ABSTRACT

Having predictable, stable and adequate financial resources is essential for achieving universal coverage of essential health products and services, including assistive products. Access to such resources would enable governments and participating organizations to initiate and maintain a system for providing assistive products and associated services, as well as to grow the scope and scale of their operations over time. While limited funding is not the only reason to explain the shortfall in the provision of assistive products globally, unpredictable and inadequate public funding has been cited as the primary cause of poor access to these products in many countries. Several financing options have been presented in this paper that could be considered by decision-makers to initiate or supplement the financing of assistive products.

Introduction

Having predictable, stable, and adequate financial resources is essential for achieving universal coverage of essential health products and services. Access to such resources would enable governments and participating organizations to initiate and maintain a system for providing health products and associated services, as well as to grow the scope and scale of their operations over time.

While limited funding is not the only reason to explain the shortfall in the provision of assistive products globally (World Health Organization [WHO], Citation2016a), unpredictable and inadequate public funding has been cited as the primary cause of poor access to these products in many countries. Indeed, except for a few high-income countries, many countries, for example, Tajikistan (WHO, Citation2019) and Bangladesh (Borg & Östergren, Citation2015) currently have limited public funding for the provision of assistive products, resulting in poor and inequitable access to these products for people in need. Governments in these countries often allocate financial resources to serve other healthcare needs that are perceived as having higher priority than services for people with functional difficulties, including people with disabilities and older persons. This might be because of a lack of awareness about the multitude of potential individual and social benefits that assistive products can offer (Boot et al., Citation2018; Chadha et al., Citation2014; Makinde et al., Citationn.d.). Combined with a lower priority for assistive products, many countries also have low levels of public funding for health and social care overall. Consequently, availability is dependent largely on individuals’ ability to pay in these countries.

In response to the significant gap in public provision, several domestic and international nonprofit organizations (NGOs) typically operate in countries to provide assistive products. The operations of these NGOs, however, are limited mostly to a small range of assistive products e.g., wheelchairs. The small-scale and unco-ordinated nature of this sector leads to low economies of scale and scope. From a financing point of view, this creates a perception of increased credit risk by institutional investors, thereby limiting the NGOs’ ability to access capital at reasonable costs over longer terms to support the growth in scope and scale of their operations. From a system perspective, the parallel financial flows from different NGOs have been noted to result in poor co-ordination, duplication or uneven distribution of system functions and funding allocation (Galway et al., Citation2012; Makinde et al., Citationn.d.; Vassall et al., Citation2014). It is likely that this creates inefficiency in the procurement and provision of assistive products, potentially causing wastage of the already limited capital. From the perspective of people who are in need of assistive products, it also creates considerable confusion in navigating the system to access these products.

In view of these challenges, this paper begins with a brief discussion of the importance of improving the governance and efficiency of the overall system, by taking a systems approach to financing and resource allocation, and by optimizing service delivery within the available resources to improve the financing of assistive products. This is followed by a description of different financing options that have been used in the healthcare and social sectors. Governments might consider these options, especially when setting the framework within which non-state actors operate.

The information in this paper is based on a targeted literature review. The first author also consulted telephonically or by e-mail with twelve informants,Footnote1 between August and October 2017, to gather information about the current provision of assistive products in a selected set of countries.

It is important to note from the outset that government agencies and other non-state actors who might consider the various options included in this paper, must seek financial and legal advice from appropriate professionals according to the nature and structure of their organizations, and the local legal and regulatory requirements.

Improving system governance and efficiency

System components are inextricably linked. Many problems and challenges related to the provision of assistive products are likely to be common across other parts of the health and social care system. Therefore, a broad systemic view across all relevant sectors ought to be taken to reform the system to improve the financing and provision of assistive products. That is, to the extent possible, provision of assistive products should be integrated with existing health and social care systems.

To this end, decision-makers from governmental and participating non-governmental sectors should first refer to, and be guided by, the principles of good governance from a systems perspective. This means that decision-making in the reform process should be accountable, transparent, law abiding, responsive to the needs of the community in a timely and appropriate manner, fair and inclusive, effective and efficient, as well as participatory and consensus-oriented by enabling the involvement of all affected and interested parties (Graham et al., Citation2003; United Nations Economic and Social Comission for Asia and the Pacific [UNESCAP], Citation2009). In adopting these principles, changes to the provision of assistive products, including financing, could create synergies across sectors and strengthen the overall performance of the health and social care systems.

From a technical aspect, decision-makers and system managers should ensure the “allocative efficiency” of the overall system. In its broadest sense, this means “what services and products should be included in the package to maximise welfare?” (Palmer et al., Citation1999). More specifically, the overall aim of the system should seek to allocate resources to products and services according to the population’s needs, with a view to maximizing health and societal outcomes, at a cost that represents value for money. To this end, system managers often seek to identify priorities and opportunities across all system elements by conducting environmental scans and health technology assessments (HTA). They often ensure also that decisions about the allocation of resources meet broader policy objectives, including equity and financial protection. For example, when allocating available resources, decision-makers would make choices among different interventions, such as surgical, pharmacological and social interventions, to prevent, treat and rehabilitate various health problems in the population (e.g., injury, cardiovascular disease, cancer, diseases of neuromuscular junction or muscle etc.) across different levels and settings of service provision (e.g., primary, secondary and tertiary care). The provision of assistive products must be included in this systemic decision-making process.

Furthermore, decision-makers and system managers should seek to achieve “technical efficiency” within the system. This means that the aim should be to maximize the quality and quantity of services and products delivered throughout the system with the available resources. From a financing perspective, the goal should be to raise, pool, and allocate the maximum amount of funding throughout system with the available resources to achieve technical efficiency. This must include considerations not only of the mechanisms for raising funds (i.e. financing options), but also of the purchasing procedures, provision mechanisms, payment methods and monitoring of the system (Kutzin et al., Citation2017). For example, decision-makers and system managers should find ways to minimize the costs associated with procuring assistive products, such as hearing aids, prostheses, prescription glasses and the associated services, while maximizing coverage of the population’s needs within the available budget.

Financing decisions to achieve technical and allocative efficiencies could be informed by conducting HTAs, which include assessing the health outcomes and cost-effectiveness of assistive products through economic evaluations. Existing literature indicates improved health outcomes among users of a range of assistive products. These include users of wheelchairs (Bray et al., Citation2014; Shore, Citation2017; Toro et al., Citation2016) and hearing aids or instruments to reduce hearing impairment (Ferguson et al., Citation2017; Johnson et al., Citation2016). Assistive products could increase an individual’s ability to seek meaningful employment and lead to better productivity through enhanced personal functioning (Bell & Mino, Citation2015; Shore, Citation2017; Stumbo et al., Citation2009; World Economic Forum, Citation2016). This body of evidence could be used in HTAs to determine the individual and societal value of assistive products according to the objectives of the health systems, and guide financing decisions (e.g., maximizing health, efficiency, equity). However, it is well recognized that the technical, administrative and governance aspects of HTA’s are data- and resource-intensive. For these reasons, existing guidance, such as the WHO Priority Assistive Products List, could help to inform the choices being made to have the maximum health and economic impacts at a population level (WHO, Citation2016b).

