?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the association between remittances inflow and investment. The data of five major South Asian countries that receive a significant portion of remittances including India, Sri Lanka, Pakistan, Nepal, and Bangladesh are considered from 1990 to 2016. Pooled ordinary least square (OLS), the fixed effect within group estimator (FEWGE), fixed effect (FE) and random effect (RE) are used for the analysis of the data. Unit root tests were employed and then followed by a pooled mean group (PMG) analysis to analyse the long-run relationship between private investment and remittances while controlling for several other variables, such as real-interest rate, economic growth, and the interaction between remittances inflow and business freedom. We use the error correction mechanism (ECM) to find the short-run relationship among variables. Our findings reveal that private investment is positively affected by remittances inflow. Moreover, remittances flow with low business freedom opposes the positive association in the case of these sampled countries. We recommend channelising remittances and lower barriers to business freedom, which may pave the way for a conducive investment-friendly environment.

1. Introduction

The global migration of nearly 250 million people is a key factor affecting the economies of developing countries via different channels. A recent report by The Global Knowledge Partnership on Migration and Development (KNOMAD) (Citation2017) found that remittances are a critical macroeconomic variable that contributes 596 billion dollars to the global economy, of which 450 billion flows to developing or under-developing economies.

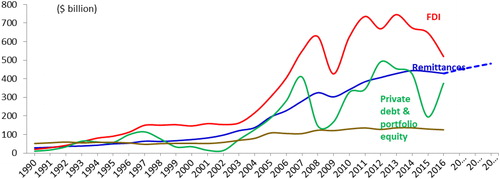

Developing countries take the major share of total remittances inflow, as indicated in . The flow of remittances is larger than private capital inflow and official development assistance to these economies. For some of the developing countries, the contribution of remittances inflow is more than foreign direct investment and contributes a large amount to the gross domestic product (GDP) (Adenutsi, Citation2011; Bjuggren, Dzansi, & Shukur, Citation2010; Connell & Brown, Citation2004; De Haas, Citation2006; Giuliano & Ruiz-Arranz, Citation2009; Heilmann, Citation2006; Rao & Hassan, Citation2011). However, South Asia countries such as India, Pakistan, Sri Lanka, Nepal, Bhutan, the Maldives, Afghanistan, and Bangladesh are the primary recipients of remittances inflow in the world, and among these countries, India takes considerable portion (World Bank, World Development Indicators, Citation2016; The Global Knowledge Partnership on Migration and Development (KNOMAD)).

Figure 1. Comparison of FDI, remittances inflow and other capital inflow to developing countries.

Source: The Global Knowledge Partnership on Migration and Development (KNOMAD) (Citation2017).

The economic power of remittances inflow is considered a vital source of support. As a capital, it affects the lives of millions of people across the globe. In the literature, the role of remittance has two different theoretical aspects: one theory is based on self-interest, and the other is based on altruistic drive. Money sent by migrants is either used for basic daily necessities or invested in some profitable ventures. Both of these motives are affected by the economic condition of the recipient, which affects both the level of investment and consumption of the receiver. Altruistic drive focuses on the utility of recipient, which is more concerned with the consumption of the recipient’s basic necessities, as most migrants remit funds from abroad due to consumption motives of their families (Barajas, Gapen, Chami, Montiel, & Fullenkamp, Citation2009). Remittances inflow significantly affects the standard of living of the recipient family, as some amount is also spent on health, capital formation, and education. In most cases, the recipient spends his or her money on physical capital or real estate for profit motives, which confirms the self-interest motive of remittances. (Mallick, Citation2008)

Empirical work suggests that remittances inflow mostly affects the consumption level of households through the multiplier effect (Stahl & Arnold, Citation1986; Rahman, Citation2009). However, the role of remittances cannot be limited only to consumption or economic growth; it is also used for foreign exchange (Maimbo & Ratha, Citation2005; Ratha, Citation2005; Ratha & Shaw, Citation2007) and allows debt constraints to be curbed due to the low number of microfinancing opportunities available in developing countries (Giuliano & Ruiz-Arranz, Citation2009).

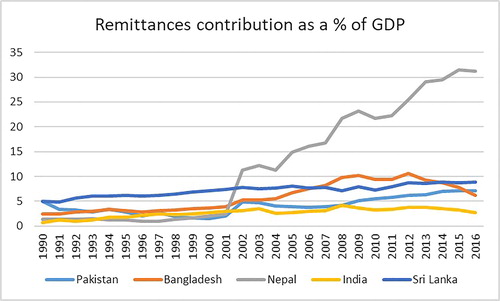

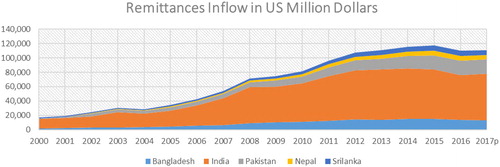

The role of remittances is multidimensional, and it has a positive effect not only on poverty, economic growth, consumption, and real-exchange rates but also on private investment in developing countries. As mentioned earlier, remittances play a vital role in Bangladesh, Sri Lanka, Pakistan, Nepal, and India; these countries collectively received 220,976 million U.S. dollars in the year 2016–2017. However, the contribution to the economy of each of these countries is different, as shown in and , in terms of remittances as a percentage of GDP as well as in terms of millions of U.S. dollars to these countries (World Bank, World Development Indicators, Citation2016; The Global Knowledge Partnership on Migration and Development (KNOMAD)).

