ABSTRACT

The oil sands have dominated Canada’s domestic energy conversations for most of the last 50 years. More recently, the resource has become an important factor in Canada’s foreign relations, in particular with respect to Canada’s commitments on climate change. Environmental concerns are not new to the oil sands, with endangered species impacts and tailings pond mitigation presenting pressing domestic concerns. This paper argues that climate change presents a unique challenge, even as prices for oil rise dramatically. Domestic action threatens to increase the cost of production and to erode cost-effective access to markets, and policy uncertainty has made investments more challenging. More importantly, global action will change the market for oil itself and shape the willingness of investors to commit to the oil sands. This paper examines the state of the oil sands industry in the context of Canadian and global commitments to action on climate change and the potential for a global energy transition. The paper concludes with a discussion of potential solutions and pitfalls for Canada’s oil sands in a carbon-constrained world.

RÉSUMÉ

Les sables bitumineux ont dominé les conversations sur l'énergie domestique du Canada pendant la majeure partie des cinquante dernières années. Plus récemment, la ressource est devenue un facteur important dans les relations étrangères du Canada, en particulier en ce qui concerne nos engagements internationaux en matière de changement climatique. Les préoccupations environnementales ne sont pas nouvelles dans le domaine des sables bitumineux, les impacts sur les espèces en voie de disparition et l'atténuation des bassins de résidus constituant des préoccupations nationales pressantes. Cet article soutient que le changement climatique représente un défi unique pour les sables bitumineux, même lorsque les prix du pétrole augmentent de façon spectaculaire. L'action nationale en matière de changement climatique menace d'augmenter le coût de production et d'éroder l'accès rentable au marché, et l'incertitude politique a rendu les investissements plus difficiles. Fait plus important encore, l'action sur le changement climatique modifiera le marché du pétrole lui-même et déterminera la volonté des investisseurs de s'engager à nouveau dans les sables bitumineux. Cet article examine l'état actuel de l'industrie des sables bitumineux dans le contexte des engagements canadiens et mondiaux en matière de lutte contre le changement climatique et du potentiel d'une transition énergétique mondiale. La conclusion de l'article consiste en une discussion sur les solutions et les pièges potentiels pour les sables bitumineux du Canada, dans un monde sous contrainte carbone.

Introduction

In one way or another, the oil sands have dominated Canada’s domestic energy conversations for most of the last 50 years.Footnote1 More recently, as energy security and climate change have increased in importance, the oil sands have played a critical role in our foreign relations as well. The first commercial operations in the oil sands began at what was then the Great Canadian Oil Sands mine in the late 1960s, with a second major mining operation at Syncrude following in the late 1970s. The viability of the oil sands resource play was central to the much-maligned National Energy Program of the 1980s, which offered a guaranteed price for oil sands production in an attempt to spur investment in domestic production, the same motivation that drove earlier policies that restricted energy trade in Canada.Footnote2 The industry stagnated for much of the late 1980s and early 1990s, as oil prices languished. The 2000s saw an oil sands boom take hold in the Province of Alberta, as hundreds of billions of dollars of foreign and domestic investment flowed into the province, and global supermajors staked out positions in the Northern Alberta muskeg. Improved near- and long-term oil price expectations along with a new, more predictable royalty regime and more generous tax treatment (Plourde, Citation2009, pp. 116–118) set the financial foundations for the boom, while innovations in extraction technology including the use of horizontal drilling opened vast new oil sands resources to profitable extraction (National Energy Board, Citation2000, p. ix). For a time, talk of labor shortages, temporary foreign worker policies and project cost inflation dominated the oil sands. The national knock-on effects of the 2000s boom, including pressure on the inflation rate and a raging debate over Canada’s affliction with the so-called Dutch Disease dominated the political discourse (Carney, Citation2012). Since late 2014, downward pressure on oil prices along with concerns about environmental impacts has led to a crash of equal proportions to the boom. No major new oil sands production projects have been sanctioned since 2015, and production now tracks far below earlier forecasts (Bishop & Sprague, Citation2019). This paper asks what the future holds for the Canadian oil sands in a world acting on climate change.

Pressing environmental concerns are not new to the oil sands, but climate change presents an altogether different challenge. Alberta’s oil sands industry has faced domestic concerns over its impact on endangered species, notably the woodland caribou (Muhly et al., Citation2015; Schneider et al., Citation2010). And, oil sands mining operations have proven unable to effectively manage fluid tailings and other local pollution challenges (Schindler, Citation2014). A growing inventory of lake-sized settling ponds now dominates the landscape in the areas in which oil sands are mined, with almost two trillion cubic meters of fluid fine tailings and process-affected water (enough to fill Toronto’s domed baseball stadium, Rogers Centre, 1150 times over) now stored on mining leases (Alberta Energy Regulator, Citation2021b, with author’s calculations re: Rogers Centre). Tailings ponds became a major source of public concern in the wake of a 2008 incident in which hundreds of ducks landed on a settling pond at Syncrude’s Aurora mine site, with most perishing as a result (Jones, Citation2010). Both of these issues have attracted substantial domestic policy responses, but neither presents the same challenge as climate change for the oil sands. Action on climate change threatens to increase the cost of production, limit access to capital and insurance, and erode cost-effective access to markets. Domestic policy uncertainty has made major project investments more challenging (see, for example, Lindsay, Citation2020). Global action on climate change is already changing the market for oil itself and will continue to shape the willingness of investors to make long-term capital allocation decisions. Global and domestic action on climate change creates an existential threat to the oil sands.

In what follows, I examine the current state of the oil sands industry in the context of Canada’s commitments to action on climate change. I build from that to examine the implications of global action on climate change for the oil industry as a whole. I turn next to an examination of the regional market for oil sands and the role of infrastructure constraints. I end with a discussion of potential solutions and pitfalls for Canada’s oil sands in a carbon-constrained world.

Alberta’s oil sands today

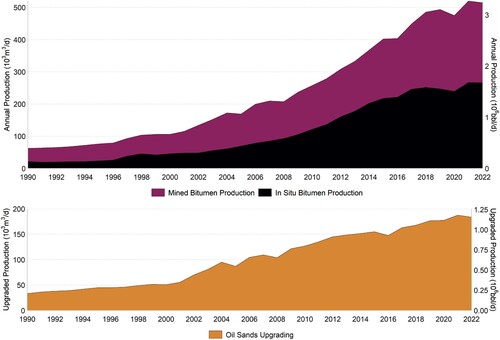

Current oil sands bitumen production (see ) is approximately 510 thousand cubic meters (3.2 million barrels) per day (Alberta Energy Regulator, Citation2022c). Production has increased rapidly over time, although growth has slowed recently. Production increased 2.5% per year on average between 2018 and 2022, compared to 9% cumulative average growth rate from 2000 through 2018 (Alberta Energy Regulator, Citation2022a). Bitumen production is split between two primary techniques: surface mining (49%) and well-based (in situ) thermal production (51%) (Alberta Energy Regulator, Citation2022a). Approximately one-third of bitumen production is upgraded to synthetic crude at purpose-built facilities in Alberta (). Oil sands bitumen production accounts for approximately 75% of total Canadian oil production (Statistics Canada, Citation2022), and approximately 85% of production is shipped out of Alberta (Alberta Energy Regulator, Citation2022a). Oil sands production is not expected to grow substantially from current levels: IHS Markit (Citation2022b), the Canadian Energy Regulator (CER) (Citation2021a) and the Alberta Energy Regulator (AER) (Citation2022a) forecast production levels of 3.5, 3.8–4, and 4.1 million barrels per day (mmbbl/d) by 2030, respectively.

