?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Homeownership rates have been slow to recover since the financial crisis. Minority groups such as Blacks and Hispanics have been particularly slow to transition to homeownership. Using uniquely constructed anonymized household panel data obtained from a credit bureau, we find that Blacks and Hispanics were, respectively, one half and two thirds as likely as Whites to transition to mortgage ownership between 2012 and 2018. We analyze the role of credit attributes, among other factors, in explaining the racial/ethnic gap in transition to mortgage ownership by 2018 for a sample of individuals who were nonmortgage holders in 2012. Using the Blinder–Oaxaca decomposition technique for nonlinear equations, we find that racial/ethnic differences in credit attributes explain a large portion of the White–minority gap in the transition rates. However, there are key differences in experience across the two minority groups. Whereas racial/ethnic differences in geographic location contribute substantially to the White–Hispanic gap in the mortgage transition rate, racial/ethnic differences in household composition and income growth matter more in explaining the White–Black gap in the mortgage transition rate. Lastly, we find there is considerable heterogeneity across states in the contribution of credit attributes and geography to the White–minority gap in the transition rate.

By nearly all measures, the Great Recession of 2008–2009 was the most severe economic contraction in the United States since the Great Depression. The crisis has led to dramatic changes in the U.S. residential mortgage market. The homeownership rate declined substantially, from 67.4% in 2009 to 64.4% in 2018, according to the U.S. Census Bureau’s Housing Vacancy Survey data.Footnote1 The Black and Hispanic homeownership rates also declined during this time.Footnote2 At the center of the Great Recession was a subprime mortgage crisis that disproportionately affected Black and Hispanic homeowners. New mortgage originations declined whereas foreclosures and other reversals in homeownership increased, wiping out gains in minority homeownership rates. An estimated 8% of Black and 8% of Hispanic homeowners who obtained a mortgage between 2005 and 2008 lost their homes to foreclosure by 2009, compared with 4.5% of non-Hispanic White homeowners (Bocian, Ernst, & Li, Citation2010).

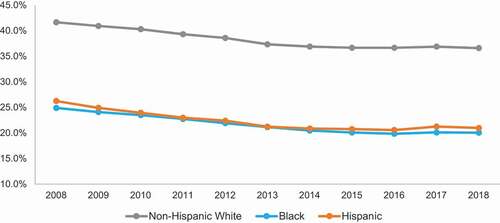

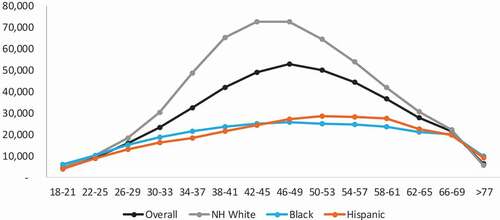

In 2006, 25% of 12.2 million new mortgagesFootnote3 were to Black or Hispanic borrowers, according to the Home Mortgage Disclosure Act (HMDA) data. By 2009, only 12% of 8.3 million new mortgages were originated to Black or Hispanic borrowers. plots the annual individual-level ownership rate of houses with a mortgage or loan using 1-year American Community Survey public-use microdata (ACS PUMS), for non-Hispanic Whites, Blacks, and Hispanics respectively.Footnote4 As the figure suggests, Black and Hispanic mortgage ownership rates declined from 25% and 26% in 2008 to 20% and 21% in 2018, respectively. As of 2018, the White–Black and White–Hispanic mortgage ownership gaps stood at roughly 17 percentage points and 16 percentage points, respectively. In this article, we focus on the trends in new mortgages as a key component in understanding the trends in racial differences in mortgage ownership.

Figure 1. Annual mortgage ownership rate at the individual level, 2008–2018

Historically, several government policies have been successful in increasing access to mortgage financing for minority borrowers, such as the government-regulated Government Sponsored Enterprise (GSE) mortgages, the Community Reinvestment Act (CRA) and GSEs’ affordable housing goals (Bostic & Surette, Citation2001; Gabriel & Rosenthal, Citation2008),Footnote5 and low-down payment mortgages backed by Ginnie Mae and GSEs. Despite these initiatives, the racial/ethnic homeownership gap is far from being alleviated, and in fact has been widening for Blacks since the financial crisis. Although there has been a slight uptick in the Hispanic homeownership rate during the recovery period from the Great Recession, the Black homeownership rate was at the same level in 2019 as in 1968 when the Fair Housing Act was adopted. What are some major barriers to mortgage ownership transition following the crisis—changing demographics, credit conditions, or geography? What factors explain the unequal recovery across the two minority groups? This article investigates these key questions using uniquely constructed administrative data.

Our article makes two key contributions. First, we investigate the more recent trends for consumers acquiring new mortgages, including the role of credit attributes likely used by the lenders in originating new mortgages. We explore the extent to which credit characteristics, along with income, education, household composition, age, and house prices, explain new mortgages. Second, we study the racial/ethnic patterns in the transition for consumers acquiring new mortgages. We examine the extent to which racial/ethnic differences in credit factors, age, income, household composition, education, and geography contribute to the White–minority gap in the rates of transition to new mortgage ownership. We recognize and document differences in the experiences of Black and Hispanic consumers in the mortgage market. Therefore, we explore how credit and other factors relate to the mortgage transition for each group, separately. These differences suggest overlapping but distinct implications.

For our analysis, we use a uniquely constructed household panel data set that combines anonymized individual credit bureau records with the credit bureau’s marketing data containing race/ethnicity information for the months of September 2012 and September 2018. The core credit bureau data—onto which the anonymized marketing data are merged—is based on a representative sample of 2% of the credit-visible population in the United States in September 2016.

We estimate logistic regression models to investigate the determinants of who became a mortgage owner during this period. Our analysis variable is nonmortgage holders in 2012 who transitioned to acquiring new mortgages by 2018. We control for several socioeconomic characteristics, key credit attributes, and macroeconomic variables. To partially capture the demand side, we control for an indicator of mortgage inquiries made in the recent past. Our regression results suggest age (especially being between 36 and 45), income growth, marital status, mortgage inquiries, and local unemployment rates are big drivers of the decision to enter mortgage ownership. Consumers with missing credit scores or insufficient or inadequate credit histories are least likely to transition to mortgage ownership. Other factors such as gender, household-level debt obligations (including student loan debt), and education level play less important roles.Footnote6

Next, estimates from our sample indicate that Blacks and Hispanics have lower rates of transition to new mortgage ownership from 2012 to 2018. Our estimates suggest that whereas the Black rate of transition to mortgage ownership is approximately one half the White rate, the Hispanic rate is two thirds the White rate. We use the Blinder–Oaxaca decomposition technique for nonlinear equations to decompose the racial/ethnic gaps in transition rates.

Our decomposition exercise yields several interesting findings. First, racial/ethnic differences in credit attributes contribute the most in explaining the racial/ethnic gap in transition rates. Blacks and Hispanics are more likely than Whites to have low credit scores, missing scores, delinquencies, bankruptcies, and high debt liabilities, making them less likely to transition to acquiring new mortgages. They are also less likely to make mortgage inquiries, indicating a lower demand for mortgages. Hence, after accounting for credit-risk measures likely used by lenders to originate mortgages, our research goes beyond the studies that conclude that most of the homeownership gap between White and minority households is due to differences in endowments, such as income and wealth, and household characteristics, such as age, marital status, number of children (see Acolin et al., Citation2019; Wachter and Megbolugbe, Citation1992; Gabriel and Rosenthal, Citation2008; Seah, Fesselmeyer, and Le, Citation2017; and Newman, Holupka, and Ross, Citation2018). Furthermore, if lenders’ lower appetite for rep and warrants risk is encouraging overlays, it will impose additional constraints on underrepresented minority borrowers who are struggling to meet the credit standards for obtaining mortgages.Footnote7

Second, racial/ethnic differences in the distribution of age reduces the racial/ethnic gap in the transition rate for both Blacks and Hispanics. This is because both minorities are skewed younger than Whites, and younger consumers have a higher average probability of entering mortgage ownership. Third, the racial/ethnic difference in income growth shrinks the White–Hispanic gap but contributes to the White–Black gap. This is because Hispanics (Blacks) experienced higher (lower) income growth than Whites from 2012 to 2018, and higher (lower) income growth implies higher (lower) average probability of entry. We suggest this may be a contributing factor to the unequal recovery across the two minority groups. Fourth, racial/ethnic differences in geography contribute substantially to the White–Hispanic gap but explain virtually none of the White–Black gap. Hispanics are more concentrated in unaffordable areas, making it harder for them to transition. Lastly, racial/ethnic differences in household composition, such as marital status, matter more for Blacks in explaining the racial/ethnic gap in transition rates. Blacks are more likely to be single than Whites, and being single decreases the probability of transitioning to mortgage ownership.Footnote8 Despite controlling for key variables, 34% of the White–Black gap and 21% of the White–Hispanic gap in national transition rates is not explained by our benchmark specification. This could be attributed to variables that are not in the model, such as parental wealth, information networks, or consumers’ ability to meet the required down payment.

