Abstract

This is the first study that presents a full picture of the field by using a combination of two methodologies, bibliometric and social network analysis (SNA). Thus, this work maps the knowledge of previous research and suggest new avenues for future research for the relationship between board characteristics and corporate social responsibility (CSR) and CSR disclosure (CSRD). We analysed 242 articles published on Web of Science database (WoS) journals for the period 1992–2019. The results show that board characteristics have a significant impact on CSR literature in terms of citations and high-quality journals. Moreover, the trend of the papers published in the field is increasing in the last five years. Our work clusters the literature according to keywords and draws the primary authors’ networks. This study also draws potential future avenues for research in the field in terms of research gaps (governance mechanisms, variables, countries, etc.). Furthermore, our results suggest some potential areas of interest for future political reforms of board of directors’ guidelines.

1. Introduction

Corporate social responsibility (CSR) has become a familiar debate among researchers, organisations, and standard setters. Even stakeholders are increasingly becoming more aware of its importance, particularly concerning its role in ensuring a proper balance in the long run between the commercial viability of a firm and its loyalty to society (Galant & Cadez, Citation2017; Harjoto & Jo, Citation2011; Skare & Golja, Citation2012; Zemigała, Citation2019). Moreover, CSR is a management concept connected to quality and environmental management (Zemigała, Citation2017). Specifically, one of the main areas that has attracted attention during recent years is CSR disclosure (CSRD) (Khan et al., Citation2013). Companies have several reasons behind their CSRD, such as enhancing their image and reputation (Siregar & Bachtiar, Citation2010), strengthening their relationship with clients, government and community (Williams & Pei, Citation1999), reducing the asymmetric of information between the companies’ managers and their stakeholders (Jizi et al., Citation2014) and to legitimise their activities (Deegan et al., Citation2002). All these reasons ensure economic viability in the long run.

Shareholders elect board of directors to control and manage companies’ matters (Monks & Minow, Citation1995). As a fundamental corporate governance feature, the board of directors has an essential role in aligning management concerns with those of stakeholders (Harjoto et al., Citation2015). However, the efficiency of the board supervising is measured among various board characteristics (Brick et al., Citation2006). Thus, board characteristics (such as independence, gender, size, CEO duality, and meetings) are expected to affect the level of CSR

The literature on the connection between CG and CSR has grown expeditiously in recent years. Besides, most of these efforts have been dedicated to examining the effect of board characteristics on CSR (i.e., Bear et al., Citation2010; Jizi et al., Citation2014; Jo & Harjoto, Citation2011; Khan et al., Citation2013; Zaid, Abuhijleh, et al., Citation2020; Zaid, Wang, et al., Citation2020). Board independence would enhance the controlling and monitoring of the management’s behaviour (Fama & Jensen, Citation1983), and is more capable of meeting stakeholders interests (Zahra & Stanton, Citation1988); thus, the existence of an independent board would lead to more information disclosure, fewer information asymmetries and better corporation image (Fama & Jensen, Citation1983). According to Barako and Brown (Citation2008), the participation of women on the board gives a broader experience and knowledge, which improves the decision-making process. Furthermore, females pay more attention to charitable and philanthropic activities (Angelidis & Ibrahim, Citation2011). Thus, the existence of women on the board would enhance the level of CSR Board size affects the role of controlling and monitoring (Liao et al., Citation2018). Adams et al. (Citation2005) argued that larger boards would have a variety of knowledge and experiences, which enhances the board’s ability to supervise and control the company’s disclosures. It is suggested that CEO duality leads to concentration of decision-making and control; this, in turn, would lead to compromising the governance performance function (Haniffa & Cooke, Citation2002); this consequently reduces the disclosure policy, including CSR (Li et al., Citation2010). Jizi et al. (Citation2014) point out that companies with active board would be more interested in providing information regarding CSR

Given the preceding discussion, this study makes significant contributions to the current literature by synthesising several new insights and offer deeply rooted discussions of avenues for further future research. More clearly, previous bibliometric studies have either introduced CSR (Carroll, Citation1999; Wood, Citation2010; Zemigała, Citation2015), sustainable development (Zemigała, Citation2019), or corporate governance (Terjesen et al., Citation2009). However, to the best of our knowledge, there is no bibliometric study that analyses the link between CG and CSR Therefore, it is worthwhile exploring what was ignored by ancestors and open the black box, which, in turn, helps in supporting and enriching the current literature. In this vein, this study contributes to the literature by offering a comprehensive scenery of the previous studies regarding the link between board and CSR More precisely, a bibliometric and social network analysis (SNA) techniques were applied in this study to produce a persuasive analytical view and build robust implications. Besides, depending on the Web of Science (WoS) database, a prolonged period was covered in this study (1992–2019).

Moreover, Zemigała (Citation2015) shows different countries perspective by performing a bibliometric study on the CSR articles published in Scopus database from 2000–2009. Feng et al. (Citation2017) studied a literature review and bibliometric analysis to evaluate the CSR for supply chain management. Moreover, Jaén et al. (Citation2018) conducted a bibliometric study on CSR in Latin America. More recently, Zemigała (Citation2019) analyse the tendencies of sustainable development studies in management sciences. He examines the articles published in WoS and Scopus form the period 1974–2016. On the other hand, there are also bibliometric studies of CG, such as Huang and Ho (Citation2011), they conducted a bibliometric analysis study for all CG articles published in WoS (SSCI) from 1992–2008.

Our study is different from it is former in different ways. First, as we mentioned earlier, as far as our knowledge goes, this is the first bibliometric study that examines the link between board and CSR. Second, to provide a more in-depth view and presents a full picture of previous research; our study uses a combination of bibliometric and SNA techniques. Third, this study covers a prolonged period (1992–2019), it is worth mentioning that almost 63% of our sample is from 2017–2019, and have not been covered by the previous literature review and bibliometric studies. Moreover, this study aims to cover studies related to board characteristics and different measures of CSR (i.e., CSR performance, CSRD quality, and quantity).

Additionally, our study is expected to be valuable and beneficial not only for academicians but also for policymakers and professionals. More pointedly, it provides new directions and insights for future research by summarising the empirical results of the impact of board characteristics on CSR and offering some favourable variables that could be reflected. Moreover, it provides the most influential articles, authors, institutions, journals, and countries in the field. Our results also suggested some critical attributes concerning the analysis and progress of the Board–CSR guidelines.

1.1. Study objectives

Given the previous discussion, the objectives of this study are to fill the literature gap by applying bibliometric and SNA techniques to a collection of scholarly articles in the field of board and CSR To achieve these objectives, we explore the published articles on Board–CSR from (1992–2019) and attempts to use cited references to analyse/identify:

The distribution patterns of papers.

Top players: authors, networks, institutions, and journals.

The core articles that influence international literature.

The relevant topics in the literature.

The main measures of dependant (CSR) and independent variables (board characteristic) used in the scientific literature (and its relations).