Figure 1. Oil sands bitumen production (top) and upgrading (bottom). Data: AER (Citation2022c).

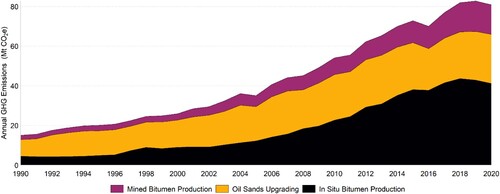

Oil sands greenhouse gas emissions (GHGs) have risen with production, as shown in , although with declining emissions-intensity over time. In 2020, the most recent inventory data available, GHGs from the oil sands accounted for 81 million tonnes of carbon dioxide equivalent emissions (Mt CO2e) of the 672 Mt CO2e national total. Oil sands GHGs have increased to almost two-and-a-half times their 2005 levels, and five-and-a-half times their 1990 levels (Government of Canada, Citation2021b). Emissions are split between in situ production (41 Mt CO2e), mining (15 Mt CO2e), and on-site upgrading to lighter, synthetic crude (25 Mt CO2e).

Figure 2. GHG emissions from oil sands production and upgrading. Data: Government of Canada (Citation2022a).

Despite improvements, oil sands production remains relatively emissions-intensive compared to the global average barrel (Bergerson et al., Citation2012; Gordon et al., Citation2015; IHS Markit, Citation2022a; Masnadi et al., Citation2018, Citation2021; Sleep et al., Citation2020, Citation2021) and compared to other Canadian oil production (Government of Canada, Citation2022a, in particular Figures 2–27.). There is substantial variation in estimated emissions-intensity between oil sands facilities, even among facilities of similar types (Guo et al., Citation2020; Orellana et al., Citation2018; Sleep et al., Citation2020, Citation2021). California Air Resources Board (Citation2021) regulatory data mirror the academic literature and show that the average oil sands barrel imported into California had an estimated emissions-intensity about 45% higher than the average barrel refined in the state, with substantial variation between oil sands crude streams. IHS Markit (Citation2022a) finds that the life-cycle GHG emissions of an oil sands barrel, including emissions from eventual combustion, are 8–22% higher than those of the average barrel refined in the United States.

Oil sands are also relatively expensive and have extremely long project life-cycles, which each increase the industry’s exposure to climate change policies and future energy transition risks. A new oil sands project is likely to require at least $1 billion in up-front investment, and it often takes 3–5 years for even a small project to reach full production capacity (for a more extensive discussion of the economics of the oil sands, see Bošković & Leach, Citation2020; or Heyes et al., Citation2018). To earn a competitive rate of return on invested capital, new in situ oil sands projects need West Texas Intermediate (WTI) prices to average approximately US$50 per barrel plus inflation over their project lifespans of twenty years or more, with higher WTI prices of US$75–85 per barrel required over longer time horizons for mining projects (AER, Citation2022a; Bošković & Leach, Citation2020; CER, Citation2021a). Once built, however, oil sands projects offer stable production with relatively low operating and sustaining capital costs and limited exposure to domestic GHG emissions policy (Bošković & Leach, Citation2020; Leach & Boskovic, Citation2014).

The oil sands and Canada’s GHG policy challenge

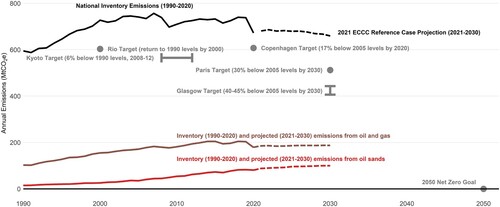

Oil and gas emissions are on a collision course with Canada’s climate change targets. Canada’s targets pledge emissions 40–45% below 2005 levels by 2030 (Government of Canada, Citation2021a), and projected emissions from the oil and gas sector as a whole and from the oil sands sector in particular would account for significant shares of Canada’s target without stringent new policies or other changes from current trends (Environment and Climate Change Canada, Citation2021). leaves no doubt that oil and gas emissions generally and oil sands emissions specifically must turn downward in order for Canada to meet its international commitments.

Figure 3. Canadian emissions, projections, commitments and long-term goals (Government of Canada, Citation2022a, Citation2021b).

Canada has introduced significant policies meant to drive emissions down nationally and specifically in the oil and gas sector. The Greenhouse Gas Pollution Pricing Act provides a federal carbon pricing backstop, although the federal legislation’s requirements with respect to the oil sands are presently being met through provincial carbon pricing policies.Footnote3 The Technology Innovation and Emissions Reduction Regulation (TIER) in Alberta implements a system of carbon pricing and output-based allocations of emissions credits which establishes, as of 2022, an effective $50/tonne marginal price on emissions from the oil sands.Footnote4 The average cost of emissions is substantially lower, since the output-based allocations can and often do cover a substantial share of a project’s emissions liabilities (Canadian Institute for Climate Choices, Citation2021, p. 43).

Further policies targeted at the oil and gas sector are in various stages of implementation. First, clean fuel regulations introduced under the Canadian Environmental Protection Act are scheduled to take effect in 2024. The regulations require a reduction in carbon intensity of produced or imported barrels every year through 2030 relative to 2016 levels. Facilities will be able to comply either through blending lower-carbon fuels or lowering their own carbon footprint, with provisions for offsets to be generated by lowering fuel use through investments in fuel-switching, electrification, and similar initiatives (Clean Fuel Regulations, Citation2022).

Next, the 2022 Federal Budget introduced an investment tax credit for carbon capture, utilization and sequestration (CCUS), worth up to 50% of invested capital (Government of Canada, Citation2022b, pp. 97–98). This is not exclusively targeted to the oil sands, but the hydrogen production facilities associated with oil sands upgrading present potential low-cost opportunities for CCUS. An oil sands industry consortium, the Oil Sands Pathways to Net Zero Initiative (Citation2021), sees CCUS as essential to decarbonizing oil sands bitumen production.

Finally, Prime Minister Trudeau (Citation2021) promised during his speech at the Glasgow climate change conference to impose a regulatory cap on oil and gas emissions that would lead to reductions “at a pace and scale needed to reach net-zero by 2050.” The Prime Minister also pledged that oil and gas emissions would not increase beyond current levels. Both will be very challenging goals.Footnote5 A discussion paper proposing two options to implement the oil and gas emissions cap was published in July of 2022 (Government of Canada, Citation2022c).

The global context: oil in a carbon-constrained world

Canada’s oil sands are affected by global prices and overall oil demand. Oil sands production amounts to roughly 5% of global crude oil supply, and the industry is highly export-dependent. In 2021, more than 2.5 million barrels per day of oil sands production was shipped out of Alberta, both to markets in the United States and in Canada (Alberta Energy Regulator, Citation2022a). One of the primary drivers of future global oil demand is likely to be action on climate change. How other global suppliers see and respond to these trends will, in turn, determine the evolution of prices for oil and, in turn, the financial viability of the oil sands.

