?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Financial statements provide significant information about the financial position and performance of an enterprise. In the global world, it is necessary that the information is comparable at the international level. This requirement poses a problem for small and medium-sized enterprises as they do their reporting in compliance with the national legislations, which are based on Directive 2013/34/EU in the EU member states. No application of the Directive in national legislations guarantees the harmonisation of financial statements. Another direction in harmonisation is the IFRS for Small and Medium-sized Entities (SMEs) which the EU has not acknowledged as a basis for financial statement creation although its significance is not negligible globally – around 80 jurisdictions use it or allow its use currently. The paper aims to analyse the current state of harmonisation of financial statements of small and medium-sized enterprises. Based on the identification of essential differences between the national legislation and the Standard, it attempts to answer the question whether (and how) the financial position and performance of an enterprise will change if the accounting framework changes, i.e., in the case of transfer from reporting based on national legislations to reporting based on the Standard.

1 Introduction

Small- and medium-sized enterprises and micro-enterprises (hereinafter SMEs) represent 99% of companies in the European Union. They provide two-thirds of jobs in the private sector and they contribute over a half to the total added value formed by companies in the EU. Nine out of ten small and medium-sized enterprises are micro-enterprises with fewer than ten employees. The EU policy in the area of SMEs aims to ensure that the Union measures are helpful for them and that they contribute to Europe becoming a more attractive place for companies and business. (European Commission Citation2016)

An essential source of information about the financial position and performance of an enterprise is financial statements. In this context, companies are described by the accounting system and at the same time evaluated based on the outputs of accounting, i.e., financial statements.

Therefore, the general requirement laid on accounting – to capture the facts of the entity’s economic life properly – comes naturally. To meet such a requirement (in a situation of non-existent precise limits), it is necessary to adopt a convention valid to a large extent for all accounting entities, a convention determining the framework of the ‘space’ in which the accounting will picture the economic activities of the company so that the necessary rate of unified creation of the accounting picture of the economic facts is maintained (Janhuba, Citation2010). This convention can be national or supranational and it can direct the companies towards consistent data within the international environment. The adoption of a supranational convention is currently topical within the segment of SMEs. As international cooperation is increasing, there is the need of internationally comparable information provided in financial statements.

The paper deals with the current state of harmonisation of accounting of SMEs and its possible development. In detail, it explores the differences arising in results of the differing accountings systems.

The conclusion to the paper compares whether the reporting based on a unified concept will influence all the facts that the creators of the Standard assume and various authors deduce.

2. Methodology

The paper aims to analyse the current state of the harmonisation of financial statements of small and medium-sized enterprises with focus on the IFRS for Small and Medium-sized Entities (IFRS for SMEs) and to identify the essential differences between the national (in this case Czech) legislation and the Standard. At the same time, it attempts to verify the effect that the change of the used reporting concept from national legislation to the Standard will have on the information capacity of financial statements. This is theoretical research in correspondence to the definition provided by Reichel (Citation2009). The research design contains elements of qualitative research as defined by Strauss, Juliet and Corbin (Citation1998) or Creswell (Citation2009). The data sources are documents, i.e., directives, acts and decrees.

The following methods have been used to reach the aim:

description,

analysis,

synthesis,

modelling,

comparison.

Of the specific methods used in financial reporting, recognition and measurement of basic items of financial statements are used.

The method of description is used in Chapters 3 and 4, which contain the description of the current state and the development of financial statements, the contents of Direction 2013/34/EU, which is the basis for national accounting legislations of EU member states and the IFRS for SMEs.

Individual parts of the Direction and the Standard have been analysed with focus on the harmonisation of financial reporting of small and medium-sized enterprises, the aims of financial statements and the quality of information they provide. Additionally, the methods used for the process of financial statement creation, i.e., methods used for the recognition of the items of financial statements (assets, liabilities, expenditures, revenues, equity) and the methods of measurement of assets and liabilities, have been analysed. The method of synthesis has been used as supplementary to analysis: the individual parts were combined as a whole, i.e., financial statements which, based on different methods of recognition and measurement of assets and liabilities can have several forms that are then manifested either in the structure or in the value of the items. These forms affect the information capacity as they provide different information on the financial position and performance of an accounting entity.

The method of modelling was used in Chapter 5, where essential differences between the IFRS for SMEs and the national legislation were selected to verify the issue given. Based on the differences, changes that will occur in financial statements were generally expressed. This is a simplified image of reality, which however respects the features that can be attributed to real-life entities. This method has been selected as it is very difficult to verify the possibilities using practical cases. The results were then compared – method of comparison was used.

