?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article revisits the relationship between the contagion and co-movement of 10 Central and Eastern European (C.E.E.) financial markets in relation to two major Western European capital markets using wavelet-based methodology. Based upon an A.R.D.L. panel model we found that foreign monetary policy, national exchange rate and economic cycle play a key role in both short- and long-term co-movement between capital markets. While a stable economic environment coupled with a strong national currency can reduce the degree of short-term co-movement between capital markets, changes in foreign monetary policy could increase the effect of external shocks. Furthermore, we find that inflation, foreign exchange rate and foreign economic cycle play an important role after longer periods. By ensuring a stable economic environment national authorities can help mitigate the effects of external shocks on national capital markets.

1. Introduction

The debates surrounding the effects of exogenous shocks on a financial market has been a key focus of many studies, especially since the recent financial crisis. In general, investors, risk managers, national regulators and international financial institutions are interested in analysing the contagion and interdependence phenomenon due to adverse implications of exogenous shocks on national financial markets. The economic literature related to capital markets pays close attention in identifying mechanisms through which an exogenous shock propagates between two capital markets. Thus, many studies focus on detecting the interactions among international financial markets, while also identifying determinant factors of contagion and co-movement phenomenon among capital markets.

While many studies try to identify macroeconomic determinants of the contagion phenomenon between markets, we try to test if the impact of macroeconomic factors depends on to the degree of interdependence between two capital markets in the short- or the long-term. Even if we only consider only ‘pure’ contagion or the ‘fundamental’ based contagion we need to acknowledge the role of certain macroeconomic factors on the degree of interdependence between two markets (Dornbusch, Park, & Claessens, Citation2000; Kaminsky & Reinhart, Citation2000). Therefore, national authorities need to investigate both short-term pure contagion manifested via the spillovers of external shocks on national capital markets, but also fundamental based contagion that reveals long-term co-movement between markets. Therefore, by identifying the role of macroeconomic factors in pure contagion, national authorities can adequate measures to reduce and combat the effect of external shocks on national capital markets. On the other hand, in the case of fundamental contagion, testing the role of macroeconomic factors may reveal potential risks that could arise in the long-term which could hinder the growth and development of domestic capital markets.

The aim of this study is to investigate the role of macroeconomic actors on the interdependence and contagion phenomenon between Western European and Central Eastern European (C.E.E.) capital markets. There is a large literature on the interdependence of financial markets (e.g. Gulzar, Kayani, Xiaofeng, Ayub, & Rafique, Citation2019; Marfatia, Citation2017; Newaz & Park, Citation2019), but many of these studies, however, analysed mostly West European markets (Boubaker & Raza, Citation2016; Burzala, Citation2016; Nikkinen, Piljak, & Rothovius, Citation2019). The motivation for choosing these emerging economies is that their financial markets are fully consistent with the world's major financial markets, with strong chances of interdependence and contagion effects on these Eastern European economies. By conducting this study, we are interested in answering the following questions: (1) Is there any contagion effect from West European on East European capital markets?; and (2) What is the effect of the macroeconomic environment on the degree of interdependence between capital markets?

In addition, we believe that by using a modern analysis methodology such as wavelet analysis, we can offer a new perspective of analysis of the interdependence and contagion relationships between Western European and Central Eastern European (C.E.E.) capital markets. By using the wavelet methodology, we want to highlight the manner in which the interdependence between the C.E.E. and West European capital markets evolves over time, as well as to test several macroeconomic determinants, similar to other studies (e.g. Kiviaho, Nikkinen, Piljak, & Rothovius, Citation2014; Tiwari, Mutascu, & Albulescu, Citation2016). Furthermore, we can also offer a broader perspective of the phenomenon in C.E.E. countries because previous studies focus rather on a single country (Hsing, Citation2011) or fewer countries than in our sample (Cevik, Korkmaz, & Cevik, Citation2017; Draženović & Kusanović, Citation2016; Peša & Festić, Citation2014).

Our article contributes to existing articles that try to identify factors that influence the degree of contagion or co-movement between developed and emerging capital markets. One of our major contribution relates to the use of the wavelet methodology in order to identify macroeconomic factors that influence the contagion phenomenon between Western European and C.E.E. capital markets. Furthermore, we contribute to the existing literature that tries to distinguish between the role of the economic environment in reducing both pure and fundamental contagion.

The rest of the article is organised as follows: Section 2 marks the literature review, Section 3 presents the data, Section 4 the methodology, while Section 5 empirical results, and Section 6 concludes.

2. Literature review

Investors seek to increase the degree of diversification of their portfolio by acquiring financial assets worldwide in order to protect themselves against the losses incurred when a national capital market is affected by crisis. However, if the degree of contagion or co-movement between two financial markets is strong, the beneficial effects of international portfolio diversification is reduced when an external shock is transmitted uniformly to another interdependent capital markets (Rua & Nunes, Citation2009; Syllignakis & Kouretas, Citation2011). Therefore, identifying internal factors that could reduce the effect of external shock could increase the efficiency of international portfolio diversification (Ajayi, Mehdian, & Stoica, Citation2018; Thomas, Kashiramka, & Yadav, Citation2019).

