?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the link between corporate social responsibility (CSR) and the performance of small and medium enterprises (SMEs) and the mediating role of firm reputation from a developing country perspective. Empirical research was carried out, and data were gathered using a questionnaire from 402 owners/managers of SMEs in Eritrea, a country in East Africa. Smart-Partial Least Squares structural equation modelling was employed. The results showed that CSR significantly influences the performance of SMEs, and this relationship is partially mediated by firm reputation. This research contributes to the knowledge of how CSR activities lead to SMEs’ financial performance. This strengthens prior evidence on the impact of CSR on business performance while also contributing significantly to the literature on the mediating role of reputation between social and financial performance. The application of the relationship to SMEs in developing nations reinforces the originality of this study. It makes substantial contributions to the literature in terms of theory, practice, and policy.

JEL CLASSIFICATIONS:

1. Introduction

Over the last few decades, the concept of Corporate Social Responsibility (CSR) has attracted the attention of several researchers, and its importance continues to grow. A company has obligations to the community beyond that of its shareholders’ revenues. Regardless of their size and type, businesses should become environmentally sustainable, economically competitive, and socially responsible (Orlitzky et al., Citation2011). From the stakeholders’ perspective, ‘the business has an obligation towards its stakeholders, who can affect or are affected by company politics and practices’ (Lantos, Citation2001). Edwards (Citation2005) contended that to achieve organisational objectives, firms should look at the ecological and social effects of their business processes and products. CSR is strategically vital for a business to be competitive (Bai & Chang, Citation2015).

Several studies have analysed the association between CSR and the performance of business organisations. However, as previous findings are inconclusive, the relationship between these two has become the most questioned issue in the literature on CSR (Fassin et al., Citation2015; Margolis & Walsh, Citation2003). No consensus has been reached on the relationship between CSR and enterprise performance. Research has produced mixed results, indicating positive correlation (Oeyono et al., Citation2011; Orlitzky et al., Citation2003; Tian, Citation2009), negative correlation ( Wagner et al., Citation2002; W. Yang & Yang, Citation2016), and the absence of a relationship altogether (Hao et al., Citation2011; Liping et al., Citation2016; McWilliams & Siegel, Citation2000). Galant and Cadez (Citation2017), amongst others, recognised that the reasons for the mixed results are measurement issues relating to both concepts of interest. As long as the conclusion on the link remains controversial in theory and practice, research exploring the connection between CSR and company performance will be necessary.

According to Galbreath and Shum (Citation2012) and Servaes and Tamayo (Citation2013), mediation is a potential research action that can reinforce studies on this relationship. Some scholars have made efforts to clarify the explanation behind the relationship between CSR and particular outcomes. For example, CSR boosts enterprise performance through brand loyalty (Pivato et al., Citation2008), managerial interpretation (Sharma, Citation2000), and client satisfaction (Luo & Bhattacharya, Citation2006). Additional studies are required to better understand the complicated relationship between CSR practice and economic outcomes. Firm reputation, which is an essential source of sustainable competitive advantage, has attracted substantial attention as a potential mediator and is also backed by the stakeholder theory (Blanco et al., Citation2013). However, firm reputation remains under-emphasised in research (Lai et al., Citation2010), and only a few studies have examined its effect on enterprise performance (Jones, Citation2005; Zhu et al., Citation2014). It is likely to play a significant part in the impact of CSR on performance. Although few studies have empirically tested this, (Galbreath & Shum, Citation2012; Lai et al., Citation2010; Saeidi et al., Citation2015), considering the impact of the applicability of CSR in diverse contexts, it is still necessary to investigate the link with SMEs in developing nations (Tilt, Citation2016). Research on the mediating factor of intangible assets such as business reputation is in its early stages, and has produced mixed results (Grewatsch & Kleindienst, Citation2017). Thus, analysing the mediating effect of reputation can contribute towards our understanding of the means through which CSR can affect SME performance.

SMEs contribute to CSR and are connected with the economic, ecological, and communal development of society. Therefore, they are a part of the CSR movement (Spence, Citation1999; Spence et al., Citation2003). Developing nations have societal and ecological glitches, including labour and human rights issues and environmental pollution, and if businesses are involved in CSR practice, they can decrease these social and ecological issues (Henderson, Citation2001). CSR, which is interconnected with sustainable development, needs to be studied appropriately (Cadez & Guilding, Citation2017).

CSR is a strategic instrument that can be used to boost SMEs’ competitiveness through enhanced customer loyalty and satisfaction, higher motivation of workers, and improved public fund access because of improved enterprise image and augmented sales (Mandl, Citation2009; Szabo, Citation2008). According to Park et al. (Citation2014), CSR is a vital component in retaining a favourable firm reputation, and is considered an essential strategic asset leading to a firm’s competitive advantage. CSR is seen as a good strategy for improving competitive power, financial performance, and intangible assets. However, its relationship with business reputation is relatively new and under-researched (Šontaitė-Petkevičienė, Citation2015) Most research efforts have focussed on large enterprises. In Africa, studies on the relationship between CSR and SME performance are limited (Turyakira et al., Citation2012). Therefore, this paper aims to fill this gap in the literature by examining and providing empirical evidence on the association amongst CSR, reputation, and SME performance in a developing country, Eritrea. The unstable environment and economic policy of the country have been centrally planned for decades before the market-oriented system, and a wide range of economic and public policy reforms were adopted after independence in 1994 (GOE, Citation1994). According to Cadez (Citation2013), countries that have experienced significant social changes, such as the adoption of the market system, are an interesting object of inquiry. Eritrea is in the process of development, and the business environment is becoming more competitive and global.

CSR varies from region to region (Sen & Cowley, Citation2013) as well as from developed to developing countries (Idemudia, Citation2011). This paper is important to developing nations as CSR studies are context reliant, and various organisational systems observed in developing countries may bring different CSR expressions (Jamali & Neville, Citation2011). A large portion of the existing research on the association between CSR and performance has been conducted in large firms from developed nations (Jamali et al., Citation2008; Masurel, Citation2015; Rahman Belal, Citation2001). Hence, data from a Sub-Saharan African country, Eritrea, can assist in presenting CSR effects in a worldwide context, which can improve the existing literature on the relationship between CSR and SME performance.

This study contributes to the literature as follows. First, it addresses the intriguing relationship between CSR and performance from an SME standpoint, strengthening prior evidence concerning the positive impact of CSR on financial performance. Our results support the stakeholder theory, which advocates a positive influence of CSR activities on firm performance. Second, it contributes significantly to research on the mediating role of reputation between social and financial performance. We identify the essential role of firm reputation and present its significant mediation effects on the relationship between CSR and SME performance. Third, the relationship between CSR and reputation as a link that also strengthens financial performance is relatively new in the literature. Its application to SMEs in developing nations reinforces the originality of this study and substantially contributes to the literature in terms of policy, theory, and practice. Fourth, this article contributes towards expanding scant extant knowledge by confirming the relationship between reputation and financial performance in the context of SMEs and specific situations. Our findings support the theory of the resource-based view (RBV) in that firm reputation positively impacts business performance. Fifth, to the best of our knowledge, this study is the first in establishing the relationship between CSR activities and SME performance in Eritrea by taking firm reputation as a mediating factor.

The rest of this paper is as follows. It starts with a literature review focussing on SMEs. Next, the methodology section describes the sampling, measurement of variables, and data analysis. The results are presented and analysed, followed by a discussion and conclusion.

2. Literature review and hypothesis development

2.1. CSR and financial performance

There are two leading schools of thought that explain the relationship between CSR and firm performance (Goll & Rasheed, Citation2004). The first encompasses opponents of CSR and is led by Friedman (Citation1970) and other neoclassical economists. They see CSR as negatively affecting the firm’s financial performance and contend that the primary goal of a business is to maximise profit. They believe that CSR practice incurs a cost to the enterprise, and places it at a competitive disadvantage, and must be left to the government. The second school of thought encompasses the proponents of CSR (Goll & Rasheed, Citation2004). This school was founded by Freeman (Citation1984) and suggests that CSR positively influences firm performance. Advocates of this school contend that as businesses exist in society, they are social institutions and should give back to the community (Bello et al., Citation2016). Enterprises must satisfy the key stakeholders’ needs so that their business can be sustainable (Supriti Mishra & Suar, Citation2010). According to Barić (Citation2017), the quality of the relationship between the firm and its stakeholders represents a crucial factor that affects the success of the business in its idea of differentiating itself from rivals and creating sustainable competitive advantage.