3. The institutional framework of financial reporting in EU member states

The financial reporting of EU member states is currently based on Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC (hereinafter Directive) (European Commission, Citation2013). The Directive aims to improve the harmonisation of financial statements; however, based on current trends, the main emphasis is laid on the reduced administrative load of SMEs primarily. Documents focusing on the improvement of their position, (‘EUROPE 2020 - A strategy for smart, sustainable and inclusive growth’, ‘Single Market Act I, 2011’, ‘Small Business Act 2008’), are referenced.

Paragraph 4 of Directive 2013/34/EU defines objectives of a financial statement as follows: ‘Annual financial statements pursue various objectives and do not merely provide information for investors in capital markets but also give an account of past transactions and enhance corporate governance. Union accounting legislation needs to strike an appropriate balance between the interests of the addressees of financial statements and the interest of undertakings in not being unduly burdened with reporting requirements.’ True and fair views is further mentioned in paragraph 3, Art. 4: ‘The annual financial statements shall give a true and fair view of the undertaking's assets, liabilities, financial position and profit or loss.’

The Directive deals with small and medium-sized enterprises in paragraphs 10 to 15, where the effort for harmonisation of small and medium-sized enterprises in the EU is described as well as the reduction of obligatory information provided in the financial statement appendix. Small and medium-sized enterprises are defined based on the balance sheet total, net turnover and the number of employees, the specific figures being provided in Art. 3, Categories of undertakings and groups. Paragraph 27 stipulates the option to relieve small enterprises of the obligation to provide a report on company management.

Chapter 3, Art. 14, Simplifications for small and medium-sized undertakings, reports that member states can allow small and medium-sized enterprises to provide a reduced version of the balance sheet and the profit and loss statement. This is elaborated on in Chapter 7, Art. 31 Simplifications for small and medium-sized undertakings, where the lines of reports that can be aggregated are specified. Chapter 9, Art. 36 Exemptions for micro-undertakings, lists the obligations that micro-enterprises can be relieved of.

Except the above mentioned simplifications and exemptions, all the other Directive stipulations are valid for small and medium-sized enterprises just as for large companies. When selecting the accounting or measurement methods, or in some cases reporting methods, member states can choose from a range – this option is formulated as ‘states may permit or require’ in the Directive; the Directive also refers to national legislations. Significant options include various methods of recognition of formation expenses, costs of development, and intangible assets created by the undertaking itself. As regards these items, they can be recognised as assets or expenses. Other options concern the measurement of tangible assets, for which either the purchase price or the revaluated amount can be used. Financial assets can also be measured either by the purchase price or their fair value. Still further options consider the simplification of statements and additional information, mainly for small and medium-sized enterprises. All these options, exemptions, and references to national legislations degrade the harmonisation efforts and the information capacity of financial statements across the states.

We can state that the EU Directive does not play its role within the financial reporting harmonisation of small and medium-sized enterprises well enough to meet the needs of financial statement users, especially as regards international comparison. The current situation, in which there are 27 different systems, is not acceptable in the long term, as agreed by institutions such as the European Commission or the International Accounting Standards Board, as well as many studies and publications (Baldarelli et al. Citation2012, Paseková et al. Citation2010, Briciu et al. Citation2009). The need for generally comparable and comprehensible financial statements has also been mentioned by Mošnja-Škare and Galant (Citation2013).

Since 2001, there has been a project aiming to create the International Financial Reporting Standard for Small and Medium-sized Entities, hereinafter IFRS for SMEs, or Standard, for the needs of financial reporting harmonisation, independently of the Direction. After a series of consultations and comments, the Standard was published in July 2009. It has had an immediate effect although its implementation depends on national regulatory authorities – it has remained voluntary. The IASB regularly revises the Standard; the last revision was performed in May 2015. The full revised version of the IFRS for SMEs 2015 was issued in December 2015, with effect from 1 January 2017. The Standard is currently used in approximately 83 states; 11 states are considering its use, some still do not consider its use (IASB, Citation2012).

The aim of the Standard is to provide a comprehensive and simplified set of accounting principles for smaller and unlisted accounting units in order to improve the quality and comparability of financial information.

The standard for small and medium-sized enterprises is based on full IFRS, but it contains some simplifications, does not address areas that are not relevant for small and medium-sized enterprises, and greatly simplifies the requirements for data publication. In contrast to the EU Directive, the Standard uses a qualitative definition of medium-sized enterprises as entities that do not have public accountability and publish the financial statements for external users. The Standard provides general definitions of financial statement items, such as assets, liabilities, costs, revenues, profit or loss, and equity (which are not defined in the Directive or in the vast majority of national legislations).