Figure 2. Remittances contribution as % of GDP.

Source: Migration Policy Institute Data (2016).

Figure 3. Remittances shares in terms of Millions of U.S. Dollars.

Source: The Global Knowledge Partnership on Migration and Development (KNOMAD) (Citation2017).

In the case of South Asian economies, in addition to the economic growth, poverty and real-exchange rate are crucial to the role of remittances in promoting private investment. In the case of Nepal (Bank, Citation2012), findings found that remittances help farmers in acquiring lands for agricultural activities. Similarly, Pakistan is also getting a major portion of its GDP from migrant remittances. The role of remittances is essential, and it positively affects private investment, which further leads to higher economic growth (Yasmeen, Anjum, Yasmeen, & Twakal, Citation2011). However, it has been argued that remittances have a minimal effect on private investment, but as a whole are a crucial factor affecting countrywide economic growth (Ullah, Rahman, & Jebran, Citation2015, p. 178).

Following the previous literature, the role of remittances cannot be denied among major South Asian countries such as India, Pakistan, Sri Lanka, Nepal, and Bangladesh. However, most of the previous studies have analysed the effect of remittances only on economic growth, poverty, and real-exchange rates. The effect of remittances on investment in these countries has not been analysed, especially by applying more advanced econometric techniques such as pooled mean group (PMG) analysis. No cross-country analysis exists in this area of research. Therefore, this study is the only contribution to the existing literature that takes into account five cross sections (Pakistan, India, Sri Lanka, Nepal, and Bangladesh) and uses the most updated data from 1990 to 2016.

2. Previous empirical findings

On the role of remittances, numerous studies have been conducted to trace their effect on education, poverty, the health care system, economic growth, the standard of living, the balance of trade and real-exchange rates. Different studies have found remittances to have a positive effect on education, health care, economic growth, poverty, balance of trade and real-exchange rate in the recipient countries (Lopez, Fajnzylber, & Acosta, Citation2007; Alberola & Lopez, Citation2001; Barajas, Chami, Fullenkamp, & Garg, Citation2010; Burki, Citation1991; Chishti, Citation2007; Faridi & Mehmood, Citation2014; Heilmann, Citation2006; Khan, Ali, & Khalid, Citation2016; Khan, Sajid, Gondal, & Ahmad, Citation2009; Lopez, Bussolo, & Molina, Citation2007; Mughal & Anwar, Citation2012; Neyapti, Citation2004; Ratha & Shaw, Citation2007). In the case of Pakistan, the findings of Faridi and Mehmood (Citation2014), obtained by simple regression analysis, suggest that remittances help to alleviate poverty. Another study, by Lopez et al. (Citation2007) and using a Heckman two-step approach to study the effect of remittances in controlling poverty in Latin American economies, suggests that remittances help alleviate poverty but that the effect is different in different countries. It also helps to promote sustainable development and improves the skills, standard of living, and welfare of the society (Heilmann, Citation2006; Khan et al., Citation2009; Ratha & Shaw, Citation2007). However, the issue of remittances and private investment has been overlooked, despite it being an important macroeconomic variable for gauging the overall economic performance of a country. and provide detailed findings of each mentioned study.

Table 1. Summary of literature review.

Table 2. Remittances and Private Investment.

Many single-country analyses have been done by researchers, institutions, and academia on the relationship between remittances and private investment with both supporting and conflicting findings.

It has been found that, similarly to the positive effect of remittances on other macroeconomic variables, private investment is also affected positively by remittances (Akter, Citation2016; Cherono, Citation2013; Das, Citation2009; Griffith, Boucher, McCaskie, & Craigwell, Citation2008; Le, Citation2011; Malik, Citation2013; Mehra & Singh, Citation2014; Okodua & Olayiwola, Citation2013; Thagunna & Acharya, Citation2013; Ullah et al., Citation2015; Yasmeen et al., Citation2011) the role of remittances has been considered to be positive in promoting private investment when linked with a sound and well-organised financial sector that can channelise migrant money into private investment (Ojapinwa & Odekunle, Citation2013). In other studies, it has been found that only a minor portion of money sent by migrants is devoted to investment for promoting small-scale industries (Jahjah, Chami, & Fullenkamp, Citation2003; Khan et al., Citation2007).

It has further been found that migrant remittances are invested more often in housing or non-tradable goods than capital investment (Osili, Citation2004; Woodruff & Zenteno, Citation2007). On the other hand, studies have reported the positive effect of remittances on education and have linked spending on education with human capital by generating more skills and knowledge (Adams & Cuecuecha, Citation2010; Edwards & Ureta, Citation2003; Yang, Citation2005). The extensive literature mentioned above that focuses on the role of remittances in promoting investment is difficult to refute, as only one of the studies had contradictory results and did not find a positive role of remittances on promoting private investment (Mallick, Citation2012).

