?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The aim of this paper is to analyse how employees may affect firm’s corporate governance. We analyse shareholder–manager relationship through a principal-agent framework. The manager is the agent in charge of taking decisions for firm’s success. Yet, when deciding, the manager takes into account employees’ preferences, i.e., the manager wants to enjoy a ‘quiet life’. We build a theoretical (mathematical) model based on principal-agent models in which the manager (the agent) interacts with the shareholder (principal) but it is influenced by employee’s decisions. Our results highlight that having a quiet-life manager is not necessarily linked to a destruction of value, as suggested in recent research. It might even recover part of the efficient decisions (at a cost borne by the shareholder). This research links the management of human resources with corporate governance enlarging the concept of corporate governance itself. It may help to differentiate better situations where labour is highly protected from those that are not as protected, which in turn has implications on the level of manager’s discretion.

1. Introduction

Corporate governance has been traditionally studied from the perspective of the existing conflict between firm’s owners (shareholders) and who runs the firm (the manager).1 The main concern of the shareholder is, then, how to provide the manager with enough incentives and/or how to monitor manager’s activities to induce him to select the right decision (from shareholder’s point of view), since otherwise, the manager would pursue his own interests which are typically assumed to be inefficient.

However, which is the personal goal that a manager might follow as well as the departures that it imposes from shareholder’s objectives has to be defined. Several theories aim at explaining such departure. Perk consumption has been highlighted as one of the main motivation that a manager might follow, for example in the seminal papers of Jensen and Meckling (Citation1976) or Fama and Jensen (Citation1983) to name just a few. An alternative departure behaviour is known as the empire-building motivation where it is assumed that the size of the private benefits that a manager may enjoy increases with the size of the firm (the larger the firm, the larger the opportunities to extract resources).

Nonetheless, recent research proposes an alternative managerial bias aiming at explain which is the goal that departs manager from shareholder’s maximisation value. Bertrand and Mullainathan (Citation2003) empirically show that when a manager is insulated from takeovers, workers’ wages rise as well as the creation of new plants or the destruction of old plants falls. The authors suggest that avoiding conflict with employees appears to be a potential reason that can explain manager’s behaviour when taking decisions.

Therefore, in order to have a better understanding of corporate governance, it is necessary not to restrict the problem just to a conflict between managers and shareholders. Even if this is the main conflict on corporate governance enlarging our view by including other members of the firm, i.e., the stakeholders, may help to have a more complete figure of the analysis.2 In this line, for instance, Pagano and Volpin (Citation2005) or Cespa and Cestone (Citation2007) analyse how a manager can set informal contracts with different stakeholders as a mechanism to entrench his position in the firm, i.e., avoiding hostile takeovers.

In Pagano and Volpin (Citation2005), the authors claim that manager and employees are ‘natural allies’ against new acquires. The manager tends to offer a lax employment policy as a mechanism to reduce the likelihood of being under a hostile takeover. The main effect is driven because the manager wants to enjoy a ‘quiet-life’, i.e., the manager is not willing to monitor employees since he does not internalise the costs from not doing it. In Cespa and Cestone (Citation2007), the authors show that the manager is able to set informal contract with stakeholders different than employees as a mechanism to entrench his position at the firm. Differently from Pagano and Volpin (Citation2005), they show that when these implicit agreements are made explicit, the ability of the manager to increase his discretion (to entrench his position) is no longer possible. Indeed, shareholders may have a selfish interest in promoting a stakeholder society as long as shareholders and stakeholders may have some congruence of interests. Also, Cennamo et al. (2009) show that managers can use stakeholder preferences to increase power over the firm (at the expense of sharehodlers). More recently, Masulis, Wang, & Xie (Citation2018) show that manager-employees alliances reduce the disciplining effect of shareholders.

Our paper follows this strand of research by considering that managers want to enjoy a ‘quiet-life’ in the firm. We differ from Pagano and Volpin (Citation2005) and Cespa and Cestone (Citation2007) since we do not consider how this informal relations within different members of the firm may affect the market for corporate control. Instead we are concerned in analysing how this behaviour may affect firm’s internal decisions. We consider that the manager has discretion on the selection of the firm’s strategy and also the implementation of it (that is to say, the board is rubber-stamping). It is important to remark that, differently from the papers mentioned above, we do not model explicitly employees’ behaviour. We model the shareholder–manager relationship by means of a principal-agent model where the manager is aligned, up to some degree, with employees’ preferences.

In particular, we assume that the production process takes place in two stages. In the first stage, the manager chooses firm’s strategy (where does the firm want to go?) or simply the firm’s project.3 For simplicity, we assume that the manager has the discretion to choose only between two possible strategies: one alternative provides higher growth opportunities although it is riskier whereas the second strategy is assumed to be less profitable and less risky (safer) than the former one. The second stage regards day-by-day decisions: once the project is selected, the manager chooses the level of effort that maximise his own utility. An important assumption to our model is that depending on the project chosen, the manager may find easier or costlier to take day-by-day decisions. In particular, if the manager opts for the safer strategy, the one employee would like to be chosen, the firm is easier to manage.4

Our results show that having a quiet-life manager might not be directly related with an inefficient outcome, as stressed by Pagano and Volpin (Citation2005). On the contrary, if the manager has discretion not only about the level of effort but also about the choice of the firm’s strategy, we find out that there may be cases where the manager chooses more often the efficient strategy concerning a situation where the manager only controls the level of effort. There exist two effects driving this result. The first effect concerns the assumption on manager’s preferences for a quiet-life since this will tend to favour employees’ preferred project. The second effect relies on how important is the risk-taking vis-a-vis the quiet-life effect. If risk-taking is not very important relative to the quiet-life behaviour, having a quiet-life manager partially solves inefficient decision taking regarding the choice of the project. Recovering efficient decisions is borne by the shareholders since profits are lower in comparison with the case where they can contract upon the firm’s strategy. Yet, if risk-taking is huge enough, this result is no longer true and a quiet-life manager implies that the manager selects inefficient project for more combination of parameters. Summing up, the role of a quite-life manager has been considered as an inefficient behaviour, as suggested by Pagano and Volpin (Citation2005). Our results claim that this is not necessarily true since this bias may help to recover efficiency of the firm’s strategy (at a cost borne by shareholders). Hence, we expect to enrich the debate around corporate governance reforms, since improving shareholder’s protection might come not only at a cost for managers but also inefficient decision taking.

