?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article examines the impacts of the geopolitical risk, global economic policy uncertainty, and oil price shocks on stock prices in Malaysia using factor augmented SVAR approach. The findings show that while geopolitical risk has no significant direct impacts on the overall stock market, its indirect impacts are significant and transmitted through the global economic policy uncertainty and oil shocks channels. Global economic policy uncertainty exerts negative effects on the overall stock market and its impacts are magnified by geopolitical risk. Oil related shocks exhibit asymmetric effects on both the aggregated and sectoral stock price. The impacts of oil demand shock on stock price are amplified by global economic uncertainty factor whereas oil supply shocks impacts are amplified by the geopolitical risk factor. At sectoral level, the impacts of all the global shocks vary across different sectors and time. The overall findings imply that global economic policy uncertainty and oil demand shock factors are systematic risk factors that can be employed to forecast stock market returns. The findings also provide implications for policymakers to regulate markets in maintaining financial stability and investors to react to future shocks in these global economic factors with regard to the risks and opportunities.

1. Introduction

The impact of oil price shocks on stock market price and return has been extensively investigated by a large volume of empirical studies which have delivered mixed findings. Numerous studies find negative impacts of positive oil price changes on stock market price and return (for examples, Jones and Kaul, Citation1996; Miller & Ratti, Citation2009; Nandha & Faff, Citation2008; Sadorsky, Citation1999, among others). Several other studies that find positive impacts of oil price shock on stock market price and return include Oberndorfer (Citation2009), Ramos & Veiga (Citation2011), among others. The relationship between oil prices and stock market price and return has delivered mixed results because of structural differences in industry, stock market, and economic positions of the oil world markets (Aloui, Nguyen, & Njeh, Citation2012; Elyasiani, Mansur, & Odusami, Citation2011; Moya-Martínez et al., Citation2014; Narayan & Sharma, Citation2011; Ramos & Veiga, Citation2011). However, in recent years, empirical and theoretical investigations on the relation between oil prices and stock price have been enhanced with the introduction of Kilian’s (Citation2009) three structural oil shocks into the analysis. Kilian and Park (Citation2009) show that the three-underlying oil market structural shocks heterogeneously impact the US stock price. Subsequent empirical studies with similar findings are provided by Apergis and Miller (Citation2009), Broadstock and Filis (Citation2014), Fang and You (Citation2014), Cunado and de Gracia (Citation2014), Kang, Ratti, and Yoon (Citation2015), Wang, Wu, and Yang (Citation2013), Wei and Guo (Citation2017), and Zhu, Su, You, and Ren (Citation2017). These studies also indicate that the impacts of structural oil price shocks vary across different economies and industries.

Numerous studies have shown that structural oil shocks and economic policy uncertainty are interrelated and both can jointly affect stock price or returns (Antonakakis, Chatziantoniou, & Filis, Citation2014; Kang & Ratti, Citation2013a, Citation2013b; Kang, Gracia, et al., Citation2017; Kang, Ratti, et al. Citation2017; You, Guo, Zhu, & Tang, Citation2017; among others). These studies have added new insights in examining the effects of oil prices on stock price and the real economy by taking into consideration the economic policy uncertainty factor. Collectively, the findings indicate that the effects of oil prices on stock market prices and returns are magnified by economic policy uncertainty. The models of Kang, Gracia, et al. (Citation2017) and Kang, Ratti, et al. (Citation2017) built based on the endogenous relation between economic policy uncertainty and oil price shocks show that both oil prices and economic policy uncertainty jointly influence the stock market. Thus, based on the findings of Kang and Ratti (Citation2013b), Kang, Gracia, et al. (Citation2017), and You et al. (Citation2017), the present study infers that oil price shocks and economic policy uncertainty are interconnected and that both variables can influence stock market activities. Given the findings of prior research that the impacts of oil price shocks vary across different sectors, it is conjectured that economic policy uncertainty would also likely to exhibit similar effects.

In addition to oil price shocks and economic policy uncertainty, past studies have established that geopolitical risk is a major driver of global stock market movements. Based on the work of Caldara and Iacoviello (Citation2016), as stated in Apergis, Bonato, Gupta, and Kyei (Citation2017, 2) “… geopolitical risks are believed to affect business cycles and financial markets, with geopolitical risks being often cited by central bankers, financial press, and business investors as one of the determinants of investment decisions”. This statement points to the paramount importance of geopolitical risk in influencing stock price. The studies of Antonakakis, Gupta, Kollias, and Papadamou (Citation2017), Bouri, Demirer, Gupta, and Marfatia (Citation2018) Henriques and Sadorsky (Citation2008), Kesicki (Citation2010), Kollias, Kyrtsou, and Papadamou (Citation2013), and among others, showed that geopolitical events can affect oil prices and stock market. Recently, Caldara and Iacoviello (Citation2016) developed an index for geopolitical risk (GPR, hereafter) in which Caldara and Iacoviello (Citation2016, 4) defines as “the risk associated with wars, terrorist acts, and tensions between states that affect the normal course of domestic politics and international relations”. Additionally, it is also argued geopolitical events and global economic policy are interrelated (Baker, Bloom, & Davis, Citation2016; Held, McGrew, Goldblatt, & Perraton, Citation2000, Knight, Citation2012).

Based on the above discussions, the current study aims to examine the impacts of global shocks as such geopolitical risk, global economic policy uncertainty, and oil shocks on stock price both at aggregated and sectoral levels.1 Although existing studies have investigated on related topics, this study differentiated itself from past studies and contributes to the literature in the following ways. First, to the best of our knowledge, this is the first study that investigates how sectoral stock price in the Malaysian stock market are affected by the impacts of geopolitical risk, global economic policy uncertainty, and structural oil shocks. Prior research has established that these three factors can create movements and volatilities in the global financial markets. Hence, understanding the impacts of these global shocks is important for both investors and policy makers in the contexts of asset pricing, risk management policy formulation and portfolio diversification. So far, no study has examined the impacts of oil shocks in combination with global economy policy uncertainty on the Malaysian stock market and other emerging stock markets. Additionally, the impact of geopolitical risk on sectoral stock price has yet to be explored by prior research. Unlike the study of Broadstock and Filis (Citation2014) which examine only selected sectors, the current study analyses all sectors in the Malaysian stock market for investigating the oil price shocks together with geopolitical risk and global economic policy uncertainty. Second, this study employs the factor-augmented VAR (FAVAR, hereafter) model to capture the effects of external influences on the overall economy. The main advantage of FAVAR is that it extracts information for many related data series into a latent factor which is able to capture the dynamics of a large scale of information (see, Stock & Watson, Citation2005, Citation2016).2 Additionally, by integrating shocks of all the three global risk factors into a VAR model, the current study provides new insights in modelling various global shocks in an economic model. Third, past studies that investigate oil price shocks, global economic policy uncertainty, and geopolitical risk focused mainly on developed and oil importing markets (e.g., Wang et al., Citation2013; Kang & Ratti, Citation2013b, 2015; Kang, Gracia, et al. Citation2017; Kang, Ratti, et al. Citation2017). The current study expands the literature by focusing on Malaysia which is an oil exporting emerging nation. As stated in Badeeb, Lean, and Smyth (Citation2016, 156), according to Energy Information Administration (Citation2016a, Citation2016b), “Malaysia is the second largest oil and natural gas producer in Southeast Asia, and the second-largest exporter of liquefied natural gas globally”. From the year 2009 to 2014, Malaysia's oil revenue and oil production contributed more than 25% of gross domestic products (GDP) in each fiscal year, which had helped the Malaysian economy to maintain its sustainable economic growth. However, in the year 2015, the contribution from oil revenue slightly dropped to 22% due to lower oil price. Thus, any shocks in oil price can have impacts on the Malaysia’s real economy and its financial market. Furthermore, being an oil exporting emerging economy, Malaysia tends to respond strongly to any external shocks such as oil shocks and shocks related to international economic policy uncertainty (Basher & Sadorsky, Citation2006; Sum, Citation2013). By examining Malaysian stock market, the current study extends studies on oil exporting markets such as Kang and Ratti (Citation2013a), Kang, Gracia, et al. (Citation2017), among others. However, unlike Kang, Gracia, et al. (Citation2017), Kang, Ratti, et al. (Citation2017) and You et al. (Citation2017), this study includes geopolitical risk together with global economic policy uncertainty in the structural model because geopolitical factor plays important role in influencing oil price shocks and uncertainty in global economic policy uncertainty. Such consideration combines the three domineering strands3 of the literature into a single empirical study, and also provides a strong basis for modelling VAR models and identifications under open economies setting. Fourth, this study shows that geo political risk shocks have indirect impacts on the Malaysian stock market, hence confirming that geopolitical risk shock transmits through global economic policy uncertainty and oil price shocks. Such findings add new evidence to the existing studies that there is a pass-through effect of geopolitical risk (Antonakakis et al., Citation2017; Apergis et al., Citation2017; Apergis & Apergis, Citation2016; Arin, Ciferri, & Spagnolo, Citation2008; Aslam & Kang, Citation2015; Balcilar, Bonato, Demirer, & Gupta, Citation2018; Bouri et al., Citation2018; Henriques & Sadorsky, Citation2008; Kesicki, Citation2010; Kollias et al., Citation2013). Fifth, this study confirms that global economic policy uncertainty shocks have negative influences on all sectoral stock price, which are consistent with extant studies on global economic policy uncertainty and stock price nexus (Arouri, Rault, & Teulon, Citation2014, 2016; Chang, Chen, Gupta, & Nguyen, Citation2015; Liu, Ye, Ma, & Liu, Citation2017, Sum, Citation2013; Tsai, Citation2017). The findings suggest that global economic policy uncertainty can serve as a predictor of stock price and is a priced risk factor for Malaysian stock performances as it has similar effects throughout the stock market. In addition, we also add the effects of global economic policy uncertainty pass-through oil market shocks towards Malaysian stock market performance (Kang & Ratti, Citation2013b; Kang et al. Citation2015; Kang, Gracia, et al., Citation2017; Kang, Ratti, et al. Citation2017). In doing so, this study shows that the three structural oil shocks have asymmetric effects on both aggregated and disaggregated levels of stock price, thus confirming that the impacts of oil price shocks on oil exporting economies’ stock market and industry performance vary across the nature of the oil price shocks and also across different sectors of the stock market. The findings add new evidence to the Malaysian stock market and oil exporting economies’ stock market, in addition to confirming the findings of numerous studies (see, Apergis & Miller, Citation2009; Broadstock & Filis, Citation2014; Cunado & de Gracia, Citation2014; Fang & You, Citation2014; Kang et al., Citation2015, Kang, Gracia, et al., Citation2017; Kang & Ratti, Citation2013a; Wang et al., Citation2013; Wei & Guo, Citation2017; Zhu et al., Citation2017). In addition, our findings that global economic policy uncertainty shocks have negative influences on all sectoral stock prices provide support for extant studies on economic policy uncertainty and stock market nexus (Arouri et al., Citation2014, Citation2016; Chang et al., Citation2015; Liu et al., Citation2017, Sum, Citation2013; Tsai, Citation2017).

