Abstract

On January 1, 2018, IFRS 9 became effective in the EU. It introduced the expected credit loss model to allow for timely recognition of credit losses, estimated not only on the actual credit loss experience but also on forward looking information related to current loan portfolio. Although the transition to IFRS 9 should lead to increased impairments and decrease in banks’ equity, this effect is ambiguous in the settings characterised by combined effects of optimistic macroeconomic outlook and strong regulatory intervention related to extensive loan portfolio restructuring. This paper investigates day-one transition effect of IFRS 9 on level of loan impairments and total equity of banks in Slovenia, Eurozone country, which barely averted international bailout in 2013 by extensive state assisted bank restructuring. The comparative analysis is done on banks that transferred deteriorated loan portfolio to the state’s Bank Assets Management Company and all other banks. In line with expectations we find that banks without extensive asset portfolio improvements recognised additional loan impairments on transition to IFRS 9, whereas the opposite effect is observed for banks which performed state-assisted loan portfolio restructuring. Our study provides additional insight on the effect of institutional and regulatory setting on IFRS 9 implementation effects.

1. Introduction

On January 1, 2018, the new IFRS 9 Financial Instruments became effective in the EU. IFRS 9 introduced the new, more principle-based classification and measurement of financial instruments, the forward-looking expected loss impairment model of financial assets and new hedge accounting rules better aligned to risk management activities. All the above-mentioned changes also provide a direct response to the mandate given by G20 (Citation2009) to improve standards for the valuation of financial instruments to eliminate shortcomings induced by the 2008 financial crisis. In the accompanying press release Hans Hoogervors, chairman of the International Accounting Standards Board (IASB), stressed that ‘the new standard will enhance investor confidence in banks’ balance sheets and the financial system as a whole’ (International Financial Reporting Standards (IFRS), 2014).

Even before the 2008 financial crisis, financial instruments accounting regulation has been one of the most controversial areas in both anecdotal evidence and accounting literature. More specifically, the preceding International Accounting Standard (IAS) 39 has been criticised for excessive complexity of hedge accounting (Bernhardt, Erlinger, & Unterrainer, Citation2014; Duh, Hsu, & Alves, Citation2012) and its valuation opacity resulting from reduced comparability induced by its classification model (Panetta, et al. Citation2009). A fierce debate flared up between the proponents of the assertion that the mark-to-market valuation induces volatility and has a procyclical effect (e.g. European Central Bank [ECB], Citation2004; Novoa, Scarlata, & Solé, Citation2009; Panetta, et al. Citation2009) and its opponents (e.g. Laux & Leuz, Citation2010; Xie, Citation2016). However, at the outbreak of the 2008 financial crisis, the professional public had reached a high level of consent regarding the criticism of the IAS 39 incurred impairment model. Various international bodies asserted that the incurred loss model resulted in a delayed and insufficient recognition of banks’ credit losses and therefore directly contributed to the crisis (e.g. Financial Stability Forum, Citation2009; G20, Citation2009; Gaston & Song, Citation2014; Novoa, et al. Citation2009). Moreover, the expected loss impairment model gained support in light of the Basel regulatory regime, where any difference between loan loss provisions and expected losses must be covered with regulatory capital (Hamadi, Heinen, Linder, & Porumb, Citation2016).

Even though IASB claims it was not the incurred loss model to blame but conditions that enabled banks to postpone recognition of even inevitable loan losses for too long, IASB did ‘what the G20 wanted it to do’ (Hoogervorst, Citation2018) and developed the IFRS 9 in response to G20 requests. The new IFRS 9 requirements were initially welcomed, but doubts are arising regarding its impact on financial stability (European Banking Federation, Citation2017) and incidence of earnings management (Giner & Mora, Citation2019; Novotny-Farkas, Citation2016) especially related to managerial discretion in loan loss provisioning. As early simulations showed a significant negative effect of the January 1, 2018, transition to IFRS 9 on banks’ equity (e.g. Abad & Suarez, Citation2017; Krüger, Rösch, & Scheule, Citation2018), the Basel Committee on Banking Supervision (Citation2017) and the European Commission (Citation2016) became fearful of its negative impact on bank capitalization. Consequently, Regulation (EU) 2017/2395 on transitional arrangements for mitigating the impact on own funds was adopted.

To deeply understand the effects of IFRS 9 implementation, the European Parliament (Citation2016) requested the new standards’ implications be studied in-depth with a focus on the possible extension of fair value measurement brought by the new classification and measurement model and on the potential procyclical effect of the expected loss model.

Despite the anticipation of increased impairments and a negative effect on bank equity at transition to the Expected Credit Loss (ECL) model, some argue this effect is ambiguous as the forward-looking models provoke strong reactions to changes in the aggregate state of the economy (Abad & Suarez, Citation2017; Seitz, Dinh, & Rathgeber, Citation2018) and differ considerably between troubled and non-troubled banks, European countries and regions (Seitz et al., Citation2018). Consequently, contrary to general expectations the transition to IFRS 9 in a post bank recovery environment such as Slovenia, imbued with an optimistic outlook for economic growth, could all but result in a negative impact on banks’ equityFootnote1. Existing empirical evidence on actual day-one effect of transition to IFRS 9 is scarce and focused on global and/or systemic banks. Moreover, it is consistent with the forecasts indicating that on transition to IFRS 9 banks reported additional impairments and reduction of equity as compared to IAS 39 (European Banking Authority (EBA), 2018; EY, Citation2018; Deloitte, Citation2019), yet the magnitude of this effect varies both across institutions and different regulatory settings (KPMG, Citation2018). To the best of our knowledge, none of the existing studies has analysed the actual effect of the extensive state-assisted loan portfolio restructuring on the level of impairments and total banks’ equity on the transition from the incurred IAS 39 to the IFRS 9 expected credit loss model. The aim of the paper is therefore to investigate the effect of such restructuring on the day-one transition to IFRS 9 on the level of impairments and banks’ equity in a single regulatory setting.

