ABSTRACT

This article describes how Sweden developed a hybrid defence-industrial infrastructure with three prioritized ‘essential strategic interests’ pointing to parts of the domestic defence industry: ‘a partial strategic autonomy’. The article focuses on Sweden’s declared three essential security interests – combat aircraft capability; underwater capabilities; and integrity-critical parts of the command, control, communication and intelligence domain (C3I). The article finds that the possibilities and ways forward for the essential security interests vary, with a general trend towards more shared and increasingly partial autonomy. Six change factors are formulated as drivers towards Sweden’s partial strategic autonomy of today: Autonomy as a result of failed internationalization; Techno-nationalist perception of Sweden leading to industrial protectionism; Strategic choice; Corporate lobbying; Export incentives leading to political support of technologies; and Europeanization of the EU defence industry. Techno-nationalism and strategic choice are the factors with the most evident impact. The overall governance of the defence industry is clear on the priority of ensuring security of supply and a high degree of autonomy regarding the three essential security interests. Other parts of the defence industry operate under globalized and more competitive conditions. In order to apply increased economic rationality and strive for shared autonomy, Sweden must increase its engagement in multilateral arms collaboration.

Introduction

To an outside observer Sweden’s defence industry and materiel procurement policy may seem like oddities. With its Armed Forces consisting of roughly 51,000 personnel, including the Home Guard, and military expenditure amounting for about 1.3 percent of GDP, Sweden could hardly be described as a military powerhouse. Nevertheless, Sweden is home to one of Europe’s most sophisticated defence industries with one of the world’s highest arms exports per capita. Furthermore, Sweden is the only country in Europe, besides France, which designs and produces its own combat aircraft, and only one of four Western European countries which designs and produces its own conventional submarines.Footnote1

However, Sweden does not have the same level of self-sufficiency or autonomy as it did during the Cold War – several vital systems are currently being imported and even in areas where Sweden does develop its own equipment, the defence industry relies on foreign suppliers and partners for several key components and technologies. This article outlines the development of the Swedish defence industry, from comprehensive strategic autonomy during the Cold War to what can be described at present as a hybrid model of governance resulting in a partial strategic autonomy.

Focusing on the essential security interests (ESI) of combat aircraft capability, the underwater domain and C3I capabilities, the article asks what partial autonomy means for a small country like Sweden with an advanced, but internationally interdependent, defence industry. The article’s theoretical framework draws on the work of Bitzinger (Citation2015) which classifies defence industries in a pyramid according to their level of capacity and autonomy, in which Sweden is identified as a country with an advanced, but niched defence industry. This article suggests that the description of partial strategic autonomy might be more suitable to describe Sweden’s position. Nevertheless, this ‘pyramid of autonomy’ forms the framework for the discussion of whether or not the Swedish defence industry can maintain and develop its current level of partial autonomy.

The purpose of this article is to describe the present Swedish defence-industrial landscape and analyze what change factors that through actions, policies, strategies and priorities from government and industry have led to its present structure. The article’s conclusions discusses challenges for the future development of the Swedish defence industry with a focus on the parts of the defence industry defined as being covered by the three essential strategic interests. This article strives to find what driving forces – internal or external, implicit or explicit – can be seen as explanations for the development leading to Sweden’s present characteristics for self-sufficiency of arms.

Sweden’s policy for self-sufficiency in arms was gradually developed after World War II. Somewhere around the late 1970s Sweden’s most comprehensive defence-industrial and defence-development infrastructure was attained. This level was largely upheld until the sudden implosion of the Soviet Union and the end of the Cold War. Around 40 years after its peak, Sweden now has a very different domestic infrastructure for developing defence technology. The factors that have shaped this development can be summarized under the following six change factors (CF):

CF1 Autonomy as a result of failed internationalization

CF2 Techno-nationalist perception of Sweden leading to industrial protectionism

CF3 Strategic choice

CF4 Corporate lobbying

CF5 Export incentives leading to political support of technologies

CF6 Europeanization of the EU defence industry

The change factors will be discussed below in more detail under ‘Discussion of change factors’.

Theoretical Framework

The development of the Swedish defence industry and production of defence technology has been the subject of several previous studies. Britz (Citation2004) discussed how Sweden’s defence-industrial policies were being integrated into the wider EU context. Andersson (Citation2007) stated that the Swedish military’s role had changed from primarily having a role for national defence into becoming a contributor to international peace-keeping. Ikegami (Citation2013) put forward that the Swedish defence industry had become so reliant on export that it had become increasingly irrelevant to Swedish defence needs. This in turn was suggested to lead to an erosion of Swedish military capabilities and readiness. DeVore (Citation2015) described how the Swedish defence industry covered many types of defence systems until the 1980s and then gradually became specialized as niche actors in successful segments, driven by established products requiring incremental innovation, whereas new products would require radical innovation. Lundmark (Citation2019)described how Sweden’s defence posture and capabilities prioritisation radically changed around 2014 following Russia’s increasingly aggressive posture, the annexation of Crimea and the invasion of Eastern Ukraine in 2014. Olsson (Citation2019b)discussed the challenges and possibilities currently facing Sweden with regard to increasing equipment costs, decreasing equipment volumes and problems with the current materiel supply strategy and the need for long-term planning.

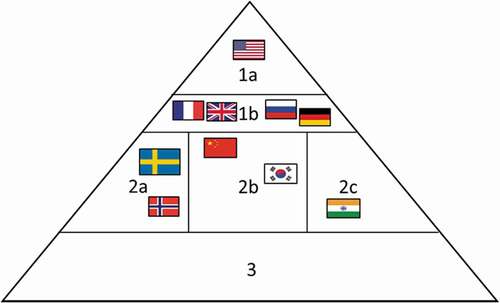

[. Sweden’s defence industrial position as a Tier 2a-country.]Footnote2

Figure 1. Sweden’s defence industrial position as a Tier 2a-country.

Bitzinger (Citation2015) discusses how nations can position themselves as arms producing nations based on their degree of specialisation and degree of autonomy in arms supply. Nations are classified according to defence industrial capabilities in a pyramid-shaped figure, see . In this pyramid Sweden is categorised as a Tier 2a-country: ‘Smaller, niche-oriented, technologically advanced defence industrial bases’. The question is, what defence systems and platforms does Sweden specialize in, what has led to this and why?

Defence materiel consists of different product categories, e.g. surface combatants, combat aircraft, helicopters, armoured vehicles, missiles, and command and control systems. Within each category there are several types of systems, e.g. corvettes, multirole fighters, search and rescue helicopters, infantry fighting vehicles, surface-to-air missiles, and radars. Each such type can in turn be specific products or niches, e.g. short range surface-to-air missiles and artillery radar. While the Swedish defence industry does not cover entire product categories, it develops and produces types of systems or specific products. Since the word niche could easily be interpreted to mean industrial capabilities in specific narrow fields of excellence, Sweden is instead described here as having a partial strategic autonomy regarding its defence industrial capability. Autonomy is not a binary condition but rather a spectrum of choices, reflecting favourable and unfavourable dependencies.Footnote3 There are concepts related to autonomy, e.g. autarky, sovereignty, self-sufficiency and dependence. Autarky can be defined as ‘national economic independence or self-sufficiency’. Meanwhile, sovereignty implies independence from anybody outside the nation, and ‘defence autarky’ implies that a state is able to produce all its defence needs domestically.Footnote4 Partial autonomy relates to Bitzinger’s concept of ‘limited autarky’,Footnote5 but partial autonomy connects more directly to what is regarded as essential to national security.

