?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Our study aims to quantitatively assess some of the determinants of shadow banking dynamics in 11 European Union (E.U.) countries from Central and Eastern Europe (C.E.E.) over the period 2004–2017. Using panel data estimation techniques and a quarterly data set compiled from several publicly available data sources, we alternatively evaluate the impact of six macroeconomic and financial variables on two dependent variables corresponding to two different measures of the shadow banking sector, namely the broad one (including all non-monetary financial institutions, except insurance corporations and pension funds) and the narrow one (excluding from the above one the investment funds, other than money market funds [M.M.F.]). Our findings confirm that shadow banking is sensitive to overall macroeconomic conditions and that economic growth positively influences the expansion of this segment of the financial sector. In addition, a higher demand for funds from institutional investors, which also reveals a more developed financial system, supports the expansion of the shadow banking sector. Moreover, in a low interest rate environment, the search for yield makes investors turn to shadow banks, while the development of the shadow banking sector is also found to be complementary to the development of the rest of the financial system, in particular, traditional banks.

1. Introduction

Shadow banking has become more significant in recent years, especially during and after the financial crisis of 2007/2008. Although this less-regulated sector of the financial system continues to increase, and the studies and speeches around the topic abound, there is yet no single, generally accepted definition and no suitable form of measurement to accommodate the particularities of the sector in different countries. The phenomenon has been nonetheless tackled by members of the academia as well as various international financial bodies, thus revealing the importance of the topic, although most of the studies and reports focus on the cases of the U.S., the euro area, and the U.K.

An overall survey of previous studies shows that advanced economies are the ones researchers usually prefer to focus on, mainly because there is more data on the shadow banking system in such countries. When looking at the shadow banking system in these economies, one can easily notice that the credit intermediation process comprises multiple steps, various partners connected by complex linkages, as well as a peculiar and sophisticated relationship with the traditional banking system or other components of the financial system. In the shadow banking systems of emerging market and developing economies (as those in Central and Eastern Europe [C.E.E.]) the processes and relationships are not so complex and diverse. Having shared a socialist central planning system in the past, these particular countries are still making significant efforts towards establishing a well-functioning financial system (Du, Li, & Wang, Citation2017), in this way depriving shadow banking of a context that could allow its institutions and activities to flourish. In addition, the main entities that form the shadow banking system in C.E.E. are simple and very easy to identify (Ghosh, Gonzalez del Mazo, & Ötker-Robe, Citation2012). Therefore, the simplicity, recent development and lack of data are some of the reasons why the C.E.E. countries have generally been deprived of a thorough analysis of the phenomenon. Previous studies that refer to these particular countries usually dedicate to them only a minor section in their whole research.

To fill this gap, the current study aims to empirically assess how different variables from the macroeconomic and financial environment influence the dynamics of the shadow banking sector in the C.E.E. economies. Using panel data estimation techniques on a quarterly data set compiled for a group of 11 New European Union (E.U.) member states from C.E.E. and almost 13 years (2004Q2–2017Q1) we address the following research question: which are the macro determinants that significantly influence the expansion of shadow banking in C.E.E?

Based on previous evidences, we formulate and test the validity of the following hypotheses: (1) the overall macroeconomic and global liquidity conditions have positive effects on the development of shadow banking (the procyclicality and high liquidity hypotheses); (2) the search for yield makes investors turn to shadow banks and, therefore, positively influences the development of this sector (the search for yield hypothesis); (3) the development of the shadow banking system is complementary to the development of the rest of the financial system (the complementarity hypothesis); and (4) the higher the demand from institutional investors is, the more developed the shadow banking system is (the institutional cash pool hypothesis).

Our article contributes to enhancing knowledge on shadow banks in two major ways. Firstly, it provides both a theoretical and quantitative analysis of the phenomenon, whilst most pre-existing studies address only conceptual issues related to the different facets of shadow banking (e.g. definition, measurement, dynamics, potential triggers, and risks to the overall financial stability). Secondly, it offers a perspective on shadow banking development and its drivers in the European countries, in particular in the 11 New EU Member States from C.E.E. This contribution may be very relevant since the bulk of existing literature focuses on the U.S., whereas the European shadow banking system has quite different features compared to the later (Jeffers & Plihon, Citation2016). Also, to our knowledge, this is the first empirical article entirely dedicated to assessing the determinants of shadow banking’s dynamics in the C.E.E. countries.

The remainder of the article is organised as follows: Section 2 outlines the developing approaches on shadow banking and overviews some of the main theoretical and empirical findings on its determinants; Section 3 emphasises the main common characteristics of C.E.E. countries and particularities of their shadow banking systems, in this way providing a rationale for a separate analysis of the determinants of shadow banking dynamics in this regional group; Section 4 presents the data and methodology employed in the manuscript; and Section 5 discusses the results. The last Section of the article outlines the conclusions of the research.

2. Short literature survey on shadow banking and its determinants

When narrowing down the meaning of ‘shadow banking’ to a complex and peculiar process of credit intermediation that takes place outside the regulated banking system, one could trace this phenomenon decades ago. However, the concept was first employed in this form more then ten years ago, in a speech held by the economist Paul McCulley (Citation2007) at the annual financial symposium hosted by the Kansas City Federal Reserve Bank in Jackson Hole. Since then, the concept has been extensively used by members of the academia and international financial institutions alike, to an extent that it has acquired various and sometimes different definitions and interpretations. In fact, the ‘shadow economy’ term is not a firmly fixed concept in the literature, but subject to change and varying criteria (Bejaković, Citation2015) and also known by different names such as the hidden, grey, black, or informal economy (Hassan & Schneider, Citation2016).

The necessity of having a clear, precise and commonly agreed-upon definition of the concept is perfectly emphasised by Kabelik (Citation2012, p. 4): ‘if regulation is to be effective, it needs to be applied on accurately defined entities otherwise a potential for regulatory arbitrage emerges. Therefore, the discussion about the definition matters.’ However, the job of defining the concept is not simple, because of the amorphous character of the shadow banking itself, resulting from its high complexity, interconnectedness with other financial as well as non-financial institutions, and heterogeneity across systems and countries).

Some of the studies that first focused on analysing shadow banking were performed soon after McCulley’ s proposal, including here the ones of Adrian and Shin (Citation2009), Pozsar (Citation2008), Pozsar, Adrian, Ashcraft, and Boesky (Citation2010), and Tucker (Citation2010). To date, much of the literature on shadow banking originates in the staff reports developed by financial and monetary institutions, among which we include: the Federal Reserve System or the Fed, the International Monetary Fund (I.M.F.), the Financial Stability Board (F.S.B.), and the European Systemic Risk Board (E.S.R.B.).

After surveying the literature and analysing the multitude of definitions and specific approaches, some common characteristic can be agreed upon when ‘unpacking’ the concept of shadow banking, as pointed out below.

There is clearly a process of credit intermediation, associated with some forms of maturity and liquidity transformation as well as leverage. Unlike traditional banking, which implies a one-step transformation process (from deposits to loans), shadow banking presumes a more complex intermediation process consisting in a series of steps or ‘vertical slicing’; this specific process has been analysed in detail by Girasa (Citation2016, pp. 51–52). Bakk-Simon et al. (Citation2012) also broadly define the shadow banking system as all the activities related to credit intermediation, liquidity and maturity transformation that happen outside the regular banking system (this definition being accepted and used by the European Central Bank). An important driver in this regard is considered to be the process of ‘financial innovation’, a topic about which the standard economic theory has remarkably little to say (Guttmann, Citation2016).