The remaining article is organized as follows. Section 2 reviews the related literature and the section that follows presents the modelling framework with large dataset. Section 4 illustrates and discusses the empirical results. Section 5 provides summary of the results with concluding remarks and policy making implications.

2. Related existing studies

The aim of this study is to examine the effects of oil shocks, global economic policy uncertainty, and geopolitical risk on stock prices. The oil shocks examined include oil supply shocks, oil demand shocks due to global economic activities as well as oil demand shock that are driven by oil specific demand and speculation. That said, the study reviews three main strands of literature on global shocks namely oil price shocks, global economic policy uncertainty, and geopolitical risk which examine the impacts of these global shocks on stock market prices and returns. This study also reviews studies that investigated the effects of macroeconomic factors on stock prices and returns.

The first strand of the literature is related to the impacts of oil price shocks on stock market prices and returns. The relationship between stock price or return and oil price shocks has been investigated extensively (e.g., Apergis & Miller, Citation2009; Cunado & de-Gracia, 2014; Elyasiani, et al., Citation2011; Fang & You, Citation2014; Huang, Masulis, & Stoll, Citation1996; Jones and Kaul, Citation1996; Kilian & Park, Citation2009; Lee, Yang, & Huang, Citation2012; Narayan & Sharma, Citation2011; Sadorsky, Citation1999; Scholtens & Yurtsever, Citation2012; Wei, & Guo Citation2017; You et al., Citation2017, among others). Numerous studies have also examined the impacts of oil price on industry stock price or returns. Lee et al. (Citation2012) analyze the effects of oil price shocks on different sectoral stock indices in the G7 economies. They find that while there are insignificant impacts of oil price shocks on aggregated stock market performances, the impacts on sectoral indices are significant. However, the impacts on sectoral indices vary across sectors and countries. Broadstock & Filis (Citation2014) investigate the impacts of oil price shocks on both aggregated stock market and sectoral returns of the US and China stock markets. They find that the aggregate stock market and industrial sectors in the US respond positively to oil demand shock originated from world economic activity. However, such findings are not observed in the China’s stock market. Caporalea, Alia, and Spagnolo (Citation2015) examine the effects of oil price uncertainty on the stock prices of Chinese stock market focusing on ten sectoral indices. They document that oil supply-side shocks have negative influences on the oil and gas industry and the financial industry. The findings also show that seven sectoral returns namley healthcare, telecommunications, basic materials, consumer goods, industrials, utilities, and technology are all positively affected by oil demand shocks arising from global economic activtiy. Phan, Sharma, and Narayan (Citation2015) shows that oil price changes have significant impacts on stock returns of oil producers, while oil price changes have insignificant impacts on the stock returns of oil consumers’ stocks. Shaeri, Adaoglu, and Katircioglu (Citation2016) finds that the impacts of oil risk exposure are not similar across financial and non-financial subsectors.

The second strand of the literature is related to the impacts of economic policy uncertainty on stock market returns and volatility at aggregated, industry, and firm levels. Antonakakis, Chatziantoniou, and Filis (Citation2013) find that increases in economic policy uncertainty causes US stock returns to decrease. Kang and Ratti (Citation2013b) find that economy policy uncertainty negatively impacts real stock returns, and the impacts are amplified by oil price shocks. Sum (Citation2013) shows that the US economic policy uncertainty has significant negative impact on the stock market returns of the ASEAN nations. Similarly, Arouri et al. (Citation2014) finds that the stock market returns of US, Europe, China and the Gulf Cooperation Council are negativity impacted by economic policy uncertainty, and the effects of economic policy uncertainty are moderated by changes in oil price. Mensi, Hammoudeh, Reboredo, and Nguyen (Citation2014) evidence that foreign policy uncertainty does not affect the stock prices of BRICS economies. Chang et al. (Citation2015) find that economic policy uncertainty in the US and UK results in stock price changes of seven OECD countries, and the economic policy has been affecting international oil prices. Ko and Lee (Citation2015) also find that there is a negative relationship between international economic policy uncertainty and stock returns. Similarly, Arouri, Estay, Rault, and Roubaud (Citation2016) finds that increases in economic policy uncertainty lead to the decline in stock price, but the impacts vary with market volatility. Liu and Zhang (Citation2015) find that increases in economic policy uncertainty causes higher stock market volatility and lower stock price. Similar findings are observed in Liu et al. (Citation2017) and thus the authors suggest that economic policy uncertainty can serve as a predictor of stock price. Tsai (Citation2017) argue that economic policy uncertainty of the world’s major countries is the systemic risk of other stock markets.

The third strand of the literature is related to the impacts of geopolitical risk. Since geopolitical risk index is a newly developed index, it has not been widely explored by researchers. However, there are many studies that investigate the impacts of events such as elections, governmental changes, political upheavals, civil strife, and terrorist attacks on economic and financial performances (Antonakakis et al., Citation2014; Apergis & Apergis, Citation2016; Aslam & Kang, Citation2015, Arin et al., Citation2008; Balcilar et al., Citation2018; Barros & Gil-Alana, Citation2009; Chen & Siems, Citation2004; Chesney, Reshetar, & Karaman, Citation2011; Darkos, 2010; Kollias, Manou, et al., Citation2011; Kollias, Papadamou, et al., Citation2011; Kollias, et al., Citation2013; Lehkonen & Heimonen, Citation2015; Mnasri & Nechi, Citation2016; Wisniewski, Citation2016). Most of these studies have documented that the effects of such events on stock market returns are negative. Recently, using geopolitical index, Caldara and Iacoviello (Citation2016) find that increases in geopolitical risk leads to decline in stock price, suggesting a negative relation between geopolitical risk and stock price. Using the geopolitical risk index of Caldara and Iacoviello (Citation2016), Balicilar et al. (2016) find that while geopolitical risk does not affect stock returns of the BIRCS countries, it does create volatility in stock prices and returns. Employing the geopolitical risk index, Apergis et al. (Citation2017) find that geopolitical risk is able to predict return volatility in 50% of the stocks of defense companies. Similar findings are observed in the study of Bouri et al. (Citation2018) that geo-political risk index predicts returns and volatility of Islamic equities and bonds.

The fourth strand of the literature is related to the interaction between macro-economic factors and stock price. Numerous studies have shown that economic output has positive effects on stock price and returns (e.g. Hsing & Hsieh, Citation2012; Peiró, Citation2016; Pradhan, Arvin, Hall, & Bahmani, Citation2014, 2015), interest rate has negative effects on stock price and returns (e.g. Peiró, Citation2016; Pradhan et al., Citation2014, Citation2015), and, money supply has positive effects on stock price and returns (e.g. Hsing & Hsieh, Citation2012; Pradhan et al., Citation2014, Citation2015). Additionally, foreign exchange rate also has been shown to have a significant influence on stock prices, returns, and market development depending on the economic structure, institutional setting, and trade orientation (Bilson, Brailsford, & Hooper, Citation2001; Hoque & Yakob, Citation2017; Hsing & Hsieh, Citation2012; Pradhan et al., Citation2014, Citation2015). Focusing on the influence of macroeconomic variable on the Malaysian stock market, Cheah, Yiew, and Ng (Citation2017), Hamidi, Khalid, and Karim (Citation2018) Ibrahim (Citation1999), Ibrahim and Aziz (Citation2003), Ibrahim & Wan Yusoff (2002), and Janor, Rahim, Yaacob, and Ibrahim (Citation2010) among others evidenced that real output, interest rate, money supply, and exchange rate affect stock price and return. Therefore, this strand of the literature suggests that macroeconomic factors should be incorporated into stock valuation models as stock market interacts with macroeconomic factors.