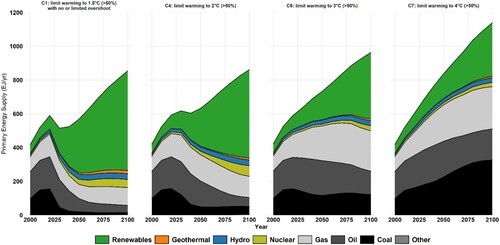

The IPCC Sixth Assessment Report (IPCC AR6) (Citation2022), and the repository of modeling scenarios gathered by the International Institute for Applied Systems Analysis (IIASA), provide an excellent lens through which to examine the relationships between global action on climate change and the evolution of global energy systems (Byers et al., Citation2022). The IIASA database classifies modeled scenarios for the IPCC report based on the implied warming trajectory (C1–C7) and the socio-economic trends (SSP1-SSP5) underlying the scenario. To limit the scope of my analysis, I focus on policy scenarios representing 1.5 and 2°C outcomes (C1 and C4), an overshoot of the 2°C goals roughly in line with current international commitments (C6), and a current policies specification (C7) each under middle-of-the-road (SSP2) socio-economic assumptions.Footnote6

The expected energy mix changes dramatically with aggressive action on climate change. The magnitude of the expected transition in energy supplies implied by aggressive climate change goals is shown in . In the left-hand panel, the average of 1.5°C scenarios, coal and oil supplies peak immediately and decline rapidly, while gas use is more stable over time and renewables grow rapidly as a share of global energy supply. In the second panel from the left, the average of 2°C scenarios, oil production peaks a bit later and sees a less rapid decline compared to coal. In the average of the 3°C scenarios, we still see oil use peak in the medium term, around 2035, but with a substantially larger use of gas on average. Only under current policies, shown in the far-right panel, do we see marked increases in fossil fuel supply on average. And, even under current policies which imply a 50% chance of 4°C of warming, mean predicted global oil use peaks before 2050.

Figure 4. Mean Primary Energy Supply, IPCC SSP2 Scenarios (Data via Byers et al., Citation2022).

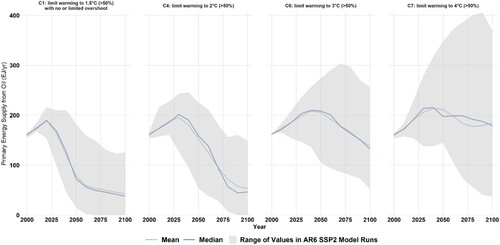

There is a wide range of plausible oil demand scenarios underlying each climate action scenario in the IPCC AR6 report. shows an isolated view of the oil market and includes both the median and mean predicted oil use as well as the range of predictions in all IPCC SSP2 model runs. In the far-left panel, we see that there are no scenarios which result in a 1.5°C transition and also see oil use rise above today’s levels, and the mean and median of these scenarios show approximately 50% reductions in oil demand compared to today’s levels by 2050. Similarly, for 2°C scenarios, no scenarios compatible with that goal showed increases in oil demand beyond 2040, and the mean and median scenario see peaks around 2026.

Figure 5. Mean, median, and range of oil demand in IPCC SSP2 scenarios for C1, C4, C6, and C7 warming scenarios (Data via Byers et al., Citation2022).

The IPCC scenarios yield results similar to those in International Energy Agency (IEA) (Citation2021a, Citation2021b). In the IEA (Citation2021a, p. 101) study of energy transitions to net-zero by 2050, the central scenario showed an average decline in oil demand of more than 4% per year from 2020 to 2050, along with dramatic reductions in the emissions-intensity of oil production. In the Sustainable Development Scenario of IEA (Citation2021b, p. 74), a less aggressive emissions reduction trajectory, oil demand drops by more than half from 2020 to 2050, while in their Net-Zero scenario, the decline is closer to 75%. Importantly, both of these IEA scenarios also predict a marked reduction in real global oil prices resulting from global action on climate change (see, for example, Table 2.2, p. 101 in IEA, Citation2021b). There should be no question that global action on climate change has and will continue to dramatically affect global oil markets and outlooks.

Oil demand is not the only important climate-change-related global factor to affect the oil sands industry. The pressure on (and from) investors and insurers to divest from emissions-intensive projects and companies has reduced the availability of global capital for the oil sands industry. Alberta has already felt the brunt of this, with global majors Shell, Total, Statoil/Equinor, and Conoco exiting their oil sands positions within the past ten years, with the European majors referencing climate change as an important driver of their decisions. Banks (HSBC) and insurance companies (Axa, Zurich, and Swiss Re) have announced intentions to exit or limit their activities in the oil sands industry as well (Flavelle, Citation2020; Jaremko, Citation2022). In a recent, revealing episode, the CER allowed the TransMountain pipeline to keep the identity of its insurance providers confidential after the pipeline proponent argued that public disclosure would likely prevent it from securing insurance coverage (CER, Citation2021b). Such pressure is unlikely to be mitigated through regulatory smokescreens alone.

Pressure from investors and insurers is likely to increase as global securities regulators advance requirements for climate change risk disclosure, in particular those which focus on financed and insured emissions. In 2022, the United States Securities and Exchange Commission (SEC) proposed new disclosure rules that would require companies to disclose levels of emissions associated with their financial activities where those companies had stated goals in respect to those emissions or where risks are material (Securities and Exchange Commission, Citation2022). Canada is also developing rules, although the initial versions are less aggressive in terms of reporting on eventual combustion emissions than the SEC proposed rules (Canadian Securities Administrators, Citation2021). These rules mirror initiatives globally in jurisdictions including the United Kingdom and New Zealand. The global adoption of disclosure rules will make it more challenging for global firms to finance or otherwise underwrite emissions-intensive projects, including oil sands and the pipelines that allow for the export of oil sands products.

The North American context: a changing oil market

For a long time, the North American market was short crude oil, with the United States shifting from a net exporter in the first half of the twentieth century to become the world’s largest importer of crude oil. Since the mid-2000s, expanded production in Canada and in the United States has disrupted the North American crude oil market, leading to altered infrastructure use, pressure to build new pipelines, and changes in trading relationships between Canada, the United States, and Mexico.

A long market for crude oil

Net imports of crude oil rose consistently in the United States from the 1950s, peaking in the mid-2000s at over 10 million barrels per day. Since that point, net imports of crude oil into the United States have dropped precipitously, to approximately 3 million barrels per day today. Canada is currently a net exporter of 3.3 million barrels per day, and Mexico is an exporter of roughly 1 million barrels per day of crude oil. In other words, in contrast to most of the last seventy years, the North American continent is a net exporter of crude oil (see, generally, Energy Information Administration (EIA), Citation2022).

For Canadian oil sands, proximity to a short market in the United States has always been part of the value proposition. Historically, United States mid-continent pricing was at a premium to global prices, and these markets were easily served by Canadian pipelines. United States refineries refit to process Canadian crude, aided by federal assistance in the Energy Policy Act of 2005.Footnote7 However, as Canadian exports grew, and domestic production increased in the United States with the advent of tight and shale oils, the market became saturated, most noticeably in the mid-continent in 2010–2014 (Kellogg, Citation2014). With new pipeline infrastructure built and existing pipelines modified to move crude oil south to the Gulf Coast, and the crude oil export ban removed in the United States, the market eventually debottlenecked, but the damage to Canadian crude oil has not completely dissipated (National Energy Board, Citation2018). The marginal barrel of Canadian crude is now shipped as far south as Texas or California, and rather than commanding a premium to global prices, many of the traditional markets for oil sands now price at or below prevailaing global prices. Net revenues to oil sands producers are a smaller share of world prices than would have been the case in a short North American market.

