?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The urban housing regime in Vienna is often regarded as one of the last integrated rental markets once described by Kemeny. Thus, according to the theory, private landlords should be forced to charge lower rents due to direct competition from the social sector. This paper formally tests this hypothesis on a very local level by linking private rent trajectories across Viennese subdistricts to their housing market structure while controlling for possible effects of location, initial prices and socioeconomic variation. Indeed significant evidence for a price dampening effect is found, as higher shares of limited-profit housing within the local rental market substantially increase the probability of a subdistrict joining a lower rent development path. However, the magnitude of the effect increases considerably for more peripheral locations associated to less demand pressure. A similar relationship is found for municipal housing, but with much lower impact, most likely due to comparatively stronger entry barriers. Thus this paper concludes a price dampening neighbourhood effect which varies with the openness of the social housing supply and the centrality of the location.

1. Introduction

In the terminology of Kemeny (Citation1995), a unitary or integrated rental market is characterized by competition between for- and non-profit housing providers. According to the theory, this should lower rents for all tenants, also those accommodated within the private segment of the market. Although originally put forth as a theory concerned with housing regimes on a national scope, recent debates have emphasized the importance of the local level – typically referring to regions or cities (Hoekstra, Citation2020; Matznetter, Citation2020). This paper goes even further and empirically investigates the role of rental market integration for intra-urban variations in rental market developments. This is done by testing the proposed relationship between social housing supply and private housing rents on a neighbourhood level.

Arguably the best environment to conduct such a case study is the city of Vienna. Housing in the Austrian capital is not only dominated by the rental sector (70%) but has a substantial supply provided by limited profit housing associations (LPHAs) with a combined market share of 21% (Statistik Austria, Citation2020b). According to some authors, Vienna might even be regarded as one of the last examples of a European city with an accommodation market that can truly be characterized by what Kemeny, Kersloot, and Thalmann (Citation2005) refer to as an integrated rental market (Matznetter, Citation2020).

Critics of this view might point towards the rapidly rising housing costs in Vienna, which have been especially pronounced in the aftermath of the financial crisis 2008 (Statistik Austria, Citation2020b). These recent developments can be traced back both to trends in market fundamentals as well as policy changes and possibly some processes of financialization. Nonetheless, price increases might still be dampened by the large supply of social housing, especially in those neighbourhoods with a high degree of competition between the market segments. Obviously the question is not whether rents were rising or not, but where they are heading and if there are diverging developments across the city. To deal with this question, one can draw on the econometric convergence literature, more specifically the idea of club convergence. Originally designed for questions of macroeconomic growth patterns between economies, Phillips and Sul (Citation2007) developed an econometric toolbox allowing for endogenous detection of so-called convergence clubs characterized by similar growth trajectories. Applied to the case of local rent levels, neighbourhoods with common price trajectories can be identified.

To test whether higher social housing shares within a neighbourhood indeed bring down prices on the private rental market, one needs to check if there are differences in those price trajectories associated to the local segmentation of the housing supply.

For this study, I use a unique micro-dataset containing 118,726 rent listings collected between 2011 and 2020 partially provided by the DataScienceService GmbH as well as the Research Unit Urban and Regional Studies of the University of Technology Vienna to construct quarterly mean prices for 190 of the 250 Viennese subdistricts (Zählbezirke). To test for rent convergence between the subdistricts in the panel a Log-t convergence test as suggested by Phillips and Sul (Citation2007) is performed. After rejecting the convergence hypothesis, the clustering algorithm also developed by Phillips and Sul is applied to detect different convergence clubs across the city. Exploiting the ordering in the outcome of the clustering process, an ordered probit model is used to investigate the relationship of social housing shares in the local housing market onto club membership and thus housing rent trajectories on the private market. Doing so, I also control for centrality, initial rent levels and socioeconomic differences within the spatial units.

Indeed significant evidence against allover convergence of private rents between subdistricts can be found. Instead, three different convergence clubs associated to an expensive, medium and comparatively affordable development path are detected. Furthermore, one can conclude a significant role of social housing shares in the local rental market onto club membership. Thus higher social housing shares are associated with lower price trajectories even when controlling for various other factors. Drawing on the econometric convergence literature, this paper is for the first time able to provide quantitative evidence on the price dampening effects of rental market integration on a neighbourhood level using a unique dataset of offering prices for Viennese rental flats. Notably, the found price dampening neighbourhood effects also vary with the openness of the social housing supply considered and the centrality of the location with is associated to the demand pressure. Both aspects do fit the underlying theoretical argument quit well. The main contributions of this paper, however, are to add an appropriately sophisticated empirical approach to the otherwise rich discussion on housing regimes and the respective strand of literature as well as the application of Kemeny's theory to explain intra-urban developments of a housing market.

The remainder of this paper is structured in the following way: Section 2 provides an overview of Kemeny's housing market typology and a brief discussion of its relevance on the sub-national level as well as an introduction to the Viennese housing market. Section 3 describes the convergence test, clustering algorithm, ordered probit model and the micro-data used. Section 4 summarizes the empirical findings while Section 5 provides both a critical discussion of these results as well as a conclusion with regard to learnings for housing policy and research.

2. Kemeny’s integrated rental market and the case of Vienna

Kemeny (Citation1995) uses the term dualist rental systems to describe housing systems which are characterized by a rather small social housing sector with strict means testing and close state control. Their goal is to provide housing for those who simply cannot afford to pay a market rent. Thus, in a given dualist rental system, non-profit and for-profit rental coexist without much interaction. The counterpart to the dualist rental systems would then be the unitary rental market which is closely associated to the social market approach applied to housing in the post-war Germany and neighbouring countries such as Austria, Denmark and the Netherlands. Within unitary rental markets, non-profit housing providers are actually encouraged to compete with for-profit landlords by the regulatory setting.

While for-profit providers generally need to charge rents able to cover both interest towards outstanding debt as well as a given market return on their equity, non-profit providers can offer rents which are only covering costs, as they are not in need for a market return on their equity. Hence, non-profit housing providers' financial costs are lower for a given ratio of equity to market value, measuring the solidity of the rental organization. Solidity should typically increase over time by debt amortization and appreciation of market values – a process referred to as maturation (Kemeny, Citation1995; Kemeny et al., Citation2005). For comparable levels of maturation, the non-profit provider should be able to set rents lower than the private landlords. If they are not constrained by tight entry barriers, non-profit organizations should be able to attract more renters than their private competitors, forcing them to adapt and also lower rents.

