?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Private health insurance is an important supplement to social health insurance. However, there is a lack of research on the impact of school-based private health insurance programs on students’ health in developing countries. This study aims to investigate the causal impact of school-based supplementary private health insurance programs on the self-rated health status of Chinese secondary school students, with an average age of 14, using a longitudinal database, the China Education Panel Survey (CEPS). The study exploits the cross-school variation and discrete feature of the response variable by applying a two-level ordered logit model with a random effect at the school level. An ordered logit propensity score matching method, clustering the standard errors by school, is applied for the robustness check. Lagged values of potential endogenous covariates are included in both methods to control the effect of unobserved individual heterogeneities. The results indicate that participating in uniform school-based private health insurance programs does not improve student self-rated health status, whereas individualized health insurance significantly improves student self-rated health status.

1. Introduction

A private health insurance policy provides a contract between an insurance company and an individual or his/her sponsor (e.g. an employer or a community organization), which can be renewable or perpetual. Private health insurance differs from social health insurance, as the latter is generally in the form of a national plan (Savedoff & Gottret, Citation2008). It is essential for governments to be involved in the health care system (Łyszczarz, Citation2016). The decommodifying potential of health care systems differs across countries (Kawiorska, Citation2016). However, the market mechanism becomes increasingly common in the health care system due to growing pressure on the public finance of welfare states. Therefore, many countries are moving toward private health insurance as a supplement to social health insurance to improve people’s health status (Dormont, Citation2019). For example, private health insurance plays a significant role in health financing in some Organisation for Economic Co-operation and Development (OECD) countries, including developed countries like the United States, France, and Germany (Colombo & Tapay, Citation2004) and developing countries like China and India (Bhattacharjya & Sapra, Citation2008). In 2009, ‘Opinions of the Communist Party of China Central Committee and the State Council on Deepening the Reform of the Medical and Health Care System’ clarified the importance of private health insurance and encouraged enterprises and individuals to actively participate (The State Council of the People's Republic of China, Citation2009). Considering an entire population, student health protection is critical. Student health conditions accumulate, and they influence family harmony, social stability, and national economy (Smith et al., Citation2012). Additionally, spending on healthcare services drives human capital development in the long run (Shuaibu & Oladayo, Citation2016). Therefore, multiple levels of health protection, with a combination of private and social health insurances, are common for students in many countries. In China, insurance premiums were generally collected with the school tuition fees. In the United States, student-athletes in the National Collegiate Athletic Association (NCAA) are required to purchase private health insurance, with required minimum levels of coverage, before participating in training and competition (Wood, Citation2012).

Previous studies on private health insurance concentrate on the demand for voluntary health insurance (Nguyen & Knowles, Citation2010) and its impact on national health insurance systems (Stabile & Townsend, Citation2014), medical service performance (Breyer et al., Citation2011), welfare improvement (Danzon, Citation2002; Hansen & Keiding, Citation2002), delivery of care (Brindis et al., Citation1995), and health enhancement. Hullegie and Klein (Citation2010) studied the impact of private health insurance on health status, using survey data from the German Social Economic Panel for 1995–2006. By applying regression discontinuity analysis, they found a positive effect of private insurance for self-assessed health in German adults age 25–55 years. Baker et al. (Citation2001, Citation2002) investigated individuals age 51–61 years with private insurance in 1992 from the Health and Retirement Study database in the United States, determining that the loss of insurance has adverse health consequences measured by self-assessed health. Dor et al. (Citation2006), using the same data, conducted follow-up research dealing with the endogenous problem using the instrumental variable method. They found that extending private insurance coverage to working-age adults may result in improved health. Research on the impact of private insurance on populations like HIV patients over 18 years old in the United States (Bhattacharya et al., Citation2003), end-stage kidney disease adult patients in Australia (Sriravindrarajah et al., Citation2020), and women age 35–64 years with breast cancer in New Jersey (Ayanian et al., Citation1993) has been conducted. Private health insurance is more effective than public insurance in preventing HIV-related deaths (Bhattacharya et al., Citation2003) and is improves health outcomes among patients (Ayanian et al., Citation1993; Sriravindrarajah et al., Citation2020). However, few studies focus on the effect of private health insurance on juvenile populations. Todd et al. (Citation2006) conducted a retrospective comparison of hospitalization-related outcomes for individuals under 18 years old in Colorado from 1995 to 2003 and nationwide in the United States in 2000, determining that individuals with public or no insurance have significantly worse health outcomes compared to individuals with private insurance. However, there are sources of error due to confounding and bias in retrospective comparison studies (Cox et al., 2009). With the delayed progress of private health insurance in developing countries compared to developed countries, relevant literature is highly based on personal opinions and experiences or on case studies from countries with developed private health insurance systems (Choi et al., Citation2018). The value of private health insurance depends on the economic, social, and institutional settings in a country or region (Drechsler & Jutting, Citation2007); therefore, the results from adults in developed countries cannot be extrapolated to juveniles in developing countries, as their economic and health situations differ (Popkin & Gordon-Larsen, Citation2004). There is a lack of empirical research to determine if private health insurance is an important supplement to public health insurance for health status improvement in developing countries, especially for student populations. The policy regarding the health status enhancement through private health insurance scheme is untested, although this is deemed as a significant field for research.