To investigate the day-one transitional effect of IFRS 9 we use a population of banks in Slovenia, a Eurozone country, which barely averted international bailout in 2013 by state-assisted bank restructuring. We focus on the subgroup of banks which transferred their non-performing assets to Bank Assets Management Company in the period between 2014 and 2016. We analyse whether these banks report a significantly different day-one effect of IFRS 9 implementation on the level of impairments and bank’s equity as compared to banks that did not perform such extensive asset portfolio improvement.

In line with expectations we find that banks without extensive asset portfolio improvements recognised additional impairments of financial assets on transition to IFRS 9, whereas the opposite effect is observed for banks which performed extensive state-assisted loan portfolio restructuring. Our study contributes to the topical discussion in the field of financial accounting focusing on diverse effects of institutional and regulatory settings on IFRS 9 implementation.

The paper is further structured as follows. First, the transition to IFRS 9 is presented along with the existing empirical evidence of its effect on bank equity. Next, the specifics of the institutional setting for the new standard implementation in Slovenian banks are outlined. This is followed by the development of the setting-specific research questions, research hypotheses and the presentation of the study of the effect of IFRS 9 implementation on the level of loan impairments and equity of Slovenian banks. Following the methodology and results sections, the paper concludes with a discussion of the main findings, conclusion, limitations of the study and future research.

2. Transition to IFRS 9

The implementation of IFRS 9 introduced a new approach to the classification and measurement of financial instruments and a new impairment model. According to the new standard, classification (and consequently measurement) of a particular financial instrument is based on both business model (i.e. the way a bank manages a group of financial assets to achieve its business goals) and cash flow characteristics (i.e. the outcome of the contractual cash flow or Solely Payments of Principal and Interest (SPPI) test). Accordingly, financial assets are either classified as measured at amortised costs (solely SPPI instruments held to collect cash flows) or at fair value either through other comprehensive income (generally SPPI instruments held to collect or sell, with some exceptions) or though profit or loss (all other instruments).

As the new classification depends on selected business model and portfolio cash flow characteristics, the outcome regarding the fair value intensity is not straightforward (see ). A plausible anticipation posed by the European Systemic Risk Board (Citation2017) suggested that IFRS 9 application would not systematically increase the use of fair value in EU banks since they (unlike their US counterparts) typically grant loans as their quantitatively most important assets that are held to maturity.

Table 1. Measurement model for banks’ typical financial assets under IAS 39 and IFRS 9.

On transition to IFRS 9, the measurement basis changed for some financial instruments, most notably loans, which are non SPPI instruments, and those debt securities – SPPI instruments, which were originally classified as Available For Sale (AFS) as they did not meet the hold-to-maturity classification requirements, but are held under the hold to collect business model under IFRS 9. Such changes of measurement bases were directly reflected in equity-related categories: (a) in the case of financial assets originally carried at amortised cost and reclassified on transition to Fair Value Through Profit and Loss (FVTPL) or Fair Value through Other Comprehensive Income (FVOCI), the difference in carrying amount at transition date was recognised in bank equity as an adjustment to other comprehensive income or retained earnings as appropriate; (b) in the case of financial assets originally classified as AFS and reclassified to FVTPL at transition, the related cumulative revaluation reserve was relocated to retained earnings.

Transition from incurred to ECL model further contributed to changes in equity. According to IAS 39, an impairment loss of an asset measured at amortised cost occurred when the present value of estimated future cash flows fell below the asset’s carrying amount (IAS 39.63). However, impairment loss recognition required the occurrence of the loss event that adversely affected estimated future cash flows (IAS 39.58-59). To avoid potential earnings management through creation of hidden reserves, banks were prohibited to recognise losses due to unfavourable future events, no matter how likely. During the 2008 financial crisis it became clear that the restrictive impairment rules enabled banks to hide even unavoidable losses (Gebhardt & Novotny-Farkas, Citation2011), frequently by recognizing them just before loan defaulted (Hoogervorst, Citation2014).

The IFRS 9 impairment model no longer requires the occurrence of the loss event to recognise impairment loss. Conversely, for all AC and FVOCI assets the banks have to recognise expected credit losses from the initial recognition of an asset onwards. Furthermore, impairment occurs in three stages. As soon as a bank originates or purchases a financial instrument, impairment at Stage 1 is recognised. At this stage the bank has to recognise all credit losses that will occur if default occurs within 12-months. The amount of non-performing loans is related to bank-specific and macroeconomic determinants (Kjosevski, Petkovski & Naumovska, Citation2019). Expected credit loss is therefore estimated on all available information such as bank’s actual credit loss experience, forward looking information on payment status and macroeconomic variables (GDP growth, changes in unemployment rate, property prices etc.). If credit risk increases significantly, the bank has to recognise impairment at Stage 2. In this case loss allowance is increased to reflect the lifetime expected credit losses. Financial assets that are credit impaired – which is at the instant when the incurred loss event was also recorded under IAS 39 –continue to impairment at Stage 3. At this stage the bank continues to recognise lifetime expected credit losses but additionally recognises interest income only on net basis (as opposed to recognizing interest on gross basis at Stage 2).

