?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

An analysis of the scientific literature has revealed that companies in advanced countries have mixed capital structures, whereas companies in less advanced countries mostly depend on bank credits and loans. The reason for dependence on bank funding lies in the fact that corporate bonds are profitable only to large companies with a high credit rating, while small and medium companies—as well as large companies with lower credit ratings—find bank loans to be a more attractive method of external financing. This article focuses on the impact of particular financial and economic determinants on corporate borrowing in Lithuania. With a view to providing not only theoretical, but also practical insight in the problems of corporate financing, we have included such financial determinants as interest rates and bond yields.

1. Introduction

Both scientific studies and business practice propose that getting access to external sources of financing is a challenging task for companies even in modern finance markets. Interaction between the policies of the central banks, commercial banks, and stock and bond markets has a tremendous effect on availability of the sources of funding that business companies can choose. In spite of the fact that a company’s capital structure largely depends on its own specific characteristics (Antoniou, Guney & Paudyal, Citation2002; Thukral, Sridhar & Joshi, Citation2015; Hutchinson et al., Citation2016; Sukcharoensin, Citation2017, etc.), the role of financial institutions in fund provision is also extremely important for business and industrial development (Beck, Demigurc-Kunt, & Martinez, Citation2007; Daquila, Citation2007; Bokpin, Citation2010; Beck, Demirgüç-Kunt, & Levine, Citation2010, etc.; Iljins & Skvarciany, Citation2015; Radivojević, Ćurčić, & Vukajlović, Citation2017).

According to Sprčic and Wilson (Citation2007), companies in advanced countries have mixed capital structures, whereas companies in less advanced countries mostly depend on bank credits and loans. The reason for dependence on bank funding lies in the fact that corporate bonds are profitable only to large companies with a high credit rating (Datta, Iskandar-Datta & Patel, Citation2000; Sprčic & Wilson, Citation2007; Sukcharoensin, Citation2017), while small and medium companies—as well as large companies with lower credit ratings—find bank loans to be a more attractive method of external financing (Thukral et al., Citation2015; Sukcharoensin, Citation2017).

Nevertheless, monetary policy implemented by central banks may create barriers for the availability of bank funding to businesses. For instance, by establishing low interest rates, central banks discourage commercial banks from lending funds; strict loan issuance procedures and high requirements for applicants make bank funds available only to a small number of companies that meet the strict requirements, etc. Having limited access to bank funds, business companies are forced to look for alternative, although sometimes less attractive, sources of external funding. What is more, by employing direct market operations, the European Central Bank redeems illiquid bonds, which has a significant impact on the bond market and bond prices. Hence, corporate bond market prices can reveal the barriers to institutional (i.e., bank) funding and disclose business needs for alternative external funding. In other words, the significant gap between the interest rates charged for institutional loans and bonds may show that business companies are facing the problem of the lack of funds/working capital, which cannot be obtained from institutional borrowers. Having no other choice, a substantial proportion of companies are forced to issue bonds and borrow funds in alternative markets (e.g., from other business corporations, credit institutions, pension and investment funds, individuals, etc.).

Although scientific literature is rich in the studies on the development of corporate bond markets (Ahmed & Mmolainyane, Citation2014; Naik & Padhi, Citation2015; Francis, Hasan, & Ofori, Citation2015; Hutchinson et al., Citation2016; Sukcharoensin, Citation2017, etc.) and the drivers of issuance of corporate bonds (Bokpin, Citation2010; Hutchinson, Fraser, Adair, & Srivatsa, Citation2011; Zabala & Josse, Citation2014; Ehlers, Packer & Remolona, Citation2014; Thukral et al., Citation2015, etc.), the determinants that make business companies look for alternative sources of funding under the impact of monetary policies have hardly been researched, especially at a national level. The purpose of this article is to identify which factors determine a preference for corporate borrowing in alternative markets over borrowing from banks under the impact of monetary policies in Lithuania. For fulfilment of the defined purpose, the following objectives were raised: (1) to analyse the theoretical aspects of the impact of monetary policies on the demand for bank and non-bank financing; (2) to review the theoretical determinants of business capital structure choice; (3) to select and present the methodology of the research; (4) to introduce the results of the empirical research on the factors that determine a preference for corporate borrowing in alternative markets over borrowing from banks under the impact of monetary policies in Lithuania. The methods of the research include scientific literature analysis, expert evaluation and linear regression model.

2. The impact of monetary policies on the demand for bank and non-bank financing

With reference to the corporate finance theory, market imperfections such as underdeveloped financial systems, information asymmetry or institutional regulation and interference may constrain companies’ abilities to fund their investment (Bokpin, Citation2010; Sukcharoensin, Citation2017). As noted by Fama (Citation1985), banks play an important role in business financing as they possess a comparative advantage in monitoring of corporate borrowers. In addition, banking funding dominates in the early phases of economic and financial development of a country (Bokpin, Citation2010) due to a small number of large and high-rated companies with transparent business and financial information and therefore low supply of corporate bonds in a developing economy. According to Bokpin (Citation2010), in such an economic setting, the majority of business companies find bank loans to be a more appropriate method of financing and do not tap into the corporate bond market.

However, it is important to note that institutional fund suppliers (i.e., banks) are very different from other market participants because they operate under the supervision of central banks – the institutions with large financial weight and virtually unlimited resources that can dramatically change the behaviour of finance markets. The power of central banks to invoke the measures of monetary policy can have a significant impact on availability of bank financing for business companies.