The presented literature shows that apart from the effects of oil shocks price, the effects of global political risk on sectoral stock prices have not been investigated. In addition, the effects of global economic policy uncertainties on sectoral stock price have also yet to be explored. Therefore, in this study, we examine the effects of oil shocks, global economic policy uncertainties and global political risk on aggregated stock market and sectoral stock prices, after controlling for the effects of macroeconomic factors, such as industrial production, interest rate, money supply, and exchange rate.

3. Empirical modelling framework

Bernanke, Boivin, and Eliasz (Citation2005) has introduced factor-augmented VAR (FAVAR, hereafter) model for capturing macro-economic response to policy shocks in rich data environment. Stock and Watson (Citation2005) included structural dynamic factor model into the FAVAR model, and refer to it as structural FAVAR or popularly known as FA-SVAR. This approach captures the dynamics of identified factors from a large set of data series representing the underlying information. In extant studies, FAVAR is modeled using two blocks such as foreign or external block and also domestic block for investigating the foreign or external impacts on real economy shocks (e.g., Benkovskis, Bessonovs, Feldkircher, & Wörz, Citation2011; Charnavoki and Dolado, Citation2014; Mumtaz & Surico, Citation2009; Ratti & Vespignani, Citation2016). Aastveit (Citation2014) and Aastveit et al. Aastveit, Bjørnland, and ThorsrudAastveit, Bjørnland, and Thorsrud (2015) modeled FAVAR using oil block and macro-economic block where oil related variables are observed factors and macro-economic factors are principal component-based latent variables.

Similar to Aastveit (Citation2014) and Aastveit et al. (Citation2015), the FA-SVAR model employed in this study represents a combination of both observed and unobserved variables.4 In the current study the model is built with global block and domestic block. The global block consists of geopolitical risk (GRP), global economic policy uncertainty (GEPU) and three structural oil shocks. The three structural oil shocks are oil supply shocks (WOP), oil shock due to global demand (GDA), and oil shock driven by oil specific demand (REA). The observable factors are GRP, GEPU and two structural oil shocks namely WOP and GDA. The aims of this study are to examine the impacts of GRP, GEPU, and three oil structural shocks on sectoral stock price of Malaysian stock market. The following vector presents the vector of structural factors.

(1)

(1)

Vector captures economic conditions through some common observed and unobserved factors. This study employs interest rate (INT), money supply (MS), exchange rate (EER), aggregated stock market (SM) as unobservable factors. These latent factors can be observed through principal components analysis using large data series. Industrial production (IPI) factor is an unobservable component which represents economic performance. Oil specific demand shocks (REA) is an unobservable component. In the current model, Kilian’s (Citation2009) oil factors such as oil supply shocks (WOP) and oil price shocks driven by global demand activity (GDA) are employed as observable factors. Other observable factors include geopolitical risk (GPR) and economic policy uncertainty (EPU). The Malaysian stock price of each sector (

) are observable factor in each of the FA-SVAR model. The sectors are construction, consumer products, finance, industrial, mining, plantation, products, property, technology, and trade-service within the stock market. It is conjectured that the dynamics of these factors have impacts on stock market. That said, the dynamics of all the factors are modelled using the FA-SVAR model, therefore, in the following, a VAR model is developed.

(2)

(2)

where

Moreover, Φ(L) stands for a conformable lag polynomial of finite order. denotes the error term, and assumed it to be i.i.d., with zero mean. The system (2) is a reduced form of VAR in

At this point, with standard VAR the difficulty is that the factors represented by the K × 1 vector

which is unobservable. Where, the factors are extracted from a given large dataset,

of dimension M × 1. Therefore, it is assumed that a N × 1 vector

can summarize the state of economy, and in the following the dynamics factor is modelled.

(3)

(3)

Where Λ shows M × (K + 11) matrix of factor loadings and stands for vector of series-specific components. In addition, this study assumes that vector and matrix are weakly correlated or uncorrelated with the common component

and across indicators (see, Bernanke et al., Citation2005; Stock & Watson, Citation2016; for details). However, in contrary to a standard dynamic factor model, this study presumes that some of the factors are observable.

3.1. Factor augmented SVAR (FA-SVAR) setting and estimation

FA-SVAR model is a combination of SVAR model and augmented factors obtained using principal component (PC) estimation. After completing the leading or 1st principal component estimation, a SVAR can be modeled with the estimated leading PC factors in which EquationEq. (1)(1)

(1) considers as standard VAR. This study assumes that the errors identified in EquationEq. (1)

(1)

(1) will be correlated. Therefore, interpretation will not be as structural shocks. In such case, it is needed to consider the moving average representation of Eq. (2) which presented in EquationEq. (4)

(4)

(4)

(4)

(4)

where,

stands for reduced form innovations, and it is assumed that it can be written as linear combinations of the underlying orthogonal structural disturbances (

), i.e.

= S

where S is a ((K + 11) × (K + 11)) contemporaneous matrix. Henceforth, this study assumes that EquationEq. (4)

(4)

(4) can be written as the following Eq. (5).

(5)

(5)

where B(L)S = H(L).

3.1.1. Model identification

The variance-covariance matrix of observed and unobserved elements is represented by the following EquationEq. (6)(6)

(6)

(6)

(6)

The Ω matrix helps to determine whether the SVAR model requires restriction. The restriction on the system is based on This FA-SVAR model has 11 variables. Thus, 55 restrictions should be identified for fulfilling the assumption and definition of just-identified SVAR model.

Following the study of Belke and Rees (Citation2014) and Razmi, Azali, Chin, and Habibullah (Citation2016), this study adopts a non-recursive structure for estimating the FA-SVAR model. A non-recursive structural structure allows for the recognition of optimal identification. In this study, the ordering of system variables is driven by economic theory and follows that of Razmi et al. (Citation2016) and Aastveit (2014). Hence, with exogenous assumptions, structural factors are ordered as shown by EquationEq. (7)(7)

(7) which is derived from Eq. (2).

(7)

(7)

where this FA-SVAR5 has two such as the global block and domestic block.6 The current block separation makes our FA-SVAR model different from the FAVAR model of Aastveit (Citation2014) as his model is devoted to oil block and domestic block. Additionally, unlike FAVAR model of Aastveit (Citation2014), the current FA-SVAR considers small country open-economic system. Rows one to five indicate global block. Thus, geopolitical risk, global economic policy uncertainty, oil supply shocks, oil demand shocks driven by global demand activity, and oil shocks due to oil specific demand are all addressed in row one to row five, respectively. Henceforth,

and

are identified as geopolitical risk shocks, global economic policy uncertainty shocks, oil supply shocks, oil demand shocks driven by global demand activity, and oil shocks respectively.

Rows six to eleven belong to the domestic block as represented by industrial output, interest rate, money supply, exchange rate, aggregated stock market, and sectoral stock price, respectively. Henceforth, shocks of industrial output, interest rate, money supply, exchange rate, aggregated stock market, and sectoral stock price are specified as, respectively, and

More importantly, Malaysian domestic economic factors do not affect the global factors because Malaysian economy belongs to small open economy (see, Razmi et al., Citation2016).

In identifying restriction for the global block, Apergis et al. (Citation2017) consider geopolitical risk exogenous to all other structural variables. This makes sense as geopolitical risk arises from events such as terrorist attacks and wars which are not driven by any other economic factors. Thus, based on the exogeneity assumption, it is conjectured that geopolitical risk is affected by system variables that are not economic related. In addition, following the study of Kang and Ratti (Citation2013a), and Kang, Ratti, et al. (Citation2017), this study identifies restrictions on global economic policy uncertainty, i.e., global economic policy uncertainty is only affected by geopolitical risk contemporaneously. Additionally, following Kilian (Citation2009), Kang and Ratti (Citation2013a), and Kang, Ratti, et al. (Citation2017), this study also identifies that world oil production is not affected contemporaneously by changes in global demand activity and oil specific demand, and that the Malaysian domestic shocks do not affect world oil production in both contemporaneous and delayed manners. Similar to Kilian (Citation2009) and Kang and Ratti (Citation2013a), Kang, Ratti, et al. (Citation2017), this study also identifies that oil specific demand shock does not affect global demand activity in same month of shocks.

For domestic block, several restrictions are drawn from existing studies that are related to the Malaysian economy and policy analysis (Karim & Karim, 2016; Raghavan, Citation2015; Raghavan, Silvapulle, & Athanasopoulos, Citation2012; Razmi et al., Citation2015, Citation2016; Shariq et al., 2016; Zaidi et al., Citation2013, Citation2016; Zaidi & Fisher, Citation2010). As Malaysia is an oil exporting and emerging economy, shocks in global oil factors have impacts on the real sectors and stock market. Industrial production in Malaysia also does not respond contemporaneously to shocks in interest rate and stock market (see, Raghavan, Citation2015; Raghavan et al., Citation2012; Razmi et al., Citation2015, Citation2016; Shariq et al., 2016). Following Kim and Roubini (Citation2000) and Razmi et al. (Citation2016), this study assumes that interest rate does not respond to domestic variable within the same month. Similar to Razmi et al. (Citation2016), this study also assumes that changes in exchange rate and stock market do not affect money supply contemporaneously. Stock market responds to sectoral shock in a delayed nature because there are many sectors within the stock market and thus changes observed in any sector do not affect the stock market immediately.

