Abstract

The recent wave of innovation in the pension and longevity risk transfer market is barely a decade old, but more than U.S. $470 billion in global transaction activity has taken place, mainly in the United Kingdom, the United States, Canada, and the Netherlands. The main deals have been buy-outs, buy-ins, and longevity swaps for pension schemes. Similar derisking solutions have spread to the market for insured annuities. But transactions must be simplified, standardized, and made available to all pension schemes, regardless of size. They must also cover younger deferred scheme participants, as well as those in collective schemes where intergenerational risks are important. New investors must be brought in, and one way of doing this is via sidecars. Capital relief is important in reducing the costs of insurance-based solutions, such as those involving tail-risk protection; regulators need to become more comfortable with such deals.

1. INTRODUCTION

Dr. Richard Sandor, economist, “father of financial futures,” and serial starter of new markets, devised the “Seven-Stage Market Development Process,” a framework for understanding how markets evolve and grow.Footnote1 According to Sandor, market development has seven stages:

A structural change occurs within an economy.

A commodity is standardized.

Evidence of ownership is created for trading purposes.

Informal markets are developed.

Formal markets are refined.

Hedging mechanisms or futures markets are established.

Diverse, bilateral transactions begin.

Sandor’s paradigm is valid for the pension and longevity risk transfer markets, which were born from structural economic changeFootnote2 and are currently undergoing worldwide standardization. With five more stages of the development process remaining, these markets hold tremendous promise, as more than U.S. $470 billion in global transaction activityFootnote3 has already occurred in just one decade, since the market took off in the United Kingdom in 2006.Footnote4

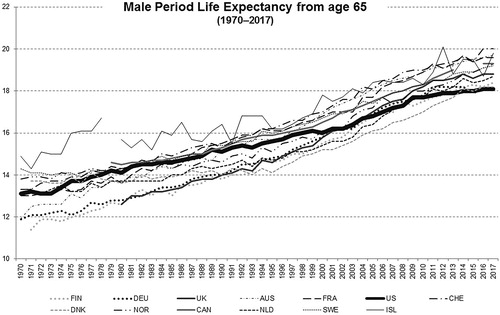

These markets are also vitally important to society as a whole, given that recent studies show life expectancies are trending upward around the world. For example, the retired lifetimes—or life expectancies at age 65 years—for males in the United States, the United Kingdom, Canada and other countries have lengthened significantly since 1970, and improvements in life expectancy are continuing.

While longer life expectancy is a favorable trend for us all, it brings with it the potential for more years spent in retirement.Footnote5 And when life expectancies rise, pension obligations increase for sponsors of defined benefit schemes, insurers that write annuities, and individuals who may not be prepared for a secure retirement.

The challenge, then, is how to provide retirement security for real people, while offering risk management solutions for pension funds delivering pensions and insurance companies writing annuities. In this article, we examine the state of innovation within the longevity and pension risk transfer markets, and explore how advancements in this essential space can help solve a pressing societal challenge: the graying of the global population.

2. RIDING A WAVE OF INNOVATION

The past decade has seen a groundswell of innovative solutions for helping defined benefit pension funds manage or transfer risk. The three primary solutions are buy-outs, buy-ins, and longevity risk transfer. Each of these solutions is flexible and customizable, and can be tailored to meet the specific needs of pension funds and insurers in a variety of countries.

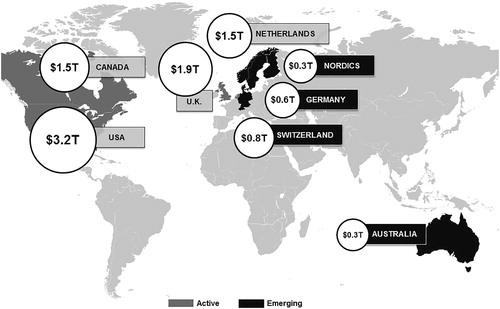

The wave of innovation has been most profound in the United States, the United Kingdom, Canada, and the Netherlands, which is no coincidence, as these are the four largest defined benefit pension markets in the world. In these markets—which range from U.S. $1.5 trillion to U.S. $3.2 trillion in defined benefit promises (see )—each country has experienced significant changes in accounting rules, funding requirements, and risk awareness, which in turn have given rise to a multitude of new solutions. As a result, companies from those nations, including firms of all sizes and from all sectors, have taken steps to proactively derisk their pension schemes.

FIGURE 1. Largest Defined Benefit Pension Markets (Market Size Estimated in USD tn). Source: Willis Towers Watson 2019 Global Pension Asset Study. U.S. data from Investment Company Institute as of Dec. 31, 2018. U.K. data from PPF, estimated in USD as of March 31, 2018. Nordics data from OECD as of 2015.

The market took off in the United Kingdom in 2006—and what happened there was observed with keen interest by scheme sponsors in other parts of the world, especially in North America. In 2012, the U.S. market experienced its own watershed moment, as mega transactions by General Motors and Verizon put U.S. pension risk transfer on the map. The Canadian market has also broken through, and now boasts over U.S. $26 billion of liabilities having been transferred since 2007.Footnote6

Over the coming decade, several smaller markets—each with less than U.S. $1 trillion in defined benefit obligations—are likely to benefit from the same pension derisking innovations employed in the United States, the United Kingdom, and elsewhere. These smaller markets include Australia, Germany, Switzerland, and the Nordic countries.

While the derisking solutions were spreading across the global pension landscape, a more recent and closely related market has emerged—the market to derisk insured annuity blocks.