Furthermore, IFRS 9 requires expected credit losses to be also recognised for bank off-balance sheet exposures, such as loan commitment and financial guarantee contracts, if those items are not measured at FVTPL. Provisioning of those items was originally regulated by IAS 37 – Provisions, Contingent Liabilities and Contingent Assets: balance sheet obligation was recognised only for amounts considerably likely to be drawn down at the balance sheet date. Under IFRS 9 banks have to also apply the ECL model on off-balance sheet exposures: they have to asses proportion of loan commitments, financial guaranties and similar off-balance sheet items, that is expected to be withdrawn within next 12 months (Stage 1) or over the remaining life (Stage 2 and 3). Thus, estimated expected credit losses are recognised as a separate liability line in balance sheet (e.g. as a provision), since amounts approved but not yet drawn down are not shown in any existing balance sheet item.

All in all, at transition to IFRS 9 the banks reclassified financial assets according to new requirements, determined impairments and provisions in line with the ECL model and adjusted retained earnings and other comprehensive income accordingly. Transitional adjustments resulted in current and/or deferred tax implications, which further affected bank equity.

3. The effect of IFRS 9 implementation on bank equity: a review of empirical evidence

Since banks implemented IFRS 9 only recently, the empirical evidence of its true effects is scarce. Encouraged by bank regulators, the vast majority of existing studies in the field estimate the day-one effect on financial stability, with the focus on ECL model impact on regulatory capital. Although initially the regulators expected significant reclassifications of financial instruments into the fair value measurement basis, the surveyed banks claimed from the very beginning that IFRS 9 classification and measurement requirements would not have a significant impact on capital requirements (EBA, Citation2016). Furthermore, the results of preliminary studies on the anticipated effect of IFRS 9 impairment model varied greatly between individual banks, showing an average anticipated day-one increase in impairments of financial assets between 18% (EBA, Citation2016) and 42% (European Systemic Risk Board, Citation2017), as compared to IAS 39.

Initially, a similar effect of transfer from incurred to ECL model was also anticipated in academic literature. Gomaa, Kanagaretnam, Mestelman and Shehata (Citation2019) used a controlled environment to find a potential increase in both level and sufficiency of periodic reserves. The authors reported this as the combined effect of two IFRS 9 related factors: (1) elimination of the minimum threshold condition for the recognition of financial assets impairment and (2) incorporation of the forward-looking information into the model.

Abad and Suarez (Citation2017) also anticipated an increase in credit loss provisions. However, using a model estimation on a typical portfolio of corporate loans by EU banks, they showed the IFRS 9 ECL model was more responsive to changes in economic conditions as compared to the IAS 39 incurred model. Therefore, the authors estimate that banks will be more capitalised in times of economic expansion and less in contraction periods, as compared to effects of the IAS 39 incurred loss model. Furthermore, Krüger et al. (Citation2018) showed this effect depends on asset portfolio quality also, as higher credit risk increases lifetime expected losses. Finally, Seitz et al. (Citation2018) combined both effects in an extensive simulation on European banking data from 2005 to 2014, which showed expected credit loss provisions to be highly sensitive to both economic conditions and asset portfolio quality.

As IFRS 9 became effective on January 1, 2018, the first evidence of its actual effect was available following the publication of financial statements for Q1, 2018. Results of these studies, focusing on the day-one impact on provisions, regulatory capital and equity of banks, indicate that the anticipated effects of IFRS 9 as reported in preliminary studies, were overestimated. Ernst & Young (EY, Citation2018) analysed IFRS 9 transition disclosures of 20 top-tier, global IFRS reporting banks. All but one German and two Canadian banks reported an increase in impairments of financial assets on transition to IFRS 9. However, banks claimed that reported impact was lower than expected before the transition due to early write-off policies, strong forward-looking macroeconomic conditions incorporated into impairment models, and reclassifications to FVTPL.

Loew, Schmidt and Thiel (Citation2019) conducted the most comprehensive study to date. On sample of 78 ECB’s supervised systemic banks, they observed on average −20 bps (with extremely high standard deviation of 145 bps) impact on regulatory capital, mostly due to increased impairments and provisions, on average reducing bank equity by 1.8%. The study also showed that banks reclassified only 4.6% of financial assets on average. Furthermore, out of 78 analysed banks, only 9 reported a positive combined effect of impairments of financial assets and provisions for off-balance sheet exposures on bank equity, including both Slovenian banks included in our sample (Abanka and Nova ljubljanska banka [NLB banka]). Khan and Damyanova (Citation2018) report similar results for the sample of 16 European banks with total assets exceeding 300 billion EUR.

The first available results therefore show that the majority of the biggest European banks reported a negative impact on bank equity, which is in line with Basel Committee on Banking Supervision (Citation2017) and the European Commission (Citation2016) predictions.

