?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Global economic growth is based on increased consumption of electricity both from renewable resources, such as water and wind and non-renewable resources, such as coal (lignite), natural gas or petroleum. Coal continues to represent an important energy source in the European Union, particularly in Germany, France and Spain, where it accounts for 15% of the primary energy, out of which 80% is used in electricity supply. The coal (lignite) mines from the Oltenia region contribute significantly to generating power in Romania. The study aims to show that an increase in production within the coal (lignite) mining industry can be determined by increasing direct and indirect costs or by increasing variable costs and profit. We also examine the non-linear relation between variable costs and production on the one hand and between profit and production on the other hand. Our results show that there is a concave relationship between variable costs and production, and also a concave relationship between profit and production, which indicate that Romanian coal enterprises have an optimal production level that maximises both variable costs and their profitability. In addition, a robustness check of our results confirms that variable costs and profitability decrease as they move away from their optimal level.

Keywords:

1. Introduction

Any enterprise within the market economy needs to generate profit, otherwise the enterprise structure and activity are meaningless. Thus, in order to improve enterprise performance, the management of mining enterprise, assessed from an overall perspective, should coordinate all its efforts. The principles underlying the strategies of national security and national energy efficiency consist in maintaining a balanced mix of energy resources, with coal representing an important part of this mix. In the present study, we aim to show that increasing production in the coal (lignite) mining industry can be achieved via increasing direct and indirect costs, but also via increasing variable costs and profit. Moreover, on the one hand, we analyse the non-linear relation between variable costs and production and between profit and production, on the other hand. Following this analysis, our results indicate that there is a concave relationship between variable costs and production, but also a concave relationship between profit and production. Hence, it can be inferred that Romanian coal enterprises have an optimal production level that maximises both variable costs and the profitability linked to them. In addition, a robustness check confirms that variable costs and profitability decrease as they move away from their optimal level.

The first goal of the article consists in identifying to what extent physical output is influenced by direct and indirect costs, because such information is extremely useful in analysing production costs based on managerial accounting data. The second goal consists in investigating the relationship between production as dependent variable and fixed costs, variable costs and profit as independent variables, due to the fact that such investigation can provide useful insights in the financial analysis area. The third goal is to analyse whether profit is influenced by lignite production, fixed costs and variable costs. Last but not least, we investigate to what extent physical output influences variable costs and the profit of mining companies.

The novelty of the article resides in the fact that, to the best of our knowledge, we conducted the first empirical research focused on costs within Romanian surface coal mining enterprises. Economic theory stipulates that, despite an increase in production, indirect and fixed costs remain constant. As a contribution, we show that production is mainly influenced by direct, indirect and variable costs. According to our results, fixed costs have no influence on production, because such costs tend to grow in line with production increase. Another important contribution of our study consists in the fact that, unlike previous studies in the literature, we find optimal Romanian coal enterprises register an optimal production level that maximises both variable costs and related profitability. The robustness check confirms that variable costs and profitability decrease as they move away from their optimal level when taking into account coal production specific to the Romanian coal mining industry.

Our results show that a cost increase could lead to an increase in coal production, which may generate a boost in economic efficiency especially when costs are constant or increasing. By the same token, our empirical research highlights the extent to which coal production can influence variable costs and profit in order to establish the maximum levels of variable costs and profit, which are useful for performing the cost-volume-profit analysis.

The reminder of the article is structured as follows: a Literature Review highlights relevant studies tackling the problem of costs within industries, with a special focus on the coal mining industry. The sections entitled Method and Research Hypotheses and Results present the hypotheses, the proposed linear and panel econometric models together with their estimated outcomes. The final part emphasises the main results of the study, limitations and avenues for future research.

2. Literature review

2.1. Brief overview of managerial and financial cost accounting

Regarding the advances in terms of costs within the area of managerial accounting, we took into consideration relevant articles from the literature. In his study, Ionescu (Citation2013) presents a manner of organising managerial accounting in order to calculate a cost on each type of manufactured product and to establish results obtained by each item and by the enterprise as a whole via correlating variable and fixed costs with the activity volume and the selling price. With regards to managerial cost accounting, Briciu, Capusneanu, and Topor (Citation2012) introduce a novel approach called SWOT-CM analysis, which can be successfully used to reach the strategic objectives of an enterprise. In another paper, Lepadatu (Citation2009) describes three methods of determining variable costs, emphasising the advantages and disadvantages of adapting the methods of variable costs to the Romanian general accounting plan.

According to Liu and Tyagi (Citation2017), a way of transforming fixed costs into variable costs within an outsourcing enterprise is by decreasing fixed costs (i.e., equipment expenditures, information technology, employees’ fixed salaries) and by turning these costs into a variable cost (i.e., the purchase price paid to the outside industry). Portz and Lere (Citation2010) analyse differences in cost centre practices with respect to cost classifications, adequate measures for cost changes, size and aim of cost centres. In their view, differences arise from the responsibility of the cost centre manager. Yükçü and Özkaya (Citation2011) show that, unlike traditional accounting theory, variable costs do not change in the same proportion as the volume of enterprise activity.

