?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Existing studies of the political determinants of top incomes and inequality tend to focus on developments within individual countries, neglecting the role of interdependencies that transcend national borders. This article argues that the sharp rises in top incomes observed in recent years are in part a product of specific features originating in the US political economy, which were subsequently exported to other economies through the global expansion of US-based financial investors. To test the argument, we collect fine-grained micro-level data on executive pay and firm ownership structures for a comprehensive sample of publicly listed firms in the United Kingdom (UK). Our analyses uncover robust evidence that the Americanization of UK firm ownership leads to the financialization of remuneration practices and sizeable pay increases for high-level managers at those firms. Scrutinizing the causal mechanisms underlying this effect, we find them to be more consistent with changes in bargaining power inside firms rather than coercion from outside or exogenous shifts in labor markets for executives. The findings show the disruptive potential of Wall Street investments abroad to empower local managerial elites to capture greater rents and, more generally, demonstrate the need to take the transnational seriously in order to understand patterns of inequality in the global political economy.

Introduction

Income inequality, and the trend toward increasing concentration of income and wealth at the top of the distribution, has generated wide scholarly and public debate. Economists have documented the growing share taken by the wealthiest households in the United States (USA), with the top 1% currently capturing as high a share of income as in the 1920s (Atkinson et al., Citation2010) whilst the popularization of the concept of the ‘one per cent’ has moved the debate into the public sphere. Research on this sharp rise in top incomes has invoked factors, such as the rising capital share (Piketty, Citation2014), the growing political power of the wealthy (Hacker & Pierson, Citation2010), technological change (Autor et al., Citation2006), the decline of trade unions and tax rates (Angeles & Kemmerling, Citation2020; Huber et al., Citation2019), and financialization (Godechot, Citation2012; Huber et al., Citation2020).

Top income growth is usually analyzed as primarily a national-level phenomenon. Yet, transnational networks and interconnections are a core feature of the global capitalist system in the early twenty-first century (Farrell & Newman, Citation2014; Lockwood, Citation2021; Oatley, Citation2019; Schwartz, Citation2019). In contrast to earlier historical periods of high inequality characterized by land- and capital-owning elites (Piketty, Citation2014), increases in inequality in twenty-first-century economies are also driven by differences in labor incomes, and the ‘explosion of supermanager salaries’ (Ibid., 334) in particular. This article shifts the focus away from the national state and instead treats (multinational) firms as key sites of redistributive struggles (Amis et al., Citation2020; Avent-Holt & Tomaskovic-Devey, Citation2014; Willman & Pepper, Citation2020). It proposes to contribute to our understanding of the politics of inequality by looking at the political-economic dynamics that drive the upwards redistribution of corporate profits inside multinational firms, with an emphasis on the transnational environment within which they operate.

Empirically, we depart from aggregate data on national-level top income shares and instead analyze individual manager-level remuneration using fine-grained micro-level data on executive pay. For reasons of data quality we focus on companies that are publicly listed in the jurisdiction with the most stringent transparency requirements on executive pay outside the USA, the United Kingdom (UK). The data we use covers several thousand high-level managers of UK-incorporated firms from 2007 to 2014. This enables us to study in detail the micro-dynamics driving variations in rewards for the highly paid executives that populate the top percentile of the income distribution.

In contrast to the emphasis on national-level institutional features in the previous literature, we are particularly interested in examining one channel of an explicitly transnational nature: the Americanization of ownership of non-US firms. Whilst trends toward a growing concentration of incomes have been a widespread phenomenon, nowhere has the growth in top incomes been more dramatic than in the USA (Bebchuk & Fried, Citation2004; Fernandes et al., Citation2013; Hargreaves, Citation2019; ‘WID’, Citation2018). Our empirical analyses assess the extent to which the global spread of US-based investors has contributed to the diffusion of American-style remuneration practices – and by implication greater income inequality – in the British economy. Our findings provide strong and robust evidence that this has indeed been the case: as US ownership in UK-incorporated firms grows, pay for top executives at those firms rises significantly.

The fine-grained nature of our data allows us to also gauge the relative importance of the different mechanisms that plausibly lie behind this outcome: market-related factors, such as premiums for specific skills in labor markets for executives brought about by the internationalization of firms; and more political explanations revolving around the imposition of incentives-based remuneration practices from outside or changes in bargaining power inside firms. We also conduct a comprehensive review of media coverage on executive pay in two British newspapers (Financial Times and The Guardian) and draw on interviews with investors, proxy advisors, campaigners and trade union representatives. Overall, our results suggest that the politics of the firm are more important than market-related factors. The entry of US investors enables top executives at UK-based firms to capture ever larger shares of corporate profits, even in the absence of improvements in performance.

Our focus on one country naturally limits the external validity of our findings. Trade unions and other corporatist arrangements are weak in the UK, and they may still act as barriers to upward pressure on executive pay in other environments. Nevertheless, our finding that US ownership has had a strong impact even in a country where the business culture is already rather ‘Americanized’ suggests that its disruptive potential could be even greater elsewhere. In any case, the size and robustness of the effects that we find in the UK case are large enough to justify further research on both the impact of US owners and the ability of institutions of corporate governance to resist these pressures.

The article proceeds as follows. The next section reviews the relevant literature on inequality and top income shares, elaborates our argument and examines possible channels for diffusion. The subsequent section presents the empirical strategy and data, followed by the analyses and results. The last section concludes.

The politics of inequality in a global economy: literature and conceptual framework

From nation-states to firms

Political science research on income inequality has traditionally focused on the gap between the lower and middle-income groups, emphasizing the role of electoral institutions (Iversen & Soskice, Citation2006), partisan control of government (Iversen & Soskice, Citation2009), welfare state arrangements (Esping-Andersen, Citation1990) and the strength and coordination of labor representation (Hall & Soskice, Citation2001). But the availability of much improved data on inequalities at the top of the distribution (Piketty, Citation2014) has opened up a new avenue of research on ‘winner-take-all politics’, looking at how wealthy and corporate interests use their financial clout to skew policy in their favor in individual countries (Gilens, Citation2012; Hacker & Pierson, Citation2010; Hopkin & Lynch Citation2016), and the role of institutional arrangements in explaining cross-national variations in top income shares (Hager, Citation2018; Huber et al., Citation2020; Scheve & Stasavage, Citation2009). Ontologically, this body of research shares a focus on nation-states as analytical units. But a focus on nation-states alone risks overlooking transnational drivers of outcomes of interest (cf. Farrell & Newman, Citation2014; Oatley, Citation2019).

There are good reasons to think that the transnational is relevant for the study of top income inequality. As in-depth studies of US (Bakija et al., Citation2012) and UK (Advani et al., Citation2020; Brewer et al., Citation2009) tax records show, the ‘top one per cent’ are predominantly salaried managers and finance professionals–social groups who live in deeply transnational environments (especially in the ‘Anglosphere’). In this sense, the study of income inequality at the top through the use of cross-national comparisons faces some inherent limitations (cf. Lockwood, Citation2021).

We therefore propose shifting the primary unit of analysis from the national level at the aggregate to the level of firms. Patterns of compensation within the firm (Avent-Holt & Tomaskovic-Devey, Citation2014; Song et al., Citation2019) play a key role in determining patterns of inequality. We conceptualize (multinational) corporations as sites of redistributive struggles that shape broader trends of inequality in the global economy. The transnational dynamic that we are particularly interested in is whether the Americanization of corporate ownership leads to higher levels of executive pay in non-US firms.

US capitalism, shareholder value ideology and the revolution in executive pay

The starting point of our analysis is the uncontroversial fact that the USA has been at the forefront of the rise in top incomes amongst the advanced economies. As Frydman and Saks (Citation2010) have shown, levels of executive pay in the USA increased gradually from the mid-1940s to the 1970s, but then exploded in the 1980s. The ratio of the average salary of the CEO of a large listed American company compared to the average worker reportedly grew from 42:1 (in 1980) to 347:1 (in 2016) (Hargreaves, Citation2019, p. 7).