The causal impact of private health insurance on health is difficult to examine, due to the adverse selection issue inherent in the system (Doiron et al., Citation2008). Specifically, people with poor health conditions are more likely to purchase private health insurance products. As stated by Rutten et al. (Citation2001), mandatory social health insurance solves the problem of adverse selection. Additionally, it is difficult to track a large group of people with similar private health insurance policies, as the policies are purchased voluntarily, and individuals can choose products from different insurance companies. These factors make an empirical study of this causal impact challenging.

A Chinese student group is an excellent sample to study to overcome the challenges of adverse selection and tracking. Prior to June 2015, the private health insurance status of students in the same school was essentially equal (Guan & Wang, Citation2017). This solves the adverse selection issue because the private health insurance premium was collected with tuition fees, additionally, students and parents did not have power over the purchase and selection of insurance products (Guan & Wang, Citation2017). This study uses a longitudinal database to track the same students in different waves. With a large population and low per capita income, China is optimum for investigating developing countries’ issues.

To the best of the author’s knowledge, this is the first study to examine the impact of private health insurance on student health status in a developing country context. This study uses China Education Panel Survey (CEPS), a longitudinal database, which includes student’s information at three levels: individual, family, and school. Multilevel (two-level) equation modelling is applied as students are clustered by schools.

This paper proceeds as follows: Section 2 introduces health insurance schemes for Chinese students. Section 3 describes the data, variables, and methodology used. Section 4 presents results and findings. Section 5 concludes.

2. Chinese students’ health insurance schemes

China requires nine years of mandatory education, which include six years of primary education and three years of junior high school education. Generally, students cannot select the junior high school they attend, and the match between school and student is based on academic score, location of residence, or random selection (Xu, Citation2000). After mandatory education, students can attend three years of senior high school education and four years of undergraduate education.

Students can join voluntary health insurance schemes, including social and private schemes. Urban students can join Urban Resident Basic Medical Insurance (URBMI), which launched in 2007, and rural students can join New Cooperative Medical Scheme (NCMS), which launched in 2003. Therefore, students participate in health insurance based on location of the school or their registration types. In 2016, China started a pilot program that combined the NCMS and URBMI. Each province selected cities for the first round, and eventually, there will be one social health insurance scheme for all Chinese children regardless of their location. Guan and Tena (Citation2018) offered details about students’ social health insurance schemes in China. There are some shortcomings for each social health insurance scheme, including limitation on medication, types of medical services, health organization, and reimbursement rate. Therefore, the importance of private health insurance scheme is becoming prevalent among Chinese students (Choi et al., Citation2018).

Originated in the 1980s, Student Accident Insurance (SAI) covers student death, disability, accident medical expenses compensation, and disease medical expenses compensation, costing approximately 100 yuan per year (Ying, Citation2005). There are three development stages of SAI. Before 2003, students obtained SAI when they attended school, and the premium was collected with the tuition fee. Commercial insurance companies were selling insurance to students through agreements with school leaders. Usually, all the students in a school which offers SAI had to purchase the same insurance product; therefore, the insurance policy was not individualized to meet student-specific needs. Additionally, to expand the scale of business, there were reports that insurance companies gave school leaders premium rebates or other bribes (Luo & Yang, Citation2003).

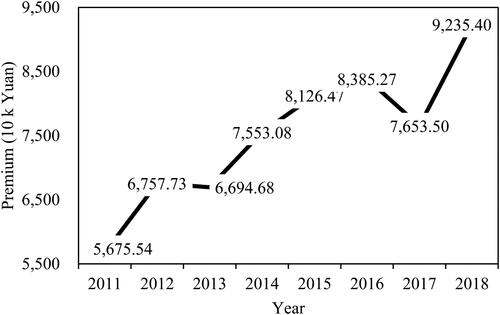

On 3 June 2015, the Ministry of Education of the People’s Republic of China and five other departments issued ‘Implementation Opinion on Regulating Education Fees and Charges in 2015’ (2015 Opinion). In article 6, it states that collection of commercial insurance premiums is strictly prohibited at all levels of schools. shows the yearly premium of SAI from one of China’s largest insurance companies, indicating the substantial decrease of total premiums after the 2015 Opinion.

