?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study deals with the relationship between corporate social responsibility (CSR) and firm competitiveness. Based on the comprehensive literature review, the theoretical model, providing linkages between CSR and corporate competences, has been developed. The created model was empirically tested, and the case study in Lithuania was conducted based on the assessment of influence of different social responsibility dimensions (environmental, social, economic, shareholder and voluntariness) on separate elements of competitiveness (financial capacity, quality of production, satisfied needs of consumers, efficiency, introduction of innovations and company’s image). The survey of 33 Lithuanian companies, i.e., all companies in Lithuania that have joined Global Compact, was performed by employing questionnaires. The conducted empirical research confirms that separate social responsibility dimensions (environmental, social, economic, shareholder, voluntariness) differently affect separate elements of competitiveness: financial capacity, quality of production, satisfied needs of consumers, efficiency, introduction of innovations and company’s image. It has been found that neither the quality of production nor the possibilities for introduction of innovations in a company are affected by the dimensions of social responsibility. Whereas company’s image, reputation and the factor of satisfied needs of consumers are affected by all dimensions of social responsibility that have been analysed. It has been noticed as well that the element of competitiveness, i.e., financial capacity, is affected by environmental and economic social responsibility dimensions; whereas, productivity and work efficiency are mostly related to social, shareholder and philanthropic dimensions. The main input of this paper is the definition of linkages between specific Corporate Social Responsibility dimensions addressed by the Global Compact and the main elements of competitiveness that have been identified based on rigorous and systematic literature review. The paper applies a completely different approach compared to the other studies that are investigating the impact of CSR on competitiveness via moderation and mediation analysis. The main approach followed in this paper is the qualitative assessment that has several limitations and advantages.

1. Introduction

The society’s needs, attitudes and values, which are constantly changing, have been influencing discussions about sustainable development at national and international levels. Sustainable development is perceived as the satisfying of contemporary society’s needs without influencing or preventing the satisfaction of future generation’s needs (Kolk, Citation2016). In order to implement this idea of sustainable development, the target to adapted activities towards sustainable development is set for every state business and its implemented activities (Lu et al., Citation2019a). Even though the concept of integrating business into sustainable development has been discussed since the middle of the past century, it was announced publicly about guiding companies towards sustainable development in 1999, i.e., after the Global Compact (Kell, Citation2005). This agreement aimed at encouraging business to draw attention to human rights, workforce, environmental protection and anti-corruption fight. It resembled an international corporate social responsibility initiative (Coulmont et al., Citation2017).

Corporate Social Responsibility (CSR) has been discussed in scientific works and is becoming an inseparable phenomenon of modern XXIst century business activities as well. Those times, when business activities were only based on achieving profitability and performance efficiency, regardless of creating social welfare and solving environmental problems, such as environmental change, air pollution etc., are already forgotten, because a contemporary business cannot ignore modern consumers’ needs. These needs state that it is vital and appropriate for business companies and organisations to base their activities on socially responsible actions, regarding social, ecological and ethical (moral) aspects (Aguinis, Glavas, Citation2012).

It is currently appropriate for a company to integrate the areas of social responsibility into its activities. In the contemporary society, which is increasingly reviewing the concept of sustainable development, the idea of socially responsible business is as important as the products or services provided by the company (Eccles et al., Citation2012). A business that aims to remain competitive at local and international level has to be socially responsible. Many scholars (Abbas et al., Citation2018; Eshra, Beshir, 2017; Li et al., Citation2019; Mandhachitara, Poolthong, Citation2011; Mei-Lien, 2011; Moisescu, Citation2017; Nochai, Nochai, 2014; Öberseder et al., Citation2013, Citation2014; Stanisavljevic, 2018; Yuen et al., Citation2016) have stated in their studies that consumers are the main factor encouraging companies to implement activities related to social responsibility. Other scholars have highlighted the impact of state policies and institutions as important drivers of CSR initiatives (Doh et al., Citation2015; Garcia-Sanchez, 2016; Ioannou, Serafeim, Citation2012; Lu et al., Citation2019c). After gaining the understanding of what encourages companies to be socially responsible, it is appropriate to explore what influence does corporate social responsibility has on the company’s competitiveness, which is the main challenge for companies in a modern dynamic world. Competitiveness is the ability to provide products and services as/or more effectively and efficiently than the relevant competitors (Jishi et al., 2017; Dupire, M’Zali, Citation2018).

There are just several studies dealing with the impact of CSR on firm competitiveness (Anser et al., Citation2018; Hadj, Citation2020; Marin et al., Citation2017; Snircova et al., 2016; Tantalo et al., 2014; Vilanova et al., Citation2009; Zait et al., Citation2015; Zhao et al., Citation2019). Most studies were focused on the impact of CSR on the performance of the firm (Kaufman, Olaru, 2012; Lee, Maxfield, Citation2015; Price, Sun, 2017; Lee, Kim, Citation2017; Li et al., Citation2018), the value of the firm and its brand ( Melo, Galan, Citation2011; Servaes, Tamayo, Citation2013; Cahan et al., Citation2016; El Ghoul et al., Citation2017; Park et al., Citation2018; Lu et al., Citation2019b ) or the profit of the firm (Maneet, Sudhir, Citation2011; Hategan et al., Citation2018; Yoo, Lee, Citation2018). However, the competitiveness is a much broader approach which has attracted a great deal of attention from scholars in the fields of international business and industrial economics (Madueno et al., 2014; Ioannou, Serafeim, 2012; Engert, Baumgartner, Citation2016; Šnircová et al., Citation2016); whereas, company competitiveness that is achieved by sustainable activity ensures long-term competitiveness.

All studies (Anser et al., Citation2018; Hadj, Citation2020; Marin et al., Citation2017; Snircova et al., 2016; Zhao et al., Citation2019), except (Tantalo et al., 2014; Vilanova et al., Citation2009; Zait et al., Citation2015), were dealing with the analysis of linkages between Corporate Social Responsibility and competitiveness via moderation and mediation analysis. Vilanova et al. (Citation2009) and Zait et al. (Citation2015) developed accurate hypotheses about the impacts of CSR on competitiveness, and the study by Tantalo et al. (2014) applied qualitative assessment framework for the assessment of aforementioned linkages. Nevertheless, a clear framework for business in linking CSR with firm competitiveness has not been provided yet, mainly due to complicated structural equations and dozens of hypotheses that appeared in previous studies.

This study aims to fill this gap and analyses the influence of CSR on corporate competitiveness by applying a simple and clear framework based on the qualitative assessment. The employed questionnaire involved Likert scale, which helped to evaluate the impact of social responsibility on the organisation’s separate elements of competitiveness by calculating coefficients of specific indicators. This study has limitations and represents just a small step in the process trying to explain a complex model of possible relationships between CSR and competitiveness. As in any qualitative study, these limitations are clearly addressed in the Methodology section.

The conducted empirical research provides that separate social responsibility dimensions (environmental, social, economic, shareholder, voluntariness) affect separate elements of competitiveness: financial capacity, quality of production, satisfied needs of consumers, efficiency, introduction of innovations and company’s image, differently. This study has implications for the managers of the company and is useful for developing business strategy, as it provides a clear understanding, which dimensions of CSR followed by a company effect the targeted area of competitive advantages of the company.

The study is structured in the following way: the first section is introduction; the second presents the literature review; the third section develops a model for the relationship between corporate social responsibility and firm competitiveness; the fourth section deals with the results of empirical study; the fifth section presents a discussion of results; the sixth section concludes the research.

2. Literature review

2.1. Corporate social responsibility

Corporate social responsibility as a new phenomenon in business activities started in about 1950s (Campbell, Citation2007; Carroll, Citation2008; Krisnawati et al., Citation2014; Riera, Iborra, Citation2017). The main global CSR initiative Global Compact was presented by the UN in 1999, integrating ten universal principles that include the areas of human and labour rights, environment and anti-corruption (Coulmont et al., Citation2017). This agreement seeks that all business companies would contribute to sustainable development, i.e., would reduce pollution through technological innovation and decrease the number of equipment that would cause pollution in the organisation. An active fight against corruption is discussed as well, aiming to repeal illegal, shadow business, bribery and corruption (Epstein, Buhovac, Citation2014; Meyer, Citation2015).

