?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The present article adopted the dynamic panel data method to investigate the effect of the inflow of remittances on financial inclusion (FI), particularly focusing on high remittance-receiving developing countries between 2011 and 2018. The current research found that remittances that foster FI are associated with better institutional quality. The evidence revealed that the effect of remittances on FI is conditional upon individuals’ perception of the institutions. Positive coefficient on the interaction terms indicates that the impact of remittances on FI can be enhanced in the recipient countries, if the public trusts the financial institutions. Hence, the overall results of the current research suggest that the impact of remittances on FI is conditional on institutions. On a final note, the policy implications of these findings are thoroughly evaluated at the end of this article.

1. Introduction

The money earned by migrants outside the country which is then sent back to their country of origin remains a significant research area among scholars and policymakers. Between 2011 and 2018, global remittances had increased from 470 to 683 billion dollars. On another note, the flow of remittances to low- and middle-income (INC) countries increased from 343 billion dollars in 2011 to 529 billion dollars in 2018, signifying a growth by 53%. It is crucial to acknowledge that the inflow of remittances to high-INC countries only grew by 21%, from 127 billion dollars in 2011 to 154 billion dollars in 2018. This clearly suggests that remittances had contributed significantly to economic development of low- and middle-INC countries. On a similar note, Bollard et al. (Citation2011) reported that remittances do not only provide a direct improvement on the welfare of recipients but also indirectly benefit those with whom the recipients conduct transactions. Regarding this matter, it should be understood that the inflow of remittances increases the ability of recipient households to join and gain access to financial services, thereby encouraging further growth and expansion of financial inclusion (FI). In particular, it has also been observed that remittances to developing economies for the last two decades have been 15 times of official transfers, 18 times of official capital flows, more than double private capital flows, about 30% of exports (Barajas et al., Citation2010), and nearly three times more than official aid flows (World Bank, Citation2016).

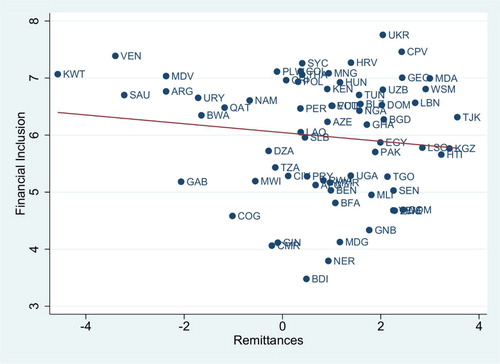

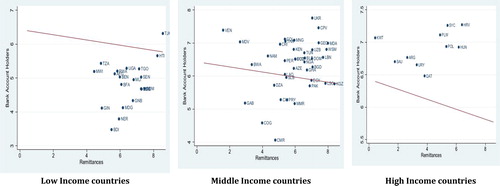

On a more important note, several scholars have stressed the importance of remittances to FI. For example, Aggarwal et al. (Citation2006) argued that migrants’ remittances can lead to financial sector development in less developed economies considering its ability to boost the total volume of deposits and loans granted by banking institutions to financially excluded segment. Similarly, Orozco et al. (Citation2006) stated that the financial development (FD) of the recipient country may be promoted through remittances by stimulating the demand and access to various financial products. At the same time, the provision of remittance transfer services allows banks and financial institutions, in general, to gather information about unbanked recipients and mitigate the adverse selection problem. Apart from capturing money flows, the remittance channel can be used to sell financial service packages that are geared towards low-INC individuals (Toxopeus & Lensink, Citation2007). However, the scatter plots for a set of 70 countries ( and in Appendix) do not support the claim that remittances can lead to the expansion of FI. As can be observed, remittances seem to have increased substantially over the years, while FI remains low. The correlation between remittances of migrant workers and FI, either in full sample or by INC group, is estimated to be negative, which suggests a contradiction with the existing theories.

Figure A1. Remittances and Financial inclusion (Bank account holders) in 2011–2018. Note: The list of 70 sample countries is provided in in Appendix. Source: Authors’ compilation from World Bank data (Citation2018).

Figure A2. Remittances and Financial inclusion (Bank account holders) in 2011–2018 according to Income Group.

The present study proposed the argument that a low expansion of FI may be the result of poor institutional quality (INQ). In particular, this can be explained by the ability of institutions to manage bureaucratic processes in the form of reducing the amount of documentation or paperwork as well as sustaining the trust of clients during remittance transactions. In addition, it should be understood that INQ is an important factor that influences the decision of individuals to gain access to financial services provided by particular financial institutions. Hence, the public may avoid using the institutions as a channel for remittance transactions if they have a general distrust of financial institutions as well as being wary of the long bureaucratic processes involved in remittances. As a result, they will prefer more conservative alternatives which may affect the expansion of the institutions. Therefore, against this backdrop, the present study examined the impact of remittances on the level of FI in accordance with the level of INQ. The main research hypothesis for this present study is as follows: an increase in remittances and INQ leads to more FI.

