?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines the relationship between the real exchange rate and the foreign trade imbalance in both the Western Balkan (WB) and Central and Eastern European (CEE) countries. During the most recent global economic crisis, examining the impact of the exchange rate on the balance of trade took on a particular importance. Countries used a variety of monetary policy regimes and, depending on their choice, they had different economic instruments available to deal with the crisis. The aim of the research was whether exchange rate devaluation and/or depreciation are capable of effectively and fully eliminating the negative effects of the global economic crisis, as well as the consequent poor export performance and contracted economic activity. Our findings show that during an economic crisis those countries that use their own currency cannot substantially adjust their trade deficit by depreciating their currency. Moreover, it is suggested that during the global economic crisis, the balance of payments deficit is not impacted significantly by the exchange rate, any more. In such cases, other factors play a more significant role, like as government spending, followed by foreign demand and direct investments.

1. Introduction

When considering the theoretical aspect of the balance of payments equilibrium, we are referring to a situation that is sustainable without any government intervention due to selected economic policy measures. The most recent economic crisis in 2008 has reinvigorated the discussion about what constitutes an adequate solution in relation to the selection of exchange rate regimes, at least from the macroeconomic adjustment viewpoint. Current account imbalances were the underlying causes of the Eurozone crisis (Baldwin & Giavazzi, Citation2015). A trade deficit per se does not represent a problem; however, it can sometimes be a symptom of a problem, as Mankiw points out (2008). The question then is raised as to whether it is possible to decide on and to maintain an exchange rate that will bring trade in goods and trade in services to equilibrium.

Many authors have pointed out that a trade imbalance requires an exchange rate adjustment. Accordingly, Freund and Warnock (Citation2007) assert that an unadjusted exchange rate is the major reason for current account deficits, while also noting that a higher level of deficit requires a longer period of time for the adjustment to take effect. Ozmen (2005) empirically e results suggest that exchange rate flexibility and economic openness create current account equilibrium. Frankel (Citation1999) stresses that no single currency regime is right for all countries or at all times. According to him, the appropriate exchange rate regime varies depending on the specific circumstances of the country in question, including the classical optimum currency area criteria, and depending on the circumstances of the time period involved. A high level of trade deficit is a serious challenge faced by the majority of European countries. As stated by the European Central Bank in an analysis conducted by Winkler, Mazzaferro, Nerlich, and Thimann (Citation2004), the majority of dollarized countries face difficulty in relation to the sustainability of the balance of trade. Calvo and Reinhart (Citation2002) point out the discrepancy between the exchange rate regime classification used by the IMF and the regimes that are actually applied in some countries.

Prior to the economic crisis outbreak, the CEE countries had higher growth rates in international trade than in the trade with the European Union countries. Nevertheless, although the regional trade is of high importance, all CEE and WB countries consider the European Union as the major export market for them. Exactly this regional export dependency represents one of the routes for transferring the economic crisis from the European Union to the CEE and WB countries’ economies. In terms of trade trends, note should be made that, relative to the European Union countries, the CEE and WB countries are mainly insufficiently developed and that they have relatively modest development potential that, to a large extent, produces import dependency.

The basic goal of the paper is to examine the impact of the exchange rate on trade flows, in bringing the balance of trade into (dis)equilibrium in the sample countries under conditions of an economic shock. This paper will present the European experience gained both by those countries using the euro that form part of the monetary union in the EU, and countries using their own domestic currencies. By way of currency devaluation and/or depreciation on the foreign exchange market, those countries using their domestic currencies increased the price competitiveness and exports of their national economies, while at the same time reducing imports. Apart from such positive effects, exchange rate fluctuations also entail various accompanying negative effects that are capable of leading to considerable problems in the stability of the financial system. The countries that form part of the Eurozone did not, and do not, have identical mechanisms by which they would have been able to influence their balance of trade. In terms of Western Balkan countries, a number of them use their own respective domestic currencies, whereas others apply regimes such as dollarization or a currency board. Thus, the goal is to point out – through the research being undertaken – both the advantages and deficiencies of the fixed exchange rate regimes (such as dollarization or a currency board) in relation to the balance of trade, particularly under conditions of external instability and economic crisis.

Through case study we are intending to present the countries that achieved an envious success by means of using different approaches to exchange rate management during the time of global economic crisis. Then, we are going to identify the correlation between balance of trade equilibrium, on the one hand, and the corresponding exchange rate regime on the other hand. The focus of the interest is on different exchange rate regimes. Fixed exchange rate models imply higher predictability of foreign currency exchange rate; however, there are considerable restrictions on the freedom of the independent macroeconomic policy running. Flexible exchange rate regime gives more freedom to national monetary authorities; however, it bears also a higher risk of inflation as well as domestic money devaluation. Exchange rate rise (national currency depreciation) is the way of stimulating export, by means of competitive pricing for national products on a foreign market. This is because nominal exchange rate rise decreases export price expressed in a foreign currency. In that way encouraged are exporters who—by decreasing the prices—can increase the competitiveness of their products on a foreign market. During the crisis, the sample countries used a variety of monetary policy regimes and, depending on their choice, they had different economic policy instruments available. The countries that opted for fixed exchange rate regime could not implement devaluation and they could not decrease their dependency on the import. For that reason, both the international trade and the economic activity were suffering in general. External shocks were especially striking for Montenegro that carried out dollarization. During the time of the financial and economic crisis, the use of the EUR as the legal tender restricted the application of exchange rate as an effective instrument for adjusting the trade deficit.