Bekaert, Ehrmann, Fratzscher and Mehl (Citation2014) analysed the contagion phenomenon during the recent financial crisis 2008–2009 and finds that the main vectors that determine the magnitude of the contagion phenomenon is related to economic fundamentals, reduced country ratings, budget and/or current account deficits rather than the country of origin. Meanwhile Mobarek et al. (Citation2016) reveals a whole series of characteristics of the economic and social system (economic growth rate, inflation rate, bilateral trade volume, size of the capital market, size of the spread between bonds between two states, culture and religion) from a country that influences contagion between capital markets, especially in times of crisis.

Ever since the first studies of Longin and Solnik (Citation1995), the researchers sought to identify a number of determinants of contagion and co-movement between capital markets. In general, the determinant role of macroeconomic factors in establishing the degree of interdependence between markets is accepted in most studies, while few studies have observed a weak relationship or even neutral relationship (Tiwari et al., Citation2016). In general, four categories of macroeconomic factors can be identified that can influence the degree of interdependence between markets such as: economic cycle (Dumas, Harvey, & Ruiz, Citation2003); inflation rate (Cai, Chou, & Li, Citation2009); monetary policy of country (Syllignakis & Kouretas, Citation2011); the exchange rate power (Kiviaho et al., Citation2014); or the interaction between macroeconomic factors in a bivariate framework (Tiwari et al., Citation2016). In C.E.E. countries there are few studies that deal with this aspect, for example Syllignakis and Kouretas (Citation2011) and Kiviaho et al. (Citation2014).

Kiviaho et al. (Citation2014) notes that in the case of C.E.E. capital markets, a country's macroeconomic fundamentals: monetary policy and exchange are more important in the short-term up to three months, while for periods longer than two years horizons the domestic and foreign monetary policy, the exchange rate are main factors that explains the interdependence between markets. Syllignakis and Kouretas (Citation2011) also reveal the importance of monetary convergence in determining the growth of degree interdependence between markets when testing the contagion phenomenon between C.E.E. capital markets and Germany, Russia and the U.S.

Furthermore, the results of Bekaert et al. (Citation2014) and Mobarek et al. (Citation2016) offer additional insights into the importance of the institutional environment into the development of the capital markets. These results are similar with many studies that reveal the importance of the relationship between legislation and the economy, highlighting the role of legal foundations and the importance of respecting property rights in the functioning and developing of an economy (e.g. Claessens & Yurtoglu, Citation2013, Cuomo, Mallin, & Zattoni, Citation2016; Hopt, Citation2011; Porta et al., Citation1998).

Based upon existing studies, we assume that factors like monetary policy, exchange rate, inflation and economic cycle can influence the degree of co-movement between two capital markets. Furthermore, we believe that general economic environment in a country is able to increase the resilience of the national capital market from the spillover effects and co-movement behaviour.

3. Data and variables

The analysis of the phenomenon of interdependence or contagion between capital markets involves testing the way a capital market evolves in relation to a second market. These raises the question what markets are appropriate in acting as initiators in European Union (E.U.). Tiwari et al. (Citation2016) argues that most developed economy Germany and the most developed capital market, the U.K. are the most influential capital markets in the E.U. Therefore, we will use the German and U.K. markets as initiators in our analysis. Furthermore, testing the co-movement and contagion relationships between the capitals markets included in the analysis is done on a sample of stock indices estimated using the closing price traded in the national currency of each state.

Empirical testing is done on the most representative stock market indices for the capital markets analyzed as follows: SOFIX – Bulgaria, CROBEX – Croatia, PX – Czech Republic, OMXT – Estonia, DAX 30 – Germany, OMXR – Latvia, OMXV – Lithuania, FTSE 100 – Great Britain, WIG – Poland, BET – Romania, SAX – Slovakia and BUX – Hungary. The data source used in the analysis is Datastream and covers the period from 20 October 2000 to 31 December 2016, the longest period for which data is available for all states in our analysis.

Because our capital markets are trading at different times, we will use the closing price in our analysis. In addition, similar to Tiwari et al. (Citation2016) in order to prevent the risk of ‘non-syncronious trading II,’ we will remove from our analysis all non-trading days in all the analyzed capital markets if there were no transactions in a capital market that day. In the end, our sample of data consists of 3,486 distinct daily records for each of the capital markets analysed by us. Furthermore, in the second part we will use monthly data for our indices. In our analysis, we will use indices expressed in national currency as in previous studies such as Rua and Nunes (Citation2009) and Cărăușu et al. (Citation2018), because Mink (Citation2015) demonstrated that testing of market contagion should be done only local currencies in order to exclude the role of the exchange rate.