This spillover effect is, however, subject to several conditions. Accessibility must be given for a wide range of potential tenants and a wide distribution of housing stock in terms of location, size and quality must be provided matching the standards of the private supply. Maximum competition is achieved when the non-profit housing supply mirrors the private supply in all characteristics but the rent. According to the authors, competitive power of the non-profit sector is thus given as an interaction of solidity and market representation.

While Kemeny used the terms unitary and integrated interchangeably at first, Kemeny et al. (Citation2005) later introduced a differentiation where the integrated rental market could be perceived as something like the highest stage of a unitary rental market. Thus a unitary market in which non-profit suppliers are strong competitors is called integrated. As integration proceeds, rent control should be phased out in favour of a looser regime of rent regulation. According to Mundt and Amann (Citation2010, p. 42)

Austria's rental market comes close to Kemeny's prototype of an integrated rental market when measured by the legal framework within which it operates, as well as by the solidity and volume of the sector, the rent levels, and competition with the for-profit sector, and the orientation to large parts of the population.

All these characteristics are arguably even more pronounced in the Austrian capital.

Kemeny's rather optimistic and in the end unfulfilled expectation of a wider development towards integrated systems has been a focal point of criticism from the likes of Stephens (Citation2020a). He argues against the notion that the organization of cost-rental housing could shape the nature of a rental system and constitute a whole housing system. Thus the theory of unitary rental markets is not able to explain how housing systems are changing. Although there is some merit to Stephens argument with regard to the dynamic component at the national level, Matznetter (Citation2020) points out that focusing too much on what is going on in the aggregate can lead to premature conclusion, as housing policies are nowadays more often devoluted to subnational entities such as regions or cities. Following Hoekstra (Citation2020), the appropriate scale of comparative housing studies would indeed be at a local level.

Due to increasing price differentials in commodified and financialized housing, Matznetter argues, it is mostly the metropolitan regions where affordability deterioration is an increasing problem and thus housing policies are developed to counter or at least dampen these trends. Berlin would be an example of a local entity that is similar to Vienna in many regards. Both have a similar history in housing policies and welfare models and are recently facing growing population as well as rising house prices (Marquardt & Glaser, Citation2020). Nonetheless, in contrast to Vienna, Berlin's tenants are still suffering from the dismantling of the unitary-type German housing regime through widespread privatization (Aalbers & Holm, Citation2008) and the regional parliament now started to use rent caps as means to get a grip on the affordability problem while there is also public discussion about expropriation of large housing companies (Stephens, Citation2020a). On the other hand, Matznetter (Citation2020) singles out Vienna as a case of a city with an integrated local rental market that kept its social housing stock intact. Given their long tradition, Vienna's social housing providers can further be thought of as mature and equipped with a substantial market representation. This both holds true for the municipality as well as the limited profit housing cooperatives. For the remainder of the paper both these social providers constitute the non-profit side of the integrated rental market. The fact that Vienna indeed was able to maintain an integrated rental market is also acknowledged by Stephens (Citation2020b) in the ongoing discussion. However, he points out that this system can only flourish as so long as the broader institutions of corporatism are maintained.

Despite recent debate about whether Kemeny’s theoretical contributions are still up-to-date, his framework undoubtedly inspired a lot of research in the field of housing studies. Or as Blackwell and Kohl (Citation2018, p. 299) put it: ‘There are numerous exponents of the housing-welfare regime framework, operating under various different guises, but the most influential is assuredly Jim Kemeny '. Independent of the strength and weaknesses of his ideas with regard to development paths of housing systems, Kemeny offers both a broader theoretical framework and a useful typology to empirical researchers. Thus it seems even more surprising that hardly any work has been done to investigate the empirical outcomes of different rental market regimes. Some exceptions can be found in Borg (Citation2015) or Hoekstra (Citation2009). This paper aims to contribute to the discussion on rental market regimes by providing empirical evidence on the potential price dampening effect of an integrated rental market and their role for intra-urban housing cost developments. We, therefore, take one of the last resorts of integrated rental markets, namely the city of Vienna to conduct an empirical study.

2.1. The case of the Viennese housing market

The City of Vienna is traditionally known for its local welfare model, large decommodified social housing stock and policy of social equality which lead to a resilient housing market in international comparison (Hatz, Kohlbacher, & Reeger, Citation2016). The Viennese housing market is very much a rental market with only 19% of the housing units being owner occupied. Today, according to Statistik Austria (Citation2020b) some 44% of the housing market belong to the social housing sector, which is either owned by the city (23%) or limited-profit housing associations (21%) providing housing at below-market rents for a large share of the population. Thus sizewise the social housing supply does not only match its private counterpart but substantially exceeds it. The city is actively targeting a better social mix through eligibility rules while LPHAs typically also provide housing to a wide range of income groups, both prioritizing people in employment as well as those with long-term residency in the city (Reinprecht, Citation2014). With up to 80% of the Viennese population having formal access to social housing in Vienna (Litschauer & Friesenecker, Citation2022; Marquardt & Glaser, Citation2020), Kemeny's accessibility criteria are very much met. However, some additional entry barriers exist for the municipal subsector compared to LPHAs with respect to previous residence in the city, age and of course social hardship (Litschauer & Friesenecker, Citation2022). Although the concentration of the social sector is higher in the more peripheral districts, it can be found all over the city, thus enabling lower income households to reside in areas with higher market rents (Kadi, Citation2015). Rents are substantially lower in both the municipal and LPHA sectors compared to the private market with an increasing gap (Litschauer & Friesenecker, Citation2022). In terms of quality LPHAs match if not exceed the private supply (Mundt, Citation2018), especially in the case newly constructed projects (Mundt & Amann, Citation2010). Meanwhile, the municipality provides a very diverse set of apartments with variations in age and condition, traditionally featuring a high quality of communal spaces (Friesenecker & Litschauer, Citation2022). Targeted refurbishment subsidies to modernize the existing housing stock are also in place (Mundt, Citation2018). Again, the LPHAs tend to outperform both the private as well as the municipal supply in terms of quality. Thus all main features of an integrated rental market are met to ensure a proper competition between the social housing sector and private landlords. Although, competition is expected to be primarily stemming from LPHAs, the municipal sector might still exert similar price dampening effects given the previous discussion.