3.2. Dataset description and diffusion indexes based factors

The employed FA-SVAR model has eleven structural variables which include five observable non-latent variables and six unobservable latent variables. A large dataset comprises 70 monthly time-series variables over the period 2009:01 to 2017:03 is employed for extracting the structural factors (See, Appendix A1 for variable descriptions with data sources and Appendix A2 for detailed description of the time series). Before the extraction of leading principal component, all series are transformed into stationary form as recommended by Stock and Waston (2005) and Ratti and Vespignani (Citation2016). The main advantage of FAVAR is that it compresses many related data series into a single factor which is able to capture the dynamics of a large scale of information (Ratti & Vespignani, Citation2016). The following EquationEq. (8)(8)

(8) through (13) are employed for extracting leading principal component indexes from many time series. These principal component indexes are known as structural factor in the VAR model. The approach of factor loading and eigen value based principal components analysis in generating latent variables was employed in Ratti and Vespignani (Citation2016). The variance explained by the first and second principal component for each structural factor is given in . In this study, the normalized factor loading of leading principal component of each factor is considered. The leading principal component of each factor has extracted more than 70% information from many data-series. Therefore, first principal component of each factor is considered in creating latent factor.

(8)

(8)

(9)

(9)

(10)

(10)

(11)

(11)

(12)

(12)

(13)

(13)

where, in EquationEq. (8)

(8)

(8) ,

is a vector containing production index of different sectors. EquationEqs. (9)–(13) present vectors of interest rate, money supply, exchange rate, aggregate stock market, and real oil price, respectively.

Table 1. Variation explained by the first and second principal components for each factor.

4. Empirical result and analysis

4.1. Preliminary analysis

Prior to the extraction of principal component based latent structural factors, all series are transformed into stationary form. Thus, model estimation can be done without performing further unit-root test of principal component based structural factors (see, Ratti & Vespignani, Citation2016). However, this study performs unit root tests for non-latent structural factor (observable factor) using two widely employed tests such as PP and ADF unit root test. present results of unit root test for observable factors. Unit root results using the two tests show that all data series are stationary at level and first difference form. According to Razmi et al. (Citation2016) and Sims, Stock, & Watson (Citation1990), SVAR model should be estimated at level form. In addition, they also said that unit root is not necessary when SVAR is estimated with non-recursive structure. Thus, we believe that SVAR estimation level can capture the true dynamics among factors and unit root related issues do not matter in the estimations.

Table 2A. Unit root test results for global factor.

Table 2B. Unit root test results for sectoral indices.

Furthermore, Razmi et al. (Citation2016) suggest that there are no break-point in Malaysian macro-economic variables starting from 2009 to 2016. As the sample period of this study starts from January 2009, following Razmi et al. (Citation2016), this study also assumes that the Malaysian macro variables do not exhibit break points in their series of observation. That said, this study procceds to FAVAR model estimation without performing structural break testing in the data series.

The order selection criteria of AIC and SIC are employed in selecting the optimal lag for all VAR models’ estimations.7 For all models, the AIC indicates lag seven, while the SIC indicates lag one. As the order selection of SIC shows the smallest lag, this study selects lag one as an optimal lag. Additionally, since the current factor augmented SVAR models are just-identified models, this study does not need to perform over-identification restrictions test. Furthermore, VAR stability tests of the VAR model with inverse root AR polynomial is performed to check for stability in the VAR model. It is shown that roots falls into the unit circle and suggesting that the estimated VAR model fulfils the stationary and stability conditions.8

4.2. Main analysis and discussion

4.2.1. Impacts of global shocks on Malaysian aggregated stock market price

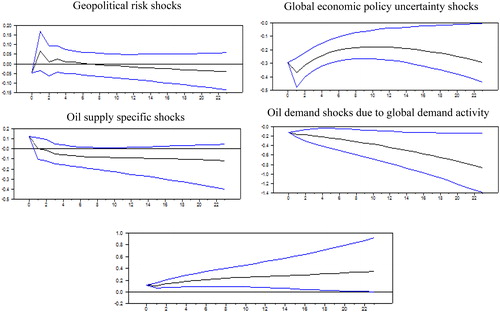

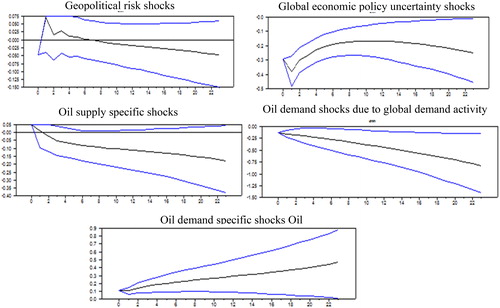

presents the impulse response function showing the impacts of shocks in global factors on the Malaysian aggregated stock market price. Geopolitical risk is found to have insignificant positive impacts in the short run, but negative impacts are observed in the long run. These finding are consistent with those of Balicilar et al. (2016) and Caldara and Iacoviello (Citation2018), while they are contradictory to those of Apergis et al. (Citation2017), Bouri et al. (Citation2018), and many others. Still, based on the findings of Balcilar et al. (Citation2018) and Iacoviello (2018), it can be implied that although geopolitical risks do not affect stock price significantly, it can create volatility in the stock market return. Theoretically speaking, if the domestic economy and stock market remain strong during geopolitical risk shocks, it is possible that the shocks may not influence the stock market performance directly and significantly in the short term. However, global geopolitical tension could create uncertainties and influence investors’ risk behavior through global policy uncertainty and oil shock, thus leading to volatilities in the stock market (see, Balcilar et al., Citation2018; Bouri et al., Citation2018). In support of this assertion, variance decomposition results reported in also suggest that there exists a possibility that the effects of geopolitical risk transmit through global policy uncertainty and oil supply shock given that it has significant power in explaining some of the variances in both global economic policy uncertainty and world oil production shocks factors. These findings suggest that events such as war and terrorist attack bring about changes in economic policy. Similarly, world oil production is affected by geopolitical risks such as sanctions on Iran and Russia, Iraq war, Arab uprising, and OPEC related oil policy. Therefore, it can be concluded that global economic policy uncertainty shocks and oil supply shocks are indeed transmitting mechanisms channels of geopolitical risk shock.

Figure 1. Reponses of Malaysian stock market to one-standard deviation of different global shocks. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

Table 3. Variance decomposition of global factor.

It is shown that global economic policy uncertainty shock has negative impacts on the Malaysian aggregated stock market price in both short and long run. That is, increases in global economic policy uncertainty contribute to reducing aggregated stock market returns in Malaysia. From financial theory point of view, such finding makes sense because policy related uncertainties bring about negative changes in the expected future cash flows due to increases in discount rates and higher investment risk. This in turn leads to lower stock returns in tandem with increases in volatility and thus results in a negative risk-return relation (Bloom, Citation2009; Brogaard & Detzel, Citation2015). In addition, Pástor and Veronesi (Citation2012, Citation2013) theoretically and empirically explained that the relationship between economic policy uncertainty and stock market price is negative. Such theoretical explanation is also empirically true for the effects of international economic policy uncertainty on stock market performance (Arouri et al., Citation2014, Citation2016; Chang et al., Citation2015; Liu et al., Citation2017; Sum, Citation2013; Tsai, Citation2017). Furthermore, as mentioned earlier, geopolitical risk indirectly influences stock market price through its effects on global economic uncertainty. Thus, the finding suggests that shock in geopolitical risk negatively affects the Malaysian aggregated stock market return and that the presence of geopolitical risk shock magnified the impacts of global economic policy uncertainty. Such conclusion is consistent with that of Apergis et al. (Citation2017). Moreover, the variance decomposition results in show that global economic policy uncertainty (GEPU) shocks has power in explaining the variance of the underlying factor of oil price shock. This implies that the impacts of oil price were enhanced or moderated by GEPU. That is, some of the impacts of GEPU shocks were passed on to stock market performances via oil market shocks. Such explanations for the transmission mechanism of GEPU effects are also consistent with those of Kang and Ratti (Citation2013b), Kang et al. (Citation2015) and Kang, Gracia, et al. (Citation2017), Kang, Ratti, et al. (Citation2017).