Scientific literature describes many different channels through which the measures of monetary policies may influence real economics, including the demand for bank and non-bank financing. The analysis of the scientific literature (Claudio & Lowe, Citation2002; Misati & Nyamongo, Citation2012; Rey, Citation2013; Rey, Citation2014; Miranda-Agrippino & Rey, Citation2015, etc.) has enabled the identification of the most influential channels of monetary policy transmission, which are as follows:

Asset price channel

Interest rate channel

Exchange rate channel

Credit channel

Investor expectation channel

Through the asset price channel, the measures of monetary policies make an impact on prices of different types of assets (including financial assets such as bonds) (Miranda-Agrippino & Rey, Citation2015). When central banks reduce interest rates, this decision determines lower costs of asset acquisition and leads to an increase in asset demand. Higher demand of financial assets generates higher prices of financial assets, which may make issuance of bonds a more attractive alternative of external funding than bank loans. When central banks toughen bank reserve requirements, commercial banks, in turn, toughen the terms of loan issuance, which makes loans available to a small circle of potential borrowers (Claudio & Lowe, Citation2002; Misati & Nyamongo, Citation2012).

Interest rate channel is a traditional channel of monetary policy transmission to economics. Through this channel, short-term interest rates make an impact on long-term interest rates and borrowing rates (Misati & Nyamongo, Citation2012; Rey, Citation2013; Rey, Citation2014). For instance, an increase in short-term interest rates inevitably affects long-term borrowing rates, which, in turn leads to an increase in real costs of borrowing. It makes borrowing from banks less attractive in comparison to borrowing in alternative markets.

Exchange rate channel – this channel works when central banks invoke strict monetary policies, which determine the rise of the local currency exchange rate against the rates of foreign currencies. Nevertheless, to keep the balance, the rate of the local currency should decrease in parallel with the interest parity (Miranda-Agrippino & Rey, Citation2015). On the other hand, the rise of the rate of the local currency can attract additional capital flows in the country, which, in turn, may promote issuance of corporate bonds rather than application for institutional funding (Misati & Nyamongo, Citation2012).

The credit channel is the channel of bank lending, household and business balance. Transmitted through this channel, the measures of monetary policies, first of all, affect the turnover of bank loans and liabilities of households and businesses. When central banks reduce money reserves in commercial banks by establishing lower reserve requirements, this means that commercial banks offer smaller amounts of money for lending. On the other hand, reduction in money reserves determines poorer balance between household and business liabilities, i.e., it reduces the net value of the assets and equities held by the above-mentioned entities (Miranda-Agrippino & Rey, Citation2015). Hence, before issuing loans, commercial banks must employ strict filters to sift out potentially insolvent debtors. This, in turn, may raise the demand for non-bank borrowing (Misati & Nyamongo, Citation2012).

Through the investor expectation channel, the interest rates established by central banks may have an impact on investors’ expectations as far as they are related to the dynamics of economics in the future, i.e., investors may start more or less to believe in future economic growth or decline (Gregorio, Citation2010). Distrust in potential economic growth may discourage investors from the acquisition of particular equities, and business companies can be forced to consider the opportunities of bank financing. On the other hand, if central banks increase interest rates, it can raise investors’ expectations about the long-term rise of the value of financial assets, and issuance of bonds can become an attractive alternative of external funding for business (Ahmad, Bhanumurthy & Sehgal, Citation2014). Nevertheless, as noted by Misati and Nyamongo (Citation2012), in some cases investors’ expectations are hard to predict as they are influenced not only by the measures of monetary policies, but also by subjective assessment. Hence, while selecting the source of financing, business companies should consider other criteria of assessment.

To summarise, being invoked by central banks, i.e., the institutions with large financial weight and virtually unlimited resources, monetary policies can dramatically change the behaviour of finance markets. The power of central banks to invoke the measures of monetary policy can have a significant impact on availability of bank financing for business companies. The most influential channels of monetary policy transmission are the asset price channel, interest rate channel, exchange rate channel, credit channel and investor expectation channel. The main measures of monetary policy transmitted through these channels to financial markets include changes in short and long-term interest rates and changes in bank reserve norms. An increase in short-term interest rates affects long-term borrowing rates, which, in turn leads to an increase in the real costs of borrowing, and makes borrowing from banks less attractive in comparison to borrowing in alternative markets, and vice versa. Reduction of bank reserve norms leads to smaller amounts of money that could be lent. On the other hand, the reduction of bank reserves determines the decline of the net value of the assets and equities held by households and businesses. This, in turn, may reduce the availability of bank loans and raise the demand for non-bank borrowing.

3. The determinants of business capital structure choice

As noted by Bokpin (Citation2010), ʽstudies have shown that the interactions in the financial market, where firms source their finance, can have tremendous effects on the available choice of financing for firmsʼ (p. 96). According to Antoniou et al. (Citation2002), a firm’s capital structure is affected not only by the internal characteristics inherent to this firm, but also by a number of external factors. Analysis of the scientific literature has enabled us to systematise the determinants of business capital structure choice (see ).

Table 1. The determinants of business capital structure choice.

As it can be seen in , the main determinants of business capital structure choice fall into the following groups: general economic determinants, bank sector determinants, money market determinants and the specific characteristics of a company.