The possible use of the Standard as a framework for the financial reporting regulation was included in the review of European directives in the form of consultations (European Commission, Citation2010). The aims of the consultation were to obtain feedback on the use of the Standard and at the same time to define the relationship between the Directive and the Standard.

In response to the consultation material, the respondents generally confirmed their support for the Directive on accounting as a basic framework for accounting in the EU. Their responses placed emphasis on the key role of directives within the EU, which should provide a set of general accounting principles applicable throughout the EU. Simplified and revised directives should provide for the needs of small and medium-sized enterprises. There were different opinions as regards the Standard.

The arguments of the opponents:

The Standard is difficult, particularly for small businesses.

Businesses that operate only locally do not need international comparability and those who create and use accounting information documents are accustomed to national accounting rules.

The costs of financial statement creation and staff training would increase as a result of the Standard implementation. Small businesses would have a more complicated access to corporate training.

The Standard does not affect the close link between accounting and taxation of trading companies, which exists in a number of member countries.

The Standard is not in compliance with the terms of profit distribution in trading companies.

The arguments of the proponents:

The Standard would contribute to greater international comparability.

It would simplify the procedures when drawing up consolidated financial statements.

It would raise the chances of international financing.

Many respondents indicated that the users of accounting would benefit from the expanded scope of the Standard, mainly due to the increased capacity to analyse and compare the financial statements prepared in different jurisdictions, and cross-border mergers and cross-border cooperation would be simpler.

The Standard is appropriate for international groups and subsidiary companies reporting under IFRS.

A common accounting language would improve the communication between business partners, investors, and creditors based abroad, contribute to easier mobility of accountants and auditors within the EU, and improve the prospects for joint training.

Investors and rating agencies would have better conditions for decision-making.

As regards the process of a possible convergence of the Directive and the Standard, some respondents said the Directive should be revised not to be in conflict with the Standard; others wanted the Standard to be adopted as an option; still others warned against radical changes and rather suggested an evolutionary process.

The Commission has examined the possible adoption of the IFRS for SMEs at the level of the EU and rejected this option. Based on the differences between the Standard and the Directive, the Commission concluded that the Standard would not be a suitable instrument for administrative burden reduction. The assessors considered that the Standard for SMEs is new – there is no experience with its application anywhere in the world. In addition, some of the differences between the Directive and the Standard were decisive, such as the reporting of unpaid subscribed capital stock or the goodwill impairment, in which the expected lifetime cannot be reliably estimated. Therefore, it was decided that the explicit full adoption of the Standard is not possible.

4. The expected impacts of the IFRS for SMEs implementation with special focus on the Czech Republic

The preparation and publication of the Standard were accompanied by many expectations, even though all parties involved were aware of the complexity of this process. Both regulatory authorities and many authors, mostly from the academic environment, but also expert in practice, have responded to this situation.

It is not simple to predict the consequences of the IFRS for SMEs potential implementation. This is only a hypothetical situation within the EU. As already mentioned, the European Commission did not approve the use of the Standard and its use is probably a matter of long-term development. A possible evaluation of the effect of the introduction of a financial regulation system and its changes as well as the effect of incremental changes to the accounting rules would require a comparison of the existing state with a hypothetical one, which would occur if no regulation existed. A determination whether a change has brought positive or negative effects would need a comparison of the present values of social welfare in both versions. This indicator cannot be practically measured, as we cannot count the value of something that actually does not exist. Therefore, in reality the qualitative analysis of the expected benefits and costs of the upcoming change in regulations compared to the current state is used (Procházka, Citation2015).

Various authors aimed to identify the users of financial statements, the entities appropriate for the Standard application, or the comparison of costs and benefits following from the Standard implementation (Di Pietra et al., Citation2008; Schiebel, Citation2008; Litjens et al., Citation2012; Quagli and Paoloni, Citation2012). Albu et al. (Citation2013) conducted a survey on the expectations of financial statement users in the Czech Republic, Hungary, Turkey and Romania.

The survey conducted in a selected sample of companies in the Czech Republic, Slovakia, Poland, and Ukraine focused on positive expectations related to the future acceptance of the IFRS for SMEs, the expected advantages and the interest in training in this field. Regarding Czech companies, only 5% of respondents expect advantages, 8% are interested in further training; in Slovakian companies, 4.5% expect advantages and 5% of companies are interested in training; 18% of Ukrainian companies expect advantages and nearly 70% are interested in training; the largest advantages are expected in Polish companies – 45% and the same percentage are interested in further training. (Paseková et al. Citation2010).

