?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The main objective of the article is to determine, on the example of the communes of the Małopolska Province, the factors that affect the efficiency of communal investment expenditures, with particular emphasis on social participation. In order to achieve this aim, appropriate two-stage empirical studies were designed. In the first stage, the efficiency of communal investment expenditure was determined using the DEA and order-m methods for all studied local government units. In turn, the second stage of the empirical study was based on an econometric analysis, which indicated that the examined efficiency is influenced by the following factors: location of the commune in the Cracow metropolitan area, level of communal investment expenditure per capita, intensity of use of external sources of financing communal investment, and level of social participation in the commune.

1. Introduction

The basic task of communes is to meet the needs of the local community (Witkowski & Kiba-Janiak, Citation2014). This task is largely implemented through communal investments in technical and social infrastructure. Local government investments have their own unique characteristics, including high capital intensity, irreversibility of the effects of investment decisions, high risk of investment failure and a significant impact on local development. Taking into account the features of local government investments and the limited financial resources of communes, it should be stated that the decisions made concerning the implementation of communal projects in the field of social or technical infrastructure should be as rational as possible, with the aim of achieving the continuous efficient management of public funds.

One factor that may assist in the more efficient spending of investment funds in communes is social participation, which nowadays plays an increasingly important role in local public administration (Strange, Citation2008). Social participation allows the local community to influence the decisions made by the public administration, which translates into greater understanding of the needs of citizens and increased effectiveness in meeting them.

Moreover, according to the public choice theory, politicians are more motivated by personal interests than public ones. A public authority aims above all to win the next election and politicians can also act to increase their private wealth. In order to limit the harmful influence of politicians, it is necessary to extend democratic control over them, which undoubtedly enables the processes of social participation. Therefore, based on these premises, it can be stated that the high involvement of citizens in public decision-making processes will translate into more efficient management of public funds, including investments.

In the face of this research problem, the main goal of the article is to determine, on the example of the majority of the communes of Małopolska Province, the factors that affect the efficiency of communal investment expenditures, with particular emphasis on social participation. From a theoretical point of view, the aim of the article is to draw attention to the problem of the principal–agent, which occurs between the local authority and the local community. In particular, our empirical research aims to verify the hypothesis that social participation is one of the factors enabling citizens to supervise politicians (agents), which leads to an increase in the efficiency of their actions, including their spending of public investment funds.

The period of the designed study covered the years 2010–2016. Both the period and the geographical scope of the research resulted mainly from the availability of statistical data. The research methodology of this work used objective statistical data and was based on the following research methods: a taxonomic method, the DEA method, the order-m method and the regression methods.

In a nutshell, the results of empirical research have shown that the efficiency of communal investment expenditures is significantly influenced by the following factors: location of the commune in the Cracow metropolitan area, level of communal investment expenditure per capita, intensity of the use of external sources of investment financing by the commune, and level of social participation in the commune.

2. Investment expenditure of polish local governments and sources of financing – an international comparison

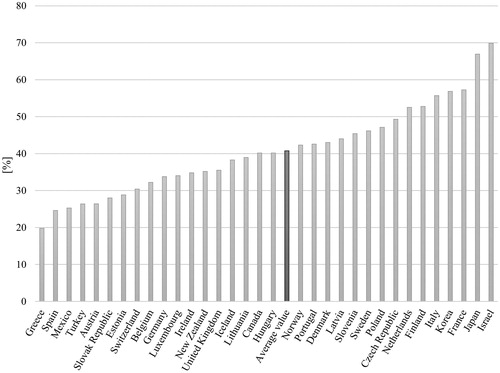

Nowadays, local governments are increasingly responsible for providing basic public services and public infrastructure, as confirmed by data from the Organisation for Economic Cooperation and Development (OECD, Citation2019). According to the OECD, on average, in the years 2010–2016, the investment spending of Polish communes accounted for 47.12% of general government investment (see ). During this period, this value was one of the highest among OECD countries (the lowest share was recorded in Greece (19.78%) and the highest in Israel (69.86%)).

Figure 1. Local government investment spending as a percentage of general government investment in the OECD countries (average values for the years 2010–2016). Source: own study based on data from OECD.

The basic condition for the implementation of public investment by communes is to have sufficient financial resources. In general, the sources for financing local government investments can be divided into own (understood as own revenues) and foreign (e.g. grants, credits, funds from bond issues). In Poland, the main source of financing for communes is grants, which on average, in the years 2010–2016, amounted to as much as 60% of local government revenues (see ). In this respect, similarities can be observed between the Polish and Hungarian, Danish and Korean local governments.

Table 1. Structure of local government revenues and tax autonomy.

According to the literature on the subject, however, the key to ensuring that communes provide an adequate level of goods and services is for them to have sufficient own revenues. This also vests officials with accountability vis-à-vis their voters, which contributes to more efficient spending of public funds (Martinez-Vazquez, Citation2015). It should be noted that the level of a commune’s own revenues depends primarily on the tax system adopted in any given state and the autonomy of local governments in shaping it. OECD countries exhibit a very large variation in this respect (see ). In some, such as Belgium, Estonia, France, Ireland, Lithuania, New Zealand, Slovakia and the United Kingdom, property taxes constitute the dominant group in the structure of local government tax revenues. An entirely different tax system operates in Denmark, Finland, Germany, Latvia, Norway, Sweden and Poland, where the main local tax revenues come from income, profits and capital gains.

