?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article investigates the dynamic relationship among competition, diversification and bank performance using data for 18 countries with a dual banking system over the period 2000 to 2016. Analyses using panel vector autoregression (P.V.A.R.) model, impulse response function (I.R.F.) and variance decomposition (V.D.C.) methods confirm that market power increases the profitability and the stability of banks the dual banking system while revenue diversification reduces them. Market power increases revenue diversification of banks. Segregating the sample of banks into emerging and developing countries, we find that positive impact of market power on profitability is stronger for emerging countries. Even though we find that revenue diversification has a more damaging effect on the profitability of banks in the developing countries, it only dampens the stability of banks in emerging countries. In addition, we find that asset diversification dampens the stability of banks. However, it has a more positive impact on the profitability of banks in emerging economies.

1. Introduction

Empirical evidence from advanced and developing economies shows that competition in the banking sector influences banks’ diversification strategies. Banks diversify their revenue by venturing into new business activities such as brokerage, trading securities, investment banking and other financial activities. Diversification enables banks to offer products that are not perfectly correlated, thereby reducing portfolio risk. However, competitive pressure may encourage banks to venture into risky activities. Banks’ exposure to non-interest income has been linked to bank fragility in the U.S. during the global financial crisis (DeYoung & Torna, Citation2013). This has brought about renewed interest in the relationship among competition, diversification and bank performance. Even though competition has an impact on banks performance, it is unclear how this effect is transmitted, or how diversification is affected as a result. In this context, understanding how competition affects diversification and bank performance is of great relevance.

The nature of competition, diversification and bank performance is different in a dual banking system where Islamic banks co-exist with the conventional ones. Islamic banks aim to promote social well-being through a justified distribution of wealth and income. They differ from conventional banks in terms of their requirement in complying with Sharia guidelines. Transactions involving elements of interest (riba), uncertainty (gharar), excessive risk (maysir) and unlawfulness under the Islamic faith (haram) are prohibited under Islamic banking. This influences the sources and uses of their funds. As a result, their exposure to risk differs from conventional banks and this has a bearing on their performance. Over the years, Islamic banking has expanded rapidly, growing from a total asset of US$820 billion in 2013 to US$1.56 trillion in 2018 (IFSB 2015, 2018). The expansion of Islamic banks has intensified competition in the dual banking system.

Islamic banks not only compete among them, but they also compete with their conventional counterparts. Competition in the dual banking system has a bearing on bank performance as shown by Alam et al. (Citation2019), Ariss (Citation2010a), González et al. (Citation2017) and Kabir and Worthington (Citation2017). In line with the developments in the banking sector, Islamic banks have also embarked upon greater non-financing related activities to enhance their earning base. Studies by Abedifar et al. (Citation2018), Abuzayed et al. (Citation2018), Chen et al. (Citation2018) and Molyneux and Yip (Citation2013) confirm that diversification influences the performance of banks in the dual banking system. In addition, Amidu and Wolfe (Citation2013) find that the relationship between bank competition and stability in emerging and developing economies is influenced by banks’ diversification strategies. A similar finding is observed by Nguyen et al. (Citation2012) in the case of four South Asian countries.

In line with the existing literature, this study aims to further explore the link among competition, diversification and bank performance. In doing so, this study will contribute to the literature in the following ways. Firstly, we will analyse the relationship among the three variables in countries with the dual banking system. This is pertinent given the different nature of competition, diversification and bank performance in a dual banking system. Secondly, we will use a different methodology compared previous studies in order to see how shock in one variable will influence the other variables. Lastly, we will further differentiate the interconnections among the three variables by segregating the sample of countries into emerging and developing. This will enable us to see if economic development influences the nature of the relation among the variables studied. Our findings confirm the positive relationship between market power and bank performance. In addition, we find that market power raises revenue diversification. Further analyses by segregating the sample into emerging and developing countries show that market power explains the higher percentage of variation in banks’ profitability in emerging countries while revenue diversification explains the higher percentage of variation in banks’ profitability in developing countries. Meanwhile, we find that greater asset diversification worsens the stability of banks in the dual banking system. However, it improves the profitability of banks in emerging economies.

The rest of the article is structured as follows. Section 2 focuses on the review of literature. Section 3 describes the methodology. Section 4 details the results while section 5 discusses the results and concludes.

2. Literature review

Existing literature has dwelled on the topic of competition, diversification and bank performance in a number of ways. One strand of literature looks at the relationship between competition and bank performance. Two opposing views exist with regard to this; one supports the ‘competition-stability nexus’ while the other supports the ‘competition-fragility’ nexus. The latter is based on the premise that greater market power is linked to cost inefficiencies, lower franchise value and higher risk taking (Ariss, Citation2010b; Berger & Hannan, Citation1998; De Nicolo, Citation2000). The former is based on the premise that greater market power enables banks to earn monopolistic profits, achieve greater efficiency and enhance revenue diversification (Amidu & Wolfe, Citation2013; Keeley, Citation1990; De Nicoló et al., Citation2006). In addition, existing theories have also linked market structure to banks profitability (Berger, Citation1995; Berger & Hannan, Citation1989; Hamid, Citation2017; Mirzaei et al., Citation2013). The Efficient Structure Hypothesis (E.S.H.) postulates that banks with higher efficiency are able to raise their market share and size and earn higher profits as a result, while the S.C.P. hypothesis asserts that collusive behaviour of firms enables them to earn monopolistic profits by charging a less favourable price to customers in a highly concentrated market. Alternatively, the R.M.P. hypothesis postulates that firms’ ability to charge higher prices and earn more income are derived from their large market share and ability to offer distinctive products.

Empirical evidence on the relationship between competition bank performance is mixed. Hamid (Citation2017) observes a positive relationship between competition and profitability for banks in A.S.E.A.N.-5 countries. Hsieh and Lee (Citation2010) finds that more concentrated markets (or less competitive markets) is more profitable using a sample of banks in 61 countries over the period 1992 to 2006. However, Perera et al. (Citation2013) finds that competition reduces bank profitability in South Asian countries. A similar observation is noticed by Tan (Citation2016) for commercial banks in China over the period 2003 to 2011. Additionally, Vardar (Citation2015) finds that competition has a negative impact on the financial fragility of Turkish banks. Leroy and Lucotte (Citation2017) finds that competition increases banks’ riskiness and fragility of banks in Europe over the period 2004 to 2013. Hamid (Citation2017) observes similar findings for A.S.E.A.N. banks. Alam et al. (Citation2019); Kabir and Worthington (Citation2017) and Risfandy et al. (Citation2018) find that competition raises the fragility of banks in a dual banking system. However, Fu et al. (2014) finds that competition makes the banking system in 14 Asia Pacific economies more stable.

