?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper evinces the ability of gold to avoid risks during periods with great fluctuations in the Bitcoin market. We apply bootstrap full- and subsample rolling-window Granger causality tests to explore the causal relationship between Bitcoin price (BCP) and gold price (GP). The empirical results show that an increase in BCP can cause GP to decrease, indicating that the prosperity of the Bitcoin market undermines the hedging ability of gold. However, a decrease in BCP causes GP to increase, and it also emphasizes that the ability of gold to avoid risks persists. Hence, the status of gold will not be completely threatened by Bitcoin, and they are complementary to each other instead of in competition. In turn, both positive and negative influences of GP on BCP suggest that fluctuations in BCP can be predicted through the gold market. In situations of severe global uncertainty and complicated investment environments, investors can benefit from complementary markets to optimize their asset allocation. Additionally, countries can grasp the trends in Bitcoin and gold prices to prevent large fluctuations in both markets and to reduce the uncertainty of the financial system.

1. Introduction

The main purpose of this paper is to investigate whether Bitcoin will threaten the status of gold in hedging risks. Bitcoin was founded by Satoshi Nakamoto (Harvey, Citation2014), who established a peer-to-peer electronic cash system that is not controlled by the central bank (Nakamoto, Citation2008). The scarcity (the total amount of Bitcoin is 21 million) and high “mining” costs of Bitcoin are similar to those of gold, referring to the total amount of gold in the world being limited and the expenditure for unearthing it being enormous (Hurlburt & Bojanova, Citation2014). In addition, the hedging ability of Bitcoin is as a medium of exchange, which is also a property of gold and the U.S. dollar (Dyhrberg, Citation2016a). Bitcoin is also known as “digital gold” (Arsov, Citation2017; Mckay & Peters, Citation2018; Smith, Citation2014), and it could threaten the status of the real gold. Although there might be certain threats to the gold market, we cannot deny the important role that gold plays in managing portfolio risks (Gkillas & Longin, Citation2019). The average monthly volatility of Bitcoin price (BCP) is greater than that of gold price (GP), but the lowest monthly volatility of BCP is less than the highest volatility of GP (Dwyer, Citation2015). Thus, Bitcoin and gold are more likely to be complementary to each other instead of in competition (Bouoiyour, Selmi, & Wohar, Citation2019). The risks of a portfolio (gold, oil and equities) with Bitcoin are fewer than an investment strategy without it (Guesmi, Saadi, Abid, & Ftiti, Citation2019). However, this view cannot always be supported, showing that Bitcoin cannot threaten the status of gold. Goldman SachsFootnote1 pointed out that Bitcoin cannot replace gold due to the restrictions on anti-money laundering and counterterrorism financing regulations. Additionally, the Bitcoin market attracts speculative funds, which attract institutional investors only with difficulty. Bitcoin faces the risks of hacking and theft, indicating low security in its market (Bradbury, Citation2013; Mauro, Kumar, Chhagan, & Sushmita, Citation2018; Zaghloul, Li, Mutka, & Ren, Citation2019). Moreover, the fluctuations in BCP are greater than those in currencies and GP, and Bitcoin cannot be considered an asset to diversify investment risks (Yermack, Citation2013). In general, the threats of the Bitcoin market to gold’s status have not been clearly explained. To resolve this major issue, this paper explores the Granger causality between BCP and GP. The interaction between these two variables is beneficial not only for investors to avoid enormous losses and maintain their wealth by diversifying investment risks but also for countries to prompt the stable development of their national financial systems by preventing the large fluctuations of Bitcoin and gold markets. However, few studies have investigated the time-varying causality between these two variables, and this paper attempts to fill the gaps in the existing studies on the mutual influence between BCP and GP.

There are several marginal contributions to this paper. First, the previous studies have not achieved consistent results about the threats posed by Bitcoin to the gold market. Some studies have supported the hedging ability of Bitcoin (Aggarwal, Santosh, & Bedi, Citation2018; Gkillas & Longin, Citation2019; Shahzad, Elie, David, Ladislav, & Brian, Citation2019), while others have reported that gold can perform better than Bitcoin to hedge risks (Al-Yahyaee, Mensi, & Yoon, Citation2018; Klein, Hien, & Walther, Citation2018; Kubát, Citation2015). Additionally, they have underscored that there is an influence from GP to BCP or vice versa (Bouri, Gupta, Lahiani, & Shahbaz, Citation2018; Obryan, Citation2019; Zhu, Dickinson, & Li, Citation2017). However, it can be obviously observed that mutual influences exist in these two variables; thus, one-way influence cannot reflect the relationship between Bitcoin and gold markets. This paper is a pioneering effort to resolve the issue of whether the status of gold is threatened by Bitcoin by examining the time-varying Granger causal relationship between BCP and GP. The results evince that the status of gold will not be completely threatened by the Bitcoin market, and these markets are complementary instead of competitive. In addition, the interaction between BCP and GP provides revelations to investors, who should weigh and invest in Bitcoin and gold markets, which can diversify investment risks and maintain their wealth. Additionally, they can avoid the significant losses caused by plunges in the Bitcoin or gold market. The implication for countries is that they can grasp the trends of BCP and GP and implement relevant policies to prevent the large fluctuations in Bitcoin and gold prices. Then, they can prompt the stable development of the national financial system. Furthermore, the causal relationship between BCP and GP can vary over time, and it has not been clearly explored in the existing studies. Thus, to ensure the robustness of the empirical results, we employ the bootstrap subsample rolling-window causality test (Balcilar, Ozdemir, & Arslanturk, Citation2010). Then, we obtain the nonconstant parameters in the test models, as well as the time-varying relationship between these two variables.

The structure of the rest of this paper is organized as follows. Section 2 reveals the related literature on this subject. Section 3 presents the tests of parameter stability and Granger causality testing. Section 4 describes the data. Section 5 shows the results of the empirical analysis. Section 6 summarizes the study.