Large disparities also exist among OECD countries in terms of the autonomy of the tax system. In Poland, as much as 59% of the tax revenues of local governments are generated within a tax-sharing arrangement in which the revenue split can be changed unilaterally by the central government. Under this agreement, Polish local governments receive a predetermined percentage of taxes on income (both individual and corporate). It should, therefore, be noted that Polish communes do not have any tax autonomy in this respect. The only leeway Polish local governments have in determining their own tax revenues is the possibility to set the rates of property tax, which constitutes about 30% of their tax revenues. This autonomy, however, is limited by the government, which sets maximum rates for this tax. Moreover, unlike many other countries where the basis for calculating property tax is the capital or rental value of a given property, Poland taxes property according to size, expressed in square metres or hectares (without any consideration for its market value). This results in insufficient revenues from this type of tax (Felis & Rosłaniec, Citation2017) and very high tax rates at an average of 80–95% of the maximum rate depending on the type of property (Ministry of Finance, Citation2019). As a whole, the ability to shape tax revenues autonomously is curtailed, which forces Polish local governments to look for other sources of financing their infrastructural investments. As Martinez-Vazquez (Citation2015) stresses, however, the ability of local governments to cater for their own required financing for public investments should be a feature practised worldwide. In order to meet the needs of public investment, communes use other conventional sources of revenue, that is, grants and borrowing. In particular, credit can be an adequate source of financing for local government investments if access to it is provided in a disciplined manner. Otherwise, it may lead to overspending.

Further, local governments in various countries are trying to develop novel ways of financing their investments. Revenues generated from public investments increasing the value of land are one such example. In Poland, the instrument par’excellence for this is the betterment levy, which consists in the commune collecting a fee calculated on the basis of the increase in the value of real estate engendered by the construction of technical infrastructure by the local government. Communes are free to set the betterment levy rate, with the proviso that it does not exceed 50% of the increase in the value of real estate. Due to social pressure, however, Polish local governments very often fail to collect such fees (Supreme Audit Office, Citation2019) or they set the rate at a very low level (e.g., in the city of Dąbrowa Górnicza, the rate was 3% for a time, and then, as a result of pressure from residents, the betterment levy was completely abolished).

Another innovative mechanism of financing investments in communes is the use of public–private partnerships (PPP). The data for the years 2009–2019, however, indicate that projects under PPP constituted only a small fraction of all local government investments. In particular, in the period in question, 564 PPP procedures were announced, of which only 137, with a total value of PLN 6.034 billion, have been or are currently realised (Ministry of Funds & Regional Policy, Citation2019). Although local governments are responsible for 122 out of the 137 PPP cases, taking into account the total value of investment projects, it should be stated that this type of financing has not been successful among Polish communes.

In summary, local governments around the world abide to different investment support schemes. Therefore, it is extremely important that the investment activity of communes continues to be the subject of investigation, in particular with regard to the identification of factors that may increase the efficiency of public investment expenditure.

It has become clear that Polish local governments lack sufficient autonomy to shape their own revenues. Therefore, in order to implement infrastructure investments, Polish communes should concentrate on external sources of financing, the wise use of which may increase expenditure efficiency (Marcinek, Czempas, & Kobiński, Citation2014).

3. Factors affecting local government efficiency

3.1. Social participation

3.1.1. Review of previous research

Literature on the factors influencing the efficiency of communal investment expenditure is rare. Therefore, the review of the relevant studies was extended to other types of efficiency related to the activity of local government.

In research conducted so far, the most frequently analysed factors influencing the efficiency of the local government sector in terms of social participation, are: turnout in local government elections and the share of people entitled to vote (Borge, Falch, & Tovmo, Citation2008; Bosch, Espasa, & Mora, Citation2012; Da Cruz & Marques, Citation2014; Geys, Heinemann, & Kalb, Citation2010; Revelli & Tovmo, Citation2007; Šťastná & Gregor, Citation2011; Citation2014). The direction of the impact of this factor, based on this study, is usually positive, that is, higher turnout in local government elections determines higher efficiency of the local public sector.

Very interesting research was also conducted by Giordano, Tommasino, and Casiraghi (Citation2009), who showed that the higher the interest in politics of the population, the bigger the efficiency of public services in Italian provinces.

The influence of direct instruments on local government efficiency was also studied in the literature. Only one empirical paper, however, contained such a study. This analysis was conducted by Asatryan and De Witte (Citation2015) and concerned the impact of citizens’ initiatives on the efficiency of the local public sector. The results of the above-mentioned study indicated that the presence of forms of direct democracy in a given commune significantly increases the analysed efficiency.

Another group of factors affecting local government efficiency concerns determinants which describe social participation in terms of information. In particular, there is research that examines whether the scope and content of local newspapers may affect public sector efficiency. The obtained results indicated that the greater the range of local newspapers, the higher the local government efficiency (Bruns & Himmler, Citation2011).

3.1.2. Theoretical framework

Social participation is a phenomenon defined as the involvement of citizens in public decision-making (Beirele & Cayford, Citation2002). The degree of participation of citizens in the process of managing a local government unit may be highly differentiated, and it results both from the level of activity of the local community and the degree of openness of public administration to given forms of participation. In the literature on the subject, the best-known ladder of social participation, defining the forms of citizens’ participation in public governance, was conceptualised by Arnstein (Citation1969). She distinguishes eight levels of social participation in the ladder, which translate into three forms of cooperation between citizens and the public administration. The first two levels, manipulation and therapy, actually mean no social participation, only denoting the preparation of citizens for the process of co-decision in public matters. The next levels of this participatory ladder are: information, consultation and placation. They consist of so-called apparent activities which, despite allowing citizens to participate in the decision-making process, do not constitute binding forms of cooperation between them and public authorities. In this situation, the local community participates in consultations, advises and receives information from government representatives. The proposals made by citizens, however, only have a consultation character and do not have to be accepted by the public administration. The last form of public participation, defined as socialisation of power, includes: partnership, delegation and citizen control. Only then, will citizens have a real influence on the decisions made by local authorities.

The participatory ladder presented by Arnstein (Citation1969) can be narrowed down to three elements: information, consultation and co-decision. Each of the above forms of social participation is implemented through appropriate instruments, which include, among others: public consultations, discussion panels, referendums and participatory budgets.