In order to define the corresponding causal relationship between the exchange rate and the balance of trade, we gathered adequate data of relevance covering the aforementioned variables. For the statistical data analysis, we used quantitative methods, in particular the panel data econometric models. We estimated various model specifications based on data for 18 countries, covering the period 1990–2016. The results demonstrate that exchange rate flexibility contributes to a reduction in trade disequilibrium; however, this is only true under normal operating conditions and not during the period of the global economic crisis.

The paper is structured as follows. After the Introduction, Section 2 reviews the literature in the field. In Sections 3 and 4, we present our empirical model and the data. Section 5 outlines and interprets our empirical findings, whereas Section 6 offers concluding remarks.

2. Literature review

The specifics of the selected countries that are examined in this paper are that some of them use the euro, a number of them apply contractionary monetary policies, specifically euroization, and others use their respective domestic currencies. External shocks were reflected in a variety of ways in each case, depending on whether the countries used a fixed or a flexible exchange rate.

This is related to the theoretical debates about how justifiable the introduction of the Euro and the creation of the Eurozone actually were. The theoretical basis for forming the Euro currency and establishing the European Monetary Union begins with the work of Mundell (Citation1961), who, when discussing the pros and cons of flexible exchange rate regimes, used the optimum currency area syntagm (Friedman, Citation1953; Meade, Citation1951). This concept refers to a geographical area within which a common monetary policy is to be applied, along with one common currency or a series of fixed mutual exchange rates.

Based on a sample of 75 developing countries during the period between 1973 and 1996, Broda (Citation2004) demonstrates that countries using fixed exchange rate regimes suffer more from trade shocks, which is a consequence of inadequate real exchange rate adjustment. Herrmann and Jochem (Citation2005) studied the currency account deficit determinants in those CEE countries that became EU member states in 2004. Their estimates suggest that most countries avoided higher currency account deficits by means of currency depreciation. Aristovnik (Citation2006) concludes that real exchange rate appreciation and worsening trade conditions increase the current account deficit. The findings showed that countries with current account deficits that were higher than 5% of their GDP encountered problem with deficit sustainability.

Calderon, Chong, and Loayaza (2002) studied the empirical relationship between the current account deficit and a wide spectrum of economic factors recorded in the literature on this topic. Their comprehensive research focused on 44 developing countries and took into account the annual data relevant to the period from 1966 to 1995. They found a statistically significant relationship between the real exchange rate and the current account deficit that was consistent with the predictions of the Mundell-Fleming model. As an advantage of flexible exchange rate regimes, the authors point out their efficiency in equalizing the balance of payments. Additional to it Edwards (Citation2004) found that countries with a more flexible exchange rate are able to better accommodate economic shocks. While Lane and Milesi-Ferretti (Citation2012) investigated the process of bringing the current account balance into equilibrium in 65 countries during the global economic crisis. They analysed the exchange rate trend and identified its modest role in the process of bringing the current account balance into equilibrium. Analysing 170 countries in the period 1971–2005, Chinn and Wei (Citation2008) did not reach a clear empirical conclusion that would confirm the Friedman hypothesis (1953), according to which a flexible exchange rate contributes to current account deficit reduction. But, Debelle and Faruquee (1996) used a panel data approach to their sample of 21 industrial countries for the period between 1971 and 1993. They found a high impact of the exchange rate on the current account and a positive effect of real exchange rate depreciation on the current account deficit. Herrmann (Citation2009) examined the relationships between the exchange rate regime and the pace of current account adjustment. The results indicate that a more flexible exchange rate regime significantly enhances the rate of current account adjustment in Central, Eastern and South-East Europe. Flexible exchange rate regimes are associated with a level of uncertainty, which causes a reduction in international volumes of trade and investment (Domac, Peters, & Yuzefovich, Citation2001). In their papers, Ghosh and Gulde (Citation1997) and Frankel and Rose (Citation2002) also confirmed the positive impact of the fixed exchange rate on trade. Ghosh found that the fixed exchange rate contributed to the volume of trade by increasing it in such a manner that it eliminated the exchange rate risk. Frankel and Rose evaluated the different characteristics of countries in a monetary union relative to countries that used their own currency empirically. The results unambiguously suggest that countries in a monetary union have a greater volume of trade and less volatility in the real exchange rate than countries using their own domestic currency. Arratibel, Furceri, Martin, and Zdzienicka (Citation2011) analysed both the EU and the CEE countries. Using panel estimations for the period between 1995 and 2008, they found that lower exchange rate volatility is associated with greater economic growth and a larger current account deficit.

In addition, several recent papers have considered the impact of the exchange rate on trade imbalance in the context of the most recent global economic crisis of 2008. Krugman, Obstfeld, and Melitz (Citation2012) analysed the costs and benefits of monetary integration. They like Mazier and Petit (Citation2013) and Cesaratto (2015) assert that differences in the costs incurred are the major cause of disequilibrium in the Eurozone and that this was due to the exchange rate adjustment restrictions imposed by the currency union.

Due to the impossibility of adjusting the exchange rate within the Eurozone, currency overvaluation resulted in the systematic deterioration of the current account of the balance of payments. Countries outside the Eurozone, which have more freedom in their price competitiveness, may allow for higher discrepancies in compliance with their trade or exchange rate policies (Gnimassoun & Mignon, Citation2013). Gnimassoun and Coulibaly (Citation2014) studied current account sustainability during the period from 1980 to 2011. They found that current account deficits are higher in countries with fixed exchange rate regimes or in those that belong to a system of monetary union.