M. Vilanova (2007) determines the main aspects of CSR activities: community relations, workplace, accountability (transparency), vision and marketplace. Community relations are related to the partnership with different stakeholders (clients, suppliers, employees and partners) and company’s philanthropic activities; workplace includes labour practices within the organisation and the assurance of human rights; accountability relates to organisation’s transparency, various financial reporting, responsibility to society and other stakeholders; vision includes values, reputation and image from the perspective of stakeholders; marketplace is concerned with the main business activities (pricing, marketing, honest competitiveness and investments). Whereas other authors (Fouad Ibrahim, Citation2017; Eshra, Beshir, 2017; Nochai, Nochai, 2014) claim that corporate social responsibility is related to four aspects of activities, i.e., economic, legal, ethical (moral) and philanthropic responsibilities.

According to Fouad Ibrahim (Citation2017), the most important is economic responsibility, followed by legal, ethical (moral) and philanthropic responsibility. Economic responsibility is the most important aspect because no business organisation could exist without the aim to reach profit and satisfy market needs. Legal responsibility is significant as well, because a business that does not follow the regulations and rules should be punished by the law; moreover, when a company disregards the aspect of transparent business, it causes harm to its reputation and image, which can reduce consumer interest in its sold goods or provided services (Garcia-Sanchez et al., 2016, Citation2018). In the third place, according to the significance, ethical (moral) responsibility requires firms to respect generally recognised standards and moral norms. The final, according to the significance, is philanthropic responsibility that does not directly influence the company’s economic results, but it can have a positive impact on the society’s attitude towards the organization and improve its image, prestige and reputation. It could be stated that all these four aspects of social responsibility directly or indirectly contribute to the improvement of the company’s activities, create consumer opinion about the company and influence the results of activities of a socially responsible organization (Godos-Díez et al., Citation2018; Kong et al., Citation2020; Ljubojevic et al., Citation2012).

R. Nochai and Nochai (Citation2014) and Eshra and Beshir (Citation2017) agree with N. A. Fouad Ibrahim (Citation2017) and as well distinguish four aspects of corporate social responsibility: economic, legal, ethical (moral) and philanthropic responsibilities. When analysing these aspects, R. Nochai and Nochai (Citation2014) state that the essence of economic responsibility is the reduction of expenditures and costs, aiming to increase profit; legal responsibility stresses absolute respect for legislation regulations while performing activities; ethical (moral) responsibility means that business organizations would operate under justice law and would not cause a threat to society’s interests. Other authors (Baumgartner, Citation2014;; Schmeltz, Citation2017) as well stress that philanthropic responsibility distinguishes company’s voluntariness, contributing to the creation of society’s welfare by encouraging culture, art and other intellectual activity that is necessary to ensure society’s development.

Other authors, contrary to Fouad Ibrahim (Citation2017), additionally name ecological and social aspects, but do not distinguish philanthropic, legal or ethical (moral) aspects. The only similarity is that the mentioned authors distinguish economic aspect that integrates performance efficiency and profitability assurance, competitiveness of goods and services, work efficiency and energy saving by trying to reduce cost of activities. It could be noticed that the distinguished ecological and social aspects could reflect the legal aspect named by Fouad Ibrahim (Citation2017), because it includes compliance with legislation related to environmental protection and employee safety. It should be stated as well that the social aspect can be partially related to ethical (moral) aspects, because it discusses taking care of society’s needs and employee wellbeing (Lombart, Louis, Citation2014; Kim, Park, Citation2011). Thus, when analysing the main activity aspects of corporate social responsibility, it has been found that all elements are interrelated, and when combining them, an optimal implementation of activities of corporate social responsibility could be achieved

Moreover, it is important to mention that social responsibility is based on three main dimensions: social, economic and ecological (Castka et al., 2007; Jankalova, Citation2016, Citation2017; Pimentel et al., 2016), see .

Table 1. The main dimensions of corporate social responsibility.

According to A. Dahlsrud (Citation2008), corporate social responsibility integrates the following dimensions: environmental, social, economic, shareholders (suppliers, employees, consumers and society) and voluntariness. Environmental dimension is oriented towards the environmental company’s policy that assures cleaner environment, sustainable use of resources and raw materials in activities and solves other problems related to nature. The social dimension is linked to the mutual cooperation and achieving a compromise between business organisation and society’s needs, solving the existing social problems. The economic dimension discusses how to ensure long-term profitability of activities (Joshi et al., Citation2007; Kaufmann, Olaru, Citation2012), at the same time contributing to the world’s sustainable economic development, cleaner environment, integration with society and philanthropic activities that are not regulated by the legislative framework. The stakeholder dimension stresses that a company, which is implementing socially responsible activities, regards the interests of stakeholder groups and respects the interests of employees, suppliers, clients and partners (Castka et al., 2007; Doh et al., Citation2015). The dimension of voluntariness represents philanthropic activities, i.e., when a company voluntarily participates in charitable activities without compulsion.

After analysing the elements and dimensions of corporate social responsibility that have been distinguished by different authors, it has been noticed that some authors emphasize different aspects. In the table below (see ), a comparison of elements and dimensions of corporate social responsibility that were analysed by different authors is provided.

Table 2. Comparison of corporate social responsibility dimensions in different studies.

When analysing the main elements of corporate social responsibility, it has been found that all these elements involve employees as well as consumers and society. According to Liu et al. (Citation2012), the interest groups related to social responsibility can be classified in details (see ).

Table 3. Interest groups of corporate social responsibility.

As it is presupposed by the provided information above in , there are quite a lot of factors that have influence on socially responsible companies. First of all, a socially responsible company draws attention to its environment, i.e., workers and stakeholders; it is such a company that takes care of employee welfare and ensures to save working environment that employee wages would be competitive and correspond to the norms imposed by the laws (Engert, Baumgartner, 2016). From the stakeholder’s perspective, a company plans to share the net profit with stakeholders that have invested in the company’s activities. Creditors are as well important for the company. If a company has creditor obligations, it must pay and cover them in due time, without delay, because it can have an influence on the company’s image and future perspectives. Suppliers are no less important. Without suppliers, a company could not produce necessary goods or provide services. Thus, a socially responsible company is bound to observe contractual terms and transparently pursue its activities (Dubee, Rugiero, 2008). When discussing consumers, it is important to mention that they create company’s income; thus, it is appropriate for a company to provide qualitative services and sell qualitative goods in order to form a positive impression of consumer shopping patterns. Moreover, the most important factor of socially responsible company is environmental effect. Most scientists determine that a socially responsible company takes into consideration the surrounding environment (Cahan et al., Citation2016; Maimunah, Citation2009; Vasi, King, Citation2012). A business that is controlling the effect of its implemented activities on the environment and encouraging sustainable use of resources contributes to the tendency of sustainable development of the society. Some authors (Maldonado-Guzman et al., Citation2017; Romani et al., Citation2016; Uddin et al., 2011; Vlachos et al., Citation2009), when analysing corporate social responsibility, claim that interest groups of socially responsible business organisations create certain benefits for a company that is related to the organisation’s interest groups.

If a company bases its activities on the aspects of social responsibility, a trust related to consumers is created (Moisescu, 2015, Citation2017). Corporate social responsibility creates a loyal customer base: when customers are making a decision to buy goods or services, they notice whether a company respects own as well as society’s interests to create safe, clean and justice-based aspects of a community. Moreover, corporate social responsibility provides benefits related to the company’s staff. If a company is socially responsible, the employees start to show more respect related to work motivation as well as loyalty to the organisation (Udin et al., 2011). Suppliers as well take notice of corporate social responsibility. Naturally and understandably, a company that bases its activities on the concept of social responsibility aims to cooperate and establish partnerships with organisations that are as well respecting society’s needs in order not to damage reputation; in fact, on the contrary, they aim to create a network of socially responsible companies for sharing common ideas and achieving desired results. Corporate social responsibility as well creates benefits related to shareholders. For a socially responsible company, it is easier to meet the set standards and requirements, participate, for example, in public procurement, win contracts and in this way satisfy the needs and expectations of shareholders, persons that invest in a company.