The current article will extend the existing literature that failed to examine the impact of remittances on FI which is associated with better INQ, particularly bureaucratic procedures and trust as well as the response of household recipients towards FI. Moreover, the present study aims to address the shortcoming by investigating the interaction effect of remittances and INQ on FI. Hence, this study will try to fill in the literature gap using a dynamic panel data framework with an orthogonalised interaction term. To this end, a dynamic system generalised method of moments (GMM) model was adopted for the current research and the major results of the present study revealed that remittances alone are unable to generate FI. However, it should be noted that FI can be increased with better INQ. Second, as suggested by Brambor et al. (Citation2006), this article calculated the marginal effects and standard errors for the interaction term. In this case, it is very important to evaluate how the marginal effect of remittances on FI changes with the degree of intuitional quality in remittance recipient countries. Regarding this matter, it should be acknowledged that omitting the calculation of marginal effects may lead to misinterpretation of the interaction term.

The rest of the current article is organised as follows: Section 2 provides a brief literature review on the demand for financial products and services, remittances, and FI. Section 3 covers the methodology, model specifications, and data description. Section 4 provides the results and result discussion. Finally, the conclusion is presented by summarising the main findings of the article along with the suggestion for further extensions of future work.

2. Literature review

Remittances have attracted considerable scholarly attention. Meyer and Shera (Citation2017) argued that remittances may sometimes exceed the flows of FDI. The result of their study found that remittances have a positive impact on growth. However, Cismaș et al. (Citation2020) found that the inflow of remittances does not stimulate economic growth.

Numerous studies have concentrated on the linkages between remittances and FI. Regarding this matter, it is crucial to understand that remittances can affect FI in at least two ways. First, remittances might increase the demand for savings instruments considering that the fixed costs of sending remittances may cause the flows to be lumpy, thus providing households with excess cash for a certain period of time. As a result, this might potentially increase their demand for deposit accounts based on the fact that financial institutions offer households a safe place to store their temporary excess cash (Misati et al., Citation2019; Muktadir-Al-Mukit & Islam, Citation2016). Second, remittances might increase the chances of recipients in obtaining a loan from formal financial institutions or banks. The processing of remittance flows provides financial institutions with the necessary information on the INC of the recipient households. Moreover, this information might increase the willingness of financial institutions to extend loans to otherwise opaque borrowers. Apart from that, they may be able to assess the creditworthiness of the remittance recipients (Giuliano & Ruiz-Arranz, Citation2009), which further suggests a positive relationship between remittances and FI. However, remittances might help to relieve the financing constraints of households, which may cause the demand for loans to fall due to the increase of remittance inflows. Meanwhile, it should be noted that steady inflows of remittances will reduce the reliance of households on loans from banks and other financial institutions in financing their basic consumption needs and other expenses. Therefore, this view hypothesises a negative relationship between remittances and FI (Chami & Fullenkamp, Citation2013). Generally, the empirical literature supports the view that both the sending and receiving of remittances increase the use of financial services between the senders and recipients (Aggarwal et al., Citation2006; Anzoategui et al., Citation2014; Gibson et al., Citation2010; Orozco & Fedewa, Citation2005).

Several factors have been identified to lead to FI. Wellalage and Locke (Citation2020) and Naz et al. (Citation2020) reported that education and INC are positive determinants of FI, while inflation retards inclusion. Dabla-Norris et al. (Citation2020) found that FD and INC are important drivers of opening bank account. Some scholars argued that education, economic institutions, INC, political stability, quality institutions, inflation, and FD are essential determinants of FI (see Adegbite & Machethe, Citation2020; Anarfo et al., Citation2020; Demirgüç-Kunt et al., Citation2020; Koomson et al., Citation2020; Ozili, Citation2020).

Moreover, some scholars have also considered the linkages between INQ and FD. Cull and Effron (Citation2008) found that INQ fosters FD. Meanwhile, Guiso et al. (Citation2008b) examined the financial markets during the crisis and concluded that formal strong institution quality and social capital which are able to foster trust by reducing the incentive to cheat are the prerequisites of a stable financial system. A considerable amount of studies have found that only individuals with sufficiently high trust are willing to participate in financial markets (see Adams-Kane & Lim, Citation2014, Citation2016; Guiso et al., Citation2008a; Guiso et al., Citation2008b; Shad et al., Citation2018). Law and Ibrahim (Citation2013) asserted that trust is more significant in the development of the banking sector, but no significant relationship was noted between trust and stock market development.

Overall, it can be argued that the available published studies have failed to examine the impact of remittances on FI which is associated with better INQ. Therefore, the present study has found the need to address the drawbacks by conducting a thorough investigation of the effect of remittances on FI conditioning at the level of INQ.

3. Methodology

3.1. Data description

The current research utilised the secondary data gathered from numerous sources, mainly the World Development Indicators of the World Bank as well as the International Monetary Fund. In the case of the present study, data were collected from 70 remittances receiving developing countries over the period of 2011–2018. Some developing countries were excluded due to lack of data for FI. The list of selected counties can be observed in provided in the Appendix.

Table A1. List of countries included in our sample.

The dependent variable in the present study is FI which was measured based on bank account holders per 1000 individuals, followed by the number of automated teller machine (ATM) per 100,000 adults. Regarding this matter, a number of studies (Anzoategui et al., Citation2014; Demirgüç-Kunt et al., Citation2011) also utilised bank account holders per 1000 individuals as a proxy for FI. Meanwhile, a recent study by (Sarma & Pais, Citation2008, Citation2011) was found to use the ATM per 100,000 adults as a proxy for FI.

