?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

In the current dynamic environment, organizations are exposed to many risks from different directions. Therefore, this study using the theoretical lens explored the effect of enterprise risk management (ERM) on both financial and non-financial firm performance and the moderating role of intellectual capital (IC) and its dimensions on the relationship between ERM and firm performance. To test the study hypotheses, a questionnaire survey was distributed to 84 Iranian financial institutions. Structural equation modeling (PLS software) was used to analyze the data statistically. The findings revealed that ERM had a positive relationship with firms’ performance. The results also showed that the overall IC had a moderating effect on ERM-firm financial performance. However, regarding components of IC, knowledge, and information technology (IT) had a positive and significant moderating effect while training, organizational culture, and trust did not affect. This study provides an insight into the impact of ERM in recent years on non-financial performance and the influence of intangible assets on ERM and its function. The model developed in the current study and result can be extended and implemented to other organizations in developing countries.

1. Introduction

Nowadays, enterprise risk management (ERM) is growing fast among different corporations in various countries (Ai et al., Citation2018). However, financial industries are more involved in ERM compare to other sectors (Nguyen & Vo, Citation2020; Saeidi et al., Citation2019). According to Saeidi et al. (Citation2019), Ai et al. (Citation2018), and Nguyen and Vo (Citation2020), financial institutions were among the first organizations implementing ERM. Several studies have documented the crucial role of financial institutions in the economic development of countries (Chen et al., Citation2019; Khafagy, Citation2019). Consequently, risk management for this sector is more critical than for other industries (Chen et al., Citation2019; Gelman et al., Citation2018). Issues occurring in financial institutions may cause considerable negative consequences on the whole economy. According to Talwar (Citation2011), the collapse of even a single financial organization can harm the entire financial mechanism of a country and cause system-wide failure, which will subsequently transfer to other industries, to the macroeconomy, and worldwide (e.g., financial crisis of 2008). Thus, ERM has risen as a significant area of interest within the financial institutions.

Aligned with financial institutions of other countries, the central bank of Iran (Bank Markazi Iran), approved a directive on the implementation of a comprehensive system of internal controls in the financial and credit institutions of Iran (i.e., ERM). The Iranian financial institutions have suffered problems which raised the necessity of risk management improvement. The exchange rate volatility is a good illustration of this case. In recent years, several factors, including war, international sanctions, and failure of proper management, causing the fluctuation in the exchange rate that eventually disturbed the functions of the financial institutions of Iran (Parveen et al., Citation2015).

Moreover, the establishment of unauthorized financial institutions in Iran could generally be seen as another issue and threat to the whole industry. These unauthorized institutions often refuse directives and orders, break their bylaws, and thus, create turbulence in domestic fiscal markets (Amini, Citation2015). In many cases, these institutions may face bankruptcy because of the inadequacy of resources, which could un-stabilize other institutions as well (Niavand & Haghighat Nia, Citation2018). Moreover, according to its 20-year perspective (vision) plan, Iran plans to rank at the first and top position in the region of the Middle East regarding technology, scientific, and economic level by the year 2025 (Afzali, Citation2011). Moreover, based on Parveen et al. (Citation2015), the role of financial institutions of Iran for financing and creating money for different economic activities such as import, export, establish new businesses, and entrepreneurs cannot be neglected. In this regard, the head of the central bank of Iran stated that the economy of Iran had relied a lot on the financial institutions, and it has bank-orientation. They are providing around 84% of the financing in different sectors and industries. Therefore, the high contribution of financial institutions of Iran in the economic development of the country is clear. Consequently, it is required to control and overcome their challenges to meet the objectives of the 20-year perspective of Iran.

Additionally, the situation of ERM among developing countries is not clear, and there is a lack of empirical studies (Chen et al., Citation2019; Silva et al., Citation2019). However, based on the discussion of Silva et al. (Citation2019), Chen et al. (Citation2019), and Khattab et al. (Citation2015), the institutions in developing countries are faced with much more uncertainty, risks, and challenges that influence their performance compared to developed countries. Therefore, developing countries often need a more robust risk management system for a better organization function. Consequently, evaluating the effect of ERM on firm performance among Iranian financial institutions could be helpful.

Furthermore, the majority of the past investigation has studied only the financial features of firm performance. Although evaluating and boosting the entire performance of firms depends on both monetary and non-monetary features, remarkably, there is no clear division between non-financial and financial performance (Saeidi et al., Citation2015). Consequently, the first goal of the present study is to evaluate the effect of ERM on non-financial and financial performance. Thus, this study would increase the insight and understanding regarding the entire impact of ERM on firm performance by observing both non-financial and financial performance. Moreover, in contrast to major ERM previous studies that evaluated ERM by a simple method (dummy variable), this study followed Saeidi et al. (Citation2019) to evaluate ERM by considering a comprehensive measurement based on ERM components by COSO (Citation2004).

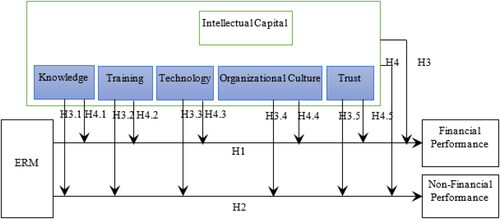

Additionally, when discussing ERM and firm performance, it is equally important to explore whether this relationship could also be influenced by other elements (Farrell & Gallagher, Citation2019; Saeidi et al., Citation2019). Based on the concept of organization systems, a corporation encompasses numerous functions to meet organizational goals and objectives (Chenhall, Citation2003). Therefore, the association between ERM and firm performance is more complicated than the merely direct link between them. Accordingly, this study attempts to improve previous researches by posing a new question: is Intellectual Capital (IC) a moderator on the relationship between ERM and firm performance? IC is known as nonphysical and nonmonetary assets, which are entirely or partially controlled by the firm to support the value generation of the firm. It is engaged in major activities of the organization, where ERM is not an exception. To the best of our knowledge, a limited practical study conducted on the issue of examining the effect of intangible factors such as IC in the field of ERM (Khan & Ali, Citation2017). Therefore, this study explores the impact of IC and its essential factors (e.g., knowledge, training, technology, organizational culture, and trust) on ERM and its influence on firm performance.

This study is highly significant because it established an increased awareness of the importance of recognition and consideration on conjunction variables when evaluating ERM-firm performance relationship. Our analysis provides a starting point for additional research into ERM in Asia emerging markets. In developing countries, due to differences in financial systems and financial regulations, ERM has different impacts between developed and emerging countries. Moreover, it encourages managers to enhance their capacity to implement and develop their strategic resources such as IC components and ERM to increase the performance of their institutions, which would consequently lead to the economic development of the country.

The following sections of this paper are structured as follows. Section 2 presented the literature review and hypotheses brought. Section 3 described the methodology of the research and data collection. Section 4 provided the analysis and the results. Lastly, in section 5, conclusions and a discussion on the study outcomes are presented.

2. Literature review and hypothesis brought

2.1. Enterprise risk management and firm performance

Based on the Agency Theory, the implementation of a strong risk management system such as ERM could increase the overall firm performance and shareholder value (Idris & Norlida Abdul, Citation2016). ERM researchers argue that it benefits firms and increase shareholder value by reducing earning and stock price fluctuation, decreasing external capital costs, and rising capital efficiency (Lechner & Gatzert, Citation2018). By utilizing a tactical and constant method (or process) for managing all of the risks meeting a company, ERM is believed to reduce the total risk failure of an organization, and raise the efficiency and the value of the firm and shareholders. Moreover, according to the Resource-Based View (RBV) theory of the organization, corporations could attain superior performance and competitive advantage through the holding, acquisition, and continuous use of strategic assets (Wernerfelt, Citation1984). An effective ERM system could be seen as a strategic asset for institutions. This mechanism does not exist in the business trade to buy or sell it. In other words, every institution has its particular ERM system that is suitable for its visions, mission, objectives, and activities (M. S. Beasley et al., Citation2005). Consequently, based on Hoyt and Liebenberg (Citation2011) and COSO (Citation2004), the ERM process and system in one institution is unable to comply with the requests of other institutions. This is unique for each institution, and the use of a proper ERM system can create many benefits for that organization. As a result, the existence of such assets in en organization could create a competitive advantage and enhance overall firm performance.

