?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Exchange rate fluctuations play a vital role in influencing macroeconomic variables including economic growth via the channels of net exports and investments. This study claims to be the first in assessing the asymmetric effect of exchange rate fluctuations on G.D.P. in Pakistan whose currency had the title of ‘worst currency of South Asia’ in 2018 after more than 20% depreciation in just three months. In this study, we employ a recently developed technique of Non-linear A.R.D.L. by Shin, Yu, and Greenwood-Nimmo (Citation2014) to test for possible asymmetric effect of exchange rate on G.D.P. along with the proxies of fiscal and monetary policies. Both A.R.D.L. and N.A.R.D.L. are applied on annual data range from 1972 to 2014. The results of A.R.D.L. are found poor and co-integration relationship lost when the assumption of symmetry is taken into consideration. On the contrary, Non-linear A.R.D.L. technique carry more rich information related to the issue at hand and co-integration relationship is confirmed. From the results we found that week currency hurts G.D.P. growth, while strong currency adds to growth. Besides these, we confirm asymmetric impact of exchange rate on G.D.P. growth in Pakistan and find the evidence of short-run, long-run and adjustment asymmetry. To achieve the objective of sustained growth, exchange rate management should focus to restore stability and go for more strong currency in Pakistan. Future research needs to consider capital flows and exchange rate regimes in the form of ‘Sudden Stop hypothesis’ when investigating the asymmetric impact of exchange rate.

Keywords:

1. Background of the study

Exchange rate plays an important role in influencing the macroeconomic variables of a country. The adoption of the flexible exchange rate system across the world has caught the attention of researchers to investigate the impact of exchange rate on key macroeconomic aggregates including economic growth, balance of payments and inflation. A group of researchers is of the view that growth targets and other desirable macroeconomic objectives could only be achieved and maintained with the help of competitive exchange rate in a country. Evidence from advanced and emerging economies, especially the East Asian economies, substantiates the positive impact of competitive exchange rate on economic performance of these countries. However, the case may not be true for all countries and over a rapid changing world scenario due to variations in the level of technological advancement, human capital, corruption and money laundering and other structural differences among the countries.

Although, the effect of exchange rate on export and economic growth has been debated by many researchers, however existing empirical literature lacks consensus about the direction and magnitude of the possible impact. There are many ways in which exchange rate can influence domestic production and employment. One possible channel in this regards could be the export-led growth. It is claimed that a competitive exchange rate makes export cheaper and import dearer thereby correcting balance of payment deficit and boosts domestic processing and employment if the Marshall–Lerner condition is satisfied. However, this condition is not necessarily satisfied in every country due to rapid globalisation and vertically integrated industries. In addition, fluctuations in exchange rate may have important implications for foreign debt servicing and investments flow. Moreover, the exchange rate may deteriorate the balance of trade in the short-run and improve it only in the long-run; the so-called J-curve phenomenon.

Pakistan is one of the emerging economies in South Asia and its economy is heavily dependent on import of oil from the international market besides import of technology and inputs for domestic processing and consumption. The economy is confronted with persistent deficit in trade and the resulting low foreign exchange reserves. For almost a decade, Pakistan’s exports have remained stagnant at US$25 billion, while imports rose to US$50 billion, thereby putting immense pressure on external balance (Economic Survey of Pakistan, 2015–2016). Such a weak performance of the exporting sector in the country could be attributed to narrow exports basket: concentrated in textile, chemical and pharmaceutical, leather, rice and sports products. Besides this, the country is lacking in product and value addition diversification which makes exporting products less competitive and as a consequent exchange rate fluctuation seems to have little impact on export performance.

Like other developing countries, Pakistan has had an overvalued currency and significant changes have been observed in the exchange rate policy in recent years. Prior to March 2013, the prime objective of the policy was to stabilise the real effective exchange rate (R.E.E.R.) and was shifted to the stability of a nominal exchange rate against U.S. dollars post 2013 (Hamid & Mir, Citation2017). Another problem in the country is poor management of exchange rate and is often driven by individuals who do not have basic understanding of economics. Consequently, the exchange rate remains more or less transparent and sometimes subjected to arbitrary changes. Some studies (Hamid & Mir, Citation2017) claim the overvalued exchange rate and misalignment are the main causes of loss of competitiveness in the international market and declining growth in tradable sector during the last decade. Intuitively, the strategy of making the currency undervalued to get competitiveness in the international market may not work in correcting deficit in external account in Pakistan. In some cases, the shapes of demand and supply curves of foreign exchange may be such that a devaluation would worsen the deficit in trade rather than correcting it (Salvatore, Citation2014).

Looking at the trade composition of Pakistan, it is evident that the country exports primary and semi-finished goods with low price elasticity and imports both capital goods and crude oil. Furthermore, the advantage of making currency undervalued seems to be subjected to the inefficiency of the exporting sector in minimising cost. Similarly, the country is confronted with the twin problems of internal insurgency and a severe energy crisis during the last decade. The benefit of undervalued currency in the form of possible gain of competitiveness is offset by the inefficiency of exporting sector due to energy crises and insecurity. Moreover, the country is also dependent on foreign remittances for its favourable current account position and suffers from unsustainable external loans. In brief, Pakistan is confronted with macroeconomic trilemma: the desirable but contradictory macroeconomic objectives of exchange rate stabilisation along with easy monetary policy to achieve the desirable goals on the pace of free capital mobilisation. The dwindling foreign exchange reserves deviate the country to achieve these goals (Adil, Citation2018). Since the country strives for economic growth, therefore appropriate policy recommendation on exchange rate management is required.

Recently some empirical studies (Hamid & Mir, Citation2017; Javed & Farooq, Citation2009; Nawaz, Citation2012; Shahbaz, Islam, & Aamir, Citation2012) showed depreciation of Pakistani currency to be growth enhancing. The common feature of these studies is that they all have assumed symmetric effect of exchange rate on growth and therefore seem to miss important insights and unable to distinguish and isolate the impact of appreciation from depreciation on economic performance. Aside this the econometric methodologies applied by these studies led to the wrong notion of exchange rate appreciation to be contractionary. Some empirical studies (Bahmani-Oskooee & Fariditavana, Citation2016; Bahmani-Oskooee & Mohammadian, Citation2017; Bussiere, Citation2013; Delatte & Lopez-Villavicencio, Citation2012) provide evidence that the pass-through of exchange rate changes on inflation, trade balance and G.D.P. growth are asymmetric. These studies are done for emerging and developed countries and therefore the conclusion cannot be extended to the experience of a developing country like Pakistan. Moreover, since the correlation between exchange rate and macroeconomic variables are expected to be more pronounced in less developed and less open economies (Stavárek, Citation2013), therefore the current study is expected to bring forth some interesting insights on the issue at hand.