Mirdala (Citation2016) examined the impact of sudden exchange rate oscillations on the current account balance in EU countries during the period from 2007 to 2014. During the global economic crisis, the impact of the exchange rate on the current account was decreased, consequently diminishing the application of currency devaluation as an appropriate instrument for lessening the external disequilibrium in those countries. Thus, the national authorities were deprived of exchange rate instruments, as argued by Schilirò (Citation2017), which, along with other factors, led to the member states’ inability to cope with emerging national disarrangements (De Grauwe, Citation2013). Cesaroni and De Santis (Citation2015) analysed two groups of countries, the EU periphery and core member states, over two periods, from 1986 to 1998 and from 1999 to 2012. The obtained results show that the real exchange rate has a considerable impact on the current account balance of payments. These findings were confirmed by Pietrucha (Citation2015), who examined the course of the crisis after 2007 in the CEE countries that were members of the EU during the period from 2008 to 2012. Observing the difference between exchange rate regimes, Comunale (Citation2015) concludes that, in general, fixed exchange rates cause higher inconsistencies when compared to variable exchange rates in the sample countries. Krugman (Citation2016) points out that the real exchange rate is very important for adjusting the balance of trade and that it has a significant effect on trade. Devaluation is particularly necessary during periods of unsustainable capital inflow. He sternly criticizes so called “elasticity pessimism”, which represents the belief that trade flows do not respond to price signals and exchange rate devaluation.

3. Methodology

The initial goal of this paper is to evaluate the impact of the exchange rate on the balance of payments disequilibrium during the global economic crisis period (from 2008 to 2012), both in EU countries that have been members as of 2004 and in the Western Balkan countries that have expressed a desire to become members. The analysis is based on a strongly balanced panel database with data on 18 countries (i) during a 27-year time period (t) from 1990 to 2016. Out of the 18 observed countries, five (Albania, Bosnia and Herzegovina, Macedonia, Serbia, and Montenegro) have engaged with the process of EU accession, while the other thirteen countries became EU members in 2004 (the Czech Republic, Estonia, Hungary, Cyprus, Latvia, Lithuania, Malta, Poland, Slovakia, and Slovenia) and in 2008 (Romania and Bulgaria).

Based on the theoretical and empirical studies of Debelle and Faruqee (Citation1996), Calderon et al. (Citation2002), Aristovnik (Citation2006), and Bussiere, Guillaume, and Steingress (2017), we established the following empirical model:

where Ca_gdpit is the dependent variable, i.e. the current account balance of payments expressed as a percentage of gross domestic product (GDP) in a specific country (i) in a given year (t), whereas the explanatory variables include the real GDP growth (Gdpgit), the real GDP growth rate in Germany (Gdpg_Germanyt), the real effective exchange rate (Reerit), the public expenses expressed as a percentage of GDP (Pe_gdpit), domestic credit yoy growth rate(Dloans yoyit), Real interest rate (Rir), foreign direct investment (net inflow) expressed as a percentage of GDP (FDI gdpit), and the country’s level of development (Dummy_eeit). The stochastic variable of the model uit is distributed as IID(0, Σ).

These variables were observed for 18 countries during a 27-year time period structured as a panel data. Any panel observation provides useful information about the structure and dynamics of the observed variables. Based on these data, five different model specifications were estimated using the same set of variables, but under different conditions (different sets of countries and different time periods), as described in Section 5. After checking the stationarity of the variables, each model specifications was estimated by employing the pooled ordinary least squares (POLS) estimator, the fixed effects estimator (in particular, the least square dummy variable version – LSDV), and the random effects estimator. In order to establish whether the individual effects can be modelled as random or fixed effects, the Hausman test was applied.

However, as the application of appropriate model diagnostics found the presence of autocorrelation and heteroscedasticity, we adopted two additional estimators: the least squares estimator with panel-corrected standard errors (OLS–PCSE) and the two-step generalized least squares method (in particular, the feasible generalized least squares version – FGLS). Chen, Lin, and Reed (Citation2005), e.g., points out that the OLS–PCSE approach is more appropriate when the focus is on hypothesis testing, whereas the FGLS method is more appropriate when the focus is on accuracy of the regression coefficients. In this paper, we present and interpret the results obtained by applying the FGLS method ( in Section 5), although there were no considerable difference in our case between the obtained values. FGLS method instead of assuming the structure of heteroskedasticity, estimate the structure of heteroskedasticity from OLS. The results obtained by applying the other four estimators are available on demand from the authors, but omitted here due to space limitations.

4. Data

We do not have complete data on all the countries and all the periods at our disposal, for a variety of reasons; either because some countries were not monitoring those variables during the 1990s or because others were just emerging as independent countries during the sample period. The database includes the following values: the current account balance of payments expressed as a percentage of GDP, real GDP growth, the real GDP growth rate in Germany, the real effective exchange rate, real interest rate, the public expenses expressed as a percentage of GDP, domestic credit growth rate, FDI, net inflow expressed as a percentage of GDP and each country’s level of development. The sources of these values were Eurostat, the World Economic Outlook (WEO), the International Monetary Fund (IMF), and World Development Indicators (WDI). The description of all the variables used is given in in the Appendix.

Based on the work of Aristovnik and Setnikar-Cankar (Citation2006), Pietrucha (Citation2015), Mirdala (Citation2016), Bussiere et al. (2017), Leigh et al. (Citation2017) and others, we extended the sample period and the sample of countries, thereby placing the model within a substantially adjusted framework. In the model, we did not use lagged balance of payments as a percentage of GDP as an explanatory variable, because based on our sample data there exists a relatively strong positive correlation between the current and the lagged variable, with the correlation coefficient as high as 0.76. Also, all other variables, which we included in or excluded form the final model were the result of adjusting to this paper topic that is specific, for example the terms of trade variable did not show a statistically significant impact in any of the model specifications and was, as such, excluded.