Some researchers have started to explore the connection between ERM and organization performance (Chen et al., Citation2019; Florio & Leoni, Citation2017; Hanggraeni et al., Citation2019; Ojeka et al., Citation2019; Teoh et al., Citation2017; Zungu et al.,Citation2018). These studies mainly focused on the link between ERM and financial performance. Among them, the studies of Tahir and Razali (Citation2011), McShane et al. (Citation2011), Hoyt and Liebenberg (Citation2011), Quon et al. (Citation2012), Forrell and Gallagher (2015), Florio and Leoni (Citation2017); Bertinetti et al. (Citation2013) evaluated Tobins’ q as the proxy for the measurement of firm performance (market performance). While, Gordon et al. (Citation2009), Pagach and Warr (Citation2010), Grace et al. (Citation2015), Manab et al. (Citation2010), Gates et al. (Citation2012), Quon et al. (Citation2012), Li et al. (Citation2014), Khan Majid et al. (2016), Florio and Leoni (Citation2017) evaluated firm performance by using other financial variables such as excess stock market return, return on asset, reduction of expenses, return on equity, earnings volatility, profitability, cost efficiency, and accounting performance (earnings before interest and tax). Therebetween, only a few studies considered both financial and non-financial performance, such as Ping and Muthuveloo (Citation2015) and Teoh et al. (Citation2017).

Furthermore, the findings of previous studies are inconclusive. For example, findings by Malik et al. (Citation2020) Saeidi et al. (2019) indicated a positive and significant relationship between ERM and firm performance. This result replicated the finding of other studies such as Saeidi et al. (Citation2019), Lechner and Gatzert (Citation2018), Chen et al. (Citation2019), Hanggraeni et al. (Citation2019), Ai et al. (Citation2018), Eckles et al. (Citation2014), Teoh et al. (Citation2017), Ping and Muthuveloo (Citation2015), Jalal-Karim (Citation2013), Farrell and Gallagher (Citation2015), Bertinetti et al. (Citation2013), and Floria and Leoni (2017). Moreover, Manab et al. (Citation2010) and Gates et al. (Citation2012) indicated that ERM could indirectly affect firm performance through increasing the capability and ability of the managers of organizations. Likewise, Silva De Souza et al. (Citation2012) specified that the effect of ERM on firm performance is influenced by the degree of involvement of the stakeholders in risk management and the maturity level on managing risk. Despite these studies, Tahir and Razali (Citation2011), McShane et al. (Citation2011), Quon et al. (Citation2012), and Li et al. (Citation2014) demonstrated no additional increase in firm performance for companies implementing ERM. Although Lin et al. (Citation2012) found a negative association between ERM and return on assets and Tobin’s q, such inconclusiveness creates ground for further investigation (Gates et al., Citation2012; McShane et al., Citation2011).

Moreover, it can be inferred that the scope of the most of investigation in the field of ERM and firm performance was conducted among advanced countries (Bertinetti et al., Citation2013; Farrell & Gallagher, Citation2015; Florio & Leoni, Citation2017; Gordon et al., Citation2009; Grace et al., Citation2015; Hoyt & Liebenberg, Citation2011; Nguyen & Vo, Citation2020; Pagach & Warr, Citation2010; Quon et al., Citation2012). Few studies have emphasized on developing nations (Hanggraeni et al., Citation2019; Li et al., Citation2014; Ojeka et al., Citation2019; Ping & Muthuveloo, Citation2015; Silva et al., Citation2019; Teoh et al., Citation2017). Institutions in developing countries require to take into account risks on a much extensive scope than those well-established institutions in developed countries (Al Khattab et al., Citation2015). The growth rate of the implementation of ERM is higher among developed countries compared to that of developing countries (Silva et al., Citation2019). This gap could be because of the absence of understanding and knowledge of ERM concepts and their effect on developing countries. Therefore, some researchers such as Li et al. (Citation2014), Manab et al. (Citation2010), Tahir and Razali (Citation2011), Jalal-Karim (Citation2013), and Silva et al. (Citation2019) suggested more research among developing countries, which could help in more awareness about the concept and importance of ERM. Especially, there are few studies among countries located in the Middle East (Jalal‐Karim, Citation2013). Consequently, conducting a study in a developing country such as Iran could be of great help in indicating ERM outcomes in a universal context. Remarkably, ERM among Iranian businesses has never been properly considered in both the academic environment and the practical terms.

In addition, while ERM is vital for financial institutions, there are inadequate studies about the effect of ERM on their performance, especially among both banking and non-banking financial institutions. In other words, the majority of previous studies among financial institutions have only focused on insurance companies (Eckles et al., Citation2014; Hoyt & Liebenberg, Citation2011; McShane et al., Citation2011; Nguyen & Vo, Citation2020). In this regard, Gatzert and Martin (Citation2015) suggested more research on the association between ERM and firm value, particularly related to financial organizations. Additionally, the real influence of the ERM on firm performance is to remain uncertain due to inconclusive and different results of previous studies. Such inconclusiveness creates ground for further investigation (Gates et al., Citation2012; McShane et al., Citation2011).

Moreover, there are scarce studies that examined ERM extensively by evaluating all its components. Majority of the past researches measured ERM through examining its implementation as a dummy variable or by asking direct questions about the adoption and the level of its implementation (Chen et al., Citation2019; Eckles et al., Citation2014; Ojeka et al., Citation2019; Pagach & Warr, Citation2010). In contrast, in this current study, ERM is evaluated by all its eight components, as suggested by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) (COSO, Citation2004), which sets out a complete view of ERM implementation. Likewise, to the best of our knowledge, there are inadequate studies that considered competitive advantage and BSC perspectives as a strategy-orientated performance measurement of organizations and proxies for evaluating firm performance. Through BSC, organizations can obtain a better view of their both non-financial and financial performance.

From the above discussion, this study sought to fill-up the abovementioned gaps and to consider the effect of ERM on firm performance by testing the following hypotheses.

H1: ERM has a positive and significant effect on firm financial performance.

H2: ERM has a positive and significant effect on firm non-financial performance.

2.2. Enterprise risk management, intellectual capital, and firm performance

As mentioned in the previous section in detail, the acceptance and application of the ERM program by organizations can generate value and enhance firm performance (Hanggraeni et al., Citation2019; Malik et al., Citation2020; Saeidi et al., Citation2019). However, the empirical results are inconsistent (Gates et al., Citation2012; McShane et al., Citation2011). This inconsistency may be due to the evaluation of merely ERM and firm performance relationship without consideration of interaction variables that affect the majority of functions of the organization.

In other words, since the relationship between ERM and firm performance has great importance in today’s business dynamic environment, the recognition of the variables that can improve this association is paramount (Saeidi et al., Citation2019; Tsai et al., Citation2017). According to the most recent method of contingency theory, the link between two parameters may influence or depends on other variables (Chenhall, Citation2003). Therefore, despite previous studies considering only a direct connection between ERM and firm performance, this study went a step further by recognizing moderating variables that could influence the strength of this relationship.

Aligned with this point and due to the changes and unforeseen tendencies of the economy from conventional to knowledge economy system and engaging of IC and its component on the majority of organizations activities, this study considered IC and some of its important components as a moderator to increase its effect on firm performance. Moreover, to the best of our knowledge, there has been no practical study conducted on the issue of examining the moderation effect of IC on the relationship between ERM and firm performance. It can be due to a large extent and difficulty of intangible evaluation assets and intellectual capital.