The importance of different types of costs for the cost-volume-profit analysis of non-profit organisations is tackled by Shim and Constas (Citation1997). They investigate factors like service level or units necessary to break even, the impact of changes in unit price, variable costs, service volume and fixed costs, change effects and appropriate strategies to break even. Lenghel (Citation2011) emphasises that, in the case of large Romanian entities, direct and indirect costs are located in several centres (departments). Hence, in order to apply the appropriate method of cost calculation in accordance with the production process, a new class of accounts is needed. Dina and Busan (Citation2009) explain that costs are key tools in making decisions about resource allocation (due to their scarce nature), volume and production structure, supply growth or withdrawal. Production cost is determined only at general level, but several factors are considered: distribution cost, labour cost, education cost, health, information, administration, time, debt, inflation, unemployment, etc.

Jonek-Kowalska and Turek (Citation2017) aim to identify and analyse the degree to which total production costs depend on production and infrastructure within the Polish hard coal mining industry. Their findings indicate that employment – a significant cost element of production and infrastructure – is not regarded as rational from an economic standpoint when considering its ratio to total production costs. Therefore, unit costs of mining production are not influenced by substantial decreases in employment or infrastructure, due to the high level of fixed costs. We find no significant relationships between infrastructure parameters and total production cost. Puzder et al. (Citation2017) report that the cost ratio, used in the production analysed process, represents an important mechanism of any mining company and a fundamental management instrument in the mining industry. Their approach consists of constructing three models that include the 100% level of production volume and various types of overhead costs included in the production process. Magda (Citation2016) indicates possible methods of reducing the production unit cost of a mining company via a decrease in the fixed unit cost. Using data from the U.S. copper industry over the period 1975–1990, Tilton (Citation2001) provides empirical evidence that mine survival depends more on labour productivity than on variable costs, especially at the beginning of a recession period.

2.2. Cost accounting and mining industry

Capusneanu et al. (Citation2016) report that enterprise performance within the mining industry may be improved by controlling costs through target costing method, which is an uncommon approach for the specificity of this industry.

Regarding the coal industry, relevant articles are provided by the literature. Thus, Epstein et al. (Citation2011) show that all stages in the coal life cycle produce waste stream and endanger the environment and people’s health to a great extent. Ignace (Citation1995) tackles the topic of accounting practices within Belgian coal mines by weighting them against contemporary textbooks. As a result, accounting practices and unit cost calculations differ significantly from textbook models. McNerney, Farmer, and Trancik (Citation2011) investigate costs in the U.S. coal-fired electricity industry for the period 1882–2006 by analysing it with respect to coal price, transportation cost, energy density, thermal efficiency, plant construction cost, interest rate, capacity factor, operations and maintenance cost. Lee (Citation2011) reports an empirical study tackling environmental management accounting and environmental cost accounting. Collins and Dent (Citation1979) find that eliminating full cost accounting negatively impacts security returns of full cost firms, but not of successful efforts firms.

Kopacz (Citation2015) analyses tailings costs resulting from coal extraction and processing and concludes that, within the Polish coal mining industry, more than 30% of total coal production is represented by extractive waste. The study quantifies the impact of tailings on economic efficiency and operating costs within a hypothetical coal mine throughout its life cycle. Michalak and Nawrocki (Citation2015) analyse 12 Polish coal companies with respect to inventory quotations for mining enterprises under examination and benchmark stock indices with the purpose of determining the prospects for coal development on the global market. Rybak and Rybak (Citation2016) analyse the coal production process in Poland based on indicators such as productivity, marginal productivity and input replacement. According to their results, the process of coal extraction is subject to decreases in scale economies, average and marginal productivity due to a misuse of available production factors. Authors conclude that such effects endanger the future of mining companies, therefore reducing production costs would be advisable.

Concerning the coal price in China, Li, Zhou, and Lu (Citation2009) analyse the economic conditions of coal mining and show that total coal cost influences coal prices and optimal resource allocation. Consequently, market pricing and government oversight are needed to ensure the full cost of coal resources. Tang and Peng (Citation2017) investigate Chinese coal production during the period 2007–2009 and conclude that total average value of production, inventory value and the extraction profits increased in the period 2007–2009. Moreover, massive coal imports did not influence the industry in the year 2009. Although few Chinese coal companies directed their products towards foreign markets, average export prices were quite significant. Therefore, the elasticity of capital outflow was higher than the elasticity of labour force, causing a decrease in mining and coal industry. Cui and Wei (Citation2017) analyse the distortion in the price of thermal coal when taking into account market forces. According to the researchers, the price of thermal coal is influenced by many variables among which: the price of electricity; the predictable elasticity of an enterprise within the electricity industry; the price elasticity of coal supplies. Taheri, Irannajad, and Ataee-Pour (Citation2011) show that capital cost is computed as the weighted cost of different financing sources (e.g., equity, debt). In their view, estimating equity cost is a fundamental part in this process and it requires financial modelling most of the times. Results show that market return rate has a direct impact on the cost rate of stocks.

Referring to the South African mining industry, Tholana, Musingwini, and Njowa (Citation2013) show that various factors influence the performance of cash costs. By using a simple algorithm for generating cost curves, the authors demonstrate the role of industry-built curves in analysing mining costs performance for three selected minerals. Korte (Citation2015) reports that coal processing industry should use low-yielding coal in the process of obtaining high quality products. This solution would not only maintain quality standards, but it would also ensure profitability.