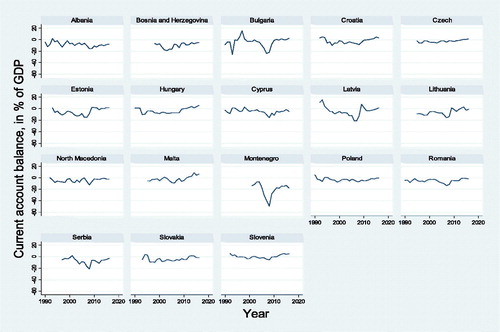

For the purposes of the model, we expressed the dependent variable, i.e. the current account balance of payments, as a percentage of GDP. This means that a positive value implies that the government runs a surplus and a negative value implies that the government records a deficit. This dynamic of this variable is shown for each country in .

Figure 1. Current account balance of payments as a percentage of GDP, by country.

Source: IMF (World Economic Outlook, April 2018): own calculations.

We classify the countries into two groups, the first comprising those countries that do not use the Euro and the second comprises those that do. By averaging the values of their trade deficit expressed as a percentage of GDP, we can conclude that both the EU new member countries and the Western Balkan countries that used their domestic currency faced on average lower trade deficits expressed as a percentage of GDP during the first years of the global economic crisis. Thereafter, the situation changed as shown in in the Appendix. Although at first glance the exchange rate may appear to be the reason for this, the empirical findings have shown us that this was not in fact the case.

Let us now address the explanatory variables of our model specifications. The real GDP growth rate is used as the variable representing (the growth of) domestic demand, whereas the real GDP growth rate in Germany represents (the growth of) foreign demand. By using public expenses to GDP variable, we intend to demonstrate both the public expenses and the government borrowings, specifically debt servicing. By using domestic credit growth rate variable, we intended to present a country’s financial sector activity through encouraging the public sector consumption and investments. Given that in countries using their respective domestic currencies the major share of credits are indexed in a foreign currency (either EUR or CHF), then the stock growth may be the domestic currency depreciation consequence and not an intensified credit activity result; therefore we calculated this growth on the stock expressed in USD. By real interest rate variable, we present the country risk. We calculated the real interest rate in as same manner as it is presented in Dabrowski and Wróblewska (Citation2015). Real interest rate is calculated as a difference between 3-month money market nominal interest rate and actual inflation. Given that we can consider the current account deficit to be the difference between saving and investments, in order to consider this variable as well we used only net foreign direct investment inflow to GDP.

A country’s level of development is represented by a dummy variable Dummy_ee, where 0 refers to developed countries (so-called advanced economies), while 1 refers to developing countries (so-called emerging economies). The classification was done according to the official grouping provided by the International Monetary Fund in the World Economic Outlook, published in April 2018. The difference between the levels of development of the two mentioned groups was derived based on a large number of macroeconomic indicators. Thus, if we consider the average GDP per capita measured at purchasing power parity (PPP) in international dollars during the 27-year sample period, this amounted in the developed countries to approximately 40 thousand dollars, whereas the same indicator for the developing countries amounted to approximately 17 thousand dollars, i.e. less than half of that in the developed economies.

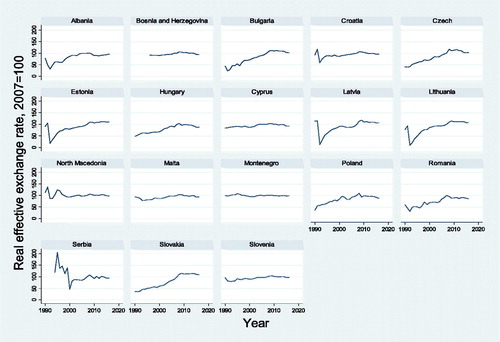

The key explanatory variable in the model is the real effective exchange rate, which is presented as an index with the base period of 2007. Increases and decreases in this variable show the real appreciation and depreciation of the currency, respectively. The real effective exchange rate is derived by dividing the nominal effective exchange rate (a measure of the value of a currency against a weighted average of several currencies) by a corresponding price deflator. This dynamic of this variable by year and by country is given in .

Figure 2. Real effective exchange rate index (2007 = 100), by country.

Source: http://bruegel.org/publications/datasets/real-effective-exchange-rates-for-178-countries-a-new-database; own calculations.

For the purposes of our analysis, two additional dummy variables were generated: Dummy_crisis and Dummy_euro. The variable Dummy_crisis is 0 for the periods not involved in the most recent global economic crisis, whereas the value 1 is assigned to the period involved, i.e. the period from 2008 to 2012. The variable Dummy_euro is 0 if a given country does not use the Euro as their legal tender, but rather uses their own currency, and 1 if a country uses the Euro as their legal tender. Seven countries introduced the Euro as their legal tender during the sample period, and the dates of their transition to using the Euro are as follows: Slovenia in 2007, Cyprus in 2008, Malta in 2008, Slovakia in 2009, Estonia in 2011, Latvia in 2014, and Lithuania in 2015. At the same time, it is important to point out that the regional non-EU countries apply different exchange rate regimes, ranging from currency substitution in Montenegro and a currency board in Bosnia and Herzegovina, to a managed-floating exchange rate in Serbia and an independently floating exchange rate in Albania.