Amongst other explanations, the reason for the mixed CSR and financial performance relationship may also be the issue of causality – the influence of CSR on performance or influence of performance on CSR. According to Hillman and Keim (Citation2001), Lev et al. (Citation2010), and Waddock and Graves (Citation1997), enhancing CSR improves financial performance and vice versa. Martínez‐Ferrero and Frias‐Aceituno (Citation2015) examined the relationship between CSR and firm performance and the direction of causality by taking a sample from international non-financial listed companies. Their findings confirmed the existence of a positive and bidirectional CSR and financial performance relationship.

Although prior empirical research has reported mixed results concerning CSR relationships with firm performance, most have confirmed that efforts to implement CSR activities improve firm performance, thus justifying the strategic significance of CSR (Van Beurden & Gössling, Citation2008). Choongo (Citation2017) revealed a significant link between CSR practice and the performance of Zambian SMEs. According to Torugsa et al. (Citation2012), SMEs can achieve high financial yield by proactively making progress in their CSR programmes. Longo et al. (Citation2005) stated that most Italian SMEs perceived social responsibility and contributed towards the growth of business value by improving business image, ensuring customer loyalty, and enhancing relationships with workers and the community at large. Miller and Besser (Citation2000) described a definite relationship between CSR and SME performance. Similarly, Juarez (Citation2017) confirmed that social and economic CSR actions have a definite influence on the business performance of SMEs. According to Greening and Turban (Citation2000), applying CSR actions can have a positive impact on enterprise performance by attracting and retaining skilled employees. Theoretical and empirical evidence demonstrates a significant definite connection between CSR and SME performance. (Doh et al., Citation2010; Hull & Rothenberg, Citation2008; Mishra & Modi, Citation2013; Peloza & Shang, Citation2011; Perrini, Citation2006; ). Companies that comply with the sustainability concept and invest in new innovative concepts such as ‘eco-innovation’ and ‘social innovation’ are expected to generate better value and social development with an equal, low-carbon, and knowledge economy (Roblek et al., Citation2014). By improving corporate responsibility strategies and developing unique non-financial reporting, firms can be more effective and efficient in society, which will reflect on their business models positively and will help them attain greater levels of sustainability (Vukić et al., Citation2020).

Stakeholder theory advocates that a higher level of social responsibility brings a greater level of performance to the company (Freeman, Citation1984). It contends that the achievement of an organisation relies on the business’ ability to administer its relations with its stakeholders. This means that business organisations should be involved in building and maintaining proper relationships with interest groups and that CSR costs may enhance financial performance benefits indirectly (Wu, Citation2006). Hammann et al. (Citation2009) and Sweeney (Citation2007), depending on the instrumental stakeholder theory, stated that CSR application enhances business performance through the effect that these activities have on the relationship between the business and stakeholders. According to Perrini et al. (Citation2011), the stakeholder theory is essential in comprehending any potential relationship amongst CSR and firm performance.

The resource-based theory advocates a definite association between CSR and performance, as CSR expenditure may support businesses in developing new interior resources such as knowhow and business culture, and in creating exterior benefits through business reputation (Branco & Rodrigues, Citation2006). Therefore, SMEs’ engagement in CSR can enrich business reputation and can enhance performance over time. Based on the above discussion, we hypothesise as follows:

H1: CSR is positively related to SME financial performance.

2.2. CSR and firm reputation

Business reputation is one of the most valued resources and is considered an intangible asset that differentiates one firm from another. Deephouse (Citation2000) defined reputation as ‘the assessment of a business organisation by stakeholders in terms of affection, admiration as well as the knowledge they have towards it’. Engaging in CSR activities may strengthen the business reputation of all organisations, regardless of size and type. There is a consensus regarding the existence of a positive correlation between CSR and reputation. Gallardo-Vázquez et al. (Citation2019) examined CSR initiatives by taking a sample of 109 SMEs in Spain, and found that CSR strongly affects the reputation of SMEs. Maldonado-Guzman et al. (Citation2017), took a sample of 308 Mexican SMEs, and analysed CSR practices, firm reputation, and brand image of products. They found that CSR practices improved the image and elevated the reputation of SMEs. Lai et al. (Citation2010) revealed a positive and robust link between CSR practice and business reputation. According to Valdez-Juárez et al. (Citation2018), SMEs that engage in social and sustainable activities can improve their image and reputation.

Compared to companies with a lower level of philanthropic practice, those businesses that had achieved a high level of philanthropy was typically found to be socially responsible and characterised with a good reputation (Brammer & Millington, Citation2005). The positive perception of consumers and business allies regarding firms’ CSR activities implemented brings the upper level of enterprise performance and reputation (Cadez et al., Citation2019; Hsu, Citation2012). In a globalised and competitive market, adopting and applying CSR activities as a business strategy can yield a higher level of company reputation (Jones, Citation2005). Similarly, Pfarrer et al. (Citation2010), stated that reputation is vital to business achievement and is an essential social approval asset, especially in the contemporary free market. Firms first have to adapt and undertake CSR activities to increase the level of their reputation significantly (Fombrun, Citation2005). Gardberg and Fombrun (Citation2006) also contended that enterprise reputation is one of the most excellent outcomes of CSR activities. Fraj-Andrés et al. (Citation2012) advocated that SMEs’ CSR practices contribute towards developing an improved image and marketing ability, which generates a competitive advantage. The clients’ perceptions of firms’ CSR practices can be considered as a source of business reputation (Bendixen & Abratt, Citation2007). Employees’ level of organisational commitment is also linked with the views they have about their organisations’ CSR practice, which can improve their evaluation of their business reputation (Stawiski et al., Citation2010). SMEs are integrating CSR activities into their operations to boost their reputation amongst stakeholders (Graafland, Citation2018; Reverte et al., Citation2016). According to Munasinghe and Malkumari (Citation2012), SMEs are interested in CSR actions to enhance their business reputation, employee motivation, and economic performance. From a theoretical perspective, the RBV asserts that CSR involvement adds intangible assets such as reputation to the business, and improves the firm’s bottom line (Margolis et al., Citation2009). Stakeholder theory is the most pertinent theoretical framework for studies on CSR (Fassin et al., Citation2017; Vashchenko, Citation2017), and reinforces the direct effect of CSR on organisational reputation. Hence, we hypothesise thus:

H2: CSR is positively related to SME reputation.

2.3. Firm reputation and financial performance

Firm reputation is a crucial asset for an organisation and is extensively known as an effective strategic resource and mechanism to attain competitive advantage (Flanagan & O’shaughnessy, Citation2005; Schmidt, Citation1995). Good firm reputation can help firms align with the market demand, attract investments, and motivate workers. It works as a means to differentiate their services and products in the market. Several empirical studies have recognised the definite relationship between firm reputation and performance. According to Sarbutts (Citation2003), firm reputation is highly valuable in organisations and is a strategic element with the ability to consolidate SMEs’ competitive advantage. Ansong and Agyemang (Citation2016) documented a definite and significant connection between business reputation and performance by drawing upon a sample of 423 Ghanaian SMEs located within the Accra Metropolis. Firms with relatively robust reputations are in an excellent position to maintain a higher income over time (Roberts & Dowling, Citation2002). Tan (Citation2007) found that a company’s reputation is positively related to higher earnings. Competent workers like to work for organisations with a good reputation, and this is a cost-saving for firms, as it helps them recruit and retain skilled workers with fewer contracting and monitoring expenses (Bergh et al., Citation2010; Boyd et al., Citation2010; Roberts & Dowling, Citation2002). Better reputation ultimately results in better enterprise performance in the long run (Eberl & Schwaiger, Citation2005).

The RBV contends that an intangible resource generates competitive advantage and improves an organisation’s baseline when it is rare, unique, and non-replaceable (Barney, Citation1991). It considers business reputation a precious and scarce resource that can bring about competitive advantage. As an intangible asset, firm reputation makes a firm unique and encourages clients to repurchase and contentedly pay a high price for goods (Eberl & Schwaiger, Citation2005; Roberts & Dowling, Citation2002). Similarly, according to Deephouse (Citation2000), RBV contends that business reputation leads to a competitive advantage by expressing the desirability of the business to interest groups, which makes them eager to contract with it. Thus, a company’s reputation is an intangible resource that is challenging for rivals to imitate and can effectively be turned into a competitive advantage, which is beneficial for business performance. Thus, we hypothesise thus:

H3: Firm reputation is positively associated with SME performance.