On Kilian’s (Citation2009) oil market shocks, the finding shows that supply specific oil price shock has negative impacts on oil exporting country’s stock market but with delayed market reaction as there is some lag time in investors’ responses to economic news. The finding could also be due to lower oil prices following the financial crisis of 2009 which negatively affect the economic performance of an oil exporting country. In this case, energy economics theory posited that oil supply shocks could have adverse effects on stock performance of oil exporting country as it causes drop in real oil price which negatively affect the overall economic performance including stock market trading (see, Cunado and de Gracia, Citation2014). In addition, our result is consistent with the findings of numerous past studies that oil supply shocks have significant negative impacts on stock market prices and returns (Apergis & Miller, Citation2009; Cunado and de Gracia, Citation2014; Kilian & Park, Citation2009). However, the result is not in line with those of Wang et al. (Citation2013) and Fang and You (Citation2014) in the context of an oil exporting country’s stock market. Wang et al. (Citation2013) find that oil supply shocks have insignificant effects on stock market activities of oil exporting countries. Similarly, Fang and You (Citation2014) document insignificant effects of oil supply shocks on the Russian stock market. These findings imply that the impacts of oil price shocks are institutional setting dependent. Furthermore, based on the results in and the above discussions, it is observed that the impacts of oil supply shocks are magnified by shocks in geopolitical risks and global economic policy uncertainty.

presents the impulse response functions of Malaysian stock market price to oil market shocks that originate in the oil market due to global demand activity (GDA). The findings indicate that oil shocks which are driven by global demand drag down Malaysian stock market price. This is because increases in oil price caused by higher global demand activity lead to higher production costs which subsequently results in lower profits and stock prices. Since oil price changes are closely related to interest rate and exchange rate factors, increases in oil price can affect stock market performance negatively through increases in interest rate and exchange rate appreciation. Moreover, if the oil price decreases are due to global demand activity, the overall economy can be affected negatively by the decreases in oil revenue, and thus the stock market does not produce positive returns for investors. Therefore, oil price shocks that are due to global demand activity have negative effects on the Malaysian stock market prices and performances. In the context of oil exporting country’s stock market, the finding is consistent with that of Fang and You (Citation2014). However, the finding differs from Fang and You (Citation2014) in that their negative effects findings are shown to be persistent from short to long run. Our finding contradicts that of Wang et al. (Citation2013) as they documented significant positive effects on stock market returns. Furthermore, similar to the impact of oil supply shocks, the impacts of oil shocks driven by global demand activity are also amplified by shocks in global economic policy uncertainty.

Additionally, also presents the impact of demand specific oil shocks on stock market price. The finding indicates that increases in oil price due to oil specific demand lead to the increases in stock market price and returns for an oil exporting country. Theoretically, such finding is as expected since oil price increases due to oil demand bring in additional oil revenue to the oil exporting country, which results in the increase of economic output and performances (Filis & Chatziantoniou, Citation2014). Hence, improved economic performance promotes better stock market performance. Such finding is consistent with Wang et al. (Citation2013) and Fang and You (Citation2014). Both studies document that oil specific demand shocks have positive effects on stock market activities of oil exporting countries. However, the finding is in contrast to the findings of other studies such as Apergis and Miller (Citation2009), Cunado and de Gracia (Citation2014), Kilian and Park (Citation2009), Wei and Guo (Citation2017), and You et al. (Citation2017). This could possibly due to differences in datasets employed and in the countries’ world oil positions. Similar to the impacts of the two previous factors of oil price shocks, the impacts of demand-specific oil price shock also are amplified by the shocks global economic policy uncertainty.

presents the variance decomposition summary of stock market price due to changes in all structural factors. The findings show that the demand-side oil price shocks dominate the supply side oil price shocks in affecting stock price. These results confirm that oil price shocks driven by demand related factors have greater impacts on the stock market of oil exporting countries than other types of oil price shocks and the findings are consistent with those of Wang et al. (Citation2013).

Table 4. Variance decomposition of stock market prices due to structural factors.

4.2.2. Impacts of global shocks on sectoral stock price

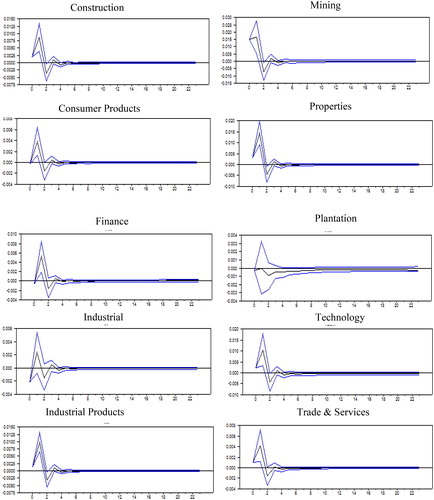

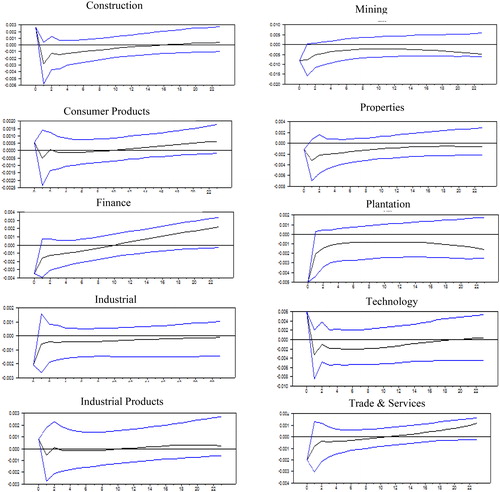

presents the results for the impacts of geopolitical risk (GPR) on sectoral stock price. The findings show that sectors that are positively affected by shocks related to geopolitical risk include construction, consumer products, finance, industrial products, property, technology, and trade & services. The magnitude of the impacts is sector specific and the positive effects are observed in the same month and at a lag of one month and the higher price reflect investors’ demand for risk premium related to geopolitical risk. However, the impacts of geopolitical risk on sectoral stock price become negative at the lag of two months. Such finding suggests that prolonged geopolitical uncertainty discourages stock investments in various sectors.

Figure 2. Sectoral responses to one-standard deviation of geopolitical risk shocks. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

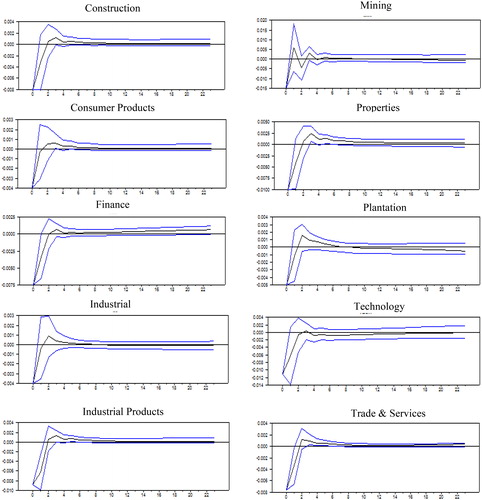

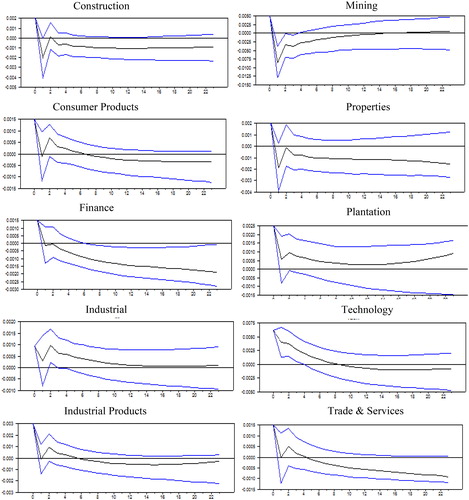

presents the impacts of global economic policy uncertainty (GEPU) on sectoral stock price. The impulse response functions show that sectoral stock price and returns are negatively impacted by global economic policy uncertainty, suggesting that increase in global economic policy uncertainty causes decline in sectoral stock price. The sectoral findings are similar to the results reported based on aggregated stock price and the impacts are sector specific. These findings are consistent with numerous past studies that investigate the relationship between global economic policy uncertainty and stock prices or returns (Arouri et al., Citation2014, Citation2016; Chang et al., Citation2015; Liu et al., Citation2017, Sum, Citation2013; Tsai, Citation2017). Given that uncertainty related to global economic policy has similar impacts on both sectoral and aggregated stock prices, it can be inferred that this global risk factor could well be a systematic risk factor in the Malaysian stock market. Said differently, the global economic policy uncertainty index can potentially serve as a predictor of the Malaysian stock market performance.

Figure 3. Sectoral responses to one-standard deviation of global economic policy uncertainty shocks. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

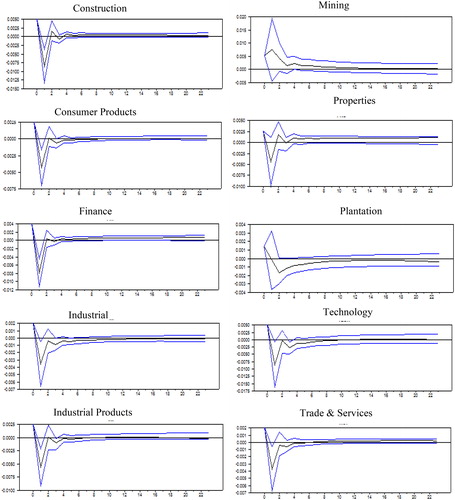

demonstrates the impulse response functions of sectoral stock price to oil supply shocks. The findings show that in the short run, oil supply shocks have negative effects on the prices of all sectors with the exception of the mining sector. However, in the long run, there are several sectors that are positively affected by oil supply shocks and these sectors are construction, properties, finance, industrial products, and trade-services. Additionally, the findings also indicate that the magnitude of the oil supply shocks impacts vary across different sectors of the stock market.