5. Empirical findings

Based on the examined data, five different specifications of the initial model were estimated by using the same set of variables, but under different conditions. The model specifications differ from each other in the following aspects: 1) in the first model, the sample comprised the countries not using the Euro as their legal tender, and non-EU countries and covered the period from 1990 through 2016; 2) in the second model, the sample comprised the countries not using the Euro as their legal tender, and non-EU countries and covered the period from 2000 to 2016; 3) in the third model, the sample comprised the countries not using the Euro as their legal tender, and non-EU countries and covered the period from 2008 to 2012; 4) in the fourth model, the sample comprised the countries using the Euro as their legal tender during the whole sample period from 1990 to 2016; and 5) in the fifth model, the sample comprised the countries using the Euro as their legal tender and covered the crisis period from 2008 to 2012. The results of FGLS model estimation are given in .

Table 1. Results of FGLS estimation, five model specifications (dependent variable is current account balance of payments as a percentage of GDP).

In model specification (1), the sample comprised those countries not using the Euro and non-EU countries as their legal tender and covered the period from 1990 to 2016, whereas in model specification (2), the countries not using the Euro as their legal tender and non-EU countries were examined and this covered the period from 2000 to 2016. Model specification (2) was estimated as, in the 1990s, the majority of the sample countries – both the ones that were going successfully throughout their transition period and those that were still war zones – went through that period in different ways and under different circumstances, while some of them did not yet exist as independent countries. At the same time, the second model’s sample period is also more adequate for making comparisons, because all the mentioned differences were mitigated over that period. However, these definitely affected the level of the economic development in the subsequent period.

Model specifications (1) and (2) suggest that both domestic demand, foreign demand, country development and foreign direct investment affect the current account balance of payments of those countries using their own currency, whereas, with reference to the period after 2000, there is also a clear impact from both the real effective exchange rate and public expenses. The obtained results show that GDP growth rate increase leads to a current account balance of payments decrease. In particular, a one percentage point increase in GDP growth, ceteris paribus, leads on average to a 0.68 percentage point decrease in the balance of trade expressed as a percentage of GDP. This result is in line with the economic theory, saying that GDP growth determines the increase in domestic demand, which is, in this particular case, realized through imported products. These results are similar to the results that Debelle and Faruquee (1996), Aristovnik (Citation2006), Leigh et al. (Citation2017), Santana-Gallego and Peres Rodriges (Citation2019) obtained.

Model specification (2) shows that domestic currency depreciation/devaluation leads to a balance of trade improvement and vice versa. In particular, a one percentage point increase in the real exchange rate, ceteris paribus, leads on average to a 0.07 percentage point decrease in the balance of trade expressed as a percentage of GDP. Domestic currency depreciation/devaluation makes export activity cheaper and thereby increases it, whereas it makes import activity more expensive and thereby decreases it at the same time, which taken together leads to a reduction in the trade imbalance. These results have already been verified in earlier researches (Aristovnik, Citation2006). Model specification (2) further suggests the significant impact of foreign demand on the trade disequilibrium during the period after 2000, as well as the fact that a foreign demand increase leads to balance of trade improvement because of the increase in exports. In particular, the model indicated that if Germany’s GDP growth rate is increased by one percentage point, ceteris paribus, the countries using their own currency will experience on average a 0.4 percentage point increase in their balance of trade expressed as a percentage of GDP.

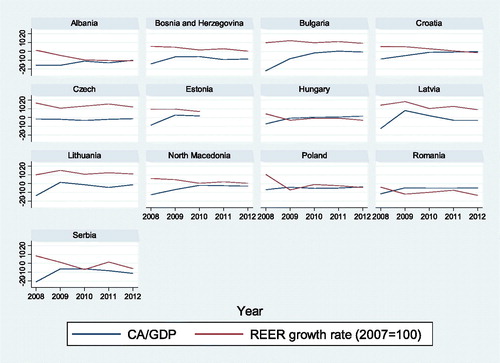

In model specification (3), the sample comprised those countries not using the Euro as their legal tender and non EU countries and covered the period of the global economic crisis (from 2008 to 2012). shows that, during the crisis period, the balance of payments is not impacted in a significant way by the foreign exchange rate. The substantial impact under these circumstances is that of both domestic and foreign demand, FDI and public expenses. A public spending increase leads to a balance of trade decrease. This is in line with the results of Petrucha (2015), Asteriou, Masatci, and Pılbeam (Citation2016), and Bahmani-Oskooee and Gelan (Citation2018).

Notably, model specification (3) suggests that if the public expenses expressed as a percentage of GDP increases by one percentage point, ceteris paribus, there is on average a 0.2 percentage point decrease in the balance of trade expressed as a percentage of GDP. If we take current account balance as a balance of investments and savings in a country, then more investment than savings means the current account deficit is taking place and, vice versa, more savings than investment means a current account surplus. Countries that use local currency have high influence of FDI on current account deficit. This is in line with economic theory as well as with the results that Sahoo, Babu, and Dash (Citation2015) published in their paper.

Based on , we can see that those countries using their own currency and wishing to become EU member states attempted to take advantage of the depreciation of their currencies, so as to mitigate their trade imbalance. However, that did not produce the expected results. As the model shows, the expected results did not realize as the real exchange rate impact on the trade deficit was reduced during the global economic crisis. Upon their accession, the new EU member states assumed a commitment to maintain exchange rate stability and to participate in the European Exchange Rate Mechanism (ERM II). This means that they must comply with a fixed exchange rate fluctuation margin and that during the period of two years prior to their accession there must not be any significant oscillations. By including their currencies in the exchange rate mechanism, the new member states do not have the possibility to undertake devaluation aimed at improving their economies competitiveness.

