Abstract

As Western-led institutions of global governance adapt to global power shifts, the question of which countries dominate, and how, increasingly animates scholarship. Yet while attention has shifted from ‘Great’ to ‘Rising’ Powers, the underlying focus on market power has changed little. In this article, we shift the focus to alternative forms of power that developing countries can wield in global governance, specifically in highly technical transnational negotiations. Reconceptualising the notion of ‘regulatory capacity’, we argue that states can overcome limited market power through socio-technical resources: expertise and professional networks. These resources form the basis through which policy claims become authoritative and they enable emerging state coalitions to influence policy-making. To demonstrate this, we analyse developing countries’ involvement in standard-setting for international corporate taxation. Specifically, we study the newly established G20/OECD Inclusive Framework, an experiment where more than 140 jurisdictions participate in negotiations that were previously the preserve of OECD states. Based on unique attendance data and interviews with dozens of participants, we perform a detailed analysis of specific policy decisions, interrogating the extent and sources of developing countries’ influence. We find that socio-technical resources allow individuals from lower-income countries to achieve narrow yet significant successes, punching above their weight in global governance.

Introduction

The power shift away from OECD countries poses a challenge to the viability and legitimacy of longstanding institutions of global economic governance (Beeson & Bell, Citation2009; Woods, Citation2010). Throughout the twentieth century, control over these institutions was understood to be the prerogative of great powers in the US and Europe. The last two decades have forced a reorientation, as developing countries are increasingly able to influence global policy-making (Wade, Citation2011; Ban & Blyth, Citation2013).Footnote1

Studying this shift has provided novel insights into the nature of influence exercised by countries historically thought to be on the margins (Hopewell, Citation2015; de Graaff et al., Citation2020). Yet, having identified that these new dynamics of power are key to understanding contemporary struggles in global governance, IPE has continued to emphasise market power. A tendency to focus on the largest emerging markets has inhibited understanding of the complex and heterogeneous forces behind developing countries’ influence on global governance (Hopewell, Citation2015). To the extent that IPE scholarship has looked at ‘the rest’ – countries outside the OECD and G20 – it often continues to de-centre them. Their agency is framed either as an attempt to resist Western states (Narlikar & Tussie, Citation2004; Panda, Citation2017; Vickers, Citation2013) or within coalitions whose primary impact is to amplify emerging markets’ power (Ban & Blyth, Citation2013; Beeson & Bell, Citation2009; Wade, Citation2011; Woods, Citation2010).

In this article, we examine how lower-income countries have begun to draw on socio-technical resources – expertise and professional networks – as an alternative source of power in deeply technical policy-making processes. As recent literature has demonstrated, e.g. on gender issues, marginalised actors can exploit “gaps and soft spots” in the social rules and shared practices of a transnational community to push forward their agenda (Waylen, Citation2021, 14). To illustrate this, we combine two streams of literature: “Regulatory capacity” considers how countries need bureaucratic expertise, coherence and authority to exercise global power (Bach & Newman, Citation2007; Bach & Newman, Citation2010; Newman & Posner, Citation2015; Aydin Citation2021). Yet its conceptualization of expertise tends to rely on state-centric measures of the expert workforce or the size of bureaucratic organisations, and regulatory capacity scholarship has paid less attention to the subjective nature of expertise, how its substance and coherence are negotiated and constructed in transnational settings (Knaack & Gruin Citation2021).

Drawing on literature on the politics of expertise, we therefore reconceptualise regulatory capacity within global governance institutions – which we see as transnational social spaces occupied by expert communities – as socially constructed (Sending, Citation2015; Eskelinen & Ylönen, Citation2017; Kranke, Citation2020; Knaack & Gruin Citation2021). For this form of power, the role of technical expertise is not to use a large bureaucratic machinery to bring market power to bear. Rather, it is to attract “deference” to certain forms of knowledge within a transnational professional community, while sanctioning other, incompatible forms (Barnett & Duvall, Citation2005; Seabrooke, Citation2014; Krisch, Citation2017). The “coherence” of expertise, in turn, arises from shared understandings among like-minded participants: interpersonal relationships may form a more powerful basis for coalitions than states’ institutional memberships. We use the term ⋅socio-technical resources’ to refer to the combination of social-constructed expertise and professional networks that enable the recognition of authoritative expertise, which countries must develop if they wish to exert an influence in highly technical transnational policy-making contexts. This is especially pertinent for developing countries and others lacking strong material capabilities (Braveboy-Wagner, Citation2010; Quack, Citation2016; Eskelinen & Ylönen, Citation2017).

Our empirical focus, global tax governance, has historically been characterised by insular and technocratic policymaking among a small group of experts at the OECD. It has recently shifted gears as a result of mounting politicisation (Seabrooke & Wigan, Citation2016; Christensen & Hearson, Citation2019), and the OECD has transferred much of its corporate tax standard-setting competence to an “Inclusive Framework” of over 140 member jurisdictions, including lower-income countries. Extant literature’s emphasis on market power and objective regulatory capacity implies that these negotiations will continue to be dominated by countries with large market power and large bureaucracies, yet the policy literature is full of claims of lower-income countries’ influence (ATAF, Citation2019; OECD 2021).

We open up the black box of Inclusive Framework negotiations using a qualitative, interview-based methodology, identifying the objectives of negotiators from lower-income countries, the extent to which they were achieved, and the determinants of success and failure. Previous scholarship has highlighted the difficulty of analysing the true extent of developing countries’ participation, because of the lack of procedural transparency (Christians & van Apeldoorn, Citation2018; Brugger & Engebretsen, Citation2020). Indeed, it is a broader concern that, “we seldom have precise details of who are the persons and the delegations that inhabit the physical space in which [global] lawmaking occurs” (Susan & Halliday, Citation2017, 162). First, we conducted semi-structured interviews with 48 experts and negotiators, most of whom had been directly involved in global tax negotiations. The qualitative research process is elaborated in Supplementary Materials Annex 1. Second, attendance records for OECD and Inclusive Framework meetings between 2015 and 2019, supplied to us by the OECD secretariat, allowed us to study the depth and breadth of participation, and to target interviews on individuals who had been present in meetings at key decision-making points. To make interviews as concrete as possible, we focused on specific policy cases that some actors claimed had been influenced by developing countries (see Supplementary Materials Annex 2). The interviews and attendance data were complemented by reviewing every OECD/Inclusive Framework document - discussion draft, consultation letter, press release, report and guidance – related to these policy cases.

The next section of this article surveys scholarship on developing countries in global economic governance, and sets out our conceptual framework. Next, we describe the history and organisation of the Inclusive Framework, offering a critical examination of the official claim that participation is on an “equal footing.” Our case studies follow. First, we provide a negative case: the OECD’s partial endorsement of the “sixth method” for transfer pricing, which we show has been incorrectly claimed as a lower-income country success. In contrast, our second case shows African tax experts working together to obtain a victory, circumscribing the influence of a new OECD norm that disadvantaged them: the so-called “Authorised OECD Approach” for attributing profits to permanent establishments. Notably, this victory had previously eluded a minority of OECD member states who had been coerced into acquiescence by major powers. The third case illustrates how assertive lower-income country intervention, through the G24, changed the high-profile and heavily contested global debate on the taxation of large digital firms. This is seen in changes to institutional procedures as well as the content of negotiations.

Developing countries and expertise in global governance

How can we understand the exercise of power by developing countries in global economic governance? Historically, they were treated as peripheral actors, exerting little or no influence because they lacked market power. Yet this narrative has rightly been challenged. The notion that African states, for example, were always on the margins of international politics has been problematized (Chipaike & Knowledge, Citation2018). “Africa has never existed separate from the world but rather has been inextricably entwined in world politics and has continually exercised its agency” (Taylor, Citation2010, 2). This discussion has only been made more pertinent by global power shifts over the past decades, which have enabled a critical re-examination of the influence of countries outside the historical Western core (Woods, Citation2010; Wade, Citation2011; Ban & Blyth, Citation2013).

