Abstract

Healthcare sector expenditures persistently rise due to various public health, demographic, and socio-cultural reasons. This fact caused repeated calls for reforms of the economic model in the healthcare sector due to increased concern for efficiency. The aim of this paper is the comparison of the Slovenian and Croatian healthcare systems, focusing mainly on the current development stage and the future challenges of the management (cost) accounting systems. The research is mainly interested in the analysis of capabilities of cost tracking according to different criteria and identification of the main constraints in the implementation of a full costing method in Slovenian and Croatian hospitals. The methodology of the literature review and electronic survey was used to assess the practice in both countries. Analysing the data collected from the responses of 26 (100%) Slovenian and 52 (91.22%) Croatian hospital accountants and financial officers, it is possible to claim that Slovenian and Croatian management accounting systems are at a very early development stage. Nevertheless, the analysis reveals several similarities, as well as differences, between the two systems, and it can be concluded that Slovenia has succeeded in making greater progress, especially when observing systematical cost monitoring and implementation of national cost analysis.

1. Introduction

In recent decades, healthcare has seen significant changes in the financing and development of technology (Cardinaels & Soderstrom, Citation2013; Stanimirovic, Citation2015). In 2016, health spending is estimated to have accounted for 9.0% of GDP on average across OECD countries (OECD, Citation2017b). The complex and changing institutional structure of healthcare systems driven by political agendas in the developed economies, is forcing governments to re-think how to fund and reform their healthcare systems (Haslam & Lehman, Citation2006). There were several different ways of reforming public healthcare systems; from increased funding (Haslam & Marriott, Citation2006) to accounting reforms in healthcare institutions (Anessi-Pessina & Cantù, Citation2016; Fiondella, Macchioni, Maffei, & Spanò, Citation2016). One of the most remarkable reforms, started in the 1980s, has been the gradual introduction of funding, based on the division of patients given by diagnosis (Diagnosis Related Group). Under this model, the payment of healthcare providers (hospitals and physicians) depends on the nature of the patient and not on the amount of funds used for treatment (Busse, Geissler, Quentin, & Wiley, Citation2011; Mathauer & Wittenbecher, Citation2013). DRG system is based on cost accounting information, which is synonymous with management accounting system (MAS) (Finkler & Ward, Citation1999; Nistor & Deaconu, Citation2016).

Our research is focused on cost accounting systems within MASs and their characteristics and role in public hospitals in Slovenia and Croatia. Based on the findings of numerous researchers (Anessi-Pessina & Cantù, Citation2016; Demir, Citation2018) considering the trends of public sector transformations in CEEC, it has turned out that accounting as a business function is deficient in all aspects, both in Slovenia and in Croatia (Duhovnik, Citation2007; Lutilsky, Vašiček, & Vašiček, Citation2012).

In accordance with the outlined role of MAS at micro and macro (internal/external) level and its usefulness in the healthcare systems, the paper strives to present the significance of MAS in a socio-economic context and highlight the research needs concerning the various aspects of MAS. The neglected function of cost accounting within MAS in public sector organisations (Jovanović & Dragija, Citation2018; Lutilsky et al., Citation2012; Spekle & Verbeeten, Citation2014) have been perceived as an administrative or even bureaucratic activity. Based on the resource-based view (RBV) in the strategic management theory of public organisations, which observes the interior structure of the organisation, as well as its resources and capabilities (Arbab Kash, Spaulding, Gamm, & Johnson, Citation2014; Bryson, Ackermann, & Eden, Citation2007; Rosenberg Hansen & Ferlie, Citation2016), the paper presents the insight into the development stage of cost accounting systems in Slovenian and Croatian hospitals. The paper is the pioneering attempt to analyse the cost (within management) accounting systems in public hospitals of two post-communist countries (Slovenia and Croatia) from the CEE region, and present new findings in this context. The research provides an in-depth analysis of the structure and functionalities of the cost accounting systems in national environments that have been left to the traditional operation of public administration (PA) and hopefully contributes to the development of the theory in the field. In view of the problem exposed, the article is focused on the following coherently-connected research goals:

Comparison of the healthcare systems in Slovenia and Croatia regarding the accounting systems in hospitals and detection of current challenges in this area;

Analysis of the capability for monitoring expenses in accordance with the source of the cost incurred (direct/indirect) and in accordance with the cost centres/organisational units in Slovenian and Croatian hospitals;

Identification of the main constraints in the implementation of a full costing method in hospitals in both countries.

2. Literature review

In 1980s the traditional Public Administration (PA) paradigm has started to transform into the New Public Management (NPM) approach. Such transformation has brought ideas and tools, which put emphasis on topics like accountability, autonomy of individual managers and public organisations, efficiency, effectiveness, etc. The NPM concept preferred accrual accounting, emphasised the importance of management and even financial accounting (Anessi-Pessina & Cantù, Citation2016; Caperchione, Demirag, & Grossi, Citation2017). While the UK has been the frontrunner, countries in continental Europe, especially southern countries and Central and Eastern European countries (CEEC), followed the trend later (Demir, Citation2018).