Finally, technical solutions to improve the governance and efficiency of the system will not lead to change unless there is a supportive politico-legal environment. Purposefulness from the public, private and other non-government sectors is required to make the change. This requires cross-sector collaboration to find a consumer-centric solution. These factors, including financing, should be considered when reforming the system to improve the provision and coverage of assistive products.

Financing options for raising revenue

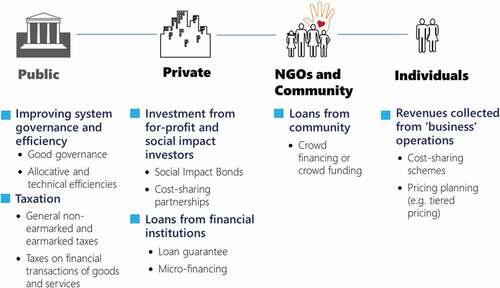

For the purpose of this paper, four broad potential sources of funding from public and privateFootnote2 sources for the provision of healthcare and social services have been presented below () for consideration by government and non-government role-players:

Taxation and social security contributions;

Investment from for-profit and social impact investors;

Loans from financial institutions and individuals; and

Revenues collected as part of “business” operations.

Figure 1. Improving system governance and efficiency and leveraging other financing options

Seven financing options that have been applied in healthcare and social service sectors have been described in Sections 3.1 to 3.7. Where applicable, specific examples for the provision of assistive products have been described in these sections. Included among these options are sources of funding that are considered to be non-traditional (also known as “innovative financing”). When considering these options, it is important to note that, while they can help to expand fiscal capacity, policy-makers need to “remain focused on total levels of public spending for health, and not merely the earmarked amount, given the possibility that budget allocations from discretionary revenues may be reduced, offsetting the revenues from newly introduced earmarked taxes” (Jowett & Kutzin, Citation2012).

Option 1: Taxation and social security contribution

Taxes and levies are the most common mechanisms that governments use to finance public provision of goods and services, with a strong public sector being the cornerstone of health financing. Many factors must be taken into consideration when designing new taxes or levies, increasing existing tax rates, broadening an existing tax base, or repurposing existing tax revenue to finance the provision of assistive products. These include political feasibility, administrative costs and benefits of taxation, economic incentives, and distributive effects of tax burden.

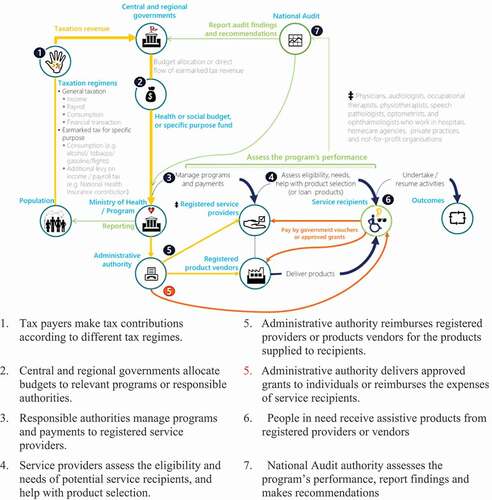

Many countries collect revenue from general taxation to support the provision of assistive products to various extents. The designs of the taxation scheme (i.e. tax structure and levels, and collection method) and how much can be raised differ vastly between countries. Some of the most common taxes include personal and corporate income tax, consumption tax (e.g., sales tax, value-added tax and excise), payroll tax, and transaction tax. In addition to general tax revenue, funding for the schemes involving the provision of assistive products typically includes supplementary revenue from compulsory monetary contributions toward national health or social security schemes (e.g., in Norway and Japan). shows a typical flow of funds through taxation.

Figure 2. Taxation and social security contribution to fund public provision of assistive products

General non-earmarked and earmarked taxes

In many countries, the governments do not allocate funding specifically for the provision of assistive products (i.e. “not earmarked”). Countries that broadly use this method of financing include Japan, Norway, and the United Kingdom (UK). Using the UK as an example, HM Revenue & Customs – the tax, payment, and customs authority – collects general tax revenue and national insurance contributions from employed individuals aged 16 years and older through payroll and income taxes. It then allocates some of the collected revenue to the Department of Health and local governments for the overall operation of health and care services, jointly provided through the National Health Service (NHS) and local government services (e.g., home modifications by local councils). The allocation of funds toward the provision of assistive products is typically not earmarked and is dependent on the decision-making and planning processes by the Clinical Commissioning Groups that consist of the local practices of general practitioners in each area.

In Japan, central governments share the financial responsibilities for the provision of disability services with the prefecture and municipal governments. For example, for people with disabilities under the age of 65 years, the national, prefecture and municipal governments, respectively, contribute toward 50%, 25%, and 25% of 90% of the total cost, with the remaining 10% being covered by individuals.

In some countries, governments implement specific levies to collect revenue to allocate toward the implementation of a designated national scheme (i.e. “earmarked” tax). Using the National Disability Insurance Scheme in Australia as an example, the Australian Government increased the Medicare levy from 1.5% to 2% of taxable income so that the additional revenue raised could be allocated to a specific purpose fund called the “Disability Care Australia Fund.” Together with general budget revenue, the fund is used for all disability care, including the provision of assistive products. In Argentina, revenue collected from taxes of bank cheque transactions is earmarked for the provision of disability services under Law 24901 enacted by the National Congress of Argentina.

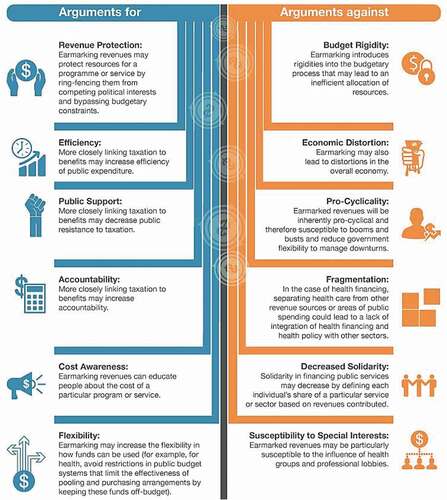

The merits, or otherwise, of financing health and social services by earmarking revenue has been a subject of much discussion. One of the main arguments for earmarking is that it ensures financial resources are used as intended (i.e. only for assistive products and other disability services), thereby enhancing accountability and, possibly, efficiency. Earmarking can be used also to improve the political acceptability of new tax measures, by explicitly linking expenditure with revenue raising. In contrast, opponents note that earmarking creates budget rigidity and can increase fragmentation (i.e. reduce pooling) of funds. illustrates the arguments for and against the earmarking of revenue.