Testing the degree of contagion between two markets is done with the coherence wavelet analysis and extracting the corresponding indicators for each pair of countries used in the analysis. Later we will use an A.R.D.L. panel model to test if there is a true cointegration between our macroeconomic variables and the degree of interdependence between our capital markets. A full description of the variables used in the analysis is depicted in . Similar to other studies like Kiviaho et al. (Citation2014) and Tiwari et al. (Citation2016) that used wavelet analysis to identify determinant factors for the degree of interdependence between two capital markets we chose as control variables a series of macroeconomic indicators.

Table 1. Variables used in the analysis of the macroeconomic determinants of the interdependence between the C.E.E. markets and Western European capital markets.

We use the Industrial Production Index (IPI) of the initiating country as a proxy for the economic cycle in that state, the Harmonized Consumer Price Index of a State (H.I.C.P.) as a proxy for inflation, the three-month interbank lending rate - proxy for the monetary policy and the Exchange Rate Index – proxy for currency evolution. In our analysis, we preferred to use these macroeconomic variables as opposed to similar indicators due to specific advantages. Thus we use: H.I.C.P. because it is the preferred indicator of inflation in the EU; interbank interest rate because some countries are members of the euro area, thus they are subject to the same monetary policy interest but may have different interbank financing costs; Exchange Rate Index because it includes the importance of the national currency of a state in international and intra-Community trade. The same group of variables was used in previous studies like Kiviaho et al. (Citation2014) and Tiwari et al. (Citation2016).

Because in the second part of our analysis, we will test the influence of macroeconomic factors on the long- and short-term of interdependence between Germany and U.K. and C.E.E. capital markets presents the descriptive statistics of the data used in the analysis. Also, the results of the correlation matrix between our variables is depicted in .

Table 2. Descriptive statistics of the variables used in the analysis.

Table 3. Correlation matrix.

4. Methodology

4.1. Wavelet analysis

The wavelet analysis provides a general framework of analysis for testing the contagion and interdependence phenomenon between two markets. The wavelet methodology offers a whole series of advantages over traditional methods of testing the contagion phenomenon Gençay, Selçuk, and Whitcher (Citation2002) and Aguiar‐Conraria and Soares (Citation2014) present in detail the benefits of using wavelet methodology in time series analysis.

The continuous wavelet transform (C.W.T.), originally developed by Torrence and Compo (Citation1998) as a method of detecting delays and synchronisations between two time series, has gained more and more popularity in recent years as a powerful tool for time series analysis. The C.W.T. transformation decomposes a time series in functions commonly called wavelets or small waves, which contain both frequency and time domain information These small ‘waves’ are the result of translating the wavelet filters onto the initial series, which can be converted to a time function

(translation parameter) and

scale (scale parameter) corresponding to each frequency Rua and Nunes (Citation2009).

(1)

(1)

Gençay et al. (Citation2002) considers that the C.W.T. for any time series x(t), t = 1,….,N can be written as in formula (2):

(2)

(2)

The wavelet coherence analysis involves testing the interactions between two time series X and Y in a bivariate analysis framework. This involves comparing the cross-wavelet spectrum with the result of the spectrum product of each series, which tests the time and the frequency range. Grinsted, Moore, and Jevrejeva (Citation2004) considers that the wavelet coherence between two variables can be determined using formula (3):

(3)

(3)

where:

and

are C.W.T. of two time series, S (.) Is the smoothing operator and s is the wavelet scale.

Previous results of Grinsted et al. (Citation2004) indicated that the most effective wavelet in C.W.T. is the wavelet Morlet because it has a Fourier period almost equal to the wavelet scale used in this analysis. Thus, the smoothing operator used in the wavelet analysis of the coherence type is as in formula (4):

(4)

(4)

Rua and Nunes (Citation2009) consider that represent the effect of smoothing along the wavelet axis, while

represents the smoothing effect in general. Finally, the smoothing operator allows us to compare the results with a Monte Carlo simulation to see if there are periods of pure contagion or co-movement. Similar to the recommendations of Rua and Nunes (Citation2009), we will interpret the results of the coherence analysis as regular correlation coefficients, where high values correspond to switching moments between variables (Kiviaho et al., Citation2014). Thus, if we find in the graphical representation of the distinct wavelet coherence zones with elevated coefficients of coherence we interpret the analysis as the result of the interaction between the two variables. Moreover, if areas with elevated coefficients of co-existence are in the reduced frequency range of the analysis, we will interpret it as a period of ‘contagion’, and if we find large coefficients of cohesiveness in high frequency areas, we interpret the results as the result of market fundamentals, respectively co-movement effect.