2. Literature review

Since the birth of Bitcoin, its hedging ability and relationship with gold have attracted great attention. Dyhrberg (Citation2016a) indicated that Bitcoin plays an important role in portfolio management, revealing several similarities to gold and the dollar and indicating hedging ability. Additionally, Dyhrberg (Citation2016b) emphasized that Bitcoin has a similar hedging ability to gold, and it can hedge against stocks in the Financial Times Stock Exchange Index and against the U.S. dollar in the short term. Aggarwal et al. (Citation2018) constructed six asset classes (equity, fixed income, commodities, real estate, gold and alternative investments) and found that portfolios including Bitcoin can obtain more risk-adjusted returns, also indicating that Bitcoin can be viewed as an investment alternative with huge potentiality. Gajardo, Kristjanpoller, and Minutolo (Citation2018) reported that, compared to other real currencies, BCP has a greater multifractal spectrum on its cross-correlation with the West Texas Intermediate (WTI), GP and Dow Jones Industrial Average (DJIA), also indicating that Bitcoin should be gradually adopted by the public. Qureshi, Rehman, and Qureshi (Citation2018) pointed out that the central bank should save other safe haven assets in reserves due to the hedging ability of gold, which is only limited to the short term. Gkillas and Longin (Citation2019) revealed that Bitcoin can be viewed as “digital gold” (also Othman, Alhabshi, & Haron, Citation2019), but real gold is still effective in diversifying investment risks. Guesmi et al. (Citation2019) suggested that Bitcoin has a place in hedging risks, and it can be viewed as an asset in a portfolio that also includes gold, oil and equities (Su, Khan, Tao, & Nicoleta-Claudia, Citation2019; Su, Li, Chang, & Oana-Ramona, Citation2017). Through the analysis of several stock market indices (developed and emerging economies, such as the U.S. and China), Shahzad et al. (Citation2019) pointed out that the hedging abilities of Bitcoin and gold are time varying and inconsistent across different stock markets. The existing studies have underscored that Bitcoin can be a hedge or a safe haven to diversify investment risks. Although there are threats to the status of gold, its ability to hedge risks has still not disappeared.

However, the view that the hedging ability of Bitcoin and its market threatens gold’s status cannot always be supported. Yermack (Citation2013) suggested that the daily exchange rates of Bitcoin have nearly no relationship with gold and currencies, and Bitcoin plays no role in diversifying or hedging risks. Baek and Elbeck (Citation2015) revealed that the Bitcoin market is highly speculative instead of an investment vehicle. Kubát (Citation2015) underlines that the risks of Bitcoin are severer than other assets, such as currencies, gold and stocks, which also indicates that Bitcoin cannot be viewed as a real currency since the value storage function is poor. Al-Yahyaee et al. (Citation2018) evidence that the efficiency of gold, stock and currency markets are greater than Bitcoin market, due to it has characteristics with stronger long-memory and multifractality. Klein et al. (Citation2018) argue that Bitcoin cannot be considered as an asset to hedge risks, while gold plays a significant role in the financial system especially during the periods with market distress. Symitsi and Chalvatzis (Citation2019) believe that if investors employ a battery of economic instruments, the portfolio that includes Bitcoin has little returns.

The previous studies have mainly explored the one-way influence from GP to BCP or vice versa. Kristoufek and Scalas (Citation2015) chose several variables, such as GP, which is denominated in Swiss francs, to analyze the main drivers of BCP. They found that BCP is not related to the dynamics of GP, and it is obvious that Bitcoin cannot be considered a safe haven. Zhu et al. (Citation2017) pointed out the determinants of BCP, and their conclusion was that the greater impact is the U.S. dollar, while that of GP is the smallest. Employing the nonlinear autoregressive distributed lag (NARDL) model, Bouri et al. (Citation2018) found that GP has an asymmetric, nonlinear and quantile-dependent influence on BCP. Obryan (Citation2019) pointed out that, as one of the BCP determinants, GP is negatively related to the price of Bitcoin. In summary, the mutual influences between BCP and GP have not been explored in depth, and there is no consistent answer to the question of whether Bitcoin will threaten the status of gold. Moreover, the existing studies have not considered the nonstable parameters in Granger causality test models or identified the time-varying interaction and direction between BCP and GP. In this paper, we perform the bootstrap subsample rolling-window causality test (Balcilar et al., Citation2010) to investigate the effects from BCP to GP and the important role of gold in the Bitcoin market.

3. Methodology

3.1. Bootstrap full-sample causality test

The Granger causal relationship test statistics, which are based on the traditional vector autoregression (VAR) model, cannot obey standard asymptotic distributions. Thus, the residual-based bootstrap (RB) method’s critical values, developed by Shukur and Mantalos (Citation1997), can prevent inaccurate results and improve the Granger causality test. In addition, they emphasize that the RB method can be used for the causality tests with standard asymptotic distributions and those with small samples. Shukur and Mantalos (Citation2000) developed the likelihood ratio (LR) tests, which can be modified by the characteristics of power and size. This paper employs the RB-based modified-LR statistic to examine the Granger causality between BCP and GP. The bivariate VAR (p) process is constructed as EquationEquation (1)(1)

(1) :

(1)

(1)

where p is optimal lag order, that is selected by the Schwarz Information Criterion (SIC). The VAR (p) process with two variables can split

into BCP and GP, that is

In addition, we introduce the U.S. dollar index (USDX) as a control variable (Dyhrberg, Citation2016a; Zhu et al., Citation2017), then the VAR (p) process can be rewritten as EquationEquation (2)

(2)

(2) :

(2)

(2)

where

is a white-noise process with zero mean and covariance matrix.

i, j = 1, 2 and L is a lag operator, we have

According to EquationEquation (2)(2)

(2) , we can examine the null hypothesis that GP does not Granger cause BCP (

for k = 1, 2, ……, p). This null hypothesis can be accepted if GP has no impact on BCP and vice versa. Similarly, the null hypothesis that BCP does not Granger cause GP (

for k = 1, 2, ……, p) can also be accepted.

3.2. Parameter stability test

It is usually not realistic to assume for the bootstrap full-sample causal relationship test that the parameters in the VAR system are invariable. Therefore, it is not appropriate to apply the full-sample test if the parameters undergo structural changes. Hence, we employ the Sup-F, Ave-F and Exp-F tests, developed by Andrews (Citation1993) and Andrews and Ploberger (Citation1994), to evince the stability of the parameters. The Sup-F test can identify the sudden structural changes in the time series and VAR system. The Ave-F and Exp-F tests can explore whether or not the parameters have gradually evolved along the time trajectory. This paper also uses the Lc statistics test (Hansen, Citation1992; Nyblom, Citation1989) to examine whether the parameters follow a random walk process. The Sup-F, Ave-F, Exp-F and Lc tests can demonstrate the stability of the parameters, and if structural changes exist, the relationship between these two variables is time varying. Thus, we can apply the subsample test to investigate the Granger causality between BCP and GP.