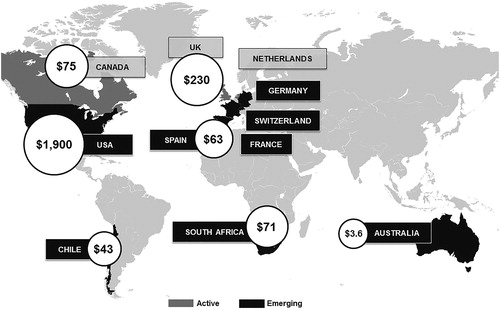

Insurance companies in Canada, the Netherlands, and the United Kingdom are benefitting from advancements in annuity risk-management solutions. And there are other markets with the potential to gain from these innovations in the years to come, such as Chile, France, Germany, Switzerland, the United States, South Africa, Spain, and Australia (see ). Combined, these advancements in pension and insured annuity risk management have set the stage for continued growth in the worldwide longevity risk transfer marketplace.

FIGURE 2. Global Market for Insured Annuities (Market Size Estimated in USD bn). Sources: USA: Morningstar, Inc. and Insured Retirement Institute, total variable annuity net assets, 2016; UK: SynThesys Life, from FSA returns, net reserves, 2008 data; Canada: CLHIA, 2016; Chile: World Bank, 2014, estimates; Spain: ICEA, 2016; South Africa: FSB, ASISA, 2017, estimates; Australia: Strategic Insight, lifetime annuity assets, 2017. Note: It proved to be very difficult to get reliable estimates for the size of the annuity market in some countries and impossible for other countries; the figures reported in this table should be treated as approximate.

3. PREPARING FOR AN OLDER SOCIETY

The innovations occurring within the pension and longevity risk transfer space are designed to help prepare for the graying of society. Across the globe, the elderly are an increasing share of the population as life expectancies increase and birth rates decline.

As evidence of this fact, consider that the retired lifetime of the average American male has increased 40% since 1970, and now U.S. and U.K. males can expect to spend 18 or 19 years in retirement, while males in Canada can expect to live even longer. Australian men surpass their U.S., U.K. and Canadian counterparts, with a half-year advantage over the United Kingdom and North America.Footnote7

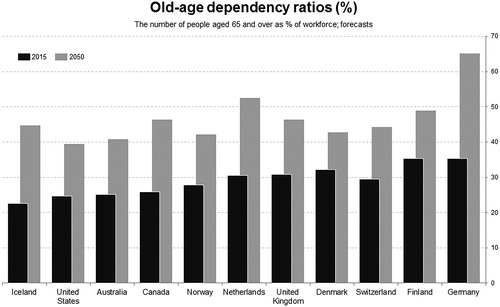

This graying of society exacerbates the old-age dependency ratio, which measures the ratio of those typically not in the labor force compared to those who are typically working. This ratio is further used to measure the pressure on the working segment of the population, and illustrates how those individuals of working age—and the overall economy—bear a greater burden in supporting an aging population.

A high dependency ratio can create significant difficulties for a nation if its governmental expenditures are heavily weighted toward public health, social security, and education—programs that are most often used by the oldest and youngest in a population. The fewer working people there are in the population, the greater is their burden to support the retired members of society.

illustrates the graying trend occurring in 11 economically developed countries. In 2015, in this handful of countries, there were approximately four to five working people for every one retired person. By the year 2050, however, these same nations will have one retired person receiving support from just two or three in the workforce—and the situation is projected to become more severe.

FIGURE 3. Growing Dependencies. Source: OECD (2015), Pensions at a Glance 2015: OECD and G20 indicators, OECD Publishing, Paris. http://dx.doi.org/10.1787/pension_glance-2015-en. Data extracted on 22 Sep 2016.

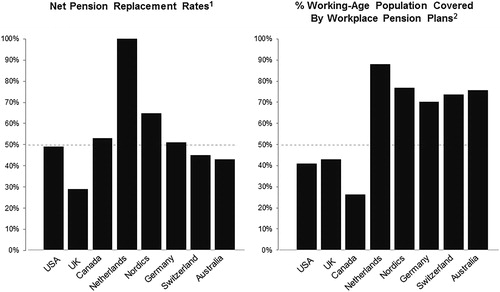

Further aggravating the problem is the fact that most of these countries are falling short of even 50% replacement rates—that is, the percentage of preretirement income that pensioners can expect to live on in retirement. Apart from a few nations, the replacement rate is less than half, and vast groups of working-age people are not even covered by workplace pension schemes (see ).

FIGURE 4. Preretirement Income Replacement Rates. 1Source: OECD, 2016. Net pension replacement rates (indicator), doi; 10, 1787/4b03r028-en (accessed on Aug. 26, 2019). The net replacement rate is defined as the individual net pension entitlement divided by net preretirement earnings, taking into account personal income taxes and social security contributions paid by workers and pensioners. Nordics data are average. 2Source: OECD, 2016. Estimates from Global Pension Statistics and OECD calculations using survey data. Coverage rates are provided with respect to the total working-age population (i.e., individuals aged 15–64 years) for all countries except Germany, where coverage rate is provided with respect to employees aged 25 to 64 years old subject to social insurance contributions. Data for Canada do not include participants covered in the Canada Pension Plan. Nordics data are average of mandatory/quasi-mandatory pensions. http://dx.doi.org/10.1787/888933634629 (accessed August 26, 2019).

The implications of this global phenomenon are clear:

Workers require greater access to retirement savings programs with access to professional investment management.

More individuals will need to continue working past their normal retirement age.

Meaningful and productive part-time work for retired people is essential.

Tax, health, and welfare policies that incentivize work, especially at higher ages, are required.

Lifetime income solutions are needed more urgently than ever before.

There is no “gray area” when examining societal aging. Rather, it is abundantly clear that a great deal of work needs to be done to address this growing global concern.

