?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The last global economic crisis set fiscal consolidation as one of the most relevant goals of economic policy. At the same time, efforts are necessary to increase economic growth rates, particularly by increasing quantity and quality of public investment. However, the lack of fiscal space and other impediments make these goals hard to attain. On the contrary, in many countries data show negative dynamics of quantity and quality of public investment. In terms of energy efficiency investment, trends are positive. However, the pace of investment significantly underperforms the goals set. We argue that one of the major reasons is the lack of financial innovation and project selection methodology. For this reason, projects have still been mainly financed under traditional procurement models. Surprisingly, most countries do not exploit the advantages of alternative models of financing which do not affect public debt level, significantly reduce fiscal deficits and reduce fiscal risks. This article argues that a multi-criteria approach used at the initial stages of project preparation increases the potential for project realisation and the overall quantity and quality. In order to provide empirical evidence, we use information on energy efficiency streetlighting projects and present a case of a traditional versus alternative financing models.

a need for a systematic approach when selecting optimal financing model is a must;

a lack of financial innovation is one of the most critical impediments to a higher level of investment in revenue-generating projects common for the energy efficiency sector;

alternative models of financing enable public investment increase without harming the fiscal position;

a new methodology for selecting the most preferable model is presented;

a policy mix should take more comprehensive stance towards complexity of public investment projects.

Highlights

1. Introduction

In practice, when preparing and implementing public projects, particularly within the decision-making process for an investment option, the public contracting authority faces the problem of choosing the optimal investment option. These are cases when it is necessary to compare different available procurement models (i.e., traditional investment procurement [T.I.P.], public–private partnership [P.P.P.], E.S.C.O. model, leasing and similar) and various available financing options (non-refundable grant, commercial financing sources, financial instruments and the like). The decision of choosing the optimal investment option is more complex if the decision is made on the basis of validation criteria (for example, the total project life costs, the value of the payment from the budget, the value of non-refundable grants or the statistical treatment in relation to the government debt). Here is the need to apply multiple criteria decision analysis (M.C.D.A.) by which different procurement and financing models have to be evaluated in terms of the importance of a particular criterion. The importance of the specific criteria will depend on many factors such as economic, financial, fiscal, statistical, political and the like.

The aim of this article is to present the importance of integrated systems of planning public investment based on the optimisation of key factors that drive the economic and financial efficiency of public investment. Our approach is based on financing issues because selection of financing models fundamentally affects the overall chance of project realisation and efficiency level. We argue that contemporary systems of capital investment planning has to be improved by selecting the financing options at the very beginning of a project’s development. Experiences in energy efficiency projects show the importance of such an approach in practice. The research proposes a method for selecting the preferred investment option in cases where different procurement models and different financing combinations are available and decisions on investment options are based on several different selection criteria. We present the application of a possible method of selecting the optimal investment option utilising the consolidated data from three public lighting projects in the Republic of Croatia.

We structure the article as follows. In the second section we present the concept of an integrated system of financing public investment. The investment projects are complex and, in order to realise them effectively and efficiently, such complexity has to be taken into consideration. The same goes for the increasing number of financial options which do not just deal with financial matters but fundamentally affect project design, structure, method of procurements and, most importantly, final outcomes in terms of a standard delivered at affordable cost (value for money [V.f.M.]). The third section briefly describes the methodology developed and real life project details used for deriving the results. The fourth section presents the results of the experiment, where we show potentials of an M.C.D.A. as a project options selection tool. Finally, the conclusion draws some recommendations and presents avenues for further research.

2. The integrated system of financial model selection

One of the surprising results of the recent I.M.F. reports (2014a, 2015) is the disturbing trend of decreasing quantity and quality of public infrastructure, not just in emerging economies, but also in advanced economies. According to the I.M.F. (2014b), the stock of public capital, which reflects, to a large extent, the availability of infrastructure, has declined significantly as a share of output over the past three decades across advanced, emerging and developing economies. In advanced economies, this reflects primarily a trend decline in public investment from about 4% of GDP in the 1980s to 3% of GDP at 2013. Thus, lack of investment in public infrastructure is identified as one of the major reasons for sluggish economic growth in some of the countries analysed and significantly reduces their future growth potentials. In addition to that, it seems that lack of public investment is even more harmful for less developed countries featured by lower stock of public capital. Izquierdo et al. (Citation2019) find robust empirical evidence that countries with low initial stocks of public capital have significantly higher public investment multipliers than countries with a high initial stock of public capital. It is important to note that their findings were robust to the sample (European countries, U.S. states, and Argentine provinces). This also means, particularly for the countries where public investments are restrained due to fiscal consolidation, that those countries reduce their growth potentials. These findings also resonate with empirical study of Fournier (Citation2016), based on the sample of OECD countries, who finds ‘large growth gains’ from increasing the share of public investment in total government spending and, also, shifting the structure of government spending towards investment. Makuyana and Odhiambo (Citation2016), in their overview of empirical studies, conclude that public investment is important to economic growth; particularly when focused in basic infrastructures that stimulate private investment. Therefore, a way to overcome the limits imposed by fiscal consolidation and support higher levels of public investment is to turn towards private sector capital where governments have to set stimulating policies (Barbosa et al., Citation2016).

