceived to have the least influence are the assessment fee (M = 4.20) and ongoing membership cost (M = 4.97).

The students were not requested to evaluate the outcomes of affiliating with a professional accounting body as they did not yet belong to one, but they were asked to rate the importance of several factors on their decision to affiliate with a professional accounting body. The ranking of these factors from the most important to the least important is provided in .

Table 6. Factors importance – students.

Students consider that the most important factor is the quality of professional education programmes (M = 6.51) followed by career and networking opportunities (M = 6.44), reputation of the professional body (M = 6.20), salary of the members (M = 6.03) and international recognition (M = 5.99). In addition, the factors perceived to have the least influence are the assessment fee (M = 4.62) and ongoing membership fee (M = 4.87). Employers covering the membership fees also appeared at the bottom of the table, despite being considered relatively important (M = 5.24). Next section details the results of the comparison between members and foundation candidates in terms of the outcome evaluation of salient beliefs.

The comparison of the perceived importance of modal outcomes and inhibiting/facilitating factors between the two groups was tested using independent t-tests and revealed the following differences:

Students (M = 4.62) place significantly more importance on assessment fee than foundation candidates (M = 4.20).

Students (M = 6.51) place significantly more importance on quality of professional education programmes than foundation candidates (M = 6.25, p = 0.002).

Students (M = 5.77) place significantly less importance on professional status than foundation candidates (M = 6.08, p < 0.001).

Foundation candidates (M = 5.27) place significantly more importance on magazines and journals than students (M = 4.90, p = 0.007).

Foundation candidates (M = 5.92) place significantly more importance on exam mode than students (M = 5.58, p = 0.013).

The comparison of the perceived importance of modal outcomes and inhibiting/facilitating factors between intenders and non-intenders was tested using independent t-test. Intenders were those respondents who rated the intention question between +1 and +3. Non-intenders were those respondents who rated the intention question between −3 and 0. shows the significant difference between those who intend to affiliate with a professional accounting body and those who do not in terms of modal outcomes and facilitating/inhibiting factors importance.

Table 7. Intenders/non-intenders significant differences on modal outcomes and facilitating/inhibiting factors importance.

The comparison between these two groups revealed the following difference: those who intend to affiliate with a professional accounting body in the near future place significantly more importance on reputation of the professional body (M = 6.28 vs. 6.03), career and networking opportunities (M = 6.47 vs. 6.21), international recognition (M = 6.17 vs. 5.84), professional status (M = 6.02 vs. 5.70), international mobility opportunities (M = 6.02 vs. 5.63), perceived expertise of the members (M = 5.86 vs. 5.44), continuing professional development (M = 5.83 vs. 5.47) and receiving magazines or journals (M = 5.16 vs. 4.78) but less importance on assessment fees (M = 4.32 vs. 4.72). Intuitively and substantively these findings make sense. Whilst both groups had a fairly consistent and relatively highly ranked top five factors (scored 6 or above) that is both groups felt generally that the same key factors were important, the slight difference in ranking reflects a subtle but important development for foundational candidates relative to students. The closer the foundational candidates move towards achieving the goal of becoming a professional accountants the greater their perceived importance of international standing and professional status of their chosen profession becomes. This is also evidence by the different ranking of salary which whilst still important for both, is ranked at 4th for students and 10thfor foundation candidates. Intuitively the findings suggest that as the participants grow closer to achieving their professional career target they consider similar factors as important but in fact reprioritise those factors.