Consequently, this study considered IC, which is the main and foundation part of today’s knowledge economy, as an influential factor in the ERM-firm performance relationship. Therefore, the next hypotheses in this study are:

H3: IC has a moderator effect on the relationship between ERM and firm financial performance.

H4: IC has a moderator effect on the relationship between ERM and firm non-financial performance.

There are several resources involved as elements of IC components in organizations. Bontis (1998) stated that the effects and roles of various items of IC are significantly complicated and, consequently, difficult to forecast and predict. However, by reviewing the literature, it can be conducted that there are some factors that are more relevant and seen as a base and foundation of other activities and intangible resources (e.g., knowledge and training for human capital, technology and organizational culture for structural capital, and trust for spiritual capital) (Ismail, Citation2005; Savolainen & Fresno, Citation2013; Zehir et al., Citation2011; Zohar & Marshall, Citation2004). To the best of authors knowledge there is not any study which consider the IC important variables in the context of ERM. Therefore, this study attempted to give a comprehensive view of the effect of important characteristics of IC as well as whole IC. The theoretical explanation for the effect of these dimensions of IC on the effectiveness of ERM is discussed below.

2.2.1. Knowledge

The literature review makes it clear that different aspects of knowledge have been constructively delineated to have a considerable impact on the effectiveness and success of ERM. To develop risk management capacity, ERM, as a multidisciplinary work, requires knowledge to support individuals, groups, organizations, and inter-organizations (Rodriguez & Edwards, Citation2009). Based on the COSO (Citation2004), ERM is accomplished and executed by the people of a company by what they say and do. People determined the entity’s objectives, mission, and strategy and set up an ERM system. Therefore, the importance of knowledge as the main and foundation part of human resource activities is evident. Oliveira et al. (Citation2019) recommended knowledge as an element that leads to a reduction of risk. Awareness and knowledge of people toward events and risk and their role and responsibility in the organization’s plan are critically crucial for managing risk (Burnaby & Hass, Citation2009; COSO, Citation2004; Yaraghi & Langhe, Citation2011). In other words, companies that have people who are more aware of the risk, organization objectives, situation and plan, events, and uncertainty are more likely to show better reaction into risks and opportunity (Carey, Citation2001; COSO, Citation2004; Neef, Citation2005; Rodriguez & Edwards, Citation2009). Awareness of risk at each stage ultimately leads to the adoption of best practices. These companies can recognize potential opportunities, as well as risk, better than other organizations without an established ERM system.

According to the above discussions, knowledge and awareness are integral components in improving the ERM program. Consequently, this study hypothesized:

H3.1: Knowledge of employees has a moderating effect on the ERM-financial performance relationship.

H4.1: Knowledge of employees has a moderating effect on the ERM and non-financial performance relationship.

2.2.2. Training

In a rapidly changing global environment that depends on skills and knowledge, investment in training programs has become the main contribution in human capital stock. A proper training program increases the knowledge and skills of employees, and enhances their productivity in tasks, resulting in achieving the overall productivity of companies (Shiryan et al., Citation2012). In the context of ERM, training is one of the most important instruments to gain and boost knowledge and awareness of employees. It helps and supports people in the organization, and equip them to deal with the new challenges, risks, and issues of the entity. According to Carey (Citation2001), in an organization’s operation, the design and growth of risk training programs and courses and the engagement of personnel in responding to an early warning system are among the abilities to answer to changing conditions. Training policies can help organizations to reinforce the levels of knowledge, understanding, and skills of people related to ERM (Ranong & Phuenngam, Citation2009; Yaraghi & Langhe, Citation2011). Thus, it ensures performance by including such practices as simulated case studies, seminars, training schools, and role-playing exercises. Yaraghi and Langhe (Citation2011) demonstrated that the responsibilities of continuous instruction, education, and training are essential in the achievement of risk management systems.

Based on those as mentioned above, it could be highlighted that training and education practices have a vital role in improving the ERM system in organizations. It can set the foundation for employees to understand their role and responsibility regarding the enhancement of ERM and its importance to the organization. Consequently, this study hypothesized:

H3.2: Training program has a moderating effect on ERM-financial performance relationship.

H4.2: Training program has a moderating effect on ERM and non-financial performance relationship.

2.2.3. Technology

The importance of information technology (IT) for all activities in organizations is a truism among managers, policymakers, and researchers. With a considerable review of the literature, it was evident that the use of IT is closely related to risk management activities. Some scholars stress the importance of such an orientation in enhancing risk management capabilities (Arena et al., Citation2010; COSO, Citation2004; Saeidi et al., Citation2019; Yaraghi & Langhe, Citation2011). Rolland (Citation2008) posited that it is almost impossible to perform effective management of risk without an efficient IT system. Research of Saeidi et al. (Citation2019), is consistent with this message. Rolland (Citation2008) indicated that IT could affect risk management in different ways, such as generating a relevant connection between risk management and business performance. Offering data security by personnel level, reducing a user’s access by time, line of commerce, commercial activity, and personal risk, and using IT instruments to gather information previously utilized so that organizations can learn through experience and prevent duplicating the same faults. Ranong and Phuenngam (Citation2009) indicated that IT is the most critical factor in the success of an organizational risk management system. Oliveira et al. (Citation2019) specified technology as one of the critical success factors for ERM. Accordingly, it can be hypothesized that:

H3.3: IT has a moderating effect on the ERM-financial performance relationship.

H4.3: IT has a moderating effect on the ERM and non-financial performance relationship.

2.2.4. Organizational culture

According to Kimbrough and Componation (Citation2009), the importance of a supportive organizational culture to ERM can be seen in all aspects of the ERM discourse, from ERM theory through application and improvement. Likewise, since ERM requires the deliberate identification, assessment, and mitigation of risks, a culture that is not characterized by openness, trust, and the absence of fear of reprisal may face challenges in improving ERM effectiveness (Kimbrough & Componation, Citation2009). According to Rodriguez and Edward (2009), ERM also requires knowledge dissemination and distribution with the aim of support people and organizations to develop risk management capacity. They opined that sharing experience is a factor influencing ERM and improving its effect on firm performance. The culture of an organization is the basis for knowledge transfer that can develop an informal learning process without the intention of teaching. Similarly, Oliveira et al. (Citation2019) stated that ERM requires risk awareness in the culture. COSO (Citation2004) mentioned that the board of directors has the liability for establishing the culture and belief that risk management is the obligation of all people across the different units of the company.

Moreover, there should be clarity among personnel regarding the company’s risk philosophy, risk capability, objectives, and strategy. It is the task of the company’s top managers to ensure this clarity through organizational culture (COSO, Citation2004). Oliveira et al. (Citation2019) mentioned that communication and awareness and risk culture is among the top critical success factor for ERM.

Based on Oliveira et al. (Citation2019), the strong risk culture means that employees understand an organization’s strategic orientation and risk appetite; further, they can freely discuss prevailing risks and opportunities. Thomya and Saenchaiyathon (Citation2015) stated that as ERM needs to collaborate cross-functionally to analyze and find the way to manage uncertain events within a dynamic environment, therefore organization that has characteristic of continuously learning could be so helpful. Ranong and Phuenngam (Citation2009) exposed the significance of culture as one of the critical success factors in the efficient risk management. Therefore, to implement and improve ERM in organizations, the culture of the organizations should support knowledge sharing, learning, communication, and risk awareness, and overall they should have a risk culture.

A review of the existing literature shows that there is a lack of empirical studies regarding the organizational culture that influence risk management system effectiveness. Therefore, this study can provide knowledge toward the influence of a company’s culture on ERM effectiveness by considering the following hypotheses:

H3.4: Organizational culture has a moderating effect on ERM-financial performance relationship.

