ABSTRACT

Despite significant policy and regulation efforts by Canada’s federal government since its signature of the Paris Agreement, the specific question of whether Canada can retain its role as an energy production powerhouse while gaining some political capital as an international leader with regard to climate change has continued to plague its GHG reduction ambitions. In this article, I argue that despite an exceptional clean energy resource endowment, options to demonstrate the country’s serious intentions to meet its international climate commitments while keeping a sizeable oil and natural gas production sector come with complex implications well beyond the simplistic economic challenge linked to replacing the sector’s exports and employment levels. I explore three such options to keep oil and gas production high by using techno-economic modeling: compensating with more reductions elsewhere, using CCS in the oil and gas sector to avoid the sector’s emissions, and using negative emission technologies to compensate them. Compared with reducing emissions through large cuts in oil and gas production levels, each of these options comes with both significantly higher costs for society and a much higher risk of not delivering the expected emissions reductions.

RÉSUMÉ

Malgré les efforts considérables déployés par le gouvernement fédéral canadien en matière de politique et de réglementation depuis la signature de l'Accord de Paris, la question particulière de savoir si le Canada peut conserver son rôle de puissance de production énergétique tout en gagnant un certain capital politique en tant que leader international de la lutte aux changements climatiques continue de peser sur ses ambitions de réduction des GES. Dans cet article, je soutiens qu'en dépit d'une dotation exceptionnelle en ressources énergétiques propres, les options permettant de démontrer le sérieux des intentions du pays de respecter ses engagements internationaux en matière de climat tout en conservant un secteur de production de pétrole et de gaz naturel important ont des implications complexes qui vont bien au-delà d'une description simpliste du défi économique lié au remplacement des exportations et des niveaux d'emploi du secteur. J'explore trois de ces options visant à maintenir la production de pétrole et de gaz à un niveau élevé en utilisant une modélisation technico-économique : compenser les GES émis par cette production par davantage de réductions ailleurs, utiliser le CSC dans le secteur du pétrole et du gaz pour en éviter les émissions, et utiliser des technologies d'émissions négatives pour les compenser. En comparaison avec une réduction des émissions par une diminution importante des niveaux de production de pétrole et de gaz, chacune de ces options s'accompagne à la fois de coûts nettement plus élevés pour la société et d'un risque beaucoup plus grand de ne pas obtenir les réductions d'émissions escomptées.

Since Canada joined the Paris Agreement on climate change at the last minute in 2015, it has been struggling to steer the course of its past emission reduction performance and try to claim a leadership position in the international community’s fight against climate change. The Liberal government of Justin Trudeau, in power ever since this shift in 2015, put this objective front and center of its platform, and was quick to introduce a broad Pan-Canadian Framework on Clean Growth and Climate Change. This policy umbrella included various actions across sectors to help decarbonize them, including a country-wide carbon pricing mechanism, the jurisdiction of which was contested by some provinces but subsequently confirmed by the Supreme Court. Various other measures were also adopted, including a country-wide phase-out of coal in power generation and several programs to accelerate the shift to renewable energy in many sectors.

After its first reelection in 2019, the Trudeau government doubled down on signaling its commitment, announcing a revised and upgraded greenhouse gas (GHG) reduction target for 2030 (now 40-45% from 2005 levels) and a zero net emissions target for 2050, joining a growing chorus of nations setting the net-zero standard. The development of a flurry of high-level policies has continued to follow, including a Clean Fuel Standard, a Net-Zero Accelerator Initiative, and the Build Smart buildings strategy, to name a few. Whether or not these and upcoming policies will deliver the desired GHG reductions remains to be seen, of course, but it would be hard to qualify this series of steps as timid.

Every country faces significant challenges with regard to reducing GHG emissions, some typical (replacing oil as the dominant source for transport, for instance) and some unique (depending on the country’s industrial landscape, for instance), and Canada’s situation is peculiar in its own terms. On the one hand, its vast territory and relatively small population is very well endowed in low-carbon energy resources (including hydroelectricity, uranium, wind and solar energy, biomass, and geothermal), giving it a plethora of options to meet the net-zero challenge. On the other hand, it has an economy where energy efficiency has historically been very poor (ranking worst of the OECD outside of Iceland both for per capita energy consumption and for GDP energy intensity). Its economy also depends on oil and gas export revenues for over 10% of its GDP, a highly emitting sector. The oil and gas industry as a whole is reluctant to move away from this production, and its political influence is bolstered by the close to 800,000 jobs which depend on it (NRCAN, Citation2022).

The road to net-zero is complex and certainly touches all sectors of the economy and beyond – as personal consumption preferences and urban design play a role alongside technological transformations. However, the specific question of whether Canada can retain its role as an energy production powerhouse while gaining some political capital as an international leader with regard to climate change has continued to plague the government’s climate change platform. So while moving toward net-zero requires a multi-faceted strategy across all sectors, which goes well beyond balancing the role of the oil and gas sector in these efforts, the specific oil and gas production conundrum is a key one to deal with for the country.