The paper is organised as follows. In Section 2, the model is presented. We determine the optimal contract under symmetric and asymmetric information in Section 3. We study the optimal contract when the manager has discretion over one decision (the level of effort) or both (the level of effort and the choice of the project) and compare the optimal decisions under asymmetric information with the efficient decisions (or decisions taken under symmetric information). Section 5 concludes and presents future research. All proofs are included in an Appendix.

2. Model

Consider the following economic situation described in . Initially, a shareholder (the firm’s owner) offers a contract to a manager. If the manager accepts, he runs the firm. We assume that the shareholder does not have the time or they lack the experience to run the firm, fact that explains why the firm is run by a manager.

Figure 1. Timeline of the model

The manager is hired in order to take decisions for enhancing shareholder’s value. Yet, we consider that the managerial decisions or the production process takes place in two different steps. First, the manager chooses the appropriate project (the firm’s strategy following Perotti & Von Thadden, Citation2006, terminology). Roughly speaking, that decision regards the level of risk the company is willing to cope. We will denote this decision by P. Second, the second decision is related with the expected value of the firm. That is to say, once the project is chosen, the manager takes decisions in order to enhance the value of the firm, i.e., ‘day-by-day’ decisions. We will denote this decision by e.

2.1. Choice of project and effort

The manager must select which is the firm’s project. We simplify the choice of the project by allowing him to choose only between two possible alternatives. The former will be called ‘safe’ and the latter ‘risky’. Roughly speaking, a safe project reduces, in relative terms, the riskiness of the company although it has also a lower expected value of the firm.

For the sake of simplicity, at the stage 3 the manager must choose among the following two alternatives P∈{R,S}. Therefore, given P the expected firm’s value is:

where

and eP is the effort implemented by the manager once the project is already chosen. Hence, given the same level of effort, choosing safe implies a lower expected value for the firm, although it is less risky. Formally,

and

.5 We assume that the manager has to choose one project or the other project, but we do not allow for a combination of both. This can be justified because the firm need a fix or even a sunk investment. Finally, we assume that the effort cannot be verified by the shareholder.

We interpret r as the opportunity cost of reducing the riskiness of the company. For instance, the manager may decide to diversify firm’s activities. Obviously, diversifying does not necessarily lead to a destruction of the expected value of the company. Yet, the shareholder can diversify their investments at least as good as the manager through the capital market and not through the firm. We can also interpret both projects by considering that the ‘risky’ project offers better growth opportunities, i.e., investing in new emerging markets while ‘safe’ means reinvesting in your own country.

2.2. Economic agents

As commented previously, the owners are risk neutral while the manager is risk averse. Thus, the shareholder’s utility function depends only on the expected value of the firm, that is to say,

which in turn imply that shareholder’s profits depend on the choice of the project. For instance, given the same level of effort, a risk neutral shareholder would prefer to choose ‘risky’.

The manager’s decision over firm’s project is the key point in this model. We assume that the choice of the project will have an effect not only on the riskiness of the company but also on the cost of managing human resources. Following Bertrand and Mullainathan (Citation2003), we consider that the manager’s decisions tend to be biased towards employees’ preferences. This implies that the manager has a tendency to choose the most preferred project from the employee’s point of view. As commented in the introduction, we assume that, among the available projects, employees would like to choose the safest one.6

Thus, the manager’s utility function takes the following form:

where we separate income from effort just for simplicity and a > 0.7 The parameter a reflects the save on costs that the manager may achieve if the choice of the project coincides with employees’ preferences, that is to say, the parameter reflects how important the ‘quiet-life’ behaviour is in the manager’s decision taking. A plausible interpretation of differences in the cost may be found in the institutional framework: different institutional frameworks regarding labour market would reflect different values of a.8 Therefore, we consider that the choice of the project has an implication on the level of effort that can be achieved.

Finally, we assume, for the sake of simplicity, that manager’s preferences are of a CARA type. Therefore, we may express the utility function of the manager through its certainty equivalent.9 Thus, we restrict attention to linear contracts, i.e., contracts of the form where α is a fix payment independent of the outcome and β depends on the firm’s performance. Thus, we can rewrite the manager’s utility function in the following way

where P∈{S,R} and ρ is the Arrow-Pratt risk-aversion coefficient and we consider, just for simplicity, the following quadratic manager’s cost of effort,

. For instance, we can rewrite manager’s certainty equivalent depending on the project selected. We can observe how the selection of the project has an effect both on the risk-taking and on the manager’s cost of effort,

3. Optimal contract with a ‘quiet-life’ manager

3.1. Symmetric information or efficient decisions

For the sake of comparison, let us analyse which is the efficient policy that the firm’s owner should adopt in this framework. Consider, initially, that both the project and the level of effort are verifiable variables. Therefore, the owner of the company can write both in a contract enforceable by the Court of Law. The optimal payment scheme and level of effort are the solution to maximise the shareholder’s wealth given that the manager accepts the contract. Formally, for P∈{S,R}

where U represents the manager’s reservation utility. Since the effort is verifiable and the manager is risk averse while the shareholder is risk neutral, she offers a fix salary to the manager (β = 0) in order to compensate him for the level of effort while she bears all the risk. The efficient level of effort is obtained by equating the marginal value of the project with the marginal cost of the manager’s effort, i.e., v′(e)=e = 1 + adP for P∈{S,R}. This means that the optimal level of effort that the shareholder can demand is, up to some extent, constrained (or enhanced) by the employees’ influence: a higher manager’s effort can be demanded whenever employees’ preferences are respected. As a result, the shareholder must balance between a higher level of effort from choosing the safe project and a higher expected value if the risky project is chosen. Formally, the levels of profits obtained from the choice of the project are