Figure 3. Arguments for and against earmarking revenue

Taxes on financial transactions

Financial Transaction Tax (FTT) is a form of levy imposed on institutional or individual traders for the purchase or selling of shares, bonds, traded funds and derivatives and currency.Footnote3 FTT rates ranging from as low as 0.00001% to a maximum of 2% per transaction have been applied in different countries (Beitler, Citation2010). The amount of tax revenue raised varies accordingly. For example, USD 0.4 billion in revenue was raised in South Africa in 2001, and as much as £4.2 billion was raised in the UK in 2007 (Darvas & Weizsäcker, Citation2011). FTT has been implemented in many countries to serve a fiscal purpose by raising revenue and redistributing some of the vast pool of capital from private sources toward the supply of health and social services for people in need, including people who are in need of assistive products (e.g., Argentina).

Another related transaction tax is the levy on civil air transport to fund the operation of UNITAID – a global health initiative to address the world’s tuberculosis, HIV/AIDS and malaria epidemics, in partnership with public and private organizations. Currently, the levy is imposed on travelers at the point of purchase in ten countries: France, Cameroon, Chile, Congo, Guinea, Madagascar, Mali, Mauritius, Niger, and the Republic of Korea. The rates of levy and contribution from different countries vary. In France, the levy is €1 per flight ticket. Overall, this transaction tax provides 70% of UNITAID’s total funding of USD 2.5 billion since its inception in 2006 (UNITAID, Citationn.d.). In September 2015, UNITAID launched a similar financing mechanism to raise funds for nutrition programs in sub-Saharan Africa. In this case, the transaction levy is imposed on industries that extract natural resources. For example, in response to the call, the Republic of Congo imposes a 10-cent levy on every barrel of oil produced.

Like an FTT, the Road Accident Fund (RAF) in South Africa raises revenue through a Fuel Levy that is imposed on every liter of fuel sold. In 2016–2017, this levy was set at 163 cents per liter (Road Accident Fund South Africa, Citation2017). The RAF revenue collected is used to rehabilitate and compensate people injured in road accidents. People receiving compensation from the RAF may use the funds toward the purchase of assistive products.

Option 2: Social Impact Bonds

A bond is a form of financing mechanism whereby the public lend money to the bond issuers through the purchase of a bond. In return, the bond issuers would pay interest to the bond holders periodically and return the principal at a future maturity date. For the bond issuers, such as a government or company, this is an alternative financing option to seeking a loan from a single lending source, such as a commercial bank, because a bank loan usually has a more restrictive contract and a higher interest rate.

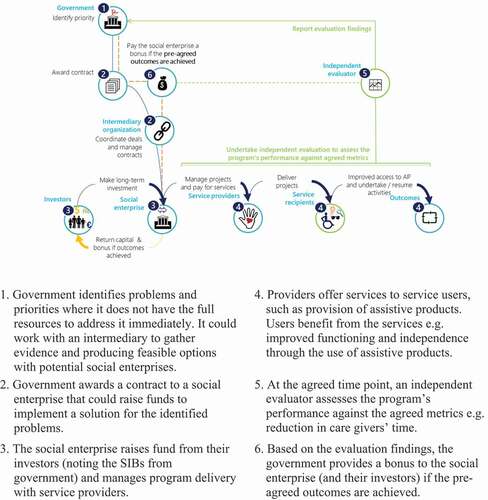

A Social Impact BondFootnote4 (SIB) is a financial instrument similar a typical bond, where the bond issuer – usually a government organization – “raises” capital from the bond holders – usually social enterprises. Unlike a typical bond, the SIB bond holders do not lend money directly to the government organization. Instead, social enterprises deliver programs on behalf of the government, using capital raised from their investors or donors. In return, social enterprises and their investors, as the bond holders, receive the capital plus performance payments from the government, upon achieving certain positive social outcomes, as stipulated in a performance contract agreed upon prior to the commencement of the program. Typically, the positive social outcomes represent a saving to the government. In other words, if the social enterprise’s program were to meet the social impact target, as ascertained by an independent evaluator, the government would pass on part of the benefits achieved as a financial reward to the social enterprises and their investors as per the agreement. If the program did not meet the minimum performance target, the government would reimburse the capital but not the bonus.

The design of SIBs carries the characteristics of a bond and pay-for-performance model to overcome several barriers for the government and the social enterprises (Harvard Kennedy School Government Performance Lab, Citationn.d.). Firstly, as mentioned in the introductory section, governments typically have many competing priorities and often aim to produce outcomes in the more immediate term. As such, SIBs are an incentive to invest in prevention that would only yield meaningful outcomes in the longer term, without the government having to commit to investment upfront. Secondly, by making performance assessment a requirement, SIBs require service delivery to be informed more effectively by data. In designing performance metrics, it would be necessary for the delivery to be customer-centric with a focus on the outcomes of program participants. Finally, SIBs bind the government, social enterprises, providers, social investors and philanthropists together in multi-year projects, thereby encouraging cross-sector collaboration (Harvard Kennedy School Government Performance Lab, Citationn.d.).

depicts the roles of stakeholders and flow of funds in SIBs. The illustration includes an intermediary between government organizations and social enterprises. This intermediary is not the commissioning government organization, social enterprises/service providers or investors. The purpose of this intermediary is to: introduce parties to the agreement; gather evidence and produce feasible options; facilitate negotiations between parties; raise investor capital; establish a special purpose vehicle; and manage performance (Centre for Social Impact Bonds, Citation2017). Social Finance in the UK is an example of such intermediary (www.socialfinance.org.uk).

Figure 4. Social Impact Bond

The world’s first SIB – the Peterborough Social Impact Bond in the UK – commenced in 2010. This bond was for a program called One Service implemented at the Peterborough Prison. The program involved pre- and post-release supports, with a view to reducing repeat offense among adult male offenders who participated in the program. In July 2017, an independent evaluator confirmed that the program had achieved its outcomes as previously agreed upon. In accordance with the contract, the bond-holders were rewarded with performance bonuses (Social Finance, Citation2017).

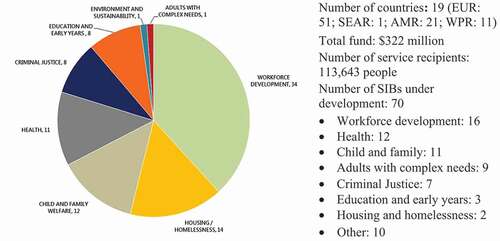

Since the Peterborough Social Impact Bond, SIBs have been used to support the delivery of a range of social programs around the world. These include programs for workforce development, health, criminal justice, and early year education. Most of these programs are for workforce development in the WHO European and American regions (). In other WHO regions, there are many SIBs being developed (e.g., scale and replicate successful eye health delivery models in Cameroon). Examples of outcome metrics for these programs include: reduction in rate re-offense, increase in the number of unemployed individuals succeeding in finding stable employment, and reduction in low-birth-weight births.