In the paper by del Rosal Fernandez (Citation2000), welfare effects of Spanish coal policy during the period 1989–1995 are estimated. According to the results, coal policy engenders substantial conventional costs in all industrial sectors, especially in the most lucrative ones. Therefore, creating and maintaining jobs in the coal-mining sector seems rather costly. Stoker et al. (Citation2005) investigate labour productivity in the U.S. coal mining industry by means of productivity change indices and find that technical progress is captured by the fixed effects of coal exploration. Mitch (Citation1995) reports an alternative method of calculating profitability within the coal mining industry by examining efficiency increase from capital inflow and exploitation practices. Shafiee and Topal (Citation2012) estimate operating costs and capital costs of coal mining industry using a novel econometric approach and compare results with data for a surface coal mine retrieved from Cost Mine and Sherpa databases. Authors report that operating costs are negatively influenced by capital cost and production rate. Kecojevic and Grayson (Citation2008) analyse U.S. coal reserves and coal industry from a historical perspective, with a particular emphasis on the number of mines, total output, productivity, staff, safety and environmental records.

Callahan, Gabriel, and Smith (Citation2009) apply analytical and simulation techniques in order to investigate to what degree production decisions and firm profitability are influenced by inter-firm cost correlation, investment and accuracy of product cost in an imperfect competitive market. To substantiate research hypotheses, they propose an analytical model that takes into account I.T. investment, inter-firm cost correlation and a product cost report. Authors illustrate that production decisions based on inter-firm cost correlation imply lower I.T. investment levels and generate higher profitability. Kostamis, Beil, and Duenyas (Citation2009) investigate how buying decisions are influenced by additional suppliers, by the link between supplier production costs and cost adjustments, as well as by additive and multiplicative total cost functions. Conrad (Citation2005) considers the degree to which accounting (i.e., current cost accounting) influences perceptions of financial performance and regulatory decisions. Bryant (Citation2003) examines two different accounting methods that are applied in the case of exploration and development expenditures within oil and gas enterprises.

With respect to steel industry, Stratopoulos, Charos and Chaston (Citation2000) suggest a method for computing firm performance starting from neoclassical production theory. In their view, profitability can be predicted by the deviation of the average per-unit cost from the fitted value. Fleming et al. (Citation2000) investigate cost systems of Western Scotland enterprises that activate in shipbuilding, engineering and metals industries in the period 1900–1960. In the forest industry, studies attempt to provide more up-to-date information, because it has substantially decreased since the publication of the annual report series ended in 1999. For instance, Gale and Gale (Citation2006) aim to critically assess the 1997 annual report both from a social impact and a cost perspective.

Besides determining the degree of lean awareness and lean implementation, Sorokhaibam and Chandan (Citation2017) survey perceptions of barriers, enablers, potential benefits and tools concerning lean within the Indian coal mining industry. Al-Chalabi et al. (Citation2015) propose a linear regression between cost factors (i.e., acquisition, operating, maintenance; costs related to machine downtime) and the economic replacement time of production machines.

Piper and Green (Citation2017) investigate coal political economy corresponding to the second half of the twentieth century, with a special focus on the coal production revival in the 1960s that followed a decline in the post-war period. Van Zyl (Citation2015) reports on the relationship between production and productivity, cost, profitability within the African coal industry. Bansal and Bhave (Citation1995) emphasise that purchasing energy at the right price influences development to a great extent, especially when coal is a primary energy resource in the Indian economy.

In this study, we investigate how production is influenced by direct and indirect costs, as well as by fixed and variable costs. In the same token, we focus on the relationship between profit and coal production, fixed costs and variable costs. Moreover, we are also interested in whether there is a U-shaped relationship between variable costs and production, as well as between profit and production when analysing a sample of Romanian coal (lignite) mining enterprises over a period of 24 years.

3. Method and research hypotheses

Our approach is focused on identifying ways to improve three surface coal (lignite) mining enterprises with seven subunits located in the Oltenia coal (lignite) basin, which provides around 70% of Romania’s lignite production. By analysing the period 1993–2016, we show how managerial accounting data on production, costs and profit reflect into the income statement, provided through financial accounting.

The process of cost calculation is quite complex: it requires a series of cost transfers between managerial accounts and an identification of indirect costs depending on products and services. In line with managerial accounting of surface exploitation in lignite quarries, total costs are divided into direct and indirect costs. Direct costs include expenditures that are identified on a particular calculation object (product, service, work, order, phase, activity, function, centre, etc.) from the moment they are incurred, such as the cost of raw materials used in production, energy consumed for technological purposes, direct labour (wages, insurance and social protection, etc.), other direct expenses.

Indirect costs include costs that cannot be identified and attributed directly to a particular item of calculation, but such costs concern the entire production of a subunit or enterprise as a whole, as following: depreciation of machinery and equipment, maintenance of sections and machinery, expenses with managing production subunits in cost centres.

In order to determine the break-even point, total costs can be structured into variable costs and fixed costs. Variable costs are costs of basic subunits and include: material expenses, wages, other variable expenses (electricity, water, and steam for technological needs) and distribution expenses. In the case of surface mining, the basic subunits are lignite quarries and conveyor belts for coal transportation. Therefore, variable costs depend on the production volume.

