?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article proposes a new data envelopment analysis (DEA)-based approach to deal with mergers and acquisitions (M&As) matching. To derive reliable matching degrees between bidder and target firms, we consider both technical efficiency and scale efficiency. Specifically, an inverse DEA model is developed for measuring the technical efficiency, while a conventional DEA model is employed to identify the return of scale of the merged decision-making units (DMUs). Then, an optimization model is formulated to generate matching results to improve DMUs’ performance. An empirical study of M&As matching Turkish energy firms is examined to illustrate the proposed approach. This study shows that both technical efficiency and scale efficiency have impacts on M&As matching practices.

1. Introduction

Mergers and acquisitions (M&As) refer to amalgamation or consolidation of firms through various types of business and financial transactions (Braguinsky et al., Citation2015; Vizcaíno-González & Navío-Marco, Citation2018). Often such consolidation is represented as a bidder (acquirer) firm takes over another target firm, and establishes itself as a new entity. As one of the most ordinary affairs in the corporate world, M&As are recognized as one of the most essential ways of entering a new market, accelerating globalization, reducing business risk and improving competitive edge (Steigenberger, Citation2017).

Typically M&As are associated with the characteristic of two-sided matching (TSM) (Gale & Shapley, Citation1962; Roth, Citation1982), where each participant aims to form a profitable coalition with a partner under acceptable matching criteria. In the framework of TSM, the matching degrees among the candidates (acquirer or target) on two sides need to be derived before applying a specific strategy. For achieving this a variety of evaluating methods have been utilized. Data envelopment analysis, which based on linear programming, is one of the most important techniques among them and has been proved an effective way for performance assessment (Charnes et al., Citation1978, Liang et al. Citation2008, Cook & Seiford, Citation2009, Zheng et al., Citation2018).

Participants during an M&A naturally care about if the merged firm can operate in a global efficient way. The implication of the global efficiency is twofold within the framework of DEA. On one hand, can it produce the maximum outputs by consuming the minimum required resources, which refers to the problem of technical efficiency in economic field (Farrell, Citation1957; Yannick et al., Citation2016). On the other hand, does the combined size of the new firm is too large to manufacture agilely, which refers to the problem of scale efficiency (Banker & Thrall, Citation1992). Usually, a bidder is reluctant to accept a merger without an improvement in scale efficiency. Sometimes, participants are expected to learn the maximum possible profit after an M&A. In other words, they may probably be more interested in how much they can earn in the future instead of the immediate profit of the present moment. So a challenge is how to calculate the maximum outputs as well as technical efficiency of a merged DMU under the given inputs. However, as an ex-post planning tool, DEA is typically used for efficiency evaluation under the existing information and cannot provide mechanisms for ex-ante prediction (Amin & Oukil, Citation2019). An alternative approach for dealing with this problem is the inverse DEA (InvDEA), which developed by Wei et al. (Citation2000) based on the theory of inverse linear programming. In contrast to conventional DEA models, the InvDEA assumes the relative efficiency as a parameter and determines the best possible outputs (or inputs) that are required to achieve the efficiency goal.

This study aims to address the strategic matching in M&A considering both technical efficiency and scale efficiency, where the technical efficiency is measured using an optimal efficiency of each DMU and scale efficiency captures the impact of scale size on productivity (Banker et al. 1984). The main contribution and novelty lies in that we develop a new approach by integrating the InvDEA with return to scale (RTS) measurement to obtain the matching degree, and present a streamlined approach for M&A decision. Specifically, an InvDEA model is formulated to estimate the technical efficiency of the merged DMUs, and a traditional DEA model is employed to identify their scale efficiency. Furthermore, both the two efficiencies are aggregated to generate the matching degrees. As can be seen later, the proposed approach can deal with M&A matching without explicit preference provided by the two-sided participants.

The remainder of this article is organized as follows: Section 2 reviews related theories. Section 3 briefly introduces the CCR and basic InvDEA model; In Section 4, the proposed approach for M&A matching is developed; Section 5 gives an empirical study of M&A matching about Turkish energy-related firms; finally, conclusions are drawn in Section 6.

2. Literature review

Mergers and acquisitions (M&As) have been an important way for modern firms to reposition organizations in a constantly changing market. A successful M&A could result in technological advances and value creation (Chanmugam et al., Citation2005; Halkos & Tzeremes, Citation2013), yet huge losses such that costs rising, profits declining, or resources waste would occur due to an unfit M&A (Qian et al., 2017). By scanning the literature, there have been plenty of studies about the various process in M&A over the past few decades, such as acquisition planning, potential target searching, purchase contract, or financing negotiations, etc. (DeYoung et al., Citation2009). This article focuses on one critical step in M&A, the M&A matching (or fit), which refers to the procedure of mutual election between bidders and targets.