3.3. Bootstrap subsample rolling-window causality test

Balcilar et al. (Citation2010) developed this method to split the overall time series into small samples, based on the rolling-window width. The selection of the rolling-window width is complex, a small one may lead to biased test results. A large one may cause the times of scrolls to reduce, though it will make the test results more accurate. In order to solve this problem, Pesaran and Timmermann (Citation2005) highlight that if the parameter stability does not hold, the rolling-window width should not be less than 20. Then, based on the rolling-window width, the split small samples are gradually scrolled from the start to the end of the overall sample. The specific steps are as follows. First, suppose the length of the time series is T, and the rolling-window width is l. The end of each split small sample is l, l + 1,……, T, and T-l + 1 subsamples can be achieved. Second, by applying the RB-based modified-LR test, every subsample can obtain a Granger causal relationship. Third, by calculating all of the p-values and LR statistics of each subsample in the chronological order, the results of the bootstrap subsample rolling-window test can be obtained. The mean values of a large number of estimations ( and

where Nb is the frequency of the repetitions.

and

are the parameters in the VAR system) reveal the impact of GP on BCP and the effect from BCP to GP. Additionally, this paper applies a 90% confidence interval, with the corresponding lower and upper bounds, indicating that the 5th and 95th quantiles of

and

respectively (Balcilar et al., Citation2010; Su, Khan, et al., Citation2019).

4. Data

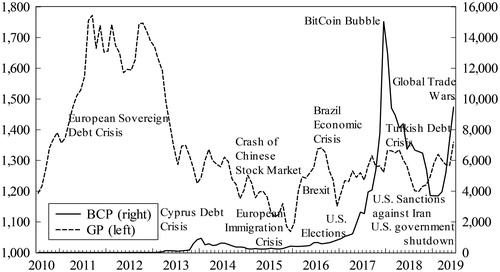

We choose monthly data, covering the period from 2010:M7 to 2019:M6, to explore the causal relationship between the price of Bitcoin and gold and further to resolve the issue of whether the status of gold is threatened by Bitcoin. On July 11, 2010, Bitcoin was first reported by the technology media Slashdot, attracting a large number of traders to the Bitcoin market. Also in July 2010, the first Bitcoin trading platform MT.Gox was developed, prompting the public to conduct Bitcoin transactions. We use Bitcoin price (BCP), which is denominated in U.S. dollarsFootnote2, to represent the international digital currency market. Since then, BCP has increased dramatically, and Bitcoin is considered an asset to hedge risks due to economic crises and geopolitical events (Bouri, Gupta, Tiwar, & Roubaud, Citation2017; Dyhrberg, Citation2016b). Moreover, gold is a hedge or safe haven in the traditional view, and Bitcoin is also known as “digital gold” (Arsov, Citation2017; Mckay & Peters, Citation2018; Smith, Citation2014). Since U.S. President Donald J. Trump has launched trade wars and geopolitical conflicts with Iran, public panic has increased the demand for safe-haven assets (e.g., gold and Bitcoin). Thus, the relationship between gold price (GP) and BCP can be described as one falling and the other rising. However, BCP and GP moved in the same direction in June 2019Footnote3 due to the intensification of trade wars and global uncertainty. We can observe that BCP could have a close relationship with GP. Thus, we choose the price of gold, which is also denominated in U.S. dollarsFootnote4, to represent the international gold market. Therefore, there could be causality between the real and digital (Bitcoin) gold markets.

shows that BCP does not always move in the same direction as GP. When Bitcoin was new, BCP was at a very low level due to the lack of investors and formal exchanges. The Cyprus debt crisis in 2013 led investors to consider that digital currencies could be a valuable asset to hedge risks and maintain wealth. Further, this crisis caused demand for Bitcoin to increase, also causing a rise in BCP. However, since the public is more willing to hold Bitcoin, it sells gold, which causes GP to fall during this period. Additionally, this negative relationship can be observed in December 2013. Since 2014, BCP has decreased, and GP is also on a downward trend, showing a positive relationship between these two variables. Moreover, both internal (e.g., investment boom and speculative bubbles) and external (e.g., Brexit, Brazil economic crisis and U.S. election) factors caused BCP to rise sharply since 2016. In 2017, BCP increased by nearly 2000% over the whole year, while GP did not always move in the same direction. After Trump became President of the U.S., global trade wars and geopolitical conflicts with Iran led to an increase in public demand for hedging or safe-haven assets. Since both Bitcoin and gold have a certain ability to avoid risks, investors are willing to hold the asset that they consider more rewarding, so BCP and GP have an inverse relationship during this period. However, the negative relationship between these two variables cannot be supported in June 2019. In addition, both BCP and GP are denominated in U.S. dollars, which could affect the fluctuations in Bitcoin and gold markets. An interest rate cut could decrease the value of the U.S. dollar (e.g., quantitative easing policy), which could lead to increases in BCP and GP and vice versa (e.g., Federal Reserve System (Fed) interest rates hike). Thus, the U.S. dollar (USDX) might have influences on the Granger causality between BCP and GP; thus, we choose this indexFootnote5 as a control variable in EquationEquation (2)(2)

(2) . In summary, the causal relationship between BCP and GP is complicated and time varying. presents descriptive statistics.

Figure 1. The trends of BCP and GP.

Source: Authors' calculations.

Table 1. Descriptive statistics for BCP, GP and USDX.