H4.4: Organizational culture has a moderating effect on ERM and non-financial performance relationship.

2.2.5. Organizational trust

ERM is an interactive process that needs communication, exchanging of opinion and information among individuals, employees, and groups in institutions (Oliveira et al., Citation2019). It needs teamwork, synergy, and cooperation; thus, encouraging success (COSO, Citation2004). All phenomena, as mentioned above, are complicated without inter-organizational trust. In other words, trust is essential due to the strong tendency to perceive how to make a productive collaboration, cooperation, communication, and exchanging and sharing knowledge and information inside the companies (Earle et al., Citation2010). Trust among the personnel can efficiently operate communication and interaction practices at their interfaces. Therefore, staff can jointly acquire knowledge and can build shared mental frameworks of dependability and a shared culture of safety. Risk management involves functions that motivate share commitment (COSO, Citation2004). Therefore, trust is one of the instruments of supporting efficient risk management. In another research, Ranong and Phuenngam (Citation2009) reported trust as a critical success factor for risk management systems.

Based on the above discussions, trust can be considered as a strong instrument to improve ERM; therefore, a study would clarify how improving organizational trust can promote ERM effectiveness. Consequently, this study hypothesized:

H3.5: Organizational Trust has a moderating effect on ERM-financial performance relationship.

H4.5: Organizational Trust has a moderating effect on ERM and non-financial performance relationship.

The overall framework of the present study is offered in .

Figure 1. Research framework.

Source: compiled by authors.

3. Methodology and data collection

To assessment the research framework, this study employed a self-administered questionnaire among financial institutions of Iran. The target population of the present study was all financial institutions of Iran that were listed in the Iranian central insurance, central bank, and stock exchange market websites implementing ERM. The financial institutions were selected because, based on the literature, financial institutions are among the primary organizations that hired chief risk officers and have adopted and implemented the ERM system (Chen et al., Citation2019; Nguyen & Vo, Citation2020; Ojeka et al., Citation2019). Also, they are frequently dealing with a wide array of risks due to working with various types of customers, their sophisticated trade, and different amounts of financial assets.

Consequently, risk management among these institutions is more important than others (Shafique et al., Citation2013). In addition, because of their intervening role in deficit and surplus units (Shafique et al., Citation2013), along with their role in resource distribution (Ojeka et al., Citation2019), they play a critical role in the economy of the countries. Consequently, the success and health of these institutions are essential. In other words, the collapse of even one financial organization can harm the financial system of a country and cause a system-wide failure or systemic risk, that will distribute to other industries, to the macroeconomy, and universally (Talwar, Citation2011).

Moreover, because of problems such as international sanctions, lack of proper management, fluctuation of the exchange rate, and the establishment of unauthorized financial institutions, it is crucial to managing the risk among financial institutions of Iran. Furthermore, selecting just one industry as the sample will assist the investigator in managing the differences that may occur from market variation and regulatory across industries (Hoyt & Liebenberg, Citation2011). In addition, a superior internal validity will be obtained by selecting a specific industry analysis rather than a multi-industry analysis (Chen et al., Citation2019).

After selecting the financial institutions of Iran, the next step was to recognize those that are utilizing ERM as their risk management system. Similar to previous studies, this study searched for various terms that are known as indicators of the presence of ERM in annual reports of companies. The presence of the vice president enterprise risk management, chief risk officer, executive risk manager, risk management committee, head of the risk manager, senior risk manager, and vice president risk management are recognized as proxies for implementing ERM. Thus, these terms were searched in the financial institutions’ hierarchy, announcements, and annual reports, or called one by one when the ambiguity of the sentences, reports, or missing of information. Finally, 91 companies implementing ERM out of 183 headquarters of financial institutions were found in Iran.

The present study collected data from the headquarter of every institution as a delegation of their branches. Because of the small sample size and to obtain maximum responses, this study employed census sampling techniques and a self-administered supervised method of data collection to reduce the respondent’s error (Bourque & Fielder, 2003). The respondents of the study were the top managers of the companies or anyone who was in charge and in possession of adequate information about managing the risks in the companies such as chief risk officer. As all branches of each of the financial institutions have to follow the rule and regulations of their headquarters; therefore, this study gathered information from the headquarter of each institution as a representative of their branches.

Finally, 84 usable questionnaires were used for data analysis. The target population was consistent with previous studies carried out on financial institutions. For example Hoyt and Liebenberg (Citation2011), 117 US insurance companies, McShane et al. (Citation2011), 82 insurance companies in America, Mondal and Ghosh (Citation2012), 65 Indian banks, Cabrita et al. (Citation2007), 53 Portuguese banks, Chen et al. (Citation2019) 68 Taiwanese financial firms, Ojeka et al. (Citation2019) 33 financial institutions in Nigeria, Ojeka et al. (Citation2019) 101 insurance firm from European union and Eckles et al. (Citation2014) 69 insurance firm from united states ().

Table 1. Descriptive of respondents.

Of all respondents, 42.9% of respondents (36) were from investment and fund organizations, and 20.2% of respondents (17) were from private banks as the two largest numbers of respondents of the study. Regarding the age of organizations, the largest group of respondents was between 10 and 30 years old (42.9%), and only 4.8% (4) of them were above 70 years old. Concerning the number of employees, most of the organizations, 46.2% (39), have between 1001 and 5000 employees, and 2.9% of the organizations (2) have above 31,000 personnel.

3.1. Variable measurement

To evaluate total eight variables of the ERM, the current study used Saeidi et al. (Citation2019) questionnaire which is based on both scale development work, as well as an existing scale developed by De Zwaan et al. (Citation2011), Collier et al. (Citation2007), and Al-Tamimi and Al-Mazrooei (Citation2007). In Brief, the scale development was according to the main explanations of every component presented by COSO (Citation2004) in the “Enterprise Risk Management-Integrated Framework,” including internal environment, objective settings, event identification, risk assessment, risk response, control activities, information and communication, and monitoring.

The measurement of IC and its dimensions was based on instruments employed by different researches. To evaluate the knowledge of firms, the present study adapted questionnaires of García et al. (Citation2015) and Bontis (Citation1998) by investigating the individual level of specific knowledge regarding their job and organization’s risks. For the measurement of training programs of organizations, this study adopted the questionnaires of Dumas and Hanchane (Citation2010), which focus on the training program of the organization for employees. This study followed Saeidi et al. (Citation2019) and Bergeron et al. (Citation2004), for measuring the technology of organizations by evaluating IT environment scanning, IT acquisition and implementation, and IT planning and control. Moreover, the organizational culture was measured by analyzing internal relationships, cooperation, learning, and knowledge sharing by following Bontis (Citation1998) and Youndt et al. (Citation2004) questionnaires. Furthermore, trust was measured based on the integrity and competence of the organization’s employees, as adopted from Bontis (Citation1998) and McKnight et al. (Citation2002).

The performance of firms was divided into two dimensions: (1) financial performance and (2) non-financial performance, which were measured using the balanced scorecard (BSC) perspectives as well as the competitive advantage. The financial performance was measured by evaluating return on investment (ROI), return on equity (ROE), return on assets (ROA), sale growth, market share growth, return on sales (ROS), and the net profit margin of the firm. For non-financial performance, the present study used customer satisfaction, internal business process, learning and growth (innovation) perspectives, as well as the competitive advantage of organizations. Also, the firm performance was measured by adopting Kaplan and Norton (Citation1996), Blackmon (Citation2008), and Saeidi et al. (Citation2015) measurements, which were based on the operational measurement of firm performance perspectives of BSC. while competitive advantage was measured by using Saeidi et al. (Citation2015).