The U.S. economy is an agglomeration of several geographically dispersed local economies with different income and credit constraints, labor market conditions, and housing supply constraints. Recognizing this, we decompose the racial/ethnic gap in rates of transition to mortgage ownership at the state level. Our findings reveal that there is considerable heterogeneity in factors contributing to the racial/ethnic mortgage ownership gap within the nation. For instance, although geography does not matter for the White–Black gap in transition rates nationally, it contributes substantially to the local White–Black gap in states like New York and Mississippi. This is partly because Blacks are concentrated in urban and more expensive pockets in New York, and partly because they have higher unemployment rates than Whites in Mississippi. Hence, geography can be an important barrier to mortgage ownership for Blacks, depending on where they reside.

Although several studies control for demographic and neighborhood characteristics in explaining the racial/ethnic homeownership gap, very few of them investigate the role of credit constraints in explaining the gap. A few researchers seek to account for credit constraints as determinants of the racial/ethnic gap in individual tenure choice (whether to rent or buy) mostly based on credit proxies and self-reported survey data (Charles & Hurst, Citation2002; Choi, McCargo, Neal, Goodman, & Young, Citation2019; Gabriel & Rosenthal, Citation2005). To our knowledge, we are the first to consider the role of actual measures of credit risk likely observed by the banks, particularly those obtained from administrative data, in explaining the minority gap in the rate of transition to new mortgages. Using anonymized credit bureau data on households’ debt and credit characteristics, we analyze their relationship with renters’ decision to transition to mortgage ownership.

The existing literature has emphasized that timing of homeownership entry is critical in determining the trajectory of the net worth of low-income and minority households (Boehm & Schlottmann, Citation2008; Newman & Holupka, Citation2016; Wainer & Zabel, Citation2019).Footnote9 Moreover, Zabel (Citation2019) finds that homeownership exit during economic downturns like the Great Recession is predominantly due to declines in real wealth and real income for low-income households. To understand unequal recovery patterns, we should ideally investigate both mortgage entry and exit patterns across races and ethnicities. However, one limitation of our data is that they cannot identify the homeownership status of the consumers. This means we are unable to determine who exited mortgage ownership because of volatility in the economic climate, as opposed to paying off their mortgage debt. For these reasons, we focus only on new mortgage entry decisions between 2012 and 2018. Although delinquencies and foreclosures decreased during this time span, new mortgage transitions are an important measure to understand unequal recovery pattern in the period following the financial crisis.

The rest of the article is organized as follows. Section 1 reviews the literature on tenure or homeownership choice and racial/ethnic homeownership gaps. Section 2 describes the data, whereas section 3 specifies the model, presents summary statistics, and discusses the estimation results. Section 4 reports state-level decomposition results, and section 5 concludes.

1. Literature Review

This article lies at the intersection of the literature analyzing factors affecting tenure choice (tenancy or homeownership; e.g., Drew, Citation2014; Haurin, Hendershott, & Wachter, Citation1997; Linneman & Wachter, Citation1989; Park, Herbert, & Quercia, Citation2014) and the literature on factors explaining the racial/ethnic gap in homeownership rates (e.g., Borjas, Citation2002; Carrillo & Yezer, Citation2009; Coulson, Citation1999; DeSilva & Elmelech, Citation2012; Gabriel & Rosenthal, Citation2005; Hilber & Liu, Citation2008; Painter, Gabriel, & Myers, Citation2001; Wachter & Megbolugbe, Citation1992).

The literature investigating tenure choice decision partly focuses on the role of borrowing constraints on homeownership. Using data from Survey of Consumer Finances, Linneman and Wachter (Citation1989) find that households that face income and wealth constraints have a significantly reduced probability of owning a house. Haurin et al. (Citation1997) analyze the factors that affect the tenure choice of young adults, using the National Longitudinal Survey of Youth. Employing more sophisticated econometric modeling techniques, they reinforce the finding of Linneman and Wachter (Citation1989) that ownership propensities are significantly reduced when households face binding borrowing constraints. Recently, Park et al. (Citation2014) found that housing affordability has a significant effect on the likelihood of homeownership. Drew (Citation2014) shows that individuals who hold strong beliefs about the benefits of homeownership are more likely to expect to own in the future.

The second line of literature investigates the key determinants of the racial/ethnic gap in homeownership rates. A wealth of literature identifies socioeconomic factors that contribute to racial/ethnic gaps in homeownership rates, such as endowment and household composition. According to Acolin, Goodman, and Wachter (Citation2016), trends in homeownership rates will depend on shifts in three key drivers for homeownership forecasts: demographics, credit conditions, and housing costs. With demographic shifts toward a minority-majority nation, future homeownership and mortgage origination trends will be largely driven by the demand for housing among the various demographic groups that are likely to be prominent. Painter et al. (Citation2001) use census microdata from 1980 and 1990 to analyze housing tenure choice decisions among racial/ethnic groups in the Los Angeles metro area. They find that whereas the White–Hispanic homeownership gap is largely accounted for by differences in endowment (such as income, education, and immigration status), the endowment-adjusted homeownership gap between Whites and Blacks more than doubled by 1990. Hilber and Liu (Citation2008) find that after controlling for paternal wealth and location choices, the White–Black homeownership gap in a standard tenure choice model entirely disappears. Acolin, Lin, and Wachter (Citation2019) estimate tenure-choice models that incorporate household endowments, such as permanent income, and market endowments to understand the racial/ethnic gap in homeownership rate over time. They find that unlike Asians and Hispanics, the increasing gap in homeownership from 2005 to 2013 for Blacks is not explained by these endowment factors and may potentially be due to tightening of credit or other institutional factors.

A few studies have documented that neighborhood effects caused by institutional barriers, such as Federal Housing Administration redlining, developed by the Home Owners Loan Corporation (HOLC) in 1940, have long-term implications for minority homeownership rates. Race/ethnicity played a key role in determining neighborhood ratings, and policies restricted access to credit by redlining minority neighborhoods (Rothstein, Citation2017; Schill & Wachter, Citation1995). Krimmel (Citation2018) shows that even after fair housing legislation was passed in the mid-1970s, there were large persistent declines in housing supply and population density in formerly redlined census tracts relative to adjacent neighborhoods that were rated more favorably. Appel and Nickerson (Citation2016) find that redlining policies have long-term effects on house values. In particular, redlined neighborhoods had 5% lower home prices in 1990 relative to the adjacent areas.

Other studies have exploited the role of geography and location in explaining the White–minority gap. Wachter and Megbolugbe (Citation1992) analyze data from the 1989 American Housing Survey using multivariate regression techniques and find that market factors such as house prices and geographic location explain a substantial part of the White–Hispanic homeownership gap. Coulson (Citation1999) finds that a higher share of immigrants, younger age, and concentration in high-cost housing markets contribute the most to the Hispanic homeownership gap. Borjas (Citation2002) shows that the national origin of immigrants and the residential location choices made by different immigrant groups are key determinants of the wide homeownership gap between immigrants and natives. DeSilva and Elmelech (Citation2012) find that immigration status and spatial attributes are key factors in determining Mexican homeownership rates in the United States.