The underlying processes behind this remarkable upwards redistribution of corporate profits toward top executives are closely connected to the financialization of the American economy. Theories of corporate governance prioritizing shareholder value, depicting firms as merely bundles of tradable assets (Tomaskovic-Devey & Lin, Citation2011), legitimized the prioritization of capital markets’ interests over those of employees and other stakeholders. The imposition of Wall Street’s preferred metrics as the new rules of the game (Lin and Megan Tobias, Citation2020, p. 84) encouraged corporate boardrooms to focus on short-term financial performance instead of more traditional strategies aimed at increasing market shares in the long term. This meant that corporate decision-making tended to sideline labor’s concerns (Froud et al., Citation2006). Financial managers sought to rein in expenses on firms’ employees through mergers and mass layoffs, instead re-channeling profits to investors through ‘overhead costs’, such as dividend payments and share buy-backs (Dünhaupt, Citation2017; Fligstein & Shin, Citation2007).

The original aim of proponents of shareholder value theories was to weaken managers (the agents), seen as too comfortable and free to prioritize their own interests over those of corporate owners (the principals). Paradoxically, however, the rise to dominance of these shareholder-value-oriented corporate governance practices ended up strengthening the position of executives vis-à-vis other stakeholders even further, as the growing numbers of managers being employed by large corporations as well as their ever higher pay attest (Bebchuk & Fried, Citation2004; Goldstein, Citation2012).

The key mechanism through which these new modes of corporate governance boosted executive pay is the emphasis on equity-based pay-for-performance (P4P). By turning managers into shareholders, remunerating managers in stock options rather than cash (and making pay-outs conditional on achievement of specific financial targets) was seen as an effective way to ensure managers acted in shareholders’ best interests by focusing on increasing firms’ market value.Footnote1 This increased executives’ total remuneration for two reasons (Conyon et al., Citation2011; Fernandes et al., Citation2013; Thomas, Citation2004). First, higher pay could now be justified as rewards for improvements in corporate performance delivering higher financial returns to shareholders. Second, equity-based remuneration is less transparent and easier to conceal than conventional salaries, assuaging fears of backlash on the part of shareholders or the public about perceived excesses in executive pay.

The effectiveness of incentive-based pay in actually improving corporate performance is dubious. Research shows that levels of pay have risen much more rapidly than share prices in the medium-term (Bivens & Mishel, Citation2013). One study indicates that firms that pay executives more actually tend to perform worse in medium- to long-term share price developments (Marshall & Lee, Citation2016). Others show how executives get systematically rewarded handsomely for exogenous ‘lucky’ events – e.g. stock market booms induced by monetary stimulus bills – whereas punishments for underperformance are rarely implemented in practice (Bebchuk & Fried, Citation2004).

Trends in executive pay in the USA and UK

Processes of financialization and the upwards redistribution of rewards that they entail are a global phenomenon, not limited to the USA (Dünhaupt, Citation2017; Flaherty, Citation2015). Yet, Wall Street actors have played a central role in propagating its emergence and success, and the US economy remains the system in which it is most deeply ingrained. Levels of executive pay in the USA outstrip those paid anywhere else by a significant margin: one of the first studies comparing executive pay data internationally found that American CEOs were paid nearly 200% more than those in the UK, and the gaps with other advanced economies were even greater (Conyon & Murphy, Citation2000). Even controlling for better economic performance and a more widespread dilution of corporate ownership, a sizable ‘US premium’ remains (Cheffins & Thomas, Citation2004; Conyon et al., Citation2011; Fernandes et al., Citation2013).

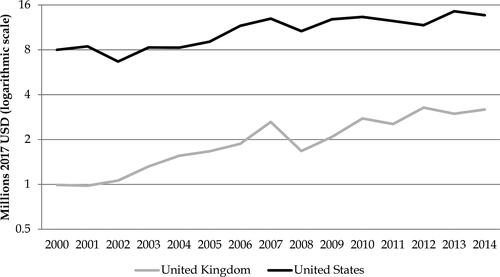

illustrates these trends using our own data on executive remuneration, comparing the USA and UK.Footnote2 The graph plots the annual remuneration of the median executive of the median company in both countries on a semi-logged scale. To improve comparabilityFootnote3 we restrict the sample to very large companies with at least 10,000 employees. Both the pay gap and the increase in total pay over the time period are remarkable: the median US executive’s pay package in the year 2000 was worth more than $8 million in inflation-adjusted 2017 USD and – despite two major financial crises in 2001 and 2007 – grew to $15 million by 2014. In the UK, median pay at similarly large companies was significantly lower at less than $1 million at the beginning of the period, but tripled to more than $3 million in 2014, only partly closing a significant pay gap between UK executives and their US peers.

Figure 1. The evolution of executive pay in the United States and United Kingdom, 2000–2014. Source: Own calculations based on BoardEx data. Note: Lines show the value of the annual salary of the median executive in the median firm in the country-sample. All values are in constant 2017 USD. Further details on the underlying data are provided in Tables A1 and A2 in the Appendix.

There is strong evidence that executive salaries are exceptionally high in the USA and their growth was driven by the shareholder primacy maxim and an associated ‘cult of personal leadership’Footnote4, as well as increasing reliance on P4P and equity-based pay. These developments began in the USA, but their effects reverberated far beyond its national borders, as these remuneration practices spread to other countries, affecting their income distributions. The next section assesses some hypotheses about the possible nature of this diffusion.

US asset managers in the global economy

Wall Street remains the core of the global financial system (Hager, Citation2017; Oatley & Petrova, Citation2020; Schwartz, Citation2019), and US-based investors own significant shares of corporations around the world (Fichtner, Citation2017; Fichtner et al., Citation2017; Starrs, Citation2013). While US investors directly control some publicly listed foreign companies in which they own more than 50% of corporate shares, the more common picture (illustrated in Appendix Table A5) is the one of US institutional investors owning substantial minority positions ranging between 1 and 20% of large listed foreign-incorporated outstanding stock. This does not grant them managerial control over those companies, but it does make them influential stakeholders (cf. Ahmadjian & Robbins, Citation2005; Deeg et al., Citation2016; Desender et al., Citation2016).

Virtually all global investors aim to invest in well-performing stocks. Yet investors’ self-understanding of their fiduciary duties, including about executive pay, are colored by notable cultural differencesFootnote5. For one, Wall Street-based investors tend to consider more generous remuneration packages as ‘normal’ or even desirable. As one interviewee put it, they ‘sometimes struggle to understand what the concerns about high pay [more common in the UK and Europe] are and where they’re coming from’Footnote6. Along similar lines, as a compensation consultant explained in an interview with the Financial Times (Marriage, Citation2015),

[asset managers in] the US are much more comfortable for pay to reflect how quickly [company] performance went up or down, and their metrics might not be as elaborate… [In Europe] there is a lot of scrutiny … from the public and from the industry. [European] remuneration committees are being very careful … it is not as easy to get full payment.

Similar differences can be observed in more systematic assessments of shareholders’ orientation. A recent ranking of the stance of 75 of the world’s largest asset managers toward responsible investment, for instance, reveals a marked difference between American and European institutional investors, with the former being notably less committed to responsibilities toward stakeholders other than short-term financial performance (Nagrawala & Springer, Citation2020, p. 4).

Potential mechanisms of diffusion

Decisions on the pay packages that top managers receive are made by firms’ internal remuneration committees, typically constituted by members of the board of directors (Hargreaves, Citation2019, pp. 10–12). These committees usually seek the advice of external compensation consultants and agree on a recommended pay package in cooperation with the firm’s HR Department (Conyon et al., Citation2009, p. 49). Depending on national corporate governance laws, the recommendation then has to be formally approved at the annual shareholder meeting through an advisory or binding vote.