Another strand of literature studies the link between competition and diversification. The ‘quiet life’ theory proposed by Berger and Hannan (Citation1998) asserts that managers will have lower incentive to venture into revenue diversification when the market power is high given that they are already earning sufficient profit by charging higher prices. Meanwhile, empirical evidence in the U.S., Europe and emerging market show that higher competition in the banking sector encourages banks to diversify their revenue (Amidu & Wolfe, Citation2013; Deyoung & Rice, Citation2004; Lepetit et al., Citation2008; Perera et al., Citation2013). Nevertheless diversification has also enabled banks to expand their revenue and obtain higher market power (Carbó Valverde & Rodríguez Fernández, Citation2007). In particular, they find that banks in Europe were able to obtain higher market power during the 1994 to 2001 period as a result of their diversification. This happens because revenue from non-traditional activities compensated for lower revenue from traditional lending activities that happened as a result of higher competition.

Additionally, existing literature has also established the theoretical link between diversification strategy and banks’ performance. One strand of literature argues that the banks’ role as a delegated monitor under the traditional banking theory may cause the diversification strategy to reduce return and improve efficiency (Acharya et al., Citation2006). The latter may happen due to economies of scope, while the former may happen due to lower cyclicality associated with non-interest income and weak correlation between the riskiness of activities that generates interest income and non-interest income. Meanwhile, the other strand of literature argues that diversification may dampen the comparative advantage of management, increase agency problem, increase the volatility of earnings and increase default risk (Deyoung & Roland, Citation2001; Mostak Ahamed, Citation2017; Saghi-Zedek, Citation2016). Empirical findings on the relationship between diversification and bank performance are also mixed. A positive relationship between diversification and bank performance has been observed in banks in Europe (Köhler, Citation2015; Mercieca et al., Citation2007); Italy (Chiorazzo et al., Citation2008); Japan (Sawada, Citation2013) and the U.S. (Shim, Citation2013). Nevertheless, Berger et al. (Citation2010) find that diversification reduces profitability and increases the riskiness of banks in Russia. Similarly, Zhou (Citation2014) and Williams (Citation2016) find that diversification increases the riskiness of banks in Vietnam and Australia.

Studies that have focused on a dual banking system also provide mixed results with regard to the relationship between diversification and bank performance. Grassa (Citation2012) analyses on the relationship between revenue diversification and risks using a sample of 42 Islamic banks from the Gulf Cooperation Council (G.C.C.) countries show that higher dependence on the income share of the profit-loss-sharing products is linked to greater bank riskiness. Molyneux and Yip (Citation2013) finds that greater reliance on non-interest incomes reduces risk adjusted return in a dual banking system based on their analyses on banks in Malaysia, Saudi Arabia, Kuwait, United Arab Emirates, Bahrain and Qatar during 1997 to 2009. Chen et al. (Citation2018) finds that asset diversification lowers the profitability of conventional banks but only has a limited effect on that of Islamic banks. Abuzayed et al. (Citation2018) find that revenue and asset diversification do not make banks in G.C.C. countries more stable. However, highly diversified banks are able to reduce risk, suggesting a non-linear relationship between both variables.

Existing literature also establishes the link among competition, diversification and bank performance. Competition can impact the performance of banks through their diversification strategies. Amidu and Wolfe (Citation2013) analysed the endogenous relationship among competition, diversification and bank performance for commercial banks, cooperative banks, development banks, savings banks, real estate and mortgage banks in 55 emerging and developing countries over the 2000 to 2007 period. Using the three-stage-least-squares (3.S.L.S.) simultaneous equation model, they find that competition is linked to greater bank stability and this happens because of banks’ diversification strategy. Their findings imply that competition pressurises banks to adopt different diversification strategies and this decision affects banks’ insolvency risk. Whereas, Nguyen et al. (Citation2012) investigates the effect of interaction between competition and revenue diversification on bank stability for four South Asian countries during 1998 to 2008 period using Generalised Methods of Moments (G.M.M.) estimations. Their findings show that market power dampens diversification but raises stability.

To date, studies that have analysed the relationship among competition, diversification and performance have only focused on conventional banks. Implications derived from existing studies may not be applicable in countries where conventional banks operate alongside Islamic ones. Hence, this study will fill the gap in the literature by analysing the relationship among the three variables in a dual banking system. In addition, existing studies have used panel data regression in analysing the relationship among the three variables. This study will add to the literature by using the panel vector autoregression (P.V.A.R.) approach that not only accounts for endogeneity but also enables us to see how the shock of one variable affects the other variable in future periods.

3. Measurement

In this section, we describe the measurement of competition, diversification and bank performance stability variables.

3.1. Competition measure

3.1.1. Lerner Index

We use the Lerner Index as a tool to measure competition for the sample. This index measures the extent of market power by estimating the mark-up of price over marginal cost. Bank level data is used to measure the following:

where

is the price of total assets for bank i at time t measured using the ratio total revenue (interest and non-interest income) to total assets.

is the marginal cost of producing an additional unit of output. The translog cost function will be estimated as the following linear regression:

where

denote the total costs of the bank that includes both financing and operating cost.

denotes the output of the bank measured as total assets. W1, W2 and W3 denote the input of the banks which includes price of deposit funds, labour and capital which are calculated respectively as the ratio of interest expenses to total deposits and money market funds, labour cost to total assets, and other operating expenses to total assets. In line with the literature, symmetry and linear homogeneity restrictions are imposed by dividing the total costs and the prices of all inputs by one of the factor prices, in this case, the price of labour (Kabir & Worthington, Citation2017):

The cost function is estimated separately using panel data for each country in the sample. This allows for the parameters of the cost function to vary from one country to another, reflecting different technologies. Year fixed effects are included with bank-specific robust standard error.

After estimating the cost function, marginal cost is calculated by taking the first derivative with respect to the output for each bank in the sample. Hence, the marginal cost is calculated for each bank as:

The average value of Lerner Index over time is included in the regression for each bank i. The value of Lerner Index near zero describes perfect competition while the value near one describes strong market power.

3.2. Bank diversification measures

In line with the existing literature, we study the impact of diversification on the performance (risk and profitability) of banks. Two types of bank diversification analysed in this study are revenue and asset diversification.