Presently there is an ongoing debate regarding ‘strategic autonomy’ in Europe, often linked to the EU military capability coupled with the defence-industrial capacities within the EU. This debate brings together challenges of the dependency on the US; the interrelationship between membership of the EU versus membership of NATO and the challenging obligations and goals of each organization; security of supply; intra-EU military capability burden-sharing issues; and also aspects of employment within the EU.Footnote6 The debate concerning the EU’s degree of autonomy in military capacity has been ongoing for decades.Footnote7 An underlying driver for improving a European strategic autonomy is the marked dominance of the US regarding defence technology. When European states buy US defence systems, there are considerable limitations for the use and maintenance of these systems. The US ITAR system restricts the use of defence systems with US subsystems, which creates a dependence on US approval. The most prevalent example is US missiles that buyers cannot modernize in any way.

A Historical Overview – from Comprehensive Self-sufficiency to Partial Strategic Autonomy

Sweden pursued an active policy of neutrality during both world wars. In order to support this neutrality, Sweden gradually began to develop a broad-based domestic defence industry during World War II, and this policy was upheld after World War II. Development and production included surface ships and submarines (produced by Karlskronavarvet, later Kockums), artillery and later missiles (Bofors), as well as indigenous fighters and combat aircraft, together with radar, communication systems and several other types of military materiel (Saab).Footnote8

During the Cold War the Swedish government supported close interaction between the defence industry, industrialists (especially the Wallenberg family), certain state-owned companies, the procurement organisation, the Armed Forces, academia and certain non-military companies. From this period in time, a strongly institutionalised and trust-based ‘military-industrial complex’ was created. Karlsson (Citation2015) describes that from 1946 to 1992 there was a stable political consensus about having a Swedish defence industry. There was also consensus that the defence industry was to be technically sophisticated, modern and cost-efficient. Up until the late 1960s there was also a highly stable corporate landscape and course of development. At this time, due to less ambitious development of Swedish defence systems, the defence industry strove for increased exports, civil production and more collaboration between companies.Footnote9

At the same time, Sweden had for several decades had strong support from the US, which transferred certain crucial technologies and equipment, such as jet engines and avionics systems to the military aircraft industry. Also, since the 1950s, there was a non-disclosed, close security and defence technology collaboration between the US and Sweden. Sweden received advanced aeronautics, avionics and jet propulsion from the US. Sweden was highly self-reliant, but depended on the US for certain missiles and critical technologies for combat aircraft.Footnote10

Sweden was at the height of its national defence technology development capacity by the mid-1980s. Sweden was by then largely autonomous within a broad spectrum of defence technology expertise and arms development. It produced its own combat aircraft, surface combatants, submarines, armoured vehicles, artillery, radars, ground combat weapons, ammunition and C3I solutions. The Swedish defence industry had developed what was arguably the world’s most advanced data-link for its Air Force, it was in the global forefront of developing a fly-by-wire combat aircraft.Footnote11

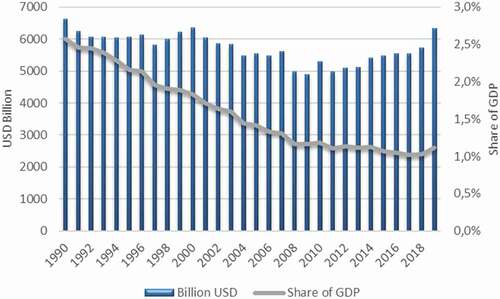

After the end of the Cold War, Sweden suddenly had no clear security threat. What followed was a long period of unclear threat perception and considerable downsizing of the Armed Forces’ infrastructure, equipment, personnel and logistics, while overall readiness levels fell. During the 1990s Swedish military expenditure stagnated, see . Meanwhile, military spending as a share of GDP dropped, from about 2.5 percent in 1990 to 1.8 percent in 2000.

Figure 2. Swedish Military Expenditure (1990–2019), Constant Prices 2018. Source: SIPRI (Citation2020).

We can set the end of the Cold War as a pivot point for the transformation towards Sweden’s present degree of self-sufficiency in arms. At this time, Sweden produced close to all of its requirement of arms. Sweden did not develop and produce helicopters, transport aircraft and air-to-air missiles. Assault rifles were produced under license. Otherwise, domestic companies were active in almost all segments of military systems. In a series of Defence White Books, the overall defence priorities and the Swedish Doctrine were adjusted, along with certain important procurement decisions. These White Books will in part render an explanation to where Sweden’s self-sufficiency has ended up today. We will in general focus on the major path changes in doctrine, and more specifically on the consecutive priorities regarding the three military domains that have been defined in the last years as being Sweden’s ‘essential security interests’: combat aircraft capability, underwater capability and integrity-critical parts of the C3I domain.

Defence White Books

The Viggen fighter system became operative in 1971, and consisted of five different configurations.Footnote12 In 1982 a decision had been taken to develop the Gripen fighter program. The Gripen program united different aircraft missions into one unit platform. 204 Gripen aircraft were ordered, which represented a decrease from the Viggen program’s total number of 329 aircraft. It was named JAS 39 Gripen, where JAS represents a combination of fighter, strike and reconnaissance. In the submarine area the Navy had received four Västergötland class submarines with the last one delivered in 1988.

The Swedish government publishes Defence White Books (Defence White Book)Footnote13 at prescribed intervals. The 1987 Defence White Book reflected the continuation of the Cold War, a focus on territorial defence and Sweden as a non-aligned nation. The Gripen program was under development, and Västergötland submarines were under delivery. The Gotland class submarine program was decided upon during this defence planning period, with production of four submarines carried out 1992–96. Kockums was state-owned, and Saab private. The 1992 Defence White Book was still trying to comprehend the full impact of the end of the Cold War. The Defence White Book underlined the security uncertainties, and did not alter the overall doctrine.Footnote14 There were considerable programs under development and production based on orders prior to 1989.

The 1996 Defence White Book declared that the security situation after the Cold War had clearly become less tense. A reduction of the defence budget by 10 % was to be made until 2001. This led to considerable closures of Army regiments and Air Force bases, as well as downsizing of the Army structure. Procurement plans for submarines and fighters were left untouched. The defence industry had previously been broadly defined as consisting of ‘industrial areas’. They now became defined as consisting of ‘base competences’, which had a number of ‘strategic competences’, in their turn consisting of ‘niches’. Thereby priorities started to be defined in terms of specific technologies, rather than industrial sectors.Footnote15 Political and media discussions questioning the size and ambition of the Gripen program were becoming more apparent in these years. Submarine development also continued as planned.

In October 1997 an important event started an internationalization of the Swedish defence industry when Hägglunds was acquired by the British company Alvis plc. There was an ongoing process in government towards liberalizing the ownership and nationality of defence companies. Large parts of the Swedish defence industry were within the Celsius company, with the state as the minority owner at 25 %, but holding preferential shares giving them 61.7 % of the voting power.Footnote16 Celsius was dismantled in 1999. Saab acquired large parts of the missile production, together with man-carried support weapons. The independent companies Kockums and Bofors Weapon Systems were created.Footnote17 The naval shipbuilder Kockums was acquired by German HDW the same year. Bofors was acquired by United Defense (US) in 2001. The Swedish ammunition facilities were merged with Finnish (Patria Oy.) and Norwegian (Raufoss) facilities, creating Nammo in 1998. Bofors’ facilities in explosives (‘energetic materials’) were merged with Finnish facilities (Patria Oy) in 1998, and later merged with French facilities (SNPE Explosives and propellants), creating Eurenco in 2004. BAE Systems (UK) acquired Alvis plc. in 2004 and United Defense in 2005, thereby uniting Hägglunds and Bofors into the same mother company. HDW was acquired by the US investment bank One Equity Partners in 2002, and Thyssen Krupp (Germany) in its turn acquired the HDW and Kockums assets from One Equity Partners in 2005. BAE SystemsFootnote18 also acquired a 35 percent minority share in Saab in 1999. However, this stake was gradually reduced and completely divested by 2005. Thus, from 1997 to 2005 there was considerable internationalization and reshuffling within the Swedish defence industry. During this period Saab became larger than before and was now an even more dominant actor in the Swedish defence-industrial landscape.

