Abstract

Uzbekistan’s unique post-independence experiment with development was led by Islam Karimov until his sudden death in September 2016. Despite defying international advice on structural reforms, under Karimov’s rule, Uzbekistan achieved an average annual growth rate of 5% in the period 1996–2016, which was particularly impressive (over 8%) in 2004–2016. Karimov also left behind strong macroeconomic fundamentals for his successor. Since taking over the presidency in December 2016, Shavkat Mirziyoyev has introduced wide-ranging reforms, creating an impression of a de facto start to transition in Uzbekistan. This study analyses Karimov’s economic legacy and assesses whether it has enabled or hindered the developmental targets set by his successor.

Uzbekistan’s development experience is unique. In the early 1990s, while most transition economies followed reform policy packages promoted by international financial institutions (IFIs), Uzbekistan stubbornly insisted on choosing its own model of gradual development. Since financial aid and technical support from the international community are often conditional on adopting a variation of reform packages recommended by IFIs, Uzbekistan lost access to these resources at a crucial moment in its development path. Nevertheless, the country experienced the shallowest output fall amongst its peers in the 1990s and managed to maintain an impressive average annual growth rate of over 8% in the 2004–2016 period, which puzzled many neoliberal economists. Over time, however, perhaps also emboldened by the success of its economic policies, the government became increasingly isolationist in its international relations and authoritarian in its domestic affairs (Akimov Citation2015). This eventually led to the excessive centralisation of power under the rule of Islam Karimov and the government essentially became a personalist dictatorship.

Karimov came to power in 1989, with the blessing of Mikhail Gorbachev, as the first secretary of the Communist Party in Uzbekistan. He became the first president of independent Uzbekistan by winning the December 1991 popular vote. Although the constitution explicitly mandates a limit of two consecutive presidential terms, he managed to stay in power by extending his presidential terms through two referenda, which deemed his terms non-consecutive. Hence, when Karimov won the March 2015 presidential elections, another five years of his rule seemed inevitable. However, on 28 August 2016, uncharacteristically, government sources announced that Karimov had been hospitalised for an unspecified treatment. His death from a brain haemorrhage was officially confirmed on 2 September 2016.

Uzbekistan has an established legal framework designed to ensure a smooth transition of power in situations like this. According to Article 96 of the Uzbek Constitution, when a sitting president dies or becomes unable to discharge their duties, the power of the office will be transferred to the Chairman of the Senate in the interim period. In reality, however, the likelihood of the transfer of power through the constitutionally prescribed channel was very slim as the Chairman of the Senate, Nigmatulla Yuldashev, was a little-known man with no de facto political power. Further, under Karimov’s autocratic reign, none of the key members of his bureaucratic apparatus were allowed to share their political views on traditional or social media and/or engage in any other forms of public exposure opportunities, as these could potentially help them gain political capital. Therefore, there was no de facto succession planning in place in September 2016 as Karimov had then entered only the second year of his five-year presidency. Hence, his sudden death, coupled with the lack of a clear heir apparent, created a moment of real anxiety for the country, its neighbours and international observers as the consequences of a potential power struggle in the most populous and geopolitically important country at the heart of Central Asia could be inconceivably disruptive.

Although two high-ranked technocrats, Shavkat Mirziyoyev and Rustam Azimov who rose up the ranks during independence, were seen as Karimov’s protégés and potential successors, Rustam Inoyatov, the secret service chief, was also a real contender. Appointed to his role by Karimov in 1995, Inoyatov was particularly well known for his ruthlessness in dealing with the regime’s political opponents and suppressing popular discontent, political or otherwise. It was, therefore, not very clear to the outside world which of the candidates would succeed.Footnote1 However, soon after the official confirmation of Karimov’s death, the Uzbek establishment appointed Mirziyoyev as the chief-mourner, to lead Karimov’s funeral procession in Samarkand on 3 September 2016. Although this was a symbolic role, it meant that, in line with the Soviet tradition of succession,Footnote2 Mirziyoyev had gathered enough support among the ruling elite to succeed Karimov.Footnote3

Although the general public knew little of the candidates’ plans for reform, insider rumours and anecdotal evidence created the strong impression that Inoyatov was a ruthless operator and Azimov a moderniser, while Mirziyoyev was portrayed as an efficient technocrat ideally suited for a strictly top-down administrative management system. Mirziyoyev’s accession to power was interpreted by independent observers as the continuation of the status quo in terms of reform sluggishness, obsession with security and the flagrant violation of individual freedoms and liberties.Footnote4 Since taking over the presidency, however, Mirziyoyev’s commitment to reforms has exceeded all expectations, at least so far. He has rapidly accelerated reforms in a wide range of areas, including the liberalisation of monetary and foreign exchange policies, trade and agriculture, and media and individual freedoms (Stronski Citation2020). An important caveat, however, is to note Uzbekistan’s very low starting point for reforms, which flatters some of the progress made.Footnote5

This study aims to analyse the economic legacy of President Karimov and assesses its impact on President Mirziyoyev’s reforms and development targets. In the second section, I discuss how the initial conditions shaped Karimov’s reform strategy and policy choices in the early 1990s. In the third section, I analyse the outcome of Karimov’s main economic policies, including the survival phase policies of the 1990s and a switch to growth phase policies in the 2000s. In the fourth section, I discuss the story behind the sustained aggregate growth in the 2004–2016 period, namely, Karimov’s industrial strategy and how it was financed. Key enabling and hindering factors related to the country’s future growth potential are analysed in the fifth section, followed by conclusions in the final section.

The early 1990s: initial conditions shape policy choices

Economic relations among the Soviet successor states were strongly intertwined by default as they had been coordinated from the centre, reflecting Union-level policy preferences. Uzbekistan specialised in commodity production and cotton, which dominated the agricultural sector. While Uzbekistan ran an inter-republican trade surplus in agriculture and light industry, it had large trade deficits in relation to food, energy and machinery (IMF Citation1991, p. 228). The sudden disintegration of the Soviet Union in August 1991 was largely unexpected, leaving member countries, especially those in Central Asia, ill-prepared for economic and political self-management. Some inter-republican trade relations that made economic sense at the Union level ceased to be commercially viable on the basis of mutual economic interests, inevitably resulting in large output losses and the deterioration of living conditions for many (Ruziev et al. Citation2007).

The output shock as well as the abrupt drying up of fiscal support from the centre had the potential to affect Uzbekistan with particular severity as a significant proportion of its large population was poor. As shows, Uzbekistan’s population was over 20 million in 1989, the third largest in the former Soviet Union (FSU) after Russia and Ukraine, and its income per capita was 62% of the USSR average. While 5% and 6% of households in Russia and Ukraine respectively earned less than R75 per month in 1989 (the effective minimum monthly wage at the time), this figure was 44% for Uzbekistan.

TABLE 1 Initial Conditions for Selected FSU Countries

Unlike most Eastern European countries, which had a long history of independent statehood and hence could afford to concentrate their reform efforts on creating functioning markets, building effective and credible state institutions was another monumental challenge for newly independent post-Soviet countries. Therefore, setting up and resourcing strong state institutions, some of which had to be created anew, to manage their internal and external affairs, defend their national borders, maintain law and order, collect taxes, and run and regulate newly created financial systems, was a vital first step to building a functioning market economy. Again, this was particularly important for a country of Uzbekistan’s size and geopolitical importance in the Central Asian region because of the material risks arising from emerging Islamist radicalism and populist nationalism, on the one hand, and the potential spill-over effects of civil conflicts in neighbouring countries, such as Tajikistan, Kyrgyzstan and the inherently unstable Afghanistan, on the other.

The customary Washington Consensus reform policy package, promoted by IFIs to developing countries ranging from the emerging economies of Latin America to the transition countries of Eastern Europe, was also on offer for Uzbekistan. The policy advice, comprising liberalisation, deregulation and privatisation, called for the removal of government intervention in matters concerning investment, production and exchange. It also implicitly recommended the gradual adoption of Western-style liberal democracy in political life (Chang Citation2002).

However, by assessing the overall situation in the country, Karimov’s government decided that it would play a proactive role in dealing with the immediate economic and political challenges, including creating a safety net to protect the country’s poor and a strong state apparatus to prevent any potential civil strife. The official government line was that policies recommended by IFIs did not take into account Uzbekistan’s particular needs and hence did not fit Uzbekistan’s gradualist approach to transition in general, and Karimov’s determination to carry out market-oriented reforms on his own terms and conditions in particular (Ruziev et al. Citation2007). In practice, however, public condemnation by Western-led institutions of the regime’s abysmal human rights record, including the harsh treatment of Karimov’s political opponentsFootnote6 and the widespread use of forced labour, including child labour, in agriculture also played an important role in the government’s decision to cool its relationship with IFIs (Akimov Citation2015). Unsurprisingly, with the rejection of the Washington Consensus framework for policymaking, the relationship between the Uzbek authorities and IFIs progressively worsened from the mid-1990s.