In this article, I argue that even though the options that Canada has to achieve GHG targets make it well-endowed in terms of its potential to claim international leadership on the climate change front, the difficulties of “striking the right balance” between drastically cutting oil and gas production and focusing on reducing emissions in other parts of the economy are, more often than not, grossly understated. In large part, this is because the implications of each option at hand, in developing a strategy to put the country on a trajectory compatible with achieving net-zero emissions while dealing with any form of transition away from oil and gas production, are not always well understood and instead are simplified to the economic dimensions linked to the sector’s place in the Canadian economic and political landscape. As a result, Canada’s international leadership ambitions on climate change are bound by this hesitation to make a strong decision with regard to any of these options.

To unpack and demonstrate these implications, I use modeling results from the Canadian Energy Outlook 2021, which used techno-economic modeling to assess the transformations associated with technological trajectories to net-zero across the Canadian energy system. I focus on three options to resolve the GHG reduction vs. oil and gas production dilemma: choosing to avoid any significant cuts in production levels for oil and gas before 2030 and compensating through reductions in other sectors; using carbon capture and storage (CCS) to rapidly cut emissions from oil and gas production instead; or using negative-emission technologies to compensate for oil and gas emissions. After presenting the methodology underpinning the modeling, I discuss each of these three options in turn, before concluding.

Methods and data

The modeling used in this study was completed with the North American Times Energy Model (NATEM), a TIMES-MARKAL model developed by ESMIA Consultants and which contains fine details on technological options and cost and GHG estimates for all emitting sources. The model performs an energy system-wide cost optimization, finding the lowest possible cost for the entire system, using four sets of constraints: (1) detailed price evolution of technologies compiled by ESMIA, with a rich database of technology readiness levels; (2) demand and price projections made by the Canadian Energy Regulator, exogenous to the model; (3) various federal, provincial and territorial policies in place that have a direct or indirect impact on emissions; and (4) GHG reduction targets (short term) and net-zero targets (long term), which must be met country-wide by the model.Footnote1,Footnote2

The main scenario (NZ50) that is used as a starting point is based on Canada’s formal GHG reduction targets. It constrains the economy to reach a 40% reduction in emissions from 2005 levels by 2030, and net-zero emissions by 2050. Two alternative scenarios are also used which considered other timelines to reach net-zero (2045 and 2060, labeled NZ45 and NZ60), which allowed to examine variations from the main net-zero scenario when a different pace is achieved. Lastly, the authors also completed various sensitivity analyzes for key areas of uncertainty, including physical, technological, economic, and political factors. All of these are compared with a business-as-usual reference scenario (REF), to get a sense of the transformations implied.

The results allowed the authors to draw many overarching observations, which are presented in the Canadian Energy Outlook 2021 (Langlois-Bertrand et al., Citation2021). For reference in the discussion that follows, it is worth noting a few of the main observations here: (1) reaching net zero in Canada is possible, even by 2045, with technology and cost information known today; (2) it involves a significant electrification of all sectors, some where it comes to represent the overwhelming share of energy service delivery through only a few final conversion technologies (space heating, for instance), others where electricity's contribution is substantial but part of a more eclectic mix (merchandise transport, for instance); (3) carbon capture plays a crucial role in helping reach net-zero, but importantly, this is mostly because of the possibility to have “negative-emissions” activities where biomass is used in conjunction with CCS; and (4) not all sectors face the same challenges, for instance space heating in buildings is very likely to be electrified but scale is the main difficulty, while decarbonizing heavy road transport requires significant risk taking, as several infrastructure-heavy technology options exist but are very early in their development.

Modeling of this type is not akin to previsions: rather, results from these scenarios are understood as possible images of the future, where a large number of well-educated assumptions are factored in. Therefore, interpretation and translation into useful information must occur through careful comparative analysis of the main scenarios, as well as additional scenarios reflecting key uncertainties.

Oil and gas production and climate leadership: three options in moving toward net-zero

The results from the net-zero scenarios are unmistakable: the model favors targeting primarily the oil and gas sector in trying to reduce the country’s emissions, by capping production levels or forcing them down significantly and at a rapid pace. Indeed, in the results, all net-zero scenarios have the oil and gas sector achieve the quickest and most sizeable decrease in its emissions in relative terms, which is the result of production level reductions of 52% for oil and 59% for gas in the NZ50 scenario, by 2030, to meet the −40% economy-wide GHG reduction target. This means that this is the cheapest way of meeting the 2030 target, In terms of direct costs for the entire energy system. Production levels are cut further in the two decades that follow, resulting in 90% less oil and 94% less natural gas coming out of Canadian sources by 2050, to reach net-zero emissions as the federal legislated target imposes.

As stated above, the contribution of this sector to GDP because of export revenues ($122 billion in 2019) and in terms of employment (close to 800,000 jobs including indirect) is quite significant. Additionally, while it may be associated with a lower number of jobs per $ invested than either clean energy or energy efficiency, the geographic concentration of oil and gas production means that numerous communities depend directly on this industrial activity, suggesting several local and regional economic shocks if activity from the sector is terminated at broad scale. In other words, cutting oil and gas production by such levels before 2030 is economically and politically challenging, to put it (very) mildly.