2.4. The mediation effect of firm reputation

The growing literature dealing with CSR and its impact on organisational financial performance produced contradictory results. This lack of consensus may reflect model specification problems such as omissions of research and development spending (McWilliams & Siegel, Citation2001). In assessing the circumstances under which CSR impacts financial performance, omitted variables must be investigated empirically. Surroca et al. (Citation2010) highlighted an indirect association between CSR and financial performance, which depends on the mediating role of intangible assets.

One of the intangible resources is business reputation, which is a fundamental element that associates CSR with financial performance (Saeidi et al., Citation2015; Surroca et al., Citation2010). The mechanism of CSR actions affecting business performance by influencing interest groups and improving business reputation is supported by the stakeholder theory (Clarkson, Citation1995; Mitchell et al., Citation1997; Polonsky et al., Citation2005). Stakeholders decide the allocation of their resources based on the evaluation of the firm with respect to its reputation as connected to its CSR activities and ultimately influence company performance (Donaldson & Preston, Citation1995).

CSR improves financial performance by influencing interest groups’ perceptions positively. These interest groups’ positive perceptions attained through the demonstration of CSR can enhance reputation. An increase in reputation generates socially complicated and unique resources that are dependent on time. Such resources result in the superior performance of the organisation (Barney, Citation1991). Hence, the mediating effect of firm reputation on CSR and performance association is legitimate from a theoretical perspective and has been confirmed by empirical studies (Galbreath & Shum, Citation2012; Saeidi et al., Citation2015). However, given that CSR is context-dependent, it is still necessary to explore the link between CSR and firm performance in SMEs from developing nations (Tilt, Citation2016). Thus, we hypothesise as follows:

H4: Firm reputation mediates CSR and SME performance relationships

3. Research method

3.1. Sampling and data collection

This study aims to examine the relationship between CSR and SME performance, with firm reputation as a mediating factor. A systematically organised and standardised approach is considered in this study as it is vital in obtaining data on this subject within a short period of time from a large group (Saunders et al., Citation2012). The target population comprised SMEs from diverse sectors in the capital city Asmara, where most of the SMEs recorded in the Trade and Industry Office are located (MTI, Citation2018). A cross-sectional study was carried out and a standardised survey was disseminated to managers of manufacturing and service SMEs. The survey was adapted from previous studies, and a pilot survey was conducted to validate it. This was done to ensure that no irrelevant questions were included and to facilitate a correct understanding of the survey questions in order to receive accurate answers from respondents. All questions were scored on a five-point Likert scale, which is broadly applied in studies on CSR in SMEs (Gallardo-Vázquez & Sánchez-Hernández, Citation2014). After circulating the questionnaire, the sample comprised 402 SMEs. The demographics of the respondents are presented in .

Table 1. Respondents profile.

3.2. Variable measurement

CSR items were adapted from a previously validated study (Guerrero‐Villegas et al., Citation2018; Lindgreen et al., Citation2009; Martinez-Conesa et al., Citation2017), and comprised 22 items classified into 4 groups: customer, employee, community, and environment. The extent of involvement in CSR was measured using a 5-point scale (ranging from strongly disagree = 1 to strongly agree =5).

Financial performance was adapted from previous studies by Gunday et al. (Citation2011) and Martinez-Conesa et al. (Citation2017). This self-administered questionnaire included 4 items on performance. A 1-5 Likert scale was used to score the SME performance (ranging from extremely unsuccessful =1 to extremely successful =5). Based on previous studies, the subjective approach of measuring SMEs’ financial performance was adapted in this study (Man, Citation2002; Sweeney, Citation2009). As SME owners/managers were unwilling, objective data concerning financial performance are not available. Thus, utilising scales as an alternative measurement of SME performance is better than using actual figures (Man, Citation2002). This approach was followed because several studies have demonstrated a robust connection between subjective and objective measurements (Wall et al., Citation2004). Therefore, it is generally presumed that owners are well-informed of their firms’ financial performance.

Reputation was measured by four items adapted from Saeidi et al. (Citation2015). Firms were asked to determine their customers’ perceptions of the organisation’s reputation. The construct comprised 5 items and was measured using a 5-point scale (ranging from strongly disagree = 1 to strongly agree =5).

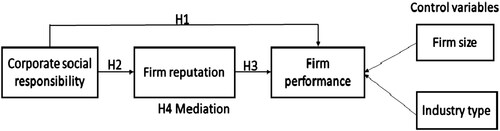

Finally, industry type and firm size were used as control variables in our study. Evidence shows that size (Russo & Fouts, Citation1997; Waddock & Graves, Citation1997; Wagner, Citation2010) and industry (Hillman & Keim, Citation2001; Husted & Allen, Citation2007; Waddock & Graves, Citation1997) can influence performance. Size is defined by the number of workers in this study. The classification of industries is carried out following the definitions of Waddock and Graves (Citation1997). shows the proposed research model.

Figure 1. Research model.

Source: Author's own work.

3.3. Data analysis

We analysed data using the Smart Partial Least Squares (PLS), which is a variance-based SEM technique. Smart-PLS was applied in carrying out SEM and testing the hypotheses through the development of path analyses. This approach was applied because it is suitability for application in predictive studies that discover complicated problems where the prior theoretical backgrounds are rare (Hulland et al., Citation2010). As this study is explanatory, PLS-SEM fits appropriately (Farooq & Radovic-Markovic, Citation2017). SEM has become a preferred method for researchers in various disciplines, particularly for research in the social sciences (Hooper et al., Citation2008). Anderson and Gerbing (Citation1988) classified SEM into measurement and structural models. The validity and reliability of the indicators for each construct were tested using a measurement model. The structural model was applied to investigate the connection between several dependent and independent variables (Smith, Citation2003). Following Hair Jr et al. (Citation2016b) guidelines, data quality and structural model consistency were ensured.

4. Results

4.1. Measurement model

offers the Smart-PLS, factor loading, reliability, and average variance explained (AVE) of the items used to measure CSR, reputation, and financial performance. The factor loadings and AVE for all items were above 0.7 and 0.5, respectively, and exceeded the standard threshold. Consequently, convergent validity was established (Henseler et al., Citation2009). The composite reliability amongst the identified constructs surpassed the limit of 0.7, as recommended by Hair et al. (Citation2014). This reveals that the reliability of all scales was maintained in this study.

Table 2. Constructs with items displaying reliability, factor loading, and convergent validity values.

Discriminant validity demonstrates whether one construct is sufficiently different from others (Hair et al., Citation2014). The criteria for discriminant validity from Fornell and Larcker (Citation1981) state that each construct’s square root of the AVE must surpass that of correlations between constructs. confirms that discriminant validity is present by displaying the square root of AVE (bold numbers) surpassing the correlations between constructs (non-bold numbers). presents the descriptive statistics and correlation. Mean values range from 3.80 to 4.08, the standard deviation range is between 0.68 and 0.72, skewness values range from −0.815 to −1.411, and kurtosis ranges from 0.475 and 1.994. There is no substantial issue in the data collected as the kurtosis value was below 10, and the skewness value was below 3 (Kline, Citation2011). There was a significant correlation amongst the constructs.

Table 3. Discriminant validity.

Table 4. Correlation and descriptive analysis.

4.2. Goodness of fit (GoF)

The goodness of fit (GoF) measures model fitness in Smart-PLS. Henseler et al. (Citation2016) defined it as ‘the geometric mean of the average AVE and average R2 (for dependent variables)’.

To measure the results of the GoF, the cut-off values were as follows, wherein 0.1 indicated a small GoF, 0.25 indicated a medium GoF, and 0.36 indicated a large GoF (Wetzels et al., Citation2009). The excellent model specifies that we have a parsimonious and reasonable model (Henseler et al., Citation2016). Using the above-mentioned formula, we attained a GoF of 0.364. This designates an excellent model fit (GoFlarge).