A few studies have explored the role of credit constraints on the homeownership gap. An important work in this direction is by Gabriel and Rosenthal (Citation2005), who use Survey of Consumer Finances data to analyze the White–minority gaps in homeownership rates. They find that although most of the gap is attributable to household characteristics, credit constraints account for no more than 5 percentage points of the racial/ethnic gap in homeownership. A study by Charles and Hurst (Citation2002) uses data from the Panel Study of Income Dynamics to analyze the White–Black gap in transition to homeownership by 1996 for a sample of households who were renters in 1991. They find that even after controlling for credit proxies and demographics, black mortgage applicants were more likely to be rejected compared with Whites. However, the lower application rate for Blacks was a more important determinant in explaining the racial/ethnic difference in homeownership transitions. A related study by Munnell, Tootell, Browne, and McEneaey (Citation1996), using local data collected by the Boston Federal Reserve on mortgage loan applications in Boston-area banks, concludes that minorities are significantly more likely to be denied a mortgage than Whites are, even after including explicit controls for credit variables. Recent work by Choi et al. (Citation2019) contemporaneously investigates the role of credit scores in explaining the Black–White homeownership gap across metropolitan areas. They conclude that marital status, credit score distribution, age, and income distribution explain a substantial proportion of the Black–White gap at the metropolitan statistical area level.

Recent changes in the housing finance market may also have implications for the White–Black or White–Hispanic homeownership gap. One salient trend is the increase in the share of mortgages originated by nondepository institutions since 2010. Nondepository institutions account for nearly 62% of mortgages reported in the 2019 HMDA data. According to a Consumer Financial Protection Bureau report (Jo, Liu, Skhirtladze, & Barriere, Citation2020), nondepository institutions are more likely to originate loans to minority borrowers.

Financial Technology (FinTech) innovations in the mortgage-lending process enhance operational efficiency and provide an opportunity to reduce lending disparities. Bartlett, Morse, Stanton, and Wallace (Citation2019) find evidence that fully automated lenders are associated with lower disparities in loan pricing and in the accept/reject decision for Hispanic and Black applicants.Footnote10 The lower price and denial rate differences suggest that such innovations in housing finance may improve access to mortgage credit for Black and Hispanic consumers.

2. Data

We obtained deidentified consumer credit panel data from one of the three major credit bureaus. The primary sample consists of a random 2% of the consumer records available in September 2016, totaling 5.3 million consumers. To form a more complete household description, we obtained depersonalized records from the credit bureau’s database for an additional 8.8 million consumers sharing a household with one of the primary sample consumers. These records were identified by starting with the 5.3 million sampled records and identifying all other individuals of any age with a credit record who shared the same address as the primary member.

To understand recent changes to the credit profiles, we also obtained their credit records from the September 2012 and September 2018 credit database. The credit data include age, various credit scores, and modeled measures of income and total debt-to-income ratio (DTI). The modeled measure of tax-reported income is based on the credit bureau’s proprietary model, which includes consumers’ credit-based attributes as model inputs. It is inclusive of all income sources such as wages, investment income, alimony, rental income, and so on. In most cases, the income source also includes spousal income if taxes are filed jointly. We also have the number, dollar amounts, and payment status of mortgage, auto, credit card, student loan, and other bank or retail debt. The credit file identifies credit inquiries, public-record bankruptcies, and foreclosures. The data include some geographic information, including zip code, county, and state.

Because the credit record data do not have information on consumers’ race or ethnicity and other demographic information, besides that mentioned above, the credit bureau matched each consumer in the primary sample to their marketing data to obtain additional household-level data. The marketing data consist of information on race, ethnicity, education level, gender, and marital status for the individuals living in the housing unit. These sociodemographic characteristics are based on the credit bureau’s proprietary models, which include consumers’ first and last name as well as their geographic location, among other things, as model inputs.Footnote11 To protect consumer privacy, all personal identification information, such as name and address, was removed, leaving only information on select attributes and those with match success. For everyone in our panel, we have individual- and household-level information for 2012, 2016, and 2018. For comparison, Appendix B benchmarks the distribution of sociodemographic variables in the sample for 2016, when our sample was drawn to 2016 ACS PUMS 1-year estimates. The patterns in the two data sources are similar. To these data, we merged the median single-family house price at a county level from the Freddie Mac Home Value Explorer, for 2012, 2016, and 2018. We also merged the data to county-level unemployment rates from the Bureau of Labor Statistics, for 2012, 2016, and 2018.

Our data represent a random sample of consumers with available credit data, not a random sample of the U.S. population. The credit bureaus have data only for those U.S. residents who have applied for or taken out a loan (auto, credit card, student loan, mortgage, or home equity line of credit). The data may also include individuals with public records such as bankruptcies and collections. Our sample is likely to understate the percentage of those who have no credit history and no items in collections, including recent immigrants with little or no credit history in the United States, because of credit invisibles with no records at any of the three major credit bureaus. Nonetheless, the data include individuals with so-called thin files.

For each record in our sample, the credit bureau captures the total number of open mortgage-type trade lines reported in the previous 6 months as of September 2012, September 2016, and September 2018. This field allows us to track mortgage ownership status over time. Using this attribute, we analyze the racial/ethnic mortgage ownership patterns in our sample between 2012 and 2018 in Appendix C. We also discuss the rate of transition to mortgage ownership (as the percentage of 2012 nonmortgage owners who obtained a new mortgage by 2018) and the rate of transition out of mortgage ownership (as the percentage of 2012 mortgage owners who transitioned out of mortgages by 2018) in Appendix C.

The factors that contribute to the racial/ethnic difference in the transition rate ultimately create the White–Black and White–Hispanic gap in the mortgage ownership rate. Understanding these factors can shed light on the unequal recovery of the two minority groups following the financial crisis. Although our data do not allow us to accurately examine transitions out of mortgage ownership, we are able to capture transition to mortgage, which is an important indicator of postcrisis recovery.

3. Model and Estimation Results

3.1. Model

To identify the determinants of entry into mortgage ownership, we estimate the logistic regression for the probability of transition to mortgage ownership on the estimation sample. Our model takes the following general form:

where transition = 1 indicates that a consumer makes the transition from having no mortgage in 2012 to at least one mortgage listed on their credit report by 2018, and 0 otherwise.

We include three sets of credit attributes as independent variables. Our panel data allow us to look at the credit profile of the same individuals for 2012, 2016, and 2018. However, since our goal is to understand who transitioned to a new mortgage by 2018 and what changed for them in the transition process, we use 2012 values for most credit attributes. This way we also address endogeneity concerns, as 2018 values of credit attributes are more likely to be endogenous with mortgage transition decisions from 2012 to 2018. The first set of credit attributes captures consumers’ credit profiles. We include consumers’ Fair Isaac Corporation (FICO) score in 2012 and indicators for missing FICO scores. These values are at the individual consumer level. Specifically, we include four indicators of missing FICO: (a) FICO missing in 2012 but not missing in 2018; (b) FICO not missing in 2012 but missing in 2018; (c) FICO missing in both years; and (d) FICO not missing in either year. Combined with the 2012 FICO score, these four indicators reflect a consumer’s credit profile between 2012 and 2018.Footnote12 We include these transition missing FICO indicators to capture whether consumers who were building their credit profiles were more likely to transition to mortgage ownership. Most consumers are required to have a credit score to obtain a mortgage, and not vice versa. Hence, unlike the levels of FICO scores in 2018, these transition dummies are less likely to be endogenous to mortgage receipt. We expect that credit score will have a positive effect on the probability of becoming a mortgage owner.

In the first set, we also include household student loan DTI growth, household credit card DTI growth, and household auto DTI growth. Household DTI is calculated by taking the ratio of the total balance of household debt as reported in the previous 6 months to the estimated tax-reported income.Footnote13 Whereas the credit card debt growth rate and auto debt growth rate could have a negative effect on the propensity for homeownership, the effect of student debt growth rate on mortgage ownership is not straightforward. Consumers with higher student debt have a higher debt obligation, which makes it hard for them to save for a down payment. Student loan debt has a negative correlation with homeownership, and the impact is more pronounced for individuals who did not complete their degree (see Miller & Nikaj, Citation2018). However, consumers, especially degree completers, with high student loan debt tend to have higher expected income and better chances of becoming mortgage owners. Furthermore, consumers with differing student loans may have different levels of education and specializations, which are also correlated with homeownership (see Mezza, Ringo, Sherlund, & Sommer, Citation2016). The last variable in this set is an indicator of consumers with so-called thin files and with clean credit records. This is an individual-level indicator. We define consumers with thin files with clean credit records as those with few trade lines (two or fewer) reported in their credit records, no delinquencies in the last 180 days, no foreclosures in the last 84 months, and no bankruptcies in the last 84 months, and whose back-end DTI does not exceed 25.Footnote14 Hence, the consumers with thin files do not have bad credit, but have credit records that are considered unscorable: that is, they contain insufficient credit history to generate a credit score.Footnote15 Consumers with clean thin files are expected to be less likely to own a home.