In addition, this study considered the age and size of the organizations as two control variables which, according to the literature, could affect firm performance, ERM, and IC (Alipour, Citation2012; Beasley et al., Citation2005; Clarke et al., Citation2011; Collier et al., Citation2007; Grace et al., Citation2015; Kleffner et al., Citation2003; Riahi‐Belkaoui, Citation2003). Each control variable was measured with only a single question. In this regard, this study considered the number of years in business and the number of employees as a factor to determine the age and size of organizations (Collier et al., Citation2007; Gates, Citation2006). There exist 39 questions for ERM, 23 questions for IC and 27 questions for firm performance used in the research built on a respondent’s agreement or disagreement on a five-point Likert-scale.

The questionnaire was validated by conducting expert interviews with three academicians related to ERM, three Chief Risk Officers, and two top managers. Moreover, to confirm a clear statement and language, the researchers used two language professionals to review the questionnaire instruments. A pilot study was also done to further improve the instrument. A small sample of institutions was requested to evaluate the questionnaire and report their feedback on the items. Lastly, a self-administration supervision method was used to gather maximum response. From 91organizations, 86 questionnaires were filled-out, whereby 84 were applicable.

4. Data analysis and results

The analysis of the raw data was conducted using SPSS 17 and SmartPls. Researchers have claimed that SEM techniques are more accurate than the first-generation methods in estimating and examining causal relations, particularly in the area of management (Hair et al., Citation2014). This method overcomes the weaknesses of first-generation techniques, which focused only on the analysis of variance, logistic regression, and multiple regression by simultaneously testing the causal relationship between several dependent variables and independent variables (Hair et al., Citation2014).

Consequently, PLS was used to evaluate the causal relations among the latent variables of the complex model of this study. PLS is an association of principal components, path analysis, and regression. PLS offers several advantages. It is particularly appropriate for exploratory studies and model testing with minimum sample size needs (Hair et al., Citation2014). PLS involves a two-stage method. First, to assess the validity and reliability of the instruments, the measurement model is evaluated. Secondly, the structural model for the relationships between the variables is tested.

Before conducting the measurement model, the descriptive statistics of the main variables and Multicollinearity were tested by SPSS 17. shows the number, mean, and standard deviation of the main constructs.

Table 2. Descriptive statistic of main variables.

As illustrated in , almost all variables were at the medium level (assumed mean, i.e., =3); whereby, technology, event identification, control activities, risk assessment, and monitoring were above medium level (i.e.,>3). This indicated that while the mean of four variables of ERM is above medium level (EI, RA, CA, M), the ERM as a whole is at a medium level (2.95). In other words, it shows that Iranian financial institutions are implementing ERM and IC at the average level. Also, among all factors of IC, only technology (i.e., mean: 3.08) is higher than the average level.

Moreover, Multicollinearity was used as an instrument to pre-analyze the data. By running the stepwise regression analysis, the variance inflation factor (VIF) was tested, as shown in . If VIF is above ten, and tolerance is less than 0.1, it expresses the presence of Multicollinearity (Hair et al., Citation2014). Consequently, following the values in , the unavailability of Multicollinearity is confirmed.

Table 3. Multicollinearity results.

4.1. Measurement model

This study evaluated the adequacy of the measurement model through an examination of reliability, discriminant, and convergent validity of all constructs ( and ). Convergent validity shows the verification of the measurement of a construct. A measure has a convergent validity when it is highly correlated with different measures of similar constructs. Convergent validity is supported when the average variance extracted of each construct (AVE) is 0.50 or higher and when each item has a factor loading (Outer Loadings) above 0.70 (Hair et al., Citation2014). shows that the factor loadings of four items (IE4, RA1, INCO3, and ORC2) were below the adequate value (0.7); consequently, those items were removed from the study. The factor loadings of remaining items were between 0.79 and 0.98, indicating that after removing four items, all items had acceptable factor loadings. Therefore, the first condition of convergent validity is confirmed. Moreover, as shown in , the value of AVE higher than 0.5 thresholds support the convergent validity of constructs (between 0.79 and 0.93) (Hair et al., Citation2014).

Table 4. Construct measurements.

The discriminant validity is approved when the AVE of each variable is more significant than the shared variance entre any two variables (the square of their inter-correlations) (Fornell & Larcker, Citation1981). There was no correlation entre any two latent constructs equal to or even higher than the square root AVE of these two constructs (). Moreover, to evaluate discriminant validity, this study examined cross-loading. The items loading values were analyzed to specify whether the indicators have the highest value on their latent construct (see ). The analysis showed that all indicator variables highly loaded on their related latent variables. Thus, this criterion was also fulfilled. Accordingly, discriminant validity was confirmed and affirmed that all constructs in the research model accurately represented distinct concepts and latent variables (Fornell & Larcker, Citation1981; Hair et al., Citation2014).

Table 5. Fornell and Larker’s AVE test.

Finally, Cronbach’s alpha scores and composite reliability (CR) were used to evaluate the reliability of the measures proposed by Hair et al. (Citation2014). According to Sekaran and Bougie (2016), Cronbach’s alpha can adopt as a suitable index of the inter-item consistency reliability of independent and dependent variables. Based on the literature, the reliability scores above 0.7 as the lowest threshold. Moreover, as reported by Hair et al. (Citation2014) minimum value of 0.7 is required for composite reliability. Therefore, following , the reliability of constructs was above the thresholds (0.7). According to the above discussions, all measured model criteria, including the reliability and validity of the instrument and constructs, were confirmed.

4.2. Structural model (hypothesis testing)

In this study, a path-weighting scheme was used to examine all the hypotheses. This test determines the variance of the endogenous variables, as explained by the exogenous variables (Hair et al., Citation2014). Usually, this value is recognized as R square (R2), which ranges between 0 and 1 (Hair et al., Citation2014). For evaluation, the statistical significance of the path estimates (t-value), the bootstrapping method with 250 resamples, was utilized. Also, a direct effects model (without the moderators) was initially examined, followed by interaction models (with the moderators) to check whether considering the moderators improved the explanatory power of the model. presents the results of the structural model for both a direct effect and moderator models.

Table 6. Hypothesis testing.

Analyzing the measurement model facilitated testing each of the proposed hypotheses. There are two direct effects, ERM effects on non-financial and financial performance. The results indicated that all direct hypotheses are supported. In other terms, ERM has a significant positive effect on both financial and non-financial performance (β = 0.542, p < 0.001, t value = 6.09; β = 0.550, p < 0.001, t value = 6.387).

Regarding indirect relationships (moderators), the analyses indicated that the moderating effect of knowledge and technology on the relationship between ERM and both financial and non-financial are significant (financial: β = 0.185, p < 0.05, t value= 2.464; β = 0.177, p < 0.05, t value= 2.382; non-financial: β = 0.167, p < 0.05, t value= 2.196; β = 0.100, p < 0.05, t value= 1.995). Specifically, knowledge as a moderator increased the variance explained (R2) in company financial and non-financial performance from 29.4% and 30.2% in the direct structural model to 41.8% and 43.6% in the moderating effect model, respectively. Likewise, technology as a moderator increased the variance to 39.3% and 41.6%, indicating that the coefficient value of ERM increased as the level of knowledge and technology increased. However, the result indicated that training does not have any moderation effect between ERM and firm financial performance, and between ERM and non-financial performance (β = 0.063, t value= 1.139; β=-0.072, t value= 1.333), which is similar to the effect of organizational culture and trust on the relationship between both ERM and financial and non-financial performance (organizational culture: β = 0.124, t value= 1.932; β = 0.109, t value = 1.435; trust: β=-0.053, t value= 0.822, β=-0.041, t value= 0.648).