During the 2000s Sweden’s military spending continued to fall, both in absolute terms and as a share of GDP. Meanwhile, security policy focus shifted towards participation in international missions, such as peacekeeping in Kosovo and Afghanistan. At the same time defence spending declined, making the Swedish defence industry more reliant on exports.

During this turbulent period a Defence White book was published in 2000, and one in 2004. The 2000 Defence White Book continued the downsizing of the Armed Forces personnel and regiment structure. Prioritized industrial ‘strategic competences’ were broadly described. These were competences that were strategically essential for the requirements of the Armed Forces and that Sweden had to have access to, or be in control of. This was a slimming of the 1996 breadth of competences. Underwater, fighter technology, signature technology and electronic warfare were four of the eleven prioritized areas; these four matched the future essential strategic interests.

The 2004 Defence White Book set more emphasis on ‘industrial niches’. These were defined as being indispensable for the Armed Forces’ long-term development, and the niches were to rely on industrial capabilities where Swedish companies could become (or remain) globally competitive and also capable of international arms collaboration. The areas primarily accentuated were network-based C3I systems; aerial vehicles; armoured vehicles systems; short-range strike systems; sensor and data fusion; robust telecom systems; signature-, protection- and system design. Interestingly, the underwater area (not surface vessels) was highlighted.Footnote19 In 2004 an ambitious project was launched by the Ministry of Defence in order to create a defence-industrial strategy, based on the concept of identifying competence niches over the technology readiness scale scale, from research at the Swedish Defence Research Agency through Försvarets materielverk (FMV)Footnote20 and industry to the Armed Forces. This project lasted until 2006, but never resulted in an official strategy. The 2004 Defence White Book also formulated that at that time there were no military threats to Sweden, and that the Armed Forces could be further downsized, together with defence research and arms development. The Armed Forces’ size and capabilities were to be increased during a ten-year period if the security situation changed. This important declaration became popularly known as the ‘strategic time-out’.

The Swedish Armed Forces were in Afghanistan 2004–2011. During this time, urgent financial and resource reinforcements for this mission became needed. This led to substantial cuts or delays in planned procurement, development and defence research. The areas later defined as essential security interests were largely left untouched in these reshufflings.

The 2009 Defence White Book came two years after the ‘Armed Forces defence materiel acquisition strategy’. This 2007 strategy outlined a radical shift in procurement priorities. The primary procurement option would be to buy already developed systems (‘off-the-shelf’); if this was not possible, the second option was to develop in collaboration with other nations. If this was not possible, the third and exceptional option would be to develop domestically. The 2009 Defence White Book pushed this a bit further by formulating the primary option being to upgrade existing materiel, preferably with other nations. The 2009 Defence White Book also underlined that the ‘Armed Forces’ operative capabilities’ were the overarching highest priority, thereby to some degree decreasing the priority of materiel and systems. Russia’s invasion of Georgia in 2008 was seen as an important event that made the security environment close to Sweden worse.

Gripen’s second version (the C/D) became operative in 2004, and further development was not decided upon. Development of a new submarine had been discussed, with several studies made, but a development decision was not yet taken. The Sweden-Norway-Denmark joint submarine project Viking was cancelled in 2004. With the importance of international arms collaboration being stressed in the Defence White Book, the potential for very large domestic development projects was questioned.

In 2010 an important acquisition precedence case vis-á-vis the new acquisition principles was finalized. Hägglunds had for decades had a preferential position with the Swedish Army, and had delivered thousands of armoured vehicles. The acquisition of a new ‘armoured modular vehicle’ stressed the new acquisition principles. Hägglunds’ ‘SEP’ prototype lost to a Finnish competitor – with a competing vehicle that was already operative in several nations. This outcome shook the institutionalized patterns between Hägglunds, FMV and the Army.

In 2012 a decree from the Parliament declared that all new larger development projects must be performed with an international partner. Thereby further development of Gripen and the initiation of the production of a new submarine class had these obligations. Switzerland was close to signing an agreement to become a partner of the next Gripen Generation, but cancelled in 2010. After having had discussions with several other nations, in 2013 Brazil and Sweden signed an agreement for joint development of the Gripen E/F.Footnote21

The 2015 Defence White Book stressed the deteriorating security situation, now with the recent Russian military campaign in Ukraine, together with Russia’s increasingly aggressive posture. For the first time the essential security interests Combat aircraft capability and Underwater capability were introduced in the Defence White Book. The central importance of the Armed Forces’ operative capabilities was further underlined; all defence research, all international collaboration in research and development could only be continued or initiated if it could be seen as contributing to the Armed Forces’ operative capabilities.

In the summer of 2015 a contract was signed with Saab to produce two submarines of the new Blekinge class, with an option for a third submarine. There is no international partner nation, but Saab Kockums is ordered to search for international partners.

In 2018 a third essential security interest was formulated: integrity-critical parts of the C3I domain.Footnote22 This formulation’s coverage is less obvious compared to the previous two: Fighter aircraft and underwater capability. Capabilities falling under the third essential security interest are cryptology, cyber technologies, electronic warfare, sensors and certain types of communication – without being specific on what more is included. The concept of ‘integrity-critical’ denotes that these technologies are critical to Swedish integrity, and will to a very limited extent – if at all – be shared with others. The capabilities and technological competence inherent in this third ESI have, however, in practice been treated as an ESI for a long time. Some capabilities and technologies have long been withheld and developed in networks consisting of only state actors from the Armed Forces, FOI and experts from the intelligence authorities FRA (the National Defence Radio Establishment) and MUST (the Swedish Military Intelligence and Security Agency). Industry is not a part of the innermost, most sensitive capabilities. In certain parts of the industry that develop systems for electronic warfare and countermeasures, units within the company are strictly compartmentalized under government scrutiny. This is done in order to highly delimit the number of people that could attain full understanding of these systems and capabilities.

A reform of the Swedish regulations for arms export were set in place in 2018.Footnote23 One important clause is intended to delimit Swedish arms export by stating that Sweden should not allow arms export to states with ‘weak democratic structures’. A large share of the Swedish arms export goes to nations in the Middle East and Southeast Asia, and several of these nations display political conditions which could fall under the definition ‘weak democratic structure’. Arms export that might require scrutiny based on this clause is handled on a case-by-case basis, and no apparent guiding practice has yet been established. In any case, arms export will likely be restrained at some level.Footnote24

The 2020 Defence White Book marked a 40 % increase in overall defence spending, gradually over the years 2021–2025. The defence budget had been gradually declining for more than twenty years, so this was a dramatic change. The development of the Blekinge class submarine is ongoing, with delivery (according to plan) of the submarines in 2021 or 2022. The search for international partners is still going on, with the Netherlands as (it appears) the most promising partner, with Poland as a second and more uncertain option. Gripen E will become operative in 2022 or 2023. The 2020 Defence White Book also envisaged substantial orders for e.g. artillery, armoured vehicles, surface vessels and an upgraded sensor chain. On 25 January 2021 Saab announced that FMV had issued an order for a ‘production definition phase’ of two of the next generation corvettes. This will be a further development of the Swedish Visby corvette, the next corvette being cleverly named Visby 2.Footnote25

Trends over the Period

The Russian military aggression towards Georgia in 2008 and above all Ukraine in 2014, paired with Russia’s military build-up and aggressive security rhetoric, changed the Swedish posture and doctrine. Once again the primary military priority became operational military capabilities and homeland defence. Thus, after a period of market liberalisation and international harmonisation, a clear shift occurred in the Swedish defence posture and priority. Sweden’s military expenditure started to increase during the 2010s. However, military expenditure as a share of GDP continued to decline markedly, hitting a low of 1.0 percent in 2018. This discrepancy can be attributed to the fact that the Swedish economy grew faster than military expenditure. The Parliament’s allocation of the defence budget (2020) for the five-year period 2021–2025 is shown in .