Cross-border infrastructure challenges

Pipeline capacity constraints for routes out of Alberta have defined the oil sands debates in Canada for much of the last decade, with the Northern Gateway, Keystone XL, Energy East, and TransMountain pipelines each having their turns in rocky regulatory, legal, and political processes. Central to each of these was the question of climate change. This was most evident in the fight over the cross-border Keystone XL pipeline which President Obama first vetoed, stating that approving the project would have undercut leadership by the United States in the global fight against climate change. After the permit for the pipeline had been re-issued by President Trump, President Biden rescinded it in 2021 echoing the need for leadership on climate change and stating that, in a time of climate crisis, the pipeline “disserves the U.S. national interest” in his first Executive Order (Government of the United States, Citation2021).

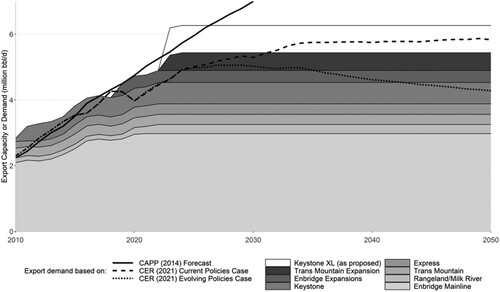

Even with Keystone XL off the table, the current portfolio of cross-border pipelines appears sufficient to meet shipping demand from the oil sands if climate change policy stringency continues to accelerate. In fact, when projected supply available for export in a world acting on climate change is considered, it seems more likely that Canada will have too much pipeline capacity than too little (see the dotted line in ). For pipeline capacity constraints to be material to oil sands development, you would need one of two conditions to be true: either, you would need to see some existing capacity removed (for example, capacity of the Enbridge Mainline system could be reduced if Line 5 in Michigan were shut down) or you would need to see a sustained willingness to invest in new oil sands production projects as is the case in the Current Policies scenario in CER (Citation2021a), shown by the dashed line in .

Figure 6. Forecast Western Canadian oil export demand (Canadian Association of Petroleum Producers, Citation2014; CER, Citation2021a) and pipeline capacity (CER, Citation2020, Citation2021a).

Crude-by-rail also provides substantial export capacity, both as a means to ship oil sands and other oil products to markets not served by pipelines or as an alternative to pipelines when capacity is constrained. For example, in the first two months of 2020, over 400,000 barrels per day of Canadian crude oil exports were delivered by rail (CER, Citation2021c). Current rail car loading capacity in Alberta is estimated at over 800,000 barrels per day, which provides a significant buffer against pipeline capacity constraints (Oil Sands Magazine, Citation2022). While crude oil transport by rail is generally more expensive than transport by pipeline, transporting bitumen by rail requires less (or in some cases, no) dilution, lowering total volume requirements which, in turn, leads to rail shipping costs closer to the costs of shipping by pipeline (IHS Markit, Citation2013). When rail capacity is added to the pipeline capacity shown in , it seems even more unlikely that new pipeline projects will be required beyond those already under construction.

If there were to be a demand for increased pipeline capacity, projects would face greater scrutiny under new regulatory processes established for new or expanded international or inter-provincial pipelines. The Canadian Energy Regulator Act and the Impact Assessment Act (often collectively referred to as Bill C-69) place climate change front-and-centre in major project assessment in Canada, and these rules will apply to any major new pipeline project.Footnote8 The Canadian Energy Regulator Act and the Impact Assessment Act each impose a series of climate-change-related constraints on both review panels and political decision-makers that combine to make regulatory approval of any new pipeline project more challenging. Decision-makers would need to show that the pipeline project does not materially compromise Canadian climate change goals in order to approve the pipeline, or expressly accept and acknowledge any induced emissions increase.Footnote9 Any material impact of these rules on oil sands pipeline capacity seems unlikely in a case where the balance of the country’s economy is facing stringent emissions constraints, and where global action on climate change is restricting oil demand growth. International pressure, particularly as applied on insurance and financing providers, can also be expected to play a role in making new pipelines more difficult to build in a world acting on climate change.

Regulatory proceedings for new pipelines have assessed the degree to which new pipelines lead to increased GHG emissions (See, for example United States Department of State, Citation2019, on Keystone XL.) While most regulatory processes have found the impact of new pipelines to be positive and small (see also Environment and Climate Change Canada, Citation2016), recent discourse with respect to the Russia-Ukraine conflict may serve to renew these debates in a way not yet widely acknowledged. We now hear how, but for the resistance to pipelines, Canada would be producing much more oil and the world would be less dependent on crude from Russia. In the future, it may be difficult to return again to the arguments made by many pipeline proponents that pipelines don’t, in and of themselves, increase production and GHGs.

The future of the Canadian oil sands

The future of the Canadian oil sands has already been fundamentally disrupted by global and, albeit to a lesser degree, domestic concern with and action on climate change. What solutions, if any, could alter the fate of the oil sands industry in a climate-constrained world? Scaling-up of existing technologies can further reduce the emissions-intensity of oil sands production (Al-Aini et al., Citation2022; IHS Markit, Citation2022b). There are several new or emerging technologies, in particular those which de-carbonize electricity and hydrogen supplies, which can reduce upstream emissions and move production closer to net-zero goals. The fact remains, however, that the world’s climate change solutions must include reduced consumption of oil and other fossil fuels. The climate- and technology-driven shift away from oil presents important risks, financial and social, for the oil sands in a carbon-constrained world. I discuss each of these in turn below.

Solutions

The most discussed solutions to de-carbonizing the oil sands are the deployment of small modular nuclear reactors (SMNRs) and the scaling-up of CCUS. Other solutions (solvents, cold-flow, etc.) exist as well, but none are as transformative as either SMNRs or widescale deployment of CCUS and so I do not discuss them in detail here (see Al-Aini et al., Citation2022 for more detail). Another class of solutions, perhaps with more salience in the context of global action on climate change, is the development of uses for bitumen beyond combustion.

Small modular nuclear reactors are a potential solution to de-carbonize the oil sands because of their potential to replace combined heat-and-power currently used in the industry. Both the electricity and steam can be used either by in situ or mining operations in the oil sands and so, while the technology would not be a simple plug-and-play solution, it does fit within existing process designs. The timelines are challenging however, as there currently exists no regulatory framework for commercial deployment of SMNRs, and so deployment before 2030 is highly unlikely (Al-Aini et al., Citation2022, p. 41). The regulatory environment is likely to be further complicated by federal jurisdiction over nuclear power overlapping with primarily provincial jurisdiction over oil sands operations. And, beyond these challenges, deploying SMNRs in the oil sands would be a very costly endeavor even if such plans were to garner regulatory approval and social acceptability, and would be a poor fit for oil sands projects close to their end-of-life.

