Abstract

This paper aims to provide a detailed demographic description of poverty in Pakistan with an attempt to highlight those segments of the poor who can be aided to transition out of extreme poverty through appropriate policy measures. Data are collected from the Household Integrated Economic Survey (HIES) for the years 1985–2016 and captures falling poverty, gender-wise division of the employed and unemployed, type of employment (self-employed, unpaid workers, employers, employees) by gender, labour participation of vulnerable age groups, as well as unemployed widows. The paper discusses the effectiveness of conditional (CCT) and unconditional (UCT) cash transfer programs across the world and using data indicators, highlights the appropriate target groups in need of such intervention in Pakistan. The existing components of BISP are discussed, with policy recommendations targeted to enhance its impact by focusing UCTs on the most vulnerable segments. CCTs can be used to improve health and education outcomes; given Pakistan’s lagging performance, illiteracy among youth, infant and maternal health are of particular consideration. Cash transfers can be made conditional, subject to regular health checkups for mothers and children and mandatory school attendance to improve these outcomes. The paper further suggests an extension of the program to provide short-term financial relief to the temporarily unemployed.

1. Introduction

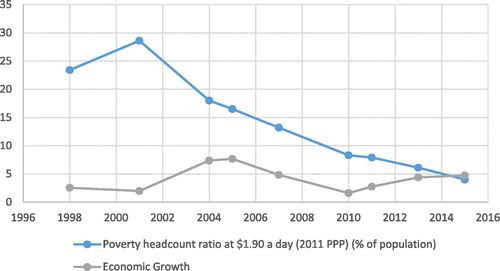

Despite inconsistent economic growth, Pakistan has made remarkable progress in reducing poverty, particularly since 2002 (). The share of people living below the poverty line (as estimated by $1.25 per day) has declined from 64.7% in 1990 to 12.7% in 2010 while according to the official national poverty line, poverty has declined from 25.5% in 1992 to 12.4% in 20101 (World Bank, Citation2015). The official figures for poverty in the country do not seem to follow a trend in line with its economic performance (), indicating that there is no established relationship between poverty and macroeconomic performance in Pakistan.

Figure 1. Economic Growth and Incidence of Poverty in Pakistan, 1998–2015.

Source: Economic Growth – Ministry of Finance, Government of Pakistan

Poverty Headcount – World Development Indicators, World Bank

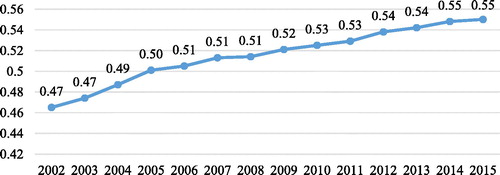

The fall in poverty despite poor growth is also substantiated by the World Banks Human Development Index (HDI), which shows that Pakistan has made stable progress in terms of income levels, education, health and inequality ().

Figure 2. HDI, Pakistan.

Source: World Development Indicators, World Bank

As evident from the figures, reduction of poverty in Pakistan does not necessarily follow its economic growth (); for example, despite declining economic growth between 2005 and 2010, the poverty headcount ratio at national poverty lines continued to fall from 50.4 in 2005 to 36.8 in 2010. Therefore, the answers for Pakistan’s declining poverty do not lie in its economic growth; rather, the policies introduced to mitigate poverty need to be examined for possible answers. Effective public services are of paramount importance in reducing poverty (Joshi, 2008); therefore it is essential to take into account the human development arising from the provision of such public services, especially in the form of social safety nets.

Given that poverty alleviation in Pakistan does not appear to be directly linked to economic growth, it is necessary to evaluate whether the fall in poverty is realised across all segments of the country. shares the average monthly income of the highest and lowest 20% households in terms of income; the data show that the income gap between the richest and poorest 20% households has increased over the years. This suggests that despite declining poverty in the country, the poorest may not be benefiting from this trend. So even though the median income levels are increasing, it is possible that the income for the richest is growing more significantly than that for the poor, widening the gap between them.

Table 1. Income gap and average monthly income of upper 20% and lowest 20% households.

The apparent disconnect between economic growth and the fall in poverty leads to the question, what policies have contributed to the decline of poverty in Pakistan. For our research, we focus on the expansion of cash transfer programs. In recent years, public spending on 17 pro-poor sectors has increased; the Benazir Income Support Program (BISP) in particular has been a boost to the safety-net for the poor as an unconditional cash transfer (UCT) program.

The use of social safety nets is increasing rapidly, with unconditional cash transfer programs being adopted in 40 countries in 2015, which is nearly twice the figure in 2010 (World Bank, Citation2015). In addition to UCTs, conditional cash transfers (CCTs) have also gained traction and have been producing remarkable results in countries like India, Brazil, Mexico and China. As the popularity of social safety nets increases across the world, it is imperative that the programs are targeted towards the appropriate focus group so as to maximise the efficiency of resources and have maximum impact at alleviating poverty.