4. Institutional setting for IFRS 9 implementation in Slovenian banks

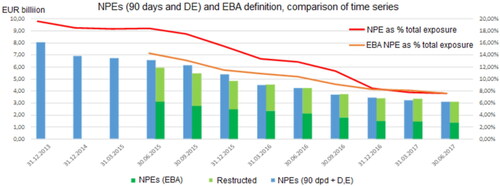

Non-performing exposures (NPEs) became the focus of the credit risk management for the majority of Slovenian banks in 2012 and 2013. The banking system’s NPE ratio rose to 19.5% at the end of 2013 and presented a systemic risk to financial stability. As performance of the banking system is highly dependent on the legal and institutional environment (Arias et al., Citation2020), the situation called for action by the supervisor, the Bank of Slovenia (Citation2017). Supervisory requirements and projects that particularly targeted banks’ NPEs were introduced. The major project in the field, undertaken by the Bank of Slovenia in cooperation with the Slovenian Ministry of Finance and monitored by the European Commission, the EBA and the ECB between June and December 2013, was a thorough review of the Slovenian banking sector (better known as the Asset Quality Review and Stress Test) which aimed to evaluate whether the Slovenian banking system was able to resist a three-year stress scenario of worsening macroeconomic conditions, and to assess the regulatory capital that would be required in such a scenario for each participating bank. The result of the Asset Quality Review called for additional impairments and provisions resulting in reduced banks’ equity. Bank portfolios, based on the Asset Quality Review were used in the second step – the Stress Test (Bank of Slovenia, Citation2015) − that assessed the projected capital shortfall for each of the participating banks. In total, eight Slovenian banks were selected for the Asset Quality Review and Stress Test: NLB banka, Nova kreditna banka Maribor [NKBM banka], Abanka, UniCredit Banka, Banka Celje, Hypo Alpe Adria Bank, Gorenjska Banka and Raiffeisen Banka. In terms of total assets these banks represented about 70% of the Slovenian banking sector and were chosen on the basis of the quality of their portfolios, market shares and capital adequacy. The stress test assessed the total forecasted capital shortfall for all the participating banks to be between 4.05 and 4.78 billion EUR.

The ensuing stability measures built on the outcomes of this comprehensive review comprised of (1) the transfer of deteriorated assets to the Bank Assets Management Company and (2) recapitalisation of the banks (Bank of Slovenia, Citation2013).

The Government of the Republic of Slovenia adopted the Act Defining the Measures of the Republic of Slovenia to Strengthen Bank Stability (the Bank Stability Act) in 2012 that called for the establishment of the Bank Assets Management Company [BAMC] in March 2013 to endorse stability of the financial system. The main activities of BAMC included the assessment of application for support, transfer of deteriorated assets and asset management (BAMC, Citation2019a). In line with the Bank Stability Act, BAMC acquired NPEs from four Slovenian banks with highest forecasted capital shortfall: NLB banka and NKBM banka in December 2013, Abanka in October 2014 and Banka Celje in December 2014. The total value of transferred non-performing assets of these banks amounted to 4.9 billion EUR and was completed at a transfer value of 1.57 billion EUR (BAMC, Citation2019b).

The recapitalisation of the Slovenian banks was the second measure taken to strengthen the stability of the banking sector. The Slovenian government recapitalised five banks in December 2013. The amount of recapitalisation was highest in NLB banka and totalled 1551 million EUR, followed by NKBM banka 870 million EUR, Abanka 348 million EUR, Factor banka 269 million EUR and Probanka 176 million EUR (Bank of Slovenia, Citation2015).

The Bank of Slovenia (Citation2017) reports that the NPEs of Slovenian banks further decreased during the post bank recovery period () as the result of additional transfers to the BAMC, write-offs, sale of claims and actual repayment.

Figure 1. NPEs of Slovenian banks between Dec 31, 2013 and June 30, 2017.

Notes: NPEs – Non-performing exposures; D,E – D and E rated default loan; EBA – European Banking Authority. Source: Bank of Slovenia, Citation2017.

The ensuing empirical analysis aims to answer the following research questions: (1) How did the implementation of the new standard affect the equity of Slovenian banks? (2) More specifically, how did the transition from the incurred to the ECL model affect the level of impairments of financial assets in Slovenian banks? and (3) Do the effects on total equity and level of impairments of financial assets differ between the banks where the Asset Quality Review revealed the highest forecasted capital shortfall which resulted in transfer of deteriorated assets to BAMC and other Slovenian banks?

Based on the described setting we set the following hypotheses:

H1: The effect of IFRS 9 implementation on total equity differs between the banks which transferred the deteriorated assets to BAMC and other Slovenian banks.

H2: The effect of IFRS 9 implementation on the level of loan impairments differs between the banks which transferred the deteriorated assets to BAMC and other Slovenian banks.

5. The effect of IFRS 9 implementation on Slovenian banks’ equity and level of impairments

5.1. Methodology

We measure the day-one impact of IFRS 9 implementation on equity of Slovenian banks and on the level of impairments. Day-one impact is measured by comparing the data from financial statements and notes as at December 31, 2017 (in accordance with IAS 39) and January 1, 2018 (in accordance with IFRS 9),Footnote2 available in individual audited annual reports.

The statement of changes in equity for year 2018 provides information on the opening balance of equity before restatement (December 31, 2017) and opening balance of equity for the reporting period after restatement (January 1, 2018). The difference between the two figures – the IFRS 9 related effects of changes in accounting policies – represents the total day-one impact on bank equity. Moreover, the statement of changes in equity disentangles the total IFRS 9 effect to two categories: retained earnings including profit/loss from current year and accumulated other comprehensive income.

The level of impairments is disclosed in the notes to the financial statements. Financial reports for year 2018 include a comprehensive section on IFRS 9 transition and disclosures upon the introduction of the new standardFootnote3. In this section, the cumulative effect of IFRS 9 on each of the two aforementioned equity-related categories is further divided and comprises of (positive or negative) effect of reclassification and measurement, effect of impairments and provisions, and effect of current and deferred taxes. Using additional disclosures on day-one provisions for off-balance sheet exposures, we further separate the effect of transition to the ECL model on provisions for off-balance sheet exposures from the effect of IFRS 9 transition on impairments of financial assets.

As at January 1, 2018, a total of 12 commercial banks were granted authorization to provide banking services under the Slovenian Banking Act. presents the list of commercial banks as at January 1, 2018, derived from the register of banks in Slovenia. The list is supplemented by information on total assets of individual banks and their (total assets based) market shares, derived from individual audited annual reports.