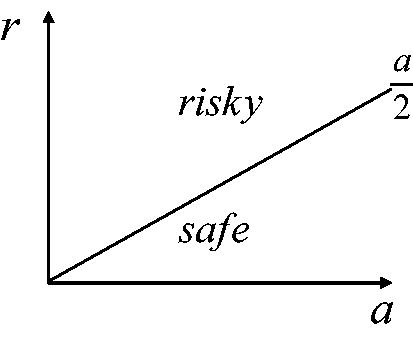

It is important to highlight that the shareholder is risk neutral, and therefore the optimal choice of the project and effort does not depend on the level of risk. It, then, depends only on how employees may affect to the firm’s management compared to the differences on profits from choosing one project or the other. In particular, if the shareholder will implement the risky project while the safe project is preferred whenever the opposite is true. The following figure graphically represents this effect ().

Figure 2. Optimal decisions regarding the choice of the strategy under symmetric information

3.2. Asymmetric information

In this section we would like to focus on the role played by the discretion that a ‘quiet-life’ manager enjoy when deciding both on the choice of the project as well as the level of effort. If the manager has discretion over the level of effort, the shareholder will have the need to provide incentives to reduce the moral hazard behaviour. Yet, this optimal payment scheme under moral hazard has real effect on shareholder’s decision upon the choice of the firm’s project by distorting them. Nevertheless, if the manager has also discretion concerning firm’s project, it may be the case that some of the efficiency is recovered.

3.2.1. Asymmetric information: effort is not contractible

We consider instructive to present the case where the manager’s effort is not verifiable whereas the choice of the project is still verifiable. By analysing this case, we observe that the level of effort is distorted due to the manager’s risk aversion. Moreover, we can observe how the moral hazard on effort generates distortions on firm’s project even if the shareholder can contract on such decision.

If the manager has discretion about the level of effort, he will choose the level that maximises his utility, i.e., eR∈ argmax CER (α,β). Yet, as we can note, this decision depends not only on the level of incentives provided by the shareholder but also on the shareholder’s choice of the project. If the shareholder finds worthy to implement the ‘risky project’, the level of incentives solves

(1)

(1)

that is to say, if the shareholder wants to implement a larger level of effort she must propose a higher powered incentive scheme. Differently, if the shareholder would find optimal to implement the safe project, the managerial incentives to exert effort are modified since the manager find less costly to implement this project. Formally,

(2)

(2)

highlighting the role of employees when a shareholder is contracting with a quiet-life manager.

Therefore, the shareholder chooses the payment scheme anticipating this behaviour in order to maximise expected profits given that the manager accepts the contract as well as she provides incentives to exert effort. If the shareholder wants to implement the risky project, she looks for an optimal payment scheme and an induced level of effort solving

(1)

(1)

The solution to this program follows the classical trade-off regarding providing incentives with a risk-averse agent. That is to say, since effort is non-verifiable, the shareholder optimally links compensation to the only source of available information (given that the outcome, this piece of information, is a noisy signal of manager’s effort). Yet, providing incentives is costly since the manager is a risk-averse agent, which in turn implies that the shareholder must pay a higher expected salary in order to let the manager accept the contract. As a result, the optimal level of effort induced by the payment scheme is lower than the efficient case (as well as the level of profits).

In a similar way, we can replay the exercise when the shareholder would prefer to implement the safe project. Choosing safe has both advantages and disadvantages. On the one hand, implementing ‘safe’ induces a lower cost of management of human resources, measured by a and, on the other hand choosing safe has a lower expected a lower expected value, which is measured by r. Formally,

(2)

(2)

As already mentioned, when ‘safe’ is selected the level of effort depends on the ‘quiet-life’ behaviour and on the incentives provided through the mechanism scheme. Eventually, the optimal level of incentives depends on the quiet life behaviour, as well. Hence, let us summarise the optimal contract in the following Lemma,

Lemma 1.

The optimal contract when effort is non-verifiable displays the following characteristics:

If ‘risky’ is chosen

and

if ‘safe’ is chosen

Therefore, the shareholder decides the optimal choice of the project by comparing the level of profits when implementing the optimal payment scheme. Let us define the threshold as the combination of parameters where the shareholder is indifferent between implementing ‘risky’ or ‘safe’. Intuitively, the shareholder will choose to implement ‘risky’ if the opportunity cost from choosing ‘safe’ are large enough while ‘safe’ should be selected if the opposite happens.

Proposition 1.

When a quiet-life manager has discretion on the choice of effort, the shareholder implements the risky project if while the safe project is implemented if the opposite takes place.

Thus, given the threshold we identify which kind of distortions regarding project’s choice are expected derived from the lack of verifiability on manager’s effort.

Proposition 2.

Moral hazard over effort generates distortions over firm’s project and these distortions are shaped by differences over risk between both projects. To be precise:

If these differences are large enough (

If differences are not large enough ((

b.1) for low values of a quiet-life behaviour, i.e.,

b.2) for high values of a quiet life behaviour, i.e.,

Our first result states that distortions compared to the efficient decisions are obtained around the efficient threshold (). In other words, if the opportunity cost is high the shareholder will select ‘risky’ independently of the moral hazard behaviour. Similarly, if the concerns about employees are huge enough, that is to say, the quiet-life behaviour is important then we should observe ‘safe’ as the optimal decision regardless of the opportunity cost. In both cases, we do not have a conflict between efficient and optimal decisions.