Figure 1. Student Accident Insurance yearly insurance premium from one of China’s largest insurance companies. Source: Collected by author.

Chinese authorities consider the sales model of SAI unethical (Guan & Wang, Citation2017). Multiple policies forbid campuses from collecting SAI premiums, and school-based SAIs gradually disappeared (Guan & Wang, Citation2017). The 2015 Opinion is not opposed to commercial insurance products, but rather, criticizes the sales model involving students. Parents also consider the sales model as evidence of corruption in schools and insurance companies. The 2015 Opinion regulates the behaviour of insurance companies somewhat, but it contradicts the concept of promoting commercial insurance development for students.Footnote1

3. Data and methodology

3.1. Data

This study uses data from CEPS, conducted by the National Survey Research Centre at the Renmin University of China. CEPS is a nationally representative, school-based survey which selects samples of approximately 20,000 students from 438 classrooms of 112 junior high schools in 28 provinces in mainland China. It provides information at individual, family, and school levels. CEPS includes demographic characteristics, insurance information, health outcome, as well as household and basic school information. This study uses data from seventh-year students in the 2013/14 academic year and subsequent observations from the same students in the 2014/15 academic year.

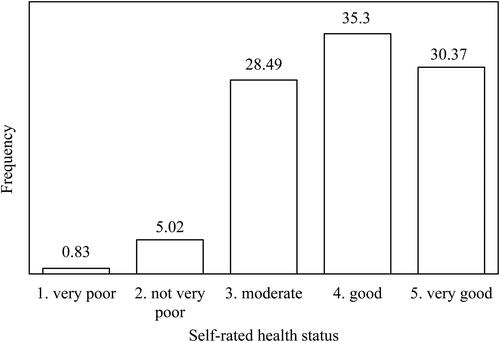

The response variable corresponds to students’ health status, which is measured by the self-rated health status (SRHS). SRHS takes discrete values from 1 to 5, corresponding to an individual’s self-evaluated health status: 1 = very poor, 2 = not very good, 3 = moderate, 4 = good, and 5 = very good. SRHS, as a tool to measure health status among individuals, has been used widely (Baker et al., Citation2001, Citation2002; Hullegie & Klein, Citation2010). presents the distribution of the response variable (SRHS). SRHS does not follow a normal distribution, indicating that the conventional ordinary least squares estimation could be biased, and a non-linear regression is required.

Figure 2. Distribution of response variable. Source: Author's processing.

The treatment variable is continuous, measuring SAI premiums collected by schools which is donated by School Level Insurance. As a robustness test, this variable is converted into a binary variable which takes the value 1 or 0 depending on whether the student is covered by SAI and is denoted by School Level Insurance Dummy. As the analysis period is prior to the 2015 Opinion, students were automatically insured in schools offering SAI. The combination of this information with the fact that students cannot choose which school to attend indicates the exogeneity of participation in SAI at the individual level. SAI is only available in the second wave. However, the lagged values of SRHS and other potential endogenous covariates can be employed by using the longitudinal feature of the database.

Covariates are divided into two lists: school characteristics and individual characteristics. School characteristic covariables include the type and the location of the school. Type of school is based on the percentage of students admitted to key senior high schools, which have high-quality education resources (Luo & Wendel, Citation1999), out of the total number of junior high students graduating from the corresponding school. Type of school could affect the school’s ranking and financial resources. Location of school is a binary variable which equals 1 when a school is located in the centre or peripheries of a city/town and equals 0 when a school is located in the rural-urban fringe zone of the city/town, settlements outside of the city/town, or rural areas. The location of school is related to the community environment which might influence students’ health status.