Some initial conditions were advantageous to the young Uzbek government, which aided its choice of policy approach. To begin with, Uzbekistan was established in the mid-1920s in central parts of the lands occupied by the Timurid Empire from the fourteenth to the sixteenth century, and then by the three independent kingdoms centred on Bukhara (emirate), Khiva (khanate) and Kokand (khanate), which ruled Central Asia until Russia invaded the region in the second half of the nineteenth century. Tashkent served as the regional administrative hub for the rule of Central Asia by Imperial Russia and subsequently by the Soviet government in its early years. This history meant that the Uzbek government had both a strong ideological narrative of independent statehood and the robust institutional capacity to create functioning state institutions. Furthermore, it had easily exportable tradeable goods such as cotton and gold, which jointly accounted for more than two-thirds of the country’s export revenues in the early 1990s. These resources meant that the Uzbek government had some policy breathing space, as it did not have to rely on the reform-conditional help of IFIs in stabilising the country’s macroeconomic conditions, including its balance of payments problems. Since joining the IMF in 1992, Uzbekistan has borrowed only twice from the Fund, US$106 million in 1995 and US$59 million in 1996.Footnote7

Islam Karimov, a Soviet-trained economist and former head of Uzbekistan’s central planning committee, was the main architect and the implementer of the Uzbek model of economic development, which was built on the following five principles (Karimov Citation1995, Citation1998).Footnote8 First, the state would play a guiding role throughout the transition period. This implied that the government would play a leading and proactive role in designing and implementing its own policy reforms. Second, maintaining law and order would be a priority. The dramatic economic and political instabilities of the early 1990s severely weakened public institutions’ ability to uphold law and order, which resulted in the erosion of trust in state institutions. As a result, racketeering and street gangs, alongside self-proclaimed paramilitary mafia-type informal institutions offering dispute-resolution services, became part of daily life. Hence, restoring public confidence in the ability of state institutions to uphold the basic rule of law was a key policy priority. The third principle was the provision of strong social protection. This meant that the government would create a strong social safety net in terms of staple food security, price controls, subsidies and targeted social assistance to the most vulnerable households. The fourth was a gradual and evolutionary transformation to a market-based economic system: the privatisation of large enterprises in key sectors of the economy, which almost exclusively referred to the natural resource sector, would not be immediate. This was Uzbekistan’s way of rejecting the emergence of an economic oligarchy. Fifth, economics would be prioritised over politics. In other words, the government would not rush to democratise the governance system. In effect, the heads of central, regional and sub-regional government offices would be appointed, not elected by popular vote. This also meant the rejection of a viable political opposition.

Main economic policies and outcomes

Karimov’s main economic policies, which were broadly in line with the generic transition strategy outlined above, can be divided into two distinct phases: the ‘survival phase’ and the ‘growth phase’. The survival phase policies, which lasted until the early 2000s, focused on ensuring food security, reviving the reputation and prestige of state institutions, creating a robust social safety net to prevent potential civil discontent and strife, setting up national monetary and financial systems, and achieving macroeconomic stability. Among other things, building a strong and effective state apparatus involved offering generous salary and pension packages to police, secret service and defence forces who then effectively implemented the government’s zero-tolerance policy against street gangs and mafia-type informal dispute-resolution groups. As a result, these organised criminal structures were eradicated by the mid-1990s, which was relatively swift compared to the experiences of other FSU countries such as Russia (Galeotti Citation2018).

At the start of transition, Uzbekistan found itself heavily dependent on the import of basic foodstuffs and energy resources, each accounting for about 20% of the country’s imports in 1993 (Ruziev et al. Citation2007). To achieve self-sufficiency in basic consumption goods, some of the land previously reserved for cotton production was reallocated to key agricultural produce such as wheat and potatoes. As can be seen from (Panel A), wheat production increased by more than 520%, while the production of potatoes almost doubled during this period. In terms of energy (see Panel B of ), the production of crude oil increased by over 80% (150% compared to the 1991 level) and that of natural gas by over 35% during the same period.

TABLE 2 Uzbekistan’s Selected Early Transition Performance Indicators, 1993–2003

The output contraction in the early 1990s was not as severe as in other transition economies. The average annual growth rate for the 1993–2003 period was strong (about 4%) but not exceptional. The combination of these factors helped the country to surpass its pre-1989 output level by 11% by 2003 (see Panel C of ), a significantly better performance compared to the average output performance of other transition economies for the same period. By analysing various potential determinants of Uzbekistan’s ‘growth puzzle’ such as favourable initial conditions and measurement errors, Zettelmeyer (Citation1998) concluded that good policy and public investments were the major explanatory factors. Other scholars put Uzbekistan’s success down to a combination of factors, including favourable external conditions, namely, the resource boom (Pomfret Citation2003; Ruziev et al. Citation2007), preservation of the capacity of state institutions, good macroeconomic policy and export-oriented industrial policy (Popov Citation2013).Footnote9 In particular, the government actively used state orders, subsidised loans and undervalued exchange rates as tools to achieve important structural shifts in the economy: attaining self-sufficiency in food, becoming a net fuel exporter and increasing industry’s share in GDP (Popov Citation2013, p. 12).

As can be seen from Panel D in , the country managed to reduce its dependence on food imports by almost half between 1993 and 2003 and became a net exporter of energy. This helped to improve Uzbekistan's current account (CA) position from a deficit of 8% of GDP in 1993 to a surplus of almost 9% of GDP in 2003. The government also tightened public spending and monetary policy, thereby reducing the inflation rate to moderate levels by the late 1990s. The generally frugal approach to spending, which was aided by the modest but persistent aggregate economic growth as well as the rents generated from the natural resources sector, also allowed the government to keep debt levels under control. By 1998, the public debt was only about 30% of GDP. Although this figure went up to around 42% in 2003, it was not a cause for concern as the overall budget was in a small surplus and the debt was almost exclusively long-term external borrowing (Ruziev & Majidov Citation2013).

Although the Uzbek authorities always referred the appropriateness of the ‘Uzbek model’ of development to the country’s unique social and economic context (Karimov Citation1995, Citation1998), the official narrative never went beyond the above-mentioned five principles associated with its gradualist approach to transition. Indeed, the exact nature of the Uzbek growth model remained undefined (Pomfret Citation2000; Ruziev et al. Citation2007). By the early 2000s, however, it became clear that the authorities were using the conventional ‘development’ planning approach that prioritised growth (Chenery & Strout Citation1966). In this approach, the targeted growth rates necessitate improvements in the accumulation of capital, which in turn requires investments to be financed through domestic saving. If a country’s saving is insufficient to achieve the required level of investment, growth targets can still be achieved by borrowing from abroad, or by increasing the efficiency of its investments, or both. Since domestic saving is the most important of these factors, the growth policies in the 1960s and 1970s in the developing world focused on directing scarce domestic savings to finance their industrialisation drive. This was done by imposing various restrictions on the financial sector, including interest rate ceilings on bank loans, directed lending by state-owned banks to certain industries, maintaining multiple exchange rate regimes and restricting international capital flows. Although the counterproductive nature of some of these repressive policies is well known in the literature (McKinnon Citation1973; Shaw Citation1973), the Uzbek government went ahead with them anyway, as it was sceptical about the underlying theoretical arguments (Williamson & Mahar Citation1998) that liberalisation, deregulation and privatisation would remove detrimental market distortions and result in a better and more sustainable method of capital accumulation (Ruziev et al. Citation2007).

Emboldened by the success of the early economic policies, Karimov’s government set a more ambitious growth target for the 2000s and beyond, with the aim that Uzbekistan would become an upper middle income group country by 2030 (IMF Citation2013, p. 4). In effect, this meant a switch from ‘survival phase’ to ‘growth phase’ policies. Despite the distortions created in the financial sector (Ruziev & Ghosh Citation2009), which will be discussed in detail later, the Uzbek authorities managed to double the 4% average growth rate achieved in 1993–2003 in the 2004–2016 period. It is important to note, however, that economic policies were not the only driving force behind this success: there also was an element of luck. Constrained by limited investable resources, the government decided to invest in capital-intensive sectors such as in gold mining and natural gas extraction, which expanded the natural resource sector. The increased production of natural resources in turn coincided with the global resource boom, particularly after 2003 (Pomfret Citation2019, p. 97), helping the government to achieve its growth targets and to keep its macroeconomic fundamentals, including the inflation rate, the government budget deficit and the public debt, in order.

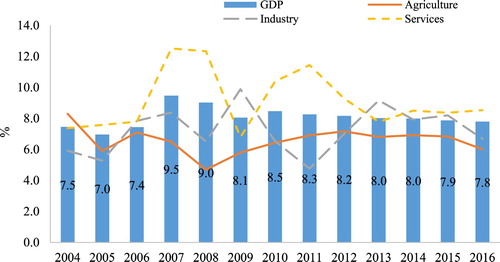

As can be seen from , the average annual GDP growth rate for the 2004–2016 period was more than 8%. This is indeed an impressive outcome as achieving growth rates of 5% or higher for a sustained period of ten years or more is very rare in practice. Although one must be cautious when dealing with official statistics, it has been suggested recently that Uzbekistan still relies on a Soviet-style system to compile its national statistics (IMF Citation2018a, p. 9), which leaves some economic activities in the services and small-scale manufacturing sectors not fully reflected in GDP figures (Pajank Citation2019).

