Abstract

Nowadays audit profession is faced with an excessive evolution of the information and communication technology (ICT). The effects of ICT on auditing are dual. On the one hand, auditing is faced with the digitalization of companies’ business operations, and on the other, auditors must be able to adapt their methodologies to these changes in order to be able to audit implemented ICT in the companies’ business operations. One of the latest ICT innovations includes the application of blockchain technology (BCT) in different business operations of a company, which represents the object of auditing. In order to audit BCT, auditors must apply appropriate audit procedures, whereas analytical procedures (APs) represent the most useful one. The subjects of this paper are external and internal auditors, and their application of APs for auditing implemented BCT in the companies’ business operations, in Croatia. Therefore, the main objective of this paper is to investigate the differences in the APs’ application and its usefulness for auditing BCT, as an emerging ICT, between external and internal auditors. To investigate the main objective of the paper, desk research and survey research were conducted. Overall results indicated that external and internal auditors in Croatia are aware that auditing BCT requires the application of advanced APs, for what they need to possess excellent knowledge about APs and BCT. Obtained results showed that auditors in Croatia possess below-average knowledge about APs and BCT. Therefore, the necessity for specialized education of external and internal auditors is inevitable. Regarding the investigation of differences in the readiness to audit BCT between external and internal auditors in Croatia, the results confirmed that external auditors are more ready to audit BCT than internal auditors. Finally, research results confirmed that the application of advanced APs in audit engagements will increase the efficiency and effectiveness of companies’ business operations supported by the BCT.

JEL CLASSIFICATION:

1. Introduction

The audit profession nowadays is faced with inevitable information and communication technology (ICT) developments, from the aspect of audited objects on the one side, and applied methodologies on the other (Tušek et al., Citation2018a, Citation2018b). In general, auditing can be defined as “the accumulation and evaluation of evidence about information to determine and report on the degree of correspondence between the information and established criteria” (Arens et al., Citation2012, p. 4). Therefore, auditing has a purpose to determine and ensure whether information, that management or those charged with governance, and other stakeholders use for decision making and governance processes, are reliable and credible. In this process, external and internal auditing have leading roles.

The traditional, historically oriented audit approach has been replaced with a contemporary, agile, risk-based and forward-looking approach, which focuses on the risk analysis and management in order to predict, prevent, detect and correct potential mistakes and frauds that, in the end, leads to increasing the efficiency and effectiveness of companies’ business. Although external and internal auditing have different objectives and objects, they apply similar methodologies, face the same challenges, and technological confrontations. Advanced ICT represents significant risks for auditors in the context of new auditing areas or audit objects, and the need to continuously develop new knowledge, skills, and abilities (Halar, Citation2020). Additionally, contemporary ICT offers auditors numerous possibilities for advancing their methodologies and approaches to auditing.

If companies, in a contemporary, uncertain business environment, want to survive and achieve competitive advantage, they need to embrace and implement new and emerging ICT. Technological advancement, fuelled by the development of basic and emerging ICT, is completely changing traditional companies’ business operations and is driving innovation in every industry (PwC, Citation2018b). New and innovative ICT include, among others, mobile technology, social networks, cloud computing, big data, sensors and Internet of Things, additive manufacturing, robotics, drones, blockchain technology, wearable technologies, artificial intelligence, virtual and augmented reality, and many more (PwC, Citation2018b, p. 5; Spremić, Citation2018, pp. 3–13, 31–34; Tušek et al., Citation2018b, pp. 266–271). Blockchain technology (BCT) represents an emerging ICT, or a ‘game-changer’, that is completely transforming companies’ business operations and ways on which management achieves strategic business goals, and overall business strategy (PwC, Citation2018a, Citation2018b; Spremić, Citation2018; Tušek et al., Citation2018b). From the aspect of auditing, the application of BCT in companies’ business represents the change in the auditing object. In order to audit BCT, as well as other basic and emerging ICTs, auditors must apply appropriate audit procedures or techniques that are performed by computer-assisted audit tools and techniques (CAATTs). Among different audit procedures that are available to auditors, analytical procedures (APs) represent the most useful and prospective one for auditing new ICT as part of companies’ business. APs are the science of analysis (Soileau et al., Citation2015, p. 11), or an in-depth technique to produce audit evidence in an effective and efficient way (Jans et al., Citation2014, p. 1752; Moolman, Citation2017, p. 171).

Therefore, it can be concluded that implementation of ICT (Banarescu, Citation2015; Cangemi, Citation2016; PwC, Citation2018b; Schmitz & Leoni, Citation2019; Tušek et al., Citation2018a, Citation2018b; Wang & Kogan, Citation2018; Zhang et al., Citation2020) and application of APs (Brender et al., Citation2019; Cangemi & Brennan, Citation2019; Dagilienė & Klovienė, Citation2019; Jans et al., Citation2014; Li et al., Citation2018; Moll & Yigitbasioglu, Citation2019; Moolman, Citation2017; Rooney et al., Citation2017; Soileau et al., Citation2015; Sun et al., Citation2015) denote development of audit profession nowadays, and enable remote auditing (Teeter et al., Citation2010).

The research problem of this paper involves questioning the differences between external and internal auditors in Croatia related to the application and usefulness of APs for auditing BCT used in the business operations of their clients. In that context, the research questions are:

To what extent external and internal auditors apply advanced APs in their engagements

Are APs crucial for auditing emerging ICTs, as BCT

Shall the intensive application of APs by external and internal auditors used for auditing BCT increase efficiency and effectiveness of companies’ business operations.

Following the research problem and questions, the research objectives are:

To analyse and investigate the importance of the application of advanced APs for auditing emerging ICT, as BCT

To investigate whether there exist differences in readiness for auditing emerging ICTs and technological advancements as BCT between external and internal auditors

To investigate whether the implementation of the BCT in companies’ business operations will result in the application of more advanced APs by auditors and will advanced audit methodology increase the effectiveness and efficiency of companies’ business operations.

The paper is structured as follows. The second chapter covers a literature review regarding the current trends and future opportunities of BCT application in companies’ business operations, that represents object of auditing, as well as a comprehensive literature review about APs, as an essential procedures or techniques for auditing BCT. The second chapter also includes development of hypothesis and conceptual framework of the research. The third chapter describes data obtaining and processing methodology. The following, fourth chapter presents research results followed by a discussion and concluding chapter.