One important theoretical foundation of M&A matching is the methodology of two-sided matching (TSM). TSM initially originated from the problem of marriage and college admission (Gale & Shapley, Citation1962). Many economic systems can be modeled as TSM markets, with a sort of preference for each candidate on one side over the potential partners on another side. TSM now has been broadly applied across a wide spectrum of socio-economic activities, such as electronic brokering (Jiang et al., Citation2011; Le et al., Citation2018), person-job fit (Azevedo, Citation2014; Lin et al., Citation2019a), venture capital matching (Sørensen, Citation2007), mergers and acquisitions (Akkus et al., Citation2016; Park, Citation2013; Shi et al., Citation2017; Wanke et al., Citation2019), etc. An introductory survey of TSM has been carried out by Roth and Sotomayor (Citation1992); Bando et al. (Citation2016) also summarized some existing matching models with externalities.

As to the issue of M&A matching, primary research streams can be categorized into three domains: strategic matching, organizational matching and resource-based matching (Tsai, Citation2000). The first one focuses on strategic relevance of bidders and targets, and the integration of information and resources driven by profit sharing and mutual incentive. Salter and Weinhold (Citation1979) firstly introduced the notion of strategic matching into M&A, and distinguished them as the relevant and irrelevant acquisition; Chen et al. (Citation2018) focused on the strategic matching of M&As in Chinese banking industry by employing a new stochastic frontier method. Cartwright and Schoenberg (Citation2006) discussed some possible reasons causing failure of acquisitions, especially when a target firm has close commercial links with the acquirer. The second organizational matching is paid attention to matching effect on soft power such that cultural and institutional incentives of a merged company; Cartwright and Cooper (Citation1993) argued that a successful organizational matching would benefit the partnership from a positive synergy effect on organizational culture and personnel exchange. The third strand of research examines the overall coordination of both sides from the angle of each own resource and the transferability of resource caused by the potential synergy effects. Wernerfelt (Citation1995) introduced the concept of resource position barrier and suggested that analyzing the acquisition behavior of firms from the resource perspective; based on the viewpoint of resource sharing, Capron and Pistre (Citation2002) addressed the mechanisms of value creation and transfer within M&A.

Prior to an M&A transaction, how to measure the matching degree of a bidder and a target from either side should be addressed. It is relatively simple if the candidates have preferences over the partners, and the goal is to pair them to achieve a maximum matching degree under the given criteria. Nevertheless, it is not easy for participants to consider all aspects in detail and give preference over the candidates directly due to the complexity of M&A practices. As a non-parametric mathematical tool for assessing the relative efficiency of a set of DMUs, DEA is powerful in handling such evaluation problems (Wang & Chin, Citation2010). Following the original CCR model (Charnes et al. Citation1978), many classical models have been proposed in DEA literature, such as the BCC model, the slacks-based measure, and the cross-efficiency evaluation. Under the context of M&A, one line of study aims at investigating the efficiency of the gains after an M&A. Bogetoft and Wang (Citation2005) established an economic production model to calculate the potential gains from mergers by the CCR model; Kristensen et al. (Citation2010) followed Bogetoft and Wang’s work and advised a DEA-based model to examine the hospital mergers in Denmark. Taking Singapore banks as the background, Sufian and Majid (Citation2007) applied DEA to examine the efficiency gains (or loss) resulting in a merger. Rahman et al. (Citation2016) conducted an empirical study about the banking company mergers in US through the method of DEA window analysis. Shi et al. (Citation2017) employed the cross-efficiency DEA to derive a matching degree in M&A with participants’ contrasting attitudes. By assuming a DMU is composed of two or more candidates, Shi et al. (2018) developed a novel two-stage DEA model to decompose and calculate the potential gains from an M&A.

DEA is often applied as a post-merger analysis tool that focusing on the assessment of gain and loss under the observed information. On the contrary, some scholars attempted to use InvDEA instead of DEA to address pre-merger analysis. This reversed technique is a helpful managerial tool in dealing with problems such as resource allocation (Hadi-Vencheh et al., Citation2008), investment optimization (Chen et al., Citation2017), and production prediction (Lin et al., Citation2019b). Especially, the InvDEA facilitates pre-analysis as it deems the given efficiency as a parameter and optimizes the outputs (or inputs). By scanning the literature, there are merely a few studies on M&A using the InvDEA method. Gattoufi et al. (Citation2014) developed an InvDEA method for strategic merger decisions in the banking industry. Amin and Oukil (Citation2019) addressed a new InvDEA model with a flexible target setting, and applied this model in university merger practices. Amin et al. (Citation2019) also combined the goal programming method with InvDEA in target setting of an M&A in the banking industry. Based on the above literature review, the research of M&A practices based on InvDEA has attracted scholars’ attention gradually, but more efforts still need to be done.