The present study is among the first that challenges this established notion and seeks to test for possible asymmetric effect of exchange rate on G.D.P. growth in a developing country like Pakistan. The study assumes the impact of appreciation of Pakistani currency on G.D.P. growth to be different from depreciation. The study employs a recently developed Non-Linear A.R.D.L. methodology by Shin et al. (Citation2014) to test for possible asymmetric impact of E.R. changes on G.D.P. in the context of a developing economy like Pakistan. In South Asia, Pakistani currency has remained more volatile as compared to their counterparts with the same level of development. To the best of our knowledge no study has investigated the asymmetric effect of E.R. on economic growth in Pakistan. This study would be the first in providing the analysis of asymmetric effect of E.R. changes on G.D.P. in Pakistan and is expected to add to the empirical literature on the issue for the best management of E.R. policy to achieve desirable goals.

2. Review of literature

In Financial and Monetary Economics one of the most debated and extensively investigated questions is the relationship between exchange rates and macroeconomic aggregates; including investments, money supply, balance of trade and output (Stavárek, Citation2013). However, Obstfeld and Rogoff (Citation2001) point out six major puzzles in the field of International Economics. Among these, the exchange rate disconnect puzzle is related to the missing relationship between exchange rates and macroeconomic variables. Economists have long pointed to the negative impact of a poorly managed exchange rate on growth of the economy (Rodrick, Citation2008). Countries around the world avoiding significant overvaluation of their currencies have boosted their economies and this exchange rate-growth relationship is supported by cross-country statistical evidence (Johnson, Ostry, & Subramanian, Citation2007; Kocenda, Maurel, & Schnabl, Citation2013; Rajan & Subramanian, Citation2006). Theoretically, the contractionary effect of devaluation on national output can be traced from Keynesian and Monetarist models. According to the Keynesian model, such contractionary impact is attributed to the initial deficit in trade, differences in propensities to consume from wages and profits and positive response of government revenue to devaluation. The monetarist model also shows a similar effect via a reduction in both nominal and real money balances.

In recent years, researchers are interested in estimating the asymmetric impact of E.R. on domestic processing and production in both developing and developed economies. In their study, Bahmani-Oskooee and Mohammadian (Citation2017) locate some studies on the relationship between devaluation and G.D.P. growth. Borrowing such references from their paper, we find studies for the panel of both developed and developing countries. For East European and O.E.C.D. countries, the studies include the work of Bahmani-Oskooee and Kutan (Citation2008) and Kalyoncu et al. (Citation2008) respectively. While for the panel of Asian countries the studies have been conducted by Bahmani-Oskooee et al. (Citation2002) and Kim and Ying (Citation2007); for Latin American economies by Mejía-Reyes et al. (Citation2010); and for Africa by Bahmani-Oskooee and Gelan (Citation2013). In the case of a single country, Bahmani-Oskooee and Rhee (Citation1997) cover Korea, while Narayan and Narayan (Citation2007) and Shahbaz et al. (Citation2012) cover Fiji and Pakistan in such analysis. Turkey and Palestine were studied by Sencicek and Upadhyaya (Citation2010) and Eltalla (2013).

The response of G.D.P. to E.R. stems from the Aggregate Demand (A.D.) and Aggregate Supply (A.S.) model. The impact of E.R. depreciation can be expansionary or contractionary depending on the responses of net exports. If the Marshall–Lerner condition is satisfied then devaluation will encourage net exports thereby increasing domestic processing. The J-curve further differentiates between the short-run and long-run impact of devaluation. According to J-curve effect, devaluation in the short-run will deteriorate balance of trade and in the long-run it will improve the situation and as a result A.D. will increase. On the other hand, costs of imported inputs will rise due to depreciation and A.S. will be affected. Devaluation will be expansionary if a rise in A.D. exceeds the fall in A.S. and is likely to be contractionary in the opposite situation (Bahmani-Oskooee & Mohammadian, Citation2017).

Since the pioneering work by Cooper (Citation1971) and Krugman and Taylor (Citation1978), the traditional channel through which a depreciation of currency boosts domestic production became ambiguous. These studies show how the demand- and supply-sides channels work; which results in net output loss due to depreciation. The prices of tradable products increase with currency devaluation that appear in a fall in the real balance of the economy and as a consequent lead to loss in output and growth. In the same vein, other studies that support the hypothesis of devaluation to be contractionary are conducted by Edwards (Citation1986) and Lizondo and Montiel (Citation1989). The mechanism behind this hypothesis induces from redistribution of income from wage class to entrepreneurs having excess savings. Consequently, total consumption falls, which results in falling A.D. and the resulting low output. While on the supply-side channel, depreciation increases cost of inputs and escorts to reduction in output (Krugman & Taylor, Citation1978). Agenor and Montiel (Citation1996) pinpoint the importance of wage indexation mechanism on the supply side and show that output falls due to fall in net benefits on the entrepreneur side.

In Pakistan, limited studies have been carried out on the impact of exchange rate on G.D.P. growth. Shahbaz et al. (Citation2012) examines the impact of devaluation on growth for Pakistan. Applying A.R.D.L., the study affirms the co-integration relationship between real G.D.P. and a set of explanatory variables including R.E.E.R., supply of money, government expenditures, and foreign remittances over a period of 1975 to 2008. The study found contractionary effect of devaluation on growth. The study however, assumed symmetric effect of E.R. on economic growth by applying linear A.R.D.L. Similarly in another study, Javed and Farooq (Citation2009) also examine the impact of E.R. on growth in Pakistan. Employing A.R.D.L. over a quarterly data range from 1982-I to 2007-IV, the study finds the influence of exchange rate on G.D.P. to be contractionary.