CCUS is currently in use at the Quest project at the Scotford oil sands upgrader in Fort Saskatchewan, and at the Redwater refinery which processes oil sands bitumen. Similar technical opportunities exist in upgraders in the oil sands mining operations, since hydrogen production in these facilities produces a very pure stream of CO2, but these facilities account for less than 10% of total oil sands emissions (Al-Aini et al., Citation2022, p. 47). The balance of oil sands emissions are either unsuitable for CCUS or are released in much lower concentrations in flue gas streams, which in turn increases the costs of CCUS. As mentioned above, the federal and provincial governments are both active in direct funding of CCUS projects, and the federal government recently announced a new tax incentive to better align Canada’s investment climate with that created by 45Q tax credits in the United States (see the consultation process in Government of Canada, Citation2021c, and the measures in the budget in Government of Canada, Citation2022b).Footnote10 There are also major infrastructure projects to provide some transportation capacity for captured CO2, but even if this infrastructure were fully utilized, it would accommodate less than half of current oil sands production emissions.

Alberta’s government, facing the prospect of a carbon-constrained world, has also funded and promoted prospective uses of bitumen beyond combustion (see, for example, Zhou et al., Citation2021). Non-combustion uses for bitumen have been examined for a long time, although asphalt applications have been the most common commercial use of the heavier ends of oil sands barrels. Recently, other initiatives including using bitumen as a feedstock for carbon fiber and petrochemical production have been funded in Alberta although, if bitumen is to compete with existing feedstocks for these activities, it may need to be offered at a larger discount than is the case today.

Each of these solutions could act to reduce the exposure of the oil sands industry to global action on climate change, but transition risks remain substantial. Many of the technologies mooted as means to reduce emissions are speculative, in particular at the scale required to offset annual oil sands emissions (Al-Aini et al., Citation2022). And, as discussed in IHS Markit (Citation2022a) and Al-Aini et al. (Citation2022), much of the life-cycle emissions in an oil sands barrel occur when the oil is combusted. As the world moves away from the combustion of fossil fuels, the risk of stranded assets and other losses are real. Some of these are discussed below.

Risks

Substantial risks to the oil sands industry will arise as the world transitions away from fossil fuels. There is the potential for – although by no means a guarantee of – lower oil prices leading to insolvency. These risks are amplified as domestic regulations increase the costs of production and, as a result, raise the oil price required to maintain existing projects as going concerns. There is a compounding effect if increased costs and lowered future margins make investments in abatement less attractive all-else-equal.

The statement that lowered oil demand might not equate to lower oil prices might seem surprising coming from an economist, but it is entirely consistent with the basic model of supply and demand. We observe equilibrium prices – the price that balances supply and demand – and while action on climate change is likely to reduce demand, if firms forecast this reduction in demand, they are less likely to invest in new supply. This paper provides an excellent example – you’ve likely read to this point imagining a world of climate-change-induced low oil demand and low oil prices. You’ve perhaps convinced yourself that an investment in new oil supplies, or even in the maintenance of production from existing fields would be foolhardy. And, if everyone else thinks like you, a climate-constrained world with high oil prices is plausible, because both supply and demand will shift. What’s less likely, of course, is a world with higher net producer revenues in the long-term, but we should not discount the oil market maxim which holds that the surest cure for high prices is high prices, and vice versa. In the case of climate change, one way to guarantee high prices is to create a world that is convinced that only low prices are possible.

With that said, it is still certainly the case that, all else equal, less demand for oil implies lower prices and higher risks of stranded liabilities. And the oil sands have a lot of liabilities at risk of stranding, with tailings ponds and site reclamation responsibilities at the top of the list. Fluid fine tailings are the residuals from oil sands mining operations, comprised of water, sand, clay, bitumen, and heavy metals. They are stored in tailings ponds, and the current volume of these ponds is staggering. As of the end of 2020, 1360 million cubic meters of fluid fine tailings and 479 million cubic meters of process-affected water were stored in ponds on Northern Alberta. To put this figure into perspective, Toronto’s domed baseball stadium, Rogers Centre, has an interior volume of 1.6 million cubic meters and so the volume of fluid tailings and process-affected water in the oil sands could fill the home of the Blue Jays 1150 times over. (This, and tailings statistics to follow taken from Alberta Energy Regulator, Citation2021b; Rogers Centre volume from Major League Baseball, Citation2022.) The situation is also getting worse – between 2014 and 2020, non-remediated fluid fine tailings volume increased by 27%, while stored water volume increased by 17%. And, the timelines to reclamation are long: for example, the CNRL Horizon mine has an approved tailings management plan that sees stored tailings volumes doubling from current levels by 2030, and has most tailings remediation planned for the early 2060s (Alberta Energy Regulator, Citation2021b). The potential for stranded liabilities is substantial if oil sands mining projects become insolvent. Estimates of the total oil sands reclamation liability lie in the tens to hundreds of billions of dollars (Pembina Institute, Citation2018; Yewchuk, Citation2021). The Government of Alberta holds minimal surety against these liabilities: less than $1 billion today (AER, Citation2021a), held in the form of cash, letters of credit, or approved demand forfeiture bonds (AER, Citation2022b). The surety regime effectively allows companies to use the forward-looking value of their mining assets as collateral against their reclamation liabilities, and global energy transitions and international and domestic actions on climate change will likely erode the value of that collateral.

Another significant potential for stranded liabilities lies in the infrastructure serving the oil sands. The major pipelines which allow the export of oil sands products rely either on common carrier pipeline regulations or on long-term contracted shipping with the oil sands producers. Both are subject to significant risk due to global action on climate change. The contracts held by pipeline companies are subject to counter-party risk, and that risk is highly correlated since global events that affect any one oil sands producer are likely to affect all producers. Furthermore, as volumes are eventually reduced, both pipeline financial structures are subject to regulatory downward spirals. Canada has already seen a similar evolution of the financial viability of the natural gas mainline whereby a vicious cycle of reduced volumes leading to increased tolls led to the regulator restricting the capacity for the owner to recover all costs from shippers (Reuters, Citation2013). Regardless of the specific regulatory environment for each pipeline, a reduction in shipping volumes risks creating insolvencies in the pipeline sector over time, and thus the stranding of environmental and other liabilities. In the context of cross-border pipelines, this risk is exacerbated by the interaction of regulatory regimes in Canada and the United States.

Finally, there are domestic consequences, both in the labor force and in the financial sector, to be considered. While oil sands production is a capital-intensive industry, the oil sands boom in the early 2000s led to dramatic increases in employment and earnings Marchand, Citation2012, with employment and investment impacts spilling over into related industries. Currently, direct employment in the oil sands industry is over 30,000 workers (PetroLMI, Citation2020), to which indirect jobs in construction, retail, services, and manufacturing should be added (see Marchand, Citation2012), although note that Marchand studies times of construction booms versus the environment of sustained operations that we see today). Previous rapid industrial collapses, whether in the forestry, fisheries, or manufacturing areas have led to decades-long hollowing out of affected regions, and the same is likely to be true of the oil sands region and much of northeastern Alberta over time. The financial industry in Canada also faces risks that could have global implications. The size of the oil sands industry in Canada implies substantial exposure of the country’s financial sector to any major insolvencies and, as with the discussion of pipelines, the risks of insolvency resulting from a global energy transition is highly correlated among what is now a mostly pure-play oil sands industry. With the exception of Exxon-Mobil, which is the parent of major oil sands player Imperial Oil, the remaining major entities of Suncor, Cenovus, and Canadian Natural Resources are all heavily exposed to global oil trends, but also to oil-sands-specific trends. Each has substantially expanded their oil sands holdings in recent years through mergers and acquisitions (Fawcett, Citation2020), increasing the concentration and decreasing the diversification in their asset holdings.

