?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Citizenship by investment (CBI) programs have recently garnered significant academic and media attention. Turkey introduced such a program in 2017 that offers citizenship in exchange for investment in residential property. Through the program, thousands of foreigners, mainly from the Middle East and Asia, have purchased houses, particularly in Istanbul. Foreigners’ share of total houses sold in Istanbul almost sextupled and exceeded 10% of total sales. This study estimates the short-run impact of relatively wealthy foreigners on the residential property prices in Istanbul investing to buy a Turkish passport. It finds that the Turkish CBI program positively impacts house prices by 2% in the districts, which are likely to be favored most by immigrant investors.

In recent years there has been a proliferation of investment-based migration programs (Dzankic, Citation2019; Gamlen, Kutarna, & Monk, Citation2019; Surak, Citation2020). Several countries around the globe try to attract investment by granting investors either residence or citizenship rights. These are featured in advertorials as golden visa and golden passport options. The former is a more common practice adopted by countries worldwide such as the United States, the United Kingdom, Canada, Belgium, Australia, Portugal, and Singapore.Footnote1 The latter is relatively new and includes both discretionary acquisitions of citizenship on the grounds of national economic interest and detailed citizenship by investment (CBI) programs (Dzankic, Citation2018, Citation2019). Economic difficulties after the European debt crisis have led several European countries to launch either economic residency programs, as in Portugal, Spain, Greece, and Ireland, or CBI programs, as in the case of Malta and Cyprus (see, among others, Ampudia de Haro and Gaspar, Citation2019; Parker, Citation2017; Xu, El-Ashram, & Gold, Citation2015).

This year marks the 37th anniversary of CBI programs. In simple terms, they refer to the direct exchange of a financial disbursement, in the form of capital investment or property purchase, for citizenship status. Several islands in the Caribbean Sea, including St. Kitts and Nevis and the Commonwealth of Dominica, have long-running CBI programs. In Europe, for example, Austria has been granting citizenship to investors since 1985, but its regulations are less detailed than those of the Caribbean Islands, and more reliant on the discretionary power of the state authority. More recently, several CBI schemes have been introduced in small Caribbean countries such as Antigua and Barbuda, Grenada, and St. Lucia and in relatively large emerging countries such as Turkey (see ). According to the Citizenship by Investment index (https://cbiindex.com/reports/) published by The Financial Times’ Professional Wealth Management magazine, 14 countries offer their passports for sale to the wealthy as of 2020. There has been an increase in the number of countries offering CBI schemes together with a substantial increase in the number of applicants (Dzankic, Citation2019). The global market for CBI programs is estimated to be around $25 billion a year (Treanor & Vivienne, Citation2019).

Table 1. Selected citizenship by investment program: A comparison

The CBI programs have an economic rationale. Cross-border capital flows into host countries can be substantial for small countries. For example, St. Kitts and Nevis witnessed significant inflows to its public sector alone, reaching nearly 25% of its gross domestic product in 2013 (Xu et al., Citation2015). In addition to such direct effects, these programs can also lead to positive spillover effects in some sectors, depending on the design and magnitude of the program. Lately, CBI schemes with real estate options are very popular, where investment in residential houses is offered in exchange for citizenship.

Foreign investment in real estate is expected to increase real estate prices. It is reported that it led to a boom in the construction sector in St. Kitts and Nevis in 2015 and boosted the price of luxury real estate in Portugal in 2012 (Xu et al., Citation2015). Leaving aside the extant literature on the impact of migration on house prices, there is, however, a shortage of empirical studies directly examining the relationship between CBI programs and real estate prices. As a latecomer to the CBI club, Turkey offers a unique environment in which to investigate the impact of CBI schemes on local house prices. Its program particularly encourages investment in the property market. It does not require any other contribution to the government, in the form of a registration fee or any additional nonrefundable contribution to any government fund.

Turkey launched its CBI program in January 2017. Since then, it has witnessed a dramatic increase in house sales to foreigners and received a lot of public attention through extensive media coverage. We aim to investigate the impact of this program on the residential house prices in Istanbul, where more than half of total house sales to foreigners have materialized during this period. We compare local house price movements in the short window immediately preceding and following the implementation of the CBI program in January 2017. We also compare the effect of this program on the house prices in the districts of Istanbul with high immigrant concentration versus low immigrant concentration over the same period.

We base our assumption of destination choice of new immigrants on the concept of social networks, according to which immigrants tend to live in districts with a large share of immigrants with a similar background or a shared ethnicity. Card (Citation2001) applied this assumption in the migration literature. It implies that the destination choice of current immigrants within the country is highly correlated with the number of compatriots already established in that specific destination (i.e., city, province, or region). We demonstrate that the destination choice of current immigrants in Istanbul through the Turkish CBI program has contributed to an upsurge in house prices in several districts where the share of foreign-born Istanbul residents (i.e., immigrants) is relatively high. That is, we show that local house prices rise disproportionally more in districts with a higher foreign population density (more than 5%) after the implementation of the CBI program. We find that the program had a positive impact on house prices by 2% in the districts that are likely to be most favored by immigrant investors.

Our article contributes to the extensive literature on the economic effects of immigration in three specific ways. First, there has been little work directed toward understanding the effects of relatively better-off immigrants on housing markets. It should be noted that Turkey is not one of the top destinations for high-net-worth individuals (HNWIs) from developing countries. Therefore, the relatively better-off or wealthy immigrants mentioned in this article do not correspond to HNWIs. They instead designate persons whose investible wealth exceeds $250,000. How wealthy foreigners (immigrants) affect local housing markets is an empirical question. They can directly increase the demand for housing, leading to an increase in local house prices. However, the preferences of domestic residents can offset the direct effects of wealthy foreigners. If residents would like to avoid cultural diversity, and relocate to do so, then native outflows can offset the upward price pressure. Empirical evidence concerning the overall relationship between immigration and property prices is, so far, mixed. Some studies predict that immigration increases house prices because of an increase in demand for accommodation (Gonzalez & Ortega, Citation2013; Saiz, Citation2003, Citation2007), whereas others argue the opposite because of a decline in the perceived desirability of new neighbors (Sa, Citation2015) or differences in housing tenure and usage of housing space between natives and immigrants (Braakmann, Citation2019). In a comprehensive meta-regression analysis, Larkin et al. (Citation2019) find that immigration leads to an increase in house prices on average, but that the effect is more limited in countries where locals are less hospitable to immigrants.