Individual characteristic covariables include health insurance at an individual level (Individual Level Insurance), wellbeing, age, squared age, gender, household registration type (hukou), ethnicity, height, weight, and household income level. Individual Level Insurance is a binary variable that equals 1 or 0 depending on whether a student was covered by health insurance at an individual level. Other insurance policies that are not offered by the school might influence students’ SRHS. The wellbeing covariable takes the corresponding value if the respondent has 1 = never, 2 = seldom, 3 = sometimes, 4 = often, or 5 = always felt unhappy in the last week. The correlation between wellbeing and SRHS has been widely investigated in studies (Rasciute & Downward, Citation2010). Gender is a binary variable 1 = male and 0 = female. Hukou equals 1 if a student has an agriculture hukou, or 0 otherwise. The hukou system places a restriction on rural populations from accessing urban social resources (Liu, Citation2005), leading to a disparity of health status between rural and urban students. Ethnicity is a binary variable equalling 1 for Han people and 0 otherwise. Compared to the Han people, most non-Han people live in less-developed areas of China with fewer social resources (Hannum & Wang, Citation2010). Height is measured in centimetres and weight is measured in kilograms, both of which are common factors for measuring health status (Baker et al., Citation2001). Household income levels are: 1 = very poor, 2 = somewhat poor, 3 = moderate, 4 = somewhat rich, and 5 = very rich. Generally, students of rich families have access to better medical treatment and can purchase a variety of insurance products. Given the longitudinal feature of the database, the lagged value of SRHS is included to capture the effect of past health on current health. Some covariances could be endogenous, such as Individual Level Insurance, wellbeing, height, weight, and income. An issue of reverse causality might occur between current values of covariates and SRHS (Rasciute & Downward, Citation2010). To deal with reverse causality, lagged values, rather than the current values, are analysed (Bania et al., Citation2007).

provides descriptive statistics for the variables. The last column shows the difference between treated (School Level Insurance Dummy = 1) and non-treated groups (School Level Insurance Dummy = 0). No significant differences between the two subgroups are observed in terms of SRHS. However, this does not indicate that SAI does not have a causal effect on SRHS, as the two groups of students are significantly different in terms of the explanatory variables at school and individual levels. Therefore, a proper causal analysis is required, controlling for the different confounding factors in the estimation.

Table 1. Statistical description of variables.

3.2. Methodology

This study aims to estimate the causal impact of SAI on students’ SRHS. Here, student SRHS is denoted by the current SRHS of student

in school

Health is defined as a categorical variable allowing for clustering at the school level. Therefore, a two-level ordered logit model with random effect at the school level is applied. The outcome is regressed on treatment variables and controls for school and individual characteristics. The observed ordinal response

is generated from the latent continuous response. The model in terms of a latent linear response is written as:

(1)

(1)

and

where

is the school-based private health insurance program, measured by School Level Insurance (Dummy).

is a vector of explanatory variables defined at student and school levels, and

(where p = 1, 2) are the associated coefficients (fixed effects).

represents random effects, allowing the regression intercept to vary randomly across schools. The errors

are logistic-distributed with mean zero and variance

and are independent of

Based on Chinese junior high school enrolment rules mentioned in Section 2, students cannot select which school to attend. Therefore, resources allocated to schools are not likely to be related to unobservable determinants of student SRHS.

Another assumption of this two-level regression model is that the residual at the individual level is uncorrelated with the predictor variables, To deal with potential reverse causality between an individual’s SRHS and personal characteristics, the lagged values of Individual Level Insurance, wellbeing, height, weight, and income are applied.

A robustness test was conducted using an alternative methodology, namely, propensity score matching approach (PSM), which is generally used to deal with selection bias (Rosenbaum & Rubin, Citation1983). Specifically, when the treated (School Level Insurance Dummy = 1) and non-treated (School Level Insurance Dummy = 0) groups are unbalanced with respect to covariates, the multilevel regression method could be biased. There are various ways of conducting PSM under multilevel data (Arpino & Cannas, Citation2016), including consideration of the multilevel feature at the propensity score calculation stage or at the matching stage. Following Arpino and Cannas (Citation2016), this study uses naïve PSM by clustering the standard errors at the school level. However, additional approaches proposed by Arpino and Cannas (Citation2016) cannot be applied to this study. The treatment variable in this study is at the school level; therefore, within-cluster matching is not applicable. Using the fixed effect model by including school dummies at the propensity score calculation stage is also not possible due to a large number of clusters (n = 95).

The choice of matching technique is important. This study uses the kernel matching method, as it allows more observations’ information to be considered. An individual belongs to the treated or control group depending on whether the school offers SAI (Yes = 1, No = 0). A counterfactual individual in the control group is constructed by giving more weight to similar individuals (Mensah et al., Citation2010). All observations with propensity scores not within the overlapping distribution are deleted. As the response variable is categorical, an ordered logit PSM model clustering standard errors by schools is applied.