There are no public safety nets (investors are not offered public guarantees if their funds are mismanaged by shadow banking institutions) and no access to central bank liquidity (shadow banks cannot request financial aid if they confront themselves with funding problems). The lack of public support is very well highlighted in the definition provided by Pozsar et al. (Citation2010): ‘shadow banks are financial intermediaries that conduct maturity, credit, and liquidity transformation without access to central bank liquidity or public sector credit guarantees’. Nonetheless, although shadow banking activity is removed from ‘official public-sector enhancements’, it typically receives indirect or implicit enhancements according to Adrian and Ashcraft (Citation2012).

The entities and activities in the ‘shadows’ are fragile and less regulated as opposite to traditional banking institutions, hence the frequent encounter of the ‘outside’ term in many definitions. ‘Less’ must not be confused with ‘lack’ because, although there are fewer restrictions, this does not mean that entities from the shadow banking system are entirely exempt from supervision and regulation; an example provided by Broos, Carlier, Kakes, and Klaaijsen (Citation2012) is the case of the shadow banking entities that form part of a financial group that is itself subject to supervision. Examples of definitions in this regard are the ones of Agresti (Citation2016), Bernanke (Citation2013), EC (Citation2012), FCIC (Citation2010), FSB (Citation2011), FSB (Citation2012a), Gennaioli, Shleifer, and Vishny (Citation2013).

The absence or trivial regulation associated with the lack or weak regulatory arbitrageurs in the shadow banking sector may drive the financial system towards a point of systemic fragility (associated with high levels of systemic risk). A proper definition of shadow banking in the view of the I.M.F. (Citation2014a) should cover also the relevant risk dimensions. In this regard, the institution identifies five specific risks, as follows: (1) run risk – see Adrian (Citation2014); (2) agency problems – see Adrian, Ashcraft and Cetorelli (Citation2013); (3) opacity and complexity – see Caballero and Simsek (Citation2009); (4) leverage and procyclicality – see (Brunnermeier and Pedersen (Citation2009); and (5) spillover effects – see Pozsar et al. (Citation2013).

One of the more widely recognised and accepted official (institutional) definitions of shadow banking is the one provided by the F.S.B. (Citation2012b) and includes the ‘entities and activities outside the regular banking system’ that ‘raise: (1) systemic risk concerns …; and/or (2) regulatory arbitrage concerns’. Nonetheless, there are also efforts made at the European level to gauge the phenomenon. The E.S.R.B. proposes a dual approach when investigating the potential financial stability risks of shadow banking-type activities in the E.U. (ESRB, Citation2016), in the sense that it looks for shadow banking threats that may rise either from financial institutions (‘entity-based approach’) or from their activities (‘activity-based approach’). Yet one of the most useful approaches in describing the shadow banking sector in Europe is provided by the European Economic and Social Committee (E.E.S.C.), which highlights that shadow banking activities occur both outside as well as partially inside the traditional banking system (EESC, Citation2012).

With regard to the forces that drove the development of the shadow banking sector in recent decades, theories and hypotheses abound. Some explanations can be traced in the more general framework of research on shadow economy. For instance, F. Schneider shows that ‘the increase of the intensity of regulations … as well as the increase of the tax and social security contribution burdens’ (Schneider, Citation2002) or ‘the poor quality of institutions, the inefficient application of tax laws, and the bureaucracy and corruption’ (Davidescu & Schneider, Citation2017) are drivers of the shadow economy. In many of his works, Schneider uses an innovative measure to estimate the dimension of the shadow economy of a specific country, namely the M.I.M.I.C. structural equation model. Based on this model he figures what variables can be considered drivers of a country’s shadow economy (Davidescu & Schneider, Citation2017; Hassan & Schneider, Citation2016). Basically, the M.I.M.I.C. model explicitly considers multiple causes, as well as multiple indicators of measuring the hidden economy. In our article, we use panel data estimation techniques to connect multiple causes but with a single indicator.

More potential drivers of shadow banking emerge from the survey of the previous literature in the field: tight banking regulation, economic growth, innovation, high demand from institutional investors, the search for yield, or the overall development of the financial sector – among others: Beck and Kotz (Citation2016), Bouveret (Citation2011), Caballero (Citation2010), Claessens et al. (Citation2012), Duca (Citation2016), Ghosh et al. (Citation2012), Goda, Lysandrou, and Stewart (Citation2013), Goda and Lysandrou (Citation2014), Gorton and Metrick (Citation2010), Helgadóttir (Citation2016), IMF (Citation2014b), Lysandrou and Nesvetailova (Citation2015), Perotti (Citation2013), and Pozsar et al. (Citation2013). The bulk of these studies is tackled within the content of the article and referred to when necessary. The inclination of financial institutions to avoid taxes, accounting rules, or capital requirements (arbitrage) is also a major driver of shadow banking expansion (Adrian & Ashcraft, Citation2012). In fact, tax burden is, in general, the main factor influencing the development of an unofficial economy or a ‘shadowy economy’ (Mikulić & Nagyszombaty, Citation2013). Moreover, some specific factors to each country also contributed to this outcome.

The theoretical framework with regard to shadow banking is quite a complex network of concepts and approaches. Arora and Zhang (Citation2018) overview the existing theories and dedicate a section in their work to the theoretical analysis. Nonetheless, for a comprehensive literature on the theories around ‘guaranteed off-balance sheet’ development (a form of expressing shadow banking, especially in China) one can look into the work of An and Yu (Citation2018). The authors develop their ideas around the following theories: regulation avoidance theory; moral hazard theory; risk diversification theory; market power theory; and scale economy theory.

Although theories explaining the reasons behind the emergence and development of shadow banks over the last decade abound, little empirical effort has been done until present days to assess the contribution of potential determinants. Among the first empirical works approaching this issue is that of Acharya, Khandwala, and Öncü (Citation2013) who analyse the case of an emerging market economy (India) and document that, in this particular case, banks see lending to non-deposit taking non-bank financial corporations as a substitute for direct lending in rural areas. Therefore, the insufficient bank branch network development in such areas could be considered an important driver of shadow banks development, complementary to the traditional banking system. Michael (Citation2014) finds as well that shadow banking serves as a complement to traditional banking in countries like South Africa or China, but in countries like Russia or Chile this unconventional funding system acts as a substitute.

Referring to the case of one single country, the U.S., Duca (Citation2016) examines the determinants of the credit supply from non-bank financial intermediaries to non-financial corporations (N.F.C.), which is one of the main dimensions of shadow banking activity. The author finds that, in the long-run, capital and reserve requirement arbitrage, together with information costs, are the main drives of shadow banking development. On the other hand, among the relevant short-term determinants are included the economic outlook, deposit regulation, event risk and risk premium. In addition, the shadow banking sector is found to be vulnerable to liquidity shocks and pro-cyclical.

A more extensive panel data analysis was conducted by the I.M.F.’s staff (IMF, Citation2014b) on a sample that mostly comprises developed countries and spans more than 20 years (1990–2013). The study highlights that the tighter banking regulations, possibly combined with ample liquidity conditions, and the rising demand from institutional investors are the main drivers of non-banking activities in the selected economies. Also, the study confirms the hypothesis of complementarity between shadow banks and the traditional banking system. Referring to a shorter period of time (2002–2013), Kim (Citation2016) confirms the same hypothesis for the G20 countries and emphasises that the development of shadow banking is significantly influenced by the demand from institutional investors.

For the euro area countries Malatesta, Masciantonio, and Zaghini (Citation2016) show that the loans granted by shadow banks to N.F.C.s (which could largely be considered a measure of shadow banking activity) more than doubled during 1999–2014, and that the macroeconomic variables used to control for domestic demand and supply conditions (in particular, the real G.D.P. growth rate, inflation rate, and the term spread) are by far the main determinants of this dynamics. In addition, the development of institutional investors sector is also found to be positively correlated with the lending activity of shadow banks.