Our study is partly related to this strand of the literature but focuses on the impact of the CBI program on residential property prices tout court. To the best of our knowledge, this is the first empirical article examining the short-run impact of a CBI program on the housing market. Second, most of the existing literature understandably focuses on the advanced countries cited above because of the massive influx of immigrants into those countries. There are arguably only a few articles studying the effect of immigration on housing markets in emerging countries, despite the increase in human and capital mobility (Kim, Citation2017; Kim, Han, & O’Connor, Citation2015). In the case of Turkey, studies have investigated the impact of refugees, but not that of immigrants or foreigners. For example, Balkan, Tok, Torun, and Tümen (Citation2018) and Tumen (Citation2016) show that Syrian refugee inflows have generated an increase in the rents of higher quality housing units in the neighboring cities in the southeastern part of Turkey. They argue that this lends support to the residential segregation story in the Turkish case. Our article is undoubtedly different regarding motivation, driving force, location, and unit of analysis.

Finally, our work contributes to the burgeoning literature on the determinants of real estate prices in Turkey. Most of the previous studies, such as Tunc (Citation2020) and Yener, Unal, Ertugrul, and Alp (Citation2020), employ house price data at the national level (or province level, at best) and emphasize the role of macroeconomic indicators such as capital inflows, interest rates, and disposable income, or some regional dynamics such as population density, unemployment, climate, and education. Our study utilizes district-level data and points to the role of the Turkish CBI program and the inflow of relatively wealthy foreigners as another determinant of house prices, at least in some specific districts of Istanbul. Last but not least, from a political economy perspective, the current CBI program can be considered not merely another example of the commodification of citizenship but more an extension of the financialization of housing, where the state itself effectively continues to expand the scale and scope of the housing–finance nexus.Footnote2 The design of the Turkish CBI program lends support to the understanding that the Turkish government places the utmost importance on the development of the construction industry and takes an active role to back it in times of economic slowdown.

The article is organized as follows. The next section provides context on Istanbul and Turkey’s CBI program. Then, the methodology and data are explained in the following two sections. In section 4, empirical results are presented and discussed, along with their implications. Finally, the last section concludes.

1. The Context of Istanbul and the CBI Program

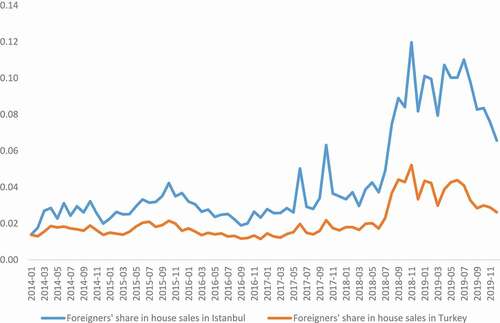

For a long time, Turks have considered Istanbul a city whose land and stone are made of gold. Decades-long internal migration has played a role in establishing this convention among the inhabitants. As recently as 2016, the number of out-migrants exceeded that of in-migrants in Istanbul, but the trend reversed in 2019 partly because of a rise in the number of foreign-born residents.Footnote3 Property investment in Istanbul has lately received increasing attention from foreign investors. The year 2019 set a record in terms of total houses sold to foreigners in Turkey and Istanbul when house sales figures reached 45,483 and 20,857, respectively, up from 18,189 and 5,811 in 2016. More importantly, foreigners were responsible for almost 10 out of every 100 house sales in Istanbul in 2019, compared with 3 out of every 100 house sales in 2016 and 2017 (see ). The strong growth in property sales to foreign buyers in recent years has occurred not so much because of robust tourism but largely because of the CBI program.

Figure 1. Foreigners’ share in house sales in Istanbul and Turkey.

The Turkish property market has been open to foreign buyers since 2002 (Polat, Citation2019). However, in some zones only nationals of countries like Britain and Germany that allow Turkish citizens reciprocal rights were allowed to purchase properties. These zones were abolished in 2005, and the reciprocity condition ended in 2012.Footnote4 Since then, thousands of foreigners from Russia to GCC (Gulf Cooperation countries) countries, which were previously banned, have successfully acquired properties in Turkey, most notably in Istanbul, in the Mediterranean resort city of Antalya, and in the industrial city of Bursa. Foreigners can now buy up to 30 ha of property (up from 2.5 ha) without special permission. On the other hand, a significant policy change occurred when Turkey introduced its CBI scheme in January 2017, following the July 15, 2016 coup attempt, which sent a shockwave throughout the economy. Among the several options in the scheme, purchasing property was a particularly attractive way to obtain a Turkish passport, which formerly required a minimum $1 million investment. This amount was reduced in recognition of financial hardship starting in August 2018. New regulations were introduced in September 2018; these grant citizenship to foreigners in exchange for:

Purchasing real estate worth at least $ 250,000 (down from $1 million);

Or putting $500,000 into a fixed capital investment;

Or keeping a minimum of $500,000 in a Turkish bank account for at least 3 years (down from the earlier minimum of $3 million);

Or generating 50 jobs (down from 100 jobs).Footnote5

This scheme was widely seen as a bid to stimulate the slumping real estate market. It arrived after the Turkish Lira had already plummeted by more than 40% against the U.S. dollar in August 2018 and economic activity in the real estate and construction industry continued to decline.Footnote6 Later, in December 2018, the Turkish government put in place another amendment that allows foreigners to apply for Turkish citizenship by purchasing real estate from unfinished or off-plan projects.Footnote7 These rules have made the real estate route in Turkey one of the lowest cost CBI programs, and its immediate impact on the housing market was widely covered and commented on by the press (Smith, Citation2019; TRTWorld, Citation2019).Footnote8 According to the Turkish Statistical Institute, the number of houses sold to foreigners more than doubled, reaching 4,200 homes per month after September 2018. It reached an all-time high in October 2018 with 6,327 monthly sales. The number of houses sold between January 2017 and August 2018 was about 41,151 units, whereas it reached 67,288 homes between September 2018 and December 2019. Most of the foreign buyers are citizens of Turkey’s neighboring countries; Iraqis, Iranians, and Saudis were the biggest buyers of Turkish property. According to 2019 cumulative statistics, citizens of Arab countries, including Iraq, Saudi Arabia, Kuwait, Jordan, Yemen, Palestine, Libya, Egypt, Qatar, and Lebanon, constitute 42% of total foreign buyers. Iranians follow them with a 12% share. Nationals of advanced countries, including Germany, the United Kingdom, Sweden, and the United States, account for 10%. The remaining countries represented by the foreign buyers are Russia (5%), Afghanistan (5%), and Azerbaijan (3%).