Discussion and implications

In support of H1, the results indicate that only attitude is significant in explaining the intention of accounting students and foundation candidates in affiliating with a professional accounting body. This means that only positive or negative outcomes of affiliating with a professional accounting body matter when it comes to making the decision. Pressure from important referents such as employers, co-workers and family does not seem to be significant, which is contrary H2 and not supported. The expectation that in collective societies such as Vietnam, the weight of the group is an important factor (Vietnam Culture, Citation2013) and despite the fact that the respondents did perceive some normative pressure to affiliate. However, this falls in line with several studies finding no effect of subjective norm on intention (Bagley et al., Citation2012; Davis et al., Citation1989). Additionally, PBC was not significant, which means H3 was not supported in that respondents perceived no inhibiting factor of becoming member of a professional body including the cost of affiliating or the difficulty in passing examinations but this did not affect their decision to affiliate either way. This finding is contrary to previous findings regarding the influence of PBC on intention (Bagley et al., Citation2012; Cohen & Hanno, Citation1993; Dalton et al., Citation2014; Tan & Laswad, Citation2006).

A comparison of students and foundation candidates in terms of factor importance shows that students are mostly preoccupied with the quality of the programmes but not with their professional status, which may be explained by age differences and lack of professional experience. Foundation candidates place more importance on exam mode, probably by virtue of their focus on passing exams to complete levels.

The comparison between those who intend to professionally affiliate compared to those who do not reveals the main factors affecting the decision are the reputation of the professional body (Annisette, Citation2000), career and networking opportunities, international mobility opportunities, (Bennell & Pearce, Citation2003; Birrell & Betts, Citation2018), international recognition (Hopper et al., Citation2017; Mihret et al., Citation2019), professional status (Yapa, Citation2006), perceived expertise of the members and continuing professional development. These findings are consistent with most professionalisation projects in EEs (See Yapa, Citation2003, Citation2006, Citation2010; CIMA, Citation2014) and supports the perception that whilst both groups share a common approach to important factors that the relative importance of these factors shifts subtly as they grow closer to achieving their career aspirations.

Implications for the profession

For those who are concerned with the deepening professionalisation of accounting the practical implications of these results suggest that the size impact of the profession can be enhanced through promoting the benefits of affiliation. Greater professional affiliation may be achieved via the reputation of the professional body, career and networking opportunities, professional status, international recognition and quality of programmes. This last factor is crucial in light of the perceived lack of quality of training offered by local professional accounting bodies and so is the flexibility of these programmes for those completing them (See Sidaway et al., Citation2013). Promotional efforts should be directed at the Big 4 accounting firms as the main employers of members with the financial capacity to cover their employees’ membership and programme fees. In general for a profession seeking to make greater inroads into a EE more targeted efforts are require to highlight options in terms of careers, industries and locations. Those attempting greater professional closure ought to develop creative means to attract more female members by promoting the quality of their programmes and developing more flexible working arrangements. Professional closure could also be driven with more overall members by promoting the range of career opportunities as well as advertising the profession as dynamic rather than rules based. A reduced pricing strategy for members in EE’s might be considered, in particular for tuition fees.

One of the differentiating factors between accounting students and those who have already entered the profession is their emphasis on the quality of professional programmes, which confirms once more that professional accounting bodies have a role to play in ensuring adequate training for the profession. It also highlights that professional status is largely unimportant to students, so accounting educators need to improve their communication and ‘sell’ the profession better by emphasising social status.

Implications regarding TPB

Attitude is significant in predicting the intention of foundation candidates and accounting students to affiliate with a professional accounting body. In this study, the attitude construct was measured through an average of three statements relating to how good or bad, positive or negative and useful or useless affiliation with a professional accounting body is. Despite the fact that the reliability of this scale was sufficient it is interesting to note that if the first pair of adjectives (good/bad) had been dropped, the reliability of the attitude scale would have increased even further. This seems to contradict previous findings arguing that the good/bad scale has been found to be a consistently high load on the evaluative factor, regardless of the context (Fishbein & Ajzen, Citation1975). It might be that in the Vietnamese context, good/bad is too generic and that positive/negative and useful/useless can be better associated with professional outcomes.