One of the sectors where the private capital role is gaining more importance is the energy efficiency sector. In terms of the energy efficiency sector, the effects of fiscal consolidation are observable through the significant underperformance of most of the countries in terms of goals set within supranational or national strategical documents. Even though the evidence shows that participation of the private sector in providing infrastructure services has been increasing, the problem is that the pace of investment is not satisfactory. This refers very much to the issues of energy efficiency investment as well. Deloitte (Citation2017a, Citation2017b) reports on energy efficiency in the European Union (E.U.) and warns that, despite the emphasis on energy efficiency from both international experts and policymakers, there is a consensus that the measures targeting an increase in energy efficiency implemented so far have not enabled the E.U. to reach its targets.

Numerous studies deal with the issue of lack of public investment and unsatisfactory level of efficiency. Authors state different causes of such state. Some authors (Collier et al., Citation2010) argue that there is a lack of robust and systematic procedures which resolve major impediments for the investment project realisation – ‘invest in the investment process’. Others state inefficient and corrupt bureaucracies (Chakraborty & Dabla-Norris, Citation2009). Investment in public infrastructure is massive by its nature and such projects have always been one of the vehicles for rent-seeking activities. Esfahani and Ramı́rez (Citation2003) and Haque and Kneller (Citation2015) reflect on the quality of project selection, management and implementation. Project selection procedures in practice are poorly developed across countries. In the best case, cost benefit analysis studies are used which are insufficient tools for decision-making in projects where multi-criteria procedures are necessary. The quality of management and implementation varies significantly depending on the financing (procurement) model selected. Additional issue refers to limited information and technical capacity (Collier et al., Citation2010) which not only refer to the public sector but to private sector companies also. Technical progress in terms of the development of new materials, electrical and other equipment, I.o.T. sensorics and other components of infrastructure increases the traditional asymmetry of information. In that sense, even the standard tools of economic and financial analysis have immense difficulties in coping with such disruptive change. Therefore, financial models have to be flexible, i.e., move from deterministic to stochastic assumptions of factors that determine future revenues and costs. In addition to technical issues, the legal framework and abundance of financial options make project framework increasingly comprehensive to all stakeholders. Henisz and Zelner (Citation2006) blame interest group pressures that often make project implementation impossible if the majority of interests are not vested. Vendors often pressure development and implementation of public infrastructure projects. They operate in a very competitive market and are eager to exploit any potential for market advantage. Guasch et al. (Citation2007) discuss impediments set by weak operational frameworks. One of the major obstacles related to lack of public investment is the issue of fiscal space (Collier et al., Citation2010; Easterly et al., Citation2007; Serven, Citation2007). After the latest economic crisis, public deficits and debt soared in many countries and even in in the aftermath, during recovery, countries engaged in fiscal consolidation efforts in order to prepare for a potential new recession period. In that sense, a lack of understanding of accounting classification and the favourable potential of alternative models of financing in terms of financing the project ‘off’ the government balance sheet is not an impediment per se, but more of an unexploited potential.

Considering the numerous issues that present challenges for the implementation of public investment projects, we argue that the integrated approach to the selection of a financing model resolves the numerous stated problems. One of the key elements of the integrated approach presented in this research is in the fact that it entails long-life cycle (L.L.C.) concept of investment project which, as a concept, strongly advocates E.U. institutions in recent periods. The key conceptual change refers to the shift towards measuring the revenues and costs of each project within the natural lifetime of the project cycle (or the length of the contract in case of public and private cooperation). Such an approach enables the transparent and precise measurement of V.f.M. of different procurement and financing options. Such approach upgrades traditional procurement models that are based on the public work provided and the alternative procurement models that focus on service, i.e., standards delivered by particular public infrastructure ().

Table 1. Procurement/financing models.

An integrated model of capital project selection not only reflects proper measurement of net present value of the project, which includes assumed capital and maintenance costs coupled with evaluation of risk materialisation. There are many other differences regarding the cost of capital, risk allocation and evaluation, statistical treatment of the financial transaction (or property ownership), tax treatment, discount rate differences and also issues of blending procurement models with grants and financial instruments (guarantees, loans or equity). These numerous factors affect the final decision on selection of most preferred models of procurement and financing in public projects and have to be part of the decision-making criteria: statistical classification, discount rate selection, tax issues (particularly in regards to value added tax), project maturity, cost of capital, financial structure (weighted average cost of capital [W.A.C.C.]) and identification/allocation of risks, etc.

In terms of statistical classification (European Union, Citation2013a, Citation2016), there are several main issues. Firstly, key question, which affects relation of public investment transaction and fiscal position (public deficit or debt), is government accounting system in place. In the case of accrual budgeting, public investment depreciates according to the value of the capital stock and accounting period of particular infrastructure. Such an approach is more favourable in terms of fiscal position and presents ‘accounting incentive’ for public investment. Cash-based government accounting systems accounts public investment as capital expenditure of the year in which the costs occurred and, thus, immediately negatively affects government fiscal position. In countries with a weak fiscal position, such accounting system has negative impact on the volume of investment. In addition, governments that undergo fiscal consolidation processes often reduce investment in order to improve fiscal position. The second issue relates to the statistical treatment of alternative funding options such as P.P.P.s and concessions. Eurostat provides options that public infrastructure financed by private capital, under certain criteria integrated within the contract, accounts as ‘off balance’ project and, therefore, does not present public debt. Of course, it will affect the fiscal position in terms of rise of expenditures due to government annual instalments as a fee for public sector services.