Current literature suggests that that economic growth and poverty reduction do not necessarily affect all income groups to the same extent and some of the poor are presented with more opportunities than others (Ravallion, Citation2001). Given that countries with lower inequality have more success in translating their economic growth into poverty reduction, the rising income inequality is particularly concerning (Fosu, Citation2011). Therefore, while reducing overall poverty is an important objective, it is imperative that the most vulnerable segments of the society are not overlooked during the planning and implementation of social safety programs.

This paper attempts to outline the demographics of poverty in Pakistan and evaluate how well the current cash transfer programs have been implemented in the country, providing grounds for improvement to the target demographics of cash transfer programs. Section 1 discusses conditional and unconditional cash transfer programs and the channels through which they affect poverty, Section 2 assesses Pakistan’s largest cash transfer program and discusses the countries poverty demographics while section 3 concludes.

2. Poverty and cash transfer programs

According to the World Bank, every country in the word has a minimum of one social safety net program in place. From the 1.9 billion recipients of social safety programs, 44% receive transfers in-kind, 37% receive cash transfers while the remaining 19% receive fee-waivers (World Bank, Citation2015). In recent years, an increasing number of countries have adopted cash transfer programs to support the poorest segment of the population. Some of the most successful examples include the Dibao program in China, Bolsa Familia in Brazil, and the National Rural Employment Guarantee Act (NREGA) in India.

Cash transfer programs provide financial assistance to poor households in the form of cash. Under such programs, the effects of the program are only seen on the target population, rather than at a national level (de Janvry & Sadoulet, Citation2006). For countries with a large share of population living below the poverty line, effective implementation of cash transfer programs can lead to the maximum fall in poverty per unit of money transferred (de Janvry & Sadoulat, 2006). In 2014, 119 developing countries had implemented at least one type of unconditional cash assistance program, and 52 countries had conditional cash transfer programs for poor households (Gentilini, Honorati, & Yemstov, Citation2014). As of 2017, the number of countries offering cash transfer programs has increased to 149 (World Bank, Citation2017). Cash transfer programs have played a vital role in reducing the poverty headcount and the benefits of such programs justify their cost to donors and taxpayers alike (Fiszbein & Schady, Citation2009). For example, in 2009 alone, Brazil’s Bolsa Família led to a decrease in poverty headcount index between 12% and 18% (Higgins, Citation2012).

2.1. Conditional and unconditional cash transfers

Targeted cash transfer programs have received considerable attention from policy makers and researchers, especially in terms of choosing the most appropriate programs. There are two kind of cash transfer programs: conditional (CCTs) and unconditional (UCTs). UCTs are typically less costly to implement than CCTs due to lesser monitoring involved for the usage of funds (Haushofer & Shapiro, Citation2016). In the past, UCTs have often been disregarded due to their image of being free ‘handouts’ and reducing the incentive to work; however, this claim is not validated by research. In a presence of cash transfer programs, expenditures on food consumption, health and education are likely to increase, while there may be little to no effect on expenditure on luxuries (Haushofer & Shapiro, Citation2016). Similarly, research suggests that unconditional cash transfers do not impact the spending on ‘taboo’ goods like alcohol and cigarettes (Evans & Popova, Citation2014), which lessens the expected negative effects of UCTs. Moreover, the presence of cash transfer programs does not seem to have any effect on the willingness to work of the recipients or the lack thereof (Banerjee, Hanna, Kreindler, & Olken, Citation2017). UCTs have been successfully employed in various countries across the world. One most successful example is that of Di Bao program in China, which provides income support to households falling below a pre-determined income level.

Regardless of their conditionality, cash transfer programs produce better results as compared to no cash transfer programs (Baird, Ferreira, Özler, & Woolcock, Citation2014). However, evidence suggests that the impact of CCTs on human development is greater, as compared to UCTs (Baird, Ferreira, Özler, & Woolcock, Citation2014). As compared to in-kind transfers, cash transfer programs allow the parents greater freedom in determining how to best allocate the money received towards the health and wellbeing of their children (Miller & Neanidis, Citation2015). Typically, CCTs have two purposes: (a) poverty alleviation through the cash transfer in the short run and (b) accumulation of long-term human capital accumulation through health care and education in the long run (Handa & Davis, Citation2006).

The existence of a cash transfer program, however, does not automatically result in poverty reduction. For example, China’s Dibao program is one of the largest minimum income cash transfer schemes in the world, providing income support to poor beneficiaries; however, literature suggests that it has not significantly reduced the overall level of poverty in the country (Golan, Sicular, & Umapathi, Citation2017). When it comes to making the decision between a CCT and a UCT, the end objectives need to be kept in mind. When the goal is to improve human development, for example through school enrolment or access to healthcare, CCTs may have greater impact. For example, research shows that a dollar unit spent on a CCT is 8 times more effective than a dollar unit spent on a UCT (de Janvry, Sadoulet, Solomon, & Vakis, 2006). In addition to improving education, CCTs also increase household consumption and improve preventative healthcare (Hunter & Sugiyama, Citation2014; Rawlings & Rubio, Citation2005). However, the effect of CCTs on education may be contingent upon other factors. A study from Kenya suggests that unconditional cash transfers have strong effects on schooling rates, but that the additional impact of making the cash payments conditional on school attendance is limited (Baird, McIntosh, & Ozler, Citation2011). For example, Malawi and Burkina Faso have experienced positive results with CCTs but Morocco does not exhibit any significant impact of cash transfer programs (Baird, Ferreira, Özler, & Woolcock, Citation2014). Moreover, the increase in school attendance rates do not necessarily translate to greater learning among children (Behrman, Parker, & Todd, Citation2005; Baird et al., Citation2011).