This article is structured as follows: First, an introduction and objective of the study are provided. Second, the methodology and data collections method of the study, while the third section analyses the result of bibliometric and SNA. Finally, the last section provides discussion, conclusions, limitations, and recommendations for future research.

2. Methodology

2.1. Bibliometric and social network analysis

Bibliometric analysis is a research technique that describes patterns in literature with a specific subject and time using quantitative data (Sarkar & Searcy, Citation2016). In general, there are two methodological approaches to quantify the flow of information. First, using a whole publication or using its features, such as citations, keywords, author’s name, etc. Second, by identifying the links among objects, their networks, and co-occurrences (Ding et al., Citation2001).

In general, scalar techniques are used in the first approach. In our research, such techniques are based on direct counts (occurrences) of particular bibliographic items, (Ding et al., Citation2001), provide the significant characteristics of various representatives (individual researchers, countries, fields, etc.) and research performance (Verbeek et al., Citation2002), as well as its evolution and trends over time. For scientific production, this approach is considered satisfying, but it can only be treated as a partial indicator of contributions to knowledge.

The SNA is the second approach used to recognise and classify related nodes of keywords, authors or research institutions to assess associations and collaborations (DeNooy et al., Citation2005). Thus, these procedures identify the relations (co-occurrences) of certain items, such as the number of times that keywords (co-word), citations (co-citation), and authors (co-authorship) are mentioned together in publications in a particular research field. This approach is mainly used to understand the underlying frame of the interrelationships between articles (Ding et al., Citation2001).

Citations show the relation between the investigation and the work of another author. Thus, citation analysis deals with the links among the citations (Sandison, Citation1989). On the other hand, Diodato (Citation1994) identifies co-citation when two or more works (also authors or journals) are cited by another document simultaneously. The co-citation strength depends on the number of times that two earlier documents are cited together by a new article.

Bibliographic coupling was introduced by Kessler (Citation1963), and it happens when two papers use a reference as a unity of coupling between those two papers. Its strength depends on the number of references the two papers have in common (Egghe & Rousseau, Citation1990).

To achieve a global view of the effect of the boards on CSR in the literature, we have used a combination of both techniques (scalar and analytical).

2.2. Data collection

In line with previous bibliometric and social networks analysis studies (Franceschini et al., Citation2016; Seguí-Mas et al., Citation2019; Zhu & Hua, Citation2017); we search the WoS database, it includes different citation indices in it is core collection and we used all indexes from 1992 to 2019 because the first articles in this search appear in 1992. We use WoS because is the world’s leading scientific citation search and analytical information platform, used in thousands of academic papers over the past decades (Li et al., Citation2018). In the last 50 years WoS has covered all the publications and corresponding citations from more than 34,000 professional journals, which constitute the core of the international scientific serial literature for many fields (Clarivate, Citation2020). Thus, the journals included in WoS database are recognised as ‘top journals’ (Merigó-Lindahl, Citation2012).

To cover all possible related articles on the field of board and CSR, we developed a combined keyword includes Board with CSR, Sustainab* and Philanthrop*. Sustainab* (to ensure that all the possible variations such as ‘Sustainable development,’ ‘Sustainability Reporting,’ and ‘Sustainability’ were included in our sample). Philanthropy was previously used to refer to CSR because, in the past, companies used to focus mainly on philanthropic activities such as charitable activities and donations (Wang & Coffey, Citation1992). Therefore, we have used ‘Philanthrop*’ to cover all possible variations such as ‘Philanthropy’ and ‘Philanthropic activities.’ The search criteria included the joint appearance of the words (‘board’ and ‘CSR’ OR ‘Sustainab*’ OR ‘Philanthrop*’) in one area or jointly of the title, abstract, and keywords. After eliminating all results other than articles and English language and choosing the fields that of our interests, which are: Business, Management, Business Finance, Economics, and Environmental Studies, the result of this search showed 580 articles. We then reviewed 580 articles for their abstract and title to exclude the irrelevant articles that were not tightly focused on the relationship between board and CSR Thus, the remaining sample included 242 articles. Afterword, we used Bibexcel software to make a bibliometric analysis and VOSviewer to analyse the social networks and the visualisation tool for our research.

3. Results

First, we develop a descriptive analysis to study the structure of the literature in the field by counting its years of publication and contributing authors, institutions, countries, and journals.

3.1. Study objective 1: Distribution pattern of the literature

We analysed the trend of publications in the periods from 1992 to 2019.

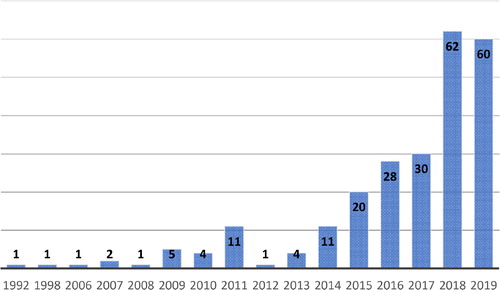

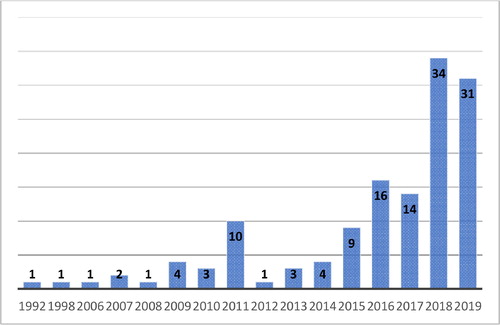

shows the publications trend from 1992 to 2019. Only almost 11% (26 of 242) articles published between 1992 and 2011; the leading research period can be considered after 2011. can be split into two periods: the initial period from 1992 to 2011, and the second is the growth period from 2012 to 2019. It shows that the interest from researchers on board of directors and CSR are increasing with a rising number of published researches.

Figure 1. Publications Trend. Source: Created by the authors based on WoS database.

Interestingly, there is a massive growth of published researches in the last six years, which accounts for almost 86% of the total publications in this field. This result is in line with Montiel and Delgado-Ceballos (Citation2014), they reported that after 2012, when the studies of CSR started to increase. Moreover, some journals such as JBE have even published special issues related to CSR in 2013 (Montiel & Delgado-Ceballos, Citation2014). The increase in the number of publications may be due to the 2008 financial crisis, and its effect on CSR and CG Velte (Citation2017) reported that the international and national stander sitters initiated various amendments to improve the quality of board characteristics and CSR disclosure after the 2008–2009 financial crisis. Besides, the strengthening of an institutional framework aimed to enhance the research activity and reflects the recognition of scholars to field importance. The trend also shows that publications will continue to grow.

3.2. Study objective 2: Top players: authors, networks, institutions, countries, and journals

3.2.1. Authors and Institutions

Five hundred and forty-two different authors from 323 different institutions participated in 242 articles. shows the top nine institutions with five publications or more. The most productive institutions were from four countries (Spain, the US, Australia, and Lebanon). The top three institutions were from Spain, which are: University of Salamanca, Jaume I University, and University of Granada with 19, 10, and eight, respectively. It is worth mentioning that the top two leading authors (see ) are Garcia-Sanchez with 16 publications from University of Salamanca and Pucheta-Martinez with eight publications from Jaume I University.