Discount rate selection reflects the fact that countries use different discount rates for economic and financial evaluation of investment projects. It is important to bear in mind that discount rates impose different effect depending on the nature of the investment project. For example, revenue-generating projects (EU, 2014) such as energy efficiency projects will have a lower net present value in case of higher discount rates because nominal revenues usually increase over time. This means that financial gap calculated for each project will be higher and the potential subsidy will increase. Thus, the selection of the discount rate is itself a policy tool for stimulating revenue-generating projects. E.U. policy allows for different sectoral discount rates and the use of higher discount rates for projects financed by the private sector (EU, 2014). Thus, there is a widely unused tool for stimulating sectoral investment (particularly in the domain of energy efficiency).

Regarding the tax issues, the fundamental difference between traditional government procurement and alternative models of financing is in the fact that in first case, government is providing public works, and in the second case, government is tendering for provision of services. The V.A.T. directiveFootnote1 clearly defines tax treatment of provision of public works versus provision of services. Due to its nature that entails capital expenses and works, V.A.T. in case of traditional financing applies per transaction. In the case of services (i.e., the energy efficiency service or providing a standardised level of quality of public lighting), V.AT. is charged based on service delivered (compensated by the monthly unitary charge).

Project maturity relates to several issues. One is related to the aforementioned statistical treatment which is based either on the accounting period of certain assets or the duration of the contract. However, in real life, the duration of the project very often depends on the ability or strength of the financial market. More developed financial markets are able to extend the length of financing which makes the project more sustainable in terms of budget potential. Of course, there is a trade-off between the market rate and maturity of the project, but such a conflict which may increase financing costs can be solved by appropriate financial structuring of the project, i.e., the use of financial instruments, participation of institutional investors or interest rate arbitrage coming from the investor from more favourable markets).

Cost of capital is primarily related to the basic credit rating of the particular country, however, there are many possibilities of credit cost reductions which stem from previously mentioned options such as different forms of subsidies, institutional investors or development bank participation, private investor with access to affordable capital costs, etc.

Finally, it is important to address identification of risks. Traditional procurement processes usually completely ignore the plethora of risks related to the complexity of capital infrastructure projects. Thus, there is no information about true quality and efficiency of particular public projects. There is no relation between the public standards delivered and the financial burden on the taxpayers. A transparent model that covers and provides monetisation of the potential risks resolves these inefficiencies. Therefore, the comprehensive risk matrix should be part of every public investment regardless of the project procurement model.

In terms of the characteristic features of traditional and alternative procurement models, we can list the following features ( presents the main features of different mixed procurement and financing models):

Table 2. Main differences between procurement and financing models.

Traditional models: in many countries the focus is on capital costs instead of whole life costs (W.L.C.), there is no risk matrix preparation and no identification, quantification and appropriate allocation, maintenance costs are ignored, no mechanism of measurement delivered standards, no mechanism of sanctioning non-delivered standards, no systematic ex ante as well as ex post measurement of V.f.M.;

Alternative models: a W.L.C. approach, focus on risk identification, quantification and allocation, defined standards of delivered services before procurement, very strong payment mechanism in case of non-delivered or partially delivered standards, systematic measurement of V.f.M. during whole project life cycle.

Generally, in traditional models of procurement one can find a relatively shorter repayment period of financing, smaller value of discount rate, risk retained to public investors and a relatively simple structure. All options within traditional models are on the balance sheet. In contrast, in alternative model of procurement one can find a longer contracting period, V.A.T. will apply on a (usually) monthly unitary charge, relatively higher costs of capital and significantly complex project structures.

In the case of research on M.C.D.A. of public investment options which is presented in this study, the research is mainly based on the use of different multiple criteria decision models applied to different issues and also sectoral analysis of application of service based methods on particular energy efficiency investment (usually by P.P.P. or E.S.C.O. model). The methodology of this research draws from study of Communities and Local Government (Citation2009) where the most relevant methods of M.C.D.A. are covered, such as continuous M.C.A. models, non-compensatory methods, multi-attribute utility models, linear additive models, the analytical hierarchy process, outranking methods, fuzzy M.C.A. and others. Among the many methods of multiple criteria decision-making, there are advantages and disadvantages of each method, these are well researched and described within the literature. In this study we use a linear additive methodology which is one of the most used methods due to its intuitive appeal and transparency.

In terms of application of the previously mentioned methodologies, we have not been able to find similar research which combines the concept of life cycle costs (L.C.C.), multiple decision-making methods and application of the fiscal aspect of public investment. However, it is interesting to present the results of several studies. Limaye and Limaye (Citation2011) particularly address the energy efficiency sector as a cost effective option for meeting energy requirements. However, they stress many barriers which lead to insufficient utilisation of E.S.C.O.s. They also provide examples of institutional solutions from Belgium, Croatia, the Philippines and India to stimulate private sector involvement. Campisi et al. (Citation2018) provide energy efficiency improvements of street lighting systems in Rome by using real options methodology to evaluate the investment strategy. Pantaleo et al. (Citation2014) researches the profitability of E.S.C.O. business models in the sector of biomass heating and CHP. Polzin et al.’s (Citation2016) research found market-based solutions, such as energy performance contracts (E.P.C.) in particular, can accelerate the diffusion of innovative technologies. They research modes of governance for municipal energy efficiency services – in the case of LED street lighting in Germany. Meyer et al. (Citation2017) provide a case-based overview of different business models of financing and procuring street lighting.