General economic determinants cover the general economic development of a country, the level of stock market development, the size of the banking sector and the level of financial market development. The significance of the environment surrounding a company, including the general health of the economy, was emphasised by Antoniou et al. (Citation2002), Bokpin (Citation2010), Misati and Nyamongo (Citation2012), Thukral et al. (Citation2015), Sukcharoensin (Citation2017) and many other authors. Developed economies ensure openness of capital markets and promote transparency of business financial behaviour (Mutenheri & Green, Citation2003). As capital markets are open, it becomes less expensive for business companies to raise their funds, and access to non-banking financing becomes as important as specific characteristics of a company (Agarwal & Mohtadi, Citation2004; Abor & Biekpe, Citation2006; Bokpin, Citation2010).

Theoretical explanation of the impact of stock markets on business finance choice was provided by Booth, Aivazian, Demirguc-Kunt, and Maksimovic (Citation2001), Bokpin (Citation2010), Ahmed and Mmolainyane (Citation2014), Francis et al. (Citation2015), Hutchinson et al. (Citation2016), Sukcharoensin (Citation2017) and many other researchers who note that developed stock and equity markets are a viable option of corporate financing. The research conducted by Genenc (Citation2003) provided the empirical evidence that the level of a stock market development is one of the main determinants of business capital structure choice in Turkish firms. The impact of the level of a stock market development manifests as the guarantee of ‘liquidity, diversification, information acquisition, resource mobilisation for corporate finance, investment and growthʼ (Bokpin, Citation2010, p. 97). As a result, developed stock markets provide opportunities to business companies to finance their operations through equity capital without issuance of bonds or borrowing from banks.

Comparative advantage of banks while providing financing for business companies was emphasised by Mutenheri and Green (Citation2003), Kristiansen (Citation2004), Agarwal and Mohtadi (Citation2004), Misati and Nyamongo (Citation2012), Rey (Citation2013), Rey (Citation2014) and others. With reference to Bokpin (Citation2010), banks simply help to minimise the problems of information asymmetries that arise between businesses and debtholders. Mutenheri and Green (Citation2003) provided the empirical evidence that the extension of the bank finance system in Zimbabwe led to a significant increase in short-term bank financing. Hence, a developed banking sector with a large number of operators is a promotive determinant of the share of bank financing in the general structure of business capital, although, as it was noted by Kristiansen (Citation2004), many of the long-term benefits of business-bank relationships can be determined by the companies themselves, and the benefits obtained from bank financing ‘do not necessarily depend on exogenous factors like, for instance, the level of competition in the banking industryʼ (Bokpin, Citation2010, p. 98).

According to Bokpin (Citation2010), the development of finance markets means maturity of the sources of financing, and although assessment of the efficiency of financial markets is an empirical issue (Bokpin, Citation2010; Ahmed & Mmolainyane, Citation2014; Francis et al., Citation2015; Naik & Padhi, Citation2015, etc.), it is also the case that high levels of finance market development alleviates market imperfections, which, in turn, helps to prevent pooling of society’s savings (Masoud & Hardaker, Citation2012).

Bank sector determinants of business capital structure choice cover the procedures of bank loan issuance, legal regulation of the banking sector, the rate of deposit insurance premiums, (in)dependency of a business company from bank financing and a company’s credit rating. Simple procedures of bank loan issuance act as a promotive determinant, which commonly leads to an increase in the share of bank financing in business capital structure and vice versa – complicated loan issuance procedures are usually related to high requirements for potential debtors, big responsibilities and obligations of debtors to banks, etc. (Beck et al., Citation2007; Daquila, Citation2007; Beck et al., Citation2010). The impact of strict legal regulation on the banking sector manifests just in the same way. It means that under strict legal regulation, loan issuance procedures get complicated, and bank loans become available only to a small part of business companies, while the companies who fail to meet the strict requirements are forced to look for alternative sources of financing (Bokpin, Citation2010). High rates of deposit insurance payment discourage banks from attracting deposits, which may lead to a significant reduction in bank funds available for borrowing (Misati & Nyamongo, Citation2012).

According to Sukcharoensin (Citation2017), in many cases companies prefer non-bank financing in order to stay independent from complicated bank funding procedures and strict obligations. What is more, the choice of bank financing for particular companies might be restricted (for example, banks may refuse to fund young and small businesses, which are considered extremely risky). Hence, business capital structure choice is often determined by the level of business dependency or independency from bank financing. When access to different sources of funding is available, companies may choose non-banking funding to stay independent, while if bank financing is restricted, companies are forced to borrow funds in alternative markets (Bokpin, Citation2010). The determinant of a company’s credit rating may also play an important role in business capital structure choice because, as it was noted by Datta et al. (Citation2000) and Sprčic and Wilson (Citation2007), issuance of corporate bonds is profitable only to large companies with a high credit rating, while other companies are to a large extent dependent on bank financing. Lithuania cannot boast of having a large number of business corporations with high international credit ratings, which means that the vast majority of Lithuanian business companies are dependent on bank financing.