2.2. Firm competitiveness

When analysing the understanding of company’s competitiveness, it has been noticed that company’s competitiveness is determined by such activity aspects as financial capacity, human and technological resources, innovations, operational efficiency, quality of goods/services and customer satisfaction (Hong et al., Citation2010). The financial capacity provides an opportunity for a company to be independent from creditors and allows strengthening technological capacity, introducing innovations, strengthening brand and at the same time taking a strong position in a competitive market. Human resources are as well an important element in the spectrum of competitive aspects (Maimunah, Citation2009). Competitive workers provide for a company such benefits as an opportunity to implement advanced technologies and modern projects by successfully pursuing long-term company’s strategy. Whereas technological resources and innovations allow firms to lessen operational costs and prices of products and allow more sustainable use of resources, contributing to solving environmental problems (Markota, Vukić, Citation2015). Another element that is influencing competitiveness is the quality of goods/services, which can ensure the loyalty of clients, consumers and the creation of a positive business image and a good reputation (Mei-Lien, 2011). It could be stated that the satisfaction of consumers as well as the quality of goods/services form loyal customer base and contribute to the creation of a wider consumer segment (Mandhachitara, Poolthong, 2011). It could be stated that all these activity elements that are causing business competitiveness help organisations to create and develop their competitive advantage and company’s immunity that is necessary when adapting in narrow market or surviving and strengthening positions in the present market segment.

The competitiveness is starting to be understood as the organisation’s ability to differ from competing companies with its implemented sustainable activity and transitioning from one target, i.e., from own profit, to the satisfaction of needs of the organisation as well as the environment that is surrounding it (Ioannou, Serafeim, 2012; Engert, Baumgartner, 2016). According to J. Šnircová et al. (Citation2016), corporate competitiveness that is achieved by sustainable activities ensures long-term competitive advantage that cannot be easily repeated by the competitive companies in the market. This could be explained by a modern, contemporary business organisation that is corresponding to the sustainable development concept. This organisation regards ecologic, economic and social environments and creates a loyal customer base, because society becomes more conscious and understands that the governments of countries as well as business subjects operating in countries have to turn to the natural environment and aim to foster, save it and in such a way contribute to the world’s sustainable economic development. Thus, it has been noticed that the appearance of a sustainable society and further development encourages companies to change their attitude towards competition by integrating social, economic as well as the ecological elements in their activities to create not only short-term, but long-term organisational competitive advantage that is based on the added value that is created for the market by a socially responsible and sustainable company; this advantage cannot be easily repeated by other competing companies and is related to the regard of changing needs of society and consumption patterns (Ioannou, Serafeim, 2012; Engert, Baumgartner, 2016). It is as well important to mention that when a business organisation is developing and aiming for long-term competitiveness that is based on social responsibility and sustainable development, the previously discussed interest groups of the company should be regarded, i.e., workers, shareholders, creditors, consumers, suppliers, society and government, in order to retain all interests.

When analysing what issues of competitiveness are linked to corporate social responsibility, it has been found (see ) that corporate social responsibility influences company’s reputation, brand, financial capacity, loyalty of consumers and attracting highly-qualified workers (Ljubojevic et al., Citation2012; Maneet, Sudhir, 2011; Minkiewicz et al., Citation2011). Whereas Madueno et al. (Citation2016) argue that corporate social responsibility influences the following elements of firm activity: reputation, consumer loyalty, attracting highly-qualified workers, market share, work efficiency and consumer satisfaction. According to Battaglia et al. (Citation2014), the specificity of the product, attracting highly-qualified workers, market share, work efficiency, consumer satisfaction, cost reduction as well as risk reduction are influenced.

Table 4. Links between corporate social responsibility and competitiveness.

When discussing reputation, it could be stated that a company that is working in a socially responsible way improves its reputation and image in respect to consumers as well as all previously mentioned interest groups, and a positive reputation, in turn, influences the strengthening of the brand. Socially responsible company appears more prestigious in respect of stakeholder groups and creates a picture of a transparent business, which strengthens the brand. Strong brand, as it is stated by Battaglia et al. (Citation2014), provides an opportunity for a company to develop occupied market share and penetrate into new markets, because in certain markets, green products are demanded and are more attractive to the consumers (Romani et al., Citation2016). The green products that are created by a company form loyal consumer base and their satisfaction, because when using production of a socially responsible company, consumers consciously contribute to solving environmental problems. When discussing the attraction of highly-competent workers, it could be stated that this aspect is partially related to the company’s positive reputation and strong brand, because for an organisation that is characterised by a strong brand it is frequently easier to attract highly-competent workers, as workers strive for such a company. The reduction of cost and risk is related to investments used in the activities of a socially responsible company that are technologically advanced and, in turn, influence the reduction of costs that are employed in the production processes.

3. Model for addressing the relationship between corporate social responsibility and competitiveness

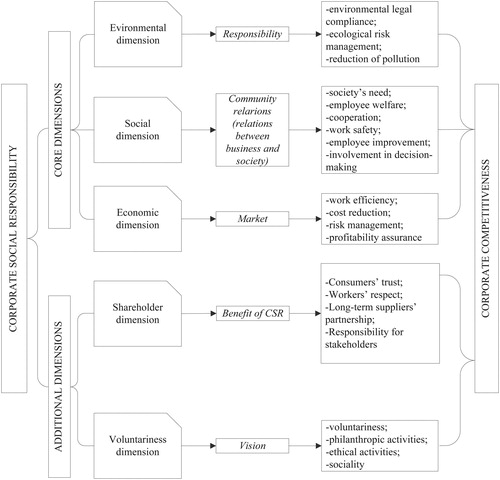

Following the analysis of understandings of corporate social responsibility and competitiveness and how corporate social responsibility influences certain activity aspects as well as competitiveness of firms, a model has been created to reflect how corporate social responsibility and competitiveness correlate with each other (see ).

Figure 1. Model for relations between corporate social responsibility and competitiveness.

The model shows how socially responsible activities that are implemented by companies influence competitiveness and through which company’s activity perspectives it is achieved. As it has been noticed, when analysing various concepts, dimensions and aspects of social responsibility, it can be noticed that it is a complex phenomenon composed of several different dimensions and elements; thus, this model begins by classifying social responsibility dimensions into two broad groups, i.e., a group of core dimensions discussed in (Castka et al., 2007; Jankalova, 2016, 2017; Pimentel et al., 2016) and a group of additional dimensions discussed in (Vilanova, 2007; Dahlsrud, Citation2008; Fouad Ibrahim, Citation2017; Nochai, Nochai, 2014). It could be stated that the core and initial dimensions of corporate social responsibility are environmental, social and economic dimensions. However, besides the mentioned core dimensions of corporate social responsibility, there are distinguished additional dimensions, i.e., shareholder and voluntariness. Different authors name these dimensions differently: shareholder dimension–dimension of community relations, ethical responsibility vision; voluntariness dimension – philanthropic responsibility.