4. IDENTIFYING THE RIGHT SOLUTION

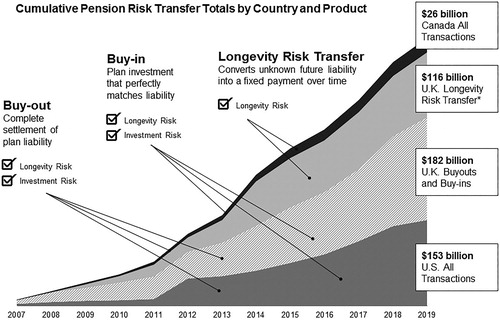

shows the geographical breakdown of the more than U.S. $470 billion in pension and longevity risk transfer transactions that have occurred since 2006 in the United States, United Kingdom and Canada. It also shows that the transactions completed to date have included pension buy-outs, buy-ins and longevity risk transfer agreements. This variety of solutions begs the question: which approach is right for each individual pension fund?

FIGURE 5. Growing Global Marketplace. Note: Data in USD. Sources: LIMRA, Hymans Robertson, LCP and Prudential analysis as of June 30, 2019. *Includes the HSBC $8.7 billion (£7.0 billion) captive longevity swap completed in Q3 2019.

The U.K. market has involved all three types of agreement. By contrast, all the transactions in the United States to date have been pension buy-outs or buy-ins. These are holistic (full indemnity) solutions, whereby the insurer assumes all asset and liability risks. Given the massive size of the United States, it is striking that the country’s total transaction volume is significantly less than that of the United Kingdom.

Over and above transaction volume, there are several other key differences between the U.S. and the U.K. markets. For example, a large majority of agreements occurring in the United States are pension buy-outs, wherein the liability is settled and completely removed from the scheme sponsor’s balance sheet. With these transactions, the insurer issues annuity certificates to the participants, who look only to the insurer for payment thereafter. This solution is ideal any time a company wants to reduce the size of the pension liability, and can be particularly helpful in corporate restructurings.

Conversely, most U.K. transactions are pension buy-ins, whereby an annuity contract is held as a liability-matching asset that pays the pension fund the exact amount needed to fulfill the benefit obligations for as long as scheme participants live—and regardless of what happens to the underlying assets. Because the liability is not settled, this option is rarely used in the United States, but is commonly employed in the United Kingdom for pension funds that are on the road to a scheme termination. A pension buy-in is also appropriate for companies taking steps in a phased derisking program.

An increasingly popular solution in both the United Kingdom and Canada is longevity risk transfer (or longevity swap). The longevity risk transfer products available today convert an unknown future liability into a fixed liability cash flow by locking in an agreed set of mortality assumptions and hence fixing the life expectancy of the scheme participants.

Under the terms of these full indemnity contracts, insurers pay the pension funds if participants outlive projections, providing the funds with a known and certain benefit obligation, with any excess being the responsibility of insurers and reinsurers. With a fixed and known future obligation, large pension funds can more easily manage an asset portfolio against a liability. Longevity risk transfer is often the last step for pension funds in “do-it-yourself” pension derisking programs.

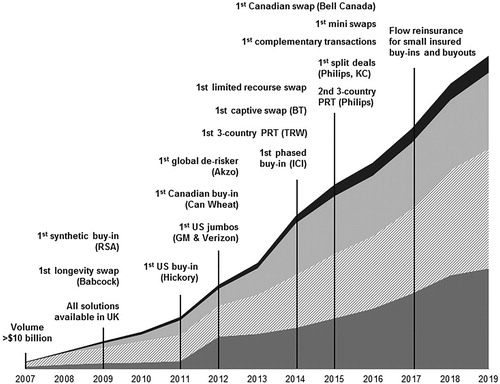

illustrates how the Canadian market (shown in black at the top)—while diminutive when compared to the United States and United Kingdom—is exceptional, as it is the only market outside of the United Kingdom where pension buy-ins, buy-outs, and longevity risk transfer have all been completed. As also shown in , there have been many notable innovations over the past decade.

FIGURE 6. Milestones in Pension Derisking. Sources: LCP, Hymans Robertson, LIMRA and Prudential analysis, as of Q3 2019.

A defining moment occurred in 2007—the first year market volume in the United States, the United Kingdom, and Canada combined exceeded U.S. $10 billion. By 2009, all three solutions—buy-out, buy-in, and longevity risk transfer—had become available in the United Kingdom, and that same year the first longevity swap involving a pension scheme was completed in Great Britain by Babcock International and Credit Suisse. The U.K. market also saw its first “synthetic” buy-in agreement in 2009, which involved combining a total return swap with a longevity swap to create a synthetic buy-in solution.

5. CROSSING THE POND

Pension risk transfer solutions popular in the United Kingdom “crossed the pond” in 2011 with the completion of the first U.S. pension buy-in, a U.S. $75 million agreement with North Carolina-based Hickory Springs Manufacturing Company.

A year later the U.S. market’s potential became apparent with a groundbreaking, U.S. $25 billion pension buy-out transaction with General Motors. That mega deal was quickly followed by a market-defining, U.S. $7.5 billion buy-out agreement with Verizon Communications.

These two transactions stand out as the largest U.S. pension buy-out agreements ever completed. And although buy-out transactions have been occurring in America since 1928, agreements on the scale of GM and Verizon were game-changing. Having determined that the burden of managing enormous pension liabilities was diverting focus from their firms’ core businesses, GM and Verizon took action to divest those liabilities—and other scheme sponsors soon followed suit.

The Canadian market also achieved an important milestone in 2012 with its first pension buy-in transaction, a Can$150 million deal between the Canadian Wheat Board and Sun Life Financial.

6. LAUNCHING “MOON SHOTS”Footnote8

While Canada was bearing witness to its first pension buy-in agreement, the world’s first global derisking company emerged: AkzoNobel. In 2012, the Dutch chemical and manufacturing giant embarked on a multiyear, transnational journey to derisk its numerous pension funds—a journey that continues to this day. Take, for example, Imperial Chemical Industries (ICI), a United Kingdom-based AkzoNobel company. ICI—which was acquired by AkzoNobel in 2008—began derisking its pension funds in phases in 2014, and to date has completed 11 buy-in transactions with four different insurers, covering more than £8 billion of liabilities.