Conclusions

Canada’s oil sands are substantially exposed to global action on climate change, and these actions are likely to have more impact on Canada and Alberta than domestic policies. With over 160 million barrels of reserves and almost 2 trillion barrels of resource in place (AER, Citation2022a), the oil sands represent a compelling source of natural capital and a potential driver of economic activity. The oil sands account for about 4% of global oil supply, more than all but the top-8 oil producing countries in the world. However, this paper argues that the future of the oil sands is much less bright today compared to previous years. I’ve shown that global oil demand is highly negatively correlated with global action on climate change and, using scenarios from the recent IPCC Sixth Assessment report, showed the stronger result that increases in oil demand are incompatible with meeting global climate goals. I’ve discussed both the domestic and international challenges to both further oil sands project development and even to sustained production in the long term and, finally, discussed some potential solutions and material risks facing the oil sands and by extension Canada in this global energy transition. The major barrier facing the oil sands industry, in a carbon-constrained world, is that there remains no solution that de-carbonizes the oil itself, meaning that no matter how much production emissions are reduced, the main link between oil sands and climate change – combustion emissions – will remain unaffected.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Andrew Leach

Andrew Leach is an energy and environmental economist and is professor of economics and law at the University of Alberta. He has a Ph.D. in Economics from Queen's University, and a B.Sc. (Environmental Sciences) and M.A. (Economics) from the University of Guelph and recently completed an L.L.M. (Constitutional Law) from the Faculty of Law at the University of Alberta. His research spans energy and environmental economics with a particular interest in climate change policies and their intersection with constitutional law.

Notes

1 For a comprehensive history of Alberta’s oil sands, see The Patch (Turner, Citation2017).

2 For an extensive discussion of oil and gas policies in Canada, see Plourde (Citation2012).

3 Greenhouse Gas Pollution Pricing Act, SC 2018, c 12, s 186.

4 Technology Innovation and Emissions Reduction Regulation, 2019, Alta Reg 133-2019.

5 The House of Commons Standing Committee on Natural Resources (RNNR), 44th Parliament, 1st Session, examined the prospect of a regulatory cap on oil and gas emissions in the Spring of 2022 in meetings 4–9, 11–13, and 16.

6 The other SSP socio-economic assumptions are Sustainability (SSP1), Regional Rivalry (SSP3), Inequality (SSP4) and Fossil-fueled Development (SSP5). For more detail, see Riahi et al. (Citation2017).

7 Section 1323 of the Energy Policy Act of 2005 created a temporary expensing provision for refinery improvements which increased the processing capacity for qualified fuels. Qualified fuels (s. 45K(c)(1)(A)) include fuels produced from “shale and tar sands” which allowed a deduction for retrofits designed to process Canadian oil sands imports.

8 Impact Assessment Act, SC 2019, c 28, s 1; Canadian Energy Regulator Act, SC 2019, c 28, s 10.

9 The impact of these rules on pipelines serving the oil sands are assessed in detail in Leach (Citation2021), while Bishop and Sprague (Citation2019) examine the broader impacts of the legislation on resource development.

10 26 USC 45Q: Credit for carbon oxide sequestration provides a tax credit worth up to US$50 per metric tonne carbon oxides captured and sequestered. Several proposals have been made to increase this tax credit amount (McMahon, Citation2021). Canada’s proposal is for an investment tax credit rather than a sequestration credit.

References

- Al-Aini, E., Severson-Baker, C., & Gorski, J. (2022). Getting on track: A primer on challenges to reducing carbon emissions in Canada’s oilsands. Pembina Institute. https://www.pembina.org/reports/getting-on-track.pdf.

- Alberta Energy Regulator. (2021a). Mine Financial Security Program. Alberta Energy Regulator. https://www.aer.ca/regulating-development/project-closure/liability-management-programs-and-processes/mine-financial-security-program.

- Alberta Energy Regulator. (2021b). State of Fluid Tailings Management for Mineable Oil Sands, 2020. Alberta Energy Regulator. https://static.aer.ca/prd/documents/reports/2020-State-Fluid-Tailings-Management-Mineable-OilSands.pdf.

- Alberta Energy Regulator. (2022a). Alberta Energy Outlook (ST98). Alberta Energy Regulator.

- Alberta Energy Regulator. (2022b). Manual 024: Guide to the Mine Financial Security Program. AER. https://static.aer.ca/prd/documents/manuals/Manual024.pdf.

- Alberta Energy Regulator. (2022c). ST3. Alberta energy resource industries monthly statistics. https://www.aer.ca/providing-information/data-and-reports/statistical-reports/st3.

- Bergerson, J. A., Kofoworola, O., Charpentier, A. D., Sleep, S., & MacLean, H. L. (2012). Life cycle greenhouse gas emissions of current oil sands technologies: Surface mining and in situ applications. Environmental Science & Technology, 46(14), 7865–7874. https://doi.org/10.1021/es300718h

- Bishop, G., & Sprague, G. (2019). A crisis of our own making: Prospects for major natural resource projects in Canada. C.D. Howe Institute. https://www.cdhowe.org/public-policy-research/crisis-our-own-making-prospects-major-natural-resource-projects-canada.

- Borenstein, S., & Kellogg, R. (2014). The incidence of an oil glut: Who benefits from cheap crude oil in the Midwest? The Energy Journal, 35(1), 15–34. https://doi.org/10.5547/01956574.35.1.2

- Bošković, B., & Leach, A. (2020). Leave it in the ground? Oil sands development under carbon pricing. Canadian Journal of Economics/Revue Canadienne D’économique, 53(2), 526–562. https://doi.org/10.1111/caje.12436

- Byers, E., Krey, V., Kriegler, E., Riahi, K., Schaeffer, R., Kikstra, J., Lamboll, R., Nicholls, Z., Sandstad, M., Smith, C., van der Wijst, K., Lecocq, F., Portugal-Pereira, J., Saheb, Y., Stromann, A., Winkler, H., Auer, C., Brutschin, E., Lepault, C., … Skeie, R. (2022). AR6 Scenarios Database. https://doi.org/10.5281/zenodo.5886912.

- California Air Resources Board. (2021). Calculation of 2020 crude average carbon intensity value. CARB. https://ww2.arb.ca.gov/sites/default/files/classic/fuels/lcfs/crude-oil/2020_crude_average_ci_value_final.pdf.

- Canadian Association of Petroleum Producers. (2014). Crude oil forecast, markets & transportation. CAPP. https://perma.cc/L28P-S3JU.

- Canadian Energy Regulator. (2020). Canada’s Energy future 2020—energy supply and demand projections to 2050. Canadian Energy Regulator. https://www.cer-rec.gc.ca/en/data-analysis/canada-energy-future/2020/index.html.