There are many studies which deal with technical issues of energy efficiency. For example, Rabaza et al. (Citation2013) present a simple model for designing public lighting based on optimising the technical parameters. Carli et al. (Citation2015) use M.C.D.A. to show its benefits within optimisation of energy management of smart cities. Carli et al. (Citation2018), as well as Beccali et al. (Citation2018) use M.C.D.A. to define the optimal decision strategy related to multiple and conflicting objectives in the planning of street lighting refurbishment. On the other hand, Neves et al. (Citation2018) deal with designing a municipal sustainable energy strategy by using M.C.D.A. where they find much importance on prioritising public lighting, biomass, bus/train improvements and solar photo-voltaic investment.

Therefore, as previously stated, there are many studies which cover the issues of selecting models of financing and procurement, as well as technical optimisation of energy efficiency projects. There are also numerous studies that cover different energy efficiency and energy sectors. However, we rarely find studies that cover the use of M.C.D.A. to support decisions within models of procurement and fiscal cost and benefits of public entities engaged in the project.

3. The data and methodology

In practice, as already mentioned, preparation and implementation of public investment projects fundamentally differs depending on the selected available procurement model (e.g., T.I.P., P.P.P., E.S.C.O. model, financial or operational lease and similar) and various available financing options (non-refundable grant, commercial financing sources, financial instruments and the like). In the Republic of Croatia, the valuation of the preferred investment option is mainly based on one criterion – the present value of W.L.C.s (AJPP, Citation2014). However, this is not the just case in the Republic of Croatia, but in other countries as well ( Burger & Hawkesworth, Citation2011; HM Treasury, Citation2011; World Bank Institute, Citation2013). The decision of choosing the optimal investment option is more complex, both on the programme and project level, if it is based on more than one validation criteria. Instead of deciding on the preferred investment option based on one of the criteria (e.g., W.L.C.s), it is possible to decide on the most affordable investment option based on multiple criteria. This criterion could be, for example, the W.L.C.s, the value of the payment from the budget, the value of domestic (Non-E.U.) grant or the statistical treatment in relation to the government debt. In our research, we strictly separate the ‘procurement model’ (T.I.P., P.P.P.) from co-financing and financing options (grant, financial instruments, commercial financing). The reason for this separation is that both in theory and practice concepts of procurement models often mix with the financing model. P.P.P. is not a ‘financing model’ but a public procurement model (European PPP Expertize Centre (EPEC), Citation2010). Here is the need to apply M.C.D.A. by which we can evaluate different procurement models and financing options in terms of the importance of a particular criterion (Communities & Local Government, 2009). The importance of the specific criteria will depend on many factors such as economic, financial, fiscal, statistical, political and the like.

The data needed to conduct the analysis are available by using the Public Sector Comparators made for three P.P.P.s of street lighting projects on the coast of the Croatian Adriatic. The data we used from mentioned P.P.P.s relates to T.I.P. used to assess L.C.C.s of T.I.P. We did not use the assessment of P.P.P. option because our assumption is that public administration and private partner are equally efficient. The reason for this assumption is that we want to focus not on the efficiency of the private sector but on different financial variation in potential procurement and financing option. The data we use from P.S.C.s are capital expenses (Capex), savings in electricity consumption, operating costs (Opex) and quantified annual risks. We present the consolidated data extracted from the P.S.C.s in :

Table 3. Consolidated data related to tree PSCs in street lighting projects.

In order to be able to compare projects, besides the fact that they are very similar investment processes (energy renewal of the public lighting system – replacement of energy non-efficient lamps with efficient L.E.D.s), we set the investment period equal to 12 years. The first year refers to process of implementation (renewal), which means that the exploitation of the investment starts at second year and ending at the finish of twelfth year.

Data on the sources of co-financing and financing are market based. We divide non-refundable grant support into the one from the E.U. funds and on national (domestic) non-refundable grant. The price of a commercial loan in the case where the beneficiary of a public contractor (in the application of the T.I.P. model) is 4% per year with and repayment period of 11 years. The financial instrument is a loan with a reduced interest rate of 0.5% per annum with and repayment period of 11 years. The price of a commercial loan in the case where the beneficiary is a private partner (when applying the P.P.P. model) is 4.5% with a repayment period of 11 years, while the price of equity is 7% per annum. The structure of financing sources when applying the P.P.P. procurement model is 20:80 (equity: debt). For the need to calculate the preferred investment option, we implement the procedure described in Scheme 1.

Scheme 1. Decision-making process on optimal investment option based on validation of four criteria

Source: Authors.

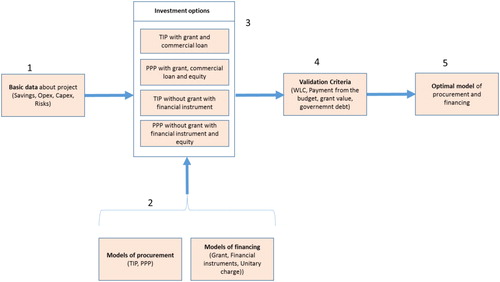

Basic data (1)

The model primarily defines basic project assumptions, such as expected capital expenses, operating costs, risks, and investment period (contract duration). Based on these data, it is necessary to calculate the financial viability of the project, i.e., the project’s ability to recover investment, operating costs and the risks from savings in energy consumption. It is a standard function of the financial rate of return (European Commission, Citation2014):

(1)

(1)

where FRR stands for – financial rates of return; I – capital expenditures; OR – operating income (savings); OC – operational costs; R – risks; i – current year; and n – investment period (duration of the contract). We compare the F.R.R. with the target discount rate (d). If the F.R.R. is different from the target discount rate, we can make the appropriate financial decisions as presented in the :

Table 4. The decision about financing based on the relationship between FRR and wanted discount rate.