Figure 3. Dynamics in the effective exchange rate and trade deficit expressed as a percentage of GDP, in the countries using their own currency during the crisis.

Source: IMF; http://bruegel.org/publications/datasets/real-effective-exchange-rates-for-178-countries-a-new-database; own calculations.

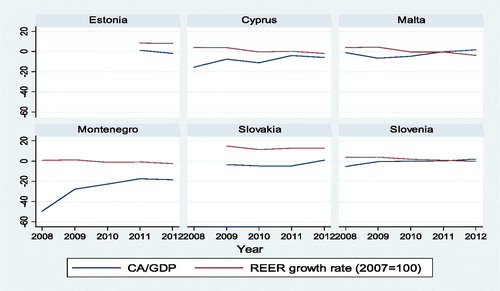

In model specification (4), the sample comprised those countries using the Euro as their legal tender. It should be remembered that the Euro banknotes and coins were introduced on 1 January 2002 and that all the sample countries had their respective currencies at that time, as well as that the transition to using the Euro as their legal tender was gradual in the years thereafter. Upon the transition to the Euro, those countries completely lost the option of improving their competitiveness by means of devaluation/depreciation of their own currencies, which is evident based on results of model specification (4).

These suggest that the most significant impact on the trade imbalance is foreign demand, real interest rate, the credit activity and the level of a country’s development. Credit activity shows a negatively and significant impact on the current account balance, higher spending of private sector causes higher deficit of current account. The obtained result is in line with the results of Erdem, Ucler, and Bulut (Citation2013), Turgutlu (Citation2014), and Isik and Yilmaz (Citation2017).

Model specification (4) also demonstrates that the more underdeveloped a country that uses the Euro is, the more it faces higher trade deficits, regardless of the presence of an economic crisis. At the same time, we need to take into account that the sample comprises just one non-EU member country that uses the Euro as its legal tender, as well as that the indicators pertaining to it depart significantly from the values pertaining to the other countries in the sample, which speaks in favour of the justifiability of the existing strict rules for the transition to Euro as legal tender. That country is under a double burden: it is not allowed to improve its trade deficit by means of the exchange rate and, concurrently, the exchange rate that is used is not appropriate for the economy. The real exchange rate is considered as the quotient of the prices of non-tradable and tradable goods. The very fact that the country belongs to the group of developing countries means that already from the beginning there is a considerable disproportion between tradable and non-tradable goods. Regardless of these points, introducing the Euro is not crucial for the structural reforms that this country should undertake.

In model specification (5), the sample comprised the countries using the Euro as their legal tender and covered the crisis period (2008–2012). The results demonstrate that during the global economic crisis, domestic and foreign demand, real interest rate, credit activity and country development have an impact on the balance of trade. On the one hand, the rise of domestic demand, credit activity, as well as the low level of a country’s development have a negative impact, whereas, on the other hand, the increase in real interest rate and foreign demand have a positive effect on trade disequilibrium. Calderon et al. (Citation2002), Erdem et al. (Citation2013), Turgutlu (Citation2014), and Isik and Yilmaz (Citation2017) published similar results in their earlier papers ().

Figure 4. Dynamics in the real exchange rate and trade deficit expressed as a percentage of GDP, in the countries using the Euro during the crisis.

Source: IMF; http://bruegel.org/publications/datasets/real-effective-exchange-rates-for-178-countries-a-new-database; own calculations.

6. Concluding remarks

During the global economic crisis, the Western Balkan and the Central and Eastern European countries attempted to accommodate the economic shocks and pressure caused by the deteriorated business conditions. The balance of trade disequilibrium imposed itself as a serious problem for sustainable economic growth. Complementary to the research findings the paper’s scientific contribution is composed primarily of validating and explaining the foreign exchange rate role in establishing a sustainable balance of trade equilibrium in less developed countries such as the Western Balkan and Central and Eastern European countries, under contemporary conditions of more and more capital flows and increasingly frequent emergence of financial crises. Countries strived to maintain their balance of trade in equilibrium by means of adjusting their exchange rates. The paper contributed in supplementing the existing (scarce) literature on dollarization/euroization effects on international trade balance, particularly during crisis periods.

Our results demonstrate that during the global economic crisis the real exchange rate impact on the current account was reduced, which consequently limited the applicability of devaluation as an appropriate instrument for the reduction of external imbalances. Those countries applying a fixed exchange rate recorded faster adjustments in the aftermath of the economic crisis, while their trade balance was also considerably improved. The trade balance improvements were primarily achieved by increased exports and not by import restrictions.

It was shown that the exchange rate is a powerful instrument by which trade imbalances can be reduced when the economic environment is stable. One conclusion that one can derive is that domestic currency depreciation/devaluation leads to improvements in the balance of trade. This is consistent with economic theory, according to which domestic currency depreciation/devaluation makes export activity cheaper and thereby increases it, whereas, at the same time, it makes import activity more expensive and thereby decreases it, altogether leading to a reduction in the trade imbalance. Moreover, it is suggested that during the global economic crisis, the balance of payments deficit is not impacted significantly by the exchange rate any more. Under such circumstances, public expenses gains significance. In addition, it has been demonstrated that countries using their own currencies and wishing to become EU member states attempted to take advantage of the depreciation of their currencies to mitigate the trade imbalance. However, that did not produce the expected results, as during the global economic crisis the real exchange rate impact on the balance of trade was reduced.