Fixed costs refer to expenditures with a relatively unchanged size or expenditures that change in insignificant proportions with the rise or fall of production volume. Fixed costs include material expenses, wages and other fixed costs of ancillary (maintenance, repair), departmental and mining management. To a large extent, the amount of fixed costs depends on the time factor and production capacity of the enterprise (machinery depreciation, plant), on expenditure with the maintenance of production structures, and on various expenses regarding the organisation, administration and production management.

Therefore, analyses were conducted on data regarding several variables retrieved from three mining enterprises in Romania, pertaining to the period 1993–2016. These variables are: production (Q) measured in thousands of tons of coal; direct costs (DC); indirect costs (IC); variable costs (VC); fixed costs (FC); profit (PR). Excepting the first variable, all the other variables are expressed in million lei.

Our empirical research is based on the following hypotheses:

H1: An increase in direct and indirect costs causes an increase in production.

H2: An increase in variable costs and profit determines an increase in coal (lignite) production.

H3: An increase in production determines an increase in the profit of coal mining enterprises.

H4: There is a non-monotonic relationship between variable costs and production of coal in Romanian enterprises.

H5: There is a concave relationship between profit and coal production.

The research was divided in two parts. In the first part, we study the link between the abovementioned variables, according to the following three linear econometric models:

where:

represents fixed-firm effects intended to control for time-invariant firm-specific factors;

In order to compensate for omitting other factors that influence production or profitability, the specific unobserved effect () of an enterprise should be considered. As with time common shocks have an impact on the dependent variable, we also run parameter estimation with and without fixed effects.

In the second part of our research, we are interested to see whether there is a U-shaped relationship between variable costs and production, on the one hand and between profit and production, on the other hand. The existence of such relationships implies the necessity to optimally dimension production and fixed costs so as to obtain maximum profitability within the mining industry. In this respect, we test the following panel econometric models:

If in model 4 parameter there is a maximum point of the relationship between variable costs and production. Starting with this production level, variable costs tend to decrease, therefore this level can be considered as the minimum production point. Similarly, if in model 5 parameter

there is a maximum point of the relationship between profit and production. Exceeding this maximum leads to a decrease in the profitability of the mining activity.

4. Results

The estimations of production and profit models are presented in .

Table 1. Estimations of production and profit via econometric models.

4.1. Model 1

In the first equation of this model, the value 0.802 of the coefficient of determination (R2) indicates that the model is representative for estimating the relationship between the dependent variable Q and independent variables DC and IC. In this case, there are no fixed time effects. The robust t-statistic for DC of 2.21 indicates statistical significance at 5% level. For IC, the robust t-statistic of 0.65 indicates statistical non-significance. In this equation, one can see that a change of one million lei in DC will increase coal production with 28.39 thousands of tons.

In the second equation, when taking into account fixed time effects, the robust t-statistic for variable DC of 3.64 indicates statistical significance at 1% level. For variable IC, the robust t-statistic of 2.64 indicates statistical significance at 5% level. In this case, a one-million lei increase in direct costs generates a production increase of 47.61 thousand tons of coal. Furthermore, an increase in indirect costs of one million lei generates a boost in production of 8.32 thousand tons of coal. In addition, the 0.802 value for the coefficient of determination (R2) indicates that the model is representative for the relationship studied.

4.2. Model 2

In the first equation (without time series effects), the value 0.799 of the coefficient of determination (R2) indicates that the model is representative for the relationship between the dependent variable Q and independent variables FC, VC and PR. The robust t-statistic for FC of −1.25 indicates statistical non-significance. For variable VC, the robust t-statistic of 6.73 shows a statistical significance at 1% level. Furthermore, in the case of the independent variable PR, the robust t-statistic of 4.77 indicates a statistical significance at a 1% level. As it can be inferred, a one million lei increase in fixed costs triggers a decrease in production of 9.31 thousand tons of coal. At the same time, a one million lei increase in invariable costs and profit generates a change in production of 33.09 and a change of 24.01 thousand tons of coal.

In the second equation, when taking into account fixed time effects, the robust t-statistic for FC of 0.51 indicates statistical non-significance. For variable VC, the robust t-statistic of 3.82 indicates statistical significance at a 1% level. In addition, in the case of the independent variable PR, the robust t-statistic of 2.98 shows statistical significance at 1% level. If fixed costs increase with one million lei, production boosts with 3.504 thousand tons of coal. At the same time, a one million lei increase in variable costs and profit determines a change in production of 36.53 and a change of 29.05 thousand tons of coal.

4.3. Model 3

The value 0.364 of the coefficient of determination (R2) in the first equation (without time series effects) indicates that 35.4% of PR variance is explained by the independent variables Q, FC and VC. In addition, the robust t-statistic for FC of 0.71 indicates statistical non-significance. In the case of VC, the robust t-statistic of −0.91 indicates statistical non-significance. In the case of the independent variable Q, the robust t-statistic of 3.46 indicates statistical significance at 1% level. In this situation, a one million lei increase in fixed costs triggers a 0.294 million lei profit surplus. Furthermore, a one million lei increase in variable costs generates a 0.235 million lei decrease in profit. Finally, an increase in production of 1,000 tons of coal generates a change in the profit of 0.006 million lei.