From a theoretical perspective, the relationship between social participation and the efficiency of communal investment expenditure can be analysed on the basis of Niskanen’s economic theory of bureaucracy and, in particular, the problem of the principal–agent (Geys et al., Citation2010). In this model, local authorities function as agents acting for citizens (principals) who want to satisfy their needs as much as possible. There is a conflict of interest here, however, that manifests itself in the fact that agents can benefit more from less productive activities, such as salary increases or overstaffing (Borge et al., Citation2008). Moreover, politicians very often act in favour of certain interest groups and seek to increase private wealth at the expense of citizens (Legiędź, Citation2005), which can be explained by the theory of public choice. According to this theory, politicians behave in a similar way to consumers and entrepreneurs, which means that they tend to not meet the needs of society. In return, their aim is to maximise their own benefits, in particular income, power and prestige. In this case, politicians are very often susceptible to the influence of certain narrow interest groups, which leads to decisions concerning the implementation of infrastructure investments being beneficial only for a certain group of residents. The consequence of acting against the public interest is inefficient dispersion of technical and social infrastructure, which reduces the level of efficiency of public spending.

It is important to stress that the inefficient activities of politicians as agents can be limited by various factors. One of the most important is the ability of citizens to supervise politicians. In this case, there is a decrease in asymmetry of information between the public and local authorities, which leads to a reduction in expenditure wasting (Geys et al., Citation2010) and, consequently, in an increase in the efficiency of expenditures. Therefore, it may be stated that social participation is an extremely important factor influencing the efficiency of communal investment expenditure.

The impact of social participation on the analysed efficiency may be direct or indirect. The indirect method is based primarily on active monitoring of politicians through high turnout in local government elections. As a result of high voter turnout, one can expect that politicians will be more inclined in the face of high pressure to make decisions that will benefit the entire local community rather than narrow interest groups (Borge et al., Citation2008). The emergence of pressure causing the rational activity of local authorities may result not only from high voter turnout but also from a high number of associations, foundations or non-governmental organisations (NGOs) in the area of a given local government. Moreover, the influence of social participation on the efficiency of communal investment expenditure may also be exerted through direct supervision of local authorities’ activities (Asatryan & De Witte, Citation2015). In the case of direct impact of social participation on the efficiency of communal investment expenditure, exercising control by citizens boils down not only to assessing or consulting investment activities undertaken by communal authorities, but also to co-managing activities (for example, by using civic budget), which directly contributes to correcting erroneous policies of local authorities.

It should be noted that social participation can also have a darker side. In this instance, reference can be made to the theory of social capital, which emphasises that individual or collective actions undertaken for the good of an individual or a group may be, at the same time, harmful to other persons and society at large (Numerato & Baglioni, Citation2012). A similar situation may arise in the case of social participation. In particular, there may be influential interest groups in the local government whose objectives are not consistent with those of the local community. By referring directly to communal investment expenditure, the above-mentioned interest groups may lobby for the implementation of investments that are beneficial only for them. In such a situation, the efficiency of investment expenditure decreases because the implemented projects do not contribute to the development of the commune as a whole.

3.2. Additional factors

The participation of citizens in public management is not the only determinant of the efficient management of public funds. Therefore, other factors influencing how public expenditure is shaped on the local government level should be identified. Narbón-Perpiñá and De Witte (Citation2017b) distinguish the following groups of factors affecting local government efficiency: social and demographic, economic, political, financial, geographical and natural as well as institutional and management.

Increasing investment expenditure efficiency may also depend on other aspects of the functioning of communal self-government, which were not mentioned in the Narbón-Perpiñá and De Witte (Citation2017b) review article. In particular, the role of real estate management, spatial management and the use of external sources of financing communal investments should be emphasised here. These factors may turn out to be extremely important, especially in the context of investment expenditures.

In the case of real estate management, the role of the commune in creating appropriate real estate resources for infrastructural investments can be mentioned. A commune, which actively and timely acquires resources for future investments, minimises the risk of failure of planned projects, which in all probability may increase the investment expenditure efficiency.

No less important is spatial planning. In this case, it is primarily a matter of drawing up local spatial development plans. In such a planning document, the areas of potential communal investment are defined. Local spatial development plans are drawn up in a multi-stage process, in which a lot of time is devoted to discussing the future shape of the document. Therefore, the created solutions are well thought out and widely accepted from society. On this basis, it can be concluded that the adoption of a local spatial development plan in a given area should increase the efficiency of communal investment expenditure.

As mentioned earlier, an increase of the examined efficiency may also be accelerated by the smart use of external sources of financing communal investments. External sources of financing are divided into repayable and non-repayable funds. The latter most often concern funds from the European Union, the acquisition of which is conditioned by the preparation of various analyses of the potential costs and benefits of a given investment, which undoubtedly contributes to the implementation of much more efficient investments in local government units.

The above-mentioned factors shaping the efficiency of local government can also be classified according to the degree of dependence on local authorities. Taking this type of criterion into account, it is possible to distinguish between them:

factors fully or predominantly dependent on commune authorities

factors partly dependent on commune authorities

factors fully independent of commune authorities

The first of the above-mentioned groups contains factors, which are fully or predominantly dependent on the activities of the commune authorities. This area includes such factors over which the commune, as a self-government unit, has direct influence, and where the activity of self-government bodies may lead to significant increase or decrease in the level of a given phenomenon. This group includes primarily investment planning instruments, such as long-term investment plans or task budgets. In addition, this group of factors should also include the rational management of real estate, joint investments with other local governments and the use of additional external sources of financing investment. Social participation is also included here, the level of which can be directly shaped by local authorities in the area of a given commune unit using various participation instruments.