The effect of subjective norm on intention showed mixed results. Subjective norm is significant for foundation candidates but barely for accounting students. The direct measure of subjective norm was taken through a generic question asking respondents to rate whether they perceived that people who are important to them thought they should affiliate with a professional accounting body. Using a single question to measure subjective is quite common (Armitage & Conner, Citation2001) but makes it difficult to assess the reliability of the scale. The results show that foundation candidates perceive moderate or no pressure from the referents and generally no motivation to comply with their views, which is at odds with the fact that subjective norm is significant in explaining their intention. One possible explanation is that the list of referents has omitted an important one such as professors but given the profile of the foundation candidates (78.6% not students) this is unlikely. It could also be that subjective norm would have had a higher effect had it been measured through multiple statements rather than one, which was confirmed by previous studies.

PBC has no effect on intention for either group. The PBC construct was measured through an average of three statements relating to how easy or difficult, under the respondent’s control and up to them it is to affiliate with a professional accounting body. The first statement relates to the concept of self-efficacy and does not differentiate between external (availability) and internal factors (motivation) (Armitage & Conner, Citation2001), while the other two statements relate to controllability. For this reason and because the reliability of the scale with all three statements included was below 0.6, it was decided to drop the first statement from the PBC construct. Despite the fact that the easy/difficult scale is quite commonly used to assess PBC, it might be useful for predictive purposes to use more specific adjectives than these in contexts where the decision might be affected by a variety of internal and external factors.

The results show that some control beliefs are rated as very important (flexibility of programme, time available for studying) or important (difficulty of CPA programme, employer paying programme fees) and are likely or very likely to occur, which is at odds with the fact that PBC is not significant in explaining intention. One explanation is that even if the employer did not cover the programme fee, the respondents would still affiliate with the professional body, indicating that PBC is important but not critical. Another explanation is that positive and negative control factors cancel each other out. This idea is confirmed by the findings that general respondents do not think that becoming or remaining a member is either easy or difficult. Either way these findings are at odds with previous studies finding an effect of PBC on intention in the accounting domain (Bagley et al., Citation2012; Cohen & Hanno, Citation1993; Dalton et al., Citation2014; Tan & Laswad, Citation2006).

Limitations

There are a number of limitations inherent in this study. The first limitation is that this study focuses on only one country, Vietnam, as a reference point for affiliation of professional accounting bodies, which may limit the generalisability of the findings. Another limitation relates to the theoretical framework itself as although TPB has been used extensively to explain a range of decisions in many disciplines, it does have certain limitations that researchers need to be mindful of. These include the need for a short time interval between intention and behaviour to ensure that intentions have not changed, the potential lack of consideration for personality traits and the challenge of measuring subjective norm (Conner & Armitage, Citation1998). This study explores the attitude subjective norm/intention/behaviour link for one alternative thus ignoring attitude and subjective norm towards competing alternatives, which Sheppard et al. (Citation1988) argue is a limitation as it considers intention to perform a behaviour but ignores the subjective probability of performing the behaviour. A further limitation is that the consistent low variances in intention explained found in other studies suggests that some other factors not included in TPB (belief salience, past behavioural habit, the structure of the PBC construct, moral norms, self-identity and affective beliefs) may influence intention and behaviour (Conner & Armitage, Citation1998).

Conclusions

This study examines potential drivers that can be used by stakeholders to inform strategy to counteract the diminishing numbers of accounting students and thus provide insight into and potential options to the shortage of qualified accountants, as well as contributing to professional closure in an EE. Previous research (Inglis et al., Citation2011; Sidaway et al., Citation2013) found the factors affecting the decision of future members to choose a specific professional accounting body. Our study has discovered new evidence about drivers of professional affiliation and confirms the limited previous findings showing that career and international mobility opportunities, quality of programmes, professional status, reputation and international recognition are crucial factors in choosing a foreign professional accounting body in Vietnam. These findings are critical for the accounting and auditing profession in EE’s and Vietnam wanting to address the issue of shortage of qualified accountants.