2.1. Theoretical views on migration and remittances

The role of remittances has been in discussion for a long time among the different schools of thought on migration. There are diverse opinions on the role of remittances opinions; some migration theories support the positive role of remittances, and some of them argue against it. This has been discussed by the classical and pessimistic schools of thought in the 1950–1960s and 1970–1980, respectively. However, both theories provide reasons for the role of remittances on recipient economies regarding poverty, economic development, and growth. The pessimistic theory (1970–1980s) viewed remittances as harmful for the economy and believed that they could cause investment in nonproductive ventures such as real estate (De Haas, Citation1998, Citation2005; Haan et al., Citation2000), which does not generate any real effect on the economy or job creation.

In the same way (Binford, Citation2003; De Mas, Citation1978), consider migration as a syndrome, stating that more migration causes more underdevelopment and the circle goes on by causing damage to the economy. Following the same concept, dependency and structuralists view migration as a source of dependency (Almeida, Citation1973). Neo-Marxists viewed migration and remittances as a source of inequality, reinforcing the capitalist system and the deficit in the trade balance for the receiving country (Papademetriou, Citation1991; Taylor & Wyatt, Citation1996). In contrast, the optimist theory (1950–1960s) of migration takes remittances as a positive stimulus to the economy that bridges the gap between external deficits, increasing industrialisation, education, economic development, knowledge and other structural changes in the recipient economy (Heinemeijer, Van Amersfoort, & den Haan, Citation1977).

3. Methods and techniques for analysis

The aim of this study was to explore the effects of remittances flow on private investment for five major recipient economies of South Asia that includes Pakistan, Sri Lanka, India, Nepal, and Bangladesh. This study uses remittances as our main exogenous variables while controlling for other variables such as economic growth, interest rate and the multiplicative effect of business freedom with remittances inflow. Panel data for the years of 1990–2016 for five cross-sections is taken from The Global Knowledge Partnership on Migration and Development (KNOMAD), Citation2017) and the World Bank (2016).

3.1. Econometrics model

Where PI is private investment (PI), remittances inflow is denoted by (RI), the real-interest rate by (RIR), EG is the economic growth, the multiplicative variable of business freedom is (BF), and remittance inflow is given by RI*BF. Further, the term ‘i’ is for the cross section, is for the time period starting from 1990 to 2016,

is for constant term and

are the coefficients, and

is the error term. Further, business freedom to initiate business is measured through ten other different indicators by the Word Bank (‘World Bank, World Development Indicators,’ 2016), and it contains the minimum level of capital required for starting a business, the timing, the procedure for obtaining business licenses, the time to close a business, recovery rate and cost of starting a business. The business freedom minimum point or low level of freedom is 40, and the maximum range or high level of business freedom value is 100 (Theglobaleconomy.com, Citation2016).

3.2. Panel data models

In panel data analysis, the simple form of the method is pooled OLS; it assumes a common intercept/constant for each country and the error term is not correlated with the independent variables such as remittances inflow, real-interest rate, economic growth, and an interactive term. The function for pooled OLS is as follows:

(2)

(2)

The pooled OLS model considers all the cross sections as homogeneous and does not consider the heterogeneity problem in the model. However, the problem of heterogeneity and correlation between the error term and independent variable may produce inconsistent as well as biased results. To address the problem of endogeneity and heterogeneity, the fixed-effect model is more appropriate compared to pooled OLS and addresses the issues that remain in the pooled OLS (Asteriou et al., Citation2015). The functional for the fixed-effect model is given below:

(3)

(3)

3.3. Fixed effect within group estimator (FEWGE)

Another method in panel data, used for a robustness check and to help remove the problem of unobserved factors such as fixed effect within group estimator. It eliminates the unobserved factors effect by first taking the average and then putting it in the original equation for the estimation. Moreover, the value of the constant term also drops-out to zero (Greene, Citation2003). The method is given below:

(4)

(4)

The term ‘T’ denotes total time period, writing this equation as Equation(5)(5)

(5) , the Bar denotes the average value:

(5)

(5)

(6)

(6)

3.4. Fixed effect (FE) vs. random effect (RE)

The random effect model considers as a random variable, while

is the average value and is specified as follows:

(7)

(7)

All the variations or heterogeneity come from while

is the average value common for all. Following EquationEquation (7)

(7)

(7) , the random effect is written as:

(8)

(8)

where the error component

has both components come from

and can be written as

; it is also called the idyiosynchratic error term. Moreover,

is not correlated with indepdent variables. Further, to choose between fixed effect and random effect, a Hausman Test is employed. The null hypothesis supports the RE while the alternative prefers the FE Model for the analysis (Gujarati, Citation2009).

(9)

(9)

These methods are applicable if there is no problem with stationarity in the data. In the next section, the stationarity of each variable is tested through unit root tests; if any issue of stationarity is found, then another appropriate method will be applied.

3.2. Panel autoregressive distributive lags model (PARDL)

The methodology of the pooled mean group proposed by (Pesaran & Smith, Citation1995) addresses the problem of heterogeneous slopes, especially in dynamic panels, causing bias in the results. Moreover, the mean group (MG) estimator long-run parameters are provided for the panel by taking an average of the long-run parameters through the autoregressive distributive lags model (ARDL) for each country. The given model is as follows:

In this model, ‘i’ denotes the number of countries/cross sections such as and ‘t’ means time period.