3.2.1. Revenue diversification

Operating income of a conventional bank are divided into interest and non-interest income, whereas that of Islamic banks are divided into financing and non-financing income. In line with Abuzayed et al. (Citation2018), financing income in Islamic banking is obtained from deposit/lending activities while non-financing income is obtained from fees charged on services, trading and gains from the investment in real estate, equity or other sharia compliant investments. Revenue diversification happens when banks earn a higher percentage of their income from non-interest or non-financing activities. In measuring a bank’s revenue diversification, we method similar to Abuzayed et al. (Citation2018); Elsas et al. (Citation2010); Molyneux and Yip (Citation2013); Sanya and Wolfe (Citation2011). This method is adopted by Stiroh (Citation2006) from the modern portfolio theory framework.

The simple equation from which the income diversification measure is derived is as the following:

where

represents share of net interest income (squared) and

epresents share of non-interest income (squared). A higher value of Revenue Diversification is associated with greater income diversification while a lower value is associated with greater income concentration.

3.2.2. Asset diversification

Diversification of a bank is also be measured from an asset perspective (Abuzayed et al., Citation2018; Chen et al., Citation2018; Elsas et al., Citation2010). In line with Abuzayed et al. (Citation2018), asset diversification is measured as the following:

where

represents share of net loans (squared) and

represents share of operating earning assets (squared). The value of Asset Diversification is between zero and one. Higher values indicate higher earning asset diversity

3.3. Performance measures

3.3.1. Risk adjusted return

In line with the existing literature, we study the impact of diversification on the banks risk adjusted return. This is done by using banks profitability ratios; return on assets (R.O.A.). This variable is defined as annualised net income divided by total assets. For each bank, we also calculate the standard deviations of R.O.A. over the sample period to account for the volatility of profits. The risk adjusted return on assets (R.A.R.O.A.) is defined as following:

where this ratio represents accounting returns per unit of risk (Stiroh & Rumble, Citation2006).

3.3.2. Financial stability

A Z-Score is used as the proxy of banking stability. This variable is computed using accounting-based information as following:

where R.O.A. is the return on assets measured as net profit divided by total assets, E.Q.T.A. is measured as total equity divided by total assets and

is the standard deviation of R.O.A. over a three-year period.Footnote1 The Z-Score measures how many standard deviations returns must fall before a bank’s capital base is exhausted (Stiroh & Rumble, Citation2006). A higher score indicates that the probability of banks insolvency is lower and vice versa.

4. Empirical methodology

We use the P.V.A.R. analysis to investigate the dynamic relationship among competition, diversification and stability. The P.V.A.R. is estimated using the following equation:

where

is a vector of three random variables (competition, diversification and stability),

is a m x m matrix of coefficients,

is a vector of m individual effects and

is a multivariate white-noise vector of m residuals. The P.V.A.R. method imposes restriction that the underlying structure is identical for each cross sectional unit. Nevertheless, this restriction does not hold in practice most of the time. This is overcome by allowing for individual heterogeneity in the levels of variables with the inclusion of fixed effect in the model. In line with Love and Zicchino (Citation2006), forward-mean differencing known as the Helmert procedure is used to overcome bias coefficient that happens as a results of correlation between the fixed effects and the regressors. This method maintains the orthogonality between transformed variables and lagged regressors, allowing us to use lagged regressors as instruments and estimate the equation by system G.M.M. (Arellano & Bover, Citation1995).

Thereafter, the impulse response function (I.R.F.) and the variance decompositions (V.D.C.) are estimated using the Cholesky decomposition. The I.R.F. is used to identify the response of one variable to the shock of another variable, while holding all other shocks equal to zero. Meanwhile, V.D.C. estimates the percentage of variation in one variable that happens as a result of shock to another variable overtime. However, the residuals need to be decomposed to make it orthogonal so that the shocks to one of the variable in the system is isolated.

The Cholesky decomposition implicitly assumes that the variables placed earlier in the VAR order affect the other variables contemporaneously while the ones placed later affect the earlier placed variables only with a lag. This implies that variables listed earlier are more exogenous. We control for cross country variations in the panel data by including gross domestic product (G.D.P.) growth rate and log of total assets (Log T.A.) in the estimation. The order of variables based on exogeneity is as following: G.D.P., Log T.A., Lerner, Diversification and Bank Performance. Initially, we estimate the P.V.A.R. model for all the commercial banks. Subsequently, we estimate the same model on emerging market and developing economies separately.

5. Data

This study uses sample of banks from 18 countries with dual-banking system. These countries are divided into two categories based on their level of economic development. According to the World Bank classification, emerging economies includes Bahrain, Egypt, Indonesia, Iraq, Jordan, Lebanon, Malaysia, Pakistan, Saudi Arabia, Tunisia and Turkey. Whereas developing economies includes Algeria, Bangladesh Gambia, Mauritania, Senegal Syria and Yemen. The data period ranges from 2000 to 2016. Bank-specific data is obtained from Fitch Solutions, while macroeconomic variable is obtained from World Bank database.

6. Results

6.1. Descriptive statistics

shows the summary statistics of the variables. The overall mean of the Lerner Index for emerging countries is higher compared to the developing ones, indicating that, on average, competition is higher in the developing countries’ banking system. Banks in developing countries have higher revenue diversification compared to banks in emerging countries. But, not much difference is observed in terms of asset diversification of both groups of countries. Banks in emerging countries are more profitable and stable on average.

Table 1. Descriptive.

6.2. Empirical analysis

We present the P.V.A.R. estimation, I.R.F.s and V.D.C. of the variables. The appropriate lag length is identified before the P.V.A.R. estimation. This is done based on three model selection criteria by Andrews and Lu (Citation2001) and the over-all coefficient of determination. shows the estimated coefficient of the P.V.A.R. model with a lag. Since we are interested in studying the relationship among competition, diversification and bank performance, we will mainly focus on the links among the Lerner Index, two proxies of diversification (revenue and asset diversification) and two proxies of performance (risk adjusted profitability and Z-score). Additional analyses are done by differentiating between emerging and developing countries to account for the heterogeneity related to the level of competition and diversification in our sample. To get a better understanding of the relationship among competition, diversification and bank performance, we further our analyses by observing the I.R.F.s and V.D.C.s.

Table 2. PVAR model estimation with revenue diversification and RAROA.

Table 3. P.V.A.R. model estimation with revenue diversification and Z-score.

Table 4. P.V.A.R. model estimation with Asset Diversification and R.A.R.O.A.

