?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Although the growing body of literature that recognises a destabilising role of the trust crisis in the macroeconomic stability, the understanding of mediational pathways remains limited. The current paper fills the gap by contributing to the existing literature by examining closely the mediating effect of the trust crisis in the financial sector on the indicators of macroeconomic stability due to the anticipated impact of the financial intermediation development and the monetary policy transmission mechanism, as well as their combinatorial impact. A method of structural equation modelling was used to analyse the input data. It has been empirically confirmed that exacerbation of the trust crisis in the financial sector without the use of regulatory measures is detrimental to macroeconomic stability. The results of the mediation analysis show that transmission channels of the monetary policy mechanism and developed financial sector mitigate the harmful effects of deepening the trust crisis in the financial sector and lead to an increase in macroeconomic stability indicators. From a practical perspective, the findings revealed that interest, credit, and currency channels of the monetary policy transmission mechanism could be used to cope with the erosion of the trust crisis in the financial sector to macroeconomic stability.

1. Introduction

It is impossible to exaggerate the role of trust in the financial sector of the economy. Without trust, the financial system is deformed, and without a well-functioning financial system, it is impossible to ensure the macroeconomic stability and the potential for the country’s development. Lack of trust in banks or financial markets may undermine the functioning of macroeconomic systems in general and financial markets in particular. The global financial crisis, the inability of classical schools to explain its causes with high certainty, and the active development of behavioural finance theory have led to an increase in empirical studies of the influence of fundamental factors, including psychological ones, on the dynamics of macroeconomic stability and the development of the country. The main criticism of such studies, aimed at examining the interconnection of various aspects of behavioural finance, including public trust, confidence, optimism, is related to the difficulty of quantifying behavioural categories in the economy. Thus, even identifying the causes of behavioural distortions based on statistics and market data does not solve the problem of formalising their impact on the financial sector development or the economy as a whole.

Despite the fact that a growing body of literature recognises a destabilising role of the trust crisis in the macroeconomic stability and growth, the understanding of mediational pathways remains limited. The current paper fills the gap by contributing to the existing literature by examining closely the mediating effect of the trust crisis in the financial sector on the indicators of macroeconomic stability due to the anticipated impact of the financial intermediation development and the monetary policy transmission mechanism, as well as their combinatorial impact. There are few studies have been carried out where a trust or other behavioural variables such as loyalty, satisfaction, attitude were used as mediators. However, the undertaking study is unique in the sense that we incorporated two mediating variables such as financial intermediation development and the monetary policy transmission mechanism and examined the influence of these variables in a relationship of the trust crisis in the financial sector and macroeconomic stability in the Ukrainian context.

This investigation is salient and significant both from a theoretical and practical perspective in many folds. The reason for incorporating financial intermediation development and the monetary policy transmission mechanism dimensions is due to financial regulators’ ability to keep forcing the financial system to respond positively in the direction of its defence mechanism against deterioration of economic agents’ trust or their negative expectations. And thereby interest, credit, and currency channels of the monetary policy transmission mechanism as well as other instruments of a monetary policy intended to contribute to improved financial sector could be used to cope with the erosion of the trust crisis to macroeconomic stability.

The rest of this study is divided into sections as follows. The next section provides a theoretical background and develops hypotheses for this study. Second, the research design and method of analysis are discussed. This section outlines the methodological framework, data collection, and measure of the construct, as well as, model specification and identification. Third, data analysis and empirical results of direct and mediation models are presented. It is also performs hypothesised conceptual model testing. The last section concludes and provides directions for future research.

2. Conceptual background and hypotheses development

Considerable research has been conducted to understand what determines the macroeconomic stability of the country. One of the most common issues is related to social capital, intellectual resources, expectations and other social and psychological determinants in economic growth (Acedański & Włodarczyk, Citation2016; Golovchanskaya et al., Citation2018; Gros & Roth, Citation2010; Sapienza & Zingales, Citation2012; Tonkiss, Citation2009; etc.).

Santero and Westerlund (Citation1996) based on a study of 11 OECD countries for the period 1979–1995, using time cross-correlation coefficients and Granger’s causality test; demonstrate close causal relationships between consumer and business confidence indicators and key economic variables: gross domestic product (GDP), industrial production, real business investment, and real private consumption. Consumer and business confidence indicators for the countries studied were survey-based indicators, including composite indices for the United States (the Purchasing Managers index), Germany and Spain (Business Climate for both countries); a general indicator for Japan (Current Business Situation) and Belgium (Perspectives for the Total Economy); the expected trend of orders’ inflow for Canada and Denmark; and, for the rest of the countries, judgements about the future tendency of production. Regarding consumer confidence, a composite indicator is used for all countries. According to the research, they concluded that business confidence determines the economic situation in the country and can be used for future forecasting. However, the close relationship between business confidence indicators and macroeconomic status varies across countries. It has also been found that consumer confidence indicators are much less useful than business confidence indicators for economic analysis because of their weaker dependence on the production movement. According to Mazurek and Mielcová (Citation2017), consumer confidence index is a suitable predictor of economic growth or economic recessions, respectively. Their research is conducted based on US data for the period 1960–2015. For the study VAR models, including Granger causality tests, were employed.

It is common that structural macroeconomic models are used to build models and forecasts of macroeconomic indicators, which are interconnected functional systems of equations that describe different sectors of the economy. Such models can include several hundred and even thousands of variables and equations, often having interdependent variables. Thus, for analysing the business confidence predictive ability for investment growth, Khan and Upadhayaya (Citation2019) have used structural dependencies and found that business confidence leads US business investment growth, and structures investment, as well as exogenous shifts in business confidence, reflect short-lived non-fundamental factors, consistent with the ‘animal spirits’ view of investment.

Vector autoregression analysis is regarded as a simplified form of a structural model in which each variable regresses to its own past values and all other variables, including lags. Matsusaka and Sbordone (Citation1995) followed this method in 1995 to examine the link between consumer confidence and economic fluctuations. Consumer sentiment has been found to account for 13% to 26% of GDP decline. Utaka (Citation2003) empirically analyses whether consumer confidence affects the development of the Japanese economy using vector autoregressions. It is proved that in the cases of quarterly and monthly data, consumer confidence significantly influences the GDP fluctuations, whereas, in the case of annual data, it does not affect. In other words, consumer confidence only affects short-term economic fluctuations.

The aforementioned literature review supports that trust is a significant determinant of macroeconomic stability and influences economic growth (Błażejowski et al., Citation2019; Bützer et al., Citation2013). Thus, based on the author’s previous research (Bilan, Brychko, et al., Citation2019) and the empirical shreds of evidence mentioned earlier, researchers have formulated and tested the following hypothesis to state the association of the trust crisis in the financial sector and macroeconomic stability:

H1: The trust crisis in the financial sector is changing the consumer and investment behaviour of economic agents, contributing to destabilising processes in the country’s economy that leads to deteriorating macroeconomic stability indicators (direct effect model).

Of particular interest in modelling, structural equations are the direct and indirect (mediation) effects of the trust crisis in the financial sector on the macroeconomic stability. Thus, the mediation model allows to examine how deepening the trust crisis in the financial sector of the economy or recovering from it causes changes in one and/or several mediators, which in turn leads to a change in macroeconomic stability.

The financial system development from the financial intermediation perspective plays a decisive role in the mobilisation and redistribution of financial resources for productive activities, thereby contributing to the growth of the country’s economy. The role of systemically important banks (Buriak et al., Citation2015), imbalances in the financial sector (Vasilyeva et al., Citation2013), factors that are affecting the stability of financial system (Vasilyeva et al., Citation2016), determinants of alternative finance development (Bilan, Rubanov, et al., Citation2019) and the role financial knowledge of credit criteria on obtaining debt financing (Kljucnikov & Belas, Citation2016) have been studied. However, the institutional development of financial intermediation is the most closely linked to the destabilisation processes that occur in the financial sector of the economy due to the volatility of trust in it. Thus, the development of financial intermediation in Ukraine is in a state of institutional change, especially in recent years, which is due to the irrational behaviour of economic agents due to the volatility of the national currency and pessimistic sentiment due to information tensions about the liquidation of individual financial institutions. Furthermore, although the development of financial intermediation is adversely affected by a lack of trust in the financial sector, it may act as a buffer in terms of its ability to neutralise or minimise the volatility of the economic environment in Ukraine due to the trust crisis. Thus, based on the theoretical background, the following hypothesis is proposed to test the proposition of the mediating effect of financial sector development:

H2: Trust crisis in the financial sector has a negative but mitigating effect on the macroeconomic stability subject to the availability of developed financial sector in terms of advanced financial intermediation (the first mediating effect model).