While several streams of scholarship have fruitfully attempted to switch the focus to states on the ‘periphery’, influence over global politics is still understood to be largely limited to states with market power. To begin with, peripheral states’ agency has been cast as reactive, through “resilience” or “resistance” to powerful states’ intrusions on their policy space (Bishop, Citation2012; Scott, Citation1992). The spotlight has also turned to ‘Rising’ Powers, whose growing markets give them influence from the same source as the Great Powers, clearly distinct from that of lower-income countries (Narlikar & Tussie, Citation2004; Panda, Citation2017; Vickers, Citation2013). Alternatively, emphasis is placed on coalitions, through which peripheral states can counterbalance the influence of larger powers if they can obtain sufficient numbers and cohesiveness (Hopewell, Citation2015; Narlikar, Citation2003).

This emphasis on market power has also demarcated much work on global tax governance, which is typically cast as a game played between the US and Europe (Hakelberg, Citation2020; Lips, Citation2019) and, more recently, large emerging markets (Christensen & Hearson, Citation2022; Hearson & Prichard, Citation2018; Lesage et al., Citation2019). Where “small states” are considered, it is typically as offshore tax havens disrupting the international order or resisting Great Power intrusions (Palan, Citation2003; Sharman, Citation2006; Crasnic, Citation2020). Other developing countries are generally viewed as rule-takers, silent followers coerced into aligning with OECD tax hegemony (Rixen, Citation2008, 159–161; Brugger & Engebretsen, Citation2020). This despite the presence of tensions between capital-importing and -exporting countries in multilateral tax negotiations since their early-20th century beginnings (Jogarajan, Citation2018; Hearson, Citation2021).

In what follows, we build on research that shows how states without a strong power base, in the conventional sense, are nonetheless able to meaningfully achieve narrow yet significant change in global governance (Lee, Citation2009; Braveboy-Wagner, Citation2010; Ingebritsen et al., Citation2012; Apecu, Citation2013). We contribute a more diverse view of how such influence is achieved, based on socio-technical resources. This brings with it an insistence on seeing, analytically, new dimensions of change rather than emphasizing the stability created by the continued dominance of countries rich in market power, only rarely interrupted by exogenous shocks or critical junctures (Streeck & Thelen, Citation2005; Paul, Citation2018).

When might such narrow changes in global economic governance be significant? From the perspective of developing countries’ negotiators and others invested in global tax institutions, there are three main reasons. First, small textual changes can still be fiercely contested, of real substantive importance to those advocating and resisting it. Where Great Powers continue to get their way most of the time, it becomes even more important to understand when and why they do not. In contrast to market power perspectives, opening up the institutional black box to understand critical actors’ “practices and strategies for change inside institutions” can “allow a fuller understanding” of how these narrow yet significant changes in global economic governance are achieved (Waylen, Citation2021, 2). Second, “path-undermining” developments such as those we document demonstrate that neither the dominance of Great Powers nor the path-dependency of institutions is a foregone conclusion (Rixen & Viola, Citation2016, 12). Such developments can become self-fulfilling, emboldening actors who have brought about narrow changes, and persuading others to make common cause. Third, narrow changes layered on top of each other can lead to a “gradual transformation” (Streeck & Thelen, Citation2005, 9) that can eventually cause a systemic re-alignment (Sinha, Citation2018).

We combine two schools of scholarship to shift the focus onto the socio-technical resources of negotiating delegates, a key source of power in global governance. Regulatory capacity, in its original conception, is “the mechanism linking market size to power in international market regulation” (Bach & Newman, Citation2010, 672). States’ potential power over international regulation is a function of their market size, but this potential must be unlocked through an amalgamation of institutional resources – expertise, coherence, and sanction authority – which provide states with the “ability to formulate, monitor, and enforce a set of market rules” (Bach & Newman, Citation2007, 731). These institutional resources are based on a well-trained staff with formal regulatory powers, which arises from a large bureaucracy, experience with policy-making, and engagement with private sector policy networks (Gilardi, Citation2002; Bach & Newman, Citation2007; Büthe & Mattli, Citation2011; Aydin Citation2021). This notion of regulatory capacity can be understood within the framework of what Barnett and Duvall (Citation2005) call compulsory power – a state’s ability to leverage its market power to impose its preferred regulatory framework on others, or to resist others’ attempts to do the same. Naturally, this literature is animated primarily by attempts to understand why actors with large markets – principally the European Union and China – have struggled to translate this into compulsory power.

For our focus on states without large markets, and in transnational policy development, rather than policy exercise, we need to think differently about regulatory capacity. To do so, we incorporate insights from work on the politics of expertise (Stone, Citation2013; Sending, Citation2015; Ban et al., Citation2016; Helgadóttir, Citation2016). Rather than viewing a large bureaucracy, experienced staff and private sector engagement as ‘natural’ sources of objective expertise, this body of work considers expertise to be socially constructed. Epistemic authority derives from social relations and knowledge struggles within and between professional networks, and is possessed by individuals perceived as “knowing well” (Lazega, Citation1992; Seabrooke, Citation2014; Zagzebski, Citation2013). “Good ideas are only powerful when those promoting them are well positioned within and across professional networks” (Seabrooke, Citation2014, 52). We use the term ⋅socio-technical resources⋅ to refer to the combination of social-constructed expertise and professional networks that countries must develop if they wish to exert an influence in such contexts, especially in the face of overwhelming material capabilities (Braveboy-Wagner, Citation2010; Quack, Citation2016; Eskelinen & Ylönen, Citation2017). This is regulatory capacity closer to institutional power (Knaack & Gruin, Citation2021; Barnett & Duvall, Citation2005), and unlike the exercise of compulsory power it is not reliant on significant market power alone.

This focus on the transnational, social dynamics of global economic governance follows a stream of recent literature on international taxation (Picciotto, Citation2015; Seabrooke & Wigan, Citation2016; Jogarajan, Citation2018; Christensen, Citation2021; Hearson, Citation2021). Global tax governance is a highly technocratic issue area, heavily shaped by a transnational policy community organised around the OECD. The personal resources that are critical to struggles over standard-setting, such as expertise and professional networks, are intersubjectively constructed within this community. Experts from across countries, regions, and public/private divides unite around and compete for authority and influence based on common ideas, alongside their own organizational allegiances.

Such a technocratic, expert-dominated setting might well amplify global power dynamics. The interests of major powers continue to define the broader framework of global economic governance, and dominant forms of expertise are themselves connected to state power (Meyer et al., Citation1997). As such, deference to negotiators’ authority is in part related to their states’ standing in the geopolitical context (Roger & Belliethathan, Citation2016). One example is the dominance of ideas formulated among experts from great powers, which can be seen as a form of soft power (Genschel and Rixen 2015). These ideas are structural conditions into which individuals from peripheral states – or those lacking regulatory capacity – are socialised (Checkel, Citation2005; Johnston, Citation2008). Learning and socialization in transnational environments are often expected to shrink the policy space of developing countries, shaping their preferences along Western lines (Broome & Seabrooke, Citation2015). In the global tax domain, expertise is seen as deriving from years of specific experience working with the conceptual, policy, and practical dimensions of the established OECD rules, and is especially powerful when individuals can broker across legal, economic and accounting expertise and professional networks (Christensen Citation2021). Expertise and networks typically accrue from career exposure to elite organisations steeped in Western-derived knowledge, including universities, international organisations and large corporations.

There are, however, at least three dimensions by which regulatory capacity, understood in our sense of socio-technical resources, can give states an institutional power in spite of their limited market size. First, the contents of expertise. While the acquisition of the requisite knowledge by representatives from countries with limited market power carries with it the risk of socialisation – and thus an alignment of policy ideas with representatives from major powers – it can also be liberating. For individuals from developing countries, the development of such technical expertise can allow them to “question their own prior assumptions and those implicit in the knowledge imparted by the international community”, and thus push for alternative policy ideas without singularly internalising existing policy norms (Hearson, Citation2021, 78).