3. Theoretical background

3.1. CCR model

Consider there exist n DMUs, each (j = 1, 2,…,n) has m inputs

(i = 1, 2,…,m) and s outputs

(r = 1,2,…,s). For the

under evaluation, its relative efficiency can be measured by the CCR model (Charnes et al., Citation1978):

(1)

(1)

where

is the weight of the ith input and

is the weight of the rth output.

The dual model of CCR model (1) is formulated as,

(2)

(2)

where

is a real variable of

and

(j = 1, 2,…,n) is an intensity vector.

is referred to as CCR-efficient if

Model (2) is estimated under a constant RTS assumption as the sum of

is unconstrained. The constraint

or

can be imposed on model (2), which implies a decreasing, increasing, or variable RTS, respectively (Banker & Thrall, Citation1992).

3.2. Basic InvDEA model

In the context of inverse DEA, as its name indicate, the situation is reversed where input or output levels are to be assessed with a given efficiency score (Ghiyasi, Citation2015; Jahanshahloo et al., Citation2015). If the outputs of are increased from

to

and the inputs are changed from

to

then the following model is constructed to estimate the minimum input increment

(Ghiyasi, Citation2015),

(3)

(3)

where

is a given relative efficiency of

Note that model (3) is based on the multi-objective linear programming, which solved by integrating the multiple objectives into a single one.

4. Methodological framework

Assume there are n firms in matching market and viewed as n DMUs ( j = 1, 2,…,n). During M&As matching, these firms will be classified into two subgroups, the bidder firms

and the target firms

(

). A bidder firm (DMU) is accompanied by a CCR-efficiency

otherwise, it belongs to the other side. We limit our study to one-to-one M&A matching and introduce some hypotheses below:

Hypothesis 1 Each bidder firm takes over at most one target firm, and vice versa.

Hypothesis 2(a) Firms involved in M&A are concerned about the potential benefit.

Hypothesis 2(b) Firms involved in M&A are concerned about the economies of scale.

4.1. Derivation of technical efficiency using InvDEA

To begin with, we take the and

for illustration. Suppose an M&A is achieved between them and denoted this newly merged DMU as

(

). Inspired by model (3), the following output-oriented InvDEA model is considered to estimate the maximum outputs of

(4)

(4)

In model (4), the vector is the maximum possible outputs of

and the

is a given efficiency score. Let us discuss some further explanations about this model: 1) the new

is usually expected to be efficient, and its efficiency score is presumed to be 1.0; 2) The input amount

of

is obtained by simple summation of them; 3) The

(r = 1, 2,…, s) is a given weighting parameter, and equal weights are assigned for them.

Theorem 1.

For each merged , it exists

Proof.

It is easy to verify when

(r = 1, 2,…,s), and the equation

is hold for any

So there is at least one feasible solution to model (4) for a given DMU. On the other hand, the maximum value of

is not less than any convex combination of

and

namely,

Theorem 1

indicates the combination of output amounts may be increased or unchanged after an M&A. However, a single output such that is allowed to be less than its parented output

(r = 1, 2,…, s). Clearly, a higher value of this function value signifies a better matching result. Following this idea, we derive the technical efficiency

of the

and express as below,

(5)

(5)

4.2. Measurement of RTS

Scale efficiency tells whether a firm operates at an optimal scale. There are three types of RTS: increasing, constant, and decreasing. We calculate the RTS of the merged to estimate its productivity in an M&A. Inspired by the dual model (2), the model for evaluating the scale efficiency of

is expressed as,

(6)

(6)

Model (6) may produce multiple optimal solutions, which would affect the feasibility of scale efficiency evaluation. To resolve this problem, a secondary goal method is employed to maximize the sum of the non-negative vector

(7)

(7)

where

and

are the optimal solutions solved by model (6).

Let if

then no further treatment is needed for the scale efficiency. The remaining case, i.e.,

is addressed by replacing the constraint

in this model. According to Banker and Thrall (Citation1992), the RTS situation of

can be identified as,

then the RTS of

Taking into account the above identification rule, we derive the following expression for calculating the scale efficiency,

(8)

(8)

It is worth pointing out that a decreasing RTS is assigned with a negative value and will be eliminated by our presented approach.