When analysing the first environmental dimension, it has been noticed that it is related to corporate responsibility, which obliges companies to follow the requirements of environmental protection regulations. At the same time, corporate responsibility encourages managers to develop environmental policy in the organisation, avoid ecological risk related to the process of goods/services production/provision, aiming at minimizing the damage to the environment that is created by a company to prefer environmentally friendly technologies, pollution reduction and prevention. The second dimension is the social dimension that primarily relates to the relationships in a community, in other words, the relation between business organisations and its surrounding society. The social dimension could be related to the shareholder dimension because it stresses the relationship between the business and its surrounding environment. First, social dimension encourages business to cooperate with society. Business in this modern society that is becoming more conscious is no longer a single entity that is concerned with reaching the only aim, i.e., profit, and separated from the other person’s needs. Business organisations aim to adapt in a society with constantly changing consumers’ needs, based on socially responsible activities, such as attention to society’s needs, employee welfare, cooperation, work safety, healthy environment assurance for workers, continuous staff training, involvement in decision-making, business effect on society analysis, involvement of certain social problems in business activity processes and becoming part of the society. Another core dimension is economic dimension; it is named in theory as the economic responsibility that could be described as the organisation’s aim to maximise the profit, to sell goods or provide services and at the same time satisfy market needs. It is aimed at increasing work efficiency, respecting the right of workers, reducing costs, installing new, innovative clean technologies, financial risk management, profitability assurance and in this way contributing to raising the level of world economy.

The shareholder dimension in this model (see ) addressed the benefits of corporate social responsibility (Uddin et al., 2011). Shareholders are consumers, employees, suppliers and stockholders. If a company is based on the principles of social responsibility, then trust, which is related to consumers, is created. Corporate social responsibility creates a loyal customer base: when making a decision to buy goods or services, they notice whether a company respects own as well as society’s interests to create safe, clean and justice community needs. Moreover, corporate social responsibility provides benefits related to the company’s staff. If a company is socially responsible, employees start to show more respect related to work motivation as well as loyalty to the organisation. Suppliers as well take notice of corporate social responsibility. Naturally, a company that bases its activities on the concept of social responsibility aims to cooperate and establish partnerships with organisations that are as well respecting society’s needs in order not to damage reputation, but on the contrary, to create a network of socially responsible companies for sharing common ideas and achieving desired results. Corporate social responsibility as well creates benefits related to shareholders. For a socially responsible company, it is easier to meet the set standards and requirements, participate, for example, in public procurement, win contracts and in this way satisfy the needs and expectations of shareholders. Voluntariness dimension that could be called philanthropic responsibility accentuates voluntary desire to participate in philanthropic activities by a socially responsible company. The latter is related to the aspect of vision, when philanthropic activities contribute to the respect of ethical norms, formation of a company’s image, reputation. From society’s perspective, the creation of society’s welfare, participation in charitable activities by encouraging culture, art, uphold traditions and appearance, in the eyes of society, are seen as ethical, conscious and responsible organisation that takes care of own as well as other persons’ interests. To summarise the model for relations between corporate social responsibility and competitiveness, it could be stated that when consistently following the combination of all these social responsibility dimensions, competitive advantage is ensured in the market.

4. Empirical analysis of the impact of corporate social responsibility on firm competitiveness

Based on the developed model for addressing the relationship between corporate social responsibility and competitiveness, there was conducted an empirical research about the influence of different social responsibility dimensions (environmental, social, economic, shareholder and voluntariness) on separate elements of competitiveness (financial capacity, quality of production, satisfied needs of the consumers, efficiency and introduction of innovations and company’s image).

The survey of 33 firms, all companies of Global Compact network members in Lithuania, was conducted in September 2019. The main approach followed in this paper is a qualitative assessment. It represents just a small step to explain a complex model of possible relationships. As in any qualitative study, limitations need to be considered. First, the sample is limited to Lithuanian companies that are Global Compact members. Second, the generalisability may only be accurate when comparing companies in similar cultural institutional environments. The subjectivity is an important limitation as well. The main advantage of the followed approach is simplicity and transparency of links between dimensions of CSR and competitiveness. The future research is necessary to expand the sample of data, cover more countries and the application of more rigorous frameworks and tools like Structural Equation Modelling, regression analysis etc. The Structural Equation Modelling allows analysing the relationship between CSR and competitiveness more deeply and addressing the mediating role of innovation between CSR and competitiveness and moderators of this relationship.

The questionnaires were sent to companies via email, and the link of online questionnaire was provided as well. The responses were obtained from all 33 companies. The employed questionnaire involved Likert scale, which helped to evaluate the impact of social responsibility on the organisation’s separate elements of competitiveness by calculating coefficients of indicators (Bleich et al., 2015; Heale, Twycross, Citation2015). The scores from 1 to 4 were applied in assessing the influence of CSR on firms’ competitiveness: 1 there is no impact, 2 insignificant impact, 3 moderate impact, 4 high impact.

The answers were formalized by applying 4 unipolar grade scale (0; 0.25; 0.5; 1) to define the impact by using K coefficient.

The following formula was applied for calculating the impact assessment coefficients:

Ki is the coefficient of impact of selected CSR dimension on the ist element of competitiveness; kj is the score of impact on the ist element of competitiveness; j is the score from 1 to 5 (N = 5); ni is the number of answers that selected the score j for competitiveness element-i; n is the total number of answers.

The assessments of impact of separate social responsibility dimensions (environmental, social, economic, shareholder and voluntariness) on separate elements of competitiveness (financial capacity, quality of production, satisfied needs of consumers, efficiency, introduction of innovations and company’s image) are provided in Appendix 1. The generalized results are given in .

Table 5. The influence of corporate social responsibility dimensions on separate elements of competitiveness (based on the impact coefficients).

According to the generalized results provided in , it has been noticed that all social responsibility dimensions (environmental, social, economic shareholder, philanthropic voluntariness) mostly influence company’s image and reputation. When analysing environmental corporate social responsibility dimension, which is oriented towards sustainable innovations, energy-saving policy, participation in solving environmental problems, it has been found that from all researched elements of competitiveness, this dimension mostly influences image, reputation, secondly, satisfied needs and expectations of consumers, thirdly, financial capacity. Whereas, the least influenced element of competitiveness is the quality of production. It could be stated that the environmental dimension influences company’s image. If an organisation clearly understands the environmental problems, applying sustainable, clean and environmentally-friendly technologies in its activities, it will aim to minimise pollution caused to the environment and appear as a mature business subject in the society. This subject aims to achieve not only one task, i.e., gain profit, but to adapt in this global society, where environmental, global problems are relevant and a priority to most countries. This is related to the satisfied needs of consumers, because consumers are becoming more conscious. According to Romani et al. (Citation2016), in the market, there is appearing “green consumption” that is related to the aim of protecting nature as well as “responsible consumption” that integrates avoiding environmental damage and encompasses “green consumption”, “sustainable consumption” (preservation of resources) and “rational consumption” (minimum quantity of consumption).

Apart from the environmental aspect, consumers think about other areas of social responsibility: human rights, ethics, etc. When discussing financial capacity, it could be stated that environmental policy of a company encourages reducing expenditure and costs because of clean technologies used in activities. It is important to mention that a company that is operating under environmental standards gains “good name” from the perspective of some institutions, and this helps to participate in the public tenders published by the public authorities. Social dimension related to partnership with local organisations (schools, universities, centres for disables or retired persons, etc.), participation in public activities and solution of social problems as well as environmental and all other dimensions mostly influence organisation’s image and reputation, secondly, satisfies the needs of consumers, thirdly, improves productivity and work efficiency of the company. The least influenced is financial capacity, as it has been noticed in this study. According to Price and Sun (Citation2017), one of the main features of a modern organisation is the organisation’s ability to be “a society that is integrating and adapting relationship between a person and society and solving problems which are arising between them”. This creates an organisation that encourages social protection. A company that actively participates in the community’s life appears as a caring member of a society from the perspective of consumers and potential customers understanding that most of the company workers are members of local community, and this encourages taking care of community’s health, safety, education and more. The participation in public activities, solving social problems and partnership with local institutions initiate dynamic, innovative decisions that enable changes in the society and continuous implementation of sustainable development. It could be stated that this affects company’s productivity and work efficiency, because the mentioned favourable environment leads to having modern, creative, innovative workers.