There is no single unified approach to treating the economic impact of monetary policy impulses on major macroeconomic indicators of the country’s development, particularly among monetarists and Keynesians. Thus, Keynes (Citation1937) first formulates the concept of the transmission mechanism. Based on the aggregate demand equation, the impact of the transmission mechanism was explained, namely the change in the money supply through the interest rate channel, on investment costs and, as a result, the real volume of production. The current approach to interpreting the transmission mechanism is based on the transmission of impulses of changes in monetary policy instruments of the central bank transferred to the financial sector of the economy (the first stage), and subsequently, to the real sector of the economy (the second stage), through a different set of channels and links of diverse focus (Jiang & Wang, Citation2017). Thus, the monetary policy transmission mechanism makes it possible to remove the negative influence of the trust crisis in the financial sector on the macroeconomic stability owing different channels through which the monetary policy affects both the financial sector development and the real economy in countries. These allowed the following hypothesis to be formed:

H3: Trust crisis in the financial sector, mediated by the monetary policy transmission mechanism, has a negative but mitigating effect on the macroeconomic stability (the second mediating effect model).

Taking into account that the postulated model allows to study the mediating (indirect) effect of the trust crisis in the financial sector on the indicators of macroeconomic stability due to the anticipated impact of the financial intermediation development and the monetary policy transmission mechanism, as well as their combinatorial impact, the hypothesis parallel model of multiple mediating effects has been formulated as under:

H4: Channels of the monetary policy transmission mechanisms and developed financial sector could contribute to mitigating the negative effects of the trust crisis in the financial sector on the macroeconomic stability (parallel model of multiple mediating effects).

3. Research design and method of analysis

3.1. Methodological framework

The use of individual regression equations in economic research also has a number of limitations, the main among which is the absolute invariability of other arguments (factors) with even a significant change in another variable. However, any change in a phenomenon or process in an open economy directly or indirectly changes the whole system of interconnected traits. Consequently, creating a structural simultaneous equations system is high on the research in psychology and other social sciences. The benefit of structural equation modelling is that, unlike conventional multiple regressions, it is possible to construct, visualise, and test complex systems that are described by both observed and latent variables, whose internal structure is unknown.

Statistical verification analysis in this research was done through structural equation modelling using SEPATH (structural equation modelling and path analysis) of STATISTICA. Traditionally, researches apply five basic steps of structural equation modelling (Schumacker & Lomax, Citation2004). According to the proposed structural equation modelling approach, applying SEPATH STATISTICA the interconnection of financial intermediation development, monetary transmission mechanism, trust crisis, and macroeconomic stability implies the following algorithm:

sampling design and construct measurement;

model specification, which is developing a hypothesised conceptual model, specification exogenous and endogenous variables, establishing links, casual dependencies, and model graphical visualisation in order to reflect the functional and structural relationships between the studied systems of indicators (phenomena). This step is implemented by using a path diagram;

model identification;

model formation in the PATH system language, its software implementation towards model estimation that is the identification of multifactorial regression dependencies between exogenous and endogenous variables of macroeconomic stability, financial system development, the transmission mechanism of monetary policy and trust crises in the financial sector of the economy in order to reflect structural equations and provide them with an economic interpretation;

model testing, which is checking whether the data fit the model. Determining whether the model being tested should be accepted or rejected is based on fit indices, such as: minimising discrepancy function, maximum residual cosine, invariant under a constant scaling factor (ICSF) model criterion, invariant under changes of scale (ICS) model criterion, chi-square statistic (χ2), chi-square p-level, Steiger-Lind root mean square error of approximation fit index (Steiger-Lind RMSEA), root mean square standardised residual (RMS Standardized Residual) and others, as well as checking that the residuals of the model are subject to normal distribution law.

model modification in case of need the model improvement.

3.2. Data collection and measure of the construct

During structural equation system modelling, special attention should be paid to include all necessary variables and indicators, and only those that are relevant. In the opposite case, the conceptual model becoming overly cumbersome, misspecified, and having a lack of validity. Thus, the conceptual model should be designed as a simple structural model, incorporating all-important variables that consistent with the true model.

In recent years, there has been an increasing amount of literature on the relationship between trust in different social and economic institutions and macroeconomic indicators or the likelihood of financial crises and imbalances in the financial market. In order to quantify the subjective factors of behavioural finance such as trust, confidence, sentiments, etc., various consumer sentiment indices and economic confidence indicators like consumer confidence indicator, business confidence indicator, Chicago Booth/Kellogg School Financial Trust Index and The Centre for Risk, Banking and Financial Services Trust Index and other indicators, formed based on sociological surveys undertaken through written, telephone or oral interviews with respondents, have been widely used in international practice. By maintaining the commitment to these principles, in an attempt to quantify interpersonal trust (Gavurova et al., Citation2017), trust in authorities Transparency International Corruption Perception Index was used as a proxy (Mas’ud et al., Citation2019). Thus far, numerous studies that concentrate on measuring behaviour more frequently use questionnaire. That is, a single questionnaire measured trust in government (Çera et al., Citation2019; Oláh et al., Citation2019; Stevenson & Wolfers, Citation2011), trust in E-government (Ejdys et al., Citation2019), trust in public service delivery (Nor Zaini & Kuppusamy, Citation2017). The same approach for measuring trust in organisations in general (Oláh et al., Citation2017, Citation2019), and trust in management, trust in co-workers, trust in technologies for knowledge management (Dvorský et al., Citation2020; Smaliukienė et al., Citation2017; Virglerová, Citation2018) in particular, was used. Much of the previous research on the role of institutional (bank) trust (Buriak et al., Citation2019; Roth, Citation2009; Roth et al., Citation2012) in general, trust in banking business (Ahmed et al., Citation2017), customers’ trust in traditional banking (Skvarciany & Jurevičienė, Citation2017), trust on electronic banking (Belás et al., Citation2015; Vejačka & Štofa, Citation2017) in particular, was used either a set of formalised questions or existed indexes formed based on different questionnaires. Accordingly, a sharp decline in the confidence/sentiment indexes is seen as a trust crisis/collapse of trust/distrust. Other areas of research have been aimed at studying financial behavior (Shkvarchuk & Slav’yuk, Citation2019) and trust and cycles in the financial system (Brychko et al., Citation2019; Gazda, Citation2008) based on particularities of consumer’s consumption and investment. However, there are certain drawbacks associated with the use of questionnaires or indices derived from them. One of the main disadvantages is maintaining the representative sample.

As stated above, due to trust (confidence) indexes has a number of limitations, and, therefore, in order to identify the most influenced characteristics and test assumptions about the structure of trust crisis in the financial system, confirmatory factor analysis (CFA) was applied. Additional confirmation of construct validity of the trust crisis used in the study based on indicators that characterise the country’s financial system and therefore form an appropriate uncertainty level or trust crisis in it. CFA verified the suitability of selected variables to represent the latent variable – trust crisis in the financial sector. The selection of observed variables that describes the trust crisis in the financial sector was based on the individual-psychological perception by economic agents of negative news about destabilisation processes in the economic and financial development of the state. This hypothesis was strengthened by the empirical evidence that negative news provokes economic agents to change their preferences and/or make irrational investment decisions (Ulrike & Nagel, Citation2011; Ulrike et al., Citation2011).