Other studies that attempted to estimate macroeconomic effects of exchange rate have been conducted by Mahmood, Ehsanullah, and Ahmed (Citation2011) and Khan, Sattar, and Ur Rehman (Citation2012). Mahmood et al. (Citation2011) in their study estimate the effect of exchange rate fluctuations on G.D.P., F.D.I., growth rate and openness using O.L.S. They applied G.A.R.C.H. model to compute volatility of exchange rate. The study shows positive impact of exchange rate fluctuation on G.D.P., growth rate and openness. However, the impact of exchange rate on F.D.I. was found to be negative. In the same streak, another study by Ahmad, Ahmad, and Ali (Citation2013) also applied O.L.S. to discover the negative effect of exchange rate and inflation on G.D.P. growth. These studies suffer from applying the incorrect O.L.S. methodology on non-stationary time series data. Khan, Sattar, and Ur Rehman (Citation2012) analyse the impact of exchange rate on inflation, F.D.I., trade and G.D.P. in Pakistan. Applying Johansen’s co-integration model over annual data range from 1980 to 2009, the study claims long-run relationship of exchange rate with trade, F.D.I. and G.D.P. but affirms no such relationship with inflation. The authors also pointed out that no causality between exchange rate and G.D.P. Johansen’s co-integration techniques, when employed over a small sample size, are reliable as compared to A.R.D.L. (Narayan, Citation2005). Moreover, the study assumes symmetric impact of E.R. changes on each dependent variable including G.D.P. In case of German economy, the study of Anker and Bahmani-Oskooee (Citation2001) using Johansen Co integration technique affirms that currency deprecation has expansionary effect on domestic production. However, in some countries like Iran, massive depreciation of the currency often leads to stagflation (Bahmani-Oskooee, Citation1996).

Similarly, Aman et al. (Citation2017) use simultaneous equation models, 2S.L.S. and 3S.L.S. over annual data from 1976 to 2010 and find exchange rate to be expansionary. The study claims this positive effect through channels of exports, investment and F.D.I. growth. On the contrary, Nawaz (Citation2012) in his study affirms contractionary effect of exchange rate in the long-run and claims it to be expansionary in the short run only. The study applied A.R.D.L. and error correction model over a span of data range from 1972 to 2010. The conclusions derived by these studies seem to be misleading in policy formulation regarding sound and effective management of exchange rate in the country based on the methodologies used. In case of Turkey, Katircioglu and Feridun (Citation2011) applied A.R.D.L. in order to investigate the effect of macroeconomic variables on exchange market pressure. The study finds a level relationship between the dependent and the set of explanatory variables. The common limitation of this study like other studies conducted by Khan et al. (Citation2012), Nawaz (Citation2012), Ahmad et al. (Citation2013), and Aman et al. (Citation2017) in case of Pakistan is that all assumed symmetric relationship between E.R. and macroeconomic aggregates.

Since the mid-90s, a substantial literature has considered the joint issues of non-stationarity and nonlinearity. In this regard, the field has been dominated by three regime-switching models. The first one is associated with Balke and Fomby’s (Citation1997) threshold E.C.M.; the second is presented by Psaradakis, Sola, and Spagnolo (Citation2004) called the Markov-Switching E.C.M.; and the third one is the smooth transition regression E.C.M. by Kapetanios, Shin, and Snell (Citation2006). This literature points out that linear models are incapable of carrying sufficient information which permits drawing reliable forecasts for the future. In other words, it implies a general concern that assuming a linear adjustment may be too restrictive in a wide range of economically interesting possibilities, particularly where transaction costs cannot be ignored and where policy interventions are observed in-sample (Shin et al., Citation2014). Another plausible explanation for the asymmetric behaviour of many economic phenomena stems from the business cycle asymmetry hypothesis and can be traced to the early decades of the twentieth century, and to the pioneering work of Mitchell (Citation1927) and Keynes (1936).

Razin and Collins (Citation1999) in their study developed a fundamental-based index for real exchange rate overvaluation for 93 developed and developing economies over a data span from 1975 to 1993. They find the index to be inversely correlated with growth. The study further indicates asymmetries in the effect of undervaluation as compared to overvaluation. However, this study also suffers from the non-application of dynamic econometric model and it simply relied on the correlation of the constructed index for real exchange rate with growth. But the insights of the study provided the basis for the investigation of asymmetric effect of exchange rate on growth which is more realistic. Other studies which find undervaluation to be growth-enhancing include Rodrick (Citation2008); Rapetti, Skott, and Razmi (Citation2012) in a panel of developed and developing countries. But the study by Rapetti et al. (Citation2012) indicates a non-monotonic relationship between real exchange rate and G.D.P. and is limited to developing and advanced countries. The study invites for closer analysis to solve the puzzle.

In recent past some studies have successfully applied a more flexible econometric technique in the form of N.A.R.D.L. for many macroeconomic relationships. This method is more flexible in estimating the dynamic asymmetric relationship between two variables which is the characteristic of many social phenomena including economic variables. In a recent study, Bahmani-Oskooee and Mohammadian (Citation2017) investigated and confirmed the asymmetric effect of exchange rate on output in Japan by applying Shin et al. (Citation2014) N.A.R.D.L. technique. The study also observes both long-run and short-run asymmetry. Besides this, many researchers have successfully applied N.A.R.D.L. to capture the phenomena of asymmetry (see for instance, Katrakilidis & Trachanas, Citation2012; Bahmani-Oskooee & Bahmani, Citation2015; Bahmani-Oskooee & Fariditavana, Citation2016; Bahmani-Oskooee & Mohammadian, Citation2017; Nusair, Citation2017; Bahmani-Oskooee, Halicioglu, & Neumann, Citation2018; Shin, Baek, & Heo, Citation2018).

3. Materials and methods

To trace both the short-run and long-run effect of the exchange rate on economic growth, we follow a model which has only a flavor of A.D. The general form of the model is outlined as follows:

(1)

(1)

Where, R.G.D.P. is real G.D.P. in Pakistan, R.E.E.R. is real effective exchange rate and rise in it reflects depreciation of the home currency, B.M. is broad money as a measure of monetary policy and G.E.X. is government total expenditure to represent fiscal policy (see Appendix 1 for variables definition, measurement and data source). Descriptive statistics are given in Appendix 2 and each individual variable is normality distributed at 5% significance levels on the basis of Jarque-Bera test statistic.

As opposed to the model of A.D.–A.S. adopted by Bahmani-Oskooee and Mohammadian (Citation2017) in their analysis, this study focuses on A.D. only. The reason for focusing on the A.D. side is that the inclusion of variables to represent A.S. will reduce the degree of freedom for a sample of smaller sizes in a dynamic model. Since, we have a problem of data over a longer span on the variables of our interest in the case of Pakistan; variables representing the A.S. are therefore not considered. Besides this, to avoid the problem of multicollinearity among the explanatory variables and the complex inter-connections between the forces of A.D. and A.S., the current study focuses on the channel of A.D. only. The E.C.M. of Linear A.R.D.L. of Equation 1 is as under:

(2)

(2)

The explanatory variables including R.E.E.R. in EquationEquation 2(2)

(2) are assumed to have symmetric effect on dependent variable. The symmetric impact of the variable of our interest that is R.E.E.R. means that if X% depreciation influences G.D.P. by Y%, then X% appreciation impacts G.D.P. by the same Y% in the opposite direction. Many economic phenomena often do not follow such symmetric relationship. The influence of exchange rate changes on G.D.P. stem from the response of net exports on the A.D. side (Bahmani-Oskooee & Mohammadian, Citation2017). The effect of depreciation on G.D.P. differs from appreciation due to changes in traders’ expectations (Bahmani-Oskooee & Fariditavana, Citation2016). Another plausible explanation of asymmetric impact of exchange rate changes is put forward by Bussiere (Citation2013). Bussiere associates such asymmetric influence to price rigidities of exports and imports and lag structure that is why the responses of traders to exchange rate depreciation differ from appreciation. In this article, we expect such asymmetric influence of E.R. changes on domestic output and processing in Pakistan.