More importantly, it should be noted that most of the links between the macroeconomic variables in this area are mainly based on FD (Beck & Demirguc-Kunt, Citation2009) which encompasses FI. In this case, the discussion was centred on both considering the fact that FI is a sub-set of FD. Therefore, the independent variables for this study are the common explanatory variables for FI or FD suggested by previous studies, including migrant workers’ remittances (MWR), INQ, human capital (HC), inflation rate, and INC of the remittances recipient countries.

MWR are described as the ratio of personal remittances inflow to the total population. In this case, it should be understood that the remittances are capable to spur FD by creating a demand for the opening of bank accounts and saving instruments (Anzoategui et al., Citation2014), including the exploration of bank services by recipients (Giuliano & Ruiz-Arranz, Citation2009; Orozco & Fedewa, Citation2005; Aggarwal et al., Citation2006; Gibson et al., Citation2010). Hence, this clearly suggests that remittances may increase the usage of bank products. On the contrary, Brown et al. (Citation2014) revealed that remittances do not increase the likelihood of holding a bank account. In addition, a study by (Calderón et al., Citation2007) indicates that remittances may reduce credit demands and even impose a dampening effect on credit markets. Similarly, it was also discovered that remittances serve as a substitute for credits with no link to FI (Ambrosius & Cuecuecha, Citation2013; Brown et al., Citation2013), thus leading to a negative coefficient for this variable.

The INQ developed by Kaufmann et al. (Citation2008) refers to the measure of institutional development in terms of governance indicators, particularly the rule of law as well as government effectiveness. It is defined as higher value indicates higher institutional. More importantly, INQ has been revealed to foster FD and FI (Adams-Kane & Lim, Citation2014, Citation2016; Guiso et al., Citation2008a, Citation2008b; Shad et al., Citation2018), thus a positive coefficient is expected for this variable.

HC is described as knowledge, skills, and experiences possessed by individual workers, which is particularly measured in terms of education. Regarding this matter, remittances help poor recipients to overcome liquidity constraints and investments on HC (Calero et al., Citation2009; Taylor & Wyatt, Citation1996). According to Dwyfor Evans et al. (Citation2002), HC positively influences FD. Contrastingly, Arora (Citation2012) found a negative relationship between FD and HC. This study utilised mean years of schooling from the United Nation dataset as the proxy for HC and it is expected to provide a positive influence on FI.

In the present study, INC was measured by the per capita GDP which is expected to be positively linked to FD and FI. Regarding this matter, it is believed that the demands of financial activities tend to be greater in richer countries (Calderón & Liu, Citation2003; Demetriades & Hussein, Citation1996; Law & Azman-Saini, Citation2012; Rojas-Suarez & Amado, Citation2014; Yang & Yi, Citation2008).

CPI refers to inflation measured by consumer price index. An increase in money supply leads to inflation which makes loanable funds cheaper, thus reducing cost of borrowing for corporate and individual. In this case, it is expected that people will increase consumption and reduce demand for savings account (English, Citation1999; Hussan & Masih, Citation2014; Klapper et al., Citation2015). Therefore, inflation will have an inverse relationship with deposits account.

FD refers to financial development. In the case of the present study, it was measured by broad money. The Theory of Active Financial Development or Supply Leading Financial Development articulates that well-functioning financial intermediaries plays a key role in eliminating financial exclusion and encourages engaging in financial dealings among vulnerable segment of population by creating adequate financial products to respond to the financial needs of people which legitimately met by the financial system, then people will start to interact and open bank accounts (Kumar, Citation2011; Rasheed et al., Citation2016). FD is expected to have a positive effect on FI.

Estimation analysis was carried out with descriptive statistics (see ) for all series included in the sample. All the series displayed considerable variations for both across and within the sample countries. This justified the need to use a heterogeneous panel data estimation technique, which enables endogeneity issues. presents the Pearson correlation analysis of the series for the sample. Overall, the correlation exercise revealed that the correlation estimates were within a reasonable range (Kennedy, Citation1985). The highest correlation was found between bank account and ATM, while the lowest correlation was between bank account and CPI. Correlations among variables with the most interest were low and with reasonable direction, i.e., ranging from 0.187 to 0.623. The correlations between remittances and both proxies of FI (bank account and ATM), between INQ and FIs, as well as between remittances and INQ, were positive and seemed to be in accord with prior expectations.

Table 1. Summary of descriptive statistics.

Table 2. Correlation between series.

3.2. Empirical model specification

Since the panel data consisted of N > 25 countries and T < 25 time periods, the dynamic system GMM method was employed (Raj & Baltagi, Citation2012). Another reason for selecting this technique is due to its ability to control endogeneity issue and to remove country-specific effects from the regressions, which appear to be the main problems of other panel data techniques. The empirical model for the present study is specified below as suggested and modified from Demirgüç-Kunt et al. (Citation2011):

(1)

(1)

where β0i refers to a constant term, LnFIit−1 describes the lagged dependent variable of FI. In addition, the present study utilised two proxies, namely the number of bank account holders per 1000 adults as well as the number of ATMs per 100,000 adults in measuring FI. Meanwhile, MWR postulates the MWR measured as personal remittances received per capita (in USD currency), followed by INQ as the institutional quality. Next, Xit is described as the vector of other control variables which include HC proxied by the mean years of schooling, the inflation (CPI), and the INC proxied by GDP per capita, and FD measured by broad money. Other than that, ηt refers to the time-specific fixed effect, λi is the country-specific effect, and Eit is the unobservable error term.

