?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The paper extends geographical enquiry into the external urban relations described by central flow theory in an exploration of the roles of commercial office real estate (CORE) and advanced producer services (APS) as a conduit for inter-city flows of finance in corporate globalization. The analysis investigates and benchmarks the spatial overlap between these city-based service networks and uses this to consider how their respective servicing strategies influence international capital flows. We find that the networks are interlocked, as the connectivity in one network can significantly explain the connectivity in the other. Both CORE and APS services promote cross-border flows of finance. Cities providing multinational CORE and APS services are able to articulate direct as well as indirect inter-city capital flows and spillovers to non-service sectors.

Highlights

We extend geographical enquiry into external urban relations as central flow theory.

The interlocking between real estate and advanced producer services is investigated.

Spatially overlapped service networks articulate direct and indirect capital flows.

More central cities in the multi-service network attract more investment flows.

Inter-city service network capital flows can spill over to non-service sectors.

1. Introduction

Taylor, Hoyler, and Verbruggen (Citation2010) formulated central flow theory (CFT) to specify the increasingly crucial distinction between local and non-local urban relations in contemporary corporate globalization. Whereas Christaller’s (Citation1933/1966) central place theory (CPT) describes the local hinterland servicing relations of urban settlements, CFT seeks to describe the non-local relations of cities in line with what Capello (Citation2000) has termed the ‘city network paradigm’. CFT and CPT obviously do not speak to distinct urban universes. There is an emerging body of literature addressing the interconnections between the logics of place-based local (CPT) relations and inter-city flow-based non-local (CFT) relations. Scholvin, Breul, and Diez (Citation2019), for example, reconceptualized ‘gateway cities’ at the nexus of major cities’ global connectivity (CFT) and the interactions with their hinterlands (CPT). Meanwhile, Zhu, Pain, Derudder, and Taylor (Citation2022) explored CPT/CFT intersections in global city-regions by linking their multi-nodality with their positions in international capital investment flows.

While CPT has seen renewed interest in the past years (Van Meeteren & Poorthuis, Citation2018), there is a vibrant CFT literature devoted to analysing the non-local external relations of cities to inform understanding of urban relations under conditions of globalization (Derudder & Taylor, Citation2020; Sigler, Neal, & Martinus, Citation2023; Taylor et al., Citation2010). In this paper, we extend the latter literature by focusing on the role of ‘commercial office real estate’ (CORE) services provision in connecting cities transnationally. Calling to mind Massey’s (Citation2006, p. 64) ‘other geography – the “external geography” of a place that is especially important to a place like London’, CFT speaks to the archetypal ‘city-ness’ of an economic centre specializing in high-order business ‘advanced producer services’ (APS) with a ‘worldwide range’ (Zhu et al., Citation2022, p. 1). Reflecting the ‘massive trends towards spatial dispersion of economic activities’ and parallel ‘demand for new forms of territorial centralization of top-level management and control operations’ (Sassen, Citation2002, p. 3), a complex of city external relations has been generated by APS firms constituting strategic networks (Castells, Citation1996, p. 409). The global networks of APS offices in banking and finance, law, accountancy, advertising, and management consultancy firms providing expert advice and services to companies and governments worldwide, generate knowledge and facilitate the intercity flows of information and finance theorized by Castells (Citation1996, p. 408) as constituting a ‘space of flows’ in a ‘network society’. Cities with a functional specialization in multinational APS are embedded in these transnational networks and are thereby ‘interconnected with each other through decision-making and finance’ (Friedmann & Wolff, Citation1982, p. 2), and this has been the basis of much of the research carried out under the umbrella of the Globalization and World Cities (GaWC) research network.

CORE has special significance for the operations of multinational APS in an era defined by the simultaneous dispersion and centralization of economic activity. The supply of commercial office property in a city ‘brings together the economic agents that globalize urban space’ (Pain, Citation2018, p. 371), and it transforms locally fixed physical space into a liquid ‘quasi-financial’, tradeable asset (Coakley, Citation1984, p. 697). Information and communication technology (ICT) assisted integration and globalization of international finance and CORE markets since the late twentieth century has been instrumental in ‘building’ cities with a worldwide range and the financialization of those cities (Baum, Citation2008). CORE serves a dual role in grounding APS in the physical ‘space of places’ of such cities and in the spaces of flows of the transnational financial networks in which they are embedded (Castells, Citation1996, p. 409). In Towers of Capital (2009), Lizieri set out the thesis that CORE (as a localized city physical resource and a channel for international flows of finance) and APS (as CORE multinational occupiers and investors), are ‘interlocked’. The hypothetical interlocking process is an outcome of ‘occupational markets (functionally specialized in financial services activities), investment markets (through acquisition of offices), supply markets (both through demand drivers and the supply of finance for development), and real estate finance (through property as collateral for lending)’ (Lizieri & Pain, Citation2014, p. 440), Intuitively, this interlocking of financialized CORE and multinational APS would seem to render the local and non-local external relations of cities complementary and suggest their geographies could converge spatially.

Castells (Citation1996, pp. 409–410) referred to real estate services as one of the advanced services contributing to information flows interlinking global cities. Real estate is argued to also have an increasingly powerful role in the circulation and accumulation of financial capital, ‘especially in an economy that is transforming structurally with most of the growth coming from the service sector’ (Pain, Citation2018, p. 370). But while much attention has been devoted to studying APS office networks for more than two decades, the spatial conjunction of CORE services and APS, and their respective influences on non-local international capital flows, have lacked intensive study. The dispersion of CORE services provided through international office networks has lagged that of APS firms (Jones & Trevillion, Citation2022, p. 177). Nonetheless, major CORE firms such as Cushman and Wakefield and CBRE, which began their operations in Chicago and San Francisco respectively, now also have offices in cities across the Americas, Asia-Pacific, Europe and Middle East and Africa. If the office locations of CORE map onto those of APS, the CORE network could be argued to be interlocked with the APS network.

This paper extends the investigation into the external relations of cities through an exploration of the role of APS and CORE services as interlocked, and as a conduit for inter-city flows of finance. Accordingly, our analysis sets out to address two main research questions: Are the city offices of APS and CORE services spatially interlocked? And how do their respective multinational office network servicing strategies influence international capital flows? We first examine the spatial overlap between APS and CORE service connectivity and the determinants of the importance of their respective presences in different cities. Second, we consider whether APS and CORE service network connectivity, respectively, influence cross-border capital flows. The novel contribution of the paper is that the results go beyond the original focus of CFT on explaining external city relations generated by APS provision. It provides the empirical evidence on the external relations of cities described by CFT by putting a spotlight on the potential role of CORE services provision as a co-agent with APS in directing capital flows in an interlinked transnational network of cities.