Within this analysis, cases are considered when F.R.R. < d and F.R.R. < = d. If the F.R.R. < d project is justified to co-finance with non-refundable grant. We calculate grant amount according to (European Union, Citation2013b):

(2)

(2)

where the Grant is – value of grant (co-financing);

– co-financing rate (MaxCrpa); EC – eligible costs; PV(C) – present value of the capital expenses; PV(Nr) – present value of net revenue (OR-OC).

Models of procurement and financing (2)

In this part of the method for calculating the optimal model of procurement and financing, the procurement models are defined (e.g., T.I.P., P.P.P.,E.P.C., factoring, leasing or similar) and financing models (commercial loans, financial instruments – loans, equity or guarantee, grants and the like). In order to present the model’s performance, in this example, as a model of procurement, we use T.I.P. and P.P.P. As models (sources) of financing, we use a commercial loan, financial instrument – loan, non-refundable grant and equity.

Investment options (3)

We select four combinations of models of procurement and sources of financing and funding in the previously mentioned sense:

T.I.P. with grant and commercial loan;

P.P.P. with commercial equity and commercial loan;

T.I.P. without grant and with financial instrument (T.I.P.-F.I.);

P.P.P. without grant, with financial instrument and commercial equity (P.P.P.-F.I.).

Calculation continues with combination 1 with annuity calculation:

(3)

(3)

where A stands for – annuity; P – principal; i – interest rate; and n – number of periods of repayment loan. The resulting annuity values (projections of interest and principal) are included in the basic characteristics of the project (Capex, Opex, savings and risks) and according to (2) the financial sustainability of the project is re-examined. If it turns out that the project is not financially viable, the output of this step will be the additional value of the grant.

Finally, from the received complete model, they select the key outputs that will represent, in the last step of the method, the criteria for calculating the optimal investment option. In the case of the P.P.P. model of procurement (combination 2), we start calculation with the main features of the project (Capex, Opex, savings and risks) and calculate in accordance with (2) value of the grant (in case that project is not financially sustainable). After the financial sustainability test, the calculation of the costs of the financing source follows. Costs of financing sources, when applying a P.P.P. procurement model, based on W.A.C.C. since P.P.P. options are represented by debt and equity at different rates and different tax treatment. We calculate the projection of the depreciation of the total sources of financing according to (3), with the price being calculated in accordance with the formula for the calculation of W.A.C.C.Footnote2:

(4)

(4)

where the WACC stands for – weighted average cost of capital;

– expected rate of return;

– expected interest rate on debt;

– share of equity in total financial sources;

– share of debt in total financial sources; and t – corporate tax rate .

After the linkage of the basic project criterion with financial costs, we derive the value of the unitary charge in such a way that the cumulative net cash flow at the end of the project is equal to zero:

(5)

(5)

where

– unitary charge of i-th period; and

– financial costs of i-th period.

Validation criterion (4)

Since in practice, especially in economic and financial practice, there are often many criteria for deciding on a particular action or business, this is also the case when choosing the optimal investment decision. Authorities often encounter a selection problem in circumstances when a criterion (e.g., Capex or W.L.C.s) is not enough to make a decision. Then, often, decision-makers bring suboptimal decisions. This article shows how the authorities could be able to decide on the choice of investment options in case of multiple criteria. Based on previously stated recommendations (EPEC Citation2010; European Commission, Citation2014), we select the following criteria:

Criterion 1: W.L.C.;

Criterion 2: Payment from the budget;

Criterion 3: Value of domestic (non-E.U.) grants;

Criterion 4: Statistical treatment of the project (existence of government debt).

It is worthwhile to briefly elaborate importance of the following criteria. W.L.C.s or L.C.C.sFootnote3 have been applied by a large range of sectors in the E.U. Also, under the 2014 E.U. procurement rulesFootnote4 a contract must be awarded based on the most economically advantageous tender (M.E.A.T.), which is also used in this article. L.C.C. means that all of the costs incurred during the lifetime of the project have to be considered (purchase price and all associated costs; operating costs, including energy, fuel and water use, spares, and maintenance; end-of-life costs or residual value). Unfortunately, most of the projects within traditional public procurement are still based only on capital costs which is problematic for project selection as well as future sustainability of a particular public entity. In terms of the importance of payment from the budget, clearly this criterion presents preference of the public entity to reduce payments from the budget and, therefore, improves fiscal position. Similarly, the value of domestic grants denote transfers from other government entities which reduce needs for own budget spending, but still affect public deficit and debt. Ideally, in financial terms, projects financed by an E.U. grant would reduce capital payments from the budget and need for grants of other government entities. Finally, statistical treatment of the project becomes important criteria under fiscal consolidation pressure. Service-based models, particularly P.P.P. can be treated as private investment and accounted off balance sheet of the government entity. This criterion can be the most relevant in case of severe problems with fiscal position.

4. Results and discussion

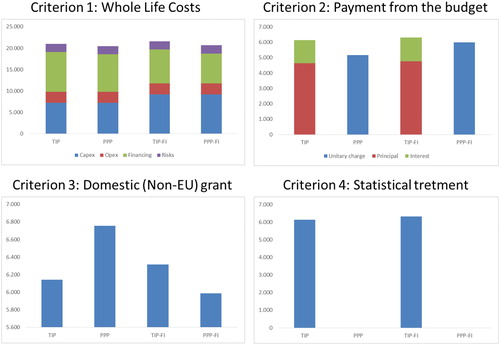

In this section, we present the empirical results of methodology previously drafted. presents the present value of financial alternatives depending on the criteria applied. We can observe notable differences between financial options within each criteria used for the calculations.