Table 2. Commercial banks in Slovenia, total assets and market shares as at January 1, 2018.

In three of the banks that were still operating in 2018 – namely Abanka, NLB banka and NKBM banka – the Asset Quality Review in 2013 revealed high capital shortfall which resulted in transfer of deteriorated assets to BAMC. On January 1, 2018, the total assets of this group of banks amounted to 17.25 billion EUR which represents a 49.1% market share.

We obtained the data for our analysis from audited annual reports of all 12 commercial banks. We identified the total effect of the transition to IFRS 9 on banks’ total equity and decomposed it to the following four components: (1) effect of reclassification and measurement, (2) effect of impairments of financial assets, (3) effect of provisions for off-balance sheet exposures, and (4) effect of current and deferred taxes. For three banks (Banka Sparkasse, SID banka and Unicredit banka) we identified the total effect on equity but were not able to decompose the cumulative effect into the four aforementioned components due to lack of disclosures (in two cases further disclosures of day-one transition were provided for retained earnings but not for accumulated other comprehensive income). Therefore, the final sample consists of 9 commercial banks, representing a vast majority (81.84%) of the Slovenian banking sector.

5.2. Results

The presentation of results in is aligned to the posed research questions as regards: (1) the total effect of day-one transition to IFRS 9 on equity of Slovenian banks, (2) the effect of transition from the incurred to the ECL model on the level of impairments, and (3) the differences between the banks with the worst Asset Quality Review results and other Slovenian banks.

Table 3. Effect of day-one transition to IFRS 9 on equity of Slovenian banks.

The results reveal a positive cumulative effect of IFRS 9 implementation on equity of the banks in the sample. On transition, the total equity increased by 10.9 million EUR, despite a strong negative effect (-50 million EUR) deriving from reclassification and measurement of assets. Within the combined positive effect of impairments, provisions and taxes (60.81 million EUR), the prevailing effect derives from impairments (36.9 million EUR). Contrary to expectations, the level of impairments of financial assets decreased at transition from the incurred to ECL model.

The relatively small cumulative effect on total equity is calculated as the sum of effects of all the banks in the sample. Doing this, the relatively large separate positive and negative effects of individual banks cancel out. In relation to the post bank recovery setting in Slovenia, the division of banks into two groups (where Group 1 consists of banks that transferred deteriorated assets to BAMC in 2013 and 2014; Group 2 includes all other banks) unveils an interesting finding: while banks from Group 2 recognised additional impairments of financial assets at day-one transition (resulting in a negative total effect on equity of 14.8 million EUR), the opposite effect (resulting in 51.8 million EUR increase of equity) was observed for banks in Group 1. Following the division, the impairments contribute the dominant effect on equity in both groups of banks at day-one transition to IFRS 9. Moreover, the analysis of the two groups reveals that the total effect on equity (10.9 million EUR) is the result of the positive effect of day-one transition to IFRS 9 in Group 1 (33.1 million EUR) and the negative effect in Group 2 (−22.2 million EUR).

To test hypotheses 1 and 2 and determine whether the differences between the mean values of effects of two groups are also statistically significant, we perform the Monte Carlo permutation test. As the use of t-test is inappropriate when sample sizes are very small (i.e. 3 banks in Group 1 and 6 banks in Group 2), Ludbrook and Dudley (Citation1998) recommend using the permutation test (also known as the randomization test), which determines the significance of mean value of parameter for Group 1 by randomly permuting the values of parameter. The advantage is that the test also provides accurate p-values even when the sampling distribution is skewed (Hesterberg, Moore, Monaghan, Clipson, & Epstein, Citation2005). The results in confirm Hypothesis 2 that the effect of IFRS 9 on the level of loan impairments differs between the banks which transferred the deteriorated assets to BAMC and other Slovenian banks. Moreover, statistically significant differences between the two groups of banks are also reported for the effect on provisions for off-balance sheet exposures. Hypothesis 1, that the effect of IFRS 9 on total equity differs between the two groups of banks was not confirmed, due to the strong, yet statistically insignificant, effect of reclassification and measurement of assets.

Table 4. Test for normality and Monte Carlo permutation test.

To test whether the impact of transition to IFRS 9 in Group 1 is a result of the deliberate overly aggressive impairment policies related to managerial discretion in the periods immediately prior the transition, we also analysed the dynamic of impairment losses and capital adequacy ratios of both groups in 2016 and 2017.

shows there is no significant difference in the level of impairment losses between the two groups of banks in the periods prior the transition to IFRS 9. Therefore, there is no evidence to suggest that banks in Group 1 reported positive effect on equity on the transition to IFRS 9 due to overly aggressive write-off policies in the periods immediately prior the transition as compared to write-off policies of banks in Group 2. Furthermore, Group 1 had statistically significantly higher capital adequacy ratios as compared to Group 2. Since their capital adequacy ratios were well above the minimum capital requirements, banks in Group 1 had no incentive to intentionally reverse impairment losses to report positive day-one impact of IFRS 9 implementation on equity to improve their regulatory capital.

Table 5. The dynamic of impairment losses and capital adequacy ratios of Slovenian banks prior to the IFRS 9 implementation.

As results of Group 2 are in line with expectations, the results of Group 1 represent a prominent finding and merit a viable explanation and context placement. Our evidence suggests that despite the anticipation of increased impairments and a negative effect on bank equity at transition to IFRS 9, actual effect depends not only on general macroeconomic environment but on the specifics of regulatory and institutional setting, too. Slovenian legislation, aimed at deleveraging and restructuring of Slovenian troubled banks through transfer of deteriorated assets to the BAMC and recapitalisation, resulted in decreased levels of NPEs in these banks which, in turn, resulted in a positive effect on bank equity at transition to IFRS 9 through the reversal of impairment losses.