Closer to our research, the study of Barbu, Boitan, and Cioaca (Citation2016) evaluates the macroeconomic determinants of shadow banking for a panel of 15 E.U. countries (among which four C.E.E. economies) and a time span of about eight years (2008Q1–2015Q3). Using the net value of the total assets of monetary funds as a proxy for shadow banking activity, the authors find that the dynamics of this sector is negatively influenced by G.D.P. growth, short-term interest rates, liquidity, and development of investment funds, and positively influenced by stock index dynamics and long-term interest rates.

Also looking at the situation of the European countries, Jeffers and Plihon (Citation2016) run a principal component analysis to evaluate two major groups of variables, one related to the main aspects of shadow banks’ activities and the other to the institutional environment in which these entities operate. One interesting result of their analysis is that nine C.E.E. countries form, based on the similarities in terms of the two principal components identified, a cluster separate from the other European countries, which could offer a rationale for our study.

The short overview of the literature on shadow banking and its determinants highlights that, despite the great interest for this topic, most studies are conducted for developed countries, while emerging markets and developing economies are deprived of a more in-depth analysis of the phenomenon. In particular, to our knowledge there is no empirical study explicitly dedicated to C.E.E. countries, where the shadow banking system has quite different features compared to other, more developed economies.

3. Characteristics of the Central and Eastern European countries and particularities of their shadow banking systems

The focus of our article is on C.E.E., in particular on the 11 countries belonging to this regional group that joined the E.U. so far, with five of them also in the eurozone. Among these countries, according to the I.M.F. there are five emerging and developing economies (namely Bulgaria, Croatia, Hungary, Poland, and Romania) and six advanced economies (the Czech Republic, Estonia, Latvia, Lithuania, Slovenia, and Slovakia) (IMF, Citation2018). However, the classification by the level of economic development varies depending on the classifying body. As Hampl (Citation2018) argues, the post-communist countries of Central Europe are typically classified as ‘developed’ by most governmental or international institutions (such as the I.M.F., the World Bank, and the E.B.R.D.), but as ‘emerging’ by various market institutions (F.T.S.E., M.S.C.I., Standard & Poor’s and J.P. Morgan, among others). Moreover, once a country enters the euro area it is almost automatically treated as developed, which is sometimes considered to be confusing and raise doubts. This was the case of the majority of our advanced C.E.E. countries, which progressively adopted euro in recent years (starting with Slovenia, in 2007). Therefore, although some of our C.E.E. economies are considered to be developed, they present features that are more typical to the emerging and developing countries from C.E.E. than to the advanced economies from Western and Northern Europe. Nonetheless, nobody can deny that the differences between the C.E.E. countries and the more developed E.U. economies tended to fade in time.

Despite some small differences in the degree of economic development, the C.E.E. economies shared the socialist central planning system in the past. Having overcome their background, these countries enrolled in a process of transition to market economy marked by country specific features and in various speeds. Once the transition process completed, the C.E.E. countries found themselves in similar stages of institutional development, financial and macroeconomic reform, as well as banking sector depth (IMF, Citation2010). In addition, the structure of the banking sector appears to be similar in C.E.E. countries (Ramotowski, Citation2015) and they share the same ‘condition of the financial markets’, making it easier to generate cross-country comparisons (Du et al., Citation2017, p. 538). Among other characteristics that the C.E.E. countries share, one can include: they are open economies, with average exports of about 80% of G.D.P. in 2017 (with the exception of Croatia, Romania and Poland, which have the largest domestic markets); they have already well-established EU legal rules and standards; they have low wages, educated workforce, and relatively fast economic growth, particularly in the pre-crisis period (Miklaszewska, Mikołajczyk, & Pawłowska, Citation2012); and they have similar stock market characteristics (Karanovic & Karanovic, Citation2018).

Long before their ascension in the E.U., the C.E.E. countries have been engaged in complex processes of bank reforms, economic restructuring and privatisation. After finally becoming a member of the E.U. family and before the 2008 financial crisis, these countries experienced vigorous banking growth against a background of rapid economic development. In addition, Andries (Citation2011) shows that the E.U. accession increased banking competition in the C.E.E. countries, which further led to higher average efficiency of banks. As the global financial crisis emerged, this dynamics was hampered and the traditional business model of banking intermediation (turning out to be the safest) was challenged. However, the resulting damages were not so important compared to the leading industrialised nations, which were more affected. Other common characteristics of the financial and banking sectors in the C.E.E.s that are still valid after more than a decade from the outburst of the crisis (turning these countries into a relatively homogeneous group) include (Miklaszewska et al., Citation2012, pp. 14–16): they have ‘a relatively liberal financial sector combined with large foreign ownership’; compared to the highly developed countries, banks in the C.E.E.s ‘remained small, following a traditional model of banking intermediation, and not presenting a significant systemic risk’ (but profitable); ‘foreign currency borrowing constitutes a significant risk’ (with different foreign exchange exposures across C.E.E. countries). Moreover, C.E.E. countries are host markets for banks owned by large cross-border banking groups primarily from the countries of the euro zone.

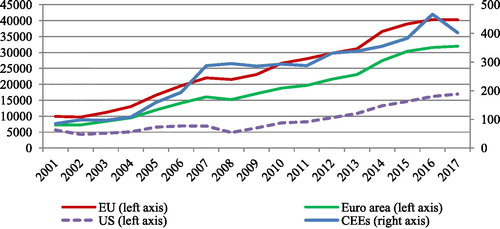

With regard to the shadow banking sector, the situation of C.E.E. countries is different in many respects compared to the other, more developed E.U. countries and the U.S. The data reflected in emphasise that prior to the crisis of 2008 shadow banking experienced a significant growth both in Europe and the U.S., fulfilling a very important role in lending within the financial system in particular, and the economy as a whole. During the period 2002–2007, the total assets of shadow banking institutions grew on average by 14.6% per year in the E.U. and 4.6% in the U.S. Although sharing a similar trend, the C.E.E. countries registered a higher expansion of this segment of the financial system, especially after 2004, clearly outpacing (in relative terms) the one in the E.U., the euro area, and the U.S. The total volume of assets of shadow banking institutions in C.E.E. countries grew on average by about 23% per year in 2002–2007. The steady expansion stopped during the crisis (the total assets of the shadow banking system amounted to around 290 billion euros during 2007–2011), but the upward trend was resumed afterwards and more sustainable this time.

Figure 1. Dynamics of shadow banking size (measured by the total non-consolidated assets of O.F.I.s and I.F.s expressed in billion euros) in C.E.E.s, E.U., euro area, and the U.S. Note: Data have not been available for the Czech Republic, in 2017. Source: Authors’ elaboration based on data from Eurostat (EC, Citation2018)

Although the shadow banking system has grown markedly in C.E.E. countries, its size remains relatively small, as also pointed out by Du et al. (Citation2017) and Ghosh et al. (Citation2012). In 2016, the total assets of this segment of the financial sector amounted to 466 billion euros in our 11 C.E.E. countries, compared to about 32 trillion euros in the euro area and 16 trillion in the U.S. Nonetheless, in C.E.E.s as in other E.U. countries, the shadow banking system has grown in leverage and complexity, as well as in terms of interconnectedness with the traditional banking sector (as also suggested by Girón & Matas-Mir, Citation2017; Portes, Citation2018; and others) to an extent that now it forms an integral part of the regular financial system.