Given the negative experience of Ukrainian society in depreciating savings as a result of significant inflation, economic agents usually perceive even a slight fall in the national currency as a signal of the country’s financial system destabilisation. Mass media and electronic exchange boards, notifying even small fluctuations of the national currency, put a destructive pressure on economic agents. Thus, information about the renewed plunge in the national currency exchange rate in 2009 from 5.05 to 7.99 hryvnias for one US dollar (devaluation was 58.12%) and in 2015 to 15.77 hryvnias for one dollar (devaluation was 97.28%) prompted economic agents to an early withdrawal of national currency deposits with further conversion of hryvnia savings into foreign currency outside the financial system. It could thus be seen as a lack of trust in the national currency and the financial system as a whole. Since 2014, the list of banks recognised as the most troubled financial institutions has started to be expanded. For the years 2014–2018, 104 banks were initially put into temporary administration and subsequently put into liquidation. Thus, the information that was distributed among the mass media about the banking system ‘clearing’ formed an outflow of time deposits and a strong demand, mainly for short-term demand deposits that may indicate the erosion of trust in the financial sector. The trust crisis in the financial system, and, accordingly, the change in money demand, along with exclusively monetary (banking) determinants, are shaped by non-monetary factors, among which the following can be noted: the political situation in the country, shadow economy, availability of financial services, financial literacy, unemployment rate, etc. (Gavurova et al., Citation2019). Recent empirical evidence suggests that as a result of the economic crisis, it is the indicators that characterise the real material economic situation of economic agents (employment, level of material security) to determine the systemic public trust, as well as for individual institutions (central bank, state authorities). The unemployment rate shapes the investment potential of economic agents and, unlike other subjective variables, is clearly defined and, where necessary, able to influence its size through various regulatory factors. Thus, the unemployment rate outside the natural range of 4%–5% may indicate a possible loss of trust.

Thus, the trust crisis in the financial system was measured using three negative news (components): (1) the devaluation of the national currency against the US dollar, (2) the number of Ukrainian banks, in respect of which a banking license has been revoked by the National Bank of Ukraine, and (3) the unemployment rate. Confirmatory factor analysis using the STATISTICA was applied to additional confirmation of the construct validity of items and constructs used in this study. Through several modifications, it was the combination of the above three indicators that formed 79% of the trust crisis in the financial sector.

There are also a vast number of recent studies on the macroeconomic stability and its determinants (Bilan, Lyeonov, et al., Citation2019; Bilan, Raišienė, et al., Citation2019; Bilan, Vasilyeva, Lyeonov, & Bagmet, Citation2019; Bilan, Vasilyeva, Lyulyov, & Pimonenko, Citation2019; Shvindina, Citation2019). This research confirmed and strengthened the conclusions that macroeconomic stability, as well as the trust crisis in the financial sector of the economy, is a multidimensional phenomenon, whose internal structure remains little known. Improving production efficiency, achieving full employment, maintaining stable prices, achieving equilibrium in foreign economic relations ensure the country’s macroeconomic stability, and further its economic growth. Thus, indicators of macroeconomic stability assessment of a country can serve statistics in the following areas: (1) country’s overall economic development (GDP, gross national product, gross investment, gross savings, the balance of payments and trade, employment and unemployment rates); (2) development of the financial and monetary sphere of the country’s economy (the size of the money supply and its structure, inflation, the national currency exchange rate, the central bank discount rate, the budget deficit and the amount of the internal and external debt).

Macroeconomic stability was measured using a GDP annual, the volume of industrial products (goods, services) sold, and Ukraine trade balance. The justification for using GDP as a proxy is based on similar contemporary studies which conducted cross-country analyses such as Bilan et al. (Citation2018), Kendiukhov and Tvaronavičienė (Citation2017), Kolodko (Citation1993), Moździerz (Citation2019), Naghshpour (Citation2019), Remeikiene et al. (Citation2018), Simionescu et al. (Citation2017), Zaman and Drcelic (Citation2009). For the macroeconomic stability construct in line with earlier studies such as Sadalia et al. (Citation2019), Santosa (Citation2018), the volume of industrial products (goods, services) sold was used as a proxy. Balance of trade or its components matches those used in earlier studies such as Marcel (Citation2019), Mihóková et al. (Citation2017), Rahman (Citation2019). Various modifications to the overall conceptual model based on confirmatory factor analysis identified that these three indicators describe 72% of the country’s macroeconomic stability.

The selection of indicators to assess the financial sector development was made based on its institutional structure from the financial intermediation perspective. Financial sector development, in agreement with earlier studies such as Duhnea et al. (Citation2017), Karkowska and Kravchuk (Citation2019), Leonov et al. (Citation2012, Citation2014), Skare and Porada-Rochoń (Citation2019), Skvarciany et al. (Citation2019), Vukovic et al. (Citation2017) was measured using the ratio of bank assets to GDP, the ratio of non-bank financial institutions assets to GDP, the ratio of securities trading to GDP that characterises the size of banking and non-banking financial and credit systems, as well as activity in the stock market. In general, according to the confirmatory factor analysis, the proposed indicators allow 72% to determine the financial sector development within the context of financial intermediation in the country.

The selection of indicators to describe the functioning of the monetary policy mechanism of the state was based on its transmission channels. A considerable amount of domestic and foreign literature has been published on transmission mechanisms of central banks (Janus, Citation2016; Pažický, Citation2018; Sicheng & Lingzhi, Citation2017) as well as macroprudential tools for the regulation of the financial sector (Vasylyeva et al., Citation2014). These studies are singled out the following channels: interest channel, credit channel, currency channel, expectation channel, inflation channel, asset price channel, as well as other specific channels developed by central banks, taking into account national peculiarities of the state and economic development of the country.

In the process of implementing the transfer mechanism of the credit channel, the forthcoming economic effect of monetary policy instruments expected to influence on the real sector of the economy and, accordingly, the macroeconomic stability of the country can be observed with some time lag. Credit channel research is represented by the identification of the expansionary monetary policy, which is directly reflected in the monetary base, the growth of which leads to increased liquidity of commercial banks and other monetary institutions, and further expansion of the credit supply (the first stage of monetary transmission), and therefore the development of the economic activity of economic entities (the second stage of monetary transmission). The selection of variables for the interest rate channel was based on identifying the most influential NBU interest rate policy instruments on the financial sector by changing short-term money market rates, and subsequently leading to changes in the real economy. Thus, being the basis for setting other official rates, adjusting the National Bank’s official discount rate leads to changes in the weighted average rate on all refinancing instruments and, accordingly, to adjusting the interest rates on national currency deposits and loans, which ensure stable development of the country’s economy in the medium and long term. Taking into account the national peculiarities of Ukrainian development, one of the most influential channels of the monetary policy transmission mechanism is the currency channel. The relevance of using this channel is due to the fact that the value of the national currency leads to changes in net exports, which is part of real GDP. In order to smooth the considerable amplitude and speed of changes in the national currency exchange rate against foreign currencies as well as to ensure price stability, the National Bank applies foreign exchange interventions by buying, selling, or exchanging foreign currency in the interbank foreign exchange market. In the process of modelling, the currency channel of the transmission mechanism is represented by the volume of gold and foreign exchange reserves in comparison with the previous year, which reflects the actions of the National Bank to smooth the functioning of the foreign exchange market (the first stage), and, accordingly, will contribute to the growth of macroeconomic stability of the country.

According to confirmatory factor analysis, selected indicators of interest, credit, and currency channels describe the effect of the monetary policy transmission mechanism by 91%. Expanding the transmission mechanism channels will lead to the development of financial intermediation in the first phase, and in the future, macroeconomic stability through the offsetting (minimisation) of the negative impact of the trust crisis in the financial sector of the economy.

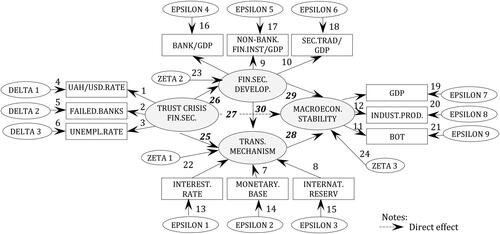

Therefore, the key indicators of the systemically important sectors generated the input data set: trust crisis (TRUST.CRISIS.FIN.SEC.), financial system development from a financial intermediation perspective (FIN.SEC.DEVELOP.), transmission mechanisms of monetary policy (TRANS.MECHANISM) and macroeconomic stability (MACROECON.STABILITY). These indicators are latent variables (constructs) that consist of a set of measurement items (also called as observed variables) presented in .