Table 5. P.V.A.R. model estimation with Asset Diversification and Z-score.

6.3. The impulse response function and variance decompositions

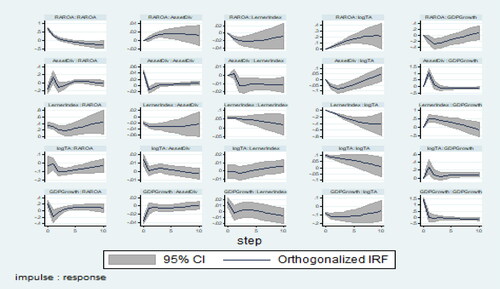

6.3.1. Lerner Index, revenue diversification and R.A.R.O.A

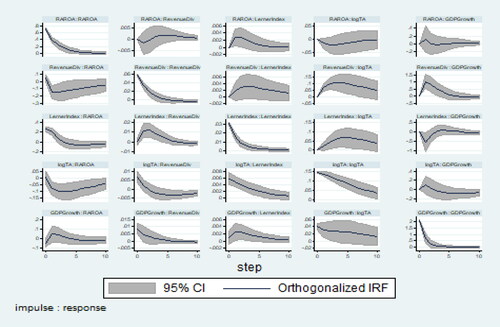

The diagram in column 3 of shows that a positive one-standard-deviation shock to the Lerner Index results in an increase in the R.A.R.O.A. for all countries. This effect remains positive before attaining equilibrium in the seventh year. This suggests a positive relationship between market power and profitability. P.V.A.R. estimation results in also showing that the lagged value of Lender Index has a positive and significant impact on risk adjusted profitability for all countries. This confirms that market power raises the profitability of the banks in dual banking system. Further analysis is done by splitting the sample of banks into emerging and developing countries. The results in and show that a shock in the Lerner Index results in an increase in RAROA for emerging countries and a decrease in RAROA for developing countries. The coefficient of PVAR estimation in show that the impact of lagged value of Lerner Index on RAROA is 11.31 for emerging countries and 1.05 for developing countries. These findings suggest that market power has a stronger impact on the profitability of banks in emerging countries.

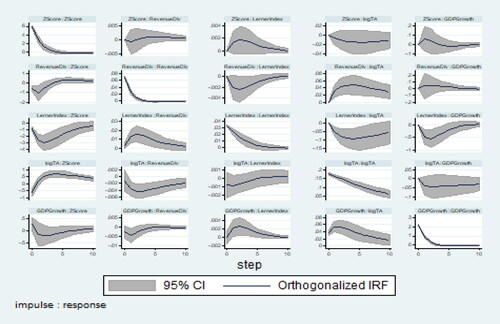

Figure 1. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Revenue Div RAROA (Sample: All Countries). Source: Authors calculation.

Figure 2. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Revenue Div RAROA (Sample: Emerging Countries). Source: Authors calculation.

Figure 3. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Revenue Div RAROA (Sample: Developing Countries). Source: Authors calculation.

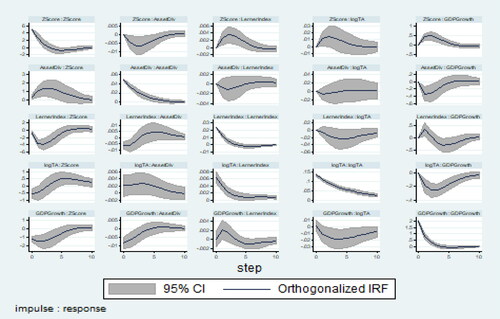

Figure 4. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Revenue Div Z-score (Sample: All Countries). Source: Authors calculation.

We also find that shock in R.A.R.O.A. has a positive impact on Lerner Index for all countries. However, this impact turns negative after a while. Similar observations are observed for developing countries. However, we find that shock in R.A.R.O.A. has a positive impact on Lerner Index for emerging countries. This suggests that higher profitability raises the market power of banks in the dual banking sector and this effect is more persistent for emerging countries. P.V.A.R. estimation in show that lagged value of risk adjusted profitability has a positive and significant impact on Lender Index in the all countries and emerging countries sample. However, the impact of risk adjusted profitability on Lender Index is negative and significant in developing countries.

In addition, the immediate reaction to the shock in Revenue Diversification is the decrease in R.A.R.O.A. in the initial years but it increases after that for all countries. Similar findings are observed for emerging countries. However, shock in Revenue Diversification has a larger negative impact on the risk adjusted profitability of banks in developing countries. This impact worsens over the years. P.V.A.R. estimation also confirms that lagged value of Revenue diversification has a negative and significant impact on RAROA for all countries and subsamples. The Revenue Diversification coefficient is twice as large in the developing countries sample than in the emerging countries one. This suggests that the negative impact of revenue diversification on the profitability of banks is more severe in case of developing countries.

The panels representing the impulse response of Revenue Diversification to a one standard deviation shock in R.A.R.O.A. show a negative impact for all countries, suggesting that higher profitability dampens Revenue Diversification. The negative impact on Revenue Diversification due to a shock in R.A.R.O.A. is larger for developing countries. However, a one-standard-deviation shock in RAROA only has a very small negative impact on Revenue Diversification that last for three periods in the case of emerging countries. This impact turns positive thereafter. P.V.A.R. estimation show that the impact of lagged value of R.A.R.O.A. on Revenue Diversification is negative but only significant in the case of developing countries.

We find that the response of the Revenue Diversification from an impulse in Lerner Index is positive for all countries. Similar observations are obtained for the subsamples. P.V.A.R. estimation also show that lagged value of Lerner Index has a positive and significant impact on Revenue Diversification for all countries. These findings suggest that market power raises the Revenue Diversification of banks in the dual banking system. However, we find that this effect is stronger in the case of emerging countries compared to developing ones. Meanwhile, shock to Revenue Diversification also has a positive impact on Lerner Index for all countries and the subsamples. However, P.V.A.R. estimation show that this impact is not significant in all cases.

The V.D.C.s in show the percentage of variation in the row variable that is explained by the column variable for 10 period ahead. We find that the Lerner Index explains the 12.72% variation in R.O.A., while Revenue Diversification explains the 10.77% variation in R.O.A. for all countries. However, by segregating the sample into emerging and developing countries, we find that the Lerner Index explains higher percentage variation (56.75%) in ROA for emerging countries while Revenue Diversification explains the higher percentage variation (39.76%) in R.O.A. for developing countries. In addition, we find that the Lerner index explains the 33.57% variation in Revenue Diversification for emerging countries and 33.74% for developing countries.