We can observe that the means of BCP, GP and USDX indicate that their series is concentrated at the 1763.816, 1350.159 and 88.120 levels, respectively. The standard deviation indicates the fluctuation of time series, and the volatility of BCP is greater than that of GP. The positive skewness of BCP and GP shows that these two variables are in right-skewed distribution, while USDX is in a left-skewed one. The kurtosis of BCP is more than 3, thereby demonstrating leptokurtic distributions. Moreover, GP and USDX satisfy platykurtic distributions since the kurtoses are less than 3Footnote6. Additionally, the Jarque-Bera test proves that these three-time series are significantly nonnormally distributed at the 1% level. Therefore, the traditional causal relationship test is not appropriate to employ. Thus, this paper uses the RB method to prevent potentially nonnormal distributions in these three variables. We also apply the subsample test to explore the time-varying Granger causal relationship between BCP and GP. To avoid potential heteroscedasticity, all three of these three (BCP, GP and USDX) are transformed by calculating natural logarithms.

5. Empirical results

To test the stationarity of the data, we apply the augmented Dickey-Fuller (ADF), Phillips-Perron (PP) and Kwiatkowski-Phillips-Schmidt-Shin (KPSS) tests (Dickey & Fuller, Citation1981; Kwiatkowski, Phillips, Schmidt, & Shin, Citation1992; Phillips & Perron, Citation1988). reports the results of the unit root tests, and we can conclude that BCP, GP and USDX are I(1). Then, we use the first differences in these three variables to construct the Granger causality test models, which can ensure the stationary of time series.

Table 2. The results of unit root test.

According to EquationEquation (2)(2)

(2) , we employ the VAR process to examine the full-sample Granger causal relationship between BCP and GP. The optimal lag order that we selected is 1, based on SIC. According to the RB-based modified-LR tests, the full-sample results are shown in . It is obvious that the causal relationship between BCP and GP is not significant. Therefore, we can conclude that BCP has no influence on GP and vice versa, inconsistent with the existing studies (Bouri et al., Citation2018; Obryan, Citation2019).

Table 3. Full-sample Granger causality tests.

The full sample estimation assumes that all of the parameters in the VAR process are stable, and there is only one causal relationship in the whole sample period. However, there could be time-varying causality between BCP and GP if these two time series and the VAR process undergo structural changes (Balcilar & Ozdemir, Citation2013). We apply the Sup-F, Ave-F and Exp-F tests (Andrews, Citation1993; Andrews & Ploberger, Citation1994) to show whether or not the parameters are constant. Additionally, the Lc statistics test (Hansen, Citation1992; Nyblom, Citation1989) is also employed to ensure the reasonableness of the Granger causality test. reports the results of parameter stability tests.

Table 4. The results of parameter stability test.

The Sup-F test indicates that, at the 1% level, BCP, GP and the VAR system undergo sudden structural changes. The Ave-F test suggests that the parameters can gradually evolve along the time trajectory in BCP and the VAR system at the 10% level, while GP is at the 5% level. BCP, GP and the VAR system can accept the alternative hypothesis of evolution along the time trajectory through the Exp-F test at the 1% level. Furthermore, the Lc statistics test reveals that we cannot accept the null hypothesis of the parameters in the VAR system following a random walk process at the 1% level. Thus, we can assume that the time series undergo structural changes, and the parameters in the VAR system are nonconstant. Then, there is a time-varying causal relationship between BCP and GP, but the bootstrap full-sample causality test can only obtain the constant parameters, which are inappropriate to employ in our analysis. We apply the bootstrap subsample rolling-window causality test to capture the time-varying interaction between BCP and GP. We choose 24-monthsFootnote7 as the rolling-window width to ensure the accuracy of the Granger causality test. We can evince whether the null hypothesis that there is no effect of BCP on GP (or there is no effect of GP on BCP) can be accepted or rejected. Additionally, we can obtain the direction of the influences from BCP to GP (or the influences from GP to BCP).

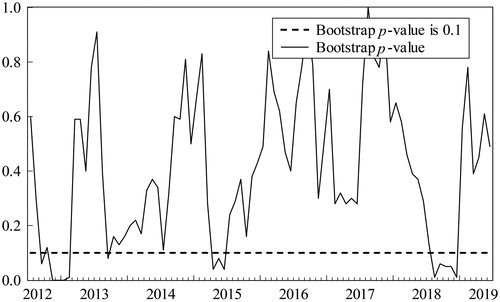

and evince the bootstrap p-value and the direction of the influences from BCP to GP, respectively. The null hypothesis that BCP does not Granger cause GP can be accepted, except for in 2012:M11-2013:M2, 2015:M4-2015:M6, and 2018:M8-2018:M12 at the 10% significance level, showing negative influences during these periods.

Figure 2. Bootstrap p-values of rolling test statistic testing the null hypothesis that BCP does not Granger cause GP.

Source: Authors' calculations.

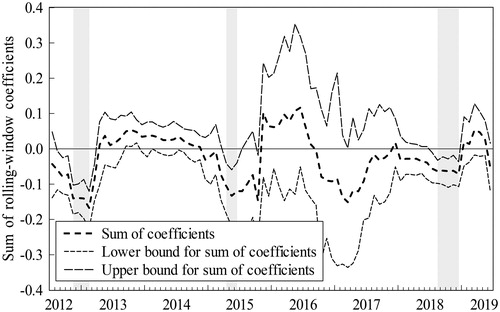

Figure 3. Bootstrap estimates of the sum of the rolling-window coefficients for the impact of BCP on GP.

Source: Authors' calculations.

The negative effects of BCP on GP show that the status of gold is threatened due to fluctuations in the Bitcoin market. In December 2012, the French Bitcoin Central Exchange, which is the first officially recognized exchange, was founded. This exchange has facilitated the convenience of Bitcoin transactions, leading to an increase in traders, and it also caused an increase in BCP during the period of 2012:M11-2013:M2. The Cyprus debt crisis broke out in 2013, and the European Union (EU) and Germany responded to it by increasing taxes on depositors. Then, the depositors in Cyprus panicked, causing them to lose confidence in the sovereign currency and seriously question the security of the banks. To avoid the risks of high taxes, the public was eager to replace the sovereign currency with Bitcoin, which is independent, and its price was in a rising cycle. As a result, the increasing demand for Bitcoin caused BCP to soar. Since the public was more willing to hold Bitcoin to avoid the risks of economic uncertainty (Bouri et al., Citation2017), the demand for gold, which is viewed as a traditional hedge or safe haven (Beckmann, Berger, & Czudaj, Citation2019; Jamal, Refk, & Wohar, Citation2018; Jones & Sackley, Citation2016), declined. In addition, since the global financial crisis subsided and the U.S. economy rebounds, the expectation of the public is that a loose monetary policy will be weakened, which could lead to a falling cycle of GP. During this time, BCP is still in an upward trend, and the public is more inclined to invest in Bitcoin rather than gold. The decline in demand for gold further reduces GP, indicating that the fluctuations in the Bitcoin market have influences on the hedging ability of gold. Therefore, the negative impact of BCP on GP can be proved.