Second, recognition of an individual’s expertise within professional networks. As shown in different dimensions of global governance, the experience, professionalism and socialisation of particular skilled individuals can enable developing countries to attract authority and effectively penetrate technical policymaking in international organisations (Shaffer et al., Citation2008; Lee, Citation2009; Apecu, Citation2013). For instance, being appointed to key WTO negotiating bodies is not merely a function of country representation, but also being recognised as authoritative in an expert community (Apecu, Citation2013). Such network-building is especially powerful where it can draw on legitimacy across both transnational and domestic networks (Diprose, Kurniawan, & Macdonald Citation2019).

Third, strategic relation-building among individuals in a transnational policy community provides the underpinning for more conventionally state-centric coalition-forming activities. Whereas coalitions of states are typically understood to arise from shared state-level interests, they can also develop from expert-level relations. As expert negotiators interact with each other, they co-produce authoritative ideas, which become new ‘focal points’ that act as ‘magnets’ for coalitions (Béland & Cox, Citation2016). In this sense, expert relations in a social environment precede and support the establishment of policy-making influence.

Our research enabled us to study the emergence of these forms of socio-technical resource in micro-detail. We focused on named individuals and specific decisions, observing that for lower-income countries the socio-technical resources of negotiators within a network of social relations determines whether they punch above, at, or below their weight.

The inclusive framework: an experiment in inclusive global governance

The taxation of multinational companies is a predominantly sovereign competence, but it is exercised within a framework of cooperation that exerts a large influence over national laws. At multilateral level there are two core soft law tools. First, the OECD and UN model bilateral tax treaties set the parameters for bilateral negotiations between states, which in turn create hard law tax treaties that divide up the right to tax the proceeds of cross-border economic activity. Second, the OECD Transfer Pricing Guidelines are the dominant framework for determining how multinational enterprises’ taxable profits are attributed among the states in which they operate. The Guidelines are referred to explicitly in the OECD model treaty and many countries use them as the basis of their domestic transfer pricing framework, even if they are not members of the OECD. It can been argued that they constitute customary international law (Avi-Yonah, Citation2007).

For almost a century, international tax institutions – rules and the states that made them – remained surprisingly stable, in spite of an ever-present tension between the interests of the rule-making ‘developed’ countries and rule-taking ‘developing’ countries (Hearson, Citation2021; Jogarajan, Citation2018). Since the turn of the 21st century, however, the OECD’s dominant position has become more precarious. In the wake of the financial crisis its political backing shifted from the G7 to G20, in recognition that major emerging markets’ consent was necessary to maintain its position (Christensen & Hearson, Citation2019; Lesage et al., Citation2019). Non-OECD G20 countries were given ‘associate’ status in the OECD’s Committee on Fiscal Affairs, allowing them to participate on an equal footing with the organisation’s full members (OECD, Citation2014b).Footnote2

In parallel, the OECD’s corporate tax standards faced a crisis of legitimacy as instances of corporate tax avoidance became front page news. Its initial response was the Base Erosion and Profit Shifting (BEPS) project, which sought to reform international tax standards to minimise aggressive tax planning. It was understood primarily as a clash between the US and Europe (Lips, Citation2019; Hakelberg, Citation2020), yet also had a strong undercurrent of conflict between OECD members and ‘rising powers’ (Grinberg, Citation2017; Hearson & Prichard, Citation2018).

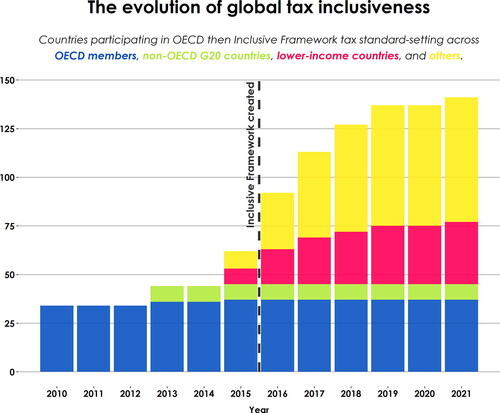

The OECD has increasingly sought to include non-members in its policy-making work as part of its broader agenda of expansion and outreach (Ougaard, Citation2010). In the tax context, this began to materialize with the inclusion of developing countries in OECD deliberations from 2010, through an informal Task Force on Tax and Development. From January 2015, several developing countries were invited to attend standard-setting meetings as observers. OECD literature was optimistic that “[n]ot only will developing countries be able to directly input and gain an improved understanding of the BEPS process, but OECD members and BEPS Associates will also be exposed first-hand to accounts of the specific perspectives of, and challenges faced by, developing countries” (OECD, Citation2014c). This meant that by May 2015, 62 countries were “directly engaged in the development of BEPS measures” (OECD, Citation2015), almost double the number of full OECD members. That same year, the G20 endorsed the OECD’s plan to establish an “inclusive framework” involving developing countries on an “equal footing” (G20 2015). It has steadily expanded, and numbered 141 jurisdictions by the time this article was published.

This expansion is remarkable in its diversity and speed (see below). To make one comparison: in trade governance, developing countries had been signing up to the General Agreement on Trade and Tariffs (GATT) for decades before they reached a critical mass that could challenge the historical core (Michalopoulos, Citation1999). Tax multilateralism thus offers a particularly striking context as an almost overnight experiment in mass integration of developing countries into historically Northern-led global governance.

Figure 1. The evolution of global tax inclusiveness.

Whereas the OECD has proclaimed the Inclusive Framework an unequivocal success, the practical reality is that both formal and effective participation in its standard-setting bodies is highly uneven. Limited participation reflects a lack of conventional regulatory capacity on the part of many developing countries, universally acknowledged by our interviewees. Because negotiations were taking place in Paris, financial constraints limited the number of meetings many negotiators were able to attend; even where they could find the resources, one or two officials would be following the work of multiple committees, usually on top of their domestic responsibilities:

One of the things I noticed is, bigger countries have bigger resources and they have teams dedicated to reading and commenting on the OECD documents. I can tell you first hand, I was sometimes reading a document on the plane, and while I was at the OECD I still had to run my department and do my day job, and try to participate in the meeting. (Interview, emerging market)

The Steering Group, which meets several times a year, is where politically sensitive decisions are usually brokered. It brings together 24 representatives equally split between OECD members and other Inclusive Framework members. Steering group members are nominated by states but participate in a personal capacity. They are formally elected, although the process is heavily steered by the OECD secretariat, which identifies capable and influential individuals while ensuring a geographically and politically balanced representation. The strength of participation here, however, varies significantly. Across our interview sample, comments concerning the effectiveness of Steering Group members from outside the OECD were broadly consistent: some were frequently cited as productive negotiators able to make their mark on discussions, while others were singled out for their erratic attendance or reluctance to speak.

The technical groundwork for negotiations takes place in the Working Parties. These groups are formally open to representatives from all Inclusive Framework members, but typically gather 10-30 experts (Christians, Citation2010). Each Working Party will meet between two and four times per year, with a mandate to focus on specific issues (e.g. tax treaties or transfer pricing rules). Each has an elected chair, co-chair and bureau, who work with the secretariat to steer the standard-setting process. In practice, the Working Parties are dominated by the OECD and G20. As a whole, non-OECD countries represent less than 25% of attendees, despite making up almost 75% of members. If G20 members are also excluded, the remaining countries comprise only 11% of attendees, yet 67% of the membership. This story is more pronounced for the bureaux that steer each Working Party’s decision-making: with the exception of Nigeria, there are no bureau members from outside the OECD and G20.