In the money market determinants group, interest rates fixed by central banks, deposit interest rates, interest rates for non-deposit funds, a surplus of free funds in households and business accounts, and the rate of bond yields can be considered the main determinants of business capital structure choice. According to Misati and Nyamongo (Citation2012), the interest rate channel is the main channel to transmit the decisions of monetary policy because through this channel nominal short-term interest rates influence long-term interest rates, which determine the level of borrowing. Although low fixed interest rates reduce real borrowing costs for potential debtors, they also mean low potential profit for banks, which, in turn, discourages them from active lending of funds (Rey, Citation2013; Rey, Citation2014). Similarly, low deposit rates do not promote the accumulation of extra funds in banks because they discourage potential depositors from depositing their available funds, which, in turn, reduces the volumes of bank lending (Miranda-Agrippino & Rey, Citation2015). The same tendencies can be observed while analysing the impact of the interest rates paid for non-deposit funds (e.g., funds in current accounts, savings accounts, etc.). Negative or close-to-zero interest rates paid for non-deposit funds promote home saving and consumption rather than keeping money in banks; as a result, banks have smaller amounts of funds that could be used for lending (Misati & Nyamongo, Citation2012; Miranda-Agrippino & Rey, Citation2015). Moreover, a surplus of free funds in households and business accounts promotes investment – individual and institutional investors are inclined to use free funds for acquisition of different kinds of equities, including bonds, because they can expect high returns on their investment (e.g., high bond yields) in comparison to profitability of deposit and non-deposit funds kept in banks (Rey, Citation2014; Gregorio, Citation2010; Ahmad et al., Citation2014).

Many authors (Genenc, Citation2003; Bokpin, Citation2010; Strickland, Citation2013; Zabala & Josse, Citation2014; Hutchinson et al., Citation2016; Sukcharoensin, Citation2017, etc.) confirm that the determinants of business capital structure choice largely depend on specific characteristics of a company. According to Antoniou et al. (Citation2002), external funding is preferred by the companies that are involved in risky businesses, for instance, gambling, trade in cryptocurrencies, etc. Issuance of bonds improves a company’s image and makes a company look more transparent in the public eye, which, in turn, helps to earn investors’ trust and contributes to an increase in stock liquidity (Hutchinson et al., Citation2016; Sukcharoensin, Citation2017). What is more, issuing bonds, a company can verify market reactions to particular business ideas. A company’s financial capacity can also be attributed to the group of specific characteristics of a company, as financially capable companies can afford to choose any sources of funding regardless of their costs, i.e., financially capable companies can afford to borrow not only the cheapest funds, but also any strategically attractive funds (Bokpin, Citation2010; Strickland, Citation2013; Zabala & Josse, Citation2014; Sukcharoensin, Citation2017). On the other hand, for financially weak, young, and risky companies issuance of bonds can be the only available source of external financing because availability of bank funding for these companies can be restricted (Sprčic & Wilson, Citation2007). Finally, the choice of a particular source of financing can be determined by the need to diversify sources of financing in the general structure of a company’s capital (Hutchinson et al., Citation2011; Ehlers et al., Citation2014; Hutchinson et al., Citation2016).

To summarise, the analysis of the scientific literature has revealed that the main determinants of business capital structure choice include general economic determinants, linked to economic development of a country, the level of a stock market development, size of the banking sector and the level of finance market development; bank sector determinants, primarily the procedures of bank loan issuance, legal regulation of the banking sector, the rate of deposit insurance premiums, (in)dependency of a business company from bank financing and a company’s credit rating; money market determinants, which cover interest rates fixed by central banks, deposit interest rates, interest rates for non-deposit funds, surplus of free funds in households and business accounts, the rate of bond yields; and specific characteristics of a company such as the nature of the business, a company’s financial and marketing objectives, financial capacity, availability of different sources of financing and the need to diversify sources of financing. These determinants will be presented for expert evaluation in the empirical part of the research.

4. The methodology of the research

Following the propositions in the scientific literature, the research based on the method of expert evaluation has to involve 10–100 experts (an accurate number of the experts depends on the primary purpose of the research and the competence of the experts in the researched area) (Augustinaitis et al. Citation2009)). For this research, the expert evaluation was carried out by applying both direct (personal in-depth interviews) and indirect (telephone and e-mail interviews) methods of data collection using a questionnaire, which was prepared in advance. Apart from creativity, attitude towards the expertise, judgement flexibility, reliability, self-criticism and related qualities, scientific literature (Augustinaitis et al., Citation2009) emphasises the significance of expert competence. Thus, while selecting the experts, we considered their competence, long-term experience, acknowledgment with the situation of bank and non-bank sectors, and an understanding of the issues of corporate financing in Lithuania. Hereby, following the above-mentioned criteria, we selected eight experts: an independently operating broker with over 15 yearsʼ experience in the area of financial intermediation, representatives of ‘Danske’ bank working with securities, and managers of the company ‘Orion Securities’ with over 20 yearsʼ experience in investment banking, assets management and financial intermediation in capital markets.

In their study, Augustinaitis et al. (Citation2009) refer to Libby and Blashfield (Citation1978), who proved that in the modules of aggregated expert evaluations with equal weights, the accuracy obtained while surveying small expert groups is not lower than the accuracy obtained while surveying large expert groups.

The questionnaire (see Appendix 1) was composed of nine questions, which helped to collect the general information about the experts and identify the determinants of corporate borrowing in alternative markets over borrowing from banks under the impact of monetary policies in Lithuania. The experts were asked to evaluate each of the statements on a Likert evaluation scale, where rank 1 stood for the lowest evaluation (I completely disagree / it is completely insignificant), and rank 5 for the highest possible evaluation (I completely agree / it is extremely significant). In accordance with the strength of agreement/disagreement with a particular statement, intermediate ranks 2, 3 or 4 could be selected. The results of the research were processed with SSP (Statistical Package for Social Sciences) and Microsoft Excel software. The generalised rank values are presented in .

Table 2. Matrix of the expert evaluation results on the determinants of corporate borrowing in alternative markets.