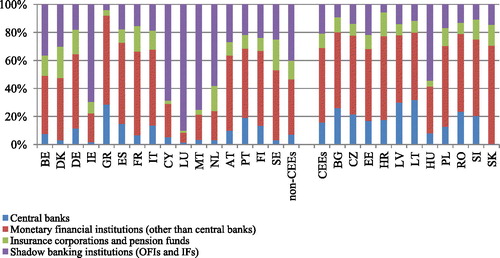

Looking at the main structural components of the financial system in C.E.E. countries in 2017 (), one can notice a relatively similar distribution among them by the total volume of assets (homogenous dispersion). The share of the assets of shadow banking institutions in the total assets of the financial system in C.E.E. countries is ranging from almost 6% to about 21%, with the exception of Hungary where shadow banking institutions own more than half of the Hungarian financial system (54.4%). Traditional banks own assets that usually exceed half of the financial system’s total volume of assets, with figures ranging between 48% and 70% (once again, with the exception of Hungary). To sum up, Hungary excluded, all the other C.E.E. countries have traditional banking systems that dominate national financial systems in terms of total assets and a rather small but increasing shadow banking system, followed by central banks and insurance corporations and pension funds.

Figure 2. Main structural components of the financial system in C.E.E.s and other E.U. countries (% of the total assets of the financial system). Notes: Data are for 2017, with the exception of the Czech Republic for which the latest data available were for 2016; the U.K. was excluded due to the lack of disaggregated data for central banks and monetary financial institutions other than central banks. Source: Authors’ elaboration based on data from Eurostat (EC, Citation2018)

By comparison, in the other (non-C.E.E.) E.U. countries the distribution of the national financial system’s assets by structural components is rather heterogeneous. Shadow banks are somehow insignificant in terms of assets in Greece (where they cover only about 4% of the financial system), and spread over almost the entire financial system in Luxembourg (cumulating above 90% of the total assets). In countries like Ireland, Cyprus, Malta and the Netherlands, the shadow banking system holds more than half of the national financial system’s total assets, leaving far behind the size of the other remaining components. On the other hand, in countries like Germany, Spain, France and Italy, far more grater is the traditional banking sector, represented by deposit takers (mainly commercial banks). Shadow banks hold here below 20% of the financial system’s total assets.

Another particularity of the shadow banking system in C.E.E. is that the main entities forming it are very easy to identify, in most of the cases being represented by finance companies (including micro-financing institutions), leasing and factoring companies, investment and equity funds, insurance companies, pawn shops, and underground entities (Ghosh et al., Citation2012). In Romania, for instance, the other financial institutions that form the shadow banking system perform activities such as: provide consumer credits and mortgage/real estate loans, provide microcredits, issuance of guarantees, factoring and financial leasing, financing of commercial transactions, discounting activities (NBR, Citation2018). Referring to the shadow banking system in emerging market and developing economies (including C.E.E.s), Ghosh et al. (Citation2012) also point out that ‘finance, leasing, and factoring companies; investment and equity funds; insurance companies; pawn shops; and underground entities’ comprise the main participants in the shadow banking system (Ghosh et al., Citation2012, p. 2). Moreover, they argue that it ‘is less about long, complex, opaque chains of intermediation and more about being weakly regulated or falling outside the regulatory sphere altogether’ (Ghosh et al., Citation2012, pp. 3–4).

4. Data and methodology

Our empirical study examines the determinants of the dynamics of shadow banking for a panel of 11 E.U. member states from C.E.E., namely Bulgaria, the Czech Republic, Croatia, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovenia, and Slovakia. Since comparable data (resulting from international/European data-collecting initiatives) on the assets of the financial sector, disaggregated by sub-sectors to a level that enables to approximate shadow banking’s dimension, are quite scarce in the case of our countries, generally being available for no more than 13 years and in some cases even less, we decided to run the regression analysis on quarterly data. This allowed us to expand the time dimension of our panel to a maximum of 52 observations per country, corresponding to the period 2004Q2–2017Q1, although common observations for all 11 countries have been available only since 2012Q4. Whilst the main data source, used for our shadow banking variables, is represented by Eurostat, some other international and European databases have been used as well, such as I.M.F.’s International Financial Statistics (IMF, Citation2017a) and Monetary and Financial Statistics database (IMF, Citation2017b), and E.C.B.’s Statistical Data Warehouse database (ECB, Citation2018) (see Appendix 1 for more details on data sources and data availability).

The model is a linear regression model linking indicators that measure the growth of the shadow banking sector in our sample countries with several potential macroeconomic and financial determinants, as depicted by EquationEquation (1)(1)

(1) .

(1)

(1)

where:

i refers to the country (i = 1–11);

t refers to time periods (quarters) (t = 1–52);

SDB is the dependent variable (a measure of shadow banking growth);

DETj is a vector of independent variables (potential determinants of shadow banking growth);

βj are the coefficients of the independent variables;

u(i,t) are the idiosyncratic (observation-specific) errors.

In choosing between the several methods available for estimating panel linear regression models, we firstly checked whether we should account for unobservable, or heterogeneity effects, which may cause the error term to be correlated with some of the considered regressors. After running a random effects (R.E.) regression, we performed the Lagrange multiplier (L.M.) test for R.E.s, allowing us to decide between the pooled O.L.S. and R.E. regressions. We failed to reject the null hypothesis that the variance of the unobserved fixed effects (F.E.) is not statistically different from zero at the significance level of 10%, and concluded that the R.E. model is not the most appropriate. We also ran the Hausman test, widely used in the literature to choose between the F.E. and R.E. regressions. The null hypothesis that the coefficients estimated by the efficient random effects estimator are the same as the ones estimated by the consistent F.E. estimator was not rejected either, leading us to the conclusion that the R.E. estimation is to be preferred. This is consistent with the observation that in the case of panels with large time dimension (T) and small cross-sectional dimension (N) (as is the case of our data set where T = 52 and N = 11) there is likely to be insignificant difference in the values of the parameters estimated by the F.E. and R.E. estimation techniques (Gujarati & Porter, Citation2009, p. 606).

All these arguments confirm that our group of countries, consisting of C economies that shared a similar pattern of economic and financial development during the last decades, can be considered quite homogenous in terms of the factors that affect shadow banking (as also pointed out by Jeffers & Plihon, Citation2016). Therefore, the pooled O.L.S. estimation technique, which does not explicitly take heterogeneity into account, is used in most of our estimations. However, since the F.E. method is widely used in the literature when investigating the determinants of shadow banking, we decided to also report the results of the fixed-effects estimation for our full model.

Besides the time-invariant entity (country) effects, we also checked the need to control for time effects. In this respect, we introduced 13 dummy variables (for the 14 years of our time span, to avoid falling into the dummy-variable trap) in the right hand-side of EquationEquation (1)(1)

(1) , along with the independent variables considered to potentially explain the dynamics of shadow banking. Alternatively, 51 dummy variables for each of the quarters of our time dimension have also been considered, although this approach presents the disadvantage of consuming a larger number of degrees of freedom. After running the dummy variable models, we tested the hypothesis that the coefficients of the categorical variables are jointly equal to zero. The null was rejected at a significance level of 5% in all cases, leading to the conclusion that time effects are needed.

To avoid high multicollinearity issues, we checked the correlations across the independent variables. All correlation coefficients were found to be below the threshold of 0.8, level suggested as a rule of thumb in the literature (Gujarati & Porter, Citation2009) (see Appendix 2). We also computed the variance inflation factors (V.I.F.s), and they resulted to be well below 5.0 (mean VIF of 2.53 in our full model with time-quarter effects).