In the following sections, I assess three options for Canada to choose not to drastically oil and gas production levels, in light of the Canadian Energy Outlook 2021 results. What happens if these production levels are kept higher, but Canada still wants to clearly show that it is doing what is needed to achieve its climate targets?

Option #1: forcing drastic and rapid reductions from oil and gas production

In and of itself, a large oil and gas export position makes Canada’s quest for international leadership in GHG reduction very arduous. First, its overall GHG profile is strongly impacted by oil and gas production’s emissions, which represent 25% of the country’s total and the most rapidly growing source, having grown by 32% since 2000 (ECCC, Citation2021). Second, downstream emissions from this production, through the burning of oil products like gasoline for transport or natural gas for heating, represent between 70% and 80% of the emissions associated with the life cycle of oil and gas (EDC, Citation2022). However, these (Scope 3Footnote3) emissions are not assigned to Canada’s GHG inventory for exported oil, as per the Paris Agreement accounting rules, which represents more than 80% of total Canadian oil production. Therefore, oil and gas exporters do not merely contribute emissions ascribed to their country of operation, but much more importantly to consumption elsewhere.

If we forget about Scope 3 emissions (following the Paris Agreement framework) and focus on Canada’s perspective on meeting its own GHG targets, we can assess the implications of the option to keep higher production levels from oil and gas and ask the model what it would do instead to meet the targets. To do so, a sensitivity analysis was conducted through two alternative scenarios to NZ50: one in which oil and natural gas production are maintained at a minimum of 25% of the reference scenario levels at all times (OilExpA); and a second alternative scenario where they are maintained at a minimum of 50% of the reference scenario at all times (OilExpB). In terms of other constraints, these alternative scenarios are identical to NZ50, in that they must reach the −40% economy-wide 2030 target and the net-zero target by 2050.

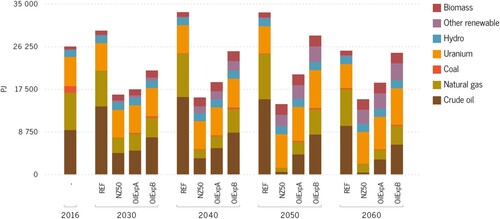

By design, both alternative scenarios require smaller cuts in production levels when compared with NZ50, but these levels are still reduced compared with the reference scenario. Results presented in and highlight two things: (1) short-term reductions in oil and gas production levels remain very important in both alternative scenarios (i.e. before 2030), suggesting that it remains the cost-optimal option to meet the 2030 target but transformations induced by the different floor levels for alternative scenarios lead to growth after 2030; and (2) consumption of oil products and natural gas in these alternative scenarios goes down when compared with NZ50.

Figure 1. Primary energy production in alternative scenarios. Source: Langlois-Bertrand et al. (Citation2021).

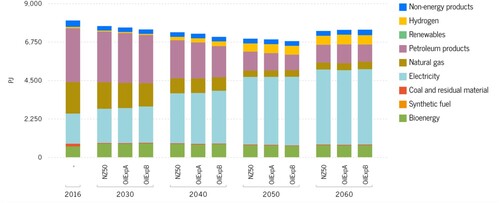

Figure 2. Final energy consumption in alternative oil production scenarios. Source: Langlois-Bertrand et al. (Citation2021).

Put differently, comparing the results from these scenarios to the original NZ50 allows to contemplate the shifts required in net-zero sectoral trajectories, especially before 2030, in order to protect the sector and maintain these levels of production (which, it must be stressed, would still be decreased). As can be seen on , OilExpA sees important reductions in production levels for both oil and gas, but smaller in size compared with NZ50 (46% vs. 52% for oil, and 55% vs. 59% for natural gas). As expected, OilExpB maintains even higher production levels, so reductions are to the tune of 16% for oil and 48% for gas.

The more important question, of course, is how these smaller reductions from the oil and gas sector impact the rest of the sectors on the road to the 2030 GHG target. From a policy perspective, this can be understood as contrasting two options: one would be to strictly constrain emissions from the oil and gas sector to achieve reductions as in NZ50, and to act on the economic disruption to compensate parts of the workforce going through it (through re-training programs, relocations, development of new industries to create jobs in stricken communities, etc.); the other would be constrain emissions less and allow more production from the sector, which would also have the benefit of reducing the spending needed to compensate the disruption (option #1, in this discussion), allowing to redirect these funds to additional reduction efforts in other sectors.

In any scenario where country-wide reductions are fixed, a smaller reduction in one sector has to be compensated by larger ones elsewhere. In the OilExpA and OilExpB scenarios, the missing reductions from oil and gas reductions come from several sources. First, overall final energy consumption () moves away from fossil fuels more rapidly than in NZ50, mainly through an accelerated electrification at the expense of natural gas. Oil products are more costly to replace than natural gas in the short term, so favoring electric technologies over ones using natural gas becomes more economical. This effect is present by 2030, then declines by 2040, and all three scenarios converge by 2050, showing how the net-zero target is too constraining to allow more consumption of fossil fuels in any case.