In , value Vjn reflects the level of significance, which was attributed to statement n by expert j. By employing the introduced matrix, rank sum Vi for statement i, as well as rank sum Si’s average for statement i were estimated, and the significance of each of the statements along with compatibility of the experts’ opinions (expressed as Kendall’s coefficient of concordance (W)) were established. Variability of Kendall’s coefficient of concordance falls into the interval 0 ≤ W ≤ 1, which means that the values of the coefficient close to 1 show high compatibility of the experts’ opinions. When W ≤ 0.6, compatibility of the expert evaluation results is considered weak, but if p < 0.05, the data can be treated as reliable.

When introducing the results of the expert evaluation, special attention should be drawn to interpretation of the values of the Cronbach alpha coefficient. Some scientists, e.g., Nunnally and Bernstein (Citation1994), point out that the Cronbach alpha coefficient must be higher than 0.7. To obtain the most accurate results, we additionally employed the method of linear regression model.

Many previous scientific studies focus on the theoretical impact of economic indicators on corporate borrowing in finance and bank markets. In our research, we aimed to disclose the determinants that have the greatest impact on corporate borrowing in finance markets from a practical point of view. For this reason, apart from the general indicators, we included such financial determinants as interest rates and bond yields.

5. The results of the empirical research

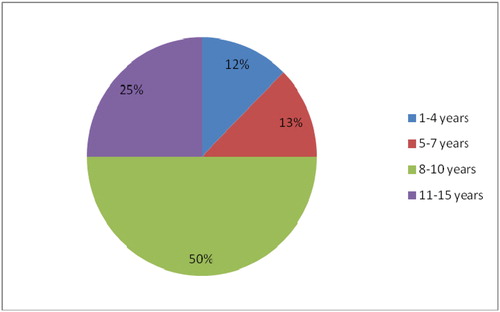

Data processing allowed us to draw up the chart that reflects distribution of the experts’ experience in the area of financial intermediation (see ).

Figure 1. Experts’ experience in the area of financial intermediation, per cent (source: compiled by the authors with reference to the results of the expert evaluation).

shows that 50 per cent of the experts have acquired eight-to-ten yearsʼ experience, and 25 per cent of the experts had eleven-to-fifteen-yearsʼ experience in the area of financial intermediation. Seven experts have a licence for financial intermediation, the average duration of which is equal to 6.625 years.

Using their professional experience, the experts evaluated the proposed bank sector determinants of corporate borrowing in alternative markets over borrowing from banks (see ).

Table 3. Bank sector determinants of corporate borrowing in alternative markets.

The results of the estimations (see ) are interpreted as follows: if a mean rank estimated for a particular determinant is equal to or higher than 3.5, it is considered that the determinant is statistically significant; if a mean rank estimated for a particular determinant is equal to or lower than 3.4, it is considered that the determinant is statistically insignificant. The data in indicates that Lithuanian business corporations, in particular, young and risky ones, feel the need to fill the gap in bank financing and reduce their dependence from bank financing (estimated mean rank is equal to 4.13). With reference to the research results, it can be stated that corporate borrowing in finance markets is also promoted by strict internal procedures of bank loan issuance and high requirements for potential borrowers determined by strict legal regulation of the banking sector (estimated mean ranks are equal to 3.88). Seventy-five per cent of the experts indicated that strict regulation of the banking sector burdens corporate financing with long and complicated loan issuance procedures, credit limits for a single borrower, etc. What is more, strict regulation of the banking sector makes bank financing unavailable to young or fast expanding corporations. According to the experts, strict regulation, for instance, over mortgages, restricts bank financing opportunities, especially for corporations with non-standard capital structures. Bank financing was recognised as necessary for corporate risk management and financial stability, while high deposit insurance premium rates and absence of the internationally entrenched corporations with high credit ratings were not indicated as significant determinants of corporate borrowing in alternative markets. Nevertheless, some experts noted the impact of banking flexibility and the existence of the sectors which are not financed by banks.

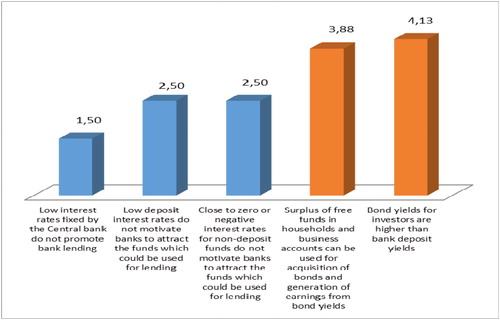

Further, the experts were asked to evaluate the impact of money market determinants (see ). The data in show that the main money market determinant of corporate borrowing in alternative markets is bond yield (which is more attractive to investors in comparison to bank deposit yield) (estimated mean rank is equal to 4.13). A surplus of free funds in households and business accounts also contributes to corporate borrowing in alternative markets (estimated mean rank is equal to 3.88), while low interest rates fixed by central banks, low deposit interest rates or low (close to zero) interest rates for non-deposit funds do not have any significant impact on business capital structure choice in Lithuania.

Figure 2. Money market determinants of corporate borrowing in alternative markets, mean ranks (Kendall’s coefficient of concordance is equal to 0.876, and value p is equal to 0.000).

While evaluating the impact of specific characteristics of a company, the experts ranked the proposed statements on a Likert evaluation scale (see ). Mean ranks in show that Lithuanian business companies are inclined to issue bonds, as access to alternative financing is much better than access to bank financing (estimated mean rank is equal to 3.88). The improvement of a company’s image in the public eye was recognised as a less significant determinant (estimated mean rank is equal to 3.63).