In the presence of heteroskedasticity, although the OLS estimators are unbiased and consistent, they are not efficient and the standard errors are inconsistent. Therefore, we had to check if the variance of the residuals is constant and ran the White general test for heteroskedasticity. One shortcoming of this test is that it does not work well and is less powerful when many explanatory variables are included, although it allows testing more types of heteroskedasticity (including the non-linear ones). Therefore, we could not use it for the models with time (in particular, quarter) dummy variables. Instead, the relative simpler Breusch-Pagan/Cook-Weisberg test was used in these cases. When the null hypothesis that the variance of the residuals is homogenous was rejected, Huber/White heteroskedasticity-robust standard errors were reported. Also, to test for serial correlation, we ran the Wooldridge test for autocorrelation in panel data models, and we failed to reject the null hypothesis of no first order autocorrelation at the 5% level of significance.

One difficult task when specifying the econometric model and selecting the variables was to choose the appropriate measure of shadow banking, which could best capture the true dimensions of this sector in our group of countries. From this point of view, different alternatives of measurement have been advanced in theory and practice, designed to accommodate the increasing complexity of shadow banking.

One widely employed measure consists in using the aggregated financial assets of other financial intermediaries (O.F.I.s) as an instrument to measure shadow banking (an ‘entity-based’ approach). O.F.I.s include all non-bank financial corporations and quasi corporations that are engaged mainly in financial intermediation and provide primarily long-term funding. In general terms, here are not included central banks, banks (all deposit-taking corporations), insurance corporations, pension funds, public financial institutions, and financial auxiliaries. This measure was initially adopted by the F.S.B., which also made a distinction between a broader approach and a narrower one, the later filtering out non-bank financial activities that have no direct relation to credit intermediation (e.g. equity investment funds) or that are already prudentially consolidated into banking groups (FSB, Citation2014, Citation2015).

Nonetheless, this measure is often contested because it accounts for entities that are not engaged in shadow banking activities, therefore overstating the true dimensions of shadow banking in many countries. To remedy this deficiency, ‘activity-based’ approaches on measuring shadow banking have been advanced. The F.S.B. proposed a new ‘economic-function-based’ measure of shadow banking, classifying non-bank financial institutions in accordance with five economic functions that involve non-bank credit intermediation with some risks to financial stability (FSB, Citation2015).

Although activity-based approaches are generally considered to be more accurate, it is not yet possible to use these measures of shadow banking for the New E.U. member states from C.E.E., because of limited data availability. In fact, the most complete financial data source for this regional group is represented by Eurostat, which only reports data on the assets and liabilities of the financial sector, disaggregated by sub-sectors. Because of this limitation, the entity-based approach in measuring shadow banking was adopted.

Moreover, based on the F.S.B.’s distinction between the broad and the narrow approaches and the structure of available data for the C.E.E. countries, two alternative definitions of shadow banking institutions have been considered. The broad one includes all non-monetary financial institutions, except insurance corporations and pension funds. Therefore, from the overall financial sector the following institutions are excluded: monetary and financial institutions (central banks, deposit-taking corporations, and money market funds [M.M.F.]), public financial institutions, insurance corporations, and pension funds. However, between this definition and the F.S.B.’s broader definition of shadow banking there are some minor differences. In particular, M.M.F.s) are excluded from our approach, due to the lack of quarterly data for the assets of monetary and financial institutions disaggregated by sub-sector. However, this is not a major problem since M.M.F.s are less developed in C.E.E. Moreover, the same approach is suggested by Bakk-Simon et al. (Citation2012) as appropriate for the euro area countries, since data can be easily retrieved from the Eurosystem’s financial accounts. Besides excluding entities like M.M.F.s that are for sure engaged in shadow banking activities, another shortcoming of the above definition is that it includes intermediaries for which such a classification is sometimes considered to be questionable in the literature, like regulated investment funds (Malatesta et al., Citation2016). Therefore, we also took into account a second approach on shadow banking that excludes non-M.M.F. investment funds, corresponding to the F.S.B.’s narrower definition. In this way we hope to capture those activities that are closer to the banking sector, and identify if there is a complementarity with this regulated area of the financial system.

Therefore, the dynamics of the shadow banking sector is captured in our model by two dependent variables that measure the quarterly growth rate of the aggregated assets of shadow banking, both in the narrow (the SDB_NARROW variable) and broad (the SDB_BROAD variable) approach (see for further explanations and Appendix 3 for the descriptive statistics).

Table 1. Variables description.

Based on previous findings, six macroeconomic and financial variables were considered as potential determinants of shadow banking dynamics in our sample countries. Their description and expected effects are shortly presented in .

One macroeconomic variable – the real G.D.P. growth rate (GDP) – was included to capture the overall effects of the domestic supply and demand conditions. In periods of fast economic growth, traditional banks may not be able to cope with the high demand for credit from households and nonfinancial corporations, due to their inherent rigidity (such as legal constraints, high costs) (IMF, Citation2014b). Therefore, since one of the shadow banks’ functions is to provide alternative funding to the real economy, we would expect that, as macroeconomic conditions improve and the demand for money (credit) increases, shadow banking activity expands. On the other hand, in periods of economic distress shadow banks tend to be considered less reliable compared to traditional banks due to their lack of appropriate safety nets, which may explain why they are very vulnerable to changes in the economic outlook. In line with these explanations, we expect for a positive and significant impact of the G.D.P. growth rate on our two dependent variables, which is consistent with the shadow banking procyclicality hypothesis mentioned by Adrian and Shin (Citation2009) and empirically evidenced by Duca (Citation2016), Hodula, Machacek, and Melecky (Citation2017), and Malatesta et al. (Citation2016).

As proxy for global liquidity conditions we use the growth rate of total reserves, excluding gold (LIQUIDITY). Besides being procyclical, the shadow banking sector is said to be very vulnerable to liquidity shocks, as shown by Adrian and Shin (Citation2009, Adrian & Shin, Citation2010), Duca (Citation2016) and Gorton and Metrick (Citation2012). Liquidity drops lead to the decrease of the total value of shadow banks’ assets, whilst in a high liquidity environment this segment of the financial sector flourishes. Therefore, we expect the total liquidity of the economy to be positively associated with our two determined variables.

Two financial variables, the term spread (TSPREAD) computed as difference between risk-free long-term and short-term interest rates, and the money market rate (MMR) are considered as potential determinants of the dynamics of shadow banking, in line with the search for yield hypothesis. In a low interest rate environment, the search for higher yield could make investors turn to shadow banks, so a decrease of these variables should positively influence our dependent variables, as previously evidenced by the I.M.F. (Citation2014b).

The hypothesis of complementarity between the development of shadow banking and of the rest of the financial system is captured in our study by the two remaining explicative variables. The growth rate of the total assets of monetary and financial institutions excluding central banks (MFI) is intended to emphasise potential complementarities between shadow banks and traditional banks, which are at the core of the financial system in C.E.E. countries. On the same path of reasoning, the growth rate of the total assets of insurance corporations and pension funds (INSTIT_INVEST) is intended to capture the complementarities between the development of institutional investors and non-bank financial intermediaries, while also emphasising, on the demand-side, the consequences of an increased demand for shadow banking products from this segment of the financial sector (the institutional cash pool hypothesis). We expect both of these variables to be positively associated with the dynamics of the shadow banking sector, in agreement with the findings of the I.M.F. (Citation2014b) and Malatesta et al. (Citation2016).