The private rental sector which makes up the remaining 34% of the housing supply in Vienna can similarly be subdivided into two parts. On the one hand, a free pricing segment and a price controlled segment. The letter constitutes at least 78% of the private rental supply and mainly consists of so-called ‘Altbau’1 housing units with a construction permit before 1945 (Kadi & Verlič, Citation2019). This leaves only about 7.6% of the total housing stock traded at free market rent (Simons & Tielkes, Citation2020).

However, the private segment subject to rent controls has undergone several transformations which do not provide rents at costs but mirror market developments through a complex set of regulations. Part of the rent increases can be traced back to a reform of the tenancy law that was already introduced in 1994, but became particularly relevant since the financial crisis. The reform enabled private landlords to add location bonuses on top of regulated rents in areas with high land prices. With land prices on the rise, location bonuses took off since 2010. In the city centre, location bonuses went up from 4 euros per square meter in 2010 to 12.21 euros in 2019. Generally, location bonuses increased most in those areas with high initial levels and vice versa. At the same time, the number of short-term contracts massively increased, reinforcing upward price trends through the possibility to adapt to the fast changing market situation at a higher frequency (Kadi, Citation2015; Kadi & Verlič, Citation2019).

Meanwhile, a rather long-term restructuring of the private supply from a ‘low-quality, low-priced sector, to a high-quality, high-priced sector’ has taken place at least since the 1990s also leading to price increased (Bauer, Citation2006). Another major pricing factor of course is the increase in demand, reflected in steady population growth stemming from both internal as well as external migration towards Austria (Simons & Tielkes, Citation2020). However, the Viennese population has been growing since the late 1980s and not experienced similar upward shifts in rents (Statistik Austria, Citation2020a). Thus not all trends in private sector pricing can be traced back to market fundamentals. Especially in the aftermath of the financial crisis Viennas real estate market experienced processes of financialization (Springler & Wöhl, Citation2020) and increasing deviation from fundamental prices. According to the fundamental price indicator by Schneider (Citation2014), the Austrian National Bank (Citation2020) reports that overpricing started in early 2011 and has been constantly rising ever since. This of course spills back to the private rental market in terms of rapidly increasing rents. Hence, Viennas housing market is experiencing some recommodification, upgradings in terms of housing quality, together with fast population growth and some processes of housing financialization. Altogether, average prices in the rental market rose from 6 euros per square metre in 2009 by 40% to 8.4 euros in 2019. The trend was even more pronounced in the private segment where prices rose by 50% in the same time span (Statistik Austria, Citation2020b).

While going through all these processes that are challenging housing affordability in the Austrian capital, not only tenants in the social sector but also those subject to private landlords should still profit from the dampening effect the large social housing sector exerts onto the for profit sector. At least if we are to believe in Kemeny’s idea of the integrated rental market.

3. Methods and data

It is already clear that Viennese rents were rising in the post-financial crisis context, but are all parts of the city heading in the same direction or are there different trajectories and if so, can they be explained by the rental market structure? Given a very dynamic market situation and ongoing upward trend in rent prices neither momentarily differences in prices nor price changes across the city are sufficiently informative. Let us assume a spatial unit with low shares of social housing may have entered the panel at a high price level and now faces small price increases while a formerly lower priced ones with high social housing share exhibits strong price increases. Both are similar in all other relevant characteristics. We could either come to the conclusion that more social housing leads to lower rents or to higher rents dependent on whether a cross-sectional or time series approach is taken. However, if one could tell that the unit with low social housing share is approaching a more expensive rent level than the high social housing unit in the medium to long run irrespective of where they are on that transition path, this would be much more informative about the impacts of social housing shares onto the rent level.

Methods concerned with such trajectories can be found in the econometric convergence literature, enabling the identification those potentially diverging paths in rent price development. If allover convergence is rejected but some common trajectories are found, one can look at different characteristics of these so-called convergence clubs. In this paper, the 250 subdistricts of Vienna are taken as units to conduct such an analysis. They allow for enough variation across the city while there is still administrative data on rental market composition as well as socioeconomic information available.

3.1. Phillips and Suls log-t test of convergence and clustering algorithm

To test whether private sector rent prices converge between Viennese subdistricts, one could turn towards a variety of econometric convergence tests, with the β convergence test suggested by Barro, Sala-i Martin, Blanchard, and Hall (Citation1991) arguably being the most prominent. In this paper, however, I choose to make use of the so-called Log-t convergence test developed by Phillips and Sul (Citation2007, Citation2009). The authors proposed a time-varying factor model that allows for both individual and transitional heterogeneity to model economic variables such as income or prices. Thus the model allows for different time paths towards convergence. Furthermore the convergence test based on this time-varying factor model does not impose any restrictions regarding trend stationarity and is robust to heterogeneity which makes it a powerful tool for applied econometric convergence testing.

Suppose we have some panel data then, according to Phillips and Sul, it can be decomposed in the following way:

(1)

(1) where

is the systemic component and

is the so-called transitory component. To separate idiosyncratic from common components, one can rewrite Equation (Equation1

(1)

(1) ) as

(2)

(2) where

is the common factor and

is the systemic idiosyncratic element, which is allowed to evolve over time and also includes the random component

. While

determines the steady-state growth path,

gives us the transition path. Although we cannot directly estimate

, it is possible to construct a statistic, the authors call the relative transition component,

(3)

(3) which can be easily computed from the available data. In the case of overall convergence, we expect the transition component

to converge towards unity for all

as

. This implies that the cross-sectional variation2

(4)

(4) should converge to zero as

. Decreasing cross-sectional variation by itself, however, does not automatically imply convergence of the whole sample but could rather be due to convergence within subgroups.