Secondly, it fills the gap in the existing literature on the use of TPB (Ajzen, Citation1991) by extending TPB into research in the accounting field, and by confirming that positive or negative attitudes towards accounting (majoring in accounting, choosing a general or specific career in accounting or affiliating with a professional accounting body) explain individuals’ intentions and thus behaviour. Excitingly, the effect of subjective norm, similarly to previous findings, is still inconclusive with the construct very significant for one group but not the other and for only one referent group (employer) having a marginal effect. This could potentially confirm as previous researchers have concluded that attitude and subjective norm are overlapping rather than distinct constructs. Surprisingly, the originality of our study is that PBC is not significant for either group. This tends to contradict previous research, suggesting PBC may also overlap with attitude.

Third, this study contributes to the literature on professionalisation of accounting in state-controlled EE and serves to depart from an Anglo-American model of professionalisation with the central tenet of self-regulation. The professionalisation process of accounting and auditing in Vietnam seems to be one where foreign professional accounting bodies do not compete with local ones but provide benefits (career and networking opportunities, quality programmes and international recognition amongst others) that are yet to be found with local bodies. These local professional bodies are indeed in their infancy and it is advisable for them to think that healthy partnerships and mutual recognition schemes with foreign bodies will help develop the Vietnamese accounting profession in its own right.

Lessons learned for policy makers in accounting and auditing, accounting educational institutions and the state authorities in Vietnam and international professional accounting bodies can be used in EE settings. These stakeholders will be able to understand the future directions of the accounting profession and the challenges ahead to organise themselves with appropriate strategies for enhanced sustainability.

Future research might seek to expand the range of data collected by including other Southeast Asian countries. It is important to try and include different types of universities, public and private, small and large, domestic or foreign in order to capture the wide range of profiles of accounting students. It might also be wise to include several professional accounting bodies to avoid a single member bias and in particular to include both domestic and foreign bodies in order to ascertain which factors differentiate between these two types of membership.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 We ran a non-response bias test by splitting the sample into two groups: early and late respondents. Results of this comparison show no significant differences in responses between the two groups.

2 We also conducted Structural Equation Modelling (SEM) and Partial Least Squares (PLS) analysis. They yielded largely the same results as the regression analysis and therefore are not included in the paper (Thoradeniya et al., Citation2015).

3 We conducted discriminatory validity tests using the method recommended in Henseler et al. (Citation2015) which is to calculate the HTMT ratio, which (roughly) compares the (average) correlation between items when both are in different constructs to (average) correlations between items when both are in the same construct. The HTMT ratio for ATT and PBC was 0.52. Values greater than 0.85 suggest a lack of discriminate validity. It was not possible to formally test for discriminate validity between other pairs of constructs because these were the only two that were measured with more than one item/question. It should also be noted that our correlation matrix shows low to middling correlation coefficients (all 0.48 or less) between variables, so we do not think that multi-collinearity is an issue.

References

- Abbott, A. (1988). The system of professions: An essay on the division of expert labor. University of Chicago press.

- ACCA. (2016). About ACCA Vietnam. http://www.accaglobal.com/vn/en/discover/about/about-acca-vietnam.html

- Ajzen, I. (1988). Attitudes, personality, and behavior. Dorsey Press.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/https://doi.org/10.1016/0749-5978(91)90020-T

- Ajzen, I. (2002). Perceived behavioral control, self-efficacy, locus of control, and the theory of planned behavior. Journal of Applied Social Psychology, 32(4), 665–683. https://doi.org/https://doi.org/10.1111/j.1559-1816.2002.tb00236.x

- Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behavior. Prentice-Hall.

- Ajzen, I., & Fishbein, M. (2005). The influence of attitudes on behavior. In D. Albarracín, B. T. Johnson, & M. P. Zanna (Eds.), The handbook of attitudes (pp. 173–221). Lawrence Erlbaum Associates Publishers.

- Albrecht, W. S., & Sack, R. J. (2000). Accounting education: Charting the course through a perilous future (Vol. 16). American Accounting Association.