This setup opens up a variety of potential mechanisms through which larger US-based ownership stakes can translate into upwards pressure on executive pay at non-US firms. We focus on three distinct types: one market mechanism centered on firm internationalization’s potential impact on labor markets for CEOs; and two political mechanisms centered on how growing foreign ownership may lead to either coercive imposition from outside, or the triggering of shifts in bargaining power inside of firms. As theories of (new) interdependence and policy diffusion suggest (Farrell & Newman, Citation2014; Citation2016), they all involve interactions of structural change and instrumental agency, but to different extents. Some derive primarily from the exogenous transformation of market structures. Others are the result of direct coercion exercised by US investors as agents (push from outside). And some, centered on local agents taking advantage of structural change (pull from inside), fall somewhere in between. The following paragraphs introduce the hypothesized main mechanisms and observable implications that we can test with our data at hand. provides a structured overview.

Table 1. Overview of hypothesized causal mechanisms.

Internationalization of labor markets for executives

The first set of mechanisms relates to the logic of demand and supply in labor markets for top executives – the internationalization of corporate ownership structures may put a premium on top managers’ ability to communicate effectively with investors from different cultural backgrounds. Following a similar logic to that of skill-biased technological change (Autor et al., Citation2006), the extra skills that this demands (e.g. cross-cultural communication skills, an MBA degree from an internationally prestigious business school, etc.) may mean that the pool of potential candidates in a local job market shrinks as foreign investors become more prominent as shareholders, allowing qualified candidates to ask for higher remuneration (Oxelheim & Randoy, Citation2005). Growing influence from US investors specifically may equally increase the likelihood of appointing managers from the USA who are likely to ask for US-levels of pay.

Coercive imposition of the shareholder value model

An alternative set of potential mechanisms relates to US investors’ strong preference for P4P remuneration techniques. Since the profitability of their investments hinges on the stock market performance of target firms, advocates of P4P argue, shareholders should generously reward executives for improvements in performance, but sharply punish them for underperformance (Jensen & Murphy, Citation1990). Survey evidence suggests that these views are particularly widespread among US institutional investors, with a majority of over two-thirds indicating the rigor of performance targets to be the single most important criterion when evaluating levels of pay (Morrow Citation2017, p. 20). To the extent that US investors insist more strongly on P4P than other shareholders, growing US investments may also lead to higher, equity-based pay, conditional on corporate performance.

Shifting bargaining power inside firms

The third set of mechanisms relates to executives’ bargaining power within firms. As proponents of managerial power theory have pointed out, there are various ways for executives themselves to influence their own pay. Managers can take advantage of weak monitoring by labor unions and independent directors on remuneration committees (Bebchuk & Fried, Citation2004), or influence the selection of peer groups in the latter’s benchmarking exercises (DiPrete et al., Citation2010; Godechot, Citation2017). Growing foreign ownership potentially facilitates both these strategies. Domestic shareholders may be better able to monitor the actions of executives than US and other foreign ones, meaning that levels of pay may be under less scrutiny as firm ownership passes into foreign hands. Foreign investors are less likely to listen to local trade unions’ concerns, and – especially if they are based in the USA – they may be more at ease with higher (US-style) levels of executive remuneration. In either case, agents (i.e. executives) may face fewer internal obstacles to appropriating greater shares of corporate profits for themselves when ownership stakes pass to foreign investors. Simultaneously, the internationalization of corporate ownership may also be an opportunity for executives to push for a modification of remuneration committees’ benchmarking exercises, arguing that their salaries should be benchmarked to the earnings of international, rather than domestic or firm-internal, peers. In view of the sizable US pay premium, this should lead to particularly large effects if executives are able to claim American executives as the appropriate benchmark.

Observable implications

Some of these mechanisms, such as the appointment of US citizens or the effects for various pay components, we can observe directly in our data, whilst others entail observational implications that can only be evaluated indirectly. First, we use the relationship between pay and performance to distinguish the relevance of coercive pressures from political dynamics inside firms. Pay increases driven by improvements in corporate performance point to the former, whilst increases in pay without improvements in performance are indicative of the latter. Second, we draw on a comparison between the effects of US vs. non-US foreign investors and across industrial sectors to evaluate the relevance of skills-related factors in labor markets for executives: if key developments are related to exogenous shifts in the demand and supply of managerial skills, these effects should be similar for US and other foreign investments and across industrial sectors. If, in contrast, the effects are significantly larger for US than other foreign owners or concentrated in industrial sectors in which levels of pay are particularly high in America (e.g. finance, cf. Lord & Saito, Citation2010), benchmarking mechanisms would seem to be more prominent. Finally, to examine the role of workers’ bargaining power, we investigate whether trade union density of the sector in which a firm operates affects executive pay. In the sections that follow, we examine these alternative hypotheses econometrically.

Empirical strategy

To assess the relationship between foreign ownership and executive pay in the UK and the mechanisms underlying them, we collect detailed time-series panel data on the yearly pre-tax remuneration of several thousand high-level executives at publicly listed UK-incorporated firms during the period 2007–2014.

We are not the first to investigate the effects of the Americanization of European companies (see e.g. Almond et al., Citation2006; Sapp, Citation2008; Zeitlin & Herrigel, Citation2000). Empirically, our research departs from these studies in three ways. First, our sample is more comprehensive, covering a consistent time period of 8 years where most other studies cover just one year (see Gerakos et al., Citation2013 for an exception), including salary information of several top executives of the same firm (not only CEOs). Second, US ownership is a more plausibly exogenous variable to study the impact of Americanization than outcomes of decisions of the executives themselves used in previous studies (e.g. sales or a cross-listing in the US market).Footnote7 Finally, the richness of our dataset allows for a more systematic evaluation of the various causal mechanisms theorized in the preceding section.

Data

The regulatory framework for executive pay during our period of observation consists of the UK Corporate Governance Code and the Directors’ Remuneration Report Regulations, both issued in 2002, and broadly unchanged during the period of observation (Bender & Moir, Citation2006; Petrin, Citation2015). The legislation does not impose any cap on levels of pay, but requires publicly listed firms to make detailed information on the remuneration of top executives publicly available. It also subjects remuneration reports to an advisory ‘say-on-pay’ vote at annual shareholder meetings.

Our data on executive pay is from BoardEx, a London-based business intelligence firm that collects data on the remuneration, network and career trajectory of over one million high-level executives around the world.Footnote8 BoardEx does not employ an explicit sampling methodology, the collection of data being driven by availability and ‘client interest’.Footnote9 Information on executive pay at publicly listed firms is collected predominantly from companies’ annual reports. The data is widely used and random cross-checking of selected data points with annual reports found them to be accurate.

To evaluate the coverage and representativeness of our sample, we compare the number of companies with executive remuneration data with the total number of companies listed on the London Stock Exchange in the same year. As illustrated in Appendix Table A3, more than half of all publicly listed UK-incorporated firms are included in the BoardEx dataset and information on executive pay is available for about 40% of the entire population of companies. The mean market capitalization of companies in our dataset is three to four times larger than the average of all LSE-listed firms, suggesting that the data is skewed toward larger firms. The market value of all companies with remuneration data combined exceeds 90% of the value of all UK-incorporated companies listed on the LSE. We are therefore confident that the data offers a representative sample of publicly listed firms in the UK, and especially of those most likely to receive substantial foreign investments.

Data on the key independent variable of corporate ownership is from Bureau van Dijk’s (BvD) Orbis database. BvD is one of the largest providers of corporate data. Independent assessments have found the quality of the data to be good and coverage for the UK is nearly complete for companies employing more than 50 employees (Garcia-Bernardo & Takes, Citation2016, p. 4).