To construct a formal statistical convergence test based on the described factor model, it is necessary to impose some further assumptions on the behaviour of . Phillips and Sul (Citation2007, Citation2009), therefore, suppose the systemic idiosyncratic element to follow a semiparametric model that allows for heterogeneity over time and across individual units

(5)

(5) with a time invariant component

being fixed,

being i.i.d. (0,1) across i but may be weakly dependent over t. Together the terms

and

allow for the aforementioned heterogeneity over time and across individual units even if there is a common steady state. Meanwhile

is a slowly varying function converging towards infinity as

. Here the authors suggest

although other specifications might be possible. Last but not least, the parameter α gives us the convergence rate. It becomes apparent that for

to converge as

two conditions have to be met. First the convergence rate parameter α has to be at least zero or greater for the second term to vanish over time. Which brings us the second condition that there actually is a common time invariant component. More formally we test the

against the

for some

. The alternative hypothesis includes the possibilities of total divergence but also of club convergence. As it is not possible to directly test whether

the focus is on the second part of the Null

. Thus the task is to get an estimate

.

As Phillips and Sul show, one can obtain such an estimate for the convergence rate by running the following regression model:

(6)

(6) where the initial observation used is

with some r>0, meaning the first

of the data are discarded to focus the attention onto what is going on at latter parts of the sample. As a result of Monte Carlo simulations, the authors recommend the use of

for a small sample size (T<50). The second term on the left-hand side of Equation (Equation6

(6)

(6) ) acts as a penalty, giving the test discriminatory power between overall convergence and club convergence. Finally,

which allows to test the

by looking at the heteroskedasticity and autocorrelation robust t-statistic of γ and conducting a standard one sided t-test of

. If

assuming a confidence level of 95%3 the null hypothesis of convergence is rejected.

In the case of rejecting the hypothesis of overall convergence, there could still be convergence between some units. Therefore, Phillips and Sul also provided a clustering algorithm to detect such convergence clubs. If rejected for the whole sample, the test procedure can be repeated using the following steps:

| (1) | Sort the units in descending order using the last observation of the panel | ||||

| (2) | Select the k highest units to form the core of the first subgroup for some | ||||

| (3) | Add one by one additional units to the core-subgroup and rerun the log-t test. Include a unit if the associated t-statistic is greater than a criterion | ||||

| (4) | Form a second group from those units not part of the first convergence club after step 3. Run the Log-t test to see whether the second group shows convergence. If the null hypothesis of convergence holds, conclude that there are two distinct convergence clubs in the sample. If there is divergence within the second group, repeat steps 1–3 for the units not included in the first convergence club. If step 2 cannot produce any k for which | ||||

As the clustering algorithm described is very much dependent on the arbitrarily set the authors further suggest a club merging algorithm to avoid over determination. The merging algorithm can be described by the following steps:

| (1) | Combine the first two clubs detected and run the Log-t convergence test. If the combined groups are not divergent, thus the t-statistic is larger than −1.65, they are merged to a new convergence club. | ||||

| (2) | Take the next convergence club and add it to the newly merged group. Again run the Log-t test and check whether the basic condition for convergence holds. If so, also add the new group to the merged convergence club. | ||||

| (3) | If the null hypothesis of convergence is rejected at any point, the previous subgroups (of course excluding the last one) are thought to form a joint convergence club. Restart the merging algorithm beginning with the last group for which the convergence hypothesis was rejected. | ||||

This concludes the three main steps of which the methodology suggested by Philipps and Sul consists.

3.2. Explaining club membership using an ordered probit model

The next task is to investigate the relationship between a subdistricts club membership, thus rent trajectory and its local housing market structure. Ideally, this should be done also controlling for other factors such as initial rent levels, socioeconomic differences and centrality of the subdistrict. Conveniently, the ordered nature of the clustering algorithm described in Section 3.1 can therefore be exploited using an ordered probit model as first described by McKelvey and Zavoina (Citation1975). Similar approaches combing the Phillips and Sul approach with an ordered probit model can be found for example in Tomal (Citation2021) and Bartkowska and Riedl (Citation2012) or Basel, Gopakumar, and Rao (Citation2020). See Section 3.3 for details on the explanatory variables used and their sources.

Assuming club membership is associated to a continuous latent variable a linear model can be written down to explain this latent variable

(8)

(8) where X contains the explanatory variables of initial conditions in the subdistrict. The observed ordinal variable y indicates club membership, then takes on the values

dependent on the corresponding thresholds

. Thus

(9)

(9) By artificially setting

and

Equation (Equation9

(9)

(9) ) can be written down more generally as

(10)

(10) which under normality of the error term translates into

(11)

(11) Due to the nonlinearities involved, the model cannot be estimated by OLS, however, Maximum Likelihood estimation is feasible. For the same reason, the coefficients in β cannot directly be interpreted as a ceteris paribus effects onto y, thus average marginal effects are reported as is common in the literature. Furthermore predicted probabilities of each club membership given varying levels of the explanatory variables including prediction intervals based on bootstrapping are presented.

The econometric framework suggested in this section may appear rather complicated to some readers, but comes with several desirable features compared to other possible techniques. As indicated earlier, one could also try to estimate a price dampening effect by reverting to either a panel model of rent growth or a conditional beta convergence model. However, the procedure put forth has several technical advantages as well as favourable theoretical implications. In contrast to a common panel model, it does not rely on any stationarity or unobserved common factor assumptions. Furthermore, only a random effects specification would be feasible, as the variable of interest is only available in the base year. Thus additional independence and normality assumptions, which may or may not hold, would be required within a classical panel setup. While a conditional beta convergence model with focus on the social housing share condition would not rely on such assumptions, it could only make use of a rather small proportion of the available information and automatically discard any observation between the first and final periods. From a theoretical viewpoint, the Phillips and Sul approach towards detecting common trajectories is also tempting, as it focuses on the identification of long-term trends rather than short-term variations. In the context of housing regime research, it is exactly that long-term perspective which is of interest.