Another group concerns factors that are only partly dependent on local authorities. These factors cannot be directly shaped by the authorities, or the influence on them by the commune authorities is negligible. One can mention here, among others, the level of total income of the commune. This factor mainly depends on the state of development of a given commune, and the presence of natural resources or large enterprises. Although the local authorities have the possibility to influence the future income of the commune, this influence is indirect. Another factor which, we estimate, should be included in this group is the level of investment expenditures. It should be noted that the level of such expenditures depends mainly on the available financial resources of the commune, which are the result of income generated by the self-government unit. This group also includes factors describing the number of inhabitants in a commune or the share of councillors with higher education in the commune council. Although the result of direct decisions made by voters, the latter factor is influenced by the local authorities through the election campaign process.

The last group consists of factors fully independent of the commune authorities. This includes, first of all, the type of commune and its specific location. These are shaped neither directly nor indirectly by the commune authorities.

4. Research methodology

4.1. Research sample and time range of the study

The study on the impact of social participation on the efficiency of communal investment expenditures will be conducted on the basis of data from communes of the Małopolska Province. The narrowing down of the analysed local government units to communes of the Małopolska Province results from the lack of availability of data for other provinces. Moreover, cities with county rights, that is, Cracow, the City of Tarnów and the City of Nowy Sącz, were excluded from the study. This is due to the fact that these units are diametrically different from the other communes of the Małopolska Province.

Furthermore, in order to increase the generalisability of research results to all communes in Poland, the compatibility of the selected research sample and population was checked. Two features were examined: the administrative structure of the communes and the average amount of communal investment expenditure per capita. Statistical tests showed that the communes of the Małopolska Province do not differ significantly from the wider population in terms of the two above-mentioned characteristics. Therefore, it may be stated that the research sample, selected in a targeted manner, reflects well the scale of investment activity in all communes in Poland, both in terms of size and structure, as the latter directly depends on the type of a given commune (rural communes have different needs in terms of investment activity in comparison to urban ones). On this basis, it can be reasonably expected that the factors identified in this study affecting the efficiency of communal investment expenditure in the Małopolska Province will also have a significant impact in other local governments in Poland.

The temporal scope of the empirical research covers the period from 2010 to 2016 and also results mainly from the availability of data, in particular in terms of the use of instruments of social participation by the communes. In addition, there are no changes in the administrative structure of the examined communes in this period, which makes the study consistent.

4.2. Specification of regression model

The next stage of the research was the construction of multiple regression models, the aim of which is a statistical analysis of the impact of social participation on the efficiency of communal investment expenditure. The starting point for the creation of these models was the selection of other variables that may affect the efficiency of investment expenditures. This stage is necessary to ensure that the obtained results are not apparent. On the basis of data availability and the literature review, nine control variables were proposed. Basic descriptive statistics for all variables in the regression models are presented in . The initial regression models are cross-sectional in nature. In particular, the average values of the variables from 2010 to 2016 are used. The application of another type of model, for example, a panel model, is not possible due to the very limited access to data, especially in the scope of measuring the level of social participation, as well as the specifics of measuring the efficiency of communal investment expenditures.

Table 2. Descriptive statistics for variables in regression models.

It should be noted that some variables are synthetic in nature, that is, their values are calculated on the basis of several diagnostic characteristics. This occurs in the case of variables concerning: social participation, rational real estate management and the use of external sources of financing communal investments. Also, the dependent variable, which describes the efficiency of communal investment expenditure, was created on the basis of taxonomic analysis. The process of this research is presented in the following subchapters.

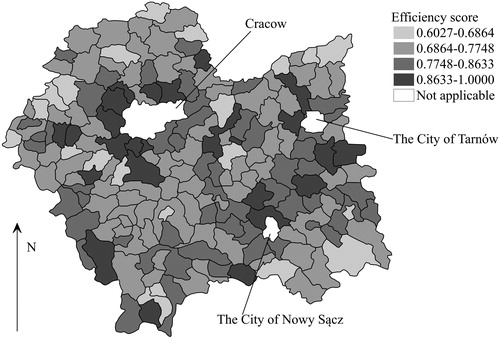

In order to obtain proper model specification, it was checked whether the residuals of the basic models contain spatial autocorrelation. If such autocorrelation is actually present, the regression models that does not take into account spatial dependencies are incorrect due to the problem of omitted variables (Mathur, Citation2019). The possibility of spatial autocorrelation in this study is indicated by other empirical studies on local government efficiency (Balaguer-Coll, Brun-Martos, Márquez-Ramos, & Prior, Citation2019; Geys, Citation2006; Revelli & Tovmo, Citation2007), and that presents the investment expenditure efficiency (using the DEA method) of the investigated communes.

Figure 2. Efficiency scores for examined local government units (using the DEA method). Source: same as .

In order to assess statistically the possibility of spatial dependencies, Moran’s I tests were conducted for the residuals of the basic regression models. The statistics of this test indicated that there is no spatial autocorrelation among the residuals. In addition, we ran the LM-lag and LM-error tests, whose results confirm the absence of spatial autocorrelation both in the dependent variables and in the error terms. For the spatial autocorrelation tests, we used the spatial weight matrix, which was based on the common borders of the analysed local governments units. In particular, the elements of this matrix have two values: 1 – when there is a common border between two communes; 0 – when there is no common border.

On the basis of the above tests, a regression model takes the following form:

(1)

(1)

where

denotes commune;

is the dependent variable calculated using the DEA method or the order-m method;

and

is a set of independent variables,

is the error term.

4.3. Method of measuring social participation, the use of external sources of financing communal investments and rational real estate management

The phenomena describing social participation, the use of external sources of financing communal investments and rational property management are multidimensional in nature, that is, they cannot be described with a single measure. Therefore, in order to assess their level in a given commune, a taxonomic analysis will be used, which makes it possible to describe a given phenomenon with any number of diagnostic features. The process of this study is as follows:

• Selection of variables characterising the investigated phenomenon (a detailed list of diagnostic features is presented in )

Table 3. Set of diagnostic features to calculate independent synthetic variables in the regression model.