Table 4. Specific characteristics of company that determine corporate borrowing in alternative markets.

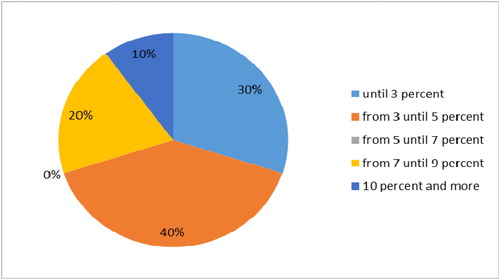

The experts also stressed the importance of the difference (in percentage points) between alternative financing and bank financing costs (see ).

Figure 3. Importance of the difference (in percentage points) between alternative financing costs and bank financing costs.

The data in show that 40 per cent of the experts were of the opinion that the difference between alternative financing costs and bank financing costs in Lithuania is from three to five per cent; Thirty per cent of the experts indicated that this difference may be three to twenty per cent; twenty per cent of the experts marked the difference from 7 to 9 per cent; and ten per cent of the experts noted that alternative financing is ten per cent more expensive than bank financing.

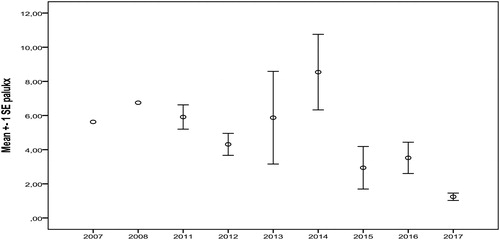

Figure 4. Interest average rates ± standard deviation over the period 2007–2017.

To obtain the most accurate results from the research, a linear regression model was employed. represents the results of the estimated interest average rates.

The data in show that interest average reached its highest value (8.54 ± 2.21, with 95 per cent reliability interval [3.31–13.8]) in 2014. Over the period from 2015 to 2017, interest average was equal to 2.78 ± 0.59, with 95 per cent reliability interval [1.52–4.04]. While verifying the hypothesis about the average differences, it was established that over the period from 2015 to 2017, interest average was significantly lower than in 2014: the value of Mann-Whitney criterion p was equal to 0.032; interest average, estimated for the periods from 2007 to 2013 and 2015 to 2017, was significantly lower than the average, estimated for 2014 (the value of Mann-Whitney criterion p was equal to 0.003).

The statistical comparisons of the interest average rates for the periods 2007–2014 and 2015–2017 have been presented in and . The data in and show that the interest average rate, estimated for the period 2007–2014, was significantly higher (6.6) than the average rate, estimated for the period 2015–2017 (value p of t criterion was equal to (0.004). Nevertheless, statistically significant trends of the annual interest rate reduction have not been captured; the annual trend explains only 7.3 per cent of the changes in the variable; the value p of F criterion is equal to 0.105 and exceeds the level of significance (see Annex 2). The coefficients, estimated for the regression model, show that the average interest rate decreased by only 0.499 per cent over the period under research (see Annex 3). Since the regression model for the variable interest average rates R2 = 0.073 and the F criterion Sig. value> 0.05, it shows that the included variable year in this case is not significant, which means that the model is not reliable, even not applicable. The dynamics of AAR annual average rates have been depicted in . The data in show that AAR annual average rates were slightly increasing from 2006 to 2008, but in 2008 began to decrease. Over the period 2007–2017, AAR annual average rates significantly decreased by 0.354 per cent (see Annex 4). The annual trend explains 87.3 per cent of the changes in AAR. The variable ARR model is R2 = 0.873 and the F criterion is Sig. value <0.0, which indicates that variable year included into the model is significant and the model itself is reliable.

Figure 5. AAR annual average rates ± standard deviation over the period 2006–2017.

Table 5. Comparison of the basic statistical data of the interest average rates for the periods 2007–2014 and 2015–2017.

Table 6. The results of the equality of variance tests.

By employing the standardised AAR and interest rate data (so-called z points, when z is estimated by the formula z = (an indicator − an average)/(standard deviation)), we established that the annual interest rate decreased by approximately 0.118 (95 per cent reliability rate (−0.261; 0.026) of its standard deviation) (see Annex 5), however, the findings are unreliable, since the Sig. value> 0.05 while the annual AAR average rate decreased by approximately 0.276 (95 per cent reliability rate (−0.294; −0.258) of its standard deviation) (see Annex 6). As the regression coefficient reliability intervals do not intersect, it can be concluded that over the period under research, AAR rate was decreasing significantly faster than interest rate.

Summarising the results of the empirical research, it can be stated that Lithuanian business corporations prefer alternative financing (i.e., issuance of bonds) with a view to reducing their dependence from bank financing, especially in the cases when banks refuse to fund young and risky businesses. The main money market determinant of corporate borrowing in alternative markets is attractiveness of bond yields to potential investors. In addition, Lithuanian business corporations issue bonds because access to alternative financing is better than access to bank financing. The results of the linear regression model have not revealed any statistically significant trends of the annual interest rate reduction. The annual trend explains only 7.3 per cent of the changes in the average interest rate; value p of F criterion is equal to 0.105 and exceeds the level of significance. Therefore, making any conclusions about the variable average interest rate on the basis of a regression model for the period 2007–2017 would not be correct. Over the same period, AAR annual average rates significantly decreased by 0.354 per cent, and the annual trend explains 87.3 per cent of the changes in AAR. Employment of the standardised AAR and interest rate data (i.e., the method of z-point estimation) has disclosed that the annual AAR average rate decreased by approximately 0.276 over the period under research. As the regression coefficient reliability intervals do not intersect, it can be concluded that over the period under research, AAR rate was decreasing significantly faster than interest rate.