3.3. Data and aggregation

As Vienna is both the Austrian capital and an own province, there is city wide survey data on rents available from the EU-SILC and the Austrian Mikrozensus. Unfortunately rent price information from the Austrian census cannot be disaggregated on a subprovince level. Hence, I have to construct my own time series for each subdistrict. To do so, data collected by the DataScienceService GmbH as well as data from the Research Unit Urban and Regional Studies of the TU Vienna are used. Both Sets of Data together contain offering prices for 111,749 flats listed on the Viennese private rental market between the first quarter of 2011 and the fourth quarter of 2020. Listing price data generally has to be treated with caution as demonstrated by Kolbe, Schulz, Wersing, and Werwatz (Citation2021). However, these authors also suggest that index construction is indeed still the most useful application for listings data, when compared to other applications like price prediction. After controlling for duplicates, the microdata is aggregated across all subdistricts and quarters. The easiest way to do this would of course be to just take the mean of the observations within each areal unit and for every point in time. However, random sampling cannot be ensured and the amount of data available varies significantly between subdistricts and over time, thus this approach would be prone to outlier problems. Without any knowledge about the underlying distribution of the actually offered numbers and types of flats, this issue cannot be resolved by properly weighting the observations.

One way to circumvent this issue is the use of a multilevel approach to obtain more realistic aggregates in areas and periods with low number of observations. It allows to shrink outlying subdistricts with little amount of information more towards the city and time independent unit average .5 There are indeed many ways to write down such a multilevel or random effects model, in this case I follow the notation suggested by Gelman and Hill (Citation2009)

(12)

(12) where y is the listed rent, i denotes the observed flat, j denotes the subdistrict it belongs to and t is the period in which the observation was made. Aggregate prices per squaremeter are then obtained as the exponential of

. Missing values of up to 2 years per subdistrict are then imputed by moving averages. Subdistricts with more consecutive missing values are discarded leaving 190 of 250 subdistricts available for the analysis. However, those units discarded are mostly peripheral and accommodate only a very small proportion of Viennese residents.

It should be emphasized that the resulting rent estimates are reflective of the gross rent level in a given area. Hence, they are not quality adjusted indices as one could obtain by hedonic regression modelling (Hill, Citation2013). Although applying such a quality adjustment may be sensible in some cases, there are two main arguments for not doing so in the given setting. From a rather practical point, developing a proper hedonic model for the Viennese rental market with all its particularities and regulations is not straight forward and would go far beyond the scope of this paper. However, as the question of housing affordability is central to the theoretical content of this investigation, it might be more sensible to work with data reflecting the housing cost burden local tenants are actually facing.

Last but not least the time series is smoothed using the classic Hodrick–Prescot (HP) filter (Hodrick & Prescott, Citation1997) as suggested by Phillips and Sul (Citation2009). However, due to criticism of the traditional HP filter over the choice of the smoothing parameter λ, Phillips and Shi (Citation2021) developed a so-called boosted-HP filter which has already been deployed within a similar study on housing rent convergence between polish provincial capitals by Tomal (Citation2021). Therefore, I will check the results for sensitivity regarding the filtering technique by repeating the Log-t test using data smoothed through the boosted-HP filter.

The dataset later used to explain convergence club memberships can largely be obtained from administrative sources. All variables are from the base year 2011 as they are meant to reflect initial conditions. Rental market structure is reflected by the share of LPHA flats and the share of municipal flats in the subdistricts rental market. Both are measured in percentage points and sourced from the Register Based Census (Registerzählung) 2011. Data on the local share of academics, here defined as residents holding at least a bachelor's degree, as well as the share unemployed residents are reported by the city of Vienna. Again, both variables are measured in percentage points. The initial rent level is retrieved from the aggregation described above. Lastly, setting up dummy variables indicating a subdistricts location within the city centre or the inner districts is straight forward.

4. Results

After aggregating the microdata and smoothing with the HP filter, the first step is to run the Log-t convergence test with the null hypothesis of rent price convergence across all subdistricts. With and t = −28.183, there is significant evidence against allover price convergence. Therefore the clustering algorithm described in Section 3.1 is applied to detect convergence clubs within the panel. The results of the clustering steps are reported in . Initially three convergence clubs and no divergent units are detected. Applying the merging algorithm club does not change the outcome.

Table 1. Price convergence club classification.

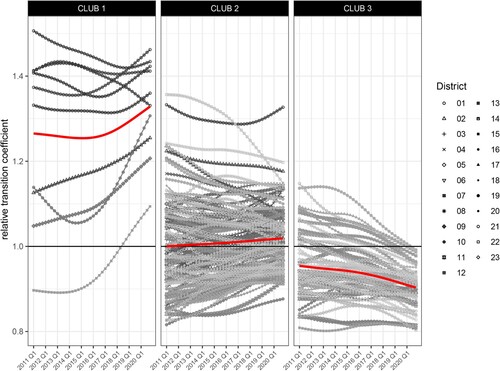

The first club with the highest rent price trajectory consists of only 10 subdistricts while the second club contains 122 subdistricts and the below average developing club has 58 subdistricts. Club 1 and Club 3 do have a positive convergence parameter, while Club 2 exhibits a insignificantly negative parameter. Using data smoothed with the boosted-HP filter, the allover picture stays the same, however, a small number of the units currently assigned to Club 3 move to Club 2 instead. The relative transition paths of each subdistrict's rents are plotted in . Note, that an up- or downward trend in the relative transition coefficient does not imply an absolute in- or decrease in the rent level but rather a change relative to the average level. The graphs clearly shows, that Club 1 is composed of two types of subdistricts. There are six initially high priced units all located in the city centre and four subdistricts with strong upgrading during the observation period. Club 2 and 3 both accommodate initially above average as well as below average units. However, Club 2 subdistricts move towards a slightly above average rent level while Club 3 subdistricts converge towards an below average level.

Figure 1. Relative transition paths of subdistricts by club. The thick red line shows clubs average transition path. Each line representing a subdistrict. Symbols indicate the district to which a subdistrict belongs.