While ICI was derisking in phases, TRW—an automotive and aerospace company—was launching a successful pension risk transfer “moon shot” of its own. In 2014, TRW became the first multinational corporation to simultaneously complete three derisking transactions in three different countries: Canada, the United Kingdom, and the United States. This was a tremendous accomplishment, for although the three nations have comparable buy-in and buy-out strategies available, they are vastly different when it comes to the pension benefits and regulatory procedures to be addressed in a derisking process.

The longevity risk transfer market also had a banner year in 2014—both in transaction volume and in innovation. On July 4 of that year, the British Telecom (BT) Pension Scheme became the first pension fund to establish its own insurance captive to gain access to nearly U.S. $28 billion in longevity reinsurance capacity. The deal stands as the world record holder for the largest and most innovative pension risk transfer agreement ever consummated.

Also in 2014, the Aviva Staff Pension Scheme took a different approach to longevity hedging by completing the first limited recourse longevity swap. That transaction, which involved £5 billion in liabilities and 19,000 participants, is discussed later in this article.

With 2015 came another successful pension risk transfer “moon shot.” The technology company Philips not only completed simultaneous pension risk transfer agreements in multiple countries, it also increased the degree of difficulty by splitting its U.S. transaction among three insurers to optimize price and capacity.

Those who have experience in pension derisking understand that these agreements can be quite intricate, which makes the Philips transaction so remarkable. Transacting in multiple segments, with multiple insurers and in multiple countries, demonstrated extraordinary commitment on behalf of Philips—a commitment that ensured its participants’ retirement benefits would continue to be provided and protected.

In another 2015 multi-insurer transaction, Kimberly-Clark Corporation purchased group annuity contracts from two insurers that reduced the company’s pension liabilities by approximately U.S. $2.5 billion. The split transaction enabled Kimberly-Clark to achieve the most favorable pricing and capacity, while enhancing the security of its retirees' benefits.

7. COMPLETING COMPLEMENTARY DEALS

While split transactions were trending in the United States and United Kingdom, the Canadian market introduced something completely different: the first complementary pension risk transfer buy-in agreement. With this creative solution, two unrelated Canadian companies collaborated to purchase an approximate Can$530 million joint annuity contract from Sun Life Financial, thereby transferring investment, inflation, and longevity risk to the insurer.

This unique agreement came about when the team from Sun Life noticed the two firms each had unusual cost-of-living adjustments in their pension benefits. Individually they would be difficult to hedge, but the cost-of-living adjustments complemented one another, creating an opportunity that led to the simultaneous closing of both transactions, with inflation risk managed on a combined basis. This generated significant cost savings for both companies because Sun Life was able to pool the inflation risk for both schemes and create a more efficient asset strategy.

In 2015, the first mini-longevity swaps closed in the United Kingdom, as well as a groundbreaking longevity risk transfer transaction in Canada. In the latter agreement—the first of its kind in North America—Bell Canada transferred Can$5 billion in pension liabilities for current retirees to Sun Life Financial, which in turn received reinsurance capacity from Reinsurance Group of America and SCOR Global Life. This transaction marked a turning point in the global market, with Canada becoming the first nation apart from the United Kingdom to have all three pension risk transfer solutions actively in use.

Viewed retrospectively, it is clear the past decade of pension risk transfer innovation has been driven by three key marketplace dynamics:

Greater customization and capacity.

Globalization of derisking techniques that have begun in the United Kingdom.

Heightened global support for companies seeking to reduce pension risk—be it via large transactions in multiple countries, or gradually in phases.

8. TRANSFERRING LONGEVITY RISK

The longevity risk transfer market has seen its own share of innovations, and now boasts a comprehensive set of solutions for jumbo pension funds seeking to transfer risk into the deep and relatively liquid global reinsurance market.

Designed to create certainty around future benefit obligations, longevity risk transfer enables pension funds to better manage assets against known liabilities. If scheme participants live longer than expected, the insurers and reinsurers in this market will pay the incremental benefits for as long as the covered persons live, giving the pension fund a fixed and known future obligation.

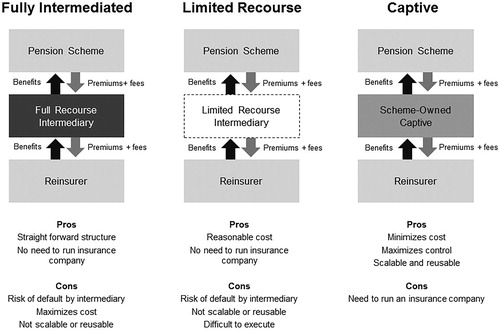

The key to each of the longevity risk transfer solutions for pension funds is the entity serving as the intermediary between the pension scheme and the reinsurer. In the United Kingdom, pension schemes cannot transact directly with reinsurers—there must be a primary insurer in the middle (see ).

FIGURE 7. Reinsurance Solutions for Jumbo Schemes.

The earliest longevity risk transfer solution was fully intermediated, with a bank or an insurer serving as a full-recourse intermediary between the pension scheme and the reinsurer (, left diagram). These transactions could be cost-prohibitive, however, as the intermediary assumes credit risk from both the scheme and the insurance company.

Additionally, there is the limited recourse solution pioneered by the Aviva Staff Pension Scheme (, center diagram). Within this approach, the intermediary exchanges only the premiums, fees, and benefits payments it actually receives from the other parties. The downside to these transactions is the risk of intermediary default, which is beyond the pension fund’s control, but could result in loss of cover and financial loss to the scheme.