The identification of the owners of publicly listed corporations faces two challenges. First, only relatively large investors whose holdings exceed a certain threshold are legally obliged to declare their ownership stakes. The precise threshold depends on the applicable regulation which varies by type of investor and investee, but generally ranges between 1 and 5% of a company’s outstanding stock.Footnote10 By implication, available ownership data will be biased toward relatively large investors obscuring some positions by small investors. However this is a minor problem, since nearly 90% of shares in the UK stock market are held by institutional investors (Office for National Statistics, Citation2017), and in any case our focus is on investors large enough to influence managerial decision-making. Second, investment flows in globalized capital markets are commonly channeled through several jurisdictions. As a result, ownership relations in the contemporary economy are frequently opaque (Linsi & Mügge, Citation2019). A key strength of the Orbis ownership data in this respect is BvD’s development of a proprietary methodology aimed at estimating shareholders’ total ownership stakes, including both direct and indirect positions, leveraging their database’s archive of over 300 million observed ownership links to track down the beneficial owners of indirect positions as long as all nodes in the ownership chain are included (Bureau van Dijk, Citation2018). Ultimate ownership positions can also be validated by cross-checking records filed with regulatory agencies on both ends of the ownership chain. We therefore believe the ownership data to be reasonably reliable for stakes held by large institutional owners who are subject to strict legally mandated declaration obligations.

To operationalize US and other foreign ownership of publicly listed UK-incorporated firms we calculate the aggregate value of all positions of ultimate owners domiciled in the USA or any other foreign country as identified in the Orbis database. Summary statistics are provided in Appendix Table A4. On average about 50% of the shares of publicly listed UK-incorporated firms are owned by foreign investors,Footnote11 of which approximately a fifth are held by investors domiciled in the USA.

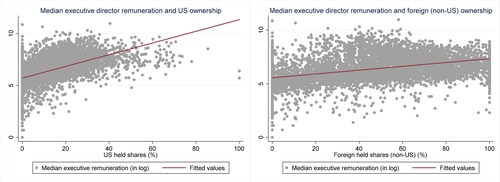

plots the relationship of pay with US-held shares on the left, and with non-US foreign investor-held shares on the right.

Figure 2. Foreign ownership and executive remuneration.

The plots indicate a clear positive and fairly linear relationship between US investor presence and executive pay, which we take into account in our baseline specification modeling assumptions. The association between executive remuneration and non-US ownership is also positive, but clearly weaker. Our regression analyses probe the robustness of these associations.

To look behind these aggregate figures, we used the Orbis data to identify the largest shareholders present in the UK stock market. Appendix Table A5 lists the 10 largest shareholders by country of domicile – distinguishing between US investors, domestic UK investors, and others – for the years 2007–2015. Without exception, they are institutional investors: investment banks (e.g. Goldman Sachs), mutual and exchange-traded funds (e.g. Blackrock), insurers (e.g. Legal and General) and one sovereign wealth fund (Norges Bank). In line with other studies (e.g. Babic et al., Citation2020), we find the importance of US passive funds and sovereign wealth funds grows over the time period under consideration. But on the whole, our categories of US and other foreign investors are both populated with similar types of actors, i.e. large mutual funds.

Econometric strategy

Our econometric strategy unfolds in several steps. First, we run a set of standard panel fixed-effects regressions with firms as units of observations (and the level at which the ‘treatment’ occurs) to evaluate the association between marginal increases in US and non-US foreign ownership and individual pay packages disbursed to executives at UK-incorporated firms. We then exploit the individual-level data to validate these results. Having established the baseline result, we leverage both company- and individual manager-level analyses to explore the relevance of various diffusion mechanisms through which US ownership affects remuneration, corporate performance, and the hiring of US citizens as executives.

Company-level

We first estimate the relationship between foreign ownership and executive pay at the company-level. Using our sample, we estimate the following baseline specification:

(1)

(1)

where j indicates companies, and t years. Yj,t measures the median remuneration of executives (in log) at a given firm in year t.

refers to the percentage of a company’s shares that are foreign-owned, and

is the main parameter we are interested in estimating. Wj,t is a vector of company covariates. In line with previous literature on executive pay, we control for corporations’ operating revenue and profit margins to proxy business profitability; the solvency ratio to proxy for financial sustainability of a company; stock price performance to take into account the change in companies’ valuation on financial markets; BvD’s ownership concentration index to proxy for management independence; and union density at the industrial sector level to evaluate the role of worker bargaining power.

are company-fixed effects, which absorb the influence of any characteristics that are constant within firms over time, such as internal culture or industrial branch. Year-fixed effects

control for macroeconomic shocks affecting all firms simultaneously in a year, and sector-specific linear time trends

capture heterogeneous trends in managerial pay across industrial sectors. νj,t is the error term. Standard errors are clustered at the company level. Descriptive statistics can be found in Appendix Table A6.

The identification assumption to interpret our results causally is the absence of any firm-specific shocks that correlate with both pay packages and ownership structures. Company fixed effects and year effects remove the influence of firm-idiosyncratic factors and over-time developments common to all firms. Sector-trends account for the different trajectories economic sectors might be following. Company time-varying covariates aim at controlling for additional company-specific characteristics that may jointly affect remuneration and ownership. Despite this fairly extensive set of fixed effects and controls, we cannot rule out unobserved factors which may bias our results. Taking this identification threat into account, we perform numerous robustness checks designed to address these potential concerns.

Individual manager-level

In addition to the company-level analyses, the richness of our dataset also allows us to carry out the analysis at the level of individual managers. This enhances our leverage in two ways: by including additional individual-level control variables to help with precision, and by offering opportunities to further explore potential channels of diffusion.

Since the treatment of interest (US ownership) varies at the company-level, only time-varying variables measured at that level can be potential sources of omitted variable bias. However, if it is the case that the composition of companies changes as a result of US investors’ acquisition of substantial ownership blocs in UK firms (for instance, if the number of directors per company changes as a result of incoming US investors’ influence over hiring decisions), that would affect the interpretation of our results. Reassuringly, our findings at the level of individual managers generally confirm the results from the company-level analysis.

With the switch from the company- to the individual manager-level our baseline specification changes to:

(2)

(2)

where i denotes individual executive directors, j indicates companies, and t years. Yi,j,t measures the remuneration of executives (in log). Xi,j,t is a vector of individual (male dummy, age, age squared, US citizen dummy) and company covariates and εi,j,t is the error term. The model includes company- and year-fixed effects as well as sector-specific linear time trends. Standard errors are clustered at the company level. Descriptive statistics can be found in Appendix Table A7.

Results

Baseline findings

The main analyses examine the robustness of the relationship between foreign ownership and executive pay. We evaluate the relationship between US and other foreign ownership first at the company- and then at the individual manager-level.

The three columns in model a linear relationship between our variables of interest. Moving from left to right, we gradually introduce more covariates in order to assess how the removal of potential sources of confounding variation affects our results. In Column 1, we only include company and year fixed effects. In Column 2, we also control for a range of company covariates. In Column 3, we add sector linear trends.

Table 2. The impact of foreign ownership on executive pay.

In line with our theoretical argument, we find a strongly positive and statistically significant coefficient for the US ownership continuous measure throughout the first three columns. The estimates, significant at the 1% level, indicate a 10% point increase in US ownership translating into a pay increase for top executives of approximately 5% points. The association between continuous non-US foreign ownership and pay is also positive and significant (when company-level controls are included), but much less strongly so in substantive terms.

Alongside the ownership results, the findings in indicate that better corporate performance in terms of operating revenue and increased profit margins also leads to higher pay. Improvements in solvency or stock price are statistically insignificant when these other performance measures are included. More concentrated ownership and higher levels of trade union density (measured at the sectoral level) are negatively associated with executive pay, although the relationships are weak in statistical terms.