There is limited information regarding the overall number and breakdown of foreigners acquiring citizenship through their investment in Turkey. The Ministry of Internal Affairs stated that overall, more than 9,000 foreign investors have benefited from the Turkish CBI program and invested around $2.8 billion within 3 years, and that the overwhelming majority of the investment was realized in 2019.Footnote9 Iranians occupy the top spot and have a share of 26% in the total number of citizenships granted. Nationals of Arab countries—Iraq, Yemen, Palestine, Jordan, Libya, and Egypt—represent 48% of the total citizenships granted. Other countries with significant representation are Afghanistan, with a share of 15%, China (8%), and Pakistan (3%).Footnote10 Anecdotal evidence from the field, the written press, and social media also suggests that Iranians, Arab nationals, and Afghan people are interested in investing in the Istanbul property market and receiving citizenship in due course.Footnote11 It is reasonable to assume that relatively wealthy nationals of Iraq, Iran, Yemen, Libya, and Afghanistan would prefer to invest in the property market to obtain a Turkish passport. Citizens of these countries have suffered a great deal from recent political and economic uncertainties in their homelands. Correspondingly, Badarinza and Ramadorai (Citation2018) emphasize the role of foreigners facing political risk in their home countries and foreign demand as an important determinant of London house prices. Indeed, several foreign investors designate Turkey as a haven, an open society, and a relatively Europeanized country. Furthermore, a Turkish passport allows them to travel more freely across the globe, with more visa-free travel options, than their home countries’ passports do (Wither & Erkoyun, Citation2019).

1.1. Migrant Networks and Segregation in Istanbul

Turkey has been experiencing an influx of foreigners for a long time, as a country of transit to the European Union for irregular migrants and a country of refuge for asylum seekers. More recently, it has also become a country of immigration as a result of intense migratory movements over the last three decades (among others, see İçduygu & Kirişci, Citation2009; Kirişci, Citation2007). In particular, Istanbul has become a top destination for movers from the Middle East, Africa, and Asia through migrant networks. Migrant networks are sets of interpersonal ties connecting movers, former movers, and nonmovers in countries of origin and (in this case) Istanbul through social connections, which are primarily based on kinship and friendship.

After the continuous waves of immigration to Istanbul starting in the 1980s, it is possible to observe a cumulative causation whereby multiple ties to communities or origin facilitate ongoing and at times increasing migration (Massey et al., Citation1993; Massey, Citation1994; Wilson, 1994). For instance, İçduygu and Karadağ (Citation2018) and Kaya (Citation2017) show how new migrants and refugees join the earlier settlers in particular locations and tend to live in Istanbul, primarily by coming through their networks of relatives and friends. As observed in several countries, foreigners, particularly those with a shared community, ethnicity, and culture, prefer to live together in the same neighborhood or district. Indeed, some of the districts of Istanbul are associated with the spatial concentration of particular migrant networks. Some of the prominent ones are the Syrian community in Zeytinburnu, Küçükçekmece, Fatih, Bağcılar, and Sultanbeyli districts, the Iraqi community in Fatih and Esenyurt districts, the Afghan community in Zeytinburnu and Beykoz districts, the Chinese nationals from Xinjiang Uygur Autonomous Region of China in Zeytinburnu, Kucukcekmece, and Silivri districts, and the Syrian Turkmens in Esenler district.Footnote12

An obvious outcome of such spatial concentration is segregation from the broader local population, which refers to the segregated geographies of neighborhoods or districts reflecting a history of immigration, internal migration, class and intergroup ethnic and racial relations, and conflict (Newbold, Citation2021). Parallel to the findings of the related literature, Istanbul broadly seems to display two patterns of residential segregation (Allen & Turner, Citation1996; İçduygu & Millet, Citation2016; Price & Singer, Citation2008; Zelinsky & Lee, Citation1998). On the one hand, most immigrants continue to settle in traditional and segregated enclaves in the inner city that offer less expensive housing, public transportation, and access to employment, such as Fatih and Zeytinburnu districts. On the other hand, newly arriving groups bypass traditional inner-city enclaves to settle in more dispersed and newer suburban areas such as Basaksehir and Esenyurt, reflecting different housing opportunities. In the latter case, more often, both poor and wealthier immigrants coexist in the same district, albeit in separate quarters reflecting their distinct levels of economic characteristics. Most of them have the same ethnicity (i.e., Arab), and find it easier to forge friendships with coethnics. As it is very well known, immigrants are more likely to have strong ties to coethnics and family members in the host country (Fietz & Kaschowitz, Citation2019; Viruell-Fuentes, Morenoff, Williams, & House, Citation2013). Moreover, immigrants can talk to each other in their mother tongue and maintain familiar habits in a different culture, which keep them well grounded (Jasinskaja-Lahti, Liebkind, Jaakkola, & Reuter, Citation2006). In fact, in Istanbul, a common language seems to be more relevant than a common country of origin in determining the geographical boundaries of immigrant enclaves. It is an essential factor that separates immigrants from Turkish citizens, as well (Kaya, Citation2017).Footnote13

2. Methodology

We employ the difference-in-differences (DiD) approach to identify house price variation in the districts of Istanbul before and after the implementation of the CBI program, which we treat as an exogenous shock. In a similar fashion to Badarinza and Ramadorai (Citation2018), we conjecture that districts of Istanbul with relatively high preexisting shares of foreign-born residents are preferred habitats for foreign property purchases. Moreover, Bailey, Farrell, Kuchler, and Stroebel (Citation2020) show that social connectedness is a strong predictor for migration. Theoretically, homophily is known to be an important explanatory factor for the configuration of personal networks (McPherson, Smith-Lovin, & Cook, Citation2001). For example, leaving aside numerous cases in developed countries, Kim et al. (Citation2015) show that the location of foreign-owned houses is linked to the geography of ethnic clusters in Seoul, Korea. The assumption that new immigrants tend to locate in areas with a large share of immigrants of the same origin or ethnicity is well known in the literature and mentioned above. If this conjecture were correct, we would expect to see relatively higher house prices in these specific districts of Istanbul than other districts after the implementation of the CBI program. Accordingly, we define our control group as the districts where the proportion of the foreign population (i.e., immigrants) is low, and our treatment group as the districts where the proportion of the foreign population is relatively higher. In other words, our empirical strategy relies on comparing house prices that are subject to larger compatriot inflows with those that are not, before and after January 2017. More specifically, the pretreatment period includes the period between 2014m1 and 2016m12, whereas the posttreatment period spans from 2017m1 to 2019m11. We ignore more recent dates because of the impact of the COVID-19 pandemic. Tumen (Citation2016) and Altındag, Bakış, and Rozo (Citation2020) also adopted a DiD approach in their analysis of the economic impact of Syrian refugees in Turkey.