For countries considering interventions through CCT programs, the disbursement to funds needs to be transparent and the conditions of the program must be stated in clear, concrete terms and results need to be monitored rigorously. Moreover, transparency in implementation encourages learning, minimises corruption and ensures that beneficiaries understand how the program works (Son, Citation2008).

2.2. Cash transfers and channels of poverty alleviation

Cash transfer programs have been widely praised for their success, particularly when they are well implemented. When appropriately targeted, such programs have been observed to reduce the incidence of household poverty, as well as its intensity (Molyneux, Jones, & Samuels, Citation2016). One of the primary criticisms of cash transfer programs is the fact that such initiatives fail to create sustained means of livelihood for recipients and there is a demand for such programs to be ‘transformative’ in terms of bringing about long lasting changes (Molyneux, Jones, & Samuels, Citation2016). The primary channel for cash transfer programs to reduce poverty is through their impact on human development (World Bank, Citation2009) and literature over the years suggests the same. The human development indicators include health, nutrition and education (Cotto, Citation2018) as well as female empowerment and labour force participation. For example, positive effects of cash transfers on children’s health and education outcomes have been recorded in multiple studies (Cecchini & Madariaga, Citation2011, Arnold, Conway, & Greenslade, Citation2011; Schady & Araujo, Citation2006; Son, Citation2008). The education outcomes include enrolment, attendance and achievements in school (Son, Citation2008) while health outcomes include immunisation, incidence of illness and sick days availed. The nutrition outcomes include incidence of stunting and malnutrition amidst the recipient households.

Several studies have been also targeted to be more ‘gender-aware’ (Holmes & Jones, Citation2013), and focus on empowering women by providing them with better opportunities. For example, the Estancias program in Mexico and the Bolsa Familia program in Brazil provide subsidised childcare (crèches) for women with children, while the BISP program seeks to elevate the social status of women by making them the primary beneficiary of payments in Pakistan.

3. Cash transfer programs and lessons from Pakistan

The Benazir Income Support Program (BISP) is a federal unconditional cash transfer initiative by the Government of Pakistan, which attempts to reduce poverty and promote equitable distribution of wealth especially for the low-income groups. Started in 2008, the primary objective of the program was to provide a financial cushion to the poor in the face of higher cost of food and fuel; it has since evolved into an income support program for the poorest and most vulnerable segment. Under BISP, a disbursement of PKR 1,500 per month is made to women from impoverished households on a quarterly basis; in 2008, each recipient household received PKR 1,000 per month. Since its inception, BISP has gained international approval for its implementation, ranking at 5th internationally in terms of targeting performance (World Bank, Citation2015).

To identify its target audience, BISP has adopted the ‘Poverty Scorecard’ instrument developed by the World Bank, under which 7.7 million families have been identified and 5.7 million currently receive assistance across all provinces (‘Benazir Income Support Programme’, 2018). Since 2011, BISP has used Proxy Means Test (PMT) to access the poorest 15% of households (Ambler & De Brauw, Citation2017). The PMT makes use of 23 variables taken from the PSLM and the cut off score is currently set at 16.17. However, exceptions may be made for poor households with a disabled member, senior citizens and those with more than four children under 12. Following reports of misappropriation of funds, the payment method was changed from conventional mail to ATM cards issued to women with valid CNICs in 2012. Roughly 48% of the recipient households belong to the poorest quintile in the country (BISP, 2016).

At the time of its inception, BISP did not require households to make an effort to invest in human or physical capital, which would hasten the transition out of poverty. Hence, while the program does ease financial burden, it is likely that there would be no progress towards the recipient households becoming self-sufficient. The effective transition out of poverty for recipient households is also one of the benchmarks for the success of social safety programs (Nayab & Farooq, Citation2014). Over the years, conditional interventions have been introduced as a part of BISP in order to increase the uptake of education and healthcare and to improve livelihoods, so that chances of transitioning out of poverty are increased. However, these programs were later scrapped by the succeeding government due to poor planning and monitoring in 2015 (Tanoli, Citation2016).