Yet, in the other cases, we have distortions on the shareholder’s selection of the firm’s project. In these cases, shareholder’s decisions not only depend on the relationship between a lower cost of managing human resources and a lower profitability but also on the manager’s attitude towards risk. In particular, part (a) of proposition 1 shows that if the differences over risk between both projects are large enough, the shareholder finds optimal to implement safe in situations where risky is efficient. The reason is that the manager is risk averse and in case the shareholder would want to implement risky she should compensate the manager for that risk taking. Hence, the larger the differences in variances, the larger the potential save in wages, and eventually the shareholder implements the safe project.

Instead, part (b) of proposition 1 states that if these differences are not large enough, shareholder’s distortions may be of two types. If the value of the quiet life behaviour is not very large, the main effect that dominates is still the save on wages through risk-taking. Yet, if the value of the quiet-life behaviour is large enough, shareholder’s distortion concerning efficient decisions depends on the relationship between having a lower managerial cost (high a) and a lower profitability (high r). In this case, the loss on profitability dominates the save on wages, which in turn imply that the shareholder implements risky when safe is the efficient decision.

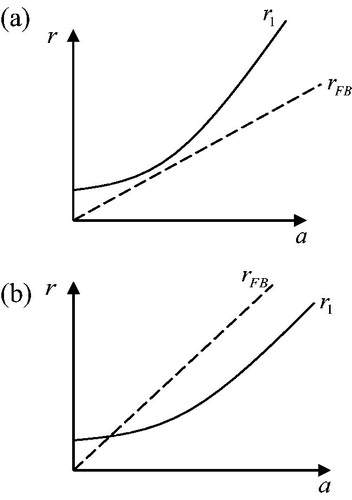

Let us represent these effects graphically in . In the first picture, we describe part (a) of proposition 1 while part (b) is described in the second picture. The black line represents the threshold in which the shareholder is indifferent between implementing P = R or P = S when effort is non-verifiable. Similarly, the dashed line represents the indifference line between implementing safe or risky when effort is contractible (symmetric information case).

Figure 3. (a) Distortion over firm’s strategy when the difference of variances between projects is large. (b) Distortion over firm’s strategy when the difference of variances between projects is small.

3.2.2. Asymmetric information: both effort and project are not contractible

The lack of verifiability of manager’s decisions imply that the shareholder must offer a contract depending only on the outcome yP, P∈{S,R}, since it is the only verifiable source of information. Recall that the choice of the manager’s effort depends not only on the incentives provided by the shareholder but also on the choice of project. Yet, the shareholder cannot contract on such decision. This implies that the payment scheme, in particular β, is the only mechanism available for the shareholder to induce the manager to select the right actions.

Thus, given that level of effort, the manager will choose the risky project if he finds worth to do it, i.e., she will offer a payment scheme such that the manager prefers to implement the risky project. Formally, R will be chosen if

and taking into account the level of effort derived previously, we get

(3)

(3)

In words, the manager will choose the risky project if the costs from adopting ‘risky’ are lower than the costs from adopting ‘safe’. The LHS of the last equation represents the costs from adopting the safe project. The safe project reduces the expected value of the firm by r, which is partially internalised through the payment scheme (β). The RHS of the equation represents the cost from adopting the risky project. The choice of the risky project implies two different costs for the manager: he must bear a higher level of risk as well as a larger cost of managing human resources. Therefore, if the shareholder wants to implement risky by providing optimal incentives, she offers an optimal payment scheme {α,β} that maximises her expected profits given that the manager accepts the contract and he has incentives to select the right effort and risky project. Formally,

Let us fix the value of the ‘quiet-life’ parameter in order to get the intuition of the solution to the shareholder’s problem. If the opportunity cost of choosing safe is high enough (a high r), the manager has the tendency to choose ‘risky’ since he internalises part of this cost (through β). Therefore, the shareholder selects the level of incentives, i.e., β, as the mechanism that induces the manager to select the right effort: the shareholder selects the same incentives to the case where firm’s project is verifiable. Instead, if the opportunity cost of switching from risky to safe is small (low r) the shareholder cannot choose the same incentive scheme since in this case the manager would change to ‘safe’. Hence, the shareholder optimally lowers the incentive mechanism. By lowering the incentives and linking them positively to the opportunity cost and negatively to the quiet-life behaviour, the manager finds optimal to implement risky.10

In order to determine the optimal decision, we need to do the same exercise by analysing which is the optimal contract that the shareholder should offer if she wants to implement ‘safe’. Formally, the shareholder should solve the following program

Yet, the solution to this problem is very similar to the previous one. Let us fix quiet-life behaviour to obtain the intuition of the shareholder’s program, as we did in the previous program. If the opportunity cost of choosing safe instead of risky (i.e., r) is not very high, the shareholder chooses the same payment scheme as if the choice of the project would have been verifiable. The idea is that the manager has a tendency to choose safe (quiet-life behaviour) and since the costs of choosing ‘safe’ are not very high she is not concerned about this restriction. Instead, if the opportunity cost is high enough the shareholder cannot opt for the same incentive scheme because the manager would implement a risky project. Therefore, the shareholder optimally empowers the incentive scheme by linking them to both the opportunity cost and the quiet-life behaviour. By doing this the manager internalises more the costs of choosing safe than the costs of selecting risky, which in turn imply that the manager opts for ‘safe’. Let us summarise the optimal contract in the following lemma, where and

are both increasing in the manager’s quiet-life parameter a.

Lemma 2.