FIGURE 1. Economic Growth in Uzbekistan, 2004–2016

Source: Asian Development Bank (Citation2018).

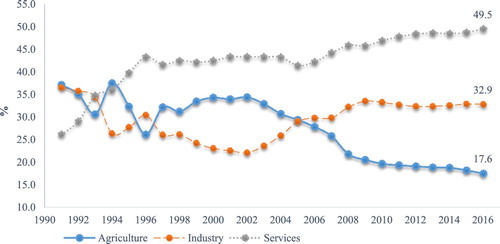

shows that, although all three sectors of the economy contracted in the early 1990s, the decline was most severe in the industrial sector, which shrank by almost 40% by 1994. This decline, combined with the government’s focus on food security, which boosted agricultural production, meant that industry’s contribution to GDP decreased from about one-third in 1992 to about one-fifth in 2002. In the 2004–2016 period, however, the industrial sector grew faster than the agricultural sector. By 2016, the industrial sector accounted for about one-third, and services almost half, of Uzbekistan’s economic activity. Agriculture as a share of GDP, in the meantime, declined from about 37% in 1992 to about 18% in 2016.

FIGURE 2. Changing Share of Economic Sectors as % of Uzbekistan’s GDP, 1991–2016

Source: Asian Development Bank (Citation2018).

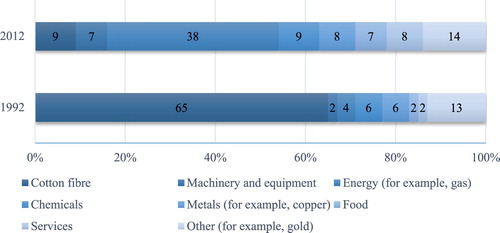

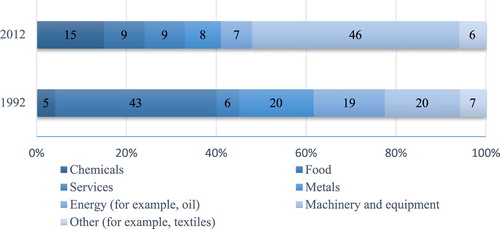

The targeted economic policies also affected the structure of the country’s exports and imports, as shown in and for the period 1992–2012. In 1992, cotton fibre was the single largest export item, accounting for 65% of exports; the second biggest category was precious metals, such as gold, which accounted for about 13% of exports. Twenty years later, the structure of exports had become much more diversified and sophisticated. In 2012, cotton fibre was only a joint third export item alongside chemicals, each accounting for 9% of exports. Other tradeable sectors of the economy, such as the energy sector, also expanded. By 2012, the country was exporting noticeably more energy (for example, natural gas), chemicals (oil and gas derivatives), machinery and food. Exports were now dominated by energy (38% of exports), the direct outcome of a conscious policy as the authorities invested heavily in the sector. In terms of imports, between 1992 and 2012 the share of foodstuffs in total imports dropped from 43% to 9%, metals from 20% to 8%, and energy from 19% to 7%, while machinery went up from 20% in 1992 to 46% in 2012. In general, the structure of the country’s imports changed noticeably from consumption goods to investment goods between 1992 and 2012.

FIGURE 3. Diversification of Uzbekistan’s Exports, 1992–2012

Source: World Bank (Citation2013, p. 7).

FIGURE 4. Changing Structure of Uzbekistan’s Imports

Source: World Bank (Citation2013, p. 7).

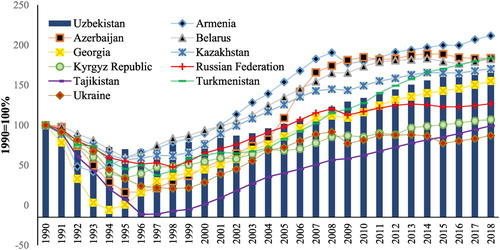

compares Uzbekistan’s income per capita in PPP terms (constant prices) to other FSU countries. Since income per capita among these countries varied widely upon their independence (see ), their comparative performances can be better assessed by setting the base year (1990) to 100%. Uzbekistan experienced the shallowest decline in living standards at the start of transition, which rose slowly but steadily until the early 2000s and then more strongly. In 2018, Uzbekistan was outperformed only by Armenia, Azerbaijan, Belarus and Turkmenistan. The fact that uses per capita figures and that the populations of Armenia (down from 3.5 million in 1990 to 3.0 million in 2018) and Belarus (down from 10.2 million in 1990 to 9.5 million in 2018) declined during this period also puts Uzbekistan’s performance—its population increased from 20.5 million in 1990 to 33 million in 2018—into perspective. Further, exceptional economic growth in Azerbaijan and Turkmenistan can essentially be explained by the expansion of their large hydrocarbon sectors.

FIGURE 5. GDP per capita in Selected Former Soviet Countries, 1990 = 100% (PPP $US, 2011 Constant Prices)

Source: World Bank (Citation2020).

The story behind sustained aggregate growth: the financing of industrial policy

Industrial policy strategy: focus on capital-intensive industries

The general consensus in the growth literature is that income levels are determined by a number of interlinked factors, including the availability of factors of production and the efficiency of their use. These in turn are influenced by other factors, such as the rate of savings and investments, the inflow of foreign capital, the quality of institutions, macroeconomic stability, and a country’s willingness to credibly commit to and carry out its development plans. Yet, the cross-country empirical evidence for the convergence of per capita income levels between rich and poor countries is dismal,Footnote10 which is hardly surprising as, unlike in orthodox models of economic growth, the production functions of individual countries are very dissimilar and not fully known (Hausmann & Rodrik Citation2003, p. 623).

However, there are more than a dozen success stories: over the 1960–2014 period, 16 countries managed to reach high income status (Cherif & Hasanov Citation2019, p. 5). This indicates that although sustaining high growth rates is indeed hard, it can be done. The World Bank (Citation2008), by carefully studying the key attributes of 13 such countries since the 1950s, concluded that their most common characteristics included high domestic savings and investment, openness to trade, macroeconomic stability, resource mobility, an active role by the governmentFootnote11 and, most importantly, an industrial policy.

Although mainstream development policy research accepted that industrial policy has a key role in growth acceleration (Cherif & Hasanov Citation2019), questions about how industrial policy strategies can be formulated and implemented are still under debate. For example, should countries conform to their traditional areas of comparative advantage, often associated with labour-intensive areas of production, and gradually build capacity to enter more capital-intensive industries (Lin Citation2012) or be more ambitious and invest in capital-intensive industries with high value-added potential from the outset, that is, defy their comparative advantage (Lin & Chang Citation2009)?

Uzbekistan’s version of industrial policy can generally be defined as defying comparative advantage. Independent Uzbekistan had an abundant supply of well-educated cheap labour and was one of the largest producers and exporters of raw cotton in the world, thus one would expect the country to focus on developing its light industry first. However, while working towards achieving survival phase policy targets in the 1990s, the government decided, early on, to invest in capital-intensive industries instead. Indeed, a recent in-depth study of the country’s per capita income growth found that practically all of the improvements in per capita income growth for the 1996–2016 period could be explained by improvements in labour productivity, which in turn was explained by the rise in the capital-to-labour ratio (Trushin Citation2018).

Depending on the nature of the industry, investments were planned and sequenced to promote potential backward and forward linkages. In the hydrocarbon sector, the expansion of crude oil and natural gas production in the 1990s was followed by the setting up of several large-scale processing plants to produce various derivative products, which could be used as intermediate goods in other industries. For example, the Shurtan Gas–Chemical Complex, which had a project value of around US$1 billion, started operations in March 2001. The complex consists of gas treatment and separation units, ethylene and butane copolymer production plants and a polyethylene plant.Footnote12 The most recent and the largest chemical plant, with a project value of around US$4 billion, started operation in 2016. Known as the Ustyurt Gas–Chemical Complex, this unique industrial complex comprises of five plants: a gas separation plant, an ethylene production plant, a polyethylene production plant, a polypropylene production plant and an energy supply plant.Footnote13 Raw materials for the chemical industry mostly come from domestically produced ethane-rich natural gas, hence the plants are usually built near large gas deposits offering them an uninterrupted supply of low-cost inputs.

The automotive industry, which was built from scratch, is perhaps the best example of industrial policy in Uzbekistan. Unlike the gas and chemical industry, the outcome of the automotive industry is immediately observable to the general population—cars on streets and in people’s garages—and can help legitimise the authorities’ approach to economic development. Hence, it became a flagship project. The strategy, which is based on assembling well-known global brands and facilitating a gradual localisation of production, started with the establishment of a car plant in 1992, followed by production plants for small trucks and buses in 1996 and the assembly of large trucks and buses in 2009 (Popov & Chowdhury Citation2016; Pomfret Citation2019).