Table 1. List of latent and observed variables in the hypothesised conceptual model.

Due to the peculiarities of the constructs, three sources were used in generating the data. For the first endogenous (dependent) latent variable, i.e., transmission mechanisms of monetary policy, for which the interest rate, money supply and the volume of gold and foreign currency reserves compared to the previous year was used as proxies, the data was sourced from the official site of the National Bank of Ukraine. For the second endogenous (dependent) latent variable, that is macroeconomic stability, for which GDP annual, the volume of industrial products (goods, services) sold and Ukraine trade balance was used as proxies, the data was sourced from both the official site of the State Statistics Service of Ukraine and Ministry of Economy of Ukraine. For the third endogenous (dependent) latent variable, that is financial system development, for which ratio of bank assets to GDP, the ratio of non-bank financial institutions assets to GDP and ratio of securities trading to GDP was used as proxies, the data was sourced from both the official site of the National Bank of Ukraine and The National Commission on Securities and Stock Market. For the exogenous (independent) variable that is trust crisis in the financial sector of the economy, for which the hryvnia to U.S. dollar exchange rate in the interbank foreign exchange market, the number of Ukrainian banks, in respect of which the winding-up procedure was initiated, and the unemployment rate was used as proxies, the data was sourced from both the official site of the National Bank of Ukraine and State Statistics Service of Ukraine.

The statistics on the indicators selected for structural equation modelling were collected for the 17-year period, starting from 2002 to 2018.

3.3. Model specification

Based on a combination of theory and empirical studies from previous research, a hypothesised conceptual model is constructed to examine what determines macroeconomic stability. The variable of interest is the trust crisis since the objective of the paper is to study by which extend the trust crisis in the financial sector determines macroeconomic instability. Financial system development and transmission mechanisms serve both as source variables (due to direct impact on macroeconomic stability) and as result variables (due to dependence on trust crisis in the financial sector) in a chain of causal hypotheses. In other words, financial system development and transmission mechanisms are mediators between the trust crisis in the financial sector and macroeconomic stability.

Developed the theoretical framework model then should be conceptualised and communicated in graphical form with the help of a path diagram. A path diagram provides a visual form of all relationships in the model, in particular direct, mediating (indirect) effects, and other complex relationships among variables under investigation. One advantage of the path diagrams in SEM is that it avoids the problem of specification errors (Diamantopoulos, Citation1994; Diamantopoulos & Siguaw, Citation2000) due to ability graphical visualisation of omitted links, dependencies and excluded variables (Diamantopoulos, Citation1994).

presents the hypothesised conceptual model that reflects links between all theoretical variables and developed hypotheses. TRUST.CRISIS.FIN.SEC. has been chosen as an exogenous (independent) variable that has a direct impact on macroeconomic stability indicators (MACROECON.STABILITY) and indirect through the hypothesised effect on financial system development (FIN.SEC.DEVELOP.) and transmission mechanisms of monetary policy (TRANS.MECHANISM) that in turn identified as endogenous (dependent) latent variables.

Figure 1. Proposed conceptual model of direct and mediating influence of trust crisis in the financial sector on macroeconomic stability. Source: Author’s elaboration.

In , rectangular boxes are used to refer to observed variables that have been chosen for the formalisation of interactions between trust crisis, transmission mechanisms, macroeconomic stability, and financial system development from a financial intermediation perspective. The model in suggests that all variables enclosed by rectangular boxes are supposedly results of latent constructs. Circular or elliptical shapes are used to refer to latent constructs (also called latent variables) that are measured indirectly by observed variables indicated in above. In accordance with generally accepted view, the majority of real models the endogenous variables are not perfectly explained by the independent variables, and, also dependent on other factors that are not accounted for in the hypothesised conceptual model (error terms). Thus, ZETA 1, ZETA 2, and ZETA 3 represent a graphic display of disturbances (residuals of structural equations or ‘errors in equations’). EPSILON 1-9, DELTA 1-3 are considered as ‘errors in measurement’ and associated with unexplained their interrelationships and variances in the model.

Targeted effects identification, comprising factor loadings and path coefficients, deserves special attention, particularly at the stage of model specification and visualisation. In graphical visualisation (see ), directional arrows (→) are used to indicate targeted effects. In addition, directional arrows could be used for the identification of endogenous and exogenous variables. Dependent (endogenous) variables are those to which arrows are pointing. Whereas, exogenous (independent) variables are those having no arrows pointing to them. Factor loadings represent hypothesised casual conceptual directions from latent constructs to observed variables (in are shown by arrows 1–3, 7–12). It should be mentioned, factor loadings BANK/GDP, INTEREST.RATE and GDP on directional arrows do not have numbers in the row. Those mentioned above suggest that the program independently defined these parameters as fixed to a constant; that is, their factor loadings are equal to one. The path coefficients that determine the relationship between the latent variables are shown in by directional arrows 25–30. These model parameters are free and are subject to quantitative estimation from the data by the program. Thus, the directional effects shown in consist of nine factors loadings and six path coefficients. Overall, the 30 model parameters (6 path coefficients, 9 factor loadings, and 15 variances) depicted in were determined for estimation.

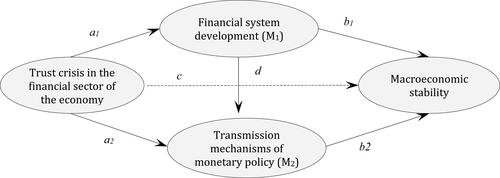

In case when financial sector development (M1) is a mediator of this relation, the trust crisis in the financial sector affects the financial sector development, and the financial sector developing, in turn, affects macroeconomic stability. Similar patterns are common to monetary policy transmission mechanisms (M2) as a mediator. That is, mediators – financial sector development (M1) and monetary policy transmission mechanisms (M2) are intermediaries, links in a causal chain. Therefore, if the effect of the trust crisis in the financial sector on mediators, or the effect of mediators on macroeconomic stability, or both, blocked, the relation of the trust crisis in the financial sector with the macroeconomic stability would be weakened (or possibly even eliminated).

In , the letters on the path arrows represent partial regression coefficients for the relation between the two variables connected by the path arrow: a1 and a2 represent the effect of the trust crisis in the financial sector on financial sector development (M1) and monetary policy transmission mechanisms (M2), respectively; b1 and b2 represent the effect of financial sector development (M1) and monetary policy transmission mechanisms (M2) on the macroeconomic stability, holding the trust crisis in the financial sector constant; and c represent the effect of the trust crisis in the financial sector on the macroeconomic stability, holding financial sector development (M1) and monetary policy transmission mechanisms (M2) constant. Thus, regression-predicting mediators with the trust crisis in the financial sector will yield the parameter estimates for a1 and a2; regression predicting the macroeconomic stability simultaneously with mediators and the trust crisis in the financial sector will yield the parameter estimates for b1, b2 and c, respectively, expressed in a standardised form (betas).

Figure 2. Graphical representation of the mediation model of the study. Source: Author’s elaboration.

The mediation (indirect) effect is the product of the regression coefficient a times regression coefficient b. First and second mediation effects can be written as follows:

(1)

(1)

The direct effect is unmediated, and according to , represented by the coefficient (the parameter estimates) c. Thus, direct effects can be written as follows:

(2)

(2)

The total mediation effect (parallel model of multiple mediating effects) is the sum of indirect effects, while total effect (TE) of the trust crisis in the financial sector on the macroeconomic stability is a sum of the indirect effects plus the direct effect:

(3)

(3)

A number of statistical tests have been developed to support (measure) mediation. In most recent studies, simpler and more rapid statistical tests such as the Sobel method (also known as z-test) and its variants for support mediation have been used. Sobel test may be calculated by dividing the value of mediation effect (a1b1 or a2b2) by the standard error of their product (SEa1b1 or SEa2b2) (Sobel Citation1982a):

(4)

(4)

When following Goodman (Citation1960), the standard error of the product ab (a1b1 or a2b2) can be estimated based on unstandardised estimates for a and b with the following expression:

(5)

(5)

Once the z-test has been calculated, a p-value from a normal probability table may be found. For the 0.05 significance level, the empirical critical z-test value is 1.96 based on normal theory. Any z-test value less than this would be interpreted as rejecting the hypothesis of the mediation effect. MacKinnon et al. (Citation2002) made an attempt to improve the Sobel test (Sobel Citation1982a). For this purpose, z’-test for the non-normal shape of the sampling distribution was developed. For p-value 0.05, the empirical critical z’-test value is proposed to be 0.97.