4.3. Two-sided M&A matching

After conducting the previous two stages, the technical efficiency and scale efficiency for a potential one-to-one match can be calculated. Both of them determine the final matching degree together.

Let and

be the matrices of technical efficiency and scale efficiency related to DMUs on either side. By introducing the 0–1 variables

(b = 1,2,…,g, t = 1,2,…,h), where

means

and

are merged and

otherwise. Thus, the following optimization model can be established:

(9)

(9)

where the

is the matching degree between the DMUs of

and

The mechanism of model (9) is to find out the maximum sum of matching degree among the DMUs on two sides. Note that any bidder (or target) would match no more than one target (or bidder) as the constraints imposed on the solution. Since model (9) is a linear program, it can be solved directly.

5. Case study

5.1. M&A in Turkish energy firms

Within the past decades, Turkey has witnessed great economic development and become one of the largest economies in the Middle East region. Nevertheless, rapid industrial growth was accompanied by overuse as well as misuse of energy resources. As a non-oil producing country, a practical resource regulation is vital for sustainable energy consumption in Turkey. On the other hand, one characteristic of Turkish energy firms is they generally are small or medium-sized institutions that have more difficulties in production due to the economic scale effects. Therefore, appropriate mergers and acquisitions are widespread in the Turkish energy industry.

Nowadays, a great number of small or medium businesses are located along Turkey’s Marmara Sea. As energy production involves a huge amount of resource consumption, the industrial energy uses are treated as the multiple inputs of a firm (DMU). In this study, we apply the developed method to the M&A matching decision for 20 energy-related firms that were selected from the Istanbul region. Each one of these firms (DMUs) has four inputs (i = 1, 2, 3, 4) and two outputs

(i = 1, 2). The detailed description of these factors is presented in . The original data of the 20 DMUs are derived from the published work (Önüt & Soner, Citation2007) and listed in , where the last column is the CCR-efficiency of each DMU.

Table 1. Variables of the DMUs.

Table 2. Original data and CCR-efficiencies of the 20 DMUs.

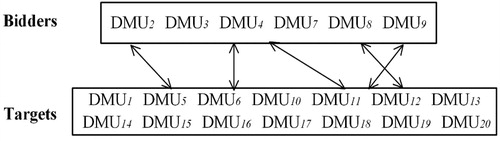

According to the obtained CCR-efficiencies, the 20 DMUs are divided into the bidder subgroup and the target subgroup on two sides, as illustrated in .

Figure 1. Description of the 20 DMUs on two sides. Source: The authors.

Based on model (4) the InvDEA model is iteratively constructed to estimate the maximum potential outputs between the one-to-one M&A matching pairs. Since there are 6 bidders and 14 target firms, the InvDEA model should be solved 614 times and each time for a different matching pair. After that, the technical efficiency

(

) can be obtained via EquationEq. (5)

(5)

(5) , which listed in .

Table. 3 Technical efficiencies of the merged DMUs.

Additionally, the scale efficiencies (

) can be yielded by using models (6) and (7). The normalized scale efficiencies

can be further generated with EquationEq. (8)

(8)

(8) . By multiplying the

with the

correspondingly, the matching degrees of all possible merged DMUs can be derived as (),

Table 4. Matching degrees of the merged DMUs.

So the matching programming is established by model (9) as,

Solving this model by Lingo 11.0, the optimal solution is respectively obtained as: So the matching results are:

5.2. Analysis and discussion

We firstly analyze the matching results only using the technical efficiencies of the DMUs. Substituting the data in into model (10), the matching results are obtained as below:

Obviously, there are some differences comparing with the previous results, where the bidder is now matched with the target

and the

is matched with the

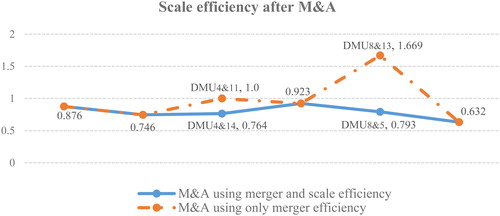

The varying scale efficiencies of the merged DMUs are summarized in . Compared with the previous results that all DMUs are identified as increasing RTS, we found this time the scale efficiencies of

and

are 1.669 and 1.0, which signifying decreasing RTS and constant RTS, respectively. That is because some pairs with higher scale efficiencies may have been matched up by model (9). Yet our method eliminates this possibility directly by imposing the constraint (8).

Figure 2. Comparison of the scale efficiencies. Source: The authors.