Another study conducted in the Czech Republic (Bartůňková, Citation2012) within the category of small and medium-sized enterprises showed that creating a financial statement in compliance with the IFRS for SMEs is interesting for medium-sized enterprises whose majority owners are foreign companies. These enterprises are of the opinion that such a financial statement would facilitate their reporting and creation of the consolidated financial statement. At the same time, it has been confirmed that there is the dependence of the willingness to use the Standard taking account of the company size: the larger the company, the higher the interest in using the Standard. On the other hand, there are worries of a higher administrative load, high expenses of the implementation, and the different relationship between accounting and income taxes.

Some results can be deduced from surveys conducted by the Ministry of Finance of the Czech Republic in cooperation with auditing companies which were published in 2005, i.e., at the time when the Standard was undergoing the approval process. The surveys concerned the potential impact of full IFRS application in Czech unlisted companies and full IFRS application in unlisted companies in six European states. Although the surveys were based on full IFRS, the results provided by the selected sample of companies could serve as a base for the assessment of future problems regarding the implementation of the IFRS for SMEs. The main advantage of the IFRS mentioned by the respondents was the simplification of international cooperation. The assessment could be considered biased in some cases and it depends on the size of a company, subject of business and complicacy of accounting procedures. Some distortion can also be caused by insufficient knowledge of the IFRS, as the respondents themselves admitted. In selected companies only the employees who created statements in compliance with the IFRS for the parent company confirmed they knew the IFRS well; others considered the knowledge unnecessary for the time being (Ministry of Finance of the Czech Republic, Citation2005).

Studies in Croatia proved that 69% of small and medium-sized enterprises consider the IFRS for SMEs suitable to be used (Klikovac, Citation2006), although in a similar survey conducted in the following years only 11% of respondents considered the IFRS for SMEs suitable (Baldarelli et al. Citation2012).

A study exploring the potentials of the IFRS for SMEs acceptance in Turkey (Arsoy & Sipahi, Citation2009) reported the acceptance as a highly complicated process hindered by the current accounting system, its links to tax regulations, and limited accountants’ education on the IFRS.

Another survey of the IFRS application in companies in six European states focused generally on the possible usage of full IFRS for unlisted companies. The survey shows that for some unlisted companies (small companies or those which are not a subsidiary or an affiliated company of listed companies) it is more suitable to use the simplified version of the IFRS, i.e., the planned IFRS for SMEs.

5. The impacts of the standard on the financial position and performance of a company

One of the prerequisites for the proper evaluation of the IFRS for SMEs usage impacts is the knowledge of the final form of statements drawn up in compliance with the Standard and its comparison with national legislation. The following chapter provides a simplified model of the conversion from the national (Czech) legislation to the Standard and draws attention to the fundamental differences in the recognition and measurement of financial statement items which may affect the value of assets, sources of financing and the profit or loss.

5.1. Changes in statements

When using the Standard for the creation of the company’s financial statement, the companies which have changed from the national legislation to the Standard will have to be aware that, as a consequence of the differing methods for recognition and measurement of assets and liabilities, they will probably achieve different values of assets, equity capital and liabilities in the statements created in compliance with the IFRS, in contrast to the national legislation. The total difference will affect the balance sheet total, the value of long-term and short-term assets, equity and liabilities, and profit or loss. The differing value of these items will be reflected in the indicators of profitability or indebtedness. The following derivations and comparisons are based on the differences between the Czech national regulations and the IFRS; some of the procedures can be generalised.

As of the day of transition to the Standard, the company has to create the initial balance sheet in which it is necessary:

to recognise all assets and liabilities whose recognition is required by the IFRS for SMEs;

not to recognise items as assets or liabilities if this IFRS does not permit such recognition;

to reclassify items that are recognised under its previous financial reporting framework as one type of asset, liability or component of equity, but are a different type of asset, liability or component of equity under this IFRS; and to apply this IFRS in measuring all recognised assets and liabilities, (International Accounting Standards Board, Citation2009).

The changes expressed in the initial balance sheet in contrast to the national legislation will be reflected as:

changes in long-term assets in consequence of a different perspective regarding recognition of an item of assets;

reclassification of items of long-term and floating capital;

changes in measurement of equity.

These types of changes can be derived and exemplified by balance sheet operations (see ). All examples are designed so that they express how an item in a statement created in compliance with the Standard will change in comparison with a statement created in compliance with national legislation. As has been mentioned in Chapter 2, this is theoretical research in which the changes are expressed using symbols +/-, without specific numbers.