The paper begins with a review of academic perspectives on the relationship between CORE and APS city network relations and international finance and how we plan to take this understanding forward. The data for our new analyses are then described leading to the main section presenting our analyses consisting of two models, one showing relations between APS and CORE networks and the second adding investments flows. These empirical analyses are subject to two limitations: (i) we use only cities in OECD countries because we only have the data for necessary control variables in our models from this data source, and (ii) all our data are for 2020 when the Covid-19 pandemic seriously affected the world economy and world cities particularly. The effects of these on the analyses are dealt with in the discussion of our results. In the conclusion we summarize our original contribution to the literature and provide pointers towards research questions for further study.

2. Commercial office real estate, advanced producer services, city external relations and international finance

The dual process of the simultaneous dispersion and centralization of APS described by Sassen (Citation1991/2001) is the starting point for understanding the specific role played by CORE in generating non-local external relations between cities and international capital flows. There is broad academic agreement that the networks of APS have come to be of increasing importance in operationalizing the twenty first century world system of financial flows (Allen, Citation2010; Wojcik, Citation2018). Recent theoretical and empirical research corroborates the centrality of APS firms for the spatial organization of international capital. Bassens and van Meeteren (Citation2015), for example, showed that a series of global cities remain an obligatory passage point for the relatively assured realization of international capital, not least because it has become the geographical backbone for the insertion of finance capital (logics) in contemporary economies and societies. Boussebaa and Faulconbridge (Citation2019) pointed out that APS firms are increasingly active participants in the shaping of economic globalization. Lizieri’s (Citation2009) analysis of the interrelationship between CORE as a physical and financial asset and APS in international financial centres provides the foundation for understanding that a critical mass of city commercial office stock has proved essential for the insertion of cities in the world economy and their exposure to risk in times of global financial crisis (Lizieri & Pain, Citation2014). Through the supply of property finance and the occupation of and investment in CORE markets by APS, mobile finance capital is ‘grounded’ in cities: ‘firms that occupy space are the same firms that acquire offices as investment assets and which provide finance for the creation of new office space’ (Lizieri & Pain, Citation2014, p. 440).

Drawing on insights of Sassen (Citation1991/2001), Castells (Citation1996) and antecedent ‘world cities’ theorists such as Hall (Citation1966) and Friedmann (Citation1986), academics of the Globalization and World City (GaWC) research network have surveyed the non-local external relations of cities generated by APS ‘network enterprises’ within the world economic system since the year 2000 (Taylor, Citation2001, Citation2004). Data gathering on the city locations, staff sizes and functions of offices providing APS worldwide, has allowed empirical specification of the connectivity of cities in a ‘world city network’ (Derudder & Taylor, Citation2020; Taylor, Citation2001, Citation2004). However, missing in these analyses are the spatial dimensions of the CORE service provision that accommodates transnational APS activities and mediates capital flows in the world city network. As highlighted by Lizieri and Pain (Citation2014, p. 440):

Analysis of the interconnectedness of ‘global’ cities conferred by international office networks – as exemplified by the Globalization and World Cities (GaWC) research network and others – emphasizes the space of flows. But real estate is a physical manifestation of the nodes of that network of cities and a conduit for flows of finance: it stores and locks down value. It provides the infrastructure for the global city production process.

Empirical studies have observed that direct international real estate office investments remain focused on a relatively small number of ‘core economy’ major world cities specified by Friedmann (Citation1986) and Sassen (Citation1991/2001) (Lizieri & Pain, Citation2015; Sirmans & Worzala, Citation2003). Given strong quantitative evidence of superior real estate returns performance in some regional secondary markets, ongoing investment concentration has been interpreted as mimetic, irrational behaviour reflecting investor ‘sentiment’ or market ‘familiarity’ (Henneberry & Mouzakis, Citation2014). Evidence from interviews with international fund managers in a study for the Urban Land Institute found that investment interest in OECD emerging markets is growing (Pain et al., Citation2018), illustrating the commoditization and ‘worlding’ of urban spaces through CORE foreign inward investment, which diversifies and ‘filters away’ investor risk (Halbert & Rouanet, Citation2014; Knox & Pain, Citation2010; Roy & Ong, Citation2011). However, the role of CORE in enabling the operationalization of indirect financial flows realized by APS, and potential ‘capital switching’ between built environment and production capital circuits (Harvey, Citation1985), has not been analysed. In addition to direct CORE capital flows, myriad other inter-city flows of finance are brokered by APS in CORE office networks. Contemporaneous surges in cross-border CORE direct capital flows (supported by CORE services) and in trade and foreign direct investment (FDI) flows (supported by APS), are likely related.

In The Production of Space (Citation1974/1991, pp. 26–27), Lefebvre conceived that dependent on ‘the energy deployed within it’ space has assumed ‘a reality’ much like commodities, money, and capital. However, the sources of this energy ‘along with the physical relationships between central points, nuclei or condensations on the one hand and peripheries on the other hand are still matters for conjecture’ (Citation1974/1991, p. 13). CORE services that physically transform and financialize urban space represent such an energy, yet attention to their deployment is missing from published city network analysis. Derudder (Citation2021) called for abstract ‘alleged’ inter-city relations mapped in city network analysis to be permanently appraised on the basis of evidence of ‘actual capital’. Zhu et al. (Citation2022) shifted CFT analysis to actual FDI capital flows between cities specializing in APS provision. Other studies have explored CORE transaction inter-city direct capital flows (Hoyler et al., Citation2014; Lizieri & Pain, Citation2015; Pain et al., Citation2018). However, the complex interdependencies between global cities and cross-border flows remain ‘a grey area, in need of empirical analysis’ (Lizieri & Pain, Citation2014, p. 441). The long overlooked spatial relationship between CORE and APS city servicing and their influence on city network financial flows, is the subject for empirical analysis in the next section of this paper.

FDI is often conceived as indicative of inward investment into cities associated with boosting high-value knowledge, skills, innovation, local economic growth and positive regional spillover effects in a territorially competitive context (Branstetter, Citation2006; De Mello, Citation1999; Madriaga & Poncet, Citation2007). FDI also signifies complex external relations and flows between cities associated with office-based commercial firms doing cross-border business (Borensztein, De Gregorio, & Lee, Citation1998). For example, Rocco and van Ness (Citation2005, p. 1) contended that increasing FDI in APS operating worldwide ‘is the most dynamic and potentially powerful factor for urban change in an increasingly globalized economy’, reflecting that APS are the ‘main economic connectors’ between global cities (Sassen, Citation1991/2001, Citation1994/2000). Mergers and acquisitions (M&A) deals have also become regarded as strong evidence for external relations associated with direct capital flows between cities, the formation of long-term, value-adding interactions between city office-based firms, and network capital (Cartwright & Shoenberg, Citation2006; Collins, Holcomb, Certo, Hitt, & Lester, Citation2009; Rodríguez-Pose & Zademach, Citation2003; Zademach & Rodríguez-Pose, Citation2009). In our analysis, we focus on a database comprised of FDI and M&A deals to represent cross-border inter-city capital flows associated with multinational APS which we speculate may be facilitated by increasingly multinational CORE services.