At the very least, therefore, if Canada chooses not to drastically reduce production in the oil and gas sector, the next cheapest way of meeting GHG reduction targets is by reducing oil products and gas consumption in other sectors (by electrifying transport or industry low-heat applications more rapidly, for instance). In the absence of other measures taken to deal with oil and gas production emissions, Canada has to choose, to a large extent, between either producing oil and gas or consuming it, if it wants to meet its 2030 and 2050 targets. The general impact of targeting oil and gas consumption more aggressively, however, would be a much higher cost of transforming other sectors more rapidly, where reductions are much more difficult on such a timescale.

Nevertheless, indeed other options exist to either reduce emissions from oil and gas production or avoid their impact on the bottom line by subtracting emissions from the atmosphere elsewhere.

Option #2: fund CCS to decarbonize oil and gas

Drastically reducing production levels from the oil and gas sector is not the only way to avoid or compensate its emissions, of course. One hotly debated option is the possibility to massively apply carbon capture and storage (CCS) technologies to oil and gas production sites. In theory, this would make it possible to capture over 90% of the emissions, and therefore, at large scale, it would enable the sector to maintain very high levels of production all the while drastically reducing emissions.

To be sure, CCS is now more likely to be an unavoidable option on the road to net-zero, as has been pointed out by several recent reports (see for instance D’Aprile et al., Citation2020; IEA, Citation2020; Larson et al., Citation2020; Ministère de la transition écologique, Citation2020; UKCCC, Citation2019). For most countries, CCS offers, in theory, one of the only ways to (mostly) avoid emissions from heavy industry, in particular, and can be applied to thermal power plants as well.

CCS remains very expensive however, and has so far largely failed to deliver on its promises – and at scale – despite two decades of significant investment. After a lull in 2017, the number of projects in development has been increasing, but remains a far shot from what it was 10 years ago (Global CCS Institute, Citation2020). Second, CCS remains uneconomical for all but a few applications (Langlois-Bertrand et al., Citation2021). And third, the rate of capture does not come anywhere close to the theoretical potential of capturing over 90% of emissions at point source: most projects in operation remain unable to reach a share of captured emissions over 75%, and taking into account lifecycle emissions related to the energy required to operate the CCS technology, this share goes below 70% of emissions (Langlois-Bertrand et al., Citation2021, pp. 166–167).

In addition to these limitations, over 80% of the CO2 captured around the world today is not stored, but rather goes to enhanced oil recovery (EOR) operations, through which the CO2 is injected in partially depleted oil wells to allow the extraction of more oil (Freites & Jones, Citation2020). This participates in the global economics of carbon capture, where EOR presents at the moment the principal option to reduce the overall cost of CCS by valuing the CO2. However, the implication is that more oil ends up being extracted because of the use of CO2 captured elsewhere. In terms of emissions, more emissions result from the additional production including mainly through combustion of the fuels downstream, in addition to a good portion of the captured and injected CO2 being released because of leaks in the process.

With all these limitations and this experience in mind, the prospects of massively applying CCS to help the low-carbon transition without more difficult GHG reductions appear to come with some important caveats. More importantly perhaps, its essential role in net-zero technological trajectories can be illustrated and nuanced by the modeling results for different net-zero scenarios.

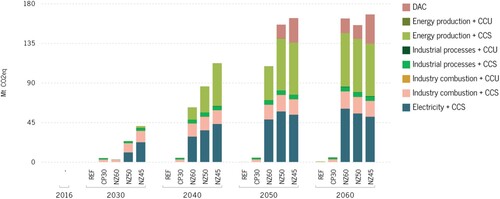

The results for all net-zero scenarios (Footnote4) show that to achieve society-wide neutral emissions, at least 155 megatonnes of carbon dioxide equivalent (MtCO2e) must be captured and stored every year from the net-zero point, an order of magnitude drastically different from the amounts dealt with today in the very few projects in operation around the world. To be clear, three categories of applications for capture can be distinguished: the capture of emissions in industrial combustion and processes, including energy production; capture in negative-emissions operations, which in the model used here means BECCSFootnote5 energy production or BECCS electricity generation (); and direct-air capture (DAC), which is meant to refer to the capture of emissions from the atmosphere with technologies other than natural processes like biomass photosynthesis. Each of these is addressed below. A further distinction is made on the chart between carbon captured and stored (CCS) as opposed to (re)utilized (CCU).

Figure 3. Captured emissions. Source: Langlois-Bertrand et al. (Citation2021).