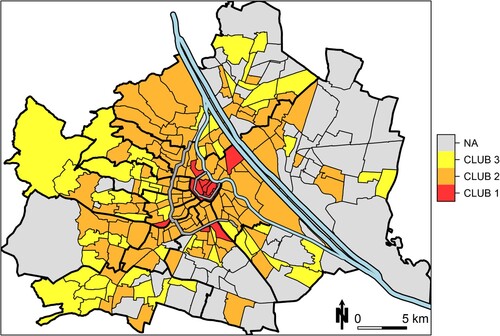

depicts the spatial distribution of the respective convergence clubs across Vienna. It becomes apparent that those subdistricts with the highest rent trajectory are mostly clustered centrally within the Ringstraße. Some are also located towards the south, their rise in rents is most likely associated to the opening of the new Viennese main station in 2012 and the ongoing upgrading of the Landstraße district. Another one can further be found in the ninth district and one is located in the fifteenth district just across the imperial Schönbrunn palace. Club 2 subdistricts are clustered around the aforementioned Ringstraße surrounding the city centre, up till the Gürtel which is usually perceived as the border between the inner and outer districts. Club 3 subdistricts are mostly found in the outer districts, however this area is much more heterogeneous. With the exception of the rather upper class districts of Währing and Döbling in the north-west, the share of Club 3 districts rises for increasingly peripheral locations.

Figure 2. Private rent price convergence clubs of Viennese subdistricts. Map also depicts the Danube (lightblue) and the Ringstraße as well as the Gürtel (darkgrey) as geographic references.

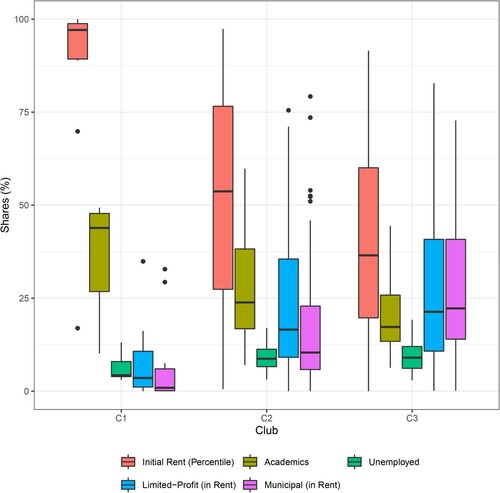

gives insight into the distribution of various variables within each convergence club for the base year 2011. One can observe that a higher price trajectory is associated with higher initial rent levels, but also a smaller share of municipal and LPHAs housing units within the rental sector. Taking a look at the socioeconomic structure of the subdistricts, it becomes apparent that more expensive Clubs tend to inhabit relatively more academics. Meanwhile, the relationship regarding unemployment is less clear with Club 1 subdistricts exhibiting the lowest and Club 2 the highest rates. This should give a first intuition about possible drivers of differences in rent price trajectories. However, in this paper I do not want to remain on a purely descriptive level but formally test the relationship between club membership and the composition of the local housing market, while also controlling for centrality and socioeconomic factors that might drive differences in club memberships. Therefore an ordered probit model is used, as described in Section 3.2. The first model specification starts with explaining club membership merely by initial housing market characteristics (M1). Then dummy variables are added indicating whether the subdistrict is located within the city centre or within the inner districts (M2). The model is then further expanded by controlling for variation in the initial rent level (M3). Last but not least, also the share of academics and unemployed is added as socioeconomic control variables (M4).

Figure 3. Subdistrict characteristics (2011).

reports the average marginal effects for all models and clubs. In M1 both social-housing variables are highly significant across clubs. On average, they clearly increase the probability of a subdistrict to follow a lower price trajectory and decrease the probability of a subdistrict to join Club 1 or 2. After controlling for location, the limited-profit housing coefficients keep their sign and stay significant in all cases. However, municipal housing coefficients turn insignificant across clubs. Also adding the log of initial rents as an explanatory variable does not change direction or significance of the two social housing coefficients across clubs. Somewhat surprisingly further adding socioeconomic control variables such as share of academics and unemployed dos not show a significant impact onto club membership. Adding the variables therefore does not significantly increase the goodness of fit compared to M3 as confirmed by Likelihood Ratio tests.

Table 2. Average marginal effects.

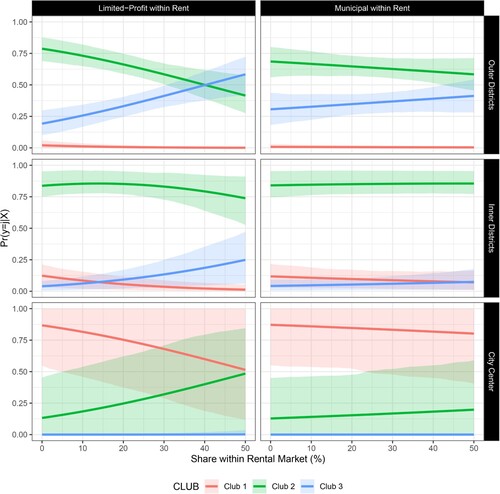

In addition to reporting the average marginal effects, the ordered probit model (M3) was used to predict conditional probabilities of club membership. This is done by evaluating the model outcomes varying one of the social housing variables at a time while holding the other variables at their respective mean. Furthermore, the investigation is conducted conditioning on either a location in an outer district, one of the inner districts or within the city centre.

The changes in probability can hereby be interpreted as the result of a redistribution from the private sector to the respective segment. The predicted probabilities along with their 95% prediction intervals are depicted in . If the share of LPHAs units within the rental market rises, one observes an substantial increase in probability of membership in Club 3 and a decrease in Club 2 membership if outside the city centre. For a subdistrict to have an expensive trajectory is highly unlikely, irrespective of the LPHAs share. For cases situated in the inner districts the impact onto both Club 1 and Club 2 membership is observed to be negative but again an increased probability of membership in Club 3 can be found. However, compared to the outer district cases the curves are much flatter, implying generally less impact and the medium price trajectory associated to Club 2 clearly remain the most likely scenario. In the city centre, Club 3 does not play a role, but higher shares of LPHAs now decrease the probability of Club 1 membership in favour of Club 2, which is again the less expensive trajectory in comparison. As findings for the city centre are based on very few observations they are not statistically significant. Hence, the corresponding effects should be interpreted with caution. Altogether, these findings imply a relevant impact onto the number of areas following lower rent price trajectories across the city. Similar relationships between clubs hold true if one takes a look at variations in the municipal share. However, the effects are much weaker in comparison across all three possible locations. These outcomes generally confirm the idea of a price dampening effect exerted by the LPHAs over the private rents. Higher shares of limited-profit sector supply within the local rental markets increase the probability of subdistrict membership in a convergence club with a lower price trajectory on the private market irrespectively of whether a subdistrict is placed in the city centre, the inner districts or the outer districts. Nonetheless, the expected effect is most notable in the outer districts. There is also a similar impact stemming from the municipal sector but of insignificant magnitude. Interestingly, both observations fit Kemeny's idea quite well. First, excess demand as clearly present in Vienna undermines the possibilities of a price dampening effect, as private landlords will have no difficulties finding tenants even when charging rents way above the social housing level. This sort of excess demand can be reasonably assumed to strongly diminish for more peripheral locations, thus strengthening the competition for tenants between private and social sectors. Second, the Municipal sector has stronger entry barriers compared to the limited-profit sector which limits the possibilities of competition with the private sector.