The long-run parameter for the model follows as:

Moreover, for the mean group (MG) estimator for the complete Panel we have,

The above-written equations show how regression for each cross-section can be estimated by the model and the unweighted averages of the coefficients without any restrictions as it follows the heterogeneity of coefficients both in the short-run and long-run. Moreover, the model requires data with a large time series dimension to have validity and consistency. In contrast, the method of PMG has been employed to find the short and long-run relationship between remittances and private investment for five different cross sections by taking into account the issue of dynamic heterogeneity; to address this issue, a panel ARDL model in ECM form is employed and estimated on the basis of the MG model developed by Pesaran, Shin, and Smith (Citation1999) and Fromentin (Citation2017). An ARDL specification follows:

The is K by 1 vector containing all the explanatory variables for each ‘i’; the term

shows the fixed effect. If the panel is unbalanced, then there is a possibility that p and q differ across cross sections. Now extending the model to Vector Error Correction (VECM) form:

In the above-given model, refers to long-run parameters while

shows the error correction mechanism (ECM) towards equilibrium. Moreover, PMG considers the

element the same across each cross section (countries):

The term shows private investment,

contains all the explanatory variables such as remittances inflow (RI), and real-interest rate by (RIR); EG is the economic growth, the multiplicative variable jointly of business freedom is (BF) and the remittance inflow is given by RI*BF. Moreover,

and

show the short-run coefficient and

is the long-run coefficient for independent and dependent variables. The term ‘

is the speed of adjustment towards long-run equilibrium. The bracket terms are for the long-run growth regression.

The decision to use MG or PMG is made on the basis of the Hausman test. The null hypothesis supports the PMG while the alternative hypothesis supports the MG model. Moreover, if the alternative hypothesis is accepted, then the dynamic fixed model (DFE) may also be applied and should be compared in the same way, through the Hausman test with MG.

More formally, the PARL methodology can be as follows:

(10)

(10)

‘’ shows the drift, while

specifies a white noise error term. Furthermore, the term with summation sign implies the error correction dynamics. First, the equation shows the short run while the second part is for long-run association. To get panel ARDL results, optimum lags should be selected using BIC, AIC and HQ criteria, and then after optimum lags, long-run relations are computed by using EquationEquation (10)

(10)

(10) :

(11)

(11)

If the long-run relationship is reported, then error correction mechanism should be used for the short-run relationship through EquationEquation (11)(11)

(11) :

(12)

(12)

The term ‘λ’ means adjustment speed or convergence towards equilibrium.

4. Interpretations and discussion

This section of the study addresses and discusses the interpretations of significant findings. It contains results obtained from pooled OLS, the fixed effect within group estimator (FEWGE), fixed effect (FE), random effect (RE), the Hausman test (HT), unit root tests, optimum lag criteria, cross-sectional dependency, long-run, and short-run coefficients, and mean group and pool mean group. Preceding with panel ARDL requires us to test the stationarity of all the variables of interest to avoid any misleading results using wrong techniques. To achieve this goal, a unit root test was applied to report the order of integration of each variable and to design methodology accordingly. To test stationarity of the data, two unit root tests such as Im, Pesaran, and Shin (Citation2003) and Levin, Lin, and Chu (Citation2002) were used, both with their specific characteristics and dealing with heterogeneity in the panel data.

reports hypothesis testing results. Hypothesis testing is useful in specifying the model and also helps to find the relevant variables, which affects the dependent variable. The results show that remittances inflow and Economic Growth positively and statistically significantly affect private investment in the case of the five sampled countries. On the other hand, real-interest rate and multiplicative term of remittances inflow and business freedom negatively and statistically significantly affect private investment in the case of India, Pakistan, Nepal, Bangladesh, and Sri Lanka. In the next section, based on Hypothesis testing, pooled OLS, FEWGE, FE, RE, and the Hausman test are employed.

Table 3. Hypothesis Testing for each variable.

reports result obtained from pooled OLS, FEWGE, FE and RE. The results show that both remittances inflow and economic growth in case of pooled OLS, FEWGE, FE and RE positively and statistically significantly affect private investment for Pakistan, Sri Lanka, Nepal, India, and Bangladesh. A one percent increase in remittances inflow causes private investment to increase by 0.036%, 0.030%, 0.11%, and 0.035%, respectively, with a 1% and 5% significance level; coefficients for RI are positive and statistically significant in all methods. The results support (Akter, Citation2016; Cherono, Citation2013; Das, Citation2009; Griffith et al., Citation2008; Le, Citation2011; Malik, Citation2013; Mehra & Singh, Citation2014; Okodua & Olayiwola, Citation2013; Thagunna & Acharya, Citation2013; Yasmeen et al., Citation2011) findings, who reported that remittances inflow and economic growth promote private investment in the recipient countries. Remittances played an essential role in the financial development of a country. These findings suggest that remittances inflow help to expand and provide the required level of capital for investment. The utilisation of remittances inflow is vital, as if it is utilised and appropriately channelised, then it will have a positive effect on small and medium enterprises (Woodruff & Zenteno, Citation2007).