Global uncertainty was increasing in 2015 (Davis, Citation2016) due to the European immigration crisis (Adina, Citation2018), the crash of the Chinese stock market (Blaschke, Citation2015) and the loosening of global monetary policies (43 authorities except for the Fed). This uncertain environment should have increased the demand for assets with hedging ability, such as Bitcoin and gold (Beckmann et al., Citation2019; Jamal et al., Citation2018; Jones & Sackley, Citation2016). However, both BCP and GP were at low levels during the period of 2015:M4-2015:M6, although there was a slight rise in BCP. The reasons for the decline in GP can be explained in two ways. On the one hand, the interest rate hike decision made by the Fed caused the U.S. dollar to be more valuable than gold. To avoid the risks of global uncertainty, the public was more willing to invest in the U.S. dollar, causing the demand for gold to decline. Then, the reduced demand for gold caused GP to fall. On the other hand, the slight increase in BCP during this period cause investors to further lose confidence in the gold market, which meant a decline in GP. Thus, we can observe that the higher value of other assets (e.g., the U.S. dollar and Bitcoin) could cause GP to fall and undermine the ability of gold to hedge risks. Thus, the negative influence of BCP to GP can be shown.

Since blockchain technology is still immature (Dos, Citation2017) and there is a lack of digital currency regulation (Bradbury, Citation2013; Mauro et al., Citation2018; Zaghloul et al., Citation2019), investors’ confidence in the Bitcoin market has declined. Additionally, there has been a large-scale sell-off in the Bitcoin market, causing the bubble to burst (Li, Tao, Su, & Lobonţ, Citation2018; Su, Li, Tao, & Si, Citation2018) and BCP to fall sharply during the period of 2018:M8-2018:M12. Although GP is at a low level, the price of gold still shows a trend of slow, upward movement. There are two reasons for the rise in GP. First, the sharp fall in BCP indicates that the hedging ability of Bitcoin is weakening, causing the demand for it to decrease. Then, the Bitcoin investors turn to the gold market to avoid the losses caused by the plunge in BCP and to achieve the purpose of maintaining their wealth. Thus, the rise in gold demand causes GP to increase. Second, the global economic and geopolitical situations are not stable during this period. The Argentine exchange rate crisis, the global trade wars launched by the U.S. and the Turkish debt crisis cause global economic policy uncertainty to increase. The large-scale airstrike on Damascus and the U.S. sanctions against Iran cause geopolitical risks to increase. The longest U.S. government shutdown (35 days) from December 22, 2018, to January 25, 2019, causes an increase in U.S. partisan conflicts. The above events reduce public confidence in the current global environment, also leading to a rise in the demand for gold to avoid risks and driving GP to increase. Hence, the Bitcoin bear market could cause a rise in GP, also improving the ability of gold to hedge risks. Thus, we can conclude that GP can be negatively affected by BCP.

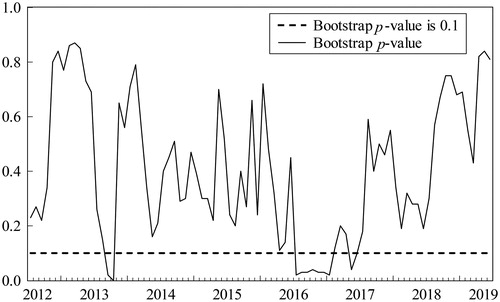

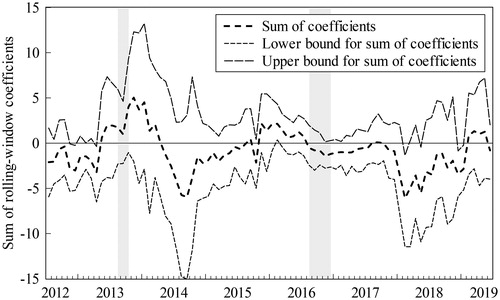

and reveal the bootstrap p-value and the direction of the influences from GP to BCP, respectively. The null hypothesis that GP does not Granger cause BCP can be accepted, except for in 2013:M8-2013:M10 and 2016:M8-2016:M12 at the 10% significance level. Further, during these periods, there are both positive (2013:M8-2013:M10) and negative (2016:M8-2016:M12) effects that exist from GP to BCP.

Figure 4. Bootstrap p-values of rolling test statistic testing the null hypothesis that GP does not Granger cause BCP.

Source: Authors' calculations.

Figure 5. Bootstrap estimates of the sum of the rolling-window coefficients for the impact of GP on BCP.

Source: Authors' calculations.

Since the Cyprus government sells gold reserves to pay off debts, the Fed prepares to end the quantitative easing (QE) policy, and the value of Bitcoin increases, GP has been in a downward trend from 2012:M11. However, there is a slight rise in GP during the period of 2013:M8-2013:M10, and the positive influence on BCP can be explained in two ways. On the one hand, the Cyprus debt crisis caused depositors to lose confidence in the sovereign currency, and its government sold enormous gold reserves to repay debts. Then, the public was more willing to hold Bitcoin to hedge risks during this crisis, causing the demand for Bitcoin and BCP to increase. Due to the inertia effect existing in BCP, even if there is a rise in GP, it will not affect the public investment preference in the short term, and BCP is still in an upward trend. On the other hand, the public expected that the slight increase in GP was temporary. Since the U.S. economy rebounded, and QE gradually weakened, the value of the U.S. dollar increased. The international price of gold is denominated in the U.S. dollar, showing a negative relationship with GP (Mo, Nie, & Jiang, Citation2018; Yang, Lin, & Chen, Citation2012; Zhou, Han, & Yin, Citation2018). Thus, the public has little confidence in investing in gold, and it still prefers to hold Bitcoin, leading to the continued growth of BCP. Therefore, we can assume that GP has a positive influence on BCP.