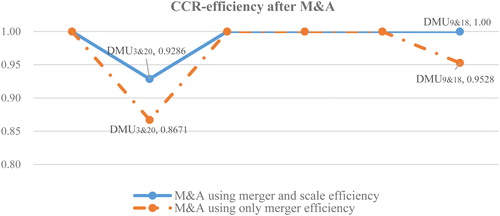

Now we compare the CCR-efficiencies of the obtained merged DMUs using the original input and output amounts. It is well known that CCR model can be used for evaluating the global efficiency (i.e., pure technical efficiency and scale efficiency) of a DMU. As shown in , there are some varieties of the two DMUs, namely, the and

where both of them have a lower efficiency if calculating only with the technical efficiency. This demonstrates they have not achieved optimal resource allocation especially when considering scale measurement. It is suggested to enhance the DMUs’ performance by taking both technical and scale efficiencies into account in an M&A matching practice. In our approach, the matching degree

in model (9) can be regarded as an integrative factor for the two efficiency measures, which remedy this deficiency to some extent. Besides, this result also supports the hypothesis 2 introduced in Section 4.

Figure 3. Calculating results of CCR-efficiency. Source: The authors.

As is seen from model (4), the determination of output weights (r = 1, 2) would have an effect on the objective function. Many weighting methods have been developed in the existing literature. Next we compare the weights of output variables with several popular methods, as shown in .

Table 5. Output weights derived by different methods.

From , the results have slight differences among these methods. However, the weight values of obtained are all larger than those of

The technical efficiency of each DMU can be calculated in a similar way. Except for the CCSD method, the other two methods achieve the same matching results as we do.

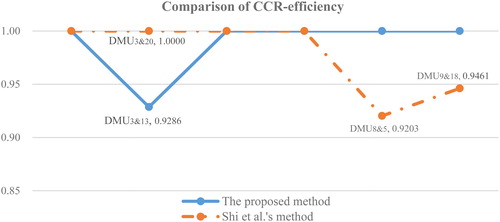

Finally, we conduct a comparison with the method in Shi et al. (Citation2017). They developed an approach for M&A matching using cross-efficiency model with contrasting attitudes. To facilitate the comparison, we only set the efficiency floor parameter in their model as Afterwards, the feasible matching matrix is calculated based on the matrices of technical efficiency and scale efficiency. Then the optimal results are generated as:

The above results are somewhat different from those obtained by our approach. The bidder is suggested to acquire the target

and the bidder

is recommend to acquire the target

by Shi et al. (Citation2017)’s method, which is different from the merged

and

obtained by our method. depicts the CCR-efficiencies derived by the two methods. There are two DMUs of

and

are evaluated as inefficient through Shi et al.’s approach. In contrast, the merged

generated by our approach has a lower efficiency score of 0.9286. The distinction lies in that different methods are applied in calculating the technical efficiency since both of them have considered the score efficiency. As a matter of fact, there are many existing DEA models can be used to determine the relative efficiencies. But in the present study, we are more interested in predicting the maximum potential production of a merged DMU rather than measuring the production at the current level of inputs.

Figure 4. CCR-efficiencies obtained by two different methods. Source: The authors.

5.3. Managerial implications

Based on the insights discussed before, we summarize the following implications for M&A matching:

Two-sided matching is a promising and attractive way for M&As when there are available candidates for bidders or targets on either side. Compared with the developed two-sided M&A matching in this article, there is another kind of one-sided matching in the existing works (Okumura, Citation2017). These models regard the bidder as the dominant part and mainly focuses on the bidder’s willingness (or preference), but neglect the target’s willingness to sell or cooperate. During a practical M&A, a bidder or a target has the option to match or reject according to his own interests. Therefore, a satisfied matching result is more likely to be achieved when considering both sides’ demand and requirement.

It is suggested to take both technical efficiency and scale efficiency into consideration during an M&A matching. Thanks to the resource dependence, high investment and high risk of energy-related firms, analysis of RTS of the merged firms is a critical step to ensure an acceptable result. When a merged DMU is evaluated only on the basis of the technical efficiency, as shown in , it may be not a practical solution with a decreasing RTS.