4. Results

presents the causal impact of SAI on student SRHS under the baseline model: two-level ordered logit model. The variance between schools in the outcome suggests a significant amount of between-school variability in the SRHS of the students. Models 1 and 2 include the covariate Individual Level Insurance, and to avoid potential overlap between this variable and SAI, it is omitted in models 3 and 4. All four models indicate that SAI does not have a positive impact on student SRHS. However, Individual Level Insurance can significantly improve individual SRHS.Footnote2 The result is expected, as SAI is not tailored to student-specific needs. Students and parents are deprived of the right to choose insurance products providing a positive impact on health status.

Table 2. The impact of Student Accident Insurance on students' self-rated health status (SRHS).

shows that the lagged values of health and wellbeing are important predictors of current health status, as both have significant positive effects on student SRHS. The results indicate that male students have a higher level of SRHS compared to female students. This is consistent with the findings of previous research showing gender disparities in accessing health-promoting resources (Doyal, Citation2001). Students from wealthier families have better health conditions. This is consistent with earlier studies that showed that a high level of income is important for acquiring goods and services related to health promotion (Marmot, Citation2002).

shows the marginal effect at means of the impact of School Level Insurance Dummy and Individual Level Insurance on SRHS based on Model 2 in . The results indicate that participating in individual-level health insurance schemes significantly decreases the probability of individuals reporting SRHS as very poor, not very good, and moderate by 0.1pp (percentage point), 0.7pp, and 3.4pp, respectively, and it increases the probability of individuals reporting SRHS as good and very good by 0.4pp and 3.8pp, respectively. However, the impact of school-based SAI on SRHS is not significant at all levels of the response variable.

Table 3. Marginal effect at means of the impact of School Level Insurance Dummy and Individual Level Insurance on students' self-rated health status (SRHS)—multilevel ordered logit regression model.

presents the marginal effect at means of the impact of School Level Insurance Dummy and Individual Level Insurance on SRHS using an alternative approach: ordered logit PSM clustering the standard errors by schools. Both methods consistently indicate that participating in individual-level health insurance program significantly improves student SRHS, while no evidence indicates that school-based SAI improve SRHS of students.

Table 4. Marginal effect at means of the impact of School Level Insurance Dummy and Individual Level Insurance on students' self-rated health status (SRHS)—ordered logit PSM.

presents the balancing test of PSM estimation. The results show that the standardized mean difference of each covariate between the treated and control groups after matching is less than 7.3, which satisfies the rule of less than 10. This suggests that the two groups achieve good balancing (Rosenbaum & Rubin, Citation1985).

Table 5. Balancing test of PSM approach.

5. Conclusions

This study presents novel findings on the impact of school-based uniform private health insurance on SRHS of Chinese students, average age of 14 years old, using two approaches: a two-level ordered logit model and an ordered logit propensity score matching model clustering the standard errors by schools. This study does not find evidence that school-based uniform private insurance improves SRHS among Chinese secondary school students. However, individualized health insurance significantly improves SRHS of students. Present results are consistent with previous literature, where a positive effect of individualized health insurance on SRHS was observed (Baker et al., Citation2002; Dor et al., Citation2006; Hullegie & Klein, Citation2010). While previous studies focus on adult populations in developed countries, this study considers the children population in a developing country and finds similar conclusions. Private health insurance enables individuals to obtain optimal therapy regardless of age and nationality (Bhattacharya et al., Citation2003; Sriravindrarajah et al., Citation2020). Additionally, this study finds that uniform private health insurance has a negligible impact on student health status. This is inconsistent with a previous study which found a significant positive effect of private health insurance on health as mentioned above (Baker et al., Citation2002; Dor et al., Citation2006; Hullegie & Klein, Citation2010). The difference might be that the SAI in this study is not individualized, and the previous study concluded that private health insurance schemes can be valuable tools to improve health status if adapted to individual needs and preferences (Drechsler & Jutting, Citation2007). Uniform insurance policy for all students within the same school may lead to the low efficiency of resource allocation, and individuals cannot receive optimal therapy under the uniform policy.

It is important to distinguish the differences between private insurance and social insurance schemes. The former needs to be tailored at the individual level to meet individual needs. This study recommends that the government encourage schools to disseminate insurance information in an effort to increase student and parent willingness to purchase private health insurance products to protect against student health risks during critical times of growth and development. Additionally, recommending the minimum level of coverage of private health insurance or offering different policy options could be more effective than offering uniform insurance policies for all students. Individualization is a critical point to consider for other countries which would like to popularize private health insurance schemes among specific populations.

Disclosure statement

No potential conflict of interest was reported by the author.

Data availability statement

The data that support the findings of this study are available at [https://ceps.ruc.edu.cn/index.php?r=index/index&hl=en].