2. Literature review

2.1. Blockchain technology as object of auditing

Among emerging ICTs, BCT is one of the most promising ICT, that has a potential to radically change non-business and business environment, as well as disrupt many traditional industries and professions, from financial services and insurance, to food, health care and government, including accounting and auditing fields (Brender et al., Citation2019; Cangemi & Brennan, Citation2019; Deloitte, Citation2017; Rooney et al., Citation2017; Schmitz & Leoni, Citation2019; Wang & Kogan, Citation2018; Zhang et al., Citation2020). BCT was firstly introduced as the core technology behind Bitcoin, Ether, and other cryptocurrencies, meaning that it does not represent a cryptocurrency in itself (Rooney et al., Citation2017; Schmitz & Leoni, Citation2019; Spremić, Citation2018; Zhang et al., Citation2020). BCT rather represents a distributed ledger or database where multiple copies of the same ledger are shared among the participants or nodes of a large network (Moll & Yigitbasioglu, Citation2019, p. 7; Wang & Kogan, Citation2018, p. 2). Furthermore, BCT provides a process or a system that ensures sharing data, without centrally storing and controlling them, among the participants or ledger users even if they do not trust each other (Brender et al., Citation2019, p. 36; Cangemi & Brennan, Citation2019, p. 2). In other words, BCT is a “publicly shared database that keeps records of all transactions ever executed within the ecosystem for a specified domain. Using cryptographic algorithms (e.g., digital signature and hash function), the blockchain protocol is able to guarantee data integrity, making it impossible to tamper with the transaction history” (Wang & Kogan, Citation2018, p. 15). The appeal of BCT is in its use of peer-to-peer network technology that is combined with cryptography, and especially this combination enables participants who do not know each other to conduct transactions without requiring a traditional trusted intermediary (Deloitte, Citation2017, p. 1).

As a consequence of BCT and business environment development, today exist various types of blockchain ledgers, for example, private blockchain ledgers, like the one a bank or supply chain participants may deploy, and public blockchain ledgers, like for a cryptocurrency as Bitcoin (Cangemi & Brennan, Citation2019, p. 2), as well as, non-distributed and distributed ledgers (Schmitz & Leoni, Citation2019, p. 332). The main advantage of BCT is that an approved transaction by the participants in the network cannot be reversed or re-sequenced (Moll & Yigitbasioglu, Citation2019, p. 7), what simplifies the back-office processes (Brender et al., Citation2019, p. 36). BCT enables standardization of business activities and digital transformation of business models with a high level of objectivity and transparency (Brender et al., Citation2019, p. 36; Zhang et al., Citation2020, p. 2). BCT “has the potential to impact all recordkeeping processes, including the way transactions are initiated, processed, authorized, recorded, and reported. Changes in business models and business processes may impact back-office activities, such as financial reporting and tax preparation” (Deloitte, Citation2017, p. 2).

Because of its pervasive impact on various traditional and modern industries, as well as different professions, several potential BCT’ applications in companies’ business exist, includingly (Deloitte, Citation2017; Rooney et al., Citation2017; Schmitz & Leoni, Citation2019; Spremić, Citation2018; Wang & Kogan, Citation2018; Zhang et al., Citation2020):

Payment processing, money transfers, and other banking processes

Issuance and transfers of private securities

Digital IDs

Monitoring supply chains

Digitization and tracking the origins and history of transactions in various commodities

Retail loyalty rewards programs

Securing the integrity of electronic records

Supporting databases and other registries, as well as data sharing

Contract management

Compliance with tax regulations

Accounting transactions

Continuous auditing and monitoring.

Among the most important features of BCT are transparency, immutability, interoperability, scalability, accuracy, performance, security, trustworthiness, disintermediation, traceability, persistency, distributed consensus approach, decentralization, auditability, smart execution, autonomous, and secured capabilities (Brender et al., Citation2019; Cangemi & Brennan, Citation2019; Rooney et al., Citation2017; Schmitz & Leoni, Citation2019; Spremić, Citation2018; Wang & Kogan, Citation2018; Zhang et al., Citation2020). This BCT features constitute possibilities for advancing business operations, but on the other side, if they are not properly managed and controlled, they can raise significant risks and disadvantages for companies’ business in financial and non-financial terms.

The biggest challenge that is impeding the adoption of BCT in companies’ business is the trade-off between information confidentiality and transparency (Wang & Kogan, Citation2018, p. 2). To eliminate this dilemma, several BCT-based transaction processing system or frameworks were developed. Besides that, other important technical challenges, as well as important risks can arise from BCT application, such as regulatory risks, cybersecurity risks, and others (Brender et al., Citation2019, p. 39).

In the end, it is particularly important to emphasize that BCT represents one incredibly significant business aspect that will, soon, become a pervasive part of, and have a substantial impact on the accounting and audit profession. As already mentioned earlier, BCT has the potential to significantly impact the audit profession. One way on which BCT can affect auditing is when it is included in audit engagements, as part of an audit object. This situation would appear in case when BCT is used within companies’ business operations and represents part of its enterprise resource planning systems (ERP), as well as its accounting information systems (AIS). Application of BCT, as a part of companies’ business operations and overall internal and external business environment, results in automated records of companies’ business and accounting transactions. By auditing BCT, as part of companies’ business, external and internal auditors can contribute to enhancing the quality of financial and operational information.

BCT, although known for more than a decade, is still emerging and has not yet been proven at enterprise scale, with its wider application for supporting enterprise information systems and continuous monitoring systems, as well as for supporting accounting and auditing fields, is still anticipated (Deloitte, Citation2017; Schmitz & Leoni, Citation2019; Wang & Kogan, Citation2018). Nevertheless, it is extremely important for both external and internal auditors to be knowledgeable of developments in this area (PwC, Citation2018b; Rooney et al., Citation2017; Schmitz & Leoni, Citation2019). The convergence of accounting and BCT, and as well as auditing and BCT, “shows great promise for reducing redundant manual effort, increasing the speed of transaction settlement, and preventing financial reporting fraud” (Wang & Kogan, Citation2018, p. 2). As companies’ business operations are being digitalized, by implementing basic and emerging ICT, like BCT, external and internal auditors need to keep track with these changes in order to be able to audit this, changed activities that, in the end, increases the efficiency and effectiveness of companies’ business. In accounting and auditing fields, the usefulness of BCT is seen in enabling real-time access to information, continuous monitoring and auditing, and fraud prevention and detection (Deloitte, Citation2017; PwC, Citation2018b; Rooney et al., Citation2017; Schmitz & Leoni, Citation2019; Wang & Kogan, Citation2018). Considering its early development stage and its main characteristics, new risks on BCT which require the implementation of new controls and development of new audit programs (Cangemi & Brennan, Citation2019, p. 1) can be expected. Regarding that, in the accounting and auditing fields, the trade-off between information confidentiality and transparency is also brought into the question (Wang & Kogan, Citation2018, p. 2). To include BCT in audit engagements, as audit objects, external and internal auditors, need to have appropriate knowledge about BCT to be able to understand this ICT as is implemented at their clients’ business, and adapt their audit methodologies to this new ICT. Besides their understanding of BCT application in companies’ business operations, auditors need to apply appropriate audit procedures to gather audit evidence, with APs being the most important one.

Another way on which BCT application in companies’ business operations can impact the audit profession, is though changing its audit methodologies, and by implementing BCT as part of their tools and techniques for engagements’ execution. In this paper, the emphasis is primarily on the BCT as audit object and APs as audit procedures or techniques, while BCT as an auditing tool remains a potential topic for future research of this interesting, but an under-researched area.