Another, i.e., economic, dimension found in this study is related to the performance accountability, reduction of costs and fair competition. Economic dimension is mostly related to the created company’s image, secondly, financial capacity, thirdly, satisfied needs of consumers. It could be stated that performance accountability is as a tool helping companies to reveal their best aspects of activities, which understandably affects consumer and improves company’s reputation in respect to clients as well as society, suppliers, stakeholders, partners and public authorities. Due to this reason, economic dimension of social responsibility influences the financial capacity as well, because the existing and potential stakeholder reacts and takes into account transparent activities of the organisation, where they invest funds. Stakeholders, including partners and suppliers, when making a decision to cooperate with a company, firstly, will consider the perspective of a long-term cooperation, because short-term cooperation will provide only short-term benefit, and long-term partnership will form loyal relations ensuring a stable future and lead to uniting forces to achieve common goals. A company that guarantees transparency of its activities does not hide or avoid tax compliance. It does not ensure a short and quick result but rather a long-term activities perspective that is as well encouraged by the conscious consumers who take care of their own as well as future generation’s position and clearly understand the damage caused to the whole community, country and region by unfair and shadow activities.

The shareholder dimension is mostly related to the organisation’s image, satisfied needs of consumers in the second place and productivity and work efficiency in the third place. As it is stated by Vasi and Kin (2012), the concept of corporate social responsibility indicates one of the important aspects: the behaviour with internal and external shareholders is revealed. The satisfaction of shareholders’ needs causes countries to trust organisations, and in turn, trust influences company’s reputation, satisfied needs of consumers, work efficiency related to loyal and motivated staff that is open to novelties and innovative solutions providing long-term benefit. Despite everything, corporate social responsibility would become merely theoretical insights and considerations described in textbooks and not a real aspect of the company’s activities. The satisfaction of shareholders’ needs, taking care of them reveal organisation’s maturity, because only an organisation that has achieved a certain level of maturity understands that by operating in the market, it is surrounded by suppliers, clients, partners and community. Thus, for an organisation, it is appropriate to consider the needs of interested parties, their evaluation and certain related decision making; otherwise, a company will not be able to remain in the market with strong market players, as it does not create “trust network”.

It could be stated that from all corporate social responsibility dimensions, philanthropic dimension enables the aspect of voluntariness. After completing this study, it has been found that the support for projects solving social problems is one of the most common measures applied in socially responsible companies. Voluntariness or philanthropic dimension is mostly related to a company’s reputation, satisfied needs of consumers in the second place, productivity and work efficiency in the third place. Companies that contribute to various projects solving social problems that are of great importance for the society (for example, social inequality, poverty, etc.) are generally accepted by the society. From the society’s perspective, they seem as an organisation characterised by socially responsible activities, taking care of sensitive social issues. In this way, company’s image is improved in society’s perspective. However, when discussing company’s philanthropic activities, the lack of information plays an important role. Therefore, public education, education/training, special workshops and consultations could be helpful (Kudlak et al., 2018). These instruments would help to educate conscious society that is aware of socially responsible businesses, which in turn, would encourage business to present, demonstrate positive examples of corporate social responsibility and create a snowball effect. Thus, public demonstration of role models is very important. The input of the public sector would be appropriate as well, when public sector will start to demonstrate examples of socially responsible activities (recycling, support for struggling employees, etc.), this will become an incentive for the private business sector to take action for the application of corporate social responsibility in activities (Visionary Analytics, Citation2015). Thus, this is a purposeful joining of forces of public and private business sectors, related to the promotion and public demonstration of corporate social responsibility.

4. Discussion

This paper applied qualitative assessment framework in order to get clearer and simpler representation of the impact of specific dimensions of CSR on the most important areas of competitiveness. The results that have been obtained in this study are in good agreement with other studies conducted in this area, but it has applied a different approach. Qualitative studies (Kong et al., Citation2020; Tnatalo et al., 2014; Vilanova et al., Citation2009; Zait et al., Citation2015) did not try to distinguish between different dimensions of CSR and specific components of competitiveness; however, their findings were supported by this study. For example, study by Zait et al. (Citation2015), based on literature review and interviews, developed hypotheses about the impacts of CSR on competitiveness in Romanian SMEs and found that this relation is not clear and not fully recognized by the company managers. Vilanova et al. (Citation2009) conducted a literature review and found that CSR and competitiveness relate through learning and innovation cycle, where corporate values, policies and practices are permanently defined and re-defined. Study Tantalo et al. (2014) applied a qualitative assessment framework for the assessment of aforementioned linkages and found that that strategic orientation to the CSR may have benefits for the competitive profile of corporations. The study stressed the importance of strategic management to CSR, and this is the reason why insignificant results were found in order to clarify the relationship between CSR and competitiveness. The study by Bataglia et al. (2014) developed a correlation analysis between competitiveness variables and various CSR practices adopted in SMEs operating inn fashion industry in Italy and France and found a significant correlation between innovations which was considered as one of the most important dimensions of competitiveness and CSR initiatives.

Some studies (Anser et al., Citation2018; Hadj, Citation2020; Marin et al., Citation2017; Snircova et al., 2016; Zhao et al., Citation2019) dealing with the analysis of linkages between Corporate Social Responsibility and competitiveness of companies via moderation and mediation analysis found the mediating role of responsible innovations and environmental management in relationship between CSR and competitiveness.

It is necessary to distinguish that even though some studies did not aim to split CSR into separate dimensions, the areas related to social dimension are similar in all studies, i.e., participation in public events and partnership with local organisations. It could be stated that in the previously conducted studies, the economic dimension could be compared to the environmental dimension that aims to reduce cost. The areas that are related to shareholders are almost identical in all studies, i.e., staff training and motivation that are mentioned in (Battaglia et al., Citation2014; Snircova et al., 2016; Zait et al., Citation2015) and employee involvement in decision-making, identified in the current study. It is necessary to stress that a fair partnership with suppliers has been distinguished in this study, whereas in other studies, the employee health and safety is discussed as a priority. The areas related to philanthropic dimension are quite similar in all studies: charitable activities (compared to scholarship granting) and support for projects solving social problems (compared to support for local community).

The results of empirical study conducted in Lithuania revealed which social responsibility dimensions have the biggest influence or are related to certain elements of competitiveness. The results of the current study were compared with the results of other studies in this field (see ).

Table 6. Comparison of studies on the relationship between corporate social responsibility and competitiveness.

As it can be seen in , based on the empirical study conducted in Lithuania, the environmental social responsibility dimension and related areas are mostly affecting company’s financial capacity, image and reputation. However, in other studies regarding the impact of CSR on competitiveness, on contrary to the research conducted in this study, the influence on the satisfaction of customers’ needs is not mentioned (Battaglia et al., Citation2014; Snircova et al., 2016; Zait et al., Citation2015). The results of Tantalo et al. (2014) presupposed that the environmental dimension involved with competitiveness is characterised by high involvement (when discussing sustainable introduction of innovations) and medium involvement (when discussing the use of ecological raw materials in production processes). When comparing social dimension, it is clear that the results of a current study stress social responsibility relationship with a company’s image, satisfied needs of consumers, productivity and work efficiency. However, the study of Tantalo et al. (2014) found that the relationship of social dimension of CSR with competitiveness was insignificant.

Economic dimension was analysed only in this study, and its involvement with the elements of competitiveness was rarely analysed in other studies. When analysing shareholder (suppliers, consumers, partners) dimension, it has been noticed that based on the results of this work, the influence on such elements of competitiveness as reputation, satisfied needs of consumers, productivity and work efficiency were identified. Whereas in other studies, only the influence on reputation, productivity and work efficiency was discussed. Low involvement of shareholder dimension with competitiveness (when discussing the creation of value for suppliers and society), medium involvement (in respect of creation of value for the employees) and high involvement (regarding the creation of value for stakeholders) have been found in the study by C. Tantalo et al. (2014). Philanthropic dimension, according to C. Tantalo et al. (2014), is characterised by low involvement with competitiveness. Whereas, the research conducted in this study stresses that philanthropic activities implemented by companies influence image and reputation as well as satisfied needs of consumers, productivity and work efficiency.