4.2. Cointegration analysis

4.2.1. Panel unit root tests

A prerequisite for testing the cointegration between two variables is the presence of stationarity in the data. Generally, we consider a time series or stochastic process as stationary if there is no unit root of the data, while the opposite – the presence of a unit root indicates that the time series is non-stationary. If a certain variable is non-stationary the unit root testing will allow us to determine the number of times a variable has to be differenced in order to achieve stationarity required for cointegration testing. A variable X, is thus integrated of order d, I(d) if we can achieve stationarity after differencing d times. In order to test the presence of a panel unit root we can choose between different modern methods (e.g. Levin, Lin & Chu, Citation2002; Breitung, Citation2000; Im, Pesaran, & Shin, Citation2003) and more traditional methods (e.g. Dickey & Fuller, Citation1981; Phillips & Perron, Citation1988).

While the previous tests used in the analysis are appropriate in testing the presence of a unit root in panel data estimation, because we want to use and A.R.D.L. model we need to test if our data allows for this testing. Thus we use the Kao Residual Cointegration Test (Kao, Citation1999) and Johansen Fisher Panel Cointegration Test (Johansen, Citation1988).

One of the assumptions in the A.R.D.L. econometric test is that the error term of the estimation is not serially correlated. Hence, we first need to determine the appropriate lag of order that has the ability to remove serial correlation. In addition, we need to take into consideration the small sample size, which limits the number of lags we can include in the analysis. We prefer to use the most common methods like The Schwartz-Bayesian Criterion (S.B.C.), Akaike Information Criterion (A.I.C.) or Hannan-Quinn Criterion (H.Q.C.). While, each method of selection allows us to choose appropriate lag values A.I.C. usually is gives a higher number of lags while S.B.C. gives a lower number of lags due to over-parameterisation. Thus, all of our A.R.D.L. models will use the automatic lag selection using the A.I.C. value.

4.2.2. Panel A.R.D.L. model to test cointegration

The A.R.D.L. bounds testing proposed by (Pesaran, Shin, & Smith, Citation2001) allows us to test if there is long run dynamic relationship between two variables that are stationary I(0) and I(1). But in our case, because we suspect that some of our series are cointegrated either I(0) and I(1) using the generic A.R.D.L. testing methodology might not be appropriate. Therefore, we will test the influence of macroeconomic factors on the degree of interdependence between markets using a panel A.R.D.L. model estimation that allows for such mixture. The baseline estimation of our model will follow the procedures recommended by Pesaran, Shin, and Smith (Citation1997, Citation1999).

The generic A.R.D.L. bounds testing methodology involves two subsequent stages in the analysis. Firstly, we must test if there is a long-run relationship between the variables in the analysis, and secondly we estimate the long-run relationship and evaluate the values of the coefficients. Subsequently, we have to test the cointegration results for the short-term period in another estimation. Therefore, our analysis will first estimate the long-term cointegration and subsequently we will estimate the short-term cointegration equation.

The generic A.R.D.L. panel model between wavelet coherence coefficients and our dependent variables is written as shown below in formula (5):

(5)

(5)

where:

- are wavelet coherence coefficients between a Western European capital market and a capital markets from C.E.E. countries;

– standard error after estimating the model for the countries i or j at the frequency f;

A complete description of all the variables used in the analysis is presented in . Model estimation is done using the A.R.D.L. panel approach proposed by Pesaran et al. (Citation1999).

5. Empirical results

5.1. Results of the wavelet coherency analysis

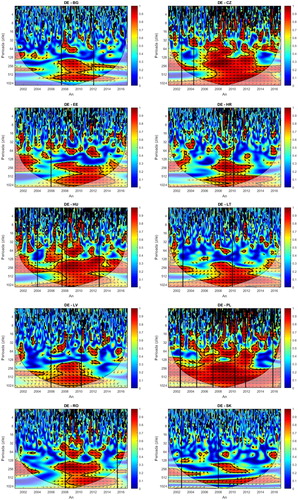

When analysing the co-movement relationship between C.E.E. capital markets and German capital market, the results are depicted in indicate some intriguing results. Firstly, there are clear moments of contagion in the 1–16 day trading days between the German capital market and the Czech Republic, Croatia, Poland, Romania and Hungary markets during the recent 2008–2009 financial crisis, which reveals the presence of the contagion phenomenon between these markets during the recent financial crisis. Our results are similar to those obtained by (Dajcman, Festic, & Kavkler, Citation2012) who analysed the phenomenon of contagion between German capital markets and the markets of the Czech Republic and Hungary and observes the same phenomenon during the 2008–2009 crisis. Or the results of Cărăușu et al. (Citation2018) who tested the presence of the contagion phenomenon between Western European capital markets and C.E.E. capital markets between 2000–2016.

Figure 1. Results of wavelet coherence analysis Germany vs C.E.E. countries. Note: Contours with black represent a 5% significance estimated on the basis of Monte Carlo simulations with random surrogate series. The colours used to represent the wavelet range from blue (low power) to red (high power). Scale-Y indicates the frequency range from the shortest (four days) to the longest (1,024 days). Scale-X is the analysis period in years. Black vertical lines are key moments in adopting codes of governance in C.E.E. countries. The relationship between two variables indicated by the direction of the arrows is as follows: (1) If the arrow indicates the direction to the right, the indices are synchronised; (2) the first index leads if the arrow points to the upper right; (3) the first index is behind if the arrow indicates the right direction down; (4) the indexes are out of sync (exerting anti-cyclic effects between them) if the arrow points to the left; (5) desynchronised and the first index leads if the arrow points to the left and top; and (6) De-synchronised and the first index leads if the arrow indicates the left-most direction. Source: Author’s estimates.