4.3. Structural model

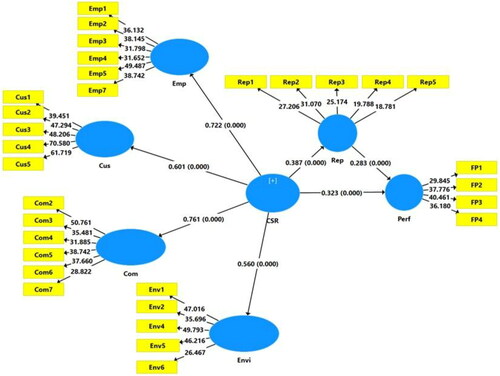

After confirming adequate reliability and validity of the measurement model and overall model fit, we applied the bootstrapping technique with 5000 sub-samples in Smart-PLS to test the hypotheses and path coefficients. Before testing the hypothesis, the values for variance inflation factor (VIF) were utilised to check multicollinearity and common method bias. VIF above 3.3 advocates the availability of high multicollinearity and can also be a sign that the common method bias is a problem (Diamantopoulos & Siguaw, Citation2006). In this study, the VIF scores are under 3.3, indicating that there is no multicollinearity problem (Hair et al., Citation2014), and the model is free from the problem of the common method bias (Kock, Citation2015). and display the SEM results, including path estimates and p-values.

Figure 2. SEM analysis result.

N.B. Emp - Employees, Cus - Customers; Com - Community; Env - Environment; CSR - Corporate social responsibility; Rep - Reputation, Perf - Performance.

Source: Author's own work.

Table 5. Path coefficients and their significance.

As shown in , there is a statistically significant definite link between CSR and financial performance with a path coefficient value of β = 0.433, t = 8.557, p < 0.001. CSR also has a significant positive impact on enterprise reputation (β = 0.379, t = 7.901, p < 0.001). Firm reputation has a significant positive effect on SME performance (β = 0.423, t = 9.827, p < 0.001). The R2 value obtained for the financial performance (dependent variable) is 0.26, indicating that the structural model accounts for around 26 percent of the variance in financial performance. Our results showed that the control variables employed in this study had insignificant influence and were thus erased from the final model.

4.4. Analysis of mediation

The analysis of mediation is performed based on the technique of Hair Jr et al. (Citation2016a), where primarily, the direct effect of CSR on performance (without a mediator) is measured. Second, by including the mediator, the indirect effect was analysed. Finally, the effect of total CSR on performance was determined. The results show that a firm’s reputation has a partial mediation role on the link between CSR and SME performance (see ).

Table 6. Mediation test.

5. Discussion and conclusion

The association between CSR and financial performance has been studied extensively. However, the evidence is still not clear, which may be because the roles of the mediating variables are neglected. The investigation of the link between CSR and financial performance from the perspective of firm reputation contributes towards clarifying this connection. Only a few studies have emphasised the area of SMEs. For this reason, the current study aimed to analyse the association between CSR practice and SME performance in Eritrea, emphasising firm reputation as a mediating factor using structural equation modelling.

5.1. Concluding remarks and relationships with previous findings

The results of this study revealed the existence of a significant association between CSR and SME performance. This implies that the progression of socially responsible actions strengthens performance and offers ample benefits for business. It is thus expected that the involvement in CSR activities such as the wise usage of water and energy can enable cost savings, and eventually improve firm performance. In comparison with previous studies, our results support the view that CSR has a positive influence on the performance of enterprises. Choongo (Citation2017) and Torugsa et al. (Citation2012) found a definite relationship between CSR and firm performance in SMEs. Thus, the results of this study build on previous studies that have examined CSR and performance, and provide additional evidence that CSR influences the financial performance of SMEs. It also indicates that CSR affects enterprise performance in non-Western contexts positively.

The results of this study show that CSR practices have a definite significant association with SME reputation. This suggests that the participation of SMEs in CSR practices is related to better enterprise reputation. Research has also established a definite relationship between CSR and business reputation in SMEs. Maldonado-Guzmán et al. (Citation2017) and Agyemang Otuo and Ansong (Citation2017) revealed that SMEs with improved CSR actions are in a better position to have an enhanced reputation. According to Turban and Greening (Citation1997), CSR practices in SMEs contribute towards building a better image and strong marketing position, which consequently brings a competitive advantage. Thus, business firms should develop CSR practices that benefit the public, protect the environment, and improve the living conditions of their workers and communicate their CSR practices to interest groups. This will allow their customers to select their products or services rather than their competitors’ products and services. At the same time, they enhance not only their business results, but also their reputation.

The findings of this study also show a definite significant connection between SMEs’ reputation and performance. This implies that better SME reputation leads to enhanced financial performance. Firms with a greater rank of reputation exceed those with a low rank of reputation (Chung, Schneeweis, & Eneroth, Citation1999). The results of this study are in congruence with the findings of Ansong and Agyemang (Citation2016), which confirmed that SMEs with a better reputation achieve higher financial performance. Brammer and Millington (Citation2005) also found a positive correlation between a firm’s reputation and performance. This is in line with the resource-based theory, in that enterprise reputation is a resource that brings competitive advantage to a business as it indicates interest groups regarding the attractiveness of the organisation, and becomes more willing to contract with it (Deephouse, Citation2000). Firm reputation is a resource that brings competitive advantage, and organisations should strive to improve their reputation through CSR, which contributes to the societal and economic development of communities. Firm reputation attracts and retains workers who are more competent and motivated, which in turn, enhances enterprise performance.

This study also examined the mediating role of enterprise reputation in the relationship between CSR and performance. Our findings indicate a partial firm reputation mediation on the relationship between CSR and performance in SMEs. This supports the stakeholder theory, which postulates that stakeholders allocate their resources to the company, based on their valuation of the reputation of the business related to CSR, and then affect business performance (Donaldson & Preston, Citation1995). The mediation of reputation is consistent with previous studies (Galbreath & Shum, Citation2012; L. Yang et al., Citation2017)

5.2. Implications

This study has the following theoretical implications. First, it extends the literature on the relationship between CSR and performance of SMEs and supports stakeholder theory, which advocates a positive influence of CSR on enterprise performance. This study empirically investigated the economic outcomes of CSR, and offers additional evidence for mixed conclusions, and contributes to the literature on stakeholder and RBV theories by examining the impact of CSR on SME performance in a new country context. Second, although it is certain that firm reputation is a source of competitive advantage, only a few studies have explored how CSR can be used to improve firm reputation (Kim & Kim, Citation2016). Thus this study contributes to the literature on the relationship between CSR and firm reputation, which is fairly new (Su et al., Citation2016). Third, the findings support the RBV in that firm reputation positively impacts business performance by serving as a crucial intangible asset for firms to enhance their bottomline. Fourth, this study explored the mechanisms through which CSR enhances enterprise performance and identifies the mediating effect of reputation on the relationship between CSR and performance from the perspective of SMEs in a developing country. This study highlights the partial mediating role of firm reputation in the relationship between CSR and performance, and contributes to a better understanding of CSR outcomes. Businesses with better CSR activities are in a better position to obtain excellent firm reputations, which can ultimately boost their financial performance.

This study also has practical implications for SME managers. The role of CSR activities in the enhancement of enterprise performance can encourage managers to get involved in executing social responsibility actions. Enterprises should invest more in CSR in terms of providing quality products and services, participating in community and environmental improvement initiatives, and boosting their reputation. Creating and developing a favourable reputation can help them benefit from high levels of differentiation and customer loyalty. SME managers should integrate CSR practices into their social goals and use it as a strategic tool to augment their competitiveness (Turyakira et al., Citation2014). CSR engagement should be perceived as a means to develop intangible assets like reputation, which are also beneficial for excellent financial performance. The findings of this study can serve as guidelines for entrepreneurs, researchers, and policymakers in understanding and implementing a CSR strategy efficiently, which is significant for attaining business reputation and improved financial performance of SMEs in developing countries.