Figure 5. Number of Social Impact Bonds by issue area, 2010–2017

SIBs have not been used within the disability and assistive product sector. Similar to other complex social interventions, SIBs might not be well suited to all programs in the assistive product sector because of the difficulties in obtaining the measurement of outcomes required to facilitate payment mechanisms. However, there has been interest in assessing the feasibility of applying SIBs for some programs in this sector. Examples include:

Developing an SIB scheme to support adults with disabilities obtaining employment by London Borough of Tower Hamlets in the UK; and

Developing new services to help young people with learning disabilities and high risk behaviors to receive residential education and/or care entry by Bradford Clinical Commissioning Groups in the UK, with a view to supporting these people to remain at home, as well as generating financial savings for the commissioners (Gribbin et al., Citation2016).

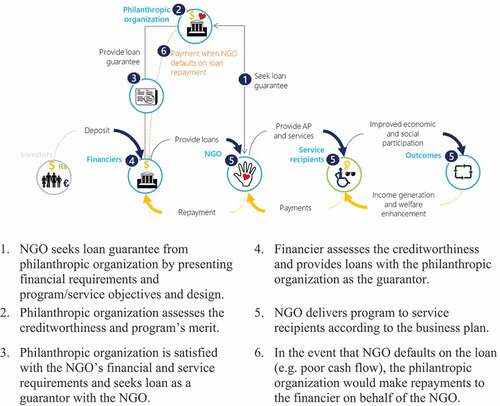

Option 3: Loan guarantees

Many nonprofit service providers that serve people with functional difficulties have limited assets and revenue streams. This creates difficulties when they try to seek a loan from a banking institution because the bank might consider their overall financial position as not being sufficient to meet their debt obligation. For these organizations, a loan guarantee from a third party, such as a private institution or philanthropic organization, might be an option. In this case, rather than seeking direct funding from the guarantor, the organization requests the guarantor to take on their debt obligation, partially or in full, only in the event of default in debt repayment. In some cases, it might be necessary for the guarantor to provide some funding to act as a security against commercial bank lending. In providing a guarantee, it would be necessary for the guarantor to ensure the creditworthiness of the organization and the merit of the business proposal. shows an overview of a loan guarantee.

Figure 6. Loan guarantee

The successful partnership between the Ford Foundation and the Grameen Bank in 1981 is one example of a loan guarantee. The Ford Foundation provided an $800,000 loan guarantee fund to the Grameen Bank to support a loan from commercial banks in Bangladesh. The Grameen Bank then used the loan to implement the planned expansion of its microfinancing operations. The repayment model was executed as planned and the commercial banks received repayment of the loan with interest (Lawry, Citation2008). A more recent example is the $30 Million Credit Support Agreement between the Bill & Melinda Gates Foundation and KIPP Houston Public Schools. This helped KIPP Houston secure $300 million in tax-exempt bond issuance so that it could further public charter school expansion in Houston (Bill & Melinda Gates Foundation, Citation2009).

Loan guarantees have been used also to help individuals obtain assistive products. For example, the GettingAhead Association and Tech-Able Incorporated, in the US State of Georgia, jointly offer a loan guarantee program called “Credit-Able.” This program provides guarantees to enable loans for assistive technology, including home and vehicle modifications, for successful applicants. The successful applicants must meet the following requirements (GettingAhead Association & Tech-Able Incorporated, Citation2017):

Georgians with a disability, and their family members or legal guardians;

Employers who want to modify their worksite for an employee with a disability who is a resident of Georgia;

Individuals who demonstrate the ability to repay the loan.

This program was authorized under the Assistive Technology Act of 1998. The funding source of the program is grants from the US Department of Education and other state and private contributors (GettingAhead Association & Tech-Able Incorporated, Citation2017).

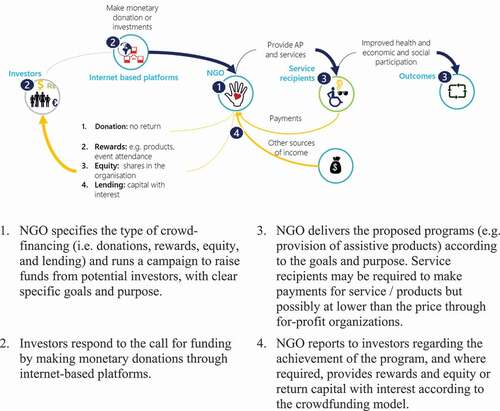

Option 4: Crowd financing or crowdfunding

The purpose of crowd financing or crowdfunding is to raise small amounts of funds from many people. It is a form of financing used typically by small organizations or start-up entrepreneurs whose credit history and business proposition present a risk that is higher than what traditional banking institutions or guarantors would normally accept.

The advent of internet-based platforms (e.g., StartSomeGood, Kickstarter, Indiegogo, Rockethub, Pozible, Causes, Razoo, Crowdrise, FUNDFLY) has made the capital-pooling mechanism and governance of crowd financing more efficient by bringing fund-seeking organizations and entrepreneurs closer to potential donors and investors through the removal of intermediaries such as the banks. The crowdfunding sector has grown substantially over the past decade because of these internet-based platforms. Based on an industry assessment in 2015, it was found that the total global crowdfunding industry had an estimated fundraising volume of USD 34 billion (Massolution, Citation2015).

There are four broad types of crowd financing: donations, rewards, equity, and lending (Fundable, Citation2017). For donation-based crowdfunding, “investors” contribute small monetary contributions in good faith to support a cause they believe in, without an expectation of receiving a reward but, perhaps, with an expectation that their money will be and has been put into good use. In contrast, reward-based crowdfunding attracts investors’ interest by offering small rewards in return for their monetary contribution (CrowdfundingPR, Citation2017). Rewards offered might include: Physical (a product); Creative (input into the project); Experiential (attending an event); Sentimental (rewards for friends/family as a show of their support); or Exclusivity (early-access to products).

The equity and lending models are similar to the reward model, except that individuals invest money in exchange for actual shares in the organization (equity) or a return of the invested capital with a set interest rate over a pre-determined period (lending). The target amount of funding for the equity and lending-based models is typically much higher (more than USD 100,000) than donation-based and reward-based models (under USD 10,000). is a schematic representation of a crowd-financing mechanism.

Figure 7. Crowd-financing

Irrespective of the models, the following principles are common to all the mechanisms to ensure the success of crowd financing: 1) building trust with the target community; 2) having a clear specific goal and purpose for the fund (project aims and timeframe, who is involved, how the fund will be used, how success is measured); and 3) choosing the model of crowd-financing appropriate for the purpose.

The A Ray of Hope project in Tiruvannamalai, India is an example of the use of crowd financing (Morgan, Citation2017). The purpose of the program is to build an Integral Education and Therapy Center that will serve one hundred children who have physical and mental disabilities. The program has offered education services and medical care such as physical therapy, sensory integration, hydrotherapy and proper medical care. The aim of this program is also to raise awareness about the importance of providing education and services to children with disabilities (Morgan, Citation2017). Through a crowdfunding platform, the program was able to raise USD 257,896 (unverified) for furnishing and equipping the center (Morgan, Citation2017). Some of the success factors of this crowdfunding campaign include: partnership with a well-established organization (the Sylvia Wright Foundation) and with a local organization (Gayathri and Namith Architects); clearly stated purpose and goals; and frequent updates to donors.