3. Data

Our data set comprises statistics collected from sources in three different areas: on corporate services within and between cities from the Globalization and World Cities (GaWC) data; on cross-border FDI flow data from the Financial Times fDi Markets database and the Zephyr database; and on macro-economic variables for cities from the OECD database and the World Bank database. Starting with the GaWC 2020 roster of 167 leading world cities and merging this with the other two data sources results in an operational roster of 143 cities in our dataset (see Appendix 2).

The GaWC data are based upon information collected on the distribution of service values – standardized measures of the importance of office presences – of major firms that provide key services for corporate globalization in 2020.Footnote1 There are two groups: (i) 175 advanced producer (APS) service firms (75 in financial services and 25 each in accountancy, advertising, law, and management consultancy) and (ii) 22 commercial office real estate (CORE) services firms.Footnote2 Compared to the widely used APS network data, the CORE service network data is new. It includes two major provider categories. First, investment banks and financial institutions offering real estate brokerage services that benefit from corporate finance and capital markets expertise. Second, integrated multi-service real estate agencies offering property owners, investors and occupiers, strategic advice and execution for a wide range of support needs (such as property sales and leasing, corporate services, property, facilities and project management, mortgage banking, appraisal and valuation, development services, investment management, and research and consulting services). Property companies and REITs also offer real estate investment advice and products to institutional, private and government investors internationally, however we do not include these providers in the present analysis due to their generally limited multinational networks of offices. The analysis cannot claim to fully disentangle the ‘unimaginable complexity’ of the network relations between economic actors mediating the ‘blizzard of transactions’ generating direct CORE and indirect finance capital flows (Thrift, Citation1999, pp. 272–274). Rather, its purpose is to provide a preliminary exploration of spatial relations between specialized APS and CORE services, and their role as a conduit for inter-city flows of finance.

These data, including both CORE and APS data, are derived from investigation of a firm’s office networks resulting in evaluations of the importance of cities in the work of the firm. Assigning these service values involved a standardization of multifarious information across firms’ networks values to arrive at a scale ranging from 0 to 5 as follows (Derudder & Taylor, Citation2018). The city housing a firm’s headquarters was scored 5, a city with no office of that firm was scored 0. An ‘ordinary’ or ‘typical’ office of the firm resulted in a city scoring 2. With something missing (e.g. no partners in a law office), the score reduced to 1. Particularly large offices were scored 3 and those with important extra-territorial functions such as regional headquarters were scored 4. Two variables are derived from these data. First, the sum of the service values in a city measures the agglomeration of work in the two service groups. Second, by using an interlocking network model the connectivity of a city to other cities is computed. Through carrying out these measurement exercises for the two different groups of corporate service firms, we are able to explore the city servicing values generated, on the one hand, by APS firms that are both occupiers of city office space and institutional investors in office assets and, on the other hand, by commercial real estate firms which service the office occupancy and investment needs of those APS. The service values are thus a proxy for the non-local, urban external relations between cities associated with the special interlocking role played by commercial real estate as a physical and financial asset, and as a service supplier supporting contemporary corporate globalization.

In order to consider whether APS connectivity and real estate connectivity influence actual cross-border investment flows between cities we use cross-border FDI flow data that are collected from two sources: the Financial Times fDi Markets database for greenfield investment flow data and the Zephyr database for cross-border M&A flow data. We merge the two databases based on the name of city and country and aggregate the total cross-border direct investment flows across cities in 2020.

The final step in the data collection is to measure four control variables, specific macro-economic features of cities that can influence relationships between service and financial flows in our modelling. Using the OECD database, a set of four macro-economic variables for both source and destination cities have been selected: a city’s unemployment rate, its share of city GDP with respect to country GDP, its income per capita, and population density. After removing missing data on income and other economic variables, our sample is reduced from 167 cities to 143 cities.Footnote3 The summary statistics are reported in . There were on average 7.77 million USD FDI flows between the 143 cities in 2020.

Table 1. Summary statistics.

To illustrate the relationship between FDI flows on the one hand, and APS and CORE connectivity on the other hand, we calculate the overall centrality of APS, CORE, and FDI for the 143 cities. First, based on the service values, we follow Taylor (Citation2001) and calculate the APS connectivity between each pair of cities:

(1)

(1) where

represents the APS connectivity between cities i and j and

denotes the service value of APS firm p in city i. As shown in , the maximum inter-city connectivity is between New York and London (1596), while the average inter-city connectivity across our sample is 63. Similarly, we calculate the CORE connectivity between each pair of cities:

(2)

(2) where

represents the CORE connectivity between cities i and j and

denotes the service value of CORE firm p in city i. The maximum inter-city CORE connectivity is also between London and New York (161) and the average CORE connectivity is 7.

Second, we calculate the APS and CORE centralities – which are akin to the notion of degree centrality in social network analysis – as the sum of connectivity of a city with respect to all other cities:

(3)

(3)

(4)

(4)

As shown in , London has the highest APS connectivity with respect to all other cities (47,181), followed by New York (41,591). For CORE centrality, London also has the largest connectivity with respect to all other cities (4892).

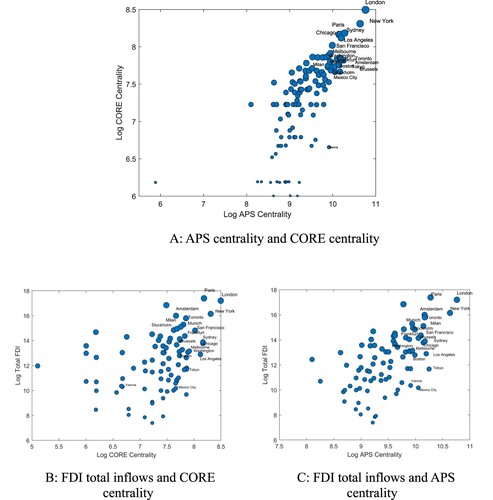

Figure 1. APS centrality, CORE centrality, and FDI total inflows.