Demetriades and Law (Citation2006), in their study, discovered that FD is more effective in middle-INC economies with abundant effects, especially with the presence of high INQ. Hence, in this view, it becomes pertinent to determine whether or not the degree of INQ in the remittances recipient countries has an influence on the usage of remittances, which may consequently develop their abilities to raise FI. Accordingly, this can be achieved by adding the orthogonalised interaction terms as well as the original terms in the FI equation as shown in EquationEquation (2). Hence, the present study investigated the interaction between these variables as well as the simultaneous effect among the variables. Regarding this matter, it is expected for the simultaneous impact of remittances and INQ on FI to be able to provide a policy direction in determining whether an increase in remittances with higher intuitional quality will lead to an increase in FI (Ruiz et al., Citation2009). Meanwhile, the positive coefficient on the orthogonalised interaction terms indicates that the long-run marginal impact of remittances on FI tends to be enhanced in recipient countries that possess a better quality of institutions. On the contrary, a negative coefficient on the orthogonalised interaction terms implies that the growth impact of remittances is stronger in recipient countries with weaker institutions. In other words, positive (negative) coefficients on the orthogonalised interaction terms suggest that these variables can be considered as complements (substitute) in shaping a long-run FI in remittance recipient developing countries that acted as the samples of the current research.

In addition, the present study adopted the technique of Brambor et al. (Citation2006) in calculating the marginal effects and standard errors for the interaction term. Accordingly, this allows the evaluation of how the marginal effect of remittances on FI changes with the degree of INQ in remittance recipient countries. As emphasised by Brambor et al. (Citation2006), the total effect of remittance at the margin can be evaluated by examining the partial derivatives of FD with respect to remittances at the given levels of INQ. The conditional marginal effects are described in EquationEquation (3)(3)

(3) below:

(3)

(3)

The presence of complementary tends to exist between remittance and INQ if all the derivatives are positive for the purpose of enhancing FI. Accordingly, an increase in remittance and INQ would lead to more FI which can be measured through the opening of a bank account. Nevertheless, this is only possible if the parameters β1 and β3 are all positive. On the contrary, evidence of substitutability between the interacted variables will exist if the coefficients β3 is negative. Therefore, the derivatives can be evaluated within the sample provided that the level of INQ is varied (Brambor et al., Citation2006).

The anticipated signs based on the literature of remittances, HC, INC, FD, INQ, and the interaction term of remittances with INQ are expected to be positive, whereas inflation is expected to be negative as indicated in . In the case of the present study, it was anticipated that an increase in remittances with higher INQ could increase FI (Ruiz et al., Citation2009); hence, interaction term shall carry a positive sign. Finally, the current research also conducted two diagnostics, namely AR(2) Test and Hansen Test for the purpose of checking the consistent and efficient estimation of the long-run parameters of interest. The results of GMM will be considered valid if these two tests are found to be insignificant.

Table 3. Expected signs of coefficients of variables.

4. Empirical results

reports the impact of remittances on FI obtained from the system GMM estimator. As mentioned earlier, the present study utilised two proxies for FI, namely the number of bank account holders per 1000 adults as well as ATMs per 100,000 adults. In correspond to that, Column 1 and 2 report the model that used bank account as the proxy for FI, while Column 3 and 4 report the model that adopted ATM as the proxy for FI. As can be observed, Column 1 and 3 present the estimation that was carried out by only including the dependent variable, FI, followed by the main independent variable, remittance (MWR) along with the control variables. On the other hand, Column 2 and 4 introduce an interaction term between remittances and INQ (MWR*INQ).

Table 4. Results of GMM estimations of the impact of remittances on financial inclusion.

The results showed that the lagged dependent variable is statistically significant in all six models, which clearly implies that the dynamic system GMM is an appropriate estimator. Meanwhile, it should be noted that the empirical results can be relied upon for statistical inference. The insignificance of (AR2) Test and Hansen test shows that all of the models are robust; however, the Hansen test did not reject the over-identification restriction at a 5% significance level. As expected, the null hypothesis of the second-order serial correlation (AR2) is not rejected. Generally, the estimated models in seem to be nearly well specified.

It can be observed from that remittances carry the expected positive sign and clearly shown to be statistically significant in all models. The evidence of the positive impact of remittances found in the present study is in line with the results of Mundaca (Citation2009), Ramirez (Citation2013), and Boffy-Ramirez (2017) who found the significant positive effect of remittances which reinforces the inclusive effect remittances in the recipient countries. Nevertheless, the results of the current research are not in agreement with the studies conducted by Ambrosius and Cuecuecha (Citation2013); Brown et al. (Citation2013); Calderón et al. (Citation2007); Chami et al. (Citation2012); and Giuliano and Ruiz-Arranz (Citation2009) which reported that the inflow of remittances might not be able to produce a more inclusive financial system.

In addition, it can be seen that the coefficients of INQ carry the positive expected sign in all models which are statistically significant. Hence, this suggests that the level of INQ in the migrant country of origin tends to have a positive effect on FI. Meanwhile, the work of Law and Azman-Saini (Citation2012) reported the increase of the role of INQ in promoting long-run FD along with the improvement of quality institutions in the sample countries. This finding is in accordance with the result reported by Ramirez (Citation2013), Ruiz et al. (Citation2009), and El Hamma (Citation2018) which states that the growth impact of remittances is higher in countries with INQ.