Case studies on developing country influence on global tax governance

We studied every specific policy case claimed by actors in the stakeholder ecosystem to be evidence of developing country influence, identified through our exploratory interviews and document analysis. These cases cover 2014 to 2019, the period immediately before the creation of the Inclusive Framework, as well as its first four years of existence. Our qualitative analytical process is detailed in Supplementary Materials Annex 1. This article will concentrate on three case studies, brief descriptions of which are given in . As can be seen from the summaries of all seven cases we identified in Supplementary Materials Annex 2, negotiations can be divided into three phases. We have chosen typical cases from each phase that illustrate the development of the key dynamics we identified over time.

Table 1. Illustrative cases discussed in the article.

Each of these cases consists of a proposal to modify international tax standards, in which the preferences of the larger OECD member states ran contrary to those of lower-income countries. The literature suggests several reasons why the latter might prevail despite limited capabilities. First, politicisation constitutes an exogenous influence on the technocratic milieu. Intervention by political principals at G7 and G20 summits, constraints imposed on them by legislatures, or participation by individuals from civil society organisations could all provide lower-income countries with alternative routes to influence over transnational standards. Indeed, much existing literature has been preoccupied with such highly politicised global tax negotiations (Sharman, Citation2006; Lips, Citation2019; Hakelberg, Citation2020; Vaughan, Citation2021). In contrast, these illustrative cases had a low political profile, even if they took place within larger negotiation processes that were politicised. None of our interview evidence points to political interventions shaping the outcomes. A second possible explanation is that negotiators from OECD countries trade concessions in areas that are not important to them while adopting an uncompromising stance on other topics. Yet, as we will describe, in all three of these cases negotiators from developing countries challenged a firmly held, longstanding consensus among their counterparts from larger OECD member states. Finally, large and coherent coalitions of developing countries could amass sufficient combined market power to bring about change (Narlikar, Citation2003; Narlikar & Tussie, Citation2004). While it is true that some larger emerging markets were involved in our cases, the combination of a united OECD and China’s go-it-alone or status quo preference (Christensen & Hearson, Citation2022) means that any developing country coalition will occupy a minority position. We do not discount market power, but our interview evidence firmly supports the view that socio-technical resources also determine negotiating strength at the OECD.

Case study 1: without socio-technical resources, lower-income countries had little impact

Literature from the OECD secretariat and organisations representing developing countries themselves began to make claims of their successful influence over tax standard-setting in 2014. According to the OECD secretariat: “There has already been significant engagement between the OECD/G20 BEPS Project and developing countries which has already shaped the OECD/G20 BEPS agenda” (OECD, Citation2014a). A presentation given by the African Tax Administration Forum (ATAF)’s Research Director in 2015 states that ATAF “has made already significant impact on formulation of the new standards” (Monkam, Citation2015). This narrative aligns with scholarship on global power shifts that emphasises the limited concessions granted by major powers to developing countries due to changes in global market power balances (Hopewell, Citation2015; Seabra & Sanches, Citation2019). Yet, when we examined specific cases during this period, we found that it was only large emerging markets that had any influence over policy outcomes. Lower-income countries, though participants in OECD discussions, did not yet possess the socio-technical resources to influence them.

Our illustrative case here is the “sixth method” for transfer pricing, a type of simplification applied to commodities transactions in the laws of Latin American countries and Zambia. Such approaches use publicly available market prices as a baseline to determine prices of inter-company commodity transactions, which is less open to manipulation by businesses (Grondona, Citation2018). The OECD and ATAF sources quoted above cite the introduction of key sixth method concepts into the OECD’s transfer pricing guidelines as illustrative of the influence of developing countries.

Our interview evidence differs from this prevailing policy narrative, yet is consistent with our argument. From the perspective of lower-income countries, this is not a case of success; that outcome is unsurprising since negotiators from lower-income countries had yet to acquire the socio-technical resources necessary to influence global tax negotiations. According to our interviewees, the effort was led by Latin American emerging market countries that already had the sixth method in their legislation, especially Argentina, with support from other resource-rich emerging markets favourable to simplified transfer pricing methods. “The push mainly came from the BRICS. Those were the countries that really had a lot of say”, said one (lower-income country).

The involvement of lower-income countries came in January 2015. Prior to this, the sixth method had played the role of a bargaining chip in the multidimensional BEPS conflict between OECD members and G20 emerging markets. A discussion draft published in December 2014 suggested an objective of providing “clearer guidance” in response to the “unilateral measures” implemented by the emerging markets, rather than responding to the difficulties lower-income countries faced applying transfer pricing rules to the mining sector (OECD, Citation2014d, 1). In recognition that the proposed solution did not resolve these issues, the discussion draft pointed instead to other work being undertaken by the OECD secretariat and World Bank to “supplement the BEPS work with practical tools to help developing economies make maximum use of quoted prices for commodities” (OECD, Citation2014d, 4). In what Brugger and Engebretsen (Citation2020) describe as an “absorption” response to the sixth method, the OECD’s proposal lacked the simplified nature of its unilateral versions, and was accompanied by bridging statements emphasising consistency with existing rules.

When lower-income countries did arrive in the negotiations, they were not yet capable of shifting the direction of travel. ATAF and three other countries represented on its cross-border taxation committee were among those gaining observer status in OECD tax negotiations from January 2015, and some of them attended the Working Party meetings at which final decisions were taken later that year. These were, however, discussions in which the already weak discussion draft became “very watered down” (interview, OECD country). Staff from the ATAF secretariat stated that they had helped forged the alliance of resource-rich and even submitted draft text, yet other participants in the negotiations attributed any African agency specifically to the South African participant, who had been present in OECD negotiations since 2013.

Unsurprisingly, given our evidence, our pessimistic assessment is reflected in lower-income countries themselves. Interviewees from Africa regard the outcome as largely symbolic, a partial OECD endorsement of a prevalent administrative practice that may strengthen their hand in disputes with taxpayers, but nothing more. Although ATAF has incorporated the OECD sixth method into its Suggested Approach to Transfer Pricing Legislation, it has not filtered through into its members’ tax laws.

Case study 2: African experts work together to achieve narrow yet significant changes

While 2015 marked the beginning of ATAF’s participation in standard-setting at the OECD, in subsequent years its experts grew in stature and begun to work together to achieve specific, targeted objectives. This is clearly illustrated by the decision on the “Authorised OECD Approach” (AOA) in 2018, where ATAF experts’ actions led to specific, yet important, changes to OECD documents.

The AOA, which was first adopted in the 2010 update to the OECD Model Tax Convention, is seen as a shift of taxing rights away from the host countries of multinational investment and towards headquarters countries. It introduces arm’s length transfer pricing into the relationship between a permanent establishment (broadly speaking a branch) and its parent company, potentially reducing the taxable profits declared by the branch and increasing those of the parent. As one interviewee described it, the AOA is almost like religion to many OECD insiders and member states: “[It] almost feels like a missionary, go around to all these African countries and asking them to convert to Christianity, asking them to adopt the Transfer Pricing Guidelines. When you talk about success, the OECD was actually asking everyone to agree with the AOA” (interview, lower-income country).

When the OECD began to develop new guidance on the attribution of profits to permanent establishments in 2016, lower-income countries sought to prevent an endorsement of the AOA. This was significant for African experts and their countries because it would affect their position in bilateral treaty negotiations, where capital exporters would push for inclusion of the AOA. Control over the OECD’s interpretive guidance is also important to lower-income countries because it is often considered authoritative by policy-makers, taxpayers and courts, whether or not their governments have participated in its formulation (Avi-Yonah, Citation2007).