Figure 4. Sectoral responses to one-standard deviation of oil supply specific shocks. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

presents the impulse response functions for sectoral stock price to oil price shocks driven by global demand activity. The results show that oil price shocks due to global demand activity have insignificant effects on the stock prices in all sectors with the exception of construction, mining, plantation, and trade-service sectors. The impacts on stock prices of these four sectors are negative, which are partly consistent with the results reported for aggregated stock market price. These findings indicate that sectoral price of export oriented economies are negatively affected by oil price shocks that are driven by global economic activities.

Figure 5. Sectoral responses to one-standard deviation of oil demand shocks due to global economic activity. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

presents the impulse response functions for sectoral stock prices to oil specific demand shocks. It is shown that the stock prices of five sectors such as construction, industrial, industrial products, plantation, and technology sectors are positively affected by oil specific demand shocks while that of the mining sector is affected negatively within the first month of the shocks. However, after six months of shocks, the direction of the impacts has changed to negative prices for most of the sectors. The finding implies that extended period of oil price increase induced by oil specific demand shock negatively affects sectoral stock prices. This is because as oil prices continue to move up, inflation follows in the same direction which causes interest rate to go up too. As interest rate increases, the cost of fund also increases which hinder investors from investing in the stock market. Furthermore, higher cost of fund also reflects higher required rate of returns for equity investors which corresponds to higher investment risk and hence investors may stay away from stock investment.

Figure 6. Sectoral responses to oil demand specific shocks. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

presents the variance decomposition results for sectoral price attributed to the changes in all structural factors. The table shows that shocks in global factors play important roles in explaining the variation in sectoral prices. Among all the global factors, the global economic policy uncertainty and the world oil production factors are shown to have larger influences than the remaining other global factors.

Table 5. Variance decomposition of sectoral stock prices due to shocks in global factor.

In sum, sectoral stock responses to different global shocks level are found to be heterogenous. The main reason for the heterogeneity of responses is that different sectors have different business activities and thus respond differently to different global shocks level. In addition, sectoral responses to the exposures of world oil market, global political condition and global economic policy also depend on the nature of business and trading partners, which cause the sectoral stocks to react uniquely to the shocks. Further, the findings for heterogeneity of responses of sectoral stock prices to world oil market, global politics and global economic policy support the findings of Elyasiani et al. (Citation2011) as they evidenced that different industries respond differently to oil price shocks.

5. Robustness checking

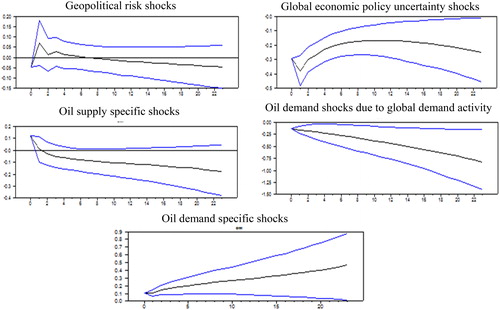

In order to check for the robustness of the empirical results, this study estimates the impulse response functions for the aggregated stock market with different lag and recursive identification, which are presented in and . The estimated responses of stock market with different lag and recursive identification show that all impulse responses of the Malaysian stock market to shocks in geopolitical risk, global economic uncertainty, oil supply, global economic activities, and oil demand are identical, even though the magnitude of the effects are divergent. Thus, it can be concluded that there are no such identifications error in FA-SVAR estimation.

Figure 7: Reponses of Malaysian stock market price to one-standard deviation of different global shocks with different lag (7 lags). The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

Figure 8. Reponses of Malaysian stock market price to one-standard deviation of different global shocks with recursive identification. The confidence bands are based on a 95% significance level and constructed from Monte Carlo simulations based on 2,500 replications.

6. Conclusion and implications

The theories of behavioral finance, financial economics, and equity pricing explain that a factor that affects the overall economic condition can potentially affect stock pricing and returns through its influences on a firm’s cash flows and profits, and on investor’s risk perception. That said, this study explores to what extent shocks induced by three prominent global factors namely, geopolitical risk, global economic policy uncertainty and oil price related factors affect the Malaysian stock prices at both aggregated and sectoral levels. This study employs the Structural Factor-augmented VAR model with 73 monthly time-series variables covering the period from January 2009 to March 2017.

The main findings of the study are as follows. First, the findings show that geopolitical risk has indirect impacts on aggregated stock market prices, and the transmission channels are through global economic policy uncertainty and oil supply shock factors. On sectoral stock prices, geopolitical risk has significant direct and indirect effects. Second, shocks in global economic policy uncertainty are found to be more pervasive as such shocks exert negative effects on stock prices at both aggregated and sectoral levels. Third, oil supply shocks produce negative returns on both the overall and sectoral stock market during the first two month of the shocks. However, at the lag of three months onwards, the sectoral effects are not similar to those of the overall stock market. Fourth, oil demand shocks that are driven by global demand activity lead to the decline in stock price and return for the overall stock market in Malaysia. At sectoral level, similar impacts are observed in the same month and at a lag of one month. Fifth, oil specific demand shock has positive effects on the Malaysian stock market. However, at sectoral level, the impacts remain positive only until the first two months lag. The overall findings of this study imply that investors can formulate investment strategies by using information on global economic policy and oil price information depending on the nature of the shocks. The findings also suggest that global economic policy uncertainty and oil price factors are systematic risk factor for the Malaysian stock performances.

The above discussed empirical results provide several implications to policy makers for regulating financial market to maintain financial stability and to sustain the momentum of stock market performances. Firstly, the negative impacts of geopolitical risk and global economic policy uncertainty on stock market prices and performances suggest that in times of heightened geopolitical risk and global economic policy uncertainty, international investors would frequently exit the economy due to higher investment risk and negative equity returns and invest in stock markets of ‘safe havens’ countries. Given such circumstances, local investors may also follow suit unless they are restricted by capital control regulations. Hence, it is suggested that policy makers provide investment incentives to boost local investors’ participations in the stock market in sustaining the overall economic performance. Secondly, the finding of heterogeneous effects of asymmetric oil price shocks on stock market price provides arbitrage opportunities to policy makers for balancing the negative financial shocks driven by oil price shocks. For example, since demand specific oil shocks usually cause oil price to increase, policy makers can establish a revenue or profit generating oil fund by benchmarking it to certain level of oil price. Some of the money from this oil fund can then be invested in the stock market during supply specific oil price shocks in order to maintain the momentum of stock market performance. This is turn would also attract investors to invest in the stock market during supply specific oil price shocks and change their past perceptions and attitude towards the stock markets of oil exporting economies. Therefore, this study suggests that oil exporting economies can consider establishing an oil fund for the purpose of maintaining financial stability during periods of oil price shocks.

Acknowledgement

This study have received no direct funding

Disclosure statement

There is no conflict.

Notes

1 The study of You et al. (Citation2017) recommends for an empirical study regarding the impacts of oil price shocks and economy policy uncertainty on stock market returns focusing on sectoral returns.

2 The current study is similar to those of Wang et al. (Citation2013), Kang and Ratti (Citation2013b), Kang et al. (Citation2015), Kang, Gracia, et al. (Citation2017), and Wei et al. (2017) among others in terms of employing structural vector autoregressive (VAR) models in analysing the relationship of different oil shocks and stock returns.

3 Namely the effects of oil price shocks on stock market performances, the influences of economic policy uncertainty on stock market performances, and the effects geopolitical risk on stock market performances.

4 Please refer Appendix A1 for definition of the variables.

5 Belke and Rees (Citation2014) have developed and used FA-SVAR with global block and domestic block.

6 Prior studies used block in SVAR for capturing external shocks on domestic variables (see, Aastveit, 2014, 2015; Cunado et al., Citation2015; Cunado & de Gracia, Citation2014; Fang & You, Citation2014; Gupta & Modise, Citation2013; Peersman & Van Robays Citation2009; Van Robays, Citation2012; Vu & Nakata, Citation2017).

7 AIC and SIC estimation for optimal VAR lag will be provided upon request.

8 Results of the VAR stability tests will be provided upon request.

Reference

- Aastveit, K. A. (2014). Oil price shocks in a data-rich environment. Energy Economics, 45, 268–279. doi:10.1016/j.eneco.2014.07.006

- Aastveit, K. A., Bjørnland, H. C., & Thorsrud, L. A. (2015). What drives oil prices? Emerging versus developed economies. Journal of Applied Econometrics, 30(7), 1013–1028. doi:10.1002/jae.2406

- Aloui, C., Nguyen, D. K., & Njeh, H. (2012). Assessing the impacts of oil price fluctuations on stock returns in emerging markets. Economic Modelling, 29(6), 2686–2695. doi:10.1016/j.econmod.2012.08.010

- Apergis, E., & Apergis, N. (2016). The 11/13 Paris terrorist attacks and stock prices: The case of the international defense industry. Finance Research Letters, 17, 186–192. doi:10.1016/j.frl.2016.03.002

- Apergis, N., Bonato, M., Gupta, R., & Kyei, C. (2017). Does geopolitical risks predict stock returns and volatility of leading defense companies? Evidence from a nonparametric approach. Defence and Peace Economics, 29, 684–696. doi:10.1080/10242694.2017.1292097

- Apergis, N., & Miller, S. M. (2009). Do structural oil-market shocks affect stock prices? Energy Economics, 31(4), 569–575. doi:10.1016/j.eneco.2009.03.001

- Antonakakis, N., Gupta, R., Kollias, C., & Papadamou, S. (2017). Geopolitical risks and the oil-stock nexus over 1899–2016. Finance Research Letter (Forthcoming).