Moreover, the control-variables which specifically refer to HC, INC, and FD have managed to meet its expected positive signs and shown to be statistically significant in all models. The current research found the INC variable to have a positive long-run effect on FI, which eventually suggests that INC in these countries has experienced an enhanced FI. The positive INC can be explained based on the fact that INC increases high potential financial considering they might receive their wages through a bank account which is a safe place to keep their funds (Beck & De La Torre, Citation2006). The positive sign of HC is in accordance with the prior expectation of the present study which states that sound or better HC positively influences FI. The positive HC explained by educated individuals who are able to comprehend various financial products has encouraged their access to financial services. These results are also supported by prior studies (Cole et al., Citation2011; Ellis & Lemma, Citation2010; Kempson et al., Citation2013; Pena et al., Citation2014). In addition, it was discovered that FD has a positive effect on FI. In particular, FD in the form of broad money and spread of banks level of comfort are convenient to the public because it allows them to carry out banking pursuits. These results are in line with prior studies which state that the increase in the number of bank branches will increase efficiency among the banks as well as FI (Beck & De La Torre, Citation2006; Beck et al., Citation2009; Beck et al., Citation2007; Beck et al., Citation2010). Meanwhile, Nitin (Citation2013) also stated that an increase in banking networks has a positive impact on FI. Other than that, it can be observed that the coefficient of inflation is positive and significant for models that used bank account as the proxy for FI (Columns 1 and 2). Unfortunately, the positive sign of inflation contradicts the prior expectation of the present study. The contradicted result indicates that an increase in inflation may encourage the opening of bank accounts, which then improves FI in the remittances-receiving countries. Overall, it should be understood that inflation can be overcome if individuals deposit at a bank to gain interest or buy an asset or financial asset rather than holding their cash in hand. Therefore, it is believed that all of these will be able to improve FI.

As one may observe, Columns 2 and 4 introduce an interaction term between remittances and INQ (MWR*INQ). The results show that the positive coefficient managed to be obtained. The positive coefficient on the interaction terms indicates that the impact of remittances on FI can be enhanced in recipient countries with a better quality of institutions. In other words, INQ is an important factor that influences individuals’ decision in accessing financial services offered by financial institutions. If the public has trust in the financial institutions, it is believed that the recipients of remittances will keep their excess in financial institutions including using the financial products or services made available by those institutions.

Next, the partial derivative of FI with respect to remittances described in EquationEquation (3)(3)

(3) was considered for the purpose of conducting a further evaluation on how the marginal effect of remittances on FI changes with the degree of INQ in remittance recipient countries. The partial derivative of FI with respect to the remittance at the minimum, mean, and maximum level of institution quality is reported in Columns 2 and 4. As can be observed, the results indicated that all of the coefficients are statistically significant and carry a positive sign. The result is consistent with the finding that remittances tend to carry a positive sign in all models. Most importantly, it can also be observed that the positive effects seem to get larger as a result of the improved level of INQ. The proportion of these derivatives at different levels of INQ showed that marginal growth effect of remittances on FI rises due to the increase in the degree of INQ. In other words, countries with better institutions will gain the most benefits from the positive growth effect of remittances considering that individuals will have better financial stability due to the enhanced level of INQ.

5. Concluding remarks

In the present study, the long-run impact of remittances on FI was successfully examined by taking into account the role of improved INQ in remittances-receiving countries. Moreover, the current research managed to achieve the objective using a panel dataset for 70 developing countries over the period of 2011–2018 through the adoption of the GMM estimation technique.

The results obtained by the current research revealed that the long-run impact of remittances on FI is positive, while FI tends to increase with better INQ. These results seem to support the studies reported so far. The present study also found evidence that the effect of remittances on FI is conditional depending on individuals’ perception of institutions. This finding sheds new light that positive perception of the public towards financial institutions does matter. Put simply, trust of remittances recipients towards financial institutions can further enhance the impact of remittances on FI.

The plausible explanation might be that the volume of remittances enables the recipients to have excess cash, which translates into the demand for deposit accounts. Apart from that, this also paves a way for them to gain access to other potential products such as payment or even credit (Ambrosius & Cuecuecha, Citation2013). These demands, in turns, can be accommodated via an increase in the provision of financial services or the maintenance of people perception against financial institutions. Hence, this clearly indicates that remittances could enhance the accessibility to financial services among the recipients. Moreover, an increase in remittances encourages the usage of formal financial services with a positive perception of financial institutions. Therefore, it is deemed necessary to improve trust to financial institution and government in the remittance’s recipient countries by promoting the opening of a bank account at financial institutions. The findings are in line with Fromentin (Citation2017) who found strong evidence supporting the view that remittances promote FD in developing countries in the long term.

The policy implication of this finding is that the countries have to improve their governance as well as instill positive perception about financial institutions to enable those involved to enjoy the benefits of receiving remittances and growth of the financial sector. Enhancing the INQ of financial institutions, such as reducing bureaucratic processes, improving credit allocation, strengthening credit regulation, ensuring higher transparency, and reinforcing information disclosure in the financial sector, can instill positive perception amidst the public towards financial institutions. Trust on financial institutions encourages the public to open bank accounts, while sustaining the trust of clients during banking transactions is important for them to use other financial services provided by banks, thus promoting FI.