Secondly, the direction of the arrows in our graphical representation indicates that, as a rule, both in the short- and long-term relationship the capital market from Germany is either synchronised or plays predominantly the role of initiator in relation to C.E.E. equity markets. Thirdly, the evolution of the capital markets in the Czech Republic, Hungary and Poland is strongly correlated with the evolution of the German capital market not only during the financial crisis but also later. We also note a desyncing phenomenon in 2012 and 2014–2016 in the relations between Estonia, Latvia, Lithuania, Poland, Romania and Hungary, respectively, compared to German market. If we develop, further our analysis or results indicate a lower degree of fundamental contagion for Romania, Estonia and Lithuania, while the degree of pure contagion (short-term contagion) was lower for Czech Republic, Poland and Hungary between 2012 and 2016.

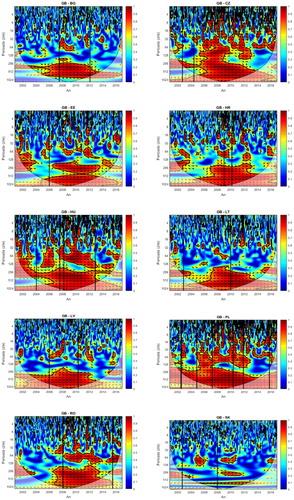

A similar perspective is provided by the results of the wavelet coherence analysis between C.E.E. capital markets and U.K. capital market presented in . From this point of view, we note both similarities and differences. Thus, we observe: a higher degree of co-movement of the capital markets from Czech Republic, Poland and Hungary, while we find lower degrees of interdependence with the other markets, or the leading role of U.K. capital market. Instead, we find a lower degree of fundamental contagion between U.K. capital markets and Slovakian capital market. Therefore, the degree of interdependence between C.E.E. equity markets and U.K. capital market is similar to the one exhibited by German capital market.

Figure 2. Results of the wavelet coherence analysis U.K. vs C.E.E. countries. Source: Author’s estimates.

While there are some differences in the behaviour of each individual C.E.E. capital markets in relation to the German and U.K. capital markets, our results reveals the evolution of the average degree of interdependence of C.E.E. capital markets. Besides finding evidence of short-term pure contagion in 2008–2010 for most C.E.E. countries, we also find that even after the recent financial crisis, the phenomenon is still present and it is more frequent than it was before the crisis. There are numerous moments of short-term contagion even after 2010 in many C.E.E. capital markets. This points out to a higher degree of sensitivity of C.E.E. capital markets to Western Capital markets even after the crisis. Furthermore, we note that more developed capital markets in the region: Poland, Czech Republic, Hungary and Romania are very sensitive to external shock from developed markets. Meanwhile, Slovakian market due to its famous low liquidity and ownership structure seem to be more resilient. On the other side, the Baltic capital markets and the Croatian have increased they degree of co-movement not only during the recent financial crisis, but also after making them more susceptible to external shock. This general state indirectly proves the need to find alternative measures of protection of the national capital markets from external shocks.

The results of the continuous wavelet analysis between C.E.E. countries and the most important Western European capital markets revealed the following: (1) there are no significant differences in the degree of interdependence between C.E.E. markets and German and U.K. markets; (2) the capital markets in Czech Republic, Poland and Hungary are more dependent on Western European markets than other C.E.E. markets; and (3) the degree of interdependence between Slovak market and Western European markets is very low.

5.2. The macroeconomic determinants of interdependence

One of the main objectives of our analysis is to test whether the macroeconomic factors can influence the degree of interdependence between C.E.E. capital markets and select capital markets. Furthermore, we want to test if their influence is important not only on the long-term due to fundamentals, but also in the shor-term. Hence, we will use an A.R.D.L. panel approach model to test our assumptions.

In the first step into estimating the impact of macroeconomic factors on contagion or co-movement phenomenon in C.E.E. capital markets, we must first test the presence of unit roots in our panels. presents the results of unit roots in our data.

Table 4. Results from panel unit root testing.

While using the generic A.R.D.L. method of testing cointegration proposed by Pesaran et al. (Citation2001) requires that all the series are stationary I(1) the results from our estimates reveal that our data is not suitable for a such test because we have many series that are either stationary in I(0) or in I(1). To get things more complicated, some of our results from different tests are sometimes even contradictory. Nevertheless, we note that short-term one and three months degree of interdependence between C.E.E. capital markets are stationary I(0) while long-term interdependence for one and two years are stationary I(1). Mixed results are present for the other remaining variables.