As with the sixth method, the intervention by lower-income countries came towards the end of a process when decisions were supposedly locked in. This time, however, the outcome was widely regarded as a success. After their concerns had been repeatedly overlooked in initial discussions, African delegates took the unusual step of jointly withholding consensus when the working party was on the cusp of reaching agreement. They secured language emphasizing that the guidance did not “extend the application of the ‘Authorised OECD Approach’ to countries that have not adopted that approach in their treaties or domestic legislation” (OECD, Citation2018, 10):

On the day the document was to be passed we raised those issues and the discussion had to be suspended. (…) We were able to listen to the other side and they were able to listen to us and we were able to come back and in the [Transfer Pricing Guidelines] we have, yes the OECD approach, but yes other methods that are also in use across the world. (Interview, lower-income country)

One of the countries that came up to me afterwards was a smaller developed country, and they came up at the end and said they’d raised it originally at a previous WP6, and it was completely rejected, and they didn’t agree with the rejection but they felt they were outnumbered, and they had given up. So they were happy that ATAF had persevered. (Interview, international organisation).

ATAF’s success in the AOA case therefore demonstrates its experts’ newfound influence over decisions, resulting from the development of socio-technical resources: expertise, authority, and networks. Many of our interviewees observed that the African bloc is stronger and more coherent than lower-income countries from other continents. For example:

I think it would be safe to say – and this is not pejorative in any way - that if a more influential developing country or persons from the African continent, their views would naturally hold more sway if decisions are ultimately to be made. And we fully understand that, because you’re looking at a bloc of countries. (Interview, emerging market)

Absent a political coalition, ATAF formed a network of technical officials, who developed a shared agenda through its Cross-Border Taxation Technical Committee (CBT), created in 2015. The CBT meets before key Working Party and Steering Group meetings to formulate a collective position. A handful of its members attend WP6 meetings regularly, speaking with a mandate on behalf of ATAF’s 38 members, and with the confidence that they are not isolated:

I’ve developed relationships with most of the especially African country delegates, and that relationship has continued beyond the conferences we’ve attended. And that helps… in terms of the fact that you know some of the positions of the counterparts, even if they are not present, you are able to speak on issues because you know what other African countries are thinking. (Interview, lower-income country)

Strengthening the relationships outside of the [WP6] meetings was a huge influential factor. I had many times we would have informal discussions, they would say ‘there’s no way we can agree with you in the room, because we have a certain country position, but definitely we understand what you’re saying’. As you get familiar and you forge these personal relationships you get to see how things really are. Also, you get to realise you have to have strong voices at the table. I saw it in my own journey at WP6. I started off being very observant, trying to understand my place in the room. I said to the secretariat, I think WP6 is a very daunting place to be. (Interview, emerging market)

Case study 3: Experts from lower-income countries and emerging markets work together to change the terms of debate

Since late 2018, the Inclusive Framework’s primary focus has been on the tax challenges of digitalisation of the economy, a process that has led to the reallocation of multinational companies’ taxable profits – especially those of high-tech firms – towards countries in which they have most sales, as well as the creation of a new global minimum tax. Our research focused on the early stages of these negotiations, during which a proposal from a group of developing countries was circulated and became a focal point for discussion. While the previous case illustrated a precisely targeted intervention by ATAF that focused on very specific wording in a near-final document, this is an example of a much broader intervention in the early stages of a negotiation that instead changed its terms.

The Significant Economic Presence (SEP) proposal was put forward by the Intergovernmental Group of 24 in Monetary Affairs and Development (G24). It was one of three proposals circulating within the Inclusive Framework at the end of 2018, alongside those from the US and the UK, all of which sought to tackle the issue of assigning taxing rights over multinational enterprises where their presence was predominantly digital rather than physical.Footnote3 The OECD secretariat eventually drafted a “Unified Approach” in an attempt to break a tough negotiating deadlock, and this became the focus of negotiations from late 2019.

The SEP proposal was very widely discussed in international tax policy circles, and the G24 delegates and OECD secretariat officials with whom we spoke agreed that it fundamentally changed the balance and frame of negotiations. The Unified Approach itself was an attempted amalgamation of the three proposals, although it did not include any of the SEP’s major technical components. One of the G24 proposal’s authors described it as “very far away from what I would call a victory for the G24 or developing countries” (interview, emerging market). Yet, this person was among the interviewees who described two enduring impacts of the SEP proposal on subsequent negotiations.

First, the secretariat’s proposal included a component known as ‘Amount B’ which would simplify the application of transfer pricing rules. Due to the complexities of transfer pricing, developing countries had long sought simplification reforms (Brugger & Engebretsen, Citation2020). “Because the international tax rules are becoming so complex, that’s really eroding our possibly of enforcing, just because of a lack of capacity” (interview, emerging market). According to a secretariat staff member involved in the drafting, the importance of Amount B was the precedent it set: “If we do this in one area, it might tell us we can do something similar in other areas – simplified methods of allocation, something that might take us beyond the [arm’s length principle]. (…) It simply would not have been there without developing country influence” (interview, international organisation).

Second, the G24 proposal had a noticeable effect on institutional procedures and norms, signalling the arrival of a new powerful alliance whose interests had to be anticipated (Athanasiou, Citation2019) rather than simply ignored to continue focusing on accommodating major power preferences. As a G24 negotiator expressed it:

The fact that we were able to bring together some of the developing world countries in one single bloc definitely made it worthwhile for the [OECD] secretariat to make sure that we were also on board before putting forward some of the decisions, or at least knowing some of what the issues would be…So I think one of the victories is that you know get these calls, you get these papers [ahead of time]. (Interview, emerging market)

It has been very helpful that they can go to the [steering group] meetings representing their countries, but they know that there are shared views there. That matters a lot. They come in stronger, to some degree…Because they had a collective view, that was what got some of the views into the discussion. (Interview, international organisation)

This would not have made the [G24] ministerial meeting or our communiqué if India hadn’t been the chair [but] no one in the group thinks this is an India proposal, that this is really India. (Interview international organisation)

I cannot lay claim to any personal idea, what I can say is that we agree with the concept, we understand the concept even though it is difficult for people from the developed world to accept, we see it as simpler and a lot easier to implement…SEP the principle, the idea is from the G24 and there are contributions from everyone. (Interview, lower-income country)

The real thing in our process is, who gets to shape the papers when we start the papers….[In one typical example, after the secretariat had an idea] the first three phone calls we made were US, India, Nigeria. The US are technically always good, they provide the very best people. But [the Indian and Nigerian delegates] because they’re smart. You can have a real conversation there. That’s where you have the influence. (Interview, international organisation)

Conclusion

Not all power in global governance stems from market size. In this article, we showed that lower-income countries can draw on socio-technical resources – expertise and professional networks – to influence deeply technical transnational policy-making processes, even those dominated by states with large market power. We make these arguments drawing on extensive interviews with negotiators and key stakeholders in global tax policy-making, as well as records of meeting attendance and policy documents. This allows us to provide the first detailed account of global tax decision-making processes in the OECD Inclusive Framework.

Our findings give rise to a series of contributions that challenge or extend existing literature. To begin with, we bring to light an underexplored institutional source of influence available to countries with limited market power: socio-technical resources. The notion of regulatory capacity usefully operationalizes the ability of states to achieve global political influence through expertise, expert coherence, and sanction authority (Bach & Newman, Citation2007). It has primarily been conceptualized in the context of emerging markets as a source of ‘unfulfilled’ market power, and focuses unduly on ‘objective’ measures of expertise at the organisational level. Bringing in insights from “politics of expertise” scholarship, we shifted the focus onto “socio-technical resources”, the expertise and professional networks that together attract deference to key policy claims and enable the mobilization of effective state interests and coalitions. Competition for claims to authoritative expertise are relational and contextual, rather than objectively defined by national hierarchies alone. Studying this competition helps us understand how marginalised actors exploit the “gaps and soft spots” (Waylen, Citation2021) of global governance to influence policy. Moreover, these dynamics are particularly central to highly technical, depoliticised transnational policy processes: whereas prior scholarship has emphasized how depoliticization can make it harder for lesser powers to resist coercion from great powers (Emmenegger & Eggenberger, Citation2018), our study suggests that depoliticized contexts can also enable lesser powers to exercise influence.