Table 4. Panel data analysis.

The effect of remittances inflow*business freedom on private investment is negative, however, and statistically insignificant at 1%, 5% and 10%, which is similar to Muhammad, Lakhan, Zafar, and Noman (Citation2013) and Wuhan and Khurshid (Citation2015) who reported that business freedom is an essential factor for promoting private investment in these sampled remittances recipient countries. The findings further revealed that a business-friendly environment is crucial for attracting private investment through remittances inflow. The more there is freedom to invest, the higher the positive effect on the economy. The real-interest rate, as expected, negatively affects private investment in the cases of India, Pakistan, Sri Lanka, Bangladesh, and Nepal. Moreover, to select the between the fixed effect and random effect models, the Hausman test is employed; the test value prefers the fixed effect over the random effect model as its value is significant at 5% supporting the alternative hypothesis. In the next section, unit root tests are employed to trace the stationarity of the data, if a stationarity problem is found then the panel ARDL model should be used.

Before applying mean group or alternatively, PMG, as panel ARDL, unit root tests are used to check the order of integration of the variables. Further, it is tested that none of the variables is of order I(2) as then F-statistics values are not valid anymore (Pesaran, Shin, & Smith, Citation2001). Im et al. (Citation2003) and Levin et al. (Citation2002) reported in verifying that variables in the model are mixed in order of integration i.e., I (1), I (0), I (1), I (1), I (1) and hence permit the possibility of employing a panel autoregressive distributive lag model (PARDL) to find the long-run coefficients and using an error correction mechanism (ECM) to get the short-run coefficients of the model.

Table 5. Unit root results.

The cross-sectional dependency test; the results support an alternative hypothesis of cross-sectional dependency. The next step is to select the optimum lags order of integration to specify the model accordingly and to ensure accurate results; without selecting the optimum lag order, it is difficult to get efficient results. There are different tests for the selection of optimum lags, which include Bayesian information criterion (BIC), Akaike information criterion (AIC), and Hannan-quin criterion (HQ). Each of these tests has their specific characteristics that differentiate one from the other (Gujarati & Porter, Citation1999). However, this study uses all three criteria to reach a solid consensus and to get more efficient results. The model selected by AIC, BIC and HQ have the same optimum lags in our analysis.

Table 6. Lags selection procedure.

Results reported in show that we have to follow the model with one lag for each variable in our analysis, i.e., PARDL (1, 1, 1, 1); lags order has been selected by taking the minimum value of AIC, BIC, and HQ. As in this case, minimum values are reported as −3.349, −2.658 and −2.839, respectively. In the next section, long-run results are presented, followed by short-run results, and then the Hausman test is employed to select between MG and PMG.

Table 7. Long-run PMG/PARDL Coefficients.

The long-run results given in correspond to the previous reported results of Okodua and Olayiwola (Citation2013), Griffith et al. (Citation2008), Malik (Citation2013), Le (Citation2011), Das (Citation2009), Thagunna and Acharya (Citation2013), Yasmeen et al. (Citation2011), Mehra and Singh (Citation2014), Akter (Citation2016), and Cherono (Citation2013) who stated that remittances inflow positively affects private investment as well as education, health care, and other spendings; recipient households also devote remittances to investment. Similarly, shows that the results confirm that a one percent increase in remittances inflow increases private investment by 0.088% in the cases of selected South Asian economies. In the long run, the results revealed that remittances inflow played an important role in increasing private and this is because the capital requirement to the businesses is covered through remittances inflow. In the case of selected South Asian economies, remittances inflow is helpful in formation of capital and job creation for the migrant’s families back home. The current findings are also in line with the view of optimistic theory (1950–1960) of migration which advocates that remittances play a constructive role by encouraging private investment.

Table 8. ECM short-run coefficients.

Further, our analysis suggests that economic growth supports private investment and has a positive relationship with private investment, verifying that a one percent increase in economic growth causes a 0.16 increase in private investment. On the other hand, interactive variables, business freedom, and remittances influx have a negative relationship with private investment in the case of Nepal, Bangladesh, Pakistan, India, and Sri Lanka; these findings support (Muhammad et al., Citation2013; Wuhan & Khurshid, Citation2015) who found that business freedom is necessary for promoting private investment. However, the analysis found a negative relationship between real-interest rate and investment in the private sector in these economies (Muhammad et al., Citation2013; Wuhan & Khurshid, Citation2015).

reports the short run findings; it is found that remittances do not have a statistically significant relationship with private investment in the short run, though it affects remittances positively. One possible reason for the lack of a statistically significant relationship in these countries is that in the initial stages of migration, migrants are trying to stabilise their level of consumption. In the initial stages, recipients spend more on necessities, such as shelter, food, and water, before they settle down and proceed towards financial stabilisation. In the stabilised stage, the recipients start saving and then convert those savings to investment in the long run, which is supported in our findings in . In the short run, the other variables respond in the same manner as in the long run except for the interaction between business freedom and remittances inflow. The error correction mechanism (ECM) term ‘λ’ reports the speed of adjustment towards long-run equilibrium or the convergence towards long-run equilibrium. At every year, 26% adjustment takes place.

Table 9. Hausman test results.