Notes: (A) shows the relation between CORE and APS centrality. (B) illustrates the relation between CORE centrality and FDI total inflows, and (C) illustrates the relation between APS centrality and FDI total inflows. Cities with zero CORE centrality or zero FDI total inflows are not illustrated in the graphs. We show the name of the 20 cities with the highest APS centrality in our sample with none-zero CORE centrality.

The total inflow FDI for each city from all other cities is measured as follows:

(5)

(5) where

represents the total direct investment inflows from city j into city i. As shown in , FDI inflows, CORE connectivity, and APS connectivity are positively correlated. The correlation coefficient between APS and CORE connectivity is 0.65: cities that are more connected to the APS network are also more likely to be connected via the CORE network. The correlation coefficient between the total FDI inflows and APS connectivity centrality is 0.55: cities that are more connected in the APS network are more likely to attract foreign capital, as illustrated in . The correlation coefficient between the total FDI inflows and CORE connectivity centrality is slightly lower, but still amounts to 0.36.

4. Analysis

To study the relationship between APS services, CORE services, and capital flows, we performed two analyses. In the first analysis, we investigate the overlap between APS service connectivity and CORE service connectivity. The second analysis studies how APS connectivity and CORE connectivity influence cross-border investment flows.

4.1. Interlocking of APS and CORE service network

We apply a gravity-type model estimated by a Generalized linear model with a Poisson distribution:

(6)

(6)

(7)

(7) where Equation (6) estimates the determinants of APS service connectivity between city i and j

, and Equation (7) focuses on CORE service connectivity between city i and j

.

(

) captures the impact of the CORE (APS) service connectivity on APS (CORE) service connectivity. We consider two categories of control variables: (1) factors associated with transaction costs due to information asymmetry (Jandik & Kali, Citation2009); and (2) local urbanization and economic fundamental variables (Jacobs, Koster, & Hall, Citation2011). The first group of factors is represented by

, which measures the ‘distance’ between cities i and j. We use two proxies: having the same legal system and the geographic distance between the two cities.

and

are a vector of coefficients of

for APS connectivity and CORE connectivity, respectively. City-level push and pull factors

and

are used for the second group of factors. The economic variables include the unemployment rate of the two cities, the share of city GDP in national GDP, income per capita, and population density.

,

,

and

are the corresponding coefficients. To account for institutional factors, we also include country dummies (

).

and

denote the error term in equations (6) and (7), respectively.

As shown in , CORE service connectivity is interlocked with APS connectivity. A one percentage increase in APS connectivity is associated with a 0.69 percentage increase in CORE connectivity, while a one percentage increase in CORE connectivity is associated with a 0.25 percentage increase in APS connectivity. On the one hand, CORE provides spaces to accommodate high skilled labour pools and innovation clusters in globalized cities (Florida, Adler, & Mellander, Citation2017; Glaeser & Saiz, Citation2003; Sassen, Citation1994/2000). On the other hand, CORE firms may also locate close to their customers (APS firms) (Pain, Citation2018). As a result, there is an ‘interlocking’ between APS location drivers and office occupation (Hoyler et al., Citation2014; Pain et al., Citation2018). Interestingly, the elasticity of APS connectivity on the CORE connectivity is more than two times larger than vice versa. This may indicate the importance of the APS locations to the location choice of CORE firms. Co-location theory (that CORE firms locate close to their customers) may play a more critical role in explaining the interlocking of the two flows. This quantitative finding corroborates qualitative evidence from interviews with senior real estate actors reported by Pain et al. (Citation2020) that there is a recursive relationship between real estate business strategies and the location and agglomeration dynamics of global financial and linked business services. Quantitative analysis in the same study demonstrated a strong association between GaWC city APS connectivity and the commercial real estate capital flows and returns on investment that are operationalized by CORE service firms, inferring a functional rationale for the spatial convergence between APS commercial office occupation, institutional investment, and CORE servicing strategies.

Table 2. Gravity model for the CORE and APS firm connectivity among 143 OECD cities.

Moreover, we find that having the same legal system increases APS connectivity, consistent with the previous finding that reduced uncertainty and information asymmetry on legal issues can facilitate the international intra-firm transfer of labour, knowledge, and capital (Zhu et al., Citation2022; Zhu & Lizieri, Citation2021). For physical distance, we can see that APS connectivity increases with the decrease in distance. However, we also find that CORE connectivity is significantly positively related to geographic distance. This can be explained by the fact that the location choice of CORE firms largely depends on the location of APS firms, and the first choice of the international real estate firms is always the global city, which may be on different continents. The positive impact of geographic distance on CORE connectivity indicates that the transfer of knowledge, labour, and capital can overcome the restrictions imposed by geographic distance. The contrasting effects of geographic distance on APS and CORE connectivity can be attributed to the sparser distribution of CORE firms compared to APS firms. Transnational real estate firms tend to concentrate their operations in the most influential gateway cities across continents and in the most significant countries. In comparison to APS firms, CORE firms offer fewer service values within each country or continent. The sparser distribution of the CORE network is also influenced by the fact that CORE represents only one subsector. In contrast, APS connectivity is based on 175 firms from five subsectors, including financial services, accountancy, advertising, law, and management consultancy. The co-location of firms across these five subsectors, such as financial service firms co-locating with accountancy firms, leads to a higher concentration of APS firms within a country. However, despite the real estate sector having a smaller number of firms compared to APS sectors, real estate firms still provide space for the majority of APS firms, which is confirmed by our sub-sector analysis in Appendix 6.

We can also see that APS and CORE connectivity is built between cities with better economic conditions, including lower unemployment rates, higher GDP share, and higher income. Interestingly, we can see that the coefficient of population density for cities i and j exhibits an opposite sign in both APS and CORE equations, indicating that APS and CORE connectivity tends to be built between cities with different levels of population density. Since the connectivity is symmetric, we are not able to distinguish the destination and source cities. Nevertheless, population density can be identified as a push and pull factor in the city network, as shown by Zhu et al. (Citation2022). Pain et al. (Citation2020) also found that urban density, especially urban hard density, is significantly correlated with office returns performance at a city level and therefore shows relevance for the distribution of office investment flows within the two cities.

4.2. Interlocking of APS network, CORE network, and investment flows

Given the problem with many zero capital flows between cities, the ordinary least squares method may be biased and inconsistent (Brodzicki & Uminski, Citation2018). Therefore, we use a zero-inflated Poisson regression with clustered standard errors.Footnote4 The zero-inflated Poisson (ZIP) model mixes two zero-generating processes: the process of generating zeros (Equation 8) and the process of a Poisson distribution that generates counts, some of which may be zero (Equation 9):

(8)

(8)

(9)

(9) where

is the cross-border capital flows between city i and j.

captures the excess zeros, which cannot be predicted by the Poisson equation. To estimate the relationship between APS and flows, we use a logit model, which predicts the probability of excess zeros in the dependent variable (

, Equation 10) and a Poisson count model, which predicts the non-zero values in the dependent variable (

, Equation 11):

(10)

(10)

(11)

(11) where

,

are APS and CORE firm connectivity between city i and j, respectively.