Table 1. Most productive country and institution.

Table 2. Top authors.

3.2.2. Authors networks

shows the authors co-occurrence with at least three frequencies. The leading author Garcia-Sanchez have 10 collaborations with Martinez-Ferrero, five collaborations with Cuadrado-Ballesteros and four with Rodríguez-Ariza. The research group of Cabeza-Garcia and Fernandez-Gago with has five collaborations in common, presents three collaboration with Nieto. It is worth mentioning that most collaborations between researchers were from the same institution, which is the University of Salamanca that was previously mentioned in , which is the most productive institution in this field. While other researchers with four collaborations, for example, Khan and Muttakin from Australia. shows the main links among the authors’ network.

Figure 2. Authors Co-occurrence. Source: Created by the authors based on WoS database using VOSviewer software.

Table 3. Authors co-occurrence.

3.2.3. Countries

Almost 67% of the publications in the field of the board of directors and CSR are conducted in developed countries. Most of the publications are from Spain, the US, China, Australia, and the UK (see ). A high number of developed countries are interestingly focusing on this topic, which reflects the importance and the impact of it. While research in developing countries is still relatively small, with a percentage of 33%. Furthermore, we noticed that Common Law countries (e.g., the US, the UK, Australia, and Canada) are the top countries producers in this filed. Zemigała (Citation2015) conclude that CSR research mainly concentrated on the Common Law countries. According to Chung et al. (Citation2012), Common Law countries pay more attention to corporate governance structure, and it focuses more on stakeholder protection than civil law countries.

Table 4. Most productive country.

3.2.4. Journals

shows the most productive journals, 242 articles published in 83 journals; this result reflects the high diversity of articles produced in this field. However, almost 56% (136 of 242) of the articles were concentrated in 10 journals. As shown from the table, the scope of the most productive journals is on CSR and corporate governance. The Journal of Business Ethics (JBE) is the most productive journal with 35 publications, while Corporate Social Responsibility and Environmental Management (CSREM) and Sustainability journals are the second and third most productive with 27 and 18 publications, respectively.

Table 5. Most productive journals.

On the other hand, we also developed a more evaluative assessment to study the use of the literature in the field by using citation analysis. Thus, it can be identified that the most cited papers are the most useful, and the most co-cited papers are the most related papers.

3.3. Study objective 3: Identify the core literature in the international literature

ranks the most cited articles. ‘The Impact of Board Diversity and Gender Composition on Corporate Social Responsibility and Firm Reputation’ by Bear et al. (Citation2010), which was published in the Journal of Business Ethics, was the most cited article (370 times) with an average of 37 citations per year. Almost 83% (201 of 242) articles were cited at least once, and nearly 42% (102 of 242) articles were cited more than 10 times. The most cited articles are from the Journal of Business Ethics (JBE), Corporate Governance – An International Review (CGIR), Corporate Social Responsibility and Environmental Management (CSREM), and Business and Society.

Table 6. Rank of the most cited articles.

3.3.1. Co-citation

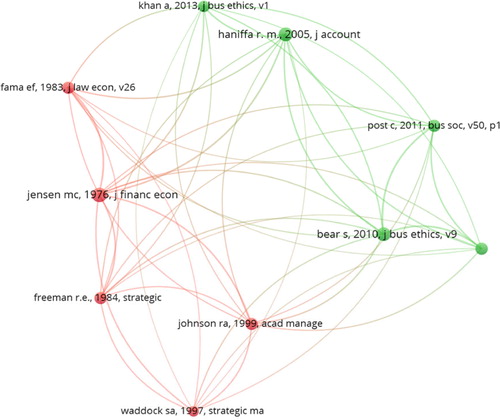

identifies two main groups of cited documents in the literature. The first cluster is focused on stakeholders and agency theory, and it is formed by five very relevant works cited frequently together in our sample (lead by Jensen, Fama, Freeman, Waddock, and Johnson). The green group is made up of four articles on corporate governance, usually cited jointly (Bear, Post, Haniffa, and Khan’s works).

Figure 3. Co-citation (Minimum of 50). Source: Created by the authors based on WoS database using VOSviewer software.

3.3.2. Bibliographic coupling

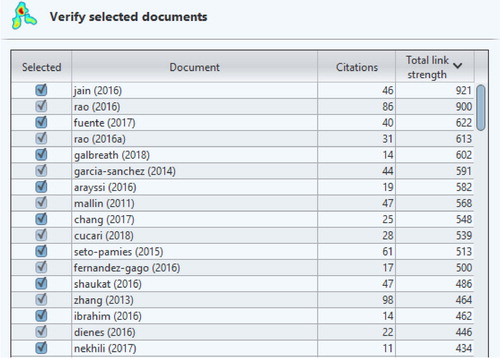

For a better understanding of the academic background of the 242 articles of the sample, we analysed the network of articles referenced, and it revealed that the largest set of connected papers contained 102 publications (i.e., 42.15% of the sample). presents the articles with the highest link strength of bibliographic coupling.

Figure 4. Bibliographic Coupling (Minimum of 10). Source: Created by the authors based on WoS database using VOSviewer software.

shows that the three studies with the highest indices of bibliographic coupling are:

• Jain, T., & Jamali, D. (2016). Looking inside the black box: The effect of corporate governance on corporate social responsibility. Corporate Governance: An International Review, 24(3), 253–273.

• Rao, K., & Tilt, C. (2016). Board Composition and Corporate Social Responsibility: The Role of Diversity, Gender, Strategy, and Decision Making. Journal of Business Ethics, 138(2), 327–347.

• Fuente, J. A., García-Sánchez, I.M., & Lozano, M.B. (2017). The role of the board of directors in the adoption of GRI guidelines for the disclosure of CSR information. Journal of Cleaner Production, 141, 737–750.

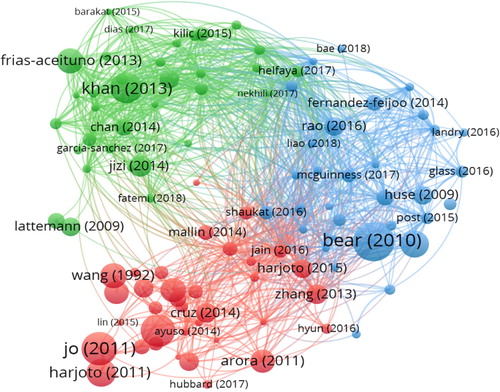

Trying to complete the Bibliographic coupling analysis of articles, presents a network visualisation. The figure reveals three main clusters of documents that are commonly cited together. Jain and Jamali, (Citation2016) has the biggest link strength and belongs to the red cluster with other articles, such as Mallin et al. (Citation2014), Zhang et al. (Citation2013), and Shaukat et al. (Citation2016). On the other hand, Rao and Tilt (Citation2016) is close to the leader in terms of bibliographic coupling and belongs to the blue cluster, like Nekhili et al. (Citation2017). Finally, Fuente et al. (Citation2017) leads the green cluster, where we can find documents with a relevant link strength such as Khan et al. (Citation2013).