The Hausman test has been used to select between the mean group and pooled mean group. Before the Hausman test, both MG and PMG models were used, and the Hausman test decides which one to use. Similarly, reports that the findings of the Hausman test suggest using PMG over MG, which allows testing the short-run and the long-run relationship inflow of remittances and investment. Pooled mean group analysis is superior to mean group analysis as it allows heterogeneous short-run coefficients, intercept and cointegrating coefficients to vary for each cross section (country) (Pesaran et al., Citation1999).

5. Conclusion

This study analysed how remittances inflow affects private investment for South Asian economies from data collected from 1990 to 2016. This study employed different econometric tests, including pooled OLS, the fixed effect within group estimator (FEWGE), fixed effect (FE) and random effect (RE) to report the relationship between Remittances Inflow and Private Investment.

Further, to check the long-run and the short-run relationship between private investment and remittances inflow pooled mean group (PMG) analysis was employed. Prior to PMG, Im et al. (Citation2003) and Levin et al. (Citation2002) were used for testing the unit root problem in the data and was followed by Bayesian information criterion (BIC) Hannan-Quin criterion (HQ) and Akaike information criterion (AIC) tests for selecting the optimum lag structure of the model. Similar to earlier studies, the current study also found a positive effect of remittances inflows on private investment in the context of India, Sri Lanka, Bangladesh, Pakistan, and Nepal.

The results reported in this study are also consistent with the findings of earlier work on the current issue for different countries, regions and time periods by Mehra and Singh (Citation2014), Das (Citation2009), Cherono (Citation2013), Thagunna and Acharya (Citation2013), Yasmeen et al. (Citation2011), Okodua and Olayiwola (Citation2013), Ullah et al. (Citation2015), Akter (Citation2016), Le (Citation2011), Griffith et al. (Citation2008), and Malik (Citation2013). Moreover, the long-run relationships for other variables such as economic growth, remittances inflow, and business freedom interaction and real-interest rate were also reported. An error correction mechanism (ECM) confirmed the short-run relationship between other variables and private investment. The negative relationship between the interactive variable (remittances inflow and business freedom) is due to that fact that these five sampled countries are underdeveloped countries and not very business friendly due to complex bureaucracy. Barriers, such as obtaining a license, cost of starting a business and the minimum level of capital required, are the key constraints to business freedom; this is why there was an inverse relationship between both. Studies by Imtiaz and Bashir (Citation2017) and Amponsem (Citation2017) also reported the need for a business-friendly environment for gaining investors’ interest in the case of South Asian countries. The findings of this study also support the optimistic theory (1950–1960) of migration, advocating that remittances play a supportive role in encouraging investors and promoting investment. Pakistan, India, Bangladesh, Sri Lanka, and Nepal need to channelise remittances inflow and should develop strong financial systems to seize the benefit of remittances inflow fully. In addition, they should make business licenses easily available, lower restrictions on new businesses, reduce the cost for starting a new business and keep the interest rate at a minimum level to compensate investors in these five major South Asian remittances recipient countries.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Lopez, J. H., Fajnzylber, P., & Acosta, P. (2007). The impact of remittances on poverty and human capital: Evidence from Latin American household surveys The World Bank.

- Adams, R. H., Jr., & Cuecuecha, A. (2010). Remittances, household expenditure and investment in Guatemala. World Development, 38(11), 1626–1641. doi:10.1016/j.worlddev.2010.03.003

- Adenutsi, D. E. (2011). Do remittances alleviate poverty and income inequality in poor countries? Empirical evidence from sub-Saharan Africa (No. 37130). Germany: University Library of Munich.

- Akter, S. (2016). Remittance inflows and its contribution to the economic growth of Bangladesh. (62), 215–245.

- Alberola, E., & Lopez, H. (2001). Internal and external exchange rate equilibrium in a cointegration framework. An application to the Spanish peseta. Spanish Economic Review, 3(1), 23–40. doi:10.1007/PL00013583

- Almeida, C. C. (1973). Emigration, espace et sous‐développement. International Migration, 11(3), 112–117. doi:10.1111/j.1468-2435.1973.tb00904.x

- Amponsem, F. (2017). The effects of economic freedom on inflows of foreign direct investment. Lethbridge: University of Lethbridge, Dept. of Economics.

- Anwar, A. I., & Mughal, M. Y. (2012). Motives to remit: Some microeconomic evidence from Pakistan. Economics Bulletin, 32(1), 574–585.

- Asteriou, D., Hall, S. G., Johnston, J., DiNardo, J., Harris, R. I. D., & Sollis, R. (2015). Applied Econometrics. In other words, 1, 18200.

- Bank, N. R. (2012). Impact evaluation of remittances: A case study of Dhanusha district. Janakpur: Banking and Development Unit.

- Barajas, A., Chami, R., Fullenkamp, C., & Garg, A. (2010). The global financial crisis and workers’ remittances to Africa: What’s the damage? IMF Working Papers, 10, 1. doi:10.5089/9781451962413.001

- Binford, L. (2003). Migrant remittances and (under) development in Mexico. Critique of Anthropology, 23(3), 305–336. doi:10.1177/0308275X030233004

- Bjuggren, P., Dzansi, J., & Shukur, G. (2010). Remittances and investment. Centre for Excellence for Science and Innovation Studies (CESIS) (No. 216). Working Paper.