6. Discussion

The study aimed to answer three setting-specific research questions involving (1) the effect of day-one IFRS 9 implementation on equity of Slovenian banks, (2) its effect on level of impairments, and (3) the assertion that differences exist between the banks that prior to IFRS 9 implementation transferred deteriorated assets to the BAMC and other Slovenian banks.

Overall, the day-one effect of IFRS 9 implementation on cumulative equity of the banks in the sample is positive (10.9 million EUR), but relatively small (0.04% of total assets of the banks in the sample). This is contrary to expectations as both early simulations and first post-adoption studies report a negative effect on equity at transition date (Abad & Suarez, Citation2017; Gomaa et al. Citation2019; Khan & Damyanova, Citation2018; Krüger et al., Citation2018). However, while Khan and Damyanova (Citation2018) report that only one bank in their sample of 16 selected large European banks reported a positive effect on equity, Sultanoğlu (Citation2018) predicted that Turkish banking industry would encounter opposite effects, primarily due to country-specific prudential regulation and a series of structural reforms performed during domestic and global financial crises. Similar to our study, her study provides evidence that IFRS 9 effects may not be in line with general predictions under country-specific settings.

Out of nine banks in our study, five reported a positive cumulative effect of impairments and provisions on bank equity (Abanka, NKBM banka and NLB banka from Group 1, Addiko banka and DBS from Group 2). Although not in line with expectations of IFRS 9 proponents, these findings are consistent with small, but increasing body of literature that suggests this effect is not straightforward. Existing studies provide evidence that forward-looking models provoke strong reactions to changes in economic conditions such as GDP growth, changes in unemployment rate, property prices etc. (Abad & Suarez, Citation2017; Seitz et al., Citation2018). As the projected growth of Slovenian GDP on January 1, 2018, (2019: 2.6%, 2020: 2.7%, 2021: 2.7%) exceeded the projected average growth at the EU level (2019: 1.4%, 2020: 1.4%, 2021: 1.4%) (European Commission, Citation2019) a better economic outlook represents a viable explanation for the lower level of impairments of financial assets as well as of provisions for off-balance sheet exposures in Slovenia.

Regarding the assertion that differences exist between the banks that prior to IFRS 9 implementation transferred their deteriorated assets to the BAMC and other Slovenian banks, statistically significant differences are reported for impairments and provisions. In line with expectations the effect of classification and measurement is not statistically significant because it depends on the business model of individual banks, which is not related to bank recovery.

7. Conclusion

As opposed to expected effects of IFRS 9 implementation, only scarce evidence exists on its actual effects. In line with the scope of individual studies different methodologies are used and different effects are presented. While Khan and Damyanova (Citation2018) focus on aggregate impact of IFRS 9 on banks’ equity, the EY (Citation2018) study focuses on changes in loan loss provisions and coverage ratios. The results of our study differ from the prevailing findings, indicating the existence of singularities related to institutional and regulatory setting that are worth investigating.

Our analysis sheds light on the role of bank restructuring on asset portfolio quality and, consequently, on the transitional effect of IFRS 9. We analyse banks in Slovenia, a Eurozone country, which barely prevented an international bailout in 2013. Out of nine, four banks (NLB banka, NKBM banka, Abanka and Banka CeljeFootnote4 - Group 1) were part of the bank restructuring process and significantly enhanced their asset portfolio quality by transfer of deteriorated assets to the newly established BAMC. On transition to IFRS 9 these banks reversed loan loss impairments, which empirically supports recent claims by Seitz et al. (Citation2018) and Krüger et al. (Citation2018) that the actual effect of IFRS 9 on impairments strongly depends on asset portfolio quality, especially at the time of favourable macroeconomic outlook.

8. Limitations and future research

In interpreting our findings, some limitations should be considered. Due to a lack of requested disclosures, three banks were excluded from our already small population of banks. Therefore, despite the relatively low market shares of these banks, our results do not provide a comprehensive effect of IFRS 9 implementation in Slovenian banking sector. Moreover, classification of the 9 studied banks into two groups resulted in extremely small sample sizes. As statistical literature is inconsistent as regards usage of t-test on extremely small samples, we conducted the permutation test to test the difference between the means of the two groups. Even though this method is recommended for use with such small samples, it still involves methodological limitation as it assumes that observations are exchangeable.

In the EU and other jurisdictions that adopted the IFRS, comparative analysis of individual IFRS effects across different settings (i.e. institutional, regulatory, industrial, geographical, cultural and economic) has been an important research area since the launching of the first global standards. As regards IFRS 9, an increasing body of research reports transition effects in selected, usually systemically important banks and/or in designated developed countries, however different authors use different approaches to studying the effects of the new standard, resulting in lack of comparability. A broader international study, using the same methodology across the banks in different countries would enable both comparison of the aggregate IFRS effect on banks’ equity as well as disentangling the total effect to its components, including reclassification and measurement, impairments and deferred taxes. Such study would provide a more in-depth perspective of the singularities of individual countries, originating in specific institutional and regulatory settings.