Figure 5. Bibliographic Coupling (Minimum of 10). Source: Created by the authors based on WoS database using VOSviewer software.

Finally, after the evaluative assessment, this section will finish studying the variables used in the research in the field. Thus, it can be identified as the most used variables and the potential gaps in the field.

3.4. Study objective 4: Most relevant topics in the literature

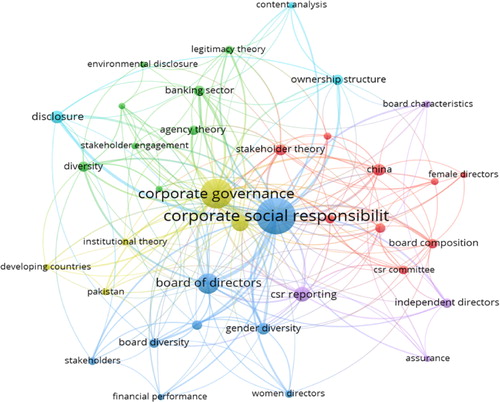

After a homogenisation process, shows the most frequent keywords with 10 times or more in the field of board and CSR CSR/Sustainability and Corporate Governance are the most keywords studied in the area with 151 and 93 times, respectively. Regarding CSR, we notice that researchs in this field were focused on both CSR disclosure and performance with keywords frequency 48 and 13, respectively. Consistent with our results, the keywords frequency table shows that most researchers examine board gender diversity and board independence with frequency of 25 and 20, respectively. This result is also reflected in keywords’ co-occurrence. Thus, indicates that most studies focus on the concept of diversity in general and specifically on gender diversity. Concerning the theoretical framework, the studies on this field mainly concentrate on stakeholder and agency theory to explain the associations between board and CSR with a frequency of 13 and 10, respectively. We can also notice that the keyword ‘China’ appears 14 times; this indicates that China is one of the most influential countries in this filed, and this is consistent with our result (see ). However, China appears neither in most productive authors nor in most productive institutions, which may reflect that there are no clear collaborations between Chinese authors and institutions.

Table 7. Keyword frequency.

Table 8. Keyword co-occurrence.

According to the keyword co-occurrence, presents keywords indicate a powerful co-occurrence, which meant that they were gist keywords in the board of directors and CSR literature

shows four main thematic clusters where each ball represents a keyword, and the size of each ball is proportional to the co-occurrence frequencies of keywords. The first cluster (the blue one) is devoted to the link between CSR, Board of Directors, diversity, and disclosure, and the red one deals with topics such as Board composition, CSR Committee, and the stakeholder theory. On the other hand, the green cluster is focused on the banking sector and environmental disclosure under the lens of agency and legitimacy theories. Finally, the yellow one analyses the state of the field in developing countries, using an institutional approach.

Figure 6. Keyword Co-occurrence. Source: Created by the authors based on WoS database using VOSviewer software.

3.4. Study objective 5: Main measures of dependent (CSR) and independent variables (board characteristics) used

3.4.1. Dependent variables

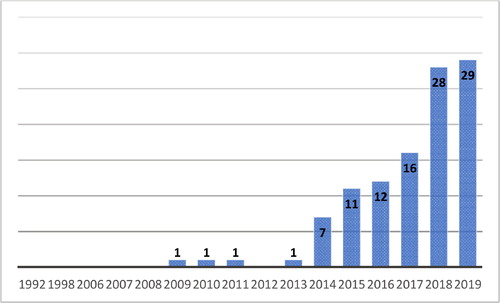

Most of the studies measure CSR in two ways: CSR Performance (CSRP) and CSR Disclosure/Reporting (CSRD). CSR Performance and CSRD are different, and we cannot deal with them synonymously, CSR disclosure is one factor affecting CSR performance, it is mainly measured by the voluntary social and environmental information disclosed by companies on its annual report or CSR separate report (Velte, Citation2017). Also, CSRD depends on standards such as Global Reporting Initiative (GRI) guidelines, which represents a set of standards that are used by corporates to report the impact of their operations on the society, environment, and economy (Global Reporting Initiative, 2016). On the other hand, CSR Performance measured using a different database such as KLD and EIRIS KLD is the database most used to measure CSR performance (Arora & Dharwadkar, Citation2011; Bear et al., Citation2010; Chen et al., Citation2019; Ghosh & Harjoto, Citation2011; Harjoto et al., Citation2015; Harjoto & Jo, Citation2011; Jo & Harjoto, Citation2011; Macaulay et al., Citation2018; Mallin & Michelon, Citation2011). Other studies used the EIRIS database (Cuadrado-Ballesteros et al., Citation2017). Moreover, some studies measure CSR performance as a dummy variable (Eberhardt-Toth, Citation2017; Godos-Diez et al., Citation2018). shows the trend of publications based on CSR performance as dependent variable. The period of the publications is relatively broad from (1992–2019), but it is noticeable that they have started to overgrow after 2012. On the other hand, shows that the interest in CSRD began in 2009 and have started to grow after 2012. It is worth mentioning that in the last three years (2017–2019), the researchers in this field become more interested in CSRD than CSR performance or practices.

Figure 7. CSR Performance Publications Trend. Source: Created by the authors based on WoS database.

Figure 8. CSRD Publications Trend. Source: Created by the authors based on WoS database.

According to Rao and Tilt (Citation2016), CSR disclosure will be included in companies’ annual reports or as individual CSR report. Fifty-one studies depend on companies’ financial statement to measure CSR disclosure and other financial variables by analysing the content of company’s annual report, website and CSR report by using a checklist, counting words and sentences (Appuhami & Tashakor, Citation2017; Barakat et al., Citation2015; Jizi et al., Citation2014; Khan et al., Citation2013; Kolsi & Attayah, Citation2018; Sharif & Rashid, Citation2014; Zaid et al., Citation2019). Other studies measure CSRD using ESG rating depending on Bloomberg database (Al-Dah et al., Citation2018; Cucari et al., Citation2018; Giannarakis et al., Citation2014), and by using KPMG international surveys of CSR reporting (Fernandez-Feijoo et al., Citation2014), using a dummy variable (Liao et al., Citation2018; Pucheta-Martinez & Chiva-Ortells, Citation2018), Dow Jones Sustainability Indices (Chang et al., Citation2017), and GRI database (Cabeza-Garcia et al., Citation2018; Fuente et al., Citation2017).