The impact evaluations of BISP show that at the very least, the program has led to an increase in women empowerment in Pakistan (Ambler & De Brauw, Citation2017), which is positively correlated with economic growth (Duflo, Citation2012). Women empowerment is also reflected in the fact that BISP has led to an increase in female applications for CNICs, whereas female registration was previously disproportionate to their actual numbers, particularly in rural areas (Ghazdar, Citation2011). The increase in female registration means that women are more ‘visible’ to policy maker; in the absence of civil registration, women lose access to basic healthcare, education and civil facilities, which hinders them in exercising their rights and having any agency in decision making (ADB, Citation2014). Since the inception of the program in 2008, 20 million women have registered themselves for CNICs (Sahi, Citation2014). The identification of women as the primary recipient in a household means that the social perception of women is also changing, leading to greater empowerment (Khan & Qutub, Citation2010). Moreover, assessment of the program shows that it has been able to provide monetary relief to the recipient households in terms of food and health expenditures are concerned (Nayab & Farooq, Citation2014; Shehzad, Citation2011).

Despite its relative success, the program is not without its criticism. For example, the program requires continued political support from future governments in order to be effective, which is of some concern given the political nature of the name of the program (Nayab & Farooq, Citation2014). However, the retention of the program and its name even after change in government is a positive sign (Nabi, Citation2013). Additionally, the different rates of disbursement among provinces may also be rooted in political causes, rather than a difference in rates of deserving families. An ongoing concern associated with cash transfers is that the recipients may develop long-term dependence on government assistance, incurring an ongoing expenditure for governments (McCord, Citation2009). The long term objective of cash transfer programs is to hasten the transition out of poverty and two important components are receiving the payments on time each time and knowing the amount of stipend in advance (Slater & Farrington, Citation2009). This allows poor households to plan in advance and make the best use of their resources. Late or missing payments may force the recipient households to take credit from other sources and lose a proportion of their cash transfer in debt payment. BISP disburses its payment in quarterly instalments, which is supported by existing research, which finds that small, regular cash transfers are mostly spent on consumption expenditure but larger, lump sum cash transfers have a greater likelihood of being used for productive activities (Farrington & Slater, 2009).

3.1. Present and future demographics for cash transfer programs

shows that the incidence of poverty at the national poverty line has declined in both urban and rural areas; in the last 18 years, poverty has declined by more than half. Historically, poverty rates have been higher in rural areas, as compared to urban; from 2011 to 2014, rural poverty has been nearly twice as high as urban poverty. To encapsulate the urban-rural disparity, shows the population trends and share of urban population. The table shows that poverty in Pakistan has been declining steadily, particularly post-2002. The incidence of poverty in urban areas has dropped from 50 in 2001–2002 to 18.2 in 2014, while in rural areas it has declined from 70.2 in 2001–2002 to 35.6 in 2004. Urban poverty has declined by 63.6% between 2002 and 2014 while rural poverty has fallen by 50.5%; this shows that the fall in poverty has been greater in urban areas.

Table 2. Incidence of poverty at national poverty line, rural and urban.

The data indicate that poverty in rural areas is relatively higher and 60% of the total population reside in rural areas (). Since 1985, the increase in share of urban population has been gradual as more people emigrate to urban areas in search of better livelihood. Given the historically high rates of poverty in rural areas, one possible intervention is to target the unconditional cash transfers primarily towards rural areas. Another possible model for Pakistan to adopt is that of India, with its National Rural Employment Guarantee Act (NREGA), which provides 100 days of waged labour to volunteer households in the form of unskilled manual labour. In the event that applicants do not receive work within 15 days of application, they may withdraw an unemployment allowance.

Table 3. Share of urban population.

Since 2006, there have been small fluctuations in the unemployment figures for Pakistan (). shows that despite having more male and female earners per household, the poorest are still unable to transition out of poverty. This shows that the poorest households also ‘work poor’, i.e., despite having a greater number of earners per household, their household income still remains lower. The poor often work in poor conditions, with long hours and hazardous conditions and low income and employment stability (Mahmood, Citation2006). This is also substantiated by the data in , which shows relatively low figures for employment in the lowest 20% of the population; UCTs may be expanded to include a component that is targeted towards the unemployed, by providing financial support to those out of jobs for a limited number of days.

Figure 3. Unemployment in Pakistan.

Source: Pakistan Bureau of Statistics

Table 4. Percentage of employed persons and earners per household in upper 20% and lowest 20% of population.

One possible avenue to explore is the introduction of cash stipends for workers that are temporarily unemployed. The benefits of such a program would be: (a) financial support to the poorest in times of greater financial hardship and (b) the time limit of cash transfers ensures that recipients continue to actively seek employment. The NREGA program in India provides wages for 100 days; similarly, Pakistan may adopt a model that provides unemployment benefits for up to 3 months or 90 days, providing job seekers with ample time to search for employment while receiving financial assistance. Furthermore, the incentives can be modified for widows (), handicapped and those living in extreme poverty with a large number of dependents, who fall close to BISP cut-off poverty score but are not current beneficiaries under BISP. This would help avoid the problem of benefits being disbursed to the same recipients under different schemes.