2.1. Legitimation view contra instrumental view

The effective MAS is not just certain accounting technique, accounting standard, or accounting IT support. Such conceptual diversity reflects in the fact that the MAS studies are not uniform, neither by methodology nor by results, which happen to be proved also by several theoretical approaches. NPM concept has caused the transformation of the focus on MAS research from technical tool oriented to a more socio context-specific phenomenon (Baldvinsdottir, Mitchell, & Nørreklit, Citation2010; Burns & Scapens, Citation2000; Burns & Vaivio, Citation2001; Malmmose, Citation2015). The conceptual perspective of the MAS literature review divides the literature into two streams; one that depicts accounting as legitimating activities (Lapsley, Citation1994; Pettersen, Citation1995) and another from the instrumental (technical) view, named also ‘accountingisation’ (Osborne & Gaebler, Citation1992; Power & Laughlin, Citation1992). The legitimation view in healthcare organisation addresses distinctive elements, which arise from the organisation’s key healthcare professionals and the nature of the organisation itself. The instrumental view has a more functional and technical understanding of the role of accounting, considering it as the lever for the efficiency achievement (Kurunmaki, Lapsley, & Melia, Citation2003). The technical perspective relies on economic-based theories (Boland & Gordon, Citation1992, p. 148) that see MAS as a set of techniques aimed at providing information in order to bring ‘better’ decision-making, focusing on cost effectiveness and efficiency (Caperchione et al., Citation2017; Fiondella et al., Citation2016). Nevertheless, the development of the technical perspective reflected in cost accounting subsystems seems to form precondition but not sufficient basis for successful and effective MAS (Modell, Citation2001; Osborne, Citation2006). The development and implementation of successful MAS is critically dependent on the balanced and effective combination of a legitimating and instrumental approach (Fiondella et al., Citation2016).

Since operationalisation of the NPM concept started much later in the CEE than in Western European countries, the developing countries and CEEC are much less represented (Duhovnik, Citation2007; Hassan, Citation2005; Naranjo-Gil, Citation2004; van Helden & Uddin, Citation2016) in the literature, especially Slovenia and Croatia (Albreht et al., Citation2009; Dimitrić, Škalamera-Alilović, & Duhovnik, Citation2016; Farkaš, Citation2017; Lutilsky, Žmuk, & Dragija, Citation2016; Vašiček et al., Citation2016). There is a limited scope of the literature focusing mainly on MASs and its characteristics in relation to RBV, although the research of MAS, is more frequent and systematic. Consequently, the systematic review of the literature according to main research streams (legitimation view and instrumental view), authors and general research ideas is presented in . It includes the papers addressing MAS from a wider perspective, focusing also on certain aspects and segments of strategic management and RBV. The authors are well aware of the fact that the presented literature review is certainly not complete, nor is it comprehensive. Nevertheless, it provides a general overview of the research approaches to the implementing of successful MAS, based on RBV in the management of healthcare organisations.

Table 1. Systematic review of the MAS literature.

2.2. Technical view

Based on the extensive review of the literature, we can deduce that existing research only partially addresses the technical view of MASs, as illustrated in the and the text below.

Hassan’s study (Citation2005) of Egyptian hospitals showed that the hospitals offer most health services at a high cost and that some clinics had little profit while others had big losses. A study on a sample of 112 Spanish public hospitals (out of 218) revealed that there is an indirect effect of sophisticated accounting information systems on the performance of public hospitals through a prospector strategy (Naranjo-Gil, Citation2004). Similar research on a sample of 54 Greek public hospitals (out of 132) reveals a number of benefits from the use of accrual cost allocation within sophisticated MAS (Stamatiadis, Citation2009). The revision of the transferring accounting system technologies designed for the private sector to the UK public hospitals, revealed several problems pointing to necessary development of a public sector specific MAS, based on qualitative cost accounting (Ellwood, Citation2009). Additionally, Azoulay et al. (Citation2007) argues that the MAS report should not be used just for decision-making but can be used also by stakeholders in formulating policies and strategic plans and for health service research.

3. Theoretical background

Among all the above-mentioned theoretical concepts and research approaches, our study uses the RBV for the baseline theory, being one of the strategic management theories. These theories generally observe the corporate management from the systems perspective; contingency approach and IT approach (Omalaja & Eruola, Citation2011). RBV argues that the organisation's performance depends on the degree of utilisation of its internal resources. In the past, this theory was predominantly applied in the research of the private sector, where RBV was used to explain the competitive advantages and efficiency of business operations of private companies. Considering that the theory focuses on the analysis of the potentials and the utilisation of internal resources, which are important elements in the public sector as well, it has recently become increasingly used in public sector organisations (healthcare).

Although there is no single generally-accepted definition of organisational resources, according to Butler (Citation2009), the key organisational resources can be typically summarised as:

organisational culture focused on providing the highest quality of service,

knowledge and its exchange within the organisation,

involvement of managers in the improvement of the organisation,

ability of organisational learning.

Under the NPM approach influence, the organisational structures of public sector organisations have transformed from strict hierarchical to more decentralised, flat organisations, based on matrix structures and teams, which rely on knowledge and responsibility transfer. The application of new technologies enables efficient information flow through communication systems, and increases opportunities to control and monitor activities on a strategic level and enable better coordination and cooperation at operational level. The changes have involved raising the awareness of the costs of activities, which resulted in seeking cost-cutting opportunities and effectiveness in the whole sector of public services (Frączkiewicz-Wronka & Szymaniec, Citation2012).

Bearing in mind the scope of preconditions for and requirements of MAS, and particularly the importance of the resources in the healthcare environment, the RBV was considered the most favourable theoretical concept, which we could build our research platform on. The previous studies confirmed that the strategy development is primarily driven by external environmental factors, while on the other side the strategy implementation is influenced by internal resources according to RBV approach (Arbab Kash et al., Citation2014). Accordingly, our research goals are focused on exploring the factors for successful development and adequate resources for implementation of the effective cost accounting system.

4. Methods

4.1. Research design

Leaning on RBV theory, our study employs a single explanatory/exploratory case study design focusing on the strategic resources (internal and external) of the hospitals. RBV sees organisations as a bundle of tangible (ex. buildings, machines, etc.) and intangible (patients, branding, collective culture, etc.) assets, which is engaged within the organisation aiming to succeed in the unpredictable external environment. The complexity of the required resources (human, financial, IT, political, etc.), which conceptually create cost accounting within MAS, are the focus of our research, which has been divided into two stages. In the first stage, the research framework was built on the literature review (regulation, research papers, institution documents, etc.) and analysis, focusing on the detection of challenges in the cost accounting systems of both countries. In the second stage, the research has been upgraded using the survey observations to obtain the second and the third research goals.