To estimate and test whether E.R. has symmetric or asymmetric effect on G.D.P., Shin et al. (Citation2014)’s N.A.R.D.L. methodology is employed. To proceed further, first changes in R.E.E.R. are constructed which would include positive changes denoted by and negative changes denoted by

. After this, two new time series variable are developed, the one represents devaluation denoted by POSt and the other represents revaluation denoted by NEGt as partial sum of positive and negatives changes respectively.

(3)

(3)

(4)

(4)

Following, Shin et al. (Citation2014), of EquationEquation 2

(2)

(2) will be substituted by POSt and NEGt as below:

(5)

(5)

The E.C.M. of N.A.R.D.L. can be estimated by O.L.S. and Pesaran, Shin, and Smith (Citation2001)’s bound testing procedure is equally applicable to it and is form of N.A.R.D.L. as against the linear A.R.D.L. (Shin et al., Citation2014). Besides these, this approach is simple and flexible in testing reaction, impact and adjustment asymmetry (Bahmani-Oskooee & Fariditavana, Citation2016). Once the test indicated co-integration relationship, then both the short-run and long-run asymmetry can be tested accordingly. Also, this short-run impact asymmetry is testable via this technique. These hypotheses to be tested are framed as under:

Short-run adjustment asymmetry from EquationEquation 5(5)

(5) can be established if the number of lags associated with the variable of ΔPOSt-i is not equal to that of ΔNEGt-i and can only be determined by observation, while the size effect can be inferred if

differs from

for a given value of ‘i’ (Bahmani-Oskooee et al., Citation2018). Similarly, if the null hypothesis is rejected via the Wald-Test and long-run asymmetry can be evidenced in case the Wald-Test rejects the null hypothesis associated with the normalised coefficients ( displays hypotheses formulation). Since, N.A.R.D.L. model incorporates one extra explanatory variable as compared to L.A.R.D.L. Shin et al. (Citation2014) therefore recommend to treat both POSt and NEGt variables as one.

Table 1. The null and alternate hypotheses for short-run, short-run impact and long-run asymmetry.

4. Empirical analysis

Before estimating EquationEquation 2(2)

(2) and EquationEquation 5

(5)

(5) , we check for stationarity of the variables via Dickey-Fuller Generalized Least Square (D.F.-G.L.S.) and Philips–Perron tests in order to be sure that none of the variable is integrated of order 2 in which case the bound testing procedure beaks down (Pesaran et al., Citation2001). We applied D.F.-G.L.S. test instead of the conventional A.D.F. test, as the latter may be unreliable in case of small sample data is as the case of this study (DeJong et al., Citation1992; Harris, Citation1992, Citation2009) and is an improvement of the A.D.F. test (Elliot, Rothenberg, & Stock, Citation1996). From Philips–Perron tests given in , all the variables of our interest are integrated of order 1 at 1% level of significance in both cases of ‘with drift’ and ‘with drift & trend’ and none of them is I(2). It is obvious that most macroeconomic variables have the properties of being stationary at level {I(0)} or at maximum become stationary at first difference {I(1)}. Therefore the A.R.D.L. approach does not normally need pre-testing for the unit root. Furthermore, this method takes sufficient lags of the variables which serve as an instrument for the removal of the endogeneity problem (Bahmani-Oskooee & Hajilee, Citation2010). Pesaran et al. (Citation2001) describe this instrument as ‘our approach is quiet general in the sense that we can use a flexible choice for the dynamic lag structure in … as well as allowing for short-run feedbacks’.

Table 2. Unit root test based on Dickey–Fuller G.L.S. (E.R.S.) and Philips–Perron (P.P.).

However, D.F.-G.L.S.-test shows a bit different conclusion. From the test results, all variables become stationary at first difference in case of ‘with drift’ and only one variable that is broad money (lnBM) becomes stationary at 5% probability level. Since, the conventional A.R.D.L. (Pesaran et al., Citation2001) and N.A.R.D.L. (Shin et al., Citation2014) do not require pre-testing the stationarity of the variables, the overall conclusion does not change. After checking for stationarity, we estimate the model of linear A.R.D.L. of EquationEquation 2(2)

(2) along with important diagnostic checking. The bound test result is reported in , which indicates the existence of a long-run relationship.

Table 3. Linear-A.R.D.L. bound test.

The F-test value is 5.733 which lie above upper bound critical value at 5% level of significance. However, for the existence of co-integration relationship, the coefficient of E.C.M. term should be statistically significant. Moreover, it should lie between −1 and 0 in order to check and test the speed of adjustment back to equilibrium after a shock occurs (Banerjee, Dolado, & Mestre, Citation1998). The E.C.M. term reported in is statistically insignificant indicating no equilibrium long-run relationship between dependent and explanatory variables. Such contradictory signals of the L.A.R.D.L. appeal for and justify the application of N.A.R.D.L.

Table 4. Estimates of E.C.M. of linear-A.R.D.L.

From the long-run estimates reported in , the coefficient of R.E.E.R. is insignificant. Such statistically insignificant impact may be due to the assumption of symmetric effect of devaluation and appreciation in linear A.R.D.L.

Table 5. Long-run estimates of linear-A.R.D.L. model.

The diagnostic tests like tests of Normality, Serial Correlation, Heteroskedasticity and Specification of L.A.R.D.L. model are reported in Appendix 3. Despite the fact that we find no evidence of non-normality, autocorrelation, heteroscedasticity and misspecification from the diagnostic checking, but all in all the estimates of L.A.R.D.L. do not stand with the expectations of dynamic A.R.D.L. The long-run coefficient associated with exchange rate (L.R.E.E.R.) is positive but statistically insignificant and plausibly results from the assumption of symmetric influence. The poor results of the L.A.R.D.L. model necessitated the estimation of N.A.R.D.L. and both the short- and long-run results are therefore estimated. But before estimating the short- and long-run dynamics, we have to compute F-Statistics (Wald-Test) in order to be sure that co-integration relationship exits.