There are only three car producers in the sector, all focusing on a particular segment of the market, so they are not direct competitors. For example, UzAuto Motors specialises in the production of passenger cars, SamAuto specialises in the production of small trucks and buses, and MAN Auto-Uzbekistan produces large trucks and buses. The government’s industrial strategy for the sector is implemented through Uzavtosanoat (Uzbekistan Automotive Industry), a state-owned umbrella organisation that controls all the major projects relating to the automotive industry in the country.

UzAuto Motors was originally established by a government decree in November 1992 as a joint venture with a Korean producer, Daewoo Motors, in Asaka, a small town in the Andijon region. The new plant, with an annual production capacity of 200,000 cars, started production in 1996. In 2001, Daewoo Motors in Korea was acquired by General Motors (GM), which resulted in the rebranding of the joint venture from UzDaewooAuto to GM Uzbekistan in 2008. Uzavtosanoat initially owned 75% and GM the remaining 25% of the company shares. In 2019, Uzavtosanoat became a sole owner of GM Uzbekistan and rebranded it to UzAuto Motors. UzAuto Motors has three plants located in Andijon, Khorazm and Tashkent with a combined annual production capacity of 300,000 passenger cars. The company sells its products under the Chevrolet brand in the domestic market and the Ravon brand in export markets. The localisation of production has been gradual and relatively slow. According to UzAuto Motors, it reached 50% in 2019.Footnote14 The most notable example of the localisation programme was the establishment of an engine plant in Tashkent in 2008. The plant, GM Powertrain Uzbekistan, has a maximum production capacity of 360,000 engines per annum (Popov & Chowdhury Citation2016, p. 10).

In 1996, the authorities set up another joint venture, this time with Turkish capital, which specialised in the production of buses (four models) and small to medium sized trucks. The new plant, located in Samarkand and branded SamKochAuto, started production in 1999. In 2006, Uzavtosanoat purchased the Turkish share in the company and rebranded it to SamAuto (Samarkand Automobile Plant).

In 2009, another joint venture to produce heavy goods vehicles was set up in Samarkand with MAN Bus and Truck Company. The plant, named JV MAN Auto-Uzbekistan, started the production of trucks with a gross vehicle weight of 15–50 tonnes in 2009. It has an annual production capacity of 3,000 trucks.Footnote15 In order to benefit from economies of scale and potential positive externalities, the government intends to expand the sector and make it more competitive in the near future.Footnote16 For example, in March 2020, Uzavtosanoat signed an agreement with Volkswagen Group to produce light commercial vehicles.Footnote17 It is also working with Hyundai to produce buses, trucks and electric cars.Footnote18 As an infant industry, however, the automotive industry is highly protected. Imported cars, buses and trucks are subject to high custom duties, which can vary depending on year of manufacturing, country of origin and engine volume (Popov Citation2013; Popov & Chowdhury Citation2016). There are many precedents for protectionist policies towards fledging industries: Japan protected its car industry for nearly four decades (Lin & Chang Citation2009).Footnote19

Industrial policy financing: natural resource rents and external borrowing

Although Uzbekistan has used multiple policy measures to support its industrial strategy, the country’s rich natural resource endowment base has played a key role in shaping its overall approach to industrial policy financing. shows some of the key indicators relevant to this discussion. For concise representation, only presents five data points (1996, 2001, 2006, 2011 and 2016) from Karimov’s final 20 years in office. also includes 2017 when the latest data were available for all indicators. As can be seen from row 1, Uzbekistan has generated significant resource rents, calculated as the difference between the price of a commodity and the average cost of producing it, from its natural resources industry. Natural resource rents are prone to wide fluctuations depending on prevailing commodity prices. Uzbekistan’s average rents were around 9% of GDP in 1990–1999, around 28% of GDP in 2000–2009, and around 19% of GDP in 2010–2016 (World Bank Citation2019). The rents generated from the sector helped the government to keep domestic finances in order and to offer a decent social safety net to the general population and enabled the channelling of surplus funds to targeted industrial projects. These rents also served as implicit collateral in attracting large amounts of publicly guaranteed external loans.

TABLE 3 Key Macroeconomic Variables, Selected Years

In order to manage the resource rents more effectively, the government set up a special sovereign wealth fund, the Fund for Reconstruction and Development (FDR), in 2006. The FDR’s main objectives are to accumulate resource rents in excess of a certain cut-off price and to use these funds to co-finance strategic government-selected projects. The government usually spends a stable proportion of tax revenues from the natural resource sector, equivalent to about 2–3% of GDP, and saves the rest with the FDR (IMF Citation2013, p. 7). The FDR has accumulated around US$20 billion since its establishment (IMF Citation2019b).

Foreign direct investments (FDI) did not play a particularly strong role in the country’s industrialisation drive until 2006 (Row 2 in ). The cumulative FDI for the entire 1992–2006 period was less than US$1.5 billion. In 2016, the cumulative stock of inbound FDI was less than 15% of GDP, which compares poorly against the CIS average of over 60%. In the absence of strong FDI flows, the government resorted to significant external borrowing to finance its investment projects (, rows 3 and 4): in 2001, the ratio of external debt to GDP was more than 41%. About four-fifths of these loans were public or publicly guaranteed loans, of which more than 90% were long term (ADB Citation2019). From the mid-2000s, the government started allowing external investments in the exploration and development of new oil and gas deposits, which resulted in cumulative FDI of around US$10 billion for 2007–2016. This, combined with the healthy expansion of the economy, allowed the authorities to reduce, first, the ratio of external debt to GDP from over 41% to around 24% and, second, the share of government-guaranteed loans from over 80% to 47% between 2006 and 2016 respectively.Footnote20

Uzbekistan has also benefited greatly from the large inflow of private remittances from its citizens working abroad. Although the economy has grown steadily since the 2000s, most of the aggregate growth has been driven by the expansion of capital-intensive sectors, making the growth elasticity of employment very low (Trushin Citation2018). Various studies have estimated the unemployment rate in Uzbekistan at around 30% of the labour force (Ruziev & Majidov Citation2013, p. 696; Trushin Citation2018). Kazakhstan and Russia, with per capita income levels respectively three and five times higher than that in Uzbekistan in 1990 and which enjoyed particularly strong economic growth in the 2000s, are the most favoured destinations for a significant proportion of the country’s unemployed and underpaid workers. As of 2013, it was estimated that there were around two million Uzbek citizens working in Russia alone (Ilkhamov Citation2013, p. 260). According to more recent estimates (Eraliev & Urinboev Citation2020, p. 258), more than two million Uzbeks were in Russia in 2019.

Unfortunately, official data for remittances are patchy (see the fifth row of ). For the 2006–2016 period, the average ratio of remittances to GDP was around 7.5%. To put this in perspective, the cumulative net FDI flows for the 1992–2018 period was only US$13.0 billion, whereas the cumulative private remittances for the 2006–2018 period exceeded US$46 billion. Remittance flows contribute significantly to domestic demand, and, more importantly for the government’s industrial policy financing. They also serve as a vital source of foreign exchange revenues which are used for both paying the country’s import bill and servicing its external debt.

The final row in shows the official exchange rate, which, however, does not tell the full story, as Uzbekistan used multiple exchange rates as a policy tool to promote its industrial strategy (Popov Citation2013; Holzhacker Citation2018). The multiple exchange rate regime was in place for most of the time from July 1994, when the national currency was launched, to September 2017, when the official exchange rate was finally liberalised after Mirziyoyev came to power. For example, before the liberalisation of the foreign exchange market, there were three exchange rates: the official rate, the bourse rate and the black-market rate. Only legal entities with special government permission, which effectively meant large state-owned enterprises (SOEs) in preferred industries, had full access to foreign exchange at the official rate. Exporters surrendered 25–50% of their foreign exchange earnings to the central bank. The rest could be sold to legal entities, which usually were small- and medium-sized wholesale and retail traders importing non-strategic consumption goods, using the bourse rate. Finally, the black market was used by shuttle traders and the general public. Normally, the bourse and black-market rates were about twice as high as the official rate. Just a few weeks before the liberalisation of the market in September 2017, the official exchange rate was around 4,100 so’ms per US dollar, the bourse rate around 8,500 so’ms, and the black-market rate around 8,400 so’ms.Footnote21

Keeping the official exchange rate artificially low had several advantages. First of all, it allowed the government to direct resources from export industries producing gold, minerals and cotton to finance industrial projects in the automotive and gas and chemical industries. It also helped to keep the prices of strategically important capital goods as well as socially important consumer goods, such as pharmaceuticals imported from abroad, low. Further, since most of the industrial projects were financed using publicly guaranteed external loans, the low exchange rate significantly reduced the debt burden of favoured industries (Holzhacker Citation2018, p. 8). However, the strict forex controls had many disadvantages too; they discouraged independent exporters and fuelled rent-seeking behaviour by a select few, often with strong political connections to high-level public officials.