In the banking sector, impairments are influenced by two sets of approaches: IFRS and the Basel Regime that both influence banks’ loan loss provisioning practices. Gaston and Song (Citation2014) point out the diverging perspectives between accountants and bank supervisors in this regard and refer to this phenomenon as the dual-approach system. Although accountants are required to follow IFRS, their judgment may also be influenced by the rules-based bank regulation requirements, especially when using the ECL model and determining whether credit risk has increased significantly. Furthermore, the introduction of prudential bias in banks’ loan loss accounting may differ in different jurisdictions. A broader international comparative study, focusing on the role of bank regulation in IFRS 9 loan loss provisioning, would therefore be warranted.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 Unlike most existing studies (e.g. Loew, Schmidt and Thiel, 2019; EY, Citation2018; European Systemic Risk Board, 2017) our analysis is not focused on regulatory capital but on equity, as defined by IFRS Conceptual Framework for Financial Reporting. Throughout our study the term ‘equity’ is used consistently to avoid confusion with term ‘capital’ used for banks' capital measured according to EU Capital requirements regulation.

2 Any other method does not fulfill the ceteris paribus assumption as it entails adding new variables (economic conditions, size/structure/quality of asset portfolio, etc.) with particular effects on bank equity. Disentangling such composite effect to individual variables would result in less accurate findings.

3 Although IFRS 9 general principle on transition is retrospective application, all Slovenian banks used exception to recognise only differences between previous carrying amount and carrying amount at the beginning of the period in the opening retained earnings and/or other comprehensive income at January 1, 2018.

4 Banka Celje and Abanka merged in 2015.

References

- Abad, J., & Suarez, J. (2017). Assessing the cyclical implications of IFRS 9 – A recursive model. Occasional Paper Series, 12 (July). European Systemic Risk Board. https://doi.org/https://doi.org/10.2849/2685

- D'agostino, R. B., Belanger, A., & D'agostino, R. B. (1990). A suggestion for using powerful and informative tests of normality. The American Statistician, 44(4), 316–321. https://doi.org/https://doi.org/10.1080/00031305.1990.10475751

- Arias, J., Maquieira, C., & Jara, M. (2020). Do legal and institutional environments matter for banking system performance? Economic Research-Ekonomska Istraživanja, 33(1), 2203–2228. https://doi.org/https://doi.org/10.1080/1331677X.2019.1666023

- BAMC. (2019a). Short presentation (BAMC). http://www.dutb.eu/Lists/Articles/news-itemEN.aspx?ID=298&ContentTypeId=0x0100538800840CA7C64297DD192C5B41C270

- BAMC. (2019b). Transfer of non-performing assets. http://www.dutb.eu/en/history.aspx

- Bank of Slovenia. (2013). Full report on the comprehensive review of the banking system. Bank of Slovenia.

- Bank of Slovenia. (2015). Report of the Bank of Slovenia on the causes of the capital shortfalls of banks. Bank of Slovenia.

- Bank of Slovenia. (2017). Information on non-performing exposures [Press Release]. https://www.bsi.si/en/media/1162/pregled-dogajanja-na-podrocju-nedonosnih-izpostavljenosti

- Basel Committee on Banking Supervision (2017). Regulatory treatment of accounting provisions – interim approach and transitional arrangements. Bank for International Settlements.

- Bernhardt, T., Erlinger, D., & Unterrainer, L. (2014). IFRS 9: the new rules for hedge accounting from the risk management perspective. ACRN Journal of Finance and Risk Perspectives, 3(3), 53–66.

- Deloitte. (2019). After the first year of IFRS 9: Analysis of the initial impact on the large UK banks. https://www2.deloitte.com/uk/en/pages/financial-services/articles/after-the-first-year-of-ifrs-9.html

- Duh, R. R., Hsu, A. W., & Alves, P. A. P. (2012). The impact of IAS 39 on the risk-relevance of earnings volatility: Evidence from foreign banks cross-listed in the USA. Journal of Contemporary Accounting & Economics, 8(1), 23–38. https://doi.org/https://doi.org/10.1016/j.jcae.2012.03.002

- EBA. (2016). Report on results from the EBA impact assessment of IFRS 9. EBA.

- EBA. (2018). First Observations on the Impact and Implementation of IFRS 9 by EU Institutions. https://eba.europa.eu/documents/10180/2087449/Report+on+IFRS+9+impact+and+implementation.pdf

- European Banking Federation. (2017). EBF position on IFRS 9 transition period (Proposed Article 473a of CRR2). https://www.ebf.eu/wp-content/uploads/2017/04/EBF_026190-EBF-Position-on-IFRS-9-Transition-Period-Proposed-Article-….pdf

- European Central Bank. (2004). The impact of fair value accounting on the European banking sector – a financial stability perspective. European Central Bank.

- European Commission. (2016). Proposal for a Regulation of the European parliament and of the council amending Regulation (EU) No 575/2013. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM%3A2016%3A0850%3AFIN

- European Commission. (2019). Economic performances and forecasts. https://ec.europa.eu/info/business-economy-euro/economic-performance-and-forecasts_en

- Parliament, E. (2016). Resolution of 6 October 2016 on International Financial Reporting Standards: IFRS 9 (2016/2898(RSP)). http://www.europarl.europa.eu/doceo/document/TA-8-2016-0381_EN.html?redirect

- European Systemic Risk Board (ESRB). (2017). Financial stability implications of IFRS 9. https://www.esrb.europa.eu/pub/pdf/reports/20170717_fin_stab_imp_IFRS_9.en.pdf

- EY. (2018). IFRS 9 Expected Credit Loss: Making sense of the transition impact. Ernst & Young.

- Financial Stability Forum. (2009). Report of the Financial Stability Forum on addressing procyclicality in the financial system. Financial Stability Forum.

- G20. (2009). Declaration on strengthening the financial system. G20.