5.3. Limitations and future research

This study has several limitations that offer fruitful directions for future research. First, it used cross-sectional data. As a result, we are not able to ascribe causality on the CSR and performance association. Relationships for data pertained only to a specific point in time and these data face challenges related to endogeneity. Remedies suggested by Li (Citation2016) and other studies are usually applied when there is adequate data for a certain period of time. Thus, an additional longitudinal study is necessary to examine the association over time and to address the problem of endogeneity. Second, we used subjective measures of financial performance because of the absence of objective measures in SMEs, although subjective measures correlate with objective ones (Keh et al., Citation2007). For future research, collecting objective data are recommended. Third, the existing literature has revealed that an inclusive measurement of firm reputation should elicit the valuation of internal and external stakeholders; nonetheless, our study merely concentrated on assessing SME managers and owners. Therefore, future studies should address these issues. Fourth, many factors may impact the association between CSR and business performance. Thus, other mediating and moderating variables should be explored in the future. Finally, this study was carried out in the Eritrean context. Future studies should focus on other African nations by examining the model to enhance the generalisability of the outcomes.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Agyemang Otuo, S., & Ansong, A. (2017). Corporate social responsibility and firm performance of Ghanaian SMEs: Mediating role of access to capital and firm reputation. Journal of Global Responsibility, 8(1), 47–62. https://doi.org/https://doi.org/10.1108/JGR-03-2016-0007

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modelling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411–423. https://doi.org/https://doi.org/10.1037/0033-2909.103.3.411

- Ansong, A., & Agyemang, O. S. (2016). Firm reputation and financial performance of SMEs: The Ghanaian perspective. EuroMed Journal of Management, 1(3), 237–251. https://doi.org/https://doi.org/10.1504/EMJM.2016.081040

- Bai, X., & Chang, J. (2015). Corporate social responsibility and firm performance: The mediating role of marketing competence and the moderating role of market environment. Asia Pacific Journal of Management, 32(2), 505–530. https://doi.org/https://doi.org/10.1007/s10490-015-9409-0

- Barić, A. (2017). Corporate social responsibility and stakeholders: Review of the last decade (2006–2015). Business Systems Research Journal, 8(1), 133–146. https://doi.org/https://doi.org/10.1515/bsrj-2017-0011

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/https://doi.org/10.1177/014920639101700108

- Bello, K., Jusoh, A., & Nor, K. (2016). Corporate social responsibility and consumer rights awareness: A research agenda. Indian Journal of Science and Technology, 9(46), 1–10. https://doi.org/https://doi.org/10.17485/ijst/2016/v9i46/107134

- Bendixen, M., & Abratt, R. (2007). Corporate identity, ethics and reputation in supplier–buyer relationships. Journal of Business Ethics, 76(1), 69–82. https://doi.org/https://doi.org/10.1007/s10551-006-9273-4

- Bergh, D. D., Ketchen, D. J., Jr, Boyd, B. K., & Bergh, J. (2010). New frontiers of the reputation—Performance relationship: Insights from multiple theories. Journal of Management, 36(3), 620–632. https://doi.org/https://doi.org/10.1177/0149206309355320

- Blanco, B., Guillamón-Saorín, E., & Guiral, A. (2013). Do non-socially responsible companies achieve legitimacy through socially responsible actions? The mediating effect of innovation. Journal of Business Ethics, 117(1), 67–83. https://doi.org/https://doi.org/10.1007/s10551-012-1503-3

- Boyd, B. K., Bergh, D. D., & Ketchen, D. J. Jr, (2010). Reconsidering the reputation—performance relationship: A resource-based view. Journal of Management, 36(3), 588–609.

- Brammer, S., & Millington, A. (2005). Corporate reputation and philanthropy: An empirical analysis. Journal of Business Ethics, 61(1), 29–44. https://doi.org/https://doi.org/10.1007/s10551-005-7443-4

- Branco, M. C., & Rodrigues, L. L. (2006). Corporate social responsibility and resource-based perspectives. Journal of Business Ethics, 69(2), 111–132. https://doi.org/https://doi.org/10.1007/s10551-006-9071-z

- Cadez, S. (2013). Social change, institutional pressures and knowledge creation: A bibliometric analysis. Expert Systems with Applications, 40(17), 6885–6893. https://doi.org/https://doi.org/10.1016/j.eswa.2013.06.036

- Cadez, S., Czerny, A., & Letmathe, P. (2019). Stakeholder pressures and corporate climate change mitigation strategies. Business Strategy and the Environment, 28(1), 1–14.

- Cadez, S., & Guilding, C. (2017). Examining distinct carbon cost structures and climate change abatement strategies in CO2 polluting firms. Accounting, Auditing & Accountability Journal, 30(5), 1041–1064. https://doi.org/https://doi.org/10.1108/AAAJ-03-2015-2009

- Choongo, P. (2017). A longitudinal study of the impact of corporate social responsibility on firm performance in SMEs in Zambia. Sustainability, 9(8), 1300. https://doi.org/https://doi.org/10.3390/su9081300

- Chung, S. Y., Schneeweis, T., & Eneroth, K. (1999). Corporate reputation and investment performance: The UK and US experience. Available at SSRN 167629.

- Clarkson, M. E. (1995). A stakeholder framework for analysing and evaluating corporate social performance. Academy of Management Review, 20(1), 92–117. https://doi.org/https://doi.org/10.5465/amr.1995.9503271994

- Deephouse, D. L. (2000). Media reputation as a strategic resource: An integration of mass communication and resource-based theories. Journal of Management, 26(6), 1091–1112. https://doi.org/https://doi.org/10.1177/014920630002600602

- Diamantopoulos, A., & Siguaw, J. A. (2006). Formative versus reflective indicators in organisational measure development: A comparison and empirical illustration. British Journal of Management, 17(4), 263–282. https://doi.org/https://doi.org/10.1111/j.1467-8551.2006.00500.x

- Doh, J. P., Howton, S. D., Howton, S. W., & Siegel, D. S. (2010). Does the market respond to an endorsement of social responsibility? The role of institutions, information, and legitimacy. Journal of Management, 36(6), 1461–1485. https://doi.org/https://doi.org/10.1177/0149206309337896

- Donaldson, T., & Preston, L. E. (1995). The stakeholder theory of the corporation: Concepts, evidence, and implications. Academy of Management Review, 20(1), 65–91. https://doi.org/https://doi.org/10.5465/amr.1995.9503271992

- Eberl, M., & Schwaiger, M. (2005). Corporate reputation: disentangling the effects on financial performance. European Journal of Marketing, 39(7/8), 838–854. https://doi.org/https://doi.org/10.1108/03090560510601798

- Edwards, A. R. (2005). The sustainability revolution: Portrait of a paradigm shift. : New Society Publishers.

- Farooq, M. S., & Radovic-Markovic, M. (2017). Impact of business simulation games on entrepreneurial intentions of business graduates: A PLS-SEM approach. Paper presented at the organisational behaviour and types of leadership styles and strategies in terms of globalisation, presented at the sixth international conference “Employment, Education and Entrepreneurship”, Compass Publishing.

- Fassin, Y., De Colle, S., & Freeman, R. E. (2017). Intra‐stakeholder alliances in plant‐closing decisions: A stakeholder theory approach. Business Ethics: A European Review, 26(2), 97–111. https://doi.org/https://doi.org/10.1111/beer.12136

- Fassin, Y., Werner, A., Van Rossem, A., Signori, S., Garriga, E., von Weltzien Hoivik, H., & Schlierer, H.-J. (2015). CSR and related terms in SME owner–managers’ mental models in six European countries: National context matters. Journal of Business Ethics, 128(2), 433–456. https://doi.org/https://doi.org/10.1007/s10551-014-2098-7

- Flanagan, D. J., & O’shaughnessy, K. (2005). The effect of layoffs on firm reputation. Journal of Management, 31(3), 445–463. https://doi.org/https://doi.org/10.1177/0149206304272186

- Fombrun, C. J. (2005). A world of reputation research, analysis and thinking—building corporate reputation through CSR initiatives: evolving standards. Corporate Reputation Review, 8(1), 7–12. https://doi.org/https://doi.org/10.1057/palgrave.crr.1540235

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/https://doi.org/10.1177/002224378101800104

- Fraj-Andrés, E., López-Pérez, M. E., Melero-Polo, I., & Vázquez-Carrasco, R. (2012). Company image and corporate social responsibility: Reflecting with SMEs' managers. Marketing Intelligence & Planning, 30(2), 266–280.

- Freeman, R. (1984). Strategic management: A stakeholder approach. Pitman Publishing.

- Friedman, M. (1970, September 13). The social responsibility of business is to increase its profits. New York Times Magazine, 33, 126.