• Preliminary analysis of the variables adopted for the study in the scope of:

• level of variability – variables whose coefficient of variation value is equal to or lower than 0.10 should be discarded from further analysis

• correlation with other variables – in case of correlation of a pair of variables exceeding 0.70, one variable from the pair should be discarded

• Conversion of destimulants into stimulants by changing the character of destimulants into the opposite one

• Standardisation of the variables to ensure comparability of the measures adopted for analysis. The zero unitarisation formula is used in this article. The choice of such a standardisation formula is highly beneficial, as it meets all the demands established for this type of transformation. We can highlight here, the non-negative values or stability of ranges of variability of normalised variables. The zero unitarisation formula takes the form:

(2)

where: – normalised value of the jth variable for the ith object,

– the original value of the jth variable for the ith object,

– the maximum value of the jth variable among the ith objects,

– the minimum value of the jth variable among the ith objects

Calculation of a synthetic indicator explaining a given phenomenon. In this article, we use the following formula:

where – value of the synthetic indicator for the ith object,

– number of diagnostic features.

Preliminary analysis of diagnostic features in the scope of variability and mutual correlation allowed to set the final list of characteristics used to estimate synthetic variables in the regression models. In particular, the following diagnostic features were removed from further analysis: and

4.4. Method of the measurement of communal investment expenditure efficiency

The DEA method is used to measure the efficiency of investment expenditure of the communes in the Małopolska Province. This is a non-parametric method that takes into account a specified number of inputs and outputs, and determines the efficiency of each analysed unit on the basis of linear programming (Škuflić, Rabar, & Šokčević, Citation2010). The efficiency of each unit is determined as a quotient of the weighted sum of outputs to the weighted sum of inputs, and then compared to the model observation. Efficient units are on the production frontier and their efficiency value is 1. Conversely, units whose efficiency values calculated with the use of DEA are smaller than unity, are defined as inefficient. Within the framework of the DEA method, one can distinguish output-oriented, input-oriented and non-oriented models. The choice of a particular orientation depends on a number of factors that should be carefully determined in each case. In the study of Polish communal self-governments, one of the prerequisites is the current law on public finance, which specifies that when spending public funds, the administration should be guided by a best-results policy from given expenditures (Public Finance Act, Citation2009, §44). Therefore, an output-oriented model assuming variable returns to scale (BCC-O) was chosen to study the efficiency of communal investment expenditures. This model can be presented in the following mathematical formula:

(4)

(4)

where:

– efficiency of the o-th object,

– variable providing the convexity condition,

– number of inputs,

– number of outputs,

– number of objects,

– rth weight of a given output,

– ith weight of a given input,

– the ith input for the jth object,

– the rth output for the jth object.

The above model, which assumes variable returns to scale, seems to be more accurate due to the different nature of the analysed units. This conclusion is also confirmed by Sekuła and Julkowski (Citation2017), who investigated the efficiency of communal expenditures internationally.

Furthermore, it should be noted that the DEA method has several drawbacks. In particular, the sensitivity to outliers and susceptibility to measurement errors should be mentioned here (Balaguer-Coll et al., Citation2019). Therefore, we have decided to use a robust non-parametric methodology, namely the order-m method, which is outlined in detail in the Daraio and Simar (Citation2005) article. In the order-m method we set the size of the artificial reference sample at 140 (from this value the results were stable) and the number of resampling replications at 2000.

The use of the DEA and order-m methods to study local government efficiency also requires the definition of inputs and outputs. In this study, a variable describing the average value of investment expenditures of a municipality per capita in the period 2010–2016 was used as an input. To the contrary, defining the effects of these expenditures is a much more difficult task. The literature review conducted by Narbón-Perpiñá and De Witte (Citation2017a) revealed that in the field of local government efficiency research, variables describing, among others, population size, building area, administrative services, saturation of technical and social infrastructure, quality of municipal services, quality of health services, quality of social services and the level of public safety were assumed as the outputs. Moreover, it should be emphasised that, in previous studies, several variables were taken as outputs or one synthetic variable was calculated on the basis of selected diagnostic features. In our opinion, the most accurate proposal in this respect was presented by Zimny (Citation2008), who adopted as indicator the pace of socio-economic development of the commune. This indicator is based on the taxonomic method presented in the previous subchapter, but instead of static values of diagnostic variables, it adopts values of slope parameters of trend lines, which are estimated for the assumed time period. Treating the problem of measuring the effects of communal investment expenditures in this way ensures that their dynamics are taken into account. It should be noted that the indicator outlined by Zimny (Citation2008), at its basis, assumes diagnostic features describing the development of the commune from an economic aspect (e.g. new jobs) and a social aspect (e.g. higher number of kindergartens). Determining the effects of communal investment expenditures in this way is extremely relevant, because the new infrastructure that results from these expenditures is one of the main factors driving the development of a given territory (Wołowiec & Skica, Citation2013). To sum up, this article uses the approach outlined by Zimny (Citation2008) to determine the effects of communal investment expenditures. Conversely, diagnostic features determining the pace of the socio-economic development of communes were selected on the basis of the quality and availability of public statistics data (none of the features was rejected after a preliminary analysis of data consisting in checking the variation coefficients and mutual correlation). A detailed list of the mentioned features is presented in .

Table 4. Set of diagnostic features used to assess the pace of socio-economic development of the examined communes.

5. Research results

5.1. Baseline regression models

The first stage of the empirical research was to estimate the efficiency of investment expenditures in communes of the Małopolska Province. Using the DEA method, the study revealed that only five communes out of 179 units proved to be efficient in terms of investment expenditure. Similar results were observed with the order-m method. In this case, ten municipalities were shown to be efficient or super-efficient. It should be noted that rural communes dominate among efficient units, irrespective of the efficiency measurement method.

Upon estimating the efficiency of communal investment expenditures, the next stage of the analysis is estimation of the previously defined regression models. Detailed results of this study are presented in . It should be noted that the basic models include a number of insignificant variables. Therefore, the stepwise regression procedure with backward elimination was applied.