3.4. Model identification

Before a software implementation of SEM, it is crucial to resolve the identification problem. For subsequent estimation model should be just identified or over-identified (Ullman, Citation1996; Woody, Citation2011). That means that the number of parameters to be estimated should be less the number of variances and covariances of observed variables for covariance structure models (Hoyle, Citation1995). Raykov and Marcoulides (Citation2000) offer a simplified approach to determining an identification status of a model based on the calculation of the degrees of freedom that is derived by taking the difference between a number of non-redundant elements in the sample correlation matrix and the number of observed variables in the model. The following formula is used to determine the number of non-redundant elements in the sample correlation matrix (E):

(6)

(6)

where р − the number of observed variables in the model.

Based on the hypothesised conceptual model shown in and , thirty observed (manifested) variables are used. Thus, the number of non-redundant elements in the sample correlation matrix is equal to 12 (12 + 1)/2 = 78, then, the degrees of freedom constitutes 78 − 30 = 48.

Since the difference between the number of variances and covariances of observed variables for the covariance matrix and the number of parameters to be estimated is positive, the hypothesised conceptual model of structural modelling the relationship between trust crisis in the financial sector and macroeconomic stability is considered to be over identified. The essential point, in this case, is to select one of a number of possible solutions that best explains the observed data (perfect model-data fit) given a certain estimation criterion (maximum likelihood) (Kelloway, Citation1998; Lei & Wu, Citation2007). In the opposite extreme (case), when the degree of freedom is negative, the conceptual model is said to be under-identified (Maruyama, Citation1998). This fact illustrates the inability to determine one unique or a number of possible solutions values for the model coefficients due to the insufficiency of empirical information provided.

4. Empirical results and discussion

To generate numerical values for the free parameters, the model estimation should be carried out. The estimation process of the free parameters involves iterative procedures to minimise the difference between the sample covariance matrix, and the model implied covariance matrix. In order to estimate the model parameters, several discrepancy functions could be used. Publications that concentrate on SEM in social science more frequently use maximum likelihood (Ohunakin et al., Citation2018), generalised (Ejdys et al., Citation2019; Indartono & Faraz, Citation2019; Obidjon et al., Citation2017), partial (Nor Zainal & Kuppusamy, Citation2017; Alnsour, Citation2018; Hu et al., Citation2019; Victor et al., Citation2019) and weighted least squares (Suifan, Citation2019).

Statistical significance of parameter estimates is presented in .

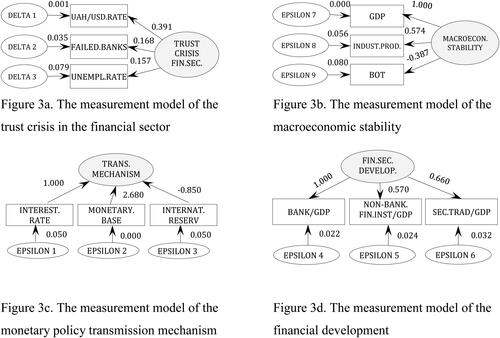

Figure 3. Output path diagrams. (a) The measurement model of the trust crisis in the financial sector. (b) The measurement model of the macroeconomic stability. (c) The measurement model of the monetary policy transmission mechanism. (d) The measurement model of the financial development. Source: Created by the authors based on their own calculation.

The results ascertained that any potential exacerbation of the trust crisis in the financial sector ensure national currency depreciation against the US dollar, a rise in the number of Ukrainian banks, in respect of which the winding-up procedure was initiated, and the unemployment rate accordingly. The outcome of the analysis shows that the coefficient of value the hryvnia to the US dollar exchange rate in the interbank foreign exchange market is the highest among all, which is 0.391. This authenticates the evidence that the hryvnia exchange rate on the interbank foreign exchange market to the US dollar is clearly more volatile. That explains the anomalous currency fluctuations caused by both rational and irrational factors related to the panic sentiment of economic agents. The number of Ukrainian banks, in respect of which the winding-up procedure was initiated (0.168) is the second most significant factor, which is influenced by the trust crisis in the financial sector and followed by the unemployment rate (0.157).

According to obtained results, the expansion of the transmission mechanism channels by one p.p. increases discount rate and the monetary base by 1.000 p.p. and 2.680 p.p. accordingly, and the decrease of foreign exchange reserves by 0.850 p.p. Findings of such minor reaction of the interest rate changes give us insights on the relative limited regulatory influence of the National bank of Ukraine and deformation of the interest rate channel. The best multiplier effect of the transmission mechanism is the credit channel, which leads to the accumulation of sufficient liquidity by banking institutions and an increase in the nominal income of economic agents.

This work has revealed several relations and interdependencies that are responsible for financial sector development in financial intermediation perspective. Thus, an increase in the rate of growth of financial intermediation per unit leads to an increase in the ratio of banks’ assets to GDP by 1.000 p.p., the ratio of non-banking financial institutions’ assets to GDP by 0.570 p.p., and the ratio of securities trading to GDP by 0.660 p.p., respectively. It should be noted that the ratio of banks’ assets to GDP is most in relative terms responds to the development of financial intermediation. This is evidenced by a bank-centric financial system in Ukraine with a low level of the securities market and non-bank financial institutions’ development.

The growth of the economy, expressed by the growth of GDP, is ensured by macroeconomic stability, which is characterised by the stability of the financial and monetary parameters of the national economy over time. A positive link is also observed between ensuring macroeconomic stability and the volume of industrial output sold. Thus, ensuring macroeconomic stability at 1.000 p.p. provides an increase in the volume of manufacture and sale of industrial goods and services by 0.574 pp. However, increasing macroeconomic stability leads to a decrease in the country’s trade balance (−0.387). This may be explained by the surplus of imported products over exports due to the growth of economic agents’ income.

4.1. Direct effect analysis

The result of the structural model is presented in .

Table 2. Hypotheses testing summary.

The analysis showed a direct effect from the leading indicators characterising the level of trust crisis in the financial sector to the monetary policy transmission mechanism. The research suggested that a 1.000 p.p. increase in the trust crisis in the financial sector would translate into a 0.103 p.p. expansion of the monetary policy transmission mechanism channels. That is, increase in exchange rate hryvnia to US dollar in the interbank foreign exchange market, a number of Ukrainian banks, in respect of which a banking license has been revoked by the National Bank of Ukraine and the unemployment rate leads to the increased interest rate, money supply, and decreased volume of the National Bank of Ukraine gold and foreign currency reserves. This situation can be explained by the fact that in the conditions of socio-economic upheavals that result in erosion of trust in the financial sector, the state uses various monetary policy instruments that lead to the expansion of its channels, in particular, interest and credit.

In case of an increase in the trust crisis in the financial sector by one p.p., the level of financial intermediation development decrease by 0.480 p.p. That is, the social tensions that occur in the financial sector of the economy lead to a decrease in the assets of banks and non-bank financial institutions, as well as a decrease in trading volumes in the stock market. Using the monetary policy transmission mechanism, that is, by expanding its channels by 1.000 p.p., the rate of financial intermediation development increases four times, which accordingly negates the negative effect of erosion of public trust in the financial sector of the economy. Thus, exacerbation of the trust crisis in the financial sector leads to the degradation of financial intermediation development, which can be fully offset by the transmission mechanisms of monetary policy. These findings confirm the positive impact of the monetary policy transmission mechanism in the first stage on the financial system of the country (the development of financial intermediation), and subsequently on the indicators of macroeconomic stability.