,

, and

are defined as in section 3.1. To account for institutional factors, we also include country dummies (

).Footnote5 Considering the fact that investment flows are path dependent, we include the lagged investment flows between city i and j. Because our baseline model is for 2020, we use the capital flow in 2018 as the lagged investment flows. Previous literature on the impact of language, institutional and regulatory differences suggests that geographic proximity is an important ingredient in international portfolio allocation decisions as it reduces the cost of obtaining information about foreign markets (Blonigen & Piger, Citation2014; Hyun & Kim, Citation2010; Tesar & Werner, Citation1995). The unemployment rate, GDP share of the country, income, population, and population density represent the fundamental economic situation in the destination and source cities, which are also considered important long-term factors for cross-border investments (Hyun & Kim, Citation2010).

The results are reported in . Column 1 includes only APS connectivity, Column 2 focuses on CORE connectivity, and Column 3 shows the results based on APS, CORE connectivity, and the interaction between APS and CORE networks. As reported in , Column 1, we find a significant positive relationship between APS connectivity and cross-border investment flows in the Poisson count model, confirming the assumption that the shared presence of an organization in any pair of cities presents the potential for inter-city interaction. A one percentage increase in APS connectivity is associated with a 0.86 percentage increase in capital flows. This is consistent with the previous finding by Zhu et al. (Citation2022) that capital flows can be mapped to APS connectivity. For the zero-inflation part, APS connectivity can significantly reduce the probability of having zero inter-city investment flows. The marginal effect of a one percentage increase in APS connectivity on the probability of zero cross-border capital flow, ranges from – 0.30% to zero.Footnote6 Overall, these findings confirm that APS can be regarded as a source ‘to mobilize city space as an arena both for market-oriented economic growth and for elite consumption practices’ (Brenner & Theodore, Citation2002, p. 21; cited by Lizieri, Citation2009, p. 117).

Table 3. Gravity model for foreign investment flows among 143 OECD cities.

If we include only CORE connectivity, as shown in Column 2, we find that cross-border investment flows are significantly positively related to CORE connectivity. A one percentage increase in CORE connectivity is associated with a 0.56 percentage increase in capital flows. For the zero-inflation part, a one percent increase in CORE connectivity decreases the probability of having zero cross-border capital flows with a range from – 0.12% to zero. These results confirm that the physical infrastructures of cities also play a role in ‘locking down’ cross-border capital flows (Lizieri, Citation2009). Although the impact on the non-zero investment flows is similar, APS connectivity reduces the probability of zero investment flows more than two-fold compared to CORE connectivity. This further confirms the more important role of APS in interlocking capital flows than CORE. The coefficients of other control variables remain quite robust when using APS connectivity as the key variable.

However, when the interaction variable is added, the APS and CORE connectivity coefficient becomes insignificant (, Column 3). Instead, the interaction of APS and CORE connectivity can significantly positively explain the amount of capital flows between cities and reduce the likelihood of zero capital flows between cities. A one percent increase in the interaction of APS and CORE connectivity leads to 0.18 percent increase in the capital flows. This indicates the synergy of CORE and APS connectivity: CORE and APS networks interact with each other and attract flows of investment capital. The effects are stronger when the cities are connected both by APS and CORE networks. Moreover, the results for the zero-inflation part indicate that the interaction of APS and CORE reduces the likelihood of zero capital flow between cities. The marginal effect ranges from – 0.05% to zero in Column 3. This further confirms the synergy effect of the CORE and APS networks on the capital flows. The coefficient for APS connectivity remains significantly negative in the zero-inflation part, but the coefficient for CORE connectivity becomes positive. The change in the significance of the coefficient for CORE and APS connectivity when both are included in the regression, can partly be explained by the high correlation between APS and CORE connectivity. Overall, the results indicate that the presence of both APS and CORE networks escalates investment flows.

Apart from that, cross-border investment flows increase with a shorter geographic distance, higher income in both destination and source cities, and a higher population density in the source city. A shorter geographic distance and the same legal system also reduce the probability of zero investment flows between two cities. Better economic conditions, including higher GDP share and a higher population density in the source city, as well as higher income in both source and destination cities, can reduce the likelihood of zero investment flows. Moreover, previous capital flows also reduce the likelihood of zero capital flows, which confirms the path dependence of the capital flows. Investments tend to happen between cities that already share offices. Furthermore, the BIC corrected Vuong Non-Nested test statistic is significant at the 1% level, confirming that adding the zero-inflation part can significantly improve the model’s fit.

5. Discussion and limitations

While increasing FDI can promote a better APS network and CORE network between cities, our goal in this paper is not to identify any directional causal effect. The interlocking model indicates that the APS network, CORE network, and capital flows are interconnected. This is also supported by Appendix 3 and 4. As shown in Appendix 3, the capital flow in 2018 significantly explains the APS connectivity and CORE connectivity. As shown in Appendix 4, the interaction of APS and CORE in 2018 can reduce the probability of zero capital flows in 2020 and increase the capital flows in 2020. This further confirms the interlocking nature of APS, CORE connectivity, and capital flows.

Our results illustrate the logic and impetus behind state territorial strategies to ‘world’ cities in the era of ‘capitalist globalization’ (Roy & Ong, Citation2011; Sklair, Citation2006). The proportion of foreign direct investments coming from the advanced services sector (over 80%) can explain competition between governments to attract APS firms to their primary economic centres. But London’s high APS network connectivity to cities worldwide (4892), endorses extant research illustrating that urban external relations are complementary when it comes to service economy commercial activity (Hoyler & Pain, Citation2001). The capacity of the interaction between APS and CORE to increase capital flows suggests that governments should consider how local economic development objectives can best be supported by policies that take the wider network links of cities into account. Since connectivity in APS and CORE service networks and FDI inflows are positively correlated, encouraging investments in CORE material and communications infrastructures is likely to be a priority for the realization of local economic growth and capital spillovers to other cities and sectors.