Table 1. Development of Sweden’s defence expenditure 2020–2025 (Source: Swedish government (2020), Budget bill 2021, 2020/21:1)

Due to falling budgets and the cost escalation of military equipment, Sweden has gradually reduced the quantity of its equipment. This is not something unique to Sweden, rather a general international trend. Similarly to most other Western European nations, Sweden’s focus on international operations during the 2000s meant a decreased quantity of heavier army equipment, with the number of tanks and artillery pieces being drastically reduced, focusing instead on lighter and more mobile, armoured personnel carriers. The Air Force and Navy have maintained their equipment volumes to a larger degree than the Army, but even these services have seen diminishing equipment numbers during the last decades.Footnote26 Reduced equipment volumes also meant diminishing economies of scale for the defence industry, as fixed costs have to be divided over fewer and fewer systems.

After 2014 Sweden has increased its defence spending more markedly. The Corona pandemic has taken a heavy toll on Sweden’s government finances and will likely continue to do so for a foreseeable future. This has also put into question whether or not the ambition of 84 million SEK by 2025 will be realised. In spite of increased dependency on exports and international ownership in the last two decades, the Swedish defence industry still provides Sweden´s Armed Forces with several key systems. Furthermore, Sweden still has an advanced defence industry for its size.

[. Origin of selected equipment 2020. Source: IISS.]Footnote27

Table 2. Origin of Selected Equipment 2020. Source: IISS

Swedish participation in international armaments collaborations had occurred earlier, but only began in earnest in the late 1990s. Examples of collaboration which started in the 1990s are Cision, Bonus, Meteor, Archer, Iris-T, NH90 and Excalibur.Footnote28 In recent years, Sweden has engaged in fewer and smaller collaborations. The primary exception is the bilateral development of Gripen E/F with Brazil, where Brazil has acquired 36 of the combat aircraft for 38 billion SEK. This project is a cooperation between Saab, Embraer and the Brazilian state. The Swedish state and Saab are also eagerly searching for an international partner for the development of the Blekinge Class submarine.

Following the deteriorating security environment in its neighbourhood, Sweden is currently refocusing on national defence and military spending is once again increasing. This should offer opportunities for the domestic defence industry. However, the industry also faces several challenges. Many significant acquisition projects, such as combat aircraft JAS 39 Gripen E and Blekinge class submarine from Saab, are close to delivery which prompts the question of what will come next.

Essential Security Interests

As previously mentioned, the Swedish defence industry can best be described as displaying partial autonomy. While it is difficult to claim that Sweden has specific niches, the country has identified three prioritised areas under the concept of essential security interests. The concept of essential security interests has its background in the Treaty on the Functioning of the European Union from 1958. The treaty declared the European community’s free movement of labour and goods. Meanwhile, Article 223 of the Treaty exempted defence materiel from this obligation. The article’s numeration has over the years changed to the present Article 346. For years European Union member states utilized the defence trade exemption in a highly protectionist manner. The 2009 EU Defence and Security Procurement Directive for procurement of defence and security (2009/81/EC) declared that defence procurement no longer would be exempted from the intra-community freedom of trade.Footnote29

Article 346 was complemented with a clause stating that ‘no member state shall be obliged to supply information the disclosure of which it considers to the essential interests of its security’ and ‘to take such measures as it considers necessary for the protection of the essential interests of its security which are connected with the production or trade in arms, munitions and war materiel’.Footnote30 All other acquisitions of defence-related goods and services shall be performed as competitive bids, so that companies from all member states have the possibility to offer a bid. EU member states can choose to exempt certain strategic acquisitions from competition. The intent of the Directive was to minimize such strategic acquisition to highly strategic matters, based on what member states view as essential security interests. EU member states have utilized and formulated what they define as their essential security interests in different ways.

Implementation of Essential Security Interests

Sweden transposed the directive into national legislation in 2011 and has since declared three essential security interests: combat aircraft capability and underwater capability in 2014, and integrity-critical areas in the C3I domain in 2018Footnote31. They have certain characteristics and a historical background. They have certain shared traits, but also different traits and conditions. All three are the government’s designated, domestic assets of capability sustainment, and not solely based on physical defence systems.

Combat aircraft capability revolves around the procurement and development of the JAS 39 Gripen version E. The Gripen E, as well as its predecessors, is primarily an interceptor, but also has attack and reconnaissance capabilities. It is not stealth designed in the same manner as the F-35, but prioritises electronic warfare (EW) and EW countermeasures. Regarding strategic autonomy, the Gripen’s share of technology from foreign sources is estimated at around 50 percent, where the engine from General Electric (US) constitutes the largest share. This essential security interest also covers other systems besides the aircraft that are required in order to ensure the required aerial capability.Footnote32

Sweden’s underwater capabilities are highly specialized for the conditions of the Baltic Sea. The Baltic Sea is characterised by shallow water, highly specific hydrographic conditions due to the Baltic Sea’s ‘brown water’, and shallow littorals with large archipelagos. Swedish submarines have conventional Stirling propulsion that optimises stealth conditions. The Swedish-made torpedoes are wire-guided whereas most nations have fire-and-forget torpedoes. Communication and surveillance solutions are highly specialized solutions. With the exemption of sonars, Swedish submarine subsystems are developed and produced domestically.

The denomination ‘integrity-critical parts of the C3I domain’ is a less precise definition. The concept ‘integrity-critical’ denotes highly strategic solutions for the innermost integration and coordination of situational awareness, intelligence and communication. The knowledge and command of these capabilities is held within very restricted communities, and is primarily performed by actors within the state. These C3I capabilities are for the most part not shared with any other nation. Some highly sensitive information is shared with a small group of prioritised nations, most of all US and Finland. Command and control systems are primarily developed by Saab.

Shared Traits of the Essential Security Interests

The three Swedish essential security interests share some common traits, but also differences:

Formulation of ESI

‘Combat aircraft capability’ is centered on the fighter platform, but brings with it systems that are needed in order to optimize the aircraft’s performance. ‘The underwater capability’ is formulated as a domain-bound capability. In Sweden it tends to be interpreted as that the submarine is the ESI, but it links to (as with fighters) to a system-of-systems capability. Integrity-critical C3I is the least specific formulation. It can be understood as the most strategic and sensitive areas of the national military communication and intelligence.

Platform connection

Based on the formulation, ‘combat aircraft capability’ points to the Gripen aircraft. The underwater domain can be understood as that the submarine is the pillar of the underwater domain, and it also covers other remotely operated underwater platforms (ROVs) and autonomous underwater vehicles (AUVs). Integrity-critical C3I relates to capabilities and systems that provide communication, intelligence and sensor data. Integrity-critical C3I connects indirectly to certain platforms, e.g. communication and sensor systems on fighters, submarines and surface ships.

Technology autonomy

However, even for systems connected to essential security interests, autonomy can only be described as partial. Regarding combat aircraft, Gripen has around 50 percent foreign content. The engines for JAS 39 Gripen are developed by General Electric (US), both for the E version which is equipped with an F414 engine and the previous C/D versions which are equipped with the RM12 engine, a licence-produced version of GE F404. The Raven-05 AESA radar is developed by Selex ES, a subsidiary to Italian Leonardo. Most of Gripen’s armament is also developed by foreign companies or though international cooperation. The new Blekinge class submarines are developed and produced with a greater degree of national autonomy, however, the sonars are sourced from foreign companies. To my knowledge all systems for integrity-critical C3I are Swedish. Certain systems and interfaces are organized in order to enable sensitive communication with selected strategic nations’ militaries. There is a continued dependence on foreign suppliers and supply lines within the essential security interest’s combat aircraft capability and underwater capability.