Almost 44% of the sampled articles used CSRD as a dependent variable (see ), while nearly 54% used CSR (performance, practices, actions, engagement, and strategies). For example, Macaulay et al. (Citation2018), Harjoto et al. (Citation2015) and Zhang et al. (Citation2013), used CSR performance rating as a measurement of CSR

Table 9. Dependent variable – country analysis.

shows the dependent variable (CSR/CSRD) across different countries. Forty-eight countries studied 242 articles, and almost 67% of the studies, as mentioned earlier conducted in developed countries. However, CSR disclosure studies are focused on developing countries; this result is consistent with Velte (Citation2017), while studies in developed countries mainly focused on CSR performance. The US is the second most producer country with 38 articles; 34 of them are focused on CSR performance and mainly depending on KLD database as the primary data source to measure CSR Future research in developed countries such as the US could pay more attention to studying CSRD Moreover, studies in developing countries in CSR (disclosure/performance) are relatively low; it could be more interesting for future research in these countries to consider this point.

3.4.2. CSR disclosure

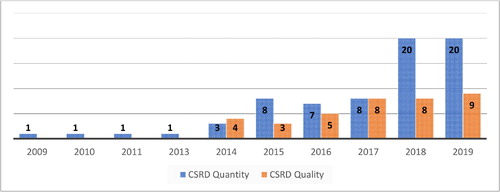

Almost 44% (107 of 242) of the sampled articles used CSRD as a dependent variable, nearly 65% (70 of 107) of these articles used CSRD quantity, while almost 35% (37 of 107) focus on CSRD quality. According to Velte (Citation2017), most of the studies in CSRD depend on CSRD quantity because it is simpler to measure, by using a checklist, counting words and sentences, and using unweighted code to limit subjectivity and bias problem. However, few researchers used both (see, for example, Alotaibi & Hussainey, Citation2016; Cuadrado-Ballesteros et al., Citation2015; Appuhami & Tashakor, Citation2017; Helfaya & Moussa, Citation2017). As shown in , the interest of CSRD quantity has started earlier than CSRD quality. Moreover, the trend was almost alike. However, the variation between the trend of publications have reached its peak in the last two years (2018–2019), and CSRD quantity research have gained much more interest from researchers. However, the quantity of disclosed CSR items is not always enough, and sometimes the quality of disclosed information could give a more accurate measurement. Future research may, therefore, give more interest to CSRD quality.

Figure 9. CSRD quantity and quality Publications Trend. Source: Created by the authors based on WoS database.

3.4.2. Most used independent variables

shows the top independent variables used with a frequency of more than 18. However, we avoid three variables from the table above (ownership concentrations, government ownership and institutional ownership with frequency of 13, 11 and nine respectively), because this study focuses on board characteristics, not other CG variables such as ownership structure. As shown in , board independence, gender diversity, and board size are the most used variables with frequency of 101, 95, and 71, respectively. On the other hand, few studies on the field of the board of directors and CSR have studied other board variables for example; audit committee characteristics (Dwekat et al., Citation2020), board age, board education and experience, board tenure, board interlocking, board compensations, CSR committee characteristics. Thus, it could be useful for future research to focus on these variables. shows the most used independent variables measurement.

Table 10. Top six independent variables used.

Table 11. Measurement of independent variables.

4. Conclusion

In general, the growing literature shows how the interest of the relationship between board and CSR are increasing, especially since 2014. Besides, most of the most productive journals in the field are of high-quality with a high scientific impact, which emphasise the increasing awareness of the importance of the research on the topic. Our results also indicate the significant impact of the literature since almost 83% of articles are cited at least once, and nearly 42% are cited more than 10 times. Bear et al. (Citation2010), Jo and Harjoto (Citation2011) and Jamali et al. (Citation2008) have the most important value on the literature, since they are the most cited articles in the field (with more than 250 citations).

Although the research on this field is distributed worldwide, almost 67% of the academic articles are in developed countries and concentrated mainly in Spain, the US, China, Australia, and the UK Thus, the most productive institutions and authors are primarily located in the same countries. While, on the other hand, research in the field is still relatively low in developing countries. Therefore, future research may consider focusing on these countries.

Regarding topics of interest in the literature, the most used keywords were ‘CSR’ (or Sustainability), ‘Corporate Governance’, ‘CSR Disclosure’ (or Reporting) and ‘Board of directors’. Besides, the keywords co-occurrence identifies ‘Corporate governance and corporate social responsibility’, ‘Board of directors and corporate social responsibility’ and ‘Corporate social responsibility and Disclosure’ are the most used keywords.

SNA results also show that two or more than authors study almost 93% of sampled articles; this means that researchers in this field tend to work cooperatively. Garcia-Sanchez and Martinez-Ferrero have the highest Authors co-occurrence with ten articles, noting that they both are from University of Salamanca. On the other hand, the collaborations in other countries such as Khan and Muttakin in Australia and Harjoto and Jo in the US are relatively low with four and two collaborations, respectively. Thus, the literature structure does not identify a robust network of collaborations between authors. The study identifies only one significant network of authors, all of whom are Spanish.

The co-citation analysis indicates two main groups of cited documents in the literature. The first cluster is focused on theory (stakeholders and agency theory), and the second group is made up by four articles on the impact of corporate governance on CSR, usually cited jointly (Bear, Post, Haniffa, and Khan’s works). The results of the keywords and co-citation analysis show that agency theory and stakeholder are the most popular theories used by researchers to explain the relationship between board and CSR According to Clarkson (Citation1995), the best way to understand CSR is to analyse how companies manage their relationship with stakeholders. Moreover, stakeholder theory has been used in most areas of CSR and has given rise to a large body of literature. Agency theory suggested that the primary function of the corporate board is to supervise the management to protect shareholders’ interests, therefore, reducing conflict of interests (Jensen & Meckling, Citation1976).

One critical contribution of this investigation has been to identify the key variables to explain the relationship between board and CSR In this sense, literature measures CSR in two ways: CSR Performance and CSRD CSRD depends on standards such as GRI guidelines, and CSR Performance is measured using a database such as KLD and Asset4(Eikon). They both have started to overgrow after 2012, but the researchers become more interested in CSRD than CSRP. Across countries, most of the studies were conducted in developed countries. Nevertheless, CSRD works are focused mainly on developing countries, while CSRP. studies are commonly focused on developed countries. Therefore, there are different gaps for future research, for studies on CSRD in developed countries and on CSR Performance in developing countries. Moreover, the interest of CSRD quantity have started earlier than CSRD quality, although sometimes the quality of disclosed information could give a more accurate measurement. Therefore, future research may give more interest to CSRD quality.

On the other hand, as the independent variables, the academic literature has studied the impact of a wide range of board characteristics, highlighting the board independence, gender diversity, board size, CEO duality, board meetings, and CSR committee. While a few studies take into consideration the attributes of these variables. Thus, future research could give more consideration to some characteristics of board independence (such as gender, education, experience, age), of women on the board (independent, experience, education, age), and CSR Committee (age, gender, independent, experience, education, duality). Most of the researchers’ as mentioned earlier, concluded that the level of CSR/CSRD would increase with a high percentage of independent directors, the presence of women in the board, larger board size, non-CEO duality, and the existence of the CSR committee. On the other hand, there are some board characteristics that studies did not draw enough attention towards their relationship with CSR/CSRD, such as audit committee characteristics, board age, board education, experience diversity, and board interlocking.