The third longevity risk transfer strategy involves a scheme-owned captive insurer—a solution that the Prudential Insurance Company of America (PICA) introduced for the groundbreaking BT Pension Scheme transaction (, right diagram). That agreement covered liabilities of £16 billion, or nearly U.S. $28 billion. To complete the transaction, the scheme created its own captive insurer located in Guernsey, which insured the longevity risk. The captive insurer then reinsured the risk to PICA in a fully collateralized arrangement. The scheme’s immense scale and advanced capabilities helped it to become the first to execute such a transaction—now, smaller schemes can benefit from this advance.

With this longevity hedge in place, the BT Pension Scheme can continue managing its assets against a fixed and known future liability, which is much easier than managing assets against obligations that are unknown and unknowable. The transaction also enables BT to pay for its derisking over time, and to divest a risk it views as unrewarded.

By creating its own captive to transact directly with a reinsurer, BT was able to save on transaction fees and gain wider access to the global reinsurance markets, thereby achieving the best value for the scheme. The transaction enabled the BT Pension Scheme to overcome the expense and risk of the other two solutions—but only because BT was able to operate its own insurance captive for the life of the transaction, which requires significant commitment.

With three proven strategies available, jumbo pension schemes from a variety of circumstances and with widely diverging objectives can gain access to the global reinsurance markets and leverage the solutions that best meet their needs.

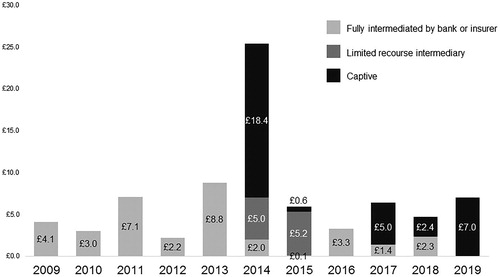

Captive and limited recourse transactions have dominated the market since 2014, when the first of these agreements were completed. As illustrated in , fully intermediated solutions (shown in the lightest gray) have decreased in popularity, primarily due to the expense involved. The introduction of the limited recourse structure (shown in the darker gray) and the captive solution (shown in black) have tipped the scales in favor of these two more cost-effective solutions.

FIGURE 8. U.K. Longevity Transactions Since 2008. Source: Hymans Robertson as of Q3 2019, and Prudential analysis.

While the longevity risk transfer market has gained considerable momentum in the past decade and has been propelled by the advent of innovative and highly effective solutions, a significant challenge still remains. The transactions that have proven beneficial to jumbo pension schemes must be simplified, standardized and made available to smaller pension schemes because longevity risk is not only a burden of the largest schemes.

9. EXAMINING LIABILITY RISK

As mentioned earlier, pension funds assume the very real risk of participants living longer than projected. Lengthening life expectancy obligates pension sponsors to contribute additional resources to their schemes to fund future liabilities, and when participants outlive expectations, sponsors’ liabilities increase. Pension funds are then burdened with heightened inflation, interest rate, and duration risk.

illustrates the retired lifetimes—or life expectancy at age 65—for men in a variety of developed countries. It shows how long 65-year-old males have been expected to live since 1970, and how expectations have changed around the globe.

FIGURE 9. Increasing Retired Lifetimes. Source: OECD (2019), Life expectancy at 65 (indicator). https://doi.org/10.1787/0e9a3f00-en (accessed on 13 August 2019).

As mentioned previously, the typical male in the United States and United Kingdom can expect to spend 18 to 19 years in retirement, compared to just 12 and 13 years in 1970. This trend is consistent across developed countries, including Germany and the Netherlands, Canada, France, Switzerland, Australia, and the Nordics.

As shows, there is an unmistakable trend toward longer life, but the pace of the longevity improvements varies through time and has slowed in recent years. As advances in medical breakthroughs emerge, we will see higher rates of longevity improvement and an increase in pensioner annuity liabilities. These liabilities may rise sharply if actuaries adopt new mortality tables that represent a significant shift in assumptions. Or they may increase gradually if the extent of the improvements is recognized slowly over time.

10. CHALLENGING MARKETPLACE CONDITIONS

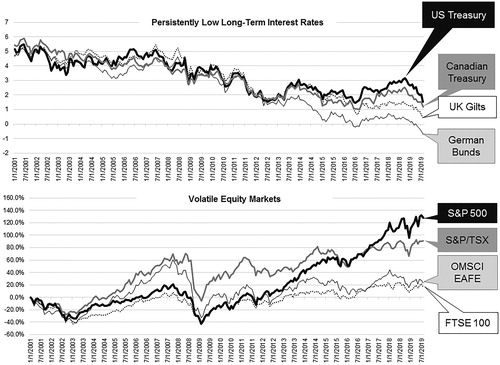

While the pension and longevity risk transfer markets have experienced significant momentum and growth over the past decade, activity in 2016 was noticeably reduced by difficult financial market conditions, in particular, increased pension scheme deficits.

Interest rates have generally been declining since 2000 (see ), and as rates fall, liabilities discounted at bond yields have skyrocketed. Today, several economies across the globe are facing the prospects of negative interest rates, with central banks in the Nordic countries, Japan, and Europe all testing these lower bounds.

FIGURE 10. Low Rates and Volatile Equities. Source: Barclay’s Live and S&P Capital IQ, as of August 31, 2019.

Pension schemes are also affected by market volatility. For example, twice since 2000, the 100 largest U.S. corporate pension schemes lost more than 30% of funded status due to market declines (see ). When funded-status downturns occur, cash infusions are often required, corporate income can fall, and liabilities rise, just when the underlying business is struggling, because volatility is worst during recessions.

FIGURE 11. Funded Status Volatility. Sources: Milliman 100 Pension Funding Index; the 100 largest U.S. corporate pension plans reporting under GAAP, June 30, 2019 (88.0%). Aon Hewitt, “Aon Hewitt Global Pension Risk Tracker,” as of June 30, 2019 (99.3%). https://PensionRiskTracker.aon.com, accessed August 13, 2019. Funding ratio (cumulative assets/liabilities) of all pension schemes in the FTSE 100 Index on the accounting basis.