Table 5. The results of regression model estimations.

The final regression models was positively verified in terms of collinearity and residuals normality (at the level of ). Moreover, an HC estimator was used because of the high probability of heteroskedasticity.

Based on the results of the final models, it can be concluded that apart from the constant, only four variables turned out to be significant, in particular variables and

In the case of variable

describing the location of the commune in the Cracow metropolitan area, an increase in its value by 1 results in an increase in the dependent variable by ca. 0.03, while other factors remain unchanged. This means that communes located closer to Cracow are more efficient than other communes. This conclusion is consistent with expectations and other empirical studies (Afonso & Fernandes, Citation2008; Šťastná & Gregor, Citation2011). Moreover, it should be noted that variable

can be classified into a group of factors fully independent from local authorities.

The next variable, which turned out to be significant in the models, explains the level of investment expenditures of the commune per capita. In this case, the estimated parameter has a negative sign, which means that the increase in investment expenditures of the commune results in a decrease in the efficiency of these expenditures. In particular, along with other unchanged factors, the increase in investment expenditures by PLN 100 causes a decrease in the explained variable by ca. 0.01. It should also be emphasised that the level of investment expenditures depends mainly on the income obtained by the commune, which confirms the value of the correlation coefficient between these variables, which in this study is equal to 0.70. Therefore, the parameter sign obtained with variable should not raise any doubts. This is due to the fact that communes with lower income may try to spend their funds in a much more rational way. The negative correlation between efficiency and investment expenditure is also confirmed by studies conducted by Šťastná and Gregor (Citation2011), as well as by Sekuła and Julkowski (Citation2015). Moreover, it should be noted that variable

can be classified into the group of factors partly dependent on local authorities.

Another important variable in the final models, describes the level of use of additional, external sources of financing investments by the commune. It should be noted that this type of sources can include non-repayable resources such as grants, subsidies, EU funds, as well as repayable resources such as loans, credits or bond issues. Active diversification of investment financing sources through rational use of external funds, especially non-repayable ones, may significantly increase the efficiency of communal investment expenditures. It should be stressed that, to the best of our knowledge, there are no empirical studies that analyse the impact of this variable on local government efficiency so widely. Only the components of the

synthetic measure calculated by us have been taken into account in the analyses conducted so far. One can recall here the work of Zioło (Citation2012), which indicated that the level of loans taken out is positively correlated with the efficiency of investment expenditure. Research in this area was also conducted by Karbownik and Kula (Citation2009), who proved that the use of EU funds by the commune significantly increases expenditure efficiency.

The final significant variable in the above models concerns the level of social participation in a given local government unit. The estimated regression parameter turned out to be positive, which means that an increase in social participation in a given commune contributes to improving the efficiency of spending of communal investment funds. In more detail, an increase in this synthetic measure by 0.01 or 0.1 results in an increase in the value of the dependent variable by 0.0012 and 0.012, respectively, while other factors remain unchanged. The result obtained for this variable is consistent with the theoretical considerations presented in this article. It should also be noted that both the variable describing social participation and the variable concerning the use of additional sources of investment financing by the commune belong to the group of factors that are mostly dependent on local authorities.

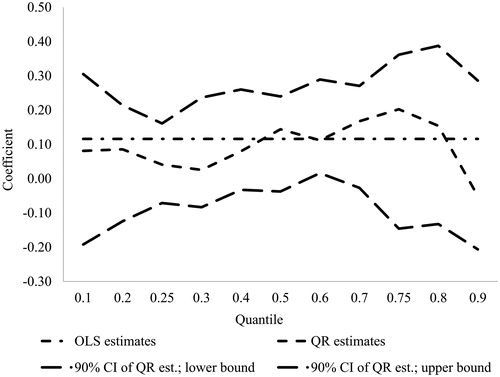

Moreover, we decided to take a closer look at the relationship between social participation and the analysed efficiency. Therefore, in order to describe fully the above dependence we adopted the quantile regression method. Detailed results of this study are presented in and . In particular, the findings reveal an inverted U-shaped pattern among quantile regression coefficients for the variable describing social participation. This result, however, requires further in-depth research because of the very wide confidence interval.

Figure 3. The coefficients of the quantile regression model. Source: same as .

5.2. Robustness checks

After estimating the baseline regression models (see ), we considered some robustness checks to control our results. In particular, we have estimated several new models (only for variables significant in the baseline regression models, i.e.

and

) taking into account the following problems:

A potential problem of endogeneity of variable

The possibility of a time lag between the social participation variable and the studied efficiency. It should be noted that citizens dissatisfied with public spending can put pressure on the authorities. It may take several years, however, for policy-makers to correct wrong actions. In order to control the occurrence of this problem, we have included the variables explaining the level of social participation in the examined communes for the years 2007–2013, 2008–2014 and 2009-2015 in additional regression equations. It should be added that we have estimated models that take into account both the current value of the

In addition, the possibility of a joint occurrence of time lag between social participation and efficiency, as well as the problem of endogeneity were considered.

The results of the estimation of additional regression models (see ) confirmed the conclusions of that the current level of social participation has a significant impact on the studied efficiency. In particular, the variable was significant in almost all additional models, in some cases after the elimination of insignificant variables. There is little support, however, for the conclusion that the lagged variable of social participation (for 2008–2014) also has a significant impact on the dependent variable.

Table 6. Estimations of additional OLS regression models.

Summarising the results obtained with the use of all regression models, it can be stated that the research hypothesis presented at the beginning of the article, namely that social participation is one of the factors enabling citizens to supervise politicians (agents), which leads to an increase in the efficiency of their actions, including their spending of public investment funds, has been positively verified.