The selection of the research method was adapted to the particularities of the research problem (Patton, Citation1990; Yin, Citation2009), considering also the particularities of the research topic and the specifics of the respondents (public hospitals).

The study was based on a survey carried out among accountants and financial officers in Croatian and Slovenian public hospitals. Our findings have been enriched through the intensive process of the survey response collection, including several reminders and personal calls due to which response rate is very high.

4.2. Sample

Due to the small number of public hospitals in both countries, the whole population of public hospitals was chosen (without sampling) for research design. The questionnaires were sent to 26 hospital accounting and financial officers in Slovenia and 57 in Croatia. The respondent share was 100% in Slovenia and 91.22% (52) for Croatia. The survey was conducted in March 2017. The respondents were 97.2% female, aged between 35 and 55 years old, and in the professional position of Head of Accounting and Finance Department in public hospitals. Selection of the respondents was based primarily on their expertise in accounting systems, as well as structural, organisational, and contextual characteristics of the healthcare system, which ensures credibility and validity of their views and recommendations.

4.3. Data collection

Before commencement of the survey process, one pilot survey was carried out in Slovenia, after which the final set of questions was revised in line with the comments and suggestions. All participants were told the purpose and objectives of the study. The surveys provided anonymity and assured confidentiality of the information obtained. The survey consisted of four questions, which were focused on exploring the exact information about cost tracking in the current accounting system, especially focusing on direct and indirect cost allocation and on cost centre allocation. Additionally, the constraints for the implementation of a full costing method were assessed in the last question.

4.4. Data analysis

The RBV’s focus is on competitive advantage, based on the internal resources that an organisation develops or hires (Arbab Kash et al., Citation2014). Joining this growing trend of RBV approach in healthcare organisations, our research has been conceived to include the analysis of two datasets, namely: 1) literature (journal articles, papers, strategy documents, project reports, online resources, etc.); and 2) survey data.

After an extensive review of the literature, we systematically isolated the concept of MAS and potential resources for cost accounting implementation within MASs. These concepts were then operationalised through a set of items, which were administered to Slovenian and Croatian hospitals to examine the characteristics of MASs and cost accounting impact specificities of healthcare systems of these two countries. Relative frequencies of certain response options were analysed, together with average values and variability measures, where applicable.

5. Results

After 1991, both countries declared independence, and the development of once-unique healthcare systems of high-level services went their separate ways (Toth, Citation2003, p. 462). The reform model of several CEEC was very similar. Slovenia has gone through a much slower and much more careful reform process than other similar countries. It resulted in solid functioning of the healthcare system and comprehensive healthcare protection, which was accessible to all the population at that time (Albreht, Citation2010; Istenič, Citation1998; Markota, Svab, Klemencic, & Albreht, Citation1999).

In Croatia, the transition approach towards a market-oriented economy and democratic political system was much more radical. The reforms in the 1990s were consequences and reactions to the old Yugoslavian healthcare system (inefficient decentralisation, huge healthcare expenditures, etc.), to new societal problems (economic problems of transition and war) and to new social circumstances (private health services, etc.).

5.1. Comparison of the healthcare systems in Slovenia and Croatia regarding the accounting systems in hospitals and detection of current challenges in this area

The healthcare systems in Slovenia and Croatia are centralised, and local communities have limited powers. The Ministries of Health are the highest bodies in both countries, spreading powers from policy design to executive and supervisory tasks, whereas local communities are responsible for establishing and maintaining community health centres. Based on the Bismarck healthcare financing model, more than 70% (even 80% in Croatia) of all revenues are collected through compulsory health insurance contributions, while the minor share of financing takes part in state budgets and voluntary health insurance premiums (Albreht et al., Citation2009; Farkaš, Citation2017; Vašiček et al., Citation2016). Public health insurance institutions (Croatian Health Insurance Fund and Health Insurance Institute of Slovenia) are responsible for collecting contributions and allocating funds to hospitals.

The main substantial (not formal) difference in accounting systems of Croatian and Slovenian public hospitals is the accounting principle (basis) for recording business events in their business books. The accounting system in Slovenian public hospitals is based on an accrual accounting platform, bookkeeping additionally on a cash flow basis (Accounting Act), while Croatian public hospitals are using a modified accrual accounting basis (Budget Act). The budgetary accounting in both systems is created on the cash flow principle (Jovanović, Citation2016). The Croatian model of modified accrual principle assumes that revenues are registered during the reporting period in form of inflows of cash and cash equivalents. The expenses are recognised at the moment when the transaction or business event appears regardless of the time of payment. Consequently, hospitals do not account for depreciation of the asset as well as the systematic allocation of the cost over the useful life of its usage (Lutilsky et al., Citation2012).

The Slovenian accounting model provides a more accurate measure of a financial position and a more accurate picture of the assets and liabilities at the end of an accounting period since accrual accounting has been expected to provide more appropriate information for decision makers and lead to better decision making (Anessi-Pessina & Cantù, Citation2016). Consequently, Slovenian public hospitals have a better predisposition to provide more relevant and reliable information about full costs of the programmes, which is needed for making economic decisions at micro and macro level. Eriotis, Stamatiadis, and Vasiliou (Citation2011) and Cohen, Kaimenaki, and Zorgios (Citation2007) have revealed similar results for Greece hospitals and municipalities.