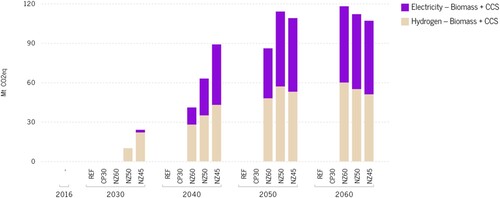

Figure 4. Captured emissions from bioenergy with carbon capture and storage (BECCS). Source: Langlois-Bertrand et al. (Citation2021).

adds precisions to the distribution of capture operations shown in . One is that the “electricity with CCS” in , which can include powerplants equipped with CCS, is in fact overwhelmingly BECCS electricity production, and not CCS-equipped coal-fired or natural gas-fired power plants. Second, the “energy production with CCS” in is in fact BECCS hydrogen production. Therefore, carbon capture in net-zero scenarios, which here are modeled in a techno-economic optimization, requires the very extensive application of CCS outside of the oil and gas industry. All emissions not avoided, such as those resulting from keeping more oil and gas production, will require both more storage of CO2 (if CCS is applied to this production in addition to everywhere else) and more BECCS or DAC (to compensate for whatever portion of CO2 from oil and gas production not captured by the technology because of technical limitations).

also shows that between storage and utilization in the industrial and energy production sectors, the main route for captured emissions (over 99%) is storage, not utilization. DAC and BECCS electricity, shown on the chart, also result in a similar share of storage. On the one hand, this shows the limited reutilization potential of CO2 in terms of cost, with storage being the cheaper option to participate in meeting the net-zero constraint. On the other, it also illustrates the main constraint on reutilization, which more often than not results in the release of the captured emissions at some point downstream after the utilization of the CO2 initially captured. This adds to the economic uncertainty facing the future of CCS in oil and gas production, as using EOR to recoup the high cost of capture becomes more problematic on the road to net-zero.

Importantly, one could make the point that CCS in oil and gas production could at least help in the short term, reducing emissions rapidly while the industry reduces its production more gradually and avoids the shock of rapid reductions in employment and export revenue. But CCS requires significant infrastructure (for capture, transporting CO2, and storage facilities), which would largely and rapidly become stranded assets later on, and in any case would fail to deliver GHG reductions rapidly. For the 2050 horizon, massively investing in CCS for any given industry today means a long-term choice, which must retain compatibility with the net-zero end state.

A more general concern about the role of capture technologies in the results from the optimization modeling is also that these results should not obscure the significant uncertainties that remain about the true potential for capture to be efficient from a technical, economic and energy requirement perspective. As noted earlier, experience so far with carbon capture in industrial applications shows a much lower share of emissions captured than theoretically feasible, as well as significant emissions resulting from energy use to operate the capture technologies. Experience with BECCS is even more limited, while no DAC technology is currently operated on a large scale, making it impossible to confirm costs for these processes. As a result, the quantity of emissions captured in the net-zero scenario results discussed above is likely to be an underestimation of what would be required to fully compensate remaining emissions.

Even disregarding these uncertainties about CCS, the amount of captured emissions raises the issue of the implications of storing such large quantities every year, even after net-zero has been reached. While there is theoretically substantial storage capacity across Canada and elsewhere, experience in storing quantities of this magnitude is lacking and some risk assessments suggest that large-scale storage should be considered with care.Footnote6 Opportunities for CO2 reutilization that do not result in the eventual release of CO2 are also very limited, and specific applications like CCS-equipped steam methane reforming for hydrogen production do not solve any of the difficulties mentioned above.

So when considering the option of using CCS as a way for Canada to respect its international commitments on GHG reductions while keeping a sizeable oil and gas production sector, this set of caveats makes the future dire for CCS in oil and gas production, and would certainly raises the risks and costs of the net-zero transition for the rest of society.

Option #3: compensate oil and gas emissions by using negative emission technologies

Another option to meet the GHG reduction and net-zero targets while keeping high levels of oil and gas production is to compensate a larger amount of emissions from the sector through greater use of negative emission technologies, i.e., DAC or BECCS. As presented in the previous section, resorting to these technologies is required in order to achieve net-zero in NZ scenarios, so if production levels are kept high, using more DAC and BECCS could be considered as a way for the country to meet its international obligations nonetheless.

DAC technology may be promising, but cost projections currently available see it at a very expensive backstop option for reducing emissions. By extracting CO2 directly from the atmosphere, it offers one of the only options to compensate for unavoidable emissions from agriculture, transport or some industrial processes, resulting in negative emissions. While shows DAC contributes only a small part of all emissions captured, the very limited experience with concrete DAC applications means that even this result should be treated with care since considerable uncertainties remain given the cost of operating this technology. In fact, capture with DAC appears only in the late 2040s in the model, as a last resort option, reflecting the high cost.

The other main negative emission option is BECCS. Bioenergy plays a key role in the net-zero scenarios results, especially given that Canada has significant quantities of biomass available. However, even with these quantities, it must be noted that in NZ50, all of the estimated available biomass is used. In the short term, biomass is useful to reduce emissions in sectors difficult or too costly to electrify rapidly, for instance through biofuels for some transport applications. The advantages over other options are both technological and economic, as liquid biofuels require relatively little additional distribution infrastructure, and can be used in relatively large proportions in standard internal combustion engines or heat applications.