As our initial hypothesis, it was determined that an increase in the trust crisis in the financial sector and the level of financial intermediation development by 1.000 p.p., the macroeconomic situation in Ukraine deteriorates by 0.127 and 0.496 p.p., respectively. The negative impact of financial intermediation development on macroeconomic stability indicators can be explained by the significant financialisation of the country’s economy, which exacerbates the risks of financial instability and stimulates economic agents’ panic. While expanding the credit, interest and currency channels of the monetary policy transmission mechanism by 1.000 p.p. leads to an increase in the macroeconomic stability indicators by 3.458 p.p. Thus, expanding the transmission mechanism channels can fully offset the negative impact of the trust crisis in the financial sector and the significant financialisation of the country’s economy.

4.2. Indirect effect (mediation) analysis

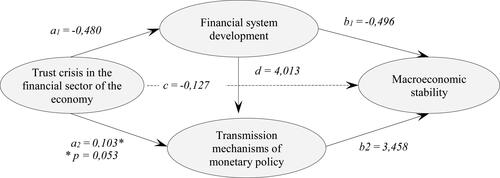

This current study, however, is aimed mainly at identifying the mediation model. shows the visualising direct effect and mediation model (indirect effect) proposed by the researchers, together with the standardised regression coefficients estimated from the data.

Figure 4. Graphical representation of the mediation model of the study with path coefficients. Source: Created by the authors based on their own calculation.

reports the results for the mediation model (indirect effect) depicted in .

Table 3. Mediating effects and hypotheses testing summary.

For the measurement of indirect (mediation) effect analysis, we employed a Sobel test (Sobel Citation1982b). The results of exhibited the significant impact of the financial sector development (M1) and monetary policy transmission mechanisms (M2) as mediating variables between the trust crisis in the financial sector and the macroeconomic stability. Hence, the decisions of null hypotheses H2 and H3 have been supported. The single most striking observation to emerge from the data that stands out in was the positive mediation effect of the trust crisis in the financial sector on the macroeconomic stability through the financial sector development (M1) is formed by two negative path coefficients. Thus, any lack of trust (the trust crisis) in the financial system significantly impairs its functioning or even undermine the system as a whole (a1 = −0.480). Meanwhile, the expansion of the financial system contributes to the increased risk of the large-scale financial crisis that is the barrier to economic growth and macroeconomic stability (b1 = −0.496). In general, however, a one standard deviation increase in the trust crisis in the financial sector could expect the causal chain through the financial sector development to yield an increase in the macroeconomic stability of 0.238 standard deviations (p = 0.002).

The unmediated (direct) effect, as can be seen from above, is −0.127 (p = 0.038). This implies that a one standard deviation increases in the trust crisis in the financial sector, through other processes, distinct from whatever financial sector development (M1) and monetary policy transmission mechanisms (M2) transmits, would yield decrease the macroeconomic stability indicators of 0.127 standard deviations. Thus, the results obtained confirm that exacerbation of the trust crisis in the financial sector destabilises the economic situation in the country. Thus, hypothesis H1 is accepted.

The total mediation effect (parallel model of multiple mediating effects) introduced by the sum of indirect effects is about 0.594. Thus, this positive relationship confirmed that hypothesis H4 was supported. These results suggest that a one standard deviation increase in the trust crisis in the financial sector could expect the causal chain through the monetary policy transmission mechanisms and financial sector development to yield an increase in the macroeconomic stability of 0.594 standard deviations. Taken together, the total effect of the trust crisis in the financial sector on macroeconomic stability is 0.467. Thus, when considered direct effect as a mediated effect in which the relevant mediators have yet to be discovered or specified in the model, the total effect indicates positive mediation of financial sector development (M1) and monetary policy transmission mechanisms (M2), while other processes (or mechanisms) distinct from them have a negative mediation in the relation between the trust crisis in the financial sector and the macroeconomic stability.

In particular, the positive impact of the monetary policy transmission mechanism on the financial system development in terms of financial intermediation should be noted (d = 4.013, p = 0.046). This conclusion confirms the need for effective and transparent monetary policy in order to achieve stability of the macroeconomic environment in Ukraine with the previous development of financial intermediation in the country. Thus, the expansion of the interest rate channel, mediated by changes in interest rate policy, the credit channel, which determines the volume of bank lending, and the currency channel, which characterises foreign exchange interventions, causes the accumulation by financial companies (banking and non-bank financial and credit institutions) sufficient liquidity volumes that leads to an increase in the level of financial intermediation.

It is also important to note that when the connection (causal link) between the transmission mechanism of monetary policy and financial sector development is eliminated in the second and third stages of structural equation modelling (), the structural and functional connections of the whole system (model) cannot be traced, in that sense, they are insignificant. This indicates that the components of the system are selected appropriately, the internal and external connections and links are established correctly, and therefore exclusion from the model of one or more components (links, dependencies and/or variables) leads to the collapse of the whole system which implies that the hypothesised conceptual model is an inadequate and requires significant and urgent changes.

4.3. Model testing

Once the parameters of the hypothesised conceptual model have been estimated, the next step of structural equation modelling is to determine whether the model being tested fits the data. Based on this information, the dichotomous decision about the hypothesised conceptual model should be either accepted or rejected. For this purpose, a number of fit indices have been developed.

STATISTICA independently performs the model testing, that is, checks its adequacy with the help of a set of proposed criteria. The path diagram depicted in shows a conceptual model of structural analysis, which was created on the basis of repeated testing and improvement after verification and confirmation of alternative hypotheses for the relationship between constructs and observed variables.

A higher degree of the constructed structural model adequacy is achieved with minimal values of the discrepancy function. It should be noted that the iterative process has been converged: the program conducted 22 iterations, which resulted in the minimisation of the discrepancy function, which characterises a sufficient level of quality modelling of structural equations. Maximum Residual Cosine is a numerical criterion that should be minimised in the interactions process for a good fit. In this study, the iteration process was successful because the calculated Maximum Residual Cosine value is close to zero. Chi-square statistics () is the most common absolute test of model fit that determines whether the model is plausible in the population.

should be close to zero in order to confirm the absence of a model specification error. However, it is established that the Chi-Square Statistic is quite sensitive to sample size. This means that chi-square statistics may reject the proposed model due to the large sample size, even when the model fits the data reasonably well. Accordingly, given the large sample size and the number of observations,

tends to increase, and therefore the Chi-square statistic could not be used as the sole criterion for model selection. Chi-Square p-level is used to test the null hypothesis that the model fits the data. In this study, the Chi-square p-level reaches zero, and therefore the constructed model is considered adequate (correctly specified; that is, the constructed regression equations adequately describe the structural relationships of the complex system.

ICSF Criterion and ICS Criterion are measures of the structural model invariance under a constant scaling factor (ICSF) or changes of scale (ICS). These criteria should be close to zero. Since the calculated values of the ICSF and ICS criteria are close to zero, the proposed model is invariant under both a constant scaling factor and changes of scale.

In recent years as a reaction to sample size sensitivity problems, attention to the alternative goodness-of-fit indices has been focused (). Steiger-Lind RMSEA evaluates the quality of the model fit. The point estimate of the calculated index for the proposed model exceeds the normative value of 0.05 and therefore indicates insufficient fit given the analysis of the lower 90% and upper 90% boundaries of the confidence interval. The value of RMS Standardized Residual is 0.258. This testifies to the rather good quality of model improvement, taking into account the complexity and interdependence of the studied interrelations of the socio-economic system. Thus, when considering the modelling of complex systems, it is considered that the constructed model does not adequately describe the real data if the RMS Standardized Residual index exceeds 0.3. In this case, an index of less than 0.1 is considered almost unattainable.

Table 4. Goodness-of-fit statistics of the hypothesised conceptual model.

5. Conclusions

In this study, we explore the impact of the trust crisis in the financial sector on macroeconomic stability, where financial sector development and monetary policy transmission mechanisms were analysed as mediators. Our research results provide theoretical implications and enhance the existing literature on the trust crisis in three primary ways.