The second set of credit attributes captures several severe derogatory credit variables, such as an indicator of any foreclosures in the 84 months prior to September 2018 and an indicator for 90-day delinquencies in 2012. We expect these derogatory variables to have a negative impact on the rate of transition to mortgage ownership. We include a categorical variable capturing bankruptcies in the 84 months prior to September 2018, as it allows for different impacts based on the timing of a bankruptcy. Our data also enable us to consider the role of individual beliefs and perceptions concerning tenure decision by controlling for mortgage inquires, which serves as a proxy for homeownership preferences. The last credit attribute we include is an indicator capturing whether consumers inquired about a mortgage in the 12 months prior to September 2012 but did not get approved.Footnote16 This indicator, mortgage inquiry, partially captures consumers’ demand for housing and is expected to have a positive impact on the mortgage ownership rate. All these credit attributes enter at the individual level in our model.

Our explanatory variable race is a vector of race/ethnicity indicators, whereas X bundles the sociodemographic characteristics such as gender, age cohort, marital status, number of children, estimated tax-reported income growth, and education. We use individual-level information for these variables. Education enters the regression in the form of five dummy variables indicating each of the main levels of educational attainment (high school diploma, some college, bachelor’s degree, graduate degree, and unknown). To get the most updated information on consumers’ skill set and household composition, we include 2018 values for education and number of children. Consumers’ age in 2018 is transformed into eight categories: missing, 18–25, 26–35, 36–45, 46–55, 56–65, 66–70, and over 70. We include consumers’ marital status in 2012 and two dummy variables capturing change in marital status: a first variable indicating those who transitioned from being single in 2012 to married by 2018; and a second variable indicating those who transitioned from being married in 2012 to single by 2018. Marriage has certain legal and economic benefits that can lower the cost of homeownership. Marriage introduces a legal structure that makes the transfer of property easier in the event of death and simplifies the process of fully utilizing the mortgage interest deduction and capital gains exemption (see Miller & Park, Citation2016). We expect a consumer’s probability of becoming a mortgage owner increases with household income growth, age, education level, number of children, and being married.

Lastly, Z captures national/local business cycles and trends. We include an affordability index, such as the ratio of logged median house prices for single-family houses to median individual income, and local unemployment rates. Both these variables are measured at the county level. We expect both to have a negative impact on transition rate. Consumers may have the credit profile to qualify for a mortgage, but if they are living in unaffordable areas, they are unable to meet down payment requirements, which negatively affects their chances of owning a mortgage. We also include state dummies to account for local business cycles that may affect the mortgage ownership rate. Although imprecise, we hope that these variables account for many unobserved characteristics of local housing submarkets, such as the stock of houses, economic situations, public services, and natural amenities.

3.2. Summary statistics

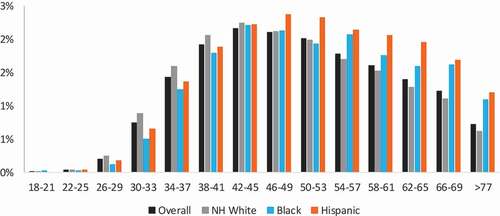

presents the summary statistics of the key control variables in our estimation sample. Columns 1, 2, and 3 report the shares and mean values for the full estimation sample who did not have mortgages in 2012, the subsample who transitioned to mortgages by 2018, and the subsample who did not transition.Footnote17 The average age of those who transitioned was 44 as of 2018, as opposed to 50 for those who did not transition. As the table suggests, consumers who transitioned into new mortgages by 2018 are more likely to be non-Hispanic Whites, male, and younger.Footnote18 In terms of their household composition, they are more likely to be married with children. Compared with consumers who did not transition, consumers who transitioned are also more likely to have a higher estimated tax-reported income (in terms of both dollar amount and growth rate) and education level.

Table 1. Summary statistics of the independent variables

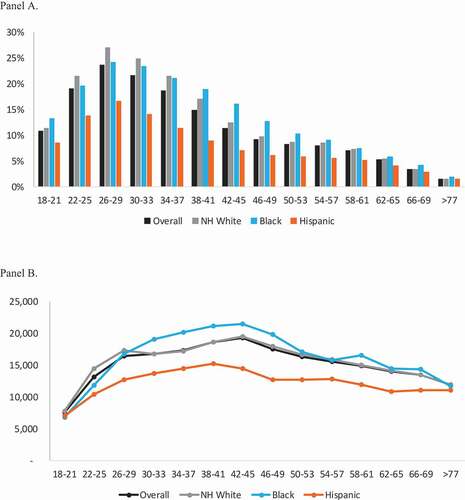

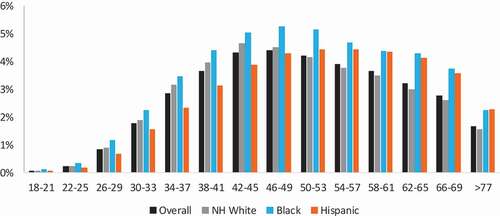

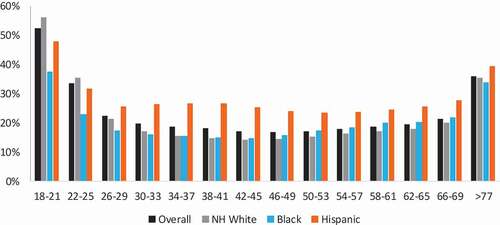

The average FICO score in our full sample is 668, with 19% having missing FICO scores in 2012. Furthermore, the group that successfully transitioned to mortgages had higher FICO scores and were less likely to have missing FICO scores in 2012. Since we have missing FICO indicators, we include adjusted FICO scores that take a value of 0 for missing scores to avoid multicollinearity. The adjusted FICO scores are also substantially higher on average for the group that transitioned. What do the consumers with missing FICO scores look like? To dig in, in panel A of , we look at the average number of open trade lines reported in the previous 6 months by FICO bucket. We find that the number of trade lines increases with FICO score, suggesting that consumers with missing FICO scores were less likely to have enough credit history to generate a score. Furthermore, around 35% of the overall population with a missing FICO score in 2012 had a FICO score by 2018. Panel B in reports the distribution by age and race/ethnicity of the overall population, the population with missing FICO scores in 2012 who had a FICO score in 2018, and the population with missing FICO scores in both years. The panel indicates that compared with consumers who had missing FICO scores in both years, consumers who had a FICO score by 2018 were more likely to be younger minorities. For example, whereas the median age of consumers who had missing FICO scores in both years was 49, the median age of consumers who had a FICO score by 2018 was 39.

Table 2. Open mortgage trade lines by FICO bucket and missing FICO data

According to , average household debt (student loan debt, auto loan debt, and credit card debt) is substantially higher for the group that transitioned, which could be highly correlated with their income and wealth. Note that the household DTI growth rates are negative for all groups. Our analysis is based on a random sample of people who were credit visible in 2012. The negative growth rate of DTI over the period of 6 years implies, on average, that these people are paying down their household debt at a faster rate than what is being accumulated by the same cohort during this time period. Furthermore, the table suggests that consumers who obtained mortgages by 2018 are more likely to be associated with lower delinquencies and higher mortgage inquiries. Lastly, the consumers who transitioned are more likely to be living in affordable areas with lower average unemployment rates.

3.3. Transition to Mortgage Ownership Outcomes

Next, we turn to the results from our multivariate analysis. reports results for logit models for the pooled sample representative of the U.S. credit-visible population.Footnote19 Model 1 includes the sociodemographic characteristics. Model 2 includes credit variables capturing credit profiles. Model 3 includes credit variables capturing severe derogatory credit. Model 4 includes mortgage inquiries. Model 5 includes controls for macroeconomic trends. Most of the variables in all model specifications are statistically significant and have the expected signs.Footnote20 The coefficients on the minority race dummy variables are negative and statistically significant for both Blacks and Hispanics. Our pooled regressions suggest that whereas Black consumers are 3.0–7.0 percentage points less likely to own a house relative to the average non-Hispanic White consumer, Hispanic consumers are 1.0–3.0 percentage points less likely to do so.