If the manager has discretion on both the effort and the firm’s project, then:

In order to implement P = R, the optimal incentive scheme is:

In order to implement P = S, the optimal incentive scheme is:

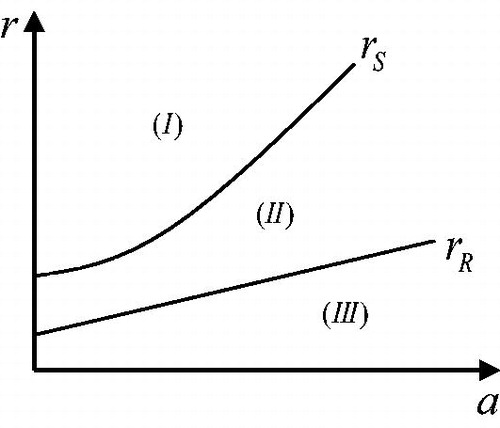

From Lemma 2 we learn which is the optimal payment scheme that the shareholder should implement when she wants to induce a given project and the corresponding level of effort. Yet, the shareholder wants to know which is the project that maximises profits and this is attained by comparing the level of profits achieved when the shareholder induces the manager to implement the safe project and the profits obtained when she induces the manager to implement risky project. Let us represent graphically the constraint stated in Lemma 2 since we will find helpful for understanding the optimal decision.

represents for every combination of parameters (r,a) which is the shape of the optimal contract when the shareholder implements either ‘safe’ or ‘risky’. To be precise, the dashed line represents part (a) of Lemma 2, i.e., the combination of parameters such that the shareholder is indifferent about the shape of the contract in order to implement ‘risky’. Analogously, the continuous line represents part (b) of lemma 2 and determines which should be the shape of the contract if ‘safe’ is the project to implement. Let us focus on the area (II) of the : in this area the shareholder can implement both risky and safe project by using the same incentives to the case where the project was verifiable. Yet, both in region (I) and (III) this is not the case anymore. For instance, in region (I) the shareholder can implement ‘risky’ by using the optimal incentives obtained in Lemma 1 while we need to distort incentives with respect to Lemma 1 for implementing ‘safe’.

Figure 4. Implementation of both strategies through optimal incentive scheme

A first intuition about the optimal decision regarding firm’s project would suggest that in the region (I) risky seems more appropriate since the opportunity costs of implementing safe are large. Analogously, in region (III) the shareholder would have a tendency to choose safe since the quiet-life behaviour is large. Finally, in region (II) although it seems unclear, we are coming back to the case where the decision about the firm’s project is verifiable where we have already defined where it is better to implement safe or risky. The following proposition analyses the comparison of the optimal profits and defines the optimal decision regarding firm’s project.

Proposition 3.

When a quite-life manager has discretion both on the level of effort and on the firm’s project, then

If

if

if

c.2) the optimal payment scheme is and ‘safe’ is chosen. This situation takes place if

As suggested in the initial intuition, the shareholder offers a contract that implements ‘Risky’ for large opportunity cost (relative to the quiet-life behaviour) as well as she offers a contract that implements ‘Safe’ whenever the opportunity cost (relative to the quiet-life behaviour) is low enough. This is the situation stated in parts (a) and (b) of proposition 2, respectively. In other words, even if a ‘quiet-life’ manager has also discretion on the choice of the project, these decisions are not distorted for this range of parameters. Moreover, the level of incentives provided to the manager is exactly the same to the case where project was verifiable (Lemma 2).

Nonetheless, part (c) of Proposition 3 determines the range of parameters where there exist distortions regarding firm’s project when it was verifiable. From Proposition 1 we know that the shareholder would have selected the risky project in case the shareholder would be able to contract upon the project. Yet, this is not true anymore and the manager has a tendency (quiet-life) to choose the safe project. The shareholder tries to correct this behaviour by lowering incentives (i.e., if

). However, lowering incentives has also an effect on the level of effort that the manager will achieve in the next stage of the production process. Therefore, the shareholder finds profitable to induce the manager to select ‘risky’ only if the opportunity cost is high within this region (

), while she prefers to induce the manager to select ‘safe’ if the opposite takes place (

). This corresponds to part c.1) and c.2) of Proposition 3, respectively.

Therefore, Proposition 3 states that if the manager has also discretion on the selection of the project, the shareholder has to implement ‘safe’ in more situations (part c.2 of Prop.3) than in the case the manager has no discretion about this decision. Yet, we are concerned with the effect of such discretion in the managerial decision taking vis-a-vis the efficient decisions. We find that the discretion of a quiet-life manager regarding project’s choice is not necessarily bad from the efficiency point of view, that is to say, this behaviour may be a source of recovering efficient decisions (at a cost bear by the shareholder). The following corollary summarises the comparison of the choice of the project when the manager has discretion over this decision and the efficient decisions,

Corollary

(of Proposition 3). When a quiet-life manager has discretion not only on effort but also on the choice of the project, it may be the case that

‘safe’ is chosen when ‘risky’ is efficient. This inefficient behaviour is enlarged compared to the situation where the manager has no discretion on such decision. This situation takes place if the differences on variance between both project is large enough (

efficient decisions are recovered in some situations compared to the case where the manager has no discretion on such decision. This situation takes place if the differences on variance between both project is low enough (

Corollary of Proposition 3 shows that an increase in manager’s discretion when he is concerned about employees’ preferences might be counterproductive but we find cases where this is not the case. Similar to Proposition 3, the distortions are also induced by the difference on risk between both projects. If the difference on variance is high, a higher manager’s discretion is clearly counterproductive since the manager has the tendency to choose safe even more since he has control on this decision. However, when the difference is low enough, the manager opts for ‘safe’, which is the efficient decision, whereas if the manager has no discretion on such decision, the shareholder would offer a contract implementing ‘risky’.

3.2.3. Discussion of the results and relationship with the literature

The quiet life effect is assumed to be an ability of the manager to construct some implicit relationships with workers that allows the firm to be managed easily (or in a more productive way). The model presented in this paper suggests that the level of manager’s discretion should be balanced with its ability to engage in relationships with employees, or enjoying the quiet-life effect. The introduction of regulations that reduce manager’s discretion for all firms, as many Corporate Governance regulations calls for, should be carefully analysed and try to accommodate for particular local conditions such as labour market. This ability, as presented in the model, may entail several costs.