The market’s expectation of interest rate hikes in the U.S. continues to intensify, causing investing in dollars to be more valuable than gold. Then, the decline in gold investment demand causes GP to fall. Although Trump was elected as the U.S. president, it did not cause GP to rise, although the U.S. dollar and stock prices soared. In addition, the reduction in demand from major consumer countries (e.g., China and India) is also a main reason for the decline in GP. However, BCP sharply increased during the period of 2016:M8-2016:M12. First, the fall in GP increased the willingness of the public to invest in other assets with higher return, leading to more attention being paid to the Bitcoin market. Second, uncertain events, such as Brexit, the Brazil economic crisis and the U.S. elections (Donald J. Trump versus Hillary D. R. Clinton), made the public more willing to hold assets with hedging ability. Then, the downturn in GP led to an increase in the demand for Bitcoin to avoid the risks of global uncertainty (Bouri et al., Citation2017). Third, the annual production of Bitcoin began to shrink, causing its supply to decrease. Additionally, combined with the investment boom (especially in China, Japan and South Korea) in the Bitcoin market, BCP increased sharply (Li et al., Citation2018; Su et al., Citation2018). Therefore, the negative effects of GP to BCP can be proved.

In summary, the results of the full-sample test cannot support the causal relationship between BCP and GP, which is not reliable due to the parameters being assumed to be constant. Subsequently, the stability tests reveal that the time-series and VAR systems undergo structural changes. Thus, this study employs the bootstrap subsample rolling-window causality test to explore the time-varying Granger causality between BCP and GP. The empirical results establish that BCP has negative influences on GP. An increase in BCP can cause GP to decrease, which also means that the status of gold to avoid risks is threatened by Bitcoin. Additionally, the decline in BCP causes GP to increase, indicating that gold still has hedging ability and can avoid the risks of the Bitcoin market. Thus, both gold and Bitcoin have certain abilities to hedge risks, and they are not substitutes. The status of gold will not be completely threatened by Bitcoin, and they can complement each other to diversify investment risks. These results are consistent with the previous studies (Gkillas & Longin, Citation2019; Shahzad et al., Citation2019), while they were not supported by other analyses (Baek & Elbeck, Citation2015; Klein et al., Citation2018; Kubát, Citation2015; Yermack, Citation2013). In turn, there are both positive and negative influences from GP to BCP, indicating that the price of Bitcoin can be grasped through the gold market. Among these influences, the rise in BCP driven by the decline in GP reveals that Bitcoin can be viewed as a new basket for eggs, and it also plays a role in the downside of traditional hedging assets.

6. Conclusion

To explore whether or not the status of gold is threatened by Bitcoin, we apply the bootstrap subsample rolling-window causality test to identify the time-varying mutual influences between BCP and GP. The empirical results reveal that there are negative influences from BCP to GP, which also show that gold’s status can be threatened by Bitcoin during a few periods. The rise in BCP can cause GP to decrease, and it indicates that the prosperity of the Bitcoin market undermines the hedging ability of gold. However, the decline in BCP causes GP to increase, also emphasizing that gold still has the ability to avoid risks, especially during the Bitcoin bear market. Thus, the status of gold will not be completely threatened by Bitcoin, and the ability to hedge risks remains effective. In turn, the positive and negative effects of GP on BCP point out that the price of Bitcoin can be predicted by the gold market. Furthermore, a decline in GP will cause BCP to soar, suggesting that Bitcoin can be viewed as a new asset to diversify investment risks, and it can also avoid losses caused by the downside of the gold market. By examining the causal relationship between BCP and GP, we can conclude that the abilities of Bitcoin and gold to hedge risks are time varying, they are more likely to be complementary to each other, rather than being in competition. As a traditional hedging asset, the status of gold persists, although sometimes the Bitcoin market will pose threats to it.

Understanding the status of gold and the interaction mechanisms between BCP and GP can provide implications for investors and countries. First, the rise in BCP could cause GP to decrease, so investors can reduce their gold holdings when in the Bitcoin bull market. Additionally, they should pay attention to the risks of price bubbles and the security of the Bitcoin market (e.g., hacking and theft), which can lead to enormous costs. Second, the decline in BCP will cause GP to increase, so investors should increase gold investments when Bitcoin is in a bear market. Then, they can avoid the significant losses caused by plunges in the Bitcoin market. Third, GP plays an important role in predicting BCP, and investors can invest in Bitcoin when in the gold bear market. Then, they will diversify investment risks and maintain their wealth. Since Bitcoin and gold are complementary, instead of competitive, full consideration should be given when making investment decisions. Investors should optimize their asset allocation to achieve the principle of risk minimization and avoid the threats caused by the Bitcoin or gold bear markets. Moreover, countries can grasp the trends in BCP based on the fluctuations in GP and vice versa. They should formulate corresponding measurements and policies based on future trends. During soaring periods, the bubble burst should be suppressed, and during down periods, negative market sentiment should be reduced. Additionally, the security issues of the Bitcoin market must also be fully examined. When the great fluctuations in both markets are effectively prevented and controlled, the healthy development of the national economy can be prompted, which will be shown in a future study. A natural extension of our analysis, thus, is to compare the abilities of Bitcoin and gold, as well as other assets (e.g., the U.S. dollar) to avoid risks of economic uncertainty or geopolitical events. In addition, whether Bitcoin is a hedge asset, diversifier or safe haven should be further explored, and its interactions with other assets should also be paid significant attention.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 Goldman Sachs is one of the oldest and largest investment banks in the world, providing a broad range of investment, consulting and financial services.

2 The price of Bitcoin in U.S. dollars is obtained from the Yahoo Finance Database (https://finance.yahoo.com/quote/BTC-USD?p = BTC-USD&.tsrc = fin-srch).

3 In June 2019, BCP and GP increased by 24.55% and 5.68%, respectively, indicating that both BCP and GP increased, and these two variables moved in the same direction.

4 The price of gold in U.S. dollars is obtained from the World Gold Council (https://www.gold.org/goldhub/data/gold-prices).

5 The U.S. dollar index is obtained from the Federal Reserve Board (https://www.federalreserve.gov/econres/notes/ifdp-notes/IFDP_Note_Data_Appendix.xlsx).