5.2. Analysis of the capability for monitoring expenses in accordance with the source of the cost incurred (direct/indirect), or in accordance with the cost barriers (organisational units) in Slovenian and Croatian hospitals

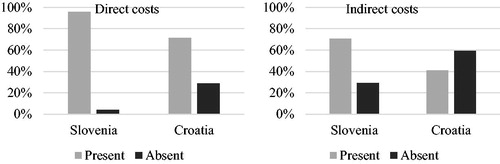

In the second stage (part) part of our empirical work, the analysis of the capacities to track costs by source (direct/indirect) and by cost/organisational unit in hospitals in Slovenia and Croatia, was performed. As it can be noticed from the , a greater number of public hospitals in Slovenia allocate direct costs to cost centres/organisational units, than in public hospitals in Croatia, but the trend remains the same, with direct costs most often allocated in this way in both countries. However, when looking at the indirect cost allocation, there are certain differences between the countries, but those are not so outstanding compared to direct cost allocation. It can be concluded that more than 60% of Slovenian and 40% of Croatian hospitals employ allocation of indirect costs to places of costs/organisational units.

Figure 1. Direct and indirect costs allocation to places of costs or organisational units by country.

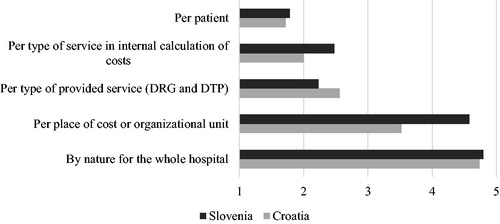

In the second research question, the respondents were asked to report about the possibility to track costs by different categories. Since the ranking scale was from 1 - the least used method to 5 – the most used method, categories 1 and 2 were merged in the category ‘low frequency of use’, while categories 4 and 5 were merged in the ‘high frequency of use’ category ( and ). Due to the small number of units in the observed population, the 3-point scale sufficiently differentiated the frequency of use of the methods. The relative frequencies are presented in and for each category, while descriptive statistics consider frequency of use of the method as measured on a 5-point Likert scale.

Table 2. Frequency of use of costs calculation methods in public hospitals in Slovenia.

Table 3. Frequency of use of costs tracking in public hospitals in Croatia.

shows the results for Slovenian public hospitals. It reveals that almost all Slovenian hospitals very frequently employ a calculation of costs for the whole hospital, as well as a calculation per place of cost or organisational unit. Calculation per type of service is the third most frequently used method of cost calculation, while the calculation of cost per patient is the least used method.

As displayed in , 94% of the Croatian hospitals reported the most frequently employed method. Besides this, more than half of the Croatian hospitals frequently calculate costs per place of cost/organisational unit, while other methods are far less frequently employed. Other methods of cost calculation are rarely used within Croatian hospitals, which proves the assumption that cost accounting systems are at the early development stage, if there is any cost accounting system at all.

presents the differences in costs allocation methods between the countries. It is evident that calculation of costs at hospital level is the most frequently used approach. However, there are two major differences between the countries. Unlike their Croatian counterparts, Slovenian hospitals allocate costs per type of service more frequently, which puts this method ahead of allocation per type of provided service in Slovenia. The second difference concerns the frequency of the per patient cost calculation, which is, still comparatively more frequently used in Slovenia. Nevertheless, this method is the least used in both countries. Combining the results of the first three research questions have expanded the research findings. Because the majority of Slovenian hospitals allocate, not just direct but also indirect, costs to places of costs or organisational units, the accuracy of cost calculations is much more reliable than in Croatian hospitals. Adding the fact that Slovenian hospitals use the full accrual accounting principle enables the conclusion that the exploitation of the resources is much more timely and comprehensively monitored in Slovenian than in Croatian hospitals. However, it does not change the finding that the cost accounting systems in both countries are at an early development stage, considering the fact that not all hospitals allocate direct and indirect costs when calculating costs by different cost methods. Regardless of the cost accounting system used, the direct – indirect (overhead) cost allocation is indispensable part of MAS establishment (Busse et al., Citation2011). The process of MAS establishment seems to be in the domain of economists and accountants, despite the fact that the knowledge provided by the physicians and other staff is the key resource for the quality MASs development (Jacobs, Marcon, & Witt, Citation2004).

Figure 2. Comparison of different costs calculation methods frequency of use in Croatia and Slovenia.

5.3. Identification of the main constraints in the implementation of a full costing method in hospitals in both countries

According to RBV theory, our research goal has been focused on the isolation of those internal resources of the hospitals that would mainly contribute to the development of a full costing method calculation. The analysis isolated human resources, financial resources, IT support, lengthiness of the process, political and legislative support, and the hospital’s management and administration support as factors that obstruct a full cost method implementation. The accountants and financial officers in Slovenian and Croatian hospitals were asked to rate five constraints that were chosen by the authors as the most important ones in the implementation of a full costing method. Constraints were rated on a scale from 1 - being the lowest score and indicating that the observed constraint has very weak impact on the implementation of a full costing method, up to 5 being the highest score, indicating that the observed constraint has very strong impact on the implementation of a full costing method. For the purpose of more meaningful and easier interpretation of the results, scores were re-categorised in such way that scores 1 and 2 were merged into a low importance of a constraint category, while scores 4 and 5 were merged into a high importance of a constraint category ( and ).

Table 4. Perception of constrains in full costing method implementation in public hospitals in Slovenia.

Table 5. Perception of constrains in full costing method implementation in public hospitals in Croatia.

Among the accountants and financial officers in Slovenia (), the perceived overall level of constraints is somewhat more discriminative for the purposes of analysis, with four of the constraints rated as highly important from roughly more than 70% of respondents and with no low grades for these constraints. According to the mean scores, first ranked is IT support, with financial and human resources in second and third place respectively. The least important constrain is political and legislative support, as seen by Slovenian accountants and financial officers.

presents the perception of the constrains evaluation for a full costing method by Croatian accountants and financial officers. It has turned out that perceived importance of all of the constraints has been evaluated as high, since for most of the constraints (with the exception of long duration and complexity of a process), more than 50% percent of the answers are above the theoretical mean value of 3. Between 8% and 15% of all of the respondents marked the importance of the constraints as low, from which it can be assumed that they perceive cost accounting system development as needless in the conditions of budgetary financing. IT support, management and administration support, and financial resources are ranked as the most important constraints standing, while duration and complexity of a process are not seen as important as the previous ones.