Finally, the comparison of linkages between remittances and FI in countries based on different characters such as INC level and the geographical situation is recommended for future research. On another note, it is suggested for future work to employ other control variables such as interest rate and urbanisation growth considering that it would lead to a more interesting result. Future researchers also may look into the nonlinear impact of remittances on FI.

Acknowledgements

We benefited from comments and suggestions from Aleksandar Stojkov, Leila Aghabarari, Joseph Pelzman, and two anonymous participants at ASSA/AEA 2020 Conference in San Diego, CA. The remaining errors are ours.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Adams-Kane, J., & Lim, J. J. (2014). Institutional quality mediates the effect of human capital on economic performance. The World Bank.

- Adams-Kane, J., & Lim, J. J. (2016). Institutional quality mediates the effect of human capital on economic performance. Review of Development Economics, 20, 426–442. https://doi.org/10.1111/rode.12236

- Adegbite, O. O., & Machethe, C. L. (2020). Bridging the financial inclusion gender gap in smallholder agriculture in Nigeria: An untapped potential for sustainable development. World Development, 127, 104755. https://doi.org/10.1016/j.worlddev.2019.104755

- Aggarwal, R., Demirguc-Kunt, A., Martinez Peria, M. S. (2006). Do workers’ remittances promote financial development? World Bank Policy research Working Paper 3957. The World Bank.

- Ambrosius, C., & Cuecuecha, A. (2013). Are remittances a substitute for credit? Carrying the financial burden of health shocks in national and transnational households. World Development, 46, 143–152. https://doi.org/10.1016/j.worlddev.2013.01.032

- Anarfo, E. B., Abor, J. Y., & Osei, K. A. (2020). Financial regulation and financial inclusion in Sub-Saharan Africa: Does financial stability play a moderating role? Research in International Business and Finance, 51, 101070. https://doi.org/10.1016/j.ribaf.2019.101070

- Anzoategui, D., Demirguc-Kunt, A., & Martinez Peria, M. (2014). Remittances and Financial Inclusion: Evidence from El Salvador. World Development, 54(C), 338–349. https://doi.org/10.1016/j.worlddev.2013.10.006

- Arora, R. U. (2012). Financial inclusion and human capital in developing Asia: The Australian connection. Third World Quarterly, 33(1), 177–197. https://doi.org/10.1080/01436597.2012.627256

- Barajas, A., Chami, R., Espinoza, R. A., Hesse, H. (2010). Recent credit stagnation in the MENA region: What to expect? What can be done? IMF Working Papers No. 10/219, 1–19. https://doi.org/10.5089/9781455208845.001

- Beck, T., De La Torre, A. (2006). The basic analytics of access to financial services. Policy Research working paper No. WPSS 4026. The World Bank.

- Beck, T., Demirguc-Kunt, A. (2009). Financial institutions and markets across countries and over time-data and analysis. Policy Research working paper; No WPS 4943. The World Bank.

- Beck, T., Demirgüç-Kunt, A., & Honohan, P. (2009). Access to financial services: Measurement, impact, and policies. The World Bank Research Observer, 24(1), 119–145. https://doi.org/10.1093/wbro/lkn008

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27–49. https://doi.org/10.1007/s10887-007-9010-6

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2010). Financial institutions and markets across countries and over time: The updated financial development and structure database. The World Bank Economic Review, 24(1), 77–92. https://doi.org/10.1093/wber/lhp016

- Boffy-Ramirez, E. (2017). The heterogeneous impacts of business cycles on educational attainment. Education Economics, 25(6), 554–561. https://doi.org/10.1080/09645292.2017.1336511

- Bollard, A., McKenzie, D., Morten, M., & Rapoport, H. (2011). Remittances and the brain drain revisited: The microdata show that more educated migrants remit more. The World Bank Economic Review, 25(1), 132–156. https://doi.org/10.1093/wber/lhr013

- Brambor, T., Clark, W. R., & Golder, M. (2006). Understanding interaction models: Improving empirical analyses. Political Analysis, 14(1), 63–82. https://doi.org/10.1093/pan/mpi014

- Brown, R. P., Carmignani, F., & Fayad, G. (2013). Migrants’ remittances and financial development: Macro‐and micro‐level evidence of a perverse relationship. The World Economy, 36(5), 636–660. https://doi.org/10.1111/twec.12016

- Brown, R. P., Connell, J., & Jimenez‐Soto, E. V. (2014). Migrants’ remittances, poverty and social protection in the South Pacific: Fiji and Tonga. Population, Space and Place, 20(5), 434–454. https://doi.org/10.1002/psp.1765

- Calderón, C., Fajnzylber, P., & López, J. H. (2007). Remittances and growth: the role of complementary policies. In Remittances and development: Lessons from Latin America (pp. 335–368). World Bank.

- Calderón, C., & Liu, L. (2003). The direction of causality between financial development and economic growth. Journal of Development Economics, 72(1), 321–334. https://doi.org/10.1016/S0304-3878(03)00079-8

- Calero, C., Bedi, A. S., & Sparrow, R. (2009). Remittances, liquidity constraints and human capital investments in Ecuador. World Development, 37(6), 1143–1154. https://doi.org/10.1016/j.worlddev.2008.10.006

- Chami, R., & Fullenkamp, C. (2013). Worker’s Remittances and Economic Development: Realities and Possibilities. In Maximising the development impact of remittances. (pp. 30–38). UNCTAD.