Table 1. Recognition of a long-term asset in the balance sheet.

Table 2. Exclusion of a long-term asset from the balance sheet.

Table 3. Reclassification of short-term and long-term assets.

Table 4. Changes in measuring assets and liabilities by the current value.

Table 5. Repayment of liabilities by the effective interest rate method.

Table 6. Changes in the profit or loss.

The progress of changes in statements in a situation when an accounting entity recognises a long-term asset which used to be recognised as an expense (and vice versa) in compliance with national legislation is shown in and .

With the difference appearing in consequence of an expense in compliance with national legislation being recognised as an asset in compliance with the Standard, it is necessary to deduct the value of the item which was originally recognised as an expense from total expenses. At the same time, expenses will be increased by means of depreciations, see .

shows a situation when an accounting unit does not report assets, which are however recognised in compliance with the national legislation, as the Standard does not allow their reporting and they are recognised in expenses at the time of their origination.

In a balance sheet created in compliance with the Standard, the difference will be reflected in a decrease in the value of assets and an increase in expenses in the year of the asset recognition. The expenses increase by recognising the entire value of the item as an expense; at the same time they decrease by excluding the original depreciations.

The reclassification of the items which the company used to report in compliance with the previous system of reporting as one type of asset, liability or component of equity but are a different type of asset, liability or component of equity in compliance with the Standard can be exemplified using the transition of some items between long-term and floating assets. The most frequently used example is spare parts as their price is significant and their usability lasts over one year. If the national legislation reports spare parts within short-term assets and in a statement created in compliance with the Standard they will be long-term assets which will be depreciated, a difference in the values of long-term and short-term assets, or even expenses, will occur. The differences are presented in .

When reclassifying stocks, the short-term assets are decreased and long-term assets are increased as the item of stock is transferred. If the spare part becomes a long-term asset, it has to be depreciated and expenses are increased by depreciations.

The changes in statements which will be brought about by the change in the recognition method are presented in . In some cases of recognition the Standard uses the current value (property purchased by leasing, property purchased by instalments, long-term liabilities, etc.). The current value is the discounted value of future net inflow or outflow of money which is expected to be created by the item or to be needed for the settlement of liabilities. Repayments of liabilities are divided between financial expenses and a decrease in an unpaid liability by the method of an effective interest rate. The changes in the value of the items, when the current value replaces the purchase price of an asset, are presented in .

If the current value is used for the initial recognition of a long-term asset, the difference appears in values of long-term assets, depreciations and liabilities. When the value of the asset is recalculated to the current value and the temporal value of money is considered, the value of long-term assets, depreciations and liabilities decreases in comparison to the original measurement in purchase prices. When the liabilities are paid, the value of the instalment is divided between a decrease in the liability and an interest; the changes are shown in .

When the method of effective interest rate is used for repaying liabilities, the value of the liability is not decreased by the entire sum of the instalment – it is divided into a decrease in the liability and an interest which increases expenses.

5.2. Changes in company performance

Performance is a relation between revenues and expenses of an accounting unit during an accounting period; a change in the performance due to the two accounting concepts is brought about by the effect of the changes in the way individual items are recognised as profit or loss. The changes pictured in are summarised in .

When recognising a long-term asset captured within the national legislation as an expense (), expenses are decreased by excluding the item and increased by means of depreciations. The overall effect on profit or loss is its increase.

When an asset is excluded (), expenses increase by excluding the item and at the same time expenses decrease by the modification of depreciations. Altogether, the profit or loss decreases.

When assets are reclassified by changing the classification of stocks (), expenses increase by depreciations, and the profit or loss decreases.

When changing assets and liabilities (), expenses decrease due to the decreased value of depreciations and the profit or loss increases.

In the case of using the effective interest rate method for paying off a liability (), the profit or loss decreases due to the interests which appear during repaying.

In this situation, a combination of changes in measuring () and repaying () occurs. The final effect on the profit or loss is a result of the combination of a change in the value of depreciations and interests and depends on the specific values of these items.

5.3. Statement of the financial position

A financial position of a company is captured in the statement of the financial position, where the balance is defined by the balance sheet Eq. [1], which needs to be maintained even after the changes that occur in relation to the transfer from the national legislation to the IFRS Eq. [2].

[1]

[1]

[2]

[2]

The overall change in the balance sheet equation is a sum of partial changes: basic modifications based on the differences between the national legislation and IFRS for SMEs are shown in Eqs. [3]–[8]. When a long-term asset is recognised in the statement of financial position (see ), the balance sheet Eq. [3] changes and the result is an overall increase Eq. [4]. An increase in equity arises from a decrease in expenses by capitalising an item. The value of depreciations decreases the equity but the final difference is always in favour of an increase in equity Eq. [5].