The F-Stat of bound test of N.A.R.D.L. reported in is 7.102. This calculated value exceeds than the upper bound critical value of 5.72 at 1% level of significance thereby indicating co-integration relationship. Moreover, the E.C.M. term represented by CointEq(-1) in is −0.7428 is not only statistically significant at 1% probability level, but also lies between −1 and 0. This implies that the speed of adjustment towards equilibrium is 74.28% per annum when a shock occurs.

Table 6. N.A.R.D.L. bound test result.

Table 7. Estimates of E.C.M. of N.A.R.D.L. model.

Table 8. Long-run estimates of N.A.R.D.L. model.

Table 9. Test for short-run, short-run impact and long-run asymmetry.

Pesaran et al. (Citation2001) focus on significant F-Statistic and while Banerjee et al. (Citation1998) prefers the significance of E.C.M. term along with the value lies between -1 and zero for the confirmation of long-run equilibrium relationship. Both these criteria have been satisfied by N.A.R.D.L. version. The long-run coefficients of N.A.R.D.L. model reported in are all statistically significant.

From the results it is evident that devaluation negatively affects G.D.P. and revaluation impacts it positively in Pakistan. Such a negative impact can be associated with persistent deficit in trade and such contractionary effect is argued by Bahmani-Oskooee and Mohammadian (Citation2017) in their study. In the context of Pakistan, our results of N.A.R.D.L. confirm the findings of Shahbaz et al. (Citation2012) and Nawaz (2012) who conducted study for Pakistan but in their study they assumed symmetric impact of exchange rate changes. Both these studies applied A.R.D.L. in their analysis and Nawaz (2012) reported devaluation to be contractionary in the long-run, while expansionary in the short run.

Our results however are not in conformity with findings of Mahmood et al. (Citation2011) and Aman et al. (Citation2017) who did not apply co-integration techniques in their analyses. O.L.S. and G.A.R.C.H. models used by Mahmood et al. (Citation2011) in their study are not the relevant methodologies when the variables are non-stationary at levels. Similarly, the use of simultaneous equation models, 2S.L.S. and 3S.L.S. in the study by Aman et al. (Citation2017) also suffer from applying poor methodology. A.R.D.L. methodology in general and N.A.R.D.L. in particular is flexible in that both the short-run and long-run symmetric (asymmetric) relationship can be estimated and tested which other competing methodologies lack.

From the long-run results it is clear that a 1% devaluation is likely to reduce G.D.P. by 1.66% on average. But contrary to devaluation, revaluation is expected to increase G.D.P. by 5.84% on average in the long-run. From the tests of asymmetry, we find short-run, log-run and adjustment asymmetric impact of exchange rate changes over G.D.P. in Pakistan ().