First, assume the safe project is the status quo project and a new project (risky) is available. The model predicts that managers that want to enjoy a quiet-life easily block innovative strategies. Moreover, corollary 1 posit it as negative from an efficiency point of view. Therefore, policies aiming at reducing manager’s discretion or promoting investor protection should be taken in consideration in sectors where innovation is a crucial source of creation of value. Otherwise, managers have incentives to deter new efficient projects in order to gain on quiet-life. This is consistent with recent literature. For instance, Atanassov (Citation2013) shows that protecting against takeovers does not foster innovation whereas in a similar line Chen, Leung, and Evans (Citation2018) find out that introducing more stringent monitoring systems (through more women on the board) positively affects corporate innovation. If the firm is instead in a less innovative industry, then the effect is less clear and does not necessarily lead to overall welfare destruction. Koetter, Kolari, and Spierdijk (Citation2012) analyses precisely the quiet life hypothesis in the banking sector during the U.S. deregulation process showing that the quiet life effect has a negative impact on profits but it has no effect on cost efficiency.

Second, it is not obvious that a quiet life manager is always detrimental. Since Shleifer and Summers (Citation1988) shareholder gains/losses may arise at the expense/benefits of other stakeholders. If we only pay attention to shareholders, managers that internalise employees’ preferences are in general detrimental since shareholder may bear the cost of efficient strategy choice. However, recent literature suggests that having a being friendly may have positive effects during domestic acquisitions (see Liang, Renneboog, & Vansteenkiste, Citation2017).

Moreover, and as highlighted in this paper if we include other stakeholders and therefore we treat the firm as a Stakeholder society (see Tirole, Citation2001, Allen & Gale, Citation2002 for crucial contributions and more recently Magill, Quinzii, & Rochet, Citation2015), then it is not necessarily true that a manager that internalises preferences from workers must be always detrimental. In our view that depends on the whole corporate governance system. Hence, it is important to relate the quiet life effect to Corporate Governance systems (or even Legal Systems, see La Porta, López-de-Silanes, & Shleifer, Citation1999) since many reforms have a focus on the Anglo-Saxon system without not always taking into account the specifics and differences of other models, like the Continental European system (or even the Japanese Model).

While the Anglo-Saxon model is typically characterised by companies financed basically through equity with dispersed ownership, a very active market for corporate control and a very flexible low regulated labour market, the Continental European model is, instead, characterised by long-term debt finance, the presence of dominant shareholders and more regulated and rigid labour markets (see Botero, Djankov, Porta, Lopez-de-Silanes, & Shleifer, Citation2004 for an analysis of labour regulation in terms of different legal origins and Aguilera & Jackson, Citation2003 for a detailed analysis of the different Corporate Governance models). Moreover, CEO preferences are radically different depending on the system they are embedded in.11

One of the main findings of the literature is that the existence of this manager–worker alliance may reduce the strength of the market for corporate control. This is clearly negative for a corporate governance system to perform correctly. However, this external mechanism is less relevant in the Continental European than in the Anglo-Saxon model. Therefore, the existence of potential alliances between workers and managers may lead to improved productivity under the Continental European model. Indeed, under corporate governance structures that take explicitly into account worker’s preferences (for instance, German co-determination), these influences may lead to a welfare improvement for the stakeholder society. As showed in Kim, Maug, and Schneider (Citation2018) labour participation in governance structures in Germany improves risk sharing between firm and its employees, reducing the adverse effects of layoffs. In return to this, employees accept lower wages as compared to firms in which labour is not directly involved in corporate governance structures.12

4. Conclusions

This paper conveys the attention to a shareholder–manager relationship where the manager is aligned with employees’ preferences. We model it by means of a principal-agent model. We assume that the manager is an agent having discretion not only on the implementation of the project but also on the selection of it. A quiet-life manager is not indifferent between different projects for two reasons: the manager is risk averse and employees put pressure on the manager for choosing the safest project among the available ones. Under this framework, we show that if the manager has discretion on both decisions and the quiet-life behaviour is important, it might be better (in terms of choosing the right project) that the manager has discretion over both variables than a situation where the choice of the project is in hands of the shareholder. In other words, if improving corporate governance means reducing manager’s discretion (as any Corporate Governance Code suggests), it may be the case that it generates distortions on the manager’s decision taking. Therefore, if the regulator is concerned about efficiency the design of corporate governance rules should take into account this bias.

Under this framework, some predictions regarding corporate governance systems can be obtained. While the existence of worker-manager alliances may hinder the market for corporate control and it is expected detrimental in Anglo-Saxon countries, this is not the case in Continental European countries because of different internal mechanism can be used to correct inefficient quiet-life behaviours (for instance, through the use of dominant or large shareholders)

Another relevant aspect that we do not analyse is the degree of competition. In this sense, two opposing forces play a role. On the one hand, more competitive environments mitigate managerial slack which implies that the negative effects of a quiet life effect manager are lower. Giroud and Mueller (Citation2010) find evidence of this since only in non-competitive industries the reduction of anti-takeover devices increases wages and overhead costs (signal of quiet-life behaviour). However, looking for more friendly policies towards employees might allow the manager to build value-enhancing relationships with employees (Allen & Gale, Citation2002). A firm that has to compete in these environments may be able to build a competitive advantage with regard to a firm where the manager is not internalising employee’s preferences, faces a lower influence from employees.

Faleye and Trahan (Citation2011) finds out that labour friendly policies are not necessarily used as a mechanism used by managers to entrench themselves, but simply as a mechanism to improve firm’s productivity. In a similar line, Edmans (Citation2011) also show that companies where employees are satisfied are more profitable than its industry peers. We hypothesise that this potential competitive advantage may also take place when firms compete in highly protected labour market.