Consider this: Since the end of the financial crisis in 2009, favorable U.S. equity market performance and more than U.S. $500 billion in cash contributions have largely been neutralized by falling interest rates, leaving the average scheme funded status only modestly better than at the end of the Great Recession.

U.K. schemes in the FTSE 100 have generally been more stable and better funded, though only a few have been resilient to the recent market turmoil caused by the Brexit vote. In general, we find a “tale of two cities” in the defined benefit pension arena.

Companies that started on a steady derisking path and moved toward fixed income years ago—when rates were higher—are generally stable and can continue managing and reducing risk. But those still waiting for rates to return to historical norms may be waiting endlessly, and in vain. Solutions are needed for those pension schemes that are waiting in the wings—solutions that help them manage risky assets while they take aim at a lower-risk future.

11. INTRODUCING NEW SOLUTIONS

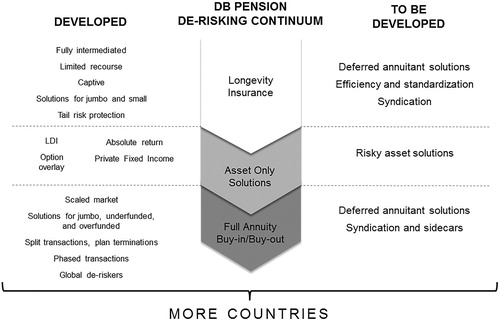

The past decade has given rise to a spate of innovative defined benefit scheme derisking solutions—but more are required. Pension derisking can be thought of as existing on a continuum: one that includes longevity-only solutions, asset-only solutions, and combined solutions that address all risk (see ).

FIGURE 12. Developing New Solutions.

Within the longevity-only segment, pension schemes both large and small can choose how they come to market, and whether to transfer all risk, or just tail risk (i.e., a severe loss event that has a small likelihood of occurring). However, more needs to be done toward:

Covering younger deferred scheme participants.

Creating efficiency and standardization in smaller transactions.

Syndicating larger ones.

In the asset-only segment, pension funds have many asset classes from which to choose, but in today’s extreme low interest-rate environment, many require assistance in managing the volatility associated with the riskier assets they must hold to earn a return.

In the full-annuity segment, pension schemes of all sizes and sectors can be assisted with a host of challenges. But here too, more work is needed in covering younger deferred scheme participants, and syndication and sidecar solutions will be required in the future to support continued growth.

Perhaps most importantly, all of the solutions currently being used in the United States, the United Kingdom, Canada, and the Netherlands must be made available to more pension schemes in more countries.

12. GOING DUTCH

There is an important area of the pension market that has not garnered enough attention: the Dutch model of collective defined contribution (CDC) schemes (see ). These schemes can be thought of as hybrids that include the characteristics of both defined benefit and defined contribution schemes.

FIGURE 13. Annuity Insurer Transactions. Note: As of July 2019. Source: Prudential analysis of disclosed transactions. Note that many transactions are not disclosed. Transactions have occurred in Germany, Canada, and the United States but transactions sizes were not disclosed. *These deals provide tail risk protection against future longevity improvements.

With a CDC scheme, members’ benefits build throughout their working lifetime. There are no individual accounts; rather, members accumulate savings in a professionally managed fund and pool their risk. Members receive lifetime payments starting at retirement, and the schemes are designed to deliver a level of income that is comparable to conventional defined benefit schemes.

Employers bear limited risk; the risk of investment losses and people living longer than projected is assumed by the members as a group. Benefits can be reduced if assets fail to perform, or if longevity exceeds expectations. Collective schemes often have tens of thousands of members in a single scheme and often also benefit from economies of scale and world-class asset management.

A downside to these schemes exists, however, and that is significant intergenerational risk. Younger members paying into the scheme may have to subsidize the increasing longevity of members who are already retired, which could be burdensome. To address this shortcoming, the risk budgeting and risk transfer techniques currently available for the defined benefit pension sector must be adapted for CDC schemes, which many believe are the savings vehicle of choice for expanding access to pension programs for the millions who do not have a workplace benefit.

13. MANAGING INSURED ANNUITY RISK

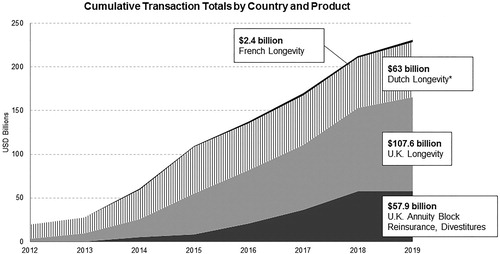

Pension schemes are not the only entities seeking relief from pension and longevity risk. In fact, since 2012, there have been U.S. $230 billion in transactions for insurers managing annuity risks (see ). These include:

$57.9 billion of U.K. annuity blocks that have been reinsured or sold.

$173 billion in longevity risk transfer transactions for U.K., French and Dutch insurers.

understates the total market activity, however, as several billion in transactions have been completed for German, Canadian, Dutch, and U.S. annuity writers, but scant details have been disclosed on those arrangements. Regardless, the market is clearly flourishing, and it has been driven by the emergence of several key innovations (see ).

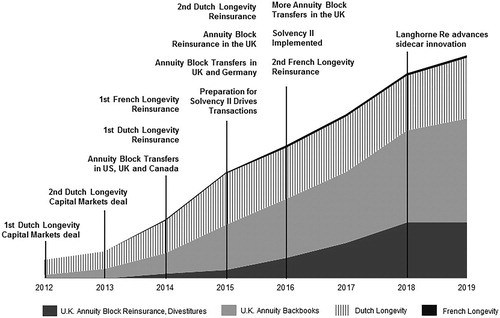

FIGURE 14. Insured Annuity Innovations. Note: As of July 2019. Source: Prudential analysis of disclosed transactions. Note that many transactions are not disclosed. Transactions have occurred in Germany, Canada, and the United States but transactions sizes were not disclosed.