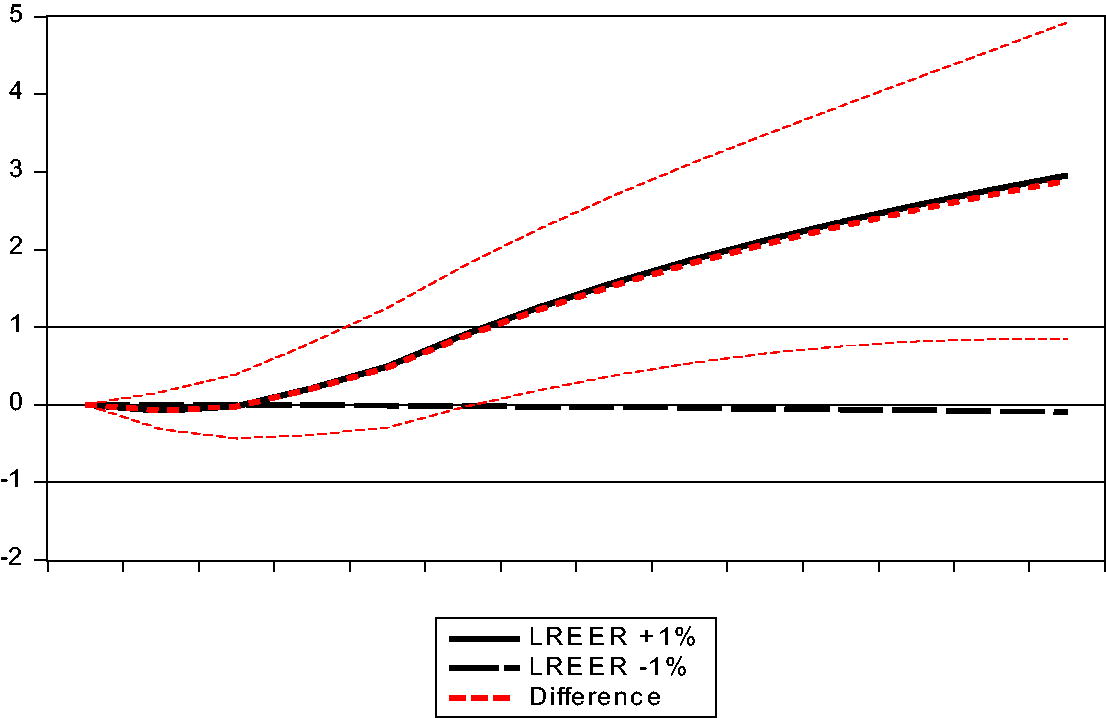

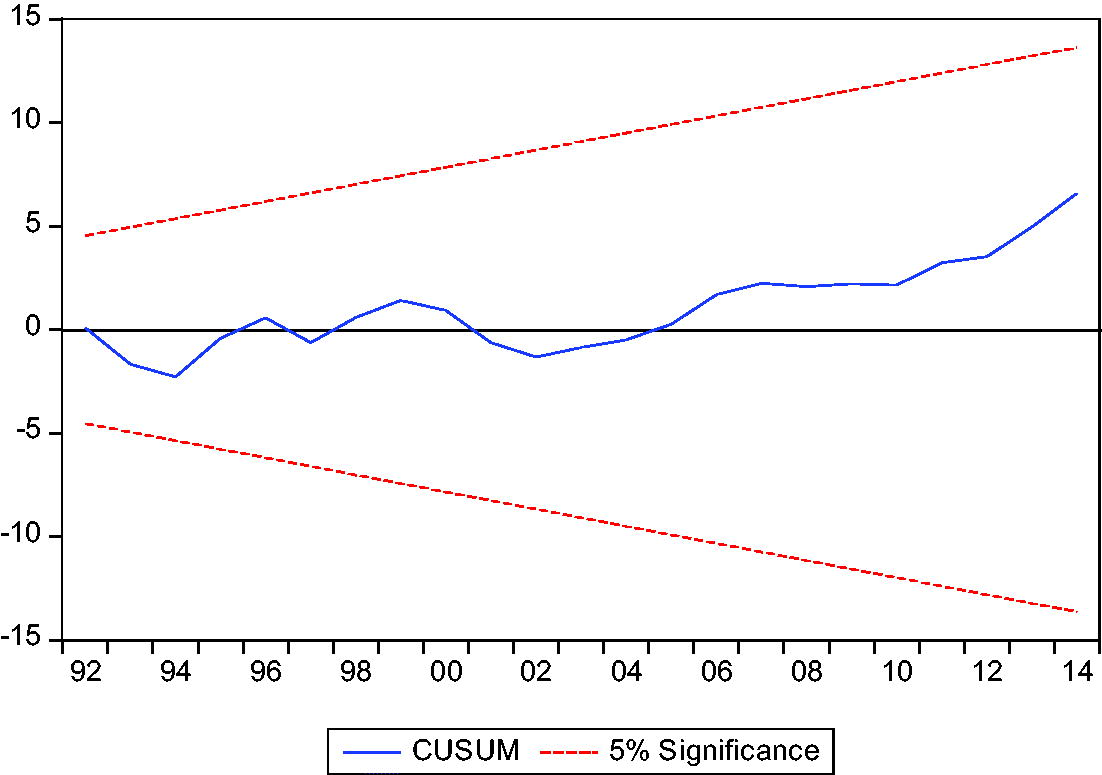

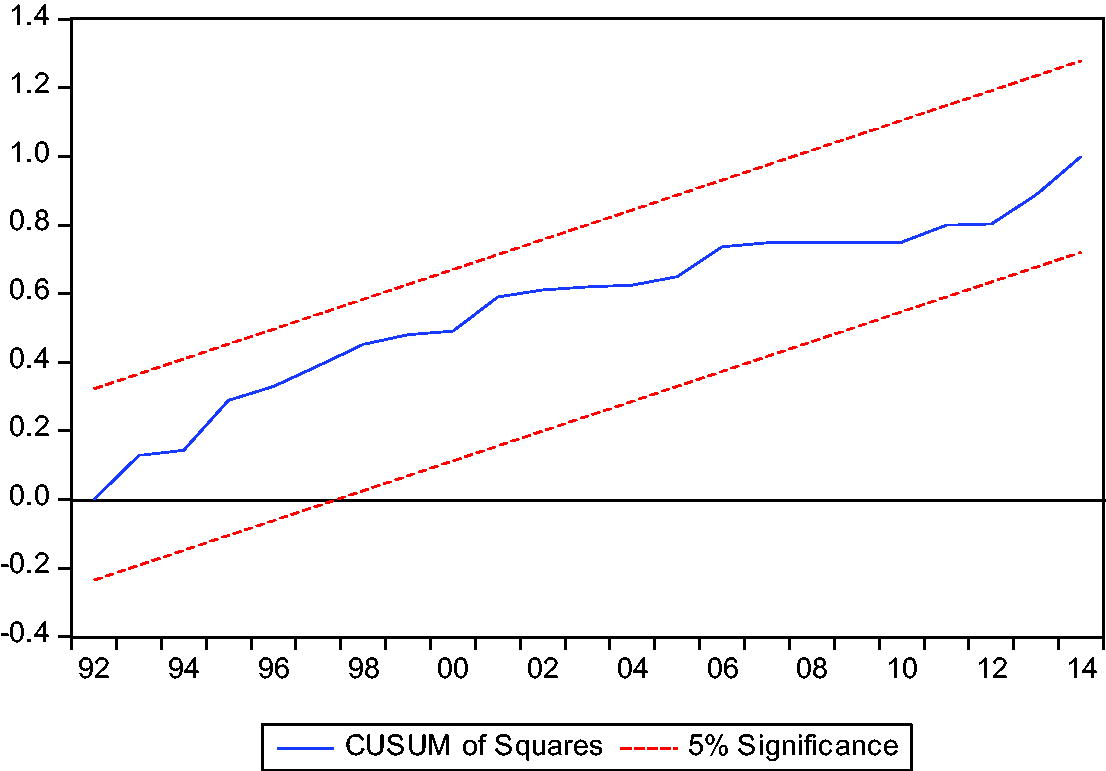

Diagnostic checking for the N.A.R.D.L. is presented in Appendix 4. Again, the traditional assumptions of the dynamic model are tested and we find no evidence of non-normality, serial correlation, heteroscedasticity and miss-specification. Aside this, the co-integration graph of N.A.R.D.L. shown in Appendix 5 indicates the existence of the asymmetric long-run relationship between G.D.P. growth and exchange rate. Similarly, a parameters stability test is done via C.U.S.U.M. and square of C.U.S.U.M. and reported in Appendix 6, which also confirm that parameters of N.A.R.D.L. are stable over gradual/multiple structural changes, missing predictors and neglected non-linearity. To draw further inferences, Vector Error Correction (V.E.C.) Granger causality also known as block exogeniety Wald test is conducted under both L.A.R.D.L. and N.A.R.D.L. approaches. The summary of the test under N.A.R.D.L. is presented in , while that of L.A.R.D.L. is reported in Appendix 7. The result under L.A.R.D.L. shows no causality between L.R.G.D.P. and L.R.E.E.R., while under the N.A.R.D.L. both positive (L.R.E.E.R._P.O.S.) and negative (L.R.E.E.R._N.E.G.) multipliers have unidirectional causality running to the L.R.G.D.P.

Table 10. V.E.C. Granger causality Wald tests (summary) under N.A.R.D.L.

5. Conclusions and policy recommendations

Exchange rate fluctuations play a vital role in influencing macroeconomic variables including economic growth via the channels of net exports and investments. This study claims to be among the firsts in assessing the asymmetric effect of E.R. changes on G.D.P. in a developing country like Pakistan whose currency has got the title of ‘worst currency of South Asia’ in 2018 after more than 20% depreciation over the last seven months. The Pakistani rupee which was Rs.110 per US$ in April 2018 started its depreciation and in the last week of July 2018 has fallen to Rs. 142 per US$ in just seven months. Such changes seem to have some serious macroeconomic consequences for the country. The possible reasons for such fluctuations may be associated with election cycle of 2018 and heavy trade deficit of $30 billion along with budget deficit of approximately $12 billion on the pace of political uncertainty. However, in the current study, our objective is to estimate the asymmetric impact of E.R. changes on G.D.P. in a developing country like Pakistan.