All of the constraints in both countries have been evaluated with average scores above 3, which leads to a conclusion that the implementation of full costing methods in public hospital accounting systems in Croatia and Slovenia is perceived as constrained and difficult to implement in general. The major difference in response patterns, visible from , is that the Croatian respondents provided less possibility for discrimination of important constraints from the less important ones, due to the similarity of average scores and response patterns for all of the constraints. In contrast, the Slovenian respondents pronounced the importance of IT support and financial resources, and indicated less importance for the two lowest ranked constraints.

Figure 3. Comparison of constraints perceptions in Croatia and Slovenia.

IT support is perceived as the most important constrain to a full costing method implementation in both countries, followed by the lack of financial resources (). The results are indicative, due to the fact that both factors are interdependent and representatively assign the direction in which future resources allocation should be emphasised. These results indicate that, if the full costing methods are going to be implemented within the Croatian and Slovenian public healthcare systems, the emphasis should be put first on IT development by informing decision makers about the benefits of this cost accounting method, in order to ensure more financial resources. Further supporting this view are the results that accountants and financial officers in both countries do not consider that the process would be long and complex to implement, or not be supported by their political and legislative bodies. All of the above-mentioned facts extend the research findings in a manner that it is more than obvious that both systems suffer from lack of knowledge. The knowledge factor (resource) is one of the most important organisational resources. Butler (Citation2009) operationalises it as the knowledge and its exchange within the organisation and ability of organisational learning, but stressing the involvement of managers in the improvement of the organisation as a very important resource for the organisation’s performance. Referring to knowledge, the humane capital has been exposed as one of the key resources for performance of public organisations (Carmeli and Tishler, 2004), while our research revealed it as one of the most important constrains to a full costing method implementation in both countries.

6. Discussion

A problem solving approach by increasing financial resources in both countries turned out to be insufficient, since hospital healthcare is delivered in a complex financial, physical, clinical and demographic matrix, in which the connection between policy and intended outcomes are not straightforward (Haslam & Marriott, Citation2006). This argument is shifting logic into internal resources strengthening within RBV theory. The RBV approach in public organisations (hospitals) is searching for solutions within resources transformation and allocation, which would guarantee a balanced relationship between the legally defined citizens’ rights to a particular scope and volume of public services on one side, and economic effectiveness of those organisations on the other. Internal resources in an organisation have more significant impact on increased effectiveness than external ones (Rosenberg Hansen & Ferlie, Citation2016).

An accurate cost accounting system based on accrual principle could provide the full costs of the medical treatment and structured overview of the performed services and consumables used (Guthrie, Citation1998). Currently, bottom-up micro-costing is the preferred method in terms of accuracy and managerial relevance in the hospitals and general accounting literature (Vogl, Citation2012). The DRG systems have been developed and implemented to facilitate the allocation of resources internally, as well as to provide a convenient objective and neutral cost containment discourse. It is a great challenge to even adequately define the places of costs or organisational units in healthcare, since it involves a certain level of subjectivity, and physicians’ and administration’s cooperation (Covaleski, Dirsmith, & Michelman, Citation1993; Kurunmaki et al., Citation2003). Considering the resources needed for MAS improvement, based on a cost accounting framework, the focus is not on static resources but instead on integrating, building and reconfiguring resources and competences to deal with major and rapid changes in the environment over time (Rosenberg Hansen & Ferlie, Citation2016).

Central to the assumption of economic rationality contained in much of the health reform literature, particularly that reflecting NPM, is the assumption of the availability of information relating to cost, performance, standards and targets (Marcon & Panozzo, Citation1998; Robinson, Citation1999). This notion includes an effective organisational information system, providing financial and performance information to key decision-makers. Besides physicians, who have been traditionally perceived as the key decision-makers, the managers and nurses are becoming increasingly more engaged in recent times in the implementation of MASs (Griffiths & Hughes, Citation2000). The engagement of the management is even more important, keeping in mind Costello’s (Citation1994) claims that innovation of MAS considerably affects the developmental, transitional and transformational areas of the organisation. However, due to physicians’ considerable power and autonomy, their attitude towards and use of financial and performance information is a critical indicator of whether NPM is anything more than rhetoric in the healthcare setting (Jacobs et al., Citation2004).

It is evident that the public hospitals’ reimbursement financing model, together with supervisory authorities excluding any personal responsibility, have de-stimulated MASs development in both countries. The results of the research indicate that the current MAS models in the Slovenian and Croatian public hospitals are still largely unable to provide fully relevant and reliable information needed for management decision-making at micro level, but also public finance and public health decision-making at macro level. MASs in both countries, with certain differences, are also generally not able to provide complete information, which would enable effective control over the healthcare providers, their performance and costing (Ministry of Health, Citation2017a, Citation2017b, OECD Citation2017a). Due to the accrual-based accounting model of reporting, stricter controls of the funder a smaller number of units (hospitals), better organisation of hospitals and other specific reasons, MASs in Slovenian hospitals have achieved a slightly higher development stage compared to Croatia. Still, both systems are at the very early stage of a full cost accounting system implementation.

Deriving from research results, based on our own survey and literature review (Arbab Kash et al., Citation2014; Burton & Rycroft-Malone, Citation2014; Rosenberg Hansen & Ferlie, Citation2016; Haslam & Marriott, Citation2006; Jacobs et al., Citation2004; Lutilsky et al., Citation2012; Malmmose, Citation2015), we extracted some general conclusions, which are important also from a theoretical contribution perspective. Since public hospitals are floating between economic efficiency and high quality health services, the development of a cost accounting system should be based on analysis of the organisation’s heterogeneous resources, focusing mainly on those that create value on one side and efficiency on the other (Rosenberg Hansen & Ferlie, 2016).