In the second equation, when taking into account fixed time effects, the robust t-statistics for FC of 1.16 and for VC of −1.25 indicate statistical non-significance. For the independent variable Q, the robust t-statistic of 4.47 indicates statistical significance at 1% level. In this case, a one million lei increase in fixed costs determines a 0.398 million lei profit surplus. Furthermore, a one million lei increase in variable costs generates a 0.340 million lei decrease in profit. Finally, an increase in production of 1,000 tons of coal generates a change in profit of 0.007 million lei.

Estimates for variable costs and profit models are presented in .

Table 2. The estimations of variable costs and profit via econometric models.

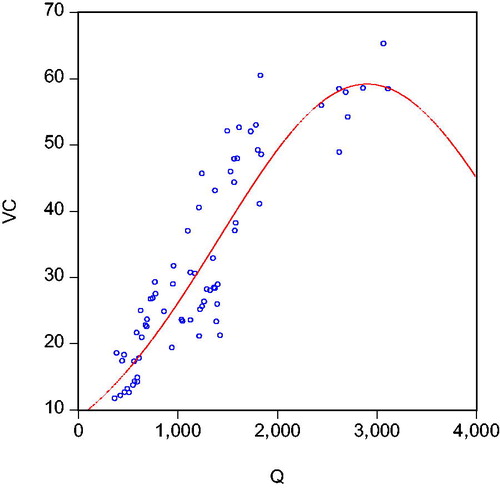

Graphically, the U-shaped relationship between variable costs and production is presented in .

4.4. Model 4

The dependent variable is VC. The value 0.890 of the coefficient of determination (R2) in the first equation (without time series effects) indicates that the model is representative for the relationship analysed. The robust t-statistic for the constant of −2.89 indicates statistical significance at 1% level. For the variables Q, Q2 and FC, the robust t-statistics of 5.41, −3.91 and 12.08 indicate statistical significance at 1% level. In this case, a one-unit increase in the constant determines a 13.54 million lei decrease in variable costs. At the same time, an increase in Q and Q2 generates a 0.028 million lei increase in variable costs and a 0.004 million lei decrease in variable costs, respectively. In addition, a one million lei increase in fixed costs generates a 1.01 million lei increase in variable costs. As parameter (−0.0004), there is a maximum point in the relationship between VC and Q. Starting with this production level Q (70 thousand tons), variable costs tend to decrease and the level may be considered as the minimum production point.

In the second equation (with fixed time effects), the value 0.924 of the coefficient of determination (R2) indicates that the model is representative for the relationship between the variables analysed. The robust t-statistic for the constant equal to −4.05 indicates statistical significance at 1% level. For variables Q, Q2 and FC, the robust t-statistics of 5.34, −3.42 and 6.53 show statistical significance at 1% level. In this case, a unit-increase in the constant determines a 7.07 million lei decrease in variable costs. At the same time, an increase in Q and Q2 of 1,000 tons of coal generates a 0.021 million lei increase in variable costs and a 0.00036 million lei decrease in variable costs. Also, a one million lei increase in fixed costs determines a 0.991 million lei increase in variable costs. As parameter (−0.00036), one can state that there is a maximum point in the relationship between VC and Q. Starting with this level of production (58.33 thousand tons), variable costs tend to decrease and the level may be considered as the minimum production point.

The U-shaped relationship between variable costs and production is represented in .

Figure 1. The relationship between variable costs (VC) and production of coal (lignite) (Q).

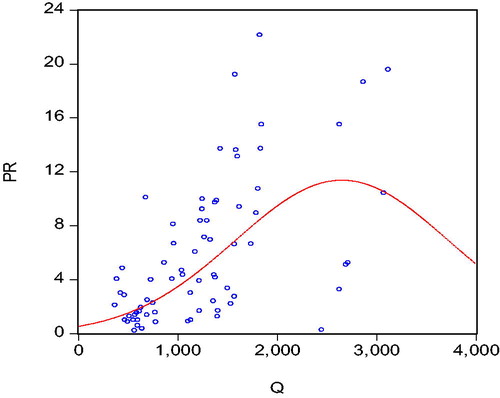

Figure 2. The relationship between profit (PR) and production of coal (lignite) (Q).

4.5. Model 5

In this model, the dependent variable is PR. The value 0.369 of the coefficient of determination (R2) in the first equation (without time series effects) shows that 36.9% of PR variance is explained by the independent variables Q, FC and VC. The robust t-statistic for the constant of −1.54 and for Q2 of −1.49 highlight statistical non-significance. In the case of the variables Q, FC and VC, the robust t-statistics of 2.34, 2.07 and −2.46 indicate statistical significance at 5% level. Furthermore, the significance value for the F-statistic is below 0.05, meaning that the variance explained by the model is not due to chance. In this case, an increase in Q generates a 0.016 million lei increase in profit. Moreover, a one million lei increase in fixed costs determines a 0.341 million lei increase in profit. Likewise, a one million lei increase in VC is followed by a 0.309 million lei decrease in profit. As parameter (−0.00002), there is a maximum point of the relationship between PR and Q. Exceeding this production maximum (Q = 800 thousand tons) leads to a decrease in the profitability of mining activity.