- Annisette, M. (2000). Imperialism and the professions: The education and certification of accountants in Trinidad and Tobago. Accounting, Organizations and Society, 25(7), 631–659. https://doi.org/https://doi.org/10.1016/S0361-3682(99)00061-6

- Armitage, C. J., & Conner, M. (2001). Efficacy of the theory of planned behaviour: A meta-analytic review. British Journal of Social Psychology, 40(4), 471–499. https://doi.org/https://doi.org/10.1348/014466601164939

- Bagley, P., Dalton, D., & Ortegren, M. (2012). The factors that affect accountants’ decisions to seek careers with Big 4 versus non-Big 4 accounting firms. American Accounting Association, 26(2), 239–264. https://doi.org/https://doi.org/10.2308/acch-50123

- Bakre, O. M. (2005). First attempt at localising imperial accountancy: The case of the Institute of Chartered Accountants of Jamaica (1950s–1970s). Critical Perspectives on Accounting, 16(8), 995–1018. https://doi.org/https://doi.org/10.1016/j.cpa.2004.02.007

- Bennell, P., & Pearce, T. (2003). The internationalisation of higher education: Exporting education to developing and transitional economies. International Journal of Educational Development, 23(2), 215–232. https://doi.org/https://doi.org/10.1016/S0738-0593(02)00024-X

- Berquist, B., Hall, R., Morris-Lange, S., Shields, H., Stern, V., & Tran, L. T. (2019). Global perspectives on international student employability. International Education Association of Australia (IEAA). www.ieaa.org.au

- Birrell, B., & Betts, K. (2018). Australia’s higher education overseas student industry: In a precarious state. The Australian Population Research Institute. Retrieved May 30, 2019, from https://tapri.org.au/wp-content/uploads/2016/04/final-report-overseas-student-industryV2.pdf

- Bodewig, C., Badiani-Magnusson, R., Macdonald, K., Newhouse, D., & Rutkowski, J. (2014). Skilling up Vietnam: Preparing the workforce for a modern market economy. The World Bank. Retrieved July 12, 2018, from https://openknowledge.worldbank.org/handle/10986/18778

- Bui, B., Hoang, H., Phan, D., & Yapa, P. W. S. (2017). Governance and compliance in accounting education in Vietnam–case of a public university. Accounting Education, 26(3), 265–290. https://doi.org/https://doi.org/10.1080/09639284.2017.1286603

- Bui, B., & Porter, B. (2010). The expectation-performance gap in accounting education: An exploratory study. Accounting Education, 19(1-2), 23–50. https://doi.org/https://doi.org/10.1080/09639280902875556

- Bui, T. M. V. (2011). A study of the development of accounting in Vietnam [Unpublished PhD thesis]. RMIT University.

- Bui, T. M. V., Yapa, P. W. S., & Cooper, B. (2011). Accounting development in Vietnam: The state and the accounting regulation. http://researchbank.rmit.edu.au/view/rmit:14298

- Burns, R. (1994). Introduction to research methods. Pearson Education.

- Carnegie, G. D., & Edwards, J. R. (2001). The construction of the professional accountant: The case of the incorporated institute of accountants, Victoria (1886). Accounting, Organizations and Society, 26(4), 301–325. https://doi.org/https://doi.org/10.1016/S0361-3682(00)00039-8

- Carnegie, G. D., & Parker, R. H. (1999). Accountants and empire: The case of co-membership of Australian and British accountancy bodies, 1885 to 1914. Accounting, Business & Financial History, 9(1), 77–102. https://doi.org/https://doi.org/10.1080/095852099330377

- Cheng, M., Kang, H., Roebuck, P., & Simnett, R. (2009). The employment landscape for accounting graduates and work experience relevance. Australian Accounting Review, 19(4), 342–351. https://doi.org/https://doi.org/10.1111/j.1835-2561.2009.00071.x