To segregate the so-called immigrant and nonimmigrant districts (in a relative sense), we sort the districts in terms of the share of the foreign population in the district population. Then, we assume that the first five districts with the highest foreign ratio make up a group. Afterward, we run a mean equality test between this group and the district with the next largest share of foreign population. If the mean does not statistically differ from this group, we add it to the group and proceed to test the next group. We stop when we find a district with a statistically significantly different (smaller) share of the immigrant population. Whereas the former constitutes our treatment, the latter becomes the control group of districts.

Given the short period, we also conjecture that the supply of housing is inelastic. The existing literature essentially confirms the expectation that the supply curve is inelastic in the short run and elastic in the long run (Harter-Dreiman, Citation2004). In other words, even in the case of an increase in demand for housing, the supply of housing will not immediately respond, as the construction of new houses takes time. More importantly, in an environment where the housing market is already struggling, entrepreneurs will not be eager to build more homes. As it takes time to build new houses, the housing supply is constant in the short run. The Turkish Statistical Institute does not publish construction permits at the district level, but Istanbul’s aggregate data shows that the average number of construction permits is even lower in the postpolicy period, most likely because of worsening economic conditions.

Finally, we estimate the following difference-in-differences model:

where hp represents real house prices in a certain district indexed by r. The year and month are indexed by y and m, respectively. The program’s impact on house prices is given by the variable DiD, which is defined as the multiplication of a dummy variable that takes on a value of 1 for the posttreatment period, and another dummy for districts, which are classified as the treatment districts. fi where are the fixed effects for the district, year, and month. In our models, we try both combined time effects, where year and month are assumed as one period, as well as decoupled time effects. We estimate all models with clustering standard errors. X represents a set of other macroeconomic explanatory variables, such as the real mortgage interest rates and real effective exchange rate of the Turkish Lira. These variables are common to all regions. Another variable that could potentially enter X is inflation. However, because all of our independent and dependent variables are real (i.e., already adjusted for inflation) we do not include it among the covariates. If X is not included among the explanatory variables, we have a simple DiD model. This is reported in the article. Although not reported in the article, we also estimate a random effect model when feasible for comparison purposes.

3. Data

Our data set includes house prices at the district level in Istanbul and covers the period between 2014m1 and 2019m11. The prices were obtained from the Central Bank of the Republic of Turkey (CBRT). As the ownership details of the properties are mostly opaque and local registry data are not circulated, we are forced to rely on time series data. Istanbul has 39 districts, among which only 34 have house price data. The banks in Turkey extend individual housing loans based on the valuation reports prepared by real estate appraisal companies. The CBRT compiles the price data from these valuation reports at the time of approval of housing loans. The actual sale or utilization of the housing loan is not required, but all appraised residential properties are included in the scope of the data. These prices are then used as a proxy for each district’s house prices after adjusting for quality changes related to housing characteristics. Our data comprise the monthly median price (in Turkish Lira) per square meter of these residential properties.Footnote14

We generate real mortgage interest rates by subtracting Consumer Price Index (CPI) inflation for Istanbul from the nominal mortgage interest rates. The CPI-based real effective exchange rates were obtained directly from the CBRT. All data are monthly for the period of 2014m1 through 2019m11.

There are two sources of information concerning the share of the foreign population in the districts, which we used to identify treatment and control groups. The Turkish Statistical Institute has published data on the foreign-born population annually starting from 2014 at the district level, based on the address-based census. However, it does not provide the nationality of those classified as foreign-born. Syrian refugees are normally not included in that registry because they are under temporary protection only. We suspect that Syrian refugees make up the majority of foreign-born residents who migrated to Istanbul after 2014.

The United Nations migration agency (International Organization for Migration—IOM) also publishes reports based on fieldwork in which the actual numbers, by nationality, of the foreign population are provided at the district level in Istanbul. Therefore, there is a discrepancy in the foreign population numbers between the official statistics and the fieldwork statistics because the fieldwork data include Syrian refugees and other unregistered foreigners.Footnote15 The figures with refugees and those without, however, correlate with each other closely. In other words, the foreigners (migrants and immigrants) and Syrian refugees seem to prefer living in the same districts, most likely because they share the same ethnicity, language, and/or other sociocultural characteristics, as discussed above.Footnote16 United Nations reports reveal that foreigners are primarily from Arab countries, Iran, Afghanistan, Turkmenistan, Uzbekistan, China, Pakistan, Azerbaijan, and the Russian Federation. Consequently, we rely on the actual data from the fieldwork study in 2017 to determine the share of foreign population in each district. Irrespective of whether we include Syrian refugees in the foreign population figures, the members of the treatment and control groups do not change substantially.

presents a visual display of our treatment and control groups based on the ratio of all foreigners to the local population in each district. Our treatment group consists of 17 districts, which are the districts with a concentration of foreigners of more than 5%. These districts are Arnavutkoy, Avcılar, Bagcılar, Bahcelievler, Basaksehir, Bayrampasa, Beyoglu, Esenler, Esenyurt, Eyup, Fatih, Gaziosmanpasa, Gungoren, Kagithane, Kucukcekmece, Sultangazi, and Zeytinburnu. The control group of districts has a much lower ratio of foreigners to population: less than 2% to 3% in many cases.

Figure 2. Map of Istanbul: visual representation of treatment and control districts.

4. Results and Discussion

As outlined above, we treat the introduction of the CBI program in January 2017 as an exogenous shock and expect an increase in house prices because of a rise in the arrival of wealthy foreigners. As in Bertoli et al. (Citation2019), we reason that foreigners who would like to become Turkish citizens choose a destination with a relatively a higher population density of foreigners with a similar origin or ethnicity to their own. We present our results in . Column 1 in the table displays a simple DiD model without any covariates (Model 1), whereas columns 2 and 3 present DiD models with covariates. In addition, all models employ clustered standard errors. As a precursor to the DiD estimation, we test the so-called parallel trend assumption and find the coefficient for the interaction between a time trend and DiD nonsignificant.Footnote17 The adjusted R2 from the simple DiD model (column 1) and the DiD model with covariates and decoupled time effects (column 3) has an explanatory power of about 98%. However, the DiD model with covariates and combined time effects (column 2) has a meager explanatory power of only 1%. Overall, our results in show that the coefficient for DiD, which is the difference in house price across the treatment and control groups, is statistically significant under different set-ups. In other words, the house prices in the treatment districts rise more than house prices in the control districts after the CBI program. The magnitude of this increase is about 2%, irrespective of the model specification.