6. Concluding remarks

This article presents an M&A matching framework for the strategic decision based on DEA techniques. The idea of our approach is to combine technical efficiency and scale efficiency for calculating the matching degree between participants. Corresponding, an InvDEA and a conventional DEA models are constructed. An optimal matching formulation is then developed to derive the M&A solutions based on the obtained matching degrees. The proposed InvDEA model for assessing technical efficiency has the following merits: 1) it has a clear modeling mechanism that measures the maximum possible outputs by consuming the merged inputs; 2) the model can easily be extended under the different assumption of RTS; 3) the given relative efficiency can be reassigned according to a real situation. Also, the scale efficiency derived by the conventional DEA model not only can identify the type of RTS, but also can be well integrated with the technical efficiency. The developed approach was demonstrated with a practical example of 20 energy firms in Turkey. Comparative analysis revealed that using the above two kinds of efficiencies together can result in a feasible matching solution. The present study can not only shed light on the performance improvement in M&A matching decision but also extend the application scope of InvDEA approach. Nevertheless, there are some weak points in this research. Firstly, we simply suppose the given efficiency scores of each DMU are efficient in model (4), yet the scores may be adjusted according to a practical situation. Also, the case study is merely conducted under a small amount of data. For future studies, one worthwhile research direction is to investigate the DEA-based approach with undesirable outputs since environmental protection has been a broad industry consensus; another direction is to extend the M&A matching into many-to-one (or many-to-many) scenario.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Akkus, O., Cookson, J. A., & Hortacsu, A. (2016). The determinants of bank mergers: A revealed preference analysis. Management Science, 62(8), 2241–2258. https://doi.org/10.1287/mnsc.2015.2245

- Amin, G. R., & Oukil, A. (2019). Flexible target setting in mergers using inverse data envelopment analysis. International Journal of Operational Research, 35(3), 301–317. https://doi.org/10.1504/IJOR.2019.10022710

- Amin, G. R., Al-Muharrami, S., & Toloo, M. (2019). A combined goal programming and inverse DEA method for target setting in mergers. Expert Systems with Applications, 115, 412–417. https://doi.org/10.1016/j.eswa.2018.08.018

- Azevedo, E. M. (2014). Imperfect competition in two-sided matching markets. Games and Economic Behavior, 83, 207–223. https://doi.org/10.1016/j.geb.2013.11.009

- Banker, R. D. (1984). Estimating most productive scale size using data envelopment analysis. European Journal of Operational Research, 17(1), 35–44. https://doi.org/10.1016/0377-2217(84)90006-7

- Banker, R. D., & Thrall, R. M. (1992). Estimation of returns to scale using data envelopment analysis. European Journal of Operational Research, 62(1), 74–84. https://doi.org/10.1016/0377-2217(92)90178-C

- Bando, K., Kawasaki, R., & Muto, S. (2016). Two-sided matching with externalities: A survey. Journal of the Operations Research Society of Japan, 59(1), 35–71. https://doi.org/10.15807/jorsj.59.35

- Bogetoft, P., & Wang, D. (2005). Estimating the potential gains from mergers. Journal of Productivity Analysis, 23(2), 145–171. https://doi.org/10.1007/s11123-005-1326-7

- Braguinsky, S., Ohyama, A., Okazaki, T., & Syverson, C. (2015). Acquisitions, productivity, and profitability: Evidence from the Japanese cotton spinning industry. American Economic Review, 105(7), 2086–2119. https://doi.org/10.1257/aer.20140150

- Capron, L., & Pistre, N. (2002). When do acquirers earn abnormal returns. Strategic Management Journal, 23(9), 781–794. https://doi.org/10.1002/smj.262

- Cartwright, S. & Schoenberg, R. (2006). Thirty years of mergers and acquisitions research: Recent advances and future opportunities. British journal of management, 17(S1): 1–5. https://doi.org/10.1111/j.1467-8551.2006.00475.x

- Cartwright, S., & Cooper, C. L. (1993). The psychological impact of merger and acquisition on the individual: A study of building society managers. Human Relations, 46(3), 327–347. https://doi.org/10.1177/001872679304600302

- Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the efficiency of decision making units. European Journal of Operational Research, 2(6), 429–444. https://doi.org/10.1016/0377-2217(78)90138-8

- Chanmugam, R., Shill, W., Mann, D., Ficery, K., & Pursche, B. (2005). The intelligent clean room: Ensuring value capture in mergers and acquisitions. Journal of Business Strategy, 26(3), 43–49. https://doi.org/10.1108/02756660510597092

- Chen, Z., Wanke, P., & Tsionas, M. G. (2018). Assessing the strategic fit of potential M&As in Chinese banking: A novel Bayesian stochastic frontier approach. Economic Modelling, 73, 254–263.