2.2. Analytical procedures as techniques for auditing blockchain technology

Application of APs in the process of external and internal auditing improves the effectiveness and efficiency of auditing activities (Appelbaum et al., Citation2017; Cangemi, Citation2016; Chan & Kogan, Citation2016; Ježovita et al., Citation2018; Lambrechts et al., Citation2011; Li et al., Citation2018; PwC, Citation2018b; Teeter et al., Citation2010), and consequently companies’ business operations. With the implementation of BCT into the companies’ business operations (Cangemi & Brennan, Citation2019; Deloitte, Citation2017; Wang & Kogan, Citation2018; Zhang et al., Citation2020), the usefulness, advantages and application opportunities of APs for external and internal auditors are coming to the fore.

Scientists, professional institutions, and practitioners use different terms in the context of APs, for example, data analytics, analytics, data analysis, analytic tools, analytical review, and others. International Standard on Auditing 520 – Analytical Procedures, defines data analytics as “evaluations of financial information made by a study of plausible relationships among both financial and non-financial data. APs also encompass the investigation of identified fluctuations and relationships that are inconsistent with other relevant information or that differ from expected values by a significant amount” (IAASB, Citationn.d.). Application of APs in external and internal auditing represents using efficient tools, techniques and procedures for the purposes of analysing, comparing, synthesizing and forecasting data to reach to certain conclusions on patterns, anomalies, trends, expected values, or to detect unexpected values that direct auditors’ attention to problematical organizational areas and control weaknesses (Ježovita et al., Citation2018, p. 20). APs technologies are computer programs that auditors use for data processing purposes to fulfil audit objectives (Lambrechts et al., Citation2011, p. 3). By using APs in audit process, the overall audit objectives and scope do not change (Lambrechts et al., Citation2011, p. 3).

According to Zhang et al. (Citation2020), the full potential of the BCT in companies’ business cannot be accomplished without the implementation and integration of basic and emerging ICT, like Internet of Things, big data analytics, cloud computing, and data visualization. In that process, auditors can provide valuable assurance, advice, insight and foresight, by providing information that is result of APs’ application. Tar-Mahomed (Citation2019) concludes that the implementation of BCT into the companies’ business operations, and having continual access to the chain, would move the audit profession closer to real-time auditing and continuous assurance. “A major challenge exists in terms of potential redefinition of audit and control activities based on the properties of BCT (transparency, traceability, security, persistency and immutability of transactions)” (Brender et al., Citation2019, p. 45).

Considering the characteristics of BCT, transaction data could serve as a high-quality audit evidence, because 100% of transactions that have occurred, could be instantly verified in BCT systems (Wang & Kogan, Citation2018, p. 5). This raises serious question regarding the necessity of conducting audit engagements over BCT application in companies’ business operations (Deloitte, Citation2017, p. 9). Cangemi and Brennan (Citation2019, pp. 8–9) are also questioning the need for auditing the BCT, and in the end they conclude that auditors will continue to be an important part of the assurance process, but by implementation of BCT in companies’ business, auditors will need to apply advanced APs and continuous auditing and monitoring activities. Furthermore, recording a transaction in a BCT system may or may not provide sufficient and reliable audit evidence related to the nature of the transaction, because the transaction can still be (Deloitte, Citation2017, p. 10):

Unauthorized, fraudulent or illegal

Executed between related parties

Linked to a side agreement that is ‘off-chain’

Incorrectly classified in the companies’ financial statements.

Therefore, auditors will need to apply appropriate audit procedures, like advanced APs, which need to be performed by relevant CAATTs. In Caseware Analytics (Citationn.d.) are also supporting the conclusion that auditing BCT should be backed by the application of APs and continuous auditing and monitoring, and that BCT may not remove auditors from assessing transactions, but it can transform the way auditors perform their activities. Even when the BCT, and other emerging ICTs, establish an extremely secure environment for transactions recording and processing, it is almost impossible to eliminate all potential risk factors, so auditors will still need to consider all the potential inefficiencies and shortcomings in the system design (Tang & Karim, Citation2019, p. 9).

The majority of scientific literature regarding the application of APs related to BCT is theoretical, and there are only a few commercial surveys conducted by global professional institutions or specialized companies, that also show that this is an especially under-researched area. Everyone agree that the application of APs in today’s technologically driven environment and companies’ digitalized business is inevitable. Concepts such as BCT also increase the need for APs’ application by auditors in conducting various audit engagements. A significant change in the business environment, and consequently in the audit profession, in forthcoming years can be expected regarding the implementation of BCT in companies’ everyday activities and operations. Questions that can be raised regarding BCT and auditing are ‘how, what, and whether to audit?’ It is expected for “blockchain or distributed ledger technology to fundamentally change the nature of auditing due to its ability to automate the tracking and recording of every transaction” (Krendl & Ruparel, Citation2019, p. 4). Furthermore, BCT enables and supports real-time auditing of the total population. BCT promotes real-time auditing by allowing auditors permanent access to the network, what allows them to inspect and sample transactions when they occur (Ortman, Citation2018, p. 63). “While access to real-time information through the blockchain may present a greater opportunity to apply audit analytics, substantive procedures will still need to be completed to achieve proper assurance” (Ortman, Citation2018, p. 65). Also, “methods for obtaining sufficient appropriate audit evidence will need to consider both traditional stand-alone general ledgers, as well as blockchain ledgers” (Deloitte, Citation2017, p. 2). In the end, it can be concluded that the application of advanced APs is necessary for auditing new and emerging ICT as BCT.

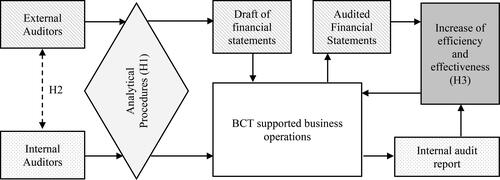

2.3. Hypothesis development and conceptual framework

The research problem of this paper involves questioning the differences between external and internal auditors in Croatia related to the application and usefulness of APs for auditing BCT used in the business operations of their clients. In this, digitalization era, advanced APs stands out as an essential technique in auditing BCT and ICT in general. In that context, the question is to what extent external and internal auditors apply advanced APs in their engagements and are APs crucial for auditing advanced ICTs as BCT. Today, advanced ICT, a few decades ago inconceivable, is available to almost everyone, especially to large and successful companies. The recent crisis caused by the COVID-19 pandemic forced many of them to accelerate the digitalization processes and implementation of remote working. The question is, where external and internal auditors in that story are, or in other words, are they ready to embrace, and deal with the advanced APs to audit ICT and BCT, and is there a difference between external and internal auditors in readiness to audit BCT. The ICT development also affected the audit profession by forcing auditors to adapt their methodologies to be able to keep track of clients’ digitalization processes. On the global level, companies are implementing continuous and agile auditing, and auditing total data sets instead of a sample has become reality. In that context, APs play a key role as a technique that provides limitless opportunities, both for external and internal auditors. Following the advancements of auditing methodology, the research question is shall the intensive application of APs by external and internal auditors used for auditing BCT increase efficiency and effectiveness of business operations of their clients. Following the research problem and earlier stated research objectives, as well as, based on the literature review, three research hypotheses were developed, whose comprehensive description is shown below.