Notes

1 In March 2002, the Ministry of Education issued the ‘Treatment methods of Students' Injury Accidents’, which encourages students to voluntarily participate in accident insurance (Ministry of Education of People's Republic of China, Citation2002). On 26 July 2019, the Ministry of Education and five other departments issued ‘Opinions on Improving the Handling Mechanism for Safety Accidents and Maintaining the Order of School Education and Teaching’, which guides parents to purchase personal insurance for students (Ministry of Education of People's Republic of China, Citation2019).

2 There are discussions about whether the lagged value of dependent variables should be included in the multilevel model as a control variable (Allison, Citation2015). Therefore, a similar regression without considering lagged SRHS as covariant is conducted. The results do not change and are available upon request.

References

- Allison, P. (2015). Don't put lagged dependent variables in mixed models. https://statisticalhorizons.com/lagged-dependent-variables

- Arpino, B., & Cannas, M. (2016). Propensity score matching with clustered data. An application to the estimation of the impact of caesarean section on the Apgar score. Statistics in Medicine, 35(12), 2074–2091. https://doi.org/https://doi.org/10.1002/sim.6880

- Ayanian, J. Z., Kohler, B. A., Abe, T., & Epstein, A. M. (1993). The relation between health insurance coverage and clinical outcomes among women with breast cancer. New England Journal of Medicine, 329(5), 326–331. https://doi.org/https://doi.org/10.1056/NEJM199307293290507

- Baker, D. W., Sudano, J. J., Albert, J. M., Borawski, E. A., & Dor, A. (2001). Lack of health insurance and decline in overall health in late middle age. New England Journal of Medicine, 345(15), 1106–1112. https://doi.org/https://doi.org/10.1056/NEJMsa002887

- Baker, D. W., Sudano, J. J., Albert, J. M., Borawski, E. A., & Dor, A. (2002). Loss of health insurance and the risk for a decline in self-reported health and physical functioning. Medical Care, 40(11), 1126–1131. https://doi.org/https://doi.org/10.1097/00005650-200211000-00013

- Bania, N., Gray, J. A., & Stone, J. A. (2007). Growth, taxes, and government expenditures: Growth hills for US states. National Tax Journal, 60(2), 193–204. https://doi.org/https://doi.org/10.17310/ntj.2007.2.02

- Bhattacharjya, A. S., & Sapra, P. K. (2008). Health insurance in China and India: Segmented roles for public and private financing. Health Affairs (Project Hope)), 27(4), 1005–1015. https://doi.org/https://doi.org/10.1377/hlthaff.27.4.1005

- Bhattacharya, J., Goldman, D., & Sood, N. (2003). The link between public and private insurance and HIV-related mortality. Journal of Health Economics, 22(6), 1105–1122. https://doi.org/https://doi.org/10.1016/j.jhealeco.2003.07.001

- Breyer, F., Bundorf, M. K., & Pauly, M. V. (2011). Health care spending risk, health insurance, and payment to health plans. Handbook of Health Economics, 2, 691–762. https://doi.org/https://doi.org/10.1016/b978-0-444-53592-4.00011-6

- Brindis, C., Kapphahn, C., McCarter, V., & Wolfe, A. L. (1995). The impact of health insurance status on adolescents' utilization of school-based clinic services: Implications for health care reform. Journal of Adolescent Health, 16(1), 18–25. https://doi.org/https://doi.org/10.1016/1054-139X(95)94069-K

- Choi, W. I., Shi, H., Bian, Y., & Hu, H. (2018). Development of commercial health insurance in China: A systematic literature review. BioMed Research International, 2018, 3163746–3163718. https://doi.org/https://doi.org/10.1155/2018/3163746

- Colombo, F., Tapay, N. (2004). Private health insurance in OECD countries (OECD Health Working Papers No. 15). https://www.oecd-ilibrary.org/content/paper/527211067757

- Cox, E., Martin, B. C., Van Staa, T., Garbe, E., Siebert, U., & Johnson, M. L. (2009). Good research practices for comparative effectiveness research: Approaches to mitigate bias and confounding in the design of nonrandomized studies of treatment effects using secondary data sources: The international society for pharmacoeconomics and outcomes research good research practices for retrospective database analysis task force Report-Part II. Value in Health : The Journal of the International Society for Pharmacoeconomics and Outcomes Research, 12(8), 1053–1061. https://doi.org/https://doi.org/10.1111/j.1524-4733.2009.00601.x