- Galant, A., & Cadez, S. (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic research-Ekonomska Istraživanja, 30(1), 676–693. https://doi.org/https://doi.org/10.1080/1331677X.2017.1313122

- Galbreath, J., & Shum, P. (2012). Do customer satisfaction and reputation mediate the CSR–FP link? Evidence from Australia. Australian Journal of Management, 37(2), 211–229. https://doi.org/https://doi.org/10.1177/0312896211432941

- Gallardo-Vázquez, D., & Sánchez-Hernández, M. I. (2014). Structural analysis of the strategic orientation to environmental protection in SMEs. BRQ Business Research Quarterly, 17(2), 115–128. https://doi.org/https://doi.org/10.1016/j.brq.2013.12.001

- Gallardo-Vázquez, D., Valdez-Juárez, L. E., & Castuera-Díaz, Á. M. (2019). Corporate social responsibility as an antecedent of innovation, reputation, performance, and competitive success: A multiple mediation analysis. Sustainability, 11(20), 5614. https://doi.org/https://doi.org/10.3390/su11205614

- Gardberg, N. A., & Fombrun, C. J. (2006). Corporate citizenship: Creating intangible assets across institutional environments. Academy of Management Review, 31(2), 329–346. https://doi.org/https://doi.org/10.5465/amr.2006.20208684

- GOE (1994). Macroeconomic policy of Eritrea. Government of the state of Eritrea.

- Goll, I., & Rasheed, A. A. (2004). The moderating effect of environmental munificence and dynamism on the relationship between discretionary social responsibility and firm performance. Journal of Business Ethics, 49(1), 41–54. https://doi.org/https://doi.org/10.1023/B:BUSI.0000013862.14941.4e

- Graafland, J. (2018). Does corporate social responsibility put reputation at risk by inviting activist targeting? An empirical test among European SMEs. Corporate Social Responsibility and Environmental Management, 25(1), 1–13. https://doi.org/https://doi.org/10.1002/csr.1422

- Greening, D. W., & Turban, D. B. (2000). Corporate social performance as a competitive advantage in attracting a quality workforce. Business & Society, 39(3), 254–280.

- Grewatsch, S., & Kleindienst, I. (2017). When does it pay to be good? Moderators and mediators in the corporate sustainability–corporate financial performance relationship: A critical review. Journal of Business Ethics, 145(2), 383–416. https://doi.org/https://doi.org/10.1007/s10551-015-2852-5

- Guerrero‐Villegas, J., Sierra‐García, L., & Palacios‐Florencio, B. (2018). The role of sustainable development and innovation on firm performance. Corporate Social Responsibility and Environmental Management, 25(6), 1350–1362.

- Gunday, G., Ulusoy, G., Kilic, K., & Alpkan, L. (2011). Effects of innovation types on firm performance. International Journal of Production Economics, 133(2), 662–676. https://doi.org/https://doi.org/10.1016/j.ijpe.2011.05.014

- Hair Jr, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016a). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hair Jr, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016b). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications.

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2014). Multivariate data analysis. Pearson Education Limited.

- Hammann, E. M., Habisch, A., & Pechlaner, H. (2009). Values that create value: socially responsible business practices in SMEs–empirical evidence from German companies. Business Ethics: A European Review, 18(1), 37–51. https://doi.org/https://doi.org/10.1111/j.1467-8608.2009.01547.x

- Hao, X., Tong, Y., & Hu, C. (2011). A study on the impact of corporate social performance on corporate financial performance: From a view of social capital. Science and Management of S. & T, 10.

- Henderson, D. (2001). Misguided virtue: False notions of corporate social responsibility. New Zealand Business Roundtable.

- Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modelling in new technology research: Updated guidelines. Industrial Management & Data Systems, 116(1), 2–20.

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modelling in international marketing new challenges to international marketing (pp. 277–319). Emerald Group Publishing Limited.

- Hillman, A. J., & Keim, G. D. (2001). Shareholder value, stakeholder management, and social issues: What's the bottom line? Strategic Management Journal, 22(2), 125–139. https://doi.org/https://doi.org/10.1002/1097-0266(200101)22:2<125::AID-SMJ150>3.0.CO;2-H

- Hooper, D., Coughlan, J., & Mullen, M. R. (2008). Structural equation modelling: Guidelines for determining model fit. Electronic Journal of Business Research Methods, 6(1), 53–60.

- Hsu, K.-T. (2012). The advertising effects of corporate social responsibility on corporate reputation and brand equity: Evidence from the life insurance industry in Taiwan. Journal of Business Ethics, 109(2), 189–201. https://doi.org/https://doi.org/10.1007/s10551-011-1118-0

- Hull, C. E., & Rothenberg, S. (2008). Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strategic Management Journal, 29(7), 781–789. https://doi.org/https://doi.org/10.1002/smj.675

- Hulland, J., Ryan, M. J., & Rayner, R. K. (2010). Modelling customer satisfaction: A comparative performance evaluation of covariance structure analysis versus partial least squares Handbook of partial least squares (pp. 307–325). Springer.

- Husted, B. W., & Allen, D. B. (2007). Strategic corporate social responsibility and value creation among large firms: lessons from the Spanish experience. Long Range Planning, 40(6), 594–610. https://doi.org/https://doi.org/10.1016/j.lrp.2007.07.001

- Idemudia, U. (2011). Corporate social responsibility and developing countries: Moving the critical CSR research agenda in Africa forward. Progress in Development Studies, 11(1), 1–18. https://doi.org/https://doi.org/10.1177/146499341001100101

- Jamali, D., & Neville, B. (2011). Convergence versus divergence of CSR in developing countries: An embedded multi-layered institutional lens. Journal of Business Ethics, 102(4), 599–621. https://doi.org/https://doi.org/10.1007/s10551-011-0830-0

- Jamali, D., Safieddine, A. M., & Rabbath, M. (2008). Corporate governance and corporate social responsibility synergies and interrelationships. Corporate Governance: An International Review, 16(5), 443–459. https://doi.org/https://doi.org/10.1111/j.1467-8683.2008.00702.x

- Jones, R. (2005). Finding sources of brand value: Developing a stakeholder model of brand equity. Journal of Brand Management, 13(1), 10–32. https://doi.org/https://doi.org/10.1057/palgrave.bm.2540243

- Juarez, L. E. V. (2017). Corporate social responsibility: Its effects on SMEs. Journal of Management & Sustainability, 7(3), 75–89.

- Keh, H. T., Nguyen, T. T. M., & Ng, H. P. (2007). The effects of entrepreneurial orientation and marketing information on the performance of SMEs. Journal of Business Venturing, 22(4), 592–611. https://doi.org/https://doi.org/10.1016/j.jbusvent.2006.05.003

- Kim, S.-B., & Kim, D.-Y. (2016). The influence of corporate social responsibility, ability, reputation, and transparency on hotel customer loyalty in the US: A gender-based approach. SpringerPlus, 5(1), 1537. https://doi.org/https://doi.org/10.1186/s40064-016-3220-3

- Kline, R. B. (2011). Principles and practice of structural equation modeling (3. Baskı). Guilford.

- Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration, ), 11(4), 1–10. https://doi.org/https://doi.org/10.4018/ijec.2015100101

- Lai, C.-S., Chiu, C.-J., Yang, C.-F., & Pai, D.-C. (2010). The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate reputation. Journal of Business Ethics, 95(3), 457–469. https://doi.org/https://doi.org/10.1007/s10551-010-0433-1

- Lantos, G. P. (2001). The boundaries of strategic corporate social responsibility. Journal of Consumer Marketing, 18(7), 595–630. https://doi.org/https://doi.org/10.1108/07363760110410281

- Lev, B., Petrovits, C., & Radhakrishnan, S. (2010). Is doing good good for you? How corporate charitable contributions enhance revenue growth. Strategic Management Journal, 31(2), 182–200.

- Li, F. (2016). Endogeneity in CEO power: A survey and experiment. Investment Analysts Journal, 45(3), 149–162. https://doi.org/https://doi.org/10.1080/10293523.2016.1151985

- Lindgreen, A., Swaen, V., & Johnston, W. J. (2009). Corporate social responsibility: An empirical investigation of US organizations. Journal of Business Ethics, 85(S2), 303–323. https://doi.org/https://doi.org/10.1007/s10551-008-9738-8

- Liping, Z., Yan, C., & Yujian, J. (2016). An empirical study on the relationship between corporate social responsibility and financial performance—based on the analysis and interpretation based on the perspective of corporate reputation. Jiangsu Social Sciences, 3, 95–102.