Figure 4. Probability of club memberships based on ordered probit model. Evaluated at the conditional mean of the currently non-varying variables. The range of the depicted x-axis are set in a way to ensure market shares add up to a maximum of 100 %. Shaded areas correspond to the 95% prediction interval based on bootstrapping.

5. Conclusion

Vienna has all of the main characteristics of Kemeny's integrated rental market and is possibly one of the last examples where the proclaimed price dampening effect of a large social housing sector onto private rents can be empirically tested. Although rents were strongly on the rise across the city in the observation period between 2011 and 2020, one should not get carried away looking at very recent price levels or changes to assess a potential price dampening effect. Instead, such an effect can be detected through lower private market rent trajectories over the medium to long run in those neighbourhoods with a higher social sector share in the rental market. The hypothesis of rent price convergence across the city is rejected using Phillips and Sul's Log-t convergence test. Instead, this paper finds three main convergence clubs with different price trajectories. By means of an ordered probit model, it can be shown that higher shares of limited-profit supply within the local rental market translate into significantly and substantially increased probabilities of a subdistrict's membership in a convergence club with a lower path of private rent development. This holds true for different possible locations within the city and controlling for various initial conditions that could also impact prices. Thus there indeed is a price dampening effect onto the development of private rents in Vienna stemming from the limited-profit sector.

Although the findings obtained in this study are very much in line with the theory, one major drawback is the underlying data quality. In the absence of administrative data on local rent developments, currently the only feasible option is using listings data which may or may not fulfil desired random sampling criteria. Although trying to circumvent these issues by means of more complex aggregation techniques, more robust data sources should be used to further test the given hypothesis once available. Thus future research in this field should focus on obtaining such data sources. Given the evidence available, there are nonetheless some learnings for housing policy. First, opening the social housing sector to a broader audience can indeed produce positive spillovers for those who do not receive accommodation there. This, of course requires the implementation of an appropriate regulatory framework with regard to entry barriers as well as an effective protection from rent seeking to actually generate at-cost rents in the limited-profit sector. Second, at least under certain conditions proximity indeed plays a role in generating a price dampening effect, therefore having building land availability for LPHAs at the right place is relevant. Hence, not only policy makers but also planners may contribute towards the success of an integrated rental market approach. Last but not least, even in a city with a huge social sector like Vienna, the expected impacts onto the private market vary considerably across locations and are by nature not targeted at the most vulnerably. Thus policies to enforce competition between social and private housing suppliers should also be coupled with other measures in order to achieve housing affordability for all tenants. Here, the municipal sector may play a crucial role. Although the analysis showed a comparatively low price dampening effect, it is still capable to offer the lowest rents on the market and target its supply towards more vulnerable groups. Thus the city of Vienna should by no means give up on municipal housing provision in favour of subsidising LPHAs, but perceive both sectors as complementary.

Policy makers in other cities or regions may also want to adopt similar models of rental market integration to achieve more affordable housing in their communities. Although the price dampening mechanisms outlined by Kemeny are rather general in their nature and thus theoretically also applicable to other cases, local context might play a crucial role in determining their respective potential to substantially support housing affordability. Due to its idiosyncrasies, empirical findings from the Viennese rental market may not be directly transferable to other cities or regions with different housing systems and regulatory settings. However, this can and should also be empirically tested in the future in order to enable policy makers and planners within different contexts to make informed decisions. Here, another more general learning from this paper should be mentioned: It is indeed possible to employ a quantitative empirical approach towards comparative and critical housing theories, which for various reasons are commonly not as much tested as their neoclassical counterparts. A lot could be gained if quantitative research does not limit itself to more formalized theories which are by design easier to test and vice versa all theoretical schools of thought within the field of housing research should be open to learn from empirical investigation.

Disclosure statement

No potential conflict of interest was reported by the author.

References

- Aalbers, M. B., & Holm, A. (2008). Privatising social housing in Europe: the cases of Amsterdam and Berlin. Urban Trends in Berlin and Amsterdam, 110, 12–23.

- Austrian National Bank. 2020, November 9. Oenb-fundamentalspreisindikator für wohnimmobilien. Retrieved from https://www.oenb.at/dam/jcr:f0e7bcc6-56ef-42c4-b2ba-d4c1ca46860c/Ergebnisse-des-OeNB-Fundamentalpreisindikators\2Q2020.xlsx.

- Barro, R. J., Sala-i Martin, X., Blanchard, O. J., & Hall, R. E. (1991). Convergence across states and regions. Brookings Papers on Economic Activity, 1991(1), 107–182.

- Bartkowska, M., & Riedl, A. (2012). Regional convergence clubs in Europe: identification and conditioning factors. Economic Modelling, 29(1), 22–31.

- Basel, S., Gopakumar, K., & Rao, R. P. (2020). Testing club convergence of economies by using a broad-based development index. GeoJournal, 86, 2351–2365.

- Bauer, E. (2006). Entwicklung der Wohnungskosten. Ursachen, lang- und kurzfristige Effekte, Auswirkungen. Kurswechsel (3) pp. 20–27.

- Blackwell, T., & Kohl, S. (2018). The origins of national housing finance systems: a comparative investigation into historical variations in mortgage finance regimes. Review of International Political Economy, 25(1), 49–74.