Firstly, the trust crisis in the financial sector of the economy is perceived as a complex phenomenon where internal structure and system of mutual interdependence are unknown. This study went beyond prior research and showed that the trust crisis in the financial sector is inferred from the devaluation of the national currency against the US dollar, number of Ukrainian banks, in respect of which a banking license has been revoked by the National Bank of Ukraine, and the unemployment rate, that could be measured directly based on official statistics. It was found that the coefficient of value the hryvnia to the US dollar exchange rate in the interbank foreign exchange market is the highest among all dimensions. This confirms that the hryvnia exchange rate on the interbank foreign exchange market to the US dollar is clearly more volatile, that explains the anomalous currency fluctuations caused by both rational and irrational factors related to the panic sentiment of economic agents.

Secondly, the results contribute to explicating and highlighting a real danger of the erosion of the trust crisis in the financial system to both long-term macroeconomic stability and prospects for economic growth. By providing empirical pieces of evidence about the unmediated (direct) effect, this paper shows that exacerbation of the trust crisis in the financial sector, through other processes, distinct from whatever financial sector development (M1) and monetary policy transmission mechanisms (M2) transmits, would yield a decrease the macroeconomic stability indicators, i.e. GDP annual, the volume of industrial products (goods, services) sold and Ukraine trade balance. This finding broadly supports the work of other studies in this area linking the role of economic agents’ pessimistic expectations that could greatly erode trust in the financial sector with the short- and long-run prospects of the economy (e.g. Angeletos et al., Citation2014; Beveridge, Citation1909; Keynes, Citation1937; Pigou, Citation1927, and others).

The last implication involves a vital role of the mediation effect of transmission channels of the monetary policy mechanism and the developed financial sector that could mitigate the negative effects of deepening the trust crisis in the financial sector and lead to an increase in macroeconomic stability indicators. From a practical perspective, the findings revealed that interest, credit, and currency channels of the monetary policy transmission mechanism could be used to cope with the erosion of the trust crisis in the financial sector to macroeconomic stability. The analysis reveals that the total effect indicates positive mediation of financial sector development and monetary policy transmission mechanisms, while other processes (or mechanisms) distinct from them have a negative mediation in the relation between the trust crisis in the financial sector and the macroeconomic stability.

Our results are significant, but still, have limitations of validity. In general, most of the model fit indices of the original conceptual model are not contradictory and are within normal limits. This testifies to the correspondence of the empirical data to the constructed model of structural relations. However, it is worth noting that the ideal fit of a hypothetical model to empirical data is difficult to achieve in the process of modelling structural equations. This is due to the fact that the STATISTICA program builds computer simulations based on linear dependencies, and therefore is only an approximation of the real relationships between the studied indicators. According to the theory of modern complex systems, the natural dependencies between public trust, macroeconomic stability, the transmission mechanism of monetary policy, and the development of financial intermediation are not characteristic linearity, and therefore the obtained diagnostic parameters of the original model indicate a sufficient level of adequacy of the model.

The proposed conceptual model can be further modified and extended by new factors to investigate their effects. Furthermore, future research might be conducted for measuring conditional effects (moderator) between the trust crisis in the financial sector and macroeconomic stability. In addition, the proposed conceptual model of direct and mediating influence of trust crisis in the financial sector on macroeconomic stability could be an altered by an interdependent link between the trust crisis in the financial sector and financial sector development. In this line, following Guiso (Citation2010) the role of trust crisis in the financial sector in the emergence of frauds in the financial industry, the warping of the demand of financial instruments, investors’ portfolios and reliance on financial markets could be investigated, as well as their ramifications in macroeconomic imbalances.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Acedański, J., & Włodarczyk, J. (2016). Dispersion of inflation expectations in the European Union during the global financial crisis. Equilibrium. Quarterly Journal of Economics and Economic Policy, 11(4), 737–749.

- Ahmed, R. R., Vveinhardt, J., Štreimikienė, D., Ashraf, M., & Channar, Z. A. (2017). Modified SERVQUAL model and effects of customer attitude and technology on customer satisfaction in banking industry: Mediation, moderation and conditional process analysis. Journal of Business Economics and Management, 18(5), 974–1004. https://doi.org/https://doi.org/10.3846/16111699.2017.1368034

- Alnsour, M. (2018). Internet-based relationship quality: A model for Jordanian business-to-business context. Marketing and Management of Innovations, 4, 161–178. https://doi.org/https://doi.org/10.21272/mmi.2018.4-15

- Angeletos, G. M., Collard, F., & Dellas, H. (2014). Quantifying confidence. NBER Working Papers No. 20807. National Bureau of Economic Research, Inc.

- Belás, J., Korauš, M., & Gabčová, L. (2015). Electronic banking, its use and safety. Are there differences in the access of bank customers by gender, education and age? International Journal of Entrepreneurial Knowledge, 3(2), 16–28. https://doi.org/https://doi.org/10.1515/ijek-2015-0013

- Beveridge, W. H. (1909). Unemployment: A problem of industry. Longmans Green.

- Bilan, Y., Brychko, M., Buriak, A., & Vasilyeva, T. (2019). Financial, business and trust cycles: The issues of synchronization. [Ciklusi financiranja, poslovanja i povjerenja: pitanja za sinkronizaciju]. Zbornik radova Ekonomskog fakulteta u Rijeci: časopis za ekonomsku teoriju i praksu/Proceedings of Rijeka Faculty of Economics: Journal of Economics and Business, 37(1), 113–138. https://doi.org/https://doi.org/10.18045/zbefri.2019.1.113

- Bilan, Y., Lyeonov, S., Lyulyov, O., & Pimonenko, T. (2019). Brand management and macroeconomic stability of the country. [Zarządzanie marką i stabilność makroekonomiczna kraju]. Polish Journal of Management Studies, 19(2), 61–74.

- Bilan, Y., Lyeonov, S., Vasylieva, T., & Samusevych, Y. (2018). Does tax competition for capital define entrepreneurship trends in Eastern Europe? On-line Journal Modelling the New Europe, 27, 34–66. https://doi.org/https://doi.org/10.24193/OJMNE.2018.27.02

- Bilan, Y., Raišienė, A. G., Vasilyeva, T., Lyulyov, O., & Pimonenko, T. (2019). Public governance efficiency and macroeconomic stability: Examining convergence of social and political determinants. Public Policy and Administration, 18(2), 241–255.

- Bilan, Y., Rubanov, P., Vasylieva, T., & Lyeonov, S. (2019). The influence of industry 4.0 on financial services: Determinants of alternative finance development. [Wpływ przemysłu 4.0 na usługi finansowe: determinanty rozwoju alternatywnych finansów]. Polish Journal of Management Studies, 19(1), 70–93. https://doi.org/https://doi.org/10.17512/pjms.2019.19.1.06

- Bilan, Y., Vasilyeva, T., Lyeonov, S., & Bagmet, K. (2019). Institutional complementarity for social and economic development. Business: Theory and Practice, 20, 103–115. https://doi.org/https://doi.org/10.3846/btp.2019.10

- Bilan, Y., Vasilyeva, T., Lyulyov, O., & Pimonenko, T. (2019). EU vector of Ukraine development: Linking between macroeconomic stability and social progress. International Journal of Business and Society, 20(2), 433–450.

- Błażejowski, M., Kwiatkowski, J., & Gazda, J. (2019). Sources of economic growth: A global perspective. Sustainability, 11(1), 275. https://doi.org/https://doi.org/10.3390/su11010275

- Brychko, M., Kuzmenko, O., Polách, J., & Olejarz, T. (2019). Trust cycle of the finance sector and its determinants: The case of Ukraine. Journal of International Studies, 12(4), 300–324. https://doi.org/https://doi.org/10.14254/2071-8330.2019/12-4/20

- Buriak, A., Lyeonov, S., & Vasylieva, T. (2015). Systemically important domestic banks: An indicator-based measurement approach for the Ukrainian banking system. Prague Economic Papers, 24(6), 715–728. https://doi.org/https://doi.org/10.18267/j.pep.531

- Buriak, A., Vozňáková, I., Sułkowska, J., & Kryvych, Y. (2019). Social trust and institutional (bank) trust: Empirical evidence of interaction. Economics & Sociology, 12(4), 116–332.

- Bützer, S., Jordan, C., & Stracca, L. (2013). Macroeconomic imbalances: A question of trust? Working paper No. 1584, European Central Bank.