Finally, this study might have some limitations in the search because of the bibliometric technique used. A significant limitation is the possibility of non-inclusion of one or more of critical vital articles, in a substantial database, which was not due to a lack of methodology.

Another limitation is related to the database used (WoS). Due to its characteristics, some exceptions may be found throughout the results. On the other hand, database characteristics will be reproduced in the measurements, and they can change (Van Raan, Citation2000). Thus, WoS has been working for decades and has changed over the years (the number of journals has grown notably).

Disclosure statement

The authors declare that there is no conflict of interest regarding the publication of this article

References

- Adams, R., Almeida, H., & Ferreira, D. (2005). Powerful CEOs and their impact on corporate performance. The Review of FinancialStudies, 18(4), 1403–1432. https://doi.org/10.1093/rfs/hhi030

- Al-Dah, B., Dah, M., & Jizi, M. (2018). Is CSR reporting always favorable? Management Decision, 56(7), 1506–1525. https://doi.org/10.1108/MD-05-2017-0540

- Alotaibi, K. O., & Hussainey, K. (2016). Determinants of CSR disclosure quantity and quality: Evidence from non-financial listed firms in Saudi Arabia. International Journal of Disclosure and Governance, 13(4), 364–393. https://doi.org/10.1057/jdg.2016.2

- Angelidis, J., & Ibrahim, N. (2011). The impact of emotional intelligence on the ethical judgment of managers. Journal of Business Ethics, 99(Suppl 1), 111–119. https://doi.org/10.1007/s10551-011-1158-5

- Appuhami, R., & Tashakor, S. (2017). The impact of audit committee characteristics on CSR disclosure: an analysis of Australian firms. Australian Accounting Review, 27(4), 400–420. https://doi.org/10.1111/auar.12170

- Arora, P., & Dharwadkar, R. (2011). Corporate governance and corporate social responsibility (CSR): The moderating roles of attainment discrepancy and organization slack. Corporate Governance: An International Review, 19(2), 136–152. https://doi.org/10.1111/j.1467-8683.2010.00843.x

- Barakat, F. S. Q., Perez, M. V. L., & Ariza, L. R. (2015). Corporate social responsibility disclosure (CSRD) determinants of listed companies in Palestine (PXE) and Jordan (ASE). Review of Managerial Science, 9(4), 681–702. https://doi.org/10.1007/s11846-014-0133-9

- Barako, D. G., & Brown, A. M. (2008). Corporate social reporting and board representation: Evidence from the Kenyan banking sector. Journal of Management & Governance, 12(4), 309–324. https://doi.org/10.1007/s10997-008-9053-x

- Bear, S., Rahman, N., & Post, C. (2010). The impact of board diversity and gender composition on corporate social responsibility and firm reputation. Journal of Business Ethics, 97(2), 207–221. https://doi.org/10.1007/s10551-010-0505-2

- Brick, I., Palmon, O., & Wald, J. (2006). CEO compensation, director compensation and firm performance: Evidence of cronyism. Journal of Corporate Finance, 12(3), 403–423. https://doi.org/10.1016/j.jcorpfin.2005.08.005

- Cabeza-Garcia, L., Fernandez-Gago, R., & Nieto, M. (2018). Do board gender diversity and director typology impact csr reporting? European Management Review, 15(4), 559–575. https://doi.org/10.1111/emre.12143

- Carroll, A. B. (1999). Corporate social responsibility: Evolution of a definitional construct. Business & Society, 38(3), 268–295. https://doi.org/10.1177/000765039903800303

- Chang, Y. K., Oh, W.-Y., Park, J. H., & Jang, M. G. (2017). Exploring the relationship between board characteristics and CSR: Empirical evidence from Korea. Journal of Business Ethics, 140(2), 225–242. https://doi.org/10.1007/s10551-015-2651-z

- Chen, W. (T.), Zhou, G. (S.), & Zhu, X. (K.). (2019). CEO tenure and corporate social responsibility performance. Journal of Business Research, 95, 292–302. https://doi.org/10.1016/j.jbusres.2018.08.018

- Chung, K. H., Kim, J.‐S., Park, K., & Sung, T. (2012). Corporate governance. Asia-Pacific Journal of Financial Studies, 41(6), 686–703. https://doi.org/10.1111/ajfs.12002

- Clarivate. (2020). Web of science group. https://clarivate.com/webofsciencegroup/

- Clarkson, M. (1995). A stakeholder framework for analysing and evaluating corporate social performance. Academy of Management Review, 20(1), 92–117. https://doi.org/10.5465/amr.1995.9503271994

- Cuadrado-Ballesteros, B., Garcia-Sanchez, I. M., & Martinez-Ferrero, J. (2017). The impact of board structure on CSR practices on the international scale. European Journal of International Management, 11(6), 633–659.

- Cuadrado-Ballesteros, B., Rodriguez-Ariza, L., & Garcia-Sanchez, I. M. (2015). The role of independent directors at family firms in relation to corporate social responsibility disclosures. International Business Review, 24(5), 890–901. https://doi.org/10.1016/j.ibusrev.2015.04.002

- Cucari, N., De Falco, S. E., & Orlando, B. (2018). Diversity of board of directors and environmental social governance: Evidence from Italian listed companies. Corporate Social Responsibility and Environmental Management, 25(3), 250–266. https://doi.org/10.1002/csr.1452

- Deegan, C., Rankin, M., & Tobin, J. (2002). An examination of the corporate social and environmental disclosures of BHP from 1983‐1997. Accounting, Auditing & Accountability Journal, 15(3), 312–343. https://doi.org/10.1108/09513570210435861

- DeNooy, W., Mrvar, A., & Batagelj, V. (2005). Exploratory social network analysis with Pajek. Cambridge University Press.

- Ding, Y., Chowdhury, G., & Foo, S. (2001). Bibliometric cartography of information retrieval research by using co-word analysis. Information Processing & Management, 37(6), 817–842. https://doi.org/10.1016/S0306-4573(00)00051-0

- Diodato, V. (1994). Dictionary of bibliometrics. The Haworth Press.

- Dwekat, A., Mardawi, Z., & Abdeljawad, I. (2018). Corporate governance and auditor quality choice: Evidence from Palestinian corporations. International Journal of Economics and Financial Issues, 8(2), 47–53.

- Dwekat, A., Seguí-Mas, E., TormoCarbó, G., & Carmona, P. (2020). Corporate governance configurations and corporate social responsibility disclosure: Qualitative comparative analysis of audit committee and board characteristics. Corporate Social Responsibility and Environmental Management, 1–14. https://doi.org/10.1002/csr.2009

- Eberhardt-Toth, E. (2017). Who should be on a board corporate social responsibility committee? Journal of Cleaner Production, 140, 1926–1935. https://doi.org/10.1016/j.jclepro.2016.08.127

- Egghe, L., Rousseau, R. (1990). Introduction to informetrics. quantitative methods in library, documentation and Information science. Elsevier Science publishers.