- Longo, M., Mura, M., & Bonoli, A. (2005). Corporate social responsibility and corporate performance: The case of Italian SMEs. Corporate Governance: The International Journal of Business in Society, 5(4), 28–42. https://doi.org/https://doi.org/10.1108/14720700510616578

- Luo, X., & Bhattacharya, C. B. (2006). Corporate social responsibility, customer satisfaction, and market value. Journal of Marketing, 70(4), 1–18. https://doi.org/https://doi.org/10.1509/jmkg.70.4.001

- Maldonado-Guzman, G., Pinzon-Castro, S. Y., & Leana-Morales, C. (2017). Corporate social responsibility, brand image and firm reputation in Mexican small business. J. Mgmt. & Sustainability, 7(3), 38–47.

- Maldonado-Guzmán, G., Pinzón-Castro, S. Y., & Morales, C. L. (2017). Corporate social responsibility and firm reputation in Mexican small business. Advances in Management and Applied Economics, 7(5), 29–44.

- Man, W. (2002). Entrepreneurial competencies and the performance of small and medium enterprises in the Hong Kong services sector (Doctoral dissertation). The Hong Kong Polytechnic University.

- Mandl, I. (2009). The interaction between local employment development and corporate social responsibility. Austrian Institute for SME Research.

- Margolis, J. D., Elfenbein, H. A., Walsh, J. P. (2009). Does it pay to be good… and does it matter? A meta-analysis of the relationship between corporate social and financial performance. Available at SSRN: https://ssrn.com/abstract=1866371 or https://doi.org/https://doi.org/10.2139/ssrn.1866371

- Margolis, J. D., & Walsh, J. P. (2003). Misery loves companies: Rethinking social initiatives by business. Administrative Science Quarterly, 48(2), 268–305. https://doi.org/https://doi.org/10.2307/3556659

- Martinez-Conesa, I., Soto-Acosta, P., & Palacios-Manzano, M. (2017). Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. Journal of Cleaner Production, 142, 2374–2383. https://doi.org/https://doi.org/10.1016/j.jclepro.2016.11.038

- Martínez‐Ferrero, J., & Frias‐Aceituno, J. V. (2015). Relationship between sustainable development and financial performance: International empirical research. Business Strategy and the Environment, 24(1), 20–39.

- Masurel, E. (2015). Social and ecological engagement and economic firm performance: Correlated or not? CSR evidence from SMEs in two Dutch retail sectors [Paper presentation]. Paper Presented at the Proceedings of the Conference of Growing Sustainable Business, Tilburg University, Tilburg, The Netherlands.

- McWilliams, A., & Siegel, D. (2000). Corporate social responsibility and financial performance: correlation or misspecification? Strategic Management Journal, 21(5), 603–609. https://doi.org/https://doi.org/10.1002/(SICI)1097-0266(200005)21:5<603::AID-SMJ101>3.0.CO;2-3

- McWilliams, A., & Siegel, D. (2001). Corporate social responsibility: A theory of the firm perspective. Academy of Management Review, 26(1), 117–127. https://doi.org/https://doi.org/10.5465/amr.2001.4011987

- Miller, N. J., & Besser, T. L. (2000). The importance of community values in small business strategy formation: Evidence from rural Iowa. Journal of Small Business Management, 38(1), 68–85.

- Mishra, S., & Modi, S. B. (2013). Positive and negative corporate social responsibility, financial leverage, and idiosyncratic risk. Journal of Business Ethics, 117(2), 431–448. https://doi.org/https://doi.org/10.1007/s10551-012-1526-9

- Mishra, S., & Suar, D. (2010). Does corporate social responsibility influence firm performance of Indian companies? Journal of Business Ethics, 95(4), 571–601. https://doi.org/https://doi.org/10.1007/s10551-010-0441-1

- Mitchell, R. K., Agle, B. R., & Wood, D. J. (1997). Towards a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Academy of Management Review, 22(4), 853–886. https://doi.org/https://doi.org/10.5465/amr.1997.9711022105

- MTI (2018). Eritrea enterprise report. Ministry of Trade and Industry Eritrea.

- Munasinghe, M., & Malkumari, A. (2012). Corporate social responsibility in small and medium enterprises (SME) in Sri Lanka. Journal of Emerging Trends in Economics and Management Sciences, 3(2), 168–172.

- Oeyono, J., Samy, M., & Bampton, R. (2011). An examination of corporate social responsibility and financial performance. Journal of Global Responsibility, 2(1), 100–112. https://doi.org/https://doi.org/10.1108/20412561111128555

- Orlitzky, M., Schmidt, F. L., & Rynes, S. L. (2003). Corporate social and financial performance: A meta-analysis. Organization Studies, 24(3), 403–441. https://doi.org/https://doi.org/10.1177/0170840603024003910

- Orlitzky, M., Siegel, D. S., & Waldman, D. A. (2011). Strategic corporate social responsibility and environmental sustainability. Business & Society, 50(1), 6–27.

- Park, J., Lee, H., & Kim, C. (2014). Corporate social responsibilities, consumer trust and corporate reputation: South Korean consumers' perspectives. Journal of Business Research, 67(3), 295–302. https://doi.org/https://doi.org/10.1016/j.jbusres.2013.05.016

- Peloza, J., & Shang, J. (2011). How can corporate social responsibility activities create value for stakeholders? A systematic review. Journal of the Academy of Marketing Science, 39(1), 117–135. https://doi.org/https://doi.org/10.1007/s11747-010-0213-6

- Perrini, F. (2006). SMEs and CSR theory: Evidence and implications from an Italian perspective. Journal of Business Ethics, 67(3), 305–316. https://doi.org/https://doi.org/10.1007/s10551-006-9186-2

- Perrini, F., Russo, A., Tencati, A., & Vurro, C. (2011). Deconstructing the relationship between corporate social and financial performance. Journal of Business Ethics, 102(S1), 59–76. https://doi.org/https://doi.org/10.1007/s10551-011-1194-1

- Pfarrer, M. D., Pollock, T. G., & Rindova, V. P. (2010). A tale of two assets: The effects of firm reputation and celebrity on earnings surprises and investors’ reactions. Academy of Management Journal, 53(5), 1131–1152. https://doi.org/https://doi.org/10.5465/amj.2010.54533222

- Pivato, S., Misani, N., & Tencati, A. (2008). The impact of corporate social responsibility on consumer trust: The case of organic food. Business Ethics: A European Review, 17(1), 3–12.

- Polonsky, M. J., Neville, B. A., Bell, S. J., & Mengüç, B. (2005). Corporate reputation, stakeholders and the social performance‐financial performance relationship. European Journal of Marketing, 39, 1184–1198.

- Rahman Belal, A. (2001). A study of corporate social disclosures in Bangladesh. Managerial Auditing Journal, 16(5), 274–289. https://doi.org/https://doi.org/10.1108/02686900110392922

- Reverte, C., Gomez-Melero, E., & Cegarra-Navarro, J. G. (2016). The influence of corporate social responsibility practices on organizational performance: evidence from Eco-Responsible Spanish firms. Journal of Cleaner Production, 112, 2870–2884.

- Roberts, P. W., & Dowling, G. R. (2002). Corporate reputation and sustained superior financial performance. Strategic Management Journal, 23(12), 1077–1093. https://doi.org/https://doi.org/10.1002/smj.274

- Roblek, V., Meško, M., Pejić Bach, M., Bertoncelj, A. (2014). Impact of knowledge management on sustainable development in the innovative economy. Paper Presented at the Business Systems Laboratory-2nd International Symposium “Systems Thinking for a Sustainable Economy. Advancements in Economic and Managerial Theory and Practice Universitas Mercatorum via Appia Pignatelli.

- Russo, M. V., & Fouts, P. A. (1997). A resource-based perspective on corporate environmental performance and profitability. Academy of Management Journal, 40(3), 534–559.

- Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. Journal of Business Research, 68(2), 341–350. https://doi.org/https://doi.org/10.1016/j.jbusres.2014.06.024

- Sarbutts, N. (2003). Can SMEs “do” CSR? A practitioner’s view of the ways small-and medium-sized enterprises are able to manage reputation through corporate social responsibility. Journal of Communication Management, 7(4), 340–347. https://doi.org/https://doi.org/10.1108/13632540310807476

- Saunders, M., Lewis, P., & Thornhill, A. (2012). Research methods for business students (6. utg.). Pearson.

- Schmidt, K. (1995). The quest for identity: corporate identity: strategies, methods and examples. Thomson Learning.

- Sen, S., & Cowley, J. (2013). The relevance of stakeholder theory and social capital theory in the context of CSR in SMEs: An Australian perspective. Journal of Business Ethics, 118(2), 413–427. https://doi.org/https://doi.org/10.1007/s10551-012-1598-6

- Servaes, H., & Tamayo, A. (2013). The impact of corporate social responsibility on firm value: The role of customer awareness. Management Science, 59(5), 1045–1061. https://doi.org/https://doi.org/10.1287/mnsc.1120.1630

- Sharma, S. (2000). Managerial interpretations and organizational context as predictors of corporate choice of environmental strategy. Academy of Management Journal, 43(4), 681–697.

- Smith, H. J. (2003). The shareholders vs. stakeholders debate. MIT Sloan Management Review, 44(4), 85–90.

- Šontaitė-Petkevičienė, M. (2015). CSR reasons, practices and impact to corporate reputation. Procedia – Social and Behavioral Sciences, 213, 503–508. https://doi.org/https://doi.org/10.1016/j.sbspro.2015.11.441

- Spence, L. J. (1999). Does size matter? The state of the art in small business ethics. Business Ethics: A European Review, 8(3), 163–174. https://doi.org/https://doi.org/10.1111/1467-8608.00144

- Spence, L. J., Schmidpeter, R., & Habisch, A. (2003). Assessing social capital: Small and medium sized enterprises in Germany and the UK. Journal of Business Ethics, 47(1), 17–29. https://doi.org/https://doi.org/10.1023/A:1026284727037

- Stawiski, S., Deal, J. J., & Gentry, W. (2010). Employee perceptions of corporate social responsibility. Center for Creative Leadership.

- Su, L., Swanson, S. R., Chinchanachokchai, S., Hsu, M. K., & Chen, X. (2016). Reputation and intentions: The role of satisfaction, identification, and commitment. Journal of Business Research, 69(9), 3261–3269. https://doi.org/https://doi.org/10.1016/j.jbusres.2016.02.023

- Surroca, J., Tribó, J. A., & Waddock, S. (2010). Corporate responsibility and financial performance: The role of intangible resources. Strategic Management Journal, 31(5), 463–490. https://doi.org/https://doi.org/10.1002/smj.820

- Sweeney, L. (2007). Corporate social responsibility in Ireland: barriers and opportunities experienced by SMEs when undertaking CSR. Corporate Governance: The International Journal of Business in Society, 7(4), 516–523. https://doi.org/https://doi.org/10.1108/14720700710820597

- Sweeney, L. (2009). A study of current practice of corporate social responsibility (CSR) and an examination of the relationship between CSR and financial performance using structural equation modelling (SEM). Doctoral Thesis. Dublin, Technological University Dublin. doi:https://doi.org/10.21427/D79C7F.

- Szabo, A. (2008). The corporate social responsibility: An opportunity for SMEs. Retrieved from http://www.unglobalcompact.org/ http://www.unece.org/indust/sme/ResponsibleEntrepreneurship.

- Tan, H. (2007). Does the reputation matter? Corporate reputation and earnings quality (August 31, 2007). Retrived from https://ssrn.com/abstract=1013127 or https://doi.org/http://dx.doi.org/10.2139/ssrn.1013127

- Tian, H. (2009). The correlation between CSR and corporate performance-cased on the empirical data in China’s telecommunication industry. Economic Management, 31(1), 72–79.

- Tilt, C. A. (2016). Corporate social responsibility research: the importance of context. International Journal of Corporate Social Responsibility, 1(1), 2. https://doi.org/https://doi.org/10.1186/s40991-016-0003-7

- Torugsa, N. A., O’Donohue, W., & Hecker, R. (2012). Capabilities, proactive CSR and financial performance in SMEs: Empirical evidence from an Australian manufacturing industry sector. Journal of Business Ethics, 109(4), 483–500. https://doi.org/https://doi.org/10.1007/s10551-011-1141-1

- Turban, D. B., & Greening, D. W. (1997). Corporate social performance and organizational attractiveness to prospective employees. Academy of Management Journal, 40(3), 658–672.

- Turyakira, P., Venter, E., & Smith, E. (2012). Corporate social responsibility for SMEs: A proposed hypothesised model. African Journal of Business Ethics, 6(2), 106–106. https://doi.org/https://doi.org/10.4103/1817-7417.111015

- Turyakira, P., Venter, E., & Smith, E. (2014). The impact of corporate social responsibility factors on the competitiveness of small and medium-sized enterprises. South African Journal of Economic and Management Sciences, 17(2), 157–172. https://doi.org/https://doi.org/10.4102/sajems.v17i2.443

- Valdez-Juárez, L. E., Gallardo-Vázquez, D., & Ramos-Escobar, E. A. (2018). CSR and the supply chain: Effects on the results of SMEs. Sustainability, 10(7), 2356. https://doi.org/https://doi.org/10.3390/su10072356

- Van Beurden, P., & Gössling, T. (2008). The worth of values–a literature review on the relation between corporate social and financial performance. Journal of Business Ethics, 82(2), 407–424. https://doi.org/https://doi.org/10.1007/s10551-008-9894-x

- Vashchenko, M. (2017). An external perspective on CSR: What matters and what does not? Business Ethics: A European Review, 26(4), 396–412. https://doi.org/https://doi.org/10.1111/beer.12162

- Vukić, N. M., Omazić, M. A., Pejic-Bach, M., Aleksić, A., & Zoroja, J. (2020). Leadership for sustainability: connecting corporate responsibility reporting and strategy leadership styles, innovation, and social entrepreneurship in the era of digitalization (pp. 44–72). IGI Global.

- Waddock, S. A., & Graves, S. B. (1997). The corporate social performance–financial performance link. Strategic Management Journal, 18(4), 303–319. https://doi.org/https://doi.org/10.1002/(SICI)1097-0266(199704)18:4<303::AID-SMJ869>3.0.CO;2-G

- Wagner, M. (2010). Corporate social performance and innovation with high social benefits: A quantitative analysis. Journal of Business Ethics, 94(4), 581–594. https://doi.org/https://doi.org/10.1007/s10551-009-0339-y

- Wagner, M., Van Phu, N., Azomahou, T., & Wehrmeyer, W. (2002). The relationship between the environmental and economic performance of firms: an empirical analysis of the European paper industry. Corporate Social Responsibility and Environmental Management, 9(3), 133–146. https://doi.org/https://doi.org/10.1002/csr.22

- Wall, T. D., Michie, J., Patterson, M., Wood, S. J., Sheehan, M., Clegg, C. W., & West, M. (2004). On the validity of subjective measures of company performance. Personnel Psychology, 57(1), 95–118.

- Wetzels, M., Odekerken-Schröder, G., & Van Oppen, C. (2009). Using PLS path modelling for assessing hierarchical construct models: Guidelines and empirical illustration. MIS Quarterly, 33, 177–195. https://doi.org/https://doi.org/10.2307/20650284

- Wu, M.-L. (2006). Corporate social performance, corporate financial performance, and firm size: A meta-analysis. Journal of American Academy of Business, 8(1), 163–171.

- Yang, L., Yaacob, Z., & Teh, S. Y. (2017). Does reputation mediate the relationship between corporate social responsibility and performance of SMEs in China. International Journal of Economics & Management, 11(2), 335–354.

- Yang, W., & Yang, S. (2016). An empirical study on the relationship between corporate social responsibility and financial performance under the Chinese context-based on the contrastive analysis of large, small and medium-size listed companies. Chinese Journal of Management Science, 24(1), 143–150.

- Zhu, Y., Sun, L.-Y., & Leung, A. S. (2014). Corporate social responsibility, firm reputation, and firm performance: The role of ethical leadership. Asia Pacific Journal of Management, 31(4), 925–947. https://doi.org/https://doi.org/10.1007/s10490-013-9369-1