5. Results and discussions

In our research approach we firstly performed univariate regression analyses between the broad measure of shadow banking and each of the explanatory variables included in the full model. The results are presented in , column (1). With the exception of the money market rate, all the explanatory variables have the right sign (in accordance with other studies and in line with our expectations) and are all statistically significant. This provides evidence that the dynamics of the shadow baking sector (in terms of its assets) has been positively influenced, among others, by the developments in the institutional investor sector, banking sector, money market rate, as well as the general liquidity and economic conditions. Only the term spread, which captures the search for yield effect, seems to have a downward pressure on the shadow banking sector.

Table 2. Regression results – broad definition of shadow banking.

Further on, the study continues with the establishment of a core model that has already been confirmed by the existing literature and that we could further use as a benchmark for other models. Model (2) reveals that the variables capturing the overall macroeconomic conditions, the institutional cash pools and financial development, as well as the search for yield have jointly a statistically significant impact on the dynamics of the shadow banking sector in C.E.E.s. Although the value of the adjusted R-squared (0.1366) is quite small, it is nonetheless comparable with the results of other representative studies (An & Yu, Citation2018; Du et al., Citation2017; IMF, Citation2014b).

Shadow banking results to be sensitive to overall macroeconomic conditions, economic growth positively influencing the expansion of this segment of the financial sector. This may be because the main function of the shadow banking sector in the C.E.E. countries is, due to its particular structure (consisting mainly of leasing and factoring companies, credit unions, cooperative banks, microfinance companies, and pawn shops), that of providing alternative funding to the economy, as pointed out by Ghosh et al. (Citation2012). As Du et al. (Citation2017) also mention in their work, in general in C.E.E. countries many credit institutions focus more on households (i.e., mortgage loans) than on enterprises. Moreover, within the bank operations performed for enterprises, a significant number is devoted to processing payments, instead of credit provision. Therefore, as many companies are unobserved or underserved by the formal financial system (Haselmann, Wachtel, & Sobott, Citation2016), they are searching for finances outside their traditional suppliers.

Also, the institutional cash pools and search for yield hypotheses are confirmed. A higher demand from institutional investors, also revealing a more developed financial system, supports the expansion of the shadow banking sector, while term spread has reversed effects (given the negative sign).

By introducing into the model the money market rate – see model (3) – the total number of observations decreases, due to low data availability, but the explanatory power of the model increases to 24%. Also, the newly introduced variable results to have the right (negative) sign. Therefore, it is confirmed our hypothesis that lower yields in the financial markets motivate investors to look for more attractive returns in riskier places, as in the shadow banking sector. As also identified by Hodula et al. (Citation2017) in their research on the Spanish case, decreasing interest rates boost the search for yield motive from the traditional banking sector, which is looking for more profitable sources of income and often engages in securitisation activities. But in contrast to the findings of Hodula et al. (Citation2017) or the I.M.F. (Citation2014a), our coefficients are statistically significant in almost all the models.

Models (4) to (8) add variables capturing the development of the banking sector and overall financial liquidity. Whilst model (4) reflects the results of a simple pooled O.L.S. regression, country F.E.s and time (quarterly and yearly) effects have alternatively been considered in the subsequent models. Although the latter approach increases the explanatory power of our models (reflected by an increase in the adjusted R-squared with up to 25%), some important independent variables (in particular, the one capturing the size of the traditional banking sector) lose their statistical significance in the process. Despite the lack of significance, all the newly introduced variables reveal the expected signs, partially supporting the validity of our hypotheses.

The values and signs of the coefficients associated with the banking sector variable prove, in models (4) and (5), that the development of this particular segment of the financial system goes hand in hand with non-traditional (shadow) banking. Therefore, there is strong evidence that the hypothesis of complementarity between the two sectors holds, supporting the view that the market-based finance can progress together with traditional banking. This could also point to the existence of some common roots for both processes (such as the development of I.T.C. technologies, the European integration, financial innovation), resulting in a generalised development of the financial system. In addition, it is possible that some common factors, like the international economic and financial crisis or the European debt crisis, equally affected the dynamics of both sectors in our sample countries. This is confirmed when time dummy variables are included in the model and the coefficients of the banking sector variable result to lose their strength and statistical significance. Although the coefficients of the categorical variables have not been reported in for reasons of space, our analysis revealed that they were statistically relevant at the 5% level of significance for the years of crisis (2008–2010).

As we take into consideration the narrower measure of the shadow banking sector (), our previous results with regard to the sign and statistical significance of the coefficients are roughly confirmed. However, the overall explanatory power of the models decreases, the maximum value of the adjusted R-squared being of just 0.31, in model (7). One possible reason may be that some of our explanatory variables (like the one capturing the demand for investment products from insurance companies and pension funds) are very important determinants for the development of one particular segment of the shadow banking sector, namely investment funds, intentionally excluded in our narrower approach. Some proof, besides theoretical arguments, lie in the coefficients of the variable capturing the dimensions of the institutional investors sector. The ones reported in are much smaller than the ones in , in all models. Moreover, while for some variables (like GDP) the coefficients do not change by much, in other cases, of variables more strongly related to bank-based finance (as TSPREAD, MMR, and MFI), their value increases in all cases. Altogether, the results of the regressions on the narrower shadow banking measure prove that this approach more adequately captures the potential complementarities with the traditional banking sector.

Table 3. Regression results – narrow definition of shadow banking.

6. Conclusion

The article provided some glimpses into a continuously evolving and intriguing phenomena that is being observed worldwide but has only in recent years speed up its growing process in C.E.E. countries, that is shadow banking. More specifically, our research aimed to empirically assess the macro determinants of its dynamics for a panel of 11 E.U. countries from this region, using quarterly data spanning 2004–2017.

Broadly speaking, we noticed an important increase in the shadow banking sector in 2004 in C.E.E. countries, clearly outpacing the growth rate in the euro area. During the recent financial crisis, the total volume of assets of the shadow banking institutions was rather stable in the region, and it resumed its upward trend afterwards. One question arises from this dynamics: what where the factors that determined the shadow banking system to develop at a greater pace compared to the traditional banking sector in the C.E.E. countries?

The empirical analysis revealed that the shadow banking sector is quite sensitive to overall macroeconomic conditions in C.E.E.s, economic growth positively and significantly influencing the expansion of this segment of the financial sector. This gives us strong arguments to confirm the hypothesis of shadow banking procyclicality for our group of countries. Moreover, because of the positive values of the coefficients of the variable used to account for global liquidity conditions, we can safely presume that the shadow banking sector is very susceptible to runs and liquidity shortages. The institutional cash pools and search for yield hypotheses are also confirmed, showing that in a low interest rate environment like the one following the financial crisis in C.E.E.s, the search for higher yield makes investors turn to shadow banking products. Moreover, the hypothesis of complementarity between the development of shadow banking and of the rest of the financial system is confirmed as well, probably with stronger evidence given the nature of the bank-based economy in C.E.E. countries. In these economies, shadow banks provide alternative funding where traditional banking is not able to do so.

One shortcoming of our analysis with regard to the selected explicative variables is that it fails to catch the effects of regulatory arbitrage opportunities on the development of bank-like activities outside the regulated banking system. This is considered to be the primary determinant of shadow banking by authors such as Harris, Opp, and Opp (Citation2014), Ordonez (Citation2013) and Plantin (Citation2015). The main explanation comes from the lack of data (and, in particular, quarterly data) on the variables that could proxy the changes in the regulatory environment in our C.E.E. countries. In addition, the changes in the regulatory environment are evidenced to affect shadow banking over the long-term (Duca, Citation2016). Therefore, an analysis including such variables should be conducted on long data series, which are not available, unfortunately, for our sample countries.