- Gaston, E., & Song, I. W. (2014). Supervisory roles in loan loss provisioning in countries implementing IFRS. IMF Working Papers, 14(170), 1. https://doi.org/https://doi.org/10.5089/9781484381120.001

- Gebhardt, G., & Novotny-Farkas, Z. (2011). Mandatory IFRS adoption and accounting quality of European banks. Journal of Business Finance & Accounting, 38(3-4), 289–333. https://doi.org/https://doi.org/10.1111/j.1468-5957.2011.02242.x

- Giner, B., & Mora, A. (2019). Bank loan loss accounting and its contracting effects: the new expected loss models. Accounting and Business Research, 49(6), 726–752. https://doi.org/https://doi.org/10.1080/00014788.2019.1609898

- Gomaa, M., Kanagaretnam, K., Mestelman, S., & Shehata, M. (2019). Testing the efficacy of replacing the incurred credit loss model with the expected credit loss model. European Accounting Review, 28(2), 309–334. https://doi.org/https://doi.org/10.1080/09638180.2018.1449660

- Hamadi, M., Heinen, A., Linder, S., & Porumb, V. A. (2016). Does Basel II affect the market valuation of discretionary loan loss provisions?. Journal of Banking & Finance, 70, 177–192. https://doi.org/https://doi.org/10.1016/j.jbankfin.2016.06.002

- Hesterberg, T., Moore, D. S., Monaghan, S., Clipson, A., & Epstein, R. (2005). Bootstrap methods and permutation tests. In D. S. Moore & G. McCabe (Eds.), Introduction to the Practice of Statistics, 2nd ed. W. H. Freeman.

- Hoogervorst, H. (2014). Closing the accounting chapter of the financial crisis [Speech]. https://www.ifrs.org/-/media/feature/news/speeches/2014/hans-hoogervorst-march-2014.pdf

- Hoogervorst, H. (2018). Are we ready for the next crisis? [Speech]. https://www.ifrs.org/news-and-events/2018/12/speech-are-we-ready-for-the-next-crisis/

- IFRS. (2014). IASB completes reform of financial instruments accounting. https://www.ifrs.org/news-and-events/2014/07/iasb-completes-reform-of-financial-instruments-accounting/

- Khan, E., & Damyanova, V. (2018). European banks’ capital survives new IFRS 9 accounting impact, but concerns remain. S&P Global Market Intelligence.

- Kjosevski, J., Petkovski, M., & Naumovska, E. (2019). Bank-specific and macroeconomic determinants of non-performing loans in the Republic of Macedonia: Comparative analysis of enterprise and household NPLs. Economic Research-Ekonomska Istraživanja, 32(1), 1185–1203. https://doi.org/https://doi.org/10.1080/1331677X.2019.1627894

- KPMG. (2018). IFRS 9: Transition impact on banks in the Gulf Cooperation Council. https://assets.kpmg/content/dam/kpmg/ae/pdf/IFRS9-transitionimpact-on-banks-in-the-GCC.pdf

- Krüger, S., Rösch, D., & Scheule, H. (2018). The impact of loan loss provisioning on bank capital requirements. Journal of Financial Stability, 36(C), 114–129. https://doi.org/https://doi.org/10.1016/j.jfs.2018.02.009

- Laux, C., & Leuz, C. (2010). Did fair-value accounting contribute to the financial crisis? Journal of Economic Perspectives, 24(1), 93–118. https://doi.org/https://doi.org/10.1257/jep.24.1.93

- Loew, E., Schmidt, L. E., Thiel, L. F. ( (2019). ). Accounting for financial instruments under IFRS 9 –First-time application effects on European banks’ balance sheets. EBI Working Paper Series, no. 48. https://doi.org/https://doi.org/10.2139/ssrn.3462299

- Ludbrook, J., & Dudley, H. (1998). Why permutation tests are superior to t and F tests in biomedical research. The American Statistician, 52(2), 127–132. https://doi.org/https://doi.org/10.1080/00031305.1998.10480551

- Novoa, A., Scarlata, J., Solé, J. (2009). Procyclicality and fair value accounting. Working Paper. WP 09/39. Washington: International Monetary Fund. https://doi.org/https://doi.org/10.5089/9781451871876.001

- Novotny-Farkas, Z. (2016). The interaction of the IFRS 9 expected loss approach with supervisory rules and implications for financial stability. Accounting in Europe, 13(2), 197–227. https://doi.org/https://doi.org/10.1080/17449480.2016.1210180

- Panetta, F., Angelini, P., Albertazzi, U., Columba, F., Cornacchia, W., Di Cesare, A., … Santini, G. (2009). Financial sector pro-cyclicality: Lessons from the crisis. Bank of Italy Occasional Paper, 44. Bank of Italy. https://doi.org/https://doi.org/10.2139/ssrn.1479499

- Seitz, B., Dinh, T., & Rathgeber, A. (2018). Understanding loan loss reserves under IFRS 9: A simulation-based approach. Advances in Quantitative Analysis of Finance and Accounting, 16, 311–357. https://doi.org/http://dx.doi.org/10.6293/AQAFA.201812_16.0010

- Sultanoğlu, B. (2018). Expected credit loss model by IFRS 9 and its possible early impacts on European and Turkish banking sector. Muhasebe Bilim Dünyası Dergisi, 20(3), 476–506. https://doi.org/https://doi.org/10.31460/mbdd.422581

- Xie, B. (2016). Does fair value accounting exacerbate the procyclicality of bank lending? Journal of Accounting Research, 54(1), 235–274. https://doi.org/https://doi.org/10.1111/1475-679X.12103