In 2012, the Dutch insurer Aegon completed the Netherlands’ first longevity hedge transaction—a deal executed specifically to manage tail risk. This “out-of-the-money” transaction only covers an extreme longevity event, and doesn’t begin to pay until mortality rates have fallen considerably farther than expected. The following year, Aegon completed its second tail risk transaction. Both of these capital markets agreements were accomplished with the assistance of investment banks, and established Aegon as the pioneer in index-based tail risk protection. Delta Lloyd, another Dutch insurer, executed two similar hedges in 2014 and 2015.

By 2014, risk transfer for insured annuity blocks was gathering momentum in the United States, the United Kingdom, and Canada, where significant annuity back books were sold in merger and acquisition (M&A) style transactions (see ). Also in 2014, Dutch tail-risk transactions came to market in reinsurance form, led by the Reinsurance Group of America, and the first-ever longevity reinsurance deal was completed in France.

FIGURE 15. Longevity Risk in Alternative Markets. Source: http://www.artemis.bm/library/longevity_swaps_risk_transfers.html. *These Dutch transactions provide “out-of-the-money” tail risk protection against future longevity improvements.

With 2015 came a wave of annuity risk transfer transactions designed to prepare European insurers for Solvency II.Footnote9 These included M&A style annuity block transfers in the United Kingdom and Germany, as well as over $11 billion of longevity reinsurance completed for U.K. annuity back books to optimize capital.

The U.K. transactions were all full-indemnity—”at the money”—swaps, wherein the parties agree on the best estimate liability, and the reinsurer covers any increase in life expectancy beyond current expectations.

The implementation of Solvency II in 2016 not only resulted in more annuity block transfers in the United Kingdom, it also compelled many non-United Kingdom insurers to question how U.K. risk management techniques could be applied to their own capital optimization challenges. What is clear to market participants today is that European annuity writers in the post-Solvency II world will need reinsurance capacity to:

Efficiently manage annuity obligations.

Provide cost-effective coverage for customers.

Optimize capital.

Without question, reinsurance capacity for the global longevity and annuity sector is paramount, and demand is almost certain to exceed supply. Today, reinsurance capacity remains sufficient for current levels of activity, but a capital market solution will be needed as demand increases. This will take time to develop for a few reasons:

Reinsurers have many advantages when analyzing longevity risk with large teams of experts and access to proprietary data that the market does not have. Reinsurers also have economic advantages, including diversification benefit between mortality and longevity, tax benefits for reserving, and lower hurdle rates of return. Hedge funds and other investors will face challenges replicating these benefits without excessive leverage.

Investor appetite has been focused on index based solutions with a relatively short tenor, which raise concerns about how well the actual risk can be hedged in the capital markets.

Pension funds and insurers with annuity obligations know that their covered groups will often be more affluent and have different longevity improvements than the population as a whole, causing them to favor indemnity reinsurance for the whole of life when they seek a longevity hedge.

Reinsurers use longevity risk to balance the trend risk in their mortality exposures. Once reinsurance capacity becomes scarce and reinsurer pricing rises, there will be more room for alternative capital to participate in the longevity risk transfer market alongside the reinsurer community. In the absence of a vibrant capital market for longevity, innovative ways to bring alternative capital into the market will be required.

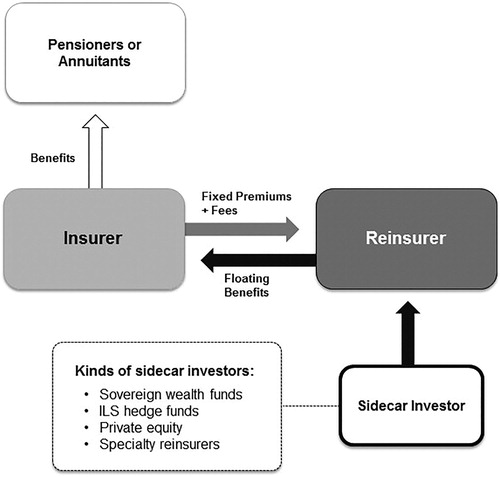

14. HITCHING UP THE SIDECAR

Because capital market solutions have been slow to materialize, sidecar arrangements may be the preferred strategy going forward. A reinsurance sidecar is a financial arrangement created to enable investors to assume the risk and benefit from the return of specific books of insurance or reinsurance business.

The sidecar approach offers many advantages. In some transactions, investors may be able to take a proportionate share of profits and losses alongside a reinsurer with its own capital at risk on the same terms. Sidecar arrangements can enable investors to co-invest with the insurers and reinsurers in the pension and longevity risk transfer markets (see ).

FIGURE 16. Sidecar Solutions.

Reinsurance sidecar

A financial structure established to allow investors (often external or third-party) to take on the risk and benefit from the return of specific books of insurance or reinsurance business. Typically set up by existing re/insurers who are looking to either partner with another source of capital or set up an entity to enable them to accept capital from third-party investors.

This approach would enable investors to benefit from insurance and actuarial expertise, as well as the access to big data on historical mortality experience that reinsurers use to analyze these opportunities. The market has seen developments in this ideal version of sidecar investing. In 2018, RGA, RenaissanceRe, and investors created Langhorne Re for transactions over U.S. $5 billion, which was a major advance for sidecar innovation.

If several market participants are allowed to come together, with each taking its preferred share of risk, the sidecar investing market could gain momentum. The question then becomes, how can sovereign wealth funds, insurance-linked securities hedge funds, private equity funds, and others provide alternative capital to fuel the continued—and explosive—growth in the pension and longevity risk transfer markets?