Table 6. Variance decomposition – revenue diversification percent of variation in the row variable (10 period ahead) explained by column variable.

6.3.2. Lerner Index, revenue diversification and Z-score

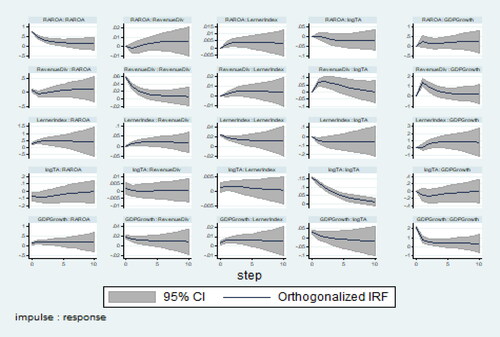

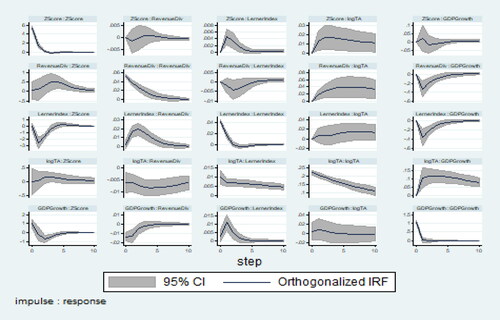

shows that the response of the Z-score from an impulse in the Lerner Index is positive. This effect remains positive in most of the periods before attaining equilibrium in the tenth period. This finding suggest that market power raises the stability of the dual banking system. Similar results are obtained by splitting the sample into emerging and developing countries. However, the positive relationship between market power and stability is more persistent in the case of emerging countries. P.V.A.R. estimation results in also show that lagged value of the Lerner Index has a positive and significant impact on Z-score in all cases. Meanwhile, the Lerner Index shows a negative response to a shock in the Z-score for all and emerging countries. A similar negative response is observed for developing countries, but this impact attains equilibrium by the fifth period. P.V.A.R. estimation show that lagged value of Z-score has a significant negative impact on the Lender Index for all and emerging countries.

The impact of a positive one-standard-deviation shock to the Revenue Diversification results in a small decrease in Z-score in the initial years for all countries. This impact remains negative and attains equilibrium in the sixth year. Similar findings are observed for developing and emerging countries as shown in and . P.V.A.R. estimation results in show that lagged value of revenue diversification has a negative and significant impact on Z-score for all countries and emerging countries. These findings imply that revenue diversification reduces the stability of banks in the dual banking system. A one standard deviation shock in Z-score reduces revenue diversification for all and emerging countries but raises it for developing countries. However, P.V.A.R. estimation shows that lagged value of Z-score does not have significant impact on revenue diversification in all cases.

Figure 5. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Revenue Div Z-score (Sample: Emerging Countries). Source: Authors calculation.

Figure 6. Impulse-responses for 1 lag VAR of GDP growth log TA Lerner Index Revenue Div Z-score (Sample: Developing Countries). Source: Authors calculation.

Panel B of shows that Lerner Index explains 11.75% variation in Z-score for all countries. Further analysis show that Lerner Index explains higher variation in Z-score for emerging countries than for developing countries (40.14% vs 22.09%). However, Revenue Diversification does not explain much of the variation in Z-score for all samples.

6.3.3. Lerner Index, asset diversification and R.A.R.O.A

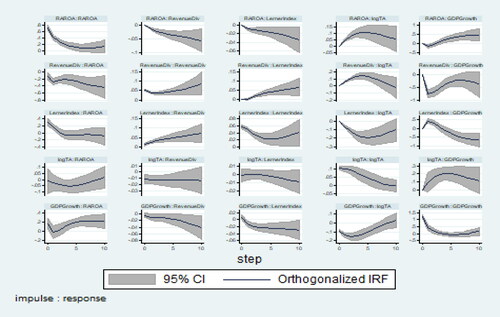

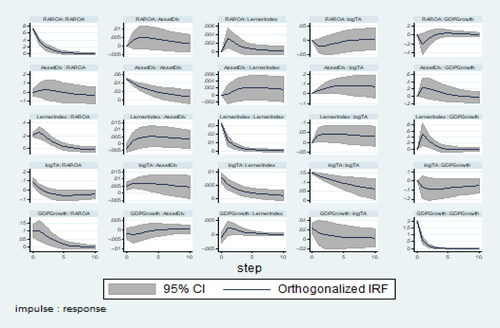

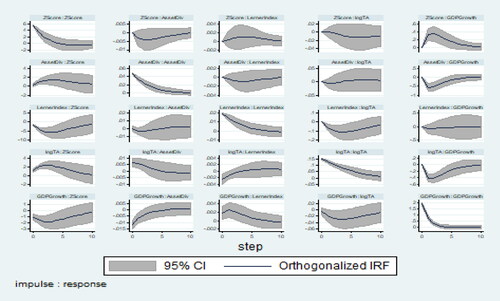

Shock in Asset Diversification has a positive impact on R.A.R.O.A. for all countries as shown in . This implies that asset diversification improves the profitability of banks in dual banking system. Further analyses by dividing the sample of banks into emerging and developing countries also show similar results as shown in and . P.V.A.R. estimation results in show that the lagged value of Asset Diversification coefficient are positive and significant for emerging and developing countries. Nevertheless, the impact of lagged value of Asset diversification on R.A.R.O.A. is higher for emerging countries compared to the developing ones. This confirms that emerging countries benefit more as a result of asset diversification. A positive one-standard-deviation shock to R.A.R.O.A. results in an increase in Asset Diversification for all countries, but this effect only last for five periods. The impact of a shock in R.A.R.O.A. on Asset Diversification of banks in emerging countries is highly positive and persistent. However, the impact of a shock in R.A.R.O.A. on Asset Diversification is very volatile in the case of developing countries. It reduces in the initial period but turns positive in the second period before falling back again. Equilibrium is attained in the fifth period. P.V.A.R. estimation shows that the impact of lagged value of R.A.R.O.A. on Asset Diversification is positive but only significant for all countries and emerging countries.

Figure 7. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Asset Div RAROA (Sample: All Countries). Source: Authors calculation.

Figure 8. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Asset Div RAROA (Sample: Emerging Countries). Source: Authors calculation.

Figure 9. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Asset Div RAROA (Sample: Developing Countries). Source: Authors calculation.