Table 3. Logit models of transition to mortgage ownership

Age is a big driver of mortgage ownership and has a nonlinear relationship: the marginal probability of transitioning to mortgage ownership increases with age and then decreases after 45 years. The large and statistically significant coefficients indicate that the likelihood of transitioning is the highest for consumers age 36–45 in 2018. A consumer 36–45 years old is associated with an increase of 11.0–14.0 percentage points in the probability of transitioning to mortgage ownership. A female consumer’s probability of transitioning is 1.0–2.0 percentage points lower, and a single consumer is associated with a 6.0–8.0 percentage point decrease in transition probability. Consumers who marry between 2012 and 2018 are also more likely to acquire new mortgages, which confirms our expectations. Specifically, transitioning to marriage from 2012 to 2018 is associated with an 8.0–9.0 percentage point increase in the probability of transitioning to new mortgage ownership.Footnote21 Contrary to our expectations, the number of children has a small impact on the transition rate in all model specifications.

Consumers with higher income growth are more likely to transition to mortgage ownership: a 1 percentage point increase in income growth is associated with a 13.0–16.0 percentage point increase in the probability of transitioning to mortgage ownership. After controlling for income, level of education does not seem to have a big impact on the transition rate, because it is highly correlated with income level. For most model specifications, the higher the educational attainment, the greater its impact on the transition rate, which confirms our expectation.

Next, we turn to the three sets of credit attributes. The variable indicating having a credit score has a small but significant impact on transition rates. If a FICO score increases by 1 point, the transition probability increases by 0.03–0.04 percentage points.Footnote22 Relative to the group that always had a FICO score, those who had a missing FICO score in 2012 and have a FICO score in 2018 are more likely to transition to mortgage ownership. The marginal probability of transitioning for this group increases by 18.0–24.0 percentage points, which is substantially higher than the impact of credit scores. A possible explanation is that because this group was skewed younger than the overall population (see , panel B), they were preparing themselves for homeownership or getting into a better credit position. Not surprisingly, still having a missing FICO score in 2018 lowers one’s probability of attaining a new mortgage.Footnote23

The indicator for thin files is large, negative, and statistically significant, suggesting that consumers with insufficient credit histories are less likely to transition to mortgage ownership. Household student loan DTI growth has a negative impact on the mortgage ownership transition rate. According to , a 1% increase in household student loan DTI growth decreases the transition probability by 1.0 percentage point.Footnote24 However, in all our model specifications, household auto loan DTI growth and credit card DTI growth have a positive impact on the rate of transition to new mortgages. Consumers with higher incomes tend to consume more and may have higher credit card and auto DTIs as they smooth consumption over their lifetime. They also tend to transition more quickly into acquiring new mortgages.

Any delinquencies in the preceding 90 days decrease the probability of entry into new mortgages, which confirms our expectations. Contrary to our expectations, the coefficient on the foreclosure dummy is positive in all model specifications, but the magnitude drops significantly in Models 4 and 5. The coefficients on the bankruptcy dummies are not only statistically significant but also depict an interesting pattern. Those with more recent bankruptcies are less likely to acquire a new mortgage. However, those with older bankruptcies (6 years and older) seem to have recovered and are more likely to transition to mortgage ownership. The large and positive coefficient on the mortgage inquiry dummy provides evidence that the relationship between demand for mortgages and probability of entry is very strong. A consumer who inquired about mortgages in 2012 has a 12.0 percentage point higher probability of transitioning, which provides strong evidence that consumer interest in buying a house is a big driver for transitioning to mortgage ownership.

Lastly, Model 5 suggests that the macroeconomic variables, such as the house price-to-income ratio and unemployment rate, have a negative and significant effect on the probability of entering into new mortgages. A consumer who lives in an area with higher unemployment rates is 35.0 percentage points less likely to transition to mortgage ownership. Similarly, a consumer living in less affordable areas with a high median house price-to-income ratio is less likely to transition to mortgage ownership. Model 5 also includes state dummies. Many of them have statistically significant coefficients.

3.4. Transition to Mortgage Ownership Outcomes by Race/Ethnicity

reports the logit results by race/ethnicity, allowing coefficients to vary across groups. The coefficient estimates from these logit regressions are used to determine whether there are racial/ethnic differences in the processes of generating transitions into new mortgages, and to compute the contribution of racial/ethnic differences in individual characteristics to the racial/ethnic gaps in the transition rates.

Table 4. Logit models of transition to mortgage ownership by race/ethnic group

Column 1 uses the non-Hispanic White sample only, column 2 uses the Black sample only, column 3 uses the Hispanic sample only, and column 4 uses the pooled sample that combines all racial/ethnic groups as a reference. The size of the coefficient estimates in suggests that the relationship between age and entry into mortgage ownership is weaker for both minority groups compared with non-Hispanic Whites, although the pattern is similar: The probability of transitioning increases with age, peaks at age 36–45, and decreases thereafter. However, the marginal probability of transitioning for Blacks is highest for the age cohort 46–55, which provides evidence that Blacks buy homes later in life compared with Whites (Choi et al., Citation2019). The marginal contribution of income growth to the propensity for mortgage ownership of Blacks is 7 percentage points lower than that for non-Hispanic Whites, indicating that the income link in entry into new mortgages appears to be weaker for Blacks than Whites and Hispanics.

There are some key differences in the impact of credit attributes on mortgage ownership propensities across race/ethnicity. The coefficients on the dummy variable indicating any delinquencies in the past 90 days is negative and statistically significant for all races/ethnicities, but the impact is lower for the minorities (4% for non-Hispanic Whites; 2% for Blacks; 1% for Hispanics). In addition, the relationship between mortgage inquiries and entry into mortgage ownership appears to be much stronger for non-Hispanic Whites than for minorities. This indicates that even when minorities demonstrate a strong preference for mortgage ownership, they are not transitioning at the same rate as non-Hispanic Whites. The differences in the relationship of credit attributes to mortgage ownership for minorities and non-Hispanic Whites suggests additional challenges such as down payment constraints, differences in endowment (Acolin et al., Citation2019), or other impediments to being approved for mortgages.

Unemployment has a large, negative, and statistically significant impact on the propensity for homeownership for all racial/ethnic groups. Being unemployed decreases the probability of transitioning to new mortgages by 42% for non-Hispanic Whites, 30% for Blacks, and 25% for Hispanics. Lastly, the relationship between affordability and probability of transitioning is stronger for Hispanics than for non-Hispanic Whites (−0.0837 vs. −0.0543), indicating that affordability is a bigger challenge for Hispanics in obtaining new mortgages.

3.5. Decomposing the Racial/Ethnic Gap in the Rate of Transition to Mortgage Ownership

The coefficient estimates reported in and identify several characteristics that are important in the process of generating the transition to mortgage ownership. In this section, we investigate to what extent the racial/ethnic differences in the distributions of variables contribute to the racial/ethnic differences in transition rates. We perform a decomposition analysis using a variation of the Blinder–Oaxaca technique. A decomposition analysis is a useful construct for presenting the relative contribution of endowments in explaining an observed gap. The Blinder–Oaxaca technique has been widely used to identify potential discrimination in labor and housing markets, which is typically attributed to the unexplained residual. However, the decomposition method does have some limitations. The most contentious critique is that the residual will be inflated by omitted variables or any proxy measures designed to represent a variable that is hard to collect or measure. Therefore, we refrain from assuming that the residual in our decomposition analysis represents only market discrimination. For instance, we are not able to observe wealth or actual mortgage demand, which would be key factors in obtaining a mortgage.