Based on the analyses in , the moderating effect of the IC as a whole on the relationship between ERM and firm financial performance was significant (β = 0.340, p < 0.001, t value= 4.452). The moderator increased the variance explained (R2) in firm financial performance from 29.4% in the direct structural model to 48.8% in the IC moderating effects model. Specifically, IC had a positive effect on the relationship between ERM and firm financial performance. The positive sign indicated that the value of the coefficient of ERM in explaining firm financial performance increased as the level of IC increased. In contrast, the moderating role of aggregated IC on the relationship between ERM and firm non-financial performance was not significant and requires further investigation (β=-0.128, t value= 1.934).

Additionally, the change in R2 value (ΔRsq) was examined to measure the contribution of the interaction terms. To verify the significance of the change in the R2 or to examine the effect size or significance of ΔRsq, Cohen’s was calculated.

(1)

(1)

If Cohen’s is 0.02, the moderating effect is considered small, while 0.15 is medium, and 0.35 is a significant value (Cohen, Citation1988). The

values of influential moderators are shown in . Based on the result of the Cohen’s

formula, the effect size of the IC as a whole on ERM and financial performance with the value of 0.378 has a strong effect size. Among IC factors, knowledge with a value of 0.213 and 0.237 has almost a medium effect on both financial and non-financial performance. Technology, with values of 0.163 and 0.195, is in second place.

It should be noted that the analysis of control variables did not show any significant difference between different groups of age and size in terms of other variables. The findings suggest that Iranian financial institutions should be aware that the positive effects of ERM on firm performance and the moderation effect of IC do not depend on the age and size of firms. In other words, all organizations (i.e., new, young, or old, with the low or high number of employees) may enjoy of ERM and IC benefits.

5. Discussion

The first aim of this study attempted to evaluate the relationship between ERM and both firm non-financial and financial performance. The result of empirical analyses of data showed that there is not only a positive and significant effect between ERM and firm financial performance but also the relationship between ERM and non-financial performance is positive and significant. These findings are consistent with Tsai et al. (Citation2017), Grace et al. (Citation2015), Florio and Leoni (Citation2017), Farrell and Gallagher (Citation2019), Silva et al. (Citation2019), Iswajuni et al. (Citation2018), Chen et al. (Citation2019), Hanggraeni et al. (Citation2019), where ERM showed a positive and significant effect on firm financial performance. However, the current finding is also incompatible with McShane et al. (Citation2011), Pagach and Warr (Citation2010), and Tahir and Razali (Citation2011), Li et al. (Citation2014), who observed no additional increase in performance of organizations implementing ERM as their risk management system.

As mentioned in the literature, ERM is a holistic technique, and it is related to all organizations’ activities (COSO, Citation2004). It makes integration among different risk management practices (Beasley et al., Citation2008). therefore, it has to affect total parts of performance in an organization, not only financial. In other words, it considers all risks in all sections of the organization, as well as the residual risks and potential effects of each hazard on other sections and activities of firms (Beasley et al., Citation2008). Consequently, the firms are able to properly manage their risk related to all sectors; thus, bringing many advantages to the firm such as increasing the trust of customers, improving internal business process, innovation of organization, and obtaining higher competitive advantage. Thus, the effect of ERM on non-financial performance by evaluating BSC perspectives shed new light on the role of ERM on overall performance in organizations.

This result also is in consists of agency theory, which mentioned all the activities of organizations should increase the shareholder value. In this regard, the implementation of a robust risk management system such as ERM could increase overall firm performance and, consequently, shareholder value. ERM enables risk management to be part of the company’s total approach and allows firms to adjust risk decisions that maximize shareholder value properly. It also supports the RBV theory by controlling the risks from all avenue of the organization, especially hazards that are related to resources. It could help to reduce the resource allocation risk and to utilize resources such as capital resources. Moreover, the ERM system can be known as strategic assets that can create long term competitive advantage and superior financial performance.

In terms of the effect of the moderation variables, these findings indicated that knowledge has a positive and significant moderation effect on the relationship between ERM and both non-financial and firm financial performance. Briefly, when the people in organizations have high knowledge and awareness, they can be more useful in improving ERM systems. Knowledge and awareness of employees toward events and risk, as well as their role and responsibility in the organization’s plan, are critically important for managing risk (Burnaby & Hass, Citation2009; COSO, Citation2004; Oliveira et al., Citation2019; Yaraghi & Langhe, Citation2011). In other words, companies that have people who genuinely have adequate knowledge regarding their job, their role, responsibilities, and entities’ objectives could reduce the risks of the human actions of the organization (COSO, Citation2004). Moreover, employees who are more aware of potential risks, organization situation and plans, events, and uncertainty are more likely to show a better reaction to risks and opportunities (Carey, Citation2001). The awareness of risk at the early stage with the help of awareness employees ultimately leads to the adoption of best practices. These firms can recognize the potential opportunities, as well as risks, better than other organizations that do not establish the ERM system. Consequently, by utilizing and improving knowledge in the organization, the effect of the ERM system on firm performance could be increased.

The results further showed that, in contrast to theoretical literature, which confirms the positive effect of training on improving the influence of ERM on firm performance, it has no moderating effect on ERM-financial performance and ERM-non-financial performance links. The reason behind this surprising result might be the current training practices among Iranian financial institutions. On the one hand, lack of appropriate goal-oriented programs, lack of sufficient motivation to learn among the employees of the organization, disconformity between contents of training, and employee’s needs for training could be identified as the reasons of inefficiency in training programs in the financial institutions in Iran (Baradaran et al., Citation2015). On the other hand, it can be due to not delegating the right tasks to the right people. However, this result should be interpreted with caution because this result changes and goes towards significant effects by considering more sample size or in other countries.

Furthermore, this study, as expected, supports the moderation effect of IT on both ERM- non-financial and financial performance. Specifically, by increasing and improving technology, organizations may increase the influence of ERM on firm performance. According to Rolland (Citation2008), IT can generate a relevant connection between risk management and business performance by offering data gathering and data storage in a secure manner, which is fundamental to decision making. Moreover, it could be an excellent tool for analyzing, modeling, monitoring, and controlling risks (Rolland, Citation2008). Different IT aspects would result in strengthening ERM function, its efficiency, effectiveness, and its effect on competitive advantage in the organization (Saeidi et al., Citation2019). For example, with appropriate use, IT environmental scanning companies can better recognize threats and opportunities facing their business. In this way, IT can help the ERM system to obtain information about different internal and external forces such as the appearance of new competitors, new technologies, changes in customer preferences, changes in the economic environment, political and regulations, which help to have a rapid reaction to all environment pressure compare to competitors. Furthermore, with more information which can be acquired through IT environmental scanning, ERM system can help the organization to have a better and faster reaction to the environmental changes to have a superior position in the market compared to their competitors. Therefore, by improving information technology, organizations could better manage their risks and opportunities, which would consequently increase firm performance.

Followed by IT, the effect of organizational culture on ERM-firm performance, financially and non-financially, was evaluated. Interestingly, the results of data analyses showed that organizational culture does not have any significant effect on ERM-firm performance relationships among Iranian financial institutions. As stated by Oliveira et al. (Citation2019), awareness and risk culture must permeate in all levels of the organization in a way that the decision-making process has risk awareness as a component. In this regard, some reasons may cause this unanticipated result. Monavarian and Tonekaboni (2012) stated that the organizational culture among financial institutions of Iran has suffered from poor internal relationships, unmotivated employees, innovation, and learning.

Moreover, some managers still have a traditional ideology in their structure, which makes employees work under a regime of fear. In this ideology, people in organizations do not consider themselves as part of the organization. Employees thought that they are not adequately involved in decision-making. Likewise, they believe that they do not have enough authority to perform their job and duties. Overall, the organizations do not have internal homogeneity. Hence, they cannot easily cope with external changes and hazards (Monavarian & Ahmadi-Tonekaboni, Citation2012; Mousavi et al., Citation2015).