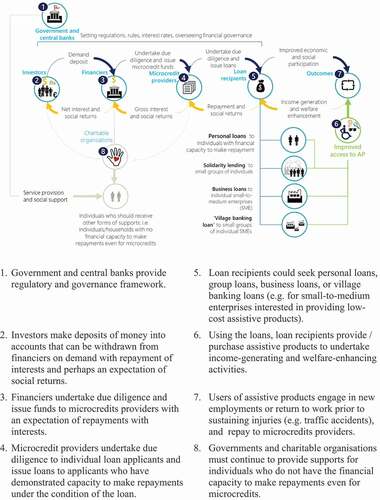

Option 5: Microfinance

Microfinance is a financing mechanism for individuals or groups of individuals with low income who would otherwise have no access to financial services. These services include small loans, insurance, and money transfers. In many countries, people only have access to credit through either informal money lenders or commercial banks. At its most basic level, microfinance institutions provide a financing option that bridges the gap between informal money lenders and commercial banks: on the one hand, microfinance is a more structured and reliable service than that which informal money lenders can typically offer; on the other hand, microfinance institutions offer loans that are much smaller than what commercial banks would typically consider as being “cost-effective.” Microfinance institutions also provide financial services to people whom a bank would typically consider to be not credit-worthy because of a lack of documented proof of income, asset holding and established credit history. To mitigate this risk, microfinance institutions ensure repayment through “social collateral” using group co-guarantees, peer pressure, joint liability, and a variety of similar mechanisms. In this case, the loan is given to self-help groups, solidarity groups or village banking.

(p. 15) shows a summary of the roles of various stakeholders and the flow of funds in microfinancing. It also shows the sub-options that could be used to support people with functional difficulties to access assistive products.

Figure 8. Microfinance

Over the past decades, microfinance has evolved to become a significant industry in many developing countries. A survey estimated that 3,652 microfinance institutions reportedly reached 205.3 million clients globally by December 2010 (Maes & Reed, Citation2012). However, this rapid growth over the decades, coupled with poor financial governance in some countries, has caused notable failures in certain regions and, indeed, harmed the microcredit recipients, for example, in Andhra Pradesh in India (World Bank/CGAP, Citation2010) and Ashanti Region in Ghana (Godwin Boateng et al., Citation2016). Despite these examples, the microfinance sector has shown that providing financial services to people with little financial means on a large scale is possible.

However, microfinance has largely excluded people with disabilities, and possibly other people with functional difficulties. Mersland (Citation2004) noted four primary reasons why people with disabilities have been excluded as follows:

Self-exclusion: a lack of self-confidence and knowledge regarding the benefits of financial services, and an expectation to be reliant on charity among some people with disabilities;

Exclusion by other members: inability to join “social collateral” groups because other members do not want to share liability jointly with people with disabilities;

Exclusion by staff: staff of microfinance institutions might not be able to differentiate between real and perceived credit risk because of preconceived prejudices about people with disabilities; and

Exclusion by design: upfront fee and repayment frequency might be higher than what a person with a disability can achieve.

Notwithstanding these reasons, microfinance might be appropriate for some people with functional difficulties, such as those people who are employed, and those people who could gain/improve functional abilities using assistive products to the extent that they are able to participate in income-generating or welfare-enhancing activities. Indeed, there has been increasing interest in encouraging the use of microfinancing in the disability sector. For example, BRAC – a multinational development organization – developed a partnership in August 2011 with the Center for Rehabilitation for the Paralyzed (CRP) in Bangladesh to provide microfinance services to CRP’s members. By July 2014, the pilot initiative had provided loans to 3000 clients with disabilities, with an average disbursed loan size of USD 582 (BRAC, Citation2011). Most of the clients were entrepreneurs, owning and operating grocery shops, tea stalls and small vending businesses. All of the clients were able to meet their repayments (BRAC, Citation2011). Furthermore, all clients saved regularly with an average savings account balance of USD 125 (BRAC, Citation2011). Based on this successful pilot, BRAC has expanded its partnership with another NGO working with people with disabilities in Bangladesh – Action on Disability and Development.

Option 6: Cross-sector partnerships

Nonprofit organizations might consider gaining access to the financial resources of the for-profit sector through partnering with a for-profit organization that has a shared purpose, aligned interests and mutually acceptable organizational culture (e.g., a “profit-with-purpose” business interested in impact investing). For example, the two organizations might adopt a cost-sharing partnership in which each party contributes different resources, such as facilities, staff, or equipment, toward the common cause. The for-profit organization might gain access to a larger market for the sales of its products through the collaboration with the nonprofit organization. The partnership might also generate recognition and goodwill. With the contribution from the for-profit organization, programs of the nonprofit organization might reach a greater number of people in need. The partnership might also attract other in-kind donations and professional development for employees of the nonprofit organization.

One example is the partnership between Essilor International – the world’s largest manufacturer of ophthalmic lenses – and two, nonprofit, eye hospitals in India – Aravind and Sankara Neth-ralaya. The aim of the partnership is to provide eye care and distribute spectacles to people living in rural India by hosting two-day, outreach “eye camps” in villages across India. Eye care services are provided through tele-ophthalmology vans and refraction vans that are fully equipped for screening for various eye disorders and dispensing custom-made spectacles (Karnani et al., Citation2011).

In this partnership, Essilor has provided the refraction vans, grinding materials and lens materials, and has provided training to optometrists. On the other hand, the hospitals have paid for the tele-ophthalmology vans and all operating costs such as wages and fuel. The project has also received funding from local government authorities, NGOs and philanthropists (Karnani et al., Citation2011). By providing low-cost spectacles priced from USD 4 to USD 8, Essilor was able to cover its operational costs in 2010, but with an expectation to make a profit from the deeper market penetration (Karnani et al., Citation2011).

In 2015, Essilor reported having 18 refraction vans in operation for the program. Since 2006, the program has reportedly visited 6000 rural villages, educated 900,000 people about vision health and dispensed 300,000 eyeglasses (Essilor International, Citation2015). Essilor was developing similar programs for rural communities in China (Essilor International, Citation2015).

Option 7: Revenue collected from ‘business’ operation

Sharing costs with end-users

A range of cost-sharing methods with end-users have been adopted for healthcare schemes globally. Cost-sharing enables the providers to recover some proportion of the costs of service provision. More fundamentally, by having the end-users sharing an adequate amount of the costs, the aim of cost-sharing schemes is to moderate users’ demand for the goods and services on offer to facilitate appropriate and efficient consumption.