- Çera, G., Meço, M., Çera, E., & Maloku, S. (2019). The effect of institutional constraints and business network on trust in government: An institutional perspective. Administratie si Management Public, 1(33), 6–19. https://doi.org/https://doi.org/10.24818/amp/2019.33-01.

- Diamantopoulos, A. (1994). Modelling with LISREL: A guide for the uninitiated. Journal of Marketing Management, 10(1–3), 105–136. https://doi.org/https://doi.org/10.1080/0267257X.1994.9964263

- Diamantopoulos, A., & Siguaw, J. A. (2000). Introducing LISREL. Sage Publications.

- Duhnea, C., Vancea, D. P. C., & Frecea, L. G. (2017). IPO underpricing in emerging capital markets: A comparative study of Romania. Bulgaria and Hungary. Transformations in Business & Economics, 16 (2A), 478–495.

- Dvorský, J., Petráková, Z., Ajaz Khan, K., Formánek, I., & Mikoláš, Z. (2020). Selected aspects of strategic management in the service sector. Journal of Tourism and Services, 11(20), 109–123. https://doi.org/https://doi.org/10.29036/jots.v11i20.146

- Ejdys, J., Ginevicius, R., Rozsa, Z., & Janoskova, K. (2019). The role of perceived risk and security level in building trust in E-government solutions. E + M Ekonomie a Management, 22(3), 220–235. https://doi.org/https://doi.org/10.15240/tul/001/2019-3-014

- Gavurova, B., Kubak, M., Huculova, E., Popadakova, D., & Bilan, S. (2019). Financial literacy and rationality of youth in Slovakia. Transformations in Business & Economics, 18(3), 43–53.

- Gavurova, B., Virglerova, Z., & Janke, F. (2017). Trust and a Sustainability of the macroeconomic growth Insights from dynamic perspective. Journal of Security and Sustainability Issues, 6(4), 637–648. https://doi.org/https://doi.org/10.9770/jssi.2017.6.4(9)

- Gazda, J. (2008). Testing real business cycle models in the Polish economy. Journal of International Studies, 1(1), 27–35. https://doi.org/https://doi.org/10.14254/2071-8330.2008/1-1/3

- Golovchanskaya, E. E., Strelchenya, E. I., Popkova, E. G., & Leonenko, O. V. (2018). The key role of intellectual resources in the economic growth models in the institutional environment of innovative activity of the Republic of Belarus: Theory and practice. International Journal of Trade and Global Markets, 11(3), 213–227. https://doi.org/https://doi.org/10.1504/IJTGM.2018.095813

- Goodman, L. A. (1960). On the exact variance of products. Journal of the American Statistical Association, 55(292), 708–713. https://doi.org/https://doi.org/10.1080/01621459.1960.10483369

- Gros, D., & Roth, F. (2010). The financial crisis and citizen trust in central banks. Centre for European Policy Studies. CEPS Working Document No. 344.

- Guiso, L. (2010). A Trust-driven Financial Crisis.Implications for the Future of Financial Markets. EIEF Working Papers Series 1006, Einaudi Institute for Economics and Finance (EIEF).

- Hoyle, R.H. (Ed.). (1995). Structural equation modelling. SAGE Publications, Inc.

- Hu, X., Ocloo, C. E., Akaba, S., & Worwui-Brown, D. (2019). Effects of business to business e-commerce adoption on competitive advantage of small and medium-sized manufacturing enterprises. Economics & Sociology, 12(1), 80–99. https://doi.org/https://doi.org/10.14254/2071-789X.2019/12-1/4

- Indartono, S., & Faraz, N. J. (2019). The role of commitment on the effect of public workers' OCBO on in-role performance. Administratie si Management Public, 32, 108–119. https://doi.org/https://doi.org/10.24818/amp/2019.32-08

- Janus, J. (2016). The transmission mechanism of unconventional monetary policy. Oeconomia Copernicana, 7(1), 7–21. https://doi.org/https://doi.org/10.12775/OeC.2016.001

- Jiang, Y., & Wang, G. (2017). Monetary policy surprises and the responses of asset prices: An event study. SocioEconomic Challenges, 1(3), 22–44. https://doi.org/https://doi.org/10.21272/sec.1(3).22-44.2017

- Karkowska, R., & Kravchuk, I. (2019). Identification of global systemically important stock exchanges. Equilibrium, 14(1), 31–51. https://doi.org/https://doi.org/10.24136/eq.2019.002

- Kelloway, E. K. (1998). Using LISREL for structural equation modelling: A researcher's guide. SAGE Publications, Inc.

- Keynes, J. M. (1937). The general theory of employment. Quarterly Journal of Economics, 51(2), 209–223. https://doi.org/https://doi.org/10.2307/1882087

- Kendiukhov, I., & Tvaronavičienė, M. (2017). Managing innovations in sustainable economic growth. Marketing and Management of Innovations, 3(3), 33–42. https://doi.org/https://doi.org/10.21272/mmi.2017.3-03

- Khan, H., & Upadhayaya, S. (2019). Does business confidence matter for investment? Empirical Economics. https://doi.org/https://doi.org/10.1007/s00181-019-01694-5

- Kljucnikov, A., & Belas, J. (2016). Approaches of Czech entrepreneurs to debt financing and management of credit risk. Equilibrium, 11(2), 343–365. https://doi.org/https://doi.org/10.12775/EQUIL.2016.016

- Kolodko, G. W. (1993). Stabilization, recession and growth in a postsocialist economy. MOCT-MOST Economic Policy in Transitional Economies, 3(1), 3–38. https://doi.org/https://doi.org/10.1007/BF01101840

- Lei, P. W., & Wu, Q. (2007). Introduction to structural equation modelling: Issues and practical considerations. Educational Measurement: Issues and Practice, 26(3), 33–43. https://doi.org/https://doi.org/10.1111/j.1745-3992.2007.00099.x

- Leonov, S. V., Frolov, S., & Plastun, V. (2014). Potential of institutional investors and stock market development as an alternative to households' savings allocation in banks. Economic Annals-XXI, 11–12, 65–68.

- Leonov, S. V., Vasylieva, T. A., & Tsyganyuk, D. L. (2012). Formalization of functional limitations in functioning of co-investment funds basing on comparative analysis of financial markets within FM CEEC. Actual Problems of Economics, 134(8), 75–85.

- MacKinnon, D. P., Lockwood, C. M., Hoffman, J. M., West, S. G., & Sheets, V. (2002). A comparison of methods to test mediation and other intervening variable effects. Psychological Methods, 7(1), 83–104. https://doi.org/https://doi.org/10.1037/1082-989X.7.1.83

- Marcel, D. T. A. (2019). The determinant of economic growth evidence from Benin: Time series analysis from 1970 to 2017. Financial Markets, Institutions and Risks, 3(1), 63–74. https://doi.org/https://doi.org/10.21272/fmir.3(1).63-74.2019

- Maruyama, G. M. (1998). Basics of structural equation modelling. SAGE Publications, Inc.

- Mas’ud, A., Manaf, N. A. A., & Saad, N. (2019). Trust and power as predictors to tax compliance: Global evidence. Economics & Sociology, 12(2), 192–204. https://doi.org/https://doi.org/10.14254/2071-789X.2019/12-2/11

- Matsusaka, J. G., & Sbordone, A. M. (1995). Consumer confidence and economic fluctuations. Economic Inquiry, 33(2), 296–318. https://doi.org/https://doi.org/10.1111/j.1465-7295.1995.tb01864.x

- Mazurek, J., & Mielcová, E. (2017). Is consumer confidence index a suitable predictor of future economic growth? An evidence from the USA. E + M Ekonomie a Management, 20 (2), 30–45. https://doi.org/https://doi.org/10.15240/tul/001/2017-2-003

- Mihóková, L., Martinková, S., & Dráb, R. (2017). Short-term fiscal imbalance comparison in V4 countries using a dynamic conditional correlation approach. Equilibrium, 12(2), 261–280. https://doi.org/https://doi.org/10.24136/eq.v12i2.14

- Moździerz, A. (2019). Macroeconomic stability as the condition for Bulgaria to join the euro area. Equilibrium, 14(2), 295–315. https://doi.org/https://doi.org/10.24136/eq.2019.014