In further analyses, presented in Appendix Table A8, we also probe the interactive relationship of US ownership with profit margins on the one hand, and with sector-level trade union density, on the other, in the same regression models. Both interaction terms are statistically insignificant, suggesting neither profitability nor sector-level trade union density moderate the effect of greater US ownership.

To check for potential selection issues behind these results, we assess the role of company-level variables as predictors of levels of US ownership. The results in show that levels of US ownership do not correlate strongly with any of the measures included in our main models. None of the variables is significantly associated with US ownership when entered on their own (Columns 1–6). When we include all variables in the same model (Column 7), we find that US investors tend to increase their ownership stakes in response to greater independence and positive performance on the stock markets; other predictors are in expected directions, but statistically insignificant.

Table 3. US ownership determinants.

In additional checks, we evaluate the robustness of our main results in the smaller, balanced sample of firms for which we have observations in every year. The findings, presented in Appendix Table A9, are strongly consistent. Furthermore, we also evaluate the robustness of our results by excluding the crisis-year of 2007 and use the log of the company-mean instead of -median remuneration as the dependent variable. As shown in Appendix Table A10, again the results remain consistent.Footnote12

Finally, we validate these baseline results at the more disaggregated individual manager-level. The results are shown in . In addition to company- and year-fixed effects, we include individual-level covariates in column 1, and both individual- and company-level controls in column 2. In column 3, we also add sector time trends. Throughout all models we obtain positive and significant coefficients at the 5% level for US ownership. The size of the effect is stable and close to the company-level estimate. According to our estimates in column 3, each 10% point increase in American ownership is associated with a 3.7% increase in pay for top executives. The effect of non-American foreign ownership is also positive, but much smaller and clearly statistically insignificant. In line with the findings of Tobias Neely (Citation2018), we also find notable effects for the gender and age variables. US citizenship is associated with higher pay, but the relationship is not statistically significant. We find very similar, although somewhat weaker, effects in a reduced sample of CEOs only. As indicated in Appendix Table A11, a 10% point increase in US ownership is associated with about a 3% increase in pay for CEOs at British-listed firms.

Table 4. US ownership and executive pay at individual manager-level.

Probing the causal mechanisms

Having established the baseline relationship between the Americanization of company ownership and higher pay for executives in the UK, we proceed to evaluate some of the observable implications of the possible mechanisms mapped out in . We examine heterogeneities of the relationship between US ownership and higher pay across industrial sectors (), the impact on various components of executive remuneration packages (), the relationship with corporate performance (), and the likelihood of British-listed firms hiring US citizens as executives ().

Table 5. The relationship between US ownership and executive pay in various industry branches.

Table 6. The effect of foreign ownership on various pay components.

Table 7. The relationship between American ownership and company performance.

Table 8. Probability of hiring American citizens.

In , we re-estimate EquationEquation (1)(1)

(1) but split our sample of firms into five broad economic sectors: financial services and real estate, non-financial services, primary resources related, general industry and high-tech.Footnote13 For each sector, we present results without covariates in the first step and then add company-specific controls. We find that the presence of American investors has a positive effect on median remuneration across all ten columns of the table. But the effects are strongest in substantive and statistical terms in precisely the sectors that stand out for exceptionally high levels of pay and use of equity-based pay incentives in the US context (cf. Lord & Saito, Citation2010; Philippon & Reshef, Citation2009): primary-resources related industries, finance and high-tech. They are weaker in manufacturing and service sectors other than finance. It is also notable that the sectoral effects differ for US as opposed to non-US foreign ownership, where they appear to be strongest in non-financial services. When we introduce the full vector of control variables, we lose some observations and work with smaller samples. While these regressions yield relatively comparable coefficients for the effect of US ownership, standard errors increase (and statistical significance decreases) due to the lower number of observations.

Both the difference in effects between US and non-US investors and these sectoral heterogeneities are inconsistent with skills factors and weaker monitoring mechanisms, but perfectly in line with expectations of either performance-related market or benchmarking-related bargaining mechanisms.

So far our analyses have focused on total pay as the outcome variable, but our dataset also allows us to study the effect of US ownership on the three main components constituting executives’ total pay packages: cash salary, bonus and equity. To the extent that pay increases in the UK are the result of the adoption of US-style remuneration practices, the impact of growing US ownership should be particularly pronounced for the equity component of managers’ pay packages. We test this expectation in the models presented in , which regress each one of the three remuneration components on both a limited (columns 1, 3 and 5) and extended (columns 2, 4 and 6) set of covariates, controlling for sector trends. The findings strongly confirm our expectations: the effects of US ownership on salary and bonus are insignificant at conventional levels of statistical significance. In contrast, our estimate of the effect on equity pay is large and statistically significant for US ownership (independent of whether we include company-covariates or not), but not non-US foreign ownership.

Next, we probe the relationship between American ownership and the performance of the firms they invest in. We are particularly interested in whether greater influence of US-based investors leads to improvements in corporate performance, which we proxy using the same four measures that we previously employed as controls: operating revenue and profit margins (accounting measures of short-term profitability), the solvency ratio (a measure of financial sustainability) and the annual percentage change in stock market share prices. We use simple models with two-way fixed effects and corporate governance controls (trade union density and BvD independence index), to which we iteratively add sector linear trends.

The results are presented in . On the whole, we do not find any solid evidence indicating that investments by US-based owners lead to improved financial results. The effect of US ownership percentages are positive and larger than those associated with non-US ownership ones, but they remain small in substantive terms and are statistically insignificant throughout the models. In short, against the predictions of performance-related market mechanisms, the positive relationship between American ownership and executive pay does not appear to be mediated by actual substantial improvements in the economic and financial performance of the firms they invest in – a finding that is in line with previous studies that found no positive impact of higher pay (Bivens & Mishel, Citation2013; Marshall & Lee, Citation2016) or the adoption of shareholder value practices more generally (Fligstein & Shin, Citation2007) on profitability. It is conceivable that US investments themselves influence share price movements if they are in most cases either perceived positively or negatively by markets, but to the extent this is the case, it would work against the absence of a significant effect that we identify here.

Finally, we leverage the individual-level data to test the hiring of US nationals as a potential mechanism. Executive directors used to US-levels of pay could plausibly demand more generous pay packages or may be offered more expensive remuneration deals by companies eager to lure them from the US market. To assess this mechanism, we test the impact of US ownership as a predictor of the probability that a company hires a manager with US nationality. Although relatively small substantially, we do find positive evidence for this channel.

In a robustness test, shown in Appendix Table A13, we test the importance of this channel in driving our baseline result. We re-run the main models in for a subsample of companies that never hired a US citizen as executive director throughout our time period of observation. We find pay-increasing effects of US ownership similar to those observed in the main analyses in this subsample. In other words, US ownership also increases levels of pay at firms that do not hire American citizens. Whereas the hiring mechanism thus does appear to play a role, it accounts for only one part of the larger story.

Discussion

Throughout our analyses, we found a statistically significant and substantially large positive effect of US ownership on executive pay at publicly listed UK-incorporated firms. Investments from other non-US foreign investors are also associated with higher pay in some specifications, but both the significance and substantive size are smaller. The pay effect of US investments is particularly strong for firms in finance, primary-resources related industries and the high-tech sector. The US-induced pay premium is strongly associated with larger shares of salary packages being tied to equity-based pay, but unrelated to corporate performance. Furthermore, we find evidence that US ownership does increase the likelihood of appointments of US nationals at UK firms, albeit executives at firms that do not hire US citizens appear to equally benefit from increases in US ownership.