- Burki, S. J. (1991). Migration from Pakistan to the Middle East. The Unsettled Relationship: Labor Migration and Economic Development, (33), 139.

- Cherono, M. (2013). The effect of remittances and financial development on private investment in Kenya (Unpublished MA Economics Research Project).

- Chishti, M. (2007). The rise in remittances to India: A closer look. Migration Information Source, 1.

- Connell, J., & Brown, R. P. (2004). The remittances of migrant Tongan and Samoan nurses from Australia. Human Resources for Health, 2(1), 2. doi:10.1186/1478-4491-2-2

- Das, A. (2009). The effect of transfers on investment and economic growth: Do remittances and grants behave similarly? Memo, University of Manitoba.

- De Haas, H. (1998). Socio-economic transformations and oasis agriculture in southern Morocco. In L. de Haan & P. Blaikie (Eds.), Looking at maps in the dark (pp. 65–78).

- De Haas, H. (2005). International migration, remittances and development: Myths and facts. Third World Quarterly, 26(8), 1269–1284. doi:10.1080/01436590500336757

- De Haas, H. (2006). Migration, remittances and regional development in Southern Morocco. Geoforum, 37(4), 565–580. doi:10.1016/j.geoforum.2005.11.007

- De Mas, P. (1978). Marges marocaines: Limites de la cooperation au développement dans une région périphérique: Le cas du Rif.

- Edwards, A. C., & Ureta, M. (2003). International migration, remittances, and schooling: Evidence from El Salvador. Journal of Development Economics, 72(2), 429–461.

- Faridi, M. Z., & Mehmood, K. A. (2014). Workers’ remittances and poverty in Pakistan. Pakistan Journal of Social Sciences (PJSS), 34(1), 13–27.

- Fromentin, V. (2017). The long-run and short-run impacts of remittances on financial development in developing countries. The Quarterly Review of Economics and Finance, 66, 192–201. doi:10.1016/j.qref.2017.02.006

- Barajas, A., Gapen, M. T., Chami, R., Montiel, P., & Fullenkamp, C. (2009). Do workers’ remittances promote economic growth? (No. 2009-2153). International Monetary Fund.

- Giuliano, P., & Ruiz-Arranz, M. (2009). Remittances, financial development, and growth. Journal of Development Economics, 90(1), 144–152. doi:10.1016/j.jdeveco.2008.10.005

- Greene, W. H. (2003). Econometric analysis. Pearson Education India.

- Griffith, R., Boucher, T., McCaskie, P., & Craigwell, R. (2008). Remittances and their effect on the level of investment in Barbados. Journal of Public Sector Policy Analysis, 2, 3–15.

- Gujarati, D. N. (2009). Basic econometrics. Tata McGraw-Hill Education.

- Gujarati, D. N., & Porter, D. C. (1999). Essentials of econometrics (Vol. 2). Singapore: Irwin/McGraw-Hill.

- Haan, A. D., Brock, K., Carswell, G., Coulibaly, N., Seba, H., & Toufique, K. A. (2000). Migration and livelihoods: Case studies in Bangladesh, Ethiopia and Mali (No. 46).

- Heilmann, C. (2006). Remittances and the migration–development nexus—Challenges for the sustainable governance of migration. Ecological Economics, 59(2), 231–236. doi:10.1016/j.ecolecon.2005.11.037

- Heinemeijer, W. F., Van Amersfoort, J., & den Haan, R. (1977). Partir pour Rester: Une enquête sur les incidences de l’émigration ouvrière à la campagne marocaine. Imwoo/Nuffic: Projets Remplod.

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. doi:10.1016/S0304-4076(03)00092-7

- Imtiaz, S., & Bashir, M. F. (2017). Economic freedom and foreign direct investment in South Asian countries. Theoretical and Applied Economics, 24(2), 277–290.

- Jahjah, M. S., Chami, M. R., & Fullenkamp, C. (2003). Are immigrant remittance flows a source of capital for development (No. 3-189). International Monetary Fund.

- Khan, M., Khattak, N., Bakhtiar, Y., Nawab, B., Rahim, T., & Ali, A. (2007). Remittances as a determinant of import function (an empirical evidence from Pakistan). Sarhad Journal of Agriculture (Pakistan).

- Khan, S., Sajid, M. R., Gondal, M. A., & Ahmad, N. (2009). Impacts of remittances on living standards of emigrants’ families in Gujrat Pakistan. European Journal of Social Sciences, 12(2), 205–215.

- Khan, Z., Ali, S., & Khalid, S. (2016). Remittances inflow and Real Exchange Rate: A Case Study of Pakistan Economy. Journal of Chinese Economics, 4(2), 89–94.

- Le, T. (2011). Remittances for economic development: The investment perspective. Economic Modelling, 28(6), 2409–2415. doi:10.1016/j.econmod.2011.06.011

- Levin, A., Lin, C.-F., & Chu, C.-S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24. doi:10.1016/S0304-4076(01)00098-7

- Lopez, H., Bussolo, M., & Molina, L. (2007). Remittances and the Real Exchange Rate. World Bank Policy Research Working Paper, (4213).