Because our time series presents a mixture of I(0) or in I(1) stationary data we will use the Kao Residual Cointegration Test (Kao, Citation1999) and Johansen Fisher Panel Cointegration Test (Johansen, Citation1988) to test the presence of cointegration. depicts the results from these tests.

Table 5. Results from panel data cointegration tests.

The results from the general cointegration test using the same models as in our A.R.D.L. panel data estimation indicated that there is a potential cointegration relationship between our variables of interest. In the following step we will estimate, the actual impact of our macroeconomic factors on our independent variables.

When assessing the influence of macroeconomic factors on the degree of co-movement the results from reveals that the importance of macroeconomic factors are dependent on the type co-movement period we take into consideration. In the case of the long run equations, we find that only the co-movement for the one year horizon or the two year horizon

are directly influence by many of our macroeconomic factors. Meanwhile, in the case of the short-term co-movement one month

or three months

the role of macroeconomic factors is less important. Our results indicate macroeconomic fundamentals are more important in the long run, or in our case for periods longer than one year. These results are in line with the previous studies of Kiviaho et al. (Citation2014) or Syllignakis and Kouretas (Citation2011).

Table 6. Results from the A.R.D.L. panel model estimation.

When we are assessing short-term cointegration between our variables we find that to a certain degree, macroeconomic factors are important factors in assessing the evolution of C.E.E. capital markets. In general, we find that the Western European monetary policy, is the most important factor in depicting the co-movement relationship for both short-term interdependence periods of one and three months but also for longer periods of time of one to two years. Taking into consideration, that we proxied the monetary policy via the average three months inter-bank rate in Western European economies, this would suggest that an increase in the interest rate in Western economies, can increases the degree of co-movement between C.E.E. countries and Western European economies.

This could also suggest that a more permissive monetary policy in Western economies could be potentially reduce the effect of external shocks from Western economies to the national capital markets. Therefore, national authorities in C.E.E. need to monitor closely the monetary policy changes, or the degree of liquidity in the banking sector of Western economies because these pose a further factor of exacerbating spillovers from external shocks. Overall, our results are similar with the results of Kiviaho et al. (Citation2014) who indicates the main role of the monetary policy in shaping the co-movement.

Another specific factors that can influence the degree of co-movement in the long-run are the national exchange rate and economic cycles. The negative effect of the national economic cycles indicates that, the general economic environment of country can help isolate the national capital market from external shocks. Meanwhile the negative sign from the exchange rate proves that countries with strong currencies that are relative stable are less sensitive to external shocks. Therefore, national authorities can also use the exchange rate as a measure to protect the national capital market. A stable exchange rate helps mitigate the effects of external shocks in C.E.E. countries. This result indirectly proves the results of Mink (Citation2015) who state that testing for contagion requires national currencies, because contagion is often mistaken with exchange rate volatilities in the financial market.

In the case of the other variables, used in our analysis: inflation, foreign exchange rate, foreign economic cycle our results indicate that in the short-term they are able to signal a potential increase in co-movement, but their effect is less predominant. For these, variables, changes in current times are reflect much slower in the degree of co-movement limiting their effectiveness. Nevertheless, these are still important factors in influencing the degree of co-movement in C.E.E. countries.

6. Conclusion

Our analysis, tests the evolution of co-movement between 10 C.E.E. countries, namely Bulgaria, Croatia, Czech Republic, Estonia, Latvia, Lithuania, Poland, Romania, Slovakia and Hungary in relation to the capital markets from in Germany and U.K. between October 2000 and December 2016. We use the wavelet coherency analysis to investigate the degree of co-movement, and an A.R.D.L. panel model to test the impact of macroeconomic factors on the degree of interdependence between markets.

The results of wavelet coherency analysis revealed not only the effects of the recent financial crisis on the degree of co-movement and contagion between C.E.E. capital markets but also the presence of pure and fundamental contagion in the aftermath of the recent financial crisis. Therefore, analysing the influence of macroeconomic factors on the degree of co-movement between capital markets is even more important now than before the recent financial crisis.

In the meantime, the results from the panel A.R.D.L. model tries to grade each individual macroeconomic factor used in our analysis by order of effectiveness in both the short-term and long-term. While, all of our variables play an important role in long-term co-movement, we find that foreign monetary policy, national exchange rate, and national economic cycle are more efficient in both short- and long-term cointegration tests. We find that foreign monetary policy can exacerbate the effect of external shock towards C.E.E. capital markets in both short-term contagion but also in fundamental based contagion. Meanwhile, a stable national exchange rate is able the reduce the effect of co-movement between developed capital markets and C.E.E. capital markets. In addition, a stable national economic environment can help isolate the national capital market from external shocks.

In the case of inflation, foreign exchange rate, foreign economic cycle our results suggest that in the short-term they are able to signal a potential increase in co-movement, but their effect is less predominant. For these, variables, current changes are reflected much slower in the degree of co-movement limiting their effectiveness.