Shortly after 2030 (and even earlier in some provinces), however, the remaining emissions associated with this type of bioenergy, coupled with its relative inefficiency as an energy source, combine to shift its use. On the longer term, biomass becomes an unavoidable part of net-zero trajectories, as it allows for negative emissions energy production (mainly electricity and hydrogen, as shown in , but also industrial heat). Indeed, when approaching net-zero, all NZ scenarios show a significant amount of emissions that remain and would be difficult to avoid, for instance in agriculture or industrial processes.

In the NZ50 scenario, for instance, 127 MtCO2e are still emitted in 2050 in net terms, coming mainly from transport (50.7 MtCO2e), agriculture (41.0 MtCO2e), industrial processes (18.1 MtCO2e), energy production (9.5 MtCO2e), and waste (5.4 MtCO2e). To put things in perspective, this quantity represents 17.3% of the country’s 2019 emissions (730 MtCO2e). Moreover, this quantity remains despite the model optimizing overall cost and efforts, including the use of carbon capture in some applications. In other words, obtaining “only” 127 MtCO2e of remaining emissions in 2050 is contingent on realizing extremely significant reductions in all sectors until then. Therefore, these 127 MtCO2e of remaining emissions are likely to be an underestimation.

Therefore, the main reason why the model does 155 MtCO2e of capture annually, as described in the previous section, is not merely because this helps avoid some emissions through capture. Specifically, most of this capture must be done in negative-emission activities (127 MtCO2e of these 155 MtCO2e), overwhelmingly from BECCS.

Factoring in the very high cost and uncertainty surrounding DAC, the bottom line is that over 100 MtCO2e of negative emissions must be realized, in optimal trajectories, with BECCS, and this is very likely an underestimation as explained above. If more BECCS is needed to compensate higher emissions from oil and gas production, therefore, it is crucial to ensure that there are enough biomass resources to achieve these levels.

Although biomass of various sources is available in significant quantities in Canada, it is worth noting that estimates of the quantity available for energy purposes vary wildly based on several uncertainties with regard to the evolution of these resources over the next decade (Langlois-Bertrand et al., Citation2021). These uncertainties include: (1) how much can be harvested and at what rate, without jeopardizing its renewal capacity or the land’s contribution to tempering emissions, i.e., acting as a carbon sink,; (2) how much additional land can be converted to usable biomass given land demand for other purposes like agriculture and cattle raising; (3) how much of the harvested portion of the resource can be used for energy purposes, as opposed to lumber and construction (including as a replacement for other building materials where the production process is highly carbon intensive, like steel) or others; and (4) how and to what extent will each of these variables be affected both by global warming itself (through increased frequency and magnitude of forest fires, among other things) and by global warming feedback loops introduced or amplified by decisions over how to manage the variables listed above.

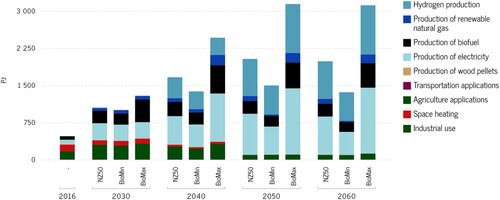

To be perfectly clear: this is quite a list of challenges. It should also be noted that at the moment, in Canada, there is no comprehensive national policy or plan on how to manage biomass, let alone direction in balancing these demand drivers, with the partial exception of some provinces having de facto policies for the resource as a by-product of agriculture or forestry regulations. Therefore, it seems reasonable to be prudent with assumptions and hypotheses about the quantity of biomass that can be used, and indeed alternative scenarios were run to consider different ways that this uncertainty may play out. Two such scenarios are presented here: one in which the quantity of biomass available for energy purposes is half what it is in NZ50, representing lower-end estimations for the overall availability, for one or several of the reasons outlined above (BioMin); and a second scenario where instead the quantity of available biomass is double what it is NZ50, representing an increase in availability which could result if significantly improved management of the resource was achieved (BioMax).

contrasts the use of bioenergy across NZ50 and the alternative scenarios. In BioMin, consumption of biomass for energy purposes is similar to NZ50 in the short term, but departs after that as the constraint on availability kicks in. Lower quantities of available biomass thus do not constrain short-term consumption (mainly through biofuels used for sectors difficult to transform rapidly). But after these initial benefits, the possibility to use biomass for BECCS production and negative emissions goes down.

Figure 5. Biomass consumption in alternative scenarios. Source: Langlois-Bertrand et al. (Citation2021).

In BioMax, in the short term, the much more substantial biomass availability allows more biofuels production and use. However, after the first decade, the picture changes completely. Biofuels growth stalls (especially from 2040), as all additional available biomass goes to BECCS production to generate negative emissions (through electricity and hydrogen production) – which becomes a cheaper way to contribute to emissions reductions compared with biofuels. Renewable natural gas production is also more sizeable in this scenario than in either NZ50 or BioMin.