Unleashing the future growth potential: enablers and obstacles

Since his election as Uzbekistan’s president in December 2016, Shavkat Mirziyoyev has introduced wide-ranging liberalisation policies in almost all spheres of economic life, apparently beginning the transition to a market economy. Past experience from successful transition economies indicates that economic performance may be bumpy in the early years of structural reforms. In Uzbekistan’s case of reform acceleration, however, the government inherited robust macroeconomic conditions from the Karimov regime that may have actually facilitated growth acceleration.

shows some of the key indicators of macroeconomic stability, including inflation, government deficit and debt, and international reserves. Inflation levels remain moderate: the average annual inflation rate in the 2007–2016 period was about 11%. Mirziyoyev’s government also inherited conservatively managed government finances (see the data rows 2, 3 and 4 in ): the average annual budget surplus for the 2007–2016 period was 4.3% of GDP. Because the country also experienced strong economic performance during this period, the share of public debt to GDP fell to about 10% by 2016. And, interestingly, ‘the government holds almost no domestic debt [and] public debt consists entirely of external debt’ (IMF Citation2018b, p. 2), which explains why the ratio of the public debt to GDP jumped to 20% in 2017 as a result of the sharp depreciation of the national currency in September 2017.

TABLE 4 Indicators of Macroeconomic Stability, Selected Years

also shows the country’s international reserves. Because of its effective commitment to a fixed exchange rate and price stability, the Central Bank of Uzbekistan (CBU) has had to sterilise large inflows of international reserves generated by commodity exports and private remittances since the early 2000s, which has resulted in significant reserve accumulation over time. The stock of international reserves was more than US$28 billion at the end of 2017, equivalent to about 60% of GDP (ADB Citation2018). As a rule of thumb, policy analysts assess international reserve adequacy in terms of the sufficiency of international reserves to cover a country’s import bill for three months. Since the late 1990s, the Greenspan–Guidotti rule of 100% reserve coverage for short-term external debt has also become a widely used measure (Jeanne & Rancière Citation2011, p. 907). Using these metrics, at the end of 2017, Uzbekistan’s reserves were equivalent to 19 months of imports, more than ten times higher than the amount required under the Greenspan–Guidotti rule. They were also about ten times higher than the IMF’s more stringent reserve adequacy metric, which measures a country’s potential foreign exchange needs in adverse scenarios under country-specific circumstances (IMF Citation2019b, p. 44).

Holding such a large stock of international reserves offers several advantages. It helps the government to avoid excess volatility of exchange rates, reduces the likelihood of balance of payments crises, and ensures economic and financial stability. It also helps to meet the country’s external obligations, including servicing its external debt and paying its import bill, and gives confidence to international lenders and investors. And, in the worst case scenario of government-led investments going wrong, the stock of international reserves can help clear the balance sheets of large SOEs in priority sectors.

Although the large stock of liquid reserves can serve as a cushion against various shocks, it does come with a huge opportunity cost. To give an example, in February 2019, Uzbekistan launched its own debut Eurobonds at the London Stock Exchange, raising US$1 billion in two US$500 million tranches with five- and ten-year maturities. As the result of a strong overbooked response, which was more than US$8.5 billion, the bonds were launched at 4.75% and 5.38% respectively.Footnote22 A simple comparison of these rates to the very humble return of 1% CBU earns on its international reserves (IMF Citation2019b, p. 44) translates into an annual opportunity cost of around US$1.2–1.5 billion or about 2–3% of GDP. When one considers that the government also attracts billions of dollars’ worth of external loans under government guarantees at higher rates, it becomes clear that the opportunity costs are actually much higher. Further, given the government’s continuous commitment to promoting industrialisation, lending the country’s excess liquidity at low rates and then borrowing external loans at much higher rates on international financial markets does not make much economic sense either.

Although the economic performance was impressive in terms of some key macro indicators under Karimov’s rule, this was achieved largely by favourably treating capital-intensive sectors of the economy, which remain state-owned and/or state controlled (for example, granting direct credits, undervaluing the national currency) and investing heavily in them. As a result, practically all of the improvements in per capita income growth for 1996–2016 were explained by the rise in the capital-to-labour ratio; also, the employment rate fell from 71% to 63% during this period (Trushin Citation2018). The regime’s excessive reliance on state-induced capital accumulation and its disregard for institutional reforms, therefore, hindered the emerging private sector’s growth prospects, first, by restricting access to important resources (such as formal finance) and, second and most importantly, by failing to credibly promote the rule of law, hence failing to protect sanctity of private property (Ruziev & Midmore Citation2015). Hence, while continuing a government-led industrial strategy, accelerating and credibly committing to reforms in these areas may facilitate greater participation by the private sector (which, in Uzbekistan, is by definition labour-intensive) in wealth creation. This, in turn, may induce more sustainable capital accumulation, augment aggregate growth and make growth more inclusive.

To unleash the country’s true growth potential, therefore, Mirziyoyev’s government also needs to reform and invest in several key areas. In particular, significant obstacles to growth include low financial intermediation, low investment in human capital, especially at the level of tertiary education, and a lack of credible commitment to institutional reforms, which are fundamental in promoting sustainable investment in, and hence the accumulation of, physical and human capital.

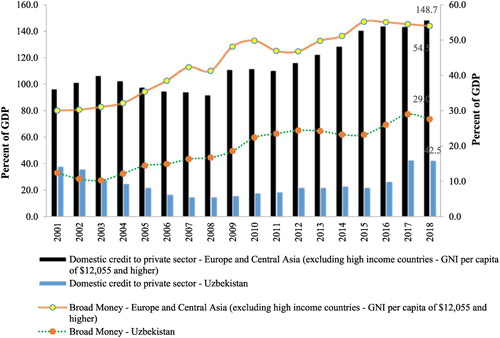

Starting with financial intermediation, and below provide some basic information about this sector. As can be seen in , Uzbekistan’s financial intermediation measures in terms of the ratios of private credit and broad money to GDP are rather shallow when compared to similar figures for the Europe and Central Asian (ECA) region.Footnote23 For example, in 2018, the ratio of private credit to GDP was 43% for Uzbekistan and almost 150% for the ECA region, and the ratio of broad moneyFootnote24 to GDP was 29% for Uzbekistan and 55% for the ECA region.

FIGURE 6. Financial Sector Development in Uzbekistan and the Europe and Central Asia (ECA) Region Compared, 2001–2018

Source: World Bank (Citation2019); ADB (Citation2019).

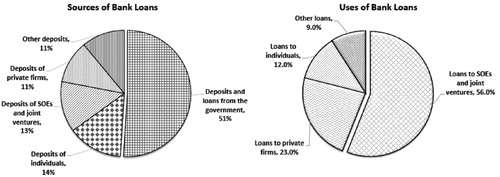

FIGURE 7. Sources and Uses of Bank Loans, 2017

Source: IMF (Citation2018c, p. 33).

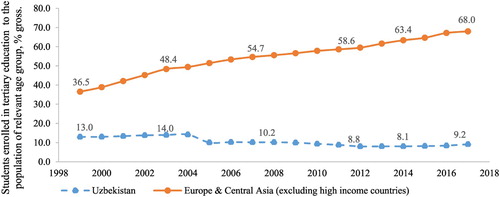

FIGURE 8. Tertiary Education Enrolment in Uzbekistan and the Europe and Central Asia Region, 1999–2017

Source: World Bank (Citation2019).

The banking sector, which was considered as one of the commanding heights in the government’s industrialisation drive, is one of the least reformed sectors of the economy. The share of state-owned and state-controlled banks in the total of banking sector assets and liabilities remains more than 80% (Ruziev & Majidov Citation2013; IMF Citation2018c). The banking sector has been mainly used by the government to channel externally and internally generated loans to priority sectors of the economy.

As shows, at the end of 2017, more than 56% of all banking sector loans were extended to SOEs and joint ventures at preferential rates, leaving a large proportion of small and medium enterprises credit-starved (Ruziev & Midmore Citation2015; Holzhacker Citation2018). Further, with regard to the sources of loanable funds, more than half were deposits and loans from the government (IMF Citation2018c, p. 33). This, combined with very low levels of deposits (14% of the total) from and loans (12% of the total) to the general public, indicates that market-based financial intermediation has not fully taken off.

The next significant bottleneck has been investment in human capital. This is of particular importance for a country like Uzbekistan, which is committed to rapid economic modernisation. As Lucas (Citation1993, p. 270) argued, the differences in human rather than physical capital explain most of the variations in per capita income levels across countries, a view strongly supported by abundant empirical evidence. Indeed, accumulation of human capital positively and significantly contributes to per capita output growth (Temple Citation1999). Education in general, and higher education (HE) in particular, contributes to human capital accumulation through the process of creating new ideas, blueprints and innovative technologies (Pegkas & Tsamadias Citation2014). As the main driver of knowledge production, HE plays an especially important role in modern knowledge-based economies (Olssen & Peters Citation2005). In well-functioning meritocratic economic systems, HE also serves as a catalyst for achieving social mobility and cohesion (Ruziev & Burkhanov Citation2018).