Some of the most common examples of cost-sharing methods are listed and explained below:

Co-payment: A user pays for part of the costs for every count or “episode” of service. The amount is set as a fixed amount, or a set percentage of the total costs. However, percentage co-payment should be avoided because it is known to expose people to health system inefficiencies and a higher likelihood of catastrophic spending (World Health Organization Regional Office for Europe, Citation2019).

Cap: A user does not pay, or has reduced payments, below a set limit. After the cap is reached, the service user must make full payment.

Deductible: A user pays the full cost of the service until a limit is reached. After the deductible amount is reached, the user either does not pay or has reduced payments (i.e. the opposite of a “capping” scheme).

Premium: A user must pay a fixed amount of a fee to be eligible for receiving goods or services (i.e. similar to a membership fee). The user may incur other fees at the point of consumption.

To protect the consumers from financial catastrophe, some of the cost-sharing schemes have parallel schemes to provide financial safeguards. These include setting a maximum out-of-pocket limit where the service users only pay up to a fixed limit or as a percentage of their incomes. Upon reaching the limit, the (public/private) insurers or service providers would cover the full costs.

In practice, cost-sharing schemes might have varying effects on consumption and cost recovery. On the one hand, no cost-sharing scheme would completely counter inefficient consumption behavior. On the other hand, cost-sharing might inadvertently create barriers for people to seek appropriate care, especially people who are most in need but have the least financial means. This would therefore jeopardize the fundamental motivation of service provision to reach people who are most in need. Cost-sharing schemes might also have minimal impact on the overall expenditure because, by design, they are intended only to recover a relatively small proportion of the total costs. The impact of user fees on health service utilization has been reported in systematic reviews (Kiil & Houlberg, Citation2013; Legarde & Palmer, Citation2008).

As indicated in the evidence above, system managers in the assistive product sectors should consider the consequences of introducing cost-sharing with caution, in line with the context of their service provision (e.g., clientele, budgetary and service goals etc.). System managers should also make sure that the time and effort required to administer the cost-sharing scheme is commensurate with the amount of money that could be raised. Finally, system managers should also seek insights from other countries where cost-sharing has been part of the system for provision of assistive products. Some examples include:

Japan’s programs delivered under the General Supports for Persons with Disabilities Act and long-term care insurance system (“Kaigo Hoken”) both of which require a 10% payment contribution toward the total cost from the recipient of assistive products.

In Manitoba, Canada, there are different cost-sharing structures for different assistive products. For example, the Manitoba Health Healthy Living and Seniors (MHHLS) allows one hearing product per ear every four years. There is a $75 deductible on all claims, after which MHHLS reimburses 80% of a fixed amount for a product or additional services (e.g., ear molds), up to a maximum of $500-$1,800 per ear. In comparison, the Manitoba Community Wheelchair Program covers 50% of the costs of an approved wheelchair, to a maximum of $2,500 per year.

In South Africa, the level of subsidy from the public system depends on patient groups classified according to income. The amount covered ranges from full subsidy to 25% of the total cost.

In the Philippines, cost-sharing arrangements differ according to the source of assistive products. For members of the public UHC scheme, administered by PhilHealth, product recipients would incur an out-of-pocket cost only if the product is not within the coverage, or if they opt-out of “No Balance Billing” to receive an “upgraded” device. Furthermore, product recipients would make payment if the cost of the device is above the fixed, per capita, budget allocation. The system does offer 20% discount to people with disabilities and senior citizens.

Pricing planning

Planning for the pricing of products and services could help to meet the revenue goal of assistive product provision, while minimizing the impact of consumers’ out-of-pocket costs. One example is to structure the prices according to the product characteristics and to consider the consumer’s overall willingness and ability to pay, using the Timor-Leste National Spectacle Program explained below.

The Timor-Leste National Spectacle Program is a public-private partnership program between the Timor-Leste Government and national and international NGOs: Fo Naroman Timor-Leste and the Fred Hollows Foundation. The Timor-Leste Government funded most of the refraction staff and clinical infrastructure. The NGOs delivered the program using grants from foreign governments and donations of new spectacles and lenses (e.g., off-season design) from manufacturers or optometric practices.

To structure the pricing of spectacles during the program, a survey was conducted of 152 people in Timor-Leste who were agreeable to wearing spectacles, if required, to ascertain their willingness to pay for ready-made spectacles. The survey found that 84.9% of the respondents were willing to pay for the spectacles. Among these, 31.6%, 58.6%, and 82.9% of the respondents were willing to pay at least USD 1.00, USD 0.25, and USD 0.10 for the spectacles, respectively. Overall, 96.3% of the stated willingness to pay at least USD 0.10 was predictive of the preferred price (Ramke et al., Citation2009).

Based on the findings of this survey, a pricing structure was adopted for the national program, ranging from USD 0 for basic ready-made plastic spectacles to USD 25 for a pair of custom-made, multi-focal glasses. Over an 18-month observation period between March 2007 and August 2008, the program dispensed 5168 ready-made spectacles and 1015 custom-made spectacles. The profit generated from higher priced spectacles was used in the program to cross-subsidize the provision of basic ready-made spectacles for people living in rural areas, with low income, who attended outreach services. Overall, the program generated a profit of USD 13,793 from the provision of spectacles. Accounting for the operational costs of the 18-month outreach service, at approximately USD 11,600, the program was left with approximately USD 2,200 (Ramke et al., Citation2012). While this amount was unlikely to meet the full cost of service administration and other expenses, the findings showed that appropriately structured pricing could enhance the financial viability of provision of assistive products.

Summary

The common problems in the provision of assistive products that have led to the under-funding and under-provision of these products in many countries were discussed in this paper. These include competing health and social care priorities, and governments’ limited capacity to raise revenue through taxation schemes. The provision of assistive products is often fragmented by duplicated programs and parallel financial flows, thereby creating inefficiencies and confusion for the users of the “system.”

The overarching solution to these problems is to improve the governance and efficiency of the system. This involves diligently observing the principles of good governance.

On the technical side, decision-makers and system managers should take a systems perspective when considering what services and products should be included in the benefit package, as informed by health technology assessments, taking the objectives of the health system into consideration. This package ought to include cost-effective assistive products needed by the population. It also means that the aim of the system should be to maximize the quality and quantity of services and products delivered with the available resources by scrutinizing every step of the provision process. Regarding financing, as a general principle, this scrutiny should include seeking ways to achieve efficiency in raising funds, procurement, provision, payment, and monitoring the system.

Finally, using any financing methods to close the financing gap will require governments’ support. No alternative financing methods will close the financing gap entirely in the absence of inputs from governments. Some examples of how governments could play a role include:

Governments should commit funding to complement any alternative funding or service models from the non-government sector. For example, the governments must provide assistive products to people whose functional difficulties are so severe that these people are precluded from participating in any form of financing scheme (e.g., microfinancing, SIB).

Governments’ investments in the assistive product sector or disability sector might also send positive signals to the private sector to boost their investment confidence. This will stimulate industry development and attract more private and institutional investment as well as encourage innovation (see examples in the provision of hearing aids (Seelman & Werner, Citation2014)).