As a result of these differences, the structure of overall emissions changes little before 2030, as biomass use grows rapidly but mostly toward more biofuels for transport. In the longer term, however, variation in biomass availability has two main impacts: one is the greater need for DAC in lower-availability scenarios (BioMin and, to a lesser extent, NZ50). In BioMax, the greater availability enables the possibility of doing more negative emissions BECCS, with 2050 and 2060 results even showing no DAC at all. Importantly, the prohibitive cost of DAC in the model leads this variation to have a further effect: less remaining emissions are found in BioMin compared with NZ50, which means that more costly reductions are necessary across sectors, especially transport. In turn, the increased possibility of negative emissions in BioMax allows more remaining emissions, with transport taking on the bulk of this difference when compared with the other scenarios. In other words, in the longer term, more biomass leads to more BECCS being the cheaper option to reduce overall emissions from an energy system perspective.

Therefore, adding a requirement to do more BECCS to keep oil and gas production levels higher, without putting more pressure on other sectors to reduce their GHG emissions further, may require a quantity of biomass that is simply not available. In practice, the decision to prioritize energy-related biomass use or (more specifically) BECCS may come at the expense of deleterious impacts in other spheres of the economy and society. Notably, the possible conversion of land to produce additional biomass for this purpose may certainly impact food or cattle prices. In many ways, this is a repeat of the long-running “food vs. fuel” debate, which emerged especially from the early twenty-first century from fears that the drive for (first-generation) biofuels would be a key driver of food prices around the world. The potential importance of BECCS energy and heat production – including to compensate for emissions remaining from oil and gas production – in net-zero futures does bring forward similar concerns, given the quantities in play. This comes on top of the very significant technological uncertainties surrounding the true technical potential for CCS technologies outlined in the previous section, including in BECCS applications.

Limitations

By design, modeling exercises such as those used to support this analysis come with a number of limitations that derive from the simplifications required and the uncertainty inherent in forward-looking initiatives. First, the territorial basis used for emission accounting sometimes results in smaller oil and gas production levels in parallel to an increase in the import of refined products, especially in the shorter term. This is a limitation stemming from the Paris Agreement framework, and this aspect is treated with special care but is inevitable within this framework.

Second, there are still considerable unknowns related to LULUCF emissions, or to the displaced emissions from transitioning to other technologies providing energy services when these are produced outside of Canada. While these uncertainties are unavoidable in such modeling exercises, they must be kept in mind while reading the analysis presented above, where they are explicitly discussed through the sensitivity analyzes and their interpretation.

Third, the advent of disruptive technological innovation in relation to oil and gas may significantly change the expectations for the emissions associated with these fuels in the future. Nevertheless, it should be noted that for these expectations to drastically change, several such disruptive innovations would need to almost simultaneously penetrate both production and consumption across most sectors, which is very unlikely. Furthermore, disruptive innovations may also happen in relation to other energy sources, raising the potential cost of not moving away toward alternative sources.

Despite these caveats, therefore, the modeling used to support the analysis above allows for the identification of general trends, which is fundamental in setting the bases for a discussion of net-zero pathways for the Canadian energy system.

Conclusion

Ambition to join international leaders in the fight against climate change is a laudable objective, given the severity of the climate crisis and its prospects for future generations. Given the importance of oil and natural gas production in Canada’s economy, it is tempting to focus on strategies that keep this production strong while acting on reducing emissions through other means. However, all other options come with both significantly higher costs for society and with much higher risk of not delivering. Even the emission capture results shown above must be considered with care, since they almost surely represent an underevaluation of what would be needed to reach net-zero, as the cost optimization model imposes rational choices among all actors in a given scenario’s trajectory in addition to the theoretical potential of capture technologies being fulfilled. In other words, both costs and technological uncertainties serve as an important warning that projections shown for capture and storage may be overly optimistic, and that an even greater quantity of DAC and negative emissions energy production (which significantly is constrained by biomass availability, as discussed above) may be required to compensate for optimism on the quantity of emissions that can realistically be captured in the various processes. This comes in addition to the risks and current unknowns of continued large-scale storage.

The term “transformation” in net-zero ambitions is a euphemism in Canada’s case, like it is in other parts of the world. Transitioning to a net-zero society will require not just a transformation of energy systems, but of the entire political-economic-social nexus in relation to the delivery of energy services to the population. If Canada is indeed serious about its climate ambitions, it may have no choice other than to show the world that the solution lies in delivering a massive program to manage the shock on the workers and communities losing from such a transition and provide truly “clean” growth, instead of betting on technological solutions that simply have no realistic potential of reducing emissions while keeping oil and gas production at their current levels.

Acknowledgements

The author is grateful for the entire research team that worked on the Canadian Energy Outlook 2021 publication, including the modeling team at ESMIA, which helped produced the results on which this study builds.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Simon Langlois-Bertrand

Simon Langlois-Bertrand is a research associate at the Institut de l'énergie Trottier, based at Polytechnique Montréal. He holds a Ph.D. in international affairs and specializes in global energy politics and policy, as well as in sustainability transitions.