6 The leptokurtic distribution shows a much higher peak around the mean value and fat tails, or higher densities of values at the extreme ends of the probability curve. The platykurtic distribution is exactly the opposite.

7 To prove the robustness of the test results, this paper also uses the rolling-window widths of 20, 28 and 32 months to explore the Granger causality, and the results are similar to the 24-month rolling-window.

References

- Adina, M. A. (2018). EU politicization beyond the euro crisis: Immigration crises and the politicization of free movement of people. Comparative European Politics, 17(3), 380–396.

- Aggarwal, S., Santosh, M., & Bedi, P. (2018). Bitcoin and portfolio diversification: Evidence from India. In A. Kar, S. Sinha, & M. Gupta (Eds.), Digital India. Advances in theory and practice of emerging markets (pp. 99–115). Cham: Springer.

- Al-Yahyaee, K. H., Mensi, W., & Yoon, S. M. (2018). Efficiency, multifractality, and the long-memory property of the Bitcoin market: A comparative analysis with stock, currency, and gold markets. Finance Research Letters, 27, 228–234. doi:10.1016/j.frl.2018.03.017

- Andrews, D. W. K. (1993). Tests for parameter instability and structural change with unknown change point. Econometrica, 61(4), 821–856. doi:10.2307/2951764

- Andrews, D. W. K., & Ploberger, W. (1994). Optimal tests when a nuisance parameter is present only under the alternative. Econometrica, 62(6), 1383–1414. doi:10.2307/2951753

- Arsov, A. (2017). Bitcoin as an innovative payment currency in Germany: Development of thee-gold standard. Journal of International Business Research and Marketing, 2(2), 33–42. doi:10.18775/jibrm.1849-8558.2015.22.3005.

- Baek, C., & Elbeck, M. (2015). Bitcoins as an investment or speculative vehicle? A first look. Applied Economics Letters, 22(1), 30–34. doi:10.1080/13504851.2014.916379

- Balcilar, M., & Ozdemir, Z. A. (2013). The export-output growth nexus in Japan: A bootstrap rolling window approach. Empirical Economics, 44(2), 639–660. doi:10.1007/s00181-012-0562-8

- Balcilar, M., Ozdemir, Z. A., & Arslanturk, Y. (2010). Economic growth and energy consumption causal nexus viewed through a bootstrap rolling window. Energy Economics, 32(6), 1398–1410. doi:10.1016/j.eneco.2010.05.015

- Beckmann, J., Berger, T., & Czudaj, R. (2019). Gold price dynamics and the role of uncertainty. Quantitative Finance, 19(4), 663–681. doi:10.1080/14697688.2018.1508879

- Blaschke, W. (2015). China’s stock market crash is the latest crisis of global capitalism. Foreign Policy in Focus, 1–33.

- Bouoiyour, J., Selmi, R., & Wohar, M. E. (2019). Bitcoin: Competitor or complement to gold? Economics Bulletin, 39(1), 186–191.

- Bouri, E., Gupta, R., Lahiani, A., & Shahbaz, M. (2018). Testing for asymmetric nonlinear short- and long-run relationships between Bitcoin, aggregate commodity and gold prices. Resources Policy, 57, 224–235. doi:10.1016/j.resourpol.2018.03.008

- Bouri, E., Gupta, R., Tiwar, A. K., & Roubaud, D. (2017). Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Finance Research Letters, 23, 87–95. doi:10.1016/j.frl.2017.02.009

- Bradbury, D. (2013). The problem with Bitcoin. Computer Fraud & Security, 11, 5–8. doi:10.1016/S1361-3723(13)70101-5

- Davis, S. J. (2016). An index of global economic policy uncertainty (NBER Working Paper). Cambridge, U.S. National Bureau of Economic Research, Inc.

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. doi:10.2307/1912517

- Dos, S. R. P. (2017). On the philosophy of Bitcoin/blockchain technology: Is it a chaotic, complex system? Metaphilosophy, 48(5), 620–633.

- Dwyer, G. P. (2015). The economics of Bitcoin and similar private digital currencies. Journal of Financial Stability, 17, 81–91. doi:10.1016/j.jfs.2014.11.006

- Dyhrberg, A. H. (2016a). Bitcoin, gold and the dollar – A GARCH volatility analysis. Finance Research Letters, 16, 85–92. doi:10.1016/j.frl.2015.10.008

- Dyhrberg, A. H. (2016b). Hedging capabilities of Bitcoin. Is it the virtual gold? Finance Research Letters, 16, 139–144. doi:10.1016/j.frl.2015.10.025

- Gajardo, G., Kristjanpoller, W. D., & Minutolo, M. (2018). Does Bitcoin exhibit the same asymmetric multifractal cross-correlations with crude oil, gold and DJIA as the Euro, Great British Pound and Yen? Chaos, Solitons & Fractals, 109, 195–205. doi:10.1016/j.chaos.2018.02.029

- Gkillas, K., & Longin, F. (2019). Is Bitcoin the new digital gold? Evidence from extreme price movements in financial markets. New York, U.S.: Social Science Electronic Publishing.

- Guesmi, K., Saadi, S., Abid, I., & Ftiti, Z. (2019). Portfolio diversification with virtual currency: Evidence from Bitcoin. International Review of Financial Analysis, 63, 431–437. doi:10.1016/j.irfa.2018.03.004

- Hansen, B. E. (1992). Tests for parameter instability in regressions with I(1) processes. Journal of Business and Economic Statistics, 20, 45–59.

- Harvey, C. R. (2014). Bitcoin myths and facts. San Francisco, U.S.: SSRN Electronic Publishing.

- Hurlburt, G. F., & Bojanova, I. (2014). Bitcoin: benefit or curse? IT Professional, 16(3), 10–15. doi:10.1109/MITP.2014.28

- Jamal, B., Refk, S., & Wohar, M. E. (2018). Measuring the response of gold prices to uncertainty: An analysis beyond the mean. Economic Modelling, 75, 105–116. doi:10.1016/j.econmod.2018.06.010

- Jones, A. T., & Sackley, W. H. (2016). An uncertain suggestion for gold-pricing models: The effect of economic policy uncertainty on gold prices. Journal of Economics and Finance, 40(2), 367–379. doi:10.1007/s12197-014-9313-3

- Klein, T., Hien, P. T., & Walther, T. (2018). Bitcoin is not the new gold: A comparison of volatility, correlation, and portfolio performance. International Review of Financial Analysis, 59, 105–116.