- Maimbo, S. M., & Ratha, D. (2005). Remittances: Development impact and future prospects. World Bank Publications.

- Malik, S. U. (2013). Role of Foreign Private Investment and Remittance in Stock Market Development: Study of South Asia (No. 54530). University Library of Munich, Germany.

- Mallick, H. (2008). Do remittances impact the economy?: Some empirical evidences from a developing economy.

- Mallick, H. (2012). Inflow of remittances and private investment in India. The Singapore Economic Review, 57(01), 1250004. doi:10.1142/S021759081250004X

- Mehra, S., & Singh, G. (2014). Migration: A propitious compromise. Economic and Political Weekly, 49(15), 24–25.

- Mughal, M., & Anwar, A. (2012). Remittances, inequality and poverty in Pakistan: Macro and microeconomic evidence (No. 2012-2013_2).

- Muhammad, D. S., Lakhan, G. R., Zafar, S., & Noman, M. (2013). Rate of interest and its impact on investment to the extent of Pakistan. Pakistan Journal of Commerce and Social Sciences, 7(1), 91–99.

- Neyapti, B. (2004). Trends in workers’ remittances: A worldwide overview. Emerging Markets Finance and Trade, 40(2), 83–90. doi:10.1080/1540496X.2004.11052567

- Ojapinwa, T. V., & Odekunle, L. A. (2013). Workers’ remittance and their effect on the level of investment in Nigeria: An empirical analysis. International Journal of Economics and Finance, 5(4), 89. doi:10.5539/ijef.v5n4p89

- Okodua, H., & Olayiwola, W. K. (2013). Migrant workers’ remittances and external trade balance in Sub-Sahara African countries. International Journal of Economics and Finance, 5(3), 134. doi:10.5539/ijef.v5n3p134

- Osili, U. O. (2004). Migrants and housing investments: Theory and evidence from Nigeria. Economic Development and Cultural Change, 52(4), 821–849. doi:10.1086/420903

- Papademetriou, D. (1991). The unsettled relationship: Labor migration and economic development (No. 33). Greenwood Publishing Group.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/jae.616

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. doi:10.2307/2670182

- Pesaran, M. H., & Smith, R. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79–113. doi:10.1016/0304-4076(94)01644-F

- Rahman, M. (2009). Contributions of exports, FDI, and expatriates’ remittances to real GDP of Bangladesh, India, Pakistan, and Sri Lanka. Southwestern Economic Review, 36(1), 141–154.

- Rao, B. B., & Hassan, G. M. (2011). A panel data analysis of the growth effects of remittances. Economic Modelling, 28(1-2), 701–709. doi:10.1016/j.econmod.2010.05.011

- Ratha, D. (2005). Workers’ remittances: An important and stable source of external development finance. Remittances: development impact and future prospects, 19-51.

- Ratha, D., & Shaw, W. (2007). South-South migration and remittances. World Bank Publications.

- Stahl, C. W., & Arnold, F. (1986). Overseas workers’ remittances in Asian development. International Migration Review, 20(4), 899–925. doi:10.2307/2545742

- Taylor, J. E., & Wyatt, T. J. (1996). The shadow value of migrant remittances, income and inequality in a household‐farm economy. Journal of Development Studies, 32(6), 899–912. doi:10.1080/00220389608422445

- Thagunna, K. S., & Acharya, S. (2013). Empirical analysis of remittance inflow: The case of Nepal. International Journal of Economics and Financial Issues, 3(2), 337.

- The Global Knowledge Partnership on Migration and Development (KNOMAD). (2017). The Global Knowledge Partnership on Migration and Development (KNOMAD, 2017). Retrieved from https://www.knomad.org/data/remittances?tid%5B71%5D=71&tid%5B142%5D=142&tid%5B191%5D=191&tid%5B201%5D=201&tid%5B232%5D=232

- Theglobaleconomy.com. (2016). theglobaleconomy. Retrieved from https://www.theglobaleconomy.com/

- Ullah, I., Rahman, M. U., & Jebran, K. (2015). Terrorism and worker’s remittances in Pakistan. Journal of Business Studies Quarterly, 6(3), 178.

- Woodruff, C., & Zenteno, R. (2007). Migration networks and microenterprises in Mexico. Journal of Development Economics, 82(2), 509–528. doi:10.1016/j.jdeveco.2006.03.006

- World Bank, World Development Indicators. (2016). Retrieved from World Bank http://data.worldbank.org/

- Wuhan, L. S., & Khurshid, A. (2015). The effect of interest rate on investment; Empirical evidence of Jiangsu Province, China. Journal of International Studies, 8(1), 81–90. doi:10.14254/2071-8330.2015/8-1/7

- Yang, D. (2005). International migration, human capital, and entrepreneurship: Evidence from Philippine migrants’ exchange rate shocks (Vol. 3578). World Bank Publications.

- Yasmeen, K., Anjum, A., Yasmeen, K., & Twakal, S. (2011). The impact of workers’ remittances on private investment and total consumption in Pakistan. International Journal of Accounting and Financial Reporting, 1(1), 152. doi:10.5296/ijafr.v1i1.949