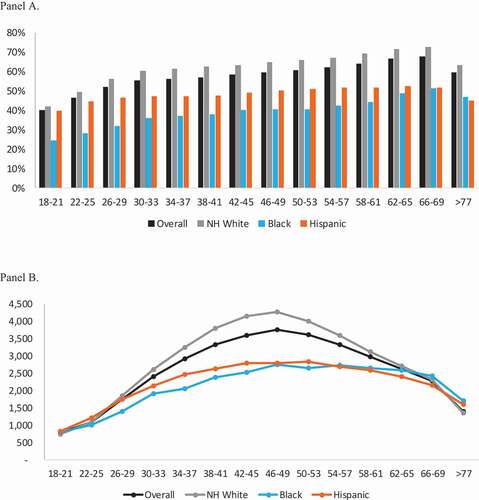

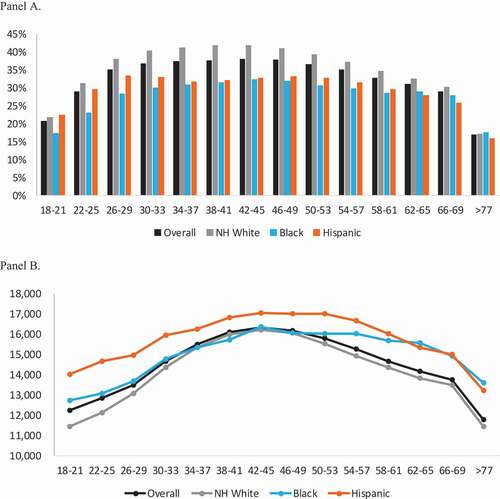

The results of a decomposition may be sensitive to the choice of the reference or benchmark demographic group. The labor and mortgage literature has adopted standardized reference groups, which facilitates interpretation across studies, such as comparing racial groups based on the non-Hispanic White equation. We also use White as the reference group; in addition, we use the equation of a pooled model and the equations for the minority groups to provide a range of estimates. To this end, we first compare the distribution of the independent variables included in the regression analysis across the racial/ethnic groups, as given by . The table indicates that minorities and Whites have different distributions of several key variables that are worth mentioning. First, Blacks and Hispanics are skewed younger compared with non-Hispanic Whites. The percentage of Blacks and Hispanics who are 26–35, 36–45, and 46–55 years old is higher than the equivalent percentage of Whites. Second, Blacks are more likely to be single than Whites. Third, the percentage of consumers with college degrees (either a bachelor’s degree or a graduate degree) is much higher for Whites (28%) than for Blacks (18%) and Hispanics (11%). Fourth, average FICO scores in 2012 are substantially lower for Blacks and Hispanics compared with Whites (Whites: 683; Blacks: 605; Hispanics: 638). Whereas a substantially higher percentage of minorities have missing FICO scores in either year compared with Whites, a lower percentage of Blacks than Whites have thin files with clean records in 2012 (21% vs. 30%). Fifth, a larger share of minorities than Whites have delinquencies. For example, the percentage of Blacks with delinquencies is roughly twice the equivalent percentage of Whites (63% vs. 36%). Lastly, the house price affordability ratio is much higher for Hispanics than for Whites (0.98 vs. 0.77), indicating that Hispanics live in less affordable areas than Whites do.

Table 5. Means of variables in samples used to estimate the logit equation for transition to mortgage ownership

The gap between the White–Black and White–Hispanic rates of transition to mortgage ownership can be decomposed into two parts: the part attributable to racial/ethnic differences in the distributions of the set of independent variables determining the gap, and the part attributable to racial/ethnic differences in the processes generating transitions into mortgage ownership. For a linear regression, the standard Blinder–Oaxaca decomposition can be expressed as:

where Y is the average value of the dependent variable, is the row vector of average values of the independent variables, and

is the vector of coefficient estimates for race/ethnic group j. The first term in parentheses represents the part of the racial/ethnic gap that is due to group differences in the distribution of characteristics X. The second term in parentheses represents the part because of differences in the group processes determining levels of Y. The second part is the unexplained portion of the gap. We will focus on the first part of the gap, which arises because of differences in the distribution of individual characteristics. The idea is that the contribution of each variable to the gap is equal to the change in the average predicted probability from replacing the White distribution with the minority distribution of that variable while holding the distribution of all other variables constant.

The coefficient estimates from a nonlinear model, such as a logit model, cannot be used directly in the standard Blinder–Oaxaca decomposition. Following Fairlie (Citation1999, Citation2005), we use the Blinder–Oaxaca decomposition technique for a nonlinear equation. In particular, decomposition for a nonlinear equation can be written as:

where Nj is the sample size for race/ethnic group j, Yj is the average probability of the binary outcome of interest for race/ethnic group j, and F is the cumulative distribution function from the logistic distribution. An equally valid expression for the decomposition is:

In the above case, the coefficient estimates for race/ethnic group j, are used as weights for the first term in the decomposition, and White distribution Xw are used as weights for the second term. Equations (3) and (4) often provide different estimates, and we report estimates under both specifications. The first term in the decomposition is calculated as follows. First, using coefficient estimates, we calculate predicted probabilities for all observations in the minority sample and all observations in a random subsample of Whites that is the same size as the minority sample. Second, we rank each member of the two samples by their predicted probabilities and match them by their respective ranks. We replace the White distribution of variables recursively with the minority distribution of variables and compute the contribution of each variable. Lastly, we repeat the above steps for 1,000 random subsamples of Whites and then calculate the mean value of estimates from all the samples.Footnote25

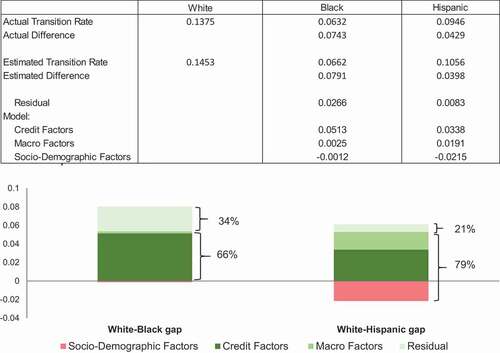

reports the estimates from the decomposition for the White–Black gap in the rate of transition to mortgage ownership using three sets of coefficients: Non-Hispanic White only, Black only, and all racial/ethnic groups (Whites, Blacks, Hispanics, and Others) pooled. We grouped the independent variables in eight subsets: (a) sex and age, which captures individual demographics; (b) marital status, dummy variables indicating change in marital status, and number of children, which captures household composition; (c) income growth; (d) education; (e) credit profiles; (f) severe derogatory credit; (g) mortgage inquiry; and (h) geography, which captures the county-level house price affordability measure, county-level unemployment rate, and the state dummies. The first three rows give the White and Black transition rates and White–Black gap in the transition rate in the sample used for estimation. The racial/ethnic gap in White–Black transition rates is 0.0791. The rest of the table reports estimates of the contributions of racial/ethnic differences in each subset to the gap in transition rate. The results are generally similar across specifications.

Table 6. Blinder–Oaxaca decomposition of difference between Black and non-Hispanic (NH) White rates of transition to mortgage ownership

The negative estimates reported in the table for individual demographics indicate that racial/ethnic differences in sex and age reduce the White–Black gap in the transition rate. This implies that if the distribution of sex and age for Whites is replaced by that of Blacks, the White–Black gap in transition rates shrinks by 23% and 21% in the White and pooled specifications, respectively. This is mainly because the Black population is skewed younger and younger consumers are more likely to transition to mortgage ownership. However, the gap shrinks less under Black coefficients (14%) because Blacks are more likely to transition later in the life cycle (see ). Household composition, which includes marital status and number of children, explains 9–11% of the White–Black transition gap. Blacks are more likely to transition from single to married in 6 years compared with Whites. Yet they are more likely to have been single compared with Whites in 2012—and being single decreases the probability of transition to mortgage ownership, contributing to the White–Black transition gap.

Income growth explains only a small part of the gap in White and pooled specifications (around 6%) because the average growth in income in the last 6 years is similar for the two races. Furthermore, income growth explains virtually none of the gap under Black coefficients, because the relationship between income and mortgage transition is very weak under the Black-only sample (see ). Similarly, the group difference in education level explains virtually none of the gap, mainly because of the weak relationship between education and the transition probability, as reported in .

The strikingly large positive contribution estimates for credit profiles (43–45%) suggest that overall, the lower credit profiles of Blacks are mostly responsible for the White–Black gap in transition rates. In all specifications, these contributions are statistically significant. Within this category, several competing forces influence the gap. For instance, a larger share of Blacks transitioned from having missing FICO scores in 2012 to having a FICO score in 2018, which contributes to shrinking the gap (see ). However, Blacks had a substantially lower average FICO in 2012 than Whites and are more likely than Whites to have a missing FICO score in 2018, decreasing their likelihood of transitioning to mortgage ownership.