- Danzon, P. (2002). Welfare effects of supplementary insurance: A comment. Journal of Health Economics, 21(5), 923–926. https://doi.org/https://doi.org/10.1016/S0167-6296(02)00060-7

- Doiron, D., Jones, G., & Savage, E. (2008). Healthy, wealthy and insured? The role of self-assessed health in the demand for private health insurance . Health Economics, 17(3), 317–334. https://doi.org/https://doi.org/10.1002/hec.1267

- Dor, A., Sudano, J., & Baker, D. W. (2006). The effect of private insurance on the health of older, working age adults: Evidence from the health and retirement study. Health Services Research, 41(3), 759–787. https://doi.org/https://doi.org/10.1111/j.1475-6773.2006.00513.x

- Dormont, B. (2019). Supplementary health insurance and regulation of healthcare systems. Oxford Research Encyclopedia of Economics and Finance. https://oxfordre.com/economics/view/10.1093/acrefore/9780190625979.001.0001/acrefore-9780190625979-e-115

- Doyal, L. (2001). Sex, gender, and health: The need for a new approach. BMJ, 323(7320), 1061–1063. https://doi.org/https://doi.org/10.1136/bmj.323.7320.1061

- Drechsler, D., & Jutting, J. (2007). Different countries, different needs: The role of private health insurance in developing countries. Journal of Health Politics, Policy and Law, 32(3), 497–534. https://doi.org/https://doi.org/10.1215/03616878-2007-012

- Guan, J., & Wang, G. (2017). Woguo tiyu baoxian de xianzhuang, pingjing yu tupo [The present situation, bottleneck and breakthrough of sports insurance in China. China Sport Science, 37(1), 81–89. https://doi.org/https://doi.org/10.16469/j.css.201701008

- Guan, J., Tena, J. D D. (2018). Do social medical insurance schemes improve children's health in China? (CRENoS Working Paper No. 201807). https://crenos.unica.it/crenos/sites/default/files/wp-18-07.pdf

- Hannum, E. C., Wang, M. (2010). Ethnicity, socioeconomic status, and social welfare in China (Language Minorities and Migration (ELMM) Network Working Paper Series No. 2). http://repository.upenn.edu/elmm/2

- Hansen, B. O., & Keiding, H. (2002). Alternative health insurance schemes: A welfare comparison. Journal of Health Economics, 21(5), 739–756. https://doi.org/https://doi.org/10.1016/S0167-6296(02)00062-0

- Hullegie, P., & Klein, T. J. (2010). The effect of private health insurance on medical care utilization and self-assessed health in Germany . Health Economics, 19(9), 1048–1062. https://doi.org/https://doi.org/10.1002/hec.1642

- Kawiorska, D. (2016). Healthcare in the light of the concept of welfare state regimes – comparative analysis of EU member states. Oeconomia Copernicana, 7(2), 187–206. https://doi.org/https://doi.org/10.12775/OeC.2016.012

- Liu, Z. (2005). Institution and inequality: The hukou system in China. Journal of Comparative Economics, 33(1), 133–157. https://doi.org/https://doi.org/10.1016/j.jce.2004.11.001

- Luo, J., & Wendel, F. C. (1999). Preparing for college: Senior high school education in China. NASSP Bulletin, 83(609), 57–68. https://doi.org/https://doi.org/10.1177/019263659908360909

- Luo, Z., & Yang, Y. (2003). Tan shangye baoxian buzhengdang jingzheng xingwei de jianguan: Dui yiqi xuepingxian xingzheng chufa de zhiyi yu sikao [The regulation on unfair competition of commercial insurance: Questioning and thinking about a case of administrative punishment of student accident insurance]. The Theory and Practice of Finance and Economics, 2003(5), 125–128. CNKI:SUN:CLSJ.0.2003-05-028

- Łyszczarz, B. (2016). Public-private mix and performance of health care systems in CEE and CIS countries. Oeconomia Copernicana, 7(2), 169–185. https://doi.org/https://doi.org/10.12775/OeC.2016.011

- Marmot, M. (2002). The influence of income on health: Views of an epidemiologist. Health Affairs, 21(2), 31–46. https://doi.org/https://doi.org/10.1377/hlthaff.21.2.31

- Mensah, J., Oppong, J. R., & Schmidt, C. M. (2010). Ghana's national health insurance scheme in the context of the health MDGs: An empirical evaluation using propensity score matching. Health Economics, 19(S1), 95–106. https://doi.org/https://doi.org/10.1002/hec.1633

- Ministry of Education of People's Republic of China. (2002). Treatment methods of students' injury accidents. http://old.moe.gov.cn/publicfiles/business/htmlfiles/moe/moe_27/201005/88522.html.