The objective of this endeavour is two pronged: firstly to investigate the asymmetric effect of E.R. appreciation and depreciation and secondly to apply more flexible and dynamic model of Shin et al. (Citation2014) to test for short- and long-run asymmetry. The study is inspired by and adopts the theoretical approach of A.D.-A.S. by Bahmani-Oskooee and Mohammadian (Citation2017) with focusing on A.D. side only. The reason of focusing on A.D. side is that the inclusion of variables to represent A.S. will reduce degree of freedom for a sample of small size in a dynamic model as in the present case. Since, we have a problem of data over a longer span on the variables of our interest in case of Pakistan; variables representing the A.S. therefore are not considered. Besides this, to avoid the problem of multicollinearity among the explanatory variables and the complex inter-connections between the forces of A.D. and A.S., the current study is focusing on the channel of A.D. only. For this purpose, we employed a recent developed technique of N.A.R.D.L. by Shin et al. (Citation2014) to test for possible non-linear relationship between G.D.P. and exchange rate along with the proxies of fiscal and monetary policies. Both A.R.D.L. and N.A.R.D.L. are applied on annual data range from 1972 to 2014. The results of linear A.R.D.L. are found poor, while that of Non-linear A.R.D.L. are found significant and carry more rich information related to the issue. From the results we found that weak currency hurts G.D.P. growth, while strong currency adds to growth. Besides these, we confirm asymmetric effect of E.R. on G.D.P. in Pakistan and found the evidence of short-run, Short-run impact and long-run asymmetry. The results are further supported with V.E.C. Granger causality test which only show asymmetric unidirectional causality running from E.R. to G.D.P. growth under N.A.R.D.L. approach. To achieve the objective of sustained growth and the ultimate objective of sustainable development, exchange rate management should focus to restore stability and go for more strong currency. However, future research needs to take into consideration the supply side variable(s) over longer data and test the ‘Sudden-Stop Hypothesis’.

References

- Adil, F. (2018, April 9). Asymmetric monetary policy response. Published in Dawn, The Business and Finance Weekly. Retrieved from https://www.dawn.com/news/1400467.

- Agenor, P. R., & Montiel, P. (1996). Development macroeconomics. New Jersey: Princeton University Press.

- Ahmad, A., Ahmad, N., & Ali, S. (2013). Exchange rate and economic growth in Pakistan (1975-2011). Journal of Basic Applied Science Research, 3(8), 740–746.

- Aman, Q., Ullah, I., Khan, M. I., & Khan, S-U-D. (2017). Linkages between exchange rate and economic growth in Pakistan (an econometric approach). European Journal of Law and Economics, 44(1), 157–164.

- Anker, P., & Bahmani-Oskooee, M. (2001). On the relationship between the value of the mark and German production. Applied Economics, 33(12), 1525–1530.

- Bahmani-Oskooee, M. (1996). Source of stagflation in an oil-producing country: Evidence from Iran. Journal of Post Keynesian Economics, 18(4), 609–620.

- Bahmani-Oskooee, M., & Bahmani, S. (2015). Nonlinear ARDL approach and the demand for money in Iran. Economics Bulletin, 35(1), 381–391.

- Bahmani-Oskooee, M., Chomsisengphet, S., & Kandil, M. (2002). Are devaluations contractionary in Asia? Journal of Post Keynesian Economics, 25(1), 69–82.

- Bahmani-Oskooee, M., & Fariditavana, H. (2016). Nonlinear ARDL approach and the J-curve phenomenon. Open Economies Review, 27(1), 51–70.

- Bahmani-Oskooee, M., & Gelan, A. (2013). Are devaluations contractionary in Africa? Global Economic Review, 42(1), 1–14.

- Bahmani-Oskooee, M., & Hajilee, A. (2010). On the relation between currency depreciation and domestic investment. Journal of Post Keynesian Economics, 32(4), 645–660.

- Bahmani-Oskooee, M., Halicioglu, F., & Neumann, R. (2018). Domestic investment responses to changes in the real exchange rate: Asymmetries of appreciation versus depreciation. International Journal of Finance and Economics, 23(4), 362–375.

- Bahmani-Oskooee, M., & Kandil, M. (2009). Are devaluations contractionary in MENA countries? Applied Economics, 41(2), 139–150.

- Bahmani-Oskooee, M., & Kutan, A. M. (2008). Are devaluations contractionary in emerging economies of Eastern Europe? Economic Change and Restructuring, 41(1), 61–74.

- Bahmani-Oskooee, M., & Mohammadian, A. (2017). Asymmetry effects of exchange rate changes on domestic production in Japan. International Review of Applied Economics, 31(6), 774–790..

- Bahmani-Oskooee, M., & Rhee, H. J. (1997). Response of domestic production to depreciation in korea: An application of Johansen's cointegration methodology. International Economic Journal, 11(4), 103–112.

- Balke, N. S., & Fomby, T. B. (1997). Threshold cointegration. International Economic Review, 38, 627–645. doi: 10.2307/2527284

- Banerjee, A., Dolado, J., & Mestre, R. (1998). Error‐correction mechanism tests for cointegration in a single‐equation framework. Journal of Time Series Analysis, 19(3), 267–283.

- Bussiere, M. (2013). Exchange rate pass‐through to trade prices: The role of nonlinearities and asymmetries. Oxford Bulletin of Economics and Statistics, 75(5), 731–758.

- Cooper, R. N. (1971). Currency devaluation in developing countries. Essay in international finance, No. 86. New Jersey: International Finance Section, Princeton University.

- DeJong, D. N., Nankervis, J. C., Savin, N. E., & Whiteman, C. H. (1992). Integration versus trend stationarity in time series. Econometrica, 60(2), 423–433.

- Delatte, A., & Lopez-Villavicencio, A. (2012). Asymmetry exchange rate pass-through: Evidence from major countries. Journal of Macroeconomics, 34(3), 833–844.

- Edwards, S. (1986). Are devaluation contractionary? The Review of Economic and Statistics, 68(3), 501–508.

- Elliot, G., Rothenberg, T. J., & Stock, J. H. (1996). Efficient tests for an autoregressive unit root. Econometrica, 64(4), 813–836.

- Eltalla, A. H. A. (2013). Devaluation and output growth in Palestine: Evidence from a CGE model. European Journal of Business and Economics, 8(4), 26–31.

- Government of Pakistan, Ministry of Finance. (2015–2016). Economic survey of Pakistan (2015-16). Islamabad: Ministry of Finance.