We acknowledge that our analyses are subject to several limitations. First, our analysis provides quantitative proof of the interlocking of APS, CORE, and investment flows, which supports the argument that both serve as the conduit for inter-city financial flows. CFT can also be applied to both the APS and the CORE sectors and can be used to explain the co-evolution of capital flows and office real estate and APS networks. However, we are not able to completely tease out all confounding factors, as we can only perform cross-sectional analysis due to the CORE connectivity data restriction in this paper. To test if our model over-estimates the effect we include the lead-lag relation in equations (6), (7), (10), (11). In the dependent variable, we consider the APS and CORE connectivity in the year 2018.Footnote7 The results are reported in Appendix 3 and 4. The results remain qualitatively robust. APS connectivity can promote CORE connectivity and vice versa. Capital flow can significantly explain the APS connectivity but not the CORE network. Moreover, the interaction of the APS and CORE networks facilitates capital flows significantly. The presence of both APS and CORE networks escalates investment flows. The coefficients are smaller in size, which may be attributed to the quality of the real estate service value data. Nevertheless, the results further confirm the interlocking of APS, CORE, and investment flow networks.

However, we acknowledge that the city-level analysis cannot provide much detail on the complex network of actors providing CORE investment services. The CORE network is integral to the APS network but also goes beyond the APS data to include niche financial institutions, REITs, and other service providers that influence inter-city capital flows but lack a global network of offices. As a result, based on a cross-sectional city-level analysis, it is difficult to identify the causal relationship between APS and CORE networks, and the predominant channel that drives financial flows.

Second, our sample only includes the 143 cities with the largest economic size in the 33 OECD cities. Importantly, this means we are only studying part of the world economy empirically, what we might call the capitalist ‘global West’, excluding key Chinese cities in globalization as well as large cities from poorer countries. As a result, our analysis is biased towards selected large economies and world cities with a high level of city infrastructure and APS service values, in other words, cities more likely to attract investment flows according to a large urban studies literature. The impact of APS and CORE connectivity on investment flows for emerging economies beyond the OECD and non-global cities, deserves investigation and can have policy relevance for understanding evolving global urban conditions, but is left for future studies. Further qualitative research is required to gain an understanding of how the routing of capital between central points and peripheries in city networks (Lefebvre, Citation1974/1991, pp. 26–27), is determined by APS and CORE day-to-day service practices.

Third, the real estate service value data are available for the year 2020. Therefore, we chose 2020 as our sample period. We acknowledge that in 2020 when our survey was conducted, many cities were suffering from reduced office working due to the imposition of Covid-19 lockdown policies and working from home. Since commercial office real estate is the physical infrastructure necessary for economic activities to operate, ‘it articulates, and is subject to, its systemic capital investment flows’ (Lizieri & Pain, Citation2014, p. 441), our results may be expected to under-represent pre-pandemic interlocking of city office occupation and inter-city capital flows. The Real Capital Analytics Top Global Investment Brokers 2020 analysis found that in 2020, worldwide commercial real estate sales fell to the lowest level since 2013 due to pandemic disruption to normal ways of doing business and economic activity (https://www.rcanalytics.com/2020-global-broker-rankings/). As Lizieri and Pain (Citation2014) noted, in a financial crisis, real estate investment in global cities gives rise to systemic risk due to the locking together of the international financial system and the cities that are hosts to firms coordinating the system. The impacts are likely to be felt most in the world’s most globalized cities. Therefore, using the 2020 data as our sample can also be expected to under-represent the pre-pandemic influence of commercial real estate on international capital flows.

6. Conclusions

Adopting a CFT lens in this paper we studied the spatial overlap between city-based APS and CORE services activities in the year 2020 and benchmarked how their respective transnational servicing strategies influence international capital flows. Although the interlocking of APS firm spatial locations and cross-border capital flows has been investigated in previous literature (Zhu et al., Citation2022), the interlocking between CORE and APS services, as well as capital flows, had not been studied. Developing the arguments of Lizieri (Citation2009), we suggest CORE services are a specific kind of APS that also facilitate the inter-scalar relations of cities and secondary inter-city flows of capital. This paper thus helps address the dearth of empirical evidence on the relationship between the CORE service network, the APS service network, and international investment flows.

Based on a comprehensive database of cross-border investment flows at the city level which includes both greenfield investment and M&A across 143 OECD cities, we find that CORE and APS network activities can be mapped to each other. In addition, the presence of both networks can promote cross-border investment flows, even during the 2020 pandemic. Being involved in APS and CORE transnational networks can escalate the inter-city capital flows and reduce the likelihood of zero inter-city capital flows. APS, CORE and investment flows are interlocked with each other. Relevant for urban policy, cities that are more central to the APS and CORE network attract more investment flows. The impact of the CORE network can spill over to other non-service sectors.

Our analysis advances inquiry into ‘alleged’ inter-city relations studied in city network analysis (Derudder, Citation2021). The results go beyond extant studies seeking evidence of ‘actual’ world city network direct property finance capital flows on the one hand or FDI flows on the other hand. The spatial conjunction between APS and CORE services provision identified along with their influence on capital flows, provides insight into city external relations as more than an abstract concept. The geography of APS and CORE service network provision, evokes Bassens and van Meeteren’s (Citation2015) description of a series of global cities as constituting an obligatory passage point and ‘backbone’ for the realization of international capital in contemporary globalization. Cities providing multinational CORE as well as APS services are able to articulate direct and indirect inter-city capital flows and spillovers to non-service sectors. An interlocking analysis reveals network relations as opposed to causal directions. Our quantitative evidence indicates that APS servicing strategies affect those of CORE nearly three times as much as CORE affect APS, raising questions of causality which we are unable to answer in this present paper. If CORE markets drive APS agglomeration as suggested by Lizieri (Citation2009), are APS centralities mapped to the geography of CORE services provision, or vice versa? The analysis contributes to understanding of transnational urban network relations in the year 2020 and paves the way for other studies of the spatial organization of APS and CORE service provision in the post-pandemic era.

Supplemental Material

Download MS Word (107.5 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 A list of the firms in the two categories are provided in Appendix 1.

2 The different number of APS and CORE firms reflects that the APS firms include five sub-categories: financial services (75 firms), accountancy (25 firms), advertising (25 firms), law (25 firms), and management consultancy (25 firms). Within each category, the number of firms is comparable to the RE sector (22 firms). To control for the different number of companies, we run robustness tests based on the connectivity of firms from each sub-sector. The results are reported in Appendix 6 and 7. As shown in the appendices, the CORE network interlocks with each of the five sub-sector firms, except for the insignificant impact of law firm connectivity on CORE firm connectivity. Regarding the impacts of each sub-sector firm on investment flows, we can see that the network of firms from each sub-sector reduces the likelihood of zero-investment flows, and the connectivity of firms from law, advertising, and management consultancy firms increases the amount of investment flows. Overall, we can see that our findings based on 175 APS firms reflect the overall condition of the five sub-sectors. The findings on the interlocking of the APS network, CORE network, and investment flows are not influenced by the number of companies in the APS firm category.