- Canadian Energy Regulator. (2021a). Canada’s energy future 2021. Canadian Energy Regulator. https://www.cer-rec.gc.ca/en/data-analysis/canada-energy-future/2021/canada-energy-futures-2021.pdf.

- Canadian Energy Regulator. (2021b). Decision: Trans mountain pipeline ULC (Trans Mountain) request for confidential treatment. https://perma.cc/P34S-738U.

- Canadian Energy Regulator. (2021c). Canadian crude oil exports by rail. Canadian Energy Regulator. https://www.cer-rec.gc.ca/en/data-analysis/energy-commodities/crude-oil-petroleum-products/statistics/canadian-crude-oil-exports-rail-monthly-data.html.

- Canadian Institute for Climate Choices. (2021). 2020 expert assessment of carbon pricing systems. Government of Canada. https://publications.gc.ca/site/eng/9.900084/publication.html.

- Canadian Securities Administrators. (2021). 51-107—climate-related disclosure update and CSA notice and request for comment proposed national instrument 51-107 disclosure of climate-related matters. https://perma.cc/UE6V-8GPB.

- Carney, M. (2012). Dutch disease. Bank of Canada. https://www.bankofcanada.ca/2012/09/dutch-disease/.

- Clean Fuel Regulations SOR/2022-140, Canada Gazette, Part II, Vol 156, N 14. (2022). https://www.gazette.gc.ca/rp-pr/p2/2022/2022-07-06/html/sor-dors140-eng.html.

- Energy Information Administration. (2022). Country-level energy data. EIA. https://www.eia.gov/international/data/world.

- Environment and Climate Change Canada. (2016). Trans mountain pipeline ULC - trans mountain expansion project: review of related upstream greenhouse gas emissions estimates (p. 62). Environment and Climate Change Canada. https://perma.cc/T7YF-RP2E.

- Environment and Climate Change Canada. (2021). Canada’s greenhouse gas emissions projections. ECCC data mart. https://data.ec.gc.ca/data/substances/monitor/canada-s-greenhouse-gas-emissions-projections/Current-Projections-Actuelles/GHG-GES/?lang = en.

- Fawcett, M. (2020, November 3). Oil sands companies are consolidating – and that could spell disaster for Calgary. Globe and Mail. https://www.theglobeandmail.com/opinion/article-oil-sands-companies-are-consolidating-and-that-could-spell-disaster/.

- Flavelle, C. (2020, February 12). Global financial giants swear off funding an especially dirty fuel. The New York Times. https://www.nytimes.com/2020/02/12/climate/blackrock-oil-sands-alberta-financing.html.

- Gordon, D., Brandt, A., Bergerson, J. A., & Koomey, J. (2015). Know your oil: creating a global oil-climate index. Carnegie Endowment for International Peace. https://carnegieendowment.org/2015/03/11/know-your-oil-creating-global-oil-climate-index-pub-59285.

- Government of Canada. (2021a). Canada’s 2021 nationally determined contribution (NDC). UNFCCC. https://www4.unfccc.int/sites/ndcstaging/PublishedDocuments/Canada%20First/Canada%27s%20Enhanced%20NDC%20Submission1_FINAL%20EN.pdf.

- Government of Canada. (2021b, April 20). 2021 national inventory data. Environment Canada. http://data.ec.gc.ca/data/substances/monitor/canada-s-official-greenhouse-gas-inventory/.

- Government of Canada. (2021c, June 7). Investment tax credit for carbon capture, utilization, and storage. Department of Finance Canada. https://www.canada.ca/en/department-finance/programs/consultations/2021/investment-tax-credit-carbon-capture-utilization-storage.html.

- Government of Canada. (2022a). 2022 national inventory report. Environment Canada. https://publications.gc.ca/site/eng/9.506002/publication.html.

- Government of Canada. (2022b). Budget 2022 [Government of Canada]. https://budget.gc.ca/2022/pdf/budget-2022-en.pdf.

- Government of Canada. (2022c, July 18). Options to cap and cut oil and gas sector greenhouse gas emissions to achieve 2030 goals and net-zero by 2050. https://www.canada.ca/en/services/environment/weather/climatechange/climate-plan/oil-gas-emissions-cap/options-discussion-paper.html.

- Government of the United States. (2021, January 21). Executive order on protecting public health and the environment and restoring science to tackle the climate crisis. The White House. https://perma.cc/Z2D5-UWZG.

- Guo, J., Orellana, A., Sleep, S., Laurenzi, I. J., MacLean, H. L., & Bergerson, J. A. (2020). Statistically enhanced model of oil sands operations: Well-to-wheel comparison of in situ oil sands pathways. Energy, 208, 118250. https://doi.org/10.1016/j.energy.2020.118250

- Heyes, A., Leach, A., & Mason, C. F. (2018). The economics of Canadian oil sands. Review of Environmental Economics and Policy, 12(2), 242–263. https://doi.org/10.1093/reep/rey006

- IHS Markit. (2013, September 10). Oil sands bitumen: A unique case for rail economics. IHS Markit. https://ihsmarkit.com/research-analysis/oil-sands-bitumen-a-unique-case-for-rail-economics.html.

- IHS Markit. (2022a). The right measure. IHS Canadian Oil Sands Dialogue. https://ihsmarkit.com/info/1020/right-measure.html.

- IHS Markit. (2022b). The trajectory of oil sands GHG emissions: 2009-35 [IHS Canadian Oil Sands Dialogue]. https://ihsmarkit.com/products/energy-industry-oil-sands-dialogue.html.

- Intergovernmental Panel on Climate Change Working Group III. (2022). Climate change 2022: mitigation of climate change. https://www.ipcc.ch/report/ar6/wg3/.

- International Energy Agency. (2021a). Net zero by 2050 – A roadmap for the global energy sector. IEA. https://iea.blob.core.windows.net/assets/4482cac7-edd6-4c03-b6a2-8e79792d16d9/NetZeroby2050-ARoadmapfortheGlobalEnergySector.pdf.

- International Energy Agency. (2021b, October 13). World energy outlook 2021. IEA. https://www.iea.org/reports/world-energy-outlook-2021.

- Jaremko, D. (2022, February 1). Oil sands on path to total emissions reductions. Canadian Energy Centre. https://www.canadianenergycentre.ca/oil-sands-on-path-to-total-emissions-reductions-new-analysis/.

- Jones, J. (2010, June 25). Syncrude guilty in 1,600 duck deaths in toxic pond. Reuters. https://www.reuters.com/article/us-syncrude-ducks-idUSTRE65O68520100625.

- Leach, A. (2021). The no more pipelines act? Alberta Law Review, 59(1), 7–7. https://albertalawreview.com/index.php/ALR/article/view/2662.

- Leach, A., & Boskovic, B. (2014). Carbon cost will not stop oil-sands work. Nature, 511(7511), 534–534. https://doi.org/10.1038/511534a

- Lindsay, D. (2020). Letter to Minister Wilkinson re: Teck Frontier project. Teck.Com. https://www.teck.com/media/Don-Lindsay-letter-to-Minister-Wilkinson.pdf.

- Major League Baseball. (2022). Rogers centre history. MLB.Com. https://www.mlb.com/bluejays/ballpark/information/history.