Another example from India is that of its targeted unconditional cash transfers for the elderly and the widows, known as National Social Assistance Program (NSAP). NSAP has proven to outperform India’s Public Distribution System (PDS) which provides subsidised food to the poor, as they are highly targeted and have lower leakages (Dutta, Howes, & Murgai, Citation2010). The data for widows as a portion of the population and the workforce are shown in . shows that a roughly 5% of the labour force comprises of individuals aged 65 years and above.

Table 5. Percentage of widows by rural and urban population and employment status.

Table 6. Workers aged 65+ in the workforce.

The data show that widows account for 2.51% of the total population and form only 0.71% of the labour force; this implies that most widows are not active earners for their families and may rely on the pensions from their deceased husbands for income, as well as other odd jobs. Individuals aged over 65 years form nearly 5% of the labour force. Following India’s model, cash transfers may be provided to the elderly (i.e., 60 years of age) that fall below the national poverty line. The elderly can be further divided into age brackets, such that an 80-year-old would receive higher benefits than a 65-year-old. Similarly, unconditional funds may also be provided to widows that fall below the national poverty line up to the age that they qualify for the pension scheme, such that there is no duplication of recipients.

Unconditional cash transfers may also be provided to disabled persons living below the poverty line. Given the effectiveness of CCTs in targeting health and education outcomes, conditional cash transfers may be introduced for the appropriate demographics. In the past few years, BISP has evolved to include conditional cash transfer components; however, they were scrapped due to lack of proper design and ineffective monitoring. In light of the data presented in the paper, these components can be improved and implemented in such way that reduces poverty at the same time as encouraging human development. One aspect that can be targeted using CCTs is Pakistan’s rapid population growth ().

Table 7. Population demographics.

Since 1955, the population of Pakistan has increased fourfold, with particularly high increases in population in the years 1980–1990 (). After 1990 however, there has been a gradual decline in population growth, as fertility rates have declined. The share of urban population has also increased to 39.5% in 2018, as more and more people migrate to the cities in search of better job opportunities and quality of life. The median age of Pakistan is only 22.7 years; meaning that there are a large number of youth in the country that require education, skills training and livelihoods. This means that there are a large number of dependents in the country, as illustrated by .

Figure 4. Dependency Ratio in Pakistan.

Source: World Development Indicators, World Bank

Moreover, shows that the poorest 20% of households are nearly twice the size of richest 20%, in terms of number of family members. So not only do the poor earn less in terms of income but they also have more mouths to feed, increasing the pressure on the earners of the household.

Table 8. Average household size of upper and lowest 20% population.

In Pakistan, the minimum age of employment is 15 years (Bureau of International Labour Affairs, Citation2017), with highest recorded incidence of child labour in Sindh. The large number of dependents is not only burdensome in terms of income but also gives rise to further issues. For example, a large number of children between the ages of 10 to 14 years are an active part of Pakistan’s labour force, accounting for nearly 20% of the total labour force (); this figure is remarkably high, given the many laws to curb child labour.

Table 9. Underage participants in labour force (10–14 years).

Given the large number of youth in the country (64% population under 30 years of age) and prevalent low literacy rates (), improvement of provision of education and school attendance is of particular importance. The Waseela-e-Taleem initiative of BISP can be expanded to target the issue of growing population, stagnant literacy rates and child labour. An increase in the monthly stipend per child per month may be considered given the importance of the objective; the current stipend of PKR 250 may be too low to provide any real incentive for parents to enrol their children in schools. This point is particularly valid if the wages earned by the children are greater than the compensation provided by the program. Existing research also shows that cash transfers reduce children’s participation in the labour force (De Hoop & Rosati, Citation2014); conditional cash transfers particularly labelled as an education fund have produced desirable results in Mexico (Benhassine, Devoto, Duflo, Dupas, & Pouliquen, Citation2015). Strong incentives for school enrolment not only mitigate the issue of child labour but will also increase the probability of these children transitioning out of poverty, at the same time as increasing human capital. Moreover, the provision of education may include both conventional and vocational education, so that the families may choose a route that best serves their needs, while also equipping the children with necessary skills.

Table 10. Literacy rates in Pakistan, 2005–2014.

Along with high fertility rates and rapid population growth (), Pakistan also has high infant mortality rates compared to its regional counterparts ( and ).

Table 11. Population growth rates.

Table 12. Infant mortality rates.

Pakistan’s performance in improving infant mortality rate (61.2 per 1000 births, as compared to 26.9 in Bangladesh and 32 in India in 2017) has been dismal, compared to its counterparts at the same level of income (). To build upon the idea of increasing the provision of healthcare services and ensuring that the poor have means to those services, regular health check-ups may be incorporated as a condition for funds across all provinces. This method of conditional cash transfers has produced favourable results in terms of health outcomes under the Bolsa Familia in Brazil and Oportunidades in Mexico.

To counter the high fertility rates in the country, discontinued Waseela-e-Sehat may be modified and relaunched to make disbursements of funds to women conditional on regular health checkups and regular vaccinations for children. This is in contrast to the previous working of this program, under which it sought to disburse medical coverage of up to PKR 25,000 per family per annum, targeted towards families that cannot afford medical expenses otherwise. Rather than provide a lump sum coverage, this approach allows for more focus on infant and maternal health.