- Kristoufek, L., & Scalas, E. (2015). What are the main drivers of the Bitcoin price? Evidence from wavelet coherence analysis. Plos One, 10(4), e0123923. doi:10.1371/journal.pone.0123923

- Kubát, M. (2015). Virtual currency Bitcoin in the scope of money definition and store of value. Procedia Economics and Finance, 30, 409–416. doi:10.1016/S2212-5671(15)01308-8

- Kwiatkowski, D., Phillips, P. C. B., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root. ? Journal of Econometrics, 54(1–3), 159–178. doi:10.1016/0304-4076(92)90104-Y

- Li, Z. Z., Tao, R., Su, C. W., & Lobonţ, O. R. (2018). Does Bitcoin bubble burst? Quality & Quantity, 53(2), 1–15.

- Mauro, C., Kumar, E. S., Chhagan, L., & Sushmita, R. (2018). A survey on security and privacy issues of Bitcoin. IEEE Communications Surveys & Tutorials, 20(4), 3416– 3452.

- Mckay, D. R., & Peters, D. A. (2018). Digital gold: A primer on cryptocurrency. Plastic Surgery (Oakville, Ont.), 26(2), 137–138. doi:10.1177/2292550318777228

- Mo, B., Nie, H., & Jiang, Y. (2018). Dynamic linkages among the gold market, US Dollar and crude oil market. Physica A: Statistical Mechanics and Its Applications, 491, 984–994. doi:10.1016/j.physa.2017.09.091

- Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. Retrieved from https://bitcoin.org/bitcoin.pdf

- Newey, W. K., & West, K. D. (1987). A simple, positive semi-definite, heteroskedasticity: An autocorrelation consistent covariance matrix. Econometrica, 55(3), 703–708. doi:10.2307/1913610

- Nyblom, J. (1989). Testing for the constancy of parameters over time. Journal of the American Statistical Association, 84(405), 223–230. doi:10.1080/01621459.1989.10478759

- Obryan, P. (2019). Exploring the dynamics of Bitcoin’s price: A bayesian structural time series approach. Eurasian Economic Review, 9(1), 29–60.

- Othman, A. H. A., Alhabshi, S. M., & Haron, R. (2019). Cryptocurrencies, fiat money or gold standard: An empirical evidence from volatility structure analysis using news impact curve. International Journal of Monetary Economics and Finance, 12(2), 75–97. doi:10.1504/IJMEF.2019.100262

- Pesaran, M. H., & Timmermann, A. (2005). Small sample properties of forecasts from autoregressive models under structural breaks. Journal of Econometrics, 129(1–2), 183–217. doi:10.1016/j.jeconom.2004.09.007

- Phillips, P. C. B., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. doi:10.1093/biomet/75.2.335

- Qureshi, S., Rehman, I. U., & Qureshi, F. (2018). Does gold act as a safe haven against exchange rate fluctuations? The case of Pakistan Rupee. Journal of Policy Modeling, 40(4), 685–708. doi:10.1016/j.jpolmod.2018.02.005

- Shahzad, S. J. H., Elie, B., David, R., Ladislav, K., & Brian, L. (2019). Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis, 63(C), 322–330. doi:10.1016/j.irfa.2019.01.002

- Shukur, G., & Mantalos, P. (2000). A simple investigation of the Granger-causality test in integrated-cointegrated VAR systems. Journal of Applied Statistics, 27(8), 1021–1031. doi:10.1080/02664760050173346

- Shukur, G., & Mantalos, P. (1997). Size and power of the RESET test as applied to systems of equations: A bootstrap approach (Working Paper). Department of Statistics, University of Lund, Lund, Sweden.

- Smith, J. B. (2014). An analysis of Bitcoin exchange rates. New York, U.S.: Social Science Electronic Publishing.

- Su, C. W., Khan, K., Tao, R., & Nicoleta-Claudia, M. (2019). Does geopolitical risk strengthen or depress oil prices and financial liquidity? Evidence from Saudi Arabia. Energy, 187, 116003. doi:10.1016/j.energy.2019.116003

- Su, C. W., Li, Z. Z., Chang, H. L., & Oana-Ramona, L. (2017). When will occur the crude oil bubbles? Energy Policy, 102, 1–12. doi:10.1016/j.enpol.2016.12.006

- Su, C. W., Li, Z. Z., Tao, R., & Si, D. K. (2018). Testing for multiple bubbles in Bitcoin markets: A generalized sup ADF test. Japan & the World Economy, 46, 56–63.

- Su, C. W., Wang, X. Q., Tao, R., & Oana-Ramona, L. (2019). Do oil prices drive agricultural commodity prices? Further evidence in a global bio-energy context. Energy, 172, 691–701. doi:10.1016/j.energy.2019.02.028

- Symitsi, E. M., & Chalvatzis, K. J. M. (2019). The economic value of Bitcoin: A portfolio analysis of currencies, gold, oil and stocks. Research in International Business and Finance, 48, 97–110. doi:10.1016/j.ribaf.2018.12.001

- Yang, S. Y., Lin, F. L., & Chen, Y. F. (2012). Does the value of US dollar matter with the price of oil and gold? A dynamic analysis from time-frequency space. International Review of Economics & Finance, 43, 59–71. doi:10.1016/j.iref.2015.10.031

- Yermack, D. (2013). Is Bitcoin a real currency? An economic appraisal. In Handbook of digital currency (pp. 31–43). Cambridge, U.S.: National Bureau of Economic Research, Inc.

- Zaghloul, E., Li, T., Mutka, M., & Ren, J. (2019). Bitcoin and blockchain: Security and privacy. arXiv:1904.11435.

- Zhou, Y., Han, L. Y., & Yin, L. B. (2018). Is the relationship between gold and the U.S. dollar always negative? The role of macroeconomic uncertainty. Applied Economics, 50(4), 354–317. doi:10.1080/00036846.2017.1313956

- Zhu, Y., Dickinson, D., & Li, J. (2017). Erratum to: Analysis on the influence factors of Bitcoin’s price based on VEC model. Financial Innovation, 3(1), 3–7.