- Antonakakis, N., Chatziantoniou, I., & Filis, G. (2013). Dynamic co-movements of stock market returns, implied volatility and policy uncertainty. Economics Letters, 120(1), 87–92. doi:10.1016/j.econlet.2013.04.004

- Antonakakis, N., Chatziantoniou, I., & Filis, G. (2014). Spillovers between oil and stock markets at times of geopolitical unrest and economic turbulence. MPRA Paper 59760, University Library of Munich, Germany. doi:10.1016/j.irfa.2017.01.004

- Aslam, F., & Kang, H. G. (2015). How different terrorist attacks affect stock markets. Defence and Peace Economics, 26(6), 634–648. doi:10.1080/10242694.2013.832555

- Arin, K. P., Ciferri, D., & Spagnolo, N. (2008). The price of terror: The effects of terrorism on stock market returns and volatility. Economics Letters, 101(3), 164–167. doi:10.1016/j.econlet.2008.07.007

- Arouri, M., Estay, C., Rault, C., & Roubaud, D. (2016). Economic policy uncertainty and stock markets: Long-run evidence from the US. Finance Research Letters, 18, 136–141. doi:10.1016/j.frl.2016.04.011

- Arouri, M., Rault, C., & Teulon, F. (2014). Economic policy uncertainty, oil price shocks and GCC stock markets. Economics Bulletin, 34(3), 1822–1834.

- Badeeb, R. A., Lean, H. H., & Smyth, R. (2016). Oil curse and finance–growth nexus in Malaysia: The role of investment. Energy Economics, 57, 154–165. doi:10.1016/j.eneco.2016.04.020

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. doi:10.1093/qje/qjw024

- Balcilar, M., Bonato, M., Demirer, R., & Gupta, R. (2018). Geopolitical risks and stock market dynamics of the BRICS. Economic Systems, 42, 295–306. doi:10.1016/j.ecosys.2017.05.008

- Basher, S., & Sadorsky, P. (2006). Oil price risk and emerging stock markets. Global Finance Journal, 17(2), 224–251. doi:10.1016/j.gfj.2006.04.001

- Barros, C. P., & Gil-Alana, L. A. (2009). Stock market returns and terrorist violence: Evidence from the Basque Country. Applied Economics Letters, 16(15), 1575–1579. doi:10.1080/13504850701578918

- Belke, A., & Rees, A. (2014). Globalisation and monetary policy—A FAVAR analysis for the G7 and the Eurozone. The North American Journal of Economics and Finance, 29, 306–321. doi:10.1016/j.najef.2014.06.003

- Benkovskis, K., Bessonovs, A., Feldkircher, M., & Wörz, J. (2011). The transmission of euro area monetary shocks to the Czech Republic, Poland and Hungary: evidence from a FAVAR model. Focus on European Economic Integration, 3, 8–36.

- Bernanke, B., Boivin, J., & Eliasz, P. S. (2005). Measuring the effects of monetary policy: A factor-augmented vector autoregressive (FAVAR) approach. The Quarterly Journal of Economics, 120 (1), 387–422. doi:10.1162/0033553053327452

- Bilson, C. M., Brailsford, T. J., & Hooper, V. J. (2001). Selecting macroeconomic variables as explanatory factors of emerging stock market returns. Pacific-Basin Finance Journal, 9(4), 401–426. doi:10.1016/S0927-538X(01)00020-8

- Bloom, N. (2009). The impact of uncertainty shocks. econometrica, 77(3), 623–685.

- Bouri, E., Demirer, R., Gupta, R., & Marfatia, H. A. (2018). Geopolitical risks and movements in islamic bond and equity markets: A note. Defence and Peace Economics, 30, 367–379. doi:10.1080/10242694.2018.1424613

- Broadstock, D. C., & Filis, G. (2014). Oil price shocks and stock market returns: New evidence from the United States and China. Journal of International Financial Markets, Institutions and Money, 33, 417–433. doi:10.1016/j.intfin.2014.09.007

- Brogaard, J., & Detzel, A. (2015). The asset-pricing implications of government economic policy uncertainty. Management Science, 61(1), 3–18. doi:10.1287/mnsc.2014.2044

- Caldara, D., & Iacoviello, M. (2016). Measuring Geopolitical Risk. Working Paper. doi:10.17016/IFDP.2018.1222

- Caldara, D., & Iacoviello, M. (2018). Measuring geopolitical risk. FRB International Finance Discussion Paper, (1222). doi:10.17016/IFDP.2018.1222

- Caporalea, G. M., Alia, F. M. & Spagnolo, N., 2015. Oil price uncertainty and sectoral stock returns in China: A time-varying approach. China Economic Review, 34(July), 311–332. doi:10.1016/j.chieco.2014.09.008

- Chang, T., Chen, W. Y., Gupta, R., & Nguyen, D. K. (2015). Are stock prices related to the political uncertainty index in OECD countries? Evidence from the bootstrap panel causality test. Economic Systems, 39(2), 288–300. doi:10.1016/j.ecosys.2014.10.005

- Charnavoki, V., & Dolado, J. J. (2014). The effects of global shocks on small commodity-exporting economies: lessons from Canada. American Economic Journal: Macroeconomics, 6(2), 207–237. doi:10.1257/mac.6.2.207

- Cheah, S.-P., Yiew, T.-H., & Ng, C.-F. (2017). A nonlinear ARDL analysis on the relation between stock price and exchange rate in Malaysia. Economics Bulletin, 37(1), 336–346.

- Chen, A. H., & Siems, T. F. (2004). The effects of terrorism on global capital markets. European Journal of Political Economy, 20(2), 349–366. doi:10.1016/j.ejpoleco.2003.12.005

- Chesney, M., Reshetar, G., & Karaman, M. (2011). The impact of terrorism on financial markets: An empirical study. Journal of Banking & Finance, 35(2), 253–267. doi:10.1016/j.jbankfin.2010.07.026

- Cunado, J., & de Gracia, F. P. (2014). Oil price shocks and stock market returns: Evidence for some European countries. Energy Economics, 42, 365–377. doi:10.1016/j.eneco.2013.10.017

- Cunado, J., Jo, S., & de Gracia, F. P. (2015). Macroeconomic impacts of oil price shocks in Asian economies. Energy Policy, 86, 867–879. doi:10.1016/j.enpol.2015.05.004

- Elyasiani, E., Mansur, I., & Odusami, B. (2011). Oil price shocks and industry stock returns. Energy Economics, 33(5), 966–974. doi:10.1016/j.eneco.2011.03.013

- Energy Information Administration. (2016a). Malaysia Report: International energy data and analysis. United States: Energy Information Administration.

- Energy Information Administration. (2016b). A: Malaysia Oil Market Overview. Energy Information Administration

- Fang, C. R., & You, S. Y. (2014). The impact of oil price shocks on the large emerging countries' stock prices: Evidence from China, India and Russia. International Review of Economics & Finance, 29, 330–338. doi:10.1016/j.iref.2013.06.005

- Filis, G., & Chatziantoniou, I. (2014). Financial and monetary policy responses to oil price shocks: evidence from oil-importing and oil-exporting countries. Review of Quantitative Finance and Accounting, 42(4), 709–729. doi:10.1007/s11156-013-0359-7

- Gupta, R., & Modise, M. P. (2013). Does the source of oil price shocks matter for South African stock returns? A structural VAR approach. Energy Economics, 40, 825–831. doi:10.1016/j.eneco.2013.10.005

- Hamidi, H. N. A., Khalid, N., & Karim, Z. A. (2018). Revisiting relationship between Malaysian stock market index and selected macroeconomic variables using asymmetric cointegration. Jurnal Ekonomi Malaysia, 52(1), 341–350.

- Held, D., McGrew, A., Goldblatt, D., & Perraton, J. (2000). Global transformations: Politics, economics and culture. In Politics at the edge (pp. 14–28). UK: Palgrave Macmillan.