3 In the OECD database, personal income is only reported to 2017, so we use personal income in 2017 as a proxy. However, given the importance of personal income as an economic factor, we keep it in our baseline model. The results and conclusions are completely robust if we drop the variable of personal income. The results without the personal income control are available from the authors by request.

4 In appendix 5, we also present the results using only the cities with non-zero capital flows. The finding that the synergy of APS and CORE network positively influence the capital flow remain robust. However, we have chosen to keep the Zero-inflated Poisson regression as it includes all cities, including those with zero values.

5 Country dummies can capture country-level policies, such as credit supply, interest rates, inflation, etc. In Appendix 8, we removed the county dummies and instead included country-level control variables. In this case, the coefficients for our key variables are larger.

6 In logistics regression, the relationship between dependent and independent variables is an S-shape curve, which is nonlinear. As a result, the marginal effect of a change in the independent variable becomes a bell shape curve. The marginal effect of a percent change in APS is an upward bell shape curve with a range of [0, when

is positive and a downward bell shape curve with a range of [

when

is negative.

7 Real estate firm service data was initially collected in 2018, however, the data quality is not as good as in 2020. Therefore we use the results based on 2020 data as the baseline model.

References

- Allen, J. (2010). Powerful city networks: More than connections, less than domination and control. Urban Studies, 47(13), 2895–2911.

- Bassens, D., & van Meeteren, M. (2015). World cities under conditions of financialized globalization: Towards an augmented world city hypothesis. Progress in Human Geography, 39(6), 752–775.

- Baum, A. (2008). The emergence of real estate funds. In A. Petersen (Ed.), Real estate finance: Law, regulation and practice (pp. 383–406). London: LexisNexis.

- Baum, A. (2015). Real estate investment A strategic approach. London: Routledge.

- Beaverstock, J. V., Smith, R. G., Taylor, P. J., & Lorimer, H. (2000). Globalization and world cities: Some measurement methodologies. Applied Geography, 20(1), 43–46.

- Blonigen, B. A., & Piger, J. (2014). Determinants of foreign direct investment. Canadian Journal of Economics/Revue canadienne d'économique, 47(3), 775–812.

- Borensztein, E., De Gregorio, J., & Lee, J. W. (1998). How does foreign direct investment affect economic growth? Journal of International Economics, 45(1), 115–135.

- Boussebaa, M., & Faulconbridge, J. R. (2019). Professional service firms as agents of economic globalization: A political perspective. Journal of Professions and Organisation, 6(1), 72–90.

- Branstetter, L. (2006). Is foreign direct investment a channel of knowledge spillovers? Evidence from Japan’s FDI in the United States. Journal of International Economics, 68(2), 325–344.

- Brenner, N., & Theodore, N. (2002). Cities and the geography of ‘actually existing neoliberalism’. In N. Brenner & N. Theodore (Eds.), Spaces of neoliberalism: Urban restructuring in North America and Western Europe (pp. 349–379). London: Blackwell.

- Brodzicki, T., & Uminski, S. (2018). A gravity panel data analysis of foreign trade by regions: The role of metropolises and history. Regional Studies, 52(2), 261–273.

- Capello, R. (2000). The city network paradigm: Measuring urban network externalities. Urban Studies, 37(11), 1925–1945.

- Cartwright, S., & Shoenberg, R. (2006). Thirty years of mergers and acquisitions research: Recent advances and opportunities. British Journal of Management, 17(S1), S1–S5.

- Castells, M. (1996). The rise of the network society: Economy, society and culture (volume I). Cambridge, MA, and Oxford: Blackwell.

- Christaller, W. (1933/1966). Die zentralen Orte in Süddeutschland. Englewood Cliffs: Prentice-Hall.

- Coakley, J. (1984). The integration of financial and property markets. Environment and Planning A: Economy and Space, 26(5), 697–713.

- Collins, J. D., Holcomb, T. R., Certo, S. T., Hitt, M. A., & Lester, R. H. (2009). Learning by doing: Cross-border mergers and acquisitions. Journal of Business Research, 62(12), 1329–1334.

- De Mello, L. R. (1999). Foreign direct investment led growth: Evidence from time series and panel data. Oxford Economic Papers, 51(1), 133–151.

- Derudder, B. (2021). Network analysis of ‘urban systems’: Potential, challenges, and pitfalls. Tijdschrift voor economische en sociale geografie, 112(4), 404–420.

- Derudder, B., & Taylor, P. J. (2018). Central flow theory: Comparative connectivities in the world-city network. Regional Studies, 52(8), 1029–1040.

- Derudder, B., & Taylor, P. J. (2020). Three globalizations shaping the twenty-first century: Understanding the new world geography through its cities. Annals of the American Association of Geographers, 110(6), 1831–1854.

- Florida, R., Adler, P., & Mellander, C. (2017). The city as innovation machine. Regional Studies, 51(1), 86–96.

- Friedmann, J. (1986). The world city hypothesis. Development and Change, 17(1), 69–83.

- Friedmann, J., & Wolff, G. (1982). World city formation: An agenda for research and action. International Journal of Urban and Regional Research, 6, 309–344.

- Glaeser, E. L., & Saiz, A. (2003). The rise of the skilled city. Harvard Institute of Economic Research Discussion Paper 2025. Harvard, Cambridge, MA.

- Halbert, L., & Attuyer, K. (2016). Introduction: The financialisation of urban production: Conditions, mediations and transformations. Urban Studies, 53(7), 1347–1361.

- Halbert, L., Henneberry, J., & Mouzakis, F. (2014a). Finance, business property and urban and regional development. Regional Studies, 48(3), 421–424.

- Halbert, L., Henneberry, J., & Mouzakis, F. (2014b). The financialisation of business property and what it means for cities and regions. Regional Studies, 48(3), 547–550.

- Halbert, L., & Rouanet, H. (2014). Filtering risk away: Global finance capital, transcalar territorial networks and the un-making of city-regions: An analysis of business property development in Bangalore, India. Regional Studies, 489(3), 471–484.

- Hall, P. (1966). The world cities. London: Weidenfeld and Nicolson.

- Harvey, D. (1982). The limits to capital. London, New York: Basil Blackwell.

- Harvey, D. (1985). The urbanization of capital: Studies in the history and theory of capitalist urbanization, 2. London, New York: Basil Blackwell.

- Henneberry, J., & Mouzakis, F. (2014). Familiarity and the determination of yields for regional office property investments in the UK. Regional Studies, 48(3), 530–546.