Figure 1. Values of selected criterion.

Source: Authors’ simulations.

The results in show that the different criteria used per each financial model results with different present value of the project. This means that according to one criterion, an investment combination would be acceptable, while the second criterion (if it would be the only criterion for the selection) would made other investment option more appropriate. In order to overcome this heterogeneity, we propose selection of investment options according to all of the previously mentioned criteria.

Selection of optimal model (5)

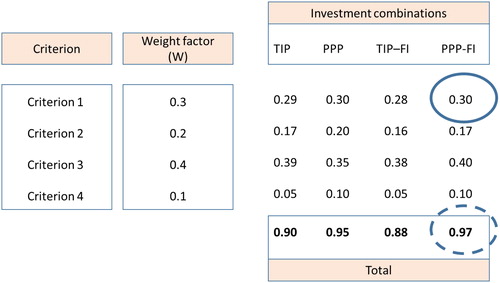

In order to calculate the optimal investment option, the method of M.E.A.T. was used. This comparison method is appropriate because it exploits the mutual relationship of different investment combinations and we can compare it with financial options based on one criterion. Depending on the economic and budgetary position of each authority, the acceptable value of individual weighting factors (W) will be determined. We present the process of evaluating investment combinations in relation to weighting factors by :

Figure 2. Comparison of investment combination by using the weighting factors.

Source: Authors’ calculations.

The valuation of an individual investment combination within each criterion is calculated using:

(6)

(6)

and total score is calculated as:

(7)

(7)

where

– the criterion of the observed investment combination;

– the minimum value of the investment combination within one criterion;

– the observed investment combination; W – weighting factor; TS – total score; n – observed investment option; and k – final number of investment options. In our example, the value of the P.P.P.-F.I. investment criterion within criterion 1 is

rounded to 0.3 (in , the rounded solid line is shown).

When calculating all the values of individual investment combinations within each of the individual criteria, the total sum of all the values for each investment combination is calculated. We obtain the following value: 0.9 for T.I.P., 0.95 for P.P.P., 0.88 for T.I.P-F.I. and 0.97 for P.P.P.-F.I. We obtain the highest number of points for the investment combination of P.P.P.-F.I. and it is the optimal investment option in the example (in rounded-off line).

It is important to emphasise that the preferred final decision will depend the most on the selected weighting factors. In that sense, special attention needs to be dedicated to the weighting factors in the phase of the preparation of the project. This value will depend on the combination of the existing fiscal, financial, economic, statistic and political position of the authority and also of the named factors’ state that wants to be accomplish in the future by executing the project. For that reason, selecting the value of weighting factors is very complex. In addition, we clearly present this case by quantitative analysis. However, the important difference between P.P.P. and the traditional model is that qualitative decision which refers to the process of defining the standard of public services and by their permanent measurement. This allows for continuous monitoring and improvements if the project does not achieve the planned V.f.M. in the project’s lifetime. Lack of use of such principles in the traditional procurement model is its detrimental flaw. For this reason, the traditional model is not transparent and taxpayers are not able to evaluate how efficiently the government spends their money.

However, the complexity of alternative models (P.P.P. and concession) and high cost of preparation often are not efficient at relatively small projects. This obstacle can be overcome efficiently with the creation of national templates which entail contracts, P.S.C.s, risk matrix and the like (EBRD, Citation2017; Iossa & Saussier, Citation2018). We can achieve substantial progress in the area of transparency and efficiency of the traditional model, if we translate and apply principles of preparation and supervising of the project over its lifetime (characteristic for P.P.P.) to T.I.P. There are no barriers for this besides the will of the public management.

5. Conclusion and policy implications

Both theoretical and empirical studies in recent period show significant economic benefits coming from the increased quantity and quality of public investments. However, much research discussed in this study show a number of obstacles which prevent accumulation of public capital. One of the oft-cited impediments refers to a lack of financial innovation which is particularly important within countries burdened with fiscal consolidation goals. In such cases, there are alternative models of financing which can enable public investment increase without harming the fiscal position. However, public sector entities do not use available methods of decision-making which could clearly show benefits of particular model of procurement. The empirical research in this article reveals the potential of using such methodology.

The analysis presented in this article shows a method by which public-contracting authorities can decide on the optimal investment option in cases where the decision to choose the investment option is based on more than one criteria. In order to identify the preferable investment option, we use a deterministic method of evaluating the results of certain criteria of a particular investment option. We combine this with the valuation of an individual investment option within a particular criterion by the standard practice used to evaluate tenders in public procurement procedures. M.E.A.T. selection methodology presented in this research can be exploited not just within energy efficiency projects but for decision-making within all public investments.