- Henriques, I., & Sadorsky, P. (2008). Oil prices and the stock prices of alternative energy companies. Energy Economics, 30(3), 998–1010. doi:10.1016/j.eneco.2007.11.001

- Hoque, M. E., & Yakob, N. A. (2017). Revisiting stock market development and economic growth nexus: The moderating role of foreign capital inflows and exchange rates. Cogent Economics & Finance, 5(1), 1329975. doi:10.1080/23322039.2017.1329975

- Huang, R., Masulis, R., & Stoll, H. (1996). Energy shocks and financial markets. Journal of Futures Markets, 16(1), 1–27. doi:10.1002/(SICI)1096-9934(199602)16:1<1::AID-FUT1>3.3.CO;2-G

- Hsing, Y., & Hsieh, W. J. (2012). Impacts of macroeconomic variables on the stock market index in Poland: New evidence. Journal of Business Economics and Management, 13(2), 334–343. doi:10.3846/16111699.2011.620133

- Ibrahim, M. (1999). Macroeconomic variables and stock prices in Malaysia: An empirical analysis. Asian Economic Journal, 13(2), 219–231. doi:10.1111/1467-8381.00082

- Ibrahim, M. H., & Aziz, H. (2003). Macroeconomic variables and the Malaysian equity market: A view through rolling subsamples. Journal of Economic Studies, 30(1), 6–27. doi:10.1108/01443580310455241

- Ibrahim, M. H., & Wan Yusoff, S. (2001). Macroeconomic variables, exchange rate and stock price: A Malaysian perspective. International Journal of Economics, Management and Accounting, 9(2), 141–163.

- Janor, H., Rahim, R. A., Yaacob, M. H., & Ibrahim, I. (2010). Stock returns and inflation with supply and demand shocks: Evidence from Malaysia. Journal Ekonomi Malaysia, 44(2010), 3–10.

- Jones, C. M., & Kaul, G. (1996). Oil and the stock markets. The journal of Finance, 51(2), 463–491. doi:10.2307/2329368

- Kang, W., Gracia, F. P., & Ratti, R. A. (2017). Oil price shocks, policy uncertainty, and stock returns of oil and gas corporations. Journal of International Money and Finance, 70, 344–359. Volume doi:10.1016/j.jimonfin.2016.10.003

- Kang, W., & Ratti, R. A. (2013a). Oil shocks, policy uncertainty and stock market return. Journal of International Financial Markets, Institutions and Money, 26, 305–318. doi:10.1016/j.intfin.2013.07.001

- Kang, W., & Ratti, R. A. (2013b). Structural oil price shocks and policy uncertainty. Economic Modelling, 35, 314–319. doi:10.1016/j.econmod.2013.07.025

- Kang, W., Ratti, R. A., & Vespignani, J. L. (2017). Oil price shocks and policy uncertainty: New evidence on the effects of US and non-US oil production. Energy Economics, 66, 536–546.

- Kang, W., Ratti, R. A., & Yoon, K. H. (2015). Time-varying effect of oil market shocks on the stock market. Journal of Banking & Finance, 61, S150–S163. doi:10.1016/j.jbankfin.2015.08.027

- Kesicki, F. (2010). The third oil price surge–What’s different this time? Energy Policy, 38(3), 1596–1606. doi:10.1016/j.enpol.2009.11.044

- Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review, 99(3), 1053–1069. doi:10.1257/aer.99.3.1053

- Kilian, L., & Park, C. (2009). The impact of oil price shocks on the U.S. stock market. International Economic Review, 50(4), 1267–1287. Volume doi:10.1111/j.1468-2354.2009.00568.x

- Kim, S., & Roubini, N. (2000). Exchange rate anomalies in the industrial countries: A solution with a structural VAR approach. Journal of Monetary economics, 45(3), 561–586. doi:10.1016/S0304-3932(00)00010-6

- Kollias, C., Manou, E., Papadamou, S., & Stagiannis, A. (2011). Stock markets and terrorist attacks: Comparative evidence from a large and a small capitalization market. European Journal of Political Economy, 27, S64–S77. doi:10.1016/j.ejpoleco.2011.05.002

- Kollias, C., Kyrtsou, C., & Papadamou, S. (2013). The effects of terrorism and war on the oil price–stock index relationship. Energy Economics, 40, 743–752.

- Kollias, C., Papadamou, S., & Stagiannis, A. (2011). Terrorism and capital markets: The effects of the Madrid and London bomb attacks. International Review of Economics & Finance, 20(4), 532–541. doi:10.1016/j.iref.2010.09.004

- Ko, J. H., & Lee, C. M. (2015). International economic policy uncertainty and stock prices: Wavelet approach. Economics Letters, 134, 118–122. doi:10.1016/j.econlet.2015.07.012

- Knight, F. H. (2012). Risk, uncertainty and profit. Courier Corporation.

- Lee, B. J., Yang, C. W. & Huang, B. N. (2012). Oil price movements and stock markets revisited: A case of sector stock price indexes in the G-7 countries. Energy Economics, 34(5), 1284–1300. doi:10.1016/j.eneco.2012.06.004

- Lehkonen, H., & Heimonen, K. (2015). Democracy, political risks and stock market performance. Journal of International Money and Finance, 59, 77–99. doi:10.1016/j.jimonfin.2015.06.002

- Liu, Z., Ye, Y., Ma, F., & Liu, J. (2017). Can economic policy uncertainty help to forecast the volatility: A multifractal perspective. Physica A: Statistical Mechanics and Its Applications, 482, 181–188. doi:10.1016/j.physa.2017.04.076

- Liu, L., & Zhang, T. (2015). Economic policy uncertainty and stock market volatility. Finance Research Letters, 15, 99–105. doi:10.1016/j.frl.2015.08.009

- Mensi, W., Hammoudeh, S., Reboredo, J. C., & Nguyen, D. K. (2014). Do global factors impact BRICS stock markets? A quantile regression approach. Emerging Markets Review, 19, 1–17. doi:10.1016/j.ememar.2014.04.002

- Mnasri, A., & Nechi, S. (2016). Impact of terrorist attacks on stock market volatility in emerging markets. Emerging Markets Review, 28, 184–202. doi:10.1016/j.ememar.2016.08.002

- Miller, J. I., & Ratti, R. A. (2009). Crude oil and stock markets: Stability, instability, and bubbles. Energy Economics, 31(4), 559–568. pp doi:10.1016/j.eneco.2009.01.009

- Moya-Martínez, P., Ferrer-Lapeña, R., & Escribano-Sotos, F. (2014). Oil price risk in the Spanish stock market: An industry perspective. Economic Modelling, 37, 280–290. doi:10.1016/j.econmod.2013.11.014

- Mumtaz, H., & Surico, P. (2009). The transmission of international shocks: A factor‐augmented VAR approach. Journal of Money, Credit and Banking, 41(s1), 71–100. doi:10.1111/j.1538-4616.2008.00199.x

- Nandha, M., & Faff, R. (2008). Does oil move equity prices? A global view. Energy Economics, 30(3), 986–997. doi:10.1016/j.eneco.2007.09.003

- Narayan, P. K., & Sharma, S. S. (2011). New evidence on oil price and firm returns. Journal of Banking & Finance, 35(12), 3253–3262. doi:10.1016/j.jbankfin.2011.05.010

- Oberndorfer, U. (2009). Energy prices, volatility, and the stock market: Evidence from the Eurozone. Energy Policy, 37(12), 5787–5795. doi:10.1016/j.enpol.2009.08.043

- Pástor, L., & Veronesi, P. (2012). Uncertainty about government policy and stock prices. The journal of Finance, 67(4), 1219–1264. doi:10.1111/j.1540-6261.2012.01746.x

- Pástor, Ľ., & Veronesi, P. (2013). Political uncertainty and risk premia. Journal of Financial Economics, 110(3), 520–545. doi:10.1016/j.jfineco.2013.08.007

- Peersman, G., & Van Robays, I. (2009). Oil and the Euro area economy. Economic Policy, 24(60), 603–651. doi:10.1111/j.1468-0327.2009.00233.x

- Peiró, A. (2016). Stock prices and macroeconomic factors: Some European evidence. International Review of Economics & Finance, 41, 287–294. doi:10.1016/j.iref.2015.08.004

- Phan, D. H. B., Sharma, S. S., & Narayan, P. K. (2015). Oil price and stock returns of consumers and producers of crude oil. Journal of International Financial Markets, Institutions & Money, 34, 245–262. Volume doi:10.1016/j.intfin.2014.11.010

- Pradhan, R. P., Arvin, M. B., & Ghoshray, A. (2015). The dynamics of economic growth, oil prices, stock market depth, and other macroeconomic variables: Evidence from the G-20 countries. International Review of Financial Analysis, 39, 84–95. doi:10.1016/j.irfa.2015.03.006

- Pradhan, R. P., Arvin, M. B., Hall, J. H., & Bahmani, S. (2014). Causal nexus between economic growth, banking sector development, stock market development, and other macroeconomic variables: The case of ASEAN countries. Review of Financial Economics, 23(4), 155–173. doi:10.1016/j.rfe.2014.07.002

- Raghavan, M., Silvapulle, P., & Athanasopoulos, G. (2012). Structural VAR models for Malaysian monetary policy analysis during the pre-and post-1997 Asian crisis periods. Applied Economics, 44(29), 3841–3856. doi:10.1080/00036846.2011.581360

- Raghavan, M. (2015). The macroeconomic effects of oil price shocks on ASEAN-5 economies. Tasmanian School of Business and Economics Discussion Paper Series N2015-10.

- Ramos, S. B., & Veiga, H. (2011). Risk factors in oil and gas industry returns: International evidence. Energy Economics, 33(3), 525–542. doi:10.1016/j.eneco.2010.10.005

- Ratti, R. A., & Vespignani, J. L. (2016). Oil prices and global factor macroeconomic variables. Energy Economics, 59, 198–212. doi:10.1016/j.eneco.2016.06.002