[3]

[3]

[4]

[4]

[5]

[5]

When a long-term asset is excluded from the balance (see ), the balance sheet total changes Eq. [6], in this case it decreases. A decrease in equity follows from an increase in costs that have arisen in relation to the transfer of an item from assets to expenses. An exclusion of depreciation follows and this increases the value of equity, but the final difference always decreases equity, Eq. [7].

[6]

[6]

[7]

[7]

When reclassifying items between short-term and long-term assets (), the balance sheet total decreases Eq. [6]. The reason for the decreased value of assets and equity is the depreciations; when the assets are reclassified from short-term to long-term ones, they need to be depreciated, Eq. [8].

[8]

[8]

When the valuation changes, specifically when the current value is used for the initial measurement of assets and liabilities (), the balance sheet total decreases by the decrease in the values of assets, liabilities and equity. Equity will be lower by the decrease in the value of depreciations, Eq. [9].

[9]

[9]

6. Discussion

There have been few publications showing financial statements drawn up in compliance with the existing national legislation and, at the same time, the IFRS for SMEs. The conversion of a financial statement from the Czech legislation to the Standard is provided, see (Paseková et al., Citation2012).

Table 7. An example recalculation of a financial statement, in thousands of CZK.

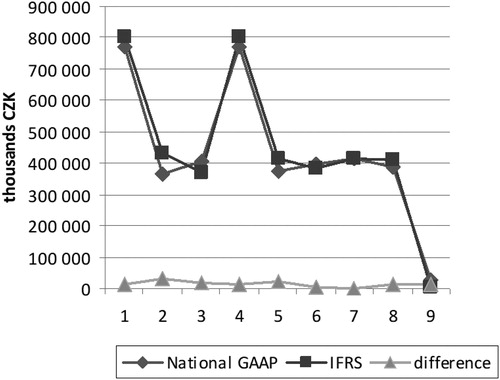

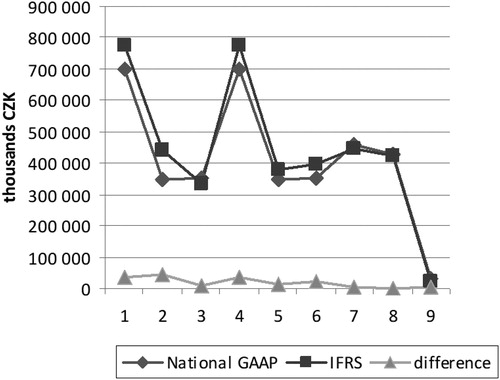

When the differences between the items reported in compliance with the national legislation and the IFRS are evaluated, we can see that the balance sheet total has increased. The increase has been substantially caused by the increase in the value of the long-term assets, and the most significant is the capitalisation of leasing. The balance sheet total has risen by 3.9% in the current period and by 9.5% in the previous period. The value of profit or loss shows even a more considerable change – there is a decrease of 86% for the current period and 27% for the previous period, brought about by the increase in depreciations of long-term assets, specifically the assets purchased by financial leasing. The other changes in the indicators, brought about by transfers between long-term and current assets, modifications of long-term asset measuring, changes in reporting of reserves, financial assets and liabilities, are shown in and .

Figure 1. Comparison of indicators reported in compliance with the national legislation and the IFRS in the current period.

Source: author

Figure 2. Comparison of indicators reported in compliance with the national legislation and the IFRS in the past period.

Source: author

The graphical analyses of the data confirm the most significant differences at points 2 (long-term assets) and 9 (profit or loss) in the current and the previous periods ( and ) and the graph follows the changes in the balance sheet equation:

Current period:

Previous period:

The analysis of the data obtained from the example financial statement does not provide results that could be generalised – it is only an indication of the future development. Besides the established rules, the results of the transfer are affected by many factors, such as the size of the company, the field of business, a selection from more methods (e.g., depreciations) and estimates. Results of each company are individual and unique.

7. Conclusion

The harmonisation of financial reporting of SMEs using Directive 2013/34/EU is not sufficient on an international scale; the differences mainly follow from the possible choice of various versions of the recognition and measurement of financial statement items when implementing the Directive into national legislations.

An alternative method of the harmonisation, which is currently not recognised by the European Commission, is the IFRS for SMEs. The Standard was issued with the aim to provide a comprehensive and simplified set of accounting principles for smaller and unlisted accounting units in order to improve the quality and comparability of financial information, particularly among individual states. These statements are significant for the evaluation of the company creditworthiness when applying for foreign loans, the assessment of the financial health of buyers, improvement of the conditions for rating agencies, and the attraction of foreign investors.