Asset diversification reacts positively to a shock in Lerner Index for all countries. Similar finding is obtained for emerging countries. This suggests that market power is linked to greater asset diversification. Nevertheless, asset diversification of banks in developing countries only reacts positively to a shock in Lerner Index during the initial period. This reaction turns negative thereafter. P.V.A.R. estimation results shown in confirms that lagged value of Lerner Index only has a negative and significant impact on Asset Diversification for developing countries. Meanwhile, a shock in Asset Diversification has a negative impact on the Lerner Index initially but this impact turns positive in the second period and remains so thereafter for all countries. The Lerner Index reacts positively to a shock in Asset Diversification in the case of emerging countries, but the opposite is true in the case of developing countries. However, P.V.A.R. estimation shows that the lagged value of Asset Diversification does not have any significant impact on the Lerner Index for all cases. This suggest that asset diversification does not have a significant influence on market power of banks in dual banking system.

V.D.C. analysis in show that Asset Diversification does not explain much of the variation of R.A.R.O.A. for all countries and developing countries but explains 32.85% variation in R.O.A. for emerging countries. We also find that Asset Diversification does not explain much of the variation of the Lerner Index, but the Lerner Index explains 10.99% variation in Asset Diversification for emerging countries and 61.33% for developing countries.

Table 7. Variance decomposition – asset diversification percent of variation in the row variable (10 period ahead) explained by column variable

6.3.4. Lerner Index, asset diversification and Z-score

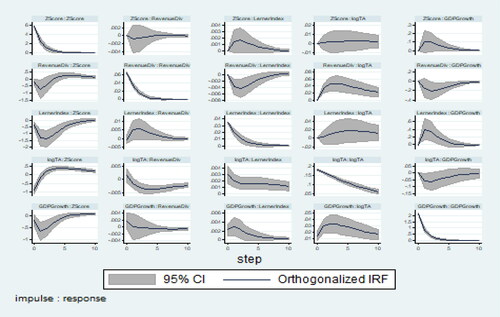

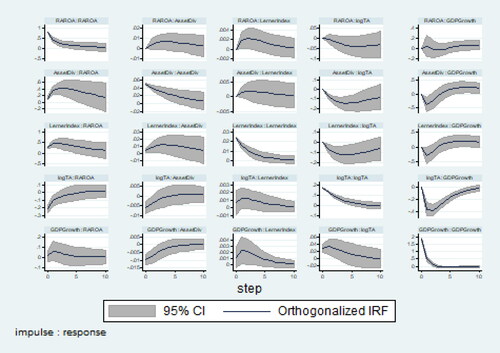

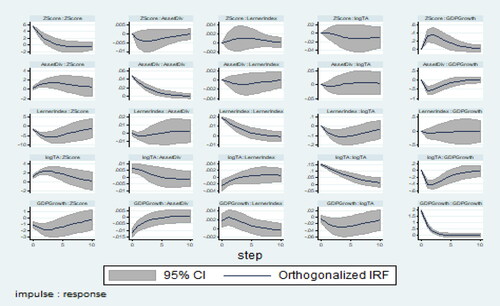

Shock in Asset Diversification has a negative impact on Z-score in all cases as shown in . P.V.A.R. estimation results in show that lagged value Asset Diversification has a negative and significant impact on Z-score in all cases. This suggest that asset diversification makes the dual banking system more fragile. I.R.F. analysis show that asset diversification reacts positively to a shock in Z-score in all cases. However, P.V.A.R. estimation shows that lagged value Z-score only has significant positive impact on Asset Diversification for all countries. V.D.C. analysis in show that Asset Diversification only explain 7.77% variation in Z-score for all countries. However, Asset Diversification only explains less than 5% of the variation in Z-score for emerging and developing countries.

Figure 10. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Asset Div Z-score (Sample: All Countries). Source: Authors calculation.

Figure 11. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Asset Div Z-score (Sample: Emerging Countries). Source: Authors calculation.

Figure 12. Impulse-responses for 1 lag VAR of GDP growth Log TA Lerner Index Asset Div Z-score (Sample: Developing Countries). Source: Authors calculation.

7. Conclusion

Developments in the banking sector show that competition influences revenue diversification and this has a bearing on bank performance. This is especially true in the case of dual banking system where Islamic and conventional banks co-exist and compete with each other. To get a better understanding about the nature of relationship among competition, diversification and bank performance, we analysed commercial bank data of 18 countries with dual banking system over the period 2000 to 2016. Lerner index is used to measure competition while bank performance is assessed using risk adjusted return (R.A.R.O.A.) and stability (Z-score) measures. Both revenue and asset diversification are used to assess banks’ diversification strategy. The P.V.A.R. estimation, I.R.F. and V.D.C. are used to account for the endogenous relationship among the three variables. Our dynamic analysis enables us to capture the changes in the relationship among the three variables that transpires over time.

The findings using I.R.F., coefficient estimates and V.D.C. derived from vector autoregressions (V.A.R.) confirm that competition and revenue diversification influence the performance of banks in the dual banking system. In addition, we obtain a number of interesting findings. First, we observe a positive bidirectional causal relationship between market power (lack of competition) and profitability. Secondly, we find that market power increases the stability of banks, but stability reduces market power. Thirdly, market power increases revenue diversification, while the reverse is not significant. Fourthly, revenue diversification reduces profitability and stability, but the reverse is not significant in both cases. Fifthly, asset diversification reduces the stability of banks, but stability increase asset diversification.

Further analyses done by separating the sample of banks into emerging and developing economies show that the positive impact of market power on profitability is higher for the former. Similarly, the positive impact of market power on revenue diversification is higher for emerging market countries. Meanwhile, the negative impact of revenue diversification on bank profitability is worse for developing countries. We find that revenue diversification only reduces the stability of banks in emerging market economies. Additionally, we find that asset diversification does not have a significant impact on the profitability of banks in the dual banking system, but it reduces the stability. However, we find that asset diversification has a more positive impact on the profitability of banks in emerging economies. We also find that market power only dampens asset diversification of banks in the developing countries.