- Chua, W. F., & Poullaos, C. (1998). The dynamics of ‘closure’ amidst the construction of market, profession, empire and nationhood: An historical analysis of an Australian accounting association, 1886–1903. Accounting, Organizations and Society, 23(2), 155–187. https://doi.org/https://doi.org/10.1016/S0361-3682(97)00009-3

- Chua, W. F., & Poullaos, C. (2002). The empire strikes back? An exploration of centre–periphery interaction between the ICAEW and accounting associations in the self-governing colonies of Australia, Canada and South Africa, 1880–1907. Accounting, Organizations and Society, 27(4–5), 409–445. https://doi.org/https://doi.org/10.1016/S0361-3682(01)00020-4

- CIMA. (2014). The Vietnam perspective. Research Project “Ready for business – Bridging the employability gap”, Chartered Institute of Management Accountants (CIMA).

- Cohen, J., & Hanno, D. M. (1993). An analysis of underlying constructs affecting the choice of accounting as a major. Issues in Accounting Education, 8(2), 219–238.

- Conner, M., & Armitage, C. J. (1998). Extending the theory of planned behavior: A review and avenues for further research. Journal of Applied Social Psychology, 28(15), 1429–1464. https://doi.org/https://doi.org/10.1111/j.1559-1816.1998.tb01685.x

- Dalton, D. W., Buchheit, S., & McMillan, J. J. (2014). Audit and tax career paths in public accounting: An analysis of student and professional perceptions. Accounting Horizons, 28(2), 213–231. https://doi.org/https://doi.org/10.2308/acch-50665

- Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982–1003. https://doi.org/https://doi.org/10.1287/mnsc.35.8.982

- De Lange, P., Jackling, B., & Gut, A.-M. (2006). Accounting graduates perceptions of skills emphasis in undergraduate courses: An investigation from two Victorian universities. Accounting and Finance, 46(3), 365–386. https://doi.org/https://doi.org/10.1111/j.1467-629X.2006.00173.x

- Department of Employment Australia. (2015). Labour market research – Accountants. https://docs.employment.gov.au/system/files/doc/other/ausaccountants.pdf

- Dyball, M. C., Poullaos, C., & Chua, W. F. (2007). Accounting and empire: Professionalization-as-resistance: The case of Philippines. Critical Perspectives on Accounting, 18(4), 415–449. https://doi.org/https://doi.org/10.1016/j.cpa.2006.01.008

- Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention, and behavior: An introduction to theory and research. Addison-Wesley.

- Ghattas, P., Soobaroyen, P., & Marnet, O. (2020). Charting the development of the Egyptian accounting profession (1946–2016): An analysis of the state-profession dynamics. Critical Perspectives on Accounting, 78. https://doi.org/https://doi.org/10.1016/j.cpa.2020.102159

- Gomes, D., Carnegie, G. D., & Rodrigues, L. L. (2013). Accounting as a technology of government in the Portuguese empire: The development, application and enforcement of accounting rules during the Pombaline Era (1761–1777). European Accounting Review, 23(1), 87–115. https://doi.org/https://doi.org/10.1080/09638180.2013.788981

- Gul, F. A., Andrew, B. H., Leong, S. C., & Ismail, Z. (1989). Factors influencing choice of discipline of study – Accountancy, engineering, law and medicine. Accounting & Finance, 29(2), 93–101. https://doi.org/https://doi.org/10.1111/j.1467-629X.1989.tb00105.x

- Hao, Z. P. (1999). Regulation and organisation of accountants in China. Accounting, Auditing & Accountability Journal, 12(3), 286–302. https://doi.org/https://doi.org/10.1108/09513579910277375

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/https://doi.org/10.1007/s11747-014-0403-8

- Hopper, T., Lassoud, P., & Soobaraoyene, T. (2017). Globalisation, accounting and developing countries. Critical Perspectives on Accounting, 43, 125–148. https://doi.org/https://doi.org/10.1016/j.cpa.2016.06.003