Company Connection

Regarding Combat aircraft, the Gripen fighter is produced by Saab. The aircraft has vital systems acquired from abroad, the General Electric jet engine being the most prominent. Around 50 percent of Gripen’s systems are sourced from other nations. The Swedish 50 percent is almost entirely produced by Saab. The second largest Swedish contributor is GKN, which is responsible for the maintenance of the jet engine. Regarding underwater capability, the degree of Swedish content is much higher with sonars as the important exception. The sonars are thereafter equipped with Swedish software solutions and algorithms. The submarine is by far the most costly component of the underwater capability, and Sweden has always had submarines developed and produced by Kockums and Karlskronavarvet. Since 2015 Kockums is a part of Saab.Footnote33 Torpedoes and C3I systems are also produced by Saab. Integrity critical C3I is by its nature and formulation not as explicitly defined. Almost all C3I systems in the Swedish Armed Forces are produced by Saab. The development of the C3I systems also engages a number of small and medium-sized enterprises that are specialists in certain C3I technologies and solutions, many of them working close to FMV and the Armed Forces. However, the innermost and most sensitive core of the C3I systems – deemed integrity-critical to Sweden – are performed and controlled by actors within the Swedish state. Industry is not a part of this innermost core.

Degree of International Collaboration

Regarding combat aircraft, Sweden together with France are the only European nations that produce fighters without collaborative partners. Sweden has considerable foreign sourcing, but these systems are not a result of arms collaboration. Sweden and Saab are, however, active in many collaborative research programs through EDA and NATO. Sweden participated in the Neuron UCAVFootnote34 programme (2003–2012) in order to maintain the development capability within Saab during a longer period of limited development of the Gripen. Regarding underwater capability, Sweden has had very little international collaboration.Footnote35 Sweden is seeking an international partner that will, by acquiring the Blekinge class submarine, take part and co-finance the development of the submarine. Regarding integrity-critical C3I, the degree of collaboration is inherently highly classified and performed nation-to-nation, and not company-to-company.

Export

In comparison with its international competitors Saab has been quite successful in the export of combat aircraft (Gripen has been acquired or leased by South Africa, Hungary, The Czech Republic, Thailand and Brazil). Regarding the underwater domain, Kockums (now Saab Kockums) has been struggling to reach export success. Three export deals have been created: Collins class to Australia in 1986 followed by two exports of upgraded Swedish submarines to Singapore (1995 and 2005). Regarding integrity-critical C3I, Saab regularly exports C3I systems to other nations, especially for surface ships. It has, for example, exported C3I systems for surface ships to Canada, South Korea, Thailand, Australia, New Zeeland, Finland, Denmark, Pakistan and Bahrain. Different radar systems have been exported to many nations. The Erieye aerial surveillance system has been exported to Mexico, Greece, Pakistan, Brazil, Saudi Arabia, Thailand and the United Arab Emirates. The C3I export success for the Land domain has been very limited. All these export deals show that Saab’s solutions are internationally competitive.

There are also other product areas where an implicit national supplier preference can be noted, without the product areas designated as essential security interests. In land-based artillery and artillery on naval vessels, Sweden has almost exclusively procured from Swedish Bofors, now BAE Systems Bofors.Footnote36 Sweden has also a long tradition of buying armoured vehicles from Hägglunds, now BAE Systems Hägglunds. In this article, however, we focus on how the essential security interests serve as defining priorities of Sweden’s partial autonomy.

Security of supply and a certain degree of self-sufficiency are strategically important for Sweden and a domestic defence industry is a key component of any such ambition. However, there are also significant costs for a small country to maintain an advanced domestic defence industry. Moreover, there is a continued reliance on export for defence companies even among the essential security interests. Autonomy is difficult to achieve given the size of the Swedish market and technological base. Sweden already now lacks key components and systems, and in the future will lack even more, such as stealth technology for future combat aircraft. However, Sweden still has some significant areas of excellence.

So what are the implications of declaring essential security interests? What is the practical meaning of the three formulated priorities? Firstly, there is a common misunderstanding that ‘combat aircraft capability’ solely refers to the Gripen, and that ‘underwater domain’ solely refers to submarines. In both cases, the essential security interest relates to vital, supporting systems that are required for reaching a desired strategic capability. Such supporting systems are e.g. related to communication, signature and situational awareness. Secondly, this formulation (and implicit meaning) of the essential security interests contains a convenient degree of imprecision; foreign analysts cannot know exactly what is included, and the Swedish state and military employ a degree of flexibility to decide what can be included as being within the essential security interest. Thirdly, ‘integrity-critical parts of the C3I domain’ is the least precise definition. What separates this interest from the first two is that the strategic core of such capabilities is performed within the state, with industry not being allowed into the innermost secrets.

Other EU Member States’ Implementation of Essential Security Interests

There is limited data available on how the 27 EU member states have formulated their essential security interests. Through a correspondence with the Swedish Ministry of Defence in 2020 some information was received regardingDenmark, Finland, France and Norway. The nations with less developed domestic defence industries (Finland, Denmark, the Netherlands) have formulated less ambitious and less specific essential security interests. France has Europe’s broadest and most advanced defence industry coupled with a high ambition of non-dependence. The Netherlands and France formulate their essential security interests in a more detailed fashion, France does so in extensive detail.Footnote37 France has moved from a previously very high self-sufficiency towards a ‘shared strategic autonomy’Footnote38 with European peers in strategic technology areas, compared to Sweden’s partial strategic autonomy.

Change Factors

Six alternative change factors were stated in the beginning of this article that suggest why Sweden’s degree and design of strategic autonomy in arms production has evolved into where it is today. These six change factors will now be discussed and compared.

CF1 Autonomy as a result of failed internationalization

Between 1997 and 2005 the Swedish defence industry experienced considerable consolidation and acquisitions from abroad. In a European comparison Sweden was uniquely market-liberal. The state had decided that these companies would and should be able to survive without state ownership, possibly under foreign ownership. Furthermore, strong incentives were created to make Sweden engage more in international arms collaboration. Saab acquired large parts of Celsius, acquired a division of EricssonFootnote39 and has since, overall, been successful on the export market. For Kockums, the foreign ownership did not bring any market success, nor any successful collaboration. Kockums’ weak order portfolio and troublesome relationship with its foreign owner resulted in a coup-like ‘repatriation’ orchestrated by Saab and the state – resulting in Saab’s acquisition of Kockums in 2015Footnote40. Hägglunds’ strong preferential relationship with FMV weakened under BAE Systems, but has survived quite well based on continued strong export. Bofors has had a period of poor order book and competitiveness, but has recovered in recent years. Bofors has had a number of successful collaborations. Out of these companies, the internationalization has worked out well for Saab and Hägglunds, and less so for Kockums and Bofors.

CF2 Techno-nationalist Perception of Sweden Leading to Industrial Protectionism

The concept of techno-nationalism views autarky (self-sufficiency in armaments) as serving not only national defence needs, but also as maximizing national political, strategic, and economic autonomy.Footnote41 The techno-nationalist preference was strong for the whole Swedish defence industry until around 2000. With the reform around 1998–1999 when state ownership ended and defence companies could be acquired by foreign companies, this preference was partially weakened. Saab’s fighter development and production continuously receives comments from politicians on how important the fighter development is for creating spin-offs and high technology. In order to preserve and nurture this cherished Swedish arms capacity, the state continuously finances this industrial capacity. Other segments of arms production do not receive the same support. In order to keep the domestic submarine design and production capability in Kockums, the state has had to entirely finance its operations since its last export in 2005.