Together, these patterns highlight changes in how executives are being paid to be an important driver of the US pay premium. While the sensitivity of pay-setting procedures makes it difficult to study these processes using qualitative research methods, the patterns in the data allow us to make some informed guesses about how US investments lead to higher pay. summarizes the evidence from our analysis in light of the expected effects of the various mechanisms.

Table 9. Summary of results.

The increased probability of hiring US nationals is in line with the first mechanism of labor market internationalization (Column 1). Dynamics centered on skill premia due to exogenous structural changes in labor markets for executives, on the other hand, are disconfirmed by the marked differences between US and non-US investors, as well as differences in the US-induced pay effects across industrial sectors. The evidence for coercive imposition of P4P practices by foreign investors (Column 2) is equally mixed. Although a larger share of US ownership appears to lead to greater use of incentive-based pay in British companies, payouts do not appear to be clearly linked to corporate performance. Instead, the patterns are relatively consistent with mechanisms of shifting bargaining power inside firms (Column 3). The fact that levels of pay do not increase invariably, but assimilate to payment practices in the USA in terms of pay components and industrial sectors in response to US investments (rather than non-US foreign ones) is in line with expectations of benchmarking dynamics. Equally, the empirical observation that executives at UK-firms are able to get higher pay even in absence of actual improvements in performance is in line with theories conceptualizing executive remuneration as rent capture (Bebchuk & Fried, Citation2004; Bivens & Mishel, Citation2013). On the other hand, our findings also indicate that, in our sample, stronger trade unions do not appear to be effective at restraining the upwards pressure on executive pay that greater US investments bring aboutFootnote14. The picture that emerges from our analyses is a situation in which remuneration increases sharply for UK managers as it gradually catches up to US levels, while simultaneously shielding them from punishments for underperformance.

Conclusions

The rising share of income taken by the highest earners across the advanced economies is by now well documented in the aggregate data, but pinpointing its causes requires a different approach. This article has addressed one of the main components of this top income inequality – the dramatic increases in executive remuneration in many advanced nations, drawing on fine-grained individual- and company-level data which allow us to identify the specific causal channels in the UK case.

We make three main contributions. First, we show that adopting a firm-level perspective can yield valuable insights by revealing previously overlooked trans-national dimensions of growing income inequality. Second, we use granular data on the compensation packages of individual top executives in individual companies over several years to test the hypothesis that US investment is a key driver of skewed top income growth. The strength of our results gives us a high degree of confidence that, all else equal, US positions in UK companies bring increased rewards for top executives. Third, while not conclusive, the richness of our dataset also allows us to draw inferences about the dynamics through which US ownership leads to higher pay. Most importantly, the evidence that we assemble suggests that local managers play an important role as agents in these processes. In other words, growing US ownership does not primarily lead to higher pay because US investors push for it, but because – as in Farrell and Newman (Citation2014, p. 347) ‘cross-national layering’ – it creates opportunities that local managers can exploit to appropriate greater shares of corporate earnings for themselves.

At the same time, our focus on one country and a relatively short time period advises caution in generalizing the findings. We are unable to control for the effects of national-level variables, such as corporate governance regulation, wage bargaining institutions, taxation policy, labor market and product market regulation, to name just a few potentially important factors that could affect how US investment feeds through into top income growth in different countries (cf. Angeles & Kemmerling, Citation2020). Looking forward, future research could fruitfully extend the approach to other country cases to further probe the mechanisms and test how well our argument travels to different institutional and political environments. National institutional arrangements, such as those that typically inform studies of economic inequality in the comparative political economy literature may have important effects in cushioning, diverting or perhaps even closing off the US investor channel to higher executive rewards. Now that similar data are also becoming available for other European countries, extending the analysis to more cases can further advance our understanding of top income growth.

More broadly, we hope that our approach will inspire more research in IPE focusing on firm-level dynamics. The transnational organization of large corporations makes them fruitful units of analysis to study political-economic processes that transcend national borders. At the same time, more detailed firm-level data can overcome some of the natural limitations of cross-national economic statistics in tracing transnational processes (Linsi & Mügge, Citation2019). Beyond the empirical case examined here, we believe that the study of boardroom politics at large multinational corporations sets out a promising avenue to better understand the micro-foundations of the macro-trends that constitute the core of the discipline of IPE.

Supplemental Material

Download PDF (302.5 KB)Acknowledgments

Previous versions of this article have been presented at the SPSA Conference 2018 in Geneva, SASE 2018 in Kyoto, the Politicologenetmaal 2019 in Antwerp and workshops at the University of Amsterdam and Trinity College Dublin. We thank the RIPE Editorial Board and anonymous reviewers, as well as Renira Angeles, Adam Leaver, Julie Lynch, Loriana Crasnic, Sandy Pepper, Raj Chari, Johan Adriaensen, Moritz Marbach, Eelke Heemskerk, Lena Ajdacic and Wouter Schakel for many useful comments and suggestions. Sebastiano Comotti provided valuable research assistance. Special thanks go to the interviewees for sharing their insider perspectives with us. The views expressed here solely represent those of the authors and should not be attributed to the World Bank Group, its Executive Directors, or the countries they represent.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

Most data used is proprietary, but can be made available to the journal editors or reviewers upon request. Replication code will be made publicly available on Harvard Dataverse upon publication.

Additional information

Funding

Notes on contributors

Lukas Linsi

Lukas Linsi is Assistant Professor of International Political Economy in the Department of International Relations and International Organization, University of Groningen. His research has been published in journals such as the European Journal of International Relations, New Political Economy and the Review of International Political Economy.

Jonathan Hopkin

Jonathan Hopkin is Professor of Comparative Politics in the European Institute and the Department of Government, London School of Economics and Political Science. He is the author of Party Formation and Democratic Transition in Spain (Palgrave Macmillan) and Anti-System Politics (Oxford University Press) and has published widely on the party politics and political economy of Europe.

Pascal Jaupart

Pascal Jaupart is an Economist in the Social Protection and Jobs Global Practice at the World Bank. He completed his PhD at the London School of Economics in 2017. Before joining the World Bank, he was a Postdoctoral researcher at Oxford University’s Blavatnik School of Government. His research has been published in journals such as Economics Letters, British Medical Journal – Global Health, and the Journal of Economic Geography.

Notes

1 See for instance the Harvard Business Review manifesto for P4P by Jensen and Murphy (Citation1990).

2 Note that in global perspective the UK is considered to be one of the highest-paying markets other than the USA, together with Switzerland, Ireland, Italy, Australia and Canada (Angeles & Kemmerling, Citation2020, p. 9; Fernandes et al., Citation2013, p. 337; 344).

3 The BoardEx data for the UK has better coverage and includes many smaller firms than data for the USA.

4 Online research interview with Luke Hildyard, Executive Director High Pay Center, 7 August 2020.

5 Online research interview with James Coldwell, Program Lead at ShareAction, 18 August 2020.

6 Online research interview with Luke Hildyard, Executive Director High Pay Center, 7 August 2020.

7 Fernandes et al. (Citation2013) is the only other study we are aware of that has used this information, but with a comparably small sample for only one year.

8 We downloaded the entire database in the summer of 2016.

9 Personal communication with BoardEx.

10 According to current UK regulations, any investor interested to acquire a share of 1% or more is legally obliged to inform the target company; in cases of 3% or more, investors must in addition inform the London Stock Exchange (Marriage, Citation2015). Outward investors domiciled in the USA must simultaneously declare substantial ownership positions to the SEC through 13F and 13D declarations, which are made publicly available on the Edgar system.

11 This estimate is very similar to the results of a recent study on foreign ownership of the UK stock market commissioned by the ONS. Tracking ultimate owners for a subsample of 200 listed UK companies in 2015, the report indicated levels of foreign ownership to amount to 53.9% (Office for National Statistics, Citation2017).

12 The positive estimates are slightly larger for models using the mean, which reflects the greater sensitivity of the mean than the median to extreme value observations.