Acknowledgement

We gratefully thank the Editors and the five anonymous reviewers of the journal for their very useful and constructive comments on the article. We are also grateful for the valuable suggestions offered by the participants of the MIC 2018 Conference Managing Global Diversities in Bled (Slovenia) and of the 16th International Conference on Finance and Banking in Ostrava (Czechia).

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Related Research Data

References

- Acharya, V. V., Khandwala, H., & Öncü, T. S. (2013). The growth of a shadow banking system in emerging markets: Evidence from India. Journal of International Money and Finance, 39, 207–230. doi:10.1016/j.jimonfin.2013.06.024

- Adrian, T. (2014). Financial stability policies for shadow banking. FRBNY Staff Reports (Vol. 664). New York: Federal Reserve Bank of New York.

- Adrian, T., & Ashcraft, A. (2012). Shadow bank regulation. Annual Review of Financial Economics, 4(1), 99–140. doi:10.1146/annurev-financial-110311-101810

- Adrian, T., Ashcraft, A., & Cetorelli, N. (2013). Shadow Bank Monitoring. FRBNY Staff Report, (Vol. 638). New York. Federal Reserve Bank of New York.

- Adrian, T., & Shin, H. S. (2009). The shadow banking system: implications for financial regulation. Banque de France Financial Stability Review, 13, 1–10.

- Adrian, T., & Shin, H. S. (2010). Liquidity and leverage. Journal of Financial Intermediation, 19(3), 418–437. doi:10.1016/j.jfi.2008.12.002

- Agresti, A. M. (2016). Shadow banking: Some considerations for measurements purposes. In B. F. I. Settlements (Ed.), Combining micro and macro data for financial stability analysis (Vol. 41). Basel, Switzerland: Bank for International Settlements.

- Andries, A. M. (2011). The determinants of bank efficiency and productivity growth in the Central and Eastern European Banking Systems. Eastern European Economics, 49(6), 38–59. doi:10.2753/EEE0012-8775490603

- An, P., & Yu, M. (2018). Neglected part of shadow banking in China. International Review of Economics & Finance, 57, 211–236. doi:10.1016/j.iref.2018.01.005

- Arora, R. U., & Zhang, Q. (2018). Banking in the Shadows: A Comparative Study of China and India. Australian Economic History Review, 1, 1–29. doi:10.1111/aehr.12167

- Bakk-Simon, K., Borgioli, S., Girón, C., Hempell, H. S., Maddaloni, A., Recine, F., & Rosati, S. (2012). Shadow banking in the euro area: An overview. ECB Occasional Paper Series, 133(April), 1–33.

- Barbu, T. C., Boitan, I. A., & Cioaca, S. I. (2016). Macroeconomic determinants of shadow banking—Evidence from EU countries. Review of Economic and Business Studies, 9(2), 111–129. doi:10.1515/rebs-2016-0037

- Beck, G. W., & Kotz, H.-H. (2016). Les activités de shadow banking dans un contexte de bas taux d’intérêt: une perspective de flux financiers. Revue d’économie financière, 121(1), 235–256. doi:10.3917/ecofi.121.0235.

- Bejaković, P. (2015). A revision of the shadow economy in Croatia: Causes and effects. Economic Research-Ekonomska Istraživanja, 28(1), 422–440. doi:10.1080/1331677X.2015.1059104

- Bernanke, B. (2013). Some Reflections on the Crisis and the Policy Response. Speech delivered at “Rethinking Finance”, a conference sponsored by the Russell Sage Foundation and Century Foundation, New York, April 13. www.federalreserve.gov/newsevents/speech/bernanke20120413a.htm.

- Bouveret, A. (2011). An Assessment of the Shadow Banking Sector in Europe. SSRN Electronic Journal, 1–31. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2027007

- Broos, M., Carlier, K., Kakes, J., & Klaaijsen, E. (2012). Shadow banking: An exploratory study for the Netherlands. DNB Occasional Studies, 10(5), 1–55.

- Brunnermeier, M., & Pedersen, L. H. (2009). Market liquidity and funding liquidity. Review of Financial Studies, 2(6), 2201–2238. doi:10.1093/rfs/hhn098

- Caballero, R. (2010). The “Other” imbalance and the financial crisis. NBER Working Paper Series, 15636.

- Caballero, R., & Simsek, A. (2009). Complexity and Financial Panics NBER Working Paper (Vol. 14997). Cambridge, MA: National Bureau of Economic Research.

- Claessens, S., Zoltan, P., Ratnovski, L., & Singh, M. (2012). Shadow banking: Economics and policy. Staff discussion note. IMF. doi:10.5089/9781475583588.006

- Davidescu, A. A., & Schneider, F. (2017). Nature of the relationship between minimum wage and the shadow economy size: An empirical analysis for the case of Romania. IZA Discussion Papers, (Vol. 11247).

- Du, J., Li, C., & Wang, Y. (2017). A comparative study of shadow banking activities of non-financial firms in transition economies. China Economic Review, 46(Supplement), S35–S49. doi:10.1016/j.chieco.2016.09.001

- Duca, J. (2016). How capital regulation and other factors drive the role of shadow banking in funding short-term business credit. Journal of Banking & Finance, 69(Supplement 1), S10–S24. doi:10.1016/j.jbankfin.2015.06.016

- EC. (2012). Green paper on shadow banking. http://ec.europa.eu/internal_market/bank/docs/shadow/green-paper_en.pdf

- EC. (2018). Eurostat database. https://ec.europa.eu/eurostat

- ECB. (2018). Statistical data warehouse. https://sdw.ecb.europa.eu/

- EESC. (2012). Green Paper – Shadow banking (Vol. INT/643), Brussels: European Economic and Social Committee.

- ESRB. (2016). EU Shadow Banking Monitor (Vol. 1 (July)). Frankfurt am Main: European Systemic Risk Board.

- FCIC. (2010). Shadow Banking and the Financial Crisis Preliminary Staff Report: Financial Crisis Inquiry Commission.

- FSB. (2011). Shadow Banking: Strengthening Oversight and Regulation. Recommendations of the Financial Stability Board.

- FSB. (2012a). Global Shadow Banking Monitoring Report 2012. http://www.fsb.org/wp-content/uploads/r_121118c.pdf

- FSB. (2012b). Shadow Banking: Scoping the Issues. Background Note of the FSB. Retrieved from www.fsb.org/wp-content/uploads/r_111027a.pdf?page_moved=1

- FSB. (2014). Global Shadow Banking Monitoring Report 2014. Retrieved from http://www.fsb.org/wp-content/uploads/r_141030.pdf

- FSB. (2015). Global Shadow Banking Monitoring Report 2015. www.fsb.org/wp-content/uploads/global-shadow-banking-monitoring-report-2015.pdf

- Gennaioli, N., Shleifer, A., & Vishny, R. W. (2013). A Model of Shadow Banking. The Journal of Finance, 68(4), 1331–1363. doi:10.1111/jofi.12031

- Ghosh, S., Gonzalez del Mazo, I., & Ötker-Robe, İ. (2012). Chasing the Shadows: How Significant Is Shadow Banking in Emerging Markets? Economic Premise, 88(72445), 7.

- Girasa, R. (2016). Shadow banking. The rise, risks, and rewards of non-bank financial services. New York: Palgrave Macmillan.

- Girón, C., & Matas-Mir, A. (2017). Interconnectedness of shadow banks in the euro area. In Bank for International Settlements (Ed.), Data needs and Statistics compilation for macroprudential analysis (Vol. 46). Basel, Switzerland: Bank for International Settlements.