Acknowledgements

Eduard Alonso-Paulí thanks the editor and the anonymous referees for valuable comments. The research has benefit also from several discussions in congresses such as Jornadas de Economía Industrial, Simposio de Análisis Económico and The Workshop on Corporate Governance. Finally, the author gratefully acknowledges financial support from grant ECO2017-86305-C4-1-R (AEI/FEDER, UE)

Notes

Notes

1 Shleifer and Vishny (1997) states that Corporate Governance deals with the ways in which suppliers of finance to corporations assures themselves of getting a return on their investment. This classical definition includes not only shareholders but also creditors. Since by law shareholders are less protected than creditors, the main concern to analyze turns into the manager-shareholder relationship.

2 There has been a debate towards the role of the stakeholder society in economics. By stakeholder we refer to any participant of the firm apart from shareholders, that is to say, employees, suppliers, customers or local community. Several authors like Tirole (Citation2001) or Allen and Gale (Citation2002) appoints the need to include in the analysis the role played by stakeholders. More recently, Magill et al. (Citation2015) model the impact of the stakeholder corporation and provides conditions by which such a corporation might be superior to a shareholder value maximisation firm. The basic idea is that the stakeholder corporation does take into account externalities on workers and consumers that other types of corporation do not.

3 We take the terminology of firm’s strategy from Perotti and Von Thadden (Citation2006). Similar to them, by firm’s strategy we refer to the choice between two disjoint projects. This is why we call strategy or project indistinctively.

4 In particular, Faleye, Mehrotra, and Morck (Citation2006) finds out that if employees are paid through an ESOP (Employee Stock Option Plan), the firm typically tend to select less risky projects. In Aoki (Citation1990) it is shown that a diversification policy may become the outcome from a cooperative agreement between managers and employees (as a policy that let the firm reduce risk in their activities).

5 Obviously, we consider that the choice of the strategy only affects the mean and the variance of the company. We are aware that the riskiness of the company (any random variable) might include other higher moments. However, we only stare at these first two moments because we work with errors normally distributed. We are aware that is not without loss of generality. Therefore, the interpretation includes not only the quiet life behavior but also the dimension of the decision.

6 It is important to highlight that we do not model employees’ behavior. We model a Shareholder-Manager relationship where employees affect, up to some degree, manager’s decisions. Regarding employees’ preferences Faleye, Mehrohtra, and Morck (Citation2006) empirically finds that if employees are paid through an ESOP, the firm invests in less risky projects.

7 We are aware that this simplification is not without loss of generality. Therefore, the interpretation includes both the quiet life behavior but also the dimension of the decision.

8 Botero et al. (Citation2004) survey the different institutional frameworks around the world. It is remarkable the differences between the US or UK versus continental Europe.

9 See for instance Holmstrom and Milgrom (87) for the optimality of linear contracts.

10 Consider that the shareholder wants to implement risky but if then it might be the case that

for some parameters. Hence, if the shareholder lowers the incentives, the RHS lowers more than the LHS, which in turn imply that the manager selects risky again.

11 In this sense, in Yoshimori (Citation1995) CEOs were asked to answer whether the firm should be run ‘for the interest of all stakeholders’ or ‘shareholder interest should be given first priority’. The answer is radically different depending on CEO being Japanese or German or CEO being from US or UK. The former CEO were in favour of all stakeholders (97% in Japan and 84% in Germany) whereas in Anglo-Saxon countries the CEO chose the shareholder view (76% in US and 70% in UK).

12 Agrawal (Citation2012) also obtains that labor pension funds tend to be more inclined to take into account other than shareholder’s interests when investing in a particular company. We thank an anonymous referee for pointing this out. An alternative mechanism is through unionisation, the influence of unions in firms may reduce the pricing of risky debt because they influence corporate decisions to choose less risky projects protecting debtholders wealth (Chen, Kacperczyk, & Ortiz-Molina, Citation2012). Therefore, if managers internalise employees’ preferences at least up to some degree, there are potential benefits that may increase overall welfare (although shareholder’s wealth does not necessarily increase).

References

- Agrawal, A. K. (2012). Corporate governance objectives of labor union shareholders: Evidence from proxy voting. Review of Financial Studies, 25(1), 187–226. doi:10.1093/rfs/hhr081

- Aguilera, R. V., & Jackson, G. (2003). The cross-national diversity of corporate governance: Dimensions and determinants. The Academy of Management Review, 28(3), 447–465. doi:10.2307/30040732

- Allen, F., & Gale, D. (2002). A comparative theory of corporate governance (Working Paper No. 03-27). Wharton Financial Institutions Center.

- Aoki, M. (1990). Toward an economic model of the Japanese firm. Journal of Economic Literature, 28(1), 1–27.

- Atanassov, J. (2013). Do hostile takeovers stifle innovation? Evidence from antitakeover legislation and corporate patenting. The Journal of Finance, 68(3), 1097–1131. doi:10.1111/jofi.12019

- Bertrand, M., & Mullainathan, S. (2003). Enjoying the quiet life? Corporate governance and managerial preferences. Journal of Political Economy, 111(5), 1043–1075. doi:10.1086/376950

- Botero, J. C., Djankov, S., Porta, R. L., Lopez-de-Silanes, F., & Shleifer, A. (2004). The regulation of labor. The Quarterly Journal of Economics, 119(4), 1339–1382. doi:10.1162/0033553042476215

- Cespa, G., & Cestone, G. (2007). Corporate social responsibility and managerial entrenchment. Journal of Economics & Management Strategy, 16(3), 741–771. doi:10.1111/j.1530-9134.2007.00156.x

- Chen, J., Leung, W. S., & Evans, K. P. (2018). Female board representation, corporate innovation and firm performance. Journal of Empirical Finance, 48, 236–254. doi:10.1016/j.jempfin.2018.07.003

- Chen, H., Kacperczyk, M., & Ortiz-Molina, H. (2012). Do nonfinancial stakeholders affect the pricing of risky debt? Evidence from unionized workers. Review of Finance, 16(2), 347–383. doi:10.1093/rof/rfq028

- Edmans, A. (2011). Does the stock market fully value intangibles? Employee satisfaction and equity prices. Journal of Financial economics, 101(3), 621–640.