As evident from the success in Brazil, the adoption of such an initiative would not only improve the provision of preventive healthcare but also lead to better health for mothers and children alike. The maternal health component of the program can also be expanded to include an additional incentive for household with less than four children, for example, which may translate into a consideration for families planning to expand further.

Similarly, income support may be provided for households with handicapped members as well, contingent on their regular health checkups, ensuring that the handicapped members of the society receive adequate care. The introduction of cash transfers for the disabled citizens would help mitigate the disproportionately higher rates of poverty and illiteracy among them and allow them to combat higher rates of unemployment than their able-bodied counterparts (Gooding & Marriot, Citation2009; Mont, Citation2006).

Historically, female participation in the workforce has been very low () and as a result of this gender inequality, Pakistan loses roughly 3.73% of its HDI value due to low female labour force participation, low literacy rates for women and poor access to health (UNDP, 2018). Given that women constitute 49% of the total participation, the female labour force participation rate is particularly worrying.

Table 13. Female participation and unemployment rates.

The data also indicate that unemployment rates are not uniform across different income groups; however, the employment gap between the richest and poorest households has declined in the last 10 years. shows that the gap in employment has decreased from 3.62% in 2004–2005 to 0.9% in 2015–2016. Interestingly, female labour force participation in the poorest 20% households has more than doubled between 2010 and 2016; this trend is particularly encouraging given the expansion of BISP and soft loans for women.

Table 14. Number of employed persons in upper 20% and lowest 20% of population.

splits the labour force of the country into four categories by gender: employers, self-employed, employees and unpaid family members. The self-employed category refers to business owners; 40.9% men and 20.4% women own their businesses A staggering 54.5% of women in the labour force work as unpaid family members. However, this is a considerable improvement from 65% in 2008, when BISP first started.

Table 15. Employment status by gender.

Discontinued in 2015, the Waseela-e-Haq component of BISP disbursed soft loans to women who have graduated from 10-day skills training courses. It may be argued that this time period is too short for any real learning to take place. Moreover, given the low female labour participation rates justify that the loan scheme is targeted towards women. However, expanding the scope of the program to include men from the poorest 10% will also help alleviate poverty. To ensure that the disbursed loans actually create a sustainable source of income for recipients, the program may introduce compulsory business training courses as a condition for eligibility. The use of microfinance not only empowers the poor and reduces poverty (Imoisi & Opara, Citation2014) but also leads to improvement in education and health outcomes (Simanowitz & Walter, Citation2002). However, existing research shows that microfinance is better suited for individuals close to but above the poverty line, while CCTs are more beneficial for those living in extreme poverty (Pantelić, Citation2011).

4. Conclusions

Despite poor economic growth and volatile political conditions, Pakistan has been successful in reducing its poverty statistics and cash transfer programs have aided Pakistan’s efforts in this endeavour. The introduction of BISP has set the foundation for an effective social protection program in Pakistan; the appropriate targeting policies of the program have allowed the program to have the intended impact on its recipients and the introduction of the conditional components in recent years will only help further improve the program. The program would further benefit the poor by introducing specialised components seeking to help the widows and the disabled. UCTs may be better suited for aiding widows and elderly living below the poverty line and provide a financial cushion, especially in old age. They may also be used to provide temporary short-term financial relief to the temporarily unemployed. CCTs can be used to improve health and education outcomes; cash transfers can be made conditional, subject to regular health check-ups for mothers and children and mandatory school attendance to improve these outcomes. Adopting these measures provides a social safety net that also works towards improving illiteracy among youth and infant and maternal health. Furthermore, soft loans and microfinance may also be provided to individuals, contingent on their participation in a mandatory business training course. Not only does it allow for empowerment for women but by including men in the scheme, the loans may provide means of developing sustainable incomes for their households. The end objective of social safety nets is to aid the transition out of poverty for individuals, which cannot be managed through dependence on government assistance alone. Therefore, the case of Pakistan highlights the importance of social safety programs being properly targeted towards their recipient group.

Notes

References

- ADB. (2014). Formal identity and civil registration for women. ADB. Retrieved from https://www.adb.org/sites/default/files/publication/42629/adb-experiences-formal-identity-women.pdf

- Ambler, K., & De Brauw, A. (2017). The impacts of cash transfers on women’s empowerment: Learning from Pakistan’s BISP program. World Bank. Retrieved from http://documents.worldbank.org/curated/en/840271488779553030/pdf/113161-WP-P103160-PUBLIC-SocialProtection-Labor-no-1702.pdf

- Arnold, C., Conway, T., & Greenslade, M. (2011). Cash transfers: A literature review. London: UK Department for International Development.