In terms of policy implications and recommendations, it is important to address current and long-term problems related to unsatisfactory attainment of energy efficiency goals set by the E.U. and other supranational entities and countries. One of the key reasons for such failures is in the lack of systematic approaches addressing the most important factors that enable the realisation of energy efficiency investments. The systematic approach presented in this article enables the selection of an optimal financial model depending on the selection of key criteria. Such procedures have a direct impact in the form of achieving V.f.M. However, an indirect impact comes from the fact that the volume of a project rises because the quality of project planning, reliability and credibility of the financial model decrease financial risks, which often curb the project’s realisation. Finally, integration of issues related to statistical classification, inclusion of W.L.C., V.f.M. concept and detailed identification, distribution and monetisation of project risks will substantially increase the overall volume and efficiency of projects on the energy efficiency market. Therefore, there are three key policy recommendations set by this article:

- When preparing energy efficiency projects, public entities should always focus on W.L.C.s instead of the traditional approach, which is based solely on capital costs;

- By applying the procedures elaborated on in this article, every project should allow for optimal variation of technological, financial and procurement option;

- A comparison of options should be conducted by utilising M.C.D.A. as described in this article.

Finally, it is important to note that the methodology presented in this research should be a standard procedure applied within public investment decision-making process across all tiers of governments. More narrowly, the methodology can provide a key tool for the selection of funding sources according to the goals of economic development and fiscal policy. It can be particularly valuable for countries with a lack of fiscal space, and thus, the inability to finance public investment within traditional procurement methods.

Future research should focus on augmenting methods of multiple criteria optimisation of investment options. It would be worth exploring the stochastic method with the inclusion of probability distributions of particular financial categories. This is particularly interesting when we compare traditional with alternative procurement models, such as P.P.P., the main feature of which is the transfer of risk from the public to a private partner. Furthermore, it would be interesting to expand the analysis further, and besides broadening financial parameters, include technical, legal and other important categories of project realisation. In addition, one of the important steps in decision-making on public investment is risk analysis. Therefore, inclusion of expected risks in terms of availability of financial sources, important financial parameters such as inflation, interest rate, exchange rate, as well as other non-financial risks would be further step in acknowledgement of risk and uncertainty within decision-making process.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

References

- Agencija za javno-privatno partnerstvo Republike Hrvatske (AJPP). (2014). Značenje i izračun vrijednosti za novac kod projekata javno-privatnog partnerstva, Priručnici za pripremu i provedbu modela javnoprivatnog partnerstva (Priručnik br. 6, Verzija 2). http://www.aik-invest.hr/wp-content/uploads/2015/11/p6-v2-vfm-finalno-za-objavudoc.pdf

- Barbosa, D., Carvalho, V. M., & Pereira, P. J. (2016). Public stimulus for private investment: An extended real options model. Economic Modelling, 52(Part B), 742–748. doi: 10.1016/j.econmod.2015.10.013

- Beccali, M., Bonomolo, M., Leccese, F., Lista, D., & Salvadori, G. (2018). On the impact of safety requirements, energy prices and investment costs in street lightning refurbishment design. Energy, 165, 739–759. doi: 10.1016/j.energy.2018.10.011

- Burger, P., & Hawkesworth, I. (2011). How to attain value for money: Comparing PPP and traditional infrastructure public procurement. OECD Journal on Budgeting, 11(1), 91–146. https://www.oecd.org/gov/budgeting/49070709.pdf doi: 10.1787/budget-11-5kg9zc0pvq6j

- Campisi, D., Gitto, S., & Morea, D. (2018). Economic feasibility of energy efficiency improvements in street lighting systems in Rome. Journal of Cleaner Production, 175, 190–198. doi: 10.1016/j.jclepro.2017.12.063

- Carli, R., Dotoli, M., & Pellegrino, R. (2015). ICT and optimization for the energy management of smart cities: The street lighting decision panel [Paper presentation]. 2015 IEEE 20th Conference on Emerging Technologies & Factory Automation (ETFA), Luxembourg, pp. 1–6.

- Carli, R., Dotoli, M., & Pellegrino, R. (2018). A decision-making tool for energy efficienc optimization of street lighting. Computers & Operations Research, 96, 223–235. voldoi: 10.1016/j.cor.2017.11.016

- Chakraborty, S., & Dabla-Norris, E. (2009). The quality of public investment (IMF Working Paper, WP/09/154). International Monetary Fund. https://www.imf.org/en/Publications/WP/Issues/2016/12/31/The-Quality-of-Public-Investment-23110

- Collier, P., Van der Ploeg, F., Spence, M., & Venables, A. J. (2010). Managing Resource Revenues in Developing Economies. IMF Staff Papers, 57(1), 84–118. https://www.elibrary.imf.org/view/IMF024/10478-9781589069114/10478-9781589069114/10478-9781589069114_A004.xml?redirect=true doi: 10.1057/imfsp.2009.16

- Communities and Local Government. (2009). Multi-criteria analysis: A manual. Department for Communities and Local Government. http://eprints.lse.ac.uk/12761/1/Multi-criteria_Analysis.pdf

- Deloitte. (2017a). Energy efficiency in Europe. The levers to deliver the potential. https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Energy-and-Resources/energy-efficiency-in-europe.pdf

- Deloitte. (2017b). IPSAS in your pocket 2017. https://www.iasplus.com/en/publications/public-sector/ipsas-in-your-pocket-2017

- Easterly, W., Irwin, T., & Serven, L. (2007). Walking up the down escalator: Public investment and fiscal stability. The World Bank Research Observer, 23(1), 37–56. doi: 10.1093/wbro/lkm014

- EBRD. (2017). Transition report 2017–18, Sustaining growth. https://www.ebrd.com/transition-report-2017-18

- Esfahani, H. S., & Ramı́rez, M. T. (2003). Institutions, infrastructure, and economic growth. Journal of Development Economics, 70(2), 443–477. doi: 10.1016/S0304-3878(02)00105-0