Conclusions

The theoretical and empirical research, presented in this article, leads to the following conclusions:

The main determinants of business capital structure choice include general economic determinants, linked to economic development of a country, the level of a stock market development, size of the banking sector and the level of a finance market development; bank sector determinants, primarily the procedures of bank loan issuance, legal regulation of the banking sector, the rate of deposit insurance premiums, (in)dependency of a business company from bank financing and a company’s credit rating; money market determinants, which cover interest rates fixed by central banks, deposit interest rates, interest rates for non-deposit funds, surplus of free funds in households and business accounts, the rate of bond yields; and specific characteristics of a company such as business nature, a company’s financial and marketing objectives, financial capacity, availability of different sources of financing and the need to diversify sources of financing.

The results of the expert evaluation indicate that Lithuanian corporate borrowing in finance markets is promoted by strict internal procedures of bank loan issuance and high requirements for potential borrowers determined by strict legal regulation of the banking sector (estimated mean ranks are equal to 3.88). Seventy-five of the experts indicated that strict regulation of the banking sector burdens corporate financing with long and complicated loan issuance procedures and credit limits established for a single borrower. In addition, strict regulation of the banking sector makes bank financing unavailable to young or fast expanding corporations, while strict regulation over mortgages restricts bank financing opportunities for corporations with non-standard capital structures. Nevertheless, strict regulation is necessary for bank risk management and stability of the finance sector.

The research has revealed that high deposit insurance premium rates and absence of the internationally entrenched corporations with high credit ratings are not treated as significant determinants of Lithuanian corporate borrowing in alternative markets. Nevertheless, some experts noted the impact of banking flexibility and existence of the sectors which are not financed by banks.

The results of the regression analysis have not revealed any statistically significant trends of the annual interest rate reduction. The annual trend explains only 7.3 per cent of the changes in the average interest rate; value p of F criterion is equal to 0.105 and exceeds the level of significance. The coefficients, estimated for the regression model, show that the average interest rate decreased by only 0.499 per cent over the period 2007–2017, but these conclusions are unreliable, since the resulting model is not suitable for application. Over the same period, AAR annual average rates significantly decreased by 0.354 per cent, and the annual trend explains 87.3 per cent of the changes in AAR. Employment of the standardised AAR and interest rate data (i.e., the method of z-point estimation) has disclosed that the annual interest rate decreased by approximately 0.118, while the annual AAR average rate decreased by approximately 0.276 over the period under research. As the regression coefficient reliability intervals do not intersect, it can be concluded that over the period under research, AAR rate was decreasing significantly faster than interest rate.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abor, J., & Biekpe, N. (2006). The South African financial market and financing choice of SMEs. Journal of Business and Society, 19 (1/2), 187–201.

- Agarwal, S., & Mohtadi, H. (2004). Financial markets and the financing choice of firms: Evidence from developing countries. Global Finance Journal, 15(1), 57–70. doi: 10.1016/j.gfj.2003.10.004

- Ahmad, W., Bhanumurthy, N. R., & Sehgal, S. (2014). The Eurozone crisis and its contagion effects on the European stock markets. Studies in Economics and Finance, 31 (3), 325–352. doi: 10.1108/SEF-01-2014-0001

- Ahmed, A. D., & Mmolainyane, K. (2014). Financial integration, capital market development and economic performance: Empirical evidence from Botswana. Economic Modelling, 42 (C), 1–14. doi: 10.1016/j.econmod.2014.05.040

- Antoniou, A., Guney, Y., & Paudyal, K. (2002). Determinants of corporate capital structure: Evidence from European countries. Working paper. Durham: University of Durham, 1–31.

- Augustinaitis, A., Rudzkienė, V., Petrauskas, R. A., Dagytė, I., Martinaitytė, E., Leichteris, E., … Žilionienė, I. (2009). Lietuvos e. valdžios gairės: Ateities įžvalgų tyrimas [Guidelines of lithuanian e government: Future insight research]. Kolektyvinė monografija. Vilnius: Mykolo Romerio Universitetas.

- Beck, T., Demigurc-Kunt, A., & Martinez, P. M. S. (2007). Reaching out: Access to and use of banking services across countries. Journal of Financial Economics, 55 (1), 234–266. doi: 10.1016/j.jfineco.2006.07.002

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2010). Financial institutions and markets: Across countries and over time. The World Bank Economic Review, 24 (1), 77–92. doi: 10.1093/wber/lhp016

- Bokpin, G. A. (2010). Financial market development and corporate financing: Evidence from emerging market economies. Journal of Economic Studies, 37 (1), 96–116. doi: 10.1108/01443581011012270

- Booth, L., Aivazian, V., Demirguc-Kunt, A., & Maksimovic, V. (2001). Capital structures in developing countries. Journal of Finance, 56 (1), 87–130. doi: 10.1111/0022-1082.00320

- Claudio, B., & Lowe, P. (2002). Asset price, financial and monetary stability: Exploring the nexus. (BIS Working Paper No. 114), Basel: Bank for International Settlements. July.