CF3 Strategic Choice

A strategic choice is defined here as a nation’s choice based on national security, and linked to this, certain desired military capabilities. To the security aspect one can also add the nation’s striving to link itself to a wider security connection to a certain nation or alliance. In the early 1900’s Sweden decided to remain non-aligned in order to be able to stay neutral in case of war. As a consequence of this, after the Second World War Sweden decided to first of all develop a national ability to produce its own fighter aircraft. Since Sweden did not experience massive wartime destruction, the Swedish industrial infrastructure was well-equipped to engage in this build-up. This was followed by a broad, further development of domestic arms development. A few decades ago Sweden had the world’s largest Air Force compared to its size. Thus there is a strong tradition of developing combat aircraft. In the underwater domain, Sweden has for a long time developed specialized underwater technologies and capabilities optimized for the unique hydrographic conditions of the shallow Baltic Sea. Since Sweden has been non-aligned for more than 70 years, it has also developed its own idiosyncratic solutions in communication, e.g. its data link and underwater communication. All such more or less unique national solutions match well with all three essential security interests.

CF4 Corporate Lobbying

The industrialist family Wallenberg and its investment group Investor have from the establishment of Saab as a producer of military aircraft in 1944 been an important actor in the development of the Swedish defence-industrial landscape. The Wallenberg family had also developed a working alliance with the Social Democrats who were in power from 1933 to 1977. This relationship was a trustful alliance between a highly powerful capitalist industrialist family and the Social Democrats’ strong, socialist state governance of the Swedish state. The Wallenberg family have played their cards well, and Saab’s aircraft production has always been coveted – despite periodical strong criticism in the media regarding why Sweden should put such vast resources into nurturing domestic fighter production. Saab was also able to acquire the parts of Celsius that it desired, and the state together with Saab orchestrated the repatriation of Kockums into Saab. Presently Saab holds the lion share of what falls under the three essential security interests; these three encompass more than 50 % of the procurement budget; and Saab stands for around 70 % of the Swedish defence industry’s output. To call this advantageous position ‘lobbying’ is too simple, it is more of an institutionalized web of dependencies with interdependent state, military and industrial incentives. The fact that the Wallenbergs also are large shareholders in several of the largest Swedish companies has also made it possible for them to organize attractive offset solutions in larger export campaigns.

CF5 Export Incentives Leading to Political Support of Technologies

Every state wants its industry to be successful in export. Larger arms export involves enormous sums of money. The export deal with Brazil is the largest Swedish export ever. Therefore potential large arms export receives massive export support from the ministries, embassies and concerned authorities. It is difficult to prove, but there is a pattern of strong state support for product categories that may result in larger arms export.

CF6 Europeanization of EU Defence Industry

Sweden became a member of the European Union in 1994. Before that Sweden’s participation in intra-European arms collaboration and defence-industrial consolidation was close to non-existent. In the years 1998–2004 a wave of defence-industrial consolidation occurred in Europe. In the 2000s the European Commission increased its efforts to harmonize the functioning and legal framework of the European defence market and defence industry, with the Directive of 2009 (Citation2009/81/EC) as the most important manifestation. Sweden has in its rhetoric vis-à-vis Brussels and in Brussels always been highly supportive of EU harmonization in these matters. However, the intra-EU defence-industrial consolidation and integration has not been orchestrated by the EU; they have all been based on corporate considerations for optimizing industrial performance and positioning. The increasing support in the Commission has of course been helpful in order to provide a more beneficial political climate regarding cross-border consolidation. However, none of the consolidations or acquisitions concerning Swedish defence companies were carried out as a result of EU-led harmonization processes. Sweden’s political rhetoric vis-à-vis Brussels has been (and still is) highly supportive of EU goals and aspirations, but the actual integration occurrences have been led by either corporate incentives (under a market-liberal Swedish governance) or, in one instance (Kockums’ ‘repatriation’), by self-sufficiency incentives.

So what change factors bear most impact on the present Swedish defence-industrial landscape?

CF1 Autonomy as a result of failed internationalization

CF2 Techno-nationalist perception of Sweden leading to industrial protectionism

CF3 Strategic choice

CF4 Corporate lobbying

CF5 Export incentives leading to political support of technologies

CF6 Europeanization of the EU defence industry

The formulations of the essential strategic interests are clearly a result of CF3, triggered by a deteriorating security environment. However, the preceding history prior to these recent formulations (2014 and 2018) provided specific conditions for what could be established.

Several armament segments have received less priority, leaving these industrial competences to the outcome of their export success: radar (Saab Surveillance), missiles (Saab DynamicsFootnote42), artillery (Bofors) and armoured vehicles (Hägglunds). To delimit the breadth of essential security interests to the three established ones is a strategic choice. The reason for not declaring a broader portfolio of essential security interests is based on a combination of adhering to EU market openness and, of course, in order to delimit the financial obligations that come with it. Sweden does, however, procure armaments from these companies under competitive bidding, and the recent Defence White Book (Ministerial Office, Defence White Book Citation2020) outlines sizeable orders to these companies. Sweden has not become a recurring partner in international collaboration (CF1), which has made politicians continuously and unwillingly support costly preservation of industrial competence, especially for fighters and submarines. Hägglunds and Bofors have, however, survived on their own merits. Regarding CF2, it is difficult to prove the techno-nationalist impulse, but we state that it is profound. Self-sufficiency in many weaponry segments combined with a stoic preservation of the non-alignment posture has created a national pride in emblematic platform systems. Saab’s and Wallenberg’s (CF4) strong position in Sweden’s economy and political landscape over a long time has created a deeply institutionalized military-industrialized complex-like cohesion between the state and these industrial actors. The sunk costs from decades of investment in the fighter and submarine domains, including the created sophisticated engineering competences, has made politicians allocate considerable resources and political investment into export initiatives in relation to these segments (CF5). Such support has been rhetorically bolstered by arguments about the defence sector’s alleged substantial spin-off contributions to other high-tech industry in Sweden, and with arguments that Sweden’s military challenges and required military capabilities are based on a unique geographical position and security environment. Europeanization (CF6) received considerable rhetorical support and promise during the years of low security threats, but cannot be said to have had strong impact on how the Swedish partial strategic autonomy has turned out.

In sum, the first five change factors all bear importance for what has created the present Swedish state of partial strategic autonomy. Sweden’s history of non-alignment, its strategy of being highly self-sufficient, the trustful relationship between the Wallenbergs and the state, Sweden’s position by the Baltic Sea, the many years of proximity to the boundary between the two Cold War adversaries – all these are conditions that have led to Sweden’s present partial strategic autonomy. The three established essential security interests made implicit defence-industrial priorities explicit. Sweden’s present governance can be seen as a hybrid model of national self-sufficiency and globalized niche production – what we name partial strategic autonomy.

If Sweden had decided not to go through with the Gripen program (it was shaky for a while), and/or not to develop the Blekinge class submarine, the situation would have been quite different. Saab would probably have become a system supplier to other European or American fighter programs, with a lower aeronautical turnover and a much lower financial support from the Swedish state. Kockums’ specialized competence and technologies might have had problems to achieve a position of supplier to the small number of European producers of conventional submarines – with the dominating nations (Germany and France) also striving for very high degrees of self-sufficiency in required systems.

The Future

With defence spending increasing as a result of the 2020 Defence White Book, the Swedish defence industry should expect brighter days ahead. Furthermore, as national defence has come into focus, issues such as security of supply has gained in importance, strengthening the argument for supporting said industry. And even if not expressed in detail, the identification of essential security interests also signals political support for the domestic defence industry. However, there are several structural challenges that complicate the future development and direction of the Swedish defence industry. Increased technological requirements push costs ever higher and make it increasingly difficult for a small country to provide the funding, competence and infrastructure needed to keep up. Even larger European countries, such as France, the UK and Germany have realized that future strategic autonomy will have to be increasingly shared. Sweden’s identification of essential security interests does not automatically mean a return to high levels of autonomy. Even within these prioritised areas Sweden still relies on critical foreign components. The possible ways forward are increased budgets, export and cooperation. Exports are highly uncertain and increasing exports may conflict with the obligation of being restrictive over who to sell to.