Table 2. Estimation results of difference-in-differences (DiD) model of real house prices

Foreigners’ share in total houses sold in Istanbul almost sextupled and exceeded 12% of total sales after the introduction of the CBI program. Assuming that most foreigners would have purchased homes in the treatment districts, this volume seems high. Furthermore, an increase in the number of Syrian refugees in the treatment districts would likely cause higher rent prices, and hence higher house prices. Incidentally, anecdotal evidence from the field indicates that some foreign investors avoid registering their ownership. Instead, they ask their naturalized Turkish relatives/friends to take ownership of the property. These people are said to be Chinese nationals from the Xinjiang Uygur Autonomous Region of China, and they keep their identity secret for reasons of security. These issues are hard to incorporate into the model, but they imply unregistered or unrecorded purchases by foreigners. Finally, a 2% difference in house prices seems a reasonable estimate and similar to those in some other countries. For instance, using a DiD approach, Pavlov and Somerville (Citation2020) recently found that an unexpected suspension of the investor immigration program in Canada negatively impacted house prices by 1.7%–2.6% in the neighborhoods and market segments favored by investor immigrants.

Additionally, as obtained via Models 2 and 3, the real effective exchange rate coefficient is positive but only significant in Model 3. This suggests that an increase in the foreign exchange rate, which is the depreciation of the Turkish currency, would indirectly make a given house cheaper, especially for foreigners. That would increase the demand for houses and thus increase house prices, ceteris paribus. However, the impact of the real effective exchange rate on real house prices would be negligible. Numerically speaking, for every 1-unit increase in the value of the foreign exchange, the house prices increase by about 0.31%. Although the negative coefficient on the real mortgage interest rates in Models 2 and 3 would be as expected, it is statistically nonsignificant in both models.

Our findings align with those of Degen and Fischer (Citation2017), Gonzalez and Ortega (Citation2013), Larkin et al. (Citation2019), and Saiz (Citation2003, Citation2007) and are opposed to those of Braakmann (Citation2019) and Sa (Citation2015), where the former group of authors also find a rise in house prices because of an increase in the immigration inflow. The likely counter-impact of domestic residents’ preference to avoid living in the same districts as immigrants—if these preferences exist in the context of Istanbul—do not offset the aforementioned positive impact. It should be noted that average house prices in the control districts are higher than those in the treatment districts both before and after the CBI program. However, there is undoubtedly a need to investigate this issue further at the neighborhood level when microdata is available. The district-level data cannot easily reveal residents’ preferences. For example, in a different context, using micro-level data, Balkan et al. (Citation2018) find that the massive influx of Syrian refugees in the southeastern part of Turkey has led to increased rents for higher quality housing units in the regions where residents live. Alternatively, wealthy foreigners appear to attenuate the adverse effects of immigrant volumes on house price levels. Their effects are similar to those resulting from foreign direct investment in residential real estate. Consequently, a sudden increase in the influx of foreigners initiates a positive housing demand shock, especially in the districts of Istanbul with a higher density of foreign population. This is in line with recent studies such as Jun, Ha, and Jeong (Citation2013) and Kim et al. (Citation2015), who show how the location of foreign-owned houses is linked to the geography of ethnic clusters in the case of Seoul, Korea.

Inevitably, one should exercise a degree of caution in interpreting the overall results. First, deciding what percentage of foreign population defines a treatment district is an important issue. For this purpose, we also used the median as a cutoff level for foreign population concentration to determine the treatment districts. Additionally, we examined the sensitivity of the results when we changed the reference year to 2014 and used the official data for the foreign-born population, a year before the influx of Syrian refugees to Istanbul. To a large degree, the results are supportive of the significant impact of the CBI program on residential property prices. One can further argue that the policy change in the Turkish CBI program seems to contribute to some relaxation in the official treatment against foreigners. This is why Istanbul now hosts thousands of unregistered migrants, and their increasing numbers contribute to housing demand. Second, because of privacy issues and the lack of micro-level data, it is challenging to identify the houses that foreign investors have purchased to acquire citizenship and to compare their prices before and after the CBI program. The issue is not, however, unique to this study. In addition to the cautious and credible determination of treatment districts carried out here, the fact that wealthy foreigners mostly from Arab countries and Iran prefer to live in relatively high-quality apartments but in the same districts or neighborhoods as those with a shared culture and similar ethnicity lends support to our approach. Moreover, it should also be kept in mind that foreigners might not purchase real estate only for the sake of acquiring a Turkish passport. Foreigners from the Gulf countries and developed countries seem to belong to this group of investors.

Additionally, Syrian refugees in Turkey are relatively poor. There seem to be two issues regarding Syrians in Istanbul. Most Syrian residents in Istanbul are from Aleppo, and Aleppo’s entrepreneurs are known to have had strong social and commercial networks with their counterparts in Istanbul and Iraq dating back to the period of the Ottoman Empire. Put simply, not all Syrians in Istanbul are poor, and at least a small part of them run their businesses successfully. In addition, those who are relatively wealthier and well educated have already acquired Turkish citizenship. As a result, some Syrian refugees have easily settled in the districts where wealthy foreigners, such as those from Iraq, also live.

Second, a common language seems to be more relevant than a common country of origin or socioeconomic background in determining the geographical boundaries of immigrant enclaves. That is one reason why poor Syrians may settle in the same districts but in separate neighborhoods known to have bad housing conditions. As in other big metropolises, one can observe a good neighborhood near a worse one, both in the same district in Istanbul. The UN statistics from the field support our contention (please see the United Nations Migration Agency situation and migration reports available at https://migration.iom.int).

5. Conclusion

Citizenship by investment programs have recently garnered significant academic and media attention. Turkey introduced such a program in 2017, which offers citizenship in exchange for investment in residential property. The program has become relatively cheap and encouraged foreigners to apply for Turkish citizenship by purchasing real estate. Since its inception, thousands of foreigners, particularly from the Middle East and Asia, have bought houses in Istanbul; foreigners’ share in total houses sold in the city almost sextupled and exceeded 10% of total sales.