- Chen, L., Wang, Y., Lai, F., & Feng, F. (2017). An investment analysis for China’s sustainable development based on inverse data envelopment analysis. Journal of Cleaner Production, 142, 1638–1649. https://doi.org/10.1016/j.jclepro.2016.11.129

- Cook, W. D., & Seiford, L. M. (2009). Data envelopment analysis (DEA)-thirty years on. European Journal of Operational Research, 192(1), 1–17. https://doi.org/10.1016/j.ejor.2008.01.032

- DeYoung, R., Evanoff, D. D., & Molyneux, P. (2009). Mergers and acquisitions of financial institutions: A review of the post-2000 literature. Journal of Financial Services Research, 36(2/3), 87–110. https://doi.org/10.1007/s10693-009-0066-7

- Farrell, M. J. (1957). The measurement of productive efficiency. Journal of the Royal Statistical Society: Series A (General), 120(3), 253–281. https://doi.org/10.2307/2343100

- Gale, D., & Shapley, L. S. (1962). College admissions and the stability of marriage. The American Mathematical Monthly, 69(1), 9–15. https://doi.org/10.2307/2312726

- Gattoufi, S., Amin, G. R., & Emrouznejad, A. (2014). A new inverse DEA method for merging banks. IMA Journal of Management Mathematics, 25(1), 73–87. https://doi.org/10.1093/imaman/dps027

- Ghiyasi, M. (2015). On inverse DEA model: The case of variable returns to scale. Computers & Industrial Engineering, 87, 407–409. https://doi.org/10.1016/j.cie.2015.05.018

- Halkos, G. E., & Tzeremes, N. G. (2013). Estimating the degree of operating efficiency gains from a potential bank merger and acquisition: A DEA bootstrapped approach. Journal of Banking & Finance, 37(5), 1658–1668. https://doi.org/10.1016/j.jbankfin.2012.12.009

- Hadi-Vencheh, A., Foroughi, A. A., & Soleimani-Damaneh, M. (2008). A DEA model for resource allocation. Economic Modelling, 25(5), 983–993. https://doi.org/10.1016/j.econmod.2008.01.003

- Kristensen, T., Bogetoft, P., & Pedersen, K. M. (2010). Potential gains from hospital mergers in Denmark. Health Care Management Science, 13(4), 334–345. https://doi.org/10.1007/s10729-010-9133-8

- Jahanshahloo, G. R., Soleimani-Damaneh, M., & Ghobadi, S. (2015). Inverse DEA under inter-temporal dependence using multiple-objective programming. European Journal of Operational Research, 240(2), 447–456. https://doi.org/10.1016/j.ejor.2014.07.002

- Jiang, Z. Z., Ip, W. H., Lau, H. C., & Fan, Z. P. (2011). Multi-objective optimization matching for one-shot multi-attribute exchanges with quantity discounts in E-brokerage. Expert Systems with Applications, 38(4), 4169–4180. https://doi.org/10.1016/j.eswa.2010.09.079

- Le, D. T., Zhang, M., & Ren, F. (2018). An economic model-based matching approach between buyers and sellers through a broker in an open e-marketplace. Journal of Systems Science and Systems Engineering, 27(2), 156–179. https://doi.org/10.1007/s11518-018-5362-z

- Liang, L., Wu, J., Cook, W. D., & Zhu, J. (2008). The DEA game cross-efficiency model and its Nash equilibrium. Operations Research, 56(5), 1278–1288. https://doi.org/10.1287/opre.1070.0487

- Lin, Y., Wang, Y. M., & Chin, K. S. (2019a). An enhanced approach for two-sided matching with 2-tuple linguistic multi-attribute preference. Soft Computing, 23(17), 7977–7990. https://doi.org/10.1007/s00500-018-3436-y

- Lin, Y., Yan, L., & Wang, Y. M. (2019b). Performance evaluation and investment analysis for container port sustainable development in china: An inverse DEA approach. Sustainability, 11(17), 4617. https://doi.org/10.3390/su11174617

- Okumura, Y. (2017). A one-sided many-to-many matching problem. Journal of Mathematical Economics, 72, 104–111. https://doi.org/10.1016/j.jmateco.2017.07.006

- Önüt, S., & Soner, S. (2007). Analysis of energy use and efficiency in Turkish manufacturing sector SMEs. Energy Conversion and Management, 48(2), 384–394. https://doi.org/10.1016/j.enconman.2006.07.009

- Park, M. (2013). Understanding merger incentives and outcomes in the US mutual fund industry. Journal of Banking & Finance, 37(11), 4368–4380.

- Qian, J. Q., & Zhu, J. L. (2018). Return to invested capital and the performance of mergers and acquisitions. Management Science, 64(10), 4818–4834. https://doi.org/10.1287/mnsc.2017.2766

- Rahman, M., Lambkin, M., & Hussain, D. (2016). Value creation and appropriation following M&A: A data envelopment analysis. Journal of Business Research, 69(12), 5628–5635. https://doi.org/10.1016/j.jbusres.2016.03.070

- Roth, A. E. (1982). The economics of matching: Stability and incentives. Mathematics of Operations Research, 7(4), 617–628. https://doi.org/10.1287/moor.7.4.617

- Roth, A. E., & Sotomayor, M. (1992). Two-sided matching. Handbook of Game Theory with Economic Applications, 1, 485–541.