Conducted literature review shows that auditing BCT assumes the application of advanced APs. Moreover, APs are becoming necessary procedures, both for external and internal auditors, for performing any type of audit engagements in a technologically advanced business environment. Implementation of emerging ICT in companies’ business operations enables the development of continuous auditing and monitoring, development of new types of audit engagements, testing the population of the data, rather than samples, etc. In that context, APs are becoming essential audit procedures or techniques. Therefore, the first hypothesis includes the following assumption:

H1: Auditing blockchain technology (BCT) used in companies’ business operations assumes the application of advanced analytical procedures (APs) by external and internal auditors in Croatia.

Differences in their job descriptions, responsibilities, audit object, and subject, engagements results, differences in applied auditing standard frameworks, as well as, differences in the level of their acquired knowledge, skill and abilities between external and internal auditors, are well known. Pervasive technological advancements bypass neither external nor internal auditors, nor their scope of work. The ICT development, and its involvement in the majority of companies’ business processes over the last few decades, resulted in significant modification of methodology auditors exploit, which is especially emphasized in the increase of application of APs as a major technique for gathering audit evidence, both by external and internal auditors. From the aspect of the implementation of BCT in companies’ business operations, neither external nor internal auditors will not be able to bypass the ICT advancements of the client’s organization/s. Auditors will be forced to learn how to audit it. Also, in the vast majority of cases, external auditors have access to more advanced procedures and techniques for auditing purposes, than internal auditors have. Considering that, the second hypothesis incorporates the following assumption:

H2: External auditors are more ready to audit blockchain technology (BCT) compared to internal auditors in Croatia.

If external and internal auditors possess better knowledge about BCT and APs, as well as, if they more intensively apply APs for auditing BCT, this would result in companies’ business effectiveness and efficiency increase. The premise should be viewed indirectly in a way that better knowledge of BCT and APs would result in more precise audit planning, which would lead to collecting more accurate and comprehensive audit evidence which are the basis for auditors conclusions, recommendations, and opinions, and which should help stakeholders, especially managers, in business decision making processes, resulting in increased effectiveness and efficiency of business operations. Accordingly, the third hypothesis incorporates the following assumption:

H3: Application of advanced analytical procedures (APs) in audit engagements by external and internal auditors will increase the efficiency and effectiveness of companies’ business operations supported by the BCT in Croatia.

Defined hypothesis can be formed into the conceptual framework of the research that is shown on .

Figure 1. Conceptual framework of the research.

Source: Authors' creation.

3. Methodology

To test research hypotheses, and to investigate the current trends and future opportunities of the BCT’ application in companies’ business operations in Croatia, as well as to research the importance of advanced APs for auditing BCT between external and internal auditors, survey research was conducted. The survey was carried out in April 2020 via LimeSurvey. The questionnaire included a general set of questions regarding education, years of experience, industry, obtained certifications, and employment position. The second part of the questionnaire included questions related to the current trends, application, education, understanding, and knowledge of BCT and APs. Questions were close type ones where examinees were offered to choose one or more options, rank suggestions, or add their own opinion for certain questions. The obtained data were processed by SPSS Statistics, and analysed using appropriate statistical methods.

Under the European and Croatian legislation, statutory audits are carried out by statutory auditors, i.e. auditors who have approval and are registered with the competent authority (Ministry of Finance in Croatia). There were 489 statutory auditors employed by 207 audit firms registered to conduct financial statement audits in Croatia in April 2020 (Republic of Croatia Ministry of Finance, Citationn.d.). In contrast to external audit or financial statement audit, internal audit in Croatia is regulated mainly for public sector entities and financial institutions within the private sector (credit institutions (banks), AIF management companies, mandatory and voluntary pension companies, insurance and reinsurance companies, leasing, and factoring companies), while others establish internal audit function voluntary. Additionally, there is no official register of certified internal auditors in Croatia. Available data from 2018 shows that 275 entities in Croatia had established an internal audit function (Ježovita et al., Citation2018). Although this research focuses on the internal auditor as an individual, rather than internal audit as a function as a test variable, almost 70% of internal audit functions in Croatia employs 1–2 internal auditors (Ježovita et al., Citation2018), and by that the number of functions can be considered as a relevant population. The questionnaire was sent via e-mail to 407 statutory auditors and 304 internal auditors. Out of the total number of sent e-mails, 213 returned as undeliverable, making a total of 498 delivered e-mails. During the 2 weeks period, 169 respondents completed the survey, and additionally, 58 of the examinees partially responded to the questionnaire. The research results cover only completed questionnaires which make a response rate of 33.93%Footnote1, which is above an average response rate for external surveys (10–15%), resulting in a margin of error 6.13% at the confidence level 95%.

To test research hypotheses descriptive, analytical, and statistical methods were used. In that context, next to descriptive statistics, multivariate statistical methods as simple and multiple regression, and binary logistic regression were used. Factor analysis (principal component analysis (PCA) with varimax rotation) was used to synthesize chosen variables and used the resulting factor as an independent variable in binary logistic regression. Obtained data is also tested by applying the non-parametric Mann-Whitney test of rank differences and binomial test of proportion, and appropriate statistics used for testing statistical assumptions of applied methods (VIF value, Durbin-Watson statistics, Hosmer & Lemeshow test, and others).

4. Empirical data and analysis

Out of the total number of examinees, 45% (77) are employed in the audit companies (external auditors), and 10% in the private sector (internal auditors), making altogether 55% of examinees employed in the private sector, and 45% (76) in public sector entities (internal auditors and other) ().

Table 1. Years of experience and sex of the examinees by employment position.

Regardless of the employment position, 82% of auditors included in the research have more than 10 years of working experience and more than half of them are females (56%). Related to the sector, i.e. employment position, audit firms have a greater percentage of less experienced employees, and they employ 21% of statutory auditors with 6–10 years of experience. Next to that, 51% (48) of internal auditors included in the research (both, private and public sector) are females.

On average, the examinee has more than one certificate (ratio of number of obtained certificates and number of examinees is 1.30) (). The largest proportion of examinees have certificate obtained by Hrvatska revizorska komora (HRK) as one of the authorized providers and organizers of educations and exams for statutory auditors in Croatia (51%). More than a third of examinees (38%) have the certificate for internal auditors obtained by Sekcija internih revizora (SIR), and 31% of examinees have the certificate for public sector internal auditor obtained by Ministry of Finance (MF) which is mandatory for conducting internal audit activities in public sector entities in Croatia. Over 7% of the examinees have certificates issued by international organizations.

Table 2. Type of certificate that examinees obtain.

By analysing general information about examinees included in the research, it can be concluded that they embody a representative sample of external and internal auditors in Croatia, and the results of conducted research can be considered as a general opinion regarding the importance of application of advanced APs to audit BCT.