Value creation through different internal resources should engage and empower various organisational stakeholders. This presumes that public hospitals should require a certain degree of autonomy. This self-sufficiency should be largely based on internal knowledge component, which is of great importance for the MASs development, especially in the healthcare sector (Jacobs et al., Citation2004). Furthermore, our results revealed that Slovenian and Croatian cost accounting systems cannot provide basic information about the costs, such as costs per service or costs per patient, not to mention the use of modified accrual accounting in Croatian hospitals. This contribution seems to be valuable for public policy-making and hospitals' management as well. Since the effective utilisation of MAS depends on external factors and internal resources, these outlined mechanisms should be intensively considered in both countries. Besides external factors, such as regulatory framework, financing model, etc., greater emphasis should be put on internal resources such as human resources, IT, business processes, management, etc. The link among resources should be built upon and strengthened by knowledge transfer. To avoid merely ceremonial introduction of MAS, hospitals' management should adopt technically sound MAS and above all learn to fully exploit its potential, and recognise effectiveness and cost containment as real priorities (Macinati & Anessi-Pessina, Citation2014).

7. Conclusion

Additionally, future research efforts in the field should include exhaustive exploration of the effects of MAS on the monitoring of resources, their utilisation, and their resulting transformation into an added value for patients, hospitals and the healthcare system. Ultimate research objectives should probably concentrate on the preparation of operative guidelines for the establishment, introduction and exploitation of MASs at all healthcare providers, and characterisation of its essential features, which could comprehensively support all business functions in the hospitals.

The paper's contribution reflects in attempt to provide an in-depth insight into the underlying issues concerning MASs in both countries and offer some applicable recommendations to hospital managers, as well as regulating authorities for the promotion and more effective implementation of MASs in the healthcare environment. Subject to certain regulatory changes and systemic harmonisation, MAS could considerably contribute to more effective control over the utilisation of public resources, thereby contributing to a more successful solution of public health problems in the Slovenian and Croatian (and probably elsewhere) healthcare systems.

The study brings to light important aspects and issues from this increasingly important area, for evidence-based decision-making in the healthcare system. Limitations of the study are most likely related to the qualitative nature of the research approach, since the implications of (in-)effective cost accounting and MAS could not be observably quantified and comprehensively evaluated in an actual healthcare environment. These issues may raise some questions of principle and therefore research findings can be open to different interpretations to some extent. These unresolved questions, mainly concerning more detailed delimitation of the cost accounting systems and MASs, and actual quantification of their role in the management systems in the healthcare setting, should be the focus of further research and future studies in the field.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Accounting Act (Official Gazette of Republic of Slovenia, NN 23/99, 30/02 - PFA-C and 114/06 - ZUE).

- Albreht, T. (2010). Slovenian health care in transition: Studies on the changes in the Slovenian health system from 1985 until 2010. Ljubljana: Inštitut za Varovanje Zdravja Republike Slovenije.

- Albreht, T., Turk, E., Toth, M., Ceglar, J., Marn, S., Pribaković Brinovec, R., … van Ginneken, E. (2009). Slovenia: Health system review. Health Systems in Transition, 11(3), 1–168.

- Anessi-Pessina, E., & Cantù, E. (2016). Multiple logics and accounting mutations in the Italian National Health Service. Accounting Forum, 40(4), 265–284. doi:10.1016/j.accfor.2016.08.001

- Arbab Kash, B., Spaulding, A., Gamm, L. D., & Johnson, C. E. (2014). Healthcare strategic management and the resource based view. Journal of Strategy and Management, 7(3), 251–264. doi:10.1108/JSMA-06-2013-0040

- Azoulay, A., Doris, M. N., Filion, K., Caron, J., Pilote, L., & Eisenberg, M. J. (2007). The use of the transition cost accounting system in health services research. Cost Effectiveness and Resource Allocation, 5(1), 11. doi:10.1186/1478-7547-5-11

- Baldvinsdottir, G., Mitchell, F., & Nørreklit, H. (2010). Issues in the relationship between theory and practice in management accounting. Management Accounting Research, 21(2), 79–82. doi:10.1016/j.mar.2010.02.006

- Boland, A., & Gordon, M. (1992). Criticising positive accounting theories. Contemporary Accounting Research, 9(1), 142–169. doi:10.1111/j.1911-3846.1992.tb00874.x

- Bryson, J. M., Ackermann, F., & Eden, C. (2007). Putting the resource‐based view of strategy and distinctive competencies to work in public organizations. Public Administration Review, 67(4), 702–717. doi:10.1111/j.1540-6210.2007.00754.x

- Budget Act. (2008). (Croatian Official Gazette, NN 87/08, 136/12, 15/15).

- Burns, J., & Scapens, R. W. (2000). Conceptualizing management accounting change: An institutional framework. Management Accounting Research, 11(1), 3–25. doi:10.1006/mare.1999.0119

- Burns, V., & Vaivio, J. (2001). Management accounting change. Management Accounting Research, 12(4), 389–402. doi:10.1006/mare.2001.0178

- Burton, C. R., & Rycroft-Malone, J. (2014). Resource based view of the firm as a theoretical lens on the organisational consequences of quality improvement. International Journal of Health Policy and Management, 3(3), 113–115. doi:10.15171/ijhpm.2014.74

- Busse, R., Geissler, A., Quentin, W., & Wiley, M. (2011). Diagnosis-related groups in Europe–Moving towards transparency, efficiency and quality in hospitals. New York: McGraw Hill.

- Butler, B. (2009). Successful performance via development and use of dynamic capabilities. Business Renaissance Quarterly, 4(3), 21–37.