- Salter, M. S., & Weinhold, W. A. (1979). Diversification through acquisition: Strategies for creating economic value. The Free Press.

- Shi, H. L., Wang, Y. M., Chen, S. Q., & Lan, Y. X. (2017). An approach to two-sided M&A fits based on a cross-efficiency evaluation with contrasting attitudes. Journal of the Operational Research Society, 68(1), 41–52.

- Shi, X., Li, Y., Emrouznejad, A., Xie, J., & Liang, L. (2017). Estimation of potential gains from bank mergers: A novel two-stage cost efficiency DEA model. Journal of the Operational Research Society, 68(9), 1045–1055. https://doi.org/10.1057/s41274-016-0106-2

- Sørensen, M. (2007). How smart is smart money? A two-sided matching model of venture capital. The Journal of Finance, 62(6), 2725–2762. https://doi.org/10.1111/j.1540-6261.2007.01291.x

- Steigenberger, N. (2017). The challenge of integration: A review of the M&A integration literature. International Journal of Management Reviews, 19(4), 408–431.

- SufianMajid, M. Z. A. (2007). Deregulation, consolidation and banks efficiency in Singapore: Evidence from event study window approach and Tobit analysis. International Review of Economics, 54(2), 261–283. https://doi.org/10.1007/s12232-007-0017-2

- Tsai, W. (2000). Social capital, strategic relatedness and the formation of intraorganizational linkages. Strategic Management Journal, 21(9), 925–939. https://doi.org/10.1002/1097-0266(200009)21:9<925::AID-SMJ129>3.0.CO;2-I

- Vizcaíno-González, M., & Navío-Marco, J. (2018). Influence of shareholders’ support over mergers and acquisitions in US banks. Economic Research-Ekonomska Istraživanja, 31(1), 228–239. https://doi.org/10.1080/1331677X.2018.1429296

- Wang, Y. M., Fan, Z. P., & Hua, Z. (2007). A chi-square method for obtaining a priority vector from multiplicative and fuzzy preference relations. European Journal of Operational Research, 182(1), 356–366. https://doi.org/10.1016/j.ejor.2006.07.020

- Wang, Y. M., & Chin, K. S. (2010). A neutral DEA model for cross-efficiency evaluation and its extension. Expert Systems with Applications, 37(5), 3666–3675. https://doi.org/10.1016/j.eswa.2009.10.024

- Wang, Y. M., & Luo, Y. (2010). Integration of correlations with standard deviations for determining attribute weights in multiple attribute decision making. Mathematical and Computer Modelling, 51(1–2), 1–12. https://doi.org/10.1016/j.mcm.2009.07.016

- Wanke, P., Azad, M. A. K., & Correa, H. (2019). Mergers and acquisitions strategic fit in Middle Eastern banking: An NDEA approach. International Journal of Services and Operations Management, 33(1), 1–25. https://doi.org/10.1504/IJSOM.2019.099652

- Wei, Q., Zhang, J., & Zhang, X. (2000). An inverse DEA model for inputs/outputs estimate. European Journal of Operational Research, 121(1), 151–163. https://doi.org/10.1016/S0377-2217(99)00007-7

- Wernerfelt, B. (1995). The resource-based view of the firm: Ten years after. Strategic Management Journal, 16(3), 171–174. https://doi.org/10.1002/smj.4250160303

- Xu, Y., Patnayakuni, R., & Wang, H. (2013). Logarithmic least squares method to priority for group decision making with incomplete fuzzy preference relations. Applied Mathematical Modelling, 37(4), 2139–2152. https://doi.org/10.1016/j.apm.2012.05.010

- Yang, G. L., Rousseau, R., Yang, L. Y., & Liu, W. B. (2014). A study on directional returns to scale. Journal of Informetrics, 8(3), 628–641. https://doi.org/10.1016/j.joi.2014.05.004

- Yannick, G. Z. S., Zhao, H., & Belinga, T. (2016). Technical efficiency assessment using data envelopment analysis: an application to the banking sector of Cote d’Ivoire. Procedia Social and Behavioral Sciences, 235(2016), 198–207. https://doi.org/10.1016/j.sbspro.2016.11.015

- Zheng, S., Lam, C. M., Hsu, S. C., & Ren, J. (2018). Evaluating efficiency of energy conservation measures in energy service companies in China. Energy Policy, 122, 580–591. https://doi.org/10.1016/j.enpol.2018.08.011