- Hoyler, M., Lizieri, C., Pain, K., Taylor, P., Vinciguerra, S., & Derudder, B. (2014). European cities in advanced producer services and real estate capital flows: A dynamic perspective. In K. Pain & G. Van Hamme (Eds.), Changing urban and regional relations in a globalizing world (pp. 115–137). Cheltenham: Edward Elgar Publishing.

- Hoyler, M., & Pain, K. (2001). London and Frankfurt as world cities: Changing local-global relations. In A. Mayr, M. Meurer, & J. Vogt (Eds.), Stadt und Region: Dynamik von Lebenswelten (pp. 76–87). Leipzig: Deutsche Gesellschaft für Geographie Leipzig.

- Hyun, H. J., & Kim, H. H. (2010). The determinants of cross-border M&As: The role of institutions and financial development in the gravity model. World Economy, 33(2), 292–310.

- Jacobs, W., Koster, H., & Hall, P. (2011). The location and global network structure of maritime advanced producer services. Urban Studies, 48(13), 2749–2769.

- Jandik, T., & Kali, R. (2009). Legal systems, information asymmetry, and firm boundaries: Cross-border choices to diversify through mergers, joint ventures, or strategic alliances. Journal of International Business Studies, 40(4), 578–599.

- Jones, C. A., & Trevillion, E. (2022). Real estate investment: Theory and practice. Cham: Palgrave Macmillon Cham.

- Knox, P., & Pain, K. (2010). International homogeneity in architecture and urban development? Special issue on international real estate markets, global real estate industry. Informationen zur Raumentwicklung (IzR), 34(2), 417–428.

- Lefebvre, H. (1974/1991). The production of space. London, New York: Blackwell.

- Lizieri, C. (2009). Towers of capital: Office markets and international financial services. Oxford: Wiley-Blackwell.

- Lizieri, C., & Mekic, D. (2018). Real estate and global capital networks: Drilling into the city of London. In M. Hoyler, C. Parnreiter, & A. Watson (Eds.), Global city makers: Economic practices and actors in the world city network (pp. 60–82). Cheltenham: Edward Elgar.

- Lizieri, C., & Pain, K. (2014). International office investment in global cities: The production of financial space and systemic risk. Regional Studies, 48(3), 439–455.

- Lizieri, C., & Pain, K. (2015, April 22). International office investment networks and capital flows in the financialization of city space (Paper presentation). Association of American Geographers (AAG) Conference, Chicago, Illinois, US.

- Madriaga, N., & Poncet, S. (2007). Fdi in Chinese cities: Spillovers and impact on growth. World Economy, 30(5), 837–862.

- Massey, D. (2006). World city. Cambridge, Malden: Polity Press.

- Pain, K. (2018). Land use policy and governance of real estate development. In G. Squires, E. Heurkens, & R. Peiser (Eds.), Routledge real estate companion (pp. 370–384). London: Routledge.

- Pain, K., Black, D., Blower, J., Grimmond, C. S., Hunt, A., Milcheva, S., … Pugh, R. (2018). Supporting smart urban growth: Successful investing in density. London: Urban Land Institute / New Climate Economy.

- Pain, K., Shi, S., Black, D., Blower, B., Grimmond, S., Hunt, A., … Manna, S. (2020). Real estate investment and urban density: Exploring the PUR territorial governance agenda using a topological lens. Territory, Politics, Governance, 11(2), 241–260.

- Rocco, R., & van Ness, A. (2005). The location of advanced producer services and urban change: A space syntax approach. 5th international Space Syntax Proceedings. Delft University of Technology The Netherlands.

- Rodríguez-Pose, A., & Zademach, H.-M. (2003). Rising metropoli: The geography of mergers and acquisitions in Germany. Urban Studies, 40(10), 1895–1923.

- Roy, A., & Ong, A. (2011). Worlding cities: Asian experiments and the art of being global. Oxford: Wiley-Blackwell.

- Sassen, S. (1991/2001). The global city. Englewood Cliffs: Princeton University Press.

- Sassen, S. (1994/2000). Cities in a world economy. London: Pine Forge Press.

- Sassen, S. (2002). Global networks, linked cities. London: Routledge.

- Scholvin, S., Breul, M., & Diez, J. R. (2019). Revisiting gateway cities: Connecting hubs in global networks to their hinterlands. Urban Geography, 40(9), 1291–1309.

- Sigler, T., Neal, Z. P., & Martinus, K. (2023). The brokerage roles of city-regions in global corporate networks. Regional Studies, 57(2), 239–250.

- Sirmans, C. F., & Worzala, E. (2003). International direct real estate investment: A review of the literature. Urban Studies, 40(5/6), 1081–1114.

- Sklair, L. (2006). Capitalist globalization: Fatal flaws and necessity for alternatives. Brown Journal of World Affairs, 13(1), 29–37.

- Taylor, P. J. (2001). Specification of the world city network. Geographical Analysis, 33(2), 181–194.

- Taylor, P. J. (2004). World city network: A global urban analysis. London: Routledge.

- Taylor, P. J., Hoyler, M., & Verbruggen, R. (2010). External urban relational process: Introducing central flow theory to complement central place theory. Urban Studies, 47(13), 2803–2818.

- Tesar, L. L., & Werner, I. M. (1995). Home bias and high turnover. Journal of International Money and Finance, 14(4), 467–492.

- Thrift, N. (1999). Cities and economic change: Global governance? In J. Allen, D. Massey, & M. Pryke (Eds.), Unsettling cities (pp. 271–321). London: Routledge.

- Van Loon, J., & Albers, M. B. (2017). How real estate became ‘just another asset class’: The financialisation of the investment strategies of Dutch institutional investors. European Planning Studies, 25(2), 221–240.

- Van Meeteren, M., & Poorthuis, A. (2018). Christaller and “big data”: recalibrating central place theory via the geoweb. Urban Geography, 39(1), 122–148.

- Wojcik, D. (2018). The global financial networks. In G. L. Clark, M. P. Feldman, M. S. Gertler, & D. Wójcik (Eds.), The New Oxford handbook of economic geography (pp. 557–574). Oxford: Oxford University Press.

- Zademach, H.-M., & Rodríguez-Pose, A. (2009). Cross-border M&As and the changing economic geography of Europe. European Planning Studies, 17(5), 765–789.

- Zhu, B., & Lizieri, C. (2021). Connected markets through global real estate investments. Real Estate Economics, 49(S2), 618–654.

- Zhu, B., Pain, K., Derudder, B., & Taylor, P. (2022). Exploring external urban relational processes: Inter-city financial flows complementing global city-regions. Regional Studies, 56(5), 737–750.