Governments should investigate the expansion and re-design of the existing provision of services to support the implementation of any alternative financing options for assistive products. Areas that governments could consider include: (1) focusing on people with the greatest needs that the private sector or NGOs are not able to service; and (2) redeploying existing capital accordingly.

Governments need to provide clarity regarding legal, regulatory, financial and fiduciary requirements.

Disclaimers

Kiu Tay-Teo and Matthew Jowett are WHO employees. The conclusions in this manuscript are theirs as individuals and do not represent WHO policy.

Acknowledgments

Johan Borg provided comments on an early draft.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 Josephine Bundoc (Philippines), Nazmul Bari (Bangladesh), Silvana Contepomi (Argentina), Brian Donnelly (United Kingdom), Brian Everton (Canada), Takenobu Inoue (Japan), Jytte Jepsen (Norway), Ed Mylles (United Kingdom), Peter Ngomwa (Malawi), Jacqueline Ramke (New Zealand), Elsje Scheffler (South Africa), Keren Worsley (United Kingdom).

2 From a health financing policy perspective, public sources include those which are compulsory and pre-paid, whilst voluntary sources are considered private (Jowett & Kutzin, Citation2012).

3 When applied to the foreign exchange market, it is known as a “Tobin tax” eponymously named after the Nobel Laureate Economist James Tobin.

4 Also referred to in the literature as “Pay for Success Financing”, “Pay for Success Bond”, “Social Benefit Bond” and “Social Bond”.

References

- Beitler, D. (2010). Raising revenue - A review of financial transaction taxes throughout the world. www.revangeldesigns.co.uk © Health Poverty Action and Stamp Out Poverty, September 2010

- Bell, E. C., & Mino, N. M. (2015). Employment outcomes for blind and visually impaired adults. Journal of Blindness Innovation and Research, 5(2), 1–12. https://doi.org/https://doi.org/10.5241/5-85

- Bill & Melinda Gates Foundation. (2009). Foundation provides $30 million credit support agreement to secure $300 million in charter school facility financing. Retrieved September 23, 2017, from www.gatesfoundation.org/Media-Center/Press-Releases/2009/11/$30-Million-Credit-Support-Agreement-to-Secure-$300-Million-in-Charter-School-Facility-Financing

- Boot, F. H., Owuor, J., Dinsmore, J., & Maclachlan, M. (2018). Access to assistive technology for people with intellectual disabilities: A systematic review to identify barriers and facilitators. Journal of Intellectual Disability Research, 62(10), 900–921. https://doi.org/https://doi.org/10.1111/jir.12532

- Borg, J., & Östergren, P.-O. (2015). Users’ perspectives on the provision of assistive technologies in Bangladesh: Awareness, providers, costs and barriers. Disability and Rehabilitation. Assistive Technology, 10(4), 301–308. https://doi.org/https://doi.org/10.3109/17483107.2014.974221

- BRAC. (2011). BRAC microfinance programme. http://www.brac.net/sites/default/files/disability/MF.pdf

- Bray, N., Noyes, J., Edwards, R. T., & Harris, N. (2014). Wheelchair interventions, services and provision for disabled children: A mixed-method systematic review and conceptual framework. BMC Health Services Research, 14(1), 309. https://doi.org/https://doi.org/10.1186/1472-6963-14-309

- Centre for Social Impact Bonds. (2017). Intermediaries. Retrieved September 21, 2017, from https://data.gov.uk/sib_knowledge_box/intermediaries

- Chadha, S., Moussy, F., & Friede, M. H. (2014). Understanding history, philanthropy and the role of WHO in provision of assistive technologies for hearing loss. Disability and Rehabilitation. Assistive Technology, 9(5), 365–367. https://doi.org/https://doi.org/10.3109/17483107.2014.908962

- CrowdfundingPR. (2017). 25 killer kickstarter reward ideas. Retrieved October 5, 2017, from http://www.crowdfundingpr.org/25-killer-kickstarter-reward-ideas/

- Darvas, Z., & Weizsäcker, J. (2011). Financial transaction tax: Small is beautiful. Society and Economy, 33(3), 449–473. https://doi.org/https://doi.org/10.1556/SocEc.33.2011.3.2

- Essilor International. (2015). See change - Our contributiong to sustainable development (Essilor International).

- Ferguson, M. A., Kitterick, P. T., Chong, L. Y., Edmondson-Jones, M., Barker, F., & Hoare, D. J. (2017). Hearing aids for mild to moderate hearing loss in adults. Cochrane Database of Systematic Reviews, 9, CD012023 doi:https://doi.org/10.1002/14651858.CD012023.pub2 RetrievedSep September 2017. https://doi.org/https://doi.org/10.1002/14651858.CD012023.pub2

- Fundable. (2017). Types of crowdfunding | Fundable. Retrieved October 5, 2017, from https://www.fundable.com/crowdfunding101/types-of-crowdfunding

- Galway, L. P., Corbett, K. K., & Zeng, L. (2012). Where are the NGOs and why? The distribution of health and development NGOs in Bolivia. Globalization and Health, 8(1), 1. https://doi.org/https://doi.org/10.1186/1744-8603-8-38

- GettingAhead Association, & Tech-Able Incorporated. (2017). Credit-able: A loan guarantee service for assistive technology, and home and vehicle modifications. www.gettingaheadassoc.org/files/gaataft/1/file/credit-able_factsheet.pdf

- Godwin Boateng, F., Nortey, S., Asamanin Barnie, J., Dwumah, P., & Acheampong, M. (2016). Collapsing microfinance institutions in Ghana: An Account of how four expanded and imploded in the Ashanti Region. International Journal of African Development, 3 2 , 37–62. http://scholarworks.wmich.edu/cgi/viewcontent.cgi?article=1048&context=ijad

- Graham, J., Amos, B., & Plumptre, T. (2003, August). Principles for good governance in the 21st century. Policy Brief, (15), 9. http://unpan1.un.org/intradoc/groups/public/documents/UNPAN/UNPAN011842.pdf

- Gribbin, R., Uk, R., Hull, D., & Uk, D. (2016). Bradford child learning disabilities social impact bond feasibility study business case summary. http://www.airedalewharfedalecravenccg.nhs.uk/wp-content/uploads/2016/09/2016-52-Appendix-1-Bradford-Child-Learning-Disabilities-Social-Impact-Bond-Feasibility-Study.pdf London: Social Finance

- Harvard Kennedy School Government Performance Lab. (n.d.). Pay for success—Social Impact Bonds | Government performance lab. Retrieved September 21, 2017, from https://govlab.hks.harvard.edu/social-impact-bond-lab

- Johnson, C. E., Danhauer, J. L., Ellis, B. B., & Jilla, A. M. (2016). Hearing aid benefit in patients with mild sensorineural hearing loss: A systematic review. Journal of the American Academy of Audiology, 27(4), 293–310. https://doi.org/https://doi.org/10.3766/jaaa.14076

- Jowett, M., & Kutzin, J. (2012). Raising revenues for health in support of UHC: Strategic issues for policy makers. Health Financing Policy Brief, 1 https://apps.who.int/iris/bitstream/handle/10665/192280/WHO_HIS_HGF_PolicyBrief_15.1_eng.pdf?sequence=1.