- Fama, E. F., & Jensen, M. C. (1983). Agency problem and residual claims. The Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Feng, Y., Zhu, Q., & Lai, K. H. (2017). Corporate social responsibility for supply chain management: A literature review and bibliometric analysis. Journal of Cleaner Production, 15, 296–307.

- Fernandez-Feijoo, B., Romero, S., & Ruiz-Blanco, S. (2014). Women on boards: Do they affect sustainability reporting? Corporate Social Responsibility and Environmental Management, 21(6), 351–364. https://doi.org/10.1002/csr.1329

- Franceschini, S., Faria, L., & Jurowetzki, R. (2016). Unveiling scientific communities about sustainability and innovation. A bibliometric journey around sustainable terms. Journal of Cleaner Production, 127, 72–83. https://doi.org/10.1016/j.jclepro.2016.03.142

- Fuente, J. A., Garcia-Sanchez, I. M., & Lozano, M. B. (2017). The role of the board of directors in the adoption of GRI guidelines for the disclosure of CSR information. Journal of Cleaner Production, 141, 737–750. https://doi.org/10.1016/j.jclepro.2016.09.155

- Galant, A., & Cadez, S. (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research-Ekonomska Istraživanja, 30(1), 676–693. https://doi.org/10.1080/1331677X.2017.1313122

- García-Sánchez, I. M., & Martínez-Ferrero, J. (2017). Independent Directors and CSR Disclosures: The moderating effects of proprietary costs. Corporate Social Responsibility and Environmental Management, 24(1), 28–43. https://doi.org/10.1002/csr.1389

- Ghosh, S., & Harjoto, M. A. (2011). Insiders’ personal stock donations from the lens of stakeholder, stewardship and agency theories. Business Ethics: A European Review, 20(4), 342–358. https://doi.org/10.1111/j.1467-8608.2011.01633.x

- Giannarakis, G., Konteos, G., & Sariannidis, N. (2014). Financial, governance and environmental determinants of corporate social responsible disclosure. Management Decision, 52(10), 1928–1951. https://doi.org/10.1108/MD-05-2014-0296

- Global Reporting Initiative. (2016). Global reporting initiative (GRI): Sustainability reporting standards (G4 version). https://www.globalreporting.org/standards/gri-standards-download-center/.

- Godos-Diez, J. L., Cabeza-Garcia, L., Alonso-Martinez, D., & Fernandez-Gago, R. (2018). Factors influencing board of directors’ decision-making process as determinants of CSR engagement. Review of Managerial Science, 12(1), 229–253.

- Haniffa, R. M., & Cooke, T. E. (2002). Culture, corporate governance and disclosure in Malaysian corporations. Abacus, 38(3), 317–349. https://doi.org/10.1111/1467-6281.00112

- Harjoto, M. A., & Jo, H. (2011). Corporate governance and CSR nexus. Journal of Business Ethics, 100(1), 45–67. https://doi.org/10.1007/s10551-011-0772-6

- Harjoto, M., Laksmana, I., & Lee, R. (2015). Board diversity and corporate social responsibility. Journal of Business Ethics, 132(4), 641–660. https://doi.org/10.1007/s10551-014-2343-0

- Helfaya, A., & Moussa, T. (2017). Do board’s corporate social responsibility strategy and orientation influence environmental sustainability disclosure? UK evidence. Business Strategy and the Environment, 26(8), 1061–1077. https://doi.org/10.1002/bse.1960

- Huang, C. Y., & Ho, Y. S. (2011). Historical research on corporate governance: A bibliometric analysis. African Journal of Business Management, 5(2), 276–284.

- Jaén, M., Auletta, N., Bruni Celli, J., & Pocaterra, M. (2018). Bibliometric analysis of indexed research on corporate social responsibility in Latin America (2000–2017). Academia Revista Latinoamericana de Administración, 31(1), 105–135. https://doi.org/10.1108/ARLA-06-2017-0190

- Jain, T., & Jamali, D. (2016). Looking inside the black box: The effect of corporate governance on corporate social responsibility. Corporate Governance: An International Review, 24(3), 253–273. https://doi.org/10.1111/corg.12154

- Jamali, D., Safieddine, A. M., & Rabbath, M. (2008). Corporate governance and corporate social responsibility synergies and interrelationships. Corporate Governance: An International Review, 16(5), 443–459. https://doi.org/10.1111/j.1467-8683.2008.00702.x

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jizi, M. I., Salama, A., Dixon, R., & Stratling, R. (2014). Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. Journal of Business Ethics, 125(4), 601–615. https://doi.org/10.1007/s10551-013-1929-2

- Jo, H., & Harjoto, M. A. (2011). Corporate governance and firm value: The impact of corporate social responsibility. Journal of Business Ethics, 103(3), 351–383. https://doi.org/10.1007/s10551-011-0869-y

- Kessler, M. M. (1963). Bibliographie coupling between scientific papers. American Documentation, 14(1), 10–11. https://doi.org/10.1002/asi.5090140103

- Khan, A., Muttakin, M. B., & Siddiqui, J. (2013). Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. Journal of Business Ethics, 114(2), 207–223. https://doi.org/10.1007/s10551-012-1336-0

- Kolsi, M. C., & Attayah, O. F. (2018). Environmental policy disclosures and sustainable development: Determinants, measure and impact on firm value for ADX listed companies. Corporate Social Responsibility and Environmental Management, 25(5), 807–818. https://doi.org/10.1002/csr.1496

- Li, K., Rollins, J., & Yan, E. (2018). Web of science use in published research and review papers 1997–2017: A selective, dynamic, cross-domain, content-based analysis. Scientometrics, 115(1), 1–20. https://doi.org/10.1007/s11192-017-2622-5

- Li, S. M., Fetscherin, M., Alon, I., Lattemann, C., & Yeh, K. (2010). Corporate social responsibility in emerging markets: The importance of the governance environment. Management International Review, 50(5), 635–654. https://doi.org/10.1007/s11575-010-0049-9

- Liao, L., Lin, T., & Zhang, Y. Y. (2018). Corporate board and corporate social responsibility assurance: Evidence from China. Journal of Business Ethics, 150(1), 211–225. https://doi.org/10.1007/s10551-016-3176-9

- Macaulay, C. D., Richard, O. C., Peng, M. W., & Hasenhuttl, M. (2018). Alliance network centrality, board composition, and corporate social performance. Journal of Business Ethics, 151(4), 997–1008. https://doi.org/10.1007/s10551-017-3566-7

- Mallin, C. A., & Michelon, G. (2011). Board reputation attributes and corporate social performance: An empirical investigation of the US best corporate citizens. Accounting and Business Research, 41(2), 119–144. https://doi.org/10.1080/00014788.2011.550740

- Mallin, C., Farag, H., & Ow-Yong, K. (2014). Corporate social responsibility and financial performance in Islamic banks. Journal of Economic Behavior & Organization, 103, S21–S38. https://doi.org/10.1016/j.jebo.2014.03.001

- Merigó-Lindahl, J. M. (2012). Bibliometric analysis of business and economics in the Web of Science. In Soft computing in management and business economics (pp. 3–17). Springer.