- Daquila, T. C. (2007). The Transformation of Southeast Asian Economies. New York, NY: Nova Publishers:

- Datta, S., Iskandar-Datta, M., & Patel, A. (2000). Some evidence on the uniqueness of initial public debt offerings. Journal of Finance, 55 (2), 715–743. doi: 10.1111/0022-1082.00224

- Ehlers, T., Packer, F., & Remolona, E. (2014). Infrastructure and corporate bond markets in Asia. Reserve Bank of Australia, Conference volume, 67–91.

- Fama, E. (1985). What’s different about banks?. Journal of Monetary Economics, 17, 239–249. doi: 10.1016/0304-3932(85)90051-0

- Francis, B. B., Hasan, I., & Ofori, E. (2015). Investor protections, capital markets, and economic growth: The African experience. In K. John, A.K. Makhija, & S.P. Ferris (Eds.), International corporate governance (Advances in financial economics), (Vol. 18, pp. 239–272). West Yorkshire: Emerald Group Publishing Limited.

- Genenc, H. (2003). Capital structure decisions under micro institutional settings: The case of Turkey. Journal of Emerging Market Finance, 2 (1), 57–82.

- Gregorio, J. (2010). Monetary policy and financial stability: An emerging markets perspective. International Finance, 13 (1), 141–156.

- Hutchinson, N., Fraser, P., Adair, A., & Srivatsa, R. (2011). The risk free rate of return in UK property pricing. Journal of European Real Estate Research, 4 (3), 165–184. doi: 10.1108/17539261111183407

- Hutchinson, N., Squires, G., Adair, A., Berry, J., Lo, D., McGreal, S., & Organ, S. (2016). Financing infrastructure development: Time to unshackle the bonds?. Journal of Property Investment & Finance, 34 (3), 208–224. doi: 10.1108/JPIF-07-2015-0047

- Iljins, J., & Skvarciany, V. (2015). The role of change management in trust formation in commercial banks. Verslas: Teorija ir Praktika, 16, 373–378. doi: 10.3846/btp.2015.557

- Kristiansen, E. G. (2004). Financial intermediation and firms’ capital structure. Bergen: Norwegian School of Economics and Business Administration.

- Libby, R., & Blashfield, R. K. (1978). Performance of a composite as a function of the number of judges. Organizational Behavior & Human Performance, 21, 121–129.

- Masoud, N., & Hardaker, G. (2012). The impact of financial development on economic growth: Empirical analysis of emerging market countries. Studies in Economics and Finance, 29 (3), 148–173. doi: 10.1108/10867371211246830

- Miranda-Agrippino, S., & Rey, H. (2015). World asset markets and the global financial cycle (Working Paper No. 21722). National Bureau of Economic Research. 1050 Massachusetts Avenue Cambridge. Retrieved from http://www.nber.org/papers/w21722.pdf

- Misati, R. N., & Nyamongo, E. M. (2012). Asset prices and monetary policy in Kenya. Journal of Economic Studies, 39 (4), 451–468.

- Mutenheri, E., & Green, C. J. (2003). Financial reform and financing decisions of listed firms in Zimbabwe. Journal of African Business, 4 (2), 155–170. doi: 10.1300/J156v04n02_08

- Naik, P. K., & Padhi, P. (2015). On the linkage between stock market development and economic growth in emerging market economies: Dynamic panel evidence. Review of Accounting and Finance, 14 (4), 363–381. doi: 10.1108/RAF-09-2014-0105

- Nunnally, J. C., & Bernstein, I. H. (1994). Psychometric theory (3rd ed., p. 264–265). New York: McGraw-Hill.

- Radivojević, N., Ćurčić, N. V., & Vukajlović, D. D. (2017). Hull-White‘s value at risk model: Case study of Baltic equities market. Journal of Business Economics and Management, 18 (5), 1023–1041. Retrieved from doi: 10.3846/16111699.2017.1357049

- Rey, H. (2013). Dilemma not trilemma: The global cycle and monetary policy independence. Proceedings - Economic Policy Symposium, Jackson Hole, 1–2.

- Rey, H. (2014). The international credit channel and monetary autonomy. CEPR & NBER Mundell-Fleming Lecture IMF, 13 November 2014. Retrieved from https://www.imf.org/external/np/res/seminars/2014/arc/pdf/Mundell.pdf

- Sprčic, D. M., & Wilson, I. (2007). The development of the corporate bond market in Croatia. EuroMed Journal of Business, 2 (1), 74–86. doi: 10.1108/14502190710749965

- Strickland, T. (2013). The financialisation of urban development: Tax increment financing in Newcastle upon Tyne. Local Economy: The Journal of the Local Economy Policy Unit, 28 (4), 384–398. doi: 10.1177/0269094213475857

- Sukcharoensin, S. (2017). A framework for benchmarking the strategic position of bond markets in the competing environment. Benchmarking: An International Journal, 24 (2), 403–414. doi: 10.1108/BIJ-05-2015-0046

- Thukral, S., Sridhar, S., & Joshi, M. S. (2015). Review of factors constraining the development of Indian corporate bond markets. Qualitative Research in Financial Markets, 7 (4), 429–444. doi: 10.1108/QRFM-01-2015-0002

- Trigueros, M. L. (2000). La Importancia de la Protección de los Derechos de Propiedad en el Sistema Financiero y en el Crecimiento Económico. Banxico: Documento de Investigación.

- Zabala, C. A., & Josse, J. M. (2014). Shadow credit and the private, middle market Pre-crisis and post-crisis developments, data trends and two examples of private, non-bank lending. The Journal of Risk Finance, 15 (3), 214–233.