- Marchand, J. (2012). Local labor market impacts of energy boom-bust-boom in Western Canada. Journal of Urban Economics, 71(1), 165–174. https://doi.org/10.1016/j.jue.2011.06.001

- Masnadi, M. S., Benini, G., El-Houjeiri, H. M., Milivinti, A., Anderson, J. E., Wallington, T. J., De Kleine, R., Dotti, V., Jochem, P., & Brandt, A. R. (2021). Carbon implications of marginal oils from market-derived demand shocks. Nature, 599(7883), 80–84. https://doi.org/10.1038/s41586-021-03932-2

- Masnadi, M. S., El-Houjeiri, H. M., Schunack, D., Li, Y., Englander, J. G., Badahdah, A., Monfort, J.-C., Anderson, J. E., Wallington, T. J., Bergerson, J. A., Gordon, D., Koomey, J., Przesmitzki, S., Azevedo, I. L., Bi, X. T., Duffy, J. E., Heath, G. A., Keoleian, G. A., McGlade, C., … Brandt, A. R. (2018). Global carbon intensity of crude oil production. Science, 361(6405), 851. https://doi.org/10.1126/science.aar6859

- McMahon, J. (2021). Will congress supercharge 45Q—The carbon-capture tax credit—or scrap it? Forbes. https://www.forbes.com/sites/jeffmcmahon/2021/07/29/will-congress-supercharge-45q-the-carbon-capture-tax-credit-or-scrap-it/.

- Muhly, T., Serrouya, R., Neilson, E., Li, H., & Boutin, S. (2015). Influence of in-situ oil sands development on Caribou (Rangifer tarandus) movement. PLOS ONE, 10(9), e0136933. https://doi.org/10.1371/journal.pone.0136933

- National Energy Board. (2000). Canada’s oil sands: a supply and market outlook to 2015. National Energy Board. https://publications.gc.ca/collections/Collection/NE23-89-2000E.pdf.

- National Energy Board. (2018). Western Canadian crude oil supply, markets, and pipeline capacity. Canadian Energy Regulator. http://www.cer-rec.gc.ca/nrg/sttstc/crdlndptrlmprdct/rprt/2018wstrncndncrd/2018wstrncndncrd-eng.pdf.

- Oil Sands Magazine. (2022). Crude-by-rail. Oil sands magazine. https://www.oilsandsmagazine.com/projects/crude-oil-by-rail.

- Oil Sands Pathways to Net Zero Initiative. (2021, November 3). Pathways plan to achieve net zero emissions. Oil Sands Pathways to Net Zero. https://www.oilsandspathways.ca/the-pathways-vision/.

- Orellana, A., Laurenzi, I. J., MacLean, H. L., & Bergerson, J. A. (2018). Statistically enhanced model of in situ oil sands extraction operations: An evaluation of variability in greenhouse gas emissions. Environmental Science & Technology, 52(3), 947–954. https://doi.org/10.1021/acs.est.7b04498

- Pembina Institute. (2018). The Alberta government has a transparency problem when it comes to oil and gas liabilities. Pembina Institute. www.pembina.org/blog/alberta-government-has-transparency-problem-when-it-comes-oil-and-gas-liabilities.

- PetroLMI. (2020). Labour market outlook 2021 to 2023: Canada’s oil and gas industry. Careersinenergy.Ca. https://careersinenergy.ca/wp-content/uploads/2021/08/Labour-Market-Outlook-2021-to-2023-FINAL-3.pdf.

- Plourde, A. (2009). Oil sands royalties and taxes in Alberta: An assessment of key developments since the mid-1990s. The Energy Journal, 30(1), 111–139. https://doi.org/10.5547/ISSN0195-6574-EJ-Vol30-No1-5

- Plourde, A. (2012). Oil and gas in the Canadian federation. In G. Anderson (Ed.), Oil & gas in federal systems (pp. 88–120). Oxford University Press.

- Prime Minister Justin Trudeau. (2021, November 1). Prime Minister’s remarks delivering Canada’s national statement at the COP26 summit. Prime Minister’s Office. https://pm.gc.ca/en/news/speeches/2021/11/01/prime-ministers-remarks-delivering-canadas-national-statement-cop26-summit.

- Reuters. (2013, March 27). Canadian regulator slashes tolls for TransCanada mainline. Reuters. https://www.reuters.com/article/transcanada-mainline-tolls-idINL2N0CJ25C20130327.

- Riahi, K., van Vuuren, D. P., Kriegler, E., Edmonds, J., O’Neill, B. C., Fujimori, S., Bauer, N., Calvin, K., Dellink, R., Fricko, O., Lutz, W., Popp, A., Cuaresma, J. C., Kc, S., Leimbach, M., Jiang, L., Kram, T., Rao, S., Emmerling, J., … Tavoni, M. (2017). The shared socioeconomic pathways and their energy, land use, and greenhouse gas emissions implications: An overview. Global Environmental Change, 42, 153–168. https://doi.org/10.1016/j.gloenvcha.2016.05.009

- Schindler, D. W. (2014). Unravelling the complexity of pollution by the oil sands industry. Proceedings of the National Academy of Sciences, 111(9), 3209–3210. https://doi.org/10.1073/pnas.1400511111

- Schneider, R. R., Hauer, G., Adamowicz, W. L. (Vic), & Boutin, S. (2010). Triage for conserving populations of threatened species: The case of woodland caribou in Alberta. Biological Conservation, 143(7), 1603–1611. https://doi.org/10.1016/j.biocon.2010.04.002

- Securities and Exchange Commission. (2022). RIN 3235-AM87: The Enhancement and Standardization of Climate-Related Disclosures for Investors. SEC. https://www.secns.gov/rules/proposed/2022/33-11042.pdf.

- Sleep, S., Dadashi, Z., Chen, Y., Brandt, A. R., MacLean, H. L., & Bergerson, J. A. (2021). Improving robustness of LCA results through stakeholder engagement: A case study of emerging oil sands technologies. Journal of Cleaner Production, 281, 125277. https://doi.org/10.1016/j.jclepro.2020.125277

- Sleep, S., Guo, J., Laurenzi, I. J., Bergerson, J. A., & MacLean, H. L. (2020). Quantifying variability in well-to-wheel greenhouse gas emission intensities of transportation fuels derived from Canadian oil sands mining operations. Journal of Cleaner Production, 258, 120639. https://doi.org/10.1016/j.jclepro.2020.120639

- Statistics Canada. (2022). Table 25-10-0063-01: Supply and disposition of crude oil and equivalent. https://doi.org/10.25318/2510006301-eng.

- Turner, C. (2017). The Patch. Simon and Schuster. https://www.simonandschuster.ca/books/The-Patch/Chris-Turner/9781501115103.

- United States Department of State. (2019). Final supplemental environmental impact statement for the keystone XL project volume 1. https://perma.cc/YS6N-VNVR.

- Yewchuk, D. (2021, October 19). Another year gone under the mine financial security program. https://ablawg.ca/2021/10/19/another-year-gone-under-the-mine-financial-security-program/.

- Zhou, J., Geo, P., Bomben, P., Chem, P., Gray, M., Helfenbaum, B., & Eng, P. (2021). How oil sands can help the world reach net-zero emissions and creat economic opportunities for Alberta and Canada. Alberta Innovates. https://albertainnovates.ca/app/uploads/2021/11/AI-BBC-WHITE-PAPER__WEB.pdf.