Autonomy by Spending

Increased budgets for the sake of just spending more on materiel comes into conflict with other concerns, conflicting public spending and cost efficient military capability building. Furthermore, anything but a high level is unlikely to be enough to support the defence industry enough to increase overall autonomy. It would require significant increases in order to boost volumes. It is not likely that spending is a sustainable path, as much larger countries are moving towards shared autonomy. Furthermore, a large share of the increased spending is allocated to a build-up of the Armed Forces’ structure and regiments, and of a more robust and reliable defence logistic capability.

Critical Export Deals

As noted above, exports are highly important for the Swedish defence industry. Sustainment of combat aircraft is highly supported by a fair stream of export deals, the latest to Brazil in 2014. Regarding submarines, there has been very limited export, the latest to Singapore in 2005, and that was of refurbished submarines from the Swedish Navy. Kockums also produces surface combatants, where the export has been even weaker. Export is equally important to BAE Systems Hägglunds and BAE Systems Bofors, but they fall outside the focus of our study. There is a trade-off between developing unique Swedish capabilities and the need for exports. If the platforms require adaptations to the international demand, this may compromise domestic capability demands.

Critical Cooperation

International cooperation has potential advantages and risks. It risks creating dependencies and potential inefficiency with regard to diverging capability requirements. Increasing costs and delays as more and more national requirements are added and compromises need to be reached. However, international cooperation grants access to technologies and can, with larger numbers, create economies of scale. Sweden pursues cooperation with other EU member states. The European defence industry has been characterised as being fragmented and suffering from insufficient investments in research and technology.Footnote43 Historically, the Swedish experience with European collaborations has been mixed. The NH-90 project ran into several problems causing delays and cost overruns. Sweden has engaged in two important missile collaborations: Iris-T (started 1995, operative in Sweden in 2009) and Meteor (started 2001, operative 2016). After these two strategic collaborations, Sweden has not participated in any multilateral collaboration in the missile area. The Meteor and IRIS-T projects seem to have progressed as planned.Footnote44 Cooperation can broadly be separated between more explorative cooperation in research; cooperation for developing demonstrators; and cooperation in developing a certain system or platform with an intended operative use at a certain point in time.

The European Defence Fund (EDF) is an attempt to increase and coordinate European defence research and technology development. Sweden is positive to the EDF as a vehicle for increased defence research and cooperation within the EU, but strives towards an inclusive approach which allows for third country access and participation.Footnote45 It is also worth noting that the Swedish principle of budget neutrality means that any increased spending on the EU level must be financed by an equal decrease in spending at the national level, within the same area.Footnote46 This could divert funds from Swedish defence research and technology investments rather than increase them, as was part of the ambition of the EDF.

On 18 July 2019 the defence secretary of Sweden, together with his counterpart from the UK, signed a Memorandum of Understanding into examining the possibilities of developing a future combat aircraft.Footnote47 This does not mean that Sweden has joined the UK Tempest programme, future combat aircraft technologies could also be used for existing systems such as the Gripen E and Eurofighter Typhoon. The UK-Sweden development has a parallel European initiative with the Franco-German SCAF (Système de Combat Aérienne du Futur).Footnote48

Boeing with SAAB as the primary partner were in 2018 awarded a contract to produce the next US trainer aircraft – the T-X. The T-X production is planned to deliver 351 aircraft. The fact that Saab was chosen as a foreign partner with around 10 percent of the order value shows that Saab and Sweden are trusted in the US. The US initiates very few collaborative programs with foreign partners.

Sweden seems to be striving to balance between a strong transatlantic link and European integration. These perspectives are not at odds. But some EU member states, such as France and Germany, have a clear preference for a European, ITAR-free strategic autonomy. Meanwhile, Sweden continues to depend on and work towards maintaining and developing both ties. Interoperability within NATO will guarantee that the transatlantic link remains relevant for all European states.

Conclusions and Future Research

The Swedish Hybrid Model

The present Swedish defence-industrial structure and the government’s governance can be described as a hybrid model with certain parts of the defence industry operating under national priority, and the other parts to a much higher extent acting in a competitive, globalized market. The partial strategic autonomy is primarily manifested through the security priorities formulated by the three essential security interests, where ‘combat aircraft’ has the most globalized sourcing structure. Through the formulation of three essential security interests, parts of the Swedish defence industry are now clearly and unequivocally identified as prioritised for Sweden’s military capabilities and security policy.

In relation to Bitzinger’s pyramid structure, Sweden has gradually over decades lowered its position in Tier 2a: ‘Smaller, niche-oriented, technologically advanced defence industrial bases’. The previously implicit strategy of partial strategic autonomy has become more explicit through the formulation of the essential security interests. There are however no official government formulations in White books or government bills that define the government’s strategic security governance of the entire domestic defence industry. Thus, ths aggregate picture is still open for interpretation.

With the three essential security interests being formulated between 2014 and 2018, the implicit priorities became marked. The essential security interests have different conditions and strengths, but reside upon substantial domestic autonomy. The underwater capability faces the highest challenges, due to unsuccessful export and non-existent international cooperation. Integrity-critical C3I is by its nature a domain that must retain self-sufficiency. Through their formulation the essential security interests confirm Saab’s considerable influence on systems integration and technology provision. The state and the military are highly dependent on Saab.

Suitability of the Swedish Model

So does Sweden have the defence-industrial capabilities that meet the demands of its impending military challenges? The present defence-industrial structure is not rational and optimized. It is a product of patterns of priorities and institutionalized inertia creating considerable path dependence. Fundamental geopolitical swings in the security situation and reprioritization – from homeland defence over to peacekeeping missions and back to homeland defence – has created shocks to the defence-industrial infrastructure and governance. The present domestic defence-industrial infrastructure and its differing degrees of globalization offers satisfactory conditions for supplying Sweden with its required military capabilities in relation to the security situation. It is however a costly set-up, especially since Sweden has such high ambitions for maintaining a high level of technological autonomy and sophistication regarding combat aircraft and submarines.

Unique Requirements?

Regarding the underwater domain, Sweden has unique conditions in the Baltic Sea that require specific solutions for military capabilities. The idiosyncratic developed technologies, however, traps the technology infrastructure into making collaboration cumbersome to create, and obviously products that are difficult to export. Producing only two, perhaps three submarines of the latest class is a very costly way of maintaining this defence–industrial competence.

In the fighter domain, Sweden cannot be said to have unique conditions. There is a great degree of path dependence due to idiosyncratic solutions, a techno-nationalist leaning and limited collaboration which has made the option of buying fighters from abroad disregarded for a long time. Will Sweden independently develop and produce a next-generation fighter? The Gripen E/F constitutes a large step in modernization compared to Gripen C/D, and Gripen E/F will likely be operative into the 2040s. Sweden’s half-hearted investment in Tempest does not show a clear leaning towards abandoning yet another Swedish fighter class. Economic rationality should, however, force Sweden to adapt towards the next fighter being a collaborative effort. Integrity-critical C3I is likely to remain all-Swedish – it strongly connects to the national security sovereignty of a nation in such a demanding geographical security position.

Change Factors

The discussion of the six change factors showed that there is an interrelationship between several factors that have led to the present Swedish state of self-sufficiency and autonomy. Sweden and its defence industry have gone from extensive strategic autonomy during the Cold War to the current state of partial strategic autonomy. This is similar to several other Western European nations. Today, few nations have the capability to independently maintain a near-complete defence industrial capability. The identification of essential security interests confirms and gives policy direction to prioritised capabilities or niches. The challenges and way forward for these security interests vary. Combat aircraft require cooperation, mainly due to increasingly advanced technological requirements. This includes cooperation with export partners. Submarine technologies are kept more closely to home with some components imported. There are fewer possibilities for cooperation as competitors within this area have historically shown limited inclination towards sharing technologies. Instead, exports are needed for economies of scale.

Future Development of the Defence Industry in Sweden

Saab’s fighter competence has 15–20 years of market presence secured through the decided investments for development and production. It is reasonable to assume that further Gripen export will materialize. During this period decisions have to be made what the next project endeavour will be.