In this context, we also contribute to work on expertise in global governance by arguing that expert-based influence is not exclusive to individuals with socio-technical resources derived from or aligned with Western institutions and norms. The expertise foundations of regulatory capacity are conventionally viewed as arising from higher education at elite Western universities, employment at key (international) bureaucracies, or experience from (Western) private sector networks. This perception means that when lower-income country experts develop expertise and experience with global economic policies, it is often understood as constraining their policy space (Broome & Seabrooke, Citation2015). In contrast, our cases demonstrated that technical expertise and expert relations applied by, amongst and for developing countries themselves can be powerful resources in global negotiations.

Next, we offer a counterpoint to scholarship rightly arguing that a better understanding of global governance requires studying a broader range of countries and power sources (Braveboy-Wagner, Citation2010; Hopewell, Citation2015; de Graaff et al., Citation2020). While much of this work has shifted attention from the traditional Great Powers towards emerging markets, it still casts lower-income countries as rule-takers, their agency framed as minimal or insignificant due to their lacking market power and seen only in relation to the more powerful states that they support in coalitions or attempt to resist. There are, however, serious questions about whether the rise of emerging markets is really a vehicle for mobilizing lower-income country interests in global policymaking: often their interests diverge, illustrating the dangers of a conceptual lens that bundles categories of the non-Western core together (Hearson & Prichard, Citation2018; Seabra & Sanches, Citation2019). Our first case on the sixth method is illustrative, since it was instigated by emerging markets with limited influence by - and little use for - lower-income countries. Moreover, a focus on emerging markets misses a more diverse view of the specific capabilities and power sources lower-income countries are able to exercise (cf. e.g. Lee, Citation2009; Apecu, Citation2013). As our second and third cases demonstrate, socio-technical resources are a prerequisite, but the route through which they lead to influence may depend on the origins and composition of coalitions that lower-income countries are able to form, and the market power they can bring to bear.

Our cases also illustrate how new focal points, key policy decisions around which states and experts coalesce, provide lower-income countries with distinct opportunities to organise. As we show, socio-technical resources can precede and enable effective coalition-work, even absent high-level political investment. The second case, on the “Authorised OECD Approach”, illustrates this clearly: African countries coalesced around firmly established domestic policies through a network of like-minded technical experts with limited political support behind them. Moreover, in our third case, SEP was a new idea that emerged in response to policy entrepreneurship by the US and UK. For the newly-formed G24 tax working group, there can be little doubt that the SEP proposal acted as a ‘coalition magnet’ that consolidated a new social group (Béland & Cox, Citation2016).

While ours was not explicitly an historical institutionalist study, it does illustrate what is missed by the prevalent analytical focus on the stabilities of market power structures, interrupted only occasionally by radical ‘shocks’ such as the rise of emerging markets (Streeck & Thelen, Citation2005; Paul, Citation2018). None of our cases were policy earthquakes, but they are significant wins because they depart from the historically dominant dynamics of global tax policy-making, because they are “path-undermining”, and because they constitute layered changes that promote the potential for systemic re-alignment. Thus, they demonstrate how lower-income countries can achieve narrow, incremental changes that are nonetheless significant to both their national interests and to global governance institutions at large.

Finally, these findings beg the question of what this means for the broader power hierarchies in global (tax) governance. While major Western and ‘Rising’ powers continue to define the broader framework in which global economic reforms take place, we show that lower-income countries can exercise influence in specific areas that matter to them by mobilising institutional rather than compulsory power (Barnett & Duvall, Citation2005). This goes for both substantive policy and its diffusion (case study 2) and the process of standard-setting (case study 3). Moreover, this is indicative of a future direction of travel. As the OECD Inclusive Framework finalises one major reform project, its secretariat is already developing a new project that specifically takes developing country interests into account. Its Secretary-General’s report to the G-20 in October 2021 states its intention to “help the G20 consolidate progress by checking that the Inclusive Framework’s strong coalition of countries continues to advance together and converge on the design and implementation of the global tax rules by paying particular attention to the needs of lower income/lower capacity countries in the Inclusive Framework” (OECD 2021).

Supplemental Material

Download PDF (220.8 KB)Acknowledgements

We thank Aleix Montana and Katharina Kuhn for their valuable research assistance, the staff of the Global Relations and Development Division of the OECD Centre for Tax Policy and Administration for sharing attendance data and providing comments on the project throughout, our colleagues at the International Centre for Tax and Development, three anonymous reviewers, and the Review of International Political Economy editorial team.

Disclosure statement

No potential conflict of interest was reported by the authors. This work was supported by UK Aid under grant number 300211-101 and the Bill & Melinda Gates Foundation under grant number OPP1197757.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Notes on contributors

Martin Hearson

Dr Martin Hearson is a Research Fellow at the Institute of Development Studies at the University of Sussex, and a Research Director of the International Centre for Tax and Development. He is the author of “Imposing Standards: The North-South Dimension to Global Tax Politics,” published by Cornell University Press.

Rasmus Corlin Christensen

Dr Rasmus Corlin Christensen is a Postdoctoral Researcher at the Department of Organisation, Copenhagen Business School, and a Research Associate at the International Centre for Tax and Development.

Tovony Randriamanalina

Dr Tovony Randriamanalina is an independent researcher who studies the appropriateness of transfer pricing rules in the case of developing countries. She has a PhD in International Tax Law from the University of Paris-Dauphine. Prior to academic work, Tovony was a Tax Official at the Malagasy Revenue Authority, and is a graduate of the National School of Administration of Madagascar.

Notes

1 We use the term “lower-income countries” to distinguish smaller economies from large emerging markets, while “developing countries” will be an umbrella term for both.

2 As OECD accession states, Colombia and Latvia also had associate status

3 SEP proposed that a company would have a taxable nexus in a country in the absence of a physical presence if a critical mass of certain factors were present, including the revenue from sales of goods and services effected through digital means, the user base and the associated data input, and the volume of digital content. Profits would be allocated to that country on a formulary basis using four factors: sales, assets, employees and users.

References

- Apecu, J. (2013). The level of African engagement at the World Trade Organization from 1995 to 2010. Revue Internationale de Politique de Développement, (4.2), 29–67. no. 4.2 (May). Institut de hautes études internationales et du développement: https://doi.org/10.4000/poldev.1492

- ATAF. (2019). The place of Africa in the shift towards global tax governance: Can the taxation of the digitalised economy be an opportunity for more inclusiveness? African Tax Administration Forum.

- Athanasiou, A. (2019). “Developing Countries Key to Digital Tax Consensus.” Tax Notes International, May 20. https://www.taxnotes.com/tax-notes-international/digital-economy/developing-countries-key-digital-tax-consensus/2019/05/20/29h74?highlight=%22user%20participation%22.

- Avi-Yonah, R. S. (2007). International tax as international law. Cambridge University Press.