The racial/ethnic differences in severe derogatory credit contribute around 7–11% of the gap, mainly because Blacks are more likely to have a delinquency in the past 90 days, which makes them less likely to transition. Mortgage inquiry explains around 11% of the racial/ethnic gap, primarily because Blacks were less likely to inquire for mortgage type loans in 2012 than Whites were. Lastly, geography explains virtually none of the gap, suggesting, in aggregate, that Blacks are not necessarily living in more unaffordable areas compared with Whites. On the one hand, this finding is encouraging, because it implies that Black neighborhoods typically do not suffer from high housing costs, making it easier for potential home buyers to meet down payment requirements and transition to homeownership. On the other hand, it implies that Black homeowners tend to build wealth and home equity at a slower rate because of depressed home values in their neighborhood (Newman & Holupka, Citation2016). This, in turn, can affect their demand for housing and their intergenerational wealth transfers.Footnote26 Overall, the decompositions reveal that group differences in all the included characteristics explain roughly two thirds of the White–Black gap in new mortgage ownership.

gives the estimates from the decomposition for the White–Hispanic gap in transition rates using three sets of coefficients: White only, Hispanic only, and all racial/ethnic groups pooled. Several similarities and differences in are worth mentioning. The White–Hispanic gap in transition rates is 0.0398, which is lower than the White–Black gap. Similar to the case for Blacks, the racial/ethnic differences in individual demographics largely reduce the White–Hispanic gap in the transition rate, primarily because Hispanics are skewed much younger than Whites and hence are more likely to transition. Note that the contribution of individual demographics drops considerably to 47% under Hispanic coefficients because of the weak relationship between age and the transition probability under the Hispanic-only sample, as reported in . The racial/ethnic difference in income growth reduces the gap under all specifications, because Hispanics experienced much larger income growth in 6 years compared with Whites (White: 17%; Hispanic: 20%; see ). This divergence, we suggest, contributes to the unequal recovery across the two minority groups. Unlike the White–Black gap, group differences in household composition explain a small portion of the White–Hispanic gap. Group differences in education explain virtually none of the gap.

Table 7. Blinder–Oaxaca decomposition of difference between Hispanic and non-Hispanic (NH) White rates of transition to mortgage ownership

Racial/ethnic differences in credit profiles explain the majority of the White–Hispanic gap—around 66–77%. Hispanics have relatively lower FICO scores and were more likely to have missing FICO scores in 2018 compared with Whites (see ). These are the main sources of their less favorable credit profile. Group differences in the severe derogatory credit explain around 10–12% of the gap in the White and pooled samples, whereas group differences in mortgage inquiries explain a small portion of the White–Hispanic gap in all specifications.

Lastly, in contrast to the White–Black gap, racial/ethnic difference in geography explains a substantial portion of the White–Hispanic gap in all specifications (43–57%). As suggests, Hispanics have lower affordability than Whites. This could be partly because they are concentrated in high-cost areas (Western and Northeastern states), and partly because they are concentrated in areas with low median income (Southern states). Lower affordability is making it more challenging for Hispanics, compared with Whites, to transition to mortgage ownership. Moreover, the contribution of geography to the racial/ethnic gap in transition rates increases to 57% if the coefficients from the Hispanic regression are used to perform the racial/ethnic decomposition. Higher house prices relative to income have a larger impact on the likelihood of transitioning when restricted to the Hispanic-only sample (see ). Therefore, when we use the Hispanic coefficients to measure the contribution of geography to the gap, it is amplified by the combination of the larger impact and concentration of Hispanics in high-cost areas compared with Whites. Our results reinforce the findings of Coulson (Citation1999) and Wachter and Megbolugbe (Citation1992) that geographic location explains a substantial part of the White–Hispanic homeownership gap. Overall, the decomposition exercise reveals that group differences in all the included characteristics can explain about 72%, 79%, and 93% of the White–Hispanic gap under White, pooled, and Hispanic specifications, respectively.

To summarize, presents the actual difference in the transition rate, the fitted difference in the transition rate (under pooled coefficients), and the contribution of sociodemographic, credit, and macro factors to the fitted difference. The residual effect is calculated as the unexplained portion of the estimated White–minority gap in transition rates. Credit factors alone explain 66–79% of this gap. For Hispanics, whereas sociodemographic factors alleviate the gap, macro factors significantly exacerbate the gap. The unexplained residual contributes 21–34% of the White–minority gap. The explanation for this residual gap is unclear, although it may be partly due to differences in factors such as assets, wealth, lender overlays, and consumers’ perceptions about required down payment (Goodman et al., Citation2017), which we cannot measure in our data.Footnote27 For example, based on the National Survey of Mortgage Originations (NSMO), Blacks have slightly higher propensities than Whites to receive gifts and inheritance as a source of down payment.Footnote28 However, we cannot observe the source of down payment in our data, which is most likely captured in the unexplained residuals of our models.

Figure 2. Decomposition of the racial/ethnic gap in the transition rate with respect to Whites. Authors' calculations using anonymized credit bureau data from 2012 and 2018

We perform several robustness checks on our baseline specification. Appendix E presents a detailed discussion of the findings from various alternative specifications. Our primary findings are consistent across all of these specifications.

4. Decomposition at the State Level

The U.S. economy is not a monolith, but an aggregate of geographically dispersed economies with varying business cycles. An analysis at the national level across a wide and diverse set of local areas may yield results that mute the effects of the diversity at the state level. Recognizing this, we examine to what extent the racial/ethnic gaps in the mortgage ownership rate persist at the state level and what the largest contributing factors are.

Panel A of reports the racial/ethnic transition rates, the White–Black gap in transition rates, and results from the decomposition exercise for each state.Footnote29 For accuracy, we report only the results for states with a Black population of more than 10,000 in our sample. For reference, we compute the national decomposition without including the state dummies, as reported in column 1.

Table 8. State-level Blinder–Oaxaca decompositions

First, in Maryland and Virginia, both Whites and Blacks are transitioning to new mortgages at a higher rate than the national average. Second, whereas states such as California, Florida, and Mississippi have a White–Black gap in the transition rate that is lower than the national average, states such as Illinois, Michigan, New Jersey, Ohio, and Pennsylvania have White–Black gaps in the transition rate higher than the national average. For example, the racial/ethnic gap in the transition rate in Illinois and Michigan is 11% and 12%, respectively, significantly higher than the national gap of 8%. For almost all states (except Mississippi), credit profiles explain most of the gap, followed by household composition, severe derogatory credit, and mortgage demand. Compared with the national case, the racial/ethnic disparity in income matters substantially more in explaining the racial/ethnic gap for California, Maryland, New Jersey, Texas, and Virginia. Furthermore, in contrast to the national case, geography explains a significant portion of the White–Black gap for New York, Mississippi, California, and Florida. This may be partly because of lower affordability, and partly because of the higher unemployment rates of Blacks residing in these states. For instance, the affordability index for Blacks is significantly higher than that of Whites in New York (1.60 vs. 1.15), indicating that Blacks are concentrated in urban and more expensive pockets within the state. In contrast, the local unemployment rate is substantially higher for Blacks compared with Whites in Mississippi (10.0% vs. 8.5%), making it harder for Blacks to obtain financing for mortgages locally.

Panel B of reports the racial/ethnic transition rates, the White–Hispanic gap in transition rates, and results from the decomposition exercise for eight states with a Hispanic population of more than 10,000 in our sample. Column 1 reports the national decomposition calculated without including state fixed effects in the regression model, for reference. Whereas New York and New Jersey have a higher than national average White–Hispanic gap in transition rates, states such as Arizona, California, and Florida have a negligible gap in transition rates.Footnote30 Similar to the national case, whereas racial/ethnic disparities in credit profiles play an important role in increasing the racial/ethnic gap in transition rates for most states, racial/ethnic differences in individual demographics shrink the gap. In contrast to the national case, income disparity contributes positively to the racial/ethnic gap in New Jersey, New York, and Texas. Lastly, geography follows an interesting trend. On one hand, it contributes 60% of the gap in New York, which is substantially higher than the national case. The affordability indices for Hispanics and Whites in New York are 1.65 and 1.15, respectively, suggesting that Hispanics are living in cities, suburbs, and exurbs within the state, making it harder for them to afford a mortgage. On the other hand, geography contributes only 7% of the White–Hispanic gap in Texas, which is significantly lower than the national average. The affordability indices for Hispanics and Whites in Texas are 0.67 and 0.69, respectively, indicating that typically, Hispanics are not living in less affordable areas compared with Whites within the state.