In this article, we show that the influx of foreigners after the introduction of the CBI program eventually contributed to an upsurge in house prices in the districts of Istanbul in which the share of foreigners is relatively high. More specifically, local house prices rose disproportionally more in districts with a higher foreign population density (more than 5%) after the Turkish CBI program started. The program has had a positive impact on house prices (by 2%) in these districts (districts that are likely to be favored by investor immigrants). This finding is in contrast to previous results on immigration and real estate prices. It suggests that if immigrants are numerous and relatively well off, they can raise the house prices in the districts where they choose to settle.

Our study has two broad policy implications. First, countries can attract more immigrants if they decrease the cost of immigrant investor programs—and vice versa. Second, if the CBI program mainly works through the real estate route, as in the case of Turkey, it can lead to changes in the house prices in particular locations. In that case, the economic benefits of the CBI may not accrue to the whole country or the whole economy but rather to some specific areas or sectors of the economy. One alternative to avoid this would be to modify the design of the CBI program so that it can help spread the inflows to other economic sectors and locations without generating excessive pressure in the construction and real estate sectors.

We acknowledge some limitations of this study. We were able to obtain data on house prices at the district level, but not at the individual house level or the foreign investor level. It is very challenging to obtain both monthly and local data, particularly in emerging markets. As such, our model essentially includes macro variables. There are undoubtedly several local demand/supply variables, including location-specific factors, that drive house prices. They vary from the local market conditions in a particular location to the quality of life and the amount of housing stock in that specific location. However, given the span of data, wild swings in the behavior of the market participants are highly unlikely based on these variables. Furthermore, considering the worsening economic climate in Turkey at the time of the CBI program, we do not think that local demand/supply variables would respond quickly and differently to reduce the program’s impact on house prices.

On the other hand, Turkey certainly should have a high level of transparency regarding its CBI program. Nonetheless, we hope to spark a much‐needed research agenda around the CBI programs and their impact on real estate prices and investment. Additional empirical studies could enhance both the debates about these programs and our understanding of their consequences.

Acknowledgments

Open Access funding was provided by the Qatar National Library.

Disclosure Statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Lokman Gunduz

Lokman Gunduz is a professor of finance in the Department of Management at Fatih Sultan Mehmet Vakif University, Istanbul. He is a former board member of the Central Bank of the Republic of Turkey. His research focuses on financial markets, housing and monetary policy.

Ismail H. Genc

Ismail H. Genc, PhD, Texas A&M University 1999, is professor of economics at the Department of Economics in the American University of Sharjah. His expertise is in applied monetary economics, economic development, migration, and remittances.

Ahmet Faruk Aysan

Dr. Ahmet Aysan is a professor at HBKU and the Program Coordinator of the PhD and MSc programs. He has been the Board Member and Monetary Policy Committee Member of the Central Bank of Republic of Turkey and served as a consultant at various institutions such as the World Bank, the Central Bank of the Republic of Turkey, and Oxford Analytica. Dr. Aysan, who has many articles published in academic journals, is a recipient of the Boğaziçi University Awards, and the MEEA Ibn Khaldun Prize. Dr. Aysan is also a Research Associate at the University College London Centre for Blockchain Technologies (UCL CBT).

Notes

1. As of 2017, nearly half of the European Union member states host golden visa programs (Surak, Citation2020).

2. See Erguven (Citation2020) and Yesilbag (Citation2020) for an extensive analysis of the financialization of housing in Turkey and Serin, Smith, and McWilliams (Citation2020) for the role of the state acting as a regulatory mechanism, a land developer, and a house builder in the commodification of urban space in Istanbul. Also, see Mavelli (Citation2018) for a discussion of the relationship between citizenship by investment and neoliberal political economy.

3. According to an address-based registration system published by the Turkish Statistical Institute, the number of foreign-born residents in Istanbul quadrupled in 2019 to 16,653 people, relative to 4,166 in 2017. Their share as a percentage of the increase in in-migration was 15.2%, which implies a significant contribution. They accounted for almost 14% of net migration and 3.4% of in-migration for Istanbul in 2019. The share of foreign-born residents in Istanbul was less than 1% of the total in-migration in 2017.

4. Under article 35 of the Land Registry Law No. 2644, amended by Law No. 6302, Turkey allowed citizens of 183 states to purchase real estate property in Turkey without being subject to any reciprocity principles as of May 18, 2012.

5. See Presidential Decree No. 106 published in the Official Gazette dated September 19, 2018.

6. By the end of the last quarter of 2018, the Turkish economy had gone into recession. See also real estate sector reports in Turkey available at https://www.gyoder.org.tr/uploads/gyoder_gosterge/GOSTERGE-CEYREK1-2019-ING-_1_.pdf [accessed September 30, 2020].

7. See Presidential Decree No. 418 in the Official Gazette dated December 7, 2018.

8. See, for example, “Turkish passport demand soars as rules relaxed,” The Financial Times, January 27, 2019; “Foreign Buyers Flood Turkey’s Struggling Housing Market,” Mansion Global, January 2019; “Turkish property sales to foreigners keep up with strong performance, post all-time high in 5 months of 2019,” Daily Sabah, June 17, 2019; “Property sales to foreigners hit record levels in Turkey,” TRTWorld, April 18, 2019; “Passport demand soars after Turkey slashes cost,” Ahval News, January 28, 2019; “Iranian home buyers dodge sanctions, make Turkey their plan B,” Reuters, October 1, 2019, available at https://www.reuters.com/article/us-Turkey-iranians-idUSKBN1WG3ON; “Saudis snap up homes in Turkey as top foreign buyers,” The Times, August 29, 2019; “House Hunting in … Turkey” The New York Times, January 9, 2019.

9. www.aa.com.tr/tr/ekonomi/yabanci-yatirimcidan-2-milyar-771-milyon-250-bin-dolarlik-katki/1748243 [retrieved November 30, 2020]., Turkey’s figures seem satisfactory from a comparative perspective as well. For example, Portugal conceded 6,687 golden visas between 2012 and 2018 (Ampudia de Haro and Gaspar, 2019). Malta has received 1,742 applications since the inception of its individual investor program, as of June 30, 2019.