- Aydin, U. (2021). Rule-takers, rule-makers, or rule-promoters? Turkey and Mexico’s role as rising middle powers in global economic governance. Regulation & Governance, 15(3), 544–560. https://doi.org/10.1111/rego.12269

- Bach, D., & Newman, A. L. (2007). The European regulatory state and global public policy: Micro-institutions, macro-influence. Journal of European Public Policy, 14 (6), 827–846. https://doi.org/10.1080/13501760701497659

- Bach, D., & Newman, A. L. (2010). Governing lipitor and lipstick: Capacity, sequencing, and power in international pharmaceutical and cosmetics regulation. Review of International Political Economy, 17(4), 665-695. https://doi.org/10.1080/09692291003723706

- Ban, C., & Blyth, M. (2013). The BRICs and the Washington consensus: An introduction. Review of International Political Economy, 20(2), 241–255. https://doi.org/10.1080/09692290.2013.779374

- Ban, C., Seabrooke, L., & Freitas, S. (2016). Grey matter in shadow banking: International organizations and expert strategies in global financial governance. Review of International Political Economy, 23(6), 1001–1033. https://doi.org/10.1080/09692290.2016.15599

- Barnett, M., & Duvall, R. (2005). Power in international politics. International Organization, 59(1), 39–75. https://doi.org/10.1017/S0020818305050010

- Beeson, M., & Bell, S. (2009). The G-20 and international economic governance: Hegemony, collectivism, or both? Global Governance: A Review of Multilateralism and International Organizations, 15(1), 67–86. https://doi.org/10.1163/19426720-01501005

- Béland, D., & Cox, R. H. (2016). Ideas as coalition magnets: Coalition building, policy entrepreneurs, and power relations. Journal of European Public Policy, 23(3), 428–445. https://doi.org/10.1080/13501763.2015.1115533

- Bishop, M. L. (2012). The political economy of small states: Enduring vulnerability? Review of International Political Economy, 19(5), 942–960. https://doi.org/10.1080/09692290.2011.635118

- Braveboy-Wagner, J. (2010). Opportunities and limitations of the exercise of foreign policy power by a very small state: The case of Trinidad and Tobago. Cambridge Review of International Affairs, 23(3), 407–427. https://doi.org/10.1080/09557571.2010.484049

- Broome, A., & Seabrooke, L. (2015). Shaping policy curves: Cognitive authority in transnational capacity building. Public Administration, 93(4), 956–972. https://doi.org/10.1111/padm.12179

- Brugger, F., & Engebretsen, R. (2020). Defenders of the status quo: Making sense of the international discourse on transfer pricing methodologies. Review of International Political Economy, 29(1), 307–335. https://doi.org/10.1080/09692290.2020.1807386

- Büthe, T., & Mattli, W. (2011). The new global rulers: The privatization of regulation in the world economy. Princeton University Press.

- Checkel, J. T. (2005). International institutions and socialization in Europe: Introduction and framework. International Organization, 59(4), 801–826. https://doi.org/10.1017/S0020818305050289

- Chipaike, R., & Knowledge, M. H. (2018). The question of African agency in international relations. Cogent Social Sciences, 4(1), 1487257. Edited by Meissner Richard. https://doi.org/10.1080/23311886.2018

- Christensen, R. C. (2021). Elite professionals in transnational tax governance. Global Networks, 21(2), 265–293. https://doi.org/10.1111/glob.12269

- Christensen, R. C., & Hearson, M. (2019). The new politics of global tax governance: Taking stock a decade after the financial crisis. Review of International Political Economy, 26(5), 1068–1088. https://doi.org/10.1080/09692290.2019.1625802

- Christensen, R. C., & Hearson, M. (2022). The rise of China and contestation in global tax governance. Asia Pacific Business Review, 28(2), 165-186. https://doi.org/10.1080/13602381.2022.2012992

- Christians, A. (2010). “Networks, Norms and National Tax Policy.” Wash. U. Global Studies Law Review. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1358611.

- Christians, A., & van Apeldoorn, L. (2018). The OECD inclusive framework. Bulletin for International Taxation, 2018(4/5), 226–233. https://doi.org/10.2139/ssrn.3393140

- Crasnic, L. (2020). Resistance in tax and transparency standards: Small states’ heterogenous responses to new regulations. Review of International Political Economy, 22(1), 255-280. https://doi.org/10.1080/09692290.2020.1800504

- de Graaff, N., ten Brink, T., & Parmar, I. (2020). China’s rise in a liberal world order in transition – introduction to the FORUM. Review of International Political Economy, 27(2), 191–207. https://doi.org/10.1080/09692290.2019.1709880

- Dickinson, B. (2019). “The inclusive framework is considering radical proposals, but in the real world…” The International Centre for Tax and Development (ICTD). https://www.ictd.ac/blog/oecd-inclusive-framework-tax-proposals-negotiation/.

- Diprose, R., Kurniawan, N. I., & Macdonald, K. (2019). Transnational policy influence and the politics of legitimation. Governance, 32(2), 223–240. https://doi.org/10.1111/gove.12370

- Emmenegger, P., & Eggenberger, K. (2018). State sovereignty, economic interdependence and US extraterritoriality: The demise of Swiss banking secrecy and the re-embedding of international finance. Journal of International Relations and Development, 21 (3), 798–823. https://doi.org/10.1057/s41268-017-0088-y

- Eskelinen, T., & Ylönen, M. (2017). Panama and the WTO: New constitutionalism of trade policy and global tax governance. Review of International Political Economy, 24(4), 629. https://doi.org/10.1080/09692290.2017.1321569

- G20. (2015). “G20 Leaders Communiqué, Antalya.” http://www.g20.utoronto.ca/2015/151116-communique.html.

- Genschel, P., & Rixen, T. (2015). Settling and unsettling the transnational legal order. In T. C. Halliday, & G. Shaffer (Eds.), Transnational legal orders (pp. 154–186). Cambridge Studies in Law and Society. Cambridge University Press. https://books.google.co.uk/books?id=wWa8BQAAQBAJ.

- Gilardi, F. (2002). Policy credibility and delegation to independent regulatory agencies: A comparative empirical analysis. Journal of European Public Policy, 9(6), 873–893. https://doi.org/10.1080/1350176022000046409

- Grinberg, I. (2016). The new international tax diplomacy, Georgetown Law Journal 104(5), 1137-1196.

- Grondona, V. (2018). Transfer pricing: Concepts and practices of the ‘sixth method’ in transfer pricing. Tax Cooperation Policy Brief 2. South Centre.

- Hakelberg, L. (2020). The hypocritical hegemon: How the United States shapes global rules against tax evasion and avoidance. Cornell University Press.

- Hearson, M. (2021). Imposing standards: The north-south dimension to global tax politics. Cornell University Press.

- Hearson, M., & Prichard, W. (2018). China’s challenge to international tax rules and the implications for global economic governance. International Affairs, 94(6), 1287–1307. https://doi.org/10.1093/ia/iiy189

- Helgadóttir, O. (2016). Banking Upside down: The Implicit Politics of Shadow Banking Expertise. Review of International Political Economy, 23(6), 915–926. https://doi.org/10.1080/09692290.2016.1224196

- Hopewell, K. (2015). Different paths to power: The rise of Brazil, India and China at the World Trade Organization. Review of International Political Economy, 22(2), 311–338. https://doi.org/10.1080/09692290.2014.927387

- Ingebritsen, C., Neumann, I., & Gsthl, S. (2012). Small states in international relations. University of Washington Press.

- Jogarajan, S. (2018). Double taxation and the league of nations. Cambridge Tax Law Series. Cambridge University Press.

- Johnston, A. I. (2008). Social states: China in International Institutions, 1980-2000. Princeton University Press.

- Knaack, P., & Gruin, J. (2021). From shadow banking to digital financial inclusion: China’s rise and the politics of epistemic contestation within the financial stability board. Review of International Political Economy, 28(6), 1582. https://doi.org/10.1080/09692290.2020.17749

- Kranke, M. (2020). Exclusive expertise: The boundary Work of International Organizations. Review of International Political Economy, 0(0), 1–24. https://doi.org/10.1080/09692290.2020.1784774

- Krisch, N. (2017). Liquid authority in global governance. International Theory, 9(2), 237–260. https://doi.org/10.1017/S1752971916000269

- Lazega, E. (1992). Micropolitics of knowledge: Communication and indirect control in workgroups. Aldine de Gruyter.

- Lee, D. (2009). Bringing an elephant into the room: Small African state diplomacy in the WTO. In Andrew F. Cooper, & Timothy M. Shaw (Eds.), The diplomacies of small states: Between vulnerability and resilience, 195–206. International Political Economy Series. Palgrave Macmillan UK. https://doi.org/10.1057/9780230246911

- Lesage, D., Lips, W., & Vermeiren, M. (2019). The BRICs and International Tax Governance: The case of automatic exchange of information. New Political Economy, March. https://doi.org/10.1080/13563467.2019.1584168.