This study has several limitations. Firstly, the analyses are based on banks in countries with dual banking system. Further studies can be done to compare how the relationship among competition, diversification and performance may vary between countries with single and dual banking system. Secondly, the findings of this study are derived using the P.V.A.R. model. Analyses done using other estimation technique may provide different insights. Nevertheless, a number of policy implications can be derived from our findings. Firstly, market power in a dual banking system need to be regulated since it influences banks’ profitability and stability. Even though market power improves banks performance, excessive markets may lead other problem related to ‘too big to fail’. Secondly, revenue diversification of banks in dual banking system also need to be monitored to safeguard the performance of banks. Thirdly, different competition and revenue diversification policy measures are needed to safeguard the performance of banks in emerging and developing economies with dual banking system. Banks profitability in emerging economies is more vulnerable to banks market power while banks profitability in developing economies is more vulnerable to revenue diversification. Fourthly, regulators in the dual banking system also need to monitor banks asset diversification strategies as they worsen banks stability. Lastly, banks in emerging and developing economies need to use different strategies to remain stable and profitable.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 In line with the literature, a three-year window is used for the standard deviations of R.O.A. to allow for variations in the Z-Score value.

References

- Abedifar, P., Molyneux, P., & Tarazi, A. (2018). Non-interest income and bank lending. Journal of Banking & Finance, 87, 411–426. https://doi.org/https://doi.org/10.1016/j.jbankfin.2017.11.003

- Abuzayed, B., Al-Fayoumi, N., & Molyneux, P. (2018). Diversification and bank stability in the GCC. Journal of International Financial Markets, Institutions and Money, 57, 17–43. https://doi.org/https://doi.org/10.1016/j.intfin.2018.04.005

- Acharya, V. V., Hasan, I., & Saunders, A. (2006). Should banks be diversified? Evidence from individual bank loan portfolios. The Journal of Business, 79(3), 1355–1412. https://doi.org/https://doi.org/10.1086/500679

- Alam, N., Hamid, B. A., & Tan, D. T. (2019). Does competition make banks riskier in dual banking system. Borsa Istanbul Review, 19, S34–S43. https://linkinghub.elsevier.com/retrieve/pii/S2214845018301388 https://doi.org/https://doi.org/10.1016/j.bir.2018.09.002

- Amidu, M., & Wolfe, S. (2013). Does bank competition and diversification lead to greater stability? Evidence from emerging markets. Review of Development Finance, 3(3), 152–166. https://doi.org/https://doi.org/10.1016/j.rdf.2013.08.002

- Andrews, D. W. K., & Lu, B. (2001). Consistent model and moment selection procedures for GMM estimation with application to dynamic panel data models. Journal of Econometrics, 101(1), 123–164. https://doi.org/https://doi.org/10.1016/S0304-4076(00)00077-4

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/https://doi.org/10.1016/0304-4076(94)01642-D

- Ariss, R. T. (2010a). Competitive conditions in islamic and conventional banking: A global perspective. Review of Financial Economics, 19(3), 101–108. https://doi.org/https://doi.org/10.1016/j.rfe.2010.03.002

- Ariss, R. T. (2010b). On the implications of market power in banking: Evidence from developing countries. Journal of Banking and Finance, 34(4), 765–775. https://doi.org/https://doi.org/10.1016/j.jbankfin.2009.09.004

- Berger, A. N. (1995). The profit-structure relationship in banking–tests of market-power and efficient-structure hypotheses. Journal of Money, Credit and Banking, 27(2), 404–431. https://doi.org/https://doi.org/10.2307/2077876

- Berger, A. N., & Hannan, T. H. (1989). The price-concentration relationship in banking. The Review of Economics and Statistics, 71(2), 291–299. https://doi.org/https://doi.org/10.2307/1926975

- Berger, A. N., & Hannan, T. H. (1998). The efficiency cost of market power in the banking industry: a test of the “quiet life “and related hypotheses. Review of Economics and Statistics, 80(3), 454–465. https://doi.org/https://doi.org/10.1162/003465398557555

- Berger, A. N., Hasan, I., Korhonen, I., Zhou, M. (2010). Does diversification increase or decrease bank risk and performance? Evidence on diversification and the risk-return tradeoff in banking. BOFIT Discussion Paper No. 9/2010. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1651131.

- Carbó Valverde, S., & Rodríguez Fernández, F. (2007). The determinants of bank margins in european banking. Journal of Banking & Finance, 31(7), 2043–2063. https://doi.org/https://doi.org/10.1016/j.jbankfin.2006.06.017

- Chen, N., Liang, H. Y., & Yu, M. T. (2018). Asset diversification and bank performance: Evidence from three asian countries with a dual banking system. Pacific-Basin Finance Journal, 52, 40–53. https://doi.org/https://doi.org/10.1016/j.pacfin.2018.02.007

- Chiorazzo, V., Milani, C., & Salvini, F. (2008). Income Diversification and Bank Performance: Evidence from Italian Banks. Journal of Financial Services Research, 33(3), 181–203. https://doi.org/https://doi.org/10.1007/s10693-008-0029-4

- De Nicoló, G., Jalal, A. M., & Boyd, J. H. (2006). Bank risk-taking and competition revisited: New theory and new evidence. IMF Working Papers, 6(297), 49. https://doi.org/https://doi.org/10.5089/9781451865578.001

- De Nicolo, G. (2000). Size, carter value and risk in banking. International Finance Discussion Papers No. 689. International Finance Discussion Papers from Board of Governors of the Federal Reserve System (U.S.). https://EconPapers.repec.org/RePEc:fip:fedgif:689

- Deyoung, R., & Rice, T. (2004). Noninterest income and financial performance at U. S. commercial banks. Financial Review, 39(1), 101–127. https://doi.org/https://doi.org/10.1111/j.0732-8516.2004.00069.x

- Deyoung, R., & Roland, K. P. (2001). Product mix and earnings volatility at commercial banks: Evidence from a degree of total leverage model. Journal of Financial Intermediation, 10(1), 54–84. https://doi.org/https://doi.org/10.1006/jfin.2000.0305

- DeYoung, R., & Torna, G. (2013). Nontraditional banking activities and bank failures during the financial crisis. Journal of Financial Intermediation, 22(3), 397–421. https://doi.org/https://doi.org/10.1016/j.jfi.2013.01.001

- Elsas, R., Hackethal, A., & Holzhäuser, M. (2010). The anatomy of bank diversification. Journal of Banking & Finance, 34(6), 1274–1287. https://doi.org/https://doi.org/10.1016/j.jbankfin.2009.11.024

- Fu, X. (M)., Lin, Y. (R)., & Molyneux, P. (2014). Bank competition and financial stability in Asia Pacific. Journal of Banking & Finance, 38(1), 64–77. https://doi.org/https://doi.org/10.1016/j.jbankfin.2013.09.012