- Monks, R., & Minow, N. (1995). Corporate governance. Blackwell.

- Montiel, I., & Delgado-Ceballos, J. (2014). Defining and measuring corporate sustainability: Are we there yet? Organization & Environment, 27(2), 113–139. https://doi.org/10.1177/1086026614526413

- Nekhili, M., Nagati, H., Chtioui, T., & Nekhili, A. (2017). Gender-diverse board and the relevance of voluntary CSR reporting. International Review of Financial Analysis, 50, 81–100. https://doi.org/10.1016/j.irfa.2017.02.003

- Pucheta-Martinez, M. C., & Chiva-Ortells, C. (2018). The role of directors representing institutional ownership in sustainable development through corporate social responsibility reporting. Sustainable Development, 26(6), 835–846. https://doi.org/10.1002/sd.1853

- Rao, K., & Tilt, C. (2016). Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. Journal of Business Ethics, 138(2), 327–347. https://doi.org/10.1007/s10551-015-2613-5

- Sandison, A. (1989). Documentation note: thinking about citation analysis. Journal of Documentation, 45(1), 59–64. https://doi.org/10.1108/eb026839

- Sarkar, S., & Searcy, C. (2016). Zeitgeist or chameleon? A quantitative analysis of CSR definitions. Journal of Cleaner Production, 135, 1423–1435. https://doi.org/10.1016/j.jclepro.2016.06.157

- Seguí-Mas, E., Jiménez-Arribas, I., & Tormo-Carbó, G. (2019). Does the environment matter? Mapping academic knowledge on entrepreneurial ecosystems in GEM. Entrepreneurship Research Journal, 9(2), 1–19. https://doi.org/10.1515/erj-2017-0170

- Sharif, M., & Rashid, K. (2014). Corporate governance and corporate social responsibility (CSR) reporting: An empirical evidence from commercial banks (CB) of Pakistan. Quality & Quantity, 48(5), 2501–2521. https://doi.org/10.1007/s11135-013-9903-8

- Shaukat, A., Qiu, Y., & Trojanowski, G. (2016). Board attributes, corporate social responsibility strategy, and corporate environmental and social performance. Journal of Business Ethics, 135(3), 569–585. https://doi.org/10.1007/s10551-014-2460-9

- Siregar, V. S., & Bachtiar, Y. (2010). Corporate social reporting: Empirical evidence from Indonesia Stock Exchange. International Journal of Islamic and Middle Eastern Finance and Management, 3(3), 241–252. https://doi.org/10.1108/17538391011072435

- Skare, M., & Golja, T. (2012). Corporate social responsibility and corporate financial performance - Is there a link? Economic Research-Ekonomska Istraživanja, 25(Suppl 1), 215–242. https://doi.org/10.1080/1331677X.2012.11517563

- Terjesen, S., Sealy, R., & Singh, V. (2009). Women directors on corporate boards: A review and research agenda. Corporate Governance: An International Review, 17(3), 320–337. https://doi.org/10.1111/j.1467-8683.2009.00742.x

- Van Raan, A. (2000). On growth, ageing, and fractal differentiation of science. Scientometrics, 47(2), 347–362. https://doi.org/10.1023/A:1005647328460

- Velte, P.(2017). Does board composition have an impact on CSR reporting? Problems and Perspectives in Management, 15(2), 19–35. https://doi.org/10.21511/ppm.15(2).2017.02

- Verbeek, A., Debackere, K., Luwel, M., & Zimmermann, E. (2002). Measuring progress and evolution in science and technology: The multiple uses of bibliometric indicators. International Journal of Management Reviews, 4(2), 179–211. https://doi.org/10.1111/1468-2370.00083

- Wang, J., & Coffey, B. S. (1992). Board composition and corporate philanthropy. Journal of Business Ethics, 11(10), 771–778. https://doi.org/10.1007/BF00872309

- Williams, S., & Pei, C. (1999). Corporate social disclosures by listed companies on their web sites: An international comparison. The International Journal of Accounting, 34(3), 389–419. https://doi.org/10.1016/S0020-7063(99)00016-3

- Wood, D. J. (2010). Measuring corporate social performance: A review. International Journal of Management Reviews, 12(1), 50–84. https://doi.org/10.1111/j.1468-2370.2009.00274.x

- Zahra, S., & Stanton, W. (1988). The implications of board of directors’ composition for corporate strategy and performance. International Journal of Management, 5, 261–272.

- Zaid, M. A. A., Wang, M., & Abuhijleh, S. T. F. (2019). The effect of corporate governance practices on corporate social responsibility disclosure. Journal of Global Responsibility, 10(2), 134–160. https://doi.org/10.1108/JGR-10-2018-0053

- Zaid, M. A., Abuhijleh, S. T., & Pucheta‐Martínez, M. C. (2020). Ownership structure, stakeholder engagement, and corporate social responsibility policies: The moderating effect of board independence. Corporate Social Responsibility and Environmental Management, 27(3), 1344–1360. https://doi.org/10.1002/csr.1888

- Zaid, M. A., Wang, M., Adib, M., Sahyouni, A., & Abuhijleh, S. T. (2020). Boardroom nationality and gender diversity: Implications for corporate sustainability performance. Journal of Cleaner Production, 251, 119652. https://doi.org/10.1016/j.jclepro.2019.119652

- Zemigała, M. (2015). Bibliometric analysis of corporate social responsibility – Different countries’ perspective. Human Resources Management & Ergonomics, 9, 123–138. https://frcatel.fri.uniza.sk/hrme/files/2015/2015_1_10.pdf

- Zemigała, M. (2017). Application of social responsibility standards in Poland and the world. Ekonomia I Prawo. Economics and Law, 16(2), 229–240. https://doi.org/10.12775/eip.2017.016

- Zemigała, M. (2019). Tendencies in research on sustainable development in management sciences. Journal of Cleaner Production, 218, 796–809. https://doi.org/10.1016/j.jclepro.2019.02.009

- Zhang, J. Q., Zhu, H., & Ding, H. B. (2013). Board composition and corporate social responsibility: An empirical investigation in the post Sarbanes-Oxley era. Journal of Business Ethics, 114(3), 381–392. https://doi.org/10.1007/s10551-012-1352-0

- Zhu, J., & Hua, W. (2017). Visualising the knowledge domain of sustainable development research between 1987 and 2015: A bibliometric analysis. Scientometrics, 110(2), 893–914. https://doi.org/10.1007/s11192-016-2187-8