Although Uzbekistan, as of 2013, spent around 8% of GDP on its education system, only a small proportion of this budget went on HE, which declined from 10% in 1990 to around 5% in 2013 (World Bank Citation2014, p. 72). In fact, Uzbekistan is the only post-Soviet country in which the share of school leavers studying university courses has fallen since independence (Huisman et al. Citation2018). compares Uzbekistan’s gross tertiary enrolment figures to that of the ECA regions for the period 1998–2017. While the ratio of students enrolled in tertiary education to their relevant age group increased from around 36% in 1999 to 68% in 2017 in the ECA region, it fell from 13% in 1999 to 9% in 2017 in Uzbekistan (Ruziev & Burkhanov Citation2018).

Uzbekistan’s industrial strategy and growth model have, so far, focused solely on state-induced capital accumulation. However, a relatively new stream of literature emphasises the importance of institutional capacity building in sustaining growth. In particular, North (Citation1994), Hall and Jones (Citation1999) and Acemoglu et al. (Citation2005) argue that factor accumulation is only a proximate cause of growth and that human-made incentive and constraint mechanisms represented by, for example, rules, regulations and conventions, provide incentives to invest sustainably in physical and human capital. In other words, by enforcing the rule of law, by protecting property rights, and by ensuring equality of opportunities to a broader cross-section of society, these institutions facilitate a more sustainable accumulation of physical and human capital and hence should be considered the fundamental cause of sustained long-run growth.

The World Bank’s Doing Business Database and the Heritage Foundation’s Economic Freedom Index provide interesting insights about overall economic climate and quality of institutions across the world. However, the Rule of Law Index developed by the World Justice Project (WJP) is a more appropriate proxy to use in our context, as it is comprehensively constructed on the basis of eight interrelated factors comprising: constraints on government powers, absence of corruption, open government, fundamental rights, order and security, regulatory enforcement, civil justice and criminal justice.Footnote25 Unfortunately, as can be seen from , Uzbekistan still performs very poorly in all but one of these factors in relation to its regional and global peers. In terms of the overall Rule of Law Index, it comes 12th out of 13 countries in the ECA region and 94th of out 126 countries in the global ranking.

TABLE 5 Uzbekistan’s 2019 Rule of Law Rank Compared

Although reforms aimed at improving institutional capacity building have accelerated since 2017, a more important message to the business community is the credibility of the government’s commitment to these reforms. In a speech on 19 May 2018, President Mirziyoyev himself admitted that: ‘People are testing us, testing us seriously. They wonder how long the reforms will last. They are afraid that sooner or later the authorities will go back to their old ways’.Footnote26 Mirziyoyev’s government is trying hard to change the image of the country for the better by accelerating the pace of economic reforms. The government also seems to be committed to taking the country away from authoritarianism and isolationism to individual freedom and economic openness. Indeed, in his interview to Bloomberg, Deputy Prime Minister Jamshid Kuchkarov noted that the main aim of issuing sovereign Eurobonds was not to raise money but to send a signal to the international community of investors that Uzbekistan was open for business and open to external scrutiny.Footnote27 Gaining credibility, however, takes time and Uzbekistan is still in the early stages of establishing itself as a trusted player.

Concluding remarks

Uzbekistan’s distinctive post-independence experiment with development was led by Islam Karimov until his sudden death in September 2016. Karimov’s economic policies in the 1990s were influenced by his desire to protect the most vulnerable households, which constituted a significantly large proportion of the general population, from the sudden shock of transition and also to prevent a sharp output loss. Emboldened by its early success, Karimov’s government shifted its attention to growth phase policies from the early 2000s. To accelerate growth, the government decided to invest heavily in capital-intensive sectors of the economy.

Upon his death, Karimov left behind a more sophisticated and diversified economy and sound macroeconomic fundamentals including moderate inflation, low government debt and a large stock of international reserves. While these factors provided a firm foundation for the successor government’s reforms, Mirziyoyev also inherited some fundamental obstacles.

While rejecting radical market reforms in the 1990s, the Karimov government had stated that its gradualist policies and associated growth targets were intended to prevent a drastic deterioration of living conditions and to strengthen social welfare. Ironically, the industrial policy followed by Karimov relied heavily on investment in capital-intensive sectors. This meant that the government’s growth targets ultimately became an end in themselves rather than a means to improve living conditions. Karimov’s growth model focused on state-induced accumulation of physical capital and failed to facilitate a more sustainable market-based method of human, physical and financial capital accumulation. The regime also stifled economic and individual freedoms and failed to commit credibly to market-based reforms, thereby curtailing economic opportunities for a broader cross-section of society.

Since his election, President Mirziyoyev has surprised many observers by his commitment to accelerating economic reforms. Building on the sound macroeconomic fundamentals and other enabling factors inherited from the Karimov regime, he has aimed both to deal with the main obstacles to the country’s growth potential and to make growth more inclusive. Mirziyoyev highlighted his overarching economic development strategy in the presidential decree, ‘On the Strategy for the Further Development of the Republic of Uzbekistan’, issued on 7 February 2017 (Government of Uzbekistan Citation2017). One of the priority areas stressed in the decree was the development and liberalisation of the economy. The decree broadly confirmed that the new government was still committed to facilitating rapid industrialisation of the economy. In the meantime, the government also aimed to make the economy more vibrant by introducing market-oriented reforms and competition to all sectors of the economy (Government of Uzbekistan Citation2019a).

The current government wants to achieve its commitment to inclusive growth by encouraging and supporting entrepreneurship and investment more in labour-intensive sectors, which were largely overlooked under the previous regime. For example, to expand the country’s tourism industry, the government has either simplified or completely cancelled visa requirements for most countries and is investing in local tourism infrastructure (Government of Uzbekistan Citation2019b, Citation2020). The government also wants to expand light industry (Government of Uzbekistan Citation2019c); for example, in 1992, cotton fibre was the single largest export item, accounting for 65% of exports; from 2020, the authorities aim to stop exporting cotton fibre altogether and replace it by more expensive yarn cotton and cotton fabric exports, etc. This is a reasonable strategy as, generally, countries can create and capture more value as they move from raw material networks (raw cotton), to component networks (yarn, fabric), production networks (the manufacturing of apparel) and export networks (branding and marketing) (Appelbaum & Gereffi Citation1994). However, the success of the policy will also depend on whether or not the country can join global value chains as, in the twenty-first century value chains, more value is actually created at the design, marketing and sales stages than at the manufacturing stage (Baldwin Citation2013, p. 37).

One of the main reasons Karimov’s autocratic regime resisted the structural reform packages advocated by IFIs in the 1990s was that such packages implicitly promoted political liberalisation and democratisation as a natural counterpart of economic reforms. Although cross-country empirical evidence regarding the impact of various measures of democracy on economic growth is not strong (Alesina & Perotti Citation1994; Acemoglu et al. Citation2008), the virtues of economic and political freedoms are hard to deny (Friedman Citation1982; Sen Citation1999; Hayek Citation2005). Further, while Friedman (Citation1982) strongly argued that economic liberalisation, through improvements in living standards, would necessarily lead to political liberalisation, Hausmann et al. (Citation2005) found that political regime changes were statistically significant predictors of growth acceleration. It remains to be seen if regime change can lead to growth acceleration and eventual political liberalisation in Uzbekistan. On balance, early indications are positive.

Additional information

Notes on contributors

Kobil Ruziev

Kobil Ruziev, Bristol Business School, University of the West of England, Bristol, BS16 1QY, UK. Email: [email protected]

Notes

1 ‘An Ailing Despot’, The Economist, 3 September 2016, available at: https://www.economist.com/news/asia/21706185-their-tyrant-nears-his-end-people-uzbekistan-hold-their-breath-ailing-despot?zid=306&ah=1b164dbd43b0cb27ba0d4c3b12a5e227, accessed 19 January 2018.

2 ‘In the Main News; The Chief Mourner in Moscow’, New York Times, 11 February 1984, available at: http://www.nytimes.com/1984/02/11/world/man-in-the-news-the-chief-mourner-in-moscow.html, accessed 15 January 2018.

3 ‘Mirziyoyev Named Acting Uzbekistan President’, Financial Times, 8 September 2016, available at: https://www.ft.com/content/63b12286-8561-3820-8f25-22d2306ed7d8, accessed 15 January 2018.

4 ‘Cloning Karimov: Uzbekistan Replaces One Strongman with Another’, The Economist, 10 December 2016, available at: https://www.economist.com/news/asia/21711263-shavkat-mirziyoyev-wins-886-vote-sham-election-uzbekistan-replaces-one-strongman?zid=306&ah=1b164dbd43b0cb27ba0d4c3b12a5e227, accessed 19 January 2018.

5 ‘The Economist’s Country of the Year: Which Country Improved the Most in 2019?’, The Economist, 21 December 2019, available at: https://www.economist.com/leaders/2019/12/21/which-nation-improved-the-most-in-2019, accessed 22 March 2021.

6 Political opponents of the regime were often sentenced to long jail terms and treated harshly in prison. From 1999, most political prisoners and human rights activists were sent to a notorious prison, Jaslyk, in the north-west of the country. Jaslyk was known informally as ‘borsa, kelmas’, meaning, ‘those who go, won’t return’, and became the symbol of the repressive regime. The prison was shut down by Mirziyoyev in September 2019 (Putz Citation2019).