13 Appendix Table A12 shows the industries included in each of these sectors.

14 Bearing in mind that trade unions were already weak in Britain during the time period of observation, this is not entirely surprising and may be different in other contexts, as noted previously.

References

- Advani, A., Koenig, F., Pessina, L., & Summers, A. (2020). Importing inequality: Immigration and the top 1 percent. IZA DP No. 13731. http://ftp.iza.org/dp13731.pdf

- Ahmadjian, C. L., & Robbins, G. E. (2005). A clash of capitalisms: Foreign shareholders and corporate restructuring in 1990s Japan. American Sociological Review, 70(3), 451–471. https://doi.org/10.1177/000312240507000305

- Almond, P., Muller-Camen, M., Collings, D. G., & Quintanilla, J. (2006). Pay and performance. In P. Almond & A. Ferner (Eds). American multinationals in Europe: Managing employment relations across national borders (pp. 119–145). Oxford University Press.

- Amis, J. M., Mair, J., & Munir, K. A. (2020). The organizational reproduction of inequality. Academy of Management Annals, 14(1), 195–230. https://doi.org/10.5465/annals.2017.0033

- Angeles, R. C., & Kemmerling, A. (2020). How redistributive institutions affect pay inequality and heterogeneity among top managers. Socio-Economic Review, 18(1), 3–30. https://doi.org/10.1093/ser/mwz048

- Atkinson, A. B., Piketty, T., & Saez, E. (2010). Top incomes in the long run of history. Top incomes: A global perspective (pp. 664–760). Oxford University Press.

- Autor, D. H., Katz, L. F., & Kearney, M. S. (2006). The polarization of the U.S. labor market. American Economic Review, 96(2), 189–194. https://doi.org/10.1257/000282806777212620

- Avent-Holt, D., & Tomaskovic-Devey, D. (2014). A relational theory of earnings inequality. American Behavioral Scientist, 58(3), 379–399. https://doi.org/10.1177/0002764213503337

- Babic, M., Garcia-Bernardo, J., & Heemskerk, E. M. (2020). The rise of transnational state capital: State-led foreign investment in the 21st century. Review of International Political Economy, 27(3), 433–443. https://doi.org/10.1080/09692290.2019.1665084

- Bakija, J. A., Cole, B. T., & Heim. (2012). Jobs and income growth of top earners and the causes of changing income inequality: Evidence from U.S tax return data. https://web.williams.edu/Economics/wp/BakijaColeHeimJobsIncomeGrowthTopEarners.pdf

- Bebchuk, L., & Fried, J. (2004). Pay without performance: The unfulfilled promise of executive compensation. Harvard University Press.

- Bender, R., & Moir, L. (2006). Does ‘best practice’ in setting executive pay in the UK encourage ‘good’ behaviour? Journal of Business Ethics, 67(1), 75–91. https://doi.org/10.1007/s10551-006-9006-8

- Bivens, J., & Mishel, L. (2013). The pay of corporate executives and financial professionals as evidence of rents in top 1 percent incomes. Journal of Economic Perspectives, 27 (3),57–78. https://doi.org/10.1257/jep.27.3.57

- Brewer, M., Sibieta, L., & Wren-Lewis, L. (2009). Racing away? Income inequality and the evolution of high incomes. No. 76. IFS Briefing Note.

- Bureau van Dijk. (2018). Corporate ownership structures. https://www.bvdinfo.com/en-us/our-products/our-expertise/find-out-how-we-add-value-to-company-information/corporate-ownership-structures

- Cheffins, B. R., & Thomas, R. S. (2004). The globalization (Americanization?) of executive pay. Berkeley Business Law Journal, 1(2), 233–290. https://heinonline.org/HOL/LandingPage?handle=hein.journals/berkbusj1&div=14&id=&page=

- Conyon, M. J., Core, J. E., & Guay, W. (2011). Are U.S. CEOs paid more than U.K. CEOs? Inferences from risk-adjusted pay. Review of Financial Studies, 24(2), 402–438. https://doi.org/10.1093/rfs/hhq112

- Conyon, M. J., & Murphy, K. J. (2000). The prince and the pauper? CEO pay in the United States and United Kingdom. The Economic Journal, 110(467), 640–671. https://doi.org/10.1111/1468-0297.00577

- Conyon, M. J., Peck, S. I., & Sadler, G. V. (2009). Compensation consultants and executive pay: Evidence from the United States and the United Kingdom. Academy of Management Perspectives, 23(1), 43–55. https://doi.org/10.5465/amp.2009.37008002

- Deeg, R., Hardie, I., & Maxfield, S. (2016). What is patient capital, and where does it exist? Socio-Economic Review, 14(4), 615–625. https://doi.org/10.1093/ser/mww030

- Desender, K. A., Aguilera, R. V., Lópezpuertas-Lamy, M., & Crespi, R. (2016). A clash of governance logics: Foreign ownership and board monitoring. Strategic Management Journal, 37(2), 349–369. https://doi.org/10.1002/smj.2344

- DiPrete, T., Eirich, G., & Pittinsky, M. (2010). Compensation benchmarking, leapfrogs, and the surge in executive pay. American Journal of Sociology, 115(6), 1671–1721. https://doi.org/10.1086/652297

- Dünhaupt, P. (2017). Determinants of labour’s income share in the era of financialisation. Cambridge Journal of Economics, 41(1), 283–306. https://doi.org/10.1093/cje/bew023

- Esping-Andersen, G. (1990). The three worlds of welfare capitalism. Blackwell.

- Farrell, H., & Newman, A. (2016). The new interdependence approach: Theoretical development and empirical demonstration. Review of International Political Economy, 23(5), 713–736. https://doi.org/10.1080/09692290.2016.1247009

- Farrell, H., & Newman, A. L. (2014). Domestic institutions beyond the nation-state: Charting the new interdependence approach. World Politics, 66(2), 331–363. https://doi.org/10.1017/S0043887114000057

- Fernandes, N., Ferreira, M. A., Matos, P., & Murphy, K. J. (2013). Are U.S. CEOs paid more? New international evidence. Review of Financial Studies, 26(2), 323–366. https://doi.org/10.1093/rfs/hhs122

- Fichtner, J. (2017). Perpetual decline or persistent dominance? Uncovering Anglo-America’s true structural power in global finance. Review of International Studies, 43(1), 3–28. https://doi.org/10.1017/S0260210516000206

- Fichtner, J., Heemskerk, E. M., & Garcia-Bernardo, J. (2017). Hidden power of the big three? Passive index funds, re-concentration of corporate ownership and new financial risk. Business and Politics, 19(2), 298–326. https://doi.org/10.1017/bap.2017.6

- Flaherty, E. (2015). Top incomes under finance-drive capitalism, 1990–2010: Power resources and regulatory orders. Socio-Economic Review, 13(3), 417–447. https://doi.org/10.1093/ser/mwv011

- Fligstein, N., & Shin, T. (2007). Shareholder value and the transformation of the U.S. economy, 1984–20001. Sociological Forum, 22(4), 399–424. https://doi.org/10.1111/j.1573-7861.2007.00044.x

- Froud, J., Johal, S., Leaver, A., & Williams, K. (2006). Financialization and strategy: Narrative and numbers. Routledge.

- Frydman, C., & Saks, R. E. (2010). Executive compensation: A new view from a long-term perspective, 1936–2005. Review of Financial Studies, 23(5), 2099–2138. https://doi.org/10.1093/rfs/hhp120

- Garcia-Bernardo, J., & Takes, F. W. (2016). The effects of data quality on the analysis of corporate board interlock networks. https://arxiv.org/pdf/1612.01510.pdf.