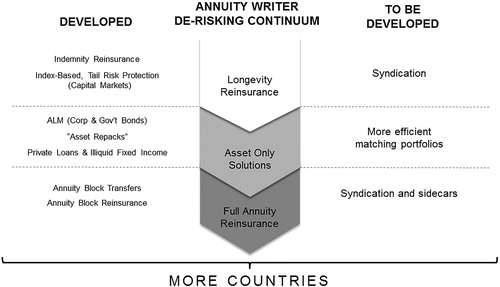

15. ANNUITY WRITER DERISKING CONTINUUM

The derisking continuum for insurers managing annuity risks shares many of the same innovations that help pension sponsors derisk their schemes (see ). Further, insurers are applying these techniques to their balance sheets to manage annuity obligations.

FIGURE 17. Development of Innovative Solutions for Annuity Writers.

In the longevity-only segment, many insurers are using longevity reinsurance and tail risk protection and would like to continue to do so. But recent questions about capital relief for tail risk dealsFootnote10 have shown that regulators still favor “at-the-money” full indemnity reinsurance. Regulators may need to become more comfortable with tail risk deals, and these deals may need to evolve to longer tenors or to minimize basis risk to allow capital relief to be granted. Further, like the pension market, syndication is becoming increasingly important for the largest transactions—as well as those covering specialized risks.

In the asset-only segment, insurers have several asset strategies from which to choose. But to optimize capital, many need help in creating efficient matching portfolios that more closely align asset and liability cash flows.

In the full-annuity segment, many block reinsurance and M&A transactions are occurring. But here too, syndication and sidecar solutions will be needed in the future to support continued growth. What’s more, the solutions currently being used in the United Kingdom, Canada, and the Netherlands must be adapted for use in other countries.

These developments are important to the availability of cost-effective annuities across Europe and around the globe. Helping people gain access to lifetime income and retirement security via these annuity solutions is an urgent worldwide concern.

16. CONCLUSION

Many problems have been solved—and many effective derisking techniques have been introduced—in the past decade of innovation. But much work remains to be done to develop the global longevity risk transfer market, including:

Enabling pension funds to derisk despite the low-interest-rate environment.

Adapting risk transfer solutions for CDC schemes.

Creating retirement savings programs for people without workplace coverage.

Bringing alternative capital and increased capacity to the market.

Introducing existing solutions to more countries.

Helping as many people as possible achieve retirement security and peace of mind.

Of course, every pension fund and every insurer is unique, and each will embrace the risk management strategy that is most suitable to its risk appetite, resources, governance, and expertise. But all share the universal goal of safeguarding members’ benefits while achieving a lower-risk future.

Discussions on this article can be submitted until September 1, 2020. The authors reserve the right to reply to any discussion. Please see the Instructions for Authors found online at http://www.tandfonline.com/uaaj for submission instructions.

Notes

1 Sandor (Citation1994, Citation2003, Citation2017).

2 Principally, the closure of defined benefit plans to new accruals, increased accounting transparency of pension liabilities on corporate balance sheets, the emergence of plan deficits and a strengthened funding standard, and the introduction of risk management solutions for dealing with both asset and liability risks.

3 Sources: LCP, Hymans Robertson, LIMRA and Prudential analysis, as of June 30, 2019.

4 For a history of the development of this market to date, see Blake et al. (Citation2006, Citation2018).

5 Unless matched by a corresponding increase in the retirement age.

6 Data in USD. Sources: LCP, Hymans Robertson, LIMRA and Prudential analysis, as of June 30, 2019.

7 Sources: CDC, OECD, Statistics Canada, Aon Hewitt Global Longevity Tracker.

8 Moon shots are huge new innovations that have not previously been attempted before.

9 Solvency II is a legislative program that introduced standardized insurance regulations across the European Union. It primarily concerns the amount of capital insurance firms must maintain as assurance against insolvency.

10 In 2015, the Dutch supervisory authority, De Nederlandsche Bank (DNB), questioned Delta Lloyd’s two index-based tail risk protection hedges. The DNB said it treats an index-based hedge as a financial instrument, whereas it treats a customized hedge as a reinsurance contract. It wanted the index-based hedges to be restructured to “ensure reinsurance treatment,” which had the effect of reducing Delta Lloyd’s capital relief (Solvency II Troubleshoot: Longevity Swaps and Risk Margin Relief, InsuranceERM, 17 May 2016; https://www.insuranceerm.com/analysis/solvency-ii-troubleshoot-longevity-swaps-and-risk-margin-relief.html).

REFERENCES

- Blake, D., A. J. G. Cairns, and K. Dowd. 2006. Living with mortality: Longevity bonds and other mortality-linked securities. British Actuarial Journal 12: 153–97.

- Blake, D., A. J. G. Cairns, K. Dowd, and A. R. Kessler. 2018. Still living with mortality: The longevity risk transfer market after one decade, Presentation to the Institute and Faculty of Actuaries, Edinburgh, United Kingdom, 29 January.

- Sandor, R. L. 1994. In search of market trees: Market architecture and tradable entitlements for CO2 abatement. In: Combating Global Warming: Possible Rules, Regulations, and Administrative Arrangements for a Global Market in CO2 Emission Entitlements. New York, NY: United Nations Conference on Trade and Development.

- Sandor, R. L. 2003. The first Chicago Climate Exchange Auction: The birth of the North American carbon market. In: Greenhouse Gas Market 2003: Emerging but Fragmented, pp. 77–81, Geneva, Switzerland: International Emissions Trading Association.

- Sandor, R. L. 2017. Financial innovation. Presentation at Longevity 12: The Twelfth International Longevity Risk and Capital Markets Solution Conference, Chicago, IL, 29 September.