Saab’s submarine and underwater competence will have a considerable stream of activities in the next five to ten years in order to develop and uphold the capabilities related to the new Blekinge class submarine. Kockums has however limited production; two submarines under delivery with a Swedish option for a third. The probability for export of submarines being unclear makes the viability of the submarine competence unclear.

The other business units of Saab (Dynamics and Surveillance), Bofors and Hägglunds appear to be able to remain in the global market despite their not as favourable position vis-à-vis the Swedish state. In the defence planning period 2021–2025, their domestic orders are clearly more promising compared to the previous defence planning period. However, we cannot know if parts of Saab, or Saab in its entirety, will be acquired from abroad. There is a possibility, and that would definitely change the conditions.

Future Development of the Swedish Model

Economic rationality and adapting to how other Western European nations act should force Sweden to increasingly abandon large, domestic development programs and turn to shared autonomy through multilateral collaboration. This would lead to a further weakening of the 2a position in the pyramid.

Even though future defence budgets will increase significantly, the overall trend suggests that autonomy will probably be increasingly niched and more dependent on international collaboration. This requires strategic evaluation and identification of integral areas. Even parts of the essential security interests will most likely be identified as niches, rather than the entire essential security interests as a whole. This raises the questions of what capabilities Sweden wants to maintain or develop further. By engaging in multilateral cooperation, compromises must be made between the partner nations and partner companies. Multilateral cooperation will thereby reduce national autonomy in favour of shared autonomy. Some actors engaged in the Swedish defence debate would like to see increased autonomy, but as this has become economically unviable for nations like the UK, France and Germany, it will make even less sense for Sweden. In order to preserve the domestic defence industry, industrial cooperation must evolve, thereby shifting Sweden to having more European shared strategic autonomy.

Pending Processes

There are two pending processes that will affect the Swedish future regarding the sustainment of Sweden’s partial strategic autonomy. Firstly, how the ambitious boost envisioned by the 2019 Defence Commission will eventually materialize. The 2020 Defence White Book confirmed the vision of the Defence Commission with a gradual increase of defence spending from 1.1 % of GDP in 2020 to 1.5 % in 2025. Secondly, the current materiel acquisition strategy from 2007 is a product of peacetime and internationalisation. In November 2020 the Ministry of Defence initiated a committee for formulating a new strategy, the committee will present their suggestions in May 2022Footnote49. These two processes will affect and maybe redefine the Swedish ambitions for the degree and nature of strategic autonomy.

Acknowledgments

I would like to extend my appreciation to the peer reviewers for their suggestions that were key in advancing this paper.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Notes

1. The UK, Germany and Italy have, however, jointly designed and produced the Eurofighter. Besides Sweden, the UK, France, Germany and Spain develop and produce their own submarines in Western Europe. In Eastern Europe only Russia develops and produces submarines.

2. Note: 1a) across the board and often leading, 1b) across the board and advanced, 2a) niched oriented but advanced, 2b) broad and/or emerging, 2 c) broad but not advanced, 3) limited and non-advanced. (Bitzinger Citation2015)

3. Fiott, D. (2018) Strategic autonomy: towards European Sovereignty’ in defence?, European Union Institute for Security Studies.

4. Trybus, M. (2014) Buying Defence and Security in Europe – The EU Defence and Security Procurement Directive in Context, pp. 40–41 (Cambridge University Press)

5. Bitzinger, Richard (2015) ‘New ways of thinking about the global arms industry: dealing with limited autarky’’, Australian Strategic Policy Institute.

6. See e.g. (Arteaga et al, 2016; Belin et al, Citation2017; Bitzinger et al. Citation2017; Fiott Citation2017, Citation2018, Citation2019; Bartels et al Citation2018; Howorth Citation2018; Lippert, von Ondarza, and Perthes Citation2019).

7. For an enhanced overview of this longstanding debate, see e.g. (Lundmark, 2011, Andersson 2015, Fiott Citation2018; DeVore Citation2019).

8. From early on, the Wallenberg industrialist family has been majority owners of Saab and companies involved in this national defence technology complex.

9. Karlsson, Birgit (2015), Svensk försvarsindustri 1945–1992 [Swedish defence industry 1945–1992], Försvaret och det kalla kriget, Karlskrona.

10. Lundmark, Citation2019b.

11. Karlsson (Citation2015); Lundmark, Citation2019b.

12. Viggen AJ: strike fighter; Viggen SH: maritime patrol; Viggen SF: aerial reconnaissance; Viggen SK: two-seat trainer; Viggen JA: fighter-interceptor.

13. The Defence White Books (Försvarsbeslut in Swedish [Defence Decision]) were published every fifth year until 1987, every fourth year between 1992 to 2004, and every fifth year after the 2009 Defence Book.

14. Hedin (Citation2011). Hedin published a comprehensive description and analysis of the five Defence White Books from 1992 to 2009.

15. Hedin (Citation2011).

16. The state divested 75 % of the shares in 1993.

17. The Swedish state created Bofors in 1646 and Karlskronavarvet in 1689. Karlskronavarvet was merged with Kockums in 1989, and Bofors and Kockums after a period in the Celsius conglomerate once again became individual companies.

18. At the time of the acquisition, the acquiring company’s name was British Aerospace. The company changed its name to BAE Systems in 2001.

19. Defence White Book 2004.

20. Försvarets materielverk (FMV): The government authority for defence acquisition.

21. The Gripen E is a one-seater version, Gripen F a two-seater version. Sweden has only ordered the E version, whereas Brazil has ordered E and F.

22. In Swedish: Integritetskritiska delar av ledningsområdet.

24. Strategisk exportkontroll (2019).

25. 20,210,125-saab-signs-two-contracts-for-next-generation-corvettes-for-sweden-en-0-3,873,882.pdf

26. Olsson, Per (Citation2019b) Pang för pengarna – En ESO-rapport om Sveriges militära materielförsörjning, ESO 2019:7.

27. APC (T) = Armoured Personnel Carrier (Tracked), APC (W) = Armoured Personnel Carrier (Wheeled), SP = Self-Propelled, SAM = Surface-to-air missile

28. Bonus: Bofors-Giat (Fra), guided munition, start 1993; Iris-T: Saab-companies from five partner nations (Germany, Greece, Italy, Norway, Spain (replaced by Canada during the development)), infra-red air-to-air missile, 1995; Cision: Kockums and DCN (Fra), submarines, 1998; Meteor: Saab-MBDA (France, Germany, Italy, Spain, UK), beyond visual range air-to-air missile, 1998; Excalibur: Bofors-Raytheon (US), guided artillery shell, 2002; NH90: Saab-NHI industries (together with Finland, France, Germany, the Netherlands,Norway), helicopters, 2004.

29. Trybus, Citation2014.

30. Treaty on the Functioning of the European Union. www.eur-lex.europa.eu.

31. My translation. In Swedish the three essential security interests are formulated asstridsflygsförmåga, undervattensförmåga and integritetskritiska delar inom ledningsområdet.

32. Lundmark, M. (2019), ‘The Gripen Fighter: Present and Future Flight’, in: Défense & Industries, n0 13, Juin 2019, pp. 14–17.

33. In 2014 an important move was made in order to safeguard the Swedish autonomy for submarine development when Saab acquired Kockums from the German owner Thyssen Krupp Marine Systems. This action can be described as a coup orchestrated by the government, FMV and Saab where orders to Kockums were cancelled by FMV, key personnel in Kockums were recruited by Saab and the German owner saw no other option than to sell Kockums to Saab. Thereby a ‘repatriation’ of Kockums was established. (See Lundmark Citation2019a, M. ‘Kockums – the Repatriation of the Swedish underwater crown jewel’, FRS, Citation2014)

34. UCAV: Unmanned combat aerial vehicle.