The value 0.483 of the coefficient of determination (R2) in the second equation (with time series effects) shows that 48.3% of PR variance is explained by the independent variables Q, FC and VC. The robust t-statistic for the constant equal to −1.56 indicates statistical non-significance. For the variable Q, the robust t-statistic of 2.62 indicates statistical significance at 5% level. In the case of Q2 and FC, the robust t-statistic of −1.85 and 1.89 indicates statistical significance at 10% level. For VC, the robust t-statistic of −2.63 indicates statistical significance at 5% level. In addition, the significance value for F-statistic is below 0.05, meaning that the variance explained by the model is not due to chance. In this case, a one-unit increase in the constant determines a 10.59 million lei decrease in profit. At the same time, an increase in Q and Q2 generates a 0.023 million lei increase in profit and a 0.00003 decrease in profit, respectively. Subsequently, a one-million lei increase in fixed costs determines a 0.540 million lei increase in profit and a one-million lei increase in VC is followed by a 0.433 million lei decrease in profit. As parameter (−0.00003), there is a maximum point in the relationship between PR and Q. Exceeding the maximum point (Q = 766.66 thousands of tons) leads to a decrease in the profitability of mining activity.

5. Conclusion

Our results show different connections between the costs system and profitability in the Romanian coal mining enterprises. Thus, through the first model we show that production depends significantly on direct costs and indirect costs which, to the best of our knowledge, is a novelty in the literature. The coefficient of determination indicates that the model is representative for the relationship between the abovementioned variables. In the same token, based on model 2, we conclude that production also depends significantly on fixed costs, variable costs and profit. Once more, the coefficient of determination registers a high value, meaning that the model is representative for the relationship between production, fixed costs, variable costs and profit.

Based on the values for the coefficient of determination in model 3, it can be stated that the model is 50% representative for the relationship between profit and production, direct costs and indirect costs.

Results from both equations in model 4 indicate that the model is representative for the non-monotonic relationship between variable costs and production. At the same time, the robust t-statistic indicates statistical significance at 1% level. Furthermore, results from the equations in model 5 show that the model is representative for the concave relationship between profit and production. Moreover, the robust t-statistic indicates statistical significance at 5% and 10% levels. The existence of these relations implies the necessity of optimally dimensioning production as well as fixed expenditures in order to obtain maximum profitability within the mining industry. Moreover, we emphasise that, in order to reach an optimal dimensioning of production and fixed costs, one has to continuously reduce variable costs so as to obtain a maximum level of profitability in the coal mining industry.

From the analyses presented above, we conclude that such models facilitate the computation of marginal production and marginal profit since the relationship between the dependent and the independent variables (see first three models) is a linear one. Marginal production and marginal profit are determined as first order derivatives of the proposed regression function.

In the surface coal mining enterprises, subunits are organised on cost centres. Hence, dividing costs into direct and indirect is very important for the process of managing mining subunits in order to establish measures of diminishing costs depending on the coal production volume.

In our opinion, dividing costs into variable and fixed is an important step both at the level of the mining enterprise and its subunits because it allows managers to assess the breakeven point of the whole coal production and to take adequate measures in order to increase coal production above this minimum threshold and to generate profit. It is generally known that when a mining enterprise produces a minimum threshold of coal, it registers losses, but above this minimum threshold it generates profit.

From an economic standpoint, it is fundamental for managers to understand the optimum ratio between direct and indirect costs, on one hand, and between variable and fixed costs, on the other hand, in order to maximise the performance of the mining unit. In the Romanian managerial accounting, direct and indirect costs represent the basis for computing the cost/ton of coal (lignite). Moreover, fixed and variable costs are financial instruments that play an essential role in establishing the breakeven point of coal production, namely the point at which all fixed costs and some of the variable costs are covered from selling the coal (lignite) production volume. If until reaching the minimum coal production threshold one could talk about an inefficient mining activity, above such threshold one talks about an increase in economic efficiency as coal (lignite) production increases.

By knowing the levels of direct and indirect costs, managers are able to take decisions that entail cost reduction or production increase via these cost types. For instance, reducing direct wage costs can be achieved either by expanding the mechanisation and automatisation of the processes related to excavation, transportation and sorting of coal from sterile in all enterprises operating in the analysed coal field, or by increasing work productivity. This way, the cost per ton of lignite will decrease and, at the same time, the profit of the mining company will increase. Moreover, a decrease in the indirect costs should represent a permanent care for managers, who can resize the staff from auxiliary departments and administration.

The research also focuses on methods of increasing production through costs and on methods of increasing profit through production. One finding we report is that profit can be increased by diminishing fixed and variable costs in the coal mining industry, which is one of the most polluting industries in the world.

Regarding the limits of the study, our research is based on data retrieved from the three major coal mining Romanian enterprises, which produced over 70% of Romanian lignite production during 24 years. Secondly, we estimated models using fixed effects, although the presence of specific transverse or temporal effects may be elicited by using techniques for both fixed and random effects. Since the period analysed 1993–2016 is too short to use random effects, we used fixed effects to control for some external influences on the relationship between the phenomenon and variables, such as the global financial crisis. Moreover, our article could be regarded as very specific and focused on the coal mining industry.