- González, L. O., Razia, A., Búa, M. V., & Sestayo, R. L. (2017). Competition, concentration and risk taking in banking sector of MENA countries. Research in International Business and Finance, 42, 591–604. https://doi.org/https://doi.org/10.1016/j.ribaf.2017.07.004

- Grassa, R. (2012). Islamic banks’ income structure and risk: Evidence from GCC countries. Accounting Research Journal, 25(3), 227–241. https://doi.org/https://doi.org/10.1108/10309611211290185

- Hamid, F. S. (2017). The effect of market structure on banks’ profitability and stability: Evidence from ASEAN-5 countries. International Economic Journal, 31(4), 578–598. https://www.tandfonline.com/doi/full/10.1080/10168737.2017.1408668

- Hsieh, M. F., & Lee, C. C. (2010). The puzzle between banking competition and profitability can be solved: International evidence from bank-level data. Journal of Financial Services Research, 38(2–3), 135–157. https://doi.org/https://doi.org/10.1007/s10693-010-0093-4

- Kabir, M. N., & Worthington, A. C. (2017). The ‘competition–stability/fragility’ nexus: A comparative analysis of Islamic and conventional banks. International Review of Financial Analysis, 50, 111–128. https://doi.org/https://doi.org/10.1016/j.irfa.2017.02.006

- Keeley, M. C. (1990). Deposit insurance, risk, and market power in banking. The American Economic Review, 80(5), 1183–1200.

- Köhler, M. (2015). Which banks are more risky? The impact of business models on bank stability. Journal of Financial Stability, 16, 195–212. https://doi.org/https://doi.org/10.1016/j.jfs.2014.02.005

- Lepetit, L., Nys, E., Rous, P., & Tarazi, A. (2008). Bank income structure and risk: An empirical analysis of European banks. Journal of Banking & Finance, 32(8), 1452–1467. https://doi.org/https://doi.org/10.1016/j.jbankfin.2007.12.002

- Leroy, A., & Lucotte, Y. (2017). Is there a competition-stability trade-off in European banking? Journal of International Financial Markets, Institutions and Money, 46, 199–215. https://doi.org/https://doi.org/10.1016/j.intfin.2016.08.009

- Love, I., & Zicchino, L. (2006). Financial development and dynamic investment behavior: Evidence from panel VAR. The Quarterly Review of Economics and Finance, 46(2), 190–210. https://doi.org/https://doi.org/10.1016/j.qref.2005.11.007

- Mercieca, S., Schaeck, K., & Wolfe, S. (2007). Small European banks: Benefits from diversification? Journal of Banking & Finance, 31(7), 1975–1998. https://doi.org/https://doi.org/10.1016/j.jbankfin.2007.01.004

- Mirzaei, A., Moore, T., & Liu, G. (2013). Does market structure matter on banks’ profitability and stability? Emerging vs. advanced economies. Journal of Banking & Finance, 37(8), 2920–2937. https://doi.org/https://doi.org/10.1016/j.jbankfin.2013.04.031

- Molyneux, P., & Yip, J. (2013). Income diversification and performance of Islamic banks. Journal of Financial Management Markets and Institutions, 1(1), 47–66.

- Mostak Ahamed, M. (2017). Asset quality, non-interest income, and bank profitability: Evidence from Indian banks. Economic Modelling, 63, 1–14. https://doi.org/https://doi.org/10.1016/j.econmod.2017.01.016

- Nguyen, M., Skully, M., & Perera, S. (2012). Market power, revenue diversification and bank stability: Evidence from selected South Asian countries. Journal of International Financial Markets, Institutions and Money, 22(4), 897–912. https://doi.org/https://doi.org/10.1016/j.intfin.2012.05.008

- Perera, S., Skully, M., & Chaudrey, Z. (2013). Determinants of commercial bank profitability: South Asian evidence. Asian Journal of Finance & Accounting, 5(1), 365–380. http://www.macrothink.org/journal/index.php/ajfa/article/view/3012 https://doi.org/https://doi.org/10.5296/ajfa.v5i1.3012

- Risfandy, T., Tarazi, A., Trinugroho, I. (2018). Competition in dual markets: implications for banking system stability. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3158510

- Saghi-Zedek, N. (2016). Product diversification and bank performance: Does ownership structure matter? Journal of Banking & Finance, 71, 154–167. https://doi.org/https://doi.org/10.1016/j.jbankfin.2016.05.003

- Sanya, S., & Wolfe, S. (2011). Can banks in emerging economies benefit from revenue diversification? Journal of Financial Services Research, 40(1–2), 79–101. https://doi.org/https://doi.org/10.1007/s10693-010-0098-z

- Sawada, M. (2013). How does the stock market value bank diversification? Empirical evidence from Japanese banks. Pacific-Basin Finance Journal, 25, 40–61. https://doi.org/https://doi.org/10.1016/j.pacfin.2013.08.001

- Shim, J. (2013). Bank capital buffer and portfolio risk: The influence of business cycle and revenue diversification. Journal of Banking & Finance, 37(3), 761–772. https://doi.org/https://doi.org/10.1016/j.jbankfin.2012.10.002

- Stiroh, K. J. (2006). A portfolio view of banking with interest and noninterest activities. Journal of Money, Credit and Banking, 38(5), 1351–1361. https://doi.org/https://doi.org/10.1353/mcb.2006.0075

- Stiroh, K. J., & Rumble, A. (2006). The dark side of diversification: The case of US financial holding companies. Journal of Banking & Finance, 30(8), 2131–2161. https://doi.org/https://doi.org/10.1016/j.jbankfin.2005.04.030

- Tan, Y. (2016). The impacts of risk and competition on bank profitability in China. Journal of International Financial Markets, Institutions and Money, 40, 85–110. https://doi.org/https://doi.org/10.1016/j.intfin.2015.09.003

- Vardar, G. (2015). Bank competition and risk taking in the Turkish banking industry. Pressacademia, 4(3), 536–567. https://doi.org/https://doi.org/10.17261/Pressacademia.2015313139

- Williams, B. (2016). The impact of non-interest income on bank risk in Australia. Journal of Banking & Finance, 73, 16–37. https://doi.org/https://doi.org/10.1016/j.jbankfin.2016.07.019

- Zhou, K. (2014). The effect of income diversification on bank risk: Evidence from China. Emerging Markets Finance & Trade, 50(suppl 3), 201–213. https://doi.org/https://doi.org/10.2753/REE1540-496X5003S312