5. Conclusions

Based on the analysis of various definitions of corporate social responsibility, it could be summed up that corporate social responsibility is a company’s voluntary decision and determination regarding the changing needs of society and business interest groups to respect social, ethical (moral), legal, economic, environmental aspects in its activities, aiming to contribute to the concept of sustainable development.

When analysing the influence of corporate social responsibility on firms’ competitiveness, it has been found that company’s implemented corporate social responsibility practices influence the following aspects of organisation’s activities: reputation, brand, financial capacity, specificity of the product, loyalty and satisfaction of consumers, attraction of highly-competent workers, market share, work efficiency, cost and risk reduction. All these aspects of activities provide a competitive advantage for a socially responsible company.

After the analysis of various empirical studies conducted by scholars all over the world, it has been found that corporate social responsibility affects company’s competitive profile. However, it has been noticed that not all directions and areas of corporate social responsibility affect socially responsible company’s competitive profile equally. Usually, socially responsible companies are oriented towards the creation of value for the employees, because it increases staff productivity and at the same time encourages company’s competitive advantage among other organisations that are operating in the market. Social responsibility that is implemented by the company has different effects on different elements of competitiveness (such as possibilities to introduce innovations, financial capacity, productivity, etc.).

The conducted empirical research provides that separate social responsibility dimensions (environmental, social, economic, shareholder, voluntariness) differently affect separate elements of competitiveness: financial capacity, quality of production, satisfied needs of consumers, efficiency, introduction of innovations and company’s image and reputation.

It has been found that neither the quality of production, nor the possibilities for introduction of innovations in a company are affected by the dimensions of social responsibility. Whereas company’s image, reputation and satisfied consumers’ needs are affected by all dimensions of corporate social responsibility that have been analysed. The important element of competitiveness, i.e., financial capacity, is affected by environmental and economic social responsibility dimensions; productivity, work efficiency is mostly related to social, shareholder and philanthropic dimensions.

The obtained results are significant because they help to eliminate the problem existing in organisations that is related to the failure to understand the benefit created by social responsibility for a company, as it determines which social responsibility dimension affects which element of competitiveness.

The main approach applied in this study is a qualitative assessment. As in any qualitative study, there are several limitations. First, the sample is limited to Lithuanian companies that are Global Compact members. Second, the generalisability may only be accurate when comparing companies in similar cultural institutional environments. The subjectivity is an important limitation as well.

The future research is necessary to test the developed model and extend it to firms operating in other countries, seeking to reveal the impact of cultural difference on corporate social responsibility and its linkages to competitive advantage. The sample of data needs to be expanded by covering more countries and application of frameworks that are more rigorous and tools as Structural Equation Modelling, and regression analysis is necessary. The Structural Equation Modelling would allow analysing the relationship between CSR and competitiveness more deeply and addressing the mediating role of innovation between CSR and competitiveness as well as moderators of this relationship.

Acknowledgments

The authors thank the anonymous reviewers and all the editors in the process of manuscript revision.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abbas, M., Gao, Y., & Shah, S. S. H. (2018). CSR and Customer Outcomes: The Mediating Role of Customer Engagement. Sustainability, 10(11), 4243. https://doi.org/10.3390/su10114243

- Aguinis, H., & Glavas, A. (2012). What We Know and Don’t Know about Corporate Social Responsibility: A Review and Research Agenda. Journal of Management, 38(4), 932–968. https://doi.org/10.1177/0149206311436079

- Anser, M. K., Zhang, Z., & Kanwal, L. (2018). Moderating effect of innovation on corporate social responsibility and firm performance in realm of sustainable development. Corporate Social Responsibility and Environmental Management, 25(5), 799–806. https://doi.org/10.1002/csr.1495

- Battaglia, M., Testa, F., Bianchi, L., Iraldo, F., & Frey, M. (2014). Corporate Social Responsibility and Competitiveness within SMEs of the Fashion Industry: Evidence from Italy and France. Sustainability, 6(2), 872–893. https://doi.org/10.3390/su6020872

- Baumgartner, R. J. (2014). Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corporate Social Responsibility and Environmental Management, 21(5), 258–271. https://doi.org/10.1002/csr.1336

- Bleich, E., & Pekkanem, R. (2013). How to Report Interview Data. In Mosley, L.(Ed.), Interview Research in Political Science (pp. 85–86). Cornell University Press.

- Cahan, S. F., Villiers, C. D., Jeter, D. C., Naiker, V., & Staden, C. J. V. (2016). Are CSR Disclosures Value Relevant? Cross-Country Evidence. European Accounting Review, 25(3), 579–611. https://doi.org/10.1080/09638180.2015.1064009

- Campbell, J. L. (2007). Why Would Corporations Behave in Socially Responsible Ways? An Institutional Theory of Corporate Social Responsibility. Academy of Management Review, 32(3), 946–967. https://doi.org/10.5465/amr.2007.25275684

- Carroll, A. B. (2008). The Oxford Handbook of Corporate Social Responsibility. In A. Crane, A. McWilliams, D. Matten, J. Moon, & D. Siegel (Eds.), A History of Corporate Social Responsibility: Concepts and Practices (pp. 19–46). Oxford University Press.

- Castka, P., Balzarova, M. A., Bamber, C. J., & Sharp, J. M. (2004). How can SMEs effectively implement the CSR agenda? A UK case study perspective. Corporate Social Responsibility and Environmental Management, 11(3), 140–149. https://doi.org/10.1002/csr.62

- Catalao, L. M., Branca, A. S., & Pimentel, L. V. (2016). International Comparisons of Corporate Social Responsibility. International Journal of Economy, Management and Social Sciences, 5, 327. https://doi.org/10.4172/2162-6359.1000327

- Coulmont, M., Berthelot, S., & Paul, M. A. (2017). The Global Compact and its concrete effects. Journal of Global Responsibility, 8(2), 300–311. https://doi.org/10.1108/JGR-02-2017-0011

- Dahlsrud, A. (2008). How Corporate Social Responsibility is Defined: an Analysis of 37 Definitions. Corporate Social Responsibility and Environmental Management, 15(1), 1–13. https://doi.org/10.1002/csr.132

- Doh, J. P., Littell, B., & Quigley, N. (2015). CSR and sustainability in emerging markets: Societal, institutional, and organizational influences. Organizational Dynamics, 44(2), 112–120. https://doi.org/10.1016/j.orgdyn.2015.02.005

- Dupire, M., & M’Zali, B. (2018). CSR Strategies in Response to Competitive Pressures. Journal of Business Ethics, 148(3), 603–623. https://doi.org/10.1007/s10551-015-2981-x

- Eccles, R. G., Perkins, K. M., Serafeim, G. (2012). How to Become a Sustainable Company. https://sloanreview.mit.edu/article/how-to-become-a-sustainable-company

- Engert, S., & Baumgartner, R. J. (2016). Corporate sustainability strategy—Bridging the gap between formulation and implementation. Journal of Cleaner Production, 113, 822–834. https://doi.org/10.1016/j.jclepro.2015.11.094

- Epstein, M. J., & Buhovac, A. R. (2014). Making Sustainability Work: Best Practices in Managing and Measuring Corporate Social, Environment and Economic Impacts. Berrett-Koehler Publishers.

- Eshra, N., & Beshir, N. (2017). Impact of Corporate Social Responsibility on Consumer Buying Behavior in Egypt. World Review of Business Research, 7(1), 32–44.