Notes

1 See Langlois-Bertrand et al. (Citation2021) and its appendices for more detail on these sets of constraints.

2 The reader should note that there is no specific legal definition for “net-zero” in Canada, other than for it to cover “all emissions” in general terms. For the purposes of this paper, therefore, “net-zero” means factoring in energy-related emissions from all sectors including fugitive emissions, as well as “non-energy” emissions from industrial processes, agriculture and waste. Emissions from land use, land use change and forestry (LULUCF) are however excluded. In terms of GHGs, CO2, methane, and hydrofluorocarbons (HFCs) are included and must be net zero overall (i.e., the sum must be neutral in CO2e terms).

3 The Greenhouse Gas Protocol classification is typically used by private and public actors around the world as a global standardized framework to measure and manage GHG emissions. Three scopes of emissions are defined as: emissions from fuel combustion and fugitive emissions resulting from the direct actions of the actor (Scope 1); emissions from the generation of electricity, heat and steam purchased by the actor (Scope 2); and all other indirect emissions that occur in the actor’s value chain, for instance from purchased goods and services, transportation and distribution, or waste disposal (Scope 3).

4 In both and , the full set of the main scenarios of the Canadian Energy Outlook 2021 is displayed. This includes the REF scenario as well as the NZ45, NZ50 and NZ60 scenarios, as well as an alternative reference scenario (CP30) which added the carbon pricing schedule announced by the federal government up to 2030. Even though this carbon pricing increase was not legislated at the time of the modelling, it was included for reference since it represented a key commitment from the government and was considered by many as an important tool in inducing the transformations required by the GHG reduction targets.

5 Bioenergy with carbon capture and sequestration (BECCS) refers to energy or heat production where biomass is the feedstock, and where emissions from the process are captured with CCS technology. Given that the biomass has already subtracted the CO2 it contains from the atmosphere, “re”-capturing this embedded CO2 when it comes out of combustion processes results in net negative emissions overall (provided, importantly, that the harvested biomass is renewed fully and rapidly).

6 See, for instance, IPCC (Citation2005) and Vernon & Stork (Citation2016).

References

- D’Aprile, P., Engel, H., van Gendt, G., Helmcke, S., Hieronimus, S., Nauclér, T., Pinner, D., Walter, D., & Witteveen, M. (2020). Net-Zero Europe: Decarbonization pathways and socioeconomic implications. McKinsey & Company. Retrieved November 2020, from https://www.mckinsey.com/business-functions/sustainability/our-insights/how-the-european-union-could-achieve-net-zero-emissions-at-netzero-cost#.

- ECCC. (2021). Canada’s official greenhouse gas inventory. Government of Canada: Environment and Climate Change Canada. Retrieved May 15, 2022, from http://data.ec.gc.ca/data/substances/monitor/canada-sofficial-greenhouse-gas-inventory/.

- EDC. (2022). Canada’s Big Oil Reality Check: Assessing the climate plans of Canadian oil and gas producers. Environmental Defence Canada and Oil Change International.

- Freites, S. G., & Jones, C. (2020). A review of the role of fossil fuel-based carbon capture and storage in the energy system. Prepared for Friend of the Earth Scotland.

- Global CCS Institute. (2020). Global status of CCS 2020. The Global CCS Institute. Melbourne, Australia. https://www.globalccsinstitute.com/resources/global-status-report/.

- IEA. (2020). Energy technology perspectives 2020: Special report on caron capture utilization and storage (CCUS in clean energy transitions). International Energy Agency.

- IPCC. (2005). Special report of carbon dioxide capture and storage. UNEP: Intergovernmental Panel on Climate Change.

- Langlois-Bertrand, S., Vaillancourt, K., Beaumier, L., Pied, M., Bahn, O., & Mousseau, N. (2021). Canadian Energy Outlook 2021 — Horizon 2060, with the contribution of Baggio, G., J oanis, M., Stringer, T. Institut de l’énergie Trottier.

- Larson, E., Greig, C., Jenkins, J., Mayfield, E., Pascale, A., Zhang, C., … Swan, A. (2020). Net-Zero America: Potential pathways, infrastructure, and impacts, interim report. Princeton University. Retrieved December 15, 2020, from https://netzeroamerica.princeton.edu/.

- Ministère de la transition écologique. (2020). Stratégie nationale bas-carbone: La transition écologique et solidaire vers la neutralité carbone, Ministère de la transition écologique. Retrieved March 2020, from https://www.ecologie.gouv.fr/strategie-nationale-bas-carbone-snbc.

- NRCAN. (2022). Energy facts. Natural Resources Canada.

- UKCCC. (2019). Net Zero – The UK’s contribution to stopping global warming, United Kingdom’s Committee on Climate Change. Retrieved May 2019, from https://www.theccc.org.uk/publication/net-zero-the-ukscontribution-to-stopping-global-warming/.

- Vernon, J. P., & Stork, A. L. (2016). Carbon capture and storage, geomechanics and induced seismic activity. Journal of Rock Mechanics and Geotechnical Engineering, 8(6), 928–935.