- Fama, E., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325. doi:10.1086/467037

- Faleye, O., Mehrotra, V., & Morck, R. (2006). When labor has a voice in corporate governance. Journal of Financial and Quantitative Analysis, 41(3), 489–510. doi:10.1017/S0022109000002519

- Faleye, O., & Trahan, E. A. (2011). Labor-friendly corporate practices: Is what is good for employees good for shareholders? Journal of Business Ethics, 101(1), 1–27. doi:10.1007/s10551-010-0705-9

- Giroud, X., & Mueller, H. M. (2010). Does corporate governance matter in competitive industries? Journal of Financial Economics, 95(3), 312–331. doi:10.1016/j.jfineco.2009.10.008

- Koetter, M., Kolari, J. W., & Spierdijk, L. (2012). Enjoying the quiet life under deregulation? Evidence from adjusted Lerner indices for U.S. Banks. Review of Economics and Statistics, 94(2), 462–480. doi:10.1162/REST_a_00155

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3, (4), 305–360. doi:10.1016/0304-405X(76)90026-X

- Kim, E. H., Maug, E., & Schneider, C. (2018). Labor representation in governance as an insurance mechanism. Review of Finance, 22(4), 1251–1289. doi:10.1093/rof/rfy012

- La Porta, R., López-de-Silanes, F., & Shleifer, A. (1999). Corporate ownership around the World. The Journal of Finance, 2, 471–517. doi:10.1111/0022-1082.00115

- Liang, H., Renneboog, L., & Vansteenkiste, C. (2017). Cross-Border Acquisitions and Employee-Engagement (Finance Working Paper No. 496/2017). European Corporate Governance Institute (ECGI).

- Magill, M., Quinzii, M., & Rochet, J. C. (2015). A theory of the stakeholder corporation. Econometrica, 83(5), 1685–1725. doi:10.3982/ECTA11455

- Masulis, R. W., Wang, C., & Xie, F. (2018). Employee-manager alliances and shareholder returns from acquisitions. Journal of Financial and Quantitative Analysis. doi:10.1017/S0022109019000036

- Pagano, M., & Volpin, P. F. (2005). Managers, workers, and corporate control. The Journal of Finance, 60(2), 841–868. doi:10.1111/j.1540-6261.2005.00748.x

- Perotti, E. C., & Von Thadden, E. L. (2006). The political economy of corporate control and labor rents. Journal of Political Economy, 114(1), 145–175. doi:10.1086/500278

- Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. doi:10.2307/2329497

- Shleifer, A., & Summers, L. H. (1988). Breach of trust in hostile takeovers. In A. J. Auerbach (Ed.), Corporate takeovers: Causes and consequences (pp. 33–68). Chicago, IL: University of Chicago Press.

- Tirole, J. (2001). Corporate Governance. Econometrica, 69(1), 1–35. doi:10.1111/1468-0262.00177

- Yoshimori, M. (1995). Whose company is it? The concept of the corporation in Japan and the west. Long Range Planning, 28(4), 2–44. doi:10.1016/0024-6301(95)00025-E

Appendix

Proof of Lemma 1.

Part (a) of Lemma 1 is obtained by solving the following program:

The Lagrangian of this program taking into account that is

Hence, from FOC:

and

which in turn imply that CEP=R=U since λ = 1. Finally, profits are obtained by plugging the optimal contract in the objective function. Formally,

In a similar vein, part (b) of Lemma 1 is obtained by solving

The Lagrangian of this program taking into account that is

Hence, looking for FOC, we get that

and profits are obtained by plugging the optimal contract in the objective function,

Proof of Proposition 1.

It follows straightforward by comparing the level of profits obtained when the project is risky and when it is safe.

Proof of Proposition 2.

Before proving this proposition, let us analyse the properties of and

. It is easy to check that

is increasing and (strictly) convex with

, while

is increasing and linear with

. Finally, there exists only one

if exists such that

. This is so since

In order to prove this proposition, recall that in case of efficient decisions, it is efficient to choose risky if and safe if the opposite is true. Then if

part (a) is obtained directly since for all a,

, which in turn imply that if

the shareholder will choose safe while risky is efficient at least for some opportunity cost r.

Part (b) is obtained if since there exist only one

such that

. Parts b.1) and b.2) are obtained by noting that

is linear while

is convex and

.

Proof of Lemma 2.

Before proving this lemma, it is clear that the [PC] is binding since the fix part α is subtracting in the objective function and therefore the shareholder wants to make it as small as possible. Hence, part (a) of Lemma 2 is obtained by solving

And from FOC and K-T conditions we derive:

where μ is the K-T multiplier associated to the incentives constraints. Therefore if

, we get

and

⇔

which implies that it happens if

. Hence, if

, then

since μ > 0. This corresponds to part (a). Part (b) is obtained by solving the analogous program for project safe. Formally,

and from FOC and K-T conditions we derive:

Therefore if μ = 0, we get and

, which implies that it happens if

. Hence, if

, then

since μ > 0.

Proof of Proposition 3

From Proposition 1: if safe is preferred to risky. From Lemma 2: if

the optimal incentive is

which implies that profits cannot be larger than profits achieved with

. In other words,

if

and since

, it implies

. Therefore, this proves part (b). Similar to this, if

and

, the optimal decision is to implement safe by applying the same argument than part (b). This corresponds to part (a).

In order to prove part (c), note that, in order to implement risky, at the shareholder is indifferent between choosing

and

. Then since in

; it implies that at

. Similarly at

, since by definition, at

, but since

this implies

. Finally, to prove part (c) we only need to check that there exists such

. Note that for all a in this set,

and

which implies the existence of this function.

Proof of Corollary 1.

The proof is analogous to the proof of Proposition 2. The only difference arises in the region corresponding to Part (c) of Proposition 3. If risk is low and we may have improved choices since now P = S is selected more often. Otherwise, there is an increase in the inefficiency regarding selection of a project.