- García-Sánchez, I. M., Cuadrado-Ballesteros, B., & Frias-Aceituno, J. V. (2016). Impact of the Institutional Macro Context on the Voluntary Disclosure of CSR Information. Long Range Planning, 49(1), 15–35. https://doi.org/10.1016/j.lrp.2015.02.004

- Garde-Sanchez, R., López-Pérez, M. V., & López-Hernández, A. M. (2018). Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017. Sustainability, 10(7), 2403. https://doi.org/10.3390/su10072403

- Ghoul, S. E., Guedhami, O., & Kim, Y. (2017). Country-Level Institutions, Firm Value, and the Role of Corporate Social Responsibility Initiatives. Journal of International Business Studies, 48(3), 360–385. https://doi.org/10.1057/jibs.2016.4

- Godos-Díez, J. L., Cabeza-García, L., & Fernández-González, C. (2018). Relationship between Corporate Social Responsibility (CSR) and Internationalisation Strategies: A Descriptive Study in the Spanish Context. Administrative Sciences, 8(4), 57. https://doi.org/10.3390/admsci8040057

- Hadj, T. B. (2020). Effects of corporate social responsibility towards stakeholders and environmental management on responsible innovation and competitiveness. Journal of Cleaner Production, 250, 119490.

- Hategan, C. D., Sirghi, N., Curea-Pitorac, R. I., & Hategan, V. P. (2018). Doing Well or Doing Good: The Relationship between Corporate Social Responsibility and Profit in Romanian Companies. Sustainability, 10(4), 1041. https://doi.org/10.3390/su10041041

- Heale, R., & Twycross, A. (2015). Validity and reliability in quantitative studies. Evidence Based Nursing, 18(3), 66–67. https://doi.org/10.1136/eb-2015-102129

- Hong, S. Y., Yang, S. U., & Rim, H. (2010). The influence of corporate social responsibility and customer–company identification on publics’ dialogic communication intentions. Public Relations Review, 36(2), 196–198. https://doi.org/10.1016/j.pubrev.2009.10.005

- Ibrahim, N. A. F. (2017). The relationship between corporate social responsibility and employer attractiveness in Egypt: The moderating effect of the individual’s income. Contemporary Management Research, 13(2), 81–106. https://doi.org/10.7903/cmr.17430

- Ioannou, I., & Serafeim, G. (2012). What drives corporate social performance? The role of national-level institutions. Journal of International Business Studies, 43(9), 834–864. https://doi.org/10.1057/jibs.2012.26

- Jankalová, M. (2016). Approaches to the Evaluation of Corporate Social Responsibility. Procedia Economics and Finance, 39, 580–587. https://doi.org/10.1016/S2212-5671(16)30302-1

- Jankalová, M., & Jankal, R. (2017). The assessment of corporate social responsibility: approaches analysis. Entrepreneurship and Sustainability Issues, 4(4), 441–459. https://doi.org/10.9770/jesi.2017.4.4(4)

- Joshi, M., Tiwari, P. S., Joshi, V. (2007). Corporate Social Responsibility: Global Perspective, Competitiveness, Social Entrepreneurship & Innovation. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=999348

- Kaufmann, M., & Olaru, M. (2012). The Impact of Corporate Social Responsibility on Business Performance–Can it be Measured, and if so, How?. The Berlin International Economics Congress.

- Kell, G. (2005). The Global Compact Selected Experiences and Reflections. Journal of Business Ethics, 59(1-2), 69–79. https://doi.org/10.1007/s10551-005-3413-0

- Kim, S., & Park, H. (2011). Corporate Social Responsibility as an Organizational Attractiveness for Prospective Public Relations Practitioners. Journal of Business Ethics, 103(4), 639–653. https://doi.org/10.1007/s10551-011-0886-x

- Kolk, A. (2016). The social responsibility of international business: From ethics and the environment to CSR and sustainable development. Journal of World Business, 51(1), 23–34. https://doi.org/10.1016/j.jwb.2015.08.010

- Kong, Y., Antwi‐Adjei, A., & Bawuah, J. (2020). A systematic review of the business case for corporate social responsibility and firm performance. Corporate Social Responsibility and Environmental Management, 27(2), 444–454. . https://doi.org/10.1002/csr.1838

- Krisnawati, A., Yudoko, G., & Bangun, Y. R. (2014). Development path of corporate social responsibility theories. World Applied Sciences Journal, 30(30), 110–120. https://doi.org/10.5829/idosi.wasj.2014.30.icmrp.17

- Lee, M., & Kim, H. (2017). Exploring the Organizational Culture’s Moderating Role of Effects of Corporate Social Responsibility (CSR) on Firm Performance: Focused on Corporate. Sustainability, 9(10), 1883. https://doi.org/10.3390/su9101883

- Lee, J., & Maxfield, S. (2015). Doing Well by Reporting Good: Reporting Corporate Responsibility and Corporate Performance. Business and Society Review, 120(4), 577–606.

- Lenz, I., Wetzel, H. A., & Hammerschmidt, M. (2017). Can doing good lead to doing poorly? Firm value implications of CSR in the face of CSI. Journal of the Academy of Marketing Science, 45(5), 677–697. https://doi.org/10.1007/s11747-016-0510-9

- Li, J., Sun, X., & Li, G. (2018). Relationships among green brand, brand equity and firm performance: Empirical evidence from China. Transformations in Business and Economics, 17(3), 221–236.

- Litfin, T., Meeh-Bunse, G., Luer, K., & Teckert, Ö. (2017). Corporate Social Responsibility Reporting - a Stakeholder’s Perspective Approach. Business Systems Research Journal, 8(1), 30–42. https://doi.org/10.1515/bsrj-2017-0003

- Liu, S., Cai, L., & Li, Z. (2012). Social Responsibilities and Evaluation Indicators of Listed Companies in the Perspective of Interest Groups. American Journal of Industrial and Business Management, 02(03), 102–107. https://doi.org/10.4236/ajibm.2012.23014

- Li, J., Zhang, F., & Sun, S. (2019). Building Consumer-Oriented CSR Differentiation Strategy. Sustainability, 11(3), 664. https://doi.org/10.3390/su11030664

- Li, M. L. (2011). Impact of Marketing Strategy [Customer Perceived Value, Customer Satisfaction Trust, and Commitment on Customer Loyalty (Doctoral dissertation]. https://spiral.lynn.edu/etds/224.

- Ljubojevic, Č., Ljubojevic, G., Maksimovic, N. (2012). Social Responsibility and Competitive Advantage of the Companies in Serbia. Proceedings of the 13th Management International Conference,.

- Lombart, C., & Louis, D. (2014). A study of the impact of Corporate Social Responsibility and price image on retailer personality and consumers’ reactions (satisfaction, trust and loyalty to the retailer). Journal of Retailing and Consumer Services, 21(4), 630–642. https://doi.org/10.1016/j.jretconser.2013.11.009

- Lu, J., Ren, L., He, Y., Lin, W., & Streimikis, J. (2019b). Linking Corporate Social Responsibility with Reputation and Brand of the Firm. Amfiteatru Economic, 21(51), 442–460. https://doi.org/10.24818/EA/2019/51/442

- Lu, J., Ren, L., Lin, W., He, Y., & Streimikis, J. (2019c). Policies to promote Corporate social responsibility (CSR) and assessment of CSR impacts. E + M Ekonomie a Management, 22(1), 82–98. https://doi.org/10.15240/tul/001/2019-1-006

- Lu, J., Ren, L., Yao, S., Qiao, J., Strielkowski, W., & Streimikis, J. (2019a). Comparative Review of Corporate Social Responsibility of Energy Utilities and Sustainable Energy Development Trends in the Baltic States. Energies, 12(18), 3417. https://doi.org/10.3390/en12183417

- Madueno, J. H., Jorge, M. L., Conesa, I. M., & Martinez, D. (2016). Relationship between corporate social responsibility and competitive performance in Spanish SMEs: Empirical evidence from a stakeholders’ perspective. Business Research Quarterly, 19(1), 55–72. https://doi.org/10.1016/j.brq.2015.06.002

- Maimunah, I. (2009). Corporate social responsibility and its role in community development: An international perspective. The Journal of International Social Research, 2(9), 199–209.