- Ministry of Education of People's Republic of China. (2019). Opinions on improving the handling mechanism for safety accidents and maintaining the order of school education and teaching. http://www.moe.gov.cn/srcsite/A02/s7049/201908/t20190819_394973.html.

- Nguyen, H., & Knowles, J. (2010). Demand for voluntary health insurance in developing countries: The case of Vietnam's school-age children and adolescent student health insurance program. Social Science & Medicine, 71(12), 2074–2082. https://doi.org/https://doi.org/10.1016/j.socscimed.2010.09.033

- Popkin, B., & Gordon-Larsen, P. (2004). The nutrition transition: Worldwide obesity dynamics and their determinants. International Journal of Obesity, 28(S3), S2–S9. https://doi.org/https://doi.org/10.1038/sj.ijo.0802804

- Rasciute, S., & Downward, P. (2010). Health or happiness? What is the impact of physical activity on the individual? Kyklos, 63(2), 256–270. https://doi.org/https://doi.org/10.1111/j.1467-6435.2010.00472.x

- Rosenbaum, P. R., & Rubin, D. B. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1), 41–55. https://doi.org/https://doi.org/10.2307/2335942

- Rosenbaum, P. R., & Rubin, D. B. (1985). Constructing a control group using multivariate matched sampling methods that incorporate the propensity score. The American Statistician, 39(1), 33–38. https://doi.org/https://doi.org/10.2307/2683903

- Rutten, F., Bleichrodt, H., Brouwer, W., Koopmanschap, M., & Schut, E. (2001). Handbook of health economics. Journal of Health Economics, 20(5), 855–879. https://doi.org/https://doi.org/10.1016/S0167-6296(01)00097-2

- Savedoff, W. D., & Gottret, P. (2008). Governing mandatory health insurance: Learning from experience. The World Bank. https://doi.org/https://doi.org/10.1596/978-0-8213-7548-8

- Shuaibu, M., & Oladayo, P. T. (2016). Determinants of human capital development in africa: A panel data analysis. Oeconomia Copernicana, 7(4), 523–549. https://doi.org/https://doi.org/10.12775/OeC.2016.030

- Smith, J. P., Shen, Y., Strauss, J., Zhe, Y., & Zhao, Y. (2012). The effects of childhood health on adult health and ses in China. Economic Development and Cultural Change, 61(1), 127–156. https://doi.org/https://doi.org/10.1086/666952

- Sriravindrarajah, A., Kotwal, S. S., Sen, S., McDonald, S., Jardine, M., Cass, A., & Gallagher, M. (2020). Impact of supplemental private health insurance on dialysis and outcomes. Internal Medicine Journal, 50(5), 542–549. https://doi.org/https://doi.org/10.1111/imj.14375

- Stabile, M., & Townsend, M. (2014). Supplementary private health insurance in national health insurance systems. Elsevier. https://doi.org/https://doi.org/10.1016/b978-0-12-375678-7.00924-x

- The State Council of the People's Republic of China. (2009). Deepening the reform of the medical and health care system. http://www.gov.cn/gongbao/content/2009/content_1284372.htm.

- Todd, J., Armon, C., Griggs, A., Poole, S., & Berman, S. (2006). Increased rates of morbidity, mortality, and charges for hospitalized children with public or no health insurance as compared with children with private insurance in Colorado and the United States. PEDIATRICS, 118(2), 577–585. https://doi.org/https://doi.org/10.1542/peds.2006-0162

- Wood, K. R. (2012). NCAA student-athlete health care: Antitrust concerns regarding the insurance coverage certification requirement. Indiana Health Law Review, 10(2), 562–627. https://heinonline.org/HOL/LandingPage?handle=hein.journals/inhealr510&div=522&id=&page= https://doi.org/https://doi.org/10.18060/18833

- Xu, Y. (2000). Jianli heli de xiaoxue sheng chuzhong fangshi - tigao jiunianzhi yiwujiaoyu zhiliang [Setting up rational ways for primary pupils to enter middle schools and improving the quality of compulsary education]. Journal of Henan Education Institute (Philosophy and Social Sciences), 19(4), 13–15. CNKI:SUN:HZJX.0.2000-04-004

- Ying, X. (2005). Xuepingxian: Zhongxiao xueshengmen de baohusan [School accident insurance: The safeguard for primary and secondary school students in China]. Financial Planner, 2005(9), 30–31. CNKI:SUN:DZLC.0.2005-09-020