In a nutshell, the state-level decomposition exercise reveals considerable heterogeneity within the nation. For example, our findings suggest that geography is a less important barrier to mortgage ownership for Blacks nationally. This is driven by a lower contribution of geography to the White–Black gap in transition rates for most states, which offsets the significantly higher contribution of geography to the White–Black gap in the transition rate in New York and Mississippi. The distribution of income, unemployment, and house prices at the more local level may affect the propensity for mortgage ownership of both minority groups.

5. Conclusion

During the Great Recession and the subprime lending crisis, Black and Hispanic homeowners were disproportionately affected by foreclosures and the tighter lending standards. New HMDA-reported mortgage originations to Black and Hispanic borrowers declined from 25% of originations in 2006 to just 12% by 2009. As of 2018, the White–Black and White–Hispanic mortgage ownership gaps stood at roughly 17 and 16 percentage points, respectively. At the same time, the White–Hispanic and White–Black homeownership rate gaps persisted. This study uses uniquely constructed credit bureau data to answer two questions: How do consumers’ credit profiles determine their decision to enter mortgage ownership? What explains the racial/ethnic gap in rates of transition to obtaining new mortgages?

Our research reveals several interesting findings. First, using a logistic regression model, we find that some of the important determinants of the decision to enter mortgage ownership are age, income growth, marital status, getting a FICO score, the individual’s demand for a mortgage, and local unemployment rates. Consumers with limited credit histories are less likely to transition to acquiring new mortgages. Other factors, such as student loan debt, auto debt, gender, number of children, and educational attainment, play less important roles.

Second, we find that Blacks are one half, and Hispanics are two thirds, as likely as Whites to transition to mortgage ownership in our sample. To allow the impact of credit-related factors to differ, we investigate the racial/ethnic gap in transition rates separately for Black and Hispanic consumers. Using the Blinder–Oaxaca decomposition technique for nonlinear equations, we find that racial/ethnic differences in the distribution of credit attributes explain a large part of the racial/ethnic gap in the rate of transition to mortgage ownership. Specifically, both minority groups have lower credit scores and higher delinquencies, and are more likely to have missing credit scores, than Whites—all of which contribute to the lower average probabilities of entering mortgage ownership for minorities than Whites. We anticipate that this effect may be amplified if lenders are imposing tighter credit standards to minimize rep and warrants risk. The lower credit profiles of Black and Hispanic consumers compared with Whites also, we suggest, explains a large part of the racial/ethnic gap in the homeownership rate.

We also find two key differences between the factors explaining the White–Black and White–Hispanic gaps in transition rates. First, whereas geography matters substantially in explaining the White–Hispanic gap nationally, it explains virtually none of the White–Black gap nationally. Recognizing that decomposition at the national level may mute local effects, we conduct a state-wise decomposition exercise to better understand factors contributing to local homeownership gaps. We find that there is considerable heterogeneity across states, especially regarding the contribution of geography. For example, geography can be an important barrier to homeownership for Blacks residing in New York, mainly because they are concentrated in the city centers or suburbs. This implies the need for strategies that support more employment opportunities, improve access to credit and availability of low-down payment programs, and increase the elasticity of housing supply, driving down prices and improving affordability.

Second, racial/ethnic differences in household composition contribute more in explaining the White–Black gap relative to the White–Hispanic gap. Although lenders are not able to directly influence potential mortgage borrowers in terms of factors such as family structure, including marriage and children, they should be aware of differences and the extent to which credit policies may interact with these differences. Overall, our analysis cannot account for about 33–35% of the White–Black gap and 7–28% of the White–Hispanic gap, which could be due to differences in institutional factors, assets, and wealth.

Our findings suggest that consumers with missing FICO scores and thin files are less likely to qualify for mortgages. Alternative credit data, such as telecom, utility, and rental information, might more accurately identify credit-worthy consumers with missing FICO scores or thin files. Goodman and Zhu (Citation2018) make the case for the inclusion of rental payments in assessing mortgage applications. They compare rental payments with mortgage payments by income level while demonstrating that past mortgage payment history helps predict future loan performance.

Increased funding for programs intended to educate potential minority homeowners to use credit as a tool would be worthwhile. Our results indicate applying the credit profile distribution of White consumers to the Black consumers in our sample would increase the predicted mortgage entry rates of Black consumers by an amount equivalent to roughly 66–79% of the observed gap in mortgage entry rates between Whites and Blacks. Counseling and credit education opportunities could help place minorities in a better position to qualify for a mortgage. It also critical to ensure that homeowners have sustainable mortgages that are less likely to result in default or foreclosure. The use of prepurchase counseling is not universal, and studies suggest it is beneficial. Argento et al. (Citation2019) estimate that 17% of first-time homebuyers receive some form of homebuyer education or counseling. The reported take-up rate was higher for Blacks in their sample, at 41%. Those who report counseling are more likely to report better mortgage knowledge. Peck, Moulton, Bocian, Demarco, and Fiore (Citation2019) find that participants randomly assigned to a homebuyer education and counseling program were more likely to have a credit score of 620 or higher after the program. They also find that participants were more likely to say they would contact a counseling agency or nonprofit prior to missing a mortgage payment, that they were confident that they could find information they needed and were more likely to set up auto payments for their mortgage payments.

Low and no down payment programs backed by enterprises, Ginnie Mae, and state and local housing finance agencies can help overcome the geographic barriers. Furthermore, to the extent that the residual gap is explained by differences in parental wealth (see Hilber and Liu Citation2008), low and no down payment programs may also help overcome the unexplained residual gap.

Lastly, it would be beneficial for the federal government to provide assistance, such as modifications, payment deferrals, or forbearance, for low-income and minority existing homeowners to stay in their homes. Moulton et al. (Citation2019) find that mortgage payment assistance programs to shield against income shocks, such as the Hardest Hit Fund, can significantly reduce the risk of default of the low-income and vulnerable population. A combination of strategies supporting counseling and credit education opportunities, income and wealth creation, and debt rehabilitation will likely be the most effective in bridging the homeownership gap between Whites and minorities over time.

Acknowledgments

We thank Robert Avery, Laurie Goodman, Raphael Bostic, Steve Ross, Stephanie Moulton, Jaclene Begley, Timothy Lambie-Hansen, Douglas McManus, Cynthia Waldron, Sam Khater, Leonard Kiefer, and Sijie Li for helpful feedback, as well as the participants of the 2019 Urban Economics Association Meeting, 2019 FDIC Economic Inclusion Advisory Committee Meeting, 2019 APPAM Meeting, 2019 Southern Economics Association Meeting, 2019 Urban Institute Data Talk, and Freddie Mac Brown Bag series. This article also benefitted from the input of three anonymous reviewers. The analysis and conclusions in this article are those of the authors and do not necessarily reflect the views of Freddie Mac.

Disclosure Statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Jaya Dey

Jaya Dey is a senior economist in the Single-Family Client and Community Engagement division of Freddie Mac. Her area of research is housing policy, with a focus on affordability, access to credit and changing demographics. Prior to arriving at Freddie Mac, she was an assistant professor of economics at Oklahoma State University and a visiting faculty member at Saint Louis University. She holds a PhD in economics from The Ohio State University and a master’s degree from the Indian Statistical Institute, New Delhi.

Lariece M. Brown

Lariece Brown is a senior economist and quantitative analytics director in the Single-Family Client and Community Engagement division of Freddie Mac. She leads a team conducting analytics of and research on underserved markets. She has extensive experience in research to support fair lending, affordable lending, and assessing opportunities to expand access to credit. She has also served as a senior financial economist and section chief with the Federal Deposit Insurance Corporation. She earned her MA in mathematics and PhD in economics from The Ohio State University.

Notes

1. Some economists expect the homeownership rate to decline even further (see Acolin, Goodman, & Watcher 2016; Goodman, Pendall, & Zhu, Citation2015; Nelson, Citation2016), whereas others hypothesize that changing demographics will slowly increase the homeownership rate (see Haurin, Citation2016).

2. The White–Black homeownership gap increased from 28 percentage points in 2007 to 31 percentage points in 2018, according to the U.S. Census Housing Vacancy Survey. The White–Hispanic homeownership rate gap was 26 percentage points in 2007 and 2018.

3. The calculations are for owner-occupied mortgages.

4. We use the ACS PUMS to define individual-level estimates that only identify the household head and spouse as the homeowners, excluding adult children and other adults living in the household. See Appendix A for detailed discussion of our methodology.