- Maldonado-Guzman, G., Pinzón-Castro, S. Y., & Leana-Morales, C. (2017). Corporate Social Responsibility, Brand Image and Firm Reputation in Mexican Small Business. Journal of Management and Sustainability, 7(3), 38–47. https://doi.org/10.5539/jms.v7n3p38

- Mandhachitara, R., & Poolthong, Y. (2011). A model of customer loyalty and corporate social responsibility. Journal of Services Marketing, 25(2), 122–133. https://doi.org/10.1108/08876041111119840

- Maneet, K., & Sudhir, A. (2011). Corporate social responsibility – a tool to create a positive brand image [Paper presentation]. Proceedings of ASBBS Annual Conference, Las Vegas.

- Marin, L., Martín, P. J., & Rubio, A. (2017). Doing good and different! The mediation effect of innovation and investment on the influence of CSR on competitiveness. Corporate Social Responsibility and Environmental Management, 24(2), 159–171. https://doi.org/10.1002/csr.1412

- Markota Vukić, N. (2015). Corporate social responsibility reporting: Differences among selected EU countries. Business Systems Research, 6(2), 63–73. https://doi.org/10.1515/bsrj-2015-0012

- Melo, T., & Galan, J. I. (2011). Effects of corporate social responsibility on brand value. Journal of Brand Management, 18(6), 423–437. https://doi.org/10.1057/bm.2010.54

- Meyer, M. (2015). Positive Business: Doing Good and Doing Well. Business Ethics a European Review, 24(52), 175–197. https://doi.org/10.1111/beer.12105

- Minkiewicz, J., Evans, J., Bridson, K., & Mavondo, F. (2011). Corporate image in the leisure services sector. Journal of Services Marketing, 25(3), 190–201. https://doi.org/10.1108/08876041111129173

- Moisescu, O. (2017). From CSR to Customer Loyalty: An Empirical Investigation in the Retail Banking Industry of a Developing Country. Scientific Annals of Economics and Business, 64(3), 307–323. https://doi.org/10.1515/saeb-2017-0020

- Nochai, R., & Nochai, T. (2014, May). The Effect of Dimensions of Corporate Social Responsibility on Consumers’ Buying Behavior in Thailand: A Case Study in Bangkok. International Conference on Economics, Social Sciences and Languages.

- Öberseder, M., Schlegelmilch, B. B., & Murphy, P. E. (2013). CSR practices and consumer perceptions. Journal of Business Research, 66(10), 1839–1851. https://doi.org/10.1016/j.jbusres.2013.02.005

- Öberseder, M., Schlegelmilch, B. B., Murphy, P. E., & Gruber, V. (2014). Consumers’ Perceptions of Corporate Social Responsibility: Scale Development and Validation. Journal of Business Ethics, 124(1), 101–115. https://doi.org/10.1007/s10551-013-1787-y

- Park, J. H., Park, H. Y., & Lee, H. Y. (2018). The Effect of Social Ties between Outside and Inside Directors on the Association between Corporate Social Responsibility and Firm Value. Sustainability, 10(11), 3840. https://doi.org/10.3390/su10113840

- Price, J. M., & Sun, W. (2017). Doing Good and Doing Bad: The Impact of Corporate Social Responsibility and Irresponsibility on Firm Performance. Journal of Business Research, 80(C), 82–97. https://doi.org/10.1016/j.jbusres.2017.07.007

- Riera, M., & Iborra, M. (2017). Corporate social irresponsibility: Review and conceptual boundaries. European Journal of Management and Business Economics, 26(2), 146–162. https://doi.org/10.1108/EJMBE-07-2017-009

- Robert, K., Ilona, S., Barbara, K., & Andre, M. (2018). The future of CSR-Selected findings from a Europe-wide Delphi study. Journal of Cleaner Production, 183(2018), 282–291. https://doi.org/10.1016/j.jclepro.2018.02.119

- Romani, S., Grappi, S., & Bagozzi, R. P. (2016). Corporate Socially Responsible Initiatives and Their Effects on Consumption of Green Products. Journal of Business Ethics, 135(2), 253–264. https://doi.org/10.1007/s10551-014-2485-0

- Schmeltz, L. (2017). Getting CSR communication fit: A study of strategically fitting cause, consumers and company in corporate CSR communication. Public Relations Inquiry, 6(1), 47–72. https://doi.org/10.1177/2046147X16666731

- Servaes, H., & Tamayo, A. (2013). The Impact of Corporate Social Responsibility on Firm Value: The Role of Customer Awareness. Management Science, 59(5), 1045–1061. https://doi.org/10.1287/mnsc.1120.1630

- Šnircová, J., Helena, F., & Lucia, B. (2016). Sustainable Global Competitiveness Model as a New Strategic Opportunity for the Companies in Slovakia. Association for Information Communication Technology Education and Science, 5(2), 241–247. https://doi.org/10.18421/TEM52-19

- Stanisavljević, M. (2017). Does Customer Loyalty Depend on Corporate Social Responsibility. Naše Gospodarstvo/Our Economy, 63(1), 38–46. https://doi.org/10.1515/ngoe-2017-0004

- Tantalo, C., Caroli, M. G., & Vanevenhoven, J. (2012). Corporate social responsibility and SME’s competitiveness. International Journal of Technology Management, 58(1/2), 129–123. https://doi.org/10.1504/IJTM.2012.045792

- Uddin, M. B., Tarique, K. M., Hassan, R. (2008). Three Dimensional Aspects of Corporate Social Responsibility. https://www.semanticscholar.org/paper/Three-Dimensional-Aspects-of-Corporate-Social-Uddin-Tarique/ed38ed10c6fe815474df232004e9ffe2135e3cae

- Vasi, I. B., & King, B. G. (2012). Social Movements, Risk Perceptions, and Economic Outcomes: The effect of primary and secondary stakeholder activism on firms’ perceived environmental risk and financial performance. American Sociological Review, 77(4), 573–596. https://doi.org/10.1177/0003122412448796

- Vilanova, M., Lozano, J. M., & Arenas, D. (2009). Exploring the Nature of the Relationship Between CSR and Competitiveness. Journal of Business Ethics, 87(S1), 57–69. https://doi.org/10.1007/s10551-008-9812-2

- Visionary Analytics (2015). Retrieved September 9, 2019, from https://www.scribd.com/document/342317889/Socialiai-atsakingas-verslas-1-pdf

- Vlachos, P. A., Tsamakos, A., Vrechopoulos, A. P., & Avramidis, P. K. (2009). Corporate social responsibility: attributions, loyalty, and the mediating role of trust. Journal of the Academy of Marketing Science, 37(2), 170–180. https://doi.org/10.1007/s11747-008-0117-x

- Wang, H., Tong, L., Takeuchi, R., & George, G. (2016). Corporate Social Responsibility: An Overview and New Research Directions. Academy of Management Journal, 59(2), 534–544. https://doi.org/10.5465/amj.2016.5001

- Yoo, D., & Lee, J. (2018). The Effects of Corporate Social Responsibility (CSR) Fit and CSR Consistency on Company Evaluation: The Role of CSR Support. Sustainability, 10(8), 2956. https://doi.org/10.3390/su10082956

- Yuen, K. F., Thai, V. V., & Wong, Y. D. (2016). Are customers willing to pay for corporate social responsibility? A study of individual-specific mediators. Total Quality Management & Business Excellence, 27(7-8), 1–926. https://doi.org/10.1080/14783363.2016.1187992

- Zait, D., Onea, A., Tatarusanu, M., & Ciulu, R. (2015). The Social Responsibility and Competitiveness of the Romanian Firm. Procedia Economics and Finance, 20, 687–694. https://doi.org/10.1016/S2212-5671(15)00124-0

- Zhao, Z., Meng, F., He, Y., & Gu, Z. (2019). The influence of corporate social responsibility on competitive advantage with multiple mediations from social capital and dynamic capabilities. Sustainability, 11(1), 218. https://doi.org/10.3390/su11010218

Appendix 1

The coefficients of impact of CSR dimensions on the elements of firm competitiveness

Appendix 1. The coefficients of impact of CSR dimensions on the elements of firm competitiveness.