- Goda, T., & Lysandrou, P. (2014). The contribution of wealth concentration to the subprime crisis: A quantitative estimation. Cambridge Journal of Economics, 38(2), 301–327. doi:10.1093/cje/bet061

- Goda, T., Lysandrou, P., & Stewart, C. (2013). The contribution of US bond demand to the US bond yield conundrum of 2004–2007: An empirical investigation. Journal of International Financial Markets, Institutions and Money, 27, 113–136. doi:10.1016/j.intfin.2013.07.012

- Gorton, G., & Metrick, A. (2010). Regulating the shadow banking system. Brookings Papers on Economic Activity, 41(2 (Fall)), 261–312. doi:10.1353/eca.2010.0016

- Gorton, G., & Metrick, A. (2012). Securitized banking and the run on Repo. Journal of Financial Economics, 104(3), 425–451. doi:10.1016/j.jfineco.2011.03.016

- Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). Singapore: Mc-Graw Hill.

- Guttmann, R. (2016). Finance-led capitalism: Shadow banking, re-regulation, and the future of global markets. New York: Palgrave Macmillan.

- Hampl, M. (2018). Examining the Resilience of Emerging Markets. Speaking points at the third Annual SSGA-OMFIF Roundtable London. Retrieved from www.cnb.cz/en/public/media_service/conferences/speeches/hampl_20180410_omfif.html

- Harris, M., Opp, C. C., & Opp, M. M. (2014). Higher capital requirements, safer banks? Macroprudential regulation in a competitive financial system. SSRN Electronic Journal. doi:10.2139/ssrn.2467761.

- Haselmann, R., Wachtel, P., & Sobott, J. (2016). Credit institutions, ownership and bank lending in transition economies. In T. Beck and B. Casu (Eds.), The Palgrave Handbook of European Banking. London: Palgrave Macmillan.

- Hassan, M., & Schneider, F. (2016). Size and development of the shadow economies of 157 countries worldwide: Updated and new measures from 1999 to 2013. IZA Discussion Papers (Vol. 10281).

- Helgadóttir, O. (2016). Banking upside down: The implicit politics of shadow banking expertise. Review of International Political Economy, 23(6), 915–940.

- Hodula, M., Machacek, M., & Melecky, A. (2017). Macroeconomic determinants of shadow banking: Evidence from Spain. In J. Nešleha, T. Plíhal, and K. Urbanovský (Eds.), European Financial Systems 2017. Proceedings of the 14th International Scientific Conference. (Vol. 1, pp. 204–212). Brno: Masaryk University.

- IMF. (2010). IMF survey magazine: Countries & regions. Retrieved from www.imf.org/external/pubs/ft/survey/so/2009/INT011409A.htm

- IMF. (2014a). Global financial stability report. Risk taking, liquidity, and shadow banking. Curbing excess while promoting growth. Washington, DC. International Monetary Fund.

- IMF. (2014b). Shadow Banking around the Globe: How Large, and How Risky? In Global financial stability report. Risk taking, liquidity, and shadow banking. Curbing excess while promoting growth (pp. 65–104). Washington, DC: International Monetary Fund.

- IMF. (2017a). International Financial Statistics. http://data.imf.org/?sk=4C514D48-B6BA-49ED-8AB9-52B0C1A0179B&sId=1390030341854

- IMF. (2017b). Monetary and Financial Statistics. http://data.imf.org/?sk=B83F71E8-61E3-4CF1-8CF3-6D7FE04D0930

- IMF. (2018). World Economic and Financial Surveys. World Economic Outlook Database – WEO Groups and Aggregates Information. Retrieved from https://www.imf.org/external/pubs/ft/weo/2018/02/weodata/groups.htm

- Jeffers, E., & Plihon, D. (2016). What is so special about European Shadow banking? FEPS Studies, (Aug.), 26. http://www.feps-europe.eu/assets/e0cfef23-a52c-4e67-b17c-09770f026dee/jeffers-plihonpdf.pdf

- Kabelik, K. (2012). Shadow Banking. Česká Bankovní Asociace Occasional paper. from www.czech-ba.cz/sites/default/files/cba_kabelik_shadow_banking.pdf

- Karanovic, G., & Karanovic, B. (2018). IPOs performance analysis: evidence from emerging markets in the Balkans. Scientific Annals of Economics and Business, 63(3), 381–389.

- Kim, S. J. (2016). What drives shadow banking? A dynamic panel evidence. Paper presented at the Eighth IFC Conference on “Statistical implications of the new financial landscape”, Basel.

- Lysandrou, P., & Nesvetailova, A. (2015). The role of shadow banking entities in the financial crisis: A disaggregated view. Review of International Political Economy, 22(2), 257–279. doi:10.1080/09692290.2014.896269

- Malatesta, F., Masciantonio, S., & Zaghini, A. (2016). The shadow banking system in the Euro area: Definitions, key features and the funding of firms. Italian Economic Journal, 2(2), 217–237. doi:10.1007/s40797-016-0032-0

- McCulley, P. (2007). Teton Reflections. PIMCO Global Central Bank Focus, no. 2. Retrieved from http://www.pimco.com/en/insights/pages/gcbf%20august-%20september%202007.aspx

- Michael, B. (2014). Playing the shadowy world of emerging market shadow banking. SKOLKOVO Business School Ernst & Young Institute for Emerging Market Studies (IEMS), 14(02).

- Miklaszewska, E., Mikołajczyk, K., & Pawłowska, M. (2012). The consequences of post-crisis regulatory architecture for banks in Central Eastern Europe. National Bank of Poland Working Paper, 131.

- Mikulić, D., & Nagyszombaty, A. G. (2013). Causes of the unofficial economy in new EU member states. Economic Research-Ekonomska Istraživanja, 26(sup1), 29–44. doi:10.1080/1331677X.2013.11517638

- NBR. (2018). National Bank of Romania Public Registers. Retrieved from http://www.bnro.ro/NBR-Public-Registers-1701.aspx

- Ordonez, G. (2013). Sustainable shadow banking. NBER Working Paper Series, 19022. http://www.nber.org/papers/w19022

- Perotti, E. (2013). The roots of shadow banking. CEPR Policy Insight, 69.

- Plantin, G. (2015). Shadow banking and bank capital regulation. Review of Financial Studies, 28(1), 146–175. doi:10.1093/rfs/hhu055

- Portes, R. (2018). Interconnectedness: Mapping the shadow banking system. Banque de France European Stability Review, 22(April), 2–10.

- Pozsar, Z. (2008). The rise and fall of the shadow banking system. Regional Financial Review, July, 13–25.

- Pozsar, Z., Adrian, T., Ashcraft, A. B., & Boesky, H. (2010). Shadow banking. Federal Reserve Bank of New York Staff Report, 458.

- Pozsar, Z., Adrian, T., Ashcraft, A. B., & Boesky, H. (2013). Shadow banking. Economic Policy Review, 19(2), 1–16.

- Ramotowski, J. (2015). The uncertain future of banks in Eastern Europe. Central European Financial Observer. https://financialobserver.eu/poland/the-uncertain-future-of-banks-in-eastern-europe/

- Schneider, F. (2002). The Size and Development of the Shadow Economies of 22 Transition and 21 OECD Countries. IZA Discussion Papers (Vol. 514).

- Tucker, P. (2010). Shadow banking, financing markets and financial stability. Remarks by Mr. Paul Tucker, Deputy Governor for Financial Stability at the Bank of England: Bernie Gerald Cantor (BGC) Partners Seminar, London, 21 January 2010.

Appendix 1.

Data sources and availability

Appendix 2.

Correlation matrix

Appendix 3.

Descriptive statistics of the variables