In terms of avenues for future research, these models could also be applied in the case of coal mining enterprises from the European Union, the U.S., China, South Africa or Brazil. Furthermore, in order to estimate models for the coal mining industry, one could consider other control variables, such as the adoption of the euro, the evolution of exchange rates and inflation indices in E.U. countries, the evolution of public debt ratios, the price per ton of coal, the unit cost per ton of coal.

Acknowledgements

The authors would like to thank the management of Oltenia Coal Energy Complex for their help in data collection.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Related Research Data

References

- Al-Chalabi, H. S., Lundberg, J., Al-Gburi, M., Ahmadi, A., & Ghodrati, B. (2015). Model for economic replacement time of mining production rigs including redundant rig costs. Journal of Quality in Maintenance Engineering, 21(2), 207–226. doi: 10.1108/JQME-07-2014-0041

- Bansal, N. K., & Bhave, A. (1995). Cost to the Indian economy of mining coal. Energy Sources, 17(2), 195–212. doi: 10.1080/00908319508946078

- Briciu, S., Capusneanu, S., & Topor, D. (2012). Developments on SWOT analysis for costing methods. International Journal of Academic Research, 4(4), 142–150.

- Bryant, L. (2003). Relative value relevance of the successful efforts and full cost accounting methods in the oil and gas industry. Review of Accounting Studies, 8(1), 5–28. doi: 10.1023/A:1022645521775

- Callahan, C. M., Gabriel, E. A., & Smith, R. E. (2009). The effects of inter-firm cost correlation, IT investment, and product cost accuracy on production decisions and firm profitability. Journal of Information System, 23(1), 51–78. doi: 10.2308/jis.2009.23.1.51

- Capusneanu, S., Topor, D. I., Rakos, I. S., Ducu, C., & Tepes-Bobescu, A. (2016). Improving performances by using cost controlling in the mining industry entities. Annals of the “Constantin Brancusi” University of Targu Jiu, Economy Series, 3, 98–108.

- Collins, D. W., & Dent, W. T. (1979). The proposed elimination of full cost accounting in the extractive petroleum industry. An empirical assessment of the market consequences. Journal of Accounting and Economics, 1(1), 3–44. doi: 10.1016/0165-4101(79)90013-2

- Conrad, L. (2005). The role of current cost accounting for financial reporting and regulation in utility industries. Public Money & Management, 25(2), 115–122. doi: 10.1111/j.1467-9302.2005.00461.x

- Cui, H., & Wei, P. (2017). Analysis of thermal coal pricing and the coal price distortion in China from the perspective of market forces. Energy Policy, 106, 148–154. doi: 10.1016/j.enpol.2017.03.049

- del Rosal Fernandez, I. (2000). How costly is the maintenance of the coal-mining jobs in Europe? The Spanish case 1989-1995. Energy Policy, 28(8), 537–547.

- Dina, I. C., & Busan, G. (2009). The necessity of lowering production cost in the management of coal mining units. Annals of the University of Petrosani, Economics, 9(3), 219–222.

- Epstein, P. R., Buonocore, J. J., Eckerle, K., Hendryx, M., Stout, B. M., Heinberg, R., … Glustrom, L. (2011). Full cost accounting for the life cycle of coal. Annals of the New York Academy of Sciences, 1219(1), 73–98. doi: 10.1111/j.1749-6632.2010.05890.x

- Fleming, A. I. M., McKinstry, S., & Wallace, K. (2000). Cost accounting in the shipbuilding, engineering and metals industries of the West of Scotland. Journal of Accounting and Business Research, 30(3), 195–211. doi: 10.1080/00014788.2000.9728936

- Gale, R., & Gale, F. (2006). Accounting for social impacts and costs in the forest industry, British Columbia. Environmental Impact Assessment Review, 26(2), 139–155. doi: 10.1016/j.eiar.2005.02.002

- Ignace, D. B. (1995). Industrial accounting theory and practice: Cost accounting in the Belgian coal industry during the first half of the twentieth century. Accounting, Business & Financial History, 5(1), 71–108. doi: 10.1080/09585209500000032

- Ionescu, I. (2013). Considerations regarding the purpose of direct costing method in a company’s management. Annals of the “Constantin Brancusi” University of Targu Jiu: Economic Series, 2(2), 37–41.

- Jonek-Kowalska, I., & Turek, M. (2017). Dependence of total production costs on production and infrastructure parameters in the Polish hard coal mining industry. Energies, 10(10), 1–22. doi: 10.3390/en10101480

- Kecojevic, V., & Grayson, L. R. (2008). An analysis of the coal mining industry in the United States. Minerals & Energy, 2, 74–83. doi: 10.1080/14041040802181790

- Kopacz, M. (2015). Evaluation of the waste rock management costs as a function of the level of coal yield on the example of the coal mine. Gospodarka Surowcami Mineralnymi-Mineral Resources Management, 31(3), 121–144. doi: 10.1515/gospo-2015-28

- Korte, G. J. (2015). Processing low-grade coal to produce high-grade products. Journal of the Southern African Institute of Mining and Metallurgy, 115(7), 569–572. doi: 10.17159/2411-9717/2015/v115n7a2

- Kostamis, D., Beil, D. R., & Duenyas, I. (2009). Total-cost procurement auctions: Impact of suppliers’ cost adjustments on auction format choice. Management Science, 55(12), 1985–1999. doi: 10.1287/mnsc.1090.1086

- Lee, K. H. (2011). Motivations, barriers, and incentives for adopting environmental management (cost) accounting and related guidelines: A study of the Republic of Korea. Corporate Social Responsibility and Environmental Management, 18(1), 39–49. doi: 10.1002/csr.239

- Lenghel, R. D. (2011). Cost calculations particularities in the context of new accounting regulations. Review of Management & Economic Engineering, 10(4), 143–152.