Upon the transition to using the Euro as legal tender, the countries completely lost the possibility to improve their competitiveness by means of devaluation/depreciation of their own currency. Our results have revealed that the most significant impact on the trade imbalance is that provided by domestic and foreign demand, real interest rate, credit activity and the level of a country’s development. During the global economic crisis, the WB and the CEE countries experienced different results in bringing their balance of trade towards equilibrium. It has been ascertained that the role of the exchange rate was significant during the whole sample time period. Nevertheless, its impact is not crucial in a period during which countries face external shocks, and the group of significant variables at this point also includes public expenses, foreign demand and FDI. The impact of these factors on the trade equilibrium remains a matter that should be the subject of further research.

Disclosure statement

No potential conflict of interest was reported by the authors.

Table A1. Description of variables and their descriptive statistics.

Table A2. Current account balance of payments as a percentage of GDP for both the EU new member states and the Western Balkan countries, by year.

Table A3. Correlation matrix.

Table A4. Country uses its own currency, whole period.

Table A5. Country uses its own currency, period after 2000.

Table A6. Country uses its own currency, crisis period.

Table A7. Country uses the Euro, whole period.

Table A8. Country uses the Euro, crisis period.

References

- Aristovnik, A. (2006). The determinants and excessiveness of current account deficits in Eastern Europe (William Davidson Institute Working Paper No. 827). Michigan: William Davidson Institute at the University of Michigan.

- Aristovnik, A., & Setnikar-Cankar, S. (2006). How excessive are external imbalances in selected transition countries? Prague Economic Papers, 2006(3), 15. doi:10.18267/j.pep.287

- Arratibel, O., Furceri, D., Martin, R., & Zdzienicka, A. (2011). The effect of nominal exchange rate volatility on real macroeconomic performance in the CEE countries. Economic Systems, 35(2), 261–277. doi:10.1016/j.ecosys.2010.05.003

- Asteriou, D., Masatci, K., & Pılbeam, K. (2016). Exchange rate volatility and international trade: International evidence from the MINT countries. Economic Modelling, 58, 133–140. doi:10.1016/j.econmod.2016.05.006

- Bahmani-Oskooee, M., & Gelan, A. (2018). Exchange-rate volatility and international trade performance: Evidence from 12 African countries. Economic Analysis and Policy, 58, 14–21. doi:10.1016/j.eap.2017.12.005

- Baldwin, R., & Giavazzi, F. (2015). The eurozone crisis: A consensus view of the causes and a few possible solutions. London: A VoxEU.org Book, CEPR Press.

- Broda, C. (2004). Terms of trade and exchange rate regimes in developing countries. Journal of International Economics , 63(1), 31–58. doi:10.1016/S0022-1996(03)00043-6

- Bussière, M., Guillaume, G., & Steingress, W. (2017). Global trade flows: Revisiting the exchange rate elasticities (Bank of Canada Staff Working Paper, No. 2017), 41. Ottawa: Bank of Canada.

- Calderon, C., Chong, A., & Loayza, N. (2002). Determinants of current account deficits in developing countries. Contributions to Macroeconomics, 2, 1–35.

- Calvo, G. A., & Reinhart, C. M. (2002). Fear of floating. The Quarterly Journal of Economics, 117(2), 379–408. doi:10.1162/003355302753650274

- Cesaratto, S. (2015). Balance of payments or monetary sovereignty? In search of the EMU’s original sin. International Journal of Political Economy, 44(2), 142–156. doi:10.1080/08911916.2015.1060830

- Cesaroni, T., & De Santis, R. (2015). Current account “Core-periphery dualism” (EMU LEQS Paper No. 90).

- Chen, X., Lin, S., & Reed, R. W. (2005). Another look at what to do with time-series cross-section data (Economics Working Paper Archive at WUSTL No. 0506004). Canterbury: University of Canterbury, Department of Economics and Finance.

- Chinn, M., & Wei, S. (2008). A faith-based initiative: Does a flexible exchange rate regime really facilitate current account adjustment? (NBER Working Paper No. 14420). Cambridge, Massachusetts: National Bureau of Economic Research.

- Comunale, M. (2015). Current Account and REER misalignments in Central Eastern EU Countries: an update using the Macroeconomic Balance approach Economics Department. Vilnius, Lithuania: Bank of Lithuania 3.

- Dabrowski, M., & Wróblewska, J. (2015). Exchange rate as a shock absorber or a shock propagator in Poland and Slovakia – an approach based on Bayesian SVAR models with common serial correlation (MPRA Paper 61441). Munich, Germany: University Library of Munich.

- De Grauwe, P. (2013). Design failures in the Eurozone: Can they be fixed? (LEQS Paper No. 57), 1–34. London: European Institute LSE.

- Debelle, G., & Faruqee, H. (1996). What determines the current account? A cross-sectional and panel approach (IMF Working Paper No. 96/58). Washington, DC: International Monetary Fund. doi:10.5089/9781451966701.001

- Domac, I., Peters, K., & Yuzefovich, Y. (2001). Does the exchange rate regime affect macroeconomic performance? Evidence from transition economies (Policy research working paper No. 2642). Washington D.C.: The World Bank, Europe and Central Asia Region.

- Edwards, S. (2004). Financial openness, sudden stops and current account reversals. American Economic Review, 94(2), 59–64.

- Erdem, E., Ucler, G., & Bulut, U. (2013). Impact of domestic credits on the current account balance: a panel ARDL analysis for 15 OECD countries. Actual Problems of Economics, 1, 408–416.