7 For comparison, Ukraine borrowed a combined total of more than US$22 billion from the Fund in the 1991–2019 period. See ‘Ukraine: Transactions with the Fund’, IMF, available at: https://www.imf.org/external/np/fin/tad/extrans1.aspx?memberKey1=993&endDate=2099%2D12%2D31&finposition_flag=YES, accessed 10 July 2019.

8 According to Karimov’s official biography (‘Biography’, The Islam Karimov Academic and Educational Complex, available at: http://www.islomkarimov.uz/en/page/tarjimai-hol, accessed 22 March 2021), the title of his Kandidat Nauk (PhD) thesis was ‘The Structure of the Uzbek Soviet Socialist Republic’s Industrial Base and the Main Directions for Its Improvement’.

9 See also Spechler (Citation2000).

10 The claim, of course, is valid only under the assumption of unconditional convergence (Barro Citation2015).

11 See also Mazzucato (Citation2011).

12 See the website of the Shurtan Gas–Chemical Complex, available at: https://sgcc.uz/en/site/index, accessed 22 March 2021.

13 Uzbekistan’s gas and chemical industry is managed by state-owned holding companies Uzneftegas (Uzbekistan Gas and Oil) and Uzkimyosanoat (Uzbekistan Chemical Industry).

14 ‘About the Company’, UzAuto Motors, available at: http://uzautomotors.com/companies, accessed 20 August 2019.

15 ‘About the Company UZTBM’, Uz Truck and Bus Motors, available at: http://man.uz/ru/company/about/, accessed 23 March 2021.

16 ‘Development of the Automotive Industry Was Discussed’, The Office of the President of Uzbekistan, 13 January 2021, available at: https://president.uz/oz/lists/view/4077, accessed 23 March 2021.

17 ‘Volkswagen Caddy Light Commercial and Leisure Activity Cars in Uzbekistan’, Uzavtosanoat, available at: http://uzavtosanoat.uz/en/VOLKSWAGEN-CADDY-LIGHT-COMMERCIAL-AND-LEISURE-ACTIVITY-CARS-IN-UZBEKISTAN.html, accessed 23 March 2021.

18 ‘Hyundai Electric Cars will be made in Uzbekistan’, Embassy of Uzbekistan in New Delhi, 16 May 2019, available at: http://www.uzbekembassy.in/hyundai-electric-cars-will-be-made-in-uzbekistan/, accessed 1 January 2020.

19 For an in-depth discussion of infant industry protection measures by successful industrialised nations when they were catching up, see, among others, Chang (Citation2003, Citation2006).

20 The sharp rise of the external debt-to-GDP ratio from 23.7% in 2006 to 41.3% in 2017 is explained mainly by a large overnight drop in the value of the national currency in 2017, which changed from 4,210 so’ms per US$ on 4 September 2017 to 8,100 per US$ on 5 September 2017 (ADB Citation2019).

21 ‘Uzbekistan Sum Jumps on Black Market on FX Reform Expectations’, Reuters, 14 August 2017, available at: https://www.reuters.com/article/uzbekistan-forex/uzbekistan-sum-jumps-on-black-market-on-fx-reform-expectations-idUSL8N1L00DP, accessed 26 August 2019.

22 ‘Uzbekistan Emerges from Isolation with $1 Billion Bond Sale’, Bloomberg, 13 February 2019, available at: https://www.bloomberg.com/news/articles/2019-02-13/uzbekistan-emerges-from-isolation-with-1-billion-eurobond-sale, accessed 29 August 2019.

23 Countries included in the ECA region are Armenia, Azerbaijan, Belarus, Bosnia & Hercegovina, Bulgaria, Georgia, Kazakhstan, Kosovo, the Kyrgyz Republic, Moldova, Montenegro, North Macedonia, Romania, the Russian Federation, Serbia, Tajikistan, Turkey, Turkmenistan, Ukraine and Uzbekistan.

24 Defined as the sum of currency outside banks, demand deposits other than those of the central government, the time, savings and foreign currency deposits of residents; bank and traveller’s cheques, and others instruments such as certificates of deposit and commercial paper.

25 See, Rule of Law Index 2019 (Washington, DC, World Justice Project), available at: https://worldjusticeproject.org/sites/default/files/documents/WJPROLI2019_0.pdf, accessed 3 September 2019. The estimates of the Rule of Law Index are derived from primary data measuring countries’ adherence to the rule of law from the perspective of ordinary people and their experiences.

26 ‘Shavkat Mirziyoyev: People are Testing us, Testing us Seriously’, Kun.uz, 19 May 2018, available at: https://kun.uz/news/2018/05/19/savkat-mirzieev-kacon-bular-eski-tos-eski-ammom-bulisiga-utadi-degan-halkimizda-ali-kurkuv-bor, accessed 3 September 2019. Translation from Uzbek by the author.

27 ‘Uzbekistan Bond Sale Will Aid Foreign Direct Investment, Says Finance Minister’, Bloomberg, 14 February 2019, available at: https://www.bloomberg.com/news/videos/2019-02-14/uzbekistan-bond-sale-will-aid-foreign-direct-investment-says-finance-minister-video, accessed 23 March 2021.

References

- Acemoglu, D., Johnson, S. & Robinson, J. (2005) ‘Institutions as a Fundamental Cause of Long-run Growth’, in Aghion, P. & Durlauf, S. (eds) Handbook of Economic Growth (New York, NY, Elsevier).

- Acemoglu, D., Johnson, S., Robinson, J. A. & Yared, P. (2008) ‘Income and Democracy’, American Economic Review, 98, 4.

- ADB (2007) Key Indicators for Asia and Pacific. Country Tables: Uzbekistan (Manila, Asian Development Bank), available at: https://www.adb.org/publications/key-indicators-asia-and-pacific-2007, accessed 21 August 2019.

- ADB (2018) Key Indicators for Asia and Pacific. Country Tables: Uzbekistan (Manila, Asian Development Bank), available at: https://www.adb.org/publications/key-indicators-asia-and-pacific-2018, accessed 22 March 2022.

- ADB (2019) ‘Key Indicators Database: Country View’, Asian Development Bank, available at: https://kidb.adb.org/kidb/sdbsCountryView, accessed 22 March 2021.

- Akimov, A. (2015) ‘The Political Economy of Financial Reforms in Authoritarian Transition Economies: A Comparative Study of Kazakhstan and Uzbekistan’, in Ruziev, K. & Perdikis, N. (eds) Development and Financial Reform in Emerging Economies (London, Pickering & Chatto).

- Alesina, A. & Perotti, R. (1994) ‘The Political Economy of Growth: A Critical Survey of the Recent Literature’, The World Bank Economic Review, 8, 3.

- Appelbaum, R. & Gereffi, G. (1994) ‘Power and Profits in the Apparel Commodity Chain’, in Bonacich, E., Cheng, L., Chinchill, N., Hamilton, N. & Ong, P. (eds) Global Production: The Apparel Industry in the Pacific Rim (Philadelphia, PA, Temple University Press).

- Baldwin, R. (2013) ‘Global Supply Chains: Why They Emerged, Why They Matter, and Where They are Going’, in Elms, D. & Low, P. (eds) Global Value Chains in a Changing World (Geneva, WTO Publications).

- Barro, R. (2015) ‘Convergence and Modernisation’, The Economic Journal, 125, 585.

- Chang, H. J. (2002) ‘Breaking the Mould: An Institutionalist Political Economy Alternative to the Neo-Liberal Theory of the Market and the State’, Cambridge Journal of Economics, 26, 5.

- Chang, H. J. (2003) ‘Kicking Away the Ladder: Infant Industry Promotion in Historical Perspective’, Oxford Development Studies, 31, 1.

- Chang, H. J. (2006) ‘Industrial Policy in East Asia: Lessons for Europe’, European Investment Bank Papers, 11.

- Chenery, H. B. & Strout, A. M. (1966) ‘Foreign Assistance and Economic Development’, American Economic Review, 56, 4.

- Cherif, R. & Hasanov, F. (2019) The Return of the Policy That Shall Not Be Named: Principles of Industrial Policy, IMF Working Paper No WP/19/74 (Washington, DC, IMF).

- EBRD (2004) Transition Report (London, European Bank for Reconstruction and Development).

- Eraliev, S. & Urinboev, R. (2020) ‘Precarious Times for Central Asian Migrants in Russia’, Current History, 119, 819.

- Friedman, M. (1982) Capitalism and Freedom (Chicago, IL, University of Chicago Press).

- Galeotti, M. (2018) The Vory: Russia’s Super Mafia (London, Yale University Press).

- Government of Uzbekistan (2017) ‘O‘zbekiston Respublikasi Prezidentining Farmoni No 4947 “O‘zbekiston Respublikasini Yanada Rivojlantirish Bo‘yicha Harakatlar Strategiyasi To‘g‘risida”’, 7 February, available at: https://lex.uz/docs/-3107036, accessed 23 March 2021.