As previously shown in the literature review section, in today’s technologically driven business environment, APs are becoming essential audit techniques for performing any type of external or internal audit engagements involving emerging ICTs, including BCT. The significant focus of companies’ digitalization processes is given to an application of BCT as a prosperous ICT, potential for various business aspects (payments, contracting, accounting records, digital identities, data sharing, etc.). Deloitte’s research from 2019 shows that 53% of respondents consider that the BCT is of critical relevance to the companies in the coming 24 months, and 86% of them think that the BCT is broadly scalable and will eventually achieve mainstream adoption (Deloitte, Citation2019, p. 4). Furthermore, PwC’s research shows that forecasts put a crucial role in BCT in fore coming years. The BCT will help to generate an annual business value of more than US $3 trillion, and according to the research results, it is predicted that up to 20% of global economic infrastructure will depend on BCT by 2030 (PwC, Citation2018a).

The results of our research show that more than 56% of companies in Croatia do not have any plans to develop or use BCT in their operating activities, and only 3% of them are actively using BCT in their daily activities. 60% of examinees think that less than 20% of transactions in companies will be processed via BCT over the next five years. Only 12,43% of examinees have an opinion that more than 50% of transactions in companies will be processed via BCT. The current trends and future opportunities of BCT application in Croatian companies are below average, and significantly lower compared to global trends.

To make conclusions regarding opportunity areas of the BCT’ application in Croatian companies, the examinees could rank examples offered to them as a result of the literature review (). The answers are coded with grades, from 8 for the most perspective area of application to 1 for the least perspective area of application BCT in Croatian companies. The most perspective opportunity of BCT application in companies’ business operations is payment processing and money transfers, where 37% of examinees ranked it in the first place, with the average grade 6.54 (maximum is 8). Payment transactions are followed by digital IDs that 22% of examinees placed in the first place, and additionally 17% in second place (average grade 5.57).

Table 3. The rank of application opportunities of the BCT by companies in Croatia rated by external and internal auditors’ opinions.

As mentioned earlier, the research hypothesis includes the premise that auditing BCT assumes the application of advanced APs (). Results show that 70% of examinees consider that is crucial to have excellent knowledge and to apply advanced APs for auditing BCT. Furthermore, almost 25% of examinees considers that the average knowledge is sufficient, and less than 5% of the examinees consider that there is no need to know and use APs for auditing purposes.

Table 4. Required level of knowledge of analytical procedures to audit BCT.

Furthermore, a higher proportion of internal auditors (77%) compared to external (65%) consider that is essential to possess excellent knowledge and skills to use APs to conduct audit engagements of BCT. Nevertheless, the Mann-Whitney U Test shows that the difference between distributions of external and internal auditors is not statistically significant (U = 3138, p = .107). To test the statistical significance of APs for auditing BCT, a one-tailed Binomial Test was used. For test purposes we coded answers (excellent knowledge = 1; average and no knowledge = 0). From the test results, it can be concluded that possessing excellent knowledge and application skills related to APs is crucial for auditing BCT, both for external and internal auditors.

To obtain more precise insight regarding the importance of APs for auditing BCT, and to test the first research hypothesis, regression analysis was used. The level of knowledge of definition, technology, and significance of BCT for business operations (SQ002) is set as an independent variable and the level of application of advanced APs in auditors’ activities (SQ001) as a dependent variable. The examinees evaluated both statements by using a five-point Likert scale, and the data results are standardized to convert variables to continuous and use it for the regression model. The assumption of the linear relationship is tested by using normal P-P Plot of regression standardized residual, and homoscedasticity by scatterplot. VIF value of 1 shows us that there is no multicollinearity problem. Independence of observations (no auto-correlation problem) is proven by using Durbin-Watson statistics (d = 2.099).

Although generated model () shows that only 11.5% of the total variation in the dependent variable can be explained by the independent variable (R2 = .115), overall results show that the model statistically significantly predicts the outcome variable (p = .000) () and that the independent variable is statistically significant in the model (p = .000). Finally, results indicate that if the level of knowledge and importance of BCT for business operations increases by 1, the level of application of AP in auditing engagements will increase by .339 ().

Table 5. Summary of simple regression model.

Table 6. ANOVA table for the regression model.

Table 7. Coefficients in the regression model.

It can be concluded that there exists a statistically significant relationship between the implementation of BCT and the application of advanced APs for auditing purposes. Considering the analysis of the survey results, the hypothesis that auditing BCT used in companies’ business operations assumes the application of advanced APs by external and internal auditors in Croatia can be accepted (H1).

External and internal auditing profession significantly differ regarding their scope of work, as well as their roles and responsibilities, knowledge, skills and abilities of auditors, and available auditing techniques. Contemporary companies’ business operations are characterized by the implementation of new and innovative ICT, which represents objects of auditing, so auditors need to adapt their existing auditing procedures, tools and techniques, or implement new ones, to be able to audit changed auditing objects. Therefore, nowadays, simple and advanced APs’ application, in external and internal auditing, is gaining more and more prominence. Considering differences in responsibilities and audit engagement objectives of external and internal auditors, the research question is, if there exists a difference in readiness to audit BCT between external and internal auditors.

Although only 3% of examinees stated that their companies actively use BCT in their business operations, there are 3.3 times more external auditors’ companies compared to internal auditors’ companies that are using this ICT (). On the other side, almost 70% of internal auditors, compared to 47% of external auditors, stated that their companies do not have plans to develop or use BCT in companies’ business operations. Conducted Mann-Whitney U Test shows that exists statistically significant difference of distributions of using BCT in companies’ business operations between external and internal auditors (u = 2708, p = .003).

Table 8. Differences in the application of BCT in companies’ business operations in Croatia observed by external and internal auditors.

As well as the application (current trends), the future perspectives of BCT implementation in companies’ business operations over the next five years in Croatia are not promising (). Most of the examinees (61%) consider that BCT will be used to process less than 20% of companies’ transaction, and only 4% of them consider that more than 70% of transactions will be processed via BCT. Considering differences between external and internal auditors, almost 95% of internal auditors have an opinion that BCT will be used to process less than 50% of transactions (compared to 82% of external auditors), and over 18% of external auditors think that more than 70% of transactions will be processed via BCT (compared to 5% of internal auditors). As well as for application level, in case of the perspectives Mann-Whitney U Test also shows that perspectives’ distributions between external and internal auditors differ (u = 2969, p = .037).

Table 9. The perspectives of using BCT in companies’ business operations in Croatia grouped by external and internal auditors’ opinions.