- Baird, S., Ferreira, F., Özler, B., & Woolcock, M. (2014). Conditional, unconditional and everything in between: A systematic review of the effects of cash transfer programmes on schooling outcomes. Journal of Development Effectiveness, 6(1), 1–43. doi: 10.1080/19439342.2014.890362

- Baird, S., McIntosh, C., & Ozler, B. (2011). Cash or condition? Evidence from a cash transfer experiment. The Quarterly Journal of Economics, 126(4), 1709–1753. doi: 10.1093/qje/qjr032

- Banerjee, A., Hanna, R., Kreindler, G., & Olken, B. (2017). Debunking the stereotype of the lazy welfare recipient: Evidence from cash transfer programs. The World Bank Research Observer, 32(2), 155–184. doi: 10.1093/wbro/lkx002

- Behrman, J., Parker, S., & Todd, P. (2005). Long-term impacts of the Oportunidades conditional cash transfer program on rural youth in Mexico. Ibero America Institute For Econ. Research (IAI) Discussion Papers, (122). Retrieved from http://www2.vwl.wiso.uni-goettingen.de/ibero/working_paper_neu/DB122.pdf

- Benhassine, N., Devoto, F., Duflo, E., Dupas, P., & Pouliquen, V. (2015). Turning a shove into a nudge? A “labeled cash transfer” for education. American Economic Journal: Economic Policy, 7(3), 86–125. doi: 10.1257/pol.20130225

- Bureau of International Labour Affairs. (2017). Findings on the worst forms of child labor. Pakistan. Bureau of International Labour Affairs. Retrieved from https://www.refworld.org/pdfid/5bd05ae50.pdf

- Cecchini, S., & Madariaga, A. (2011). Conditional cash transfer programmes: The recent experience in Latin America and the Caribbean. SSRN Electronic Journal, 95, 208. doi: 10.2139/ssrn.1962666

- Cotto, S. (2018). The effect of cash transfer programs on poverty reduction. Business and Public Administration Studies, 12(1), 1.

- De Hoop, J., & Rosati, F. (2014). Cash transfers and child labor. The World Bank Research Observer, 29(2), 202–234. doi: 10.1093/wbro/lku003

- De Janvry, A., & Sadoulet, E. (2006). When to use a CCT versus a CT approach?. In 3rd International Conference on Conditional Transfers. Istanbul: World Bank.

- de Janvry, A., Finan, F., Sadoulet, E., & Vakis, R. (2006). Can conditional cash transfer programs serve as safety nets in keeping children at school and from working when exposed to shocks? Journal of Development Economics, 79(2), 349–373. doi: 10.1016/j.jdeveco.2006.01.013

- Duflo, E. (2012). Women empowerment and economic development. Journal of Economic Literature, 50(4), 1051–1079. doi: 10.1257/jel.50.4.1051

- Dutta, P., Howes, S., & Murgai, R. (2010). Small but effective: India’s targeted unconditional cash transfers. Economic & Political Weekly, 45(52), 63–70.

- Evans, D., & Popova, A. (2014). Cash transfers and temptation goods: A review of global evidence. Washington: World Bank.

- Fiszbein, A., & Schady, N. (2009). Conditional cash transfers: Reducing present and future poverty. Washington: World Bank. Retrieved from https://siteresources.worldbank.org/INTCCT/Resources/5757608-1234228266004/PRR-CCT_web_noembargo.pdf

- Fosu, A. (2011). Growth, inequality, and poverty reduction in developing countries: Recent global evidence. SSRN Electronic Journal, 43(1), 44–59. doi: 10.2139/ssrn.1813968

- Gentilini, U., Honorati, M., & Yemstov, R. (2014). The state of social safety nets. Washington: World Bank.

- Ghazdar, H. (2011). Social Protection in Pakistan: In the midst of a paradigm shift? Economic and Political Weekly, 46, 59–66.

- Golan, J., Sicular, T., & Umapathi, N. (2017). Unconditional cash transfers in China: Who benefits from the rural minimum living standard guarantee (dibao) program? World Development, 93, 316–336. doi: 10.1016/j.worlddev.2016.12.011

- Gooding, K., & Marriot, A. (2009). Including persons with disabilities in social cash transfer programmes in developing countries. Journal of International Development, 21(5), 685–698. doi: 10.1002/jid.1597

- Handa, S., & Davis, B. (2006). The experience of conditional cash transfers in Latin America and the Caribbean. Development Policy Review, 24(5), 513–536. doi: 10.1111/j.1467-7679.2006.00345.x

- Haushofer, J., & Shapiro, J. (2016). The short-term impact of unconditional cash transfers to the poor: Experimental evidence from Kenya. The Quarterly Journal of Economics, 131(4), 1973–2042. doi: 10.1093/qje/qjw025

- Higgins, S. (2012). The impact of Bolsa Família on poverty: Does Brazil’s conditional cash transfer program have a rural bias?. Journal of Politics and Society, 23(1), 88–125.

- Holmes, R., & Jones, N. (2013). Gender and social protection in the developing world. London: Zed Books.