- Frankel, J. A. (1999). No single currency regime is right for all countries or at all times (NBER Working paper No. 7338). Cambridge, Massachusetts: National Bureau of Economic Research.

- Frankel, J. A., & Rose, A. K. (2002). An estimate of the effects of common currencies on trade and income. The Quarterly Journal of Economics, 67(2), 437–466. doi:10.1162/003355302753650292

- Freund, C., & Warnock, F. (2007). Current account deficits in industrial countries: The bigger they are, the harder they fall? In R. Clarida (Ed.), G7 current account imbalances sustainability and adjustment (pp. 69–204). Chicago, IL: University of Chicago Press.

- Friedman, M. (1953). The case for flexible exchange rates. In Milton Friedman (Ed.), Essays in positive economics (pp. 157–203). Chicago, IL: University of Chicago Press.

- Ghosh, A., & Gulde, A. M. (1997). Does the nominal exchange regime matter? (NBER Working paper No. 5874). Cambridge, Massachusetts: National Bureau of Economic Research.

- Gnimassoun, B., & Coulibaly, I. (2014). Current account sustainability in Sub-Saharan Africa: Does the exchange rate regime matter? Economic Modelling, 40, 208–226. doi:10.1016/j.econmod.2014.04.017

- Gnimassoun, B., & Mignon, V. (2013). Current-account adjustments and exchange-rate misalignments (CEPII Working Paper, 2013). Paris: CEPII Research Centre.

- Herrmann, S. (2009). Do we really know that flexible exchange rates facilitate current account adjustment? Some new empirical evidence for CEE countries. Applied Economics Quarterly, 55(4), 295–311. doi:10.3790/aeq.55.4.295

- Herrmann, S., & Jochem, A. (2005). Determinants of current account developments in the central and east European EU member states – Consequences for the enlargement of the euro area (Discussion Paper Series 1: Economic Studies 32). Frankfurt, Germany: Deutsche Bundesbank, Research Centre.

- International Monetary Fund. (2018). World economic outlook, April 2018: Cyclical upswing, structural change (Working Papers No. 12768, eSocialSciences). Washington D.C.: International Monetary Fund.

- Isik, N., & Yilmaz, S. (2017). The relationship between current account balance and types of credits: An application on selected OECD countries. Journal of the Faculty of Economics and Administrative Sciences, 7(2), 105–126.

- Krugman, P. (2016, April 16). The return of elasticity pessimism. New York Times. Retrieved from http://krugman.blogs.nytimes.com/2016/04/16/the-return-of-elasticity-pessimismwonkish/?_r=1

- Krugman, P., Obstfeld, M., & Melitz, M. (2012). International economics. Boston, MA: Pearson Addison-Wesley.

- Lane, P. R., & Milesi-Ferretti, G. M. (2012). External adjustment and the global crisis. Journal of International Economics, 88(2), 252–265. doi:10.1016/j.jinteco.2011.12.013

- Leigh, D., Weicheng, L., Ribeiro, M., Szymanski, R., Tsyrennikov, V., & Yang, H. (2017). Exchange rates and trade: Disconnect? (Working Paper No. 17/58). Washington, DC: International Monetary Fund. doi:10.5089/9781475587494.001

- Mankiw, G. (2008). Principles of microeconomics. Mason, OH: South Western Cengage Learning.

- Mazier, J., & Petit, P. (2013). In search of sustainable paths for the eurozone in the troubled post-2008 world. Cambridge Journal of Economics, 37(3), 513–532. doi:10.1093/cje/bet012

- Meade, J. (1951). The balance of payments: The theory of international economic policy. Oxford: Oxford University Press.

- Mirdala, R. (2016). Real exchange rates, current accounts and competitiveness issues in the euro area (FIW Working Paper No. 173). Vienna: Research Centre for International Economics (FIW).

- Mundell, R. (1961). A theory of optimum currency areas. The American Economic Review, 51(4), 657–665.

- Özmen, E. (2005). Macroeconomic and institutional determinants of current account deficits. Applied Economics Letters, 12(9), 557–560. doi:10.1080/13504850500120714

- Pietrucha, J. (2015). Exchange rate regime and external adjustment in CEE countries. Journal of Economics and Management, 20(2), 38–52.

- Sahoo, M., Babu, S., & Dash, U. (2015). Effects of FDI flows on current account balances: Do globalisation and institutional quality matter? Retrieved from https://www.semanticscholar.org/paper/Effects-of-FDI-flows-on-Current-Account-Balances-%3A-Sahoo-Babu/e791155a3798e3ddb34f44b6f813705fc069c69d

- Santana-Gallego, M., & Peres Rodriges, Jorge V. (2019). Internationa trade, exchange rate regimes, and financial crises. The North American Journal of Economics and Finance, 47(C), 85–95.

- Schilirò, D. (2017). Rules, imbalances and growth in the eurozone. In R. Mirdala & R. R. Canale (Eds.), Economic imbalances and institutional changes to the Euro and the European Union. International Finance Review (Vol. 18, pp. 65–890). Bingley, UK: Emerald Publishing Limited.

- Turgutlu, E. (2014). Current account balance implications of consumer loans: The case of Turkey. International Journal of Applied Economics, 11(2), 55–64.

- Winkler, A., Mazzaferro, F., Nerlich, C., & Thimann, C. (2004). Official dollarisation/euroisation: motives, features and policy implications of current cases (European Central Bank No. 2).

Appendix