- Caperchione, E., Demirag, I., & Grossi, G. (2017). Public sector reform and public private partnership: Overview and research agenda. Accounting Forum, 41(1), 1–7. doi:10.1016/j.accfor.2017.01.003

- Cardinaels, E., & Soderstrom, N. (2013). Managing in a complex world: Accounting and governance choices in hospitals. European Accounting Review, 22(4), 647–684. doi:10.1080/09638180.2013.842493

- Costello, S. J. (1994). Managing change in the workplace. Illinois: Irwin Professional Publishing.

- Cohen, S., Kaimenaki, E., & Zorgios, Y. (2007). Assessing IT as a key success factor for accrual accounting implementation in greek municipalities. Financial Accountability & Management, 23(1), 91–111. doi:10.1111/j.1468-0408.2007.00421.x

- Covaleski, M. A., Dirsmith, M. W., & Michelman, J. E. (1993). An institutional theory perspective on the DRG framework—Case-Mix accounting systems and health care organisations. Accounting, Organisation and Society, 18(1), 65–80. doi:10.1016/0361-3682(93)90025-2

- Demir, F. (2018). Post-NPM and re-centralisation: Current themes in Europe and Turkey. Journal of Contemporary European Studies, 26(2), 149–164. doi:10.1080/14782804.2017.1352494

- Dimitrić, M., Škalamera-Alilović, D., & Duhovnik, M. (2016). Public cost and management accounting system implementation and performance: An integrative approach. International Journal of Public Policy, 12(3/4/5/6), 190–209. doi:10.1504/IJPP.2016.10000556

- Duhovnik, M. (2007). The problems of accounting in a public institution: The case of Slovenia. Financial Theory and Practice, 31(4), 421–445.

- Ellwood, S. (1996). Full-cost pricing rules within the National Health Service internal market- accounting choices and the achievement of productive efficiency. Management Accounting Research, 7(1), 25–51. doi:10.1006/mare.1996.0002

- Ellwood, S. (2009). Accounting for (a) public good: Public healthcare in England. Financial Accountability & Management, 25(4), 411–433. doi:10.1111/j.1468-0408.2009.00485.x

- Eriotis, N., Stamatiadis, F., & Vasiliou, D. (2011). Assessing accrual accounting reform in Greek public hospitals: An empirical investigation. International Journal of Economic Sciences and Applied Research, 4(1), 153–183.

- Farkaš, A. (2017). The analysis of healthcare regulation–Analiza regulacije zdravstva v izbranih državah (Master thesis). University of Ljubljana, Faculty of Administration, Ljubljana.

- Finkler, S. A., & Ward, D. M. (1999). Cost accounting for health care organizations: Concepts and applications. USA: Jones & Bartlett Learning.

- Fiondella, C., Macchioni, R., Maffei, M., & Spanò, R. (2016). Successful changes in management accounting systems: A healthcare case study. Accounting Forum, 40(3), 186–204. doi:10.1016/j.accfor.2016.05.004

- Frączkiewicz-Wronka, A., & Szymaniec, K. (2012). Resource based view and resource dependence theory in decision making process of public organisation-research findings. Management, 16(2), 16–29. doi:10.2478/v10286-012-0052-2

- Griffiths, L., & Hughes, D. (2000). Talking contracts and taking care: Managers and professionals in the British National Health Service internal market. Social Science & Medicine, 51(2), 209–222. doi:10.1016/S0277-9536(99)00448-7

- Guthrie, J. (1998). Application of accrual accounting in the Australian public sector–rhetoric or reality. Financial Accountability and Management, 14(1), 1–19. doi:10.1111/1468-0408.00047

- Haslam, C., & Lehman, G. (2006). Accounting for healthcare: Reform and outcomes. Accounting Forum, 30 (4), 319–323.

- Haslam, C., & Marriott, N. (2006). Accounting for reform: Funding and transformation in the four nation's hospital services. Accounting Forum, 30(4), 389–405.

- Hassan, K. M. (2005). Management Accounting and organisational change: An institutional perspective. Journal of Accounting & Organizational Change, 1(2), 125–140.

- Istenič, M. C. (1998). Privatisation of health care in Slovenia. Croatian Medical Journal, 39(3), 288–297.

- Jacobs, K., Marcon, G., & Witt, D. (2004). Cost and performance information for doctors: An international comparison. Management Accounting Research, 15(3), 337–354. doi:10.1016/j.mar.2004.03.005

- Jovanović, T. (2016). Public sector accounting in Slovenia and Croatia. Hrvatska i Komparativna Javna Uprava: Časopis za Teoriju i Praksu Javne Uprave, 15(4), 791–814.

- Jovanović, T., & Dragija, M. (2018). Application of the accounting information at higher education institutions in Slovenia and Croatia-preparation of public policy framework. International Journal of Public Sector Performance Management, 4(4), 452–466. doi:10.1504/IJPSPM.2018.10015776

- Kurunmaki, L., Lapsley, I., & Melia, K. (2003). Accountingization v. legitimation: A comparative study of the use of accounting information in intensive care. Management Accounting Research, 14(2), 112–139. doi:10.1016/S1044-5005(03)00019-2

- Lapsley, I. (1994). Responsibility accounting revived? Market reforms and budgetary control in health care. Management Accounting Research, 5(3-4), 337–352. doi:10.1006/mare.1994.1021

- Lehtonen, T. (2007). DRG-based prospective pricing and case-mix accounting – Exploring the mechanisms of successful implementation. Management Accounting Research, 18(3), 367–395. doi:10.1016/j.mar.2006.12.002

- Lutilsky, I. D., Vašiček, V., & Vašiček, D. (2012). Cost planning and controlling Croatian public sector. Economic research-Ekonomska Istraživanja, 25(2), 413–434. doi:10.1080/1331677X.2012.11517515

- Lutilsky, I. D., & Žmuk, B., & Dragija, M. (2016). Cost accounting as a possible solution for financial sustainability of Croatian public hospitals. Croatian Economic Survey, 18(2), 5–38. doi:10.15179/ces.18.2.1

- Macinati, M. S., & Anessi-Pessina, E. (2014). Management accounting use and financial performance in public health-care organisations: Evidence from the Italian National Health Service. Health Policy, 117(1), 98–111. doi:10.1016/j.healthpol.2014.03.011

- Malmmose, M. (2015). Management accounting versus medical profession discourse: Hegemony in a public health care debate—A case from Denmark. Critical Perspectives on Accounting, 27, 144–159. doi:10.1016/j.cpa.2014.05.002

- Marcon, G., & Panozzo, F. (1998). Reforming the reform: Changing roles for accounting and management in the Italian health caresector. European Accounting Review, 7(2), 185–208. doi:10.1080/096381898336448

- Markota, M., Svab, I., Klemencic, K. S., & Albreht, T. (1999). Slovenian experience on health care reform. Croatian Medical Journal, 40(2), 190–194.