- Hamid, N., & Mir, A. S. (2017). Exchange rate management and economic growth: A brewing crisis in Pakistan. Lahore Journal of Economics, 22(Special Edition), 73–110.

- Harris, R. I. D. (2009). Small sample testing for unit roots. Oxford Bulletin of Economics and Statistics, Department of Economics, University of Oxford, 54(4), 615–625.

- Harris, R. I. D. (1992). Testing for unit roots using the augmented Dickey-Fuller test: Some issues relating to the size, power and the lag structure of the test. Economics Letters, 38(4), 381–386. doi: 10.1016/0165-1765(92)90022-Q

- Javed, Z. H., & Farooq, M. (2009). Economic growth and exchange rate volatility in case of Pakistan. Pakistan Journal of Life and Social Sciences, 7(2), 112–118.

- Johnson, S., Ostry, J., & Subramanian, A. (2007). The prospects for sustained growth in Africa: Benchmarking the constraints. IMF Working Paper 07/52. Washington: International Monetary Fund (March).

- Kalyoncu, H., Artan, S., Tezekici, S., & Ozturk, I. (2008). Currency devaluation and output growth: An empirical evidence from OECD countries. International Research Journal of Finance and Economics, 14(2), 232–238.

- Kapetanios, G., Shin, Y., & Snell, A. (2006). Testing for cointegration in nonlinear smooth transition error correction models. Econometric Theory, 22(02), 279–303.

- Katircioglu, S. T., & Feridun, M. (2011). Do macroeconomic fundamentals affect exchange market pressure? Evidence from bounds testing approach for Turkey. Applied Economics Letters, 18(3), 295–300. doi: 10.1080/00036841003636110

- Katrakilidis, C., & Trachanas, E. (2012). What drives housing price dynamics in Greece: New evidence from asymmetric ARDL cointegration. Economic Modelling, 29(4), 1064–1069.

- Keynes, J. (1936). The general theory of employment, interest and money. London: Macmillan.

- Khan, R. E. A., Sattar, R., & Ur Rehman, H. (2012). Effectiveness of exchange rate in Pakistan: Causality analysis. Pakistan Journal of Commerce and Social Sciences, 6(1), 83–96.

- Kim, Y., & Ying, Y. H. (2007). An empirical assessment of currency devaluation in East Asian countries. Journal of International Money and Finance, 26(2), 265–283.

- Kocenda, E., Maurel, M., & Schnabl, G. (2013). Short- and long-term growth effects of exchange rate adjustment. Review of International Economics, 21(1), 137–150. doi: 10.1111/roie.12025

- Krugman, P., & Taylor, L. (1978). Contractionary effects of devaluation. Journal of International Economics, 8(3), 445–456.

- Lizondo, S. J., & Montiel, P. J. (1989). Contractionary devaluation in developing countries: An analytical overview. IMF Staff Papers, 36, 182–227.

- Mahmood, I., Ehsanullah, M., & Ahmed, H. (2011). Exchange rate volatility & macroeconomic variables in Pakistan. Business Management Dynamics, 1(2), 11–22.

- Mejía-Reyes, P., Osborn, D. R., & Sensier, M. (2010). Modelling real exchange rate effects on output performance in Latin America. Applied Economics, 42(19), 2491–2503.

- Mitchell, W. (1927). Business cycles. The problem and its setting. New York: National Bureau of Economic Research.

- Narayan, P. K. (2005). The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990.

- Narayan, P. K., & Narayan, S. (2007). Is devaluation expansionary or contractionary? Empirical evidence from Fiji. Applied Economics, 39(20), 2589–2598.

- Nawaz, M. (2012). The impact of exchange rate on output level: Bounds testing approach for Pakistan. The Pakistan Development Review, 51(4II), 419–433.

- Nusair, S. A. (2017). The J-curve phenomenon in European transition economies: A nonlinear ARDL approach. International Review of Applied Economics, 31(1), 1–27.

- Obstfeld, M., & Rogoff, K. S. (2001). The six major puzzles in international economics: Is there a common cause?. In NBER macroeconomics annual 2000, edited by B. S. Bernanke and K. S. Rogoff, 339–412. Cambridge, MA: MIT Press.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326.

- Psaradakis, Z., Sola, M., & Spagnolo, F. (2004). On Markov error‐correction models, with an application to stock prices and dividends. Journal of Applied Econometrics, 19(1), 69–88.

- Rajan, R. G., & Subramanian, A. (2006). Aid, Dutch disease, and manufacturing growth. Washington: Peterson, Institute for International Economics.

- Rapetti, M., Skott, P., & Razmi, A. (2012). The real exchange rate and economic growth: Are developing countries different? International Review of Applied Economics, 26(6), 735–753. doi: 10.1080/02692171.2012.686483

- Razin, O., & Collins, S. M. (1999). Real exchange rate misalignments and growth. In The economics of globalization: Policy perspectives from public economics, edited by A. Razin and E. Sadka, 59–83. Cambridge: Cambridge University Press.

- Rodrick, D. (2008). The real exchange rate and economic growth. Brookings Papers on Economic Activity, 2008(2), 365–412.

- Salvatore, D. (2014). International economics: Trade and finance. New Jersey: Wiley.

- Sencicek, M., & Upadhyaya, K. P. (2010). Are devaluations contractionary? The case of Turkey. Applied Economics, 42(9), 1077–1083.

- Shahbaz, M., Islam, F., & Aamir, N. (2012). Is devaluation contractionary? Empirical evidence for Pakistan. Economic Change and Restructuring, 45(4), 299–316.

- Shin, C., Baek, J., & Heo, E. (2018). Do oil price changes have symmetric or asymmetric effects on Korea’s demand for imported crude oil? Energy Sources, Part B: Economics, Planning, and Policy, 13(1), 6–12.

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt (pp. 281–314). New York, NY: Springer.

- Stavárek, D. (2013). Cyclical relationship between exchange rates and macro-fundamentals in Central and Eastern Europe. Economic Research-Ekonomska Istraživanja, 26(2), 83–98. doi: 10.1080/1331677X.2013.11517608

Appendices

Appendix 1: Variables definitions, measurement and data source

Appendix 2: Descriptive statistics

Appendix 3: Diagnostic checking for L.A.R.D.L model based on A.I.C.

Appendix 4: Diagnostic checking for N.A.R.D.L. model based on A.I.C.

Appendix 5: N.A.R.D.L. co-integrating graph

Appendix 6: N.A.R.D.L. tests of C.U.S.U.M. and C.U.S.U.M. of square

Appendix 7: V.E.C. Granger causality Wald tests (summary) under L.A.R.D.L.