Based on the model of the conversion from the national legislation to the Standard in Chapters 5 and 6, it is possible to confirm that the financial statements prepared in compliance with the uniform accounting framework would be comparable, because they would use the same rules for the recognition and measurement of individual items. This would level the starting conditions and all businesses would be assessed in the same way, without an influence of some ‘misinformation’, incurred due to differing accounting methods. At the date of transition some differences may occur which would have an impact on the value of assets, liabilities, equity, profit or loss, and the related performance indicators, such as profitability. A situation may even occur in which a company’s financial position and performance will change significantly, either in a positive or in a negative direction. Basically, this is a transition from one accounting framework to another, both of which are governed by the principle of ‘true and fair view’. This principle is slightly disputable, as each accounting system claims and uses it but in clearly defined legislative limits, compliance with which is considered as ‘true and fair view’. The degree of the differences is the same as the degree of the difference between the individual national legislations and the Standard.

Quality improvement of the information provided is no longer a matter of the accounting framework only. As reported by Procházka (Citation2015), the quality of the accounting system is determined by the accuracy with which the accounting with its instruments is able to display the economic situation of the company (the financial position and performance). Companies drawing up financial statements may use a limited number of accounting methods, which do not always exactly capture the true essence of the economic transaction. There is also a difference in the quality of financial statements within the member states – developed economies tend to have a higher quality of financial statements (Albu et al., Citation2013). The effect of subjectivity in the items that are determined by a qualified estimate is not negligible.

When evaluating the benefits, the shift in the position of SMEs which has occurred since 2009, strengthening their position significantly, has to be considered. At the level of the EU, this is proven by documents such as ‘Europe 2020 - A strategy for smart, sustainable and inclusive growth’, ‘Single Market Act’, ‘Small Business Act’, and others, which are even accepted by national institutions. In addition, the financing of SMEs has improved. Disregarding the financial crisis, which made access to financial sources more difficult for all types of businesses, the availability of financial sources for this segment has increased. This is the consequence of EU support programmes and support from individual national governments, which enable also the SMEs to obtain loans. However, we have to realise that SMEs will always have a worse position compared to large enterprises because banks assess the creditworthiness of the clients applying for a loan; they do their ‘scoring'. Amongh others, the creditworthiness and the total income potential of the future loan client are explored. If the applicant’s creditworthiness does not reach the required values, the loan is not provided by the bank, since the return on the loan could be threatened. Low income potential can also affect not only whether the loan will be provided but also under what terms and conditions. Disadvantageous conditions may discourage the applicant from taking the loan.

It follows that good-quality and comparable financial statements are an important starting point for the improvement of the situation of SMEs, but are only a part of all the influences affecting the economy. A perfect harmonisation is a long-term process with an uncertain outcome, which will evolve depending on the decisions of financial reporting regulatory authorities, which may to some degree be affected by the users of financial statements.

Acknowledgements

This paper was supported by the specific research from Masaryk University MUNI/A/0904/2017.

References

- Act no. 563/1991 call, on accounting, as amended.

- Albu, C.N. et al. (2013). Implementation of IFRS for SMEs in Emerging Economies: Stakeholder Perceptions in the Czech Republic, Hungary, Romania and Turkey. Journal of International Financial Management and Accounting, (2), 140–175.

- Arsoy, A. P., & Sipahi, B. (2009). International Financial Reporting Standards for small and medium sized entities and the Turkish case. Ankara Universities SBF Dergisi, 62, 31–48. Available at: www.politics.ankara.edu.tr/dergi/pdf/62/4/2.pdf

- Baldarelli, M.-G., Demartini, P., Mosnja-Skare, L., & Paoloni, P. (2012). Accounting harmonization for SME-s in Europe: Some remarks on IFRS for SME-s and empirical evidences. Ekonomska Istrazivanja, 25 (suppl 1), 1–26. doi:10.1080/1331677X.2012.11517554

- Bartůňková, L. (2012). Are companies in the Czech Republic ready to implement IFRS for SMEs? Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 60 (7), 39–45.

- Briciu, S., Groza, C., & Gânfălean, I. (2009). International Financial Reporting Standard (IFRS) will support management accounting system for small and medium enterprise (SME)? Annales Universitatis Apulensis Series Oeconomica, 11(1), 308–318.