- Karnani, A., Garrette, B., Kassalow, J., & Lee, M. (2011). Better vision for the poor. Stanford Social Innovation Review, 9(2), 66–71. https://doi.org/https://doi.org/10.2139/ssrn.1569479

- Kiil, A., & Houlberg, K. (2013). How does copayment for health care services affect demand, health and redistribution? A systematic review of the empirical evidence from 1990 to 2011. The European Journal of Health Economics, 15(8), 813–828. https://doi.org/https://doi.org/10.1007/s10198-013-0526-8

- Kutzin, J., Witter, S., Jowett, M., & Bayarsaikhan, D. (2017). Developing a national health financing strategy: A reference guide. World Health Organization. http://www.who.int/health_financing

- Lawry, S. 2008. Early Ford Foundation support for the Grameen Bank: Lessons in philanthropic accountability, risk, and impact. https://cpl.hks.harvard.edu/files/cpl/files/workingpaper_44.pdf The Hauser Center for Nonprofit Organizations, Harvard University

- Legarde, M., & Palmer, N. (2008). The impact of user fees on health service utilization in low and middle-income countries: How strong is the evidence? Bulletin of the World Health Organization, 86(11), 839–848. https://doi.org/https://doi.org/10.2471/BLT.07.049197

- Maes, J. P., & Reed, L. R. (2012). State of the microcredit summit campaign report 2012. Microcredit Summit Campaign. http://www.microcreditsummit.org/uploads/resource/document/web_socr-2012_english_62819.pdf

- Makinde, O. A., Meribole, E. C., Oyediran, K. A., & Fadeke, A. (n.d.). Duplication of effort across development projects in Nigeria : An example using the master health facility list. Online Journal of Public Health Informatics, 10(2 e208 doi:https://doi.org/10.5210/ojphi.v10i2.9104). https://doi.org/https://doi.org/10.5210/ojphi.v10i2.9104

- Massolution. (2015). Crowdfunding industry statistics 2015–2016. Retrieved November 14, 2017, from http://crowdexpert.com/crowdfunding-industry-statistics/

- Mersland, R. (2004). Microcredit for self-employed disabled persons in developing countries (Oslo: The Atlas Alliance). https://www.microfinancegateway.org/sites/default/files/mfg-en-paper-microcredit-for-self-employed-disabled-persons-in-developing-countries-2005.pdf

- Morgan, L. (2017). A Ray of Hope. Retrieved November 14, 2017, from https://fundly.com/arayofhope

- Palmer, S., Torgerson, & . (1999, April). Economics notes definitions of efficiency. BMJ, 318 7191 , 1136 doi:https://doi.org/10.1136/bmj.318.7191.1136 Retrieved24 April 1999.

- Ramke, J., Brian, G., & Palagyi, A. (2012). Spectacle dispensing in Timor-Leste: Tiered-pricing, cross-subsidization and financial viability. Ophthalmic Epidemiology, 19(4), 231–235. https://doi.org/https://doi.org/10.3109/09286586.2012.680528

- Ramke, J., Palagyi, A., du Toit, R., & Brian, G. (2009). Stated and actual willingness to pay for spectacles in Timor-Leste. Ophthalmic Epidemiology, 16(4), 224–230. https://doi.org/https://doi.org/10.1080/09286580902999447

- Road Accident Fund South Africa. (2017). Fuel levy. Retrieved October 4, 2017, from https://www.raf.co.za/About-Us/Pages/Fuel-Levy.aspx

- Seelman, K. D., & Werner, R. (2014). Technology transfer of hearing aids to low and middle income countries: Policy and market factors. Disability and Rehabilitation. Assistive Technology, 9(5), 399–407. https://doi.org/https://doi.org/10.3109/17483107.2014.905641

- Shore, S. (2017). The long-term impact of wheelchair delivery on the lives of people with disabilities in three countries of the world research methods. African Journal of Disability, a344.

- Social Finance. (2017). World’s 1st Social Impact Bond shown to cut reoffending and to make impact investors a return. Press release. http://www.socialfinance.org.uk/wp-content/uploads/2017/07/Final-press-release-PB-July-2017.pdf

- Stumbo, N. J., Martin, J. K., & Hedrick, B. N. (2009). Assistive technology: Impact on education, employment, and independence of individuals with physical disabilities. Journal of Vocational Rehabilitation, 30(2), 99–110. https://doi.org/https://doi.org/10.3233/JVR-2009-0456

- Toro, M. L., Eke, C., & Pearlman, J. (2016). The impact of the World Health Organization 8-steps in wheelchair service provision in wheelchair users in a less resourced setting: A cohort study in Indonesia. BMC Health Services Research, 16(1), 26. https://doi.org/https://doi.org/10.1186/s12913-016-1268-y

- UNITAID. (n.d.). About us - Unitaid. Retrieved September 18, 2017, from https://unitaid.eu/about-us/#en

- United Nations Economic and Social Comission for Asia and the Pacific. (2009). What is good governance? https://doi.org/https://doi.org/10.1016/B978-012397720-5.50034-7

- Vassall, A., Shotton, J., Reshetnyk, O. K., Hasanaj-goossens, L., Weil, O., & Vohra, J. (2014). Tracking aid flows for development assistance for health, Global Health Action, 7(1), 23510 - https://doi.org/http://dx.doi.org/10.3402/gha.v7.23510.

- World Bank/CGAP. (2010). Andhra Pradesh 2010: Global implications of the crisis in Indian microfinance. CGAP Focus Note 67 , (November), 1–8. https://www.cgap.org/sites/default/files/CGAP-Focus-Note-Andhra-Pradesh-2010-Global-Implications-of-the-Crisis-in-Indian-Microfinance-Nov-2010.pdf

- World Economic Forum. (2016). Eyeglasses for global development: Bridging the visual divide. http://www3.weforum.org/docs/WEF_2016_EYElliance.pdf

- World Health Organization Regional Office for Europe. (2019). Can people afford to pay for health care? (Barcelona: WHO Barcelona Office for Health Systems Strengthening)

- World Health Organization. (2016a). Improving access to assistive technology - The need for assistive technology. Executive Board 139th session - Provisional agenda item 6.2 EB139/4 Geneva. http://apps.who.int/gb/ebwha/pdf_files/EB139/B139_4-en.pdf

- World Health Organization. (2016b). Priority assistive products list (Geneva: World Health Organization). http://www.who.int/phi/implementation/assistive_technology/low_res_english.pdf

- World Health Organization. (2019). Assistive technology in Tajikistan: Situational analysis (Copenhagen: WHO Regional Office for Europe).