- Lips, W. (2019). Great powers in global tax governance: A comparison of the US Role in the CRS and BEPS. Globalizations, 16(1), 104–116. https://doi.org/10.1080/14747731.2018.1496558

- Meyer, J. W., Boli, J., Thomas, G. M., & Ramirez, F. O. (1997). World society and the nation‐state. American Journal of Sociology, 103(1), 144–181. https://doi.org/10.1086/231174

- Michalopoulos, C. (1999). The developing countries in the WTO. The World Economy, 22(1), 117–143. https://doi.org/10.1111/1467-9701.00195

- Monkam, N. (2015). Cross border taxation in Africa: Challenges and Africa’s response. Presented at the The Politics of Fighting Tax Avoidance and Tax Evasion, German Development Institute (DIE). June 23.

- Mutava, C. N. (2019). Review of Tax Treaty Practices and Policy Framework in Africa. International Centre for Tax and Development Working Papers 102. Institute of Development Studies.

- Narlikar, A. (2003). International trade and developing countries: Bargaining coalitions in the GATT & WTO. Taylor & Francis.

- Narlikar, A., & Tussie, D. (2004). The G20 at the Cancun ministerial: Developing countries and their evolving coalitions in the WTO. World Economy, 27(7), 947–966. https://doi.org/10.1111/j.1467-9701.2004.00636.x

- Newman, A. L., & Posner, E. (2015). Putting the EU in its place: Policy strategies and the global regulatory context. Journal of European Public Policy, 22(9), 1316–1335. https://doi.org/10.1080/13501763.2015.1046901

- OECD. (2014a). Two-part report to G20 development working group on the impact of BEPS in low income countries. OECD. https://www.g20.org/sites/default/files/g20_resources/library/1OECD Report to the G20 DWG on the impact of base erosion and https://profit shifting in low income countries.PDF.

- OECD. (2014b). OECD Secretary-General Report to the G20 Leaders. http://www.g20.utoronto.ca/2014/OECD_secretary-generals_report_tax_matters.pdf.

- OECD. (2014c). The BEPS project and developing countries: From consultation to participation. https://www.oecd.org/ctp/strategy-deepening-developing-country-engagement.pdf.

- OECD. (2014d). BEPS Action 10: Discussion draft on the transfer pricing aspcts of cross-border commodity transactions. OECD Publishing.

- OECD. (2015). Meeting of the Ministerial Council, 3-4 (June 2015). https://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=C/MIN(2015)8&docLanguage=En

- OECD. (2017). Model tax convention on income and on capital (Condensed Version). OECD Publishing.

- OECD. (2018). Additional guidance on the attribution of profits to permanent establishments, BEPS Action 7. OECD Publishing.

- OECD. (2021). OECD Secretary-General Tax Report to G20 Finance Ministers and Central Bank Governors (Italy, October 2021).

- Ougaard, M. (2010). The OECD’s global role: Agenda-setting and policy diffusion. Mechanisms of OECD Governance: International Incentives for National Policy-Making? (26–49). Oxford University Press. https://doi.org/10.1093/acprof:oso/9780199591145.003.0002

- Palan, R. (2003). The offshore world: Sovereign markets, virtual places, and nomad millionaires. Cornell University Press.

- Panda, J. P. (2017). Institutionalizing the African reach: Reviewing China’s and India’s multilateral drives. Journal of Asian and African Studies, 52(6), 853–872. https://doi.org/10.1177/0021909615622348

- Paul, T. V. (2018). Assessing change in world politics. International Studies Review, 20(2), 177–185. https://doi.org/10.1093/isr/viy037

- Picciotto, S. (2015). Indeterminacy, complexity, technocracy and the reform of international corporate taxation. Social & Legal Studies, 24(2), 165–184. https://doi.org/10.1177/0964663915572942

- Quack, S. (2016). Organizing counter-expertise: Critical professional communities in transnational governance. In Andreas Werr & Staffan Furusten (Eds.), The organization of the expert society. Taylor & Francis.

- Rixen, T. (2008). The political economy of international tax governance. Palgrave Macmillan.

- Rixen, T., & Viola, L. A. (2016). Historical institutionalism and international relations (pp. 3–34), edited by Thomas Rixen, Lora Anne Viola, & Michael Zürn. Oxford University Press. https://doi.org/10.1093/acprof:oso/9780198779629.003.0001

- Roger, C., & Belliethathan, S. (2016). Africa in the global climate change negotiations. International Environmental Agreements: Politics, Law and Economics, 16(1), 91–108. https://doi.org/10.1007/s10784-014-9244-7

- Scott, J. C. (1992). Domination and the arts of resistance: Hidden transcripts. Revised ed. Edition. Yale University Press.

- Seabra, P., & Sanches, E. R. (2019). South–South cohesiveness versus South–South Rhetoric: Brazil and Africa at the UN general assembly. International Politics, 56(5), 585–604. https://doi.org/10.1057/s41311-018-0170-0

- Seabrooke, L. (2014). Epistemic arbitrage: Transnational professional knowledge in action. Journal of Professions and Organization, 1(1), 49–64. https://doi.org/10.1093/jpo/jot005

- Seabrooke, L., & Wigan, D. (2016). Powering ideas through expertise: Professionals in global tax battles. Journal of European Public Policy, 23(3), 357–374. https://doi.org/10.1080/13501763.2015.1115536

- Sending, O. J. (2015). The politics of expertise. University of Michigan Press. https://www.press.umich.edu/4016693/politics_of_expertise.

- Shaffer, G., Sanchez, M. R., & Rosenberg, B. (2008). The trials of winning at the WTO: What lies behind Brazil’s success. Cornell International Law Journal, 41, 383.

- Sharman, J. C. (2006). Havens in a storm: The struggle for global tax regulation (1st ed.). Cornell University Press.

- Sinha, A. (2018). Building a theory of change in international relations: Pathways of disruptive and incremental change in world politics. International Studies Review, 20(2), 195–203. https://doi.org/10.1093/isr/viy031

- Stone, D. (2013). Shades of grey’: The World Bank, knowledge networks and linked ecologies of academic engagement. Global Networks, 13(2), 241–260. https://doi.org/10.1111/glob.12007

- Streeck, W., & Thelen, K. A. (Eds.). (2005). Beyond continuity: Institutional change in advanced political economies. Oxford University Press.

- Susan, B.-L., & Halliday, T. C. (2017). Global lawmakers: International organizations in the crafting of world markets. Cambridge University Press.

- Taylor, I. (2010). The international relations of Sub-Saharan Africa. Bloomsbury Publishing USA.

- Vaughan, M. (2021). Field heteronomy and contingent expertise: The case of international tax justice. International Political Sociology, September. https://doi.org/10.1093/ips/olab027

- Vickers, B. (2013). Africa and the rising powers: Bargaining for the ‘marginalized many. International Affairs, 89(3), 673–693. https://doi.org/10.1111/1468-2346.12039

- Wade, R. H. (2011). Emerging world order? From multipolarity to multilateralism in the G20, the World Bank, and the IMF. Politics & Society, 39(3), 347–378. https://doi.org/10.1177/0032329211415503

- Waylen, G. (2021). Gendering global economic governance after the global financial crisis. Review of International Political Economy, 1–22. https://doi.org/10.1080/09692290.2021.1888142

- Woods, N. (2010). Global governance after the financial crisis: A new multilateralism or the last gasp of the great powers? Global Policy, 1(1), 51–63. https://doi.org/10.1111/j.1758-5899.2009.0013.x

- Zagzebski, L. T. (2013). Epistemic authority a theory of trust, authority, and autonomy in belief. Oxford University Press.