- European Commission. (2014). Guide to cost-benefit analysis of investment projects economic appraisal tool for cohesion policy 2014–2020. http://ec.europa.eu/regional_policy/sources/docgener/studies/pdf/cba_guide.pdf

- European PPP Expertize Centre (EPEC). (2010). Procurement of PPP and the use of competitive dialogue in Europe: A review of public sector practices across the EU. https://www.eib.org/attachments/epec/epec_procurement_ppp_competitive_dialogue_en.pdf

- European Union (EU). (2013a). European system of accounts ESA 2010. http://ec.europa.eu/eurostat/documents/3859598/5925693/KS-02-13-269-EN.PDF/44cd9d01-bc64-40e5-bd40-d17df0c69334

- European Union (EU). (2013b). Regulation (EU) No 1303/2013 of the European parliament and the council of 17 December 2013. Official Journal of the European Union. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32013R1303&from=HR

- European Union (EU). (2016). Manual on government deficit and debt implementation of ESA, 2010. http://ec.europa.eu/eurostat/documents/3859598/7203647/KS-GQ-16-001-EN-N.pdf/5cfae6dd-29d8-4487-80ac-37f76cd1f012

- Fournier, J. M. (2016). The positive efffect of public investment on potential growth (OECD Economics Department Working Papers, No. 1347, OECD Working Paper, 71). OECD.

- Guasch, J. L., Laffont, J.-J., & Straub, S. (2007). Concessions of infrastructure in Latin America: Government-led renegotiation. Journal of Applied Econometrics, 22(7), 1267–1294. https://doi.org/10.1002/jae.987

- Haque, M. E., & Kneller, R. (2015). Why does Public Investment Fail to Raise Economic Growth? The Role of Corruption. The Manchester School, 83(6), 623–651. https://doi.org/10.1111/manc.12068

- Henisz, W., & Zelner, B. (2006). Interest groups, veto points, and electricity infrastructure, deployment. International Organization, 60(1), 263–286. doi: 10.1017/S0020818306060085

- HM Treasury. (2011). Quantitative assessment: User guide. December. http://www.pppi.ru/sites/all/themes/pppi/img/Quantitive%20assesstment%20User%20guide.pdf

- International Monetary Fund (IMF). (2014a). Legacies, clouds, uncertainties. World Economic Outlook, October. http://www.imf.org/external/pubs/ft/weo/2014/02/

- International Monetary Fund (IMF). (2014b). Government finance statistics manual 2014. https://www.imf.org/external/Pubs/FT/GFS/Manual/2014/gfsfinal.pdf

- International Monetary Fund (IMF). (2015). Making public investment more efficienty (Staff Report). http://www.imf.org/external/np/pp/eng/2015/061115.pdf

- Iossa, E., & Saussier, S. (2018). Public-private partnerships in Europe for building and managing public infrastructures: An economic perspective. Annals of Public and Cooperative Economics, 89(1), 25–48. doi: 10.1111/apce.12192

- Izquierdo, A., Lama, R., Medina, J. P., Puig, J., Riera-Crihton, D., Vegh, C., & Vuletin, G. J. (2019). Is the public investment multiplier higher in developing countries? An empirical exploration (IMF Working Paper, 19, 289). IMF. https://www.imf.org/en/Publications/WP/Issues/2019/12/20/Is-the-Public-Investment-Multiplier-Higher-in-Developing-Countries-An-Empirical-Exploration-48836

- Limaye, D. R., & Limaye, E. S. (2011). Scaling up energy efficiency: the case for a Super ESCO. Energy Efficiency, 4(2), 133–144. https://doi.org/10.1007/s12053-011-9119-5

- Makuyana, G., & Odhiambo, N. M. (2016). Public and private investment and economic growth: A review. Journal of Accounting and Management, 6(2), 25–42.

- Meyer, M., Maurer, L., Freire, J., & De Gouvello, C. (2017). Lightning Brazilian cities: Business models for energy efficient public street lighting. ESMAP, World Bank Group.

- Neves, D., Baptista, P., Simoes, M., Silva, C. A., & Figueira, J. R. (2018). Designing a municipal sustainable energy strategy using multi-criteria decision analysis. Journal of Cleaner Production, 176, 251–260. doi: 10.1016/j.jclepro.2017.12.114

- Pantaleo, A., Candelise, C., Bauen, A., & Shah, N. (2014). ESCO business models for biomass heating and CHP: Profitability of ESCO operations in Italy and key factors assessment. Renewable and Sustainable Energy Reviews, 30, 237–253. doi: 10.1016/j.rser.2013.10.001

- Polzin, F. V., Flotow, P., & Nolden, C. (2016). Modes of governance for municipal energy efficiency services: The case of LED street lighting in Germany. Journal of Cleaner Production, 139, 133–145. doi: 10.1016/j.jclepro.2016.07.100

- Rabaza, O., Peña-García, A., Pérez-Ocón, F., & Gómez-Lorente, D. (2013). A simple method for designing efficient public lightning, based on new parameter relathionships. Expert Systems with Applications, 40(18), 7305–3315. doi: 10.1016/j.eswa.2013.07.037

- Serven, L. (2007). Fiscal Rules, Public Investment, and Growth. (Policy Research Working Paper 4382). The World Bank. November 2007, https://doi.org/10.1596/1813-9450-4382.

- World Bank Institute (WB). (2013, May 28). Value-for-money analysis–practices and challenges: How governments choose when to use PPP to deliver public infrastructure and services (Report from World Bank Global Round-Table).