6. Conclusion

This article attempts to identify factors that have a significant impact on the efficiency of communal investment expenditures. The theoretical framework of this work divides these factors into three groups: those independent of commune authorities, those partly dependent on commune authorities, and those predominantly or fully dependent on commune authorities. The research findings confirm that the efficiency of communal investment expenditures is determined by a set of factors with varying degrees of dependence on commune authorities. One of these factors is social participation, a higher level of which leads to an increase in the aforementioned efficiency. It should be stressed that the positive impact of social participation on the efficiency of communal investment expenditure confirmed in this article is consistent with other studies analysing local government efficiency, broadly understood, and carried out in Italy (Giordano et al., Citation2009), Norway (Borge et al., Citation2008; Bruns & Himmler, Citation2011; Revelli & Tovmo, Citation2007), Germany (Asatryan & De Witte, Citation2015; Geys et al., Citation2010), Spain (Bosch et al., Citation2012) and the Czech Republic (Šťastná & Gregor, Citation2014).

Moreover, to the best of the author’s knowledge, this study is the first of its type not only to be conducted for local government units in Poland, but also to take into account a very wide range of social participation processes. Studies so far have focused almost exclusively on turnout in local government elections. Nevertheless, many aspects of public participation are still not included in our study. This is due to the fact that there is significant data deficit in the Polish public statistics. For this reason, the scope of the study was narrowed down to include only the communes of the Małopolska Province. Therefore, it should be stated that this study is a starting point for further analyses in the context of the impact of social participation on the efficiency of communal investment expenditures and, more broadly, the efficiency of local government. In particular, subsequent studies could review the methodology used in this study and assess the impact of social participation on the efficiency of investment expenditure in cities with county rights or, depending on data availability, in all communes in Poland. Furthermore, the methodology of this study could be used to assess the efficiency of the investment expenditure of local governments in other countries, but only after appropriate adjustment, which results from the very different specificities of local government units around the world.

In addition, the obtained research results have extremely important implications for both the activities of local policy-makers and the local community. In particular, local authorities should support and enable citizens to participate in public decision-making through the implementation of various instruments of public participation. At the same time, the willingness to participate in public life should come from the local community itself. Residents should take a keen interest in the activities of their representatives and how they exercise the power, as this may significantly increase the efficiency of local government. It should also be stressed that these implications are universal, that is, they can be applied to local authorities in different countries. They are especially important, however, for countries where there is already a certain framework (legal, social, cultural, etc.) for the development of participatory processes, while at the same time citizen participation in decision-making remains at low levels.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Afonso, A., & Fernandes, S. (2008). Assessing and explaining the relative efficiency of local government. The Journal of Socio-Economics, 37(5), 1946–1979. doi:10.1016/j.socec.2007.03.007

- Arnstein, S. R. (1969). A ladder of citizen participation. Journal of the American Planning Association, 35(4), 216–224.

- Asatryan, Z., & De Witte, K. (2015). Direct democracy and local government efficiency. European Journal of Political Economy, 39(C), 58–66. doi:10.1016/j.ejpoleco.2015.04.005

- Balaguer-Coll, M. T., Brun-Martos, M. I., Márquez-Ramos, L., & Prior, D. (2019). Local government efficiency: Determinants and spatial interdependence. Applied Economics, 51(14), 1478–1417. doi:10.1080/00036846.2018.1527458

- Beirele, T. C., & Cayford, J. (2002). Democracy in practice. Public participation in environmental decisions. Washington, DC: Routledge.

- Borge, L. E., Falch, T., & Tovmo, P. (2008). Public sector efficiency: The roles of political and budgetary institutions, fiscal capacity, and democratic participation. Public Choice, 136(3-4), 475–495. doi:10.1007/s11127-008-9309-7

- Bosch, N., Espasa, M., & Mora, T. (2012). Citizen control and the efficiency of local public services. Environment and Planning C: Government and Policy, 30(2), 248–266. doi:10.1068/c1153r

- Bruns, C., & Himmler, O. (2011). Newspaper circulation and local government efficiency. Scandinavian Journal of Economics, 113(2), 470–492. doi:10.1111/j.1467-9442.2010.01633.x

- Da Cruz, N. F., & Marques, R. C. (2014). Revisiting the determinants of local government performance. Omega, 44, 91–103. doi:10.1016/j.omega.2013.09.002

- Daraio, C., & Simar, L. (2005). Introducing environmental variables in nonparametric frontier models: A probabilistic approach. Journal of Productivity Analysis, 24(1), 93–121. doi:10.1007/s11123-005-3042-8

- Felis, P., & Rosłaniec, H. (2017). Local authority tax policy in Poland. Evidence from the union of polish metropolises. Contemporary Economics, 13(1), 49–62.

- Geys, B. (2006). Looking across borders: a test of spatial policy interdependence using local government efficiency ratings. Journal of Urban Economics, 60(3), 443–462. doi:10.1016/j.jue.2006.04.002

- Geys, B., Heinemann, F., & Kalb, A. (2010). Voter involvement, fiscal autonomy and public sector efficiency: Evidence from German municipalities. European Journal of Political Economy, 26(2), 265–278. doi:10.1016/j.ejpoleco.2009.11.002

- Giordano, R., Tommasino, P., & Casiraghi, M. (2009). Behind public sector efficiency: The role of culture and institutions. Retrieved from CiteSeerX http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.526.915&rep=rep1&type=pdf.

- International Monetary Fund. (2019). Data portal. Retrieved from https://data.imf.org.

- Karbownik, B., & Kula, G. (2009). Efektywność sektora publicznego na poziomie samorządu lokalnego [Efficiency of the public sector at the local government level]. Materiały i Studia, 242, 1–49.

- Kik, I., & Nalepka, A. (2016). Uwarunkowania źródeł finansowania inwestycji infrastrukturalnych w gminach województwa małopolskiego [Selecting source of finance for infractructural investment at municipal level in Malopolskie Voivodship]. Acta Universitatis Nicolai Copernici Ekonomia, 47(2), 93–108. doi:10.12775/AUNC_ECON.2016.006

- Legiędź, T. (2005). Motywy działania polityków w świetle teorii wyboru publicznego [The behaviour of politicians from a public choice perspective]. Annales. Etyka w Życiu Gospodarczym, 8(1), 277–283.