Besides, this study revealed that trust does not have a moderation effect on the association between ERM and non-financial and financial performance. This inconsistency may be due to the culture of financial institutions of Iran. Organizational culture is creating and extending trust among employees inside the institutions. In other words, organizational culture is the source of trust in all organizations, and it is affected by managers’ actions. Therefore, the improper organizational culture of the financial institutions of Iran could be seen as a significant obstacle to improve organizational trust.

Finally, the aggregated IC was evaluated as a mediator on the ERM and both financially and non-financially firm performance relationship. The result of the analyses indicated that the relationship between ERM and firm financial performance is moderated by IC and its components. This positive effect indicates that the effect of ERM on financial performance will growth as the IC level increases. Moreover, this result supported the critical role of IC in the firms’ financial performance, especially when it improves the effectiveness and success of the risk management system in organizations. Unlike the traditional economy, intangible assets (i.e., IC and its components) are involved in all activities and processes of the organizations (Bontis et al., Citation2000), where risk management is not an exception. Sensing and responding to risks in a firm and enhancing organizational performance considerably depends on corporate IC (Neef, Citation2005). Based on the statement of COSO (Citation2004), risk management is conducted by employees and people in the organization.

Moreover, it is extended by the use of other intangible factors such as technology, training, organizational culture, and trust (Neef, Citation2005; Yaraghi & Langhe, Citation2011). Therefore, organizations are trying to improve the use of intangible assets because of their different effects on different aspects of organizations, such as improving the effect of ERM on firm performance. The study did not support any moderation effect of overall IC on the relationship between ERM and non-financial firm performance. The reason for these findings might be the current Iranian financial institutions’ practice, where the IC and ERM are more applied to fulfill the financial objectives of organizations. Hence, the first objective of financial institutions is to increase the shareholders’ value; therefore, it seems logical that these organizations pay more attention to the economic aspects of the performance. However, the effect of non-financial performance on financial aspects of organizations’ performance should not be neglected.

It is important to highlight that among all influential dimensions of IC, knowledge showed the greatest influence on ERM-firm financial performance relationships followed by technology, which is similar to the relationship between ERM and non-financial performance.

6. Conclusion

This study developed a model to explore the moderation role of IC and its components on the relationship between ERM and firm financial and non-financial performance. This study empirically supported the contingency theory system approach. Contrary to previous studies merely focusing on the bivariate relationship between ERM and firm performance, this investigation confirmed intangible factors and intangible assets as moderators in this link. Since limited research is available in measuring intangible assets and intellectual capital’s factors in the field of ERM, these findings shed additional light on identifying intangible factors in the risk management area. These results further support the agency theory to demonstrate the link between ERM and firm performance, because ERM would eventually protect and increase shareholders’ interest, and this reflects superior performance. Moreover, regarding the direct effect of ERM on both financial and non-financial performance, it could be confirmed that the RBV theory can be used as another foundation in ERM researches, whereby ERM could be recognized as a strategic asset leading to higher firm performance. In other words, not all financial institutions of Iran are using ERM as their risk management system. Thus, ERM as a strategic asset (i.e., which is rare, unique, not duplicable, and not salable) could be a good strategy for those organizations using ERM to obtain a competitive advantage and increase firm performance.

The findings of this study have several implications. Although most past studies were conducted in developed countries, this study was done in a developing country (Iran); thus, providing a comprehensive overall view of ERM within Iranian financial institutions. This investigation is among the first ERM studies endeavors in Iran. This study revealed that nearly half (49.7%) of the financial institutions in Iran are aware of ERM, and they are implementing ERM as their risk management system. However, the result could not be specific just to Iran. Our analysis provided a starting point for additional research into ERM in emerging markets in Asia. In emerging countries, due to variations in financial systems and financial regulations, ERM has different impacts between emerging and developed countries.

The findings provided a better realizing of the role of ERM on firm performance and the underlying concept and nature of ERM. In addition, the findings also provided evidence that from a broad perspective, ERM could affect not only financial performance but also non-financial aspects such as internal business process, customer satisfaction, learning, growth, and competitive advantage. This is consistent with Acharyya and Mutenga (Citation2013), Beasley et al. (Citation2005), COSO (Citation2004), who stated that ERM, as a system, should affect all aspects of organizational performance. Besides, the significant moderating effect on the relationship between ERM and financial performance is somehow sending a signal that this relationship is not solely a direct link. Undoubtedly, these results prove that there is great possibility that the interrelation of ERM and performance may be influenced by the other functions of the organization as moderating factors.

The results of this study also have deep implications for practitioners and top managers of organizations to focus on building up a robust risk management system (ERM) for enhancing overall firm performance both financially and non-financially. Moreover, the competition among the financial industry of Iran is considered aggressive. The institutions that can control, manage challenges and risks by the use of a holistic risk management approach are more successful. These findings might motivate the financial institutions’ managers to increase their understanding of the ERM system’s concept and its potential contribution to their firms’ performance. Financial institutions’ managers need to enhance their ability to create, implement, and develop new holistic risk management methods to increase the performance of their institutions not only financially but also non-financially.

Moreover, this study revealed that in every organization, IC is an important intangible asset at different levels. The findings of the current study increase the intuition of financial institutions’ managers to identify important intangible factors in improving risk management systems. This study highlighted the importance of IC, especially knowledge and technology, to boost the effect of ERM on firm performance. Therefore, managers of organizations can consider utilizing IC as an instrument due to their positive effect on the improvement of the ERM system. The managers must know that increasing IC and its dimensions’ level could be considered as a long term strategy that directly or indirectly leads to higher firm performance.

Furthermore, these findings will be valuable for policymakers, regulators, and planners, particularly the central insurance and central bank of Iran, to emphasis the significance of planning developed ERM as organizational control instrument to meet the uncertainties and challenges in the environment accruing from the deregulation, globalization, market competition, and rapid technological changes. In addition, they can motivate organizations to increase their level of IC to have a better risk management system and firm performance. In general terms, this study could be a point of reference for academic researchers regarding the effect of intangible assets on ERM.

These results are subjected to several limitations. First, the generalizability of these results is subjected to certain limitations. The financial institutions of Iran selected as the sample firms, their features, practices, and regulations may not be representative of all other companies and other industries of Iran. Moreover, as all the financial institutions of Iran are Islamic, there is a probability that the result of this study may have been different in non-Islamic banks and institutions in other countries. Second, while IC, as an intangible asset, includes many dimensions and factors, this study only considered foundation, important, and relevant dimensions of IC components. By considering and measuring more components and dimensions of IC, the result could be more comprehensive and valuable. Finally, this study did not attempt to make a comparison between companies that has and has not implemented ERM. Hence, a comparative study could assist in properly analyze the actual effects of ERM on firm performance.

Based on these limitations, there are some opportunities for future research by extending this study in several ways. First, the wider scope of the survey, considering different industries or all companies listed in the Tehran stock exchange, could help to achieve a comprehensive view and extend the generalizability of the study in Iran. Moreover, more research is required in Islamic and non-Islamic banks of other countries to establish whether the influence of IC on ERM and its relationship with the performance of the organization is universal. Second, to extend IC variables and evaluate the effect of other dimensions of IC components (such as employee commitment, experience, innovativeness, and business ethics, and so on) on ERM and its impact on firm performance, represent a crucial research opportunity. It would help the managers, organizations, and researchers to achieve a more comprehensive view regarding the influence of intangible assets on risk management in organizations.

Furthermore, a comparative analysis between those organizations implementing the ERM and using the traditional silo-based approach of risk management would be highly informative by offering a perspective of the possible benefits of ERM and the weaknesses and limitations of silo-based methods of risk management. Lastly, based on the framework of the current study, it is recommended future works recognize and investigate other factors (intangible and tangible) that could affect the interaction between ERM and firm performance employing both moderating and mediating factors (such as corporate governance, innovation, internal audit function) to extend the interaction model in the ERM field.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Acharyya, M., & Mutenga, S. (2013). The benefits of implementing enterprise risk management: Evidence from the non-life insurance industry. Enterprise Risk Management, 6(1), 22–24.