The selective influence of macroeconomic factors pose an important question for national authorities. While one most important factor that influences the degree of co-movement between Western capital markets and C.E.E. capital markets is foreign monetary policy, national authorities need to pay close attention to changes in monetary policy as it can exacerbate the effects of external shocks. In the meantime, by ensuring a stable economic environment and a strong and stable exchange rate, national capital markets can be protected against spillovers from external shocks. Therefore, if national authorities seek to protect and develop internal capital markets they must first ensure a stable economic environment before seeking alternative measures of protection.

Acknowledgements

We are grateful to the four anonymous reviewers for the constructive and valuable comments that helped us to improve significantly our article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Aguiar‐Conraria, L., & Soares, M. J. (2014). The continuous wavelet transform: Moving beyond uni- and bivariate analysis. Journal of Economic Surveys, 28(2), 344–375. https://doi.org/10.1111/joes.12012

- Ajayi, R. A., Mehdian, S., & Stoica, O. (2018). An empirical examination of the dissemination of equity price innovations between the emerging markets of Nordic-baltic states and major advanced markets. Emerging Markets Finance and Trade, 54(3), 642–660. doi:10.1080/1540496X.2017.1419426

- Bekaert, G., Ehrmann, M., Fratzscher, M., & Mehl, A. (2014). The global crisis and equity market contagion. The Journal of Finance, 69(6), 2597–2649. doi:10.1111/jofi.12203

- Boubaker, H., & Raza, S. A. (2016). On the dynamic dependence and asymmetric co-movement between the US and Central and Eastern European transition markets. Physica A: Statistical Mechanics and Its Applications, 459, 9–23. doi:10.1016/j.physa.2016.04.028

- Breitung, J. (2000). The local power of some unit root tests for panel data. In B. H. Baltagi (Ed.), Advances in econometrics, volume 15: Nonstationary panels, panel cointegration, and dynamic panels (pp. 161–178). Amsterdam: JAY Press.

- Burzala, M. M. (2016). Contagion effects in selected European capital markets during the financial crisis of 2007–2009. Research in International Business and Finance, 37, 556–571. doi:10.1016/j.ribaf.2016.01.026

- Cai, Y., Chou, R. Y., & Li, D. (2009). Explaining international stock correlations with CPI fluctuations and market volatility. Journal of Banking & Finance, 33(11), 2026–2035. doi:10.1016/j.jbankfin.2009.05.013

- Cărăuşu, D. N., Filip, B. F., Cigu, E., & Toderaşcu, C. (2018). Contagion of capital markets in CEE countries: Evidence from wavelet analysis. Emerging Markets Finance and Trade, 54(3), 618–641. doi:10.1080/1540496X.2017.1410129

- Cevik, E. I., Korkmaz, T., & Cevik, E. (2017). Testing causal relation among central and eastern European equity markets: Evidence from asymmetric causality test. Economic Research-Ekonomska Istraživanja, 30(1), 381–393. doi:10.1080/1331677X.2017.1305774

- Claessens, S., & Yurtoglu, B. B. (2013). Corporate governance in emerging markets: A survey. Emerging Markets Review, 15, 1–33. doi:10.1016/j.ememar.2012.03.002

- Cuomo, F., Mallin, C., & Zattoni, A. (2016). Corporate governance codes: A review and research agenda. Corporate Governance: An International Review, 24(3), 222–241. doi:10.1111/corg.12148

- Dajcman, S., Festic, M., & Kavkler, A. (2012). Comovement dynamics between central and eastern European and developed European Stock Markets during European integration and amid financial crises—A wavelet analysis. Engineering Economics, 23(1), 22–32. doi:10.5755/j01.ee.23.1.1221

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. doi:10.2307/1912517

- Dornbusch, R., Park, Y. C., & Claessens, S. (2000). Contagion: Understanding how it spreads. The World Bank Research Observer, 15(2), 177–197. doi:10.1093/wbro/15.2.177

- Draženović, B. O., & Kusanović, T. (2016). Determinants of capital market in the new member EU countries. Economic Research-Ekonomska Istraživanja, 29(1), 758–769. doi:10.1080/1331677X.2016.1197551

- Dumas, B., Harvey, C. R., & Ruiz, P. (2003). Are correlations of stock returns justified by subsequent changes in national outputs? Journal of International Money and Finance, 22(6), 777–811. doi:10.1016/j.jimonfin.2003.08.005

- Gençay, R., Selçuk, F., & Whitcher, B. (2002). An introduction to wavelets and other filtering methods in finance and economics. San Diego, CA: San Diego Academic Press.