- Creswell, W. J. (2009). Research design. Qualitative, quantitative and mixed methods approaches. 3rd ed. Thousand Oaks: Sage.

- Di Pietra, R., Evans, L., Chevy, J., Cisi, M., Eierle, B., & Jarvis, R. (2008). Comment on the IASB’s exposure draft ifrs for small and medium-sized entities. Accounting in Europe, 5(1), 27–48.

- European Commission (2010). Europe 2020 – Europe’s growth strategy. Available at: http://ec.europa.eu/europe2020/index_en.htm.

- European Commission (2010). 4th Company Law Directive and IFRS for SMEs. Final report. Available at http://ec.europa.eu/internal_market/accounting/docs/studies/2010_cses_4th_company_law_directve_en.pdf.

- European Commission (2010). Summary Report of the Responses Received to the Commission´s Consultation on the International Financial Reporting Standard for Small and Medium –sized Entities. Available at: http://ec.europa.eu/internal_market/accounting/docs/ifrs/2010-05-31_ifrs_sme_consultation_summary_en.pdf.

- European Commission. (2013). Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings. Official Journal of the European Union. L, 182, 19.

- European Commission (2016). Small and medium sized entities. Available at: http://www.europarl.europa.eu/ftu/pdf/cs/FTU_5.9.2.pdf.

- International Accounting Standards Board. (2009). International Financial Reporting Standard, IFRS for Small and Medium – Sized Entities. London.

- International Accounting Standards Board. (2012). Comprehensive Review of the IFRS for SMEs. Available at:http://www.ifrs.org/ifrs-for-smes/documents/requestforinformation_ifrsforsmes_website.pdf.

- International Accounting Standards Board (2016). About IFRS for SMEs. Available at: http://www.ifrs.org/ifrs-for-smes/pages/ifrs-for-smes.aspx.

- Janhuba, M. (2010). Teorie Účetnictví (Výběr z Problematiky), Vysoká škola ekonomická v Praze: Oeconomica.

- Klikovac, A. (2006). The influence of financial reporting harmonization in EU upon financial reporting in the Republic of Croatia. Master thesis: Zagreb.

- Litjens, R., Bissessur, S., Langendijk, H., & Vergoossen, R. (2012). How do Preparers Perceive Costs and Benefits of IFRS for SMEs? Empirical Evidence From the Netherlands. Accounting in Europe, 9, 227–250.

- Ministry of Finance of the Czech Republic (2005). Field Testing _CZ. Průzkum některých dopadů zavedení IFRS v českých nekotoaných společnostech. Available at: http://www.mfcr.cz/cps/rde/xbcr/mfcr/Field_Testing_CZ.pdf.

- Mošnja-Škare, L., & Galant, A. (2013). The quality of notes relating sme revenues and expenditures disclosures: empirical study of croatian financial reporting standards (CFRS) implementation. Economic Research-Ekonomska Istraživanja, 26 (suppl 1), 343–368. doi:10.1080/1331677X.2013.11517656

- Paseková, M., Bialic-Davendra, M., Müllerová, L., Hvastová, J., Manová, E., Sowa, B., & Chyzhevska, L. (2010). IFRS for SMEs: Current Issues in Reporting of SMEs in the Czech Republic, Slovak Republic, Poland and Ukraine. In. AMIS 2010 - Proceedings of the 5th International Conference, Accounting and Management Information Systems. Romania, Bucuresti. June 16–18, pp. 793–801.

- Paseková, M., Hýblová, E., Müllerová, L., Pálka, P., Struhařová, K., Svitáková, B., & Šteker, K. (2012). Implemetace IFRS do malých a středních podniků. Wolters Kluwer: Czech Republic.

- Procházka, D. (2015). Ekonomické dopady implementace IFRS v Evropě. Vysoká škola ekonomická v Praze. Oeconomica: Czech Republic.

- Quagli, A., & Paoloni, P. (2012). How is the IFRS for SME Accepted in the European Context? An Analysis of the Homogeneity Among European Countries, Users and Preparers in the European Commission Questionnaire. Advances in Accounting, 28, 147–156.

- Reichel, J. (2009). Kapitoly metodologie sociálních výzkumů. Praha. Grada: Czech Republic.

- Schiebel, A. (2008). Is there a solid empirical foundation for the IASB's draft IFRS for SME. Paper presented at 31st Annual Congress of the European Accounting Association. 23–25 April, Rotterdam, the Netherlands.

- Strauss, A. L., Juliet, M., & Corbin, J. M. (1998). Basics of qualitative research: techniques and procedures for developing grounded theory. 2nd ed. Thousand Oaks: SAGE Publications.