To obtain more specific details and coherent results regarding differences between external and internal auditors in readiness to audit BCT in Croatia, firstly factor analysis was used to obtain one, more inclusive factor instead of two separate variables (application and perspectives regarding BCT in companies’ business operations), and then binary logistic regression to test the second research hypothesis. Two nominal variables were coded, where score 0 was assigned for not having plans to use BCT in companies’ business operations, and 5 was assigned for active use of BCT in companies’ business operations, as well as appropriate scores in-between. The second variable was coded with scores from 1 (less than 20% of transactions will be processed via BCT) to 4 (more than 70% of transactions will be processed via BCT). Before processing them with factor analysis, both variables were standardized. For dimension reduction purposes, principal component analysis (PCA) with varimax rotation was used. The result of the PCA factor analysis is one factor with eigenvalue 1.589 explaining 79.47% of the variance. The generated factor was used as an independent variable in binary logistic regression, and represents a combination of the actual application, and opinion on future perspectives of using BCT in companies’ business operations, and is interpreted as the readability of auditors to audit BCT. The dichotomous variable in the regression model is the classification of auditors to external or internal, also coded (internal auditors with 0, and external auditors with 1).

Results of Omnibus Tests of Model Coefficients is lower compared to −2 Log-Likelihood, so it can be concluded that the final model represents an improvement over the baseline model by explaining more of the variance in the outcome (). The model is significant (chi-square = 9.347, p = .002). The pseudo-R2 for the overall model approximately shows that the model explains roughly 7.5% of the variation in the outcome. It is expected that R2 in binary logistic regression is lower compared to regular regression analysis. Hosmer & Lemeshow test shows that the model is a good fit to the data (chi-square = 4.830, p = .185 (>.05)). Overall, the model correctly classifies 57.4% of cases.

Table 10. Omnibus test of model coefficients and summary of the binary logistic regression model.

The Wald test shows that our independent factor is statistically significant in the model (Wald = 8.045, p = .005). The results of the model indicate that the odds of readiness for auditing BCT is 1.716 times higher for external compared to internal auditors (). Considering obtained results, it can be concluded that external auditors are more ready to audit BCT compared to internal auditors in Croatia, and by that the second research hypothesis can be accepted also (H2).

Table 11. Variables in the binary logistic regression model.

The hypothesis that the application of advanced APs in audit engagements by external and internal auditors will increase the efficiency and effectiveness of companies’ business operations supported by the BCT, is tested by multiple regression analysis. Taking into account all previous results regarding the importance of APs for auditing BCT and to test third research hypothesis, multiple regression model was developed in which dependent variable is an improvement of efficiency and effectiveness of companies’ business operations (SQ003) and independent variables are knowledge of definition, technology, and significance of BCT (SQ002), change of used analytical procedures in auditing activities (SQ004) and education of auditors (SQ005). The model intends to show that if external and internal auditors possess better knowledge about BCT and APs, as well as, if they more intensively use APs for auditing BCT, this would result in companies’ business effectiveness and efficiency increase, though quality conclusions, recommendations, opinions and insights, that help managers and those charged with governance, as well as other stakeholders, to making better, efficient and effective business decisions.

Firstly, considering the differences in approaches and results between external and internal auditors, it was tested if it is necessary to include an additional dummy variable in the model. The Mann-Whitney U test showed that there is no statistically significant difference of opinion between external (mean = 3.6923) and internal auditors (mean = 3.8442) (p-value = .152), and by that there is no need to observe results separately for two groups.

Durbin-Watson test of independency between observations of 1.714 shows that there is no problem with autocorrelation (). Furthermore, in the case of multivariant statistical methods, there must be no correlation between independent variables in the model. To measure multicollinearity in regression analysis, variance inflation factor (VIF)Footnote2 was used. In this case, there is no multicollinearity problem because VIF ranges from 1.052 to 1.140. A lower level of R of .588 can be accepted because is hard to predict human behaviour and beliefs. Additionally, our survey covers statistically significant predictors, and considering that it can be concluded that a value of .588 indicates a good level of prediction. The coefficient of determination (R2) of .346 shows us that independent variables explain 35% of the variability of improvement in efficiency and effectiveness of companies’ business operations in case of implementation of BCT.

Table 12. Summary of multiple regression model.

The F-ratio from the ANOVA table indicates that a designed regression model is a good fit for the data because the independent variables statistically significantly predict the dependent variable, F(3, 165) = 29.038, p < .000 ().

Table 13. ANOVA table for multiple regression model.

Unstandardized coefficients show that the increase of application of advanced analytical procedures in auditing by 1, will result in the improvement of efficiency and effectiveness of companies’ business operations by .464 (). Improvement of emerging ICT knowledge by 1, will improve efficiency and effectiveness by .112, and in case of attending education, the results will improve by .126. The results show that all independent variables are significant in the model at the significance level 1%, and in the case of education at 10%, although the result is near 5%. Taking altogether into account, the research hypothesis (H3), that the application of advanced analytical procedures (APs) in audit engagements by external and internal auditors will increase the efficiency and effectiveness of companies’ business operations supported by the BCT, can be accepted.

Table 14. Multiple regression model.

5. Results and discussion

The research problem of the paper is related to the importance and usefulness of APs for external and internal auditors, for auditing BCT in Croatia. Nowadays, both external and internal auditors, are faced with accelerating business environment and ICT changes, resulting in new audit objects, and implementation of advanced CAATTs. To retain their reputation, in the context of providing reasonable assurance related to the internal controls, efficiency and effectiveness of companies’ business operations, and ensuring that financial statements are showing fair and objective financial position, performance, and cash flows of the companies, they are forced to embrace emerging APs in their everyday activities.

The global trends of audit profession development include implementation of new audit approaches infeasible without integration with basic and emerging ICT. In that context, internal auditors highly depend on the ICT development phase of the company they are employed in, which enables them, or not, to process data with advanced APs, and audit the company’s ICT. In contrast, external auditors are not limited by their clients in the implementation of ICT’ advancements in their audit methodology. They are free to use the most advanced APs for collecting audit evidence, increasing the effectiveness of the audit process, and issuance of the auditor’s opinion. Nevertheless, the actual ability to apply advanced APs is limited to the ICT implementation level of the client.

Frontiers of advanced APs are almost limitless, providing both to external and internal auditors opportunities to analyse full sets of data of all types of business cycles and the company’s applied ICT. The APs are most often used for obtaining insights on history information, providing conclusions on the financial position, business performance, weaknesses of the internal control system, and detecting business and fraud risks. Application of advanced APs, next to descriptive conclusions, assume using them for diagnostic, predictive, and prescriptive purposes adding additional value to the available information and offering a much wider picture of the previous, current, and future business processes and expectations of the company.

The premise of the research problem is that auditing advanced ICT as BCT assumes the application of APs to get descriptive, diagnostic, predictive, and prescriptive information about weaknesses, usefulness, and consequences of BCT for the company’s financial position and business performance. In that context, it was investigated if external and internal auditors in Croatia apply advanced APs to audit ICT, as well as BCT. Research results showed a low implementation level of BCT in the Croatian companies’ business operations. More than half of auditors stated that their companies do not have any plans to develop or use BCT in its business operations, and only 3% of companies actively use BCT in daily activities. Furthermore, perspectives on the implementation of the BCT in companies’ business operations over the next five years are not promising, because only 12% of examinees consider that more than 50% of transactions in companies will be processed via BCT. Payment processing and money transfers are seen as the most perspective practice of BCT application in companies’ business operations, followed by digital IDs, and accounting transactions. Results obtained by the research show that the current state and perspectives of BCT application in Croatian companies are low, and significantly lower compared to the global level. It is not irrelevant to take into account the fact that the survey was carried out during the lockdown caused by COVID-19 pandemic, the greatest crisis during the last century, which resulted in ‘forced’ and accelerated digitalization of companies’ business operations and majority activities worldwide, and in Croatia. Taking that into the account, obtained results regarding the development and application of emerging ICTs in the Croatian business environment are even more concerning.