- Mathauer, I., & Wittenbecher, F. (2013). Hospital payment systems based on diagnosis-related groups: Experiences in low- and middle-income countries. Bulletin of the World Health Organization, 91(10), 746–756. doi:10.2471/BLT.12.115931

- Ministry of Health. (2017a). The analysis of the reasons for losses in Slovenian hospitals. Retrieved from http://www.mz.gov.si/fileadmin/mz.gov.si/pageuploads/NOVICE/27072017_Analiza_primankljajev.pdf

- Ministry of Health. (2017b). The methodology for national cost analysis implementation. Internal material of Ministry of Health.

- Modell, S. (2001). Performance measurement and institutional processes: A study of managerial responses to public sector reform. Management Accounting Research, 12(4), 437–464. doi:10.1006/mare.2001.0164

- Naranjo-Gil, D. (2004). The role of sophisticated accounting system in strategy management. The International Journal of Digital Accounting Research, 4(8), 125–144.

- Nistor, C. S., & Deaconu, A. (2016). Public accounting history in post-communist Romania. Economic research-Ekonomska Istraživanja, 29(1), 623–642. doi:10.1080/1331677X.2016.1193945

- OECD. (2017a). State of health in the EU, Country health profile 2017, Croatia. https://ec.europa.eu/health/state/country_profiles_en

- OECD (2017b). Health at a glance 2017, OECD indicators. https://ec.europa.eu/health/state/country_profiles_en

- Omalaja, M. A., & Eruola, O. A. (2011). Strategic management theory: Concepts, analysis and critiques in relation to corporate competitive advantage from the resource-based philosophy. Economic Analysis, 44(1-2), 59–77.

- Osborne, A. (2006). The new public governance? Public Management Review, 8(3), 377–387. doi:10.1080/14719030600853022

- Osborne, A., & Gaebler, T. (1992). Reinwenting government: How the enterpreneural spirit is transformed in the public sector. Boston: Addison-Wesley.

- Patton, M. (1990). Qualitative evaluation and research methods. Thousand Oaks, CA: Sage Publications.

- Pettersen, I. J. (1995). Budgetary control of hospitals—Ritual rhetorics and rationalized myths? Financial Accountability and Management, 11(3), 207–221. doi:10.1111/j.1468-0408.1995.tb00405.x

- Pettersen, I. J. (2004). From bookkeeping to strategic tools?: A discussion of the reforms in the Nordic hospital sector. Management Accounting Research, 15(3), 319–335. doi:10.1016/S1044-5005(04)00038-1

- Power, M., & Laughlin, M. R. (1992). Critical theory and accounting. In M. Alveson, & H. Wilmott (Eds.), Critical theory and accounting. (pp. 113–135). London: Sage.

- Robinson, R. (1999). Limits to rationality: Economics, economists and priority setting. Health Policy, 49(1-2), 13–26. doi:10.1016/S0168-8510(99)00040-8

- Rosenberg Hansen, J., & Ferlie, E. (2016). Applying strategic management theories in public sector organizations: Developing a Typology. Public Management Review, 18(1), 1–19. doi:10.1080/14719037.2014.957339

- Rules on the single chart of accounts for the budget, budget spending units and other entities under public law, The Official Gazette of the Republic of Slovenia, no. 112/09, 58/10, 104/10, 104/11, 97/12, 108/13, 94/14, 100/15, 84/16, 75/17 in 82/18.

- Spekle, R. F., & Verbeeten, F. H. (2014). The use of performance measurement systems in the public sector: Effects on performance. Management Accounting Research, 25(2), 131–146. doi:10.1016/j.mar.2013.07.004

- Stamatiadis, F. (2009). Governmental accounting reform in the Greek public hospitals: Some preliminary results of its implementation. In 4th Hellenic Observatory PhD Symposium, Athens, Greece pp. 25–26.

- Stanimirovic, D. (2015). A framework for information and communication technology induced transformation of the healthcare business model in Slovenia. Journal of Global Information Technology Management, 18(1), 29–47. doi:10.1080/1097198X.2015.1015826

- Toth, M. (2003). Health, healthcare and health insurance. Ljubljana: Zavod za Zdravstveno Zavarovanje Slovenije.

- van Helden, J., & Uddin, S. (2016). Public sector management accounting in emerging economies: A literature review. Critical Perspectives on Accounting, 41, 34–62. doi:10.1016/j.cpa.2016.01.001

- Vašiček, V., Lutilsky, I. D., Dragija, M., Bertoni, M., De Rossa, B., Grisi, G., & Juroš, L. (2016). Procesni pristup obračunu troškova u sustavu zdravstva. Zagreb: Tim&Pin d.o.o.

- Vogl, M. (2012). Assessing DRG cost accounting with respect to resource allocation and tariff calculation: The case of Germany. Health Economics Review, 2(1), 15. doi:10.1186/2191-1991-2-15

- Yin, R. (2009). Case study research: Design and methods (4th ed.). Thousand Oaks, CA: Sage Publications.