- Government of Uzbekistan (2019a) ‘O‘zbekiston Respublikasi Prezidentining Farmoni No 5614 “Iqtisodiyotni Yanada Rivojlantirish va Iqtisodiy Siyosat Samaradorligini Oshirishning Qo‘shimcha Chora-Tadbirlari To‘g‘risida”’, 8 January, available at: https://lex.uz/docs/4147294, accessed 23 March 2021.

- Government of Uzbekistan (2019b) ‘O‘zbekiston Respublikasi Prezidentining Farmoni No 5781 “O‘zbekiston Respublikasida Turizm Sohasini Yanada Rivojlantirish Chora-Tadbirlari To‘g‘risida”’, 13 August 2019, available at: https://lex.uz/docs/4474527, accessed 23 March 2021.

- Government of Uzbekistan (2019c) ‘O‘zbekiston Respublikasi Prezidentining Farmoni No 4453 “Yengil Sanoatni Yanada Rivojlantirish va Tayyor Mahsulotlar Ishlab Chiqarishni Rag‘batlantirish Chora-Tadbirlari To‘g‘risida”’, 16 September 2019, available at: https://lex.uz/docs/4516526, accessed 23 March 2021.

- Government of Uzbekistan (2020) ‘O‘Zbekiston Respublikasi Vazirlar Mahkamasining Qarori No 433 “O‘Zbekiston Respublikasida Turizm Sohasini Tiklash va Rivojlantirish Uchun Qulay Shart-Sharoitlarni Yaratish Chora-Tadbirlari To‘g‘risida”’, 10 July 2020, available at: https://lex.uz/docs/4930291, accessed 23 March 2021.

- Hall, R. & Jones, C. I. (1999) ‘Why do Some Countries Produce So Much More Output Per Worker Than Others?’, The Quarterly Journal of Economics, 114, 1.

- Hausmann, R., Pritchett, L. & Rodrik, D. (2005) ‘Growth Accelerations’, Journal of Economic Growth, 10, 4.

- Hausmann, R. & Rodrik, D. (2003) ‘Economic Development as Self-Discovery’, Journal of Development Economics, 72, 2.

- Hayek, F. A. (2005) The Road to Serfdom (London, Institute of Economic Affairs).

- Holzhacker, H. (2018) Uzbekistan Diagnostic: Assessing Progress and Challenges in Unlocking the Private Sector’s Potential and Developing a Sustainable Market Economy (London, EBRD).

- Huisman, J., Smolentseva, A. & Froumin, I. (eds) (2018) 25 Years of Transformations of Higher Education Systems in Post-Soviet Countries: Reform and Continuity (London, Palgrave Macmillan).

- Ilkhamov, A. (2013) ‘Labour Migration and the Ritual Economy of the Uzbek Extended Family’, Zeitschrift für Ethnologie, 138, 3.

- IMF (1991) A Study of the Soviet Economy (Paris, International Monetary Fund).

- IMF (2008) Republic of Uzbekistan: Poverty Reduction Strategy Paper, IMF Country Report No.08/34 (Washington, DC, International Monetary Fund).

- IMF (2013) Uzbekistan: 2012 Article IV Consultation, Country Report No. 13/278 (Washington, DC, International Monetary Fund).

- IMF (2018a) Uzbekistan: Informational Annex, IMF Staff Report for the 2018 Article IV Consultation, 19 April 2018 (Washington, DC, International Monetary Fund).

- IMF (2018b) Uzbekistan: Debt Sustainability Analysis, IMF Staff Report for the 2018 Article IV Consultation, 19 April 2018 (Washington, DC, International Monetary Fund).

- IMF (2018c) Uzbekistan: 2018 Article IV Consultation, Country Report No. 18/117 (Washington, DC, International Monetary Fund).

- IMF (2019a) IMF DataMapper: GDP Per Capita, Current Prices, International Monetary Fund, available at: https://www.imf.org/external/datamapper/PPPPC@WEO/THA, accessed 27 August 2019.

- IMF (2019b) Uzbekistan: 2019 Article IV Consultation, Country Report No. 19/129 (Washington, DC, International Monetary Fund).

- IMF (2019c) IMF DataMapper: Fiscal Monitor, International Monetary Fund, available at: https://www.imf.org/external/datamapper/datasets/FM, accessed 27 August 2019.

- Jeanne, O. & Rancière, R. (2011) ‘The Optimal Level of International Reserves for Emerging Market Countries: A New Formula and Some Applications’, The Economic Journal, 121, 555.

- Karimov, I. (1995) Uzbekistan on the Way of Deepening Economic Reforms (Tashkent, Sharq).

- Karimov, I. (1998) Uzbekistan on the Threshold of the Twenty First Century (New York, NY, Saint Martin).

- Lin, J. (2012) New Structural Economics: A Framework for Rethinking Development and Policy (Washington, DC, World Bank).

- Lin, J. & Chang, H. J. (2009) ‘Should Industrial Policy in Developing Countries Conform to Comparative Advantages or Defy it?’, Development Policy Review, 27, 5.

- Lucas, R. (1993) ‘Making a Miracle’, Econometrica, 61, 2.

- Mazzucato, M. (2011) The Entrepreneurial State (London, Demos).

- McKinnon, R. I. (1973) Money and Capital in Economic Development (Washington, DC, Brookings Institution).

- North, D. C. (1994) ‘Economic Performance Through Time’, American Economic Review, 84, 3.

- Olssen, M. & Peters, M. (2005) ‘Neoliberalism, Higher Education, and the Knowledge Economy: From the Free Market to Knowledge Capitalism’, Journal of Education Policy, 20, 3.

- Pajank, D. (2019) ‘Uzbekistan’s Star Appears in the Credit Rating Universe’, Future Development, available at: https://www.brookings.edu/blog/future-development/2019/01/23/uzbekistans-star-appears-in-the-credit-rating-universe/, accessed 4 September 2019.

- Pegkas, P. & Tsamadias, C. (2014) ‘Does Higher Education Affect Economic Growth? The Case of Greece’, International Economic Journal, 28, 3.

- Pomfret, R. (2000) ‘The Uzbek Model of Economic Development, 1991–1999’, The Economics of Transition, 8, 3.

- Pomfret, R. (2003) Central Asia Since 1991: Experience of the New Independent States, OECD Development Centre Technical Paper No 2012 (Paris, Organisation for Economic Co-operation and Development).

- Pomfret, R. (2019) The Central Asian Economies in the Twenty-First Century: Paving a New Silk Road (Princeton, NJ, Princeton University Press).

- Popov, V. (2013) Economic Miracle of Post-Soviet Space: Why Uzbekistan Managed to Achieve what no Other Post-Soviet State Achieved, MPRA Paper No. 48723, available at: https://mpra.ub.uni-muenchen.de/48723/, accessed 26 April 2020.

- Popov, V. & Chowdhury, A. (2016) What can Uzbekistan tell us About Industrial Policy that we did not Already Know?, UN Department of Economic and Social Affairs Working Paper No.147 (New York, NY, UN).

- Putz, C. (2019) ‘Uzbekistan to Close Notorious Prison Colony, the “House of Torture”’, The Diplomat, 5 August, available at: https://thediplomat.com/2019/08/uzbekistan-to-close-notorious-prison-colony-the-house-of-torture/, accessed 22 March 2021.

- Ruziev, K. & Burkhanov, U. (2018) ‘Higher Education in Uzbekistan: Reforms and the Changing Landscape Since Independence’, in Huisman, J., Smolentseva, A. & Froumin, I. (eds).

- Ruziev, K. & Ghosh, D. (2009) ‘Banking Sector Development in Uzbekistan: A Case of Mixed Blessings?’, Problems of Economic Transition, 52, 2.

- Ruziev, K., Ghosh, D. & Dow, S. C. (2007) ‘The Uzbek Puzzle Revisited: An Analysis of Economic Performance in Uzbekistan Since 1991’, Central Asian Survey, 26, 1.

- Ruziev, K. & Majidov, T. (2013) ‘Differing Effects of the Global Financial Crisis on the Central Asian Countries: Kazakhstan, the Kyrgyz Republic and Uzbekistan’, Europe-Asia Studies, 65, 4.

- Ruziev, K. & Midmore, P. (2015) ‘Connectedness and SME Financing in Post-Communist Economies: Evidence from Uzbekistan’, The Journal of Development Studies, 51, 5.

- Sen, A. (1999) Development as Freedom (Oxford, Oxford University Press).

- Shaw, E. S. (1973) Financial Deepening in Economic Development (New York, NY, Oxford University Press).

- Spechler, M. (2000) ‘Hunting for the Central Asian Tiger’, Comparative Economic Studies, 42, 3.

- Stronski, P. (2020) ‘Will Mirziyoyev’s Plodding Reforms be Enough for Uzbekistan?’, World Politics Review, 15 January, available at: https://www.worldpoliticsreview.com/articles/28471/will-mirziyoyev-s-plodding-reforms-be-enough-for-uzbekistan, accessed 22 March 2021.

- Temple, J. (1999) ‘The New Growth Evidence’, Journal of Economic Literature, 37, 1.

- Trushin, E. (2018) Growth and Job Creation in Uzbekistan: An In-Depth Diagnostic (Washington, DC, World Bank).