- Afzali, S. M. M. (2011). Iran’s Vision1404.

- Ai, J., Bajtelsmit, V., & Wang, T. (2018). The combined effect of enterprise risk management and diversification on property and casualty insurer performance. Journal of Risk and Insurance, 85(2), 513–543. https://onlinelibrary.wiley.com/doi/abs/10.1111/jori.12166

- Alipour, M. (2012). The effect of intellectual capital on firm performance: An investigation of Iran Insurance Companies. Measuring Business Excellence, 16(1), 53–66. https://doi.org/https://doi.org/10.1108/13683041211204671

- Al-Tamimi, H. A. H., & Mazrooei, F. M. 2007. Banks' risk management: a comparison study of UAE national and foreign banks. The Journal of Risk Finance Incorporating Balance Sheet, 8(4), 394–409.

- Amini, A. (2015). Legalizing financial institutes, vital for ending recession. Iran Daily Online Journal.

- Arena, M., Arnaboldi, M., & Azzone, G. (2010). The organizational dynamics of enterprise risk management. Accounting, Organizations and Society, 35(7), 659–675. http://www.sciencedirect.com/science/article/pii/S0361368210000565

- Baradaran, S., Rashidi, M. M., & Sahra, S. (2015). Comparative evaluation of training and development of the Personnel in Tejarat Bank and Hekmat Iranian Bank. Indian Journal of Fundamental and Applied Life Sciences, 5(1), 4507–4513.

- Beasley, M. S., Clune, R., & Hermanson, D. R. (2005). Enterprise risk management: An empirical analysis of factors associated with the extent of implementation. Journal of Accounting and Public Policy, 24(6), 521–531. http://www.sciencedirect.com/science/article/pii/S0278425405000566

- Beasley, M., Pagach, D., & Warr, R. (2008). Information conveyed in hiring announcements of senior executives overseeing enterprise-wide risk management processes. Journal of Accounting, Auditing & Finance, 23(3), 311–332. https://doi.org/https://doi.org/10.1177/0148558X0802300303

- Bergeron, F., Raymond, L., & Rivard, S. (2004). Ideal patterns of strategic alignment and business performance. Information & Management, 41(8), 1003–1020. https://doi.org/https://doi.org/10.1016/j.im.2003.10.004

- Bertinetti, G. S., Cavezzali, E., & Gardenal, G. (2013). The effect of the enterprise risk management implementation on the firm value of European companies (Working Paper(10)). Department of Management, Università Ca'Foscari Venezia.

- Blackmon, V. Y. (2008). Strategic planning and organizational performance: An investigation using the balanced scorecard in non-profit organizations. Capella University.

- Bontis, N. (1998). Intellectual capital: An exploratory study that develops measures and models. Management Decision, 36(2), 63–76. https://doi.org/https://doi.org/10.1108/00251749810204142

- Bontis, N., Chua Chong Keow, W., & Richardson, S. (2000). Intellectual capital and business performance in Malaysian industries. Journal of Intellectual Capital, 1(1), 85–100. https://doi.org/https://doi.org/10.1108/14691930010324188

- Bourque, L. B., & Fielder, E. P. (2003). How to conduct self-administered and mail surveys. https://methods.sagepub.com/book/how-to-conduct-self-administered-and-mail-surveys

- Burnaby, P., & Hass, S. (2009). Ten steps to enterprise-wide risk management. Corporate Governance: The International Journal of Business in Society, 9(5), 539–550. https://doi.org/https://doi.org/10.1108/14720700910998111

- Cabrita, M. d R. d M., Vaz, J. L., & Bontis, N. (2007). Modelling the creation of value from intellectual capital: A Portuguese banking perspective. International Journal of Knowledge and Learning, 3(2–3), 266–280. https://doi.org/https://doi.org/10.1504/IJKL.2007.015555

- Carey, A. (2001). Effective risk management in financial institutions: The turnbull approach. Balance Sheet, 9(3), 24–27. https://doi.org/https://doi.org/10.1108/09657960110696014

- Chen, Y.-L., Chuang, Y.-W., Huang, H.-G., & Shih, J.-Y. (2019). The value of implementing enterprise risk management: Evidence from Taiwan’s financial industry. The North American Journal of Economics and Finance, 100926. http://www.sciencedirect.com/science/article/pii/S1062940818303000

- Chenhall, R. (2003). Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organizations and Society, 28(2–3), 127–168. https://doi.org/https://doi.org/10.1016/S0361-3682(01)00027-7

- Clarke, M., Seng, D., & Whiting Rosalind, H. (2011). Intellectual capital and firm performance in Australia. Journal of Intellectual Capital, 12(4), 505–530. https://doi.org/https://doi.org/10.1108/14691931111181706

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences. Academic Press.

- Collier, P., Berry, A., & Burke, G. (2007). Risk and management accounting: Best practice guidelines for enterprise-wide internal control procedures. CIMA.

- COSO. (2004). Enterprise risk management – Integrated framework executive summary & framework, committee of sponsoring organizations of the treadway commission. The Committee of Sponsoring Organizations of the Treadway Commission (COSO). https://www.coso.org/Pages/default.aspx.

- De Zwaan, L., Stewart, J., & Subramaniam, N. (2011). Internal audit involvement in enterprise risk management. Managerial Auditing Journal, 26(7), 586–604. https://doi.org/https://doi.org/10.1108/02686901111151323

- Dumas, A., & Hanchane, S. (2010). How does job‐training increase firm performance? The case of Morocco. International Journal of Manpower, 31(5), 585–602. https://doi.org/https://doi.org/10.1108/01437721011066371

- Earle, T. C., Siegrist, M., & Gutscher, H. (2010). Trust in risk management: Uncertainty and scepticism in the public mind. Earthscan.

- Eckles, D. L., Hoyt, R. E., & Miller, S. M. (2014). Reprint of: The impact of enterprise risk management on the marginal cost of reducing risk: Evidence from the insurance industry. Journal of Banking & Finance, 49, 409–423. https://doi.org/https://doi.org/10.1016/j.jbankfin.2014.10.006

- Edvinsson, L., & Malone, M. S. (1997). Intellectual capital: Realizing your company’s true value by finding its hidden brainpower. HarperCollins.

- Farrell, M., & Gallagher, R. (2015). The valuation implications of enterprise risk management maturity. Journal of Risk and Insurance, 82(3), 625–657. https://onlinelibrary.wiley.com/doi/abs/10.1111/jori.12035

- Farrell, M., & Gallagher, R. (2019). Moderating influences on the ERM maturity-performance relationship. Research in International Business and Finance, 47, 616–628. http://www.sciencedirect.com/science/article/pii/S0275531918304136

- Florio, C., & Leoni, G. (2017). Enterprise risk management and firm performance: The Italian case. The British Accounting Review, 49(1), 56–74. http://www.sciencedirect.com/science/article/pii/S0890838916300221

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. http://www.jstor.org/stable/3151312

- García, V., Marqués, A. I., & Sánchez, J. S. (2015). An insight into the experimental design for credit risk and corporate bankruptcy prediction systems. Journal of Intelligent Information Systems, 44(1), 159–189. https://doi.org/https://doi.org/10.1007/s10844-014-0333-4

- Gates, S. (2006). Incorporating strategic risk into enterprise risk management: A survey of current corporate practice. Journal of Applied Corporate Finance, 18(4), 81–90. https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1745-6622.2006.00114.x

- Gates, S., Nicolas, J.-L., & Walker, P. L. (2012). Enterprise risk management: A process for enhanced management and improved performance. Management Accounting Quarterly, 13(3), 28–38.