- Gerakos, J. J., Piotroski, J. D., & Srinivasan, S. (2013). Which U.S. market interactions affect CEO pay? Evidence from UK companies. Management Science, 59(11), 2413–2434. https://doi.org/10.1287/mnsc.2013.1714

- Gilens, M. (2012). Affluence and influence: Economic inequality and political power in America. Princeton University Press.

- Godechot, O. (2012). Is finance responsible for the rise in wage inequality in France? Socio-Economic Review, 10(3), 447–470. https://doi.org/10.1093/ser/mws003

- Godechot, O. (2017). Wages, bonuses and appropriation of profit in the financial industry: The working rich. Routledge.

- Goldstein, A. (2012). Revenge of the managers: Labor cost-cutting and the paradoxical resurgence of Managerialism in the Shareholder value era. American Sociological Review, 77(2), 268–294. https://doi.org/10.1177/0003122412440093

- Hacker, J. S., & Pierson, P. (2010). Winner-take-all politics: How Washington made the rich richer - and turned its back on the middle class. Simon & Schuster.

- Hager, S. B. (2017). A global bond: Explaining the safe-haven status of US treasury securities. European Journal of International Relations, 23(3), 557–580. https://doi.org/10.1177/1354066116657400

- Hager, S. B. (2018). Varieties of top incomes? Socio-Economic Review, 18, 1175–1198. https://doi.org/10.1093/ser/mwy036.

- Hall, P. A., & Soskice, D. (2001). Varieties of capitalism: The institutional foundations of comparative advantage. Oxford University Press.

- Hargreaves, D. (2019). Are chief executives overpaid? Polity.

- Hopkin, J., & Lynch, J. (2016). Winner-take-all politics in Europe? European inequality in comparative perspective. Politics & Society, 44(3), 335–343. https://doi.org/10.1177/0032329216656844

- Huber, E., Huo, J., & Stephens, J. D. (2019). Power, policy, and top income shares. Socio-Economic Review, 17(2), 231–253. https://doi.org/10.1093/ser/mwx027

- Huber, E., Petrova, B., & Stephens, J. D. (2020). Financialization, labor market institutions and inequality. Review of international political economy (pp. 1–28). August, . https://doi.org/10.1080/09692290.2020.1808046

- Iversen, T., & Soskice, D. (2006). Electoral institutions and the politics of coalition: Why some democracies redistribute more than others. American Political Science Review, 100(2), 165–181. https://doi.org/10.1017/S0003055406062083

- Iversen, T., & Soskice, D. (2009). Distribution and redistribution - the shadow of the nineteenth century. World Politics, 61(3), 438–486. https://doi.org/10.1017/S004388710900015X

- Jensen, M. C., & Murphy, K. J. (1990). CEO incentives - it’s not how much you pay, but how. Harvard business review (pp. 138–149). May–June. https://hbr.org/1990/05/ceo-incentives-its-not-how-much-you-pay-but-how

- Lin, K. H., & Megan Tobias, N. (2020). Divested: Inequality in financialized America. Oxford University Press. https://global.oup.com/academic/product/divested-9780190638313?cc=nl&lang=en&.

- Linsi, L., & Mügge, D. (2019). Globalization and the growing defects of international economic statistics. Review of International Political Economy, 26(3), 361–383. https://doi.org/10.1080/09692290.2018.1560353

- Lockwood, E. (2021). The international political economy of global inequality. Review of International Political Economy, 28(2), 421–445. https://doi.org/10.1080/09692290.2020.1775106

- Lord, R. A., & Saito, Y. (2010). Trends in CEO compensation and equity holdings for S&P 1500 firms: 1994–2007. Journal of Applied Finance, 20(2), 1–17. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2693076.

- Marriage, M. (2015). Best-paid fund management chief executives revealed. Financial Times. 19 April. https://www.ft.com/content/68b64eca-e42f-11e4-9039-00144feab7de

- Marshall, R., & Lee, L. E. (2016). Are CEOs paid for performance? Evaluating the effectiveness of equity incentives. https://www.msci.com/documents/10199/91a7f92b-d4ba-4d29-ae5f-8022f9bb944d.

- Morrow, S. (2017). Institutional investor survey 2017: Corporate governance is no longer just about the annual meeting. https://www.morrowsodali.com/eventassets/1488278692-MorrowSodal_Institutionalinvestorsurvey2017.pdf.

- Nagrawala, F., & Springer, K. (2020). Point of no return: A ranking of 75 of the world’s largest asset manages’ approaches to responsible investment. London. https://shareaction.org/wp-content/uploads/2020/03/Point-of-no-Returns.pdf

- Oatley, T. (2019). Toward a political economy of complex interdependence. European Journal of International Relations, 25(4), 957–978. https://doi.org/10.1177/1354066119846553

- Oatley, T., & Petrova, B. (2020). The global deregulation hypothesis. Socio-Economic Review. [Epub Ahead of Print]. https://doi.org/10.1093/ser/mwaa028

- Office for National Statistics. (2017). Ownership of UK quoted shares: 2016. https://www.ons.gov.uk/economy/investmentspensionsandtrusts/bulletins/ownershipofukquotedshares/2016.

- Oxelheim, L., & Randoy, T. (2005). The Anglo-American financial influence on CEO compensation in Non-Anglo-American firms. Journal of International Business Studies, 36(4), 470–483. https://doi.org/10.1057/palgrave.jibs.8400144

- Petrin, M. (2015). Executive compensation in the United Kingdom - past, present, future. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2616495.

- Philippon, T., & Reshef, A. (2009). “Wage and human capital in the U.S financial industry: 1909–2006.” 14644. NBER Working Paper Series. http://www.nber.org/papers/w14644.

- Piketty, T. (2014). Capital in the twenty-first century. Harvard University Press.

- Sapp, S. G. (2008). The impact of corporate governance on executive compensation. European Financial Management, 14(4), 710–746. https://doi.org/10.1111/j.1468-036X.2008.00443.x

- Scheve, K., & Stasavage, D. (2009). Institutions, partisanship, and inequality in the long run. World Politics, 61(2), 215–253. https://doi.org/10.1017/S0043887109000094

- Schwartz, H. M. (2019). What’s wealth got to do with it? Global balance sheets and US geo-economic power. Review of International Political Economy, 26(5), 963–986. https://doi.org/10.1080/09692290.2019.1625419

- Song, J., Price, D. J., Guvenen, F., Bloom, N., & von Wachter, T. (2019). Firming up inequality. The Quarterly Journal of Economics, 134(1), 1–50. https://doi.org/10.1093/qje/qjy025

- Starrs, S. (2013). American economic power hasn’t declined - it globalized! Summoning the data and taking globalization seriously. International Studies Quarterly, 57(4), 817–830. https://doi.org/10.1111/isqu.12053

- Thomas, R. S. (2004). Explaining the international CEO pay gap: Board capture or market driven? Vanderbilt Law Review, 57(4), 1171–1268. https://scholarship.law.vanderbilt.edu/vlr/vol57/iss4/1/

- Tobias Neely, M. (2018). Fit to be king: How patrimonialism on wall street leads to inequality. Socio-Economic Review, 16(2), 365–385. https://doi.org/10.1093/ser/mwx058

- Tomaskovic-Devey, D., & Lin, K.-H. (2011). Income dynamics, economic rents, and the financialization of the U.S. economy. American Sociological Review, 76(4), 538–559. https://doi.org/10.1177/0003122411414827

- WID. (2018). World Inequality Database. http://wid.world/

- Willman, P., & Pepper, A. (2020). The role played by large firms in generating income inequality: UK FTSE 100 pay practices in the late twentieth and early twenty-first centuries. Economy and Society, 49(4), 516–539. https://doi.org/10.1080/03085147.2020.1774259

- Zeitlin, J., & Gary, H. (Eds.). (2000). Americanization and its limits. Cambridge University Press.