- Human Development Reports. (2018). Retrieved from http://hdr.undp.org/en/composite/GII

- Hunter, W., & Sugiyama, N. B. (2014). Transforming subjects into citizens: Insights from Brazil’s Bolsa Família. Perspectives on Politics, 12(4), 829–845. doi: 10.1017/S1537592714002151

- Imoisi, A., & Opara, G. (2014). Microfinance and its impact in poverty alleviation in Nigeria: a case study of some microfinance banks in Edo State. American Journal of Humanities and Social Sciences, 2(1), 27–41. doi: 10.11634/232907811402456

- Khan, S., & Qutub, S. (2010). The Benazir income support programme and the Zakat Programme: A political economy analysis. London: Overseas Development Institute.

- Mahmood, M. (2006). Poverty reduction in Pakistan: The strategic impact of macro and employment policies. Geneva: ILo.

- McCord, A. (2009). Political economy and cash transfers in sub-saharan Africa. London: Overseas Development Institute.

- Miller, S. M., & Neanidis, K. C. (2015). Demographic transition and economic welfare: The role of in-cash and in-kind transfers. The Quarterly Review of Economics and Finance, 58, 84–92. doi: 10.1016/j.qref.2015.01.001

- Molyneux, M., Jones, W., & Samuels, F. (2016). Can cash transfer programmes have ‘transformative’ effects? The Journal of Development Studies, 52(8), 1087–1098. doi: 10.1080/00220388.2015.1134781

- Mont, D. (2006). Disability in conditional cash transfer programs: Drawing on experience in lac. In Third International Conference on Conditional Cash Transfers. Istanbul. Retrieved from https://gsdrc.org/document-library/disability-in-conditional-cash-transfer-programs-drawing-on-experience-in-lac/

- Nabi, I. (2013). Two social protection programs in Pakistan. The Lahore Journal of Economics, 18(Special Edition), 283–304. doi: 10.35536/lje.2013.v18.isp.a1urea

- Nayab, D., & Farooq, S. (2014). Effectiveness of cash transfer programmes for household welfare in Pakistan: The case of the Benazir income support programme. The Pakistan Development Review, 53(2), 145–174. doi: 10.30541/v53i2pp.145-174

- Pantelić, A. (2011). A comparative analysis of microfinance and conditional cash transfers in Latin America. Development in Practice, 21(6), 790–805. doi: 10.1080/09614524.2011.582083

- Ravallion, M. (2001). Growth, inequality and poverty: Looking beyond averages. World Development, 29(11), 1803–1815. doi: 10.1016/S0305-750X(01)00072-9

- Rawlings, L., & Rubio, G. (2005). Evaluating the impact of conditional cash transfer programs. The World Bank Research Observer, 20(1), 29–55. doi: 10.1093/wbro/lki001

- Sahi, A. (2014). The power of cash transfer schemes. The News on Sunday. Retrieved from http://tns.thenews.com.pk/power-cash-transfer-schemes/

- Schady, N., & Araujo, M. C. (2006). Cash transfers, conditions, school enrollment, and child work: Evidence from a randomized experiment in Ecuador (Policy Research Working Paper Series No. 3930). Washington: The World Bank.

- Shehzad, I. (2011). Benazir income support programme (BISP) and its impact on women’s empowerment. SAARC Journal of Human Resource Development, 7(1), 71–81.

- Simanowitz, A., & Walter, A. (2002). Ensuring Impact: Reaching the Poorest While Building Financially Self-Sufficient Institutions, and Showing Improvement in the Lives of the Poorest Families: Summary of Article Appearing in Pathways O. Occasional Papers 23745, University of Sussex, Imp-Act: Improving the Impact of Microfinance on Poverty: Action Research Program.

- Slater, R., & Farrington, J. (2009). Lump sum cash transfers in developmental and post-emergency contexts: How well have they performed?. London: Overseas Development Institute.

- Slater, R. (2009). Cash transfers: Graduation and growth. London: Overseas Development Institute. Retrieved from https://www.odi.org/sites/odi.org.uk/files/odi-assets/publications-opinion-files/4606.pdf

- Son, H. (2008). Conditional cash transfer programs: An effective tool for poverty alleviation?. Phillipines: Asian Development Bank.

- Tanoli, Q. (2016). Shut down: BISP closes three key ‘pro-poor’ schemes. The Express Tribune. Retrieved from https://tribune.com.pk/story/1137223/shut-bisp-closes-three-key-pro-poor-schemes/

- World Bank. (2009). Conditional cash transfers: Reducing present and future poverty. Washington: The World Bank. Retrieved from http://siteresources.worldbank.org/INTCCT/Resources. 5757608-1234228266004/PRRCCT_web_noembargo.pdf

- World Bank. (2015). The state of social safety nets 2015. Washington: The World Bank. Retrieved from https://openknowledge.worldbank.org/bitstream/handle/10986/22101/9781464805431.pdf

- World Bank. (2017). The state of social safety nets 2017 “Safety nets where needs are greatest”. Washington: The World Bank. Retrieved from http://documents.worldbank.org/curated/en/811281494500586712/pdf/114866-WP-PUBLIC-10-5-2017-10-41-8-ClosingtheGapBrochure.pdf