Available at https://oriip.gov.mt/en/Documents/Reports/Annual%20Report%202019.pdf. [accessed November 30, 2020]. See also Surak (Citation2020) to compare the number of applications with those to EU member countries.

11. One can also examine Google Trends to get an understanding of how the Turkish CBI program has become more popular over time. It shows that there was a worldwide increase in search interest for the terms “Citizenship by Investment Turkey” or “Turkey passport” after the policy change in September 2018. Investors from the Arab countries, Iran, and Pakistan showed greater interest after the policy change, which was probably materialized later in official house sales statistics (see Google Trends).

12. Data from the United Nations Migration Agency situation and migration reports. Available at https://migration.iom.int

13. There is certainly room for development and future research to better understand the nature of wealthy immigrants in Istanbul within the context of social/ethnic networks, at both conceptual and empirical levels. An empirical study in particular could contribute to a better understanding of the motives for participating in the Turkish CBI program. We leave this issue for future work.

14. Please see for more detail: https://www.tcmb.gov.tr/wps/wcm/connect/EN/TCMB+EN/Main+Menu/Statistics/Real+Sector+Statistics/Residential+Property+Price+Index/

15. This is expected as there are too many unregistered foreigners. IOM’s statistics depend on the information collected from local authorities in each neighborhood (namely, from Mukhtars) and are expected to be accurate and timely.

16. Syrian refugees in Turkey are not a party to the Turkish CBI program. The majority of the Syrian refugees are poor. However, they have an influential social network in the Arab world. Some of those residing in Istanbul are relatively well-educated and successful entrepreneurs. This is perhaps one of the reasons why the Turkish government has granted citizenship to over 90,000 Syrian refugees, most of whom live in Istanbul. See https://tr.euronews.com/2019/08/02/bakan-soylu-92-bin-suriyeliye-vatandaslik-verildi-suleyman-soylu and https://www.bbc.com/turkce/haberler-turkiye-49150143

17. See Cerulli and Ventura (Citation2019) on testing the parallel trend assumption.

References

- Allen, J. P., & Turner, E. (1996). Spatial patterns of immigrant assimilation. Professional Geographer, 48(2), 140–155.

- Altındag, O., Bakış, O., & Rozo, S. V. (2020). Blessing or burden? Impacts of refugees on businesses and the informal economy. Journal of Development Economics, 146, 102490.

- Ampudia de Haro, F., & Gaspar, S. (2019). Buying citizenship? Chinese golden visa Migrants in Portugal. International Migration, 58(3), 58–72.

- Ahval News. (2019, January 28). Passport demand soars after Turkey slashes cost. Ahval News. https://ahvalnews.com/turkish-citizenship/passport-demand-soars-after-turkey-slashes-cost.

- Badarinza, C., & Ramadorai, T. (2018). Home away from home? Foreign demand and London house prices. Journal of Financial Economics, 130(3), 532–555.

- Bailey, M., Farrell, P., Kuchler, T., & Stroebel, J. (2020). Social connectedness in urban areas. Journal of Urban Economics, 119. doi:https://doi.org/10.1016/j.jue.2020.103264

- Balkan, B., Tok, E. Ö., Torun, H., & Tümen, S. 2018. Immigration, housing rents, and residential segregation: Evidence from Syrian refugees in Turkey. Discussion Paper Series 11611, IZA.

- Bertoli, S., Cintia, P., Giannotti, F., Madinier, E., Ozden, C., Packard, M., Redreschi, D., et al. (2019). Integration of Syrian refugees: Insights from D4R, media events and housing market data (pp. 179–199). In A. A. Salah, A. Pentland, B. Lepri, and E. Letouzé (Eds.), Guide to mobile data analytics in refugee scenarios. Switzerland: Springer.

- Braakmann, N. (2019). Immigration and the property market: Evidence from England and Wales. Real Estate Economics, 47(2), 509–533.

- Card, D. (2001). Immigrant inflows, native outflows, and the local labor market impacts of higher immigration. Journal of Labor Economics, 19(1), 22–64.

- Cerulli, G., & Ventura, M. (2019). Estimation of pre-and posttreatment average treatment effects with binary time-varying treatment using Stata. The Stata Journal, 19(3), 551–565.

- Daily Sabah. (2019, June 17). Turkish property sales to foreigners keep up with strong performance, post all-time high in 5 months of 2019. https://www.dailysabah.com/real-estate/2019/06/17/turkish-property-sales-to-foreigners-up-62-in-may.

- Degen, K., & Fischer, A. (2017). Immigration and Swiss house prices. Swiss Journal of Economics and Statistics, 153(1), 15–36.

- Dzankic, J. (2018). Immigrant investor programmes in the European Union (EU). Journal of Contemporary European Studies, 26(1), 64–80.

- Dzankic, J. (2019). The global market for investor citizenship. London: Palgrave Macmillan.

- Erguven, E. (2020). The political economy of housing financialization in Turkey: Links with and contradictions to the accumulation model. Housing Policy Debate, 30(4), 559–584.

- Fietz, J., & Kaschowitz, J. (2019). Counting on kin: The satisfaction of migrants with their social networks in Germany. International Journal of Intercultural Relations, 71, 14–23.

- Gamlen, A., Kutarna, C., & Monk, A. (2019). Citizenship as sovereign wealth: Re‐thinking investor immigration. Global Policy, 10(4), 527–541.

- Gonzalez, L., & Ortega, F. (2013). Immigration and housing booms: Evidence from Spain. Journal of Regional Science, 53(1), 37–59.

- Harter-Dreiman, M. (2004). Drawing inferences about housing supply elasticity from house price responses to income shocks. Journal of Urban Economics, 55(2), 316–337.

- İçduygu, A., & Karadağ, S. (2018). Afghan migration through Turkey to Europe: Seeking refuge, forming diaspora, and becoming citizens. Turkish Studies, 19(3), 482–502.

- İçduygu, A., & Kirişci, K. (2009). Land of diverse migrations: Challenges of emigration and immigration in Turkey. Istanbul Bilgi University Press.

- İçduygu, A., & Millet, E. (2016). Syrian refugees in Turkey: Insecure lives in an environment of pseudo-integration. Working Paper No. 13. Istituto Affari Internazionali.

- Jasinskaja-Lahti, I., Liebkind, K., Jaakkola, M., & Reuter, A. (2006). Perceived discrimination, social support networks, and psychological well-being among three immigrant groups. Journal of Cross-Cultural Psychology, 37(3), 293–312.