- Borg, I. (2015). Housing deprivation in Europe: on the role of rental tenure types. Housing, Theory and Society, 32(1), 73–93.

- Friesenecker, M., & Litschauer, K. (2022). Innovating social housing? Tracing the social in social housing construction. In Yuri Kazepov & Roland Verwiebe (Eds.), Vienna - still a just city? (pp. 68–82). New York: Routledge.

- Gelman, A., & Hill, J. (2009). Data analysis using regression and multilevel/hierarchical models (11). Cambridge: Cambridge University Press.

- Hatz, G., Kohlbacher, J., & Reeger, U. (2016). Socio-economic segregation in vienna: a social-oriented approach to Urban planning and housing. In T. Tammaru, M. van Ham, S. Marcińczak, and S. Musterd (Eds.), Socio-economic segregation in european capital cities: East meets west (pp. 104–133). London: Routledge.

- Hill, R. J. (2013). Hedonic price indexes for residential housing: a survey, evaluation and taxonomy. Journal of Economic Surveys, 27(5), 879–914.

- Hodrick, R. J., & Prescott, E. C. (1997). Postwar US business cycles: an empirical investigation. Journal of Money, Credit, and Banking, 29(1), 1–16.

- Hoekstra, J. (2009). Two types of rental system? An exploratory empirical test of Kemeny's rental system typology. Urban Studies, 46(1), 45–62.

- Hoekstra, J. (2020). Comparing local instead of national housing regimes? Towards international comparative housing research 2.0. Critical Housing Analysis, 7(1), 74–85.

- Kadi, J. (2015). Recommodifying housing in formerly ‘Red’ Vienna? Housing, Theory and Society, 32(3), 247–265.

- Kadi, J., & Verlič, M. (2019). Gentrifizierung am privaten Wiener Mietwohnungsmarkt. In J. Kadi and M. Verlič (Eds.), Gentrifizierung in wien (pp. 35–50). Vienna: Kammer für Arbeiter und Angestellte für Wien.

- Kemeny, J. (1995). From public housing to social market – rental policy strategies in comparative perspective. London: Routledge.

- Kemeny, J., Kersloot, J., & Thalmann, P. (2005). Non-profit housing influencing, leading and dominating the unitary rental market: three case studies. Housing Studies, 20(6), 855–872.

- Kolbe, J., Schulz, R., Wersing, M., & Werwatz, A. (2021). Real estate listings and their usefulness for hedonic regressions. Empirical Economics, 61(6), 3239–3269.

- Litschauer, K., & Friesenecker, M. (2022). Affordable housing for all? Challenging the legacy of red Vienna. In Yuri Kazepov & Roland Verwiebe (Eds.), Vienna - Still a just city? (pp. 53–67). New York: Routledge.

- Marquardt, S., & Glaser, D. (2020). How much state and how much market? Comparing social housing in Berlin and Vienna. German Politics, 1–20. doi:10.1080/09644008.2020.1771696.

- Matznetter, W. (2020). How and where non-profit rental markets survive–a reply to Stephens. Housing, Theory and Society, 37(5), 562–566.

- McKelvey, R. D., & Zavoina, W. (1975). A statistical model for the analysis of ordinal level dependent variables. Journal of Mathematical Sociology, 4(1), 103–120.

- Mundt, A. (2018). Privileged but challenged: The state of social housing in Austria in 2018. Critical Housing Analysis, 5(1), 12.

- Mundt, A., & Amann, W. (2010). Indicators of an integrated rental market in Austria. Housing Finance International, 25, 35–44.

- Phillips, P. C., & Shi, Z. (2021). Boosting: Why you can use the HP filter. International Economic Review, 62(2), 521–570.

- Phillips, P. C., & Sul, D. (2007). Transition modeling and econometric convergence tests. Econometrica, 75(6), 1771–1855.

- Phillips, P. C., & Sul, D. (2009). Economic transition and growth. Journal of Applied Econometrics, 24(7), 1153–1185.

- Reinprecht, C. (2014). Social housing in Austria. In Kathleen Scanlon, Christine Whitehead, & Melissa Fernández Arrigoitia (Eds.), Social Housing in Europe (pp. 61–73). Chichester: John Wiley & Sons, Ltd.

- Schneider, M. (2014). Ein Fundamentalpreisindikator für Wohnimmobilien für Wien und Gesamtösterreich. Österreichische Nationalbank, Hauptabteilung Volkswirtschaft, Abteilung für volkswirtschaftliche Analysen.

- Simons, H., & Tielkes, C. (2020, November 9). Wohnungsmarkt wien – eine wohnungspolitische analyse aus deutscher sicht. Retrieved from http://www.bid.info/wp-content/uploads/2020/01/Bericht\Wien\2019050endbericht-rev.pdf.

- Springler, E., & Wöhl, S. (2020). The financialization of the housing market in Austria and Ireland. In Stefanie Wöhl, Elisabeth Springler, Martin Pachel, & Bernhard Zeilinger (Eds.), The state of the european union (pp. 155–173). Wiesbaden: Springer VS.

- Statistik Austria. 2020a, November 30. Bevölkerung zu jahresbeginn 1952–2020 nach bundesland. Retrieved from http://www.statistik.at/webde/statistiken/menschen\und\gesellschaft/bevoelkerung/bevoelkerungsstand\und\veraenderung/bevoelkerung\zu\jahres-\quartalsanfang/031770.html.

- Statistik Austria. 2020b, November 9. Wohnen 2019, mikrozensus -wohnungserhebung und eu-silc. Retrieved from https://www.statistik.at/wcm/idc/idcplg?IdcService=GET\PDF\FILE\&dDocName=123361.

- Stephens, M. (2020a). How housing systems are changing and why: a critique of Kemeny's theory of housing regimes. Housing, Theory and Society, 37(5), 521–547.

- Stephens, M. (2020b). Towards a multi-layered housing regime framework: responses to commentators. Housing, Theory and Society, 37(5), 584–596.

- Tomal, M. (2021). Testing for overall and cluster convergence of housing rents using robust methodology: Evidence from Polish provincial capitals. Empirical Economics, 62(4), 2023–2055.