- Chami, R., Hakura, D. S., & Montiel, P. J. (2012). Do worker remittances reduce output volatility in developing countries? Journal of Globalization and Development, 3(1), 1948–1837. https://doi.org/10.1515/1948-1837.1151

- Cismaș, L. M., Curea-Pitorac, R. I., & Vădăsan, I. (2020). The impact of remittances on the receiving country: some evidence from Romania in European context. Economic research-Ekonomska Istraživanja, 33(1), 1073–1070. https://doi.org/10.1080/1331677X.2019.1629328

- Cole, S., Sampson, T., & Zia, B. (2011). Prices or knowledge? What drives demand for financial services in emerging markets? The Journal of Finance, 66(6), 1933–1967. https://doi.org/10.1111/j.1540-6261.2011.01696.x

- Cull, R., & Effron, L. (2008). World Bank lending and financial sector development. The World Bank Economic Review, 22(2), 315–343. https://doi.org/10.1093/wber/lhn004

- Dabla-Norris, E., Ji, Y., Townsend, R. M., & Unsal, D. F. (2020). Distinguishing constraints on financial inclusion and their impact on GDP, TFP, and the distribution of income. Journal of Monetary Economics. https://doi.org/10.1016/j.jmoneco.2020.01.003

- Demetriades, P. O., & Hussein, K. A. (1996). Does financial development cause economic growth? Time-series evidence from 16 countries. Journal of Development Economics, 51(2), 387–411. https://doi.org/10.1016/S0304-3878(96)00421-X

- Demetriades, P., & Law, S. H. (2006). Finance, institutions and economic development. International Journal of Finance and Economics, 11(3), 245–260. https://doi.org/10.1002/ijfe.296

- Demirgüç-Kunt, A., Córdova, E. L., Pería, M. S. M., & Woodruff, C. (2011). Remittances and banking sector breadth and depth: Evidence from Mexico. Journal of Development Economics, 95(2), 229–241. https://doi.org/10.1016/j.jdeveco.2010.04.002

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2020). The Global Findex Database 2017: Measuring financial inclusion and opportunities to expand access to and use of financial services. The World Bank Economic Review, 34(Supplement_1), S2–S8. https://doi.org/10.1093/wber/lhz013

- Dwyfor Evans, A., Green, C. J., & Murinde, V. (2002). Human capital and financial development in economic growth: new evidence using the translog production function. International Journal of Finance and Economics, 7(2), 123–140. https://doi.org/10.1002/ijfe.182

- El Hamma, I. (2018). Migrant remittances and economic growth: The role of financial development and institutional quality. Economie et Statistique/Economics and Statistics, 503–504, 123–142. https://doi.org/10.24187/ecostat.2018.503d.1961

- Ellis, K., & Lemma, A. (2010). Investigating the impact of access to financial services on household investment. Research reports and studies. Overseas Development Institute.

- English, W. B. (1999). Inflation and financial sector size. Journal of Monetary Economics, 44(3), 379–400. https://doi.org/10.1016/S0304-3932(99)00033-1

- Fromentin, V. (2017). The long-run and short-run impacts of remittances on financial development in developing countries. The Quarterly Review of Economics and Finance, 66, 192–201. https://doi.org/10.1016/j.qref.2017.02.006

- Gibson, J., Boe-Gibson, G., Rohorua, H. T. A. S., & McKenzie, D. (2010). Efficient remittance services for development in the Pacific. Asia-Pacific Development Journal, 14(2), 55–74. https://doi.org/10.18356/245c03fa-en

- Giuliano, P., & Ruiz-Arranz, M. (2009). Remittances, financial development, and growth. Journal of Development Economics, 90(1), 144–152. https://doi.org/10.1016/j.jdeveco.2008.10.005

- Guiso, L., Sapienza, P., & Zingales, L. (2008a). Social capital as good culture. Journal of the European Economic Association, 6(2-3), 295–320. https://doi.org/10.1162/JEEA.2008.6.2-3.295

- Guiso, L., Sapienza, P., & Zingales, L. (2008b). Trusting the stock market. The Journal of Finance, 63(6), 2557–2600. https://doi.org/10.1111/j.1540-6261.2008.01408.x

- Hussan, S., & Masih, M. (2014). Are the profit rates of the islamic investment deposit accounts truly performance based? a case study of Malaysia. MPRA Paper 57689, University Library of Munich, Germany. https://mpra.ub.uni-muenchen.de/57689/1/MPRA_paper_57689.pdf (accessed June 2020).

- Kaufmann, D., Kraay, A., Mastruzzi, M. (2008). Governance matters VII: aggregate and individual governance indicators 1996–2007. Policy Research working paper no WPS 4654. The World Bank.

- Kempson, E., Perotti, V., & Scott, K. (2013). Measuring financial capability: a new instrument and results from low-and middle-income countries. Main report (English). Financial Literacy and Education Russia Trust Fund. World Bank.

- Kennedy, P. (1985). A guide to Econometrics (2nd ed.). The MIT Press.

- Klapper, L., Lusardi, A., & Van Oudheusden, P. (2015). Financial literacy around the world. World Bank.

- Koomson, I., Villano, R. A., & Hadley, D. (2020). Intensifying financial inclusion through the provision of financial literacy training: a gendered perspective. Applied Economics, 52(4), 375–387. https://doi.org/10.1080/00036846.2019.1645943

- Kumar, P. (2011). Financial exclusion: A theoretical approach. Government Arts and Science College Paper No. 89864. India, Ambalapuzha.