- Jun, M.-J., Ha, S.-K., & Jeong, J.-E. (2013). Spatial concentrations of Korean-Chinese and determinants of their residential location choice in Seoul. Habitat International, 40, 42–50.

- Kaya, A. (2017). Istanbul as a space of cultural affinity for Syrian refugees. Southeastern Europe, 41(3), 333–358.

- Kim, H. M., Han, S. S., & O’Connor, K. B. (2015). Foreign housing investment in Seoul: Origin of investors and location of investment. Cities, 42, 212–223.

- Kim, H. M. (2017). Ethnic connections, foreign housing investment and locality: A case study of Seoul. International Journal of Housing Policy, 17(1), 120–144.

- Kirişci, K. (2007). Turkey: A country of transition from emigration to immigration. Mediterranean Politics, 12(1), 91–97.

- Larkin, M. P., Askarov, Z., Doucouliagos, H., Dubelaar, C., Klona, M., Newton, J., … Vocino, A. (2019). Do house prices ride the wave of immigration? Journal of Housing Economics, 46, 101630.

- Mansion Global. (2019, January). Foreign buyers flood Turkey’s struggling housing market. Mansion Global. https://www.mansionglobal.com/articles/foreign-buyers-flood-turkey-s-struggling-housing-market-119713.

- Massey, D. S. (1994). Immigrants and the American City. American Journal of Sociology, 99(5), 1346–1348.

- Massey, D. S., Arango, J., Hugo, G., Kouaouci, A., Pellegrino, A., & Taylor, J. E. (1993). Theories of international migration: A review and appraisal. Population and Development Review, 19(3), 431–466.

- Mavelli, L. (2018). Citizenship for sale and the neoliberal political economy of belonging. International Studies Quarterly, 62(3), 482–493.

- McPherson, M., Smith-Lovin, L., & Cook, J. M. (2001). Birds of a feather: Homophily in social networks. Annual Review of Sociology, 27(1), 415–444.

- Newbold, K. B. et al (2021). The urban geography of segregation (pp. 293–306). In K. Kourtit, B. Newbold, P. Nijkamp, and M. Partridge (Eds.), The urban geography of segregation. Switzerland: Springer Nature.

- Parker, O. (2017). Commercializing citizenship in crisis EU: The case of immigrant investor programmes. Journal of Common Market Studies, 55(2), 332–348.

- Pavlov, A., & Somerville, T. (2020). Immigration, capital flows and housing prices. Real Estate Economics, 48(3), 915–949.

- Pitel, L. (2019, January 27). Turkish passport demand soars as rules relaxed. The Financial Times. https://www.ft.com/content/0d247ad4-1d81-11e9-b126-46fc3ad87c65#comments-anchor.

- Polat, Z. A. (2019). Legal, economic, geographical and demographic analysis of the acquisition of Real Estate by foreign nationals in Turkey. Land Use Policy, 85, 207–217.

- Popescu, R. (2019, January 9). House Hunting in … Turkey. The New York Times. https://www.nytimes.com/2019/01/09/realestate/house-hunting-in-turkey.html.

- Price, M., & Singer, A. (2008). Edge gateways: Immigrants, suburbs, and the politics of reception in metropolitan Washington. In A. Singer, W. Hardwick, & C. B. Brettell (Eds.), Twenty-first century gateways: Immigrant Incorporation in Suburban America (pp. 137–170). Washington, DC: Brookings Institution Press.

- Sa, F. (2015). Immigration and house prices in the UK. The Economic Journal, 125(587), 1393–1424.

- Saiz, A. (2003). Room in the kitchen for the melting pot: Immigration and rental prices. Review of Economics and Statistics, 85(3), 502–521.

- Saiz, A. (2007). Immigration and housing rents in American cities. Journal of Urban Economics, 61(2), 345–371.

- Serin, B., Smith, H., & McWilliams, C. (2020). The role of the state in the commodification of urban space: The case of branded housing projects, Istanbul. European Urban and Regional Studies, 27(4), 342–358.

- Smith, H.L. (2019, August 29). Saudis snap up homes in Turkey as top foreign buyers. The Times. https://www.thetimes.co.uk/article/saudis-snap-up-homes-in-turkey-as-top-foreign-buyers-37q7sjr8g.

- Surak, K. (2020). Who wants to buy a visa? Comparing the uptake of residence by investment programs in the European Union. Journal of Contemporary European Studies, 1–19. doi:https://doi.org/10.1080/14782804.2020.1839742

- Treanor, S., & Vivienne, N. (2019, October 1). How selling citizenship is now big business. BBC. Retrieved https://www.bbc.com/news/business-49958628

- TRTWorld. (2019, April 18). Property sales to foreigners hit record levels in Turkey. TRTWorld. https://www.trtworld.com/turkey/property-sales-to-foreigners-hit-record-levels-in-turkey-25977.

- Tumen, S. (2016). The economic impact of Syrian refugees on host countries: Quasi-experimental evidence from Turkey. American Economic Review, 106(5), 456–460.

- Tunc, C. (2020). The effect of credit supply on house prices: Evidence from Turkey. Housing Policy Debate, 30(2), 228–242.

- Viruell-Fuentes, E. A., Morenoff, J. D., Williams, D. R., & House, J. S. (2013). Contextualizing nativity status, Latino social ties, and ethnic enclaves: An examination of the ‘immigrant social ties hypothesis’. Ethnicity & Health, 18(6), 586–609.

- Wither, E., & Erkoyun, E. (2019, October 1). Iranian home buyers dodge sanctions, make Turkey their plan B. Reuters. https://www.reuters.com/article/us-Turkey-iranians-idUSKBN1WG3ON.

- Xu, X., El-Ashram, A., & Gold, J. (2015). Too much of a good thing? Prudent management of inflows under economic citizenship programs, IMF Working Paper, WP/15/93. International Monetary Fund https://www.imf.org/external/pubs/cat/longres.aspx?sk=42884.0.

- Yener, C., Unal, S., Ertugrul, H. M., & Alp, A. (2020). Housing price dynamics and bubble risk: The case of Turkey. Housing Studies, 35(1), 50–86.

- Yesilbag, M. (2020). The state-orchestrated financialization of housing in Turkey. Housing Policy Debate, 30(4), 533–558.

- Zelinsky, W., & Lee, B. (1998). Heterolocalism: An alternative model of the socio-spatial behaviour of immigrant ethnic communities. International Journal of Population Geography, 4(4), 281–298.