- Grinsted, A., Moore, J. C., & Jevrejeva, S. (2004). Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Processes in Geophysics, 11(5/6), 561–566. doi:10.5194/npg-11-561-2004

- Gulzar, S., Kayani, G. M., Xiaofeng, H., Ayub, U., & Rafique, A. (2019). Financial cointegration and spillover effect of global financial crisis: A study of emerging Asian financial markets. Economic Research-Ekonomska Istraživanja, 32(1), 187–218. doi:10.1080/1331677X.2018.1550001

- Hopt, K. J. (2011). Comparative corporate governance: The state of the art and international regulation. The American Journal of Comparative Law, 59(1), 1–73. doi:10.5131/AJCL.2010.0025

- Hsing, Y. (2011). Macroeconomic variables and the stock market: The case of Croatia. Economic Research-Ekonomska Istraživanja, 24(4), 41–50. doi:10.1080/1331677X.2011.11517479

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. doi:10.1016/S0304-4076(03)00092-7

- Johansen, S. (1988). Statistical analysis of cointegration vectors. Journal of Economic Dynamics and Control, 12(2–3), 231–254. doi:10.1016/0165-1889(88)90041-3

- Kaminsky, G. L., & Reinhart, C. M. (2000). On crises, contagion, and confusion. Journal of International Economics, 51(1), 145–168. doi:10.1016/S0022-1996(99)00040-9

- Kao, C. (1999). Spurious regression and residual-based tests for cointegration in panel data. Journal of Econometrics, 90(1), 1–44. doi:10.1016/S0304-4076(98)00023-2

- Kiviaho, J., Nikkinen, J., Piljak, V., & Rothovius, T. (2014). The co-movement dynamics of European frontier stock markets. European Financial Management, 20(3), 574–595. doi:10.1111/j.1468-036X.2012.00646.x

- Levin, A., Lin, C.-F., & Chu, C.-S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24. doi:10.1016/S0304-4076(01)00098-7

- Longin, F., & Solnik, B. (1995). Is the correlation in international equity returns constant: 1960–1990? Journal of International Money and Finance, 14(1), 3–26. doi:10.1016/0261-5606(94)00001-H

- Marfatia, H. A. (2017). A fresh look at integration of risks in the international stock markets: A wavelet approach. Review of Financial Economics, 34(1), 33–49. doi:10.1016/j.rfe.2017.07.003

- Mink, M. (2015). Measuring stock market contagion: Local or common currency returns? Emerging Markets Review, 22, 18–24. doi:10.1016/j.ememar.2014.11.003

- Mobarek, A., Muradoglu, G., Mollah, S., & Hou, A. J. (2016). Determinants of time varying co-movements among international stock markets during crisis and non-crisis periods. Journal of Financial Stability, 24, 1–11. doi:10.1016/j.jfs.2016.03.003

- Newaz, M. K., & Park, J. S. (2019). The impact of trade intensity and market characteristics on asymmetric volatility, spillovers and asymmetric spillovers: Evidence from the response of international stock markets to US shocks. The Quarterly Review of Economics and Finance, 71, 79–94. doi:10.1016/j.qref.2018.07.007

- Nikkinen, J., Piljak, V., & Rothovius, T. (2019). Impact of the 2008–2009 financial crisis on the external and internal linkages of European frontier stock markets. Global Finance Journal. doi:10.1016/j.gfj.2019.100481. Retrieved from https://www.sciencedirect.com/science/article/pii/S1044028318302114.

- Peša, A. R., & Festić, M. (2014). Panel regression of stock market indices dynamics in south-eastern European economies. Economic Research-Ekonomska Istraživanja, 27(1), 673–688. doi:10.1080/1331677X.2014.975515

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/jae.616

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. doi:10.2307/2670182

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1997). Estimating long-run relationships in dynamic heterogeneous panels. DAE Working Papers Amalgamated Series, 9721.

- Phillips, P. C. B., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. doi:10.1093/biomet/75.2.335

- Porta, R. L., Lopez‐de‐Silanes, F., Shleifer, A., & Vishny, RW. (1998). Law and Finance. Journal of Political Economy, 106(6), 1113–1155. doi:10.1086/250042

- Rua, A., & Nunes, L. C. (2009). International comovement of stock market returns: A wavelet analysis. Journal of Empirical Finance, 16(4), 632–639. doi:10.1016/j.jempfin.2009.02.002

- Syllignakis, M. N., & Kouretas, G. P. (2011). Dynamic correlation analysis of financial contagion: Evidence from the Central and Eastern European markets. International Review of Economics & Finance, 20(4), 717–732. doi:10.1016/j.iref.2011.01.006

- Thomas, N. M., Kashiramka, S., & Yadav, S. S. (2019). The nature and determinants of comovement between developed, emerging and frontier equity markets: Europe versus Asia-Pacific. Thunderbird International Business Review, 61(2), 291–307. doi:10.1002/tie.22015

- Tiwari, A. K., Mutascu, M. I., & Albulescu, C. T. (2016). Continuous wavelet transform and rolling correlation of European stock markets. International Review of Economics & Finance, 42, 237–256. doi:10.1016/j.iref.2015.12.002

- Torrence, C., & Compo, G. P. (1998). A practical guide to wavelet analysis. Bulletin of the American Meteorological Society, 79(1), 61–78. doi: 10.1175/1520-0477(1998)079≤0061:APGTWA≥2.0.CO;2