- Law, S. H., & Azman-Saini, W. (2012). Institutional quality, governance, and financial development. Economics of Governance, 13(3), 217–236. https://doi.org/10.1007/s10101-012-0112-z

- Law, S.-H., & Ibrahim, M. (2013). Social capital and financial market development. In C. W. Hooy, R. Ali, & S. G. Rhee (Eds.), Emerging markets and financial resilience (pp. 11–37). Palgrave Macmillan.

- Meyer, D., & Shera, A. (2017). The impact of remittances on economic growth: An econometric model. EconomiA, 18(2), 147–155. https://doi.org/10.1016/j.econ.2016.06.001

- Misati, R. N., Kamau, A., & Nassir, H. (2019). Do migrant remittances matter for financial development in Kenya? Financial Innovation, 5(1), 31. https://doi.org/10.1186/s40854-019-0142-4

- Muktadir-Al-Mukit, D., & Islam, N. (2016). Relationship between remittances and credit disbursement: a study from Bangladesh. Journal of Business and Management Research, 1(1), 39–52. https://doi.org/10.3126/jbmr.v1i1.14550

- Mundaca, B. G. (2009). Remittances, Financial Market Development, and Economic Growth: The Case of Latin America and the Caribbean. Review of Development Economics, 13(2), 288–303. https://doi.org/10.1111/j.1467-9361.2008.00487.x

- Naz, M., Iftikhar, S. F., & Fatima, A. (2020). Does financial inclusiveness matter for the formal financial inflows? Evidence from Pakistan. Quantitative Finance and Economics, 4(1), 19–35. https://doi.org/10.3934/QFE.2020002

- Nitin, K. (2013). Financial inclusion and its determinants: evidence from India. Journal of Financial Economic Policy, 5(1), 4–19.

- Orozco, M., & Fedewa, R. (2005). Regional integration. Trends and patterns of remittance flows within South East Asia. Inter-American Dialogue. World Bank.

- Orozco, M., Lowell, B. L., & Schneider, J. (2006). Gender-specific determinants of remittances: Differences in structure and motivation. Report to the World Bank Group.

- Ozili, P. K. (2020). Financial inclusion research around the world: A review. Paper presented at the Forum for Social Economics.

- Pena, X., Hoyo, C., & Tuesta, D. (2014). Determinants of financial inclusion in Mexico based on the 2012 National Financial Inclusion Survey (ENIF). BBVA Bank Working Paper No. 1415, Economic Research Department. https://www.bbvaresearch.com/wp-content/uploads/2014/06/WP_1415.pdf (accessed June 2020).

- Raj, B., & Baltagi, B. H. (2012). Panel data analysis. Springer Science & Business Media.

- Ramirez, M. D. (2013). Do financial and institutional variables enhance the impact of remittances on economic growth in Latin America and the Caribbean? A panel cointegration analysis. International Advances in Economic Research, 19(3), 273–288. https://doi.org/10.1007/s11294-013-9407-2

- Rasheed, B., Law, S.-H., Chin, L., & Habibullah, M. S. (2016). The role of financial inclusion in financial development: International evidence. Abasyn University Journal of Social Sciences, 9(2), 330–348.

- Rojas-Suarez, L., Amado, M. (2014). Understanding Latin America’s Financial Inclusion Gap. Center for Global Development Working Paper.

- Ruiz, I., Shukralla, E., & Vargas-Silva, C. (2009). Remittances, institutions and growth: a semiparametric study. International Economic Journal, 23(1), 111–119. https://doi.org/10.1080/10168730802696715

- Sarma, M., & Pais, J. (2008). Financial inclusion and development: A cross country analysis. Research Paper. Madras Schools of Economics.

- Sarma, M., & Pais, J. (2011). Financial inclusion and development. Journal of International Development, 23(5), 613–628. https://doi.org/10.1002/jid.1698

- Shad, M., Ibrahim, S., Azman-Saini, W., Baharumshah, A. Z., & Burhan, N. A. S. (2018). The Impact of social capital on international financial integration. International Journal of Economics and Management, 12(S2), 583–597.

- Taylor, J. E., & Wyatt, T. J. (1996). The shadow value of migrant remittances, income and inequality in a household‐farm economy. Journal of Development Studies, 32(6), 899–912. https://doi.org/10.1080/00220389608422445

- Toxopeus, H., Lensink, R. ( (2007). ). Remittances and financial inclusion in development (No. 2007/49). Research Paper. UNU-WIDER, United Nations University (UNU).

- Wellalage, N. H., & Locke, S. (2020). Remittance and financial inclusion in refugee migrants: inverse probability of treatment weighting using the propensity score. Applied Economics, 52(9), 929–950. https://doi.org/10.1080/00036846.2019.1646876

- World Bank. (2016). Migration and Remittances F 2016. World Bank Group. https://hdl.handle.net/10986/23743.

- World Bank (2018). The World Bank Annual Report 2018. World Bank Group. https://documents.worldbank.org/curated/en/805161524552566695/pdf/125632-WP-PUBLIC-MigrationandDevelopmentBrief.pdf.

- Yang, Y. Y., & Yi, M. H. (2008). Does financial development cause economic growth? Implication for policy in Korea. Journal of Policy Modeling, 30(5), 827–840. https://doi.org/10.1016/j.jpolmod.2007.09.006

Appendix