Obtained results also showed that auditors in Croatia have below-average knowledge regarding possibilities to exploit BCT in the business environment of the company considering that a minority of them recognized monitoring supply chains, compliance with tax regulations, or retail loyalty programs as a perspective opportunity for companies to use them in the business processes. The necessity for specialized education related to the recent ICT development, including ICT, such as BCT, artificial intelligence, big data, continuous auditing and monitoring, and others represent fruitful research area, which could give to professional institutions guidelines for future development directions. Narrowly related to BCT, the first assumption of auditing BCT is understanding principles, opportunities, consequences, and the scope of the ICT. Educating auditors represents the first step in that context. Despite the low application and understanding levels, auditors in Croatia are aware that auditing BCT requires the application of advanced APs. Over 70% of them consider that possession of excellent knowledge skills and high application levels of APs is required to audit advanced ICT as BCT. It can be concluded that in the future advanced APs will have a crucial role in the audit profession. Observed altogether, implementation of BCT in the companies’ business operations, will result in a change of the way, as well as change of tools and techniques auditors use to conduct their engagements. The results of research show that if the level of knowledge and importance of BCT for companies’ business operations increases by 1 unit, the level of application of APs in auditing engagements will increase by .339 units. Although this research is focused on the application of BCT in companies’ business operations, it is crucial not to neglect other types of ICTs whose implementation also would most probably increase the application of APs.

Following the research results that both, external and internal auditors, consider the application of APs in auditing BCT extremely important, and that there is no significant difference in their opinion, it was questioned if there exists a difference in readiness to audit BCT between the two groups of auditors. Expectations of readiness between external and internal auditors can be argued. From the one side, it can be emphasized that internal auditors would be more ready considering that they are highly specialized and focused on the business processes of one particular company, but the ICT development level of the internal audit department is highly dependent on ICT development phase of that company. On the other side, external auditors are much more diversified, timely limited, and focused on the high effectiveness of getting audit results. Specialized audit companies have in focus the improvement of the efficiency and effectiveness of their auditing activities and considering that, they are more prompt in accepting ICT changes and improvements, as well as application of advanced APs. Taking that into account, our assumption that external auditors are more ready to audit BCT in confirmed by the research results. To be more precise, our results show that external auditors are 1.716 times more ready to audit BCT, compared to internal auditors in Croatia.

The most important question regarding the emerging ICT is its feasibility, i.e. cost-benefit effects. Future research should be focused on the analysis of implementation costs versus cost savings related to the implementation of BCT in companies’ business operations. In addition to the numerical, factual, cost-benefit analysis of direct impacts, it is important to investigate consequences that are much harder to measure via financial data. Although it is always important to try to convert non-financial, or even qualitative data, to financial effects, considering the fact that there is a low application level of BCT implementation in Croatian companies, future research should focus on investigating longitudinal financial effects of auditing BCT of few chosen, technologically most advanced companies. Our research can be viewed as an entering, preliminary research, which could help steer future researchers to the Croatian companies that should be investigated in detail. The results of the research show that the application of advanced APs in audit engagements will increase the efficiency and effectiveness of companies’ business operations supported by BCT. Additionally, it was found that improvement of emerging ICT knowledge, and attending specialized educations would also improve companies’ business efficiency and effectiveness.

Considering available research papers, mostly theoretical, the results of previously conducted surveys on the global level, and results of this research, focused on the importance of advanced APs for auditing BCT between external and internal auditors, the directions of future research are outlined.

6. Conclusion

The research objectives of this paper cover the investigation of the importance of the application of advanced APs for auditing emerging ICT, including BCT. Furthermore, the objective of the research was to investigate whether there exist differences in readiness to audit emerging ICTs and advancements, as BCT between external and internal auditors. In the paper, it was investigated whether the implementation of the BCT in companies’ business operations will result in the application of more advanced APs by auditors, and will advanced audit methodology increase the efficiency and effectiveness of companies’ business operations.

Papers and surveys prepared by the most significant auditing institutions at the global level, during the last five years, are focused on the implementation of modern ICT, and especially APs, into daily auditing activities. The lack of knowledge and the price of contemporary ICT could be emphasized as the main reasons for its low implementation and application levels among auditors. Nevertheless, in the upcoming years, auditors will have to face an emerging digital era that is not somewhere far away but is already here. Our research showed that external auditors are more ready for digitalization processes than internal auditors in Croatia.

The survey results show that the application of APs comes in a big way. By adapting to contemporary ICT, or digital environment and using APs in auditing BCT, auditors are significantly increasing the efficiency and effectiveness of companies’ business operations. By application of advanced APs, both, external and internal auditors are improving transparency, accountability, reliability, automation of their activities, the level of issued reasonable assurances, and comprehensiveness of their reports.

The question of whether to audit the BCT is needless. Of course, it should be audited, as a significant new audit object, whose impact is still to be seen. The high level of security and automation does not mean that there are no mistakes, fraud attempts, leaks, and other failures in companies’ business transactions. By using advanced APs for auditing BCT, for example, different statistical or visualization methods, the auditor is capable to easily notice and respond to found shortcomings and direct its resources to high-risk areas, what is, in fact, the point of the modern, contemporary risk-based auditing approach and directly increases efficiency and effectiveness of companies’ business operations. In addition to that, the aspect that should be covered by the future research, deals with the assumption that BCT could significantly encourage and accelerate the implementation of continuous auditing as an emerging auditing aspect.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 Response rate is calculated as a ratio of the number of full responses and the number of delivered invites.

2 If the result is near 1 that means that there is no multicollinearity problem, i.e. independent variables are not correlated. The result up to 5 indicates moderate multicollinearity, and greater than 5 significant correlation between variables.

References

- Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big data and analytics in the modern audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1–27.

- Arens, A. A., Elder, R. J., & Beasley, M. S. (2012). Auditing and assurance services: An integrated approach (14th ed.). Prentice Hall & ACL.

- Banarescu, A. (2015). Detecting and preventing fraud with data analytics. Emerging Markets Queries in Finance and Business. Procedia Economics and Finance, 32, 1827–1836.

- Brender, N., Gauthier, M., Morin, J.-H., & Salihi, A. (2019). The potential impact of blockchain technology on audit practice. Journal of Strategic Innovation and Sustainability, 14(2), 35–59.