- Local Bank Data of Statistics Poland. (2019). Data portal. Retrieved from https://bdl.stat.gov.pl/BDL/start.

- Marcinek, K., Czempas, J., & Kobiński, T. (2014). Rating jako narzędzie oceny wiarygodności kredytowej inwestora samorządowego [Rating as a tool of local self-government’s credit performance assessment]. Studia Ekonomiczne, 177, 110–124.

- Martinez-Vazquez, J. (2015). Mobilizing financial resources for public service delivery and urban development. In The Challenge of Local Government Financing in Developing Countries (pp. 15–36). Nairobi: United Nations Human Settlements Programme.

- Mathur, S. (2019). Impact of an urban growth boundary across the entire house price spectrum: The two-stage quantile spatial regression approach. Land Use Policy, 80, 88–94. doi:10.1016/j.landusepol.2018.09.011

- Ministry of Finance. (2019). Data portal. Retrieved from https://www.gov.pl/web/finanse/sprawozdania-budzetowe.

- Ministry of Funds and Regional Policy. (2019). Data portal. Retrieved from https://www.ppp.gov.pl/.

- Narbón‐Perpiñá, I., & De Witte, K. (2017a). Local governments’ efficiency: A systematic literature review – part I. International Transactions in Operational Research, 25(2), 431–468. doi:10.1111/itor.12364

- Narbón‐Perpiñá, I., & De Witte, K. (2017b). Local governments’ efficiency: A systematic literature review – part II. International Transactions in Operational Research, 25(4), 1107–1136. doi:10.1111/itor.12389

- Numerato, D., & Baglioni, S. (2012). The dark side of social capital: An ethnography of sport governance. International Review for the Sociology of Sport, 47(5), 594–611. doi:10.1177/1012690211413838

- Organisation for Economic Co-operation and Development. (2019). Data portal. Retrieved from https://stats.oecd.org/.

- Regional Audit Chamber in Cracow. (2019). Data portal. Retrieved from http://www.bip.krakow.rio.gov.pl/?c=410.

- Revelli, F., & Tovmo, P. (2007). Revealed yardstick competition: Local government efficiency patterns in Norway. Journal of Urban Economics, 62(1), 121–134. doi:10.1016/j.jue.2006.11.004

- Sekuła, A., & Julkowski, B. (2015). Pomiar efektywności wydatków budżetowych dużych miast w Polsce [Measuring polish cities expenditure efficiency]. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu, 404, 265–282. doi:10.15611/pn.2015.404.18

- Sekuła, A., & Julkowski, B. (2017). Zastosowanie metody DEA w ocenie efektywności wydatków jednostek samorządu terytorialnego - przegląd literaturowy wyników dotychczasowych badań w przestrzeni europejskiej [Application of DEA method in the evaluation of the efficiency of local government units’ expenditures - a literature review of the results of previous research in the european area]. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu, 477, 220–231. doi:10.15611/pn.2017.477.21

- Škuflić, L., Rabar, D., & Šokčević, S. (2010). Assessment of the efficiency of Croatian counties using data envelopment analysis. Economic Research-Ekonomska Istraživanja, 23(2), 88–101.

- Stańczyk Foundation. (2019). Data portal. Retrieved from http://www.stanczyk.org.pl/przyjazny-urzad/.

- Šťastná, L., & Gregor, M. (2011). Local government efficiency: Evidence from the Czech municipalities. Retrieved from SSRN https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1978730.

- Šťastná, L., & Gregor, M. (2014). Public sector efficiency in transition and beyond: evidence from czech local governments. Applied Economics, 47(7), 680–699. doi:10.1080/00036846.2014.978077

- Statistical Office in Cracow. (2019). Data portal. Retrieved from https://krakow.stat.gov.pl/.

- Strange, J. H. (2008). Citizen participation in community action and model cities programs. In N. C. Roberts & M. E. Sharp (Eds.), The age of direct citizen participation (pp. 124–125). New York, NY: Routledge.

- Supreme Audit Office. (2019). Ustalanie i egzekwowanie przez gminy województwa warmińsko-mazurskiego opłaty adiacenckiej [The setting and enforcement of the betterment levy by the communes of the Warmińsko-Mazurskie Province]. Retrieved from https://www.nik.gov.pl.

- Trojanek, R. (2016). The impact of green areas on dwelling prices: the case of Poznań City. Entrepreneurial Business and Economics Review, 4(2), 27–35. doi:10.15678/EBER.2016.040203

- Ustawa z dnia 27 sierpnia 2009 r. o finansach publicznych [Public Finance Act. (2009)] (Dz. U. z 2009 r. Nr 157, poz. 1240 z późn. zm.).

- Witkowski, J., & Kiba-Janiak, M. (2014). The role of local governments in the development of city logistics. Procedia - Social and Behavioral Sciences, 125, 373–385. doi:10.1016/j.sbspro.2014.01.1481

- Wołowiec, T., & Skica, T. (2013). The instruments of stimulating entrepreneurship by local government units (lgu’s). Economic Research-Ekonomska Istraživanja, 26(4), 127–146. doi:10.1080/1331677X.2013.11517635

- Zimny, A. (2008). Uwarunkowania efektywności inwestycji gminnych w sferze infrastruktury technicznej [Determinants of the efficiency of municipal investments in the sphere of technical infrastructure]. Konin: Wydawnictwo Państwowej Wyższej Szkoły Zawodowej w Koninie.

- Zioło, M. (2012). Modelowanie źródeł finansowania inwestycji komunalnych a efektywność wydatków publicznych [Modeling the sources of financing municipal investments and the efficiency of public spending]. Warszawa: Wydawnictwo CeDeWu.