- Lepadatu, G. V. (2009). Variable costs method. Application variants adapted to Romanian accounting plan. Theoretical & Applied Economics, 16(9), 41–50.

- Li, A., Zhou, M., & Lu, M. (2009). Economic analysis and realization mechanism design for full cost of coal mining. Procedia Earth and Planetary Science, 1(1), 1686–1694. doi: 10.1016/j.proeps.2009.09.259

- Liu, Y., & Tyagi, R. K. (2017). Outsourcing to convert fixed costs into variable costs: A competitive analysis. International Journal of Research in Marketing, 34(1), 252–264. doi: 10.1016/j.ijresmar.2016.08.002

- Magda, R. (2016). Ways of rationalization of unit cost of production in the mining company. Inzynieria Mineralna-Journal of the Polish Mineral Engineering Society, 2, 145–152.

- McNerney, J., Farmer, J. D., & Trancik, J. E. (2011). Historical costs of coal-fired electricity and implications for the future. Energy Policy, 39(6), 3042–3054. doi: 10.1016/j.enpol.2011.01.037

- Michalak, A., & Nawrocki, T. L. (2015). Comparative analysis of the cost of equity of hard coal mining enterprises: An international perspective. Gospodarka Surowcami Mineralnymi, 31(2), 49–71. doi: 10.1515/gospo-2015-0017

- Mitch, A. (1995). Coal mining productivity. Coal, 100(12), 34–38.

- Piper, L., & Green, H. (2017). A province powered by coal: The renaissance of coal mining in late twentieth-century Alberta. Canadian Historical Review, 98(3), 532–567. doi: 10.3138/chr.4248

- Portz, K., & Lere, J. C. (2010). Cost center practices in Germany and the United States: Impact of country differences on managerial accounting practices. American Journal of Business, 25(1), 45–52. doi: 10.1108/19355181201000004

- Puzder, M., Pavlik, T., Molokáč, M., Hlavnova, B., Vavercak, N., & Samaneh, I. B. A. (2017). Cost-ratio model proposal and consequential evaluation of model solutions of manufacturing process in mining company. Acta Montanistica Slovaca, 22(3), 270–277.

- Rybak, A., & Rybak, A. (2016). Possible strategies for hard coal mining in Poland as a result of production function analysis. Resources Policy, 50, 27–33. doi: 10.1016/j.resourpol.2016.08.002

- Shafiee, S., & Topal, E. (2012). New approach for estimating total mining costs in surface coal mines. Mining Technology, 121(3), 109–116. doi: 10.1179/1743286312Y.0000000011

- Shim, J. K., & Constas, M. (1997). Does your nonprofit break even? How to come out even. The CPA Journal, 67(12), 36–42.

- Sorokhaibam, K., & Chandan, B. (2017). Lean awareness and potential for lean implementation in the Indian coal mining industry: An empirical study. International Journal of Quality & Reliability Management, 35(6), 1215–1231. doi: 10.1108/IJQRM-02-2017-0024

- Stoker, T. M., Berndt, E. R., Ellerman, D. A., & Schennach, S. M. (2005). Panel data analysis of U.S. coal productivity. Journal of Econometrics, 127(2), 131–164. doi: 10.1016/j.jeconom.2004.06.006

- Stratopoulos, T., Charos, E., & Chaston, K. (2000). A translog estimation of the average cost function of the steel industry with financial accounting data. International Advances in Economic Research, 6(2), 271–286. doi: 10.1007/BF02296108

- Taheri, M., Irannajad, M., & Ataee-Pour, M. (2011). Estimation of the cost of equity for mining and cement industries by single-index market model. Gospodarka Surowcami Mineralnymi-Mineral Resources Management, 27(2), 169–188.

- Tang, E., & Peng, C. (2017). A macro- and microeconomic analysis of coal production in China. Resources Policy, 51, 234–242. doi: 10.1016/j.resourpol.2017.01.007

- Tilton, J. E. (2001). Labor productivity, costs, and mine survival during a recession. Resources Policy, 27(2), 107–117. doi: 10.1016/S0301-4207(01)00012-5

- Tholana, T., Musingwini, C., & Njowa, G. (2013). An algorithm to construct industry cost curves used in analyzing cash cost performance of operations for selected minerals in South Africa. Journal of the Southern African Institute of Mining and Metallurgy, 113(6), 473–484.

- van Zyl, Z. (2015). Visions for challenging assets in the South African coal sector. Journal of the Southern African Institute of Mining and Metallurgy, 115(7), 653–658. doi: 10.17159/2411-9717/2015/v115n7a12

- Yükçü, S., & Özkaya, H. (2011). Cost behavior in Turkish firms: Are selling, general and administrative costs and total operating costs “sticky”? World of Accounting Science, 13(3), 1–27.