- Cangemi, M. P. (2016). Views on internal audit, internal controls, and internal audit’s use of technology. Journal EDPACS, 53(1), 1–9. https://doi.org/https://doi.org/10.1080/07366981.2015.1128186

- Cangemi, M. P., & Brennan, G. R. (2019). Blockchain auditing – accelerating the need for automated audits! Journal EDPACS, 59(4), 1–11. https://doi.org/https://doi.org/10.1080/07366981.2019.1615176

- Caseware Analytics. (n.d.) Cangemi perspectives: Introduction to blockchain and the potential for advancing analytics. Blog. https://idea.caseware.com/blockchain-advancing-analytics

- Chan, D. Y., & Kogan, A. (2016). Data analytics: Introduction to using analytics in auditing. Journal of Emerging Technologies in Accounting, 13(1), 121–140.

- Dagilienė, L., & Klovienė, L. (2019). Motivation to use big data and big data analytics in external auditing. Managerial Auditing Journal, 34(7), 750–782. https://doi.org/https://doi.org/10.1108/MAJ-01-2018-1773

- Deloitte. (2017). Blockchain technology and its potential impact on the audit and assurance profession. Chartered Professional Accountants of Canada (CPA Canada) & American Institute of CPAs (AICPA). https://www.aicpa.org/content/dam/aicpa/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/blockchain-technology-and-its-potential-impact-on-the-audit-and-assurance-profession.pdf

- Deloitte. (2019). Deloitte’s 2019 global blockchain survey: Blockchain gets down to business. https://www2.deloitte.com/content/dam/Deloitte/se/Documents/risk/DI_2019-global-blockchain-survey.pdf

- Halar, P. (2020). Current state and perspectives of internal auditors’ professional development in digital economy era. Proceedings of the Faculty of Economics and Business in Zagreb, 18(1), 77–94.

- IAASB. (n.d.). ISA 520 – Analytical Procedures. https://www.ifac.org/system/files/downloads/a026-2010-iaasb-handbook-isa-520.pdf

- Jans, M., Alles, M. G., & Vasarhelyi, M. A. (2014). A field study on the use of process mining of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), 1751–1773. https://doi.org/https://doi.org/10.2308/accr-50807

- Ježovita, A., Tušek, B., & Žager, L. (2018). The state of analytical procedures in the internal auditing as a corporate governance mechanism. Journal of Contemporary Management Issues, 23(2), 15–46.

- Krendl, P., Ruparel, M. (2019). The digital audit revolution: Shaking the oil & gas industry. Accenture. https://www.accenture.com/_acnmedia/pdf-93/accenture-the-audit-revolution-oil-and-gas.pdf

- Lambrechts, A. J., Lourens, J. E., Millar, P. B., & Sparks, D. E. (2011). Data analysis technologies. International Professional Practices Framework (IPPF): Recommended Guidance: Supplemental Guidance – Global Technology Audit Guide 16. https://na.theiia.org/standards-guidance/recommended-guidance/practice-guides/Pages/GTAG16.aspx

- Li, H., Dai, J., Gershberg, T., & Vasarhelyi, M. A. (2018). Understanding usage and value of audit analytics for internal auditors: An organizational approach. International Journal of Accounting Information Systems, 28, 59–76. https://doi.org/https://doi.org/10.1016/j.accinf.2017.12.005

- Moll, J., & Yigitbasioglu, O. (2019). The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. The British Accounting Review, 51(6), 1008331–1008320.

- Moolman, A. M. (2017). The usefulness of analytical procedures, other than ratio and trend analysis, for auditor decisions. International Business & Economics Research Journal, 16(3), 171–184.

- Ortman, C. (2018). Blockchain and the future of the audit. CMC Senior Theses, 1983. http://scholarship.claremont.edu/cmc_theses/1983

- PwC. (2018a). Blockchain is here. What’s Your Next Move? https://www.pwc.com/gx/en/issues/blockchain/blockchain-in-business.html

- PwC. (2018b). 2018 State of the Internal Audit Profession Study – Moving at the Speed of Innovation: The Foundational Tools and Talents of Technology – Enabled Internal Audit. https://www.pwc.com/sg/en/publications/assets/state-of-the-internal-audit-2018.pdf

- Republic of Croatia Ministry of Finance. (n.d.). Register of Auditors. http://rgfi.fina.hr/RegistarRevizora

- Rooney, H., Aiken, B., & Rooney, M. (2017). Q & A. is internal audit ready for blockchain? Technology Innovation Management Review, 7(10), 41–44.

- Schmitz, J., & Leoni, G. (2019). Accounting and auditing at the time of blockchain technology: A research agenda. Australian Accounting Review, 29(2), 331–342. https://doi.org/https://doi.org/10.1111/auar.12286

- Soileau, J., Soileau, L., & Sumners, G. (2015). The evolution of analytics and internal audit. Journal EDPACS, 51(2), 10–17. https://doi.org/https://doi.org/10.1080/07366981.2015.1012441

- Spremić, M. (2018). Enterprise information systems in digital economy. University of Zagreb, Faculty of Economics & Business.

- Sun, T., Alles, M., & Vasarhelyi, M. (2015). Adopting continuous auditing: A cross-sectional comparison between China and the United States. Managerial Auditing Journal, 30(2), 176–204. https://doi.org/https://doi.org/10.1108/MAJ-08-2014-1080

- Tang, J., & Karim, K. E. (2019). Financial fraud detection and big data analytics – Implications on auditors’ use of fraud brainstorming session. Managerial Auditing Journal, 34(3), 324–337.

- Tar-Mahomed, S. (2019). Blockchain: What does it mean for the audit. The Journal of the Global Accounting Alliance, 8(2019), 48–49. http://www.gaaaccounting.com/blockchain-what-does-it-mean-for-audit/

- Teeter, R. A., Alles, M. G., & Vasarhelyi, M. A. (2010). The remote auditing. Journal of Emerging Technologies in Accounting, 7(1), 73–88. https://doi.org/https://doi.org/10.2308/jeta.2010.7.1.73

- Tušek, B., Ježovita, A., & Halar, P. (2018b). Development perspectives and challenges of internal audit function in digital business transformation era. Journal of Economy and Business, 24, 258–289.

- Tušek, B., Mamić Sačer, I., & Halar, P. (2018a). The internal audit function as an effective tool for increasing business success in digital economy era. In I. Načinović Braje, B. Jaković, & I. Pavić (Eds.), Proceedings of the 9th international conference “an enterprise odyssey: managing change to achieve quality development, Republic of Croatia, Zagreb (pp. 248–256). University of Zagreb, Faculty of Economics & Business.

- Wang, Y., & Kogan, A., (2018). Designing confidentiality-preserving blockchain-based transaction processing systems. International Journal of Accounting Information Systems, 30, 1–18. https://doi.org/https://doi.org/10.1016/j.accinf.2018.06.001

- Zhang, A., Zhong, R. Y., Farooque, M., Kang, K., & Venkatesh, V. G. (2020). Blockchain-based life cycle